43

Bualuang Securities Plc. April 3, 2014 Overview of PTTGC Business and Basic of Petrochemical

Bualuang Securities Plc. April 3, 2014

Overview of PTTGC Business and Basic of Petrochemical

Disclaimer

This presentation includes forward-looking statements that are subject to risks and uncertainties, including those pertaining to the anticipated benefits to be realized from the proposals described herein. This presentation contains a number of forward-looking statements including, in particular, statements about future events, future financial performance, plans, strategies, expectations, prospects, competitive environment, regulation and supply and demand.

PTTGC has based these forward-looking statements on its views with respect to future events and financial performance. Actual financial performance of the entities described herein could differ materially from that projected in the forward-looking statements due to the inherent uncertainty of estimates, forecasts and projections, and financial performance may be better or worse than anticipated. Given these uncertainties, readers should not put undue reliance on any forward-looking statements.

Forward-looking statements represent estimates and assumptions only as of the date that they were made. The information contained in this presentation is subject to change without notice and PTTGC does not undertake any duty to update the forward-looking statements, and the estimates and assumptions associated with them, except to the extent required by applicable laws and regulations.

2

Agenda

q Overview of PTTGC

q Basic Knowledge of Petrochemical Industry

q Competitiveness and Key Driver

q Strategy and Execution

q Conclusion

q Appendix

3 3

Agenda

q Overview of PTTGC

q Basic Knowledge of Petrochemical Industry

q Competitiveness and Key Driver

q Strategy and Execution

q Conclusion

q Appendix

4 4

Overview of PTTGC

Incorporated on October 19, 2011 from the amalgamation of PTTAR and PTTCH

• Total petrochemical capacity: 8.75 MTA

• Total distillation capacity: 280 KBD

• Number of employees 3,660 persons

Top 5 Shareholders

PTT 48.89% Thai NVDR 9.05% State Street Bank Europe Ltd 2.84% State Street Bank and Trust Co. Ltd. 1.92% HMC Polymers Co. Ltd 1.85% As of March 6, 2014

5

2013 Financial Highlights

6

2013 Financial Highlights

7

Historical Dividend Payment

8

Strategic location of each plant in Map Ta Phut Industrial Complex creates proximity to suppliers and customers

9

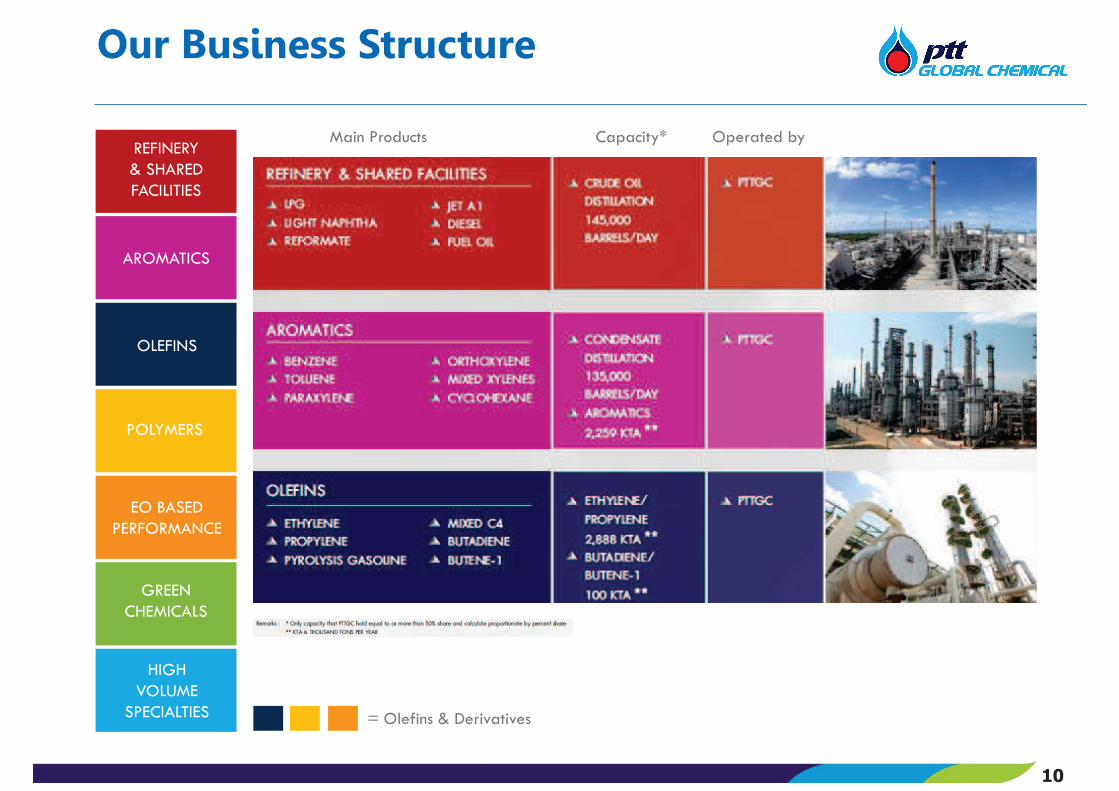

Our Business Structure

REFINERY & SHARED FACILITIES

AROMATICS

OLEFINS

POLYMERS

EO BASED PERFORMANCE

GREEN CHEMICALS

HIGH VOLUME

SPECIALTIES

Main Products Capacity* Operated by

= Olefins & Derivatives

10

Our Business Structure

REFINERY & SHARED FACILITIES

AROMATICS

OLEFINS

POLYMERS

EO BASED PERFORMANCE

GREEN CHEMICALS

HIGH VOLUME

SPECIALTIES

Main Products Capacity* Operated by

11

Natural Gas

Crude Palm Oil

Crude

Condensate

Cracker

Aromatics

Plants

Refinery

Ethylene

HDPE

LLDPE

LDPE

MEG

Propylene

Oleochemicals

Paraxylene

Benzene

PTAPET Fiber/Resin

EO

Ethanolamine

Ethoxylate

Cyclohexane

Cumene

Phenol

Acetone

EB/SM

PS

BPA

Methyl Ester(B-100)

PC

Caprolactam Nylon 6

Fatty Alcohol

MMA PMMA

Epoxy Resins

ABS

SBR

PP

PTT Phenol

Petroleum Products

- LPG

- Reformate

- Light Naptha

- Jet Fuel

- Diesel

- Fuel Oil

Reformate,

Heavy

Naphtha

Pygas

Condensate

Residue,

Hydrogen

Light

Naphtha

C3,C4

OffGas Mixed C4 Butadiene

PO

PUTDI/HDI

Toluene

Polyols

Orthoxylene

Cracker

Bottom,

Hydrogen

PA Plasticizer

1. PTTGC does not currently produce these products.

REFINERY & SHARED

FACILITIES AROMATICS OLEFINS POLYMERS

EO-BASED

PERFORMANCE GREEN CHEMICALS

HIGH VOLUME

SPECIALTIES

Feedstock Upstream Intermediates Downstream

Proximity to Suppliers and Customers

Exchange Stream Products

By-Products

Potential Product Opportunities (1)

