Center for Economic Forecasting and Analysis Florida State University 3200 Commonwealth Blvd. Suite 137 Tallahassee, Florida 32303-2770 Final Report Phase Two: The Economic Impact of Aerospace in Florida -Florida Aerospace Inventory and Economic Analysis Prepared for: Space Florida PO Box 656 Cape Canaveral, FL. 32920 321-730-5301 Phone http://www.spaceflorida.gov/ Prepared by: Center for Economic Forecasting and Analysis, The Florida State University 3200 Commonwealth Blvd. Tallahassee, FL. 32303-2770 850-644-7357 http://www.cefa.fsu.edu March 31, 2012

Transcript

Center for Economic Forecasting and Analysis Florida State University

3200 Commonwealth Blvd. Suite 137 Tallahassee, Florida 32303-2770

Final Report

Phase Two: The Economic Impact of Aerospace in

Florida

-Florida Aerospace Inventory and Economic Analysis

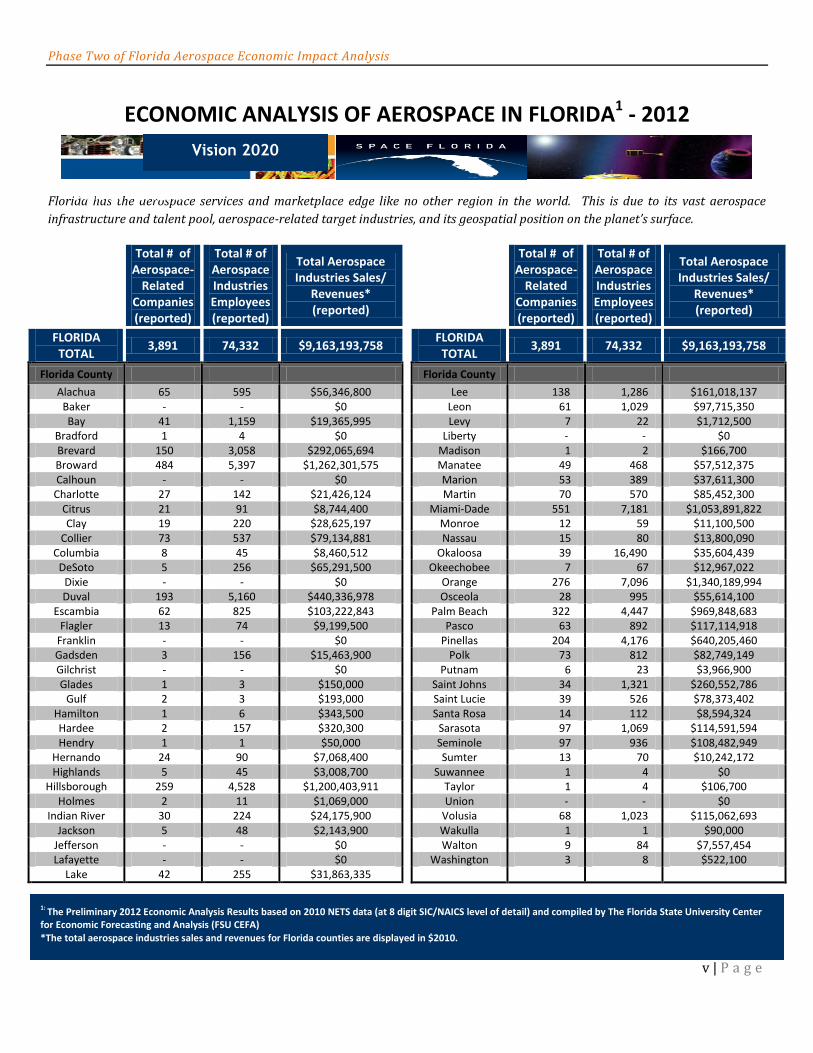

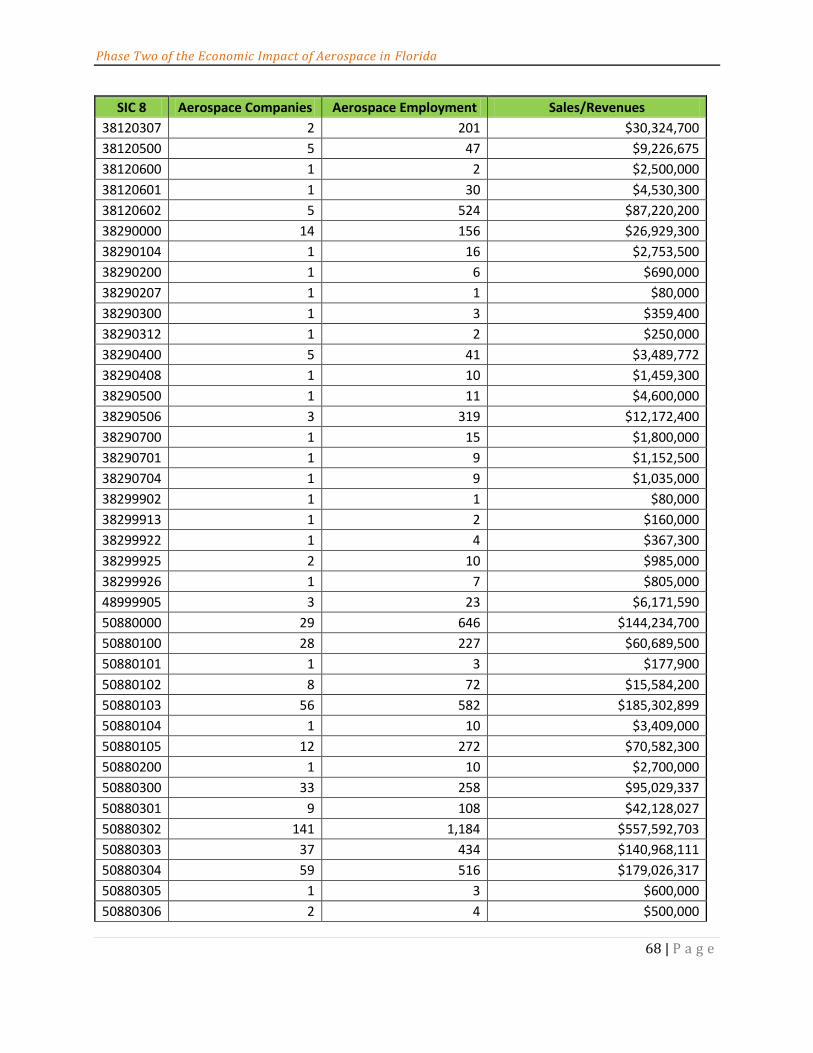

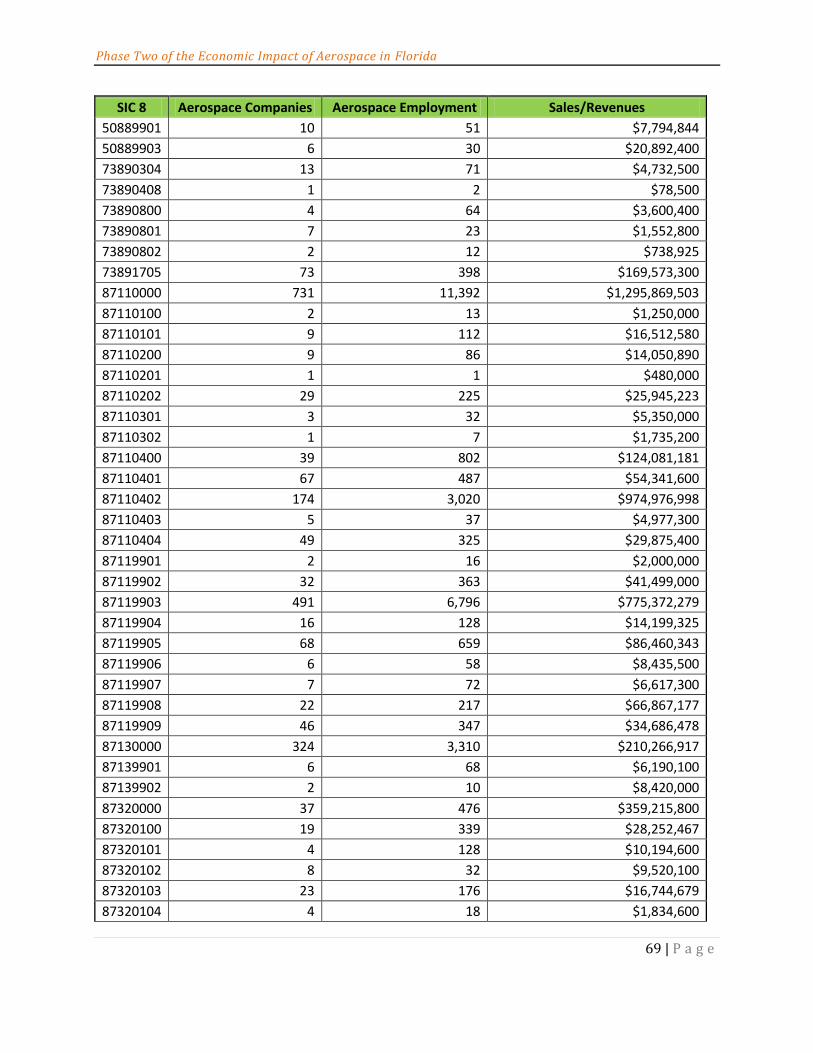

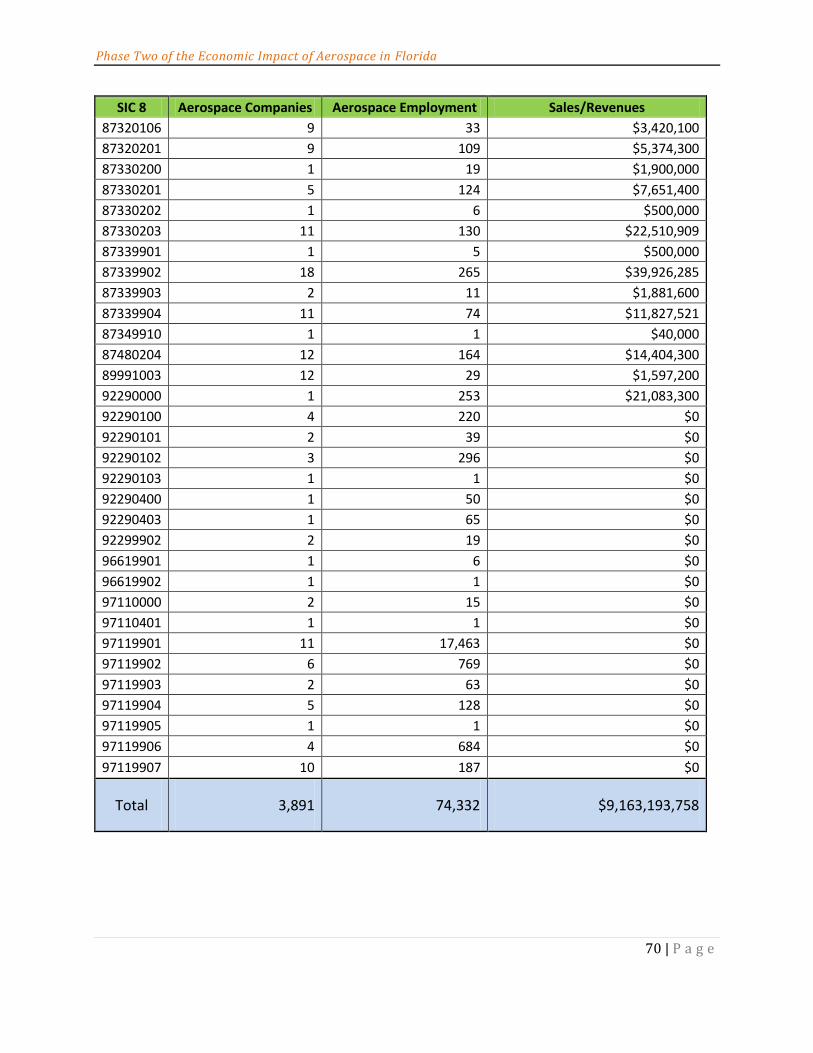

1: The Preliminary 2012 Economic Analysis Results based on 2010 NETS data (at 8 digit SIC/NAICS level of detail) and compiled by The Florida State University Center for Economic Forecasting and Analysis (FSU CEFA) *The total aerospace industries sales and revenues for Florida counties are displayed in $2010.

Phase Two of Florida Aerospace Economic Impact Analysis

Table of Contents

AUTHORS ................................................................................................................................................... I

ACKNOWLEDGEMENTS ........................................................................................................................ II

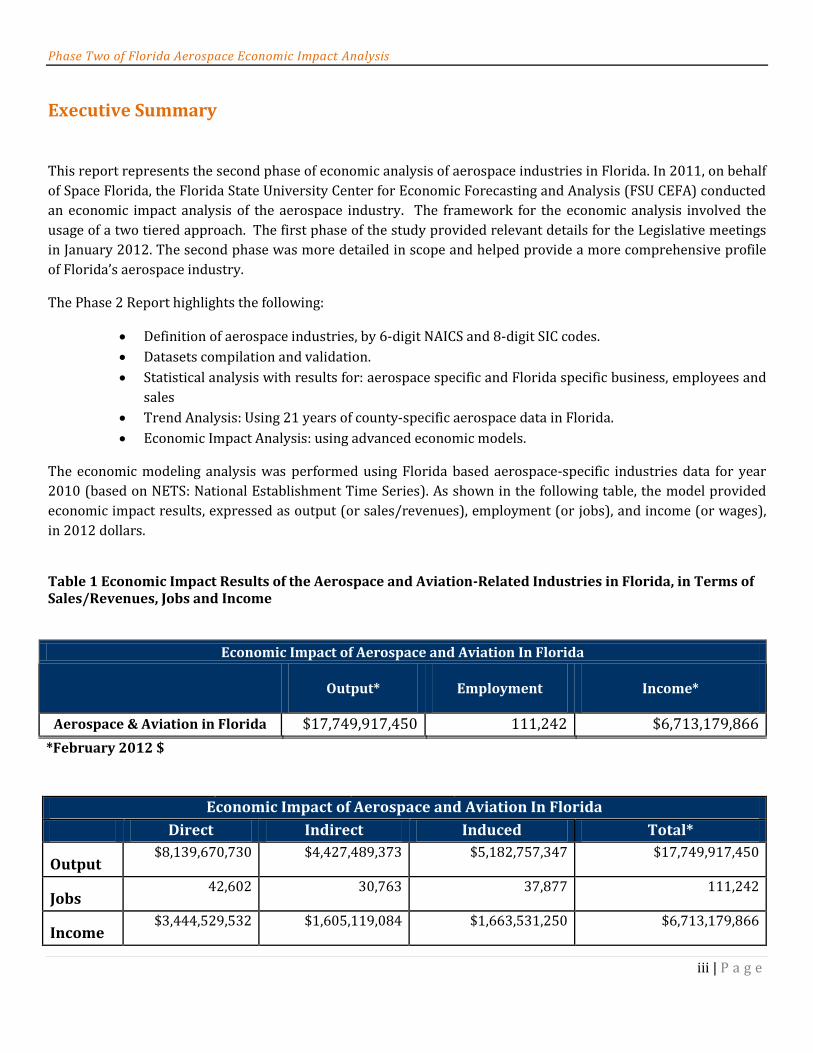

EXECUTIVE SUMMARY ....................................................................................................................... III

KEY FINDINGS ........................................................................................................................................ IV

TABLE OF CONTENTS .......................................................................................................................... VI

LIST OF TABLES .................................................................................................................................. VIII

LIST OF FIGURES ................................................................................................................................... IX

I. INTRODUCTION .................................................................................................................................. 1

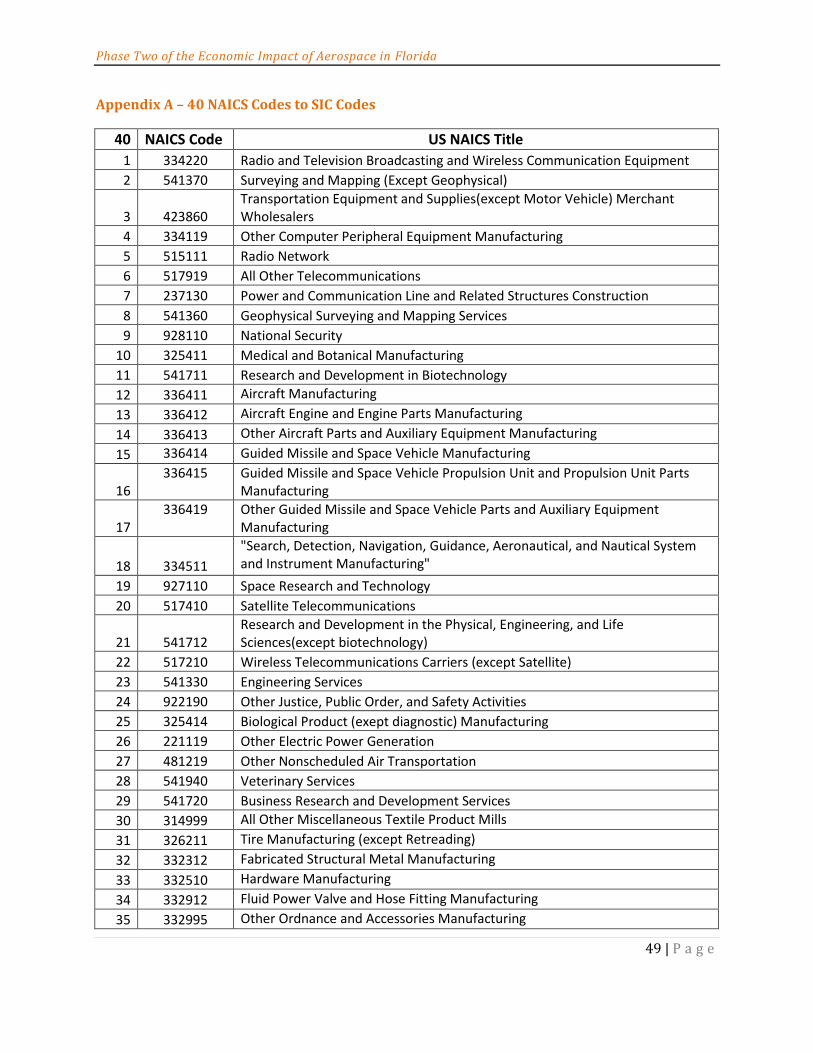

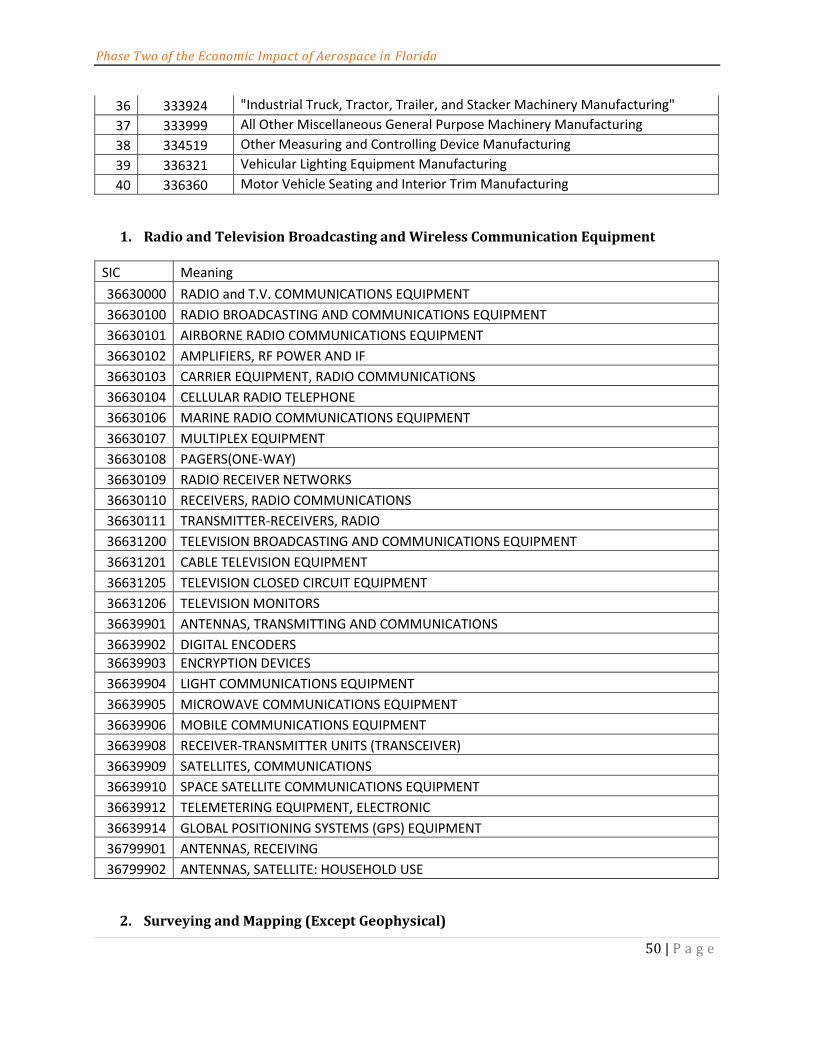

APPENDIX A – 40 NAICS CODES TO SIC CODES .......................................................................... 49

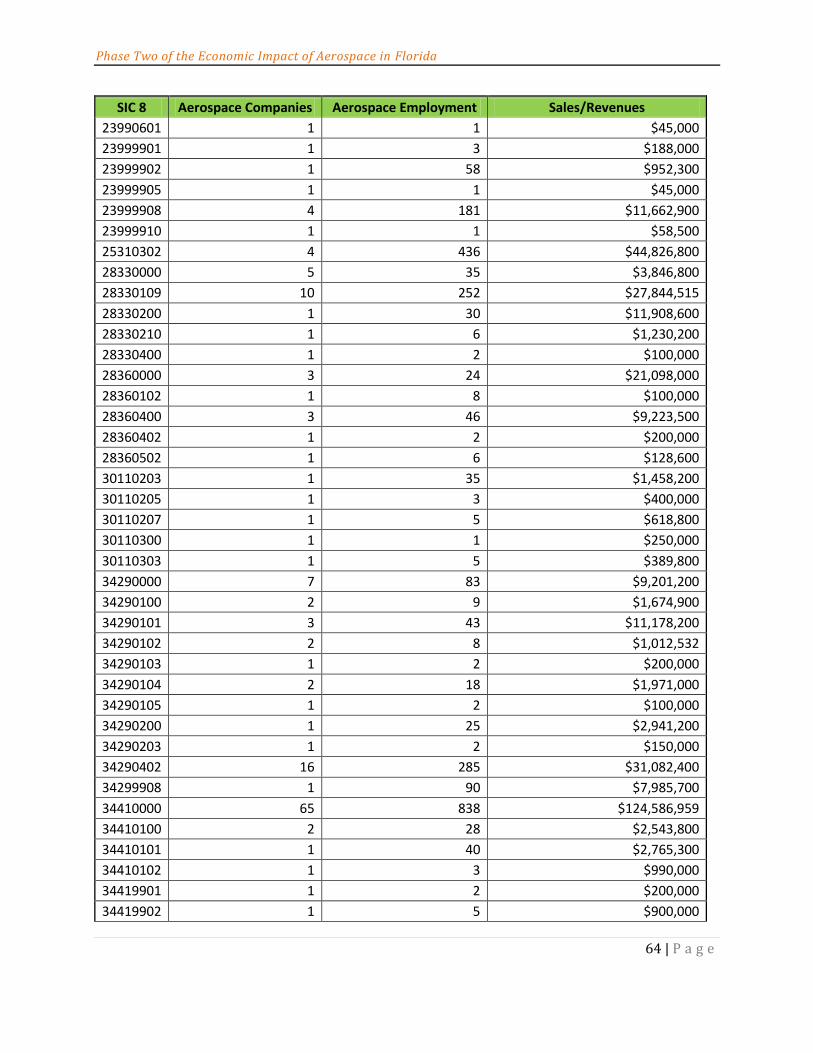

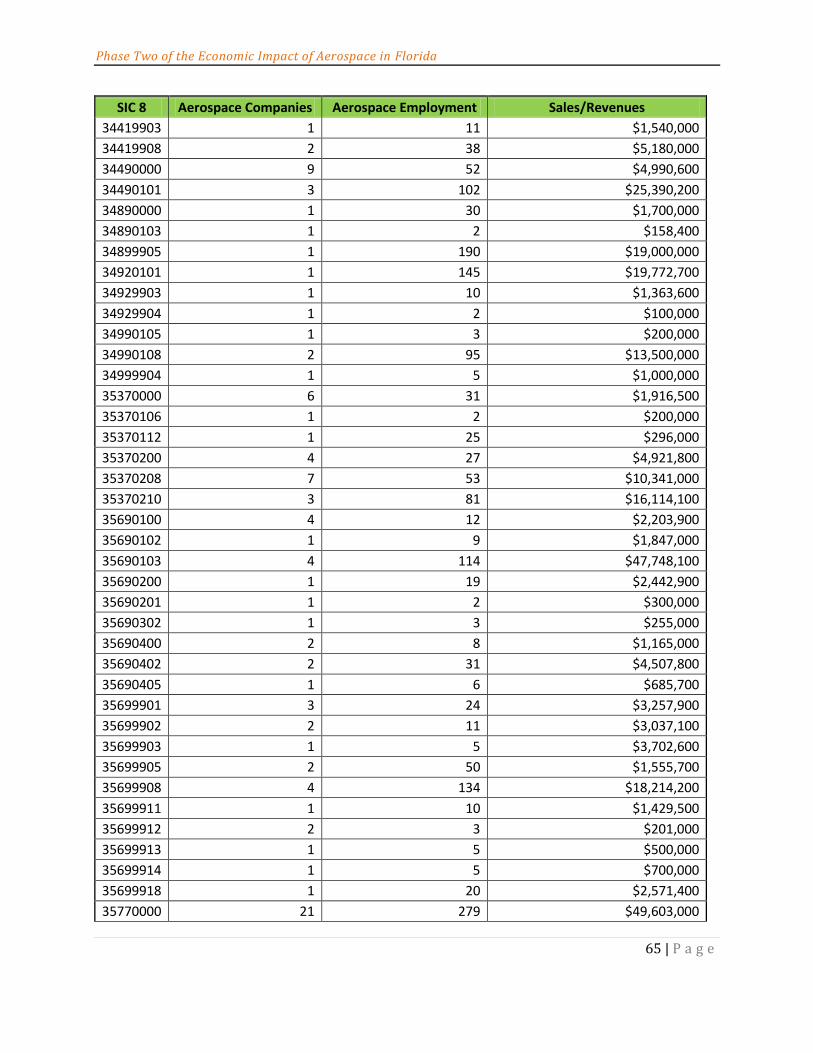

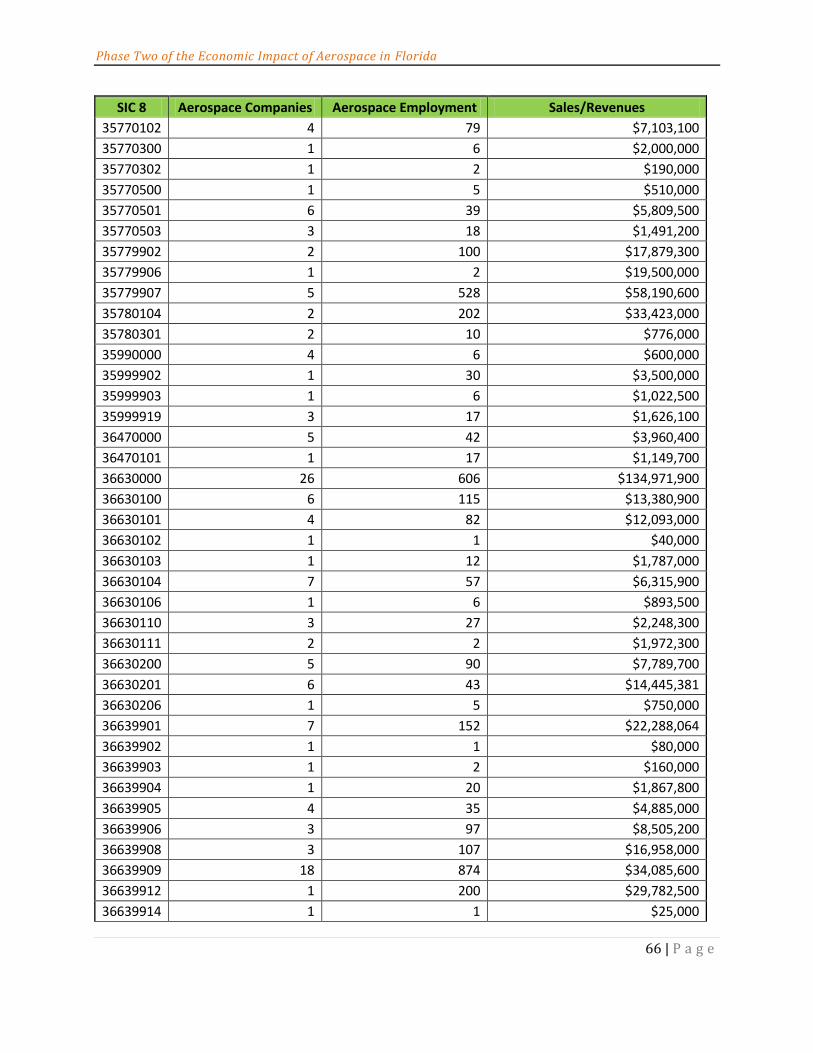

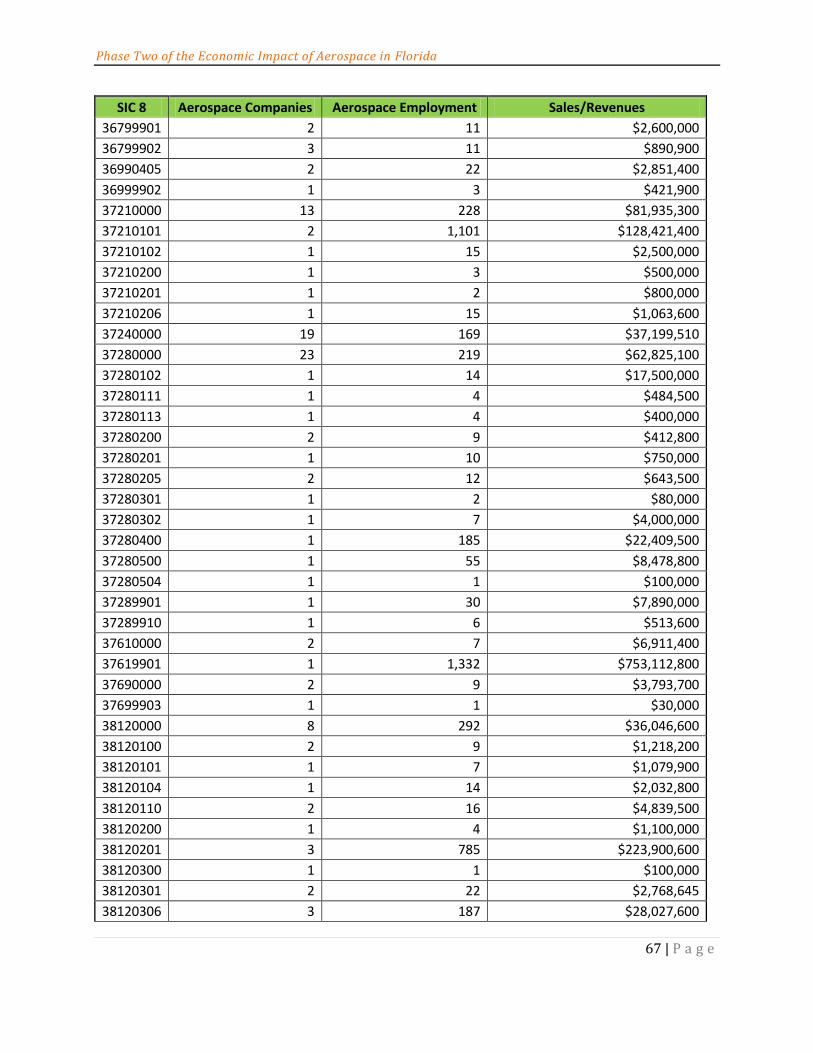

APPENDIX B – THE 8-DIGIT SIC CODES FOR AEROSPACE IN FLORIDA ............................. 63

Phase Two of Florida Aerospace Economic Impact Analysis

viii | P a g e

List of Tables

Table 1 Economic Impact Results of the Aerospace and Aviation-Related Industries in Florida, in Terms of Sales/Revenues, Jobs and Income ......................................................... iii

Table 2 Global Space Industry Revenues from Years 2005 to 2010 ................................... 3

Table 3 U.S. Government Agency Space Budgets in 2009 ....................................................... 5

Table 4 The NASA Current Projected Budget in 2010, for Years 2011 – 2015 ............... 6

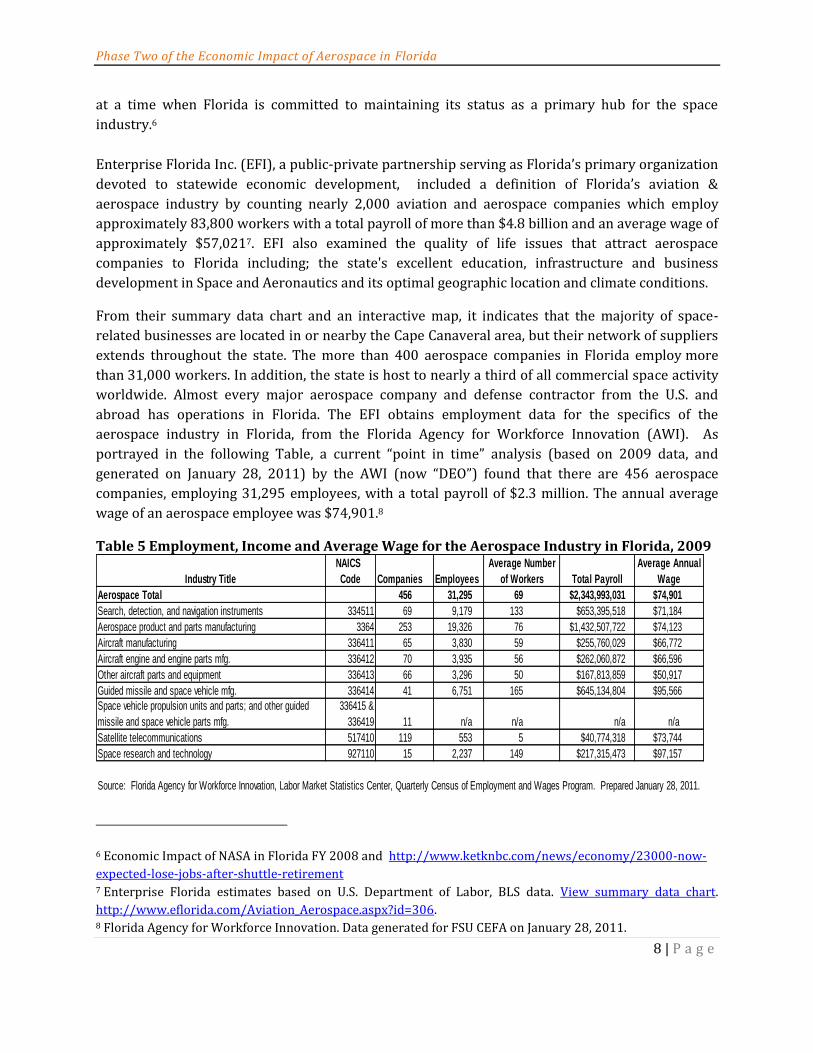

Table 5 Employment, Income and Average Wage for the Aerospace Industry in Florida, 2009 ............................................................................................................................................................. 8

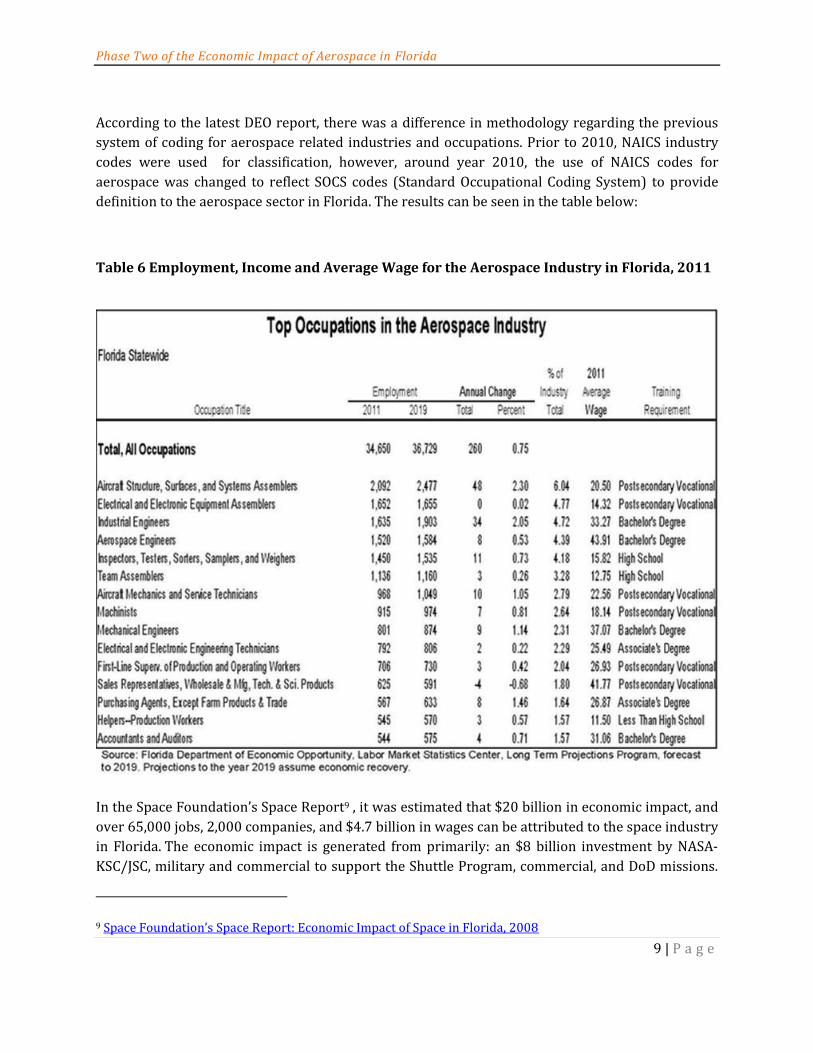

Table 6 Employment, Income and Average Wage for the Aerospace Industry in Florida, 2011 ............................................................................................................................................................. 9

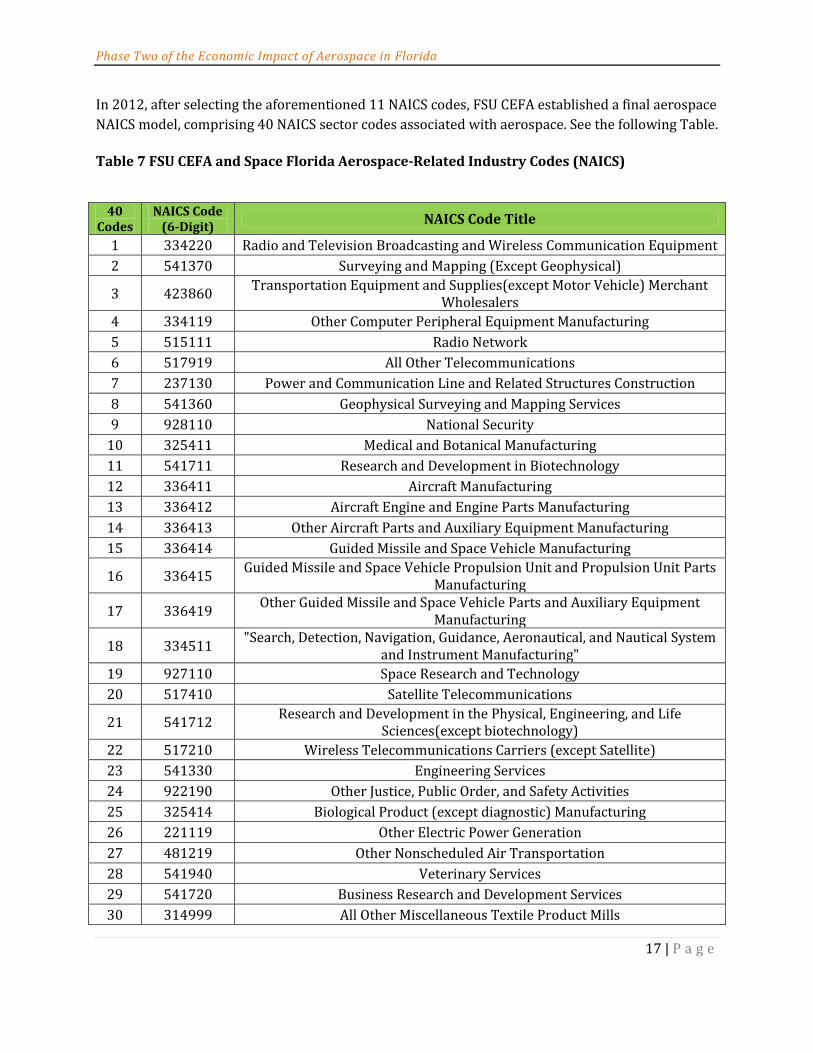

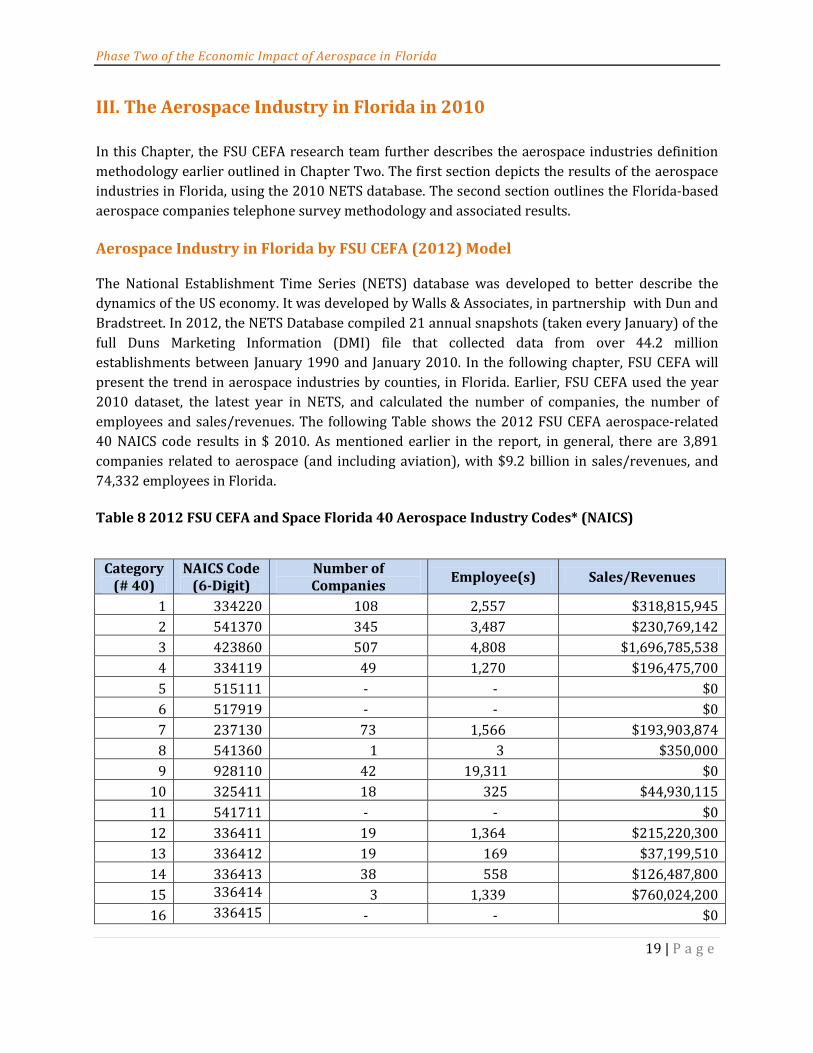

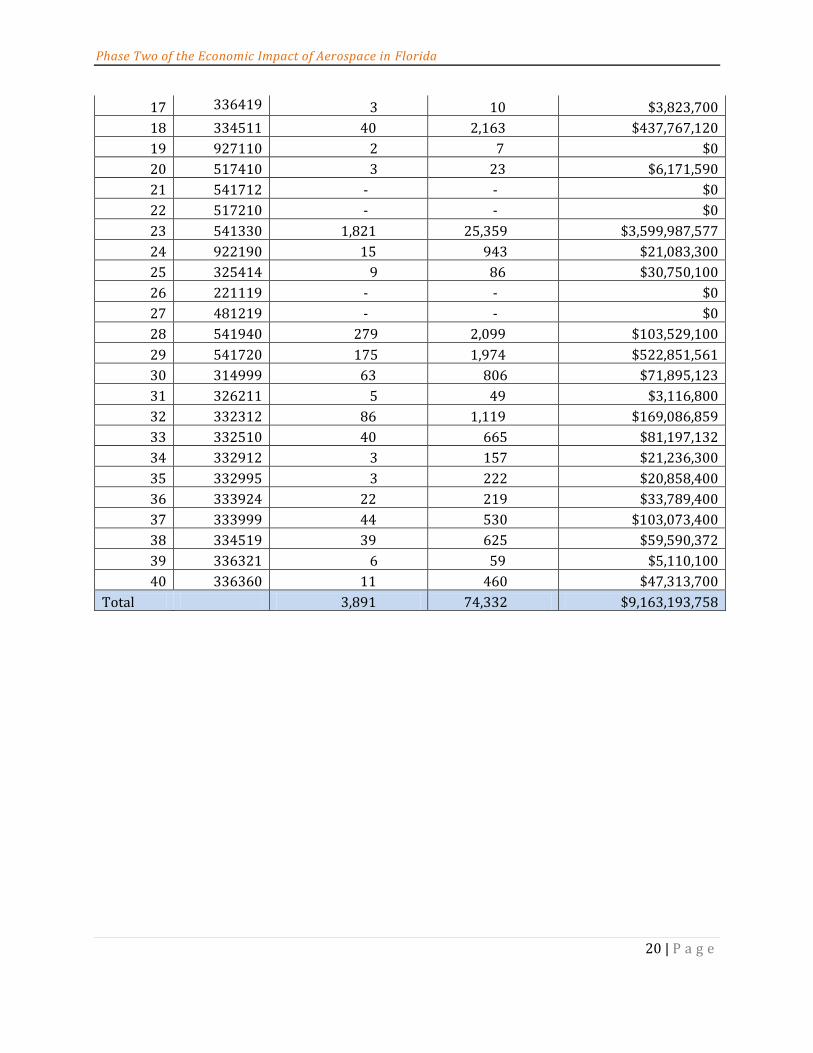

Table 7 FSU CEFA and Space Florida Aerospace-Related Industry Codes (NAICS) ... 17

Table 8 2012 FSU CEFA and Space Florida 40 Aerospace Industry Codes* (NAICS) 19

Table 9 NETS Input Data for Year 2010 by Space Florida Aerospace-Related Industries ..................................................................................................................................................................... 43

Table 10 Economic Impact Results of the Aerospace-Related Industries in Florida, in Terms of Sales/Revenues, Jobs and Income ............................................................................................ 44

Table 11 Economic Impact Results the Aerospace-Related Industries in Florida, Including Direct, Indirect and Induced Impacts, in Terms of Sales/Revenues, Jobs and Income44

Phase Two of Florida Aerospace Economic Impact Analysis

ix | P a g e

List of Figures

Figure 1 Space Budgets of G20 countries Estimates in 2010(Current US $ Million) .... 1

Figure 2 Countries with Spaceflight Capabilities in 2010 ....................................................... 2

Figure 3 Global Space Activity in 2010 ........................................................................................... 4

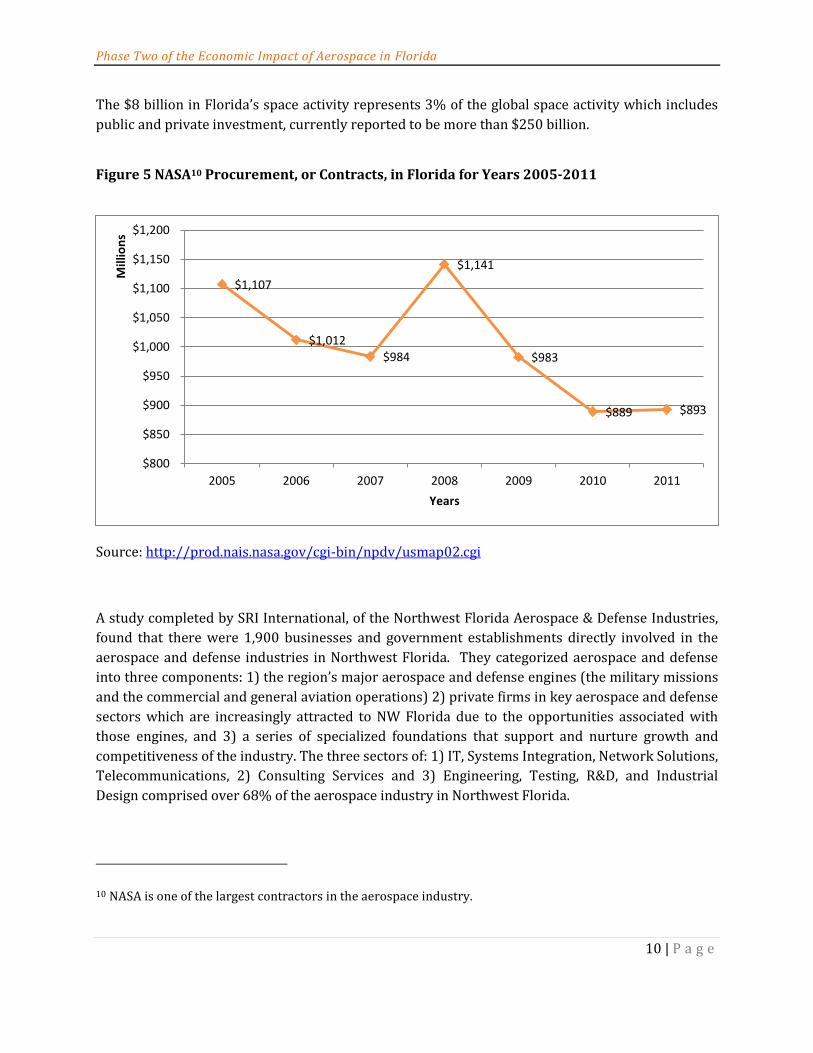

Figure 5 NASA Procurement, or Contracts, in Florida for Years 2005-2011 ................ 10

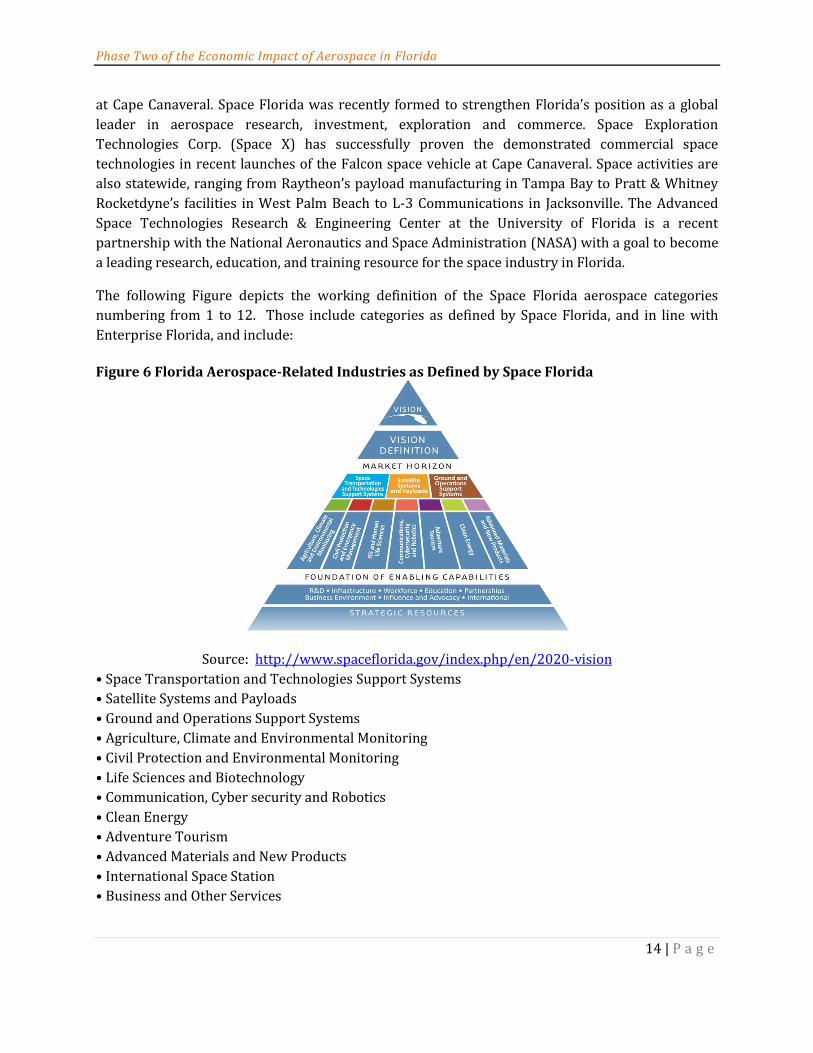

Figure 6 Florida Aerospace-Related Industries as Defined by Space Florida .............. 14

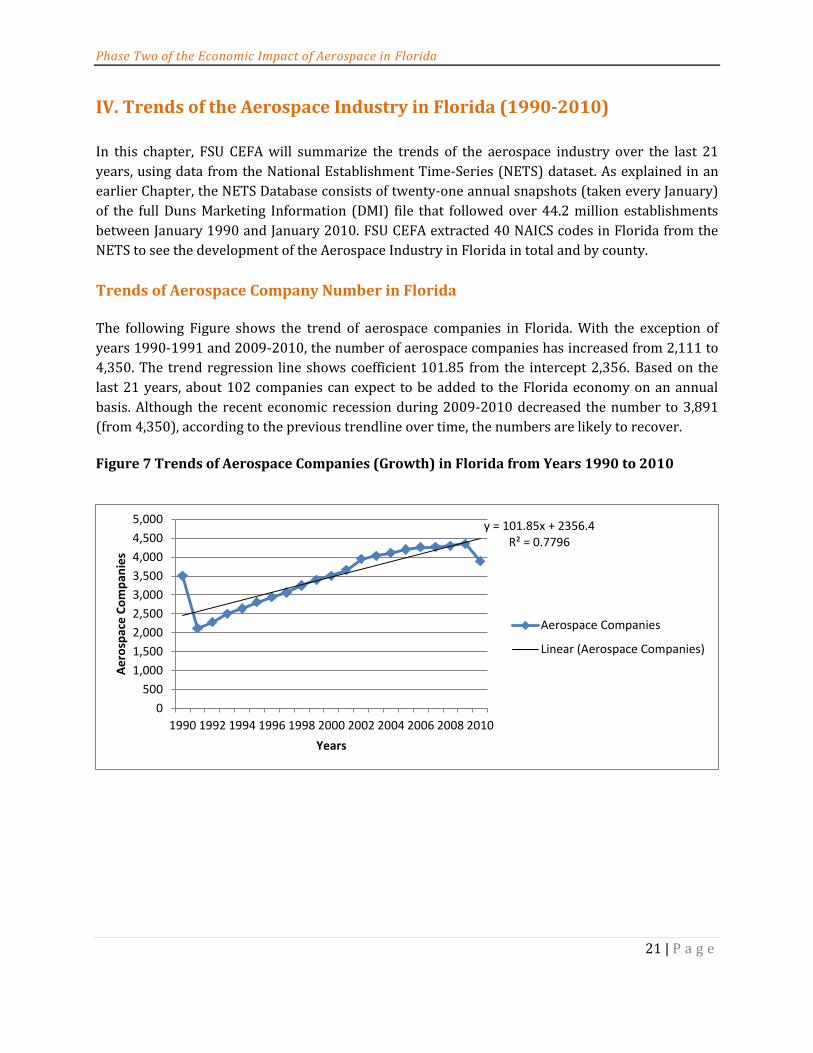

Figure 7 Trends of Aerospace Companies (Growth) in Florida from Years 1990 to 2010 ..................................................................................................................................................................... 21

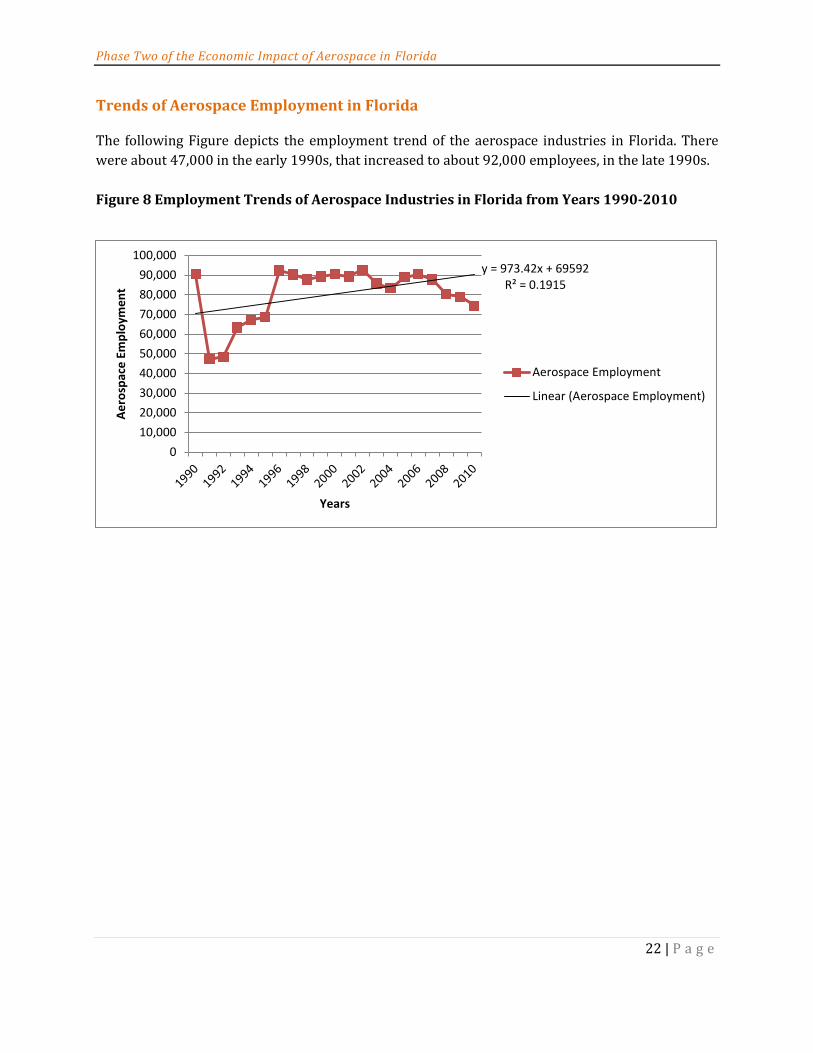

Figure 8 Employment Trends of Aerospace Industries in Florida from Years 1990-2010 ..................................................................................................................................................................... 22

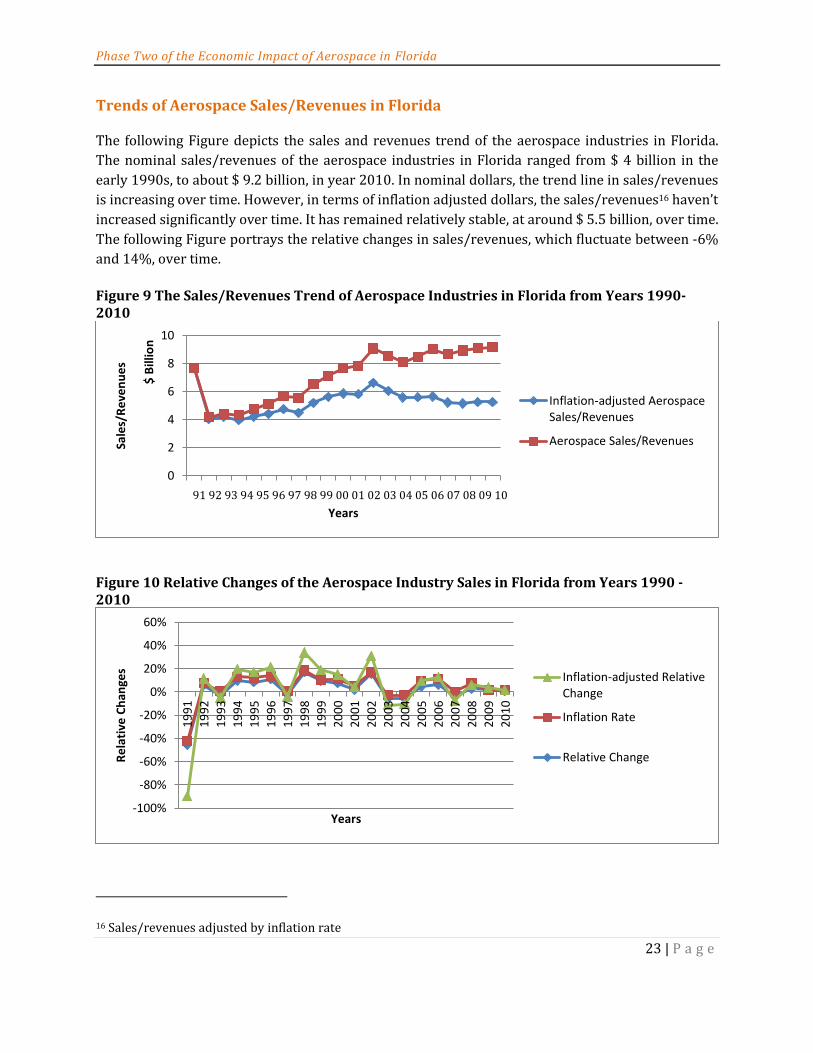

Figure 9 The Sales/Revenues Trend of Aerospace Industries in Florida from Years 1990-2010 .......................................................................................................................................................... 23

Figure 11 Relative Changes of the Aerospace Industry Sales in Florida from Years 1990 - 2010 .......................................................................................................................................................... 23

Figure 12 Aerospace Companies by Counties in Florida ...................................................... 24

Figure 13 Aerospace Companies by Counties in Florida ...................................................... 24

Figure 14 Aerospace Companies by Counties in Florida ...................................................... 25

Figure 15 Aerospace Companies by Counties in Florida ...................................................... 25

Figure 16 Aerospace Companies by Counties in Florida ...................................................... 26

Figure 17 Aerospace Companies by Counties in Florida ...................................................... 26

Figure 18 Aerospace Companies by Counties in Florida ...................................................... 27

Figure 19 Aerospace Companies by Counties in Florida ...................................................... 27

Figure 20 Aerospace Companies by Counties in Florida ...................................................... 28

Figure 21 Aerospace Companies by Counties in Florida ...................................................... 28

Figure 22 Aerospace Companies by Counties in Florida ...................................................... 29

Figure 23 Aerospace Employment by Counties in Florida .................................................. 30

Phase Two of Florida Aerospace Economic Impact Analysis

x | P a g e

Figure 24 Aerospace Employment by Counties in Florida .................................................. 30

Figure 25 Aerospace Employment by Counties in Florida .................................................. 31

Figure 26 Aerospace Employment by Counties in Florida .................................................. 31

Figure 27 Aerospace Employment by Counties in Florida .................................................. 32

Figure 28 Aerospace Employment by Counties in Florida .................................................. 32

Figure 29 Aerospace Employment by Counties in Florida .................................................. 33

Figure 30 Aerospace Employment by Counties in Florida .................................................. 33

Figure 31 Aerospace Employment by Counties in Florida .................................................. 34

Figure 32 Aerospace Employment by Counties in Florida .................................................. 34

Figure 33 Aerospace Employment by Counties in Florida .................................................. 35

Figure 34 Aerospace Sales/Revenues by Counties in Florida ............................................ 36

Figure 35 Aerospace Sales/Revenues by Counties in Florida ............................................ 36

Figure 36 Aerospace Sales/Revenues by Counties in Florida ............................................ 37

Figure 37 Aerospace Sales/Revenues by Counties in Florida ............................................ 37

Figure 38 Aerospace Sales/Revenues by Counties in Florida ............................................ 38

Figure 39 Aerospace Sales/Revenues by Counties in Florida ............................................ 38

Figure 40 Aerospace Sales/Revenues by Counties in Florida ............................................ 39

Figure 41 Aerospace Sales/Revenues by Counties in Florida ............................................ 39

Figure 42 Aerospace Sales/Revenues by Counties in Florida ............................................ 40

Figure 43 Aerospace Sales/Revenues by Counties in Florida ............................................ 40

Figure 44 Aerospace Sales/Revenues by Counties in Florida ............................................ 41

Phase Two of the Economic Impact of Aerospace in Florida

1 | P a g e

I. Introduction

Background

The aerospace economy in Florida and throughout the US has shifted from a traditional federal

(government) funding program, towards commercialization. The advancement of the US as a

revitalized worldwide leader in space exploration performing earth-benefiting research, technology

advancement and operating new space-ports, is heavily dependent upon making commercial space

travel a reality. The ‘new’ space program has finally driven home the message that it’s not just

about the 7 astronauts who fly on board the International Space Station, but the 7 billion or so who

inhabit planet earth. Competition has become ubiquitous, space flights are scarce! Florida, Virginia,

New Mexico, other US states, and indeed other countries, all seek their share of a competitive and

mixed market. That market encompasses suborbital and orbital activities, space tourism, orbital

research and habitable space stations, production of advanced materials as well as the development

of traffic at commercial space-ports. All of the above are globally competitive. However,

researchers, visionaries and realists are saying; “it’s time to fly”!

Public and private entities have responded and are investing. Elon Musk (Space-X & PayPal), Bezos

(Blue Origin & Amazon), Allen (StraoLaunch & Microsoft), Branson (Virgin & Virgin Galactic), and

Bigelow (Bigelow Aerospace & Budget Suites), are investing heavily and making their mark. Others

are in hot pursuit. Although the budget for NASA’s 2012 space operations has been cut by nearly $2

billion, many corporations such as Boeing and Lockheed Martin continue to allocate a large portion

of their R&D efforts towards continued development of the aerospace industry and more

specifically, that of future commercial space flight.

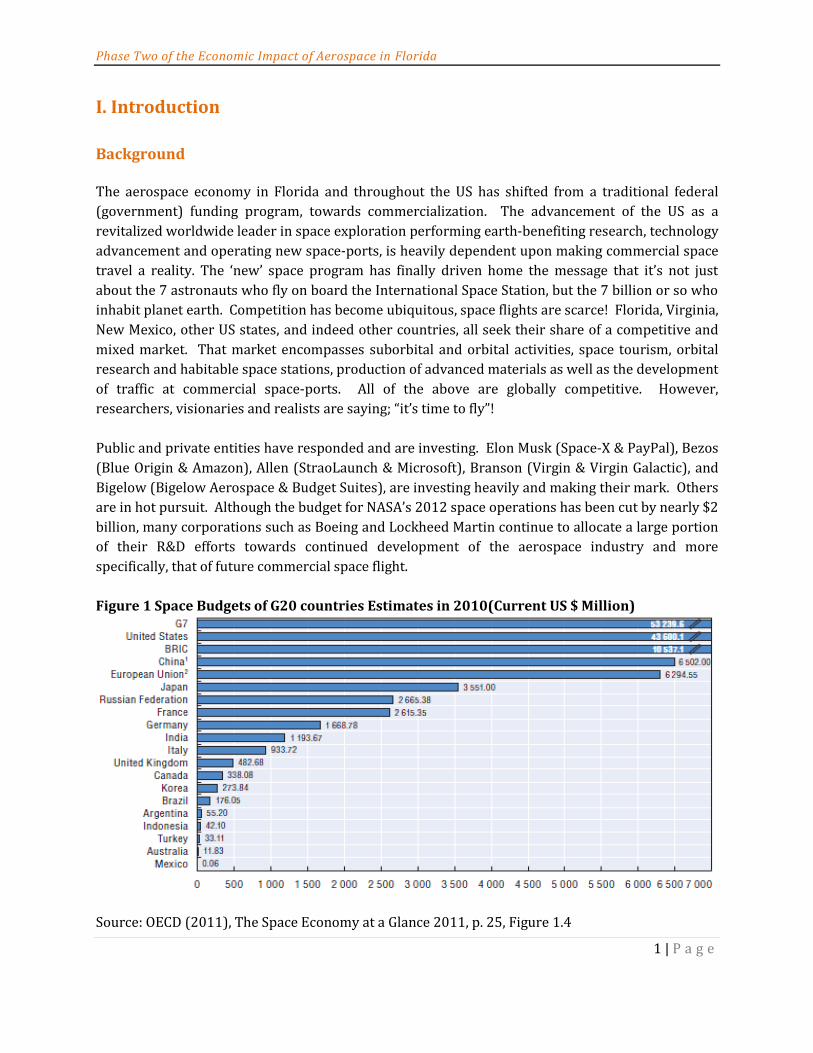

Figure 1 Space Budgets of G20 countries Estimates in 2010(Current US $ Million)

Source: OECD (2011), The Space Economy at a Glance 2011, p. 25, Figure 1.4

Phase Two of the Economic Impact of Aerospace in Florida

2 | P a g e

The aerospace sector plays an important role in the national economy; however, the aerospace

sector has high overhead costs. Historically, the government has provided considerable financial

support for aerospace R&D. On a global scale, many countries are currently directing investment to

bolstering their aerospace industries. According to the OECD (2011), the total space budget of the

35 countries examined in the report represented ~US $ 64.4 billion in 2009 and an estimated US

$ 65.3 billion in 2010. All G20 countries currently have space programs. Five countries, which

include the United States, China, Japan, France and the Russian Federation have invested more than

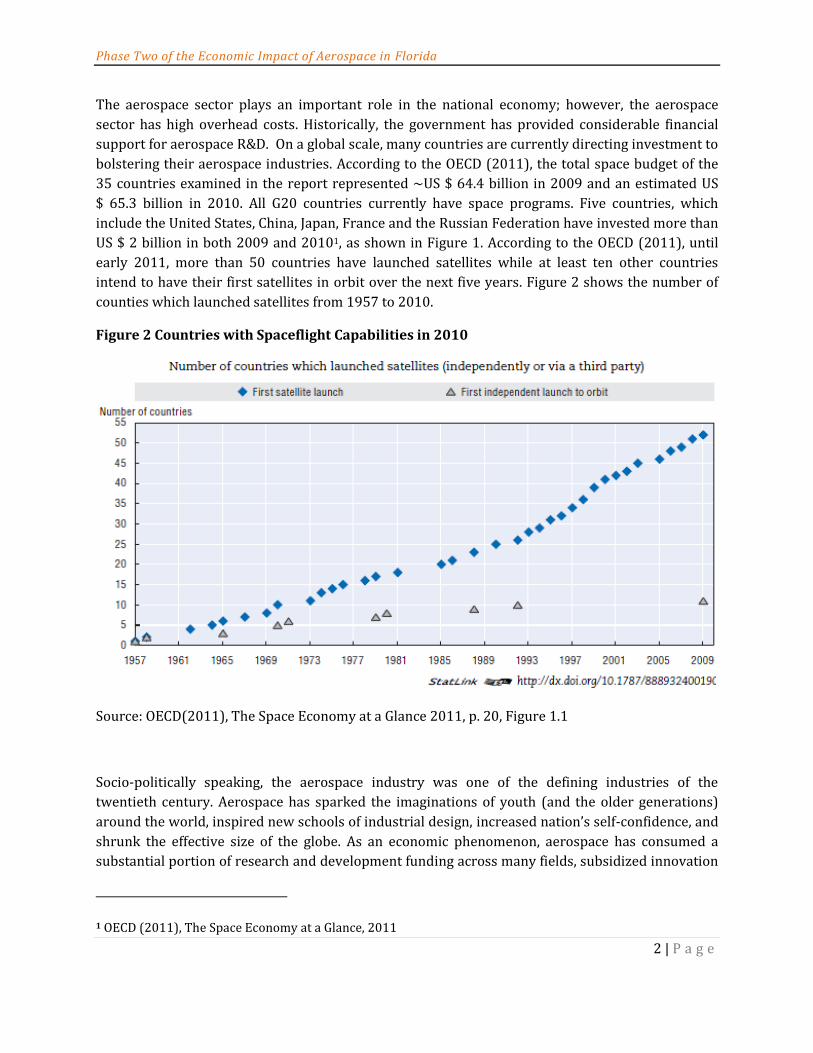

US $ 2 billion in both 2009 and 20101, as shown in Figure 1. According to the OECD (2011), until

early 2011, more than 50 countries have launched satellites while at least ten other countries

intend to have their first satellites in orbit over the next five years. Figure 2 shows the number of

counties which launched satellites from 1957 to 2010.

Figure 2 Countries with Spaceflight Capabilities in 2010

Source: OECD(2011), The Space Economy at a Glance 2011, p. 20, Figure 1.1

Socio-politically speaking, the aerospace industry was one of the defining industries of the

twentieth century. Aerospace has sparked the imaginations of youth (and the older generations)

around the world, inspired new schools of industrial design, increased nation’s self-confidence, and

shrunk the effective size of the globe. As an economic phenomenon, aerospace has consumed a

substantial portion of research and development funding across many fields, subsidized innovation

1 OECD (2011), The Space Economy at a Glance, 2011

Phase Two of the Economic Impact of Aerospace in Florida

3 | P a g e

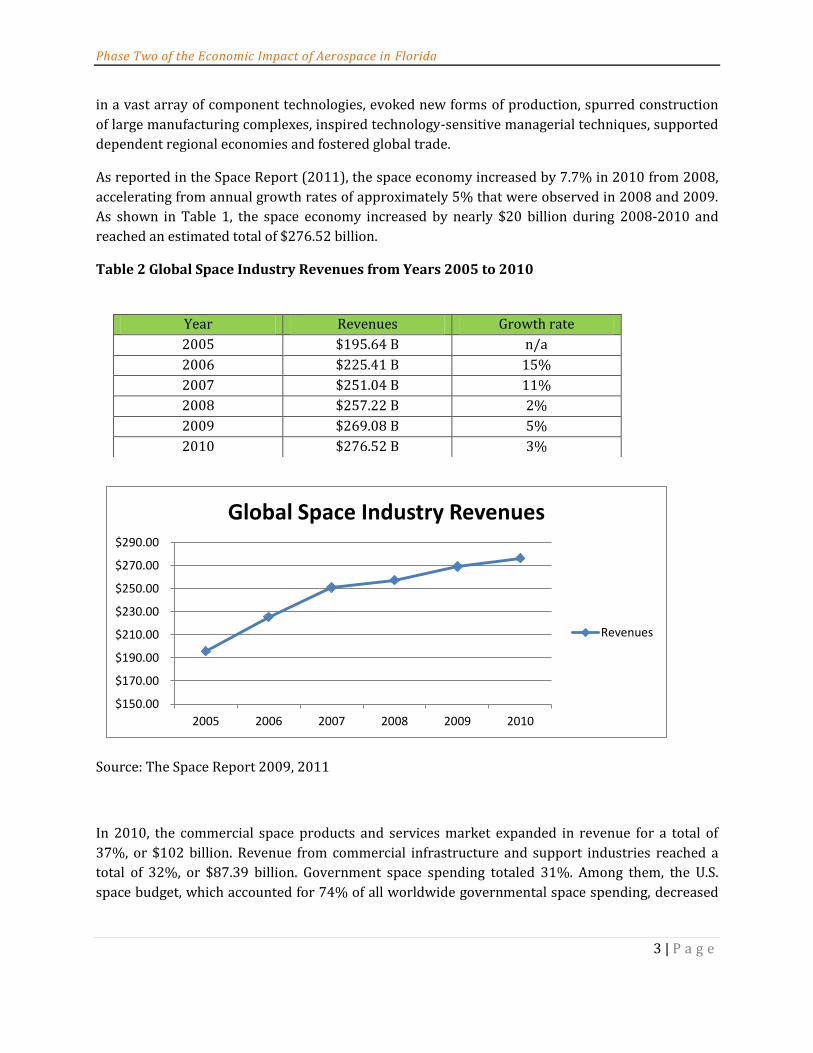

in a vast array of component technologies, evoked new forms of production, spurred construction

of large manufacturing complexes, inspired technology-sensitive managerial techniques, supported

dependent regional economies and fostered global trade.

As reported in the Space Report (2011), the space economy increased by 7.7% in 2010 from 2008,

accelerating from annual growth rates of approximately 5% that were observed in 2008 and 2009.

As shown in Table 1, the space economy increased by nearly $20 billion during 2008-2010 and

reached an estimated total of $276.52 billion.

Table 2 Global Space Industry Revenues from Years 2005 to 2010

Source: The Space Report 2009, 2011

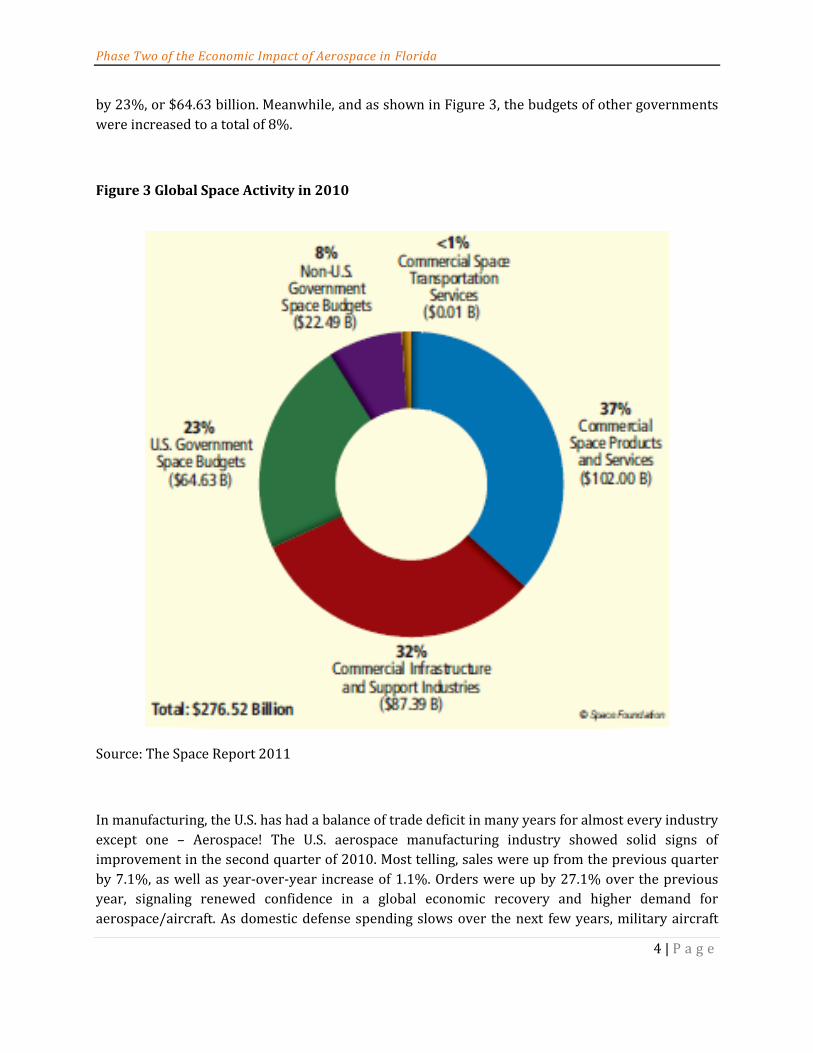

In 2010, the commercial space products and services market expanded in revenue for a total of

37%, or $102 billion. Revenue from commercial infrastructure and support industries reached a

total of 32%, or $87.39 billion. Government space spending totaled 31%. Among them, the U.S.

space budget, which accounted for 74% of all worldwide governmental space spending, decreased

Year Revenues Growth rate

2005 $195.64 B n/a

2006 $225.41 B 15%

2007 $251.04 B 11%

2008 $257.22 B 2%

2009 $269.08 B 5%

2010 $276.52 B 3%

$150.00

$170.00

$190.00

$210.00

$230.00

$250.00

$270.00

$290.00

2005 2006 2007 2008 2009 2010

Global Space Industry Revenues

Revenues

Phase Two of the Economic Impact of Aerospace in Florida

4 | P a g e

by 23%, or $64.63 billion. Meanwhile, and as shown in Figure 3, the budgets of other governments

were increased to a total of 8%.

Figure 3 Global Space Activity in 2010

Source: The Space Report 2011

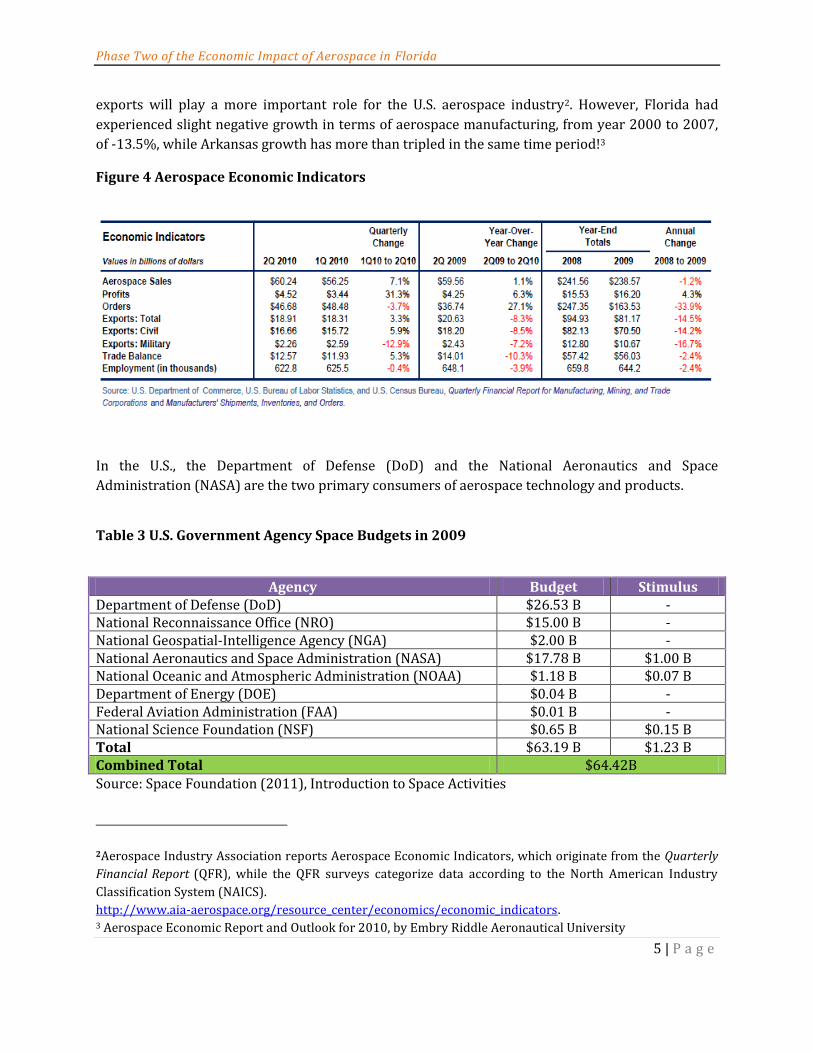

In manufacturing, the U.S. has had a balance of trade deficit in many years for almost every industry

except one – Aerospace! The U.S. aerospace manufacturing industry showed solid signs of

improvement in the second quarter of 2010. Most telling, sales were up from the previous quarter

by 7.1%, as well as year-over-year increase of 1.1%. Orders were up by 27.1% over the previous

year, signaling renewed confidence in a global economic recovery and higher demand for

aerospace/aircraft. As domestic defense spending slows over the next few years, military aircraft

Phase Two of the Economic Impact of Aerospace in Florida

5 | P a g e

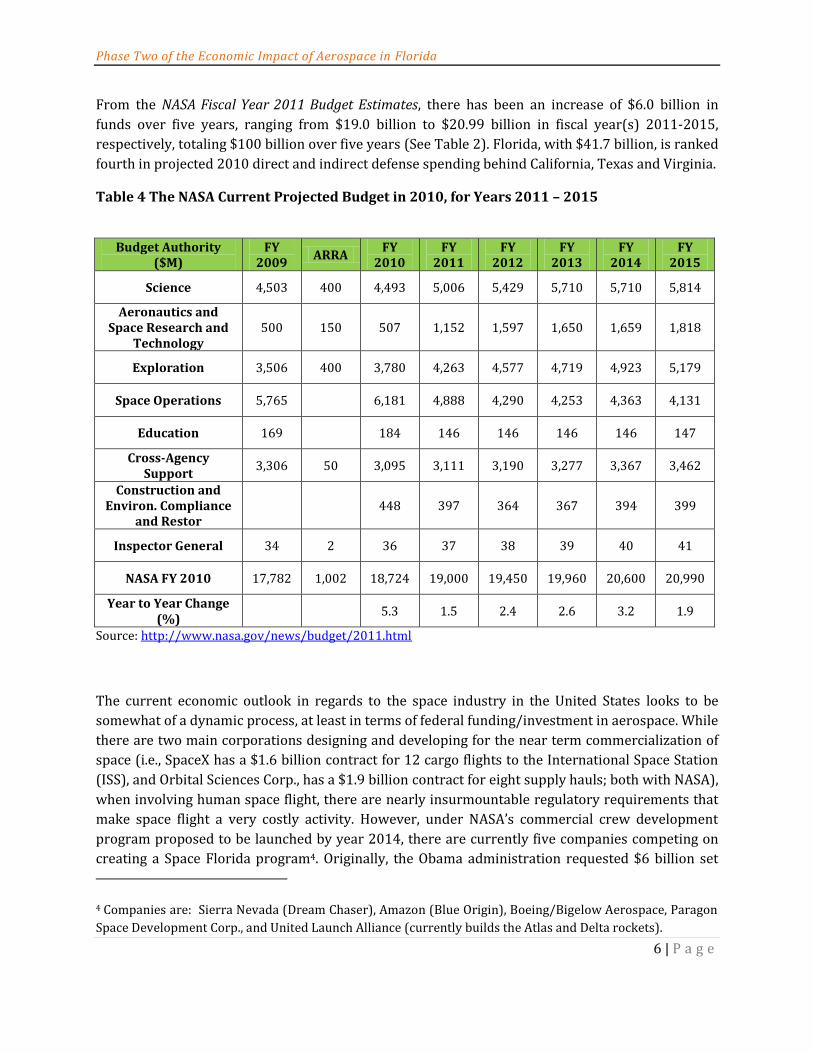

exports will play a more important role for the U.S. aerospace industry2. However, Florida had

experienced slight negative growth in terms of aerospace manufacturing, from year 2000 to 2007,

of -13.5%, while Arkansas growth has more than tripled in the same time period!3

Figure 4 Aerospace Economic Indicators

In the U.S., the Department of Defense (DoD) and the National Aeronautics and Space

Administration (NASA) are the two primary consumers of aerospace technology and products.

Table 3 U.S. Government Agency Space Budgets in 2009

Agency Budget Stimulus Department of Defense (DoD) $26.53 B - National Reconnaissance Office (NRO) $15.00 B - National Geospatial-Intelligence Agency (NGA) $2.00 B - National Aeronautics and Space Administration (NASA) $17.78 B $1.00 B National Oceanic and Atmospheric Administration (NOAA) $1.18 B $0.07 B Department of Energy (DOE) $0.04 B - Federal Aviation Administration (FAA) $0.01 B - National Science Foundation (NSF) $0.65 B $0.15 B Total $63.19 B $1.23 B Combined Total $64.42B Source: Space Foundation (2011), Introduction to Space Activities

2Aerospace Industry Association reports Aerospace Economic Indicators, which originate from the Quarterly

Financial Report (QFR), while the QFR surveys categorize data according to the North American Industry

Classification System (NAICS).

http://www.aia-aerospace.org/resource_center/economics/economic_indicators. 3 Aerospace Economic Report and Outlook for 2010, by Embry Riddle Aeronautical University

Space research and technology 927110 15 2,237 149 $217,315,473 $97,157

Source: Florida Agency for Workforce Innovation, Labor Market Statistics Center, Quarterly Census of Employment and Wages Program. Prepared January 28, 2011.

Phase Two of the Economic Impact of Aerospace in Florida

24 | P a g e

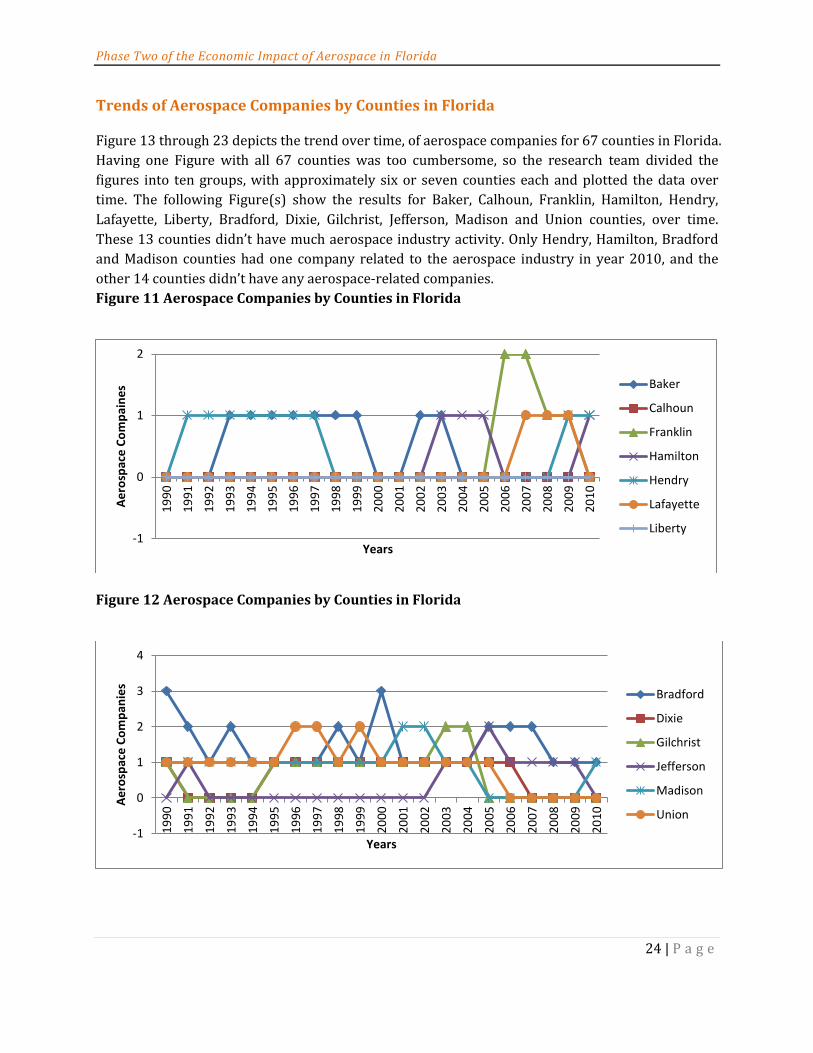

Trends of Aerospace Companies by Counties in Florida Figure 13 through 23 depicts the trend over time, of aerospace companies for 67 counties in Florida.

Having one Figure with all 67 counties was too cumbersome, so the research team divided the

figures into ten groups, with approximately six or seven counties each and plotted the data over

time. The following Figure(s) show the results for Baker, Calhoun, Franklin, Hamilton, Hendry,

Lafayette, Liberty, Bradford, Dixie, Gilchrist, Jefferson, Madison and Union counties, over time.

These 13 counties didn’t have much aerospace industry activity. Only Hendry, Hamilton, Bradford

and Madison counties had one company related to the aerospace industry in year 2010, and the

other 14 counties didn’t have any aerospace-related companies.

Figure 11 Aerospace Companies by Counties in Florida

Figure 12 Aerospace Companies by Counties in Florida

-1

0

1

2

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

ain

es

Years

Baker

Calhoun

Franklin

Hamilton

Hendry

Lafayette

Liberty

-1

0

1

2

3

4

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

Bradford

Dixie

Gilchrist

Jefferson

Madison

Union

Phase Two of the Economic Impact of Aerospace in Florida

25 | P a g e

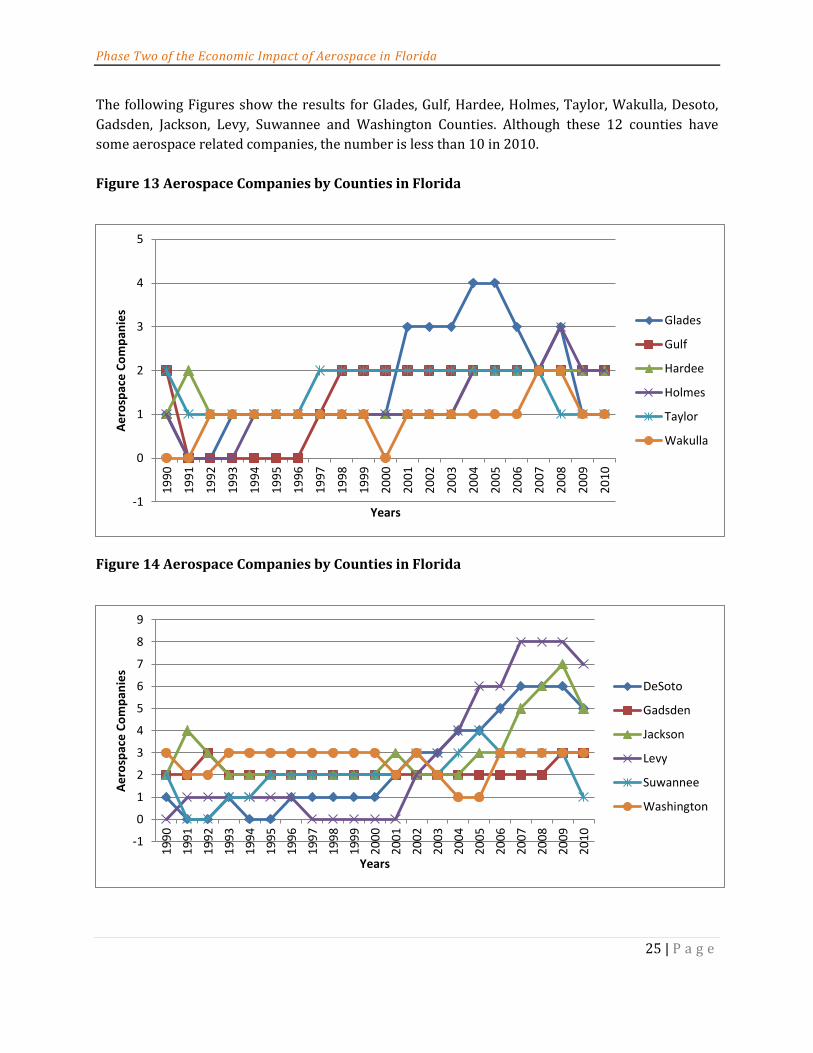

The following Figures show the results for Glades, Gulf, Hardee, Holmes, Taylor, Wakulla, Desoto,

Gadsden, Jackson, Levy, Suwannee and Washington Counties. Although these 12 counties have

some aerospace related companies, the number is less than 10 in 2010.

Figure 13 Aerospace Companies by Counties in Florida

Figure 14 Aerospace Companies by Counties in Florida

-1

0

1

2

3

4

5

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

Glades

Gulf

Hardee

Holmes

Taylor

Wakulla

-1

0

1

2

3

4

5

6

7

8

9

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

DeSoto

Gadsden

Jackson

Levy

Suwannee

Washington

Phase Two of the Economic Impact of Aerospace in Florida

26 | P a g e

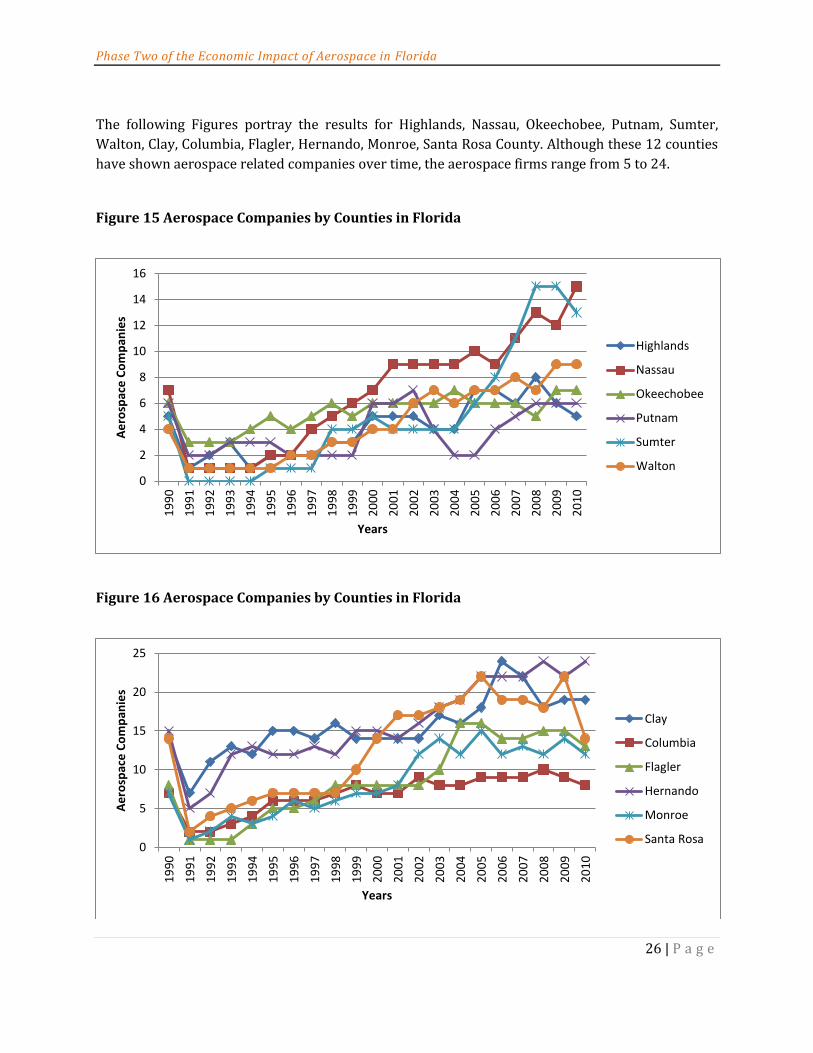

The following Figures portray the results for Highlands, Nassau, Okeechobee, Putnam, Sumter,

Walton, Clay, Columbia, Flagler, Hernando, Monroe, Santa Rosa County. Although these 12 counties

have shown aerospace related companies over time, the aerospace firms range from 5 to 24.

Figure 15 Aerospace Companies by Counties in Florida

Figure 16 Aerospace Companies by Counties in Florida

0

2

4

6

8

10

12

14

16

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

Highlands

Nassau

Okeechobee

Putnam

Sumter

Walton

0

5

10

15

20

25

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

Clay

Columbia

Flagler

Hernando

Monroe

Santa Rosa

Phase Two of the Economic Impact of Aerospace in Florida

27 | P a g e

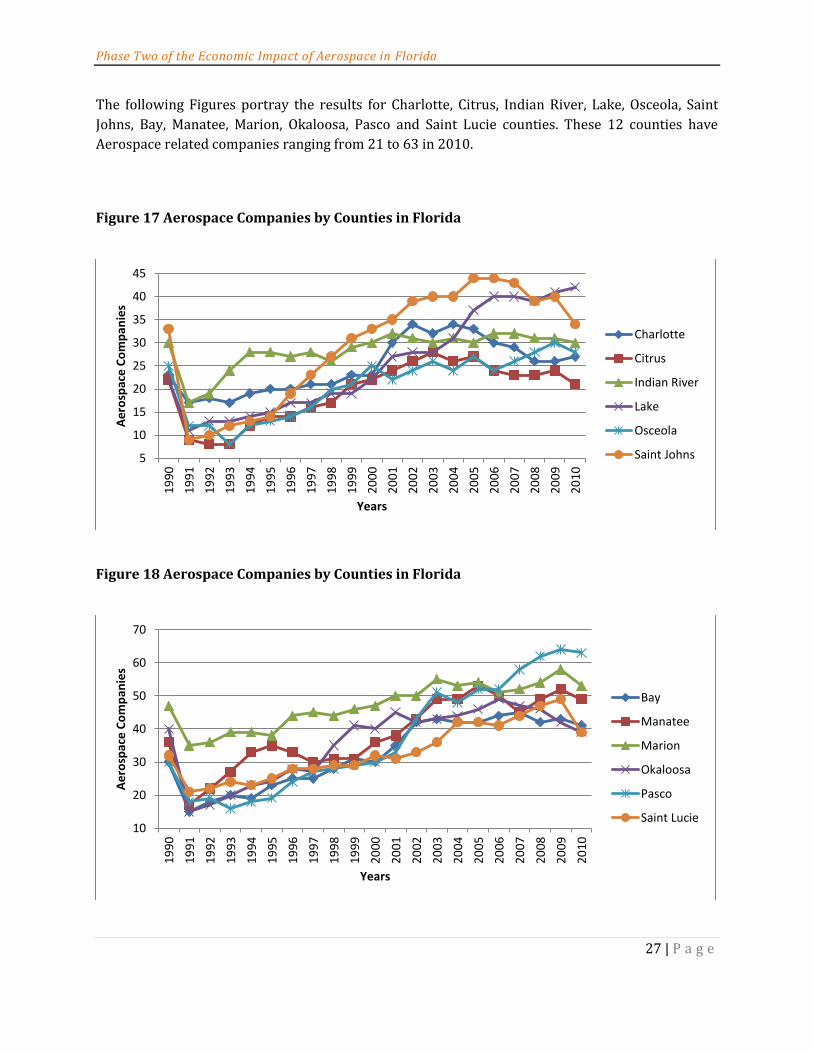

The following Figures portray the results for Charlotte, Citrus, Indian River, Lake, Osceola, Saint

Johns, Bay, Manatee, Marion, Okaloosa, Pasco and Saint Lucie counties. These 12 counties have

Aerospace related companies ranging from 21 to 63 in 2010.

Figure 17 Aerospace Companies by Counties in Florida

Figure 18 Aerospace Companies by Counties in Florida

5

10

15

20

25

30

35

40

45

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

Charlotte

Citrus

Indian River

Lake

Osceola

Saint Johns

10

20

30

40

50

60

70

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

Bay

Manatee

Marion

Okaloosa

Pasco

Saint Lucie

Phase Two of the Economic Impact of Aerospace in Florida

28 | P a g e

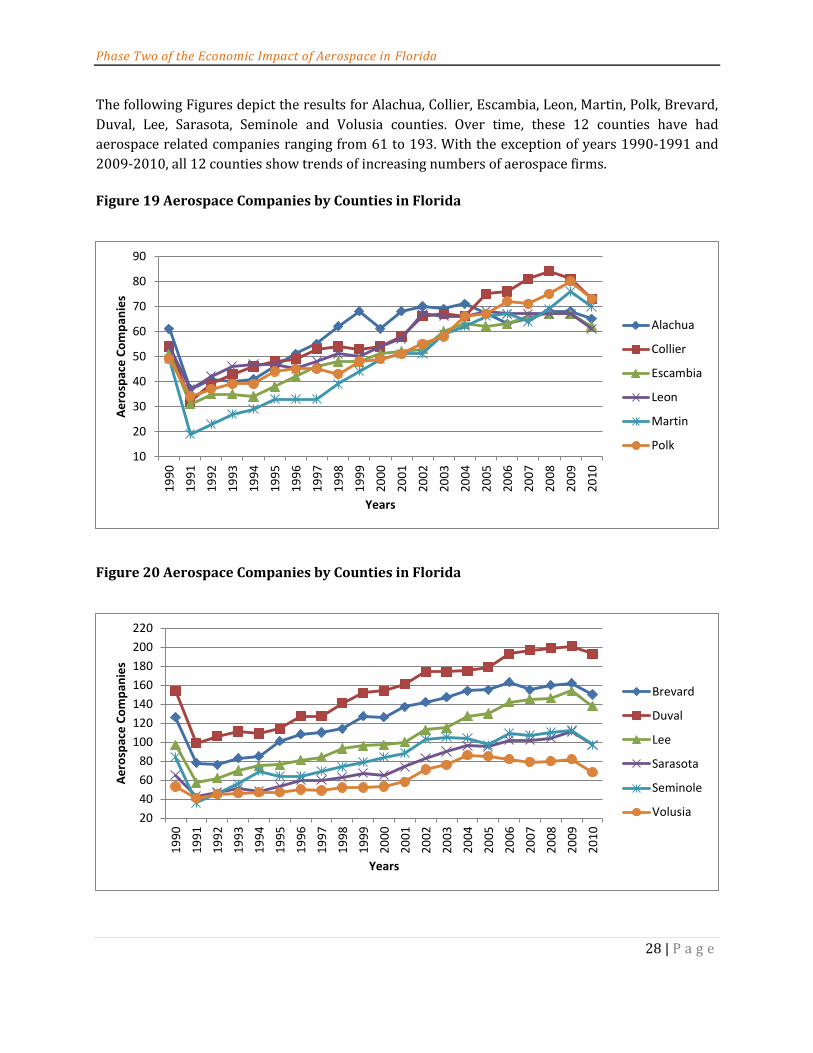

The following Figures depict the results for Alachua, Collier, Escambia, Leon, Martin, Polk, Brevard,

Duval, Lee, Sarasota, Seminole and Volusia counties. Over time, these 12 counties have had

aerospace related companies ranging from 61 to 193. With the exception of years 1990-1991 and

2009-2010, all 12 counties show trends of increasing numbers of aerospace firms.

Figure 19 Aerospace Companies by Counties in Florida

Figure 20 Aerospace Companies by Counties in Florida

10

20

30

40

50

60

70

80

90

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

Alachua

Collier

Escambia

Leon

Martin

Polk

20

40

60

80

100

120

140

160

180

200

220

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

Brevard

Duval

Lee

Sarasota

Seminole

Volusia

Phase Two of the Economic Impact of Aerospace in Florida

29 | P a g e

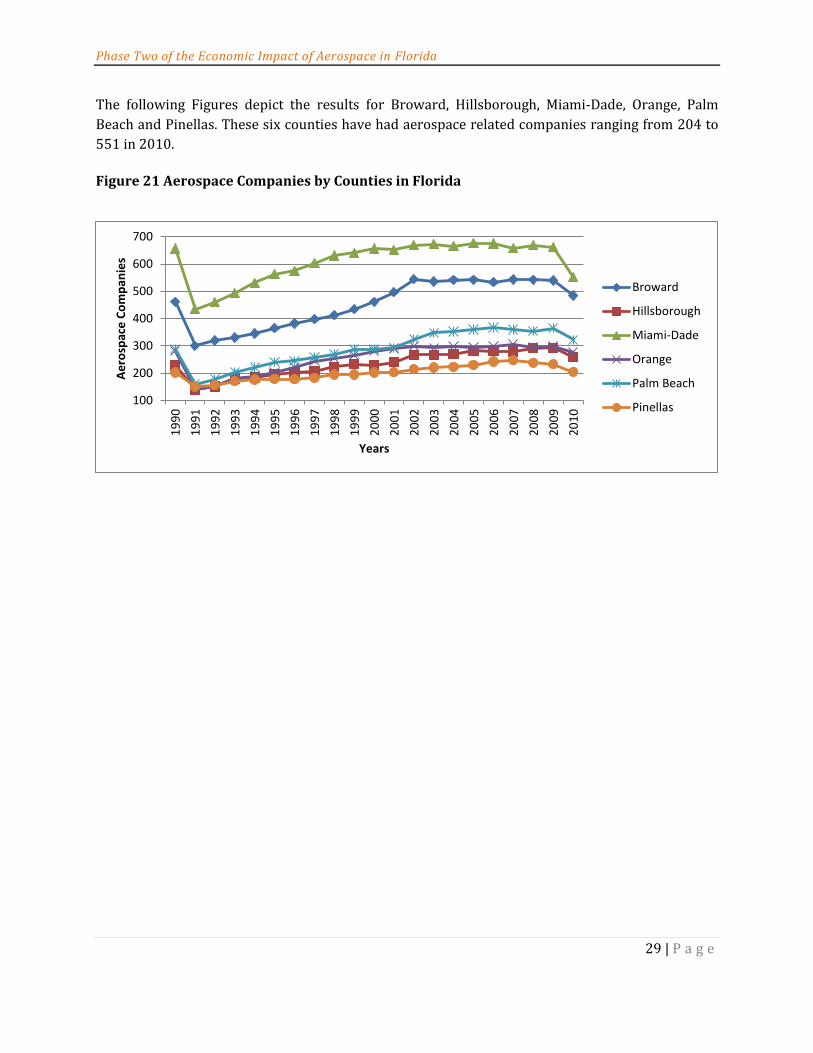

The following Figures depict the results for Broward, Hillsborough, Miami-Dade, Orange, Palm

Beach and Pinellas. These six counties have had aerospace related companies ranging from 204 to

551 in 2010.

Figure 21 Aerospace Companies by Counties in Florida

100

200

300

400

500

600

700

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Co

mp

anie

s

Years

Broward

Hillsborough

Miami-Dade

Orange

Palm Beach

Pinellas

Phase Two of the Economic Impact of Aerospace in Florida

30 | P a g e

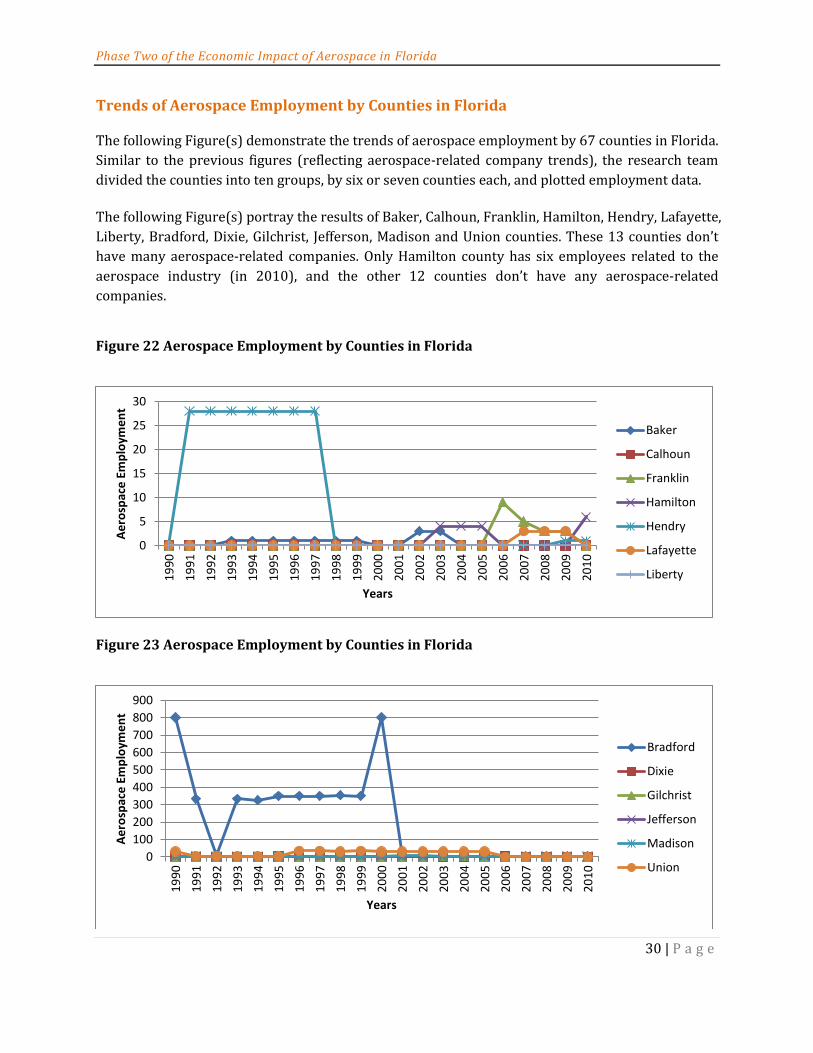

Trends of Aerospace Employment by Counties in Florida The following Figure(s) demonstrate the trends of aerospace employment by 67 counties in Florida.

Similar to the previous figures (reflecting aerospace-related company trends), the research team

divided the counties into ten groups, by six or seven counties each, and plotted employment data.

The following Figure(s) portray the results of Baker, Calhoun, Franklin, Hamilton, Hendry, Lafayette,

Liberty, Bradford, Dixie, Gilchrist, Jefferson, Madison and Union counties. These 13 counties don’t

have many aerospace-related companies. Only Hamilton county has six employees related to the

aerospace industry (in 2010), and the other 12 counties don’t have any aerospace-related

companies.

Figure 22 Aerospace Employment by Counties in Florida

Figure 23 Aerospace Employment by Counties in Florida

0

5

10

15

20

25

30

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

Baker

Calhoun

Franklin

Hamilton

Hendry

Lafayette

Liberty

0

100

200

300

400

500

600

700

800

900

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

Bradford

Dixie

Gilchrist

Jefferson

Madison

Union

Phase Two of the Economic Impact of Aerospace in Florida

31 | P a g e

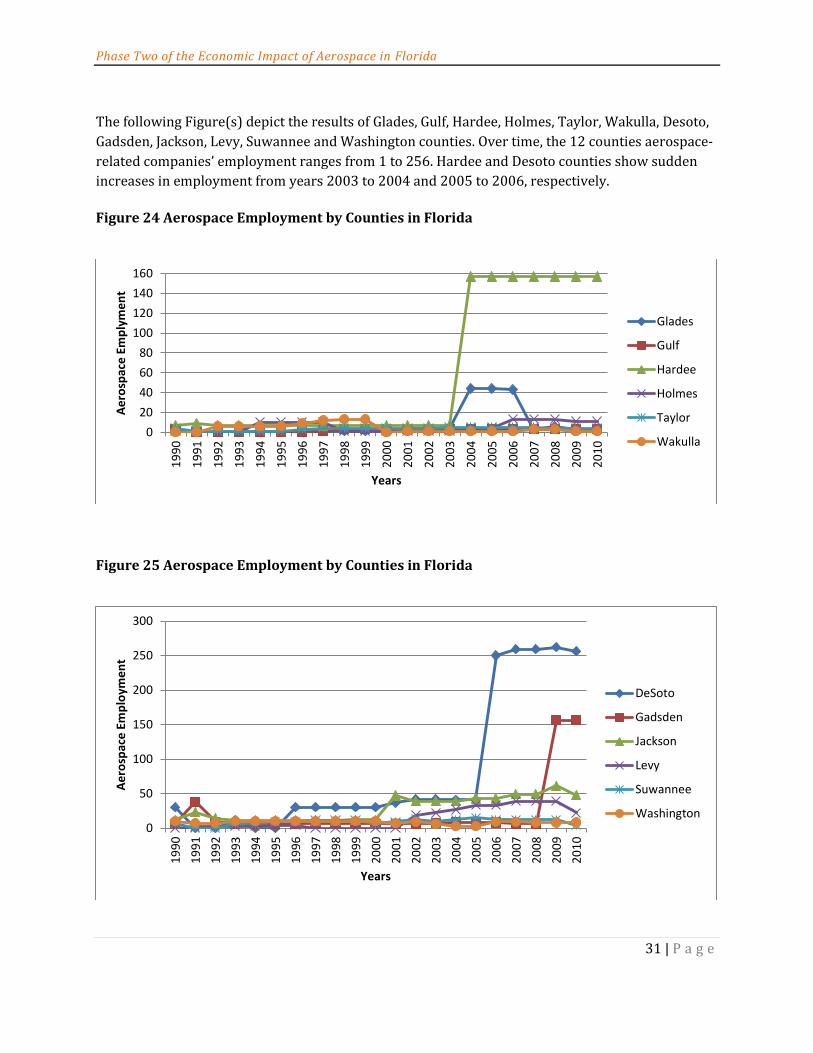

The following Figure(s) depict the results of Glades, Gulf, Hardee, Holmes, Taylor, Wakulla, Desoto,

Gadsden, Jackson, Levy, Suwannee and Washington counties. Over time, the 12 counties aerospace-

related companies’ employment ranges from 1 to 256. Hardee and Desoto counties show sudden

increases in employment from years 2003 to 2004 and 2005 to 2006, respectively.

Figure 24 Aerospace Employment by Counties in Florida

Figure 25 Aerospace Employment by Counties in Florida

0

20

40

60

80

100

120

140

160

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

ply

me

nt

Years

Glades

Gulf

Hardee

Holmes

Taylor

Wakulla

0

50

100

150

200

250

300

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

DeSoto

Gadsden

Jackson

Levy

Suwannee

Washington

Phase Two of the Economic Impact of Aerospace in Florida

32 | P a g e

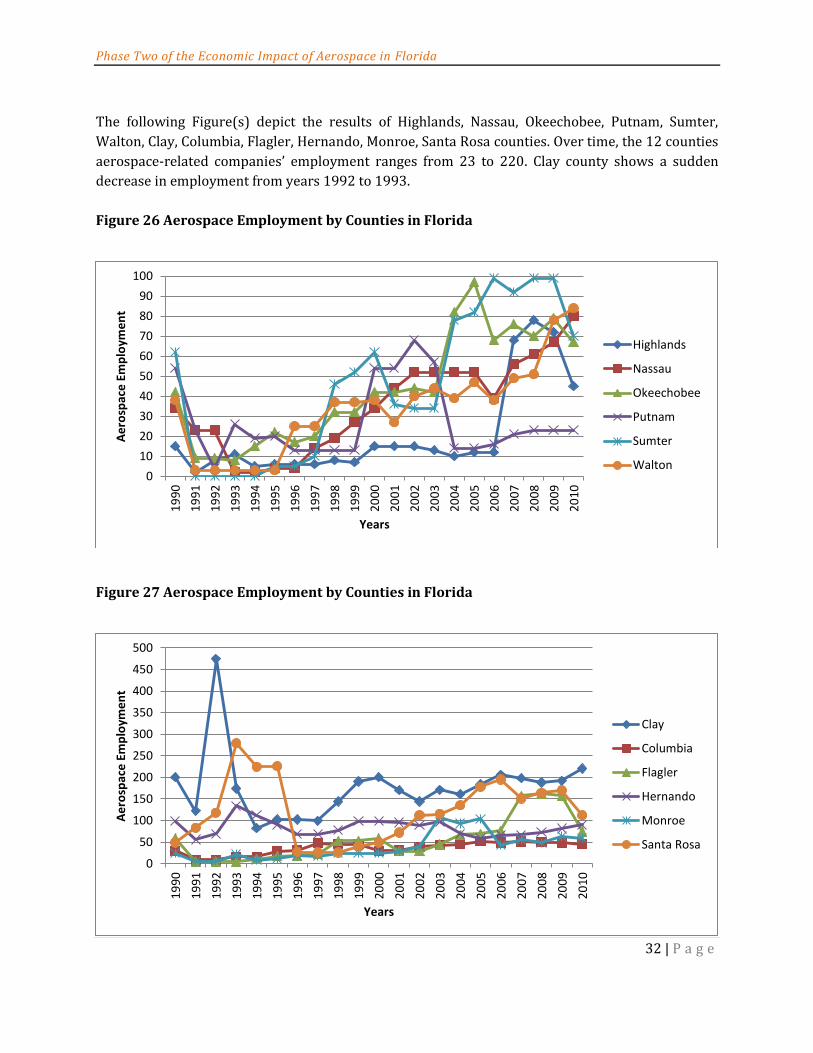

The following Figure(s) depict the results of Highlands, Nassau, Okeechobee, Putnam, Sumter,

Walton, Clay, Columbia, Flagler, Hernando, Monroe, Santa Rosa counties. Over time, the 12 counties

aerospace-related companies’ employment ranges from 23 to 220. Clay county shows a sudden

decrease in employment from years 1992 to 1993.

Figure 26 Aerospace Employment by Counties in Florida

Figure 27 Aerospace Employment by Counties in Florida

0

10

20

30

40

50

60

70

80

90

100

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

Highlands

Nassau

Okeechobee

Putnam

Sumter

Walton

0

50

100

150

200

250

300

350

400

450

500

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

Clay

Columbia

Flagler

Hernando

Monroe

Santa Rosa

Phase Two of the Economic Impact of Aerospace in Florida

33 | P a g e

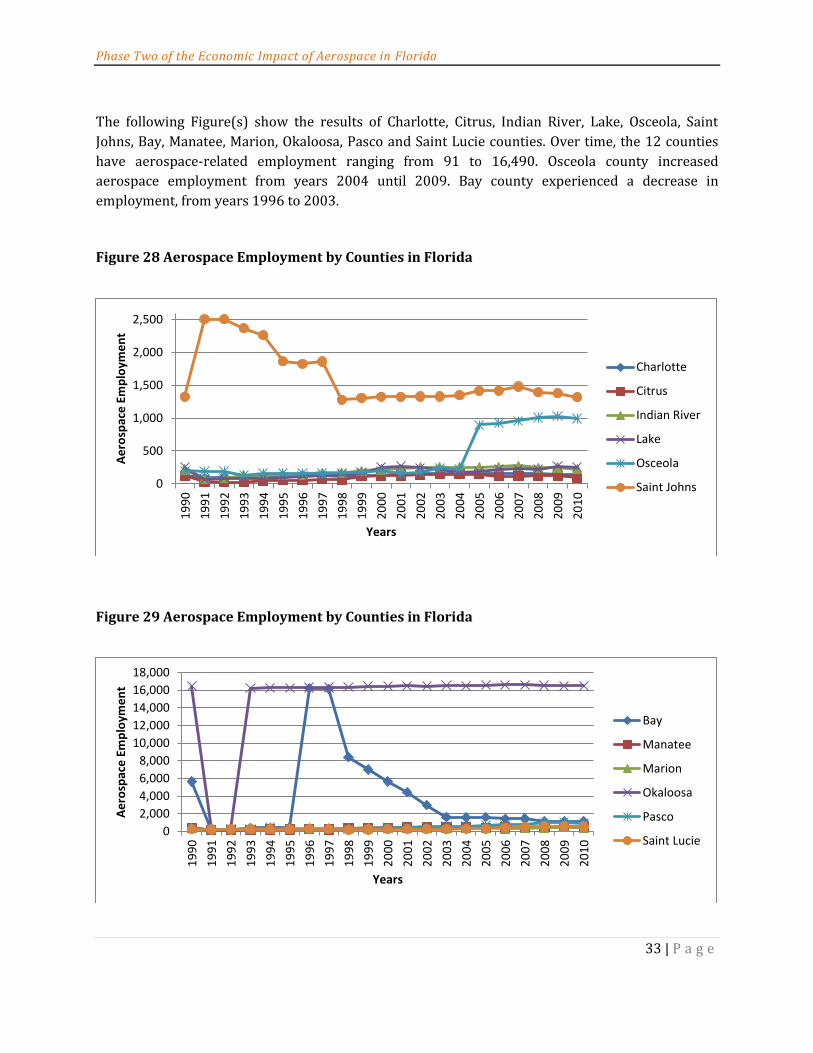

The following Figure(s) show the results of Charlotte, Citrus, Indian River, Lake, Osceola, Saint

Johns, Bay, Manatee, Marion, Okaloosa, Pasco and Saint Lucie counties. Over time, the 12 counties

have aerospace-related employment ranging from 91 to 16,490. Osceola county increased

aerospace employment from years 2004 until 2009. Bay county experienced a decrease in

employment, from years 1996 to 2003.

Figure 28 Aerospace Employment by Counties in Florida

Figure 29 Aerospace Employment by Counties in Florida

0

500

1,000

1,500

2,000

2,500

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

Charlotte

Citrus

Indian River

Lake

Osceola

Saint Johns

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

Bay

Manatee

Marion

Okaloosa

Pasco

Saint Lucie

Phase Two of the Economic Impact of Aerospace in Florida

34 | P a g e

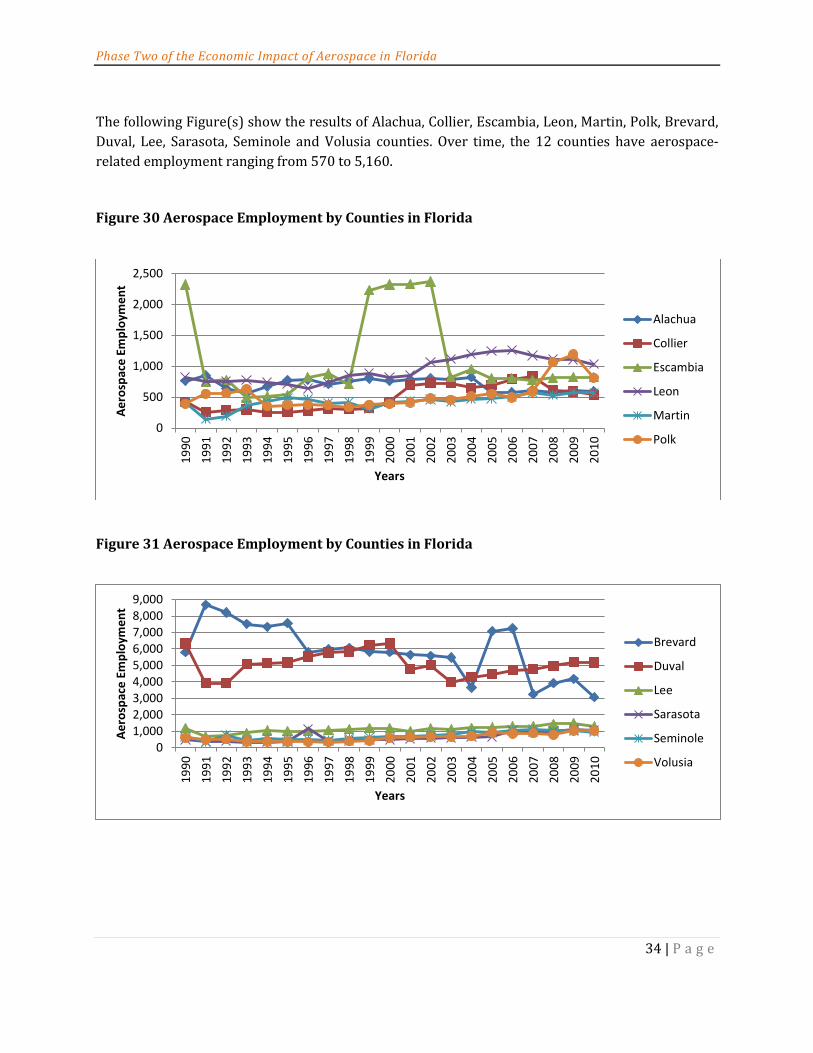

The following Figure(s) show the results of Alachua, Collier, Escambia, Leon, Martin, Polk, Brevard,

Duval, Lee, Sarasota, Seminole and Volusia counties. Over time, the 12 counties have aerospace-

related employment ranging from 570 to 5,160.

Figure 30 Aerospace Employment by Counties in Florida

Figure 31 Aerospace Employment by Counties in Florida

0

500

1,000

1,500

2,000

2,500

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

Alachua

Collier

Escambia

Leon

Martin

Polk

01,0002,0003,0004,0005,0006,0007,0008,0009,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

Brevard

Duval

Lee

Sarasota

Seminole

Volusia

Phase Two of the Economic Impact of Aerospace in Florida

35 | P a g e

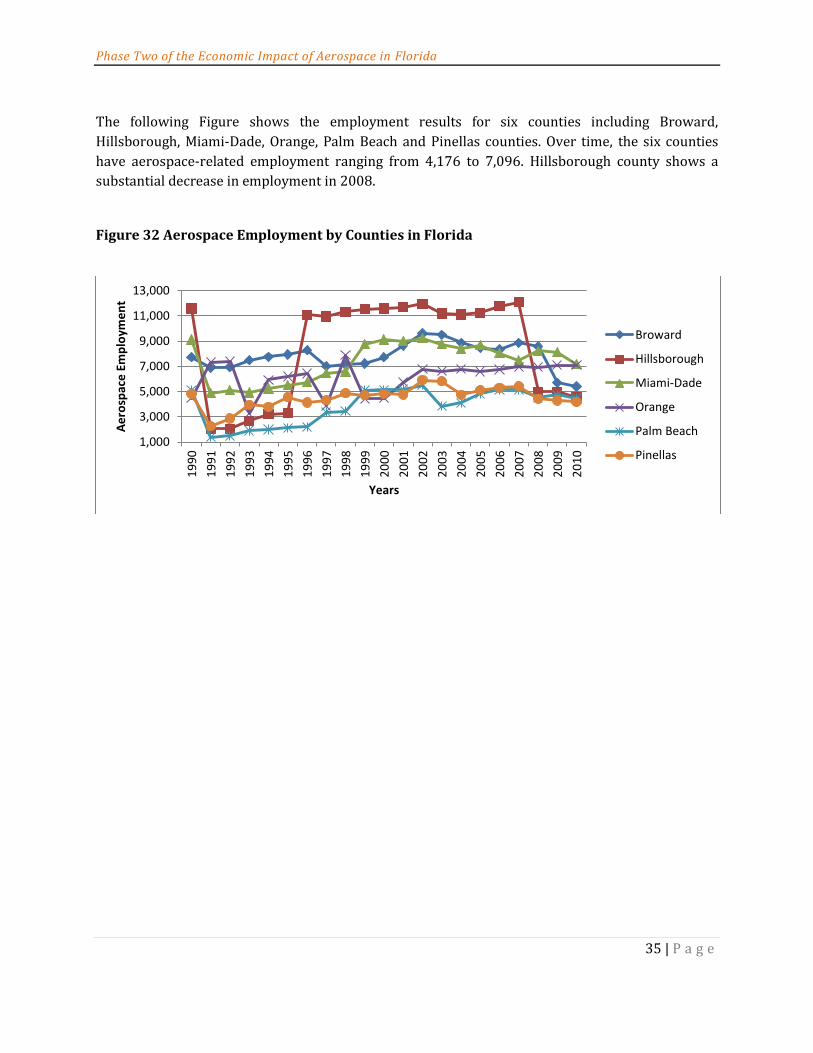

The following Figure shows the employment results for six counties including Broward,

Hillsborough, Miami-Dade, Orange, Palm Beach and Pinellas counties. Over time, the six counties

have aerospace-related employment ranging from 4,176 to 7,096. Hillsborough county shows a

substantial decrease in employment in 2008.

Figure 32 Aerospace Employment by Counties in Florida

1,000

3,000

5,000

7,000

9,000

11,000

13,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Em

plo

yme

nt

Years

Broward

Hillsborough

Miami-Dade

Orange

Palm Beach

Pinellas

Phase Two of the Economic Impact of Aerospace in Florida

36 | P a g e

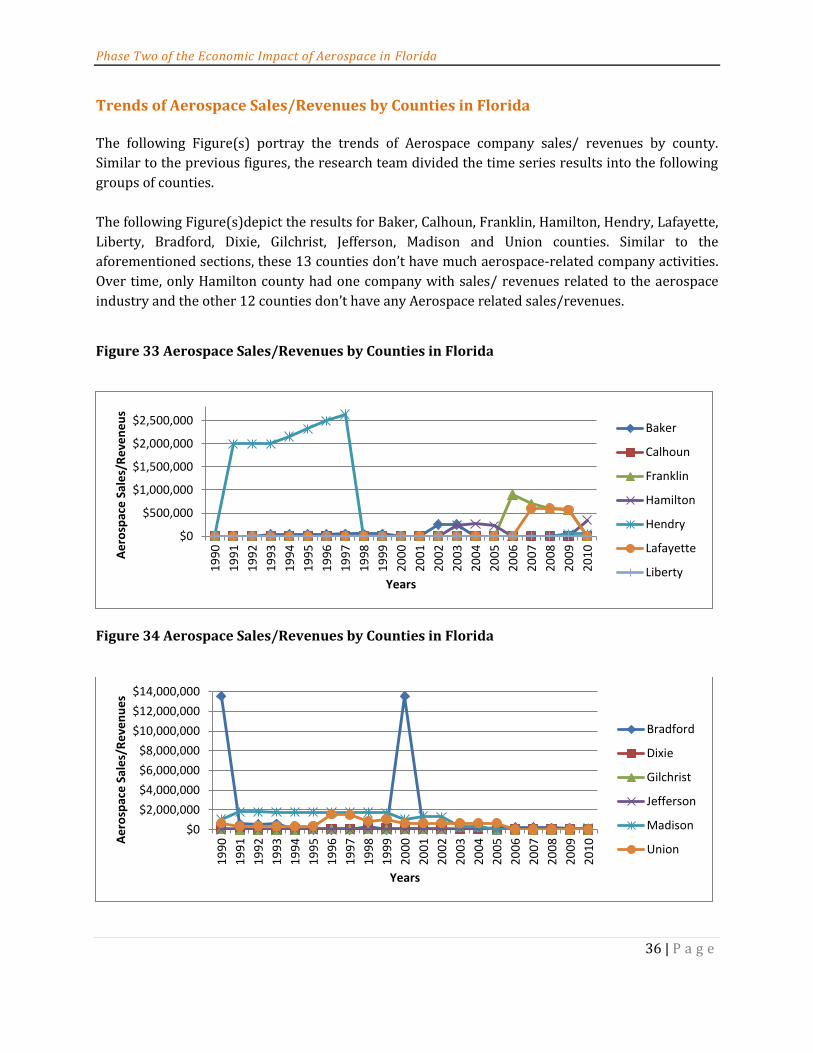

Trends of Aerospace Sales/Revenues by Counties in Florida

The following Figure(s) portray the trends of Aerospace company sales/ revenues by county.

Similar to the previous figures, the research team divided the time series results into the following

groups of counties.

The following Figure(s)depict the results for Baker, Calhoun, Franklin, Hamilton, Hendry, Lafayette,

Liberty, Bradford, Dixie, Gilchrist, Jefferson, Madison and Union counties. Similar to the

aforementioned sections, these 13 counties don’t have much aerospace-related company activities.

Over time, only Hamilton county had one company with sales/ revenues related to the aerospace

industry and the other 12 counties don’t have any Aerospace related sales/revenues.

Figure 33 Aerospace Sales/Revenues by Counties in Florida

Figure 34 Aerospace Sales/Revenues by Counties in Florida

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

eu

s

Years

Baker

Calhoun

Franklin

Hamilton

Hendry

Lafayette

Liberty

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10A

ero

spac

e S

ale

s/R

eve

nu

es

Years

Bradford

Dixie

Gilchrist

Jefferson

Madison

Union

Phase Two of the Economic Impact of Aerospace in Florida

37 | P a g e

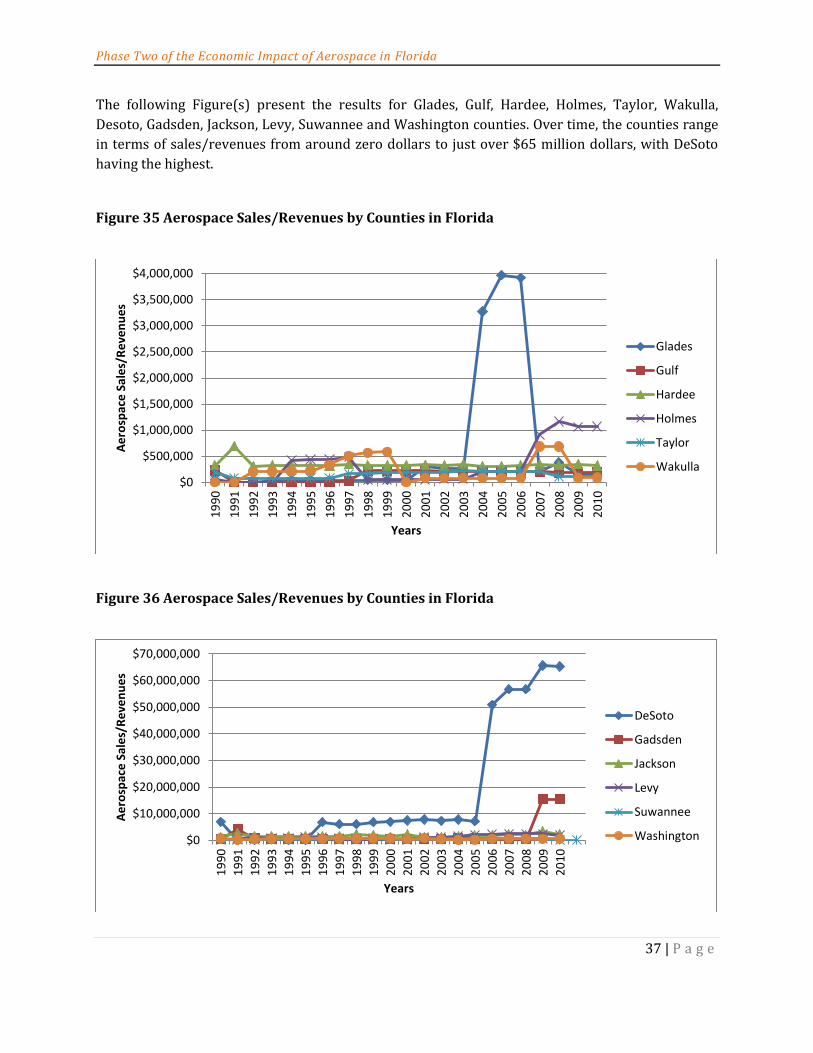

The following Figure(s) present the results for Glades, Gulf, Hardee, Holmes, Taylor, Wakulla,

Desoto, Gadsden, Jackson, Levy, Suwannee and Washington counties. Over time, the counties range

in terms of sales/revenues from around zero dollars to just over $65 million dollars, with DeSoto

having the highest.

Figure 35 Aerospace Sales/Revenues by Counties in Florida

Figure 36 Aerospace Sales/Revenues by Counties in Florida

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

ue

s

Years

Glades

Gulf

Hardee

Holmes

Taylor

Wakulla

$0

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

$70,000,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

ue

s

Years

DeSoto

Gadsden

Jackson

Levy

Suwannee

Washington

Phase Two of the Economic Impact of Aerospace in Florida

38 | P a g e

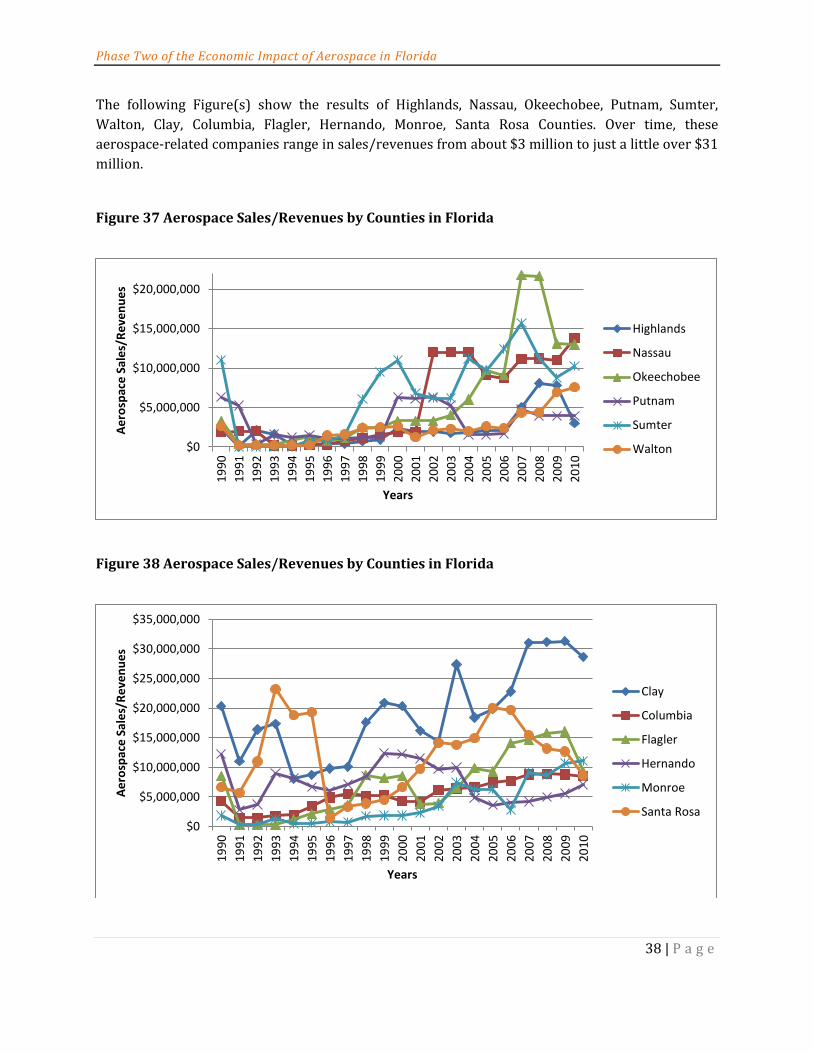

The following Figure(s) show the results of Highlands, Nassau, Okeechobee, Putnam, Sumter,

Walton, Clay, Columbia, Flagler, Hernando, Monroe, Santa Rosa Counties. Over time, these

aerospace-related companies range in sales/revenues from about $3 million to just a little over $31

million.

Figure 37 Aerospace Sales/Revenues by Counties in Florida

Figure 38 Aerospace Sales/Revenues by Counties in Florida

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

ue

s

Years

Highlands

Nassau

Okeechobee

Putnam

Sumter

Walton

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

$35,000,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

ue

s

Years

Clay

Columbia

Flagler

Hernando

Monroe

Santa Rosa

Phase Two of the Economic Impact of Aerospace in Florida

39 | P a g e

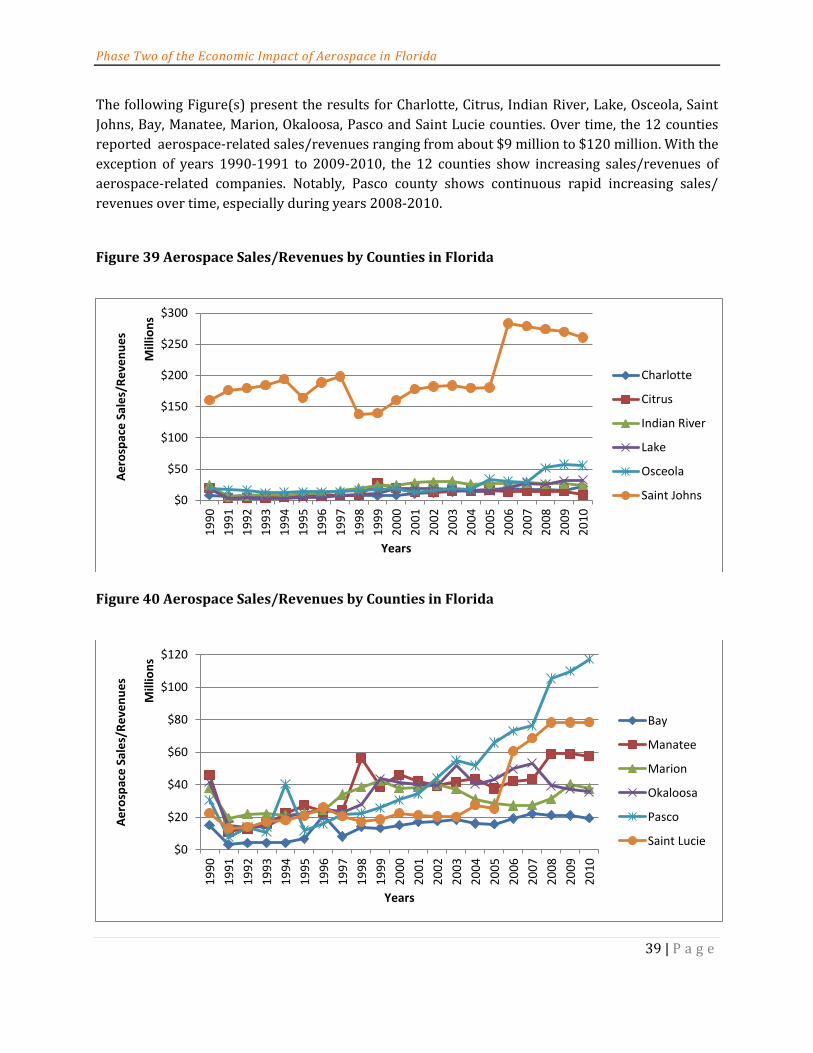

The following Figure(s) present the results for Charlotte, Citrus, Indian River, Lake, Osceola, Saint

Johns, Bay, Manatee, Marion, Okaloosa, Pasco and Saint Lucie counties. Over time, the 12 counties

reported aerospace-related sales/revenues ranging from about $9 million to $120 million. With the

exception of years 1990-1991 to 2009-2010, the 12 counties show increasing sales/revenues of

aerospace-related companies. Notably, Pasco county shows continuous rapid increasing sales/

revenues over time, especially during years 2008-2010.

Figure 39 Aerospace Sales/Revenues by Counties in Florida

Figure 40 Aerospace Sales/Revenues by Counties in Florida

$0

$50

$100

$150

$200

$250

$300

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

ue

s

Mill

ion

s

Years

Charlotte

Citrus

Indian River

Lake

Osceola

Saint Johns

$0

$20

$40

$60

$80

$100

$120

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

ue

s

Mill

ion

s

Years

Bay

Manatee

Marion

Okaloosa

Pasco

Saint Lucie

Phase Two of the Economic Impact of Aerospace in Florida

40 | P a g e

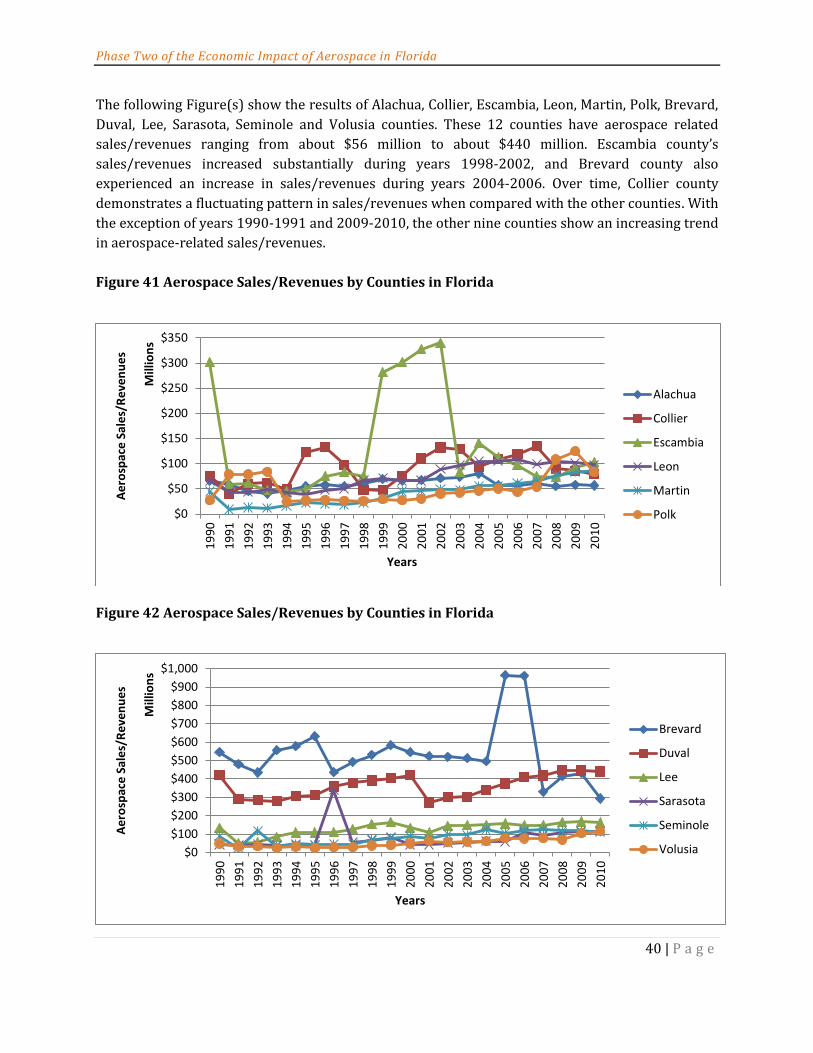

The following Figure(s) show the results of Alachua, Collier, Escambia, Leon, Martin, Polk, Brevard,

Duval, Lee, Sarasota, Seminole and Volusia counties. These 12 counties have aerospace related

sales/revenues ranging from about $56 million to about $440 million. Escambia county’s

sales/revenues increased substantially during years 1998-2002, and Brevard county also

experienced an increase in sales/revenues during years 2004-2006. Over time, Collier county

demonstrates a fluctuating pattern in sales/revenues when compared with the other counties. With

the exception of years 1990-1991 and 2009-2010, the other nine counties show an increasing trend

in aerospace-related sales/revenues.

Figure 41 Aerospace Sales/Revenues by Counties in Florida

Figure 42 Aerospace Sales/Revenues by Counties in Florida

$0

$50

$100

$150

$200

$250

$300

$350

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

ue

s

Mill

ion

s

Years

Alachua

Collier

Escambia

Leon

Martin

Polk

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

ue

s

Mill

ion

s

Years

Brevard

Duval

Lee

Sarasota

Seminole

Volusia

Phase Two of the Economic Impact of Aerospace in Florida

41 | P a g e

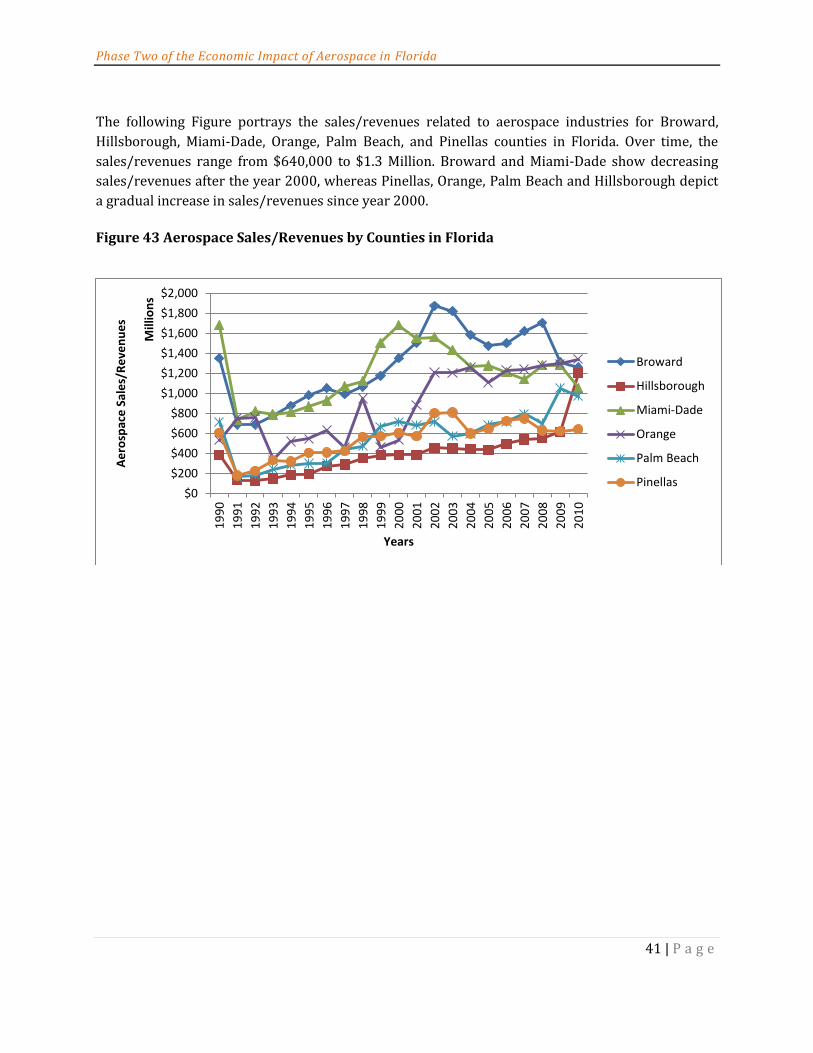

The following Figure portrays the sales/revenues related to aerospace industries for Broward,

Hillsborough, Miami-Dade, Orange, Palm Beach, and Pinellas counties in Florida. Over time, the

sales/revenues range from $640,000 to $1.3 Million. Broward and Miami-Dade show decreasing

sales/revenues after the year 2000, whereas Pinellas, Orange, Palm Beach and Hillsborough depict

a gradual increase in sales/revenues since year 2000.

Figure 43 Aerospace Sales/Revenues by Counties in Florida

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Ae

rosp

ace

Sal

es/

Re

ven

ue

s

Mill

ion

s

Years

Broward

Hillsborough

Miami-Dade

Orange

Palm Beach

Pinellas

Phase Two of the Economic Impact of Aerospace in Florida

42 | P a g e

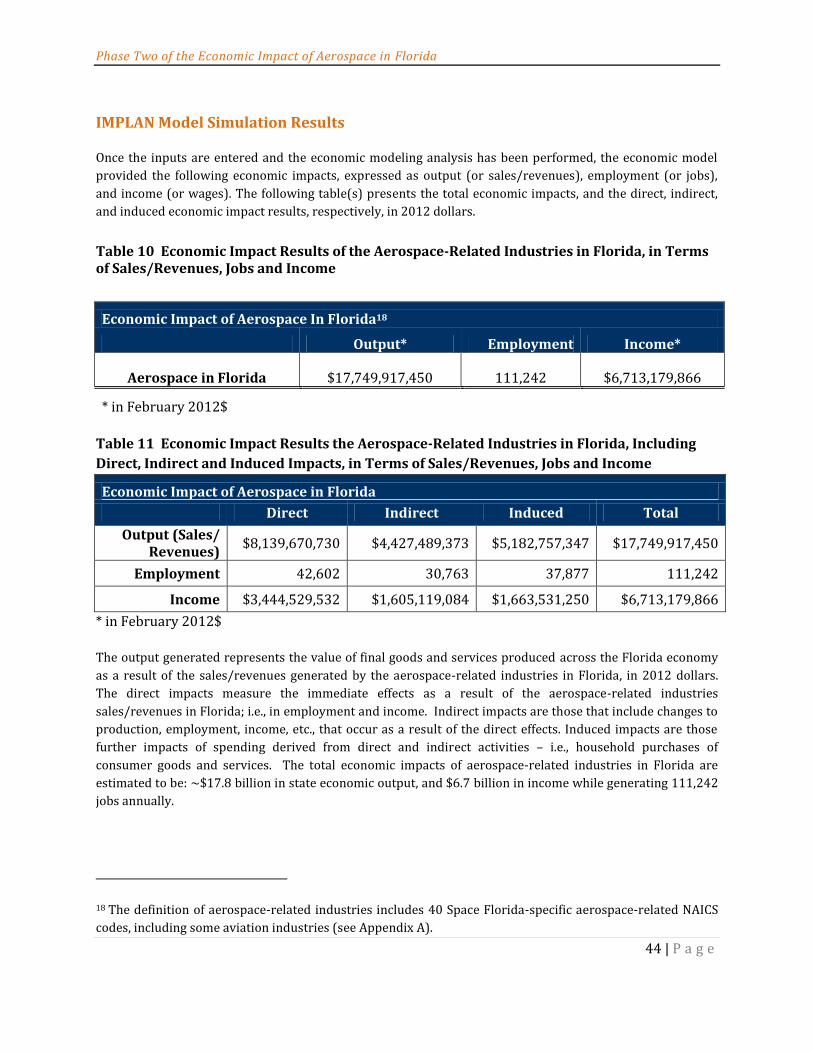

V. Economic Impact Analysis

The IMPLAN Economic Impact Model Methodology

The county-specific economic impact analysis was performed using the state of Florida Impact

Analysis for Planning, or IMPLAN, model, a widely accepted and used integrated input-output

model. IMPLAN is used extensively by state and local government agencies to measure proposed

legislative and other program and policy economic impacts across the private and public sectors. In

addition, it is the tool of choice to measure these impacts by a number of universities and private

research groups that evaluate economic impacts across the state and nation. There are several

advantages to using IMPLAN:

It is calibrated to local conditions using a relatively large amount of local county level and

state of Florida specific data;

It is based on a strong theoretical foundation

It uses a well-researched and accepted applied economics impact assessment

methodology supported by many years of use across all regions of the U.S.

The IMPLAN model used for this analysis was specifically developed for the counties of Florida, and

includes 440 sectors, and latest dataset – year 2010 data. IMPLAN’s principal advantage is that it

may be used to forecast direct, indirect and induced economic effects for an initial economic

stimulus.

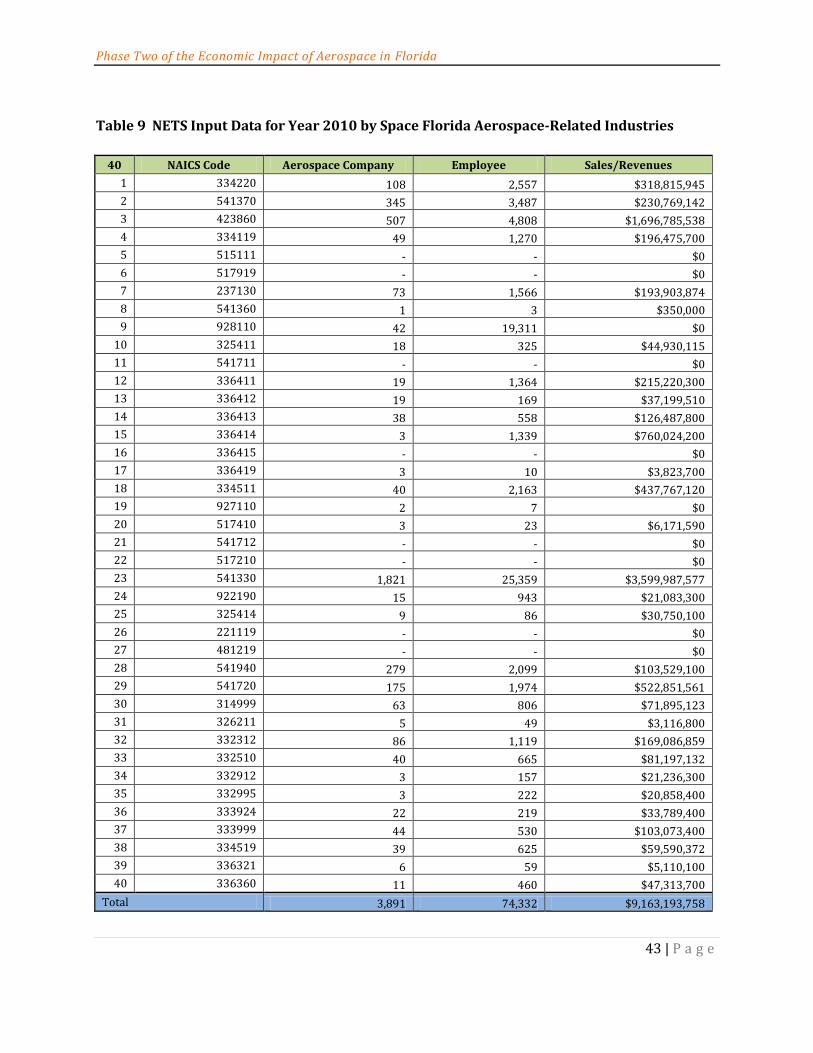

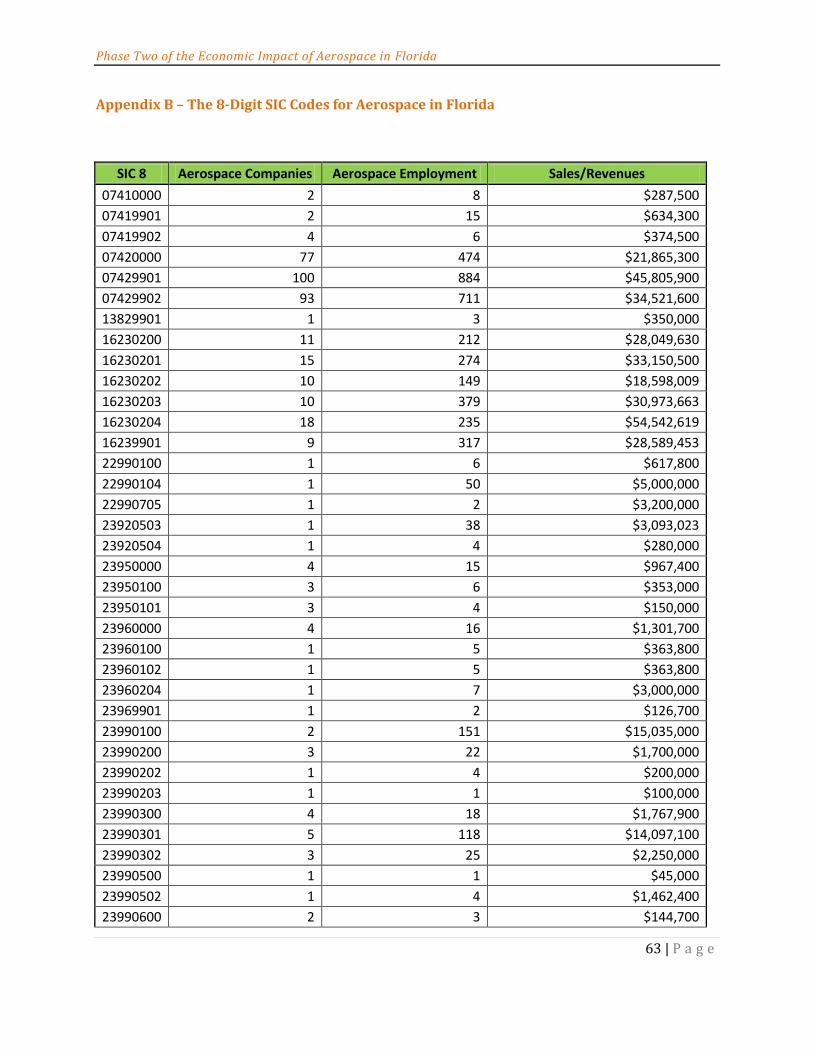

Primary Input Data for Economic Impact Model(s)

The following table presents the primary input data for the economic impact model for the Phase

One economic analysis.

National Establishment Time Series (NETS) dataset 17 for Florida aerospace-related

businesses, based on 6-digit NAICS codes and 8-digit SIC codes associated with the Space

Florida categories (see Appendix A for a listing of “aerospace” industries and other standard

definition/NAICS).

17 National Establishment Time Series (NETS) dataset was developed to better describe the dynamics of the

US economy by Walls & Associates teaming up with Dun and Bradstreet. Presently In 2012, the NETS

Database has taken twenty-one annual snapshots (taken every January) of the full Duns Marketing

Information (DMI) file that followed over 44.2 million establishments between January 1990 and January

2010.

Phase Two of the Economic Impact of Aerospace in Florida

43 | P a g e

Table 9 NETS Input Data for Year 2010 by Space Florida Aerospace-Related Industries

40 NAICS Code Aerospace Company Employee Sales/Revenues