Page 1

Page 1 of 19

29 October 2012

Susanna Chui

[email protected]

(852) 2235 7131

Trading data

52-Week Range (HK$)

3 Mth Avg Daily Vol (m)

No of Shares (m)

Market Cap (HK$m)

Listed on HKEx

IPO Price (HK$)

Major Shareholders (%)

Auditors

Result Due

1.00/2.03

0.33

1,037.73

1,432.06

Dec 2010

2.88

HiSun Tech (43%)

Hao Capital (23%)

Fidelity (9%)

PWC

FY12: Mar Company description

Founded in 2000, PAX is the no. 1 and no. 3 EFT-POS terminal solution provider in China and

the world respectively. It is strong in Asia/ Pacific

and Mideast/ Africa. Its major customers are

acquiring banks and merchant service provider

such as CCB (939.HK), BOC (3988.HK), ABC

(1288.HK) and UMS.

Price chart

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Jun

-12

Sep

-12

HK$

Undervalued leader in e-payment

Rating Buy Initiation

Target Price HKD 2.30

Current price

HKD 1.38 Upside +67%

No. 1 EFT-POS terminal solution provider in China

PAX is currently the no. 1 player in EFT-POS (electronic funds transfer

point of sale) terminal solution provider in China and rank the third

globally. Over the past years, the company has enjoyed the fastest

shipment growth amongst the top players. The potential losses from fraud

could be so significant that customers must ensure the terminals are up to

the highest security standards. Therefore, behind the company growth is

the customer confidence, supported by PAX’s advancing leading position,

qualification and established track record.

Secular growth due to low penetration and EMV upgrade

In 2011, the global payment card terminal shipment has increased 14.4%,

with 33.2% growth in emerging markets. There is still huge room for

growth in emerging markets given the low penetartion rate (emerging

markets: <5 units/1,000 people, versus developed markets: 10-35 units).

Growth will also be rekindled in developed markets with EMV (Europay,

MasterCard and Visa) upgrade which offers higher security as a mean to

combat credit card fraud. We believe PAX can benefit from these

opportunities as well as expand their overseas' market share.

Industry consolidation favorable for overseas share gain

In recent years, global top players have been pursuing growth through

aggressive M&A. As the industry consolidation leads to fewer choices and

lower bargaining power for customers, the customers will be more open to

deal with other qualified providers. We believe PAX, the third largest

global player, just after Ingenico and VeriFone, can benefit and gain

further overseas market share. With fast growing overseas sales, of which

GPM is above the company average, the blended GPM will be pulled up.

We initiate coverage on PAX Global with BUY

The company is trading at 7.3x FY12E PER (2.4x FY12E ex-cash PER,

with HKD973.2mn of cash in 1H12), which is 51.8% lower than the

average 15.2x of its peers (Verifone, Ingenico and Xinguodu). We believe

the valuation discount will be narrowed given its growth in global market

share. We initiate coverage on the stock with target price of HK$2.30,

based on 12.2x FY12E PER or 20% discount to peers.

HKD million FY10A FY11A FY12E FY13E FY14E

Revenue 724 1,103 1,291 1,596 2,011

Operating profit 173 207 234 282 354

Net Profit 145 182 195 235 295

Consensus NP 196 243 282

EPS (HKD) 0.19 0.18 0.19 0.23 0.28

P/E (x) 7.1 7.9 7.3 6.1 4.8

Sources: Bloomberg, CIRL estimates

PAX Global | 327.HK

China Puti

Page 2

Page 2 of 19

No. 1 EFT-POS terminal solution provider in China

PAX is currently the no. 1 player in EFT-POS (electronic funds transfer point of sale)

terminal solution provider in China and rank the third globally. The company is

increasingly gaining global market share. Amongst the top 5 players, it has delivered

the largest CAGR of 53.4% in shipment over 2007-2011.

Exhibit 1: POS terminal global market share in 2011

Ranking Market share Shipment Change

Ingenico (FR) 1 28.1% 4,844,000 18%

VeriFone (US) 2 25.3% 4,363,847 38%

PAX (CN) 3 5.5% 949,271 83%

CyberNet (KR) 4 4.6% 787,500 0%

Bitel (KR) 5 3.3% 563,375 32%

Castles (TW) 6 3.1% 532,100 -5%

Xinguodu (CN) 7 2.3% 400,000 82%

Gertec (BR) 8 1.5% 250,000 14%

Newland (CN) 9 1.4% 242,800 31%

Spectra Tech. (HK) 10 1.2% 213,746 27%

Total

100.0% 17,232,904 14%

Source: The Nilson Report, CIRL (excluding SZZT, which focuses on EPOS terminals)

Exhibit 2: PAX has enjoyed the fastest growth since 2007 compared with other top players

Source: The Nilson Report, CIRL (excluding SZZT, which focuses on EPOS terminals)

After years of rapid growth, the company has a well-established global presence. It is

now the top 10 provider in all regions, particularly strong in Asia-Pacific and Mideast/

Africa, accounting for 11.1% and 10.2% shipment in these regions respectively.

-20%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011

Ingenico (FR) VeriFone (US) PAX (CN)

CyberNet (KR) Bitel (KR) Industry

Page 3

Page 3 of 19

Results in the Asia-Pacific region have come about as a result of its strong presence

in its stronghold, China, whilst opportunities in Middle-East arise from their tendency

to source non-US suppliers due to their tense relationship with US.

Exhibit 3: PAX is the top 10 provider in all regions

Regions PAX shipment Region shipment Market share Ranking

Asia/ Pacific (China) 714,277 6,454,456 11.1% (30-32%) 3 (1)

Mideast/ Africa 161,878 1,588,338 10.2% 4

Europe 57,495 4,296,436 1.3% 6

Latin America 12,060 2,770,644 0.4% 9

United States 3,355 1,913,008 0.2% 10

Canada 206 210,022 0.1% 7

Total 949,271 17,232,904 5.5% 3

Source: The Nilson Report, PAX, CIRL (excluding SZZT, which focuses on EPOS terminals)

What are EFT-POS Terminals?

An EFT-POS terminal is a system which allows the customer or cashier to swipe a

payment card and authorize the transaction through either a signature or PIN. There

are various different types of terminals, including counter-top POS terminals

(supporting broadband and dial connectivity), mobile POS terminals (supporting

wireless connectivity, such as GPRS and Wi-Fi), consumer activated devices (for

inputting the PIN codes), and contactless devices (for contactless cards such as

Visa’s payWave and MasterCard’s PayPass).

Exhibit 4: PAX’s existing products

Source: PAX, CIRL

How does the payment card transaction process work?

Every payment card transaction involves multiple parties such as the cardholders, the

issuer (the consumer’s banks), the merchants, and the acquirer (the merchant's

banks/ payment processors), which are all connected with the card association’s

Page 4

Page 4 of 19

network. Processing a payment card transaction mainly involves two stages:

authorization and settlement. Here is the general overview.

Exhibit 5: Typical electronic fund transfer transaction

Source: PAX, CIRL

Who are the customers?

We generally see POS terminals at merchants, when we purchase with payment

cards. The decision on which POS terminal to buy are usually made by the merchant's

acquirers (merchant's banks or payment processors) and merchant service providers

(UnionPay Merchant Services (UMS) and independent sales organizations (ISO),

which act as agents to penetrate the small-to-medium level merchant market on

behalf of the acquiring banks). In rare instances, only the largest merchants, such as

Walmart, will get involve in the decision themselves.

Cardholder Merchant

(e.g. retailers, restaurant and hotels)

Acquirers

(Merchant's banks/ payment processors)

Card Association

(e.g. China UnionPay)

Merchant service provider

(e.g. UMS and ISO)

Issuer

(Consumer’s banks)

EFT-POS terminal solutions provider

(e.g. PAX)

Customers Other parties involved in the transaction PAX

Authorization is the process, where an electronic request is sent through various parties to either approve or decline the transaction.

1. Cardholder pays with card through an EFT-POS terminal at merchant, which sends transaction data to the acquiring bank.

2. The acquiring bank sends authorization request to the issuing bank through the network of card association.

3. The issuing bank verifies that the cardholder’s credit is sufficient and grants authorization.

4. The acquiring bank receives the response and relays it to the merchant.

5. Merchant receives the authorization response and completes the transaction accordingly.

Settlement is the process, where all parties settle their accounts.

1. Merchant deposits the transaction receipt with the acquiring bank.

2. The acquiring bank submits settlement files to the issuing bank for reimbursement via the network of card association.

3. The issuing bank posts the transaction to the cardholder account and sends the cardholder a monthly statement.

4. Cardholder receives statement and pays issuer.

Page 5

Page 5 of 19

Why the customers choose PAX? It’s all about confidence.

According to The Nilson Report, the amount of fraud losses is ~USD8.0bn, which is

equaled to 4.46¢ per $100 in total volume of purchases. The potential fraud loss is so

significant that merchants’ banks or payment processors must ensure the terminals

are up to the highest security standards. Therefore, the determining factor that drives

the purchase is all about customer confidence, supported by PAX’s advancing leading

position, qualification and established track record.

1) Higher customer confidence amid rapid market share growth: PAX is increasingly

gaining market share in global market. The company is ranked No. 3 in 2011, up

from No. 7 in 2007. At the same time, the market share of both Ingenico and

Verifone has declined to 28.1% and 25.3% in 2011, from 31.8% and 30.0% in

2007 respectively. The customers will think of PAX after Ingenico (ING.FP) and

Verifone, leading to higher chance of selecting PAX as one of their qualified

suppliers. The narrowing gap with these two largest players will also improve

customer confidence in PAX's product quality.

Exhibit 6: PAX’s global market share

Source: The Nilson Report, CIRL

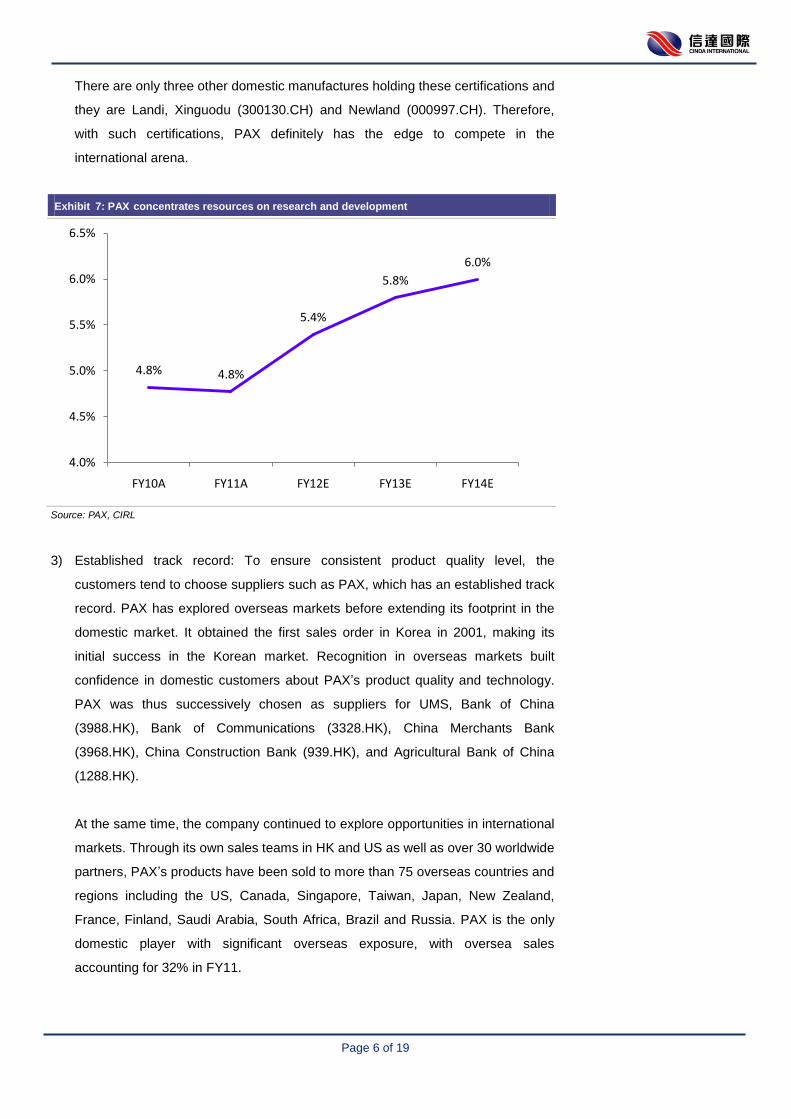

2) Boasting over the high certification barrier: PAX concentrates resources on

research and development which accounts for ~5.0% of total revenue. PAX also

outsources EMS manufacturers to provide assembly and processing services.

With over 500 employees, ~55% of them are engineers.

PAX was the first Asian POS terminal solution provider in Asia to obtain EMV

(Europay, MasterCard and Visa) 2000 certifications. It has also been awarded PCI

(Payment Card Industry) certifications, which are mandatory around the world.

31.8% 30.9%28.3% 28.1% 28.1%

30.0%

26.7%24.0%

21.7%

25.3%

1.4% 1.9% 2.3%3.5%

5.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2007 2008 2009 2010 2011

Ingenico (FR) Verifone (US) PAX (CN)

Page 6

Page 6 of 19

There are only three other domestic manufactures holding these certifications and

they are Landi, Xinguodu (300130.CH) and Newland (000997.CH). Therefore,

with such certifications, PAX definitely has the edge to compete in the

international arena.

Exhibit 7: PAX concentrates resources on research and development

Source: PAX, CIRL

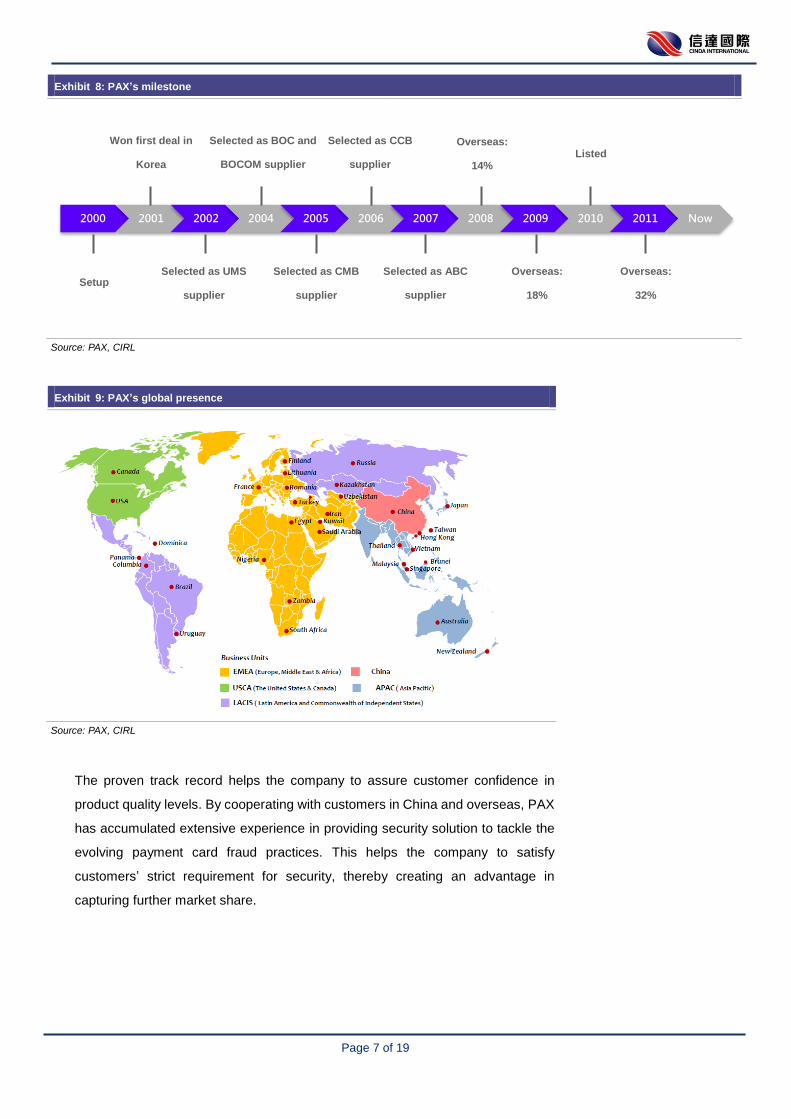

3) Established track record: To ensure consistent product quality level, the

customers tend to choose suppliers such as PAX, which has an established track

record. PAX has explored overseas markets before extending its footprint in the

domestic market. It obtained the first sales order in Korea in 2001, making its

initial success in the Korean market. Recognition in overseas markets built

confidence in domestic customers about PAX’s product quality and technology.

PAX was thus successively chosen as suppliers for UMS, Bank of China

(3988.HK), Bank of Communications (3328.HK), China Merchants Bank

(3968.HK), China Construction Bank (939.HK), and Agricultural Bank of China

(1288.HK).

At the same time, the company continued to explore opportunities in international

markets. Through its own sales teams in HK and US as well as over 30 worldwide

partners, PAX’s products have been sold to more than 75 overseas countries and

regions including the US, Canada, Singapore, Taiwan, Japan, New Zealand,

France, Finland, Saudi Arabia, South Africa, Brazil and Russia. PAX is the only

domestic player with significant overseas exposure, with oversea sales

accounting for 32% in FY11.

4.8% 4.8%

5.4%

5.8%

6.0%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

FY10A FY11A FY12E FY13E FY14E

Page 7

Page 7 of 19

Exhibit 8: PAX’s milestone

Source: PAX, CIRL

Exhibit 9: PAX’s global presence

Source: PAX, CIRL

The proven track record helps the company to assure customer confidence in

product quality levels. By cooperating with customers in China and overseas, PAX

has accumulated extensive experience in providing security solution to tackle the

evolving payment card fraud practices. This helps the company to satisfy

customers’ strict requirement for security, thereby creating an advantage in

capturing further market share.

2000 2001 2002 2004 2005 2006 2007 2008 2009 2010 2011 Now

Selected as UMS

supplier

Selected as CMB

supplier

Selected as ABC

supplier

Overseas:

18%

Overseas:

32%

Setup

Selected as BOC and

BOCOM supplier

Selected as CCB

supplier

Overseas:

14%

Listed

Won first deal in

Korea

Page 8

Page 8 of 19

Understanding PAX’s competitors

PAX faces different competitors in different battlefield. In PAX’s stronghold, China, its

products are primarily for UMS and major commercial banks in China, with domestic

competitors such as Landi, and Xinguodu, and foreign competitors such as VeriFone.

Landi, is a subsidiary of Ingenico. Due to the superior customer relationships and

product quality, we believe Landi and PAX will continue to enjoy the stable market

share. Though Xinguodu has adopted an aggressive pricing strategy, it mainly

captures the market share from foreign manufacturers such as VeriFone. This is

because VeriFone offers global models instead of customized products tailored to

customers’ needs, and is present only through distributors.

Globally, Ingenico and VeriFone are the largest players. VeriFone is the primary

terminal vendor in the US market, while Ingenico is the largest vendor in Asia-Pacific,

Europe, Latin America and Canada. Though they possess strong customer

relationship and technology advantage in certain regions and market segments, we

believe PAX, with its leading position, qualification and established track record, can

still be one of 2-3 qualified suppliers and will continuously capture further market

share in the industry consolidation.

Exhibit 10: PAX and its competitors have the strong presence in different regions

PAX Ingenico VeriFone

Home base (2011 market share) China (30-32%) Europe (43.7%) United States (59.7%)

Global ranking 3 1 2

Global market share 5.50% 28.10% 25.30%

Regional ranking and market share Asia/ Pacific: 2 (11.1%) Asia/ Pacific: 1 (22.7%) Asia/ Pacific: 4 (7.7%)

Europe: 6 (1.3%) Europe: 1 (43.7%) Europe: 2 (30.9%)

Latin America: 9 (0.4%) Latin America: 1 (36.2%) Latin America: 2 (33.2%)

United States: 10 (0.2%) United States: 2 (11.2%) United States: 1 (59.7%)

Mideast/ Africa: 4 (10.2%) Mideast/ Africa: 3 (10.7%) Mideast/ Africa: 2 (25.6%)

Canada: 7 (0.1%) Canada: 1 (54.3%) Canada: 2 (34.8%)

Shipment CAGR over 2007-2011 53.4% 6.3% 5.0%

Source: The Nilson Report, CIRL (excluding SZZT, which focuses on EPOS terminals)

Page 9

Page 9 of 19

Secular growth due to low penetration and EMV

upgrade

According to The Nilson Report, the payment card authorization terminals shipped

17.2mn units worldwide in 2011, up 14.4% from 15.1mn in 2010. The fastest growing

regions are emerging markets including Asia-Pacific, Latin America and Mideast/

Africa, with growth of 33.2% altogether.

Exhibit 11: POS terminal shipment worldwide

Source: The Nilson Report, CIRL

Exhibit 12: Emerging markets have delivered the fastest growth in 2011

2011 2010 Change

Asia/ Pacific 6,454,456 4,594,401 40.5%

Europe 4,296,436 4,148,306 3.6%

Latin America 2,770,644 2,338,586 18.5%

United States 1,913,008 2,112,075 -9.4%

Mideast/ Africa 1,588,338 1,184,776 34.1%

Canada 210,022 224,634 -6.5%

Source: The Nilson Report, CIRL

Secular industry growth driven by the emerging markets

Amongst the emerging markets, the fastest growing region is Asia-Pacific in 2011 with

a total of 6.5mn terminals, an increase of 40.5%. Mideast/ Africa and Latin America

also received 1.6mn units and 2.8mn in 2011, up 34.1% and 18.5% respectively.

Asia/ Pacific , 37.5%

Europe, 24.9%

Latin America , 16.1%

United States, 11.1%

Mideast/ Africa, 9.2%

Canada, 1.2%

Page 10

Page 10 of 19

The emerging markets have experienced boom over the last few year. However, there

are still less than 5 POS terminals per 1,000 people, versus 10-35 in the developed

markets. We expect the emerging markets’ penetration rate will grow further, driven by

1) emergence of the middle class and 2) local authorities pushing for secure

e-payment (electronic payment).

Exhibit 13: POS installed devices per 1,000 people

Source: Verifone, CIRL

China market will enjoy moderate revenue growth amid under penetration

PAX’s stronghold, China has even a larger potential along with the consumption

driven growth path. Factoring in declining ASP due to competition and cost reduction,

we expect the company will still deliver 10.2% CAGR on revenue from China over

FY11-FY14E.

Exhibit 14: PAX’s revenue from China

Source: PAX, CIRL

566

755 800

899

1,011

-

200

400

600

800

1,000

1,200

1,400

FY10A FY11A FY12E FY13E FY14E

HK

D m

n

CAGR: 10.2%

Page 11

Page 11 of 19

The key growth driver will be the overseas market amid EMV upgrade

As for developed markets, we expect growth will rekindle in the coming years despite

being sluggish in 2011, as EMV upgrade will take place, especially in US. According to

The Nilson Report, the amount of credit card fraud losses is ~USD8.0bn, which is

equaled to 4.46¢ per $100 in total volume of purchases. The losses could not be

ignored as card issuers are ultimately the one to bear such losses. A more secured

solution was required - EMV chip, an added security of protecting personal data theft

from credit cards. Different regions are successively in the process of implementing

EMV chip in credit cards as extra security measures.

Exhibit 15: Different regions are successively in converting magnetic stripe transaction to EMV chip transaction

Magnetic stripe transaction

Store data by modifying the magnetism of magnetic

particles on a band of magnetic material on the card,

which can be duplicated by the criminals

EMV chip transaction

Utilize a small data processing chip to transmit encrypted

information, acting as a form of identification for cardholder

transactions.

Source: Industry data, CIRL

UK was one of the first movers on EMV, with migration taking place between 2003

and 2008. We believe liability shifts from the card issuer to the merchant for fraud on

card transaction at a non-compliant POS terminal might have played a role in spurring

retailers to re-terminalize. Also, the reductions of interchange fee paid by the

merchant's banks (the acquiring banks) to the customer’s banks (the issuing banks),

appeared to have traction. As a result, UK’s fraud rates were nearly cut in half since

EMV became widely adopted.

In the Euro zone, the Single Euro Payments Area (SEPA) migration framework set by

Europe Payment Council included EMV chip card as a standard. Subsequently,

fraud rates at point-of-sale in France was halved after the roll-out of EMV.

Page 12

Page 12 of 19

Exhibit 16: EMV migration in various counties

Source: Industry data, CIRL

We believe the next wave will be in the US. After Euro zone upgraded to EMV, US

became a significant target for skimming of card data resulting in high fraud rate. US

contributes disproportionately to the global tally, driving 47% of global card fraud on

27% of global card volume. To lower the fraud costs, US decided to accelerate its

conversion to EMV. Key elements of the card networks’ roadmaps of US EMV

implementation include incentives for merchants starting in 2012 (possible reduced

interchange rates for early adoption), and a liability shift starting in 2015 (liability for

card fraud on non-EMV transaction in US is set to shift from the card issuers to the

merchants starting Oct 2015). The carrot-and-stick approach should contribute to the

success in a number of EMV migration efforts.

We believe the EMV migration could shorten the replacement cycle in US from ~5 yrs

to ~4 yrs, inducing 0.5mn units of potential increase in POS terminal shipment, from

the existing ~10mn units of installed base.

Exhibit 17: Quantifying the EMV opportunity in US

Normal Accelerated Potential change

Installed base in US (mn) 10 10

Replacement cycle (yrs) 5 4 -20.0%

Shipment(mn) 2 2.5 +25.0%

Source: Industry data, CIRL

While VeriFone has a home advantage in US, we believe PAX, with its growing

leading position, qualification and established track record, can still be one of 2-3

qualified suppliers in the world. We believe the company can benefit from the low

penetration rate in emerging markets and EMV opportunities in the rest of the world,

whilst expanding overseas market share amid industry consolidation. We expect the

company will deliver 42.2% CAGR on revenue from overseas over FY11-FY14E.

2003 2006 2008 2009 2012 2013 2014 2016

France Canada US

UK Australia

Page 13

Page 13 of 19

Exhibit 18: PAX’s revenue from overseas

Source: PAX, CIRL

157

348

490

697

1,000

-

200

400

600

800

1,000

1,200

FY10A FY11A FY12E FY13E FY14E

HK

D m

n

CAGR: 42.2%

Page 14

Page 14 of 19

Industry consolidation favorable for overseas

share gain

PAX is rapidly gaining market share in the global market. The company is rank No. 3

in 2011, up from the No. 7 in 2007. At the same time, the market share of both

Ingenico and Verifone has declined to 28.1% and 25.3% in 2011, from 31.8% and

30.0% in 2007 respectively. We believe narrowing the gap with these two largest

players will go on, on the back of industry consolidation.

Exhibit 19: PAX’s global market share

Source: The Nilson Report, CIRL

Generally the overseas customers will source POS terminals from 2-3 qualified

suppliers such as Ingenico, VeriFone and Hypercom. The industry consolidation has

now changed this dynamics however:

1) The top players are aggressively pursuing M&A. For example, VeriFOne has

acquired #3 Hypercom and #8 Gemalto over the past year. After a long period of

consolidation in terminals, ~50% of the global market is held by Ingenico and

VeriFone, with each party dominant in certain market segments or countries. The

industry consolidation is leading to fewer choices and lower bargaining power for

customers.

31.8% 30.9%28.3% 28.1% 28.1%

30.0%

26.7%24.0%

21.7%

25.3%

1.4% 1.9% 2.3%3.5%

5.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2007 2008 2009 2010 2011

Ingenico (FR) Verifone (US) PAX (CN)

Page 15

Page 15 of 19

Exhibit 20: Industry mergers and acquisitions

Date Major activities

2006 VeriFone buys Lipman (Israel based)

2008 Ingenico buys Sagem Monetel (France based)

2008 Ingenico buys controlling stake in Landi (China based)

2010 VeriFone buys POS terminals segment from Gemalto (France based)

2011 VeriFone buys Hypercom ex POS terminals in the UK, US, Spain (US based)

Source: Industry data, CIRL

2) Ingenico and VeriFone have taken the strategic decision to expand out of

terminals into services. For example, Ingenico acquired EasyCash in 2010, a

leading payment service provider (PSP) in Germany. VeriFone also acquired

Point, Northern Europe's largest provider of payment and gateway services and

solutions for retailers. Both Ingenico and Verifone are now competing with their

direct customers.

In order to maintain bargaining power and confront competition, we expect the

customers will be more open to consider other qualified suppliers. We believe PAX,

the third largest player, just after Ingenico and VeriFone, with qualification and

established track record, can gain further market share in the overseas market.

Overseas expansion stabilizing margins

Due to high customer concentration and Xinguodu’s aggressive pricing strategy,

PAX’s ASP has declined by ~5-10%/ year for the same products. However, the

management believes cost control and roll-out of new models can support China

segment’s GPM above 30%.

Most importantly, we expect the overseas segment will outgrow China segment. The

overseas sales proportion will rise from 32% in FY11 to 50% in FY14E. As overseas

segment’s GPM is ~38.0%, above 35.5% of company average in FY11, the blended

GPM will be pulled up to ~37% with overseas expansion.

Page 16

Page 16 of 19

Exhibit 21: PAX is increasing overseas sales proportion

Source: PAX, CIRL

Exhibit 22: PAX‘s blended GPM will be pulled up to~37.0%

Source: PAX, CIRL

78%68% 62% 56% 50%

22%32% 38% 44% 50%

0%

20%

40%

60%

80%

100%

120%

FY10A FY11A FY12E FY13E FY14E

China Overseas

39.8%

34.3%

31.0% 31.0% 31.0%

42.3%

38.0%

46.7%45.0%

43.5%

40.3%

35.5%37.0% 37.1% 37.2%

20%

25%

30%

35%

40%

45%

50%

FY10A FY11A FY12E FY13E FY14E

China Overseas Total

Page 17

Page 17 of 19

Financial analysis and valuation

We forecast revenue to grow by 17.0%/23.7%/26.0% for FY12E/FY13E/FY14E

mainly driven by 1) the opportunities from low penetration in the emerging markets; 2)

EMV migration in developed markets; and 3) overseas share gain.

Margin rebounds to ~37.0% due to increasing overseas sales proportion from 32%

in FY11 to 50% in FY14E. As overseas segment’s GPM is ~38.0%, above 35.5% of

company average in FY11, the blended GPM will be pulled up. SG&A expenses have

been stable, but will increase from 16.7% of total revenue in FY11 to 18.9-19.6% in

FY12E-FY14E, on the back of expanding overseas exposure and non-recurrent and

non-cash stock options expenses. We expect that net profit will rise

7.3%/20.6%/25.6% to HKD $195.1mn/HKD235.2mn/HKD295.3mn in

FY12E/FY13E/FY14E.

We initiate coverage on PAX with BUY. The company is trading at 7.3x FY12E PER

(2.4x FY12E ex-cash PER, with HKD973.2mn of cash in 1H12), which is 51.8% lower

than the average 15.2x of the peers (Verifone, Ingenico & Xinguodu). We believe the

valuation discount will be narrowed given its growth in global market share.

Additionally, being a cash-rich company, any potential acquisition will be the catalyst.

We initiate coverage on the stock with target price of HK$2.30, based on 12.2x FY12E

PER or 20% discount to peers.

Risk Factors

Downside risks include: 1) slower than expected growth in penetration rate in

emerging markets; 2) slower than expected EMV migration in developed markets; 3)

slower than expected pace of overseas share gain; and 4) faster-than-expected

ASP/margin erosion in China due to the competition from Xinguodu and VeriFone.

Exhibit 23:Key assumptions

2010 2011 2012E 2013E 2014E

Revenue growth

China market 39.7% 33.4% 5.9% 12.3% 12.5%

Overseas market 79.7% 121.2% 41.0% 42.2% 43.4%

Overall 46.8% 52.5% 17.0% 23.7% 26.0%

Gross Profit Margin

China market 39.8% 34.3% 31.0% 31.0% 31.0%

Overseas market 42.3% 38.0% 46.7% 45.0% 43.5%

Overall 40.3% 35.5% 37.0% 37.1% 37.2%

Source: Compnay data, CIRL

Page 18

Page 18 of 19

Exhibit 24: Financial statement

Source: Company data, CIRL

Exhibit 25: Peer comparison

Source: Bloomberg, CIRL

Income statement Cash flow

Year to Dec (HKD mn) FY10A FY11A FY12E FY13E FY14E Year to Dec (HKD mn) FY10A FY11A FY12E FY13E FY14E

Revenue 724 1,103 1,291 1,596 2,011 Pre-tax profit 173 207 234 282 354

Gross profit (reported) 292 392 477 592 748 Taxes paid (22) (30) (15) (39) (46)

EBITDA 175 211 237 286 359 Depreciation 3 3 4 5 6

Depreciation (3) (3) (4) (5) (6) Associates 0 0 0 0 0

EBIT 173 207 234 282 354 CFO bef. WC change 153 181 222 248 313

Net interest income (exp.) 0 0 0 0 0 Change in working cap (42) (211) (188) (148) (183)

Associates 0 0 0 0 0 Cashflow from operation 111 (30) 34 100 130

Exceptionals/others 0 0 0 0 0 CAPEX (5) (3) (4) (4) (6)

Profit before tax 173 207 234 282 354 Free cash flow 107 (33) 31 95 124

Tax expenses (27) (26) (39) (46) (58) Dividends 0 0 0 0 0Minority interest 0 0 0 0 0 Balance sheet adj. 0 0 0 0 0

Net profit 145 182 195 235 295 Sharse issued 719 132 0 0 0

NP (exclude option exp.) 145 182 215 252 301 Others 0 0 (0) 0 0

Net cash flow 825 99 31 95 124

Balance sheet Net cash (debt) start 244 1,069 1,168 1,199 1,294

Year to Dec (HKD mn) FY10A FY11A FY12E FY13E FY14E Net cash (debt) at year-end 1,069 1,168 1,199 1,294 1,419

Cash & equiv 1,069 1,168 1,199 1,294 1,419

Trade receivables 269 504 684 818 982 Ratios

Other receivables 0 0 0 0 0 Year to Dec (HKD mn) FY10A FY11A FY12E FY13E FY14E

Inventories 149 306 363 466 610 Growth rate (%)

Other current assets 7 17 17 17 17 Revenue 46.8 52.5 17.0 23.7 26.0Fixed assets 11 11 11 11 11 EBITDA 71.7 20.3 12.7 20.6 25.6Intangible assets 0 0 0 0 0 EBIT 72.4 20.3 12.6 20.6 25.6Investment, associates etc 0 0 0 0 0 Net profit 72.0 25.0 7.3 20.6 25.6

Total assets 1,505 2,006 2,275 2,607 3,039 EPS 70.0 (9.7) 7.2 20.6 25.6

Margins (%)

Account payables 143 250 300 388 513 Gross margin (reported) 40.3 35.5 37.0 37.1 37.2Other payables 0 0 0 0 0 EBITDA 24.2 19.1 18.4 17.9 17.9Short-term debt 0 0 0 0 0 EBIT 23.8 18.8 18.1 17.6 17.6Other current liabs 75 155 179 187 199 Net margin 20.1 16.5 15.1 14.7 14.7

Long-term debts 0 0 0 0 0 Other ratios

Deferred tax and others 0 0 0 0 0 ROE (%) 11.3 11.4 10.9 11.6 12.7Other long-term liabs 0 0 0 0 0 ROA (%) 9.7 9.1 8.6 9.0 9.7

Total liabilities 218 405 479 575 712 Net gearing (%) (83.1) (73.0) (66.7) (63.7) (61.0)

Interest coverage (x) NA NA NA NA NAShare capital 100 104 104 104 104 Receivables days 135.7 166.7 193.5 187.0 178.2Reserves 1,187 1,497 1,692 1,928 2,223 Payables days 120.9 128.0 134.5 141.2 148.3

Shareholders' equity 1,287 1,601 1,796 2,031 2,327 Inventory days 125.6 156.8 163.1 169.6 176.4

Minorities 0 0 0 0 0 Effective tax rate (%) 15.7 12.4 16.5 16.5 16.5

Total equity 1,287 1,601 1,796 2,031 2,327

Net cash (debt) 1,069 1,168 1,199 1,294 1,419

Price Market cap PE (x) PB (x) Dividend yield (%)

Ticker (HKD) (HKD mn) FY11A FY12E FY13E FY11A FY12E FY13E FY11A FY12E FY13EChina EFT-POS manufacturersShenzhen Xingu-A 300130 CH 18.03 2,061 22.7 16.6 12.4 1.8 1.7 1.5 0.7% 1.5% 2.5%Average 22.7 16.6 12.4 N/A 1.8 1.7 1.5 0.7% 1.5% 2.5%

Global EFT-POS manufacturersVerifone Systems PAY US 229.03 24,692 9.6 10.8 9.0 2.6 2.5 2.2 0.0% 0.0% 0.0%Ingenico ING FP 407.09 21,365 33.8 18.3 16.0 3.3 3.0 2.6 1.3% 1.3% 1.6%Average 21.7 14.5 12.5 N/A 3.0 2.7 2.4 1.3% 1.3% 1.6%

Pax Global 327 HK 1.38 1,432 7.9 7.3 6.1 0.9 0.8 0.7 0.0% 0.0% 0.0%

Page 19

Page 19 of 19

Rating Policy

Rating Definition

Stock Rating Buy Outperform HSI by 15%

Neutral Between -15% ~ 15% of the HSI

Sell Underperform HSI by -15%

Sector Rating Accumulate Outperform HSI by 10%

Neutral Between -10% ~ 10% of the HSI

Reduce Underperform HSI by -10%

Analysts List

Antony Cheng Research Director (852) 2235 7127 [email protected]

Hayman Chiu Senior Research Analyst (852) 2235 7677 [email protected]

Kenneth Li Senior Research Analyst (852) 2235 7619 [email protected]

Lewis Pang Research Analyst (852) 2235 7847 [email protected]

Susanna Chui Research Analyst (852) 2235 7131 [email protected]

Analyst Certification

I, Susanna Chui hereby certify that all of the views expressed in this report accurately reflect my personal views about

the subject company or companies and its or their securities. I also certify that no part of my compensation was / were,

is / are or will be directly or indirectly, related to the specific recommendations or views expressed in this report / note.

Disclaimer

This report has been prepared by the Cinda International Research Limited. Although the information and opinions

contained in this report have been compiled or arrived at from sources believed to be reliable, Cinda International

cannot and does not warrant the accuracy or completeness of any such information and analysis. The report should not

be regarded by recipients as a substitute for the exercise of their own judgment. Recipients should understand and

comprehend the investment objectives and its related risks, and where necessary consult their own financial advisers

prior to any investment decision. The report may contain some forward-looking estimates and forecasts derived from

the assumptions of the future political and economic conditions with inherently unpredictable and mutable situation, so

uncertainty may contain. Any opinions expressed in this report are subject to change without notice. The report is

published solely for information purposes, it does not constitute any advertisement and should not be construed as an

offer to buy or sell securities. Cinda International will not accept any liability whatsoever for any direct or consequential

loss arising from any use of the materials contained in this report. This document is for the use of intended recipients

only, the whole or a part of this report should not be reproduced to others.