4/17/2015 1 Physical Therapy in a Changing Health Care Market It’s all about VALUE “If the rate of change on the outside exceeds the rate of change on the inside . . . the end is in sight.” Jack Welch Former CEO, GE 2 2 BIG BIG BIG BIG Changes Changes Changes Changes 3 1 CONSOLIDATION BIG BIG BIG BIG is Strong 2 VALUE Quality ÷ Cost 1 POWERFUL POWERFUL POWERFUL POWERFUL Concept Concept Concept Concept 4 The Triple Aim Measurable Quality Measurable Quality An Exceptional Patient Experience An Exceptional Patient Experience Lower TOTAL Cost of Care Lower TOTAL Cost of Care 5 1 CONNECT the Dots.. 2 Volume to.. Value Volume Value 180° Incentives 3 Change Leadership Resist Fail OK Good Great 4 Getting Bigger Agenda Connecting the Opportunity Dots 6 Section 1 Health Care Reform and Value

”We spent $3Trillion spent on health care in the US

in 2013.”

PwC Health Care Division

7

Health Care Reform and Value

The Message . . . We SPEND a LOT of money on health care in the US

Did YOU KNOW that . . .

”Approximately 50% of the $3Trillion spent on health care

in the US in 2012 was either unnecessary or duplicative.

That’s $1.5 Trillion that added no value to patients”

PwC Health Care Division

8

Health Care Reform and Value

The Message . . . We WASTE a LOT of money in health care delivery

Did YOU KNOW that . . .

“In 2013, the US spent 17% of its health care expenditures on musculoskeletal conditions.”

Optum Health – United Health Care

9

The Message . . .

MUSCULOSKELETAL PAIN is a major

cost driver in health care

Health Care Reform and Value

Did YOU KNOW that . . .

“In 2012, the most costly procedures performed in

US operating rooms were

10

The Message . . .

ORTHOPEDIC SURGERIES are the major

cost drivers in ORs

Health Care Reform and Value

1. Spinal Fusions2. Total Knee Replacements3. Cardiac Angioplasty4. Total Hip Replacements

Optum Health – United Health Group

Did YOU KNOW that . . .

“We must insure more people and reduce the rapidly

rising costs in health care so 100% of Americans can

get better care at a lower cost.”

The Affordable Care Act

11

The Message . . .

The GOVERNMENT DEMANDS

Greater Access Better Quality

Lower Total Costs

Health Care Reform and Value

Did YOU KNOW that . . .

12

The Message . . .

The GOVERNMENT DEMANDS accountability

Providers must measure their value to

reduce costs and improve health

Health Care Reform and Value

“We will hold providers “accountable” through

accountable care organizations, outcomes, and

financial risk sharing.”

The Affordable Care Act

Did YOU KNOW that . . .

4/17/2015

3

“Even if we have a President and Congress who repeal

the ACA – health care reform will continue. Rising

costs are unsustainable for the people who pay for

health care. Providers must deliver value.”

Executives from Minnesota Health Plans

13

The Message . . . The PRIVATE SECTOR demands Value

Health Plans and ACOs will hold provides

accountable

Health Care Reform and Value

Did YOU KNOW that . . .

“We have a shortage of 1° care MDs – we need at

least 300 more 1° care MDs in our small state and at

least that many ‘mid-level’ providers. It’s going to

get worse as more people are insured.”

Medical Director of Large Health Plan in the South

14

The Message . . .

We do not have enough PRIMARY CARE providers

in the US

Health Care Reform and Value

Did YOU KNOW that . . .

“PTs serve as primary care providers for

musculoskeletal pain in the US Military and at Keiser

Permanente. It reduces pressure on primary care

MDs, is more efficient, and more effective.”

US Military and Keiser Permanente

15

The Message . . .

Skilled PTs can serve a PRIMARY CARE ROLE

Health Care Reform and Value

Did YOU KNOW that . . .

“PT is the best treatment for LBP. Same day access

to PT reduces costs dramatically and with measurable

functional gains. VMMC LBP model Results . . .

50% faster RTW, 28% fewer MRIs.

Great results lead to more patients.”

CEO Virginia Mason Health System

16

The Message . . . QUICK ACCESS to SKILLED PTs can result in

lower TCOC and better outcomes

Health Care Reform and Value

Did YOU KNOW that . . .

“TOTAL COSTS associated with over 30,000 people with

LBP revealed that when PT was provided within 2 weeks

of the first 1°Care MD visit, TOTAL COSTS were

reduced. Delayed PT resulted in higher TOTAL COSTS.”

Julie Fritz, PT, PhD Intermountain Health System

Spine Magazine 2012

17

The Message . . .

EARLY ACCESS to PTs results in lower TCOC for

LBP patients in COMMERCIAL HEALTH systems

Health Care Reform and Value

Did YOU KNOW that . . .

“In a study of over 300,000 Medicare patients with

LBP, early access to physical therapists for those

patients resulted in LOWER TOTAL COST of CARE.”

Alfred Gellhorn, MD, University of Washington Med School

Spine Magazine

2012

18

The Message . . .

EARLY ACCESS to PTs results in lower TCOC for LBP

patients in the MEDICARE SYSTEM

Health Care Reform and Value

Did YOU KNOW that . . .

4/17/2015

4

“In a Health Plan – PT Network pilot, PTs using FOTO to

manage their care and focus on achieving high functional

outcomes reduced TCOC for shoulder conditions by 20%.

Reductions in hospital, imaging, ER, Urgent Care, Chiro,

and direct PT costs.”

TPI Value-Based Reimbursement Model

in a NE State

19

The Message . . .

VALUE-FOCUSED PT care can reduce TCOC

Health Care Reform and Value

Did YOU KNOW that . . .

For people with musculoskeletal conditions who received physical therapy, here’s a look at TCOC

Therapy Partners Data from Health Plan

in NE State

20

Upstream Costs 40% PT Costs 30% Downstream 30%

1° Care Visits, Imaging,

Injections, Orthopedic

Visits, Meds

Imaging, injections,

orthopedic visits,

surgery, surgery

center, hospital stays

Health Care Reform and Value

Did YOU KNOW that . . .

For people with musculoskeletal conditions who received physical therapy, here’s a look at TCOC

Therapy Partners data from a health plan

in a Southern state

21

Upstream Costs 50% PT Costs 35% Down

stream 15%

1° Care Visits, Lot of Imaging,

Injections, Very High Specialty

Medical Visits, DME

Follow up

visits Specialty

Med Fewer

Surg

Health Care Reform and Value

Did YOU KNOW that . . .

22

Health Care Reform and Value

What if . . .

Physical Therapy is moved UPSTREAM . . .

Upstream

50%

PT

35%

Downstream

15%

BEFORE AFTER

Upstream Costs

40%

PT Costs

30%

Downstream

30%

BEFORE PT AFTER PT

Upstream

20%

PT

45%

Downstream

35%TCOC

$BEFORE AFTER

TCOC

$$

TCOC

$$$

“A majority of providers are paid based on the volume of

services – FFS. More interventions provided results in higher

costs. Care decisions are often driven not by what is in the

best interest of the patient and our delivery system but by

what provides the highest provider reimbursement.”

The Strategy that Will Fix Health Care

Michael Porter - Strategist, Harvard Business School

23

The Message . . . FFS creates incentives that drive up cost, not quality

Health Care Reform and Value

Incentives Drive Behavior

Majority of providers, payors shift to Value Based Models

Am Health Ins Plan:

90% of payers - 81% of hospitals have mix of VBR and FFS

Expect FFS to decrease from 56% to 32% in 5 years

To Transform from FFS to Value Based Payment . . .

BCBS – Invests $65B http://bit.ly/BCBS65B

UHG – Invests $43B http://bit.ly/UnitedHealthMove

24

Health Care Reform and Value

Transformation to Value

The Message . . . VBR MODELS create incentives that drive up quality, drive

down costs

4/17/2015

5

”Only 7% of people with musculoskeletal conditions

received physical therapy

care in 2013.”

25

The Message . . .

A VERY SMALL PERCENTAGE of people see a

physical therapist to solve their musculoskeletal problem

Health Care Reform and Value

Yet. . . in spite of compelling evidence

26

Health Care Reform and Value

But. . .

We can blame the powerful decision makers at health plans

because they don’t know

Andmost have never viewed PT as a

SOLUTION

We see strong FACTS that PROVE

early PT brings down TOTAL

COSTS, and we are starting to see

effective, early PT elevates

quality/function/health.

Seems like a no-brainer.

Health Care Reform and Value

27

Team Discussion

So WHY do only 7% go to PT

and how can YOU change

that to 17%? Or 27%? . . .

The

Volume to ValueRevolution

Section 2

Health Care Reform and Value

28

Volume Value

180°Incentives

the BIGChange

Is in Provider Incentives

29

Volume Based $$ Incentives

Fee for Service

The More You Do The More You Get Paid

Value Based $$ Incentives

Outcomes Based Models

The Better the OutcomeThe Better the Payments

180°Financial Incentives

Health Care Reform and Value

When Financial Incentives

Change 180°. . .

Provider Behavior Must Change

Accordingly

30

Volume Based

Financial IncentivesValue Based

Financial Incentives

180°Financial Incentives

Health Care Reform and Value

4/17/2015

6

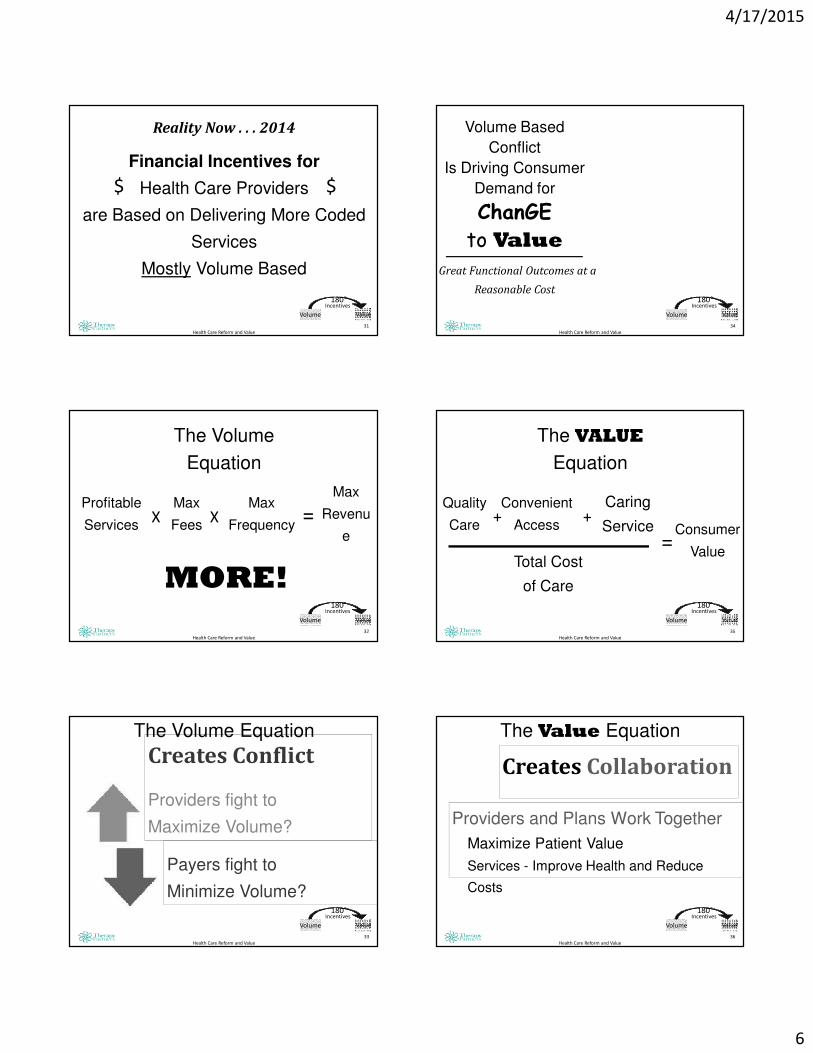

Reality Now . . . 2014

Financial Incentives for

Health Care Providers

are Based on Delivering More Coded

Services

Mostly Volume Based

31

$ $

Health Care Reform and Value

Volume Value

180°Incentives

Profitable

Services

32

The Volume

Equation

Health Care Reform and Value

Max

FeesX

Max

FrequencyX =

Max

Revenu

e

MORE!Volume Value

180°Incentives

33

Creates Conflict

Providers fight to

Maximize Volume?

The Volume Equation

Payers fight to

Minimize Volume?

Health Care Reform and Value

Volume Value

180°Incentives

Volume Based

Conflict

Is Driving Consumer

Demand for

ChanGE

to ValueGreat Functional Outcomes at a

Reasonable Cost

34

Health Care Reform and Value

Volume Value

180°Incentives

Quality

Care

35

The VALUE

Equation

Health Care Reform and Value

Convenient

Access+

Caring

Service+

=Consumer

ValueTotal Cost

of Care

Volume Value

180°Incentives

36

Creates Collaboration

The Value Equation

Health Care Reform and Value

Providers and Plans Work Together

Maximize Patient Value

Services - Improve Health and Reduce

Costs

Volume Value

180°Incentives

4/17/2015

7

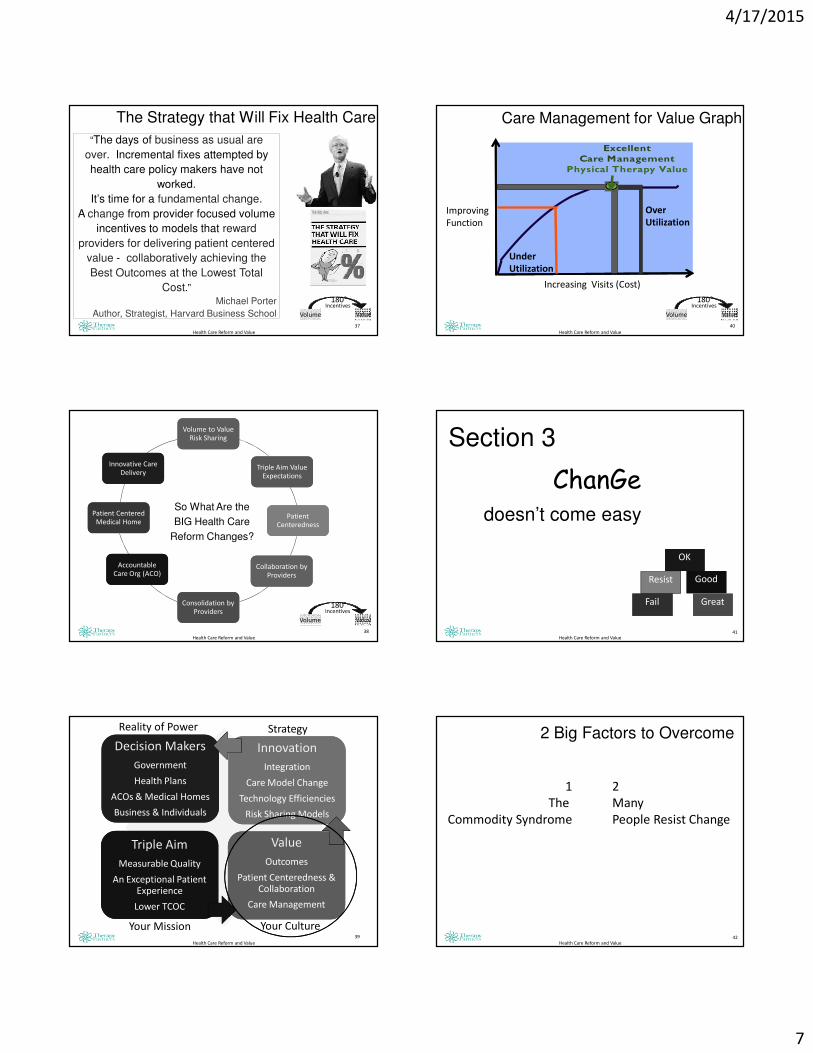

The Strategy that Will Fix Health Care

“The days of business as usual are

over. Incremental fixes attempted by

health care policy makers have not

worked.

It’s time for a fundamental change.

A change from provider focused volume

incentives to models that reward

providers for delivering patient centered

value - collaboratively achieving the

Best Outcomes at the Lowest Total

Cost.”Michael Porter

Author, Strategist, Harvard Business School

Health Care Reform and Value

37

Volume Value

180°Incentives

38

Health Care Reform and Value

So What Are the

BIG Health Care

Reform Changes?

Volume Value

180°Incentives

Volume to Value Risk Sharing

Volume to Value Risk Sharing

Triple Aim Value Expectations

Triple Aim Value Expectations

Patient Centeredness

Patient Centeredness

Collaboration by Providers

Collaboration by Providers

Consolidation by Providers

Consolidation by Providers

Accountable Care Org (ACO)

Accountable Care Org (ACO)

Patient Centered Medical Home

Patient Centered Medical Home

Innovative Care Delivery

Innovative Care Delivery

Health Care Reform and Value

39

Decision Makers

Government

Health Plans

ACOs & Medical Homes

Business & Individuals

Decision Makers

Government

Health Plans

ACOs & Medical Homes

Business & Individuals

Innovation

Integration

Care Model Change

Technology Efficiencies

Risk Sharing Models

Innovation

Integration

Care Model Change

Technology Efficiencies

Risk Sharing Models

Triple Aim

Measurable Quality

An Exceptional Patient Experience

Lower TCOC

Triple Aim

Measurable Quality

An Exceptional Patient Experience

Lower TCOC

Value

Outcomes

Patient Centeredness & Collaboration

Care Management

Value

Outcomes

Patient Centeredness & Collaboration

Care Management

Reality of Power Strategy

Your Mission Your Culture

40

Under

Utilization

Over

Utilization

Health Care Reform and Value

Improving

Function

Increasing Visits (Cost)

Care Management for Value Graph

Volume Value

180°Incentives

Excellent Care Management

Physical Therapy Value

41

ChanGedoesn’t come easy

Health Care Reform and Value

Section 3

Resist

Fail

OKOK

GoodGood

GreatGreat

42Health Care Reform and Value

2 Big Factors to Overcome

1

The

Commodity Syndrome

2

Many

People Resist Change

4/17/2015

8

43

A service or product that is delivered to the

market place and cost is the only factor in

determining its value.

Quality is not considered.

Health Care Reform and Value

The Commodity Syndrome

Health Care Reform and Value

44

Long Standing Combative

Relationship Provider and Payor

Long Standing Combative

Relationship Provider and Payor

High Profile Providers Get the

Focus

High Profile Providers Get the

Focus

Therapists Viewed as Ancillary to MDsTherapists Viewed as Ancillary to MDs

Plans Have a Silo Mentality of Cost

Control

Plans Have a Silo Mentality of Cost

Control

Lack of Significant Innovative Therapy

Solutions

Lack of Significant Innovative Therapy

Solutions

Few PTs Negotiate Contracts with Health Plans

Few PTs Negotiate Contracts with Health Plans

The Commodity Syndrome

So how did we get there??

45Health Care Reform and Value

Overcoming The Commodity Syndrome

46Health Care Reform and Value

Understand their

problem

Understand their

problem

Respect their

INTERESTS

Understand

their NEEDS

Determine Solution

They Don’t Even See

Determine Solution

They Don’t Even See

Exceed Their

Expectations

Exceed Their

Expectations

Overcoming The Commodity Syndrome

With the Powerful Decision Makers

47Health Care Reform and Value

But Change is Hard

IF you

SellVALUEYou must

DeliverVALUE

Resist

Fail

OK

Good

Great

48Health Care Reform and Value

ChanGe

Resist

Fail

OK

Good

Great

4/17/2015

9

49Health Care Reform and Value

Change? Lots of it . . .

Care ModelCollaboration

Manage Care

Decisions

Outcomes

DischargePlanning

Delegation

Communication

Population Healthvs Rehab

Resist

Fail

OK

Good

Great

50

Most People

Struggle with

Change and

Need Leaders

to Guide Them

and Managers

to Help Them

5-10%

Hate It!

Resist It!

Try to Make

It Fail!

15-20%

Hate It!

Resist It!

30-40%

Go with the Flow

But Won’t Try to

Convert Resistors15-20%

Embrace

Change

Convert

Resistors

5-10%

Love it!

I’m Your

Change

Champion

20-30%

Hold You

Back

50-70%

Take Your

Time

20-30%

Will Help

You

Health Care Reform and Value

How People Respond to Change

51Health Care Reform and Value

Resist

Fail

OK

Good

Great

52

Leaders at the Top

Vision

Drive Change - VALUE

Define Culture

Care

Leaders at the Top

Vision

Drive Change - VALUE

Define Culture

Care

Managers

Set Goals

Build Teams – Help through Change

Plan

Accountability

Managers

Set Goals

Build Teams – Help through Change

Plan

Accountability

Learn Grow

Role Model Leaders

Create a Positive Culture

Proactive Followers

Learn Grow

Role Model Leaders

Create a Positive Culture

Proactive Followers

Working Together

High Performing Team

Excellent Outcomes

Clinic Team

Working Together

High Performing Team

Excellent Outcomes

Clinic Team

Success During Times of ChangeSuccess During

Times of Change

Health Care Reform and Value

Resist

Fail

OK

Good

Great

Section 4

CONSOLIDATION

BIG is Strong

Minnesota Health Care Market

BIG is Strong

4/17/2015

10

Consolidation

3 Health PlansDominate

BCBS-

Mn

Health

PartnersMedica

Consolidation

4 ACOsDominateTwin CitiesAllina

Fairview University

HealthPartners

Park Nicollet

Health East

Consolidation

5 Care Systems/ ACOsDominateOutstate MnEssentia

Sanford

Avera

McKennon

Mayo CentraCare

Consolidation

85%

of Primary Care MDsIn Twin Cities

Are Employed by ACOs

Consolidation

Vast Majority

SpecialistsDominateTwin Cities

Gastro

Twin Cities

Ortho

Summit

Ortho

at Fairview

U of M

Phys Heart

at Fairview

Consolidation

WHY??

The Reason they Should Consolidate . . .

Improve Care

The Reason they DO Consolidate . . .

Negotiating Strength with

Health Plans

4/17/2015

11

So how about

The Independent

Physical Therapy

Practices?

Health Care Reform and Value

62

Practice Owners Have 4 Options

Stay

the

Course

Don’t consolidate

Small is better

Depend on Relationship

sCash or Out of Network

1

Grow

My

Own

Open new clinicsGrow

existing clinics

Buy other practices

Merge

2

Time

To

Sell

Consider the Big Guys

Culture Fit?CorporateSell 100%

CombinationSell 51-90%

3

Get Big

Stay

Small

Keep Practice

Collaborate with others

NetworkDetermine Value Add

Differentiate

4

63

Get Bigger Options – Value

Merge

Acquire Sell

Single TIN

Simplicity

Efficiencies

Size

Governance

High Control

Stability

Share risk

High

Accountability

Value ?

MSO

Single TIN

Simplicity

Efficiencies

Size

Governance

Control

Stability

Share risk

Accountability

High Ability to

deliver value

IPA

Multiple TINs

Complexity

No efficiencies

Size

Loose Govern.

Limited Control

Unstable

Share risk

Little Account.

Value delivery a

challenge

Network

Multiple TINs

Complexity

No efficiencies

Size

No Govern.

No Control

Unstable

No risk share

No Account.

No Value

delivery

FEAR

Small practices at risk

REALITY of POWER

Must connect with powerful decision-makers

64

WHY Make this Big Change?

STRENGTH

65

WHY

Health Plan or

ACO

Contracting &

Credentialing

Process Claims

from

Practices

Make

Payments to

Practices

Complexity

Practice

3

Practice

4

Practice

1

Practice

2

Practice

8

Practice

7

Practice

6

Practice

5

66

4/17/2015

12

Practice

7

Practice

5

Practice

3

Practice

1

Practice

8

Practice

6

Practice

4

Practice

2Organize Under a Single Tax

ID Number

One Source Contracting, Risk

Sharing, Credentialing, and

Care Management

Billing DepartmentBilling and

A/R Management

Payment Processing,

Posting and Distribution

to Practices

Health Plan or

ACO

Contracting with

Risk Sharing

Arrangements

Process Claims

from

Big Provider

Group

Make

Payments to

Big Group

Simplicity

67

Health Plan or

ACO

Invests to

Control Cost

UM

for Cost Control

Ave Visits – 12.8

Range – 8.5 to

18.5

Care Management

for Quality

No Consistent

Quality Measures

Practice

3Ave Visits – 10.0

Functional Outcomes - ?

Practice

4Ave Visits – 18.5

Functional Outcomes - ?

Practice

1 Ave Visits – 12.5

Functional Outcomes - ?

Practice

2Ave Visits – 14.1

Functional Outcomes – ?

8 Practice

8 Ave Visits – 8.5 Functional

Outcomes - ?

7 Practice

7 Ave Visits - 17.0

Functional Outcomes - ?

6 Practice

6 Average Visits - 9.8

Functional Outcomes - ?

5 Practice

5 Average Visits – 13.0

Functional Outcomes - ?

Inconsistency

68

Health Plan or

ACO

No Financial

or Human

Resources

Devoted to

Care or

Utilization

Management

Saves $$$$

Big Organization Measures

Outcomes

Efficiency

(Ave Visits or Cost)

Predictable Cost

Effectiveness

(Functional Improvement)

Predictable Functional

Change

Measurable

Value

Practice

1 Ave Visits 8.5

FOTO – 82%Visit &

Function Data

Visit &

Function Data

Visit &

Function Data

Visit &

Function Data

Visit &

Function Data

Visit &

Function Data

Visit &

Function Data

Practice

2 Ave Visits 8.2

FOTO – 77%

Practice

3 Ave Visits 8.0

FOTO – 75%

Practice

4Ave Visits 8.3

FOTO – 84%

Practice

5Ave Visits 8.0

FOTO – 78%

Practice

6Ave Visits 8.2

FOTO – 83%

Practice

7 Ave Visits 8.0

FOTO – 78%

Practice

8 Ave Visits 8.1

FOTO – 80%

Visit

&

Functional

Outcome

Data

Predictability

69

Must . . .

Have Some Size

Deliver Value

Be Willing to Share Financial Risk

Connect with Powerful Decision Makers

Be Able to Lead Change

. . .

PT is a Proven Solution

70

Tie it Together

Health Care Reform and Value

Physical Therapist and Physical Therapist Assistants in a Changing

Health Care Market

VALUE-BASED PAYMENTMODELS

PHYSICAL THERAPY POSITIONING AND BRAND

What Does the Data Show

Health Care Reform and Value

72

4/17/2015

13

Optum Health – CSM and WPTA conferences February, April 2014

data 2010-2012

Positioning of PT Services

Typical Clinical Pathway

Timing and Cost of Total Episode

Health Care Reform and Value

77

TPI Workers Comp Data

4/17/2015

14

Optum Consumer Focus Groups PT Brand

Optum Consumer Focus Groups PT Brand

“. . . And it makes me wonder”

–Led Zeppelin, Stairway to Heaven

Position

• Delayed onset of PT is a very common pathway

• Likewise significant cost in “upstream” portion of total cost

• “Silo” management is ineffective at controlling costs

• Effecting downstream costs is only part of the solution

Brand

• Extension of the doctor

• Start at the doctor first

• Time consuming

• This will take longer to get

results

• Temporary relief

• This is not a final solution

• Is our position a result of or

a cause of our brand?

Changing the Clinical Pathway

Financial Considerations-Risks and Incentives

Clinical Considerations-Outcomes and Value

Health Care Reform and Value

82

Financial Principle - 1

• Physical Therapists and

Physical Therapist

Assistants are revenue

generators

Financial Principle - 2

“One companies revenue,

is another companies line

item expense.”

Perry Hanson-Wipfli HC Consultant

Profit Margin

Return on Investment

4/17/2015

15

Risk and Incentives

Risk

• “It's important to

understand how people

perceive risk, and how that

translates into investment

behavior.”

Andrew Lo, Finance MIT

Incentives

• “The ideal of behaviorism is

to eliminate coercion: to

apply controls by changing

the environment in such a

way as to reinforce the kind

of behavior that benefits

everyone.”

B F Skinner

Health Care Reform and Value

85

Volume Value

180°Incentives

Payer Risk and Incentives

Risk

• More UNITS

• More VISITS

• More CASES

• POOR RESULTS – leading to

utilization of higher cost

services

• Medical loss ratio

• Overpayment on claims

Response (Incentive)

• Utilization Review (UR, UM

Dept.)

• Bill Review (Optum, Verisk)

• Code Bundling-NCCI, MPPR

• Annual visit limit

• Increased Co-pays

• Discount Networks (Align,

Orthonet)

Health Care Reform and Value

86

Volume Value

180°Incentives

Provider Risk and Incentives

Risk

• Decreasing

REIMBURSEMENT

• Increasing ADMINISTRATIVE

BURDEN (PQRS, FLR)

• Increased security and

OVERSIGHT (HIPPPA, PHI

policies)

• Increased CODE BUNDLING

(MPPR, NCCI)

Incentive

• Code higher RVU

• More codes per visit

• More visits per episode

• Higher productivity

standards

• Use of billing modifiers (59

or X, KX)

Health Care Reform and Value

87Volume Value

180°Incentives

Patient/Purchaser Risk

Risk

• Increased COST TO INSURE

• Mandatory ESSENTIAL

HEALTH BENEFIT

• POOR RESULTS – leading to

utilization of higher cost

services

• Shift cost to employee

• Making the wrong purchase

Incentive

• Increased DEDUCTIBLE

AMOUNT

• Increased CO-PAY Amount

• Health Resources vs. Health

Savings Account (HSA)

• Self-Insure, captive (less

regs. control benefits)

• Discount Networks (Align,

Orthonet)

Health Care Reform and Value

88

Volume Value

180°Incentives

Align Incentives

INCENTIVES

• Control UNITS = Per Diem

Payment

• Control UNITS and VISITS =

Episodic or Case Rate

• Control UNITS, VISITS, and

CASES = Capitation. Too

risky for therapy.

• Control EPISODE COST =

Bundling, TCOC

RISK• PROVIDER must control visit

units

• PROVIDER must know cost to deliver a visit

• PROVIDER must know all

costs and ratio of PT to population statistics

• PROVIDER must know

cost to deliver care, able to address upstream costs

Health Care Reform and Value

89

Quality

Care

90

The VALUE

Equation

Health Care Reform and Value

Convenient

Access+

Caring

Service+

=Consumer

ValueTotal Cost

of Care

Volume Value

180°Incentives

Profit Margin

Return on Investment

4/17/2015

16

Redefining the PT Value Equation

Quality =

# visits

Quality =

# visits

Costs = �Payment

Costs = �Payment

= Commodity

(not Value)

= Commodity

(not Value)

TECOC

FOTO

Therapy Outcomes

FOTO

Therapy Outcomes

Payer ClaimsPayer

Claims

Health Care Utilization

Health Care Utilization

Value-Based Health Care

“Health care organizations

that deliver clinical value,

are stronger and valued

by payers and ACO’s”

recently retired CMO of Local

Integrated Payer

Health Care Reform and Value

92

Outcome Measures

• That which gets

measured becomes

valued, because we

can’t value what we

don’t measure

Health Care Reform and Value

93

Defining Physical Therapy Value

9 CELL VALUE MATRIX

FEWER VISITS - Efficiency

INC

RE

ASI

NG

FU

NC

TIO

NA

L C

HA

NG

EE

ffe

ctiv

en

ess

Outcomes that are Used at Multiple Levels

Function Status Measures:IntakeScore

05/07/2014Score

05/21/2014Score

Interpretation of FS Scores/Stages Value

Patient's Physical FS Primary Measure 32 48 73

Patient’s Intake FS Score was 32 init ially placing the patient in Stage 4.Patient’s FS score now is 73 out of 100 (41 points of functional changesince intake), placing the patient in Stage 6 and means patient is an activecommunity ambulator.

Risk Adjusted Statistical FOTO* 44Given the patient’s risk-adjustment variables, like-patients nationally had aFS score of 44, Stage 4, at intake.

MCII = 13 (Points of change that is important to the patient)

MDC = 7 (Represents the smallest threshold to identify pointsof change that is greater than measurement error)

Additional ItemsFOTO

Mean atDischarge

05/07/2014Value

05/21/2014Value

Interpretation of Predicted Value

Points of Physical Change 31 16 41

Given this patient’s risk-adjustment variables, and the actual Intake FSscore, FOTO predicts this patient will experience at least an increase infunction of 31 points (to 63 or higher), putting them in the Stage 6 level orhigher at discharge.

Visits 14

Duration in Days 54 35 49

Satisfaction 97.5%

Stage: 1 Physiological ambulatorStage: 2 Limited household ambulatorStage: 3 Independent household ambulatorStage: 4 Limited community ambulatorStage: 5 Independent community ambulatorStage: 6 Active community ambulator

What Does This Mean For Improving Function

This chart displays the patient responses to the functional activities contained in the intake survey that generated the intake FS score. Theactivities are presented in the descending order of difficulty. Responses listed in the Intake column are the survey item levels of ability atintake. Responses listed in the Intake column are the survey item levels of ability at intake. Given the change experienced by the comparativerisk adjusted group in FOTO’s data, it is anticipated the patient should be able to do the activities at the level indicated in the predicted columnor higher at the completion of care, to place the patient in the predicted Stage 6 functional level by discharge.

Patient responses to functional health questions that indicate dysfunction were as follows:

Activity (Question) Amount of Limitation (Response) at:

Intake Status Predicted

Functional Limitation

Your usual work, housework, or schoolactivities?

-- A little bit of

difficultyNo difficulty Other PT/OT Primary -

G8990

Your usual hobbies, recreational orsporting activities?

-- A little bit ofdifficulty

No difficulty Other PT/OT Primary -G8990

Walking between rooms? Moderate difficulty -- No difficulty Mobility - G8978

Putting on your shoes or socks?

A little bit ofdifficulty

-- No difficulty Self Care - G8987

Squatting?

-- A little bit ofdifficulty

A little bit ofdifficulty

Changing & MaintainingBody Position - G8981

Scorecard:

Clinician

Scorecard Color Key => Green: Better than Predicted, Yellow: Within 95% Confidence Interval,