PAKISTAN The Tech Boom and Chinese Investment Wave INITIATION REPORT We initiate research coverage on Pakistan. We think structural drivers such as favourable demographic trends, increasing digitalization and infrastructure investment from China could help sustain around 6% GDP growth over the next three to five years. We think the market is ignoring the multiplier impact from technology led productivity gains and infrastructure investments. KSE100 Index is up 15x over the last 15 years and more than +230% since 2012. However, trading at 8x forward PE and dividend yields of 5% with near ROEs of close to 20%, Pakistan is still significantly under owned and undervalued. In this report, we have done a deep dive on the potential from digitalization which we think will be one of the main catalysts for attracting foreign investments and growth over the next 12-24 months. Our favourite companies are 1) MCB – Bank 2) Indus Motors – Autos 3) OGDC – Oil and Gas and 4) Pakistan Stock Exchange - Diversified Financials.

Transcript

PAKISTAN The Tech Boom and Chinese Investment Wave

INITIATION REPORT

We initiate research coverage on Pakistan. We think structural drivers such as favourable demographic trends, increasing digitalization and infrastructure investment from China could help sustain around 6% GDP growth over the next three to five years. We think the market is ignoring the multiplier impact from technology led productivity gains and infrastructure investments. KSE100 Index is up 15x over the last 15 years and more than +230% since 2012. However, trading at 8x forward PE and dividend yields of 5% with near ROEs of close to 20%, Pakistan is still significantly under owned and undervalued. In this report, we have done a deep dive on the potential from digitalization which we think will be one of the main catalysts for attracting foreign investments and growth over the next 12-24 months. Our favourite companies are 1) MCB – Bank 2) Indus Motors – Autos 3) OGDC – Oil and Gas and 4) Pakistan Stock Exchange - Diversified Financials.

1

Oxford Frontier is a fintech focused investment research and advisory firm focusing on frontier markets such as Pakistan and MENA. Our office address is: 3/31 Emperors Gate, London, SW7 4JA and KASB Securities, 14/C Bukhari Tower, Khayaban e Bukhari, Karachi, Pakistan.

_

_

1

1

Over the next 6 months, Pakistan will go through a change in the government. Political transitions are often both noisy and messy. Like in previous cycles, the interim government could have to deal with difficult fiscal and monetary adjustments. We expect another -10% PkR adjustment and a further +0.75% rate hike by the end of the year. The adjustment along with political noise, could make the market volatile over the next 12 months. However, historical precedent suggests that such corrections, are good entry points. KSE100 Index is up 159% over the past 5 years and 15x over 10 years. We think structural factors, such as increasing urbanization due to a growing young population, infrastructure investment under the Chinese One Belt & Road Initiative and growing digitalization, would drive corporate earnings (+10% CAGR over 2017-2020). We think the market is ignoring the potential multiplier impact from digital transformation and investment inflows from regional tech companies.

▪ A hard country. Despite mostly getting negative media coverage, Pakistan is an attractive growth market. Its GDP of $304bn GDP is growing by +6% FY18e, it has a large and young population (200m, +2% growth) and a rising urban middle class. Contrary to its allocation (0.1%) in MSCI EM index, Pakistan has a reasonably liquid (ADV of $100m), deep (c600 listed companies) and open stock market (40% owned by Shanghai Stock Exchange, no restrictions on ownership and capital flows). We think, Pakistan offers very attractive returns with 20% RoE, 5% dividend yield, trading at 8x PE; a 20% discount to its EM peers.

▪ Political noise and balance of payment adjustment could make the market choppy. However, the economy typically goes through such cycles after every 4 years, usually around the time of government change. This time we think two structural drivers, the Chinese infrastructure investment and growth in the digital economy could outweigh cyclical downturn.

▪ China investments of $60bn+ in infrastructure are under appreciated. Under the One Belt and Road (OBR) plan, the Chinese government has committed to invest around $60bn, mainly in infrastructure projects such as energy, roads, railways and port. This investment has led to a trade deficit in the short term however mid to long term it could transform the economy.

▪ Digitalization could drive productivity gains and M&A. Pakistan is currently the fastest growing market globally in mobile internet penetration (51m). We think mobile internet users can cross 100m over the next 24-36 months, which could attract regional tech giants such as Alibaba, Tencent, and Softbank. Alibaba and Ant Financial are reported to be finalizing acquisitions of two domestic companies, which we think would be a key catalyst for attracting additional investments.

Pakistan: Digitalization & CPEC - the primary structural drivers

Digitalization & CPEC to drive growth

Initiation report on Pakistan

1st March 2018

Our preferred top picks:

P/E P/BV ROE DY

Market Cap ($m) 2018E 2019E 2018 2018 2018

MCB 2,365 10.5 9.1 1.53 15% 7.4%

Indus 1,214 9.5 9.4 3.7 44% 7.4%

PPL 3,558 9.3 8.3 1.7 17% 4.5%

PSX 177

Source: Bloomberg

2

1

1st March 2018

Initiation report on Pakistan

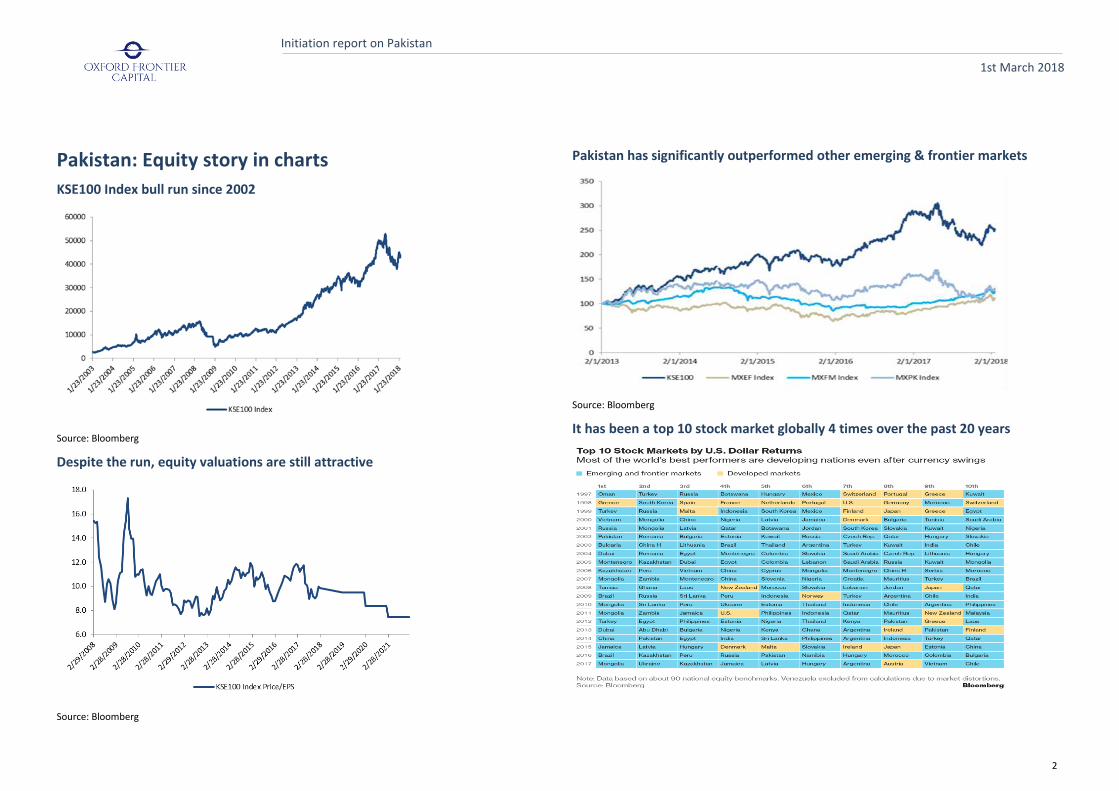

Pakistan: Equity story in charts

KSE100 Index bull run since 2002

Source: Bloomberg

Despite the run, equity valuations are still attractive

Source: Bloomberg

Pakistan has significantly outperformed other emerging & frontier markets

Source: Bloomberg

It has been a top 10 stock market globally 4 times over the past 20 years

3

1

1st March 2018

Initiation report on Pakistan

The Digital Transformation

▪ In our opinion, Pakistan is globally the most exciting market for digital adoption. It is the fastest growing market for internet adoption with more than 1m people getting connected via mobile broadband every month (click here). Internet penetration has increased from a mere 133,000 in 2000 to over 51m by the end of 2017. We expect another 50m users to move to 4G over the next 24-36 months. We think this shift to the digital economy could lead to transformational changes in sectors such as retail, financial services, healthcare, education and logistics.

▪ Pakistan has a large, young and growing middle class. More than 65% of the population is below the age of 30 and according to market research it has a middle class of around 38m, which is greater than the entire population of countries like Italy, Germany, the UK and Turkey (click here). Pakistan is the sixth largest country in the world, with 207m people, growing by 2%. Its GDP per capita of $1,470 (global rank: 137) is in similar range to countries like India ($1,741) and Bangladesh ($1,357) (click here). GDP growth has averaged over 4% over the past ten years and is expected to reach 6% in 2017/18.

A young and growing population 70% of the population is below 30 years of age (CAGR)

Source: Pakistan Economic Survey

▪ In our view the primary structural growth driver for the economy is the growth in urban population, which has increased from 32% of population in 1998 to around 40% of population by 2017. Urban population is expected to continue to grow by 2.7% and reach 50% of the population by 2025. Most academic research shows a strong positive relationship between rate of urbanization and economic growth (click here) and some indicate that every +1% growth in urban population leads to +1.3% growth in the GDP.

▪ The dividends from favourable demographics are visible in the retail sector, where Pakistan is expected to be the one of the fastest growing market in the world. According to Euromonitor, Pakistan’s retail sector revenues are expected to increase by over +8% CAGR over 2016-2021 and the number of retail stores are expected to increase by 50% over this period to 1m outlets. Similarly, the food sector has been growing by more than 25% and global companies such as Yum Food are expanding their network. Pizza Hut expects to double its outlets to 150 over the next five years (click here).

Pakistan is one of the fastest growing retail markets in the world Expected growth in retail sales over 2016-21 (CAGR)

Source: Euromonitor

▪ We think the increase in mobile internet penetration would lead to exponential growth in digital industries, ranging from ecommerce, media, logistics and financial services. Besides leading to productivity gains such as lowering cost of sales and marketing and expanding distribution coverage, the growth in the internet connectivity will also attract much needed foreign investment. E-Bay’s CEO called Pakistan one of the fastest

markets at the World Economic Forum in 2017 and Alibaba’s Jack Ma announced his plans to enter the market. According to press reports both Alibaba and Ant Financial are in final stages of acquiring domestic ecommerce and payments companies respectively. We think their entry will encourage other companies such as Tencent, JD.com, Naspers and Softbank to make strategic acquisitions to gain a foothold in the growing market.

The country has all the pre-conditions for enabling IT growth

▪ Pakistan has a vibrant technology industry which employs around 300,000 IT professionals. There are around 2,000 IT and business processes outsourcing registered companies. The country ranks 4th globally in the number of people working as IT experts on freelancing platforms such as Upwork and Fivver and each year, 20,000 IT professionals enter the industry. According to recent data, software exports have reached $3bn in 2017, up from $2bn in 2015 and are expected to grow to $5bn by 2020.

▪ Pakistani IT circles folk fore includes the mention that the first ever anti-virus software was created by a Pakistani, which was used to kill the virus they had created themselves – the Brain Virus (click here). Two brothers, Basit and Amjad Alvi, then 17 and 24 years old, created the Brain virus in 1998 as a way to protect piracy of a software they had made.

▪ Most of the IT industry has been historically focused on IT services and business processing outsourcing, catering to foreign clients. According to the Ministry of Finance, domestic IT sales were for $500m in 2016 and exports were for $2.8bn. IT exports have grown by around 25% CAGR over the last four years. Going forward we expect stronger growth from domestic companies.

▪ The other favourable factors, besides the availability of talent, are a high mobile penetration and the presence of a digital ID scheme through National Database & Registration Authority (NADRA). Pakistan has one of the most successful digital ID projects in the world, similar to the Aadhar program in India. NADRA has issued more than 100m ID cards which are linked to biometrics. Over the past few years, the telecom regulator initiated a program to link telecom SIM with NADRA ID. This lowered the number of mobile subscribers to 145m which implies 72% mobile penetration. The linking of mobile numbers with NADRA card enables digital KYC and we think this would be a main catalyst for digitalization of financial services. NADRA issued card are already being used in a range of services from mobile banking to e-government initiatives and for distributing pensions and social aid.

▪ In a way, the developments in Pakistan are very similar to what happened in other regional markets such as India and China. These parallels are one of the reasons which makes us excited about Pakistan and we expect the country to go through a similar growth inflection over the next 12-18 months.

▪ The government is cognizant of the opportunity from digitalization and has taken an active approach to support the growth of the sector. The national Digital Pakistan Policy 2017 is targeting a 3x growth in ecommerce volumes over the next three years from its current size of around $100m. The government has given a three-year tax exemption for tech start-ups and also assists in seeding IT incubators and has established“software parks”.

▪ Besides favourable public policy, international donor agencies such as USAID, DFID and social development organizations such as Bill & Melinda Gates Foundation and Acumen fund are providing financial and operational support in areas such as fintech.

▪ The growth in internet penetration has had a very material impact on incumbent companies in the digital economy. For example, the leading ecommerce platform Daraz, owned by Rocket Internet, is now getting 10m unique visitors per month. There are around 40m Facebook users from Pakistan, which exceeds the total number of bank account holders and makes Pakistan, the 11th largest country in terms of Facebook population. Similarly, Whatsapp is quickly becoming the primary channel of communication and also for sharing of news.

▪ Pakistan has only just started to attract the interest of early stage VC investors. German listed, Rocket Internet was the probably the first mover and established ventures in ecommerce and food delivery. The crowdsourcing platform Angelist has more than 5000 angel investors from Pakistan, however the website only lists 9 who have made at least one investment. We tracked around 15 VC funds and incubators which focus on the market, however we suspect the capital deployed by them is less than $100m in total.

Top websites in Pakistan by number of daily unique visitors

Digital banking has already gained critical mass

▪ The government has initiated multiple initiatives to leverage on mobile connectivity to improve financial inclusion in the country. By end of 2015, only 23% of the population was using the formal financial channel and only 17% had a bank account. In 2008, State Bank of Pakistan (SBP), introduced regulation for Branchless Banking and issued four licenses. Initial regulation was too cumbersome and it was revised in 2011. SBP

Early Stage Incubators and Funds in Pakistan

Incubators

LUMS Center for Entrepeneurship (LCE) University hosted early stage incubator

Shell Tameer Social impact investment programme

Plan 9 State backed incubator under Punjab IT board.

Plan X Also operated by PITB. Focused on linking with global investors

National Incubation Center State owned and backed by telecom operators.

Karandaz Fintech focused incubator backed by Bill & Melinda Gates Foundation.

Nest I/O Karachi based incubator backed by Google.

Early Stage Investors/VC

Rocket Internet German listed company builder.

Vostok Emerging Finance Sweden listed fintech focused fund.

Dot Edu Ventures Silicon valley based fund investing in India and Pakistan.

Abraaj Capital UAE based private equity investor. Later stage investments.

Vostok NAFTA Sweden based investor in market places.

Piton Capital

Frontier Digital Venture Malaysian frontier market venture fund.

Planet N Fintech focused early stage investor.

Invest2Inovate Incubator and early stage investor.

Dot Zero Ventures Co-working space, and early stage investor, incubator.

47.Ventures Early stage venture investments with investment size of $50k - $2m.

Sabcon Ventures Co working space and early stage investments.

Sarmayacar Angel investor syndicate.

Bakery UAE based, emerging markets focused incubator, backed by Abraaj Capital

Fatima Ventures Corporate backed venture investor

Domestically registered VC funds

Ijaza Capital Fund focus on energy, healthcare, education, infrastructure and lifestyle

Lakhson Investments VC arm of a domestic asset management company.

Ithaca Capital PE/VC fund.

Source: Oxford Frontier

6

1

1st March 2018

Initiation report on Pakistan

introduced the concept of Level 0 account which allowed digital onboarding. This change has been critical for the growth in the market.

▪ Branchless banking licenses opened up financial services to telecom operator which were well capitalized and were owned by global telecom companies. Besides strong financial backing, almost all of the 5 telecom operators had experience of mobile payments in other markets. Telenor’s Easypaisa was the first mover and was initially used for peer to peer payments. Over time, additional features such as government to business payments, retail payments and utility bill payments have also been added.

▪ In 2017, there was more than 100% growth in the number of mobile banking subscribers, which increased to 33m, surpassing even Kenya’s 31m (led by Safaricom’s M-Pesa). In 2Q17, there were $7.5bn worth of transactions and $154m of deposits raised through digital banking. Collectively the mobile wallets have built a network of 402,710 agents throughout the country.

Branchless banking customer crossed 33m last year Number of people with digital bank accounts

Source: State bank of Pakistan

▪ Two telecom operators, Veon (Russian Vimplecom)’s Jazzcash and Telenor’s Easypaisa have 89% share of the mobile wallet market. Telecom operators have acquired Microfinance banks in order to expand into financial services. This is interesting since with the exception of Kenya, there have not been many markets where telco led mobile wallets have been very successful. Telenor acquired Tameer Microfinance bank and Jazz invested in Waseela Bank. Other emerging fintech companies have also taken this approach of partnering with microfinance banks instead of larger commercial banks.

According to press reports Ant Financial is considering purchasing a 47% stake in Easypaisa (click here).

Telecom operators dominate the market Jazzcash and Easypaisa are owned by telecom operators

Source: State bank of Pakistan

▪ The leading mobile wallets such as Jazzcash and Easypaisa now also offer ecommerce payment gateway, mobile payments platform, corporate payment solutions and have also expanded in offering insurance products. We think the product maturity of Pakistan’s mobile wallets, their vast agent network and the massive opportunity in targeting the under banked population, makes Pakistan a very attractive market for fintech focused investors. While cash on delivery is still the primary payment method for ecommerce, we expect mobile wallets to gain traction over the medium term.

▪ Another interesting development is the introduction of interoperability between the various mobile wallets which the SBP intends to introduce. Pakistan Telecom Authority (PTA) is in the process of awarding licensing to third party payment companies who will be able to act as the processor between multiple payment wallets.

▪ In 2017, SBP awarded payment service provider licenses to around 10 companies in order to facilitate the growth in digital marketplaces and ecommerce companies. The Government is targeting ecommerce market to grow to over $1bn by 2020.

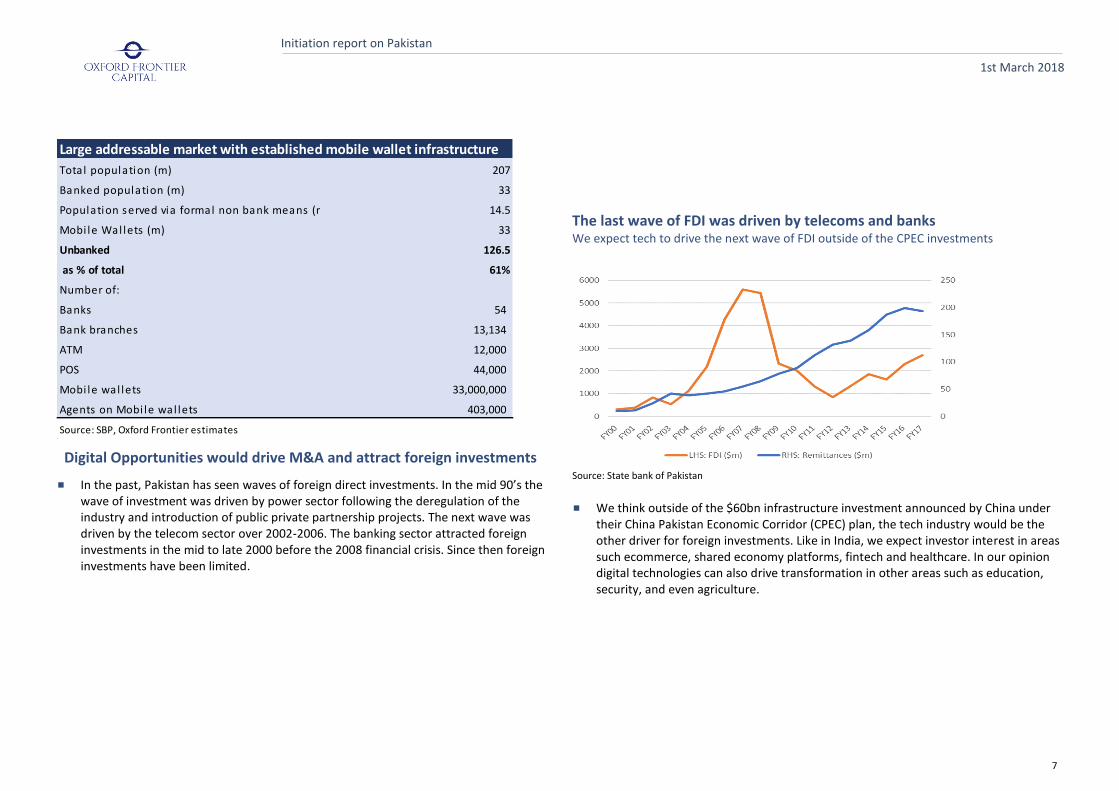

Digital Opportunities would drive M&A and attract foreign investments

▪ In the past, Pakistan has seen waves of foreign direct investments. In the mid 90’s the wave of investment was driven by power sector following the deregulation of the industry and introduction of public private partnership projects. The next wave was driven by the telecom sector over 2002-2006. The banking sector attracted foreign investments in the mid to late 2000 before the 2008 financial crisis. Since then foreign investments have been limited.

The last wave of FDI was driven by telecoms and banks We expect tech to drive the next wave of FDI outside of the CPEC investments

Source: State bank of Pakistan

▪ We think outside of the $60bn infrastructure investment announced by China under their China Pakistan Economic Corridor (CPEC) plan, the tech industry would be the other driver for foreign investments. Like in India, we expect investor interest in areas such ecommerce, shared economy platforms, fintech and healthcare. In our opinion digital technologies can also drive transformation in other areas such as education, security, and even agriculture.

Total population (m) 207

Banked population (m) 33

Population served via formal non bank means (m) 14.5

Mobi le Wal lets (m) 33

Unbanked 126.5

as % of total 61%

Number of:

Banks 54

Bank branches 13,134

ATM 12,000

POS 44,000

Mobi le wal lets 33,000,000

Agents on Mobi le wal lets 403,000

Source: SBP, Oxford Frontier estimates

Large addressable market with established mobile wallet infrastructure

8

1

1st March 2018

Initiation report on Pakistan

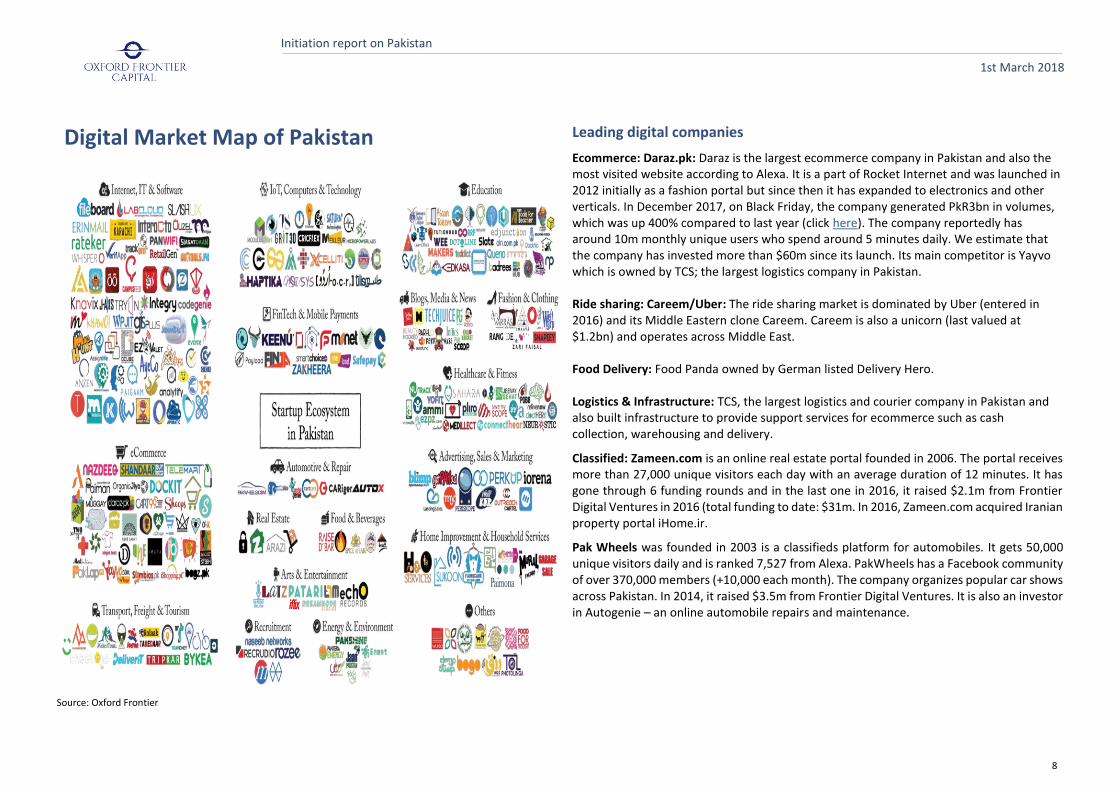

Digital Market Map of Pakistan

Source: Oxford Frontier

Leading digital companies

Ecommerce: Daraz.pk: Daraz is the largest ecommerce company in Pakistan and also the most visited website according to Alexa. It is a part of Rocket Internet and was launched in 2012 initially as a fashion portal but since then it has expanded to electronics and other verticals. In December 2017, on Black Friday, the company generated PkR3bn in volumes, which was up 400% compared to last year (click here). The company reportedly has around 10m monthly unique users who spend around 5 minutes daily. We estimate that the company has invested more than $60m since its launch. Its main competitor is Yayvo which is owned by TCS; the largest logistics company in Pakistan. Ride sharing: Careem/Uber: The ride sharing market is dominated by Uber (entered in 2016) and its Middle Eastern clone Careem. Careem is also a unicorn (last valued at $1.2bn) and operates across Middle East. Food Delivery: Food Panda owned by German listed Delivery Hero. Logistics & Infrastructure: TCS, the largest logistics and courier company in Pakistan and also built infrastructure to provide support services for ecommerce such as cash collection, warehousing and delivery.

Classified: Zameen.com is an online real estate portal founded in 2006. The portal receives more than 27,000 unique visitors each day with an average duration of 12 minutes. It has gone through 6 funding rounds and in the last one in 2016, it raised $2.1m from Frontier Digital Ventures in 2016 (total funding to date: $31m. In 2016, Zameen.com acquired Iranian property portal iHome.ir.

Pak Wheels was founded in 2003 is a classifieds platform for automobiles. It gets 50,000 unique visitors daily and is ranked 7,527 from Alexa. PakWheels has a Facebook community of over 370,000 members (+10,000 each month). The company organizes popular car shows across Pakistan. In 2014, it raised $3.5m from Frontier Digital Ventures. It is also an investor in Autogenie – an online automobile repairs and maintenance.

Growth at a reasonable price ▪ An under-owned market with attractive returns. Although Pakistan’s stock market has

been one of the best performing emerging market over the past 3, 5 and 10 years, it is relatively under-owned and offer attractive valuations. KSE100 Index is up +40% over the past 3 years and +340% since 2010. The market trades at 10x PE, which is a 20% discount to regional peers and has a dividend yield of 5% for around 20% RoE. Despite of this, foreign institutional have been net sellers over most of the past 3 years.

Foreign investors have been net sellers for most of the past 2 years Monthly net foreign portfolio investments ($m)

Source: SBP

▪ Healthy earnings growth. The rally in the equity market has been primarily driven by earnings growth as over 2012-17, nominal GDP growth was around +11% CAGR. Real GDP growth has averaged +4.2% per annum and is estimated to reach +6% in FY18 (year end May). The top 15 companies listed on the Karachi Stock Exchange, which account for 88% of the KSE30 and 70% of KSE100 Index, reported 10% CAGR in Earnings over 2010-16 even though the performance was hurt by the decline in earnings in oil and gas

companies due to declining oil prices. Excluding the oil and gas companies, corporate revenue growth averaged around 5% and Net Profits increased by 16% per annum over 2010-16. Going forward consensus expects 8% CAGR in earnings growth over the next three years. We think this is achievable, especially due to recovery in earnings growth in energy, financial and the auto sector.

▪ The upgrade to EM was downgrade to irrelevance. Last year, the market was upgraded to MSCI Emerging Markets Index, from Frontier Markets, on the back of a 5 year bull run over 2012-17, over which its benchmark’s index, the KSE100 increased by 263%. We suspect the upgrade went against the market as it had a prominent 7% allocation within the frontier market index (second after Kuwait), while in the Emerging Markets index, it has the lowest weight of 0.2% - which makes it too inconsequential from an asset allocation perspective. Only four stocks from the country are included in the MSCI Pakistan Index; three banks (HBL, MCB, UBL) and one oil and gas exploration company (OGDC). Nevertheless, even this index outperformed the MSCI EM and MSCI Frontier Market indices by 40% and 47% percent even in dollar terms since 2010.

Source: Zakheera.com, * the sample includes 28 companies (misses steel companies which listed recently)

10

1

1st March 2018

Initiation report on Pakistan

Pakistan has outperformed MSCI EM and MSCI FM indices Despite the volatility we expect the market to continue to outperform

Source: Bloomberg

▪ Low correlation with the global markets. Pakistan’s capital markets are unique on various factors. Firstly, unlike other frontier markets, it is fairly liquid ($100m average daily traded value) and deep (600 listed companies). Secondly, the market is quite diversified in terms of sector representation. Unlike most emerging markets, the economy is not driven by commodity exports or driven by foreign trade. In the benchmark KSE100 Index, Commercial Bank is the largest sector with a 25% weight, followed by Oil and Gas sector (exploration and distribution) at 20%, Cement 9% and Fertilizers at 12% and Power sector has 6% weight. Thirdly, the stock market also has low correlation with the regional and global markets.

The last wave of FDI was driven by telecoms and banks We expect tech to drive the next wave of FDI outside of the CPEC investments

Source: Zakheera

▪ Structural bull run since 2002. The stock market was opened to foreign investors in 1992 and the first wave of privatization along with the emergence of global interest in Asian markets drove the first wave of investor interest in the market. However, it wasn’t until 2002, when the market got critical momentum due to listing of state owned entities which attracted domestic retail participations. Since then, the stock market is up 15x. During this period, there have been corrections in 1999, 2004, 2008, 2015 and recently in 2017.

Pakistan has low correlation with regional markets

MSCI EM MSCI FM S&P500 SXEE Oil

Pakistan KSE100 0.107 0.13 0.12 0.05 0.07

India Sensex 0.54 0.35 0.44 0.36 0.134

Brazil IBOV 0.4 0.31 0.4 0.4 0.231

Egypt EGX30 0.08 0.01 0.2 0.08 0.02

Thailand SET 0.42 0.35 0.5 0.43 0.11

UAE DFMGI 0.45 0.2 0.36 0.45 0.201

Source: Bloomberg

11

1

1st March 2018

Initiation report on Pakistan

▪ The usual downside risks. Almost all of the downturns, including the recent one have been accompanied by political uncertainty, external exogenous economic shocks, balance of payments gap, foreign exchange crunch and exchange rate depreciation. As 2018 is going to be the election year, again the same concerns have started to emerge, which also contributed to the market correction in 2017. Although foreign inflows turned positive in January following exchange rate adjustment by the State Bank of Pakistan, and the market has partially recovered, there are still growing concerns regarding a repeat of the anti-cyclical fiscal adjustment.

Source: Zakheera

The market could be volatile over the next 12 months

▪ Over the past twelve months there has been 180 degrees shift in the economic sentiment from bullish to bearish. We think domestic investors were surprised by the bear rout which began in 2Q17. We think this was caused by outflows by foreign funds who were tracking frontier markets indices. While there is no reliable survey of investor sentiment or market consensus, we believe that most of the local sell side

and domestic investors were until that time, very optimistic about the economy and also most of the press coverage of Chinese investments under the CPEC programme were also favourable. The sentiment now seems to have shifted negative at least in the press and media, which now highlights balance of payment concerns, deterioration of the relationship with the US, political conflict between the army and the leading political party and the potential negative outcomes from Chinese investments. While we are conscious of these risks, we think the economy has gone through similar cycles in the recent past as well, most recently in 2008.

▪ The doom and gloom scenario. The bear case is fairly simple and it is mainly regarding the external balance of payments and funding requirements of the country. Over the last 24 months, Pakistan’s current account deficit has continued to widen and by end of January, it has reached $1,617m per month. In the period July 2017 to January 2018, i.e. the first seven months of the fiscal year it stands at $9.15bn, or 3.1% of GDP. This has increased by 48% compared to the same period last year. The government expects this to further deteriorate to around 4-5% of GDP for this year.

Current account deficit has reached close to 4% of GDP Pakistan has maintained a current account deficit for 17 of the last 20 years

Source: SBP

12

1

1st March 2018

Initiation report on Pakistan

▪ The primary driver of the deficit is the trade deficit and slowdown in remittances growth. The trade deficit has worsened by 24% over this period to $21.5bn (Exports: $13.9bn, +12% and Imports: $31.04bn, +18%). The import bill has grown considerably over the last two years. In 2016, the increase was primary due to machinery import from China for energy projects and in 2017, the acceleration has been caused by a +16% increase in the price of oil. Exports have lingered due to the currency peg and energy deficiency. The government has been depleting its external reserves in order to keep the exchange rate stable and foreign reserves have declined from a peak of $23bn in 2016 to $18.8bn ($12.8bn excluding reserves held by banks) by mid of Feb 2018. At the current run rate, the import cover is for around 3.5 months. While the government raised $2.5bn from international debt markets in November at competitive rates of 5.6% for the 5 year bond and 6.8% for a 10 year Eurobond, the concern is that increase in political risk and deterioration in relationship with the US could lead to a squeeze in external funding.

Trade deficit has widened significantly over the past 12 months Exports have been declining due to currency peg and imports have risen due to CPEC

Source: SBP

Reserves have declined by $5bn from the peak in 2016 Official foreign reserves have declined to $18.8bn ($12.8bn excl. bank reserves)

Source: SBP

▪ Back to the IMF. Pakistan has external debt of $89bn (30% of GDP), mostly denominated in US dollar and has annual debt servicing requirements of $8-9bn. Consequently, if the balance of payment situation stays at the same trend, then the country will either need to borrow more or need to reschedule its debt with the IMF over the next 6 to 9 months. IMF is likely to push for a significant exchange rate adjustment and increase in interest rates.

13

1

1st March 2018

Initiation report on Pakistan

We expect another 10% depreciation and 75bps rate hike in 2018

Source: Zakheera.com

▪ De ja vu all over again. While the bear thesis is fairly compelling, the reason we are still optimistic is that such economic cycle has been fairly typical of Pakistan. In fact this is also visible in previous exchange rate step changes, which often happen when the country has to go back to IMF for a financing round. Firstly, the government feels that they might be able to avoid requiring an IMF bailout. They adjusted the exchange rate by 10% by end of last year and expect that to have a positive impact on exports. Besides this they have started settlement of trade with China in Yuan and given the political significance of this to China, we think the Chinese government might become a sovereign lender or provide concessionary terms on Chinese imports. Secondly, even if Pakistan does end up back under an IMF program, that will not be a significant deviation from the past. Pakistan first received IMF bailout in 1988 and only completed the program in August 2016. Historically, IMF conditionality has been good for imposing economic discipline. Thirdly, economic fundamentals are much stronger now than they have been in previous cycle.

▪ This time it is a bit different. Firstly, not only is the economic growth strong (+5.3% and the government is targeting 6% growth for FY18) but it is being supported by growth in all three sub sectors (Services, Industrial and Agriculture). Secondly, over the past ten years the biggest drag on the economy was from energy shortfall, which according to research had led to a 2-2.5% hit to economic growth. Pakistan had an energy shortfall of 4,500 MW and at its peak load shedding of up to 12 hours even in main cities was

common. This is on the way to being resolved. Energy sector is receiving the most investments under the Chinese CPEC plan ($33bn) and the projects are expected to generate 17,000 MW of energy. Lastly, we think the government can stall machinery imports from China if they require to in order to ease the burden on the balance of payments. Also, the economic return from this investment is not being factored.

▪ We think Pakistan can sustain 5-6% economic growth rate over the next three years. We think the recent sentiment shift, especially in the media is also driven by the fact this there is a political change under way. Doom and gloom stories make interesting headline and easy election slogans. This is very typical of Pakistan and we think the stock market would be pricing a lot of this already. As stated earlier, such volatile periods have proven to be very attractive entry points, as both economic growth and stock markets returns continue to be driven by structural factors such as growing urbanization and rising domestic demand rather than by cyclical factors.

GDP growth is expected to reach 6% in FY17 – its highest level in a decade

Source: Pakistan Economic Survey

▪ Besides strong domestic demand, there are no inflationary pressures and the growth is not linked with bank lending. In fact, banks’s advances to lending ratios are near all time low at mid 50s. This is contrasting with 2008, when banks were more aggressive with lending to consumers and SME and eventually withdrew the lending following interest rates reversal. Only 2% of SMEs in the country get funding from banks and most banks are operating on Core tier 1 ratios in the high teens. Consequently, we don’t expect interest rate reversal to lead to a very sharp pull back in consumer demand. We think inflation would rise due to exchange rate depreciation but will remain in the high single digits.

14

1

1st March 2018

Initiation report on Pakistan

Inflation is near 4%, which is below is 10 year average level

Source: Pakistan Economic Survey

▪ Lastly, we think the consensus is ignoring the multiplier effect from the infrastructure investments under CPEC. Over the medium to long term, the availability of energy and upgrade to communication infrastructure should lead to a significant improvement in productivity.

15

1

1st March 2018

Initiation report on Pakistan

China: CPEC multiplier (Click here for a short video about CPEC made by National Geographic)

▪ New Silk Route. The CPEC is part of the Southern Corridor of the Chine One Belt & Road project. It is a 3,218km long route which directly connects Kashgar in Xinjiang Province to the Arabian Sea at the port town of Gwadar. The total cost of the project is around $75bn out of which $45bn is for early harvest projects which will ensure it is operational by 2020. We think the success of CPEC is critical for China as it has become the flagship part of the $1trillion+ ambitious project which is aiming to connect 65 countries.

CPEC is probably the most critical part of China’s Belt & Road project

Source: CPEC

▪ Commercially, CPEC corridor is expected to generate direct cost benefits to China of around $50bn per annum just from saving costs of shipping of oil via its current route which goes via the Strait of Malacca. 80% of Chinese Oil is imported from the Persian Gulf via this route. With Gwadar port operational, this distance would be reduced from 16,000km to less than 5,000m.

▪ For Pakistan, the project is expected to generate 700,000 new jobs over 2015-2030, upgrade and build connectivity both internally and globally and in the near term end the energy crisis. This is expected to add up +2.5% to Pakistan’s GDP growth rate.

▪ CPEC is a multi-year project, and the first wave of investment is focused on building infrastructure and energy. The Table below lists some of the projects announced.

▪ Besides these, the government of Pakistan is building 9 exports zones to encourage Chinese businesses to set up industries and local production. The project is also encouraging other Chinese companies to expand to Pakistan. Shanghai Electric has made an offer for Pakistan’s largest listed electric distribution company, Karachi Electric

CPEC: Projects Announced So Far

Sector Project MW Est. Cost ($m)

Energy Port Qasum Electric Company, Coal Fi red 1,320 1,980

and Shanghai Stock Exchange recently took a 40% stake in Pakistan Stock Exchange. Also, Chinese banks such as Bank of China and ICBC have opened up and Chinese corporates are reported to be big buyers of domestic real estate. Just the $45bn of investments announced under CPEC is equivalent to all of the FDI the country has received since 1970!

▪ We think the CPEC will drive growth in multiple sectors. For example, the Chinese government intends to lease agricultural land and export new seeds, fertilizers, machinery and methods of farming. This should support growth in domestic fertilizer and agricultural machinery sector (tractors etc). The build up of physical infrastructure such as railways, should boost domestic steel and cement industry (demand projected to grow by 10% per annum over the medium term), banking sector should benefit from higher lending growth to these mega projects, and eventually trade and commerce should pick up. Another sector which could benefit is tourism. Pakistan has been ranked as the top alternative tourist destination for 2018 by the Financial Times. Better links with China could not only attract Chinese tourists but also potentially revive the old “hippy” trail along the Himalayas.

17

1

1st March 2018

Initiation report on Pakistan

Appendix :2018: Election year Minus-one agenda is creating political tensions

▪ The current government will end its 5 year tenure on May 2018 and new elections are likely to be held by September by an interim government. Political noise has increased since last year when the former Prime Minister Mr. Nawaz Sharif was disqualified by the Supreme Court on the courts of not disclosing his financial assets. Mr. Sharif is the leader of Pakistan Muslim League (Nawaz), which holds the majority in the National Assembly and in the largest province, Punjab. The opposition parties, Pakistan People’s Party (PPP) holds majority in Sindh province and Pakistan Tehreek-e-Insaf (PTI) in KPK province. Consensus opinion is that the existing distribution of power will persist in the next elections, however the disqualification of Mr. Sharif has put him on adversarial path with the Judiciary, who he accuses is being backed by the “establishment”; a euphuism commonly used for the army. This clash is probably the major source of domestic political tension.

▪ General perception in the country is that the “establishment” is against family dynasty politics, which the two leading parties; PML(N) and PPP have become. PML – run by the Sharif family (his brother is the Chief Minister of Punjab) and PPP for Mr. Zardari (husband of the late Benazir Bhutto (2x Prime Minister). They want a “minus-one” formula, which could break this control. PTI, the third largest party also backs this agenda.

▪ We think while political news will create noise, it will have little impact on the economy and the market. All the political parties have similar economic agendas which support liberalization, deregulation and open market access. Consensus opinion based on recent surveys indicate that the likely scenario is for Mr. Shahbaz Sharif (brother of Nawaz Sharif, who is currently the Chief Minister of Punjab) to win the next elections and become Prime Minister. In our view, his main challenger comes internally from the daughter of Mr. Nawaz Sharif, Ms. Mariam Nawaz, who wants the leadership to remain with her line of the family. Mr. Shabaz Sharif is widely respected and almost has bi-partisan recognition as a good administrator.

▪ Mr. Imran Khan’s (former Cricketer and philanthropist) PTI would be the main challenger for PML’s stronghold in Punjab and is perceived and alleged to be supported by the Establishment. In our opinion, there will not be any significance difference between a Shahbaz Sharif government and a PTI government, as both have similar voter bank (Punjab/urban). PPP regimes in the past have been associated with allegations of

rampant corruption, and consequently a win by PPP could discourage new investments. However, due to such allegations, the PPP has lost its support in Punjab and is marginalized to the feudal constituencies in Sindh.

2013 Election Results: Top 3 parties formed governments in 3 provincesPolitical Party National Punjab Sindh Balochistan KPK

PML (N) 166 214 4 8 12

PPPP 42 6 69 0 3

PTI 35 24 2 1 39

MQM 24 0 34 0 0

Others 75 53 21 42 45

Total 342 297 130 51 99

Source: Govt. of Pakistan

18

1

1st March 2018

Initiation report on Pakistan

About Oxford Frontier Oxford Frontier is an investment research and advisory firm specializing in emerging technologies in frontier markets. The company is based in the UK and works in partnership with KASB Securities (www.kasb.com) in Pakistan. KASB is the oldest capital markets group in Pakistan and a TREC member of Pakistan Stock Exchange.

This report has been produced by Ali Farid Khwaja. Prior to joining Oxford Frontier, Ali was a Partner at Autonomous Research in London, where he was responsible for European Payment Tech Research. Before that Ali was Chief Financial Officer (CFO) and Board Member of SafeCharge International PlC – a European payment services provider listed on London Stock Exchange. He was also CEO of SafeCharge Card Services in Dublin, where he launched their digital wallet, Pay.com. As the CFO Ali led investments in Frankfurt listed FinTech Group and 2C2P in Singapore. Ali has more than twelve years of technology research and investment experiences at Berenberg, UBS and Kudu Emerging Markets. In 2013, he was ranked as a top 3 Analyst in Europe in Tech Hardware Sector by Thomson Reuters. He is an alumnus of Oxford, where he was a Rhodes Scholar.

IMPORTANT DISCLOSURES This publication/communication or any portion hereof may not be reprinted, sold or redistributed without the written consent of Oxford Frontier. Oxford Frontier has produced this report for private circulation to professional and institutional clients only. The information, opinions and estimates herein are not directed at, or intended for distribution to or use by, any person or entity in any jurisdiction where doing sowould be contrary to law or regulation or which would subject Oxford Frontier to any additional registration or licensing requirement within such jurisdiction. The information and statistical data herein have been obtained from sources we believe to be reliable and complied by our research department in good faith. Such information has not been independently verified and we make no representation or warranty as to its accuracy, completeness or correctness. Any opinions or estimates herein reflect the judgment of Oxford Frontier at the date of this publication/ communication and are subject to change at any time without notice.

This report is not a solicitation or any offer to buy or sell any of the securities mentioned herein. It is for information purposes only and is not intended to provide professional, investment or any other type of advice or recommendation and does not take into account the particular investment objectives, financial situation or needs of individual recipients. Before acting on any information in this publication/communication, you should consider whether it is suitable for your particular circumstances and, if appropriate, seek professional advice. Neither Oxford Frontier nor any of its affiliates or any other person connected with the company accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or the information contained therein.

Subject to any applicable laws and regulations, Oxford frontier, its affiliates or group companies or individuals connected with Oxford frontier may have used the information contained herein before publication and may have positions in, may from time to time purchase or sell or have a material interest in any of the securities mentioned or related securities or may currently or in future have or have had a relationship with, or may

provide or have provided investment banking, capital markets and/or other services to, the entities referred to herein, their advisors and/or any other connected parties.

Oxford Frontier or persons connected with it may from time to time have an investment banking or other relationship, including but not limited to, the participation or investment in commercial banking transaction (including loans) with some or all of the issuers mentioned therein, either for their own account or the account of their customers. Persons connected with the company may provide corporate finance and other services to the issuer of the securities mentioned herein, including the issuance of options on securities mentioned herein or any related investment and may make a purchase and/or sale of the securities or any related investment from time to time in the open market or otherwise, in each case either as principal or agent.

This document is being distributed in the United State solely to "major institutional investors" as defined in Rule 15a-6 under the U.S. Securities Exchange Act of 1934, and may not be furnished to any other person in the United States. Each U.S. person that receives this document by its acceptance hereof represents and agrees that it: is a "major institutional investor", as so defined; and understands the whole document. Any such person wishing to follow-up any of the information should do so by contacting a registered representative of Oxford Frontier The securities discussed in this report may not be eligible for sale in some states in the U.S. or in some countries.

Any recipient, other than a U.S. recipient that wishes further information should contact the company.

This report may not be reproduced, distributed or published, in whole or in part, by any recipient hereof for any purpose.