24

Overview of the Mexican Payments Systems: Challenges and Opportunities Lorenza Martínez Trigueros Director General of Payment Systems and Corporate Services February 2015

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | aracely-ancell |

| View: | 214 times |

| Download: | 0 times |

Overview of the Mexican Payments Systems: Challenges and OpportunitiesLorenza Martínez Trigueros Director General of Payment Systems and Corporate Services February 2015

2

Outline

1. Mexican retail payments

2. Limited adoption of payments

3. Bank of Mexico’s role

4. Opportunities

5. Final remarks

3

Mexican retail payments

• By reducing transaction costs, more efficient and reliable payments help to allocate resources more efficiently, which brings about higher social welfare.

• The challenge is to achieve efficiency in electronic payments such that they can be made anywhere, any time and of any size.

• As payment regulators, we care about ensuring the sound development of these payments so that their benefits materialize.

4

Mexican retail payments

Source: Red Book, BIS.

5

Mexican retail payments

Source: Red Book, BIS. nav – not available

Cards infrastructure, 2013

Country Number of cards per capita

Number of POS per million of inhabitants,

Dec. 2013

Card payments per capita

Number of ATM per million of

inhabitants, dec 2013

Cash withdrawals per capita

Korea 5.0 41,575 228.5 2,474 navAustralia 2.7 34,704 228.5 1,304 navItaly 1.2 26,112 29.9 825 13United Kingdom 2.4 25,807 181.1 1,060 45Canada 3.0 23,615 224.8 1,852 navSweden 2.3 22,261 248.6 337 23France 1.3 20,512 136.7 895 25Switzerland 1.9 20,474 88.7 843 15United States 3.8 16,978 248.3 1,385 navNetherlands 1.8 14,807 169.5 439 23Belgium 1.8 12,275 119.5 1,333 38Germany 1.6 9,057 44.7 1,009 26Mexico 1.1 5,798 14.6 342 13

6

• In spite of progress observed, Mexico still lags behind other economies in the usage of electronic payments.

• Mexico fares better when credit transfers are considered only.

Mexican retail payments

Per-capita electronic payments in emerging and developed economies1/

Number of yearly per-capita payments

Source: BIS. Electronic payments defined as the sum of the number of credit transfers, direct debits, E-money payment transactions and card payments.1/ Countries in the sample: Australia, Belgium, Brazil, Canada, China, France, Germany, India, Italy, Japan, Korea, Mexico, Netherlands, Russia, Saudi Arabia, Singapore, South Africa, Sweden, Switzerland, Turkey, (not considered in credit transfers due to the lack of data), United Kingdom, United States (except 2013).

0

100

200

300

400

500

600

700

800

2009 2010 2011 2012 2013

Mexico Average

690%

903

%

0

20

40

60

80

100

120

2009 2010 2011 2012 2013

Mexico Average

368 %

427

%

Per-capita credit transfers in emerging and developed economies1/

Number of yearly per-capita transfers

7

Outline

1. Mexican retail payments

2. Limited adoption of payments

3. Bank of Mexico’s role

4. Opportunities

5. Final remarks

8

• Adoption of electronic payments is still limited despite observed improvements. Issues to be tackled: Low financial inclusion Mistrust of payment schemes or banks Payment infrastructure is missing or insufficient in some areas Access to payment services could be expensive Electronic payments are rarely used by the informal sector Adoption of fraud prevention schemes and security standards

• Interoperability should be supported among payment-service providers offering the same type of service, without discourage innovation. Issues to be tackled: Entry barriers to potential new participants Increasing competition

• The legal framework should keep up pace with innovation to enable the sound development of more efficient payment alternatives (e.g., e-money). Issues to be tackled: Policies oriented to improve infrastructure Policies oriented to get faster payment systems

Limited adoption payments: Issues to be tackled

9

Outline

1. Mexican retail payments

2. Limited adoption of payments

3. Bank of Mexico’s role

4. Opportunities

5. Final remarks

10

Bank of Mexico’s role in retail payments: overview

• One of Bank of Mexico´s objectives is to promote the sound development of payments systems, on that regard it plays different roles: Operates the RTGS (SPEI), the backbone of the Mexican payments systems, not only for

large but also for retail payments transactions. Regulates the retail payments systems: Electronic funds transfers, card payments, direct

debits and checks. Bank of Mexico has issued regulation in order to promote transparency in fees and competition among clearing houses processors. • Mobile payments clearing houses rules, requirements for authorization and

technical specifications for the interoperability among such entities (SPEI).• Card payments clearing houses rules, requirements for authorization and technical

specifications for the interoperability among such entities.

• Regulatory changes have facilitated the entry of new participants, aggregators (i-Zettle, Pago Fácil, Mercado Pago, etc.), clearing houses, (two in process of authorization), new non-bank issuers and specialized companies in card processing (issuing and acquiring).

11

• Since 2005, Bank of Mexico operates the SPEI, a real time settlement system (RTGS).

• The use of SPEI, in conjunction with other policies of the Central Bank to promote more efficient means of payment, has allowed a sustained growth of electronic payments in the last years.

• Retail payments have progressively gained importance in Mexico.M

ar-0

5

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

0

20,000

40,000

60,000

80,000

100,000

Direct debit Cards SPEI1/ (<7,500 USD2/) Electronic Funds Transfers T+1

Bank of Mexico’s role in retail payments: operator

Electronic payments Billions of USD

Source: Bank of Mexico. 1/ Third-party payments: those which are both sent and received by SPEI participants on behalf of their clients. 2/ Calculated with the average exchange rate of October 2014.

Average Annual

Growth Rate

5%

44%

19%

26%

12

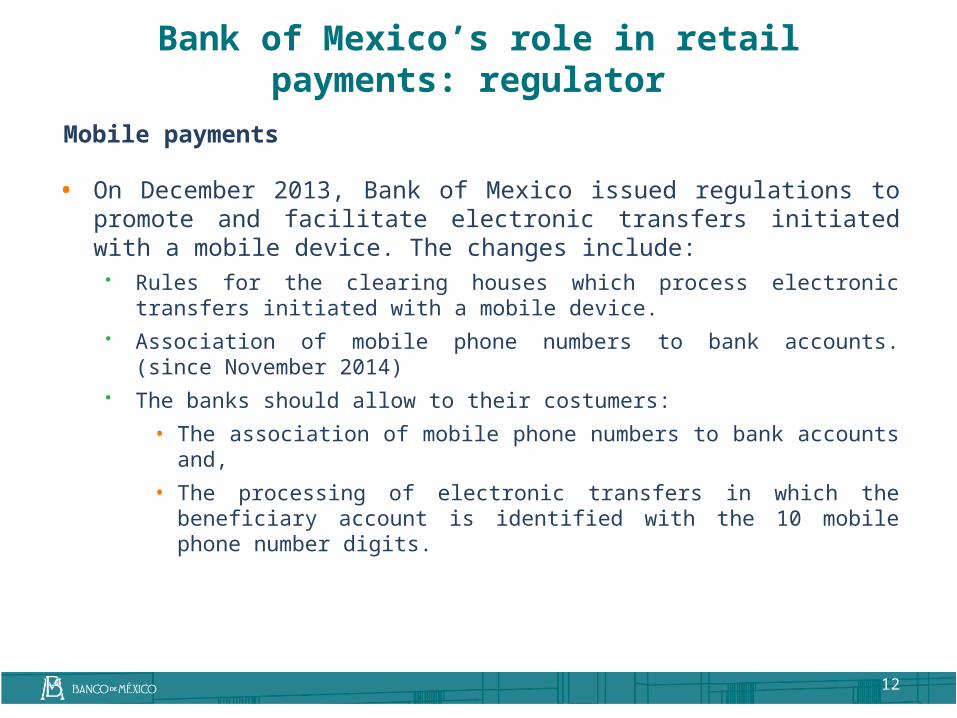

Bank of Mexico’s role in retail payments: regulator

Mobile payments

• On December 2013, Bank of Mexico issued regulations to promote and facilitate electronic transfers initiated with a mobile device. The changes include: Rules for the clearing houses which process electronic transfers initiated with a mobile

device. Association of mobile phone numbers to bank accounts. (since November 2014) The banks should allow to their costumers:

• The association of mobile phone numbers to bank accounts and, • The processing of electronic transfers in which the beneficiary account is identified

with the 10 mobile phone number digits.

Mobile payments

• Extended hours of operation and reducing processing times of mobile payments through SPEI. Service hours 11.5x7. (January 2015) Service hours 20x7. (March 2015) Service hours 24x7. (November 2015) The processing timeframe could take up to 15 seconds. (May 2015)

• 5 sec. Issuer bank • 5 sec. SPEI • 5 sec. Receiving bank

13

Bank of Mexico’s role in retail payments: regulator

14

Bank of Mexico’s role in retail payments: regulator

Tiered-system accounts

• Introduced in 2011 to enable banks to offer more flexible payment and financial products.

• Four tiers, from lower to higher functionality and from looser to stricter KYC & AML/CFT requirements.

Tier Max. monthly deposits

Max. account balance

Debit cards Electronic fund transfers**

Checks

1* 272 USD 363 USD

2 1,088 USD NA

3 3,625 USD NA

4 NA NA

* Only for domestic transactions. ** Includes direct debits, Internet and mobile payments origination .

15

Bank of Mexico’s role in retail payments: regulatorBasic accounts

• Must be offered by all banks since 2007

• Most services are free: Opening or closing the account Debit card Cash withdrawals & balance enquiries at bank’s branches or ATMs Direct debits Balance check

• There’s evidence that mandating basic accounts in Mexico has contributed to financial inclusion by enabling users to access more sophisticated financial services.1/

• Still, authorities could play a more active role in publicizing basic accounts, since branch employees sometimes don’t offer them.2/

1/ Kaiser K., Lever C., Salcedo A. (2011), “On the Impact of Mandatory Basic Accounts on Financial Development: Evidence from Mexico”, mimeo, Banco de México2/ Giné X., Martínez C., Keenan R. (2014), “Financial (Dis-)Information: Evidence from an Audit Study in Mexico”, The World Bank

16

Card payments clearing houses

• In order to accomplish the financial reform published in January 2014, in March 2014, Bank of Mexico issued: The rules for the organization and operation of card clearing houses, requirements for

authorization and technical specifications for the Interoperability among such entities.• Avoid establishment of entry barriers • Avoid market distortions and lack of transparency • Promote innovation • Improve security and risk management • Allow clearing houses to contract with third parties the provision of routing services,

clearing and settlement.• Allow clearing houses to charge in proportion to the payment amount.

Bank of Mexico’s role in retail payments: regulator

17

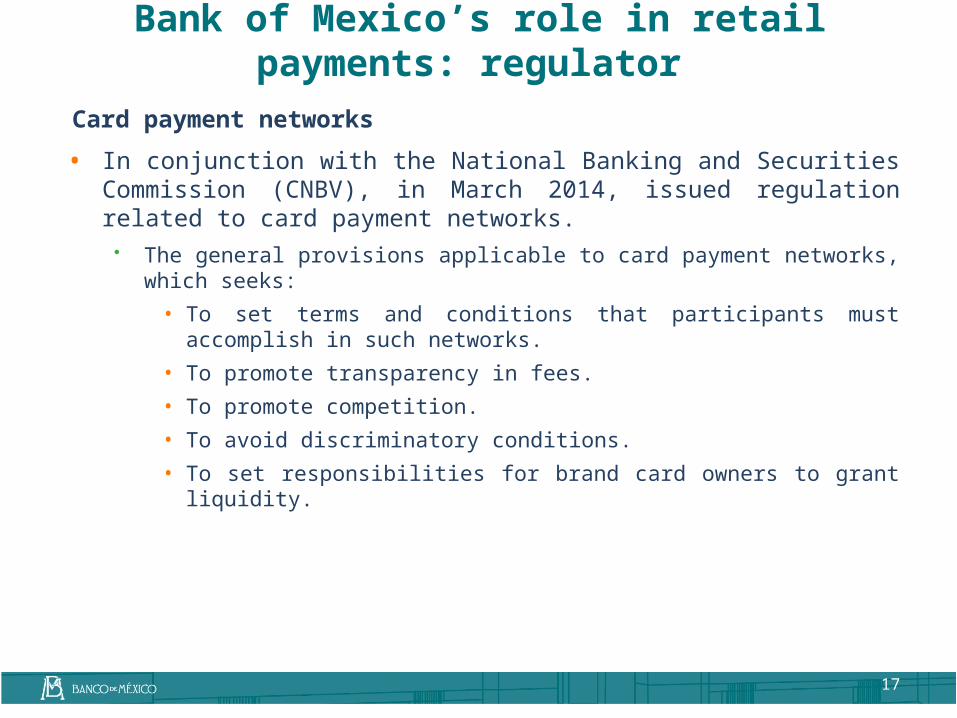

Card payment networks

• In conjunction with the National Banking and Securities Commission (CNBV), in March 2014, issued regulation related to card payment networks. The general provisions applicable to card payment networks, which seeks:

• To set terms and conditions that participants must accomplish in such networks.• To promote transparency in fees.• To promote competition.• To avoid discriminatory conditions.• To set responsibilities for brand card owners to grant liquidity.

Bank of Mexico’s role in retail payments: regulator

18

Outline

1. Mexican retail payments

2. Limited adoption of payments

3. Bank of Mexico’s role

4. Opportunities

5. Final remarks

Opportunities: mobile payments

19

• Besides P2P payments, mobile payments have potential to broaden P2B electronic payments, in addition to card payments.

• There has been a growth in value and volume of the transactions made through a mobile device; regulation is expected to incentivize higher growth.

• In Mexico, the mobile phone has, by far, a greater presence and is more affordable than a computer for most population (over 80% of the population have a mobile phone), which allows new schemes for sending and receiving payments.

Year Population (millions)

Mobile phone contracts subscribed (millions)

Contracts per capita

2005 103 47 0.52006 104 55 0.52007 105 67 0.62008 106 75 0.72009 107 83 0.82010 108 91 0.82011 109 95 0.92012 116 101 0.92013 118 105 0.9

Source: Bank of Mexico. 1/ Transactions made thorough phones or mobile devices include: transfers, payments in businesses and other operations such as payments of services

Opportunities: card payments

20

• As it can be observed, the reforms and policies implemented by Bank of Mexico in recent years, have opened the possibility for new entities to participate in the Mexican payments market.

• There is also a potential for growth on card payments transactions.

• The regulation, promotes the entrance of new participants: clearing houses, specialized service providers, aggregators, acquirers, issuers, etc.

• Although there has been an important growth in the card payments, Mexico is still fallen behind respect other countries. It is expected that these recent improvements promote further growth of card payments.

Country GNI per capita Card payments per capita

Korea 33,440 228.5Australia 42,450 228.5Italy 35,540 29.9United Kingdom 38,160 181.1Canada 42,610 224.8Sweden 46,680 248.6France 38,530 136.7Switzerland 59,210 88.7United States 53,750 248.3Netherlands 46,400 169.5Belgium 41,240 119.5Germany 45,620 44.7Mexico 16,110 14.6Source: World Bank and Red Book, BIS.

• The National Banking and Securities Commission issued regulations to allow outsourcing some banking services to banking agents, to broad access and to reduce costs. Banking agents can take cash and check deposits, commercialize banking cards related with

accounts type 1 and open accounts type 2 and 3, pay remittances, cash withdrawals . Banks are responsible that the banking agents comply with all the regulation requirements

in the banking services they provide. Banks need authorization of the National Banking and Securities Commission to hire banking

agents.

• The regulation has been useful to widen access. When the regulation was issued, there were around 11 thousand bank branches and some

unregulated service points with very limited services. Since then there have been 15 banks authorized to work with banking agents with more

than 26 thousand service points. Currently a banking agent (convenience store) has been opening an average of 5 thousand

account type 2 per day.

21

Opportunities: banking agent

Infrastructure 2010 2014 Average growth (2010-2014)

POS 482,299 872,865 16%

Branches 11,291 12,715 3%

Banking agents 9,137 26,857 31%

ATM 35,936 42,643 4%

Source: Bank of Mexico and National Banking and Securities Commission.

22

Outline

1. Mexican retail payments

2. Limited adoption of payments

3. Bank of Mexico’s role

4. Opportunities

5. Final remarks

23

Final remarks

• The Bank of Mexico has followed two strategies to enhance the availability, reliability and convenience of electronic payments:

Exploit economies of scale and scope of SPEI Improve the regulation for privately-run payment services and

providers

• Coordination with the industry is necessary to ensure that society enjoys the benefits from more efficient payment alternatives.

• Payment authorities should continue to strengthen incentives to use electronic payments, particularly for those currently excluded from formal financial services.