54

Prepared by: Lynn de Grace C.A. FINANCIAL ACCOUNTING a user perspective Sixth Canadian Edition Chapter 6 Chapter 6 Cash, Short-Term Investments, and Accounts & Notes Receivable

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | caren-nelson |

| View: | 221 times |

| Download: | 5 times |

Prepared by:

Lynn de Grace C.A.

FINANCIAL ACCOUNTING a user perspective

Sixth Canadian Edition

Chapter 6Chapter 6Cash, Short-Term Investments, and

Accounts & Notes Receivable

Cash

John Wiley & Sons Canada, Ltd. ©2011

Characteristics Asset with probable future value Purchasing power Medium of exchange Ownership is evidenced by

possession Difficult to control

• Need for internal control procedures

2

Cash Valuation Methods

John Wiley & Sons Canada, Ltd. ©2011

Issues: Record at face value

• Value is assumed not to change Unit-of-measure assumption

• Canadian practice• Results of a company’s activities

can be measured by a monetary unit—the Canadian dollar

3

Internal Control Systems

John Wiley & Sons Canada, Ltd. ©2011

Safeguarding cash: Internal controls to prevent loss or

theft Protection and control of all assets Policies and procedures established for

handling and recording assets

4

Internal Control Systems

John Wiley & Sons Canada, Ltd. ©2011

Solutions: Effective systems should include:

• Physical measures to protect assets from theft and vandalism (passwords, access cards)

• Separation of duties• The person who handles the asset should

not have responsibility for recording changes to the asset.

• An effective record-keeping system

5

Internal Control Systems

John Wiley & Sons Canada, Ltd. ©2011

Bank reconciliation• Ensures that the accounting records

agree with the bank records• Differences may be due to timing,

incomplete data, or errors• Normally performed every month

6

Gelardi Company – Bank Reconciliation October 31, 2011

Per Ledger: 9,770.44

Add: Electronic funds transfer (EFT) 312.98

Correction of error made by co. (chq#885) 180.00

Deduct: Bank charges (25.75)

Automatic deduction for loan payment (500.00)

NSF cheque (186.80)

Adjusted cash balance $9,550.87

Per Bank: 8,916.39

Add: Outstanding deposit 1,035.62

Correction of bank error 127.53

Deduct: Outstanding cheques

#873 262.89#891 200.00#892 65.78 (528.67)

Adjusted cash balance $9,550.87

John Wiley & Sons Canada, Ltd. ©2011

7

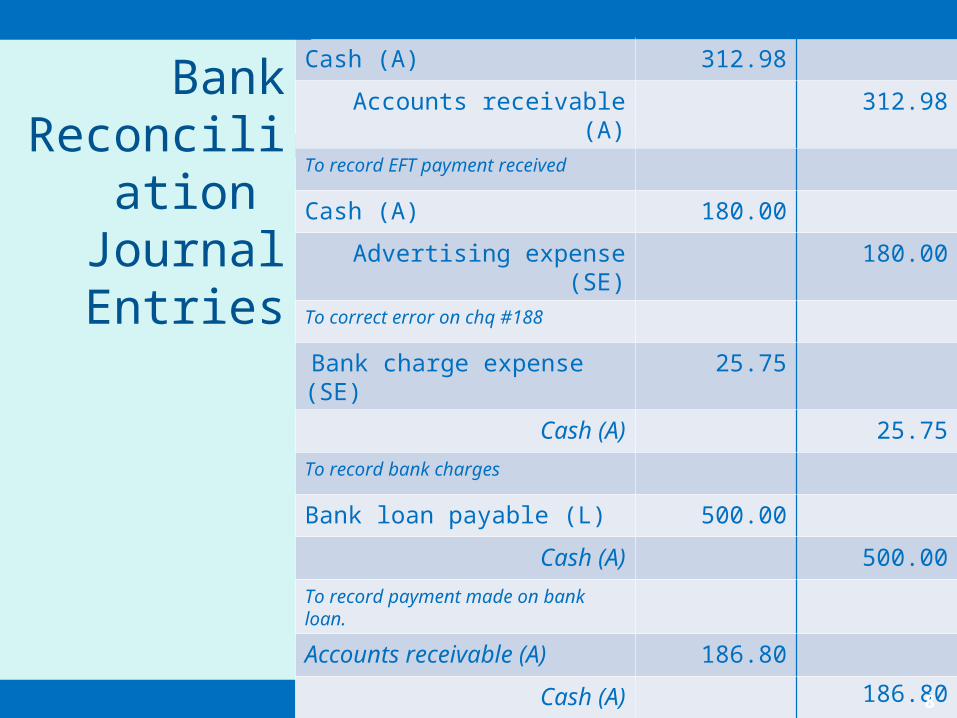

Bank Reconciliation Journal

Entries

John Wiley & Sons Canada, Ltd. ©2011

Cash (A) 312.98

Accounts receivable (A) 312.98To record EFT payment received

Cash (A) 180.00

Advertising expense (SE) 180.00To correct error on chq #188

Bank charge expense (SE)

25.75

Cash (A) 25.75To record bank charges

Bank loan payable (L) 500.00

Cash (A) 500.00To record payment made on bank loan.

Accounts receivable (A) 186.80

Cash (A) 186.80

To reinstate acct receivable re: NSF chq.

8

Bank Reconciliation

John Wiley & Sons Canada, Ltd. ©2011

Common reconciling items include:• Outstanding cheques• Outstanding deposits• Bank service charges• Errors in recording items• Any other item that affects cash

9

Internal Control Measures

John Wiley & Sons Canada, Ltd. ©2011

The person who reconciles the bank account should not be the same person who is responsible for maintaining the bank account in the accounting records—segregation of duties

Sufficient cash should be readily accessible to pay minor expenses

10

Short-Term Investments

John Wiley & Sons Canada, Ltd. ©2011

Cash may be invested in marketable securities• Short-term investments• Debt or equity interest in another entity

11

Short-Term Investments—Classification

John Wiley & Sons Canada, Ltd. ©2011

Surplus cash invested in temporary marketable securities generates earnings

Differing levels of liquidity should be assessed:• Marketable and easily liquidated

classify as current asset• Not easily convertible to cash within one

year classify as non-current

12

Short-Term Investments—Valuation

John Wiley & Sons Canada, Ltd. ©2011

What alternatives are there? Historical cost

• Changes in market value have no effect on the recorded amounts

• A realized gain or loss is recognized only when the securities are sold

Market value• Changes in market value are recognized as unrealized gains or

losses at every reporting period• Other income is recognized when interest or a dividend is

received Lower of cost and market value (LCM)

• A hybrid of the above two methods

13

Short-Term Investments

John Wiley & Sons Canada, Ltd. ©2011

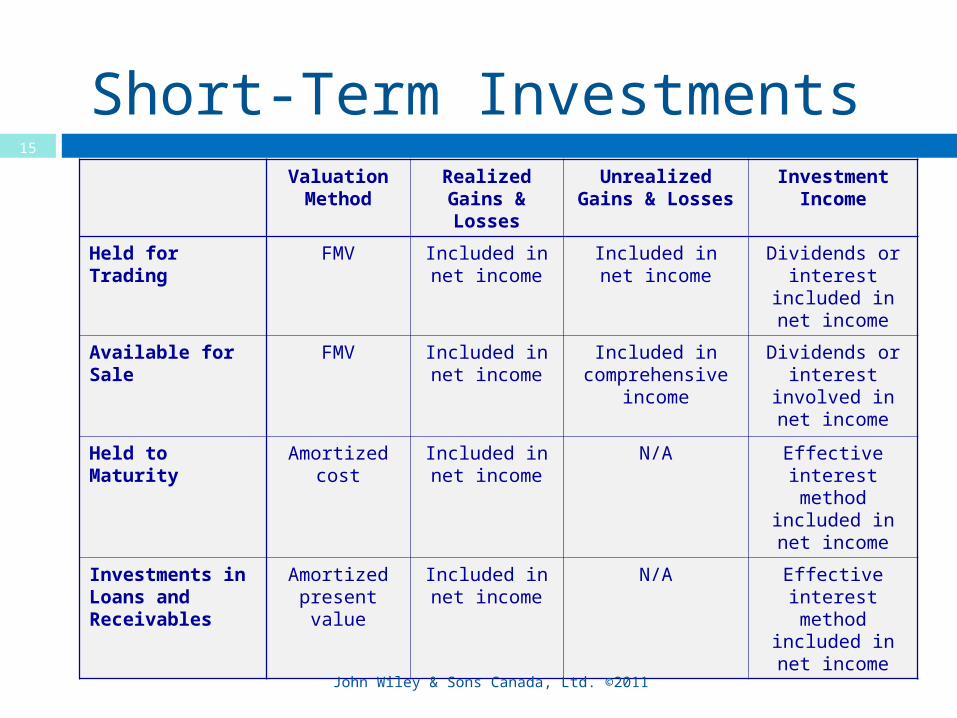

Canadian practice and IFRS —fair market value

Four types of investments1. Held for trading investments2. Available for sale3. Held to maturity4. Investments in loans & receivables

14

Short-Term InvestmentsValuation Method

Realized Gains & Losses

Unrealized Gains & Losses

Investment Income

Held for Trading

FMV Included in net income

Included in net income

Dividends or interest

included in net income

Available for Sale

FMV Included in net income

Included in comprehensive

income

Dividends or interest

involved in net income

Held to Maturity

Amortized cost

Included in net income

N/A Effective interest method included in net

income

Investments in Loans and Receivables

Amortized present value

Included in net income

N/A Effective interest method included in net

income

John Wiley & Sons Canada, Ltd. ©2011

15

Clifford Company – Example Data relating to Short-Term Investments

John Wiley & Sons Canada, Ltd. ©2011

16

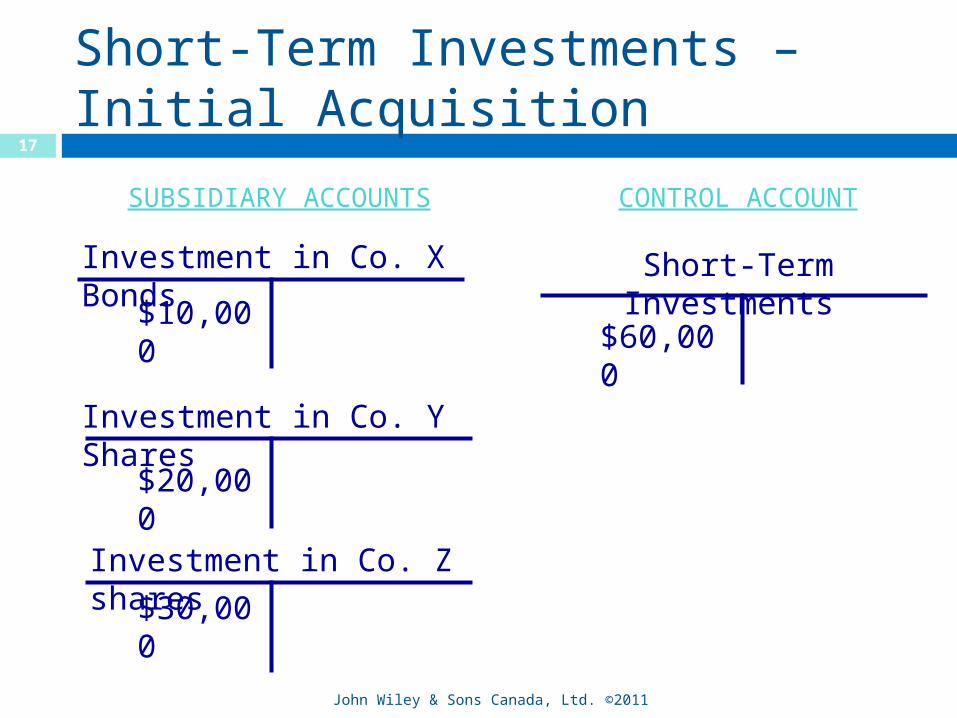

Short-Term Investments – Initial Acquisition

John Wiley & Sons Canada, Ltd. ©2011

SUBSIDIARY ACCOUNTS

CONTROL ACCOUNT

Investment in Co. X Bonds

$10,000

Investment in Co. Y Shares

$20,000

Investment in Co. Z shares

$30,000

Short-Term Investments

$60,000

17

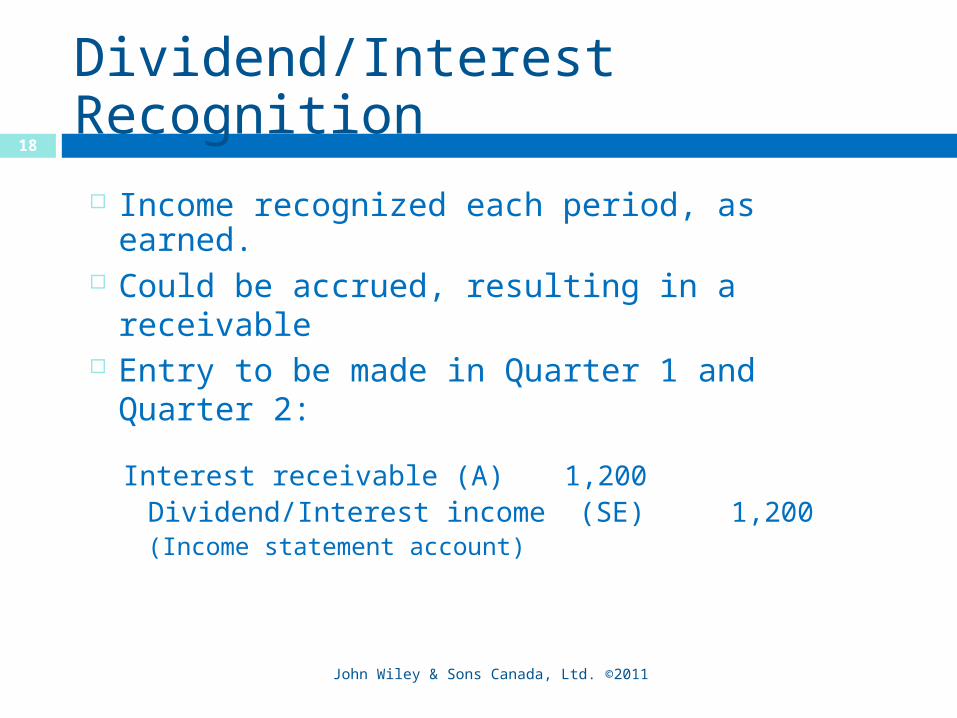

Dividend/Interest Recognition

Income recognized each period, as earned. Could be accrued, resulting in a receivable Entry to be made in Quarter 1 and Quarter 2:

Interest receivable (A) 1,200Dividend/Interest income (SE)

1,200(Income statement account)

John Wiley & Sons Canada, Ltd. ©2011

18

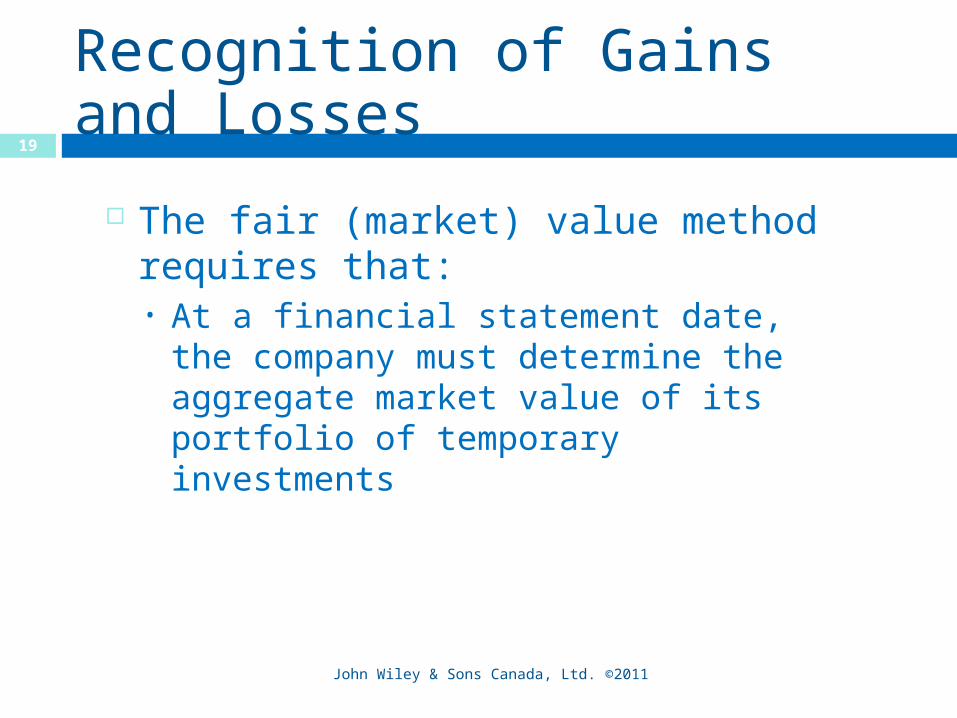

Recognition of Gains and Losses

The fair (market) value method requires that:• At a financial statement date, the

company must determine the aggregate market value of its portfolio of temporary investments

John Wiley & Sons Canada, Ltd. ©2011

19

Recognition of Gains and Losses

Quarter 1 - Market value of portfolio has declined to $57,000 Unrealized loss on short-term investments (SE) 3,000

Short-term investments (A) 3,000

John Wiley & Sons Canada, Ltd. ©2011

20

Recognition of Gains and Losses

Quarter 2: Market value of portfolio has increased to $61,000

Short-Term Investments (A) 4,000Unrealized gain on 4,000

short-term investments (SE)

If the market value has increased the original cost is no longer relevant. The company can record an unrealized gain on the investment.

John Wiley & Sons Canada, Ltd. ©2011

21

Dividend/Interest Recognition

Quarter 3: Dividend/interest revenue is recorded as:

Cash (A) 700Dividend/interest revenue (SE)

700

John Wiley & Sons Canada, Ltd. ©2011

22

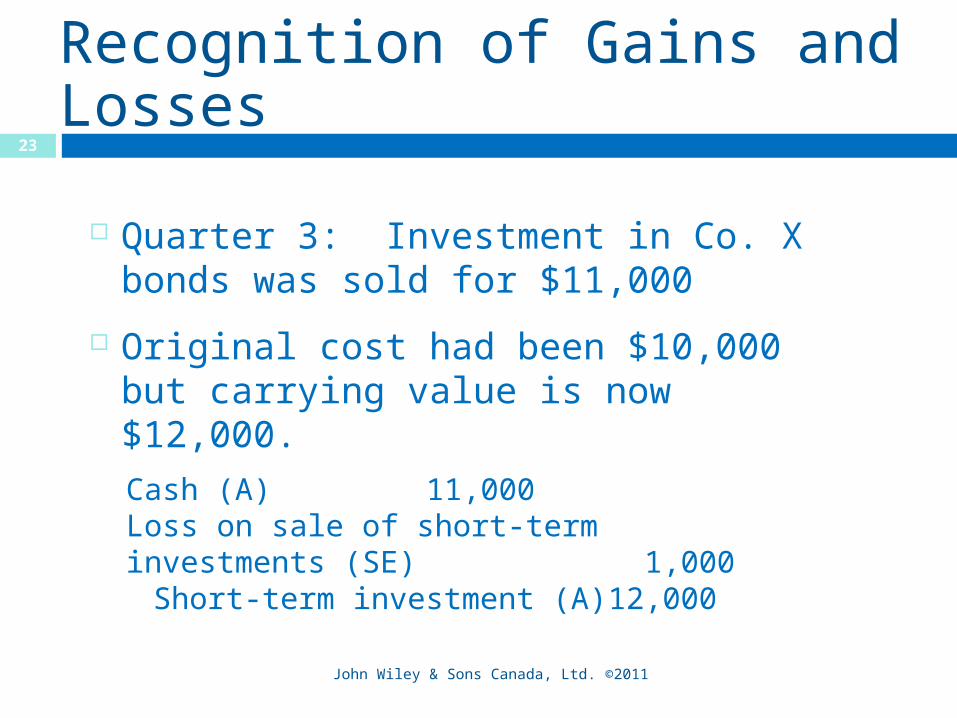

Recognition of Gains and Losses

John Wiley & Sons Canada, Ltd. ©2011

Quarter 3: Investment in Co. X bonds was sold for $11,000

Original cost had been $10,000 but carrying value is now $12,000.Cash (A) 11,000Loss on sale of short-term investments (SE) 1,000

Short-term investment (A) 12,000

23

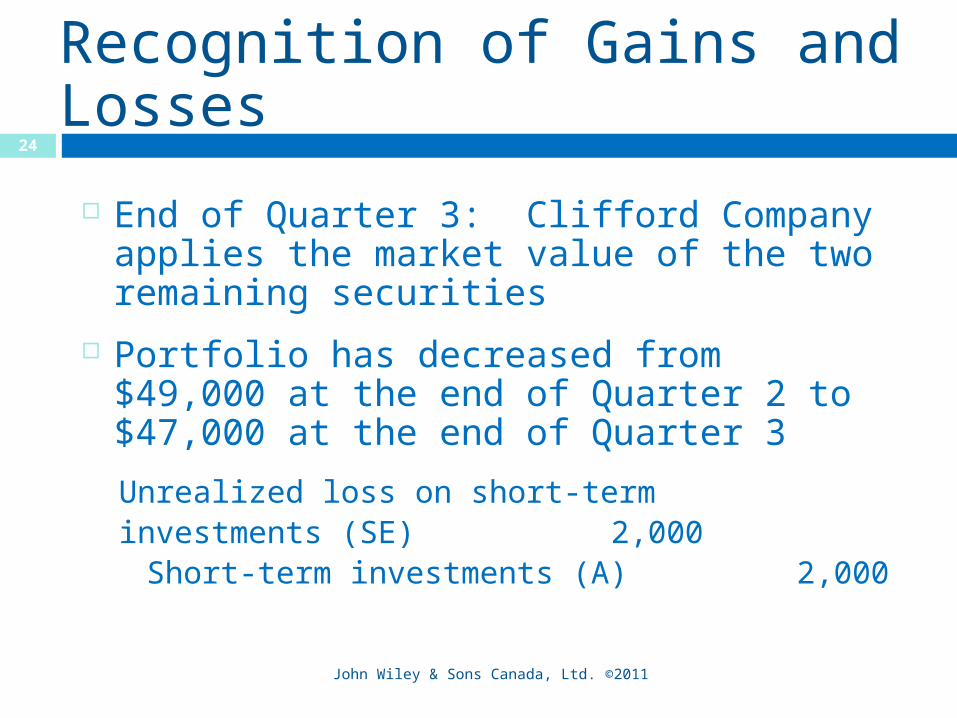

Recognition of Gains and Losses

John Wiley & Sons Canada, Ltd. ©2011

End of Quarter 3: Clifford Company applies the market value of the two remaining securities

Portfolio has decreased from $49,000 at the end of Quarter 2 to $47,000 at the end of Quarter 3

Unrealized loss on short-term investments (SE) 2,000

Short-term investments (A) 2,000

24

Recognition of Gains and Losses

John Wiley & Sons Canada, Ltd. ©2011

Quarter 4: Clifford Co. recognizes dividend/interest revenue

Interest receivable (A) 700Dividend/Interest income (SE) 700

Company sells Co. Y shares for $18,500. Co Y shares have a carrying value of $18,000.

Cash (A) 18,500Gain on sale of short-term investments (SE) 500

Short-term investment (A) 18,000

25

Recognition of Gains and Losses

John Wiley & Sons Canada, Ltd. ©2011

Quarter 4: Company applies market valuation rule to remaining investment in CO Z.

Short-Term Investments (A) 2,500Unrealized gain on short-term investments

2,500

26

Recognition of Gains and Losses

For the quarter ended Mar. 31 June 30 Sept. 30

Dec.31

Unrealized gain (loss) on temporary investments

($3,000) $4,000 ($2,000) $2,500

Realized gain (loss) on sale of temporary investments

($1,000) $500

Dividend/interest revenue $1,200 $1,200 $700 $700

John Wiley & Sons Canada, Ltd. ©2011

Partial Income Statement

27

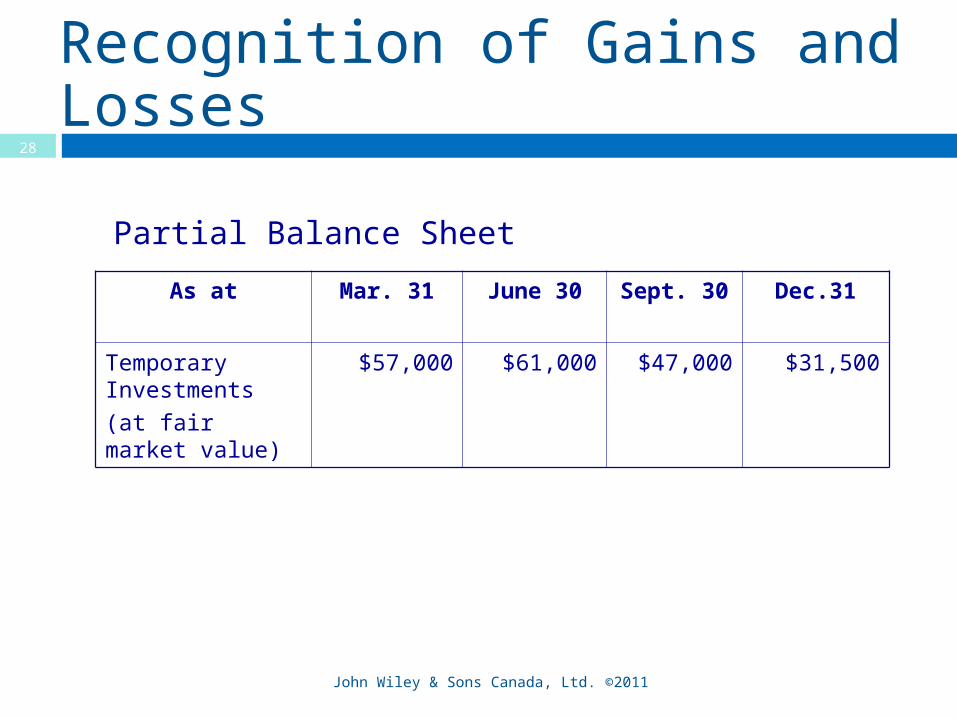

Recognition of Gains and Losses

As at Mar. 31 June 30 Sept. 30 Dec.31

Temporary Investments(at fair market value)

$57,000 $61,000 $47,000 $31,500

John Wiley & Sons Canada, Ltd. ©2011

Partial Balance Sheet

28

Accounts Receivable

John Wiley & Sons Canada, Ltd. ©2011

Amounts owed from customers as a result of selling goods and services on credit

Represents the right to receive payment at some future date

Uncertainty that the customer will not pay (bad debt)

29

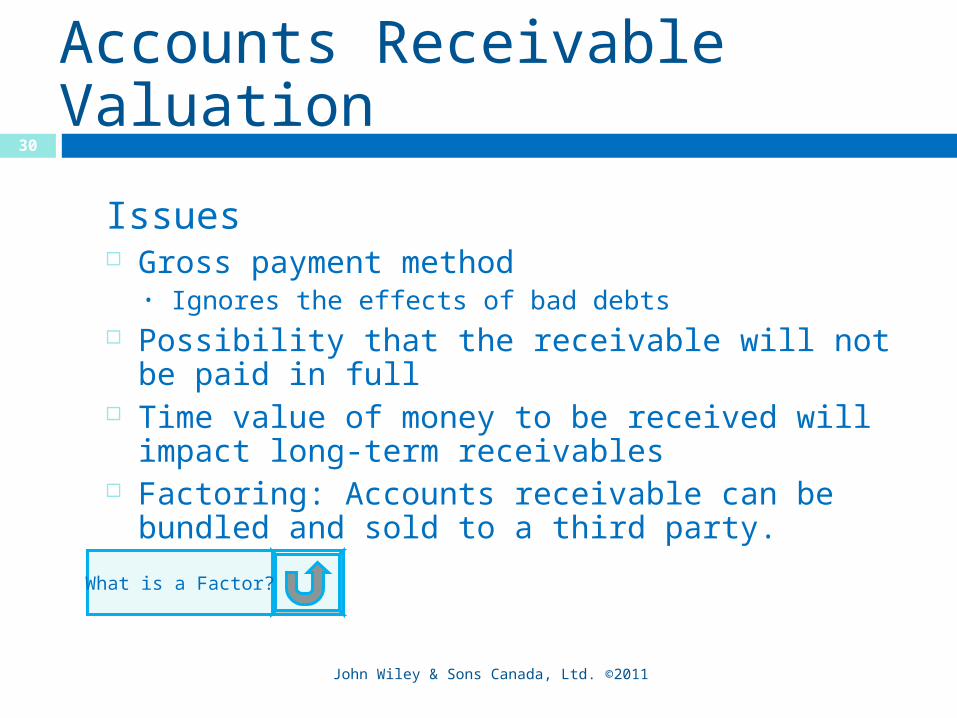

Accounts Receivable Valuation

Issues Gross payment method

• Ignores the effects of bad debts Possibility that the receivable will not be paid

in full Time value of money to be received will impact

long-term receivables Factoring: Accounts receivable can be bundled

and sold to a third party.

John Wiley & Sons Canada, Ltd. ©2011

What is a Factor?

30

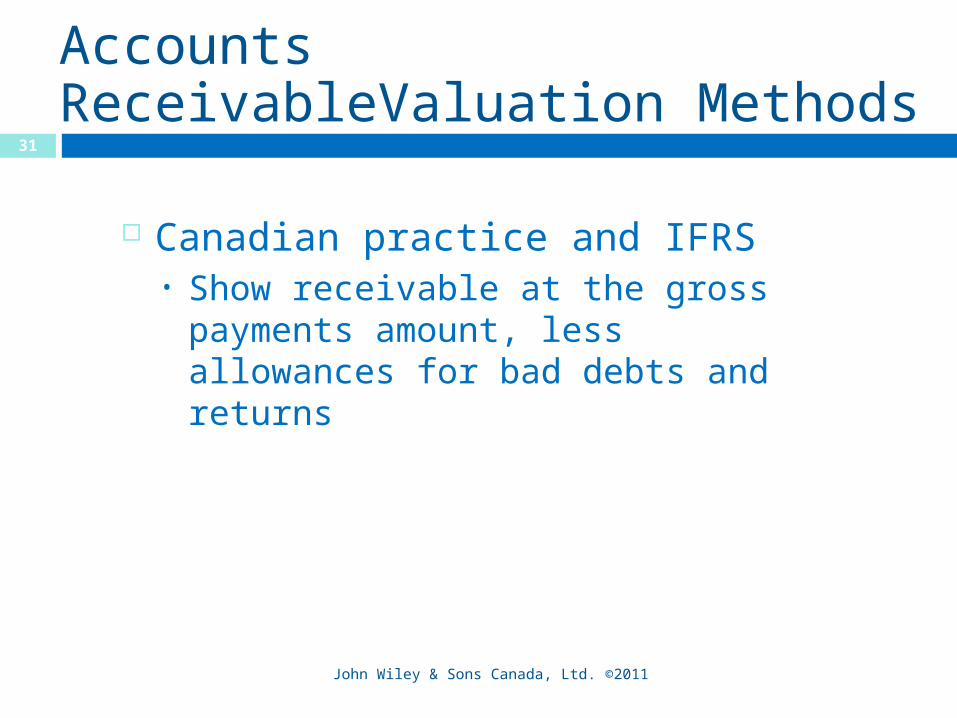

Accounts ReceivableValuation Methods

Canadian practice and IFRS• Show receivable at the gross

payments amount, less allowances for bad debts and returns

John Wiley & Sons Canada, Ltd. ©2011

31

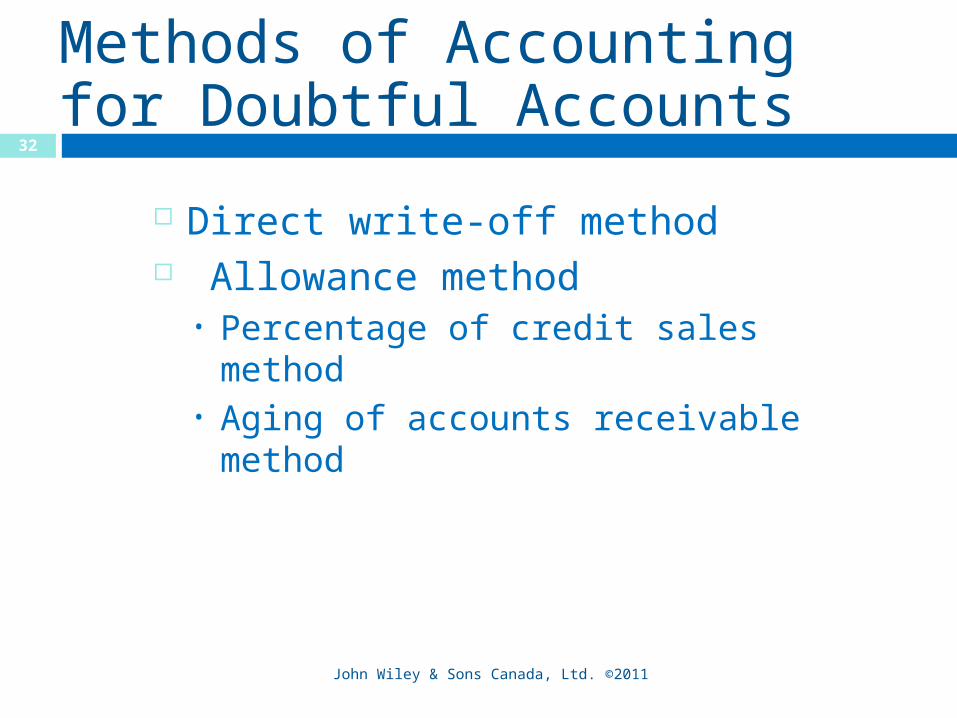

Methods of Accounting for Doubtful Accounts

Direct write-off method Allowance method

• Percentage of credit sales method• Aging of accounts receivable

method

John Wiley & Sons Canada, Ltd. ©2011

32

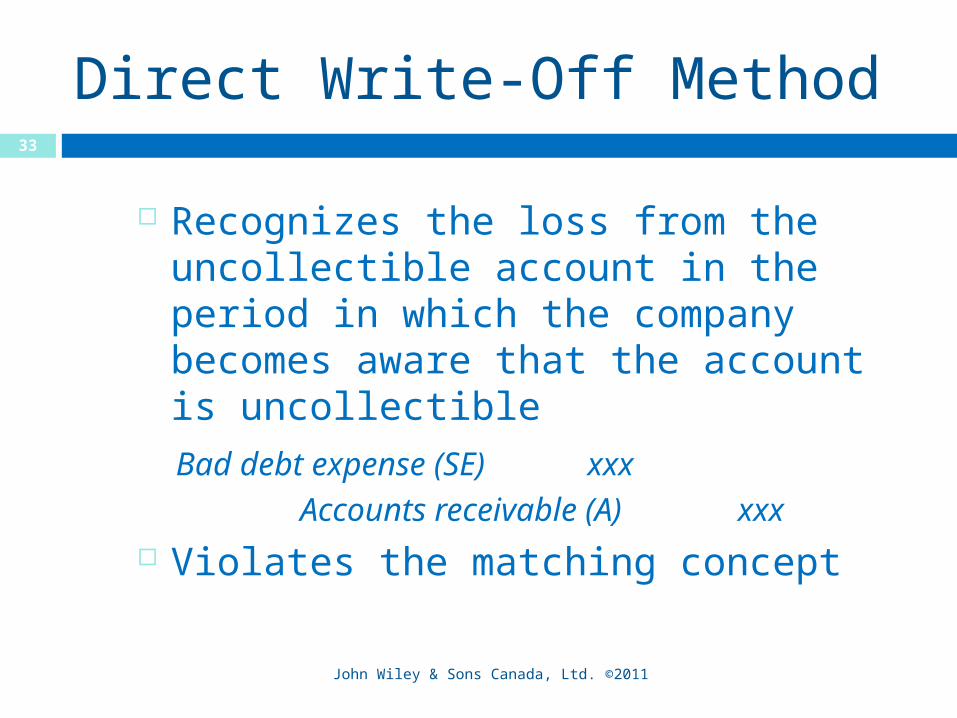

Direct Write-Off Method

John Wiley & Sons Canada, Ltd. ©2011

Recognizes the loss from the uncollectible account in the period in which the company becomes aware that the account is uncollectibleBad debt expense (SE) xxx

Accounts receivable (A) xxx Violates the matching concept

33

Allowance Method

John Wiley & Sons Canada, Ltd. ©2011

Matching concept:• When revenues from a sale are recognized,

related expenses must be recognized at the same time

Bad debts are really reductions in revenues, not expenses

Companies must estimate uncollectible (doubtful) amounts

34

Allowance Method

John Wiley & Sons Canada, Ltd. ©2011

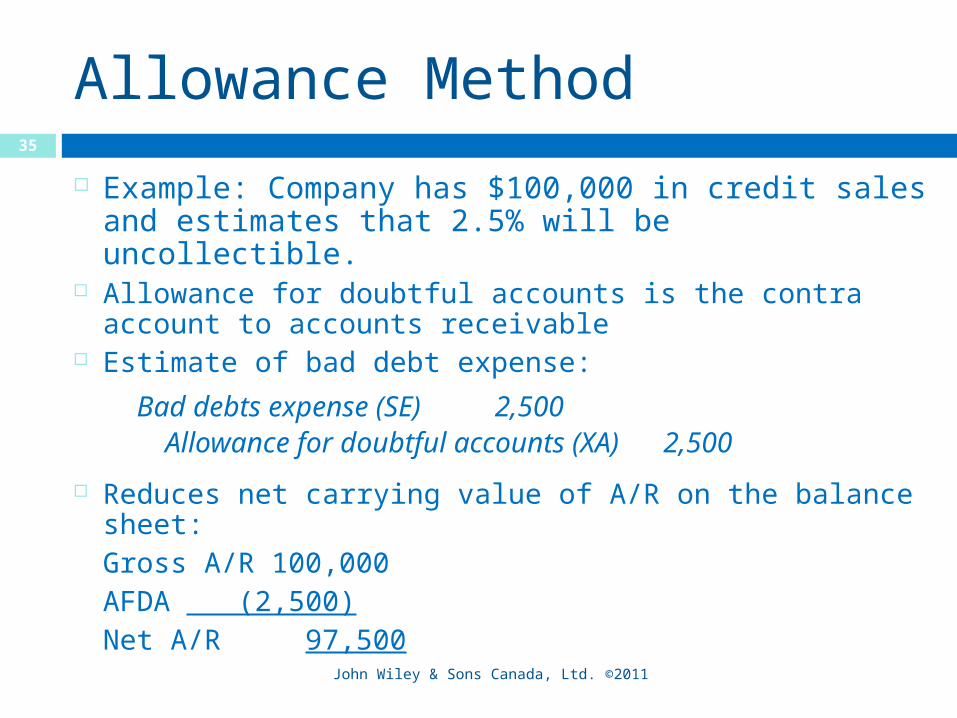

Example: Company has $100,000 in credit sales and estimates that 2.5% will be uncollectible.

Allowance for doubtful accounts is the contra account to accounts receivable

Estimate of bad debt expense:

Bad debts expense (SE) 2,500 Allowance for doubtful accounts (XA) 2,500

Reduces net carrying value of A/R on the balance sheet:

Gross A/R 100,000AFDA (2,500)Net A/R 97,500

35

Allowance Method

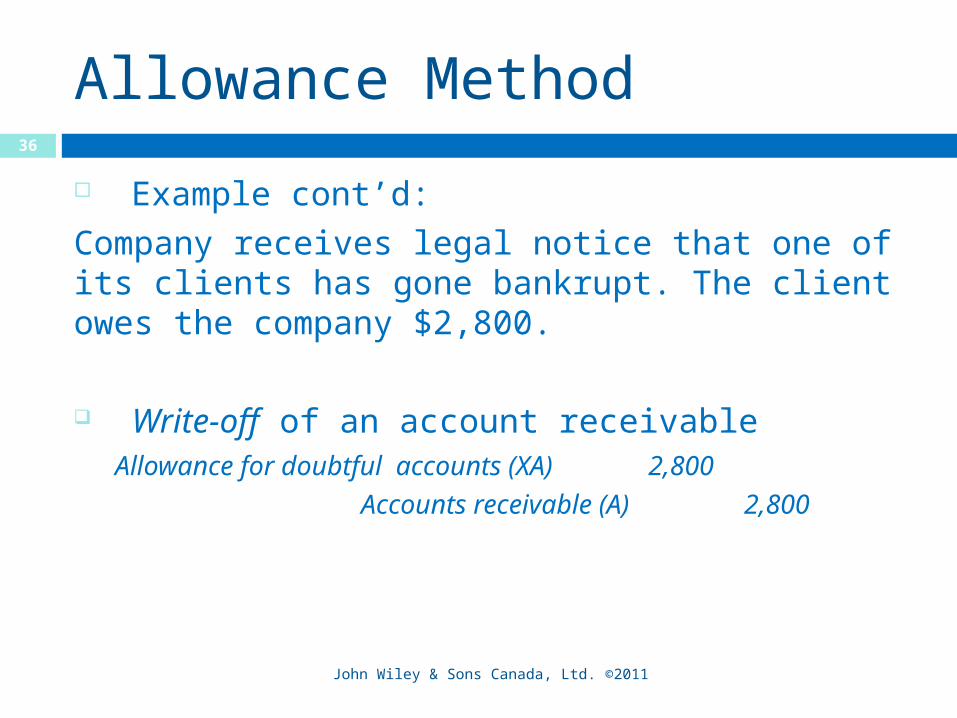

Example cont’d:

Company receives legal notice that one of its clients has gone bankrupt. The client owes the company $2,800.

Write-off of an account receivable Allowance for doubtful accounts (XA) 2,800

Accounts receivable (A)2,800

John Wiley & Sons Canada, Ltd. ©2011

36

Allowance Method

John Wiley & Sons Canada, Ltd. ©2011

Example (cont’d):In the months that follow, the company receives a $400 settlement cheque from the bankruptcy liquidation.

Recovery of account receivable previously written-off :

Accounts receivable (A) 400Allowance for doubtful accounts (XA) 400

Cash (A) 400Accounts receivable (A) 400

37

Estimating Bad Debts

Percentage of credit sales method Accounts receivable method

• Aging of accounts receivable method

Important to distinguish between a bad debt write off and estimating for

doubtful accounts.

John Wiley & Sons Canada, Ltd. ©2011

38

Percentage of Credit Sales Method

Bad debt expense is a function of total credit sales

Multiply credit sales by an appropriate percentage• Result is bad debt expense

Percentage is based on collection history The balance in the AFDA does not affect

the calculation

John Wiley & Sons Canada, Ltd. ©2011

39

Accounts Receivable Method

Bad debt expense is a function of the allowance for doubtful accounts

Work backwards: Step 1 Determine the estimated AFDA

amount required using an accounts receivable aging schedule.

Step 2 Adjust AFDA by creating the necessary amount for bad debt expense.

Step 3 Determine the NRV of accounts receivable.

John Wiley & Sons Canada, Ltd. ©2011

40

Accounts Receivable Method

Step 1Determine the estimated AFDA amount required using an aging schedule.

Totals # Days Outstanding

1-30 31-60 61-90 91-120 >120

Total A/R(from aging schedule)

$12,000 $5,500 $3,600 $800 $1,100 $1,000

Estimated % Uncollectible

1% 5% 15% 35% 65%

Total Estimated AFDA Required

$1,390 $55 $180 $120 $385 $650

John Wiley & Sons Canada, Ltd. ©2011

41

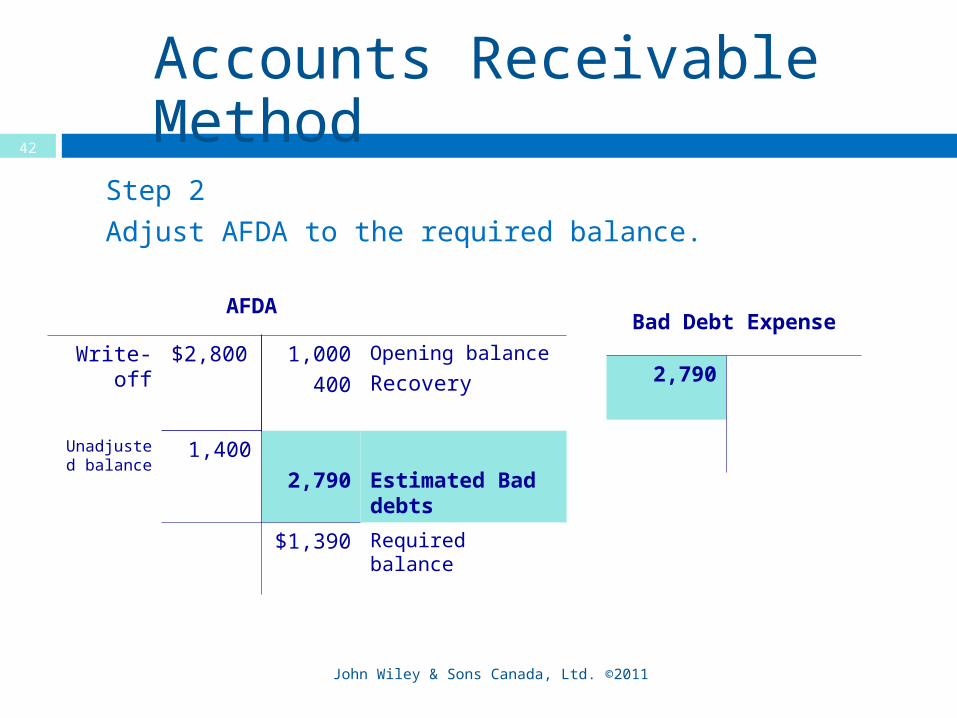

Accounts Receivable Method

Step 2

Adjust AFDA to the required balance.

AFDA

Write-off $2,800 1,000400

Opening balance

Recovery

Unadjusted balance

1,4002,790 Estimated Bad

debts

$1,390 Required balance

John Wiley & Sons Canada, Ltd. ©2011

Bad Debt Expense

2,790

42

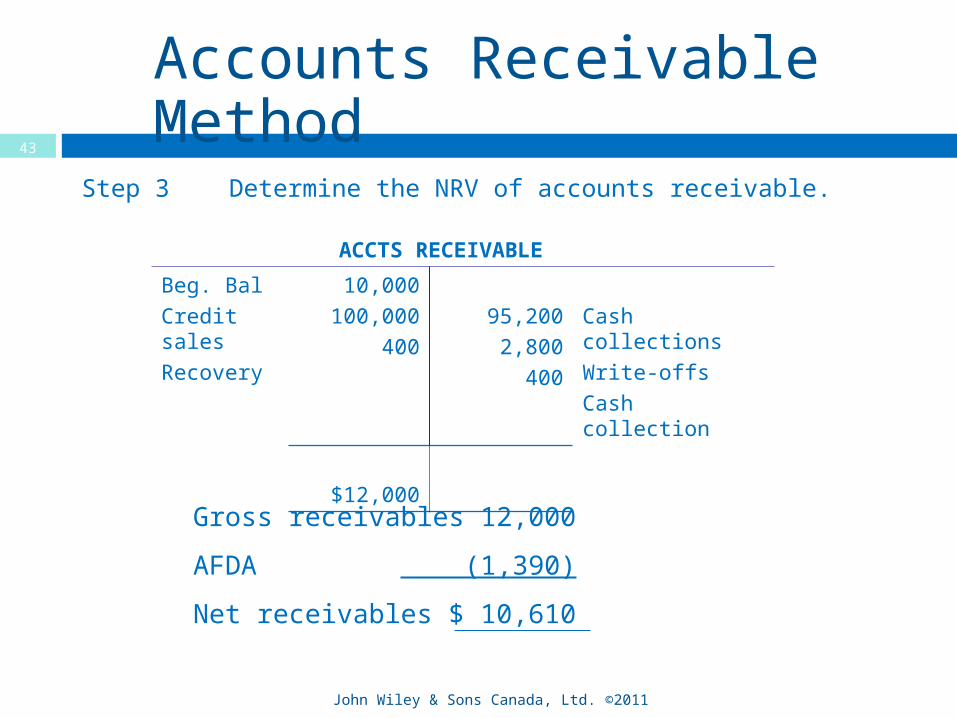

Accounts Receivable Method

Step 3 Determine the NRV of accounