17

Planning and Budgeting Chapter 13 Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

| Date post: | 23-Dec-2015 |

| Category: |

Documents |

| Upload: | cory-harrington |

| View: | 215 times |

| Download: | 2 times |

Planning and Budgeting

Chapter 13

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Budgets

• A budget is a financial plan of the resources neededto carry out activities and meet financial goals.

• Budgets play an important role in managing cash flows.

• Critical success factors are the strengths of acompany that enable it to outperform competitors.

LO1

L.O. 1 Understand the role of budgets in overall organization plans.

13 - 2

Human Element in Budgeting

L.O. 2 Understand the importance of people in the budgeting process.

Organizationgoals

Individualgoals

Goal congruence

• Participative budgeting:Use of input from lower- and middle-managementemployees; also called grass roots budgeting

13 - 3

Sales Forecasting

L.O. 3 Estimate sales.

• Forecasting sales is the most difficult aspect of budgeting.

Sales staff

Market researchers

Delphi technique

Trend analysis

Econometric models

13 - 4

Forecasting ProductionL.O. 4 Develop production and cost budgets.

• A production budget is a plan of resources neededto meet current sales demand and ensure thatinventory levels are sufficient for future sales.

Beginning balanceBB

Transfers inTI

Transfers outTO

+ – = Ending balance

Units in beginninginventory

Requiredproduction

Budgetedsales

+ – =Units in ending

inventory

13 - 5

Cash BudgetL.O. 5 Estimate cash flows.

• The cash budget is a statement of cash on hand atthe start of the budget period, expected cash receipts,expected cash disbursements, and the resulting cashbalance at the end of the budget period.

• Cash receipts:– Collection of accounts receivable– Cash sales– Sales of assets– Borrowing– Issuing stock– Other

13 - 6

Cash BudgetLO5

• Cash disbursements:– Materials purchases– Manufacturing costs– Operating activities– Debt repayment– Acquisition of new assets– Income taxes– Dividends– Other activities

13 - 7

Cash Collections ExampleLO5

Santiago PantsMonthly Collection Experience

Sales on Credit

Cash collected from current month's sales 20%Cash collected from last month's sales 75Cash discounts taken (percentage of gross sales) 2Written off as bad debt 3Total disposition of credit sales in current month 100%

Expected Sales for Three Months

January sales $500,000February sales $450,000

March sales $600,000

13 - 8

Cash Collections ExampleLO5

Santiago PantsMultiperiod Schedule of Cash Collections

For the Quarter Ended March 31

Beginning accounts receivable,January 1, $540,000

January sales, $500,000a

February sales, $450,000b

March sales, $600,000c

Total cash collections

$540,000 100,000

$640,000

$375,000 90,000

$465,000

$337,500 120,000$457,500

January

$ 540,000 475,000 427,500 120,000$1,562,500

Month

February MarchTotal forQuarter

a 20% collected in January, 75% collected in February, and 5% not collectedb 20% collected in February, 75% collected in March, and 5% not collectedc 20% collected in March, 75% collected in April, and 5% not collected

13 - 9

Cash Disbursements ExampleLO5

Santiago PantsMonthly Disbursements for Purchases Experience

Cash disbursement for current month's purchases 50%Cash disbursement for prior month's purchases 48Cash discounts taken 2Total cash disbursement for purchases 100%

Expected Purchases for Three Months

January sales $120,000February sales $200,000

March sales $250,000

13 - 10

Cash Disbursements ExampleLO5

Santiago PantsMultiperiod Schedule of Cash Disbursements

For the Quarter Ended March 31

Beginning accounts payable,January 1, $256,000

January purchases, $120,000a

February purchases, $200,000b

March purchases, $250,000c

Additional cash paymentsTotal cash disbursements

$256,000 60,000

250,000$566,000

$ 57,600 100,000

250,000$407,600

$ 96,000 125,000 250,000$471,000

January

$ 256,000 117,600 196,000 125,000 750,000$1,444,600

Month

February MarchTotal forQuarter

a 50% paid in January, 48% paid in February, and 2% discounts takenb 50% paid in February, 48% paid in March, and 2% discounts takenc 50% paid in March, 48% paid in April, and 2% discounts taken

13 - 11

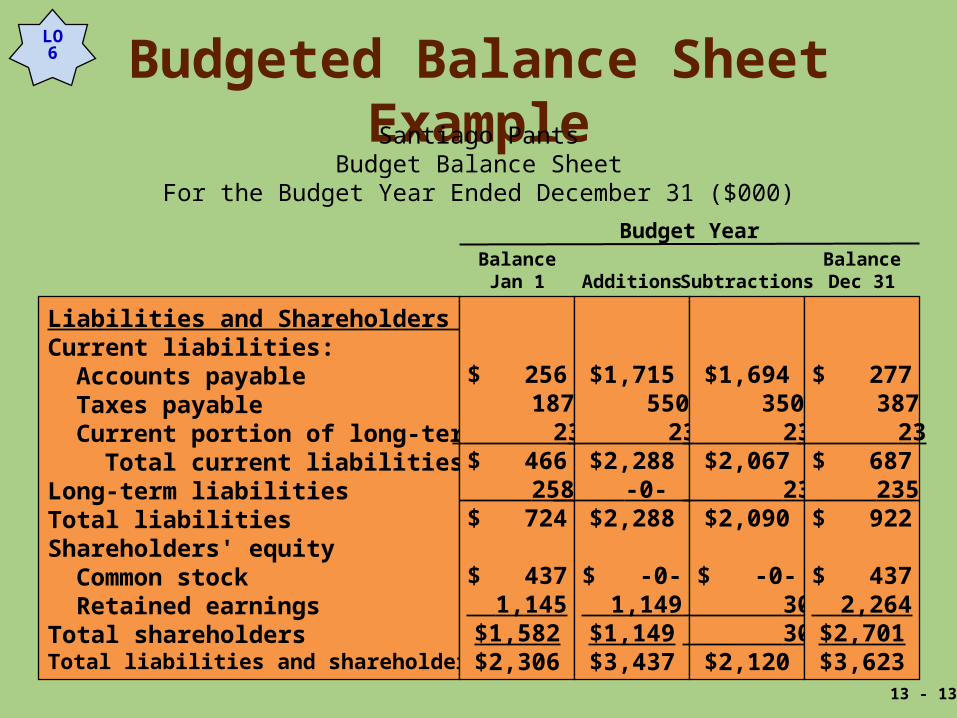

Budgeted Balance Sheet ExampleL.O. 6 Develop budgeted financial statements.

AssetsCurrent assets:

CashAccounts receivableInventoriesOther current assets

Total current assetsLong-term assets:

Property, plant, equipmentLess: Accumulated depreciation

Total assets

Budget Year

$ 830 540 155 161$1,686

1,866 (1,246)$2,306

$ 6,940 7,200 4,265 -0- $18,405

1,470 (220)$19,651

$ 7,399 6,840 3,995 100$18,334

-0- -0- $18,334

$ 371 900 425 61$1,757

3,336 (1,470)$3,623

BalanceJan 1 Additions Subtractions

BalanceDec 31

Santiago PantsBudget Balance Sheet

For the Budget Year Ended December 31 ($000)

13 - 12

Budgeted Balance Sheet ExampleLO6

Liabilities and Shareholders EquityCurrent liabilities:

Accounts payableTaxes payableCurrent portion of long-term debt

Total current liabilitiesLong-term liabilitiesTotal liabilitiesShareholders' equity

Common stockRetained earnings

Total shareholdersTotal liabilities and shareholders equity

Budget Year

$ 256 187 23$ 466 258$ 724

$ 437 1,145$1,582$2,306

$1,715 550 23$2,288 -0- $2,288

$ -0- 1,149$1,149$3,437

$1,694 350 23$2,067 23$2,090

$ -0- 30 30$2,120

$ 277 387 23$ 687 235$ 922

$ 437 2,264$2,701$3,623

BalanceJan 1 Additions Subtractions

BalanceDec 31

Santiago PantsBudget Balance Sheet

For the Budget Year Ended December 31 ($000)

13 - 13

Budgeting in Service Organizations

Marketing andadministrativecost budget

Sales forecast

Budgeted costof services

Budgetedincome

statement

Cash budgetBudgeted

balance sheets

L.O. 7 Explain budgeting in merchandising and service organizations.

13 - 14

Ethical Problems in BudgetingL.O. 8 Explain why ethical issues arise in budgeting.

• Budgets can create serious ethical issuesfor many people.

• The company must recognize the trade-offbetween encouraging unbiased reporting bymanagers and the use of budget informationin performance evaluation and rewards.

13 - 15

Budgeting Under UncertaintyL.O. 9 Explain how to use sensitivity analysis

to budget under uncertainty.

• Budgets allow management to explore manyalternatives.

• Spreadsheets are helpful in preparing budgetsand quantifying “what-if” conditions.

13 - 16

End of Chapter 13

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin