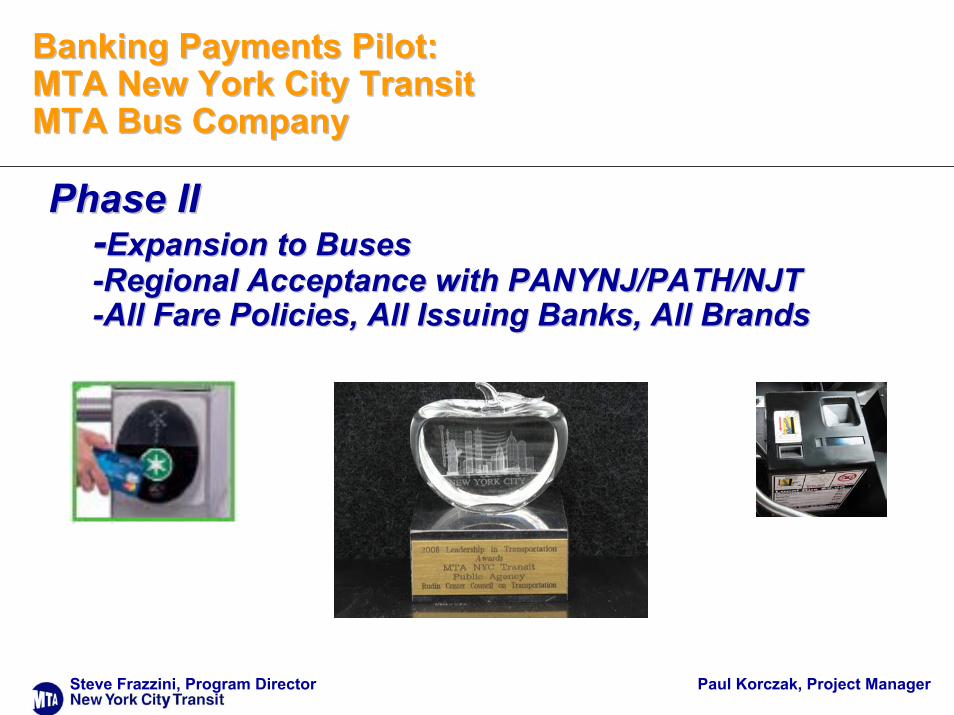

Paul Korczak, Project Manager Steve Frazzini, Program Director Banking Payments Pilot: Banking Payments Pilot: MTA New York City Transit MTA New York City Transit MTA Bus Company MTA Bus Company Phase II Phase II - - Expansion to Buses Expansion to Buses - - Regional Acceptance with PANYNJ/PATH/NJT Regional Acceptance with PANYNJ/PATH/NJT - - All Fare Policies, All Issuing Banks, All Brands All Fare Policies, All Issuing Banks, All Brands

Transcript

Paul Korczak, Project ManagerSteve Frazzini, Program Director

Banking Payments Pilot:Banking Payments Pilot:MTA New York City TransitMTA New York City TransitMTA Bus CompanyMTA Bus Company

Phase IIPhase II--Expansion to BusesExpansion to Buses--Regional Acceptance with PANYNJ/PATH/NJTRegional Acceptance with PANYNJ/PATH/NJT--All Fare Policies, All Issuing Banks, All BrandsAll Fare Policies, All Issuing Banks, All Brands

2Paul Korczak, Project ManagerSteve Frazzini, Program Director

Pilot Overview

Phase II – Buses and SubwaysEquip up to 275 buses (recommended routes on following pages); real-time authorization (on subways, via SONET)

Start 3rd Quarter 2008

Pay-As-You-Go ($2.00)

Passes, transfers, reduced fares, and value-based, 15% bonus (Prepaid)

All issuing banks, brands, and form factors (MC, Visa, Amex, etc.)All form factors from all issuers

Web, pilot CSC expanded for all payment brands; interoperable with regional pilot at PA/NJT/PATH in 2008

All form factors (card, cell phone, key fob, etc.)

Web, pilot Customer Service Center (CSC)

Scope

Timeline

Fare Options

Acceptance

Customer Support

3Paul Korczak, Project ManagerSteve Frazzini, Program Director

Phase I: NYCT Lexington Line PilotKey Findings

Customer Service (Based on formal surveys and review of claims)Overall feedback was very positive; approach easily understood/used.Web site and CSC highly effective; “self-service” approach.No issues with simplified message at point of entry (POE); need to optimize reader placement.Positive perception of MTA; issues understood banking problem.No unanticipated customer service issues.Customers see potential for a seamless regional transportation solution.

OperationsFare policy handled; all business requirements met.Proven direct cost savings.System is highly reliable, accurate, effective.

– No unanticipated technical issues: <300ms read achieved.– Bypassing legacy AFC system works.– Minimal maintenance required for field equipment; one reader failure.

Phase I average fare up 17%, ridership up 8-13% in revenues and ridership; convenience factor may play an important role.

4Paul Korczak, Project ManagerSteve Frazzini, Program Director

Key Benefits:Customers reap tangible improvements

Eliminate payment steps—no stopping to buy “tickets.”

Familiar to customers--less of a learning curve, fewer trust issues.

More flexible--customer chooses banking relationship and form factor (i.e., card, FOB, cell phone, etc.).

Simple, clean self-directed customer support via web and staffed CSC.

Faster problem resolution via electronic funds transfers.

Greater security: customer protected by extensive resources and zero liability policies.

5Paul Korczak, Project ManagerSteve Frazzini, Program Director

Key Benefits: Simplified transition to contactless fare payment

Pure banking payments solution can be “layered-on” to existing transit fare collection systems.

Key: readers on Transit equipment must be bank certified.Banks issue contactless devices.Customers pay as they would in a “retail” store.“Un- and under-banked” customers, students, employees have many options: pre-paid cards (issued on behalf of Transit,) MTA private-label banking cards, mobile phones, alternative card products.]

Connect with larger, compelling trend towards use of electronic payments

Short time line for implementation.

6Paul Korczak, Project ManagerSteve Frazzini, Program Director

Key Benefits: “Future Proof” the fare payment system

Minimize investments in areas where advances in technology lead to early obsolescence.

Share cost of technical upgrades with broad range of stakeholders.

Tap into “open market” for equipment and services.

Concentrate functionality and major investment in a central back-office to minimize investment and reduce turnaround times to address business issues.

Connect with customers in a “retail” approach that is universally recognized and understood.

7Paul Korczak, Project ManagerSteve Frazzini, Program Director

Key Benefits:Simple to support transit initiatives

Comprehensive travel incentives linked to transit benefits.Leverage bank loyalty programs by linking them to transit benefits for transit travel and parking.

Structure rewards points in terms of longest distances traveled and greatest transit usage (distance and/or multiple modes).

Spend of points remains customer choice; points can be applied to any purchase, or to transit

Permit incentive fare structures.Centralized, back-office management of fare calculations enables route-specific, time-sensitive (“weekend specials”) programming of incentives.

Leverage existing infrastructure to enable future initiatives like congestion pricing, carbon credits.

8Paul Korczak, Project ManagerSteve Frazzini, Program Director

Debunked Myths About A Retail Banking Payments Approach

Fare policy cannot be done.

Transit agencies will lose “float” and/or expired card value.

A banking approach costs more than current systems.

Customers do not use debit/credit.

Accepting bank cards will be an incremental cost for transit.

Transit will not have access to the same data as with a traditional AFC system.

Bank cards are less secure.

9Paul Korczak, Project ManagerSteve Frazzini, Program Director

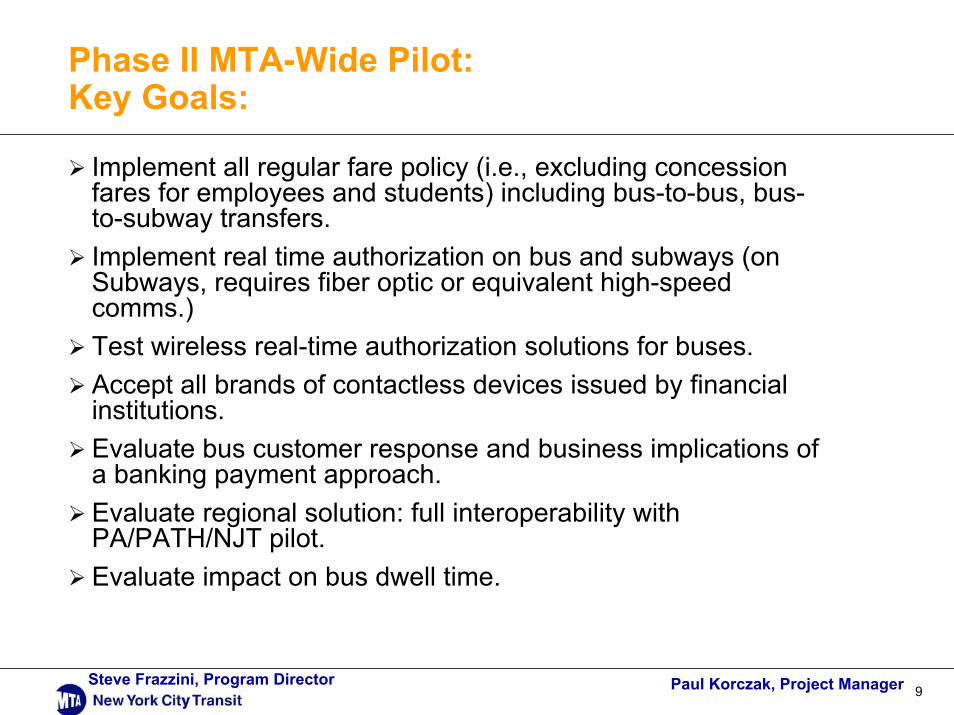

Phase II MTA-Wide Pilot:Key Goals:

Implement all regular fare policy (i.e., excluding concession fares for employees and students) including bus-to-bus, bus-to-subway transfers.Implement real time authorization on bus and subways (on Subways, requires fiber optic or equivalent high-speed comms.)Test wireless real-time authorization solutions for buses.Accept all brands of contactless devices issued by financial institutions.Evaluate bus customer response and business implications of a banking payment approach.Evaluate regional solution: full interoperability with PA/PATH/NJT pilot.Evaluate impact on bus dwell time.

10Paul Korczak, Project ManagerSteve Frazzini, Program Director

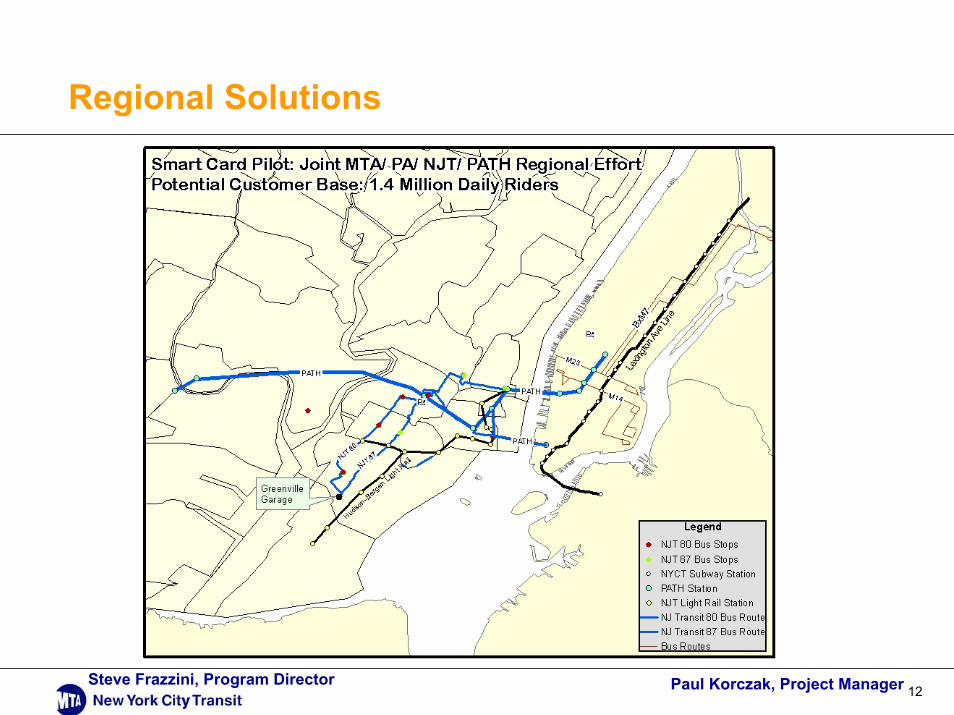

Phase II: Scope

Potential for– 1.4 million daily trips

– 30 stations on Lexington Line

– Expansion to 8 bus routes, 275 local and express buses

Intersect with PATH trains on 2 major NYCT routes

Introduce cell phone as major form factor

11Paul Korczak, Project ManagerSteve Frazzini, Program Director

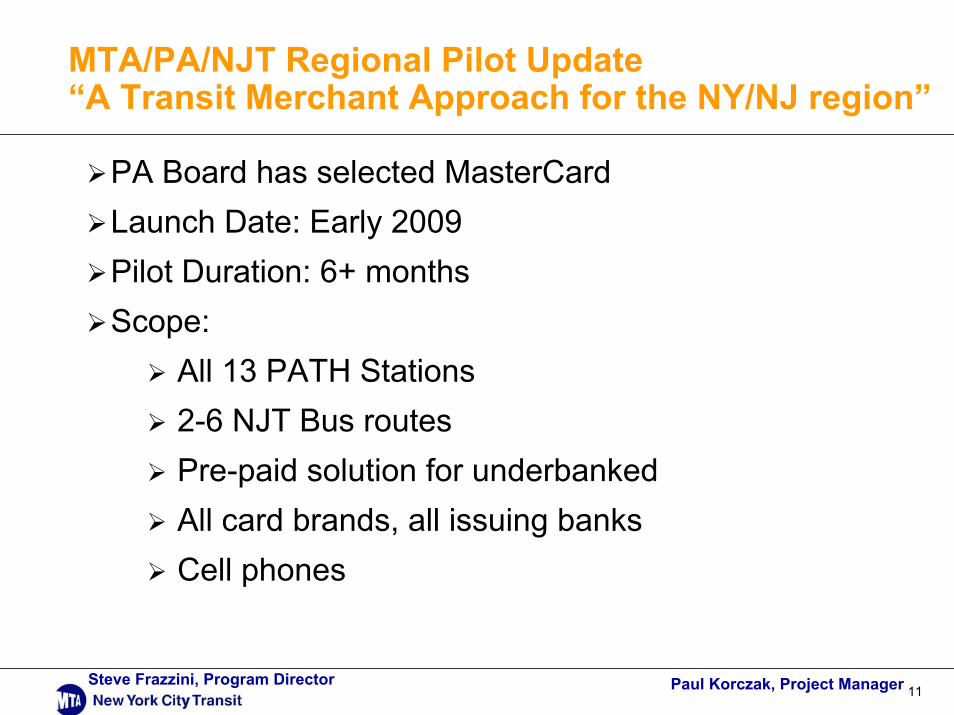

MTA/PA/NJT Regional Pilot Update“A Transit Merchant Approach for the NY/NJ region”

PA Board has selected MasterCardLaunch Date: Early 2009Pilot Duration: 6+ monthsScope:

All 13 PATH Stations2-6 NJT Bus routesPre-paid solution for underbankedAll card brands, all issuing banksCell phones

12Paul Korczak, Project ManagerSteve Frazzini, Program Director