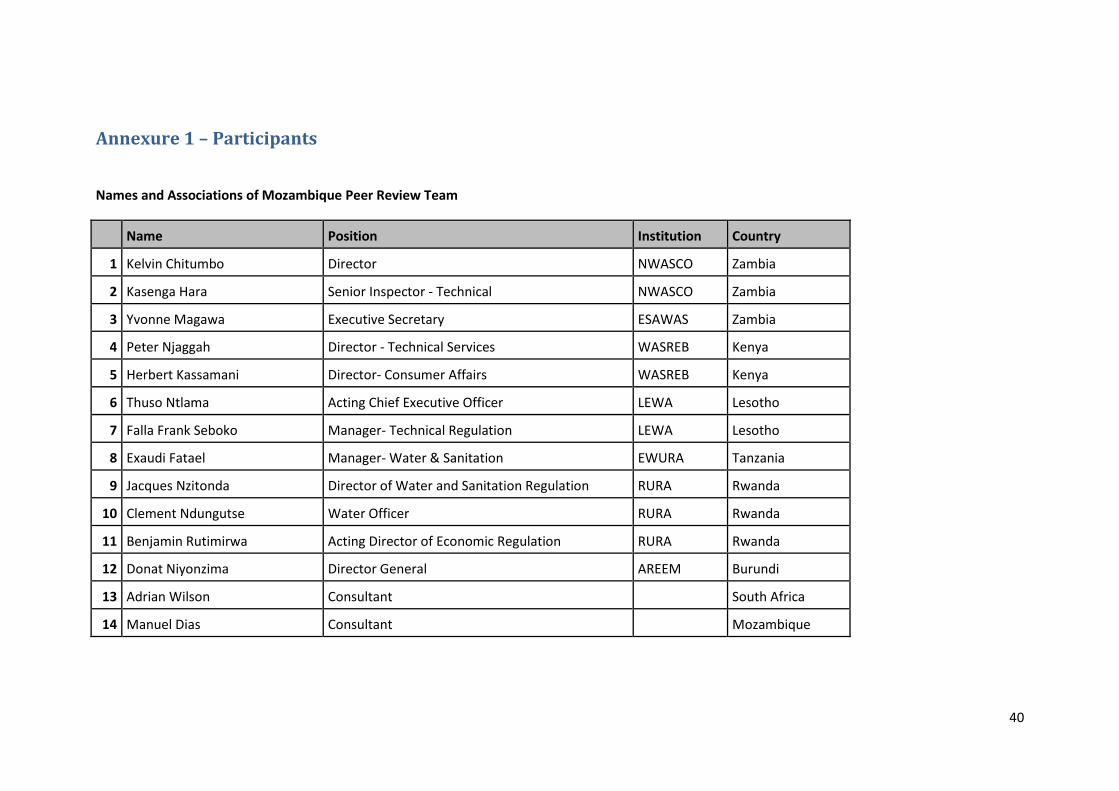

Peer Review of Water Services Regulatory System in Mozambique EASTERN AND SOUTHERN AFRICA WATER AND SANITATION REGULATORS ASSOCIATION Peer Review of Water Supply and Sanitation Services Regulatory System In Mozambique Final Report, 12 th October 2016 Prepared by: Adrian Wilson of A J Wilson and Associates International and Manuel Carilho Dias, for ESAWAS

Transcript

Peer Review of Water Services Regulatory System in Mozambique

EASTERN AND SOUTHERN AFRICA WATER AND SANITATION REGULATORS ASSOCIATION

Peer Review of Water Supply and Sanitation Services

Regulatory System In Mozambique

Final Report, 12th October 2016

Prepared by: Adrian Wilson of A J Wilson and Associates International and Manuel Carilho Dias, for ESAWAS

Acknowledgements

The authors would like to acknowledge the key inputs of the following organisations and

individuals:

The range of stakeholders interviewed who gave freely of their time (see Annexure 2).

The Peer Review Team (see Annexure 1), each of whom contributed significantly to the end

product.

CRA as the hosts and for all of the logistical arrangements

Dr Rolf Eberhard (et al) who developed the original Peer Review methodology used for this

and the three previous Peer Reviews that were carried out.

Peer Review of Water Services Regulatory System in Mozambique

i

Contents List of Tables ......................................................................................................................................... ii

Table of Figures ..................................................................................................................................... ii

Abbreviations ....................................................................................................................................... iii

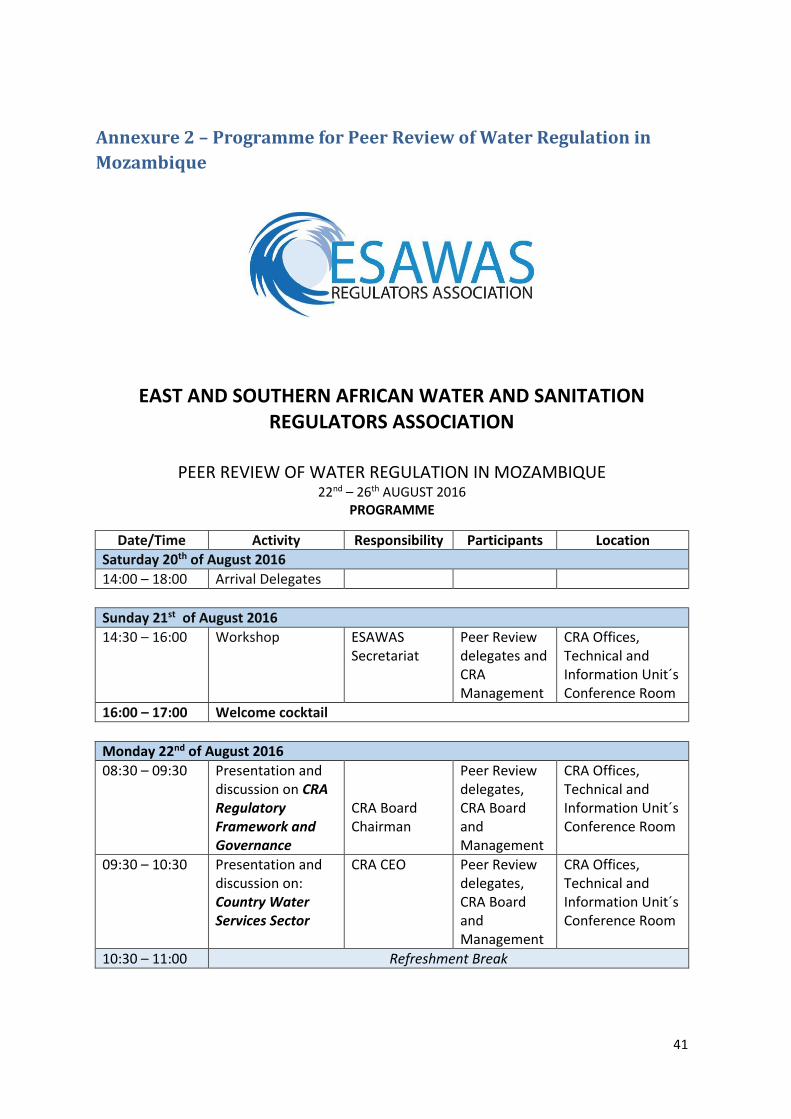

Annexure 2 – Programme for Peer Review of Water Regulation in Mozambique ............................. 41

Annexure 3 – Peer Review Process ..................................................................................................... 45

List of Tables Table 1. Schedule of Tariffs ................................................................................................................. 24

Table 2. Summary of the Regulatory Performance of Primary Systems ............................................. 29

Table 3. Projected Costs and Tariffs for Major Systems ..................................................................... 33

Table of Figures Figure 1: Evaluating Infrastructure Regulatory Systems ....................................................................... 2

Figure 8. Map of the Areas Covered by the Water and Sanitation Utilities in Mozambique ............. 21

Figure 9. Water Service Coverage ....................................................................................................... 30

Figure 10. Reliability of Supply ............................................................................................................ 31

Figure 11. Water Quality Compliance ................................................................................................. 32

Peer Review of Water Services Regulatory System in Mozambique

iii

Abbreviations AdeM Aguas da Região de Maputo

AIAS Administração de Infra-estruturas de Águas e Saneamento ALCs CRA Local Agents or Local Delegates AREEM Agence de Régulation des Secteurs de L'eau Potable, de L'électricité et des

Mines Capex Capital expenditure CEO Chief Executive Officer CORALs Local Regulatory Commissions CRA Conselho de Regulação de Águas DMF Delegated Management Framework ENASU National Water and Urban Sanitation Strategy 2011-2025 ESAWAS Eastern and Southern Africa Water and Sanitation Regulators Association EWURA Energy and Water Utilities Regulatory Authority FIPAG Water Supply Investments and Assets Fund ICP International Cooperating Partner LEWA Lesotho Electricity and Water Authority NRW Non-revenue water NWASCO National Water Supply and Sanitation Council O and M Operations and Maintenance OPEX Operating expenditure PRT Peer Review Team PTA Water Tariff Policy RF Regulatory Framework RURA Rwanda Utilities Regulatory Authority SLA Service Level Agreement VAT Value Added Tax WASREB Water Services Regulatory Board

1

1. Introduction

A Peer Review of the water services regulatory system in Mozambique was undertaken from 21st to 26th August 2016 under the auspices of the Eastern and Southern Africa Water and Sanitation (ESAWAS) Regulators Association that comprises the following agencies that are responsible for water and sanitation services regulation in their respective countries:

Conselho de Regulação de Águas 1(CRA) --‐ Mozambique

Energy and Water Utilities Regulatory Authority (EWURA) --‐ Tanzania

Lesotho Electricity and Water Authority (LEWA) --‐ Lesotho

National Water Supply and Sanitation Council (NWASCO) --‐ Zambia

Water Services Regulatory Board (WASREB) --‐ Kenya

Agence de Régulation des Secteurs de L'eau Potable, de L'électricité et des Mines (AREEM) --- Burundi

The Peer Review of the water service regulatory system in Mozambique was carried out in partial fulfilment of the objectives of the ESAWAS Regulators Association that are two‐fold: firstly capacity building and information sharing through the facilitation of information sharing and skills training at national, regional and international level to enhance the capacity of members in water supply and sanitation regulation; and secondly regional and regulatory cooperation through the identification of best practices to improve effectiveness of water supply and sanitation regulation in the region. The Conselho de Regulação de Águas hosted the Peer Review. The Peer Review Team is given in Annexure 1, the programme in Annexure 2 and the process is described in Annexure 3.

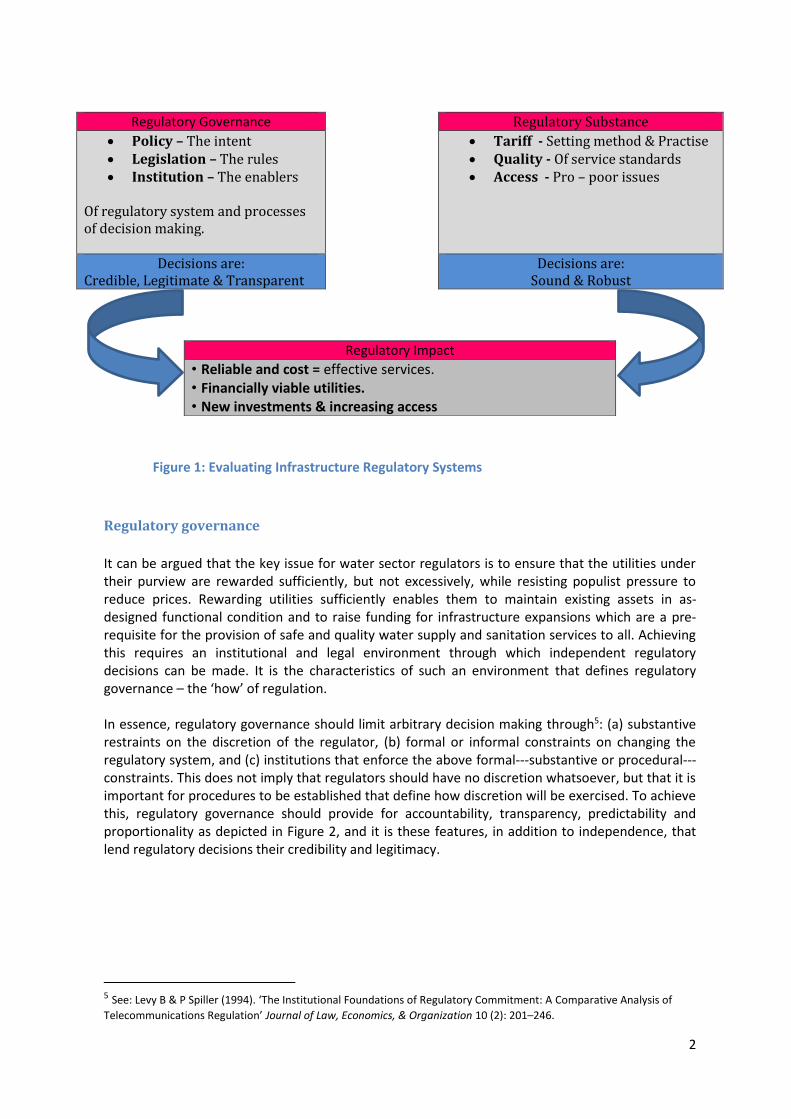

1.1 Peer Review framework The Peer Review of Mozambique’s water supply and sanitation sector (water sector2) regulatory system was premised on an adaptation of the framework detailed by Brown et al. in the Handbook for Evaluating Infrastructure Regulatory Systems3 and on the experience of the African Electricity Regulator Peer Review and Learning Network4. Brown et al. define the regulatory system as ‘the combination of institutions, laws, and processes that give government control over the operating and investment decisions of enterprises that supply infrastructure services. It is argued that the evaluation of such a system should take into the account three interrelated dimensions as depicted in Figure 1, that is, regulatory governance, regulatory substance and regulatory impact. Regulatory performance was assessed in terms of three concepts: regulatory governance, regulatory substance and regulatory impact.

1 Water Regulatory Council. 2 In this report references to the “water sector” unless otherwise specified implies the “water supply

and sanitation sector”. 3 Brown, AC, J Stern & B Tenenbaum with D Gencer (2006). Handbook for Evaluating Infrastructure Regulatory Systems.

New York: World Bank. 4 The African Electricity Regulator Peer Review and Learning Network is an initiative of the

Management Programme in Infrastructure Reform and Regulation (MIR) at the University of Cape Town (UCT) Graduate School of Business (GSB).

2

Regulatory Governance Regulatory Substance

Policy – The intent Legislation – The rules Institution – The enablers

Of regulatory system and processes of decision making.

Tariff - Setting method & Practise Quality - Of service standards Access - Pro – poor issues

Decisions are: Credible, Legitimate & Transparent

Decisions are: Sound & Robust

Figure 1: Evaluating Infrastructure Regulatory Systems

Regulatory governance

It can be argued that the key issue for water sector regulators is to ensure that the utilities under their purview are rewarded sufficiently, but not excessively, while resisting populist pressure to reduce prices. Rewarding utilities sufficiently enables them to maintain existing assets in as-designed functional condition and to raise funding for infrastructure expansions which are a pre-requisite for the provision of safe and quality water supply and sanitation services to all. Achieving this requires an institutional and legal environment through which independent regulatory decisions can be made. It is the characteristics of such an environment that defines regulatory governance – the ‘how’ of regulation. In essence, regulatory governance should limit arbitrary decision making through5: (a) substantive restraints on the discretion of the regulator, (b) formal or informal constraints on changing the regulatory system, and (c) institutions that enforce the above formal--‐substantive or procedural--‐constraints. This does not imply that regulators should have no discretion whatsoever, but that it is important for procedures to be established that define how discretion will be exercised. To achieve this, regulatory governance should provide for accountability, transparency, predictability and proportionality as depicted in Figure 2, and it is these features, in addition to independence, that lend regulatory decisions their credibility and legitimacy.

5 See: Levy B & P Spiller (1994). ‘The Institutional Foundations of Regulatory Commitment: A Comparative Analysis of

• Reliable and cost = effective services. • Financially viable utilities. • New investments & increasing access

3

Figure 2: Regulatory Governance

The assessment of regulatory governance therefore raises some important questions:

To what extent does the national policy, legislation, institutional design and governance structures of the regulator support the desirable characteristics of independent regulatory decision-making and thus engender credibility and legitimacy?

To what extent have the decisions made by the regulator been perceived by stakeholders as independent? Is the regulator viewed as credible by utilities and funders to the sector? Is the regulator seen as legitimate by consumers?

In addition an important consideration is also regulatory effectiveness. How has the regulator prioritised its activities and how effectively has it used its resources to achieve its intended goals. Does the regulator have a coherent regulatory strategy and how well is it implementing this strategy?

Regulatory substance

Regulatory substance is the content of regulation. It is also referred to as the ‘what’ of regulation. Much of the literature on the rationale for regulation is premised on the theory of natural monopoly. Infrastructure industries, such as the water sector, are highly capital intensive and are characterised by large sunk and specific investments with lifespans of 20 years or more. These characteristics lead to decreasing average cost as output increases. It is therefore less costly to have a single water reticulation system as opposed to multiple systems supplying the same number of customers. Competition and its promise of social welfare optimisation is not applicable under these circumstances. As a result, a firm with natural monopoly power could extract economic rent

4

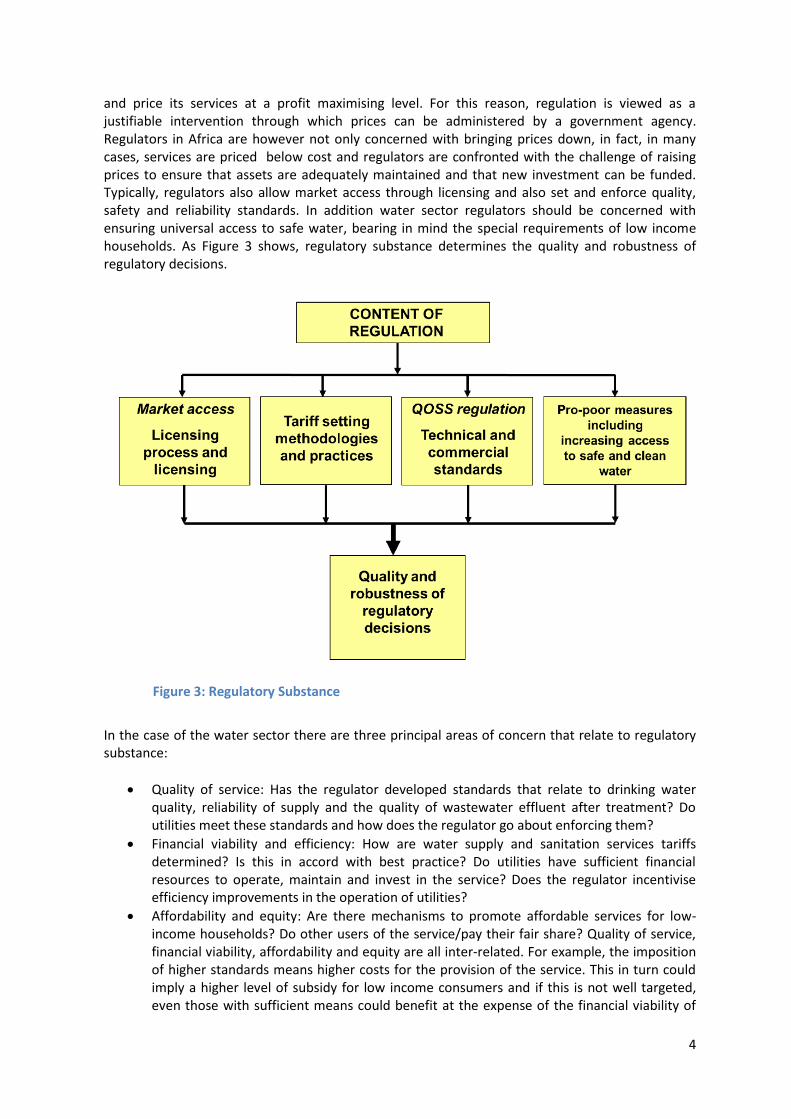

and price its services at a profit maximising level. For this reason, regulation is viewed as a justifiable intervention through which prices can be administered by a government agency. Regulators in Africa are however not only concerned with bringing prices down, in fact, in many cases, services are priced below cost and regulators are confronted with the challenge of raising prices to ensure that assets are adequately maintained and that new investment can be funded. Typically, regulators also allow market access through licensing and also set and enforce quality, safety and reliability standards. In addition water sector regulators should be concerned with ensuring universal access to safe water, bearing in mind the special requirements of low income households. As Figure 3 shows, regulatory substance determines the quality and robustness of regulatory decisions.

Figure 3: Regulatory Substance

In the case of the water sector there are three principal areas of concern that relate to regulatory substance:

Quality of service: Has the regulator developed standards that relate to drinking water quality, reliability of supply and the quality of wastewater effluent after treatment? Do utilities meet these standards and how does the regulator go about enforcing them?

Financial viability and efficiency: How are water supply and sanitation services tariffs determined? Is this in accord with best practice? Do utilities have sufficient financial resources to operate, maintain and invest in the service? Does the regulator incentivise efficiency improvements in the operation of utilities?

Affordability and equity: Are there mechanisms to promote affordable services for low-income households? Do other users of the service/pay their fair share? Quality of service, financial viability, affordability and equity are all inter‐related. For example, the imposition of higher standards means higher costs for the provision of the service. This in turn could imply a higher level of subsidy for low income consumers and if this is not well targeted, even those with sufficient means could benefit at the expense of the financial viability of

5

the utility or social welfare as a whole. The regulator should therefore attempt to balance these and other concerns in reaching regulatory decisions.

Regulatory impact

Regulatory impact is a consequence of regulatory governance and regulatory substance. As stated earlier, the central challenge for water sector regulators is to ensure that the utilities under their purview are rewarded sufficiently, but not excessively, while resisting populist pressure to reduce prices. The key stakeholders in the regulatory system are consumers and utilities. Regulatory impact should therefore strike a balance between the expectations and interests of these two groups. Consumers are ultimately concerned about having access to safe, quality, reliable and competitively priced service. This is however only possible if utilities are financially viable and are able to source funding for refurbishments and new investment. Put differently, the ‘key objective of economic regulation of infrastructure industries is to ensure the continuous supply, over the long‐term, of specified infrastructure services of defined quality at the minimum necessary cost (and prices) to the population and industry of the country6.

1.2 Stakeholder Meetings: Approach to Diagnostics

An exploratory approach was adopted where the different regulatory areas are interrogated through structured discussion in terms of prepared diagnostic checklists and identified areas for discussion. This approach was facilitated by requesting key documentation from CRA including, policy documents, relevant legislation, licenses, methods used and guidelines. Secondly, a list of the pertinent issues was developed (diagnostic sheets) and a checklist of the key issues to be covered was provided for each meeting with stakeholders.

6 Stern J (2009). The Regulatory and Institutional Dimension of Infrastructure Services. Department of Economics Discussion Paper Series, City University, London.

6

2. Key Findings

2. 1 Regulatory Governance

2.1.1 Context

In 1995, as a result of the approval of the National Water Policy (Resolution No. 7/95), the

Mozambican Government began the liberalization of the urban water supply sector. In 1998, the

reform of the urban water supply sector began after a long period of insufficient investment, as

well as technical, economic and financial downturn among companies within the sector, which had

been fully controlled by the state. The reform sought to establish a clear institutional delineation of

the different roles within the sector. One of its core features was the liberalization of the water

supply market, that is, the entry of private operators. As part of this process of liberalization, two

new bodies emerged, the Water Regulatory Council (CRA) and the Water Supply Investment and

Assets Fund (FIPAG). Later, another player was setup: Administração de Infra-estruturas de Águas e

Saneamento (AIAS).

The new governing structure within the sector, the Delegated Management Framework (DMF),

aimed to distinguish the following roles:

1. Government: definition of policies;

2. CRA: regulation of the sector;

3. FIPAG: asset owner/management/lessor, responsible for infra-structure investment and

financing, now covering the 11 water main systems;

4. AIAS: asset owner/management/lessor, responsible for infra-structure investment and

financing covering the sanitation and water secondary systems and

5. Private: system operations concessionaires, established through various forms of contracting.

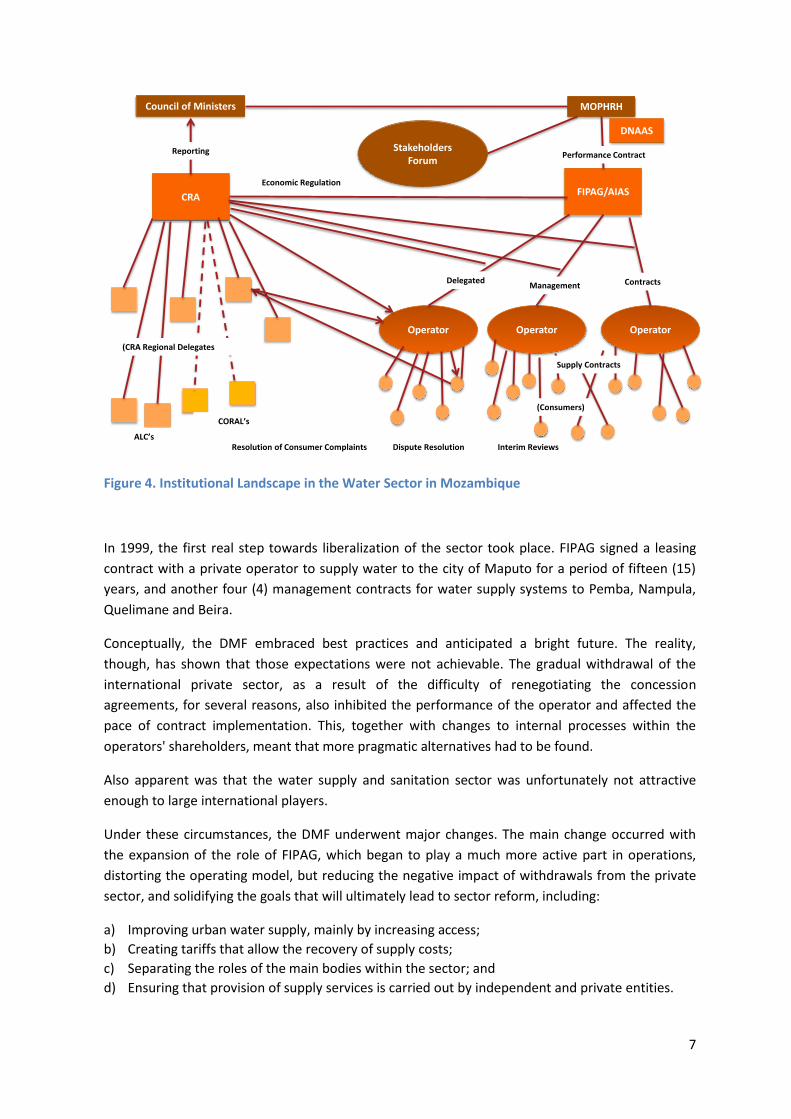

The overall institutional landscape, as it currently stands, is illustrated in Figure 4 below:

7

Figure 4. Institutional Landscape in the Water Sector in Mozambique

In 1999, the first real step towards liberalization of the sector took place. FIPAG signed a leasing

contract with a private operator to supply water to the city of Maputo for a period of fifteen (15)

years, and another four (4) management contracts for water supply systems to Pemba, Nampula,

Quelimane and Beira.

Conceptually, the DMF embraced best practices and anticipated a bright future. The reality,

though, has shown that those expectations were not achievable. The gradual withdrawal of the

international private sector, as a result of the difficulty of renegotiating the concession

agreements, for several reasons, also inhibited the performance of the operator and affected the

pace of contract implementation. This, together with changes to internal processes within the

operators' shareholders, meant that more pragmatic alternatives had to be found.

Also apparent was that the water supply and sanitation sector was unfortunately not attractive

enough to large international players.

Under these circumstances, the DMF underwent major changes. The main change occurred with

the expansion of the role of FIPAG, which began to play a much more active part in operations,

distorting the operating model, but reducing the negative impact of withdrawals from the private

sector, and solidifying the goals that will ultimately lead to sector reform, including:

a) Improving urban water supply, mainly by increasing access;

b) Creating tariffs that allow the recovery of supply costs;

c) Separating the roles of the main bodies within the sector; and

d) Ensuring that provision of supply services is carried out by independent and private entities.

Council of Ministers

CRA

Reporting

(CRA Regional Delegates

MOPHRH

Stakeholders Forum

DNAAS

FIPAG/AIAS

Performance Contract

Economic Regulation

Operator Operator Operator

DelegatedManagement Contracts

Supply Contracts

(Consumers)

Interim ReviewsDispute ResolutionResolution of Consumer ComplaintsALC’s

CORAL’s

8

In order to understand the framework in question, it is important to highlight the initial scope of

the DMF, which was initially only focused on water supply, and not sanitation, and only focused on

large urban water supply systems. Decree 18/2009 expanded the scope of the DMF, which became

part of the wider public systems for water distribution and sanitation. Public systems started to be

structured in both urban (major and secondary) and rural areas. The Decree also established the

integration of the Board of Water and Sanitation Infrastructure (AIAS) as part of the DMF.

Decree No. 74/98 established CRA, within the creation of the DMF (Decree No. 72/98) and, in 2009,

Decree 18/2009 gave CRA an expanded mandate. As a result of Decree No. 23 on June 8, 2011, the

CRA designation was modified and a review of regulation tools was created, clarifying the

enforcement mechanisms of CRA's authority. In formal terms, the CRA has been administratively

and financially independent since the start.

CRA is responsible for matching the interests of consumers of public water supply with the

objectives of operators, ensuring a balance between quality of service, public interest, and

economic sustainability of water supply provision. Thus, the CRA is responsible for:

a) Economic regulation of urban drinking water supply.

b) Monitoring and advising on the design and implementation of delegated management

contracts for water supply systems, as well as the activity of the managing bodies.

CRA is also responsible for:

a) Promoting agreements of interests between the Lessor and Operator, acting as a pre-

arbitration conciliation forum;

b) Identifying development needs and potential expansion of services according to the needs of

current and future customers, and in particular ensuring, through the tariff system, the

economic sustainability that supports the extension and improvement of the quality of water

supply systems; and

c) Performing other tasks assigned to CRA in concession or management contracts and that fit

into its global goals.

The decree 18/2009 extends CRA's mandate to regulate all public water supply systems and

sanitation through configurations and regulatory systems adapted to technical conditions and

specific management systems.

The expansion of CRA's mandate, within the framework of the DMF, should be considered in two

dimensions:

Nature of the subject of the regulation: integration of sanitation; and

Target systems: all public systems of water supply and sanitation are to be regulated.

Generally, sanitation systems are less developed than water supply systems, making them less

attractive to private investors. Currently most, if not all, sanitation systems are potentially subject

to regulation but are not economically and financially sustainable. On the other hand, sanitation is

a sectoral area where inconsistencies, overlaps or omissions within the legal and regulatory

framework are particularly evident, especially when it comes to local authority and CRA powers.

9

For CRA, sanitation is a new regulatory area. It requires the development of new models and

regulatory processes, new skills, acquisition of additional resources and even an adjustment of its

basic operating model. However, the biggest challenge may well be to obtain the necessary funding

for regulatory activity, considering the current framework of unsustainable economic and financial

operators.

As for water supply, the expansion of CRA’s mandate brings its own financial, personnel and

resource-related challenges, as well as potential difficulties at governance levels and within

operating models. The number of secondary systems that may be subject to regulation is large and

geographically widely spread. Policies and practical organizational processes will be required to

implement regulation. Additionally, the majority of secondary systems that are currently integrated

in the regulatory context, are systems in a precarious economic and financial condition. The

funding of regulatory activity will thus bring with it additional challenges.

A number of parties that were interviewed commented upon the future scope and direction of

regulation and the Regulator in the country:

a) The role of FIPAG as operator – considering that this reality results from a Government

pragmatic decision, it is largely accepted that such position should not last forever and FIPAG

should reduce or withdraw from operator role in benefit for the private sector. We were

informed that FIPAG is in process to separate its role as asset owner/lessor from operation

through the setup of additional 3 regional (North, Centre and South) utilities companies (apart

from AdeM) that will be operated by the private sector.

b) Other main concern was regarding the role of CRA in the regulation of sanitation where

Municipalities play a stronger role. It has been difficult to move forward with regulation in this

domain because the sanitation public service has not been defined yet and also because there

is a legislation conflict between the legal CRA mandate and Local Authorities powers.

2.1.2 Legislative

The performance of a public service market regulator largely depends on its independence, in

various different regards. Independence is an important characteristic of the Regulation framework

and its activity concerning public entities in the field (in this case the water supply and sanitation

sector). The Regulator acts within a given policy framework defined by Government policies. Thus,

the Government will legislate, set priorities and define sector policies.

The political and legal framework of the water supply and urban sanitation sector, and therefore

the performance of the CRA, is defined by four (4) main references:

a) Water Policy (Resolution n.º 46/2007);

b) National Strategy for Urban Water and Sanitation;

c) Water Tariff Policy; and

d) Five-Year Government Program 2015 – 2019

The Water Policy comprises a vision for the water subsector, whose aim is to provide good quality

and widely available water for future generations. This vision embraces the fundamental principles

of universality, equality, sustainability and inter-generational solidarity.

10

Some of its main goals, aligned with the Millennium Development Goals, are:

Ensuring universal access to a safe and reliable water supply and increasing the quality of

service;

Establishing sanitation improvement as a critical tool for preventing waterborne diseases and

ensuring universal access to sanitation services.

The Water Policy is also important as it recognizes the economic value of water, beyond its social

and environmental value. It maintains that, in order to allow services to become financially viable,

the price of water should reflect its economic value.

It also emphasises that the role of Government is to define priorities, standards, regulations,

minimum levels of service, and to promote and channel investments and policy-making, including

the tariff policy, as well as to promote the provision of services by the private sector. This

promotion of the private sector role in public service provision explains the need for regulation and

a strong regulator.

In order to better present the operating model of the sector within this context, and the roles of

the various bodies within it, the Water Policy states that the water supply in urban and peri-urban

areas should be managed by independent institutions operating on commercial principles, and that

in those institutions, the private sector will be involved.

The legislation also highlights that the Government and Municipalities will always ensure the

independent management of water services.

As part of the Water Policy, the Government also defines its policy guidance for regulation. For

instance, it states that regulation should be developed according to the separation of roles,

establishing independent regulation for service providers, both private and public.

The Government also states that water tariffs should ensure the economic and financial

sustainability of all systems, including provision to renew and replace short-lived goods.

The Government is a primary source of funding for the rehabilitation and expansion of

infrastructure. In terms of operation, it also accepts the subsidization of tariffs to allow access to a

basic level of services in order to ensure the operational sustainability of the systems, always within

the model of independent management of water supply services.

In the sanitation subsector, the policy guidelines are very similar to those set out for water supply.

According to the policy framework, municipalities and local authorities hold the main responsibility

for decision-making regarding the provision of sanitation services, but the operation, maintenance

and management of sanitation systems in urban areas must be undertaken by independent entities

as a municipal service, either through a municipal company or through a management contract

with a private company, operating on commercial principles.

Similarly, the Water Policy states that the Government provides the main investment for

rehabilitation and expansion of infrastructure. Politically, the public service tariff should be

economically and financially sustainable, giving the option for the Government to subsidize if

necessary.

11

In addition, the Government maintains that the water policy tariff must be guided by the following

principles:

User pays;

Polluter pays;

Sustainability;

Equality;

Efficient use of water;

Environmental conservation; and

Decentralization and participatory management.

The National Water and Urban Sanitation Strategy 2011 - 2025 (ENASU), defined within the

broader Water Policy, cements the policy’s political orientation, that water supply sustainability is

to be promoted through the involvement of independent entities, private operators or

independent municipal services, operating on a commercially orientated basis.

ENASU reinforces the political point of ensuring the separation of government roles from public

domain asset management, service provision, and regulation in order to reinforce their supervisory

activity and guarantee adequate service to citizens.

ENASU advocates decentralizing roles to local authorities as a Government priority, aiming to

ensure the provision of good quality public services, promote collective participation in decision-

making, and thus accountability, and increase responsibility levels of local agents.

Through the ENASU, the government restates its goal of ensuring a universal service of urban

water supply until 2025 and sets the minimum level of service to be guaranteed in urban areas at

access to at least 20 liters per person per day of drinking water, at a maximum distance of 250

metres and at a reasonable cost. To achieve this, the Government’s guidance is to ensure that the

tariff structure includes a social grade category to make sure that the cost of the service will not

reduce access to water supply.

ENASU also reinforces the political point of separating roles and the need to ensure collective

participation wherever possible in decision-making processes.

In terms of developing the service provision role, the ENASU considers the participation of the

private sector crucial in the management of water supply systems in small towns and villages,

based on commercial principles.

On the other hand, it also sets out a political strategy of protection of Delegated Management

contracts in order to ensure the compliance of contractual terms through the intervention of the

Regulator.

In terms of the urban sanitation sub-sector, the ENASU aims to achieve a universal service up to

2025, which currently appears potentially difficult to achieve. In order to succeed, the strategy is to

focus on the management of the urban sanitation process from wastewater and excreta deposit to

treatment and final disposal.

In terms of governance, the strategy defines the need to establish the capacity for urban sanitation

management by creating Independent Municipal Sanitation Services and developing a sanitation

12

regulatory framework, considering the degree of independence of the service. The ENASU states

that the operation, maintenance and management of urban sanitation systems must be made by

independent entities as a municipal service, a municipal company or by a management contract

with a private company.

The Water Tariff Policy (Resolution No. 60/98) is another regulatory reference, as it defines

political guidelines for tariffs calculations. As part of the separation of roles, the Government posits

that its function is to set the tariff policy and not to define or approve the specific tariff of the

service of each system, for which the regulator takes responsibility.

The most recent policy guidance tool is the Five-Year Government Programme 2015 - 2019. In

Priority II: “Develop human and social capital”, the Government defines one of its strategic goals as

increasing access to and provision of water and sanitation services.

In order to achieve this objective, the Government states that the following priority actions are to

be developed:

Continuing to establish new piped household connections (taps in outdoor yards or indoors) in

urban areas;

Continuing to implement activity aiming to reduce losses in water supply systems; and

Increasing access to basic sanitation services to ensure good quality of life of citizens and

eradicate diseases;

Rehabilitating and expanding water supply systems in cities and towns, giving priority to

municipalities, namely those referred to in the Program; and

Mobilizing financial resources for building or expanding selected water supply systems.

Key Finding: It is a common perception in the sector that the current system of Decrees (though not

of the same status as an Act of Parliament) creates a sound basis/mandate for the Regulator,

particularly for water. The situation for sanitation is more ambiguous and creates some overlaps

and confusion. A key question is whether the legislative position can be strengthened by an Act

specifically addressing water services sector regulation (and by implication CRA).

2.1.3 Independence

The governance model of CRA segregates the deliberative and executive roles, which is perceived

by the leadership of the organization as an important difference to be emphasised for the Mission

of the regulator.

The deliberative body of CRA is a collegial body named Plenário, and is composed of the President

of the organization (on a full-time basis) and 2 members (on a part-time basis), who are appointed

by the Council of Ministers, on a joint proposal of the Ministers of Public Works and Housing as well

as Finance.

All members of the Plenário are appointed on the same time and for 3 years. The fact that all

members are appointed in the same time may impact on the continuity/stability of the organisation

in case of replacement of members.

13

The Board does not elect its own Chair. In general terms this is not considered to be a best-practice

approach, though the fact that the position is appointed by the Prime Minister is positive. The

current Chairperson (President) has many years of experience and is held in high esteem in the

sector. This has resulted in some concerns about whether CRA will be able to be as effective, upon

his departure. This is highly complimentary towards the current incumbent but also poses some

questions with regard to succession planning.

The size of the board is small in comparison to other boards. It is an expertise based board, rather

than representing particular interests, which is a positive aspect. There is debate with respect to

the optimum size of a Board of this nature. Clearly small size can lead to increased effectiveness

and costs are reduced. It nevertheless has the potential to be suboptimal in terms of the range of

skills needed to fulfil the range of fiduciary responsibilities necessary. From a governance

perspective, it also does not really permit sub committees on aspects such as remuneration and

financial audit.

The financial independence of the Regulator depends on the regulation fee and the volumes of

water provision in the systems. The regulation levy is set at 2% of the gross annual revenues of the

water utilities according to the forecasted annual average revenue. 40% of the regulation fee is

remitted to the Ministry of Finance and the remaining 60% is to finance CRA. The revenues

generated by CRA depend on operators’ activity and feasibility (currently most of the systems are

not able to pay the regulation fee).

Key Findings: An aspect that could perhaps be reconsidered is that of the terms of Board members,

which are currently on a concurrent basis. This can lead to significant disruption when a new Board

is appointed. Experience with the other regulators and indeed with Boards of other organisations is

that sometimes it can take a while for new Board members to become fully acquainted with the

workings of the organisation. In practice therefore, a significant period of acclimatisation or

induction is often necessary. If staggered terms were introduced, then this potential disruption

would be reduced.

The fact that CRA reports direct to Cabinet means that it can play a high level and strategic advisory

role to the Mozambique Government with regard to the water sector. This was considered to be a

very positive function as it raises the profile of the Regulator as well as giving it the opportunity to

influence key government decisions related to the sector.

The fundamental premise when the regulation fee was set at 2% was that such a value was in line

with practice in Africa and also would be sufficient for CRA sustainability. The 40% of the fee that is

transferred to the Ministry of Finance was therefore not originally anticipated. If it were returned it

would help CRA to be financially independent in operational terms. Under the current regulatory

regime, the income secured is not sufficient to finance the operational costs of CRA.

Overall the independence of CRA was rated highly by stakeholders while at the same time

acknowledging that as it is a quasi-government organisation, it could never be fully independent.

14

2.1.4 Accountability

In terms of the system of appeals, the current process is not specifically covered in water related

legislation, it is rather addressed by civil and administrative justice procedures. The first level of

appeal is to the Plenário of CRA, thereafter matters of legality can be referred to the Administrative

Court, while civil disputes are handled by the Judicial Court. Having said this, there have been no

appeals of significance to date. The approach to dealing with appeals is something that can be

addressed when an Act specifically targeted at regulation in the water sector is addressed at some

point in the future (see later). The appeal process can then consider aspects such as the need for a

Tribunal or an Appeal Panel, consisting of industry experts.

As was noted earlier, CRA is diligent in developing a number of reports including a Sector Report,

Annual Report and Strategic Plan, and submitting these to Cabinet timeously. It was considered

that this enhances the accountability of the organisation. The CRA Annual Reports have to be made

public, by law, within 60 days of submission to Cabinet.

The Board does not approve its own remuneration. This is approved by the Cabinet.

The annual financial statements of CRA are audited externally. They are also reviewed/approved by

the Inspectorate of Finance/Administrative Court.

Key findings: There were complaints that the Sector Reports are not made available timeously to

the sector. Stakeholders were of the view that this was due to lengthy delays with their approval by

the Cabinet.7

2.1.5 Transparency and Participation

CRA is promoting transparency through the publication of an annual report that is well considered

in the sector. In this report, they disclose detailed information about the regulated sector, including

activities performed by CRA and also the performance of regulated entities. This annual report is

submitted to the Cabinet.

CRA also submits the Annual Account Report to the Administrative Court on an annual basis. This is

audited by external auditors and also by the Administrative Court or the Ministry of Finance. Most

of the people interviewed in the Peer Review process raised concerns about the delays in

publication of the Annual Report.

The principle of transparency is also promoted by the benchmarking covering all systems under the

CRA regulation and focusing on quality of service.

Some of the entities interviewed considered that, even though the benchmarking process has been

improving, the grouping criteria adopted is not the best, that is, comparison among similar sized

entities. Most of those interviewed had high regard for the value of the report but expressed

concern about time relevance in terms of the delays in publication, which sometimes is only made

7 CRA however have indicated that it is more due to technical reasons, such as the long period that the regulated entiies take to submit performance reports to CRA, particularly the audited report. Thereafter analysis and compilation by CRA and printing procedures take place. All of this currently makes it impossible to have the report available before the end of July.

15

available to the public more than one year later. Some stakeholders called for increased

verification of submitted data by CRA through field visits.

Consumer participation is one of the areas that would appear to need some improvement. Thus far

it would seem that CRA have been primarily concerned with lessors’ and operators’ participation in

decision making processes and less with consumers. It has perhaps been assumed that consumer

interests are protected by CRA and other authorities. The Peer Review Team (PRT) were informed

that even though some local authorities are involved in the initial process of tariff setting, a proper

or extensive consumer participation process has not been adopted. Some participants mentioned

that the public participatory processes in the country are still in the emerging stage and as such,

this kind of process does not trigger public participation.

In addition to the above comments, at the formal institutional level there is not any consultative

body or liaison body that includes representatives from consumer groups.

To assess the need and expectation of consumers, CRA performs Beneficiary Assessments and

Assessment of Consumer satisfaction surveys.

On the other hand, the ALCs and CORALs appear to be good instruments for CRA to reach

consumers, considering their local presence and proximity. Interviews with stakeholders revealed

that these instruments have been involved in the consumer complaints processes. It would appear

however that their role only covers a limited scope with respect to regulation.

Key findings: To some extent, participatory models are developing as a result of the evolution and

development of societies, a characteristic that will continue to grow in coming years. The challenge

for the CRA is to take advantage of this trend and strengthen its credibility with consumers and

regulated entities without compromising the effectiveness and efficiency of its processes.

2.1.6 Predictability

In general, there were few complaints from stakeholders with regards to the predictability of CRA’s

deliberations and decisions, except for the area of annual tariff increases. In this regard it is

apparent that the problem is not with the process that CRA undertakes to arrive at tariff increases.

This would appear to be understood and accepted by stakeholders. The determination is for a

period of five years, so that also provides good levels of predictability for utilities and the sector as

a whole. In terms of CRA’s mandate annual tariff increases are nevertheless submitted to the

Cabinet. In theory this is only for information however in practice this can result in political

interference in the process. To be fair, this does not always occur but can lead to problems at

sensitive times such as, for instance, when elections are soon to be held.

Key finding: It is clear that ideally the tariff approval process should be designed so that the chance

of political interference is minimised.

2.1.7 Proportionality

It was generally considered that the Regulator’s actions are proportional with no complaints made

by stakeholders with respect to this issue.

