Page 1

1

Politecnico di Milano

School of Industrial and Information Engineering

Master of Science Management Engineering

Performance implications of Sino-Foreign Joint Ventures vs.

Wholly Foreign Owned Enterprises in Chinese

Pharmaceutical industry

Supervisor: Prof. Stefano Elia Student: Salman Tahir Mirza (852547)

Student: Sarah Zafar (852654)

Academic year 2017/18

Page 2

2

Abstract

The Economy of China went through a revolutionary change when it entered into the

World Trade Organization in 2001, reducing the barriers on FDI and making the infrastructure

more favourable for Wholly Foreign Owned Enterprises (WFOE) due to which majority of the

foreign firms which existed as Joint Ventures converted to Wholly Foreign Owned Enterprises

(WFOE) while many remained as Joint Ventures.

China has the second largest pharmaceutical market in the world and this research is

done to understand whether foreign pharmaceutical companies in China perform better as

WFOE or Joint Venture.

We review established theories including Transaction Cost Economics, Eclectic

Paradigm, Resource Based View and the Institutional Theory which explain the operation

mode choice for foreign companies in China focusing our attention on the choice between

Joint Ventures and Wholly Foreign Owned Enterprises. In light of these theories we analyse

the financial performance of Joint Ventures and WFOE using extensive Oriana & Orbis

database of Bureau Van Dijk and conduct an empirical analysis using ANOVA statistics to

determine whether significant differences exist between the two groups. Our results indicate

significant differences do exists between the financial performances while it also indicates

that Sino-Foreign Joint Ventures perform considerably better than WFOE in the Chinese

pharmaceutical industry.

Page 3

3

Abstract

L’economia della Cina si addentrò in un cambiamento rivoluzionario quando nel 2001

entrò nella World Trade Organization, riducendo le barrier su FDI e creando infrastrutture

migliori per WFOE che hanno portato la maggioranza delle imprese che esistevano come Joint

Venture a convertirsi in WFOE mentre molte rimasero come Join Venture.

La Cina ha il secondo più grande mercato farmaceutico del mondo e questa ricerca è

stata fatta per capire se le imprese farmaceutiche straniere in Cina hanno performance

migliori come WFOE o come JV.

Rivediamo teorie conclamate che includono TCE, EP, RBV and IT che spiegano la

modalità di scelta dell’operazione per le compagnie straniere in Cina focalizzando la nostra

attenzione sulla scelta tra la performance finanziaria della JV e della WFOE utilizzando un

esteso database dall’Oriana database del BVD e conducendo un’empirica analisi utilizzando

statistiche ANOVA per determinare importanti differenze che esistono tra i due gruppi. I

nostri risultati indicano che Sino Foreign Joint Ventures rende considerevolmente meglio che

WFOE nell’industria farmaceutica cinese.

Page 4

4

1 Contents Abstract ................................................................................................................................................... 2

Abstract ................................................................................................................................................... 3

1. Executive summary ......................................................................................................................... 9

2. Theoretical framework ................................................................................................................. 12

2.1. Sources .................................................................................................................................. 12

2.2. Motives for FDI ...................................................................................................................... 12

2.2.1. Market Seeking ............................................................................................................. 13

2.2.2. Efficiency seeking .......................................................................................................... 13

2.2.3. Resource seeking .......................................................................................................... 14

2.2.4. Strategic Asset Seeking ................................................................................................. 14

2.3. Theories related to entry modes .......................................................................................... 14

2.3.1. Transaction Cost Economics ......................................................................................... 14

2.3.2. Transaction cost economics in case of Foreign Expansion ........................................... 16

a. Asset Specificity .................................................................................................................... 17

b. External Uncertainty ............................................................................................................. 18

c. Internal Uncertainty .............................................................................................................. 19

2.3.3. Eclectic Theory .................................................................................................................. 19

2.3.3.1. Ownership Advantages ............................................................................................. 20

• Firm Size ................................................................................................................................ 20

• Firm’s international experience ............................................................................................ 21

2.3.3.2. Location Advantages ................................................................................................. 21

• Market Size ........................................................................................................................... 22

• Host country risk ................................................................................................................... 22

• Cultural distance ................................................................................................................... 22

2.3.3.3. Internalization Advantages ....................................................................................... 23

• Contractual Risk .................................................................................................................... 23

2.3.4. Resource Based Theory ..................................................................................................... 23

2.3.5. Institutional Theory ........................................................................................................... 25

• Regulatory Institutions .......................................................................................................... 26

• Normative Institutions .......................................................................................................... 26

• Cognitive Institutions ............................................................................................................ 27

a) External Mimicry ................................................................................................................... 28

b) Internal Mimicry .................................................................................................................... 28

Page 5

5

2.4. Literature related to the performance measurement due to ownership structure and

control

3. Introduction to China .................................................................................................................... 31

3.1. Main modes of operation for companies in China ............................................................... 33

a) Representative Office ........................................................................................................... 33

b) Branch Office ......................................................................................................................... 34

c) State Owned Enterprises ...................................................................................................... 34

d) Foreign Invested Partnership Enterprise .............................................................................. 34

e) Joint Ventures ....................................................................................................................... 35

f) Wholly Owned Foreign Enterprise ........................................................................................ 36

3.2. Reforms in China ................................................................................................................... 36

3.3. Pharmaceutical Market in China ........................................................................................... 40

3.3.1. Market Breakdown ....................................................................................................... 41

a) Generics ................................................................................................................................ 41

b) Patented Drugs ..................................................................................................................... 42

c) OTC ........................................................................................................................................ 42

3.4. Research & development in China Pharma .......................................................................... 43

4. Data Analysis ................................................................................................................................. 44

4.1. Data description .................................................................................................................... 44

4.2. Data sampling and sorting .................................................................................................... 45

4.3. Methodology ......................................................................................................................... 46

4.4. ANOVA .................................................................................................................................. 46

4.4.1. Model hypothesis & assumptions ................................................................................. 47

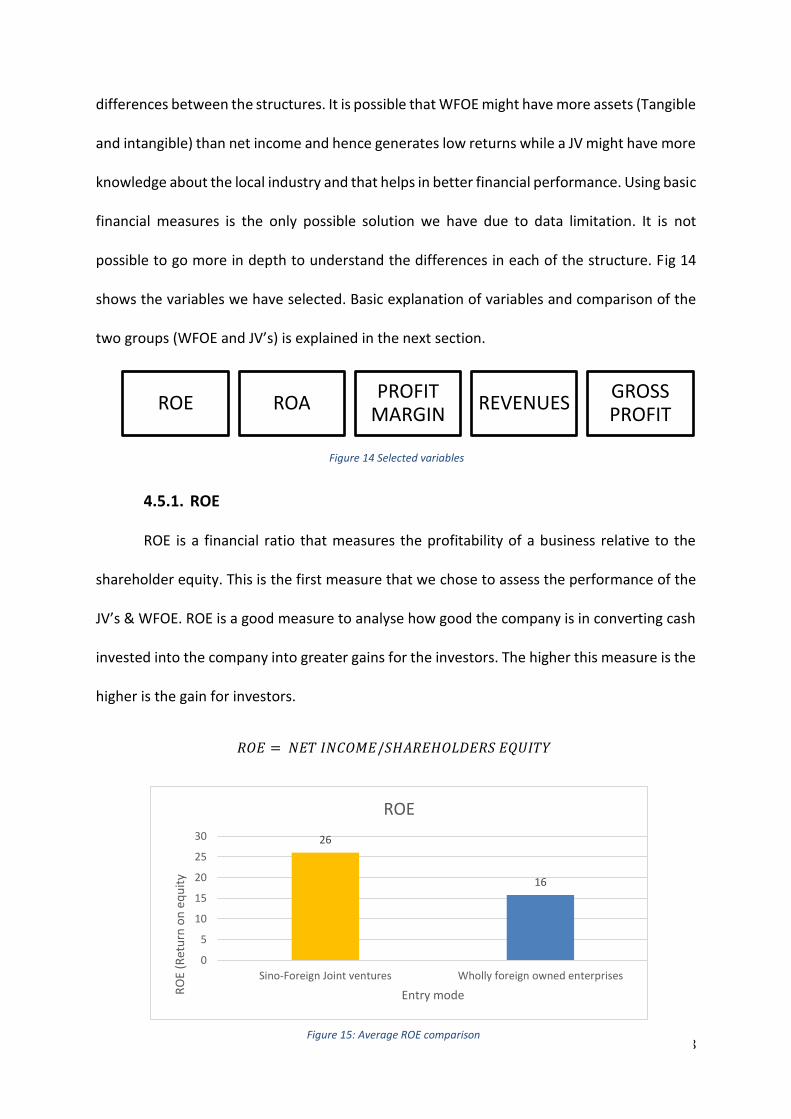

4.5. Selection of Variables ............................................................................................................ 47

4.5.1. ROE ................................................................................................................................ 48

4.5.2. ROA ............................................................................................................................... 49

4.5.3. Profit margin ................................................................................................................. 49

4.5.4. Operating Revenue/Turnover ....................................................................................... 50

4.5.5. Gross Profit ................................................................................................................... 51

4.6. Summary of the above .......................................................................................................... 51

5. Results ....................................................................................................................................... 53

5.1. ROE .................................................................................................................................... 53

5.2. ROA ................................................................................................................................... 54

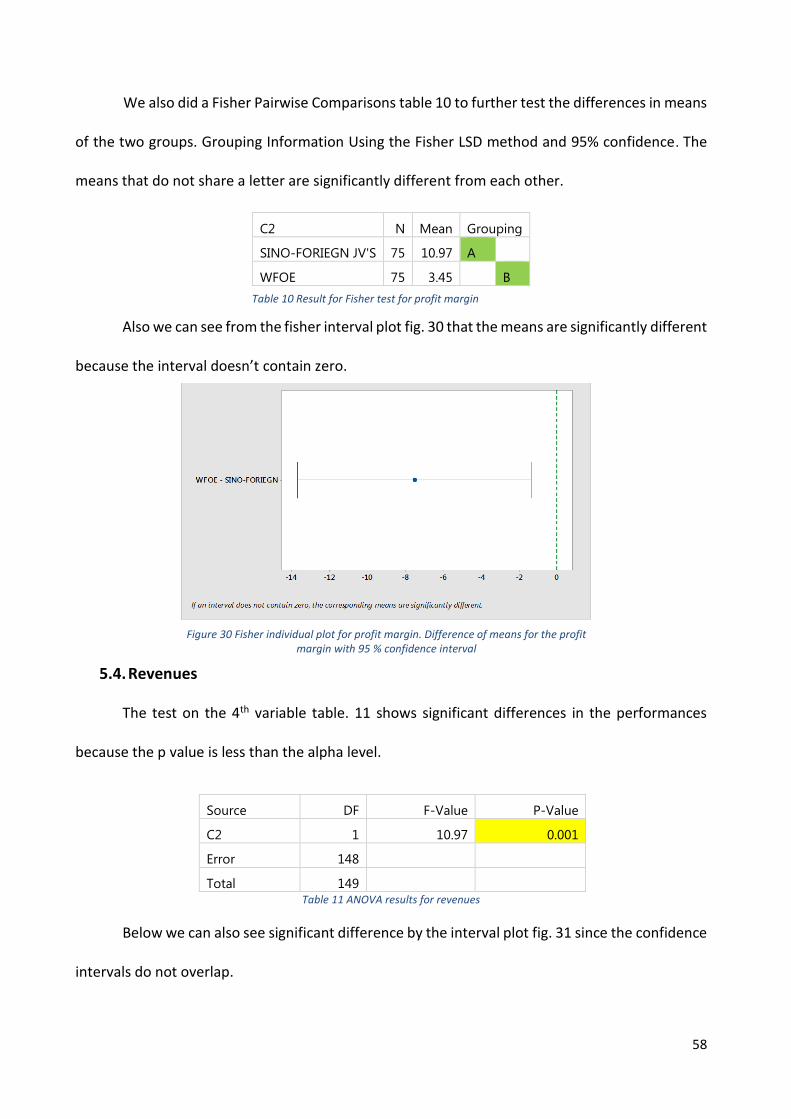

5.3. Profit Margin ..................................................................................................................... 56

Page 6

6

5.4. Revenues ........................................................................................................................... 58

5.5. Gross Profit ....................................................................................................................... 60

6. DISCUSSION AND CONCLUSIONS .............................................................................................. 63

APPENDIX .............................................................................................................................................. 66

REFERENCES .......................................................................................................................................... 69

Page 7

7

Table of Figures Figure 1 Dunning, 1993: Dunning & Lundan, 2008 ............................................................................... 12

Figure 2 Anderson & Gatigon (1986)'s transaction cost propositions .................................................. 16

Figure 3 Exposure of modes of entry to different types of risk ............................................................ 18

Figure 4 Resource based theory model of SCA. .................................................................................... 23

Figure 5 Identification of resources and capabilities. ........................................................................... 25

Figure 6: China FDI’s .............................................................................................................................. 32

Figure 7: China R&D expenditure %age ................................................................................................ 33

Figure 8 Contracted FDI inflows to China by registration type, 1992-1999 (in 100 million USD) ........ 37

Figure 9 Utilized FDI inflows to China by registration type, 1997-2006 (in 100 million USD) .............. 37

Figure 10 Market Value & Forecast for Chinese pharmaceutical industry overall ............................... 40

Figure 11 Sales of generics drugs in China ............................................................................................ 41

Figure 12: Sales of Patented drugs in China ......................................................................................... 42

Figure 13: R&D expenditures in pharma ............................................................................................... 43

Figure 14 Selected variables ................................................................................................................. 48

Figure 15: Average ROE comparison ..................................................................................................... 48

Figure 16 Average ROA comparison ..................................................................................................... 49

Figure 17 Average Profit Margin Comparison ...................................................................................... 50

Figure 18 Average Operating Revenues Comparison ........................................................................... 50

Figure 19 Average Gross Profit Comparison ......................................................................................... 51

Figure 20 Interval plot for ROE ............................................................................................................. 53

Figure 21 Box plot of ROE values ......................................................................................................... 53

Figure 22 Interval plot for ROA ............................................................................................................. 54

Figure 23 Boxplot for ROA .................................................................................................................... 55

Figure 24 Normal probability plot for ROA ........................................................................................... 55

Figure 25 Test for equal variance for ROA: Factors vs Dependent variable. Multiple comparison

interval for the std. Deviation, Alpha = 0.05 ......................................................................................... 56

Figure 26 Interval plot for Profit Margin ............................................................................................... 56

Figure 27 Box plot for Profit Margin ..................................................................................................... 56

Figure 28 Normal probability plot for Profit Margin ............................................................................. 57

Figure 29 Test for equal variances for profit margin: Factors vs Dependent variable. Multiple

comparison interval for the std. Deviation, Alpha = 0.05 ..................................................................... 57

Figure 30 Fisher individual plot for profit margin. Difference of means for the profit margin with 95 %

confidence interval ............................................................................................................................... 58

Figure 31 Interval Plot for revenues ..................................................................................................... 59

Figure 32 Normal probability plot for Revenues .................................................................................. 59

Figure 33 Test for equal variances for Revenues: Factors vs Dependent variable. Multiple comparison

interval for the std. Deviation, Alpha = 0.05 ......................................................................................... 59

Figure 34 Fisher individual plot for Revenues. Difference of means for the profit margin with 95 %

confidence interval ............................................................................................................................... 60

Figure 35 Interval Plot for gross profit .................................................................................................. 60

Figure 36 Test for equal variances for gross profit: Factors vs Dependent variable. Multiple

comparison interval for the std. Deviation, Alpha = 0.05 ..................................................................... 61

Figure 37 Fisher individual plot for Revenues. Difference of means for the gross profit with 95 %

confidence interval ............................................................................................................................... 61

Page 8

8

List of Tables

Table 1 Summary of data sorting .......................................................................................................... 45

Table 2: ANOVA results for ROE ........................................................................................................... 53

Table 3 ANOVA results for ROE ............................................................................................................. 54

Table 4 Comparison of means for ROA. Pooled StDev = 12.6233 ........................................................ 54

Table 5 Comparison of Std. Dev for ROA .............................................................................................. 56

Table 6 Results for Levene test for ROA ............................................................................................... 56

Table 7 ANOVA results for profit margin .............................................................................................. 56

Table 8 Comparison of mean for profit margin .................................................................................... 57

Table 9 Results for Levenes test for profit margin ................................................................................ 57

Table 10 Result for Fisher test for profit margin .................................................................................. 58

Table 11 ANOVA results for revenues................................................................................................... 58

Table 12 Comparison of Means for revenues ....................................................................................... 59

Table 13 Results for Levenes test for revenues .................................................................................... 59

Table 14 Results for fishers test for revenues ...................................................................................... 60

Table 15 ANOVA results for Gross profit .............................................................................................. 60

Table 16 Results for Levenes test for Gross Profit ................................................................................ 61

Table 17 Comparison of Means ............................................................................................................ 61

Table 18 Results for fisher test for gross profit .................................................................................... 61

Table 19 Summary of the results .......................................................................................................... 62

Table 20 Stata Results for Operating Revenues .................................................................................... 66

Table 21 Stata ANOVA Results for Operating Revenues ....................................................................... 66

Table 22 Stata Results for ROE .............................................................................................................. 66

Table 23 Stata ANOVA Results for ROE ................................................................................................. 66

Table 24 Stata results for ROA .............................................................................................................. 66

Table 25 Stata ANOVA Results for ROA ................................................................................................ 67

Table 26 Stata results for Profit Margin ................................................................................................ 67

Table 27 Stata ANOVA Results for Profit Margin .................................................................................. 67

Table 28 Stata results for Gross Profit .................................................................................................. 67

Table 29 Stata ANOVA Results for Gross Profit .................................................................................... 67

Table 30 Summary of stata results ....................................................................................................... 68

Page 9

9

1. Executive summary

China is the world's second largest pharmaceutical market after the US and also is the

largest exporter of Pharmaceutical ingredients and preparations. Since it is also the most

populated country in the world and it has a high rate of ageing population, the healthcare

industry is one of the most important in China. This is also the key focus of the Chinese

government, which has launched several reforms in this sector over the years. Due to the

importance of this industry, many multinational firms have been looking to gain access to the

vast pharmaceutical market of China and for this reason they have to face many economic

decisions in order to enter the market. The question that needs to be answered is: what are

the factors that make Chinese pharmaceuticals so much competitive in the world? It is

important to trace back to 1980’s when China started to open its economy and allowed

foreign firms to enter the market but with forced joint ventures. However, later in 2001, China

entered the WTO and allowed firms to enter with wholly foreign owned subsidiaries. Is the

strategy of forced joint ventures adopted by China during the early stage of opening its

economy, the main reason why Chinese market has been so successful in becoming the

largest producer of pharmaceuticals in the world? In order to answer this question we have

focused on the data for 2013 for several firms in China and see the effects of ownership on

the performance of pharmaceutical companies, in order to understand whether significant

differences exist.

We begin our work by reviewing Dunning’s theory on the reasons why companies

chose to invest abroad. The primary reasons can be classified into four groups. Firstly,

companies invest abroad in search of markets to increase their sales or competitive position

known as “Market Seeking FDI”. Secondly, we have “Efficiency Seeking” FDI where companies

Page 10

10

invest abroad to exploit economies of scale & scope as well as risk diversification. “Resource

Seeking” FDI is undertaken to access resources in a locations which can generate better

profitability for the companies. Lastly, “Strategic Asset Seeking” FDI is undertaken to attain a

long term competitive advantage.

After that, we focus our attention on theories that describe the firm’s choice of

operation mode beginning with Transaction Cost Economics (TCE). According to TCE, firms

incur transaction costs when they operate using market mechanisms due to market

imperfections such as incomplete contracts, bounded reliability, and opportunism.

Eventually, the firm’s decision on where to define the organizational boundaries in order to

reduction the transaction costs would depend on internal and external uncertainty

surrounding the transactions, on the asset specificity of the transactions and their frequency.

The Eclectic theory suggests that firms invest abroad when they believe they are going

to exploit their ownership advantages, which refer to asset advantages and minimization of

transaction costs, location advantages, referring to resource availability, and finally

internalization advantages, referring to reduction of transaction & co-ordination costs. When

a firm’s Ownership advantage refers to a large firm size, companies can afford more easily to

choose to operate as a WFOE whereas; when it refers to the firm’s international experience,

firms chose Joint Ventures when it is low and vice versa. As regards the Location advantages,

firms tend to prefer WFOE when the host country market size is big enough to exploit

economies of scale, while when the host country is risky or culturally distant, firms prefer

Joint Venture. Internalization advantages may refer to contractual risk, which, when high,

may lead to firms operating as a WFOE.

Page 11

11

The Resource Based Theory views firms as a bundle of resources which are either

valuable, rare, inimitable or non-substitutable. When a firm expands its operations abroad it

does so only in a location where the value attained from these resources remains intact thus

enabling the firm to retain its competitive advantage and will also chose between market

transactions or a higher control mode for its operation likewise.

Finally, the institutional theory says that in order to attain legitimacy, organizations

adopt structures that are isomorphic to other organization and divides isomorphic pressures

into normative, cognitive & regulative pressures. When the regulatory conditions in a host

country are not welcoming, firms prefer Joint Ventures. Similarly, as per normative pressures

if the host country is very different in terms of culture and values, firms would prefer to

operate as Joint Ventures. As per cognitive pressures, firms would most likely chose a mode

of operation similar to the one chosen already in the past by other competitor firms.

Therefore, considering the theories mentioned above we conduct an empirical

analysis to determine whether foreign companies financially perform better as Joint Venture

with a local partner or as WFOE in the pharmaceutical industry in China. Our empirical analysis

shows significant difference in the performance of Sino-foreign JVS’ and WFOE’s and also

shows that JV’s are performing considerably better than the WFOE when tested with different

financial variables. Our thesis thus develops a firm conclusion that future foreign firms trying

to enter the pharmaceutical market in China must look for a Sino-Foreign joint venture in

order to guarantee optimum financial performance and also concludes the fact that the

forced joint venture strategy of China has had no negative impact on the performance of

foreign firm in this specific sector, instead it has been favourable for the foreign firms.

Page 12

12

2. Theoretical framework

In this section we present a detailed overview of the work already done on the topic

related to foreign direct investments, firm’s behaviour related to the choice of entry mode

and the theories that focus on economics of multinational enterprises.

2.1. Sources

We performed a thorough and thoughtful research by reading different academic

papers involving past studies on the topic, published in journals and key insights, taken from

them, are used to develop better conclusion of our research work. Articles published in

journals have also been considered mainly due to the need of information regarding Chinese

pharmaceutical market and Chinese market in general. There have also been some

complexities in doing the research, which involves the study of entry modes in China and

understanding the basic market dynamics due to the lack of information available about entry

modes.

The key words that we employed for our research were: Sino-Foreign Joint ventures, Wholly

foreign owned enterprises, Entry modes and performance, control and performance of

multinational firms.

2.2. Motives for FDI

There are several reasons why companies chose to invest abroad. Their motives can

be classified as the following:

Market Seeking

Resource Seeking

Efficiency Seeking

Strategic asset

Seeking

Figure 1 Dunning, 1993: Dunning & Lundan, 2008

Page 13

13

2.2.1. Market Seeking

This approach is used by firms when they want to provide goods and services in a

foreign market by being locally present there instead of exporting (Nachum & Zaheer, 2005;

Brouthers, Gao & McNicol, 2008). It enables a firm to increase its sales in a target market

(MacCarthy & Atthirawong, 2003) and protect its competitive position (Dunning, 1993). When

a firm’s customers or suppliers relocate to a foreign market, the firm follows them by market

seeking FDI.

On the other hand, they may also make market seeking FDI in markets or locations

which are unique and the firm has an opportunity to adapt to the local needs (Dunning &

Lundan, 2008). Market seeking FDI is also justified by lower production and transaction costs,

which allows firms to stay competitive (Dunning and Lundan, 2008). Further factors include

the GDP growth, GDP per capita and the market size of the target market (Kudina and

Jakubiak, 2008)

2.2.2. Efficiency seeking

The main benefits of efficiency seeking FDI is to attain economies of scale and

economies of scope along with risk diversification (Robson, 1993 and Dunning and Lundan,

2008). Another aspect relates to attaining efficiency by assigning labour intensive activities to

developing countries and assigning value added activities to developed countries with more

relevant resources (Kim, et al., 1993; Dunning & Lundan, 2008).

Page 14

14

2.2.3. Resource seeking

Firms mainly seek two types of resources in the target country. They may seek physical

resources like precious minerals or metals available at a lower cost whereas the other reason

may be to seek cheap labour. Therefore the main objective of resource seeking FDI is to incur

lower costs and increase profits (Dunning & Lundan, 2008).

2.2.4. Strategic Asset Seeking

Strategic asset seeking FDI is carried out by firms to achieve long term competitive

advantage over its competitors (Dunning and Lundan, 2008). Firms may specifically seek

technology, marketing and management expertise in the foreign market (Makino, 2002).

These not only ensure that the firms gain competitiveness and ownership advantages but also

ensures that they do so before their competitors (Dunning and Lundan, 2008 and Dunning,

1993)

Following are the theories that discuss the choice of entry mode and operation for foreign

companies:

2.3. Theories related to entry modes

2.3.1. Transaction Cost Economics

Transaction cost economics is the most widely used theoretical framework to

understand the choice between various organizational forms as it discusses the way firms

organize their transactions with other firms and so eventually at what point do they draw

organizational boundaries.

Transaction costs are costs that occur when goods and services are provided through

the market rather than through a firm and are a result of market imperfections. They can be

Page 15

15

direct or indirect costs. The direct costs would refer to the ‘costs of negotiating and concluding

a separate contract for each transaction’ and ‘discovering what the relevant prices are’

(Coase, 1937). Indirect costs refers to the opportunity costs of a suboptimal factor allocation.

In addition it was argued that transaction costs occur also due to opportunistic

behaviours by the market participants and due to “bounded rationality” (Oliver Williamson

1975, 1985; Simon, 1956). Business partners may be expected to behave opportunistically,

which is why comprehensive contracts should be enforced but this is not possible to

implement as “bounded rationality” limits the completeness of the contracts resulting in

market inefficiencies.

According to Williamson transaction costs are especially relevant to transactions

which involve uncertainty, low frequency and asset specificity. Uncertainty occurs when it is

difficult to predict the performance of a business partner or when the events involving an

exchange cannot be predicted to be included in the contract. Transaction frequency refers to

how frequently the exchanges occur whereas asset specificity relates to the investments

made which are particular to a transaction and cannot be deployed elsewhere in the future

(Klein, Crawford and Alchian, 1978).

The internalization theory is based on the same logic as Transaction cost economics

and explains that multinational enterprises prefer to have their own subsidiaries in foreign

countries due to the costs and benefits arising from it. Along with other factors, it also focuses

on information asymmetries as a market imperfection. According to this, non-specificity of

knowledge transfer cause market inefficiency as the other party may use knowledge, which

is not protected by property rights for its own benefit (Buckley and Casson, 1976)

Page 16

16

Another recent advancement to the theory argues that “bounded reliability” is more

appropriate than opportunism in Williamson’s framework as opportunistic behaviour only

occurs ex post (Alain Verbeke and Nathan Greidanus’, 2009) and therefore cannot be a

determinant of entry choice and instead it is the anticipation of such behaviours along with a

lack of trust (Casson, 1995).

2.3.2. Transaction cost economics in case of Foreign Expansion

Transaction costs become even more relevant when firms expand their business

abroad incurring large cultural, geographic, economic and administrative differences. In

order to apply this theory to joint ventures, Anderson and Gatignon (1986) use Williamson’s

framework to explain the determinants of a firm’s high control (wholly owned subsidiary) vs

a low control (non-exclusive, non-restrictive contracts) vs intermediate control (joint

ventures) entry mode preference. These are summarized in the table below:

Figure 2 Anderson & Gatigon (1986)'s transaction cost propositions

Page 17

17

Several empirical studies have been done based on Transaction Cost Economics

constructs including asset specificity, internal uncertainty and external uncertainty to

demonstrate which mode of entry or organizational form is suitable under what conditions.

a. Asset Specificity

The most common proxy to this is the ratio of R&D to total sales or advertising

expenditure to total sales. (Hennart and Larimo, 1998). The results however have been

varying. Some studies suggest a high level of R&D investment to be related to Wholly Owned

subsidiary as a preferred organizational form. (Gatignon and Anderson, 1988; Padmanabhan

and Cho, 1996; Delios and Beamish, 1999; Makino and Neupert, 2000; Hennart and Larimo,

1998; Chen and Hu, 2002; Dikova and Witteloostuijn, 2007). Some studies find insignificant

relationships (Gomes-Casseres 1989, 1990, Hennart ,1991, Taylor et al. 1998, Meyer 2001,

Brouthers, 2002 and Chen and Hennart, 2002) and one of the studies suggests that high level

of R&D is positively associated with Joint Ventures (Palenzuela and Bobillo , 1999). As for a

high advertising intensity, some studies suggest positive relationship to WFOE (Gatignon and

Anderson 1988, and Gomes-Casseres; 1989, 1990) whereas some find no relation (Kogut and

Singh 1988, Hennart 1991 and Chen and Hu, 2002)

a. Several other studies used survey-based measure and found better conclusions. One

study suggests that when the level of tacit knowledge is high, firms prefer WFOE (Kim

and Hwang 1992). Another study finds that asset specificity is correlated to the choice

of WFOE especially in the manufacturing and service firms (Brouthers et al. 2003 and

Brouthers and Brouthers, 2003).

Page 18

18

b. External Uncertainty

The majority of studies that focused on this aspect have considered the relation

between country risk and the entry mode choice. Country risk includes risk associated with

social, political, economic stability, risk associated with nationalization policy of governments

or the risk of converting profits (Brouthers and Brouthers, 2003). It may also be associated

with perceived volatility and diversity of a transaction (Klein et al., 1990). According to a few

studies, a high country risk leads to preference of WFOE (Gatignon and Anderson 1988 and

Agarwal 1994) whereas the majority of other studies conclude the opposite (Klein et al. 1990,

Brouthers 2002, Brouthers and Brouthers 2003, Quer et al. 2007). Some studies also found

no co-relation between the two (Erramilli and Rao, 1993).

Figure 3 Exposure of modes of entry to different types of risk

Page 19

19

c. Internal Uncertainty

Internal uncertainty is caused by opportunistic behaviour and limitations due to

bounded reliability. The most commonly used measures to determine entry choices are

international experience and cultural differences (Hennart, 1991). Few studies suggest a

positive relationship between a high cultural distance and Joint Ventures as an entry mode.

(Gatignon and Anderson, 1988; Erramilli and Rao, 1993; Agarwal, 1994; Hennart and Larimo,

1998; Quer et al., 2007) whereas some suggest the opposite (Chang, Kao, Kuo and Chiu, 2012

and Lopez-Duarte and Vidal-Suarez, 2013).

As for the international experience, some studies suggest positive relationship

between a high level of international experience and WFOE (Agarwal and Ramaswami 1992,

Chu and Anderson 1992, Contractor and Kundu 1998 and Kuo et al., 2012) whereas a few

suggest the opposite (Erramilli, 1991 & Chiao et al., 2010) and some do not find any relation

(Kogut and Singh 1988, Agarwal 1994 & Padmanabhan and Cho, 1996)

2.3.3. Eclectic Theory

The Eclectic Theory was developed by a British Economist Dunning (1977, 1979, and

1988) where he not only built upon the Transaction Cost Economics theory but also added

Location and Ownership advantages to it. The theory addresses the gaps left by other works

on the same topic and defines a solid framework which can explain well the FDI related

decisions of various firms (Zhao & Decker, 2004; Goodnow, 1985). In Dunning’s own word,

the objective was to “offer a holistic framework by which it was possible to identify and

evaluate the significant factors influencing both the initial act of foreign production by

enterprises and the growth of such production” (Dunning, 1988). The theory suggests that a

firm would engage in FDI if it has at least three advantages that includes the ownership (asset

Page 20

20

advantage and minimization of transaction costs), location (resource availability in a specific

location) and internalization (reduction of transaction & co-ordination costs) advantages.

Below we highlight what each of these advantages mean and then we illustrate how they

would relate to the operation mode choice (WFOE or JV) of foreign firms.

2.3.3.1. Ownership Advantages

This suggests that firms must possess some kind of comparative advantage in their

target market in order to expand their operations to a foreign country (Dunning, 1981;

Tolentino, 2001). They can be described as “any kind of income generating assets, which make

it possible for firms to engage in foreign production” (Dunning, 1991). These ownership

advantages can be divided into two types: asset advantages and transaction cost minimizing

advantages. Asset advantages include technology specific to the firm, manpower, knowledge,

patents, product differentiation achieved through branding etc (Tan & Vertinsky, 1996;

Dunning, 1980). On the other hand transaction cost minimizing advantages relate to product

diversity, firm size, learning experience & synergies in production, purchasing, marketing,

R&D, finance etc. (Dunning, 2000). The following ownership specific advantages can explain

firms’ operation mode choice:

• Firm Size

In order to expand operations in a foreign country, a firm needs a large amount of

capital and resources to pay for the high fixed and variable costs in the foreign country (Talay

and Cavusgil 2008). A large firm size is therefore necessary to absorb that cost (Buckley and

Casson 1998). Empirical studies show that a large firm size is positively related to selecting

WFOE as the operation mode choice (e.g., Talay & Cavusgil, 2008; Dadzie, 2012). However it

Page 21

21

can be predicted that some firms might not be able to do so due to restrictive nature of the

market.

• Firm’s international experience

A firm can incur several risks and uncertainties translating into high costs when

expanding its operations abroad. This can be a real threat for some of the firms (Agarwal and

Ramaswami, 1992). However, for firms that already have experience, these might be less

significant (Buckley and Casson, 1985). Therefore, for such firms, the requirement for having

a local partner reduces, meaning they will be less likely to choose Joint venture or other

alliances as an operation mode (Erramilli, 1991). Studies also show that firms with high level

of international experience are inclined towards Wholly Foreign Owned Subsidiaries as their

mode of operation (e.g., Dikova & Willeloosuijn, 2007; Lee & Sukoco, 2010; Dadzie, 2012).

2.3.3.2. Location Advantages

Location specific advantages relate to the advantages a firm may have in carrying out

its operations in one particular location over another. When firms go abroad, they should

chose attractive markets where they can gain better profits. These advantages can be related

to the economic, legal, political, cultural environment resulting in lesser costs and higher

revenues for a firm in that location (Dunning, 1988). The advantages specifically include the

market potential in terms of size and growth, endowment factors, supply sources, logistics

costs, physical distance, trade barriers etc. (Caves 1996; Caves & Pugel, 1982). The following

ownership specific advantages can explain firms’ operation mode choice:

Page 22

22

• Market Size

A large market size means a firm has more potential for obtaining economies of scale

and earning higher profits (Wheeler and Moody, 1992). Studies show that firm prefer to

operate as a WFOE in large markets since they are able to establish market presence as well

as exploit economies of scale (e.g., Chung & Enderwick, 2001; Nakos & Brouthers, 2002).

• Host country risk

This refers to risk related directly to the economic and political environment in a country

(Agarwal and Ramaswami, 1992 and Dadzie, 2012). A host country with a risky economic and

political environment may not offer stable conditions for continued profit generation of a

foreign company due to which foreign companies may hesitate to operate solely without a

local partner (Kim and Hwag 1992). Studies subsequently show low level of commitment by

firms in countries with high risks (e.g., Brouthers & Brouthers, 2000; Tahir & Larimo, 2006).

• Cultural distance

This refers to variations in values and belief system of the host country and the home

country of the firm (Chen and Hu, 2002). High cultural distance relates directly to increased

transaction costs for the firm (Puck, Holtbrügge and Mohr, 2009) as well as difficulties in

managing operations abroad (Jung, 2004). Studies therefore show that firms do not prefer to

operate as WFOE in case of a high cultural difference (Yiu & Makino, 2002). In contrast to this,

some studies reveal that in fact firms prefer to operate as WFOE in case of a high cultural

difference (Padmanabhan & Cho, 1996)

Page 23

23

2.3.3.3. Internalization Advantages

In order to exploit the ownership advantages in a foreign country whenever the costs

of using markets are more than the costs of producing internally, firms would prefer to

internalize their operations within the firm (Dunning & Kundu, 1995). Therefore

internalization advantages suggest that whenever there are risks or uncertainty related to

buyers, suppliers, government policies, the production quality & standards need to be

protected, high level of control needs to be exercised then it is preferable for firms carry out

all activities within the firm hierarchy rather than involving other modes of operation

(Dunning, 1993 & Dadzie, 2012) .The following ownership specific advantages can explain

firms’ operation mode choice:

• Contractual Risk

This refers to the costs incurred in writing and enforcing contracts, lack of licensed

protection, patents, risks of transferring specific knowledge etc. (Dadzie, 2012). Therefore in

order to avoid contractual risk, firms internalize their operations incurring no transaction

costs, preventing unwanted spread of knowledge, avoiding costs of ensuring property rights

and controlling quality (Dunning, 1993). It is crucial for firms investing abroad to protect their

knowledge (Hill, Hwang & Kim, 1990). However, in case it is costly to protect knowledge, a

lack of doing so may cause a firm to prefer WFOE as a mode of operation (Dadzie, 2012)

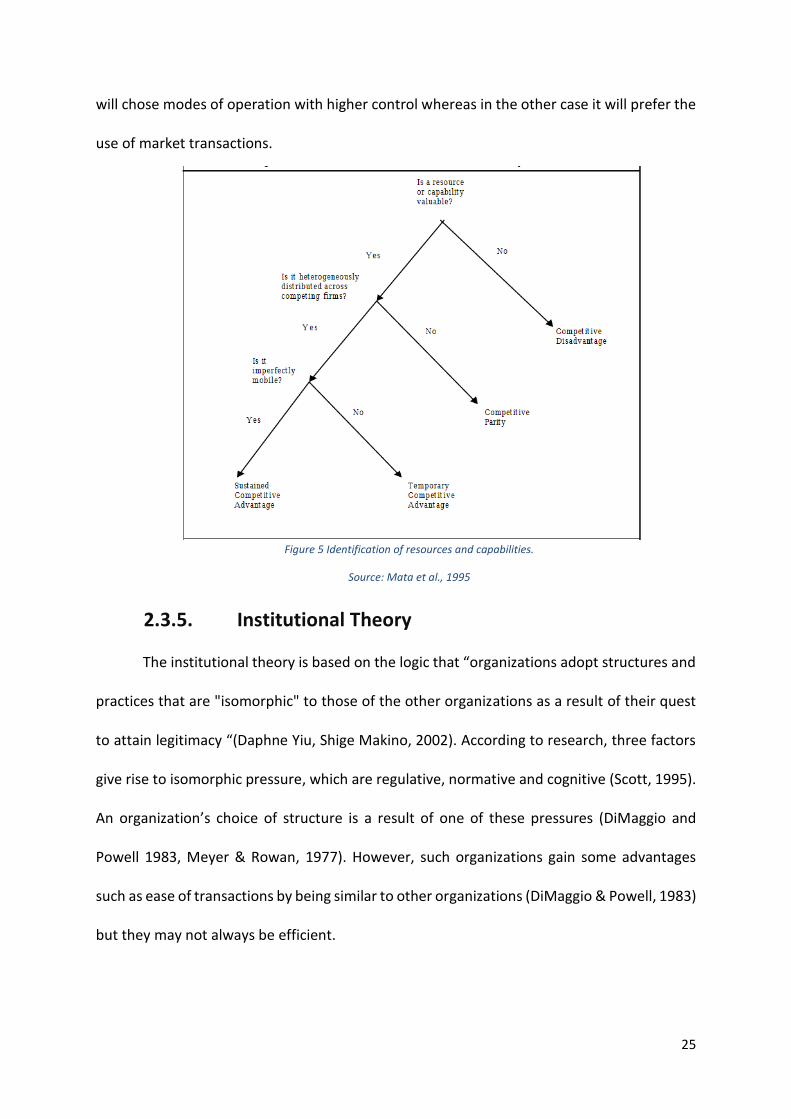

2.3.4. Resource Based Theory

Figure 4 Resource based theory model of SCA.

Source: Barney & Clark (2007, p. 69)

Page 24

24

This theory looks at the firm as a bundle of resources (Kor & Mahoney, 2004). The

resource based view offers an “inside-out” view on reasons why firms are successful or

unsuccessful without considering the external market conditions (Dicksen, 1996). It illustrates

how a firm’s resources are linked to attaining a sustainable competitive advantage over its

competitors and can be considered as an alternative to Transaction Cost Economics to explain

firm integration (Kogut & Zander, 1993). According to resource based view, a firm’s

performance and growth is determined by the kind of resources it has (Kogut & Zander, 1993).

Resources may be classified into organizational, human and physical resources

(Barney, 1991; Amit and Shoemaker, 1993). According to the theory, in order to establish and

maintain competitive advantage, a firm must possess resources which are either valuable,

rare, inimitable or non-substitutable (Barney, 1991). Valuable resources are those which

enable a firm to exploit opportunities in the market or reduce threats thereby adding strategic

value to the firm. Rare resources are the resources that the competitors cannot easily find.

Inimitable means that the resource cannot be copied easily by any competitor. Non-

substitutable refers to resources that cannot be substituted so a competitor cannot use a

substitute and attain the same advantage.

The resource based view examines firms’ choice of operation mode using the main

aspects surrounding the transfer of competitive advantage to the foreign market (Sharma and

Erramilli, 2004). It considers the probability that the firm will be able to establish its

competitive advantages and transfer it to production and marketing operations in the host

country. The framework focuses on transferring of resources to the foreign market while

keeping their value intact (Sharma and Erramilli, 2004) and therefore firms will chose

locations where this is attainable. If the firm cannot do so effectively and efficiently, then it

Page 25

25

will chose modes of operation with higher control whereas in the other case it will prefer the

use of market transactions.

2.3.5. Institutional Theory

The institutional theory is based on the logic that “organizations adopt structures and

practices that are "isomorphic" to those of the other organizations as a result of their quest

to attain legitimacy “(Daphne Yiu, Shige Makino, 2002). According to research, three factors

give rise to isomorphic pressure, which are regulative, normative and cognitive (Scott, 1995).

An organization’s choice of structure is a result of one of these pressures (DiMaggio and

Powell 1983, Meyer & Rowan, 1977). However, such organizations gain some advantages

such as ease of transactions by being similar to other organizations (DiMaggio & Powell, 1983)

but they may not always be efficient.

Figure 5 Identification of resources and capabilities.

Source: Mata et al., 1995

Page 26

26

We highlight below each of the factors that lead to isomorphic pressure and examine

how they affect an organization’s mode of operation.

• Regulatory Institutions

Regulative elements refer to rules and laws in a particular society that determine

stability and lay the foundations for organization and industry action (North 1990, Scott and

Meyer 1994; Williamson 1975, 1991). Often times, foreign countries experience more

institutional pressure from the governments in the host country (Poynter, 1985). Therefore

gaining legitimacy in the market is one the primary target for foreign companies. Studies

show that in such scenarios it may be necessary for companies to operate as Joint Ventures

with local partners (Beamish, 1985; Makino & Delios, 1996; Shan & Hamilton, 1991). If the

regulatory conditions of a host country are not very welcoming for foreign firms, they form

joint ventures in order to reduce the liability of foreignness. Moreover forming joint ventures

allows foreign firm to learn about the government policies and infrastructure from their local

partners. Studies also show that firms decide to operate as joint ventures when the host

government maintains a restrictive environment (Contractor, 1990; Fagre & Wells 1982,

Gomes-Casseres, 1990; Lecraw, 1984).

• Normative Institutions

A firms must also take into account the social norms and acceptable economic

behaviours (Zukin & DiMaggio, 1990). Normative institutions refer to understanding of “logic

of appropriateness” (March, 1981) which includes the culture, social customs, norms & values

of the host country. A foreign company is more likely to experience social difficulties in a host

country compared to its local peers (Kostova & Zaheer, 1999). Many failures in the past can

be attributed to normative factors such as Matsushita and MCA (Music Corporation of

Page 27

27

America) merger (McGarvey, 1997). It is thus important for foreign firms to meet social

expectations to survive in the host country (D'Aunno et al. 1991; DiMaggio and Powell, 1991).

This however is not simple to achieve as cultural distance poses a significant hindrance. High

cultural difference means that it will be more difficult for the foreign company to understand

the host country environment. Another factor to overcome can be cultural ethnocentricity. If

the host country has an ethnocentric culture then it can be hard for foreign firms to adjust. If

foreign firms form Joint Venture with local firms having a good social reputation, these

barriers can be overcome and firms can gain social capital (Coleman, 1988). Overall, Joint

Ventures can help companies avoid social problems and use their relationship with their

partners to their advantage by attaining social legitimacy, access to economic resources and

relevant business contacts. Studies also show that when cultural distance is large, foreign

firms choose Joint Ventures as their operation mode. (Agarwal 1994, Kogut & Singh, 1988).

• Cognitive Institutions

The mode of operation a firm chooses often depends on the cognitive mind-set of the

firm. According to studies, people categorize social events based on cognitive structures

(Markus & Zajonc, 1985). "Representativeness heurism," refers to instances where the one’s

decisions are based on their decisions related to similar events, which are stored in their

cognitive memory (Tversky & Kahneman, 1974). Such judgements transform into taken-for-

granted beliefs thereby causing decision makers to overlook other alternatives available

(DiMaggio & Powell 1991; Greenwood & Hinings, 1996). Firms may follow two ways to

achieve cognitive legitimacy:

Page 28

28

a) External Mimicry

This refers to when firms take decisions based on what other firms in the past have

done. Decisions regarding efficiency may also be taken by observing the performance of

other firms (Roberts & Greenwood, 1997). On the other hand, local constituents understand

new foreign firms by relating them to older firms and when they evaluate their legitimacy

they refer to legitimacy of other firms belonging to the same cognitive category (Kostova &

Zaheer, 1999). Thus foreign firms will choose a mode that is most common in the home

country already, as studies show that firms imitate other firms already present in the host

country based on how many firms are already operating in a certain mode and how

comparable they are to them in terms of size & status (Amburgey & Miner, 1992; Haunschild

& Miner, 1997; Haveman, 1993; Korn & Baum, 1999).

b) Internal Mimicry

This refers to when firms make decisions based on what they have been doing

themselves in the past. In a multinational enterprise, practices may be transferred often to

subsidiaries by the parent. So if a subsidiary is able to achieve a high level of legitimacy in one

country, the parent will transfer this into cognitive structure of the entire multinational

enterprise. Organizational inertia theory suggests that firms institutionalize activity patterns,

which eliminates the possibility of any changes (Romanelli & Tushman, 1986). Therefore, it

can be concluded that firms repeat what they have already done in the past successfully.

Page 29

29

2.4. Literature related to the performance measurement due to

ownership structure and control

We can now focus on the literature related to the effects of ownership and control on

the performance of firms entering into foreign countries. Not a lot of work has been done to

measure empirically the performance of these types of entry modes and which one is better,

since the availability of complete and reliable data is of paramount importance in this case.

A study done by Sea, Jaiho and Jon done in 2013 analysed the performance of IJV’s

and WFOE using data based on Chinese firms and discovered that there is a steady

improvement in the performance of converted wholly owned subsidiaries (once converted

from a joint venture to wholly owned subsidiary), as measured by ROA and Operating ROA,

which far exceeds that of continuing joint ventures. Their results suggest that the increase in

the performance due to the conversion is associated with the increased intangible and fixed

assets. This research proves the transaction cost theory, that firms perform better when the

go with a wholly owned subsidiary.

Another study worth mentioning here relates to the financial performance

measurement of Sino-foreign JV’s vs WFOE in China (Yadong Luo and Min Chen, 1995). The

findings suggest that the JV’s perform better than the WFOE in terms of gross margin ratio

while WFOE outperform JV’s in operating margin ratio which directs to the fact the WFOE

have higher costs of goods sold and lower level of operation and administrative costs, which

seconds the transaction cots theory. The fact is that it all depends on the company’s aims and

targets to enter the Chinese market. If the firm aims to have synergies between the assets

and risk reduction through globalization then WFOE is the best way to enter. Second, if the

Page 30

30

strategic objective of the investor entering the Chinese market is to pursue local market share,

the IJV is a better option than the WFOE (Yadong, Luo and Min Chen, 1995).

A study based on Japanese firms based on ownership structure of the firms found out

that there are significant differences between the performance of JV’s and WFOE. Study

showed that performance of WFOE tend to be better than JV’s (Woodcock, beamish &

makino, 1994). The study of Woodcock is based on measuring performance by using empirical

(financial) data of the firms and is not only based on theoretical data. The study of Woodcock

also supports the earlier work (Li and Guisinger, 1991) modes of entry, forms of foreign

ownership, and national culture are found to have effects on the failures and success of

foreign-controlled firms in the United States.

Study done by (Mario Henrique Ogasavara, Yasuo & Hoshino, 2004) is based on the

Japanese foreign subsidiaries in Brazil, counters the study done by Woodcock. The findings

suggest that Japanese–Japanese JV with a partner that has previous experience accumulated

in the local market performed better than WFOE and Traditional IJV. The reason for this

different result is because the study considers non-conventional form of joint ventures as

well.

It is difficult to find further literature measuring empirically the performance

differences of JV’s and WFOE due to lack of resources. So we conclude that more work is

needed to be done on this topic, hence we continue with our research to analyse the

performance differences based on the Chinese Pharmaceutical market.

Page 31

31

3. Introduction to China

In terms of Gross Domestic Product (GDP), China is the world’s second largest

economy after US with GDP amounting to $12.4 trillion in 2017 while GDP per capita was

$8,8361. Ever since economic reforms began in 1978, China has been the world’s fastest

growing economies while a major contributor to that growth has been related with export

and investment. China is the largest industrial producer and manufacturer and these

contribute to 40% of GDP. Due to reforms, China saw a major shift away from state owned

Enterprises and by 2013 they contributed only 45% to the industrial output compared to 80%

in 1978. From 1978 till 2008, the size of Chinese economy multiplied by 50 times with the

annual GDP growth rate at 10%. Initially reforms were focused on agriculture but then were

introduced in services and manufacturing as well.

China has been a member of the World Trade Organization (WTO) since 2001 and is

now the world’s largest trading power while maintaining its status as the main trade partner

for many countries. It is the world’s largest exporter and second largest importer whereas

Manufacturing, Agriculture and tele-communication are the largest industries in China.

The Chinese market can be characterized by high number of manufacturing companies

ranging from heavy-duty commodities such as steel to the most intricate electronics

manufacturing. There has been a growing trend towards research and development in new

sciences and technologies especially in the field of biological sciences. The market can be

characterized by a high influx of foreign investments in the field of R&D. China has maintained

the spot of the most cost effective (Low labour cost) manufacturing in the world since a long

1 (www.stats.gov.cn)

Page 32

32

Figure 6: China FDI’s

Source: Trading economics

time and has attracted a lot of companies across the world. However recently it has lost that

particular spot of low cost labour but still is attracting companies due the availability of

resources, good industrial infrastructure, networks, and a growing economy.

According to a report by China’s Administration for Industry and Commerce (AIC)

released on 14 January 2016, the number of companies in China are recorded to be

77,469,000 and it is expected to grow at an astonishing rate of 11.8% annually. Overall the

industrial production rose by 6.2%2 and the manufacturing economy rose by 6.5% in

December 20173. The trends are very convincing and shows a growing economy and market.

Foreign direct investment in China increased by 7.9 percent year-on-year in January to

December 2017.

The graph in figure 6 shows FDI increment in China for the year 2017 and the current

incremental trend in FDI’s of 2018. According to a recent survey by the world economic forum

the global competitiveness index (based on 12 different pillars ranging from health,

2,3 Trading Economics

Page 33

33

infrastructure and institutions etc.) for China came out to be 5 points out of 7 which confirms

the opportunities for doing good business in China.

It is important to emphasize the growing trend of the R&D in China and that is mainly

the reason a lot of big companies are still looking to shift to China even after it losing the place

for low labor cost. The R&D trend can be seen in the Figure 7. This shows a good commitment

of the Chinese government towards progressive research in future as well.

3.1. Main modes of operation for companies in China

a) Representative Office

A representative office is only meant to represent a foreign company in China for

carrying out activities related to business liaison, product/service introduction, market

research and other indirect business activities. It cannot possess its own capital and is thus

not really considered an independent legal entity.

Figure 7: China R&D expenditure %age

Source: Trading economics: Ministry of commerce of People Republic of China

Page 34

34

b) Branch Office

Only permitted for companies operating in a few sectors, it is also not considered an

independent legal entity in China and the foreign company is directly responsible for the

agreements made by the branch office.

c) State Owned Enterprises

According to the Organization for Economic Co-operation and Development (OECD),

State Owned Enterprises (SOEs) are enterprises where the state has significant control

through full, majority, or significant minority ownership. SOEs mainly operate in specific

sectors such as transport or telecommunications, which can be strategically important for the

government. According to China’s National Bureau of statistics, less than a third of Chinese

industrial output, fixed asset investment, and less than twenty per cent of Chinese real estate

investment is carried on by companies that are controlled by the state.

d) Foreign Invested Partnership Enterprise

It is relatively a new legal form of unlimited liability business entity in China referring

either to two or more than two individuals or foreign enterprises establishing a Partnership

Enterprise or it may refer to a foreign enterprise or individual establishing a Partnership

Enterprise with a Chinese individual or company. This form of entity can enter into contracts

with local and foreign businesses in China and generate revenues.

The structure allows foreign companies to obtain their own import licenses and

develop the sales structure thus making it easy for these companies to buy and export Chinese

products without going through any agent. These can be classified as a type of Wholly Foreign

Owned Enterprise due to similarities in their establishment processes, Legal status, structure

and registration. However, WFOE are fundamentally focused on manufacturing whereas

Page 35

35

while Foreign Invested Partnership Enterprises are established for trading and distributing

goods. Now we are going to focus our attention on Joint Ventures and Wholly Foreign Owned

Subsidiaries which are the main topic of our research.

e) Joint Ventures

Joint Ventures are a “distinct business units owned by 2 or more partner firms” (The

Beamish & Lupton- 2009) or it can be described as an alliance combining resources from more

than one organization to create a new organizational entity ('the child') which is different

from its parents (Inkpen & Beamish -1997). Park, S.H. and Ungson, G. (1997) writes that “an

IJV implies that a firm has to cooperate with a partner with a different cultural background”.

The drivers of international joint ventures are benefits arising from resource pooling, asset

protection, and risk hedging and immediate responses to changes in market. (Anderson and

Gatignon, 1986). Companies also chose Joint Ventures when the host government has

restrictive rules (Fagre &Wells, 1982). The partner commits to providing resources in

exchange for shared management, risks and rewards (Anderson and Gatignon, 1986). Foreign

firms choose to enter China as it is a big potential market for them and sales in China can help

them with their business in other counties. Often the reason also includes competitor

pressure on big multi nationals. Whereas the Chinese government encourages Joint ventures

in order to encourage foreign direct investment, increase jobs, efficiency and open export

opportunities for China. Spill overs from joint ventures include technology, knowledge and

skill transfer to domestic companies (Daniels, 1985).

Several other incentives like tax exemptions, low labour and production costs also

encouraged companies to form joint ventures in China. Introduction of laws favouring joint

Page 36

36

ventures (Child, 1994; Xu and Chew, 1995) and the formation of Special Economic Zones,

lowering transaction costs encouraged these (Tse, 1997).

f) Wholly Owned Foreign Enterprise

Up until 1997, Joint ventures were the most common entry mode for foreign

companies in China after which Wholly Owned Foreign Enterprises started gaining popularity

as an entry mode. A Wholly foreign owned enterprise can be defined as a firm in which 90 %

of ownership is with the foreign company (Luostarinen & Welch, 1990). While a WFOE enables

the firm owner to have more control and power, it also translates to a higher resource

commitment and leads to greater risk and less flexibility. (Hill, 1990). It is encouraged as an

entry mode when the companies going abroad already have such past experiences (Gatignon

& Anderson, 1988; Agarwal & Ramaswami, 1992) and the cultural difference between home

and the host country is not high (Anand & Delios, 1997) .

3.2. Reforms in China

China started receiving a large amount of FDI around 1992 and by 2006, China's FDI

in flows (69.5 billion USD) accounted for 18% of the total FDI flows to developing countries

(Heiwai Tang, 2008). During 1990s wholly foreign owned enterprises (WFOEs) were allowed

but not within special economic zones as per 1986 Law regarding WFOE. Therefore majority

of the FDI was in the form of Sino-foreign Joint Ventures (Cheung, 2007). The figure below

shows that more funds took the form of Joint Ventures till 1998 (for contracted FDI) & till

1999 (for utilized FDI).

Page 37

37

The explanation for Joint Ventures exceeding WFOE after FDI liberalization in 1997 lies

surely within several government policies that favoured Joint ventures over WFOE. According

to Yan and Warner (2002) “at the inception of economic reforms the Chinese government

Figure 8 Contracted FDI inflows to China by registration type, 1992-1999 (in 100 million USD)

Source: China statistical yearbook (Beijing, China statistics press)

Figure 9 Utilized FDI inflows to China by registration type, 1997-2006 (in 100 million USD)

Source: China statistical yearbook (Beijing, China statistics press)

Page 38

38

intentionally packaged EJVs with preferential privileges, while granting WFOEs virtually

nothing but regulations.

WFOE were restricted in specific important industries such as aerospace, nuclear

power generation, chemical, petrochemicals, pharmaceuticals, defense, medicine,

publications, communication, tourism, shipping etc.

Sino-foreign Joint ventures enjoyed tax exemptions as well as access to special

economic zones. They also could operate in sectors WFOE were not allowed to operate in.

There were several other reasons as well related to the governance and market dynamics due

to which foreign firms favored Joint Ventures.

One of these was the uncertain changes in laws and regulations which could only be

understood and dealt with by having a Chinese Partner who could also help with issues related

to procurement or regulatory problems caused due to a lack of Chinese state’s institutional

capacity.

Another factor was that relationships were of significant importance in establishing

a business in China. This is referred to as Guanxi and according to Clarke et al (2008, p. 407),

“discussion of Guanxi links not only relations among entrepreneurs but also relations

between entrepreneurs and government officials.” Therefore, local partners not only could

help understand the local customers better, make local connections in the government but

also enable access to distribution networks or marketing channels (Sutter, 2000).

From the point of view of local firms, they had very limited credit and also preferred

a foreign partner who could financially support them (Haggard and Huang, 2008).

Page 39

39

However in late 90s policies changed and FDI started increasing in the form of WFOE.

The Chinese constitution was changed in 1999 making the infrastructure more favorable for

WFOE. The most significant event was China’s accession into the World Trade Organization

in 2001. The world trade organization is the largest global organization with the goal to

ensure smooth and free trade among its member countries, which is ensured through several

different rules, negotiations and agreements. China officially joined the WTO in November

2001 after 15 years of negotiations, which started with its entry into General Agreement on

Tariff and Trade (GATT). China entered into very challenging negotiations with many other

member countries over several issues such as allowing foreign companies to operate in

sectors where it had competitive edge, the lowering of tariffs and the removal of barriers,

which were initially to protect its domestic industries. Eventually China had to agree to the

demands of other nations and change its economic structure. The Protocol on the Accession

of the People’s Republic of China is a document that contains details about the terms and

conditions China agreed to. Some of the most important amongst those were focused on

making the legal structure more transparent and creating a better infrastructure for foreign

direct investment including the removal of various restrictions, tariffs and other barriers on

FDI. China allowed foreign investors to establish Wholly Owned Foreign Subsidiaries in some

sectors meaning that they would not have to depend on a Chinese partner. For other sectors,

they still require a Chinese partner but can keep majority of the investment share. China

reduced or eliminated technical standards, quotas, import licensing and certification

requirements which allowed for better trade opportunities. According to a U.S. Government

Accounting Office China has “made a substantial number of important, specific commitments

in the rule-of-law-related areas of transparency, judicial review, uniform enforcement of legal

measures, and non-discrimination in its commercial policy” (Tang and Wei-, 2009).

Page 40

40

Figure 10 Market Value & Forecast for Chinese

pharmaceutical industry overall

Source: Deloitte report on Pharma in China

Therefore, after the accession of China in to the WTO many existing joint ventures

converted to wholly owned subsidiaries but many also remained as joint ventures. But More

recent studies, however, emphasize that joint venture termination should not be interpreted

as a failure but as an optimal adjustment in response to changing environmental or firm

specific conditions. According to this view, foreign firms are likely to enter new markets via

joint ventures because they confer an option to expand/divest under conditions of

uncertainty. As uncertainty resolves, foreign firms can either divest joint ventures by

exercising a put option or acquire them by exercising a call option (Kogut, 1991).

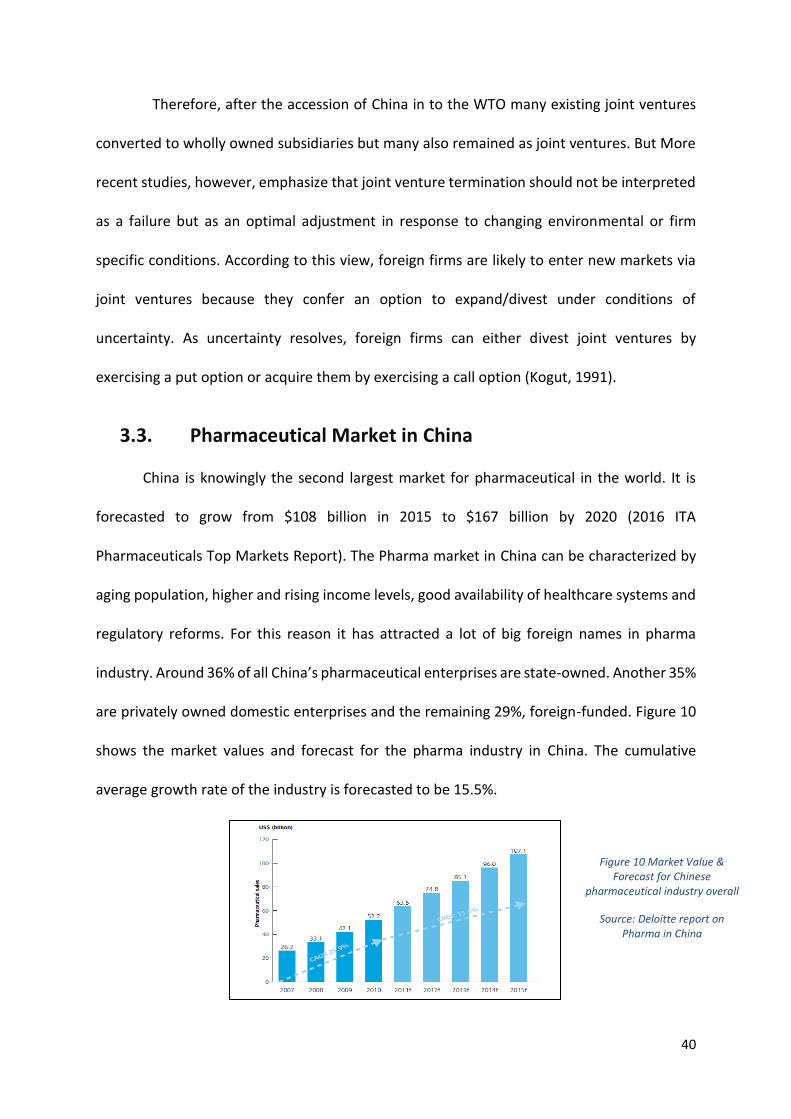

3.3. Pharmaceutical Market in China

China is knowingly the second largest market for pharmaceutical in the world. It is

forecasted to grow from $108 billion in 2015 to $167 billion by 2020 (2016 ITA

Pharmaceuticals Top Markets Report). The Pharma market in China can be characterized by

aging population, higher and rising income levels, good availability of healthcare systems and

regulatory reforms. For this reason it has attracted a lot of big foreign names in pharma

industry. Around 36% of all China’s pharmaceutical enterprises are state-owned. Another 35%

are privately owned domestic enterprises and the remaining 29%, foreign-funded. Figure 10

shows the market values and forecast for the pharma industry in China. The cumulative

average growth rate of the industry is forecasted to be 15.5%.

Page 41

41

GENERICS PATENTED OTC

The total public and private expenditure on healthcare is expected to rise from $640

billion in 2015 to $1.1 trillion in 2020.

3.3.1. Market Breakdown

The pharma industry in China can be divided into three different categories

a) Generics

Generics is defined as a copy of an ethical (prescription) drug formerly protected by

patents that have now expired. The generics mainly dominate the market with almost 85% of

share from the total sales of pharma in China, as can be seen in the graph below taken from

a report by deloitte.

Generic drugs are the mainstay of China's pharmaceutical industry, and are likely to

remain so for a long time.

Figure 11 Sales of generics drugs in China

Source: Deloitte report on Pharma in China

Page 42

42

b) Patented Drugs

Patented drugs accounted for 20 % of the total sales of pharma in China. That is due

to the improved intellectual property rights in China so more global players were willing to

invest in producing new patented drugs in China. As can be seen from the Figure 12 from 2007

to 2010 the patented drugs sales increased at CAGR of 35.7 % which is very high while it grew

at a rate of 25% during 2010-2015.

c) OTC

Over the counter market consists of drugs that are readily available in the pharmacies

and doesn’t require a prescription by a doctor. The OTC market covers medicines ranging