Page 1

This is a confidential document solely for the use of client personnel. No part of it may be circulated, quoted, or reproduced for distribution outside the client organization without prior written approval

from Tata Strategic Management Group.

Petrochem Feedstock Overview

Indian Petrochem 2014

- Charu Kapoor, Principal - Chemicals

30th October, 2014

Page 2

Overview of Global Feedstock Scenario

• Feedstocks for Indian Petrochemical Industry

• Key Imperatives

• About Tata Strategic

Page 3

3

Key strategic questions on Feedstock Availability and Imperatives for Indian

Petrochemical Industry

KEY STRATEGIC QUESTIONS

How is the feedstock scenario going to change with major shale gas discoveries in USA?

With availability of cheaper feedstock in terms of shale gas, what is the outlook for global ethylene market?

What processes/ technologies would be adopted for propylene, aromatics production?

How can India leverage its strength of large number of refineries?

What are the imperatives and opportunities for India in this changing scenario?

1

2

3

4

5

Source: Tata Strategic

Page 4

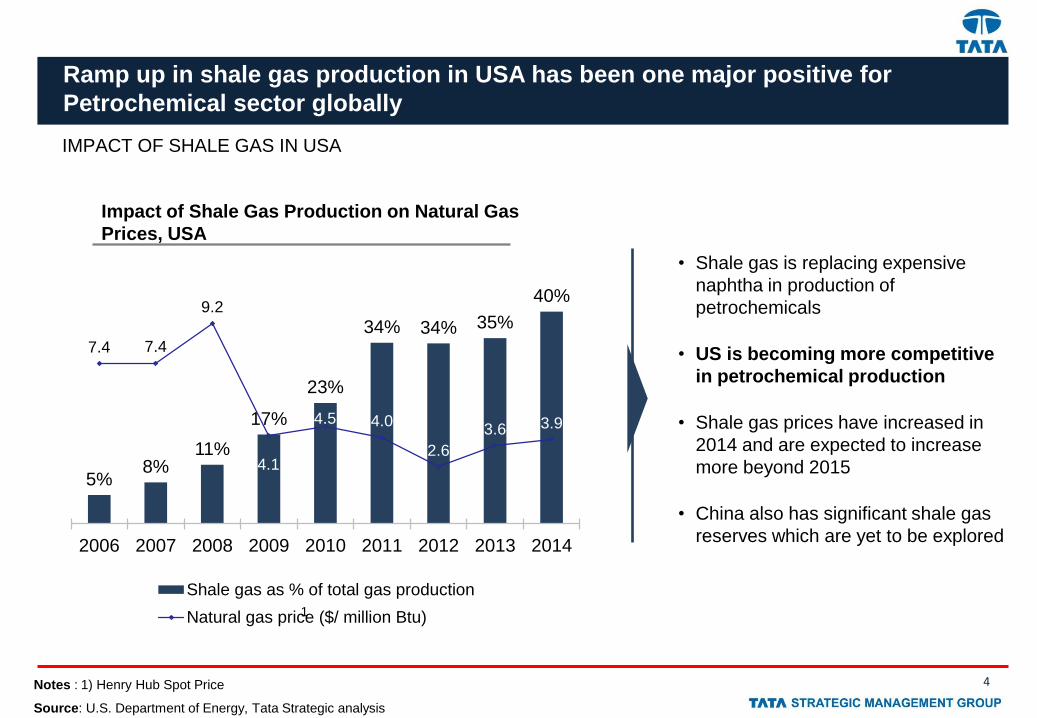

4

Ramp up in shale gas production in USA has been one major positive for

Petrochemical sector globally

IMPACT OF SHALE GAS IN USA

5% 8%

11%

17%

23%

34% 34% 35%

40%

7.4 7.4

9.2

4.1

4.5 4.0

2.6

3.6 3.9

2006 2007 2008 2009 2010 2011 2012 2013 2014

Shale gas as % of total gas production

Natural gas price ($/ million Btu)

Impact of Shale Gas Production on Natural Gas

Prices, USA

Source: U.S. Department of Energy, Tata Strategic analysis

1

Notes : 1) Henry Hub Spot Price

• Shale gas is replacing expensive

naphtha in production of

petrochemicals

• US is becoming more competitive

in petrochemical production

• Shale gas prices have increased in

2014 and are expected to increase

more beyond 2015

• China also has significant shale gas

reserves which are yet to be explored

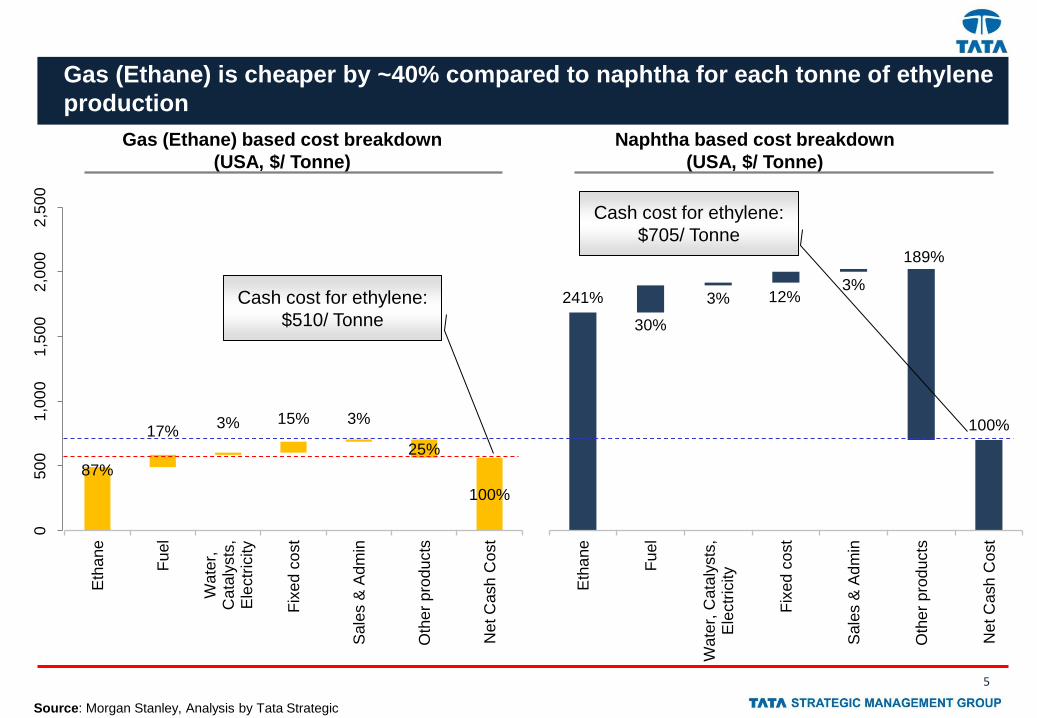

Page 5

5

Gas (Ethane) is cheaper by ~40% compared to naphtha for each tonne of ethylene

production

Gas (Ethane) based cost breakdown

(USA, $/ Tonne)

241%

30%

3% 12% 3%

189%

100%

Eth

ane

Fuel

Wa

ter,

Cata

lysts

,E

lectr

icity

Fix

ed

co

st

Sale

s &

Ad

min

Oth

er

pro

du

cts

Net C

ash

Co

st

87%

17% 3% 15% 3%

25%

100%

Eth

ane

Fu

el

Wa

ter,

Cata

lysts

,E

lectr

icity

Fix

ed

co

st

Sale

s &

Ad

min

Oth

er

pro

du

cts

Net C

ash

Co

st

05

00

1,0

00

1,5

00

2,0

00

2,5

00

Naphtha based cost breakdown

(USA, $/ Tonne)

Cash cost for ethylene:

$510/ Tonne

Cash cost for ethylene:

$705/ Tonne

Source: Morgan Stanley, Analysis by Tata Strategic

Page 6

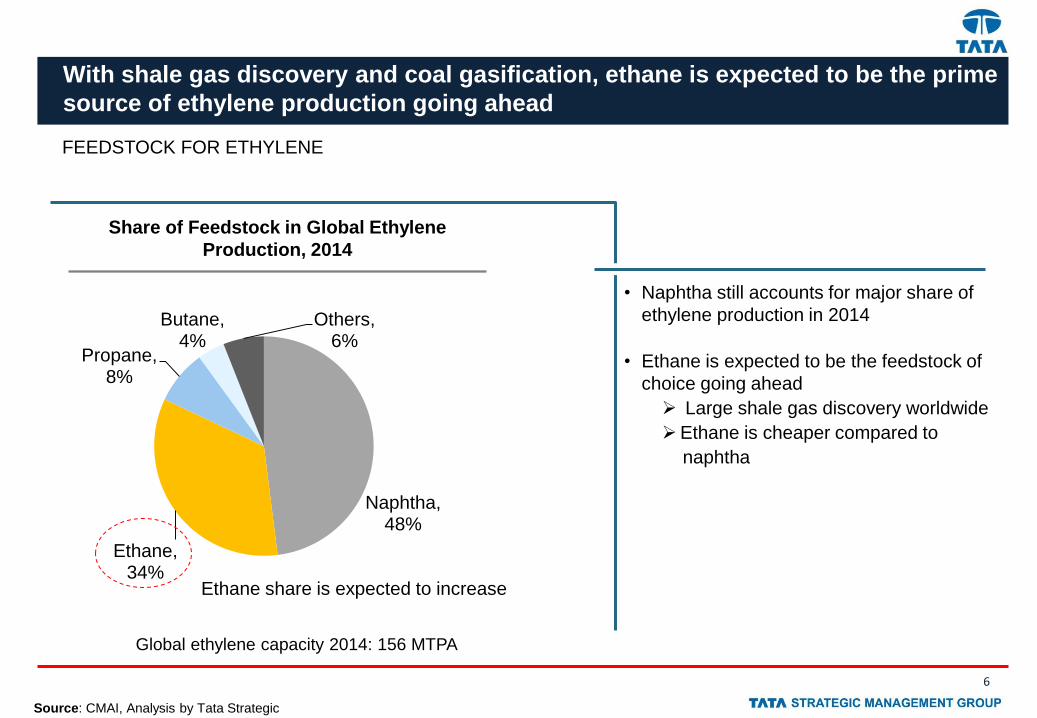

6

With shale gas discovery and coal gasification, ethane is expected to be the prime

source of ethylene production going ahead

Share of Feedstock in Global Ethylene

Production, 2014

Naphtha, 48%

Ethane, 34%

Propane, 8%

Butane, 4%

Others, 6%

Source: CMAI, Analysis by Tata Strategic

FEEDSTOCK FOR ETHYLENE

• Naphtha still accounts for major share of

ethylene production in 2014

• Ethane is expected to be the feedstock of

choice going ahead

Large shale gas discovery worldwide

Ethane is cheaper compared to

naphtha

Ethane share is expected to increase

Global ethylene capacity 2014: 156 MTPA

Page 7

7

Rising shale gas production in USA has led to overcapacity in ethylene and

polyethylene production

ETHYLENE PRODUCTION IN USA

Source: U.S. Department of Energy, Tata Strategic analysis

Ethylene Capacity, USA (Mn tons)

32 34 37 40

51

2010 2012 2014 2017 (E) 2020 (E)

• 14 million tons of ethylene and 10 million

tons of PE capacity addition is planned in

USA by 2020 leading to concerns on

margins

• If all the expansions go through as

planned, the US is looking at a massive

38% increase in existing ethylene capacity

to over 51 Mn tons by 2020

• USA will need to export 25% to 45% of PE

by 2018 if they want to operate at 90%

capacity utilization

Page 8

8

PETROCHEMICALS CAPACITY ADDITIONS

INCREMENTAL ETHYLENE CAPACITY, 2014-2019 [‘000 TONS]

• Large capacities (>1 MnTPA) by

SINOPEC-KPC PC JV in

China

Borouge in UAE

Kayan, Saudi Polymers in

Saudi Arabia

Exxon Mobil in Singapore

Reliance Industries &

OPAL in India

Coal

gasification Natural gas Natural

gas, mixed feedstock

Feedstock

Middle East and Asia would also witness significant ethylene capacity additions

in the next 5 years

Source: Deutsche Bank Chemicals

950

5600

2750

5500

2,550

Africa China India Middle East Asia ex India& China

Page 9

9

With new crackers being ethane based, supply of other olefins has become a

concern

Cracking - yield

Ethylene: 80.0%

Propylene: 1.6%

Butadiene: 1.6%

Others1: 16.8%

Ethylene: 42.7%

Propylene: 22.2%

Butadiene: 2.1%

Others: 33.0%

Ethylene: 33.3%

Propylene: 14.0%

Butadiene: 4.3%

Others: 48.4%

Natural Gas - Ethane Natural Gas - Propane Naphtha

Source: Industry reports, Analysis by Tata Strategic

Notes : 1) Includes benzene, toluene, fuel oil etc

Yield of other olefins such as Propylene, Butadiene, Benzene is low from ethane compared to naphtha

PRODUCTS FROM VARIOUS FEEDSTOCKS

Page 10

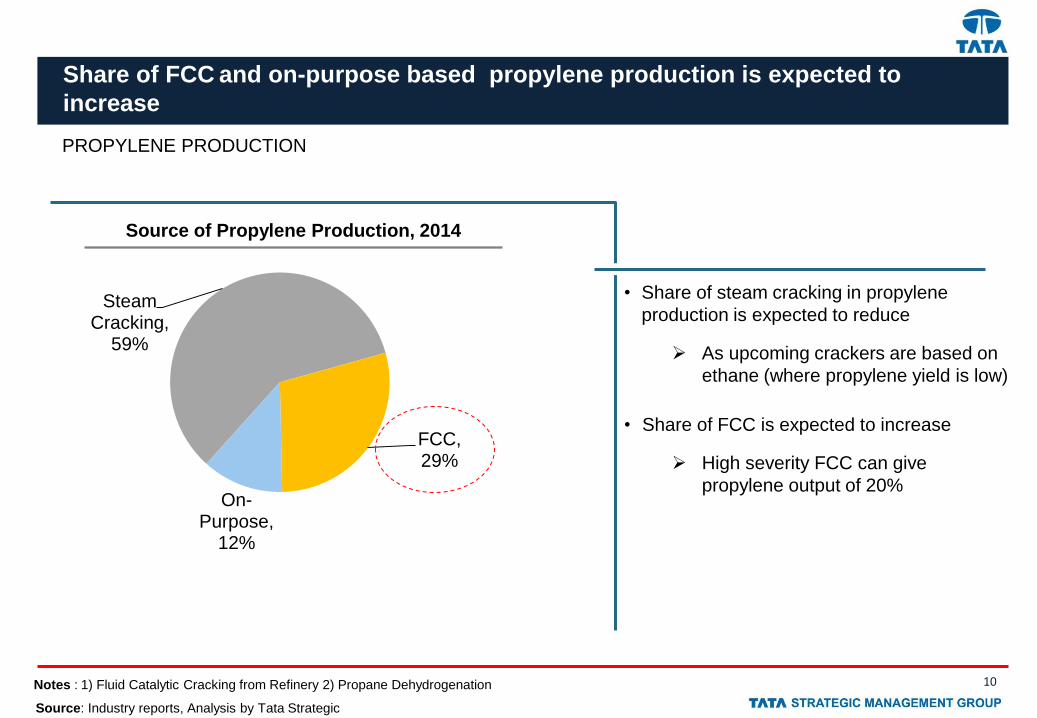

10

Share of FCC and on-purpose based propylene production is expected to

increase

PROPYLENE PRODUCTION

Source of Propylene Production, 2014

Steam Cracking,

59%

FCC, 29%

On-Purpose,

12%

• Share of steam cracking in propylene

production is expected to reduce

As upcoming crackers are based on

ethane (where propylene yield is low)

• Share of FCC is expected to increase

High severity FCC can give

propylene output of 20%

Notes : 1) Fluid Catalytic Cracking from Refinery 2) Propane Dehydrogenation

Source: Industry reports, Analysis by Tata Strategic

Page 11

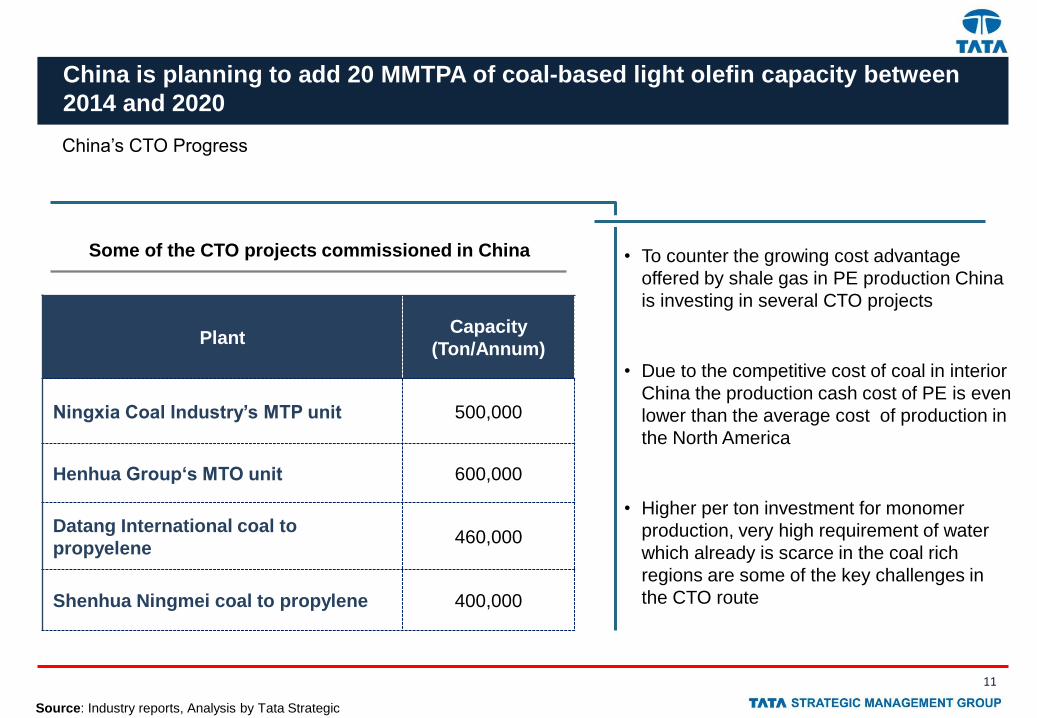

11

China is planning to add 20 MMTPA of coal-based light olefin capacity between

2014 and 2020

China’s CTO Progress

Some of the CTO projects commissioned in China • To counter the growing cost advantage

offered by shale gas in PE production China

is investing in several CTO projects

• Due to the competitive cost of coal in interior

China the production cash cost of PE is even

lower than the average cost of production in

the North America

• Higher per ton investment for monomer

production, very high requirement of water

which already is scarce in the coal rich

regions are some of the key challenges in

the CTO route

Source: Industry reports, Analysis by Tata Strategic

Plant Capacity

(Ton/Annum)

Ningxia Coal Industry’s MTP unit 500,000

Henhua Group‘s MTO unit 600,000

Datang International coal to

propyelene 460,000

Shenhua Ningmei coal to propylene 400,000

Page 12

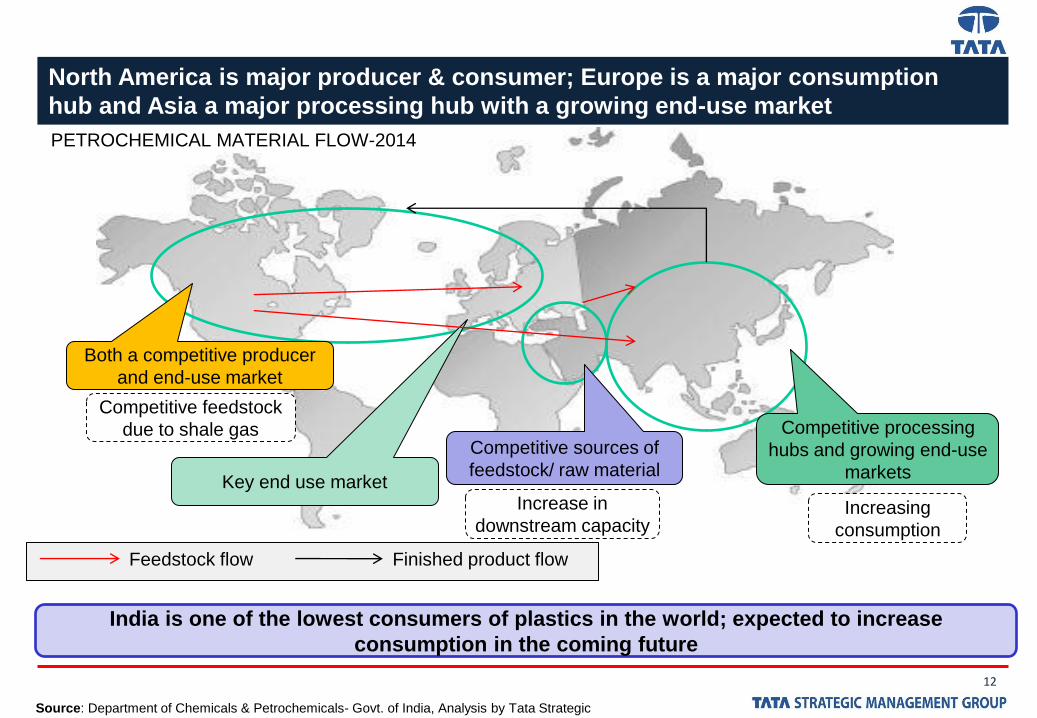

12

North America is major producer & consumer; Europe is a major consumption

hub and Asia a major processing hub with a growing end-use market

Competitive sources of

feedstock/ raw material

Competitive processing

hubs and growing end-use

markets

Both a competitive producer

and end-use market

Feedstock flow Finished product flow

Source: Department of Chemicals & Petrochemicals- Govt. of India, Analysis by Tata Strategic

Increasing

consumption

Increase in

downstream capacity

Competitive feedstock

due to shale gas

Key end use market

PETROCHEMICAL MATERIAL FLOW-2014

India is one of the lowest consumers of plastics in the world; expected to increase

consumption in the coming future

Page 13

• Overview of Global Feedstock Scenario

Feedstocks for Indian Petrochemical Industry

• Key Imperatives

• About Tata Strategic

Page 14

14

India is expected to remain surplus in naphtha, naphtha based crackers would

not be cost competitive

Demand from petrochemicals in FY19 includes demand from existing crackers, new crackers & aromatics complexes

NAPHTHA DEMAND SUPPLY SCENARIO IN INDIA

Source: MoPNG,Industry reports, Estimates by Tata Strategic

Notes : 1) Capacity utilization of refineries is assumed to stay at current levels of ~85%

2) Naphtha percentage by weight as refinery output is assumed to stay at current levels of 8.7%

Naphtha Demand supply (Mn Tons)

18.9

23.6

11.5

17.9

2014 2019 (E)

Production Consumption

NAPHTHA

• Aromatics can be produced from Naphtha

cracker Py-gas

• Py-gas is primarily used for gasoline blending in

India

• Toluene and higher aromatics can be extracted

from py-gas stream from naphtha cracker. India

is significantly short in these raw material

Advantages

Progress so far

• Currently there is no production of Styrene in

India (~100% imports)

• This can be met through the excess Naphtha

cracker capacity

Page 15

15

Petroleum coke has made significant developments in the steam coal industry

over the last few years and will continue to do so in the future

PETCOKE APPLICATIONS

Petcoke

Petcoke to

liquids

Syngas

Synthetic

Natural Gas

As a fuel in

Power Plants

Source: Analysis by Tata Strategic

PETCOKE

• Gasification of petcoke is a favorable technique

since it can capture most of the energy content

and is environmental friendly.

• Petcoke has lower ash, lower moisture, and

lower volatiles than steam coal, resulting in a

much higher heating value

• Production costs associated with pet coke are

considerably low because it is a by-product of

the refining process

Advantages

Petcoke application as a fuel or as a feedstock

Progress so far

• Major global players have plans to set up a

1.1MnTPA acetic acid plant with pet coke as

feedstock

Page 16

16

Low-rank coal as a source of carbon for conversion to olefins has a significant

raw materials advantage over crude oil

Source: Ministry of Coal, GoI, Industry Reports, Tata Strategic Analysis

COAL RESERVES IN INDIA

COAL TO OLEFINS

Raniganj

Jharia

Bokaro

Godavari

Valley

Chanda -

Wardha

Singrauli

Total estimated reserves: ~61 Bn Tonne

Tawa

Valley

Talcher

• Carbon from low grade coal is ~33 times less

costly than carbon from crude oil

• Coal to olefins also offers significant

environmental advantages as it is a wet, low-

severity thermochemical process

• The trend of oil prices staying high in the

international markets have improved the long

term outlook of this industry

Advantages

India’s position vis-à-vis

Leadership position

Progress so far

• Coal block cancellation affecting the project

feasibility

• Coal India Limited to foray into Coal to

Chemical

Reserves Production

China 114 3.8

India 61 0.6Bt

Page 17

17

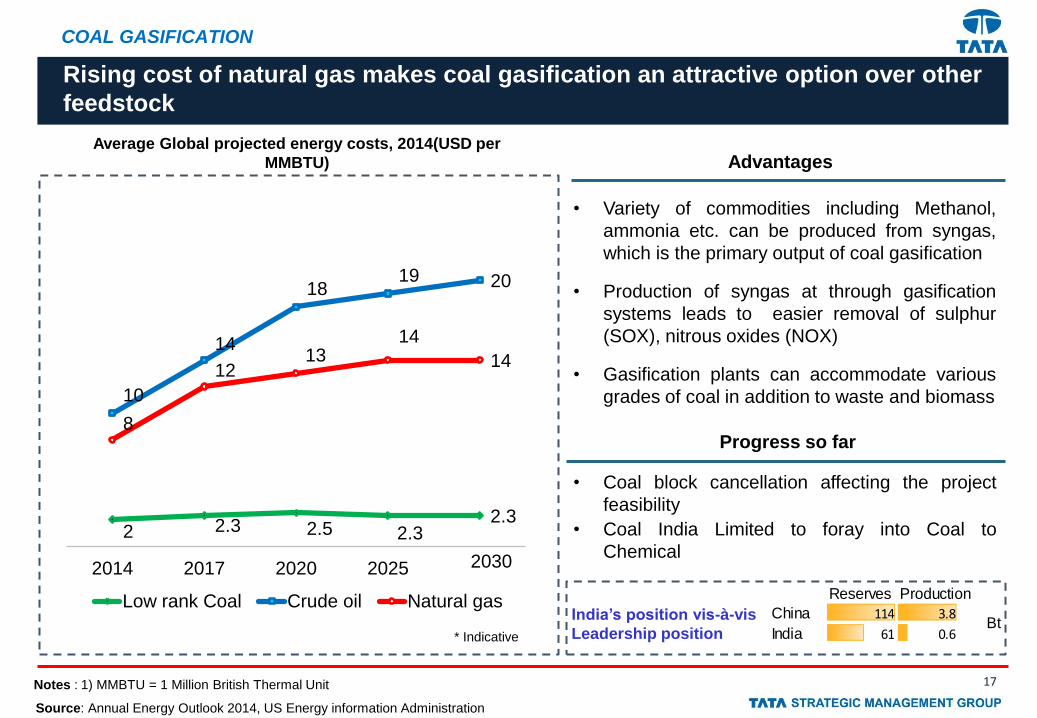

Rising cost of natural gas makes coal gasification an attractive option over other

feedstock

Average Global projected energy costs, 2014(USD per

MMBTU)

2 2.3 2.5 2.3 2.3

10

14

18 19 20

8

12 13

14

14

2014 2017 2020 2025

Low rank Coal Crude oil Natural gas

2030

Source: Annual Energy Outlook 2014, US Energy information Administration

* Indicative

• Variety of commodities including Methanol,

ammonia etc. can be produced from syngas,

which is the primary output of coal gasification

• Production of syngas at through gasification

systems leads to easier removal of sulphur

(SOX), nitrous oxides (NOX)

• Gasification plants can accommodate various

grades of coal in addition to waste and biomass

Advantages

COAL GASIFICATION

Notes : 1) MMBTU = 1 Million British Thermal Unit

Progress so far

• Coal block cancellation affecting the project

feasibility

• Coal India Limited to foray into Coal to

Chemical

India’s position vis-à-vis

Leadership position

Reserves Production

China 114 3.8

India 61 0.6Bt

Page 18

18

CBM is emerging as an alternative feedstock for production of light olefins

through methanol route

Total estimated reserves: 71 Tcf

Source: DGH, GoI

Matix Fertilizer

& Chemicals

Raniganj

Jharia

Sohagpur

Godavari

Cambay

Barmer-

Sanchor

COAL BED METHANE IN INDIA

COAL BED METHANE

• CBM can be used as a feedstock for fertilizer,

steel plants, methanol production and as an

auto fuel in compressed natural gas form

• The products produced from CBM

environmentally superior to many fuels because

they are free of aromatics, nitrogen, and

sulphur, and have a high cetane number

Advantages

Notes : 1) Tcf = Trillion cubic feet

Progress so far

• Commercial production of CBM started in 2007

and latest production numbers are close to 0.30

MMSCMD (million cubic meter per day)

India’s position vis-à-vis

Leadership position

Reserves Production

Russia 1730 1.6

India 71 0.08Tcf

Page 19

19

India’s shale gas reserves may be larger than the conventional gas deposits

and has the potential of being the new and significant contributor to gas supply

KG

Pranhita

Godavari Cambay

Jaisalmer Vindyan Damodar

Valley

Seismic

studies by OIL

in Assam

ONGC is carrying

out pilot projects

Source: EIA, Govt. of India, Industry reports, Tata Strategic Analysis

SHALE GAS RESERVES IN INDIA

SHALE GAS

Total estimated reserves: ~63 Tcf

• The unlocking of domestic shale gas can

help India meet its growing energy demand

• Shale gas industry will have a multiplier

effect on the economy. It is expected that for

every $1 investment in the shale gas

industry will have a new income generation

capability of up to $5

Advantages

Notes : 1) Tcf = Trillion cubic feet

Progress so far

• ONGC & OIL carrying out pilot studies in

Damodar valley

• ONGC to explore 30 additional wells in the

next 2 years

India’s position vis-à-vis

Leadership position

Reserves Production

US 660 4

India 63 0Tcf

Page 20

20

Source: Secondary Research, Industry Report

Biomass as a feedstock can be a significant opportunity for India

Top Field Crop Residues for FY14, Mn tons

159

116 103

Wheat Straw Rice Straw SugarcaneTops

Top Processing Crop Residues for FY14, Mn tons

59

23

6

SugarcaneBagasse

Rice Husk Rice Bran

• A huge array of diverse chemicals are available

from biomass giving the user many new

structural features to exploit.

• India has 180 million hectares of arable land

and >1.5 billion MT/year of food + agri residue

is produced, Hence a large amount of bio waste

at fields & Agri processing units

BIOMASS

Advantages

India’s position vis-à-vis

Leadership position US 16.5

India 14.5Lakh Km2

Progress so far

• India is a favorable establishment for conversion

of residual biomass to olefins due to the

abundance of raw material, but the opportunity

is still untapped.

Page 21

Global Feedstock Scenario

Feedstocks for Indian Chemical Industry

Key Imperatives

• About Tata Strategic

Page 22

22

Key Imperatives for the Industry

Initiatives that Industry can take to

compete globally

1

4 2

3

Ethylene

Source: Analysis by Tata Strategic

• Secure off-take agreements with

upcoming crackers in USA, Middle east

• Investing in downstream derivative unit

or through reverse SEZ route

Aromatics

• Invest in extracting feedstock like Toluene from Naphtha Cracker py-gas

Alternate Feedstocks

• Focus on alternatives like Coal Bed Methane, Coal To Olefins, Biofeedstocks, Domestic Shale gas

Propylene

• Set up High Severity FCCs in refineries

which can process heavier crude for

Propylene production

Page 23

Global Feedstock Scenario

Feedstocks for Indian Chemical Industry

Key Imperatives

About Tata Strategic

Page 24

24

Tata Strategic is the largest Indian owned management consulting firm

AN OVERVIEW

Founded in 1991 as a division of Tata Industries Ltd.

The largest Indian owned Management Consulting firm

Supported by a panel of domain experts

Growing client base outside India

500+ engagements, 100+ clients, across countries, across sectors

Page 25

25

We offer a comprehensive range of solutions covering Direction Setting,

Driving Strategic Initiatives and Implementation

Facilitate

Implementation

Drive Strategic

Initiatives

• Organization Structure

• Culture & HR Transformation

• Manpower Planning &

Optimization

• Leadership Development &

succession planning

Organization Effectiveness

• Revenue Enhancement

• Product Innovation

• Market Share Growth –

Rural/Urban/B2B

• Channel Effectiveness

• Route to Market

Marketing & Sales

• Supply Chain Optimization

• Throughput enhancement

• Superior Fulfillment

• Project Excellence

• Procurement Transformation

• Resource Management

Operations

Set Direction

Strategy

• Scenarios & Vision

• Market insights

• Entry / Growth Strategy

• CSR Strategy

• India Entry

• Alliance & Acquisition Planning

• Strategic due diligence

• Manufacturing Strategy

• Program Management

• Change Management

• Benefit Realization

Implementation

Page 26

26

Tata Strategic has in depth experience of the chemical industry in India

Note: The reports and Thought Notes are available for download from www.tsmg.com

Source: Tata Strategic Management Group

INDUSTRY REPORTS AND THOUGHT NOTES PUBLISHED

India Chem - Oct 2014 Industrial Green Chemistry 2013

Agrochemicals & Green Chemistry- Mar 2014

Thought Notes

Construction Chemicals Industry-May 2014

Growing through proactive M&A in Indian Specialty

Chemicals

The industry lacks in consumer standards

for construction

Strategies for Indian Pharma in a volatile

wolrd

Opportunities in a global

petrochemical market

Oleochemical opportunities

Integrated Development- A key

to sustainable growth of Gujarat as a chemical hub

Beating the slowdown blues with

vigour

Chemical Weekly June 2014

Construction Opportunities

June 2014

Pharma Bio World January 2014

Reed Business Information (ICIS)

October 2013

Speciality Chemicals Magazine

October 2013

Chemical Industry Digest

October 2013

Chemical Manufacturing

May 2013

Page 27

27

We assist clients in addressing their strategic business priorities

• How do I make existing businesses effective – sales &

distribution strategy, pricing strategy etc.?

• How do I reduce costs (material, conversion,

overheads, manpower), reduce risks, & improve

productivity?

• What should be my logistics and supply chain

strategies? How do I optimize costs and services?

• How can I grow – portfolio optimization, new products,

new technologies, new geographies?

Typical Client Concerns Tata Strategic Expertise

• Functional strategies

• Integrated cost reduction ; OPTIC/ OSMIC

• Strategic Risk Management

• Procurement, logistics and supply chain optimization

• How do I manage people, align resources, improve retention?

• How do I ensure that people are aligned with vision? • Organizational Effectiveness

• What should be the levers of growth – organic vs.

inorganic growth, strategic alliances etc.?

• Growth/ entry strategy

• Business due diligence

• Target Identification and Valuation for M&A

STRATEGY FORMULATION AND DEPLOYMENT

Page 28

Mumbai

B - 1001, Marathon Futurex,

N.M. Joshi Road

Lower Parel (East),

Mumbai 400 013. INDIA

Tel:+91 22 66376789

Fax: +91 22 66376600

Delhi

Level 12, Building No.8, Tower C

DLF Cyber City, Phase II

Gurgaon – 122002

Haryana, INDIA

Tel:+91 124 4696692

Fax: +91 124 4696970

Contacts :

MANISH PANCHAL

CHARU KAPOOR

PRACTICE HEAD – CHEMICAL, ENERGY

& SUPPLY CHAIN MANAGEMENT

Phone: +91 22 6637 6713

Mobile: +91 98205 20303

e-mail: [email protected]

PRINCIPAL – CHEMICALS

Phone: +91-22-66376756

Mobile: +91 98218 06071

e-mail: [email protected]