16

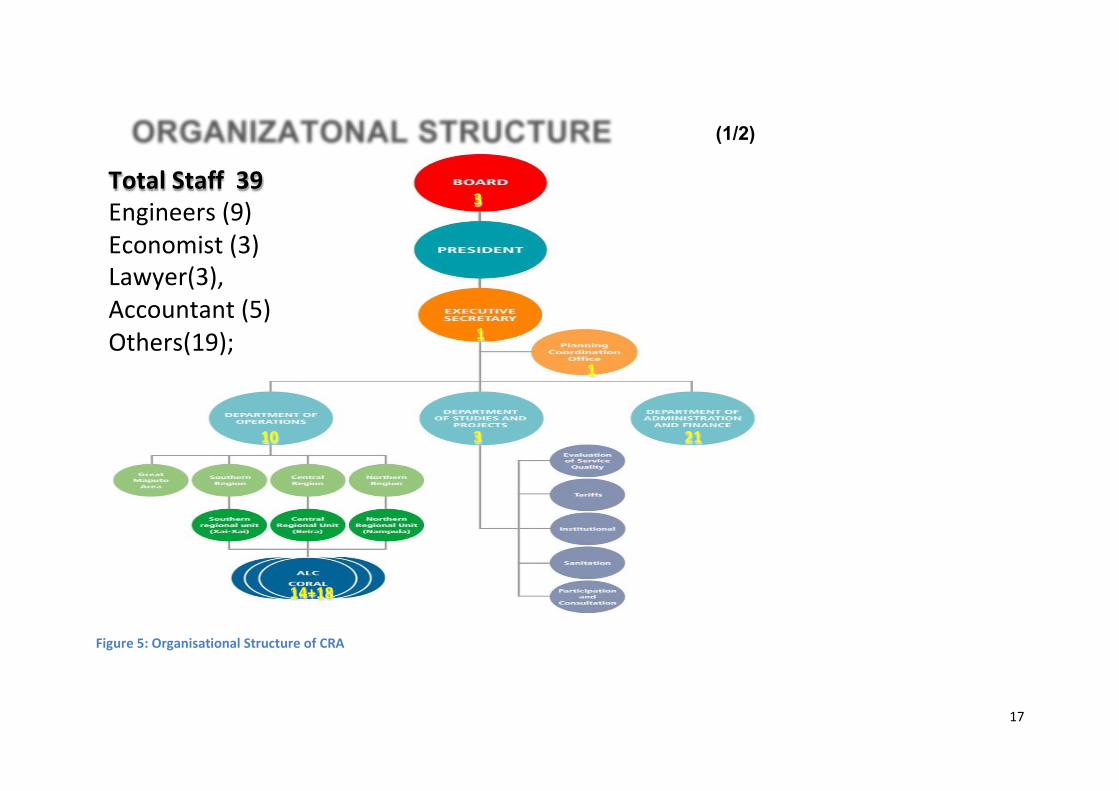

2.1.8 Internal Governance

As was noted earlier, the governance model of CRA segregates the deliberative and executive

roles.

The executive body is comprised of 2 main levels:

a) The Executive Secretary;

b) The Operational areas, including the Department of Operations, the Department of Studies and

Projects, Planning and Control Cabinet and the Department of Administration and Finance.

Under the executive body there are 2 consultation bodies, namely:

a) The Technical Counsel, coordinated by the Planning and Control Cabinet and which also takes

part in the Department of Operations and the Department of Studies and Projects; and

b) The Management Collective, led by the Executive Secretary and which also includes the

coordinators of Department of Operations, Department of Studies and Projects, Planning and

Control Cabinet and Department of Admin and Finance – and depending on the agenda to be

discussed, may include technicians and/or the President of CRA.

The Executive Secretary is appointed by the Plenary after a publicly advertised recruitment process.

The competence of the Executive Secretary is in general to ensure administrative, financial and

technical management of CRA, especially to:

a) Implement CRA’s activities; aimed at the integral achievement of its purposes, attributions and

competence;

b) Elaborate and submit to Plenary the performance, budgets and respective accounts reports;

c) Perform the routine acts necessary for the regular functioning of CRA;

d) Represents CRA from a legal perspective

The Decree 23/2011, includes provision for the creation of an Advisory Council. This has not been

implemented so far because CRA are waiting for the approval of the Statute Review.

CRA has developed some innovative strategies to regionalize and delegate. This leads to improved

subsidiarity and allows CRA to get closer to customers. For a country the size of Mozambique, this

approach is almost essential. The CORAL/ALC model is an interesting one that could have potential

for use in other countries.

The organisational design of CRA is illustrated in Figure 5 below. The quality of staff are highly

regarded in the sector.

More presence (visits) of the head office in/to the regions has been suggested in some quarters.

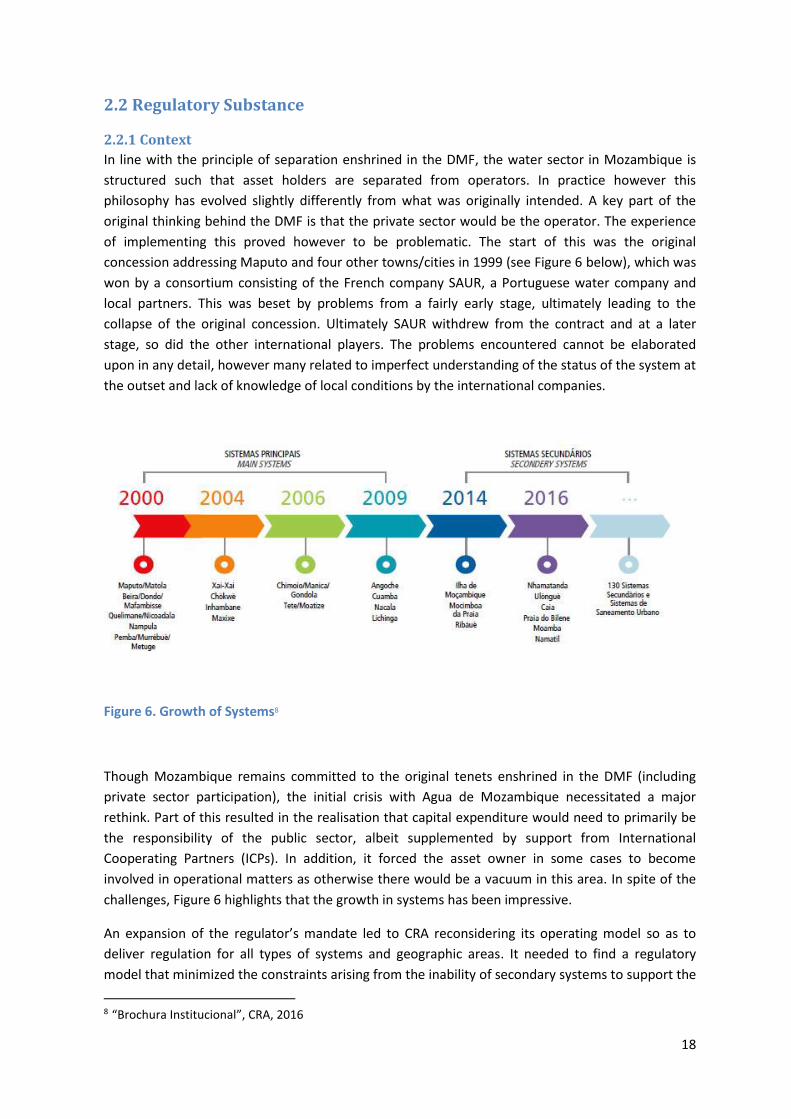

In line with the principle of separation enshrined in the DMF, the water sector in Mozambique is

structured such that asset holders are separated from operators. In practice however this

philosophy has evolved slightly differently from what was originally intended. A key part of the

original thinking behind the DMF is that the private sector would be the operator. The experience

of implementing this proved however to be problematic. The start of this was the original

concession addressing Maputo and four other towns/cities in 1999 (see Figure 6 below), which was

won by a consortium consisting of the French company SAUR, a Portuguese water company and

local partners. This was beset by problems from a fairly early stage, ultimately leading to the

collapse of the original concession. Ultimately SAUR withdrew from the contract and at a later

stage, so did the other international players. The problems encountered cannot be elaborated

upon in any detail, however many related to imperfect understanding of the status of the system at

the outset and lack of knowledge of local conditions by the international companies.

Figure 6. Growth of Systems8

Though Mozambique remains committed to the original tenets enshrined in the DMF (including

private sector participation), the initial crisis with Agua de Mozambique necessitated a major

rethink. Part of this resulted in the realisation that capital expenditure would need to primarily be

the responsibility of the public sector, albeit supplemented by support from International

Cooperating Partners (ICPs). In addition, it forced the asset owner in some cases to become

involved in operational matters as otherwise there would be a vacuum in this area. In spite of the

challenges, Figure 6 highlights that the growth in systems has been impressive.

An expansion of the regulator’s mandate led to CRA reconsidering its operating model so as to

deliver regulation for all types of systems and geographic areas. It needed to find a regulatory

model that minimized the constraints arising from the inability of secondary systems to support the

8 “Brochura Institucional”, CRA, 2016

19

regulation levy on the one hand, and economic and financial sustainability of the regulator, on the

other.

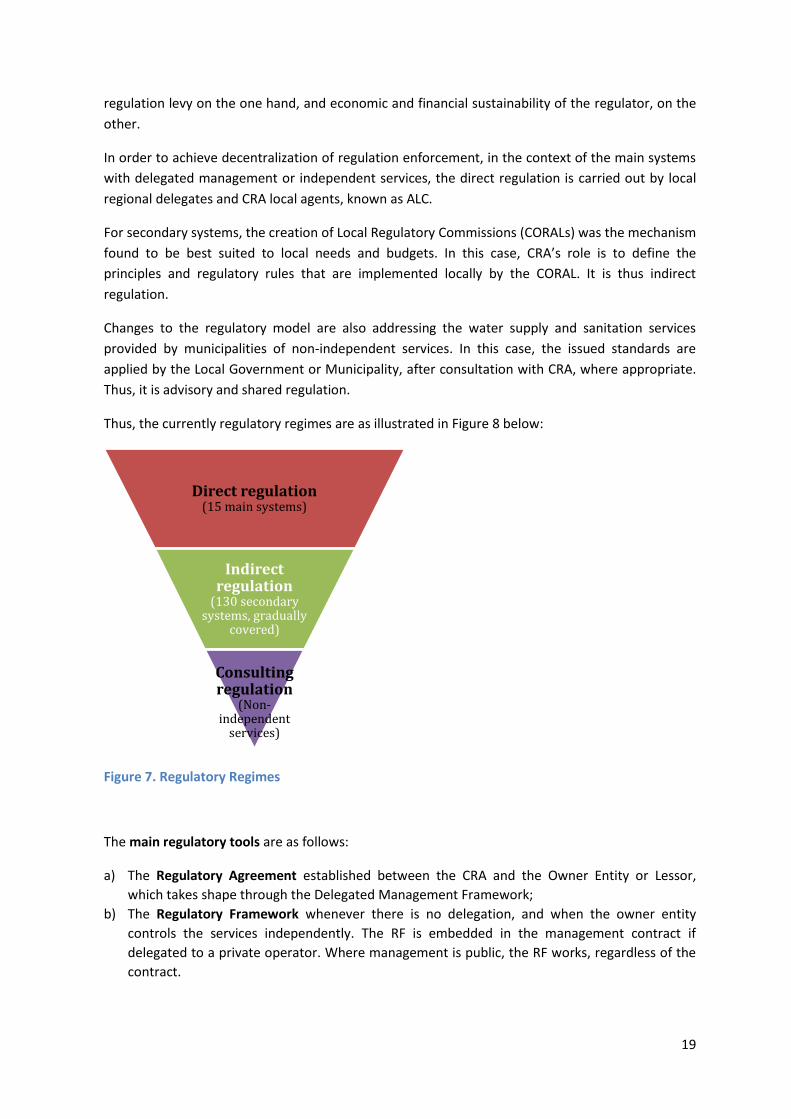

In order to achieve decentralization of regulation enforcement, in the context of the main systems

with delegated management or independent services, the direct regulation is carried out by local

regional delegates and CRA local agents, known as ALC.

For secondary systems, the creation of Local Regulatory Commissions (CORALs) was the mechanism

found to be best suited to local needs and budgets. In this case, CRA’s role is to define the

principles and regulatory rules that are implemented locally by the CORAL. It is thus indirect

regulation.

Changes to the regulatory model are also addressing the water supply and sanitation services

provided by municipalities of non-independent services. In this case, the issued standards are

applied by the Local Government or Municipality, after consultation with CRA, where appropriate.

Thus, it is advisory and shared regulation.

Thus, the currently regulatory regimes are as illustrated in Figure 8 below:

Figure 7. Regulatory Regimes

The main regulatory tools are as follows:

a) The Regulatory Agreement established between the CRA and the Owner Entity or Lessor,

which takes shape through the Delegated Management Framework;

b) The Regulatory Framework whenever there is no delegation, and when the owner entity

controls the services independently. The RF is embedded in the management contract if

delegated to a private operator. Where management is public, the RF works, regardless of the

contract.

Direct regulation(15 main systems)

Indirect regulation

(130 secondary systems, gradually

covered)

Consulting regulation

(Non-independent

services)

20

The two major asset holders that are regulated by CRA are known as FIPAG and AIAS. These only

operate in urban areas and there is no regulation in the rural areas (see Figure 7 below). FIPAG only

operates in major urban areas such as Maputo, Beira, Pemba and Nampula and it only addresses

water, not sewerage. In Maputo, the operator is a separate company called Agua da Região de

Maputo however FIPAG is the majority shareholder. In theory this is treated as an arms-length

arrangement though in practice this may prove to be difficult. FIPAG is the operator in all of the

cities other than Maputo in which they own the assets. FIPAG also operates some of the assets of

AIAS.

The mandate of AIAS is significantly different from FIPAG. With respect to water it is active in the

secondary cities. With respect to sewerage however it is active in both primary and secondary

cities. It does not operate any infrastructure. It is worth noting that sewerage is something of a

contested area in the sense that municipalities also see this as an area of their jurisdiction. The

state of sewerage infrastructure generally in Mozambique is very poor.

21

Figure 8. Map of the Areas Covered by the Water and Sanitation Utilities in Mozambique

22

2.2.2 Licencing

In Mozambique there is currently no formal licensing process and therefore CRA does not have the

mandate to license operators. The license is instead “implicit” in the contract signed between the

asset owner (FIPAG/AIAS) and the operator with a “no objection” input from CRA. This appears to

work satisfactorily.

There are 2 (two) main ways to implement “operations” under the regulatory framework:

a) The asset owner delegates operations (service delegation). In this case a DMF contract is

signed.

b) The asset owner also operates the system. If it operates the system through an “Autonomous

Service” it is signed as a “Regulatory Agreement”. If it operates under a “Non-Autonomous

Service” CRA only acts under consultative regulation9.

The Regulator is not part of the contract between the asset owner and the operator. CRA only gives

a “no objection” input on regulatory related matters.

Also under the broader subject of licences is the issue of access to water resources. In this regard it

is noted that there are significant water resource constraints impacting upon a number of the

utilities. This is obviously a matter of some importance, with Maputo being of particular concern.

Under the current regulatory environment in Mozambique, CRA appears to have limited recourse

to penalties and sanctions. Even those that it has appear to be rarely applied. It also does not make

use of formal directives. It rather achieves its objectives through negotiation, influence and

persuasion. Its high standing in the sector contributes to the fact that this approach has proved to

be effective.

When it comes to inspection, the Regulator makes use of a number of strategies. Regular and ad

hoc inspections are carried out by their Regional Offices. These are supplemented by work carried

out by the ALCs. The ALCs are part time positions located in the main urban centres. Their work is

primarily focussed on addressing customer complaints that are not resolved by the utilities (see

section 2.4). This strategy allows regulatory costs to be controlled and also enhances CRA’s capacity

in regional locations, an important consideration in a country as large as Mozambique.

Key findings: CRA makes very good use of guidelines and has also revised these, when necessary.

These are widely regarded as useful documents. Several stakeholders regarded this as a particular

strength of CRA, which have contributed significantly to best practice in the water sector in the

country.

CRA has to-date not defined detailed penalties for non-compliance. Compliance is largely enforced

through the Regulatory Framework (RF) with sanctions being limited to tariff approvals. This raises

concern regarding the ‘teeth’ of the regulator.

2.2.3 Tariffs and Pricing

The Water Tariff Policy (Resolution No. 60/98) is certainly one of the key regulatory references in

Mozambique, as it defines the political guidelines to calculate tariffs. As part of the separation of

roles, the Government has the function to set the tariff policy and not to define or approve the

9 Thus far however there has been no actual example of this.

23

specific tariff or the service requirements of each system, for which the Regulator takes

responsibility. During the PRT visit it was apparent that during the recent past this was not the case

because the process was impacted upon by political interference. Ideally a consensus should be

reached with all parties, including the Government itself, that such a situation should be eliminated

for the benefit of consumers, operators and society in general.

The Water Tariff Policy (PTA) identifies the following tariff systems for water supply and sanitation

services:

a) Water: drinking water in urban areas, and drinking water in rural areas.

b) Sanitation: conventional sanitation, and low cost sanitation.

The fundamental principles of the PTA are:

There are currently two (2) important tools for economic regulation of tariffs:

a) The tariff model, and

b) The tariff structure.

• Water is a resource with economic value and must be paid for by those who use it according to the cost of provision.

User pays and polluter pays

• Water is a social resource thanks to its obvious importance to the health and welfare of humans. Thus, tariffs should be established to ensure access to basic services of water and sanitation for all citizens.

Equality

•Rational use of water resources and control of water-polluting activities help to protect the environment. Tariffs must reflect the social cost of water use, encourage conservation, promote its rational use and impose penalties on waste.

Environmental conservation and efficient use of water

•Tariffs shall be established to ensure that companies and entities that provide services are sustainable or seek to improve their economic and financial sustainability levels, by covering operating costs, maintenance and management, while ensuring political, social and environmental feasibility.

Sustainability

•Tariffs are set so that the provision of service matches the demand and the user’s willingness to pay. The Government encourages collective participation, nevertheless considering the operational independence of managers.

Decentralization and participatory management

24

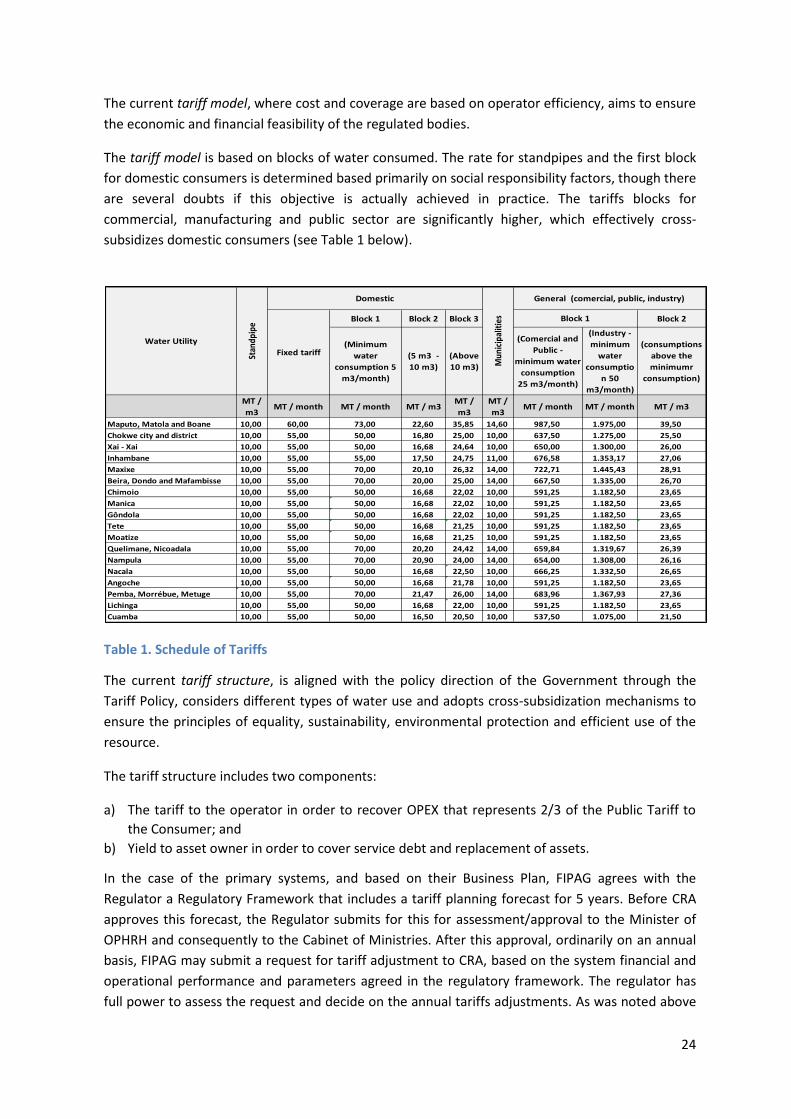

The current tariff model, where cost and coverage are based on operator efficiency, aims to ensure

the economic and financial feasibility of the regulated bodies.

The tariff model is based on blocks of water consumed. The rate for standpipes and the first block

for domestic consumers is determined based primarily on social responsibility factors, though there

are several doubts if this objective is actually achieved in practice. The tariffs blocks for

commercial, manufacturing and public sector are significantly higher, which effectively cross-

subsidizes domestic consumers (see Table 1 below).

Table 1. Schedule of Tariffs

The current tariff structure, is aligned with the policy direction of the Government through the

Tariff Policy, considers different types of water use and adopts cross-subsidization mechanisms to

ensure the principles of equality, sustainability, environmental protection and efficient use of the

resource.

The tariff structure includes two components:

a) The tariff to the operator in order to recover OPEX that represents 2/3 of the Public Tariff to

the Consumer; and

b) Yield to asset owner in order to cover service debt and replacement of assets.

In the case of the primary systems, and based on their Business Plan, FIPAG agrees with the

Regulator a Regulatory Framework that includes a tariff planning forecast for 5 years. Before CRA

approves this forecast, the Regulator submits for this for assessment/approval to the Minister of

OPHRH and consequently to the Cabinet of Ministries. After this approval, ordinarily on an annual

basis, FIPAG may submit a request for tariff adjustment to CRA, based on the system financial and

operational performance and parameters agreed in the regulatory framework. The regulator has

full power to assess the request and decide on the annual tariffs adjustments. As was noted above

however, this was not the case in the recent past and this has affected the financial and

operational performance of the operator and the asset owner. In the tariff determination process,

CRA make use of the concept of a Service Level Agreement (SLA) concept incorporating targets for

a range of key indicators. This implies that if the asset owner does not achieve its targets it may not

get the tariff increase it desires.

Tariffs and revenue collection have been increasing significantly however these are not at a full

viability level yet. Overall there is an important need to move towards fully cost reflective tariffs if

the sector is to become more sustainable.

From a strategic perspective there is clearly a need over the course of time for both the asset

owners and the operators to become fully sustainable and bankable organisations. It was noted in

this regard that this is a process that will take some time to achieve and the differing situational

aspects impacting on the utilities, and their relative strengths and weaknesses, imply that different

utilities will take different time periods to achieve this. In this regard, it is understood that FIPAG is

close to being a bankable organisation. They have been able to secure significant funding support

from the World Bank although this has required guarantees from the Mozambique government. To

what extent this is due to governance, corporate structure issues or financial limitations, is unclear.

It is nevertheless a significant accomplishment when one considers the history of the sector in

Mozambique.

Aguas de Maputo have not been able to cover their operating costs up until recently but

apparently have reached the stage whereby they are able to pay the operating fee to FIPAG for the

first time. This is encouraging and is hopefully a trend that will continue to strengthen.

A major constraint in terms of financial issues is the availability of capex funding and this is

particularly relevant in a developing country such as Mozambique that has many challenges in

terms of access to services and the need to expand service delivery. Only one or two of the utilities

are in a position to fund capex internally and/or access loan funding, and even then, only partially.

This means that they are almost completely reliant on grant funding either from the Government

or from International Cooperating Partners (ICPs). This is a major constraint for the sector and the

country as a whole. This also emphasises the importance of trying to achieve financial sustainability

for the utilities as soon as possible as thereafter they will become much more independent in

terms of accessing funding. This will benefit not only the utilities but also the sector as a whole.

Some stakeholders that the PRT met emphasized the need to promote further studies to validate

the actual benefit for poor families under the tariff first block. It was also proposed to introduce

the exemption of VAT for water services provision while retaining the current level of the tariff.

This would allow the operator to recover costs with minor impact on the consumer.

In view of the lack of progress on sanitation, a ring fenced sanitation surcharge could be considered.

This strategy has been used in Zambia with some good results.

2.2.4 Reliability, Quality and Customer Service

CRA produces technical standards and guidelines for coverage and continuity of service, water

quality and customer care. The standards set are regarded as “mandatory” by CRA and the sector.

26

In terms of coverage, the indicators include number of standpipes, house connections, commercial

connections and numbers of people served. The overall coverage target (acceptable threshold) is

set at 60%, which is relatively low. This is perhaps indicative of how big the challenges were in the

water sector in Mozambique when CRA came in to existence.

Continuity of supply has been an important and high-focus indicator for CRA. It is also apparent

that substantial gains have been made over the years with regard to this indicator. In spite of this

much still needs to be done and it clearly needs to be a continued area of focus in the country. An

acceptable target threshold of 16 hours is set.

An area that may need further consideration is the degree of variation that is “hidden” by the

average figures that are quoted in the Sector Report. Experience in other countries has shown that

there can be dramatic differences in reliability of supply between say, upmarket areas and peri-

urban areas. This is obviously a particular concern since people in these areas are much more

vulnerable due to poverty considerations. In addition, because the volumes applied tend to be

higher in industrial areas and formal residential areas, there is even more potential for problems in

peri-urban areas to be “hidden”. It is believed therefore that a more sophisticated continuity

indicator that incorporates a range of values should be considered in the future.

In terms of water quality this is again a major focus of the Regulator and much has been achieved

over the years. There are a range of applicable water quality determinands set. CRA sets two levels

of performance threshold in this regard, at 80% and 100%.

In the area of customer service, the focus is primarily on times to respond to complaints and

delivery of customer services. The broader area of customer service is, in general, not a strength of

public sector organisations and is thus a potential growth area in future. It is an area where, over

the course of time, sophisticated monitoring systems and KPIs can be introduced that are linked to

call centres, for instance.

2.2.5 Pro-Poor Regulation

Historically the poor have been supplied by community standpipes. The extent of people supplied

by this method is reducing due a number of problems in areas such as costs and customer service.

It nevertheless remains a key strategy as an interim supply strategy for the poor.

Another pro-poor measure is that of the lifeline tariff. This is effectively cross-subsidised by the

more expensive tariffs that are applicable for higher consumption levels in the stepped tariff. This

does not however apply for individual connections due to the system of relatively high fixed

charges that is used in Mozambique (see further discussion under section 2.3.4).

The subsidy and promotion of individual connections is something that has been promoted in the

past in Mozambique and it is understood that this will continue in the future since it benefits both

the customer and the utilities. For the customer it provides a higher level of service and private

connections are much easier to administer than community standpipes or kiosks.

The issue of how the poor can access the Regulator is a difficult issue, which is a challenge in many

countries. It was considered that this is perhaps an aspect that bears further research in

27

Mozambique to try and come up with proposals to improve this. This research should also possibly

look at other measures that can be considered to assist the poor.

As a rule, the provision of services to the poor, is not commercially viable in the conventional

sense. This means that it nearly always requires a capital subsidy. This effectively means funding via

loans to the asset owner(s) or by external sources such as the government or ICPs. In terms of

capital expenditure in the water sector in Mozambique currently, it is heavily dependent on ICP

funding.

2.2.6 Environment/Water Demand Management

The figures for non-revenue water have been a high priority for the Regulator. In this regard, CRA

sets a maximum threshold of 35%. A key issue with regard to NRW is the ability to measure it

accurately but it is not clear to what extent the figures presented by the operators are audited by

the Regulator. Sometimes the figures for NRW increase when measurement is more

accurate/diligent because it becomes better understood.

In the experience of the author, non-revenue water is not an easy issue to address and, in addition,

it tends not to be particularly interesting or appealing to policy makers. This is because it requires a

multiplicity of actions, tactics and strategies conducted over a sustained period (e.g. 10 years) if it is

to make a difference. It therefore requires a long-term major commitment from all players in the

industry. An effective NRW strategy will require a combination of activities covering maintenance

activities, capital maintenance and capital projects. In the Mozambique context, this will require

that the asset owner and the operator work in close cooperation as this could easily result in areas

of overlapping responsibility. While the Regulator will focus on the asset owner, the asset owner

must ensure that the operator is highly motivated in this arena.

It is apparent that the state of wastewater treatment works is extremely poor both in terms of the

condition of infrastructure and their performance. It would appear that to date this has not been a

key area of focus for the sector in Mozambique, with the emphasis being primarily on water supply.

This is also probably due to the fact that the commercial aspects of sewerage systems are more

challenging and hence there is less funding available to carry out the necessary work.

In view of the major environmental impacts, the area of on-site sanitation is another potential

growth area for CRA though it would appear that this will only be addressed at some stage in the

future.

2.3 Regulatory Impact

2.3.1 Context

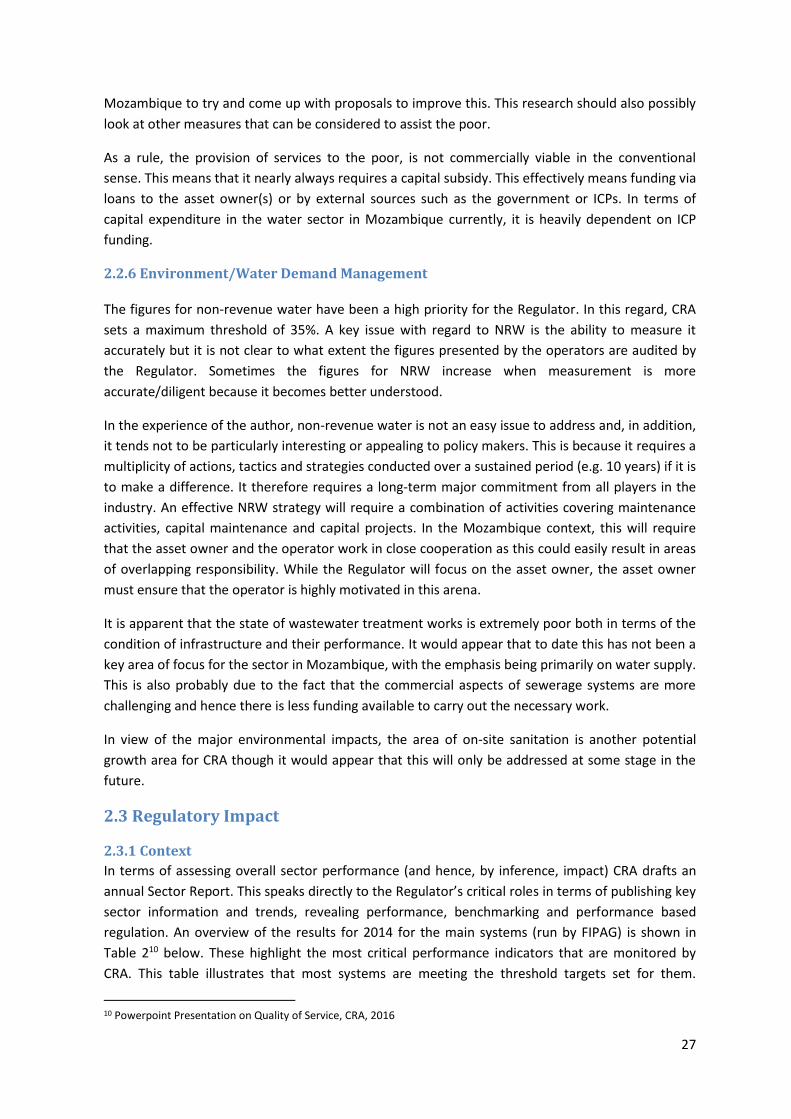

In terms of assessing overall sector performance (and hence, by inference, impact) CRA drafts an

annual Sector Report. This speaks directly to the Regulator’s critical roles in terms of publishing key

sector information and trends, revealing performance, benchmarking and performance based

regulation. An overview of the results for 2014 for the main systems (run by FIPAG) is shown in

Table 210 below. These highlight the most critical performance indicators that are monitored by

CRA. This table illustrates that most systems are meeting the threshold targets set for them.

10 Powerpoint Presentation on Quality of Service, CRA, 2016

28

Notable exceptions include response to customer complaints and water quality compliance.

Performance with respect to operational cost coverage is also mediocre.

29

Table 2. Summary of the Regulatory Performance of Primary Systems

AGREED SERVICE LEVELS

30

2.3.2 Access and Consumption

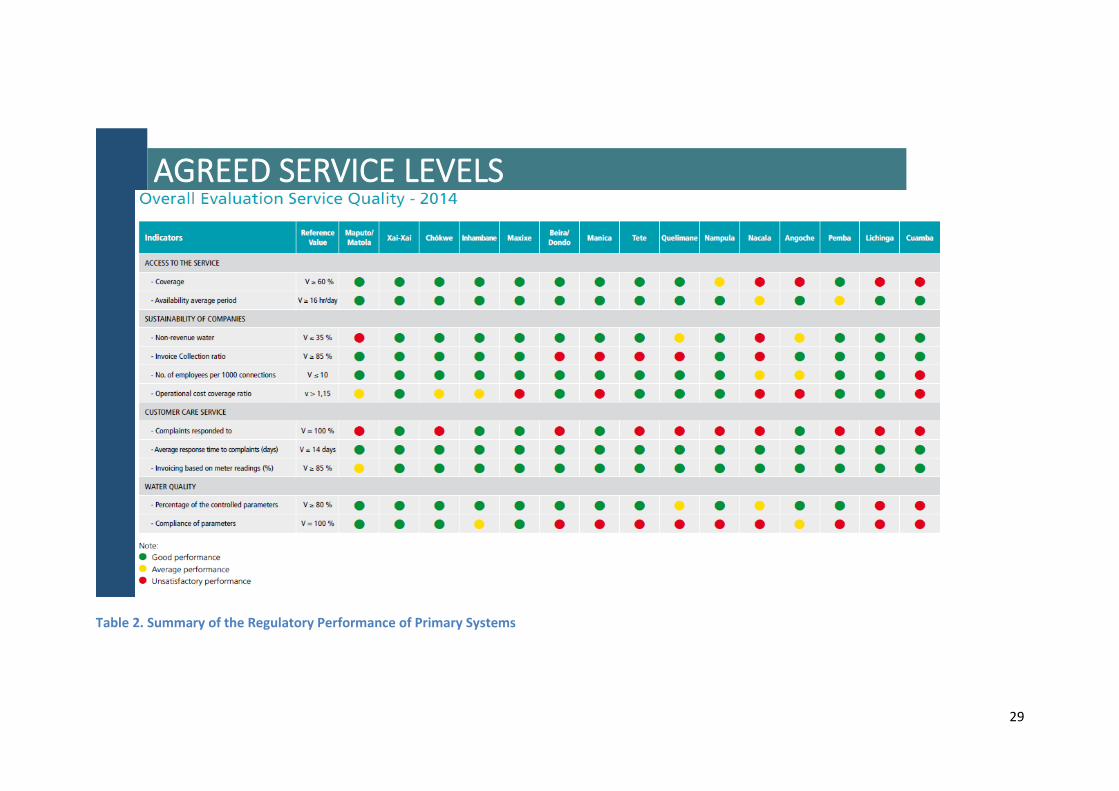

Access is obviously a critical issue in the context of a developing country with significant service

delivery backlogs and this indicator has showed a steady improvement over time. As of 2015, it was

reported that 81% of the urban population had access to an “improved” water supply and 63% in

the rural context11. This definition includes both access to water more generally, for instance via

community standpipes and individual connections. This has resulted in a very significant increase in

water consumption.

The trend with respect to water supply access is illustrated in Figure 9 below, which highlights the

progress achieved for the period from 2009 to 201412. This shows that while there was a dramatic

improvement between 2010 and 2012, this has plateaued in recent years. Apparently this is largely

due to the fact that the bulk capacity of the systems in the major cities has now been exhausted. As

a result, high priority is now being given to increasing the capacity of the bulk systems in places like

Maputo. It is also possible that consumption has stabilised due to the fact that there has been an

increase in metering and billing.

Figure 9. Water Service Coverage

Unfortunately progress on sanitation has been much less. Access to “improved” sanitation was

reported to be 42% in the urban areas and 10% in the rural areas in 2015. It is apparent that the

primary focus of the water services sector in Mozambique in the last 10 to 15 years has been on

improving water supply and not sanitation. The increased pressures of urbanisation, together with

the environmental impacts and public health risks associated with poor sanitation, are likely to

provide increased pressure to focus on sanitation in the years ahead.

11 Powerpoint Presentation by CRA (CEO – Part 1), 2016 12 “Brochura Institucional”, CRA, 2016

31

2.3.3 Safety and Continuity

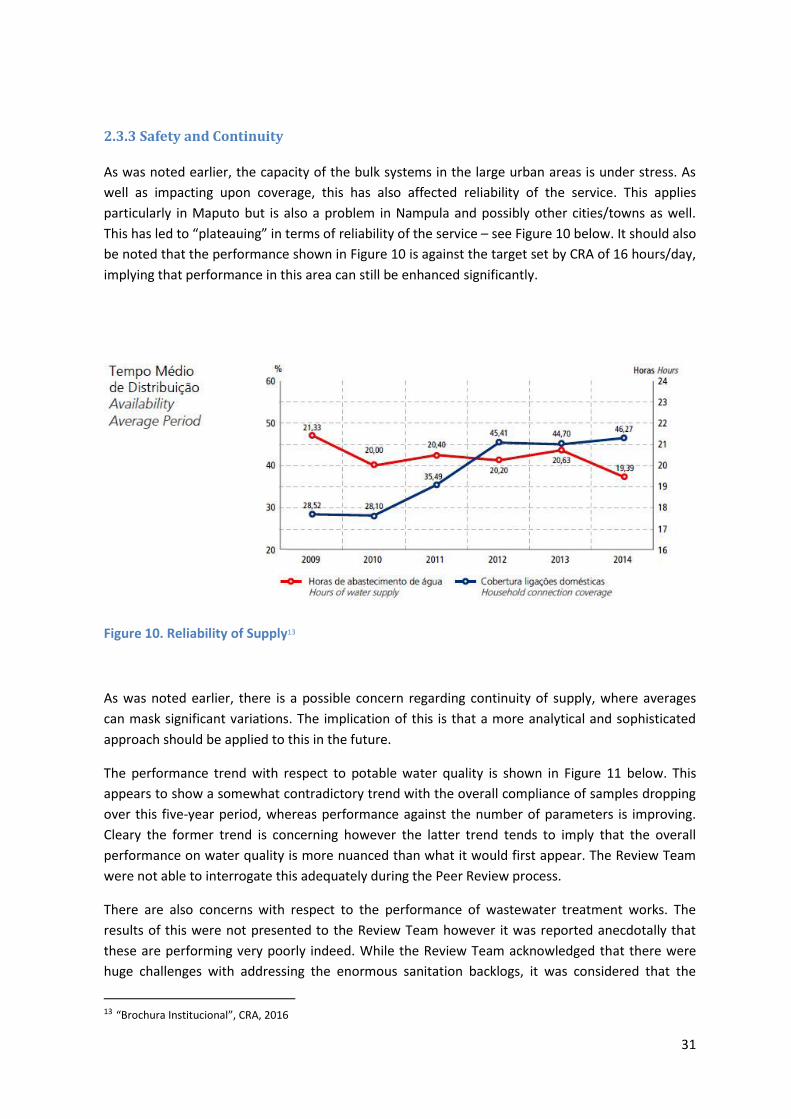

As was noted earlier, the capacity of the bulk systems in the large urban areas is under stress. As

well as impacting upon coverage, this has also affected reliability of the service. This applies

particularly in Maputo but is also a problem in Nampula and possibly other cities/towns as well.

This has led to “plateauing” in terms of reliability of the service – see Figure 10 below. It should also

be noted that the performance shown in Figure 10 is against the target set by CRA of 16 hours/day,

implying that performance in this area can still be enhanced significantly.

Figure 10. Reliability of Supply13

As was noted earlier, there is a possible concern regarding continuity of supply, where averages

can mask significant variations. The implication of this is that a more analytical and sophisticated

approach should be applied to this in the future.

The performance trend with respect to potable water quality is shown in Figure 11 below. This

appears to show a somewhat contradictory trend with the overall compliance of samples dropping

over this five-year period, whereas performance against the number of parameters is improving.

Cleary the former trend is concerning however the latter trend tends to imply that the overall

performance on water quality is more nuanced than what it would first appear. The Review Team

were not able to interrogate this adequately during the Peer Review process.

There are also concerns with respect to the performance of wastewater treatment works. The

results of this were not presented to the Review Team however it was reported anecdotally that

these are performing very poorly indeed. While the Review Team acknowledged that there were

huge challenges with addressing the enormous sanitation backlogs, it was considered that the

13 “Brochura Institucional”, CRA, 2016

32

existing waterborne systems should be an initial area of focus to try and achieve improved

performance. In this regard, CRA highlighted that the institutional arrangements with respect to

sanitation are complex with responsibility being contested between municipalities and the utilities.

This has almost certainly contributed to the lack of progress on sanitation.

Figure 11. Water Quality Compliance14

2.3.4 Pricing trend for water tariffs

The structure of water tariffs in Mozambique includes aspects such as a lifeline tariff, and tiered

tariffs, based on consumption, which are accepted best practice approaches. The tariff structure

also includes fixed elements, in conjunction with the variable charges, which is not uncommon.

What is slightly unusual is that the fixed elements are quite large in comparison to the variable

elements. Apparently this structure was adopted deliberately so as to ensure a reliable level of

income to the operators and asset owners. There is nothing wrong with this per se however in

some cases it can lead to distortions. In this regard, CRA quoted the example of relatively low-

income customers with private connections. Because of their low consumption, it ends up in a

situation whereby they pay more for water than affluent households. This is why ultimately pure

volume based tariffs are the most equitable.

Another important indicator is that of O and M coverage. This is defined as the income necessary

to cover O and M costs and is measured against the collections of the utilities. It speaks to the long

term sustainability of the utilities (and hence the sector as a whole). CRA has reported that 7 of the

15 FIPAG systems achieved a figure in excess of 1,15, while a further 3 were close to achieving this,

which is laudable. A figure well in excess of 1,00 is desirable so as to cover aspects such

depreciation, servicing debt and accumulating surpluses. The performance of the AIAS areas were

not made available to the Review Team.

14 “Brochura Institucional”, CRA, 2016

33

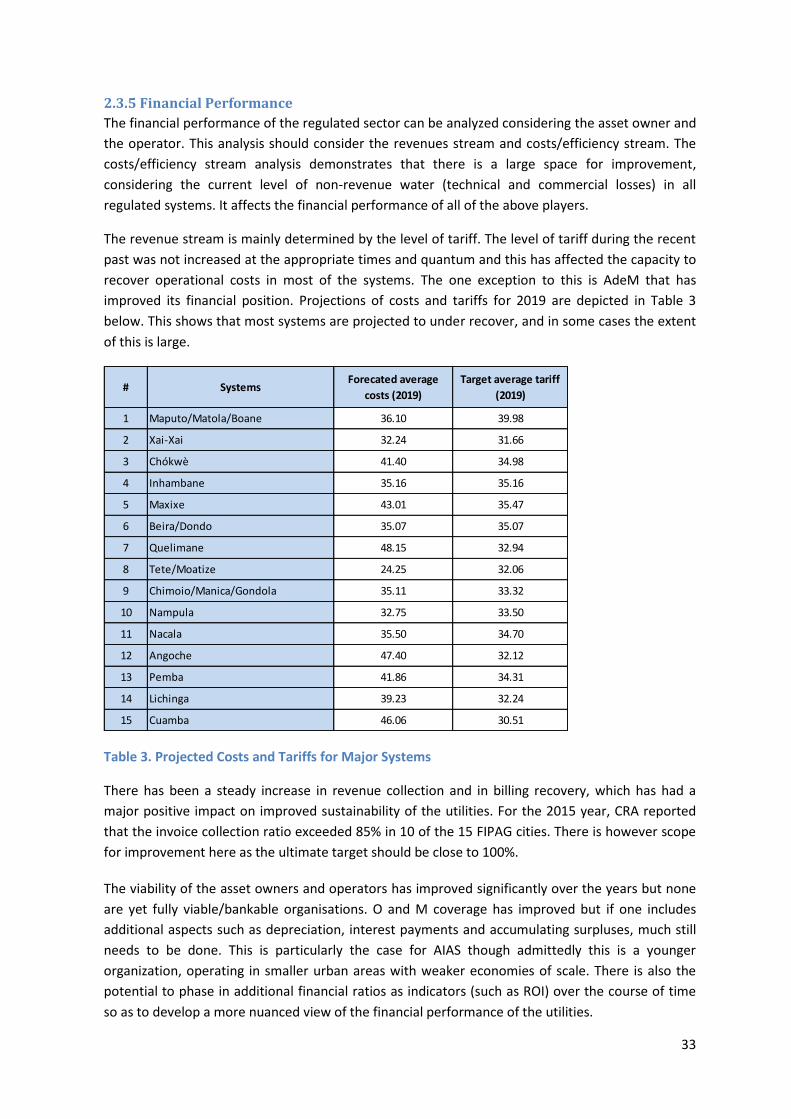

2.3.5 Financial Performance

The financial performance of the regulated sector can be analyzed considering the asset owner and

the operator. This analysis should consider the revenues stream and costs/efficiency stream. The

costs/efficiency stream analysis demonstrates that there is a large space for improvement,

considering the current level of non-revenue water (technical and commercial losses) in all

regulated systems. It affects the financial performance of all of the above players.

The revenue stream is mainly determined by the level of tariff. The level of tariff during the recent

past was not increased at the appropriate times and quantum and this has affected the capacity to

recover operational costs in most of the systems. The one exception to this is AdeM that has

improved its financial position. Projections of costs and tariffs for 2019 are depicted in Table 3

below. This shows that most systems are projected to under recover, and in some cases the extent

of this is large.

Table 3. Projected Costs and Tariffs for Major Systems