Petroleum Products

- LPG

- Reformate

- Light Naphtha

- Jet Fuel

- Diesel

- Fuel Oil

Fully Integrated Petrochemical and Refinery Operations

with Diversified Product Portfolio

12

Agenda

q Overview of PTTGC

q Basic Knowledge of Petrochemical Industry

q Competitiveness and Key Driver

q Strategy and Execution

q Conclusion

q Appendix

13 13

14

Plastic Resin Codes

15

Petrochemical Raw Materials Come from Petroleum and Gas Fractions

16

Source: www.2b1stconsulting.com/propylene/

Refinery Business

CDU

LPG REFORMATE LIGHT NAPHTHA JET A-1 DIESEL FUEL OIL

17

crude

Refinery Business

18

Aromatics Business

TOLUENE

PARAXYLENE

BENZENE

CONDENSATESPLITTER – REFORMER

19

OTHOXYLENE

CUMENE

PHENOL

ACETONE

BISPHENOL A POLY

CARBONATE

CYCLOHEXANE

TOLUENE DIISOCYANATE HEXAMETHYLENE DIISOCYANATE

POLYURETHANE

TEREPHTHALIC ACID -> PTA PET - POLYESTER

PHTHALIC ANHYDRIDE PLASTICIZER

CAPROLACTAM NYLON 6

POLYMETHYL METHACRYLATE

METHYL METHACRYLATE

Condensate

STYRENE MONOMER

POLYSTYRENE

ABS

STYRENE BUTADIENE RUBBER

XYLENE

Polyester Value Chain

20

Source: Indorama 2Q13 Analyst Meeting Presentation

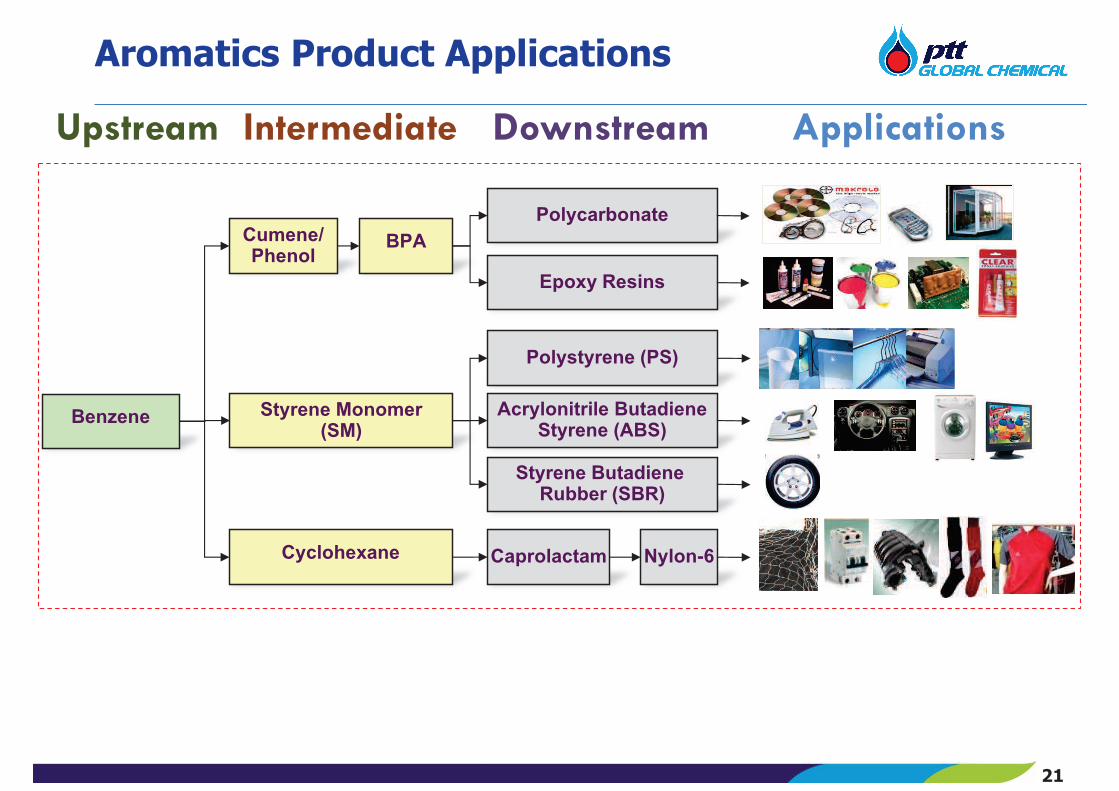

Aromatics Product Applications

Intermediate Downstream Applications Upstream

Cyclohexane

Benzene Styrene Monomer (SM)

Polystyrene (PS)

Acrylonitrile Butadiene Styrene (ABS)

Caprolactam Nylon-6

Cumene/ Phenol

BPA Polycarbonate

Epoxy Resins

Styrene Butadiene Rubber (SBR)

21

Olefins and Derivatives Business

PROPYLENE

MIXED C4

HDPE

LDPE

LLDPE

MEGETHYLENE OXIDE

POLYSTYRENE

ETHANOLAMINE

ETHOXYLATE

ETHYLENE

BUTENE-1

STYRENE MONOMER

STYRENE BUTADIENE

RUBBER

POLYPROPYLENE

PROPYLENE OXIDE

POLYOLS

CRACKER

POLYURETHANE

BUTADIENE

PET - POLYESTER

22

Natural Gas

Process Block Diagram

Product I

Film Grades Injection Grades Pipe Grades Thermoform

Monofilament Wire & Cable

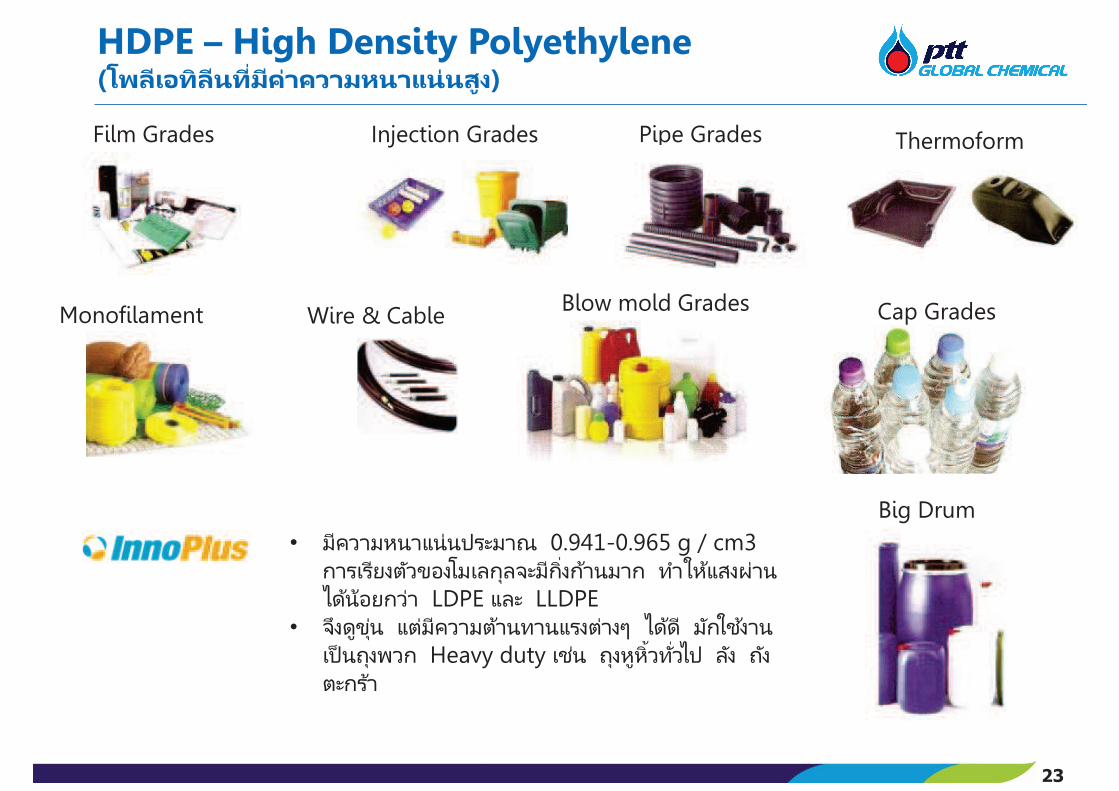

HDPE – High Density Polyethylene (โพลีเอทิลีนที)มีคา่ความหนาแน่นสูง)

Blow mold Grades

Big Drum

Cap Grades

• มีความหนาแน่นประมาณ 0.941-0.965 g / cm3 การเรียงตวัของโมเลกลุจะมีกิ!งกา้นมาก ทาํใหแ้สงผ่านไดน้อ้ยกว่า LDPE และ LLDPE

• จึงดขูุน่ แต่มีความตา้นทานแรงตา่งๆ ไดด้ี มกัใชง้านเป็นถงุพวก Heavy duty เชน่ ถงุหูหิ !วทั"วไป ลงั ถงั

ตะกรา้

23

Cap & Lid

General Purpose and

Heavy Duty Film Extrusion Coating

Shrink Film

Zip Bag

Cosmetic Tube &

Blow Mold Container Foam & Bubble Sheet

Cap &

LDPE – Low Density Polyethylene (โพลิเอทิลีนความหนาแน่นตํ2า)

• มีความหนาแน่นประมาณ 0.910-0.925 g / cm3 การเรียงตวัของโมเลกลุเป็นระเบียบกวา่ HDPE แตย่งัคงมีกิ!งกา้นอยู ่ มีความใสพอสมควร คณุสมบตัิตา่งๆ ดีกวา่ HDPE แตค่วามตา้นทานแรงตา่งๆ นอ้ยกวา่ มกัใชเ้ป็น Sealing layer

24

Tube

Zip bag

Water storage tank

LLDPE Applications LLDPE – Linear Low Density Polyethylene

LLDPE ตา่งจาก LDPE ตรงการจดัเรียงตวัของโมเลกลุไม่มีกิ!งกา้น ทําใหม้ีความใสมากกว่า LDPE และคณุภาพดา้นต่างๆ ดีกว่า LDPE มกัใชง้านที!อณุหภมูิตํ!าๆ เชน่ บรรจอุาหารแชเ่ย็นหรือแชแ่ขง็ และใชเ้ป็น Sealing layer

25

Agenda

q Overview of PTTGC

q Basic Knowledge of Petrochemical Industry

q Competitiveness and Key Driver

q Strategy and Execution

q Conclusion

q Appendix

26 26

Highly Competitive Cost Structure & Performance mainly driven by Olefins and Derivatives

27

94

244

1019 1030 1039 1107

1177 1199 1228

0

200

400

600

800

1000

1200

1400

MDEEthane

NAMEthane

WEPNaphtha

MDENaphtha

NAMNaphtha

MDELPG

NEANaphtha

SEANaphtha

NEA LPG

2013 Global Ethylene Cash Cost by Region USD/Ton

Source: IHS (formerly CMAI) average 2013. PTTGC cash cost takes into account the effect of the renewal of gas price agreement

Note: MDE = Middle East, NAM = North America, NEA = Northeast Asia, SEA = Southeast Asia, WEP = Western Europe.

MDE cash costs are average values of Iran and Saudi Arabia.

48%

20%

21%

5%

5% 1%

Adj. EBITDA Breakdown

16%

16%

56%

3%

3% 5%

Typical Revenue Breakdown

% Adj. EBITDA Margin

3 8

27

5 7 10

2

10

27

8

2

10

Refinery Aromatics Olefins and

Derivatives

Green HVS PTTGC

2012 2013

s

s

What to look at?

q PRICE & SPREAD

q DEMAND

q Product Producers

q Downstream Chain Producers

q SUPPLY

q New Technologies/New Feedstock

q New Capacity Additions

q Shutdown/Closure

q Cut-Run

q SOURCES OF INFORMATION

q In-house

q Research houses, e.g. ICIS, CMAI, IHS

q Bloomberg

q Brokerage Firms’ researches

28

Agenda

q Overview of PTTGC

q Basic Knowledge of Petrochemical Industry

q Competitiveness and Key Driver

q Strategy and Execution

q Conclusion

q Appendix

29 29

Megatrends and Implications to Business

30

Megatrends and other external factors

New Products

Elec. & Electronic

Construction

Auto & Transp.

Existing Core

Packaging

Textiles

Home & Personal

End Used Platform

Shift in global growth

Smarter, healthier population

Tech& innovation society

Competing for resources

Growing of middle class

Aging society

Emerging markets

Urbanization

Alternative energy

Green tech

New patterns of consumption

Water scarcity

Climate change

Fossil fuel scarcity

AEC 2015

ASEAN connectivity

CHN 12th FYP

Mark

et

back

Demand For

Petrochemical Products

Taking PTTGC’s Strategies into Execution The Double E (2014 – 2018)

31

PTTGC Business Principle : People Conduct & Business Conduct

GREEN

CORE UPLIFT PROJECTS

1-STEP ADJACENCIES

Operational Excellence

Synergy Excellence

Debottlenecking

Marketing Excellence

NEW GEOGRAPHIES NEW PRODUCTS

ASEAN: Pertamina

CHINA: Sinochem

System House

Compounding:

PC, PU, SBR

Olechemical

PLA

Succinic Acid

PLA/PBS Compound

EXCELLENCE

EXECUTION

EBITDA Uplift

15-30% (2012-2017)

1st Quartile

Performance

ROIC > 14%

Listed in Globally

Sustainability Index

Continues to Strive for Strong Profitable Growth

32

~800-900

~620-650

Green

563

Actual

2012

Target

2017

Target

2022

Expected EBITDA Benefit

Uplift 15-30%

Phase 1 : Foundation for Growth Phase 2: The Growth Mode

Green

HVS

New Global Hub

Debottleneck

Synergy Project Excellence

Operational Excellence Marketing Excellence Capital Expenditure Excellence

We aim to grow ~5 percent p.a. in the next ten years

Sales in THB Bn Based on constant Dubai crude year 2012 at USD 109 per bbl

32

33

CORE UPLIFT 1-STEP

ADJACENCIES GREEN

New Products | New Geographies

Adjusted Target

• Revised Operational Excellence target • Include only projects passed stage gates

*

* Debottleneck EBITDA uplift includes

1Q/14 BV project starts up 3Q/15 TOCGC Plant Improvement Project 4Q/15 PX Expansion starts up Not Including PTTPE Cracker Debottlenecking and LLDPE Expansion

>> Excellence Programs Target

EBIT

DA

Up

lift (M

USD

)

34

CORE UPLIFT 1-STEP

ADJACENCIES GREEN

New Products | New Geographies

Phenol 2 Project

TOCGC Plant Improvement Project

BOD approved EPC + Construction

Debottlenecking & Expansion

PTTPE Cracker Debottlenecking

PX Expansion

Target COD: 3Q/15

Target COD: 4Q/15

Target COD: 3Q/15

BEP

Target : 2016

LLDPE Expansion

BEP

Target : 2017

Construction Progress at 16.7%

Construction Progress at 5.3%

Construction Progress at 34.5%

BOD approved Project

BOD approved EPC + Construction

BOD approved EPC + Construction

BOD approved Project

BOD approve EPC

BOD approve EPC

Construction

Construction

2013 2015 - 2018 2014

Construction Progress at 95.3%

Target COD: 2Q/14

Synergy

Pure H2 via New PSA

Off Gas upgrading at Olefins

Construction Progress at 43.15%

Target COD: 4Q/14

Seek for additional and opportunities Synergy Benefits

Note: Progress as of Jan. 2014

>> Execution of Core uplift Projects according to Target

>> New Products: Screened Products for Further Feasibility Study

35

CORE UPLIFT 1-STEP

ADJACENCIES GREEN

New Products | New Geographies

PC Compounding

Commodity Compounding

1st Screen for Further Feasibility Study

Not qualify for 1st Screen

New Application Compounding

Using additives and modifiers to result with a particular color, texture, strength, and etc.

Blending two or more types of polymers together

Polymer Compounding

PU Chain System House HDI Derivatives

Bio-plastics Compounding

Ethylene

HDPE

LLDPE

LDPE

MEG

Propylene

Oleochemicals

Paraxylene

Benzene

PTA

Polyester Fiber

EO

Ethanolamine

Ethoxylate

Cyclohexane

Cumene

Phenol

Acetone

EB/SM

PS

BPA

Methyl Ester(B-100)

PC

Caprolactam Nylon 6

Fatty Alcohol

MMA PMMA

Epoxy Resins

ABS

SBR

PET Resin

PTT Phenol

- LPG

- Reformate

- Light Naptha

- Jet Fuel

- Diesel

- Fuel Oil

Toluene

PO

Mixed C4 Butadiene

Polyols

PP

System

House

HDI

TDI

PU

HDMA

Orthoxylene PA

Plasticizer

PLA Plant PLA

Succinic Acid Plant Succinic Acid

Petroleum

Products

Nylon 6,6

Adipic AcidPhenol

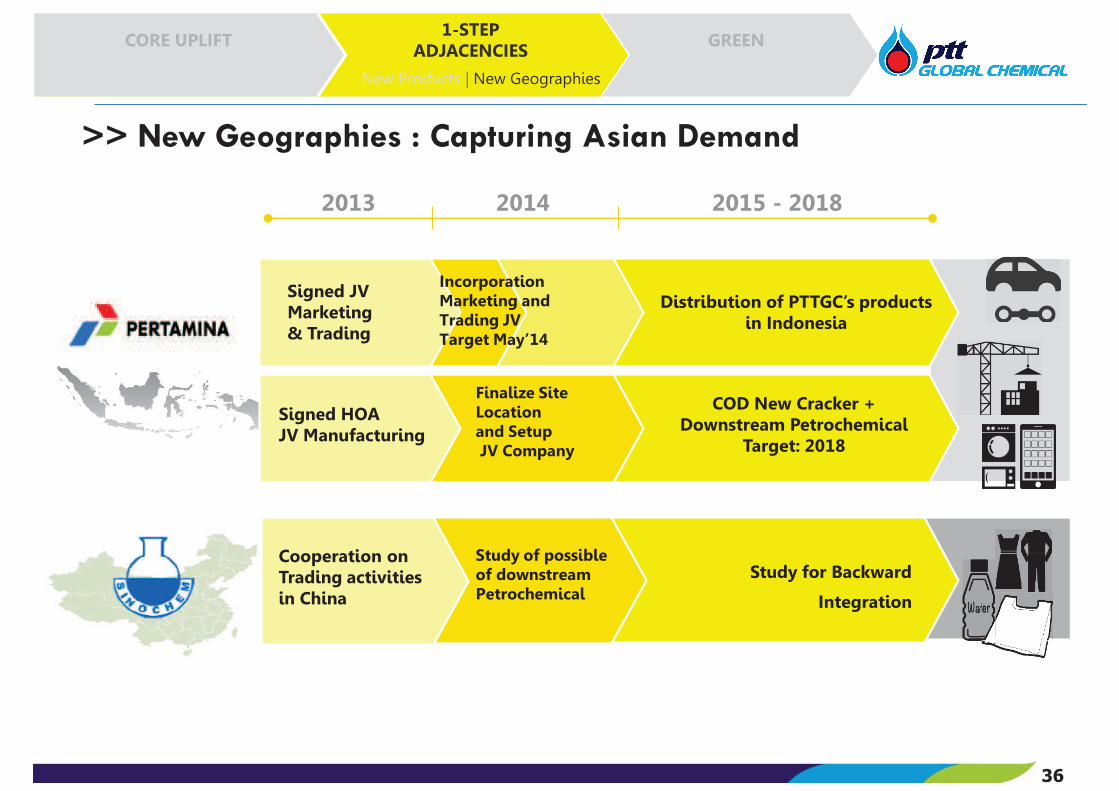

>> New Geographies : Capturing Asian Demand

36

CORE UPLIFT 1-STEP

ADJACENCIES GREEN

New Products | New Geographies

Signed HOA JV Manufacturing

2013 2015 - 2018 2014

COD New Cracker + Downstream Petrochemical

Target: 2018

Distribution of PTTGC’s products in Indonesia

Finalize Site Location and Setup JV Company

Study for Backward

Integration

Cooperation on Trading activities in China

Study of possible of downstream Petrochemical

Signed JV Marketing & Trading

Incorporation Marketing and Trading JV Target May’14

>> Green Business Roadmap

37

CORE UPLIFT 1-STEP

ADJACENCIES GREEN

New Products | New Geographies

Succinic Acid

(SAC)

Butanediol

(BDO)

Poly butylene

Succinate (PBS)

PLA/PBS

Compound

Lactic Acid

(HLA)

Poly Lactic Acid

(PLA)

Acrylic Acid

Corn/

Sugars

Cellulosic

FeedstockPolyacrylic

Acid/Acrylic ester

PLA Resin

Co

Su

PTTGC holds 50% in NatureWorks. A manufacture of polylactic acid (PLA) and lactides,

plant-based biopolymers used to manufacture plastics and fibers with world scale PLA

capacity of 150,000 ton/year. n Planned to build second plant potentially in Asia n Studied the possibilities to use alternative feedstock

PTTGC holds 84.21% in Myriant Corporation. An R&D based company with proven

technology platform.

§ In April 2013, Myriant Corporation had completed the construction of a 14,000 ton/year Succinic Acid Plant in Louisiana State and is currently commissioning.

ABSORBANT MATERIAL

35 41

240 231

101 116

60 44

238 245

137 120

61 67

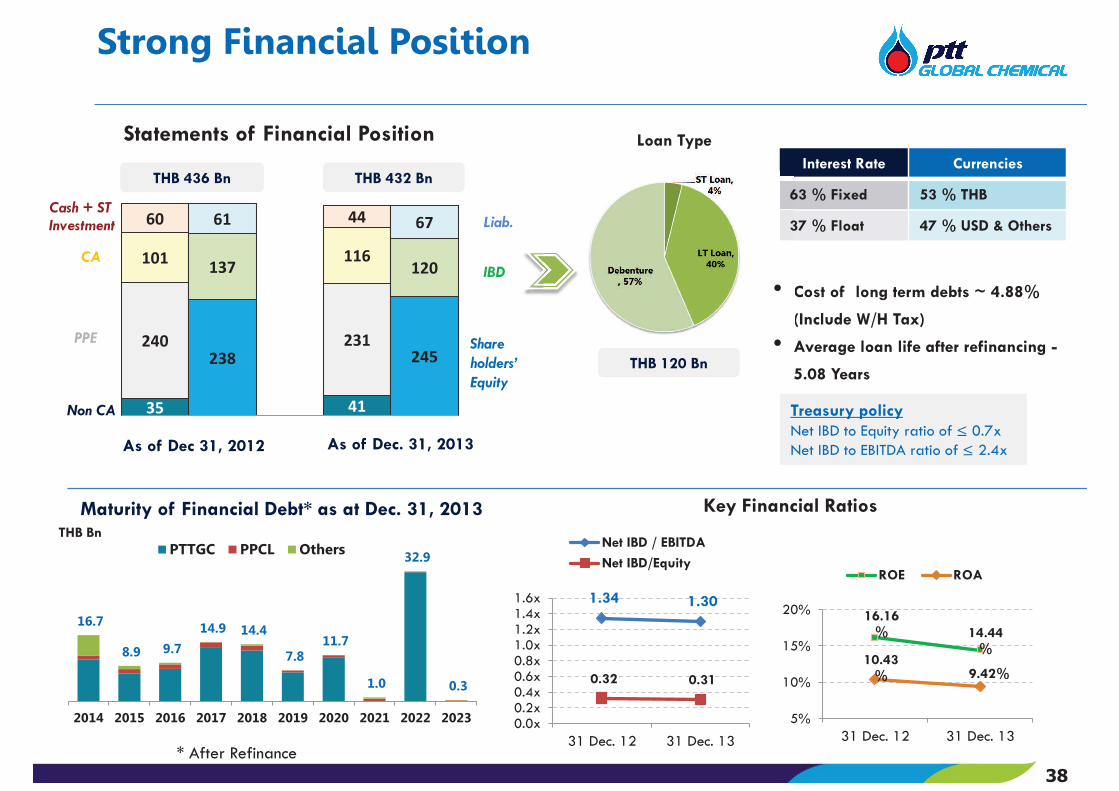

Strong Financial Position

38

Key Financial Ratios

As of Dec 31, 2012 As of Dec. 31, 2013

THB 432 Bn THB 436 Bn

Cash + ST Investment

CA

PPE

Non CA

Share

holders’

Equity

IBD

Liab.

Statements of Financial Position

Interest Rate Currencies

63 % Fixed 53 % THB

37 % Float 47 % USD & Others

Loan Type

• Cost of long term debts ~ 4.88%

(Include W/H Tax)

• Average loan life after refinancing -

5.08 Years

Treasury policy Net IBD to Equity ratio of ≤ 0.7x Net IBD to EBITDA ratio of ≤ 2.4x

Maturity of Financial Debt* as at Dec. 31, 2013

THB 120 Bn

THB Bn

* After Refinance

6

3

• C

16.7

8.9 9.7

14.9 14.4

7.8 11.7

1.0

32.9

0.3

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

PTTGC PPCL Others

1.34 1.30

0.32 0.31

0.0x0.2x0.4x0.6x0.8x1.0x1.2x1.4x1.6x

31 Dec. 12 31 Dec. 13

Net IBD / EBITDA

Net IBD/Equity

16.16% 14.44

% 10.43

% 9.42%

5%

10%

15%

20%

31 Dec. 12 31 Dec. 13

ROE ROA

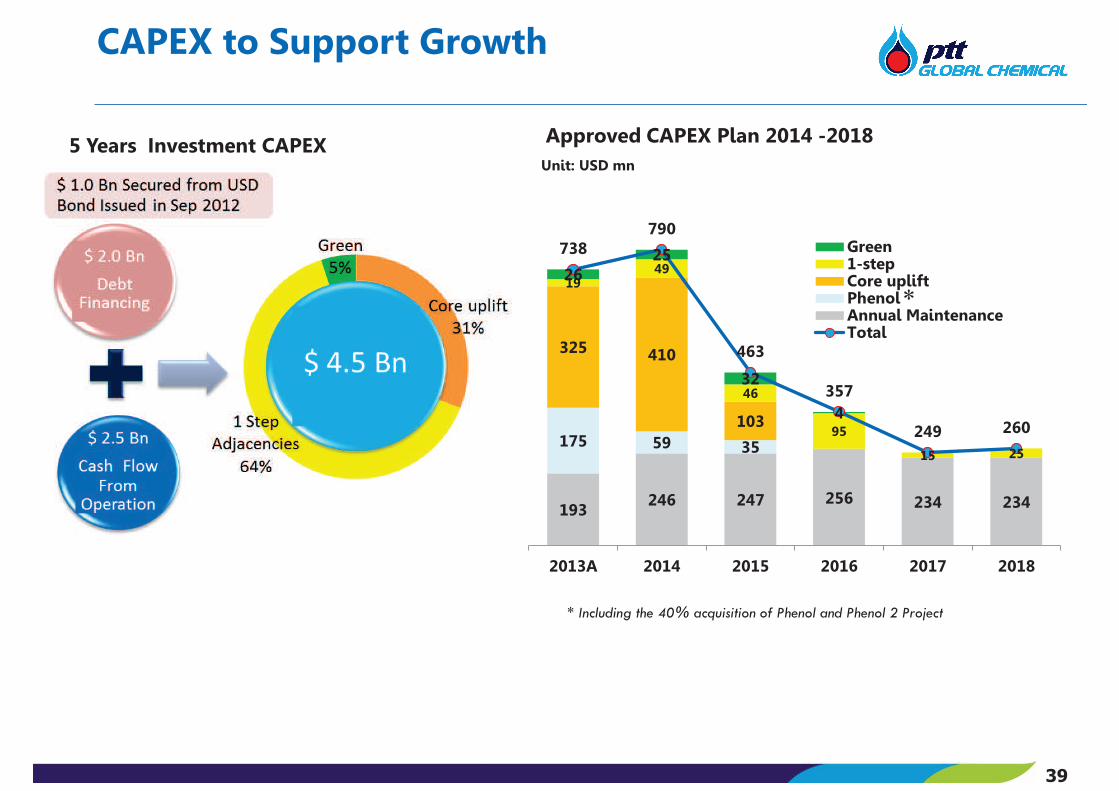

CAPEX to Support Growth Approved and Uncommitted CAPEX Plan for year 2013 - 2017

39

Approved CAPEX Plan 2014 -2018

Unit: USD mn5 Years Investment CAPEX

193 246 247 256 234 234

175 59 35

325 410

103

19 49

46

95

15 25

26 25

32

4

738 790

463

357

249 260

2013A 2014 2015 2016 2017 2018

Green1-stepCore upliftPhenolAnnual MaintenanceTotal

* Including the 40% acquisition of Phenol and Phenol 2 Project

*

Agenda

q Overview of PTTGC

q Basic Knowledge of Petrochemical Industry

q Competitiveness and Key Driver

q Strategy and Execution

q Conclusion

q Appendix

40 40

Commodity Chemical Competitiveness Criteria

41

• Thailand’s largest ethane-base cracker with integrated aromatics and refining businesses

• Highly competitive cost structure with pricing arrangement for gas feedstock based upon

equitable return on investment for both PTT and PTTGC

• Fully integrated petrochemical and refinery operations with diversified product portfolio

covering full hydrocarbon chain

• Strong footprint in fast growing regions with 5 operating countries worldwide

• Committed to operational excellence targeting best in class/ first quartile business efficiency

• PTT’s Chemical Flagship

Overview of PTTGC

42 42

43

For further information & enquiries, please contact our Investor Relations Team at [email protected]

Thank You

1 Thitipong Jurapornsiridee VP - Corporate Finance & IR [email protected] +662-265-8574

2 Puvadol Vasudhara IR Manager [email protected] +662-140-8712

3 Panugorn Puengpradit IR Analyst [email protected] +662-140-8714

4 Prang Chudasring IR Analyst [email protected] +662-265-8327

5 Chutima Jarikasem IR Coordinator [email protected] +662-140-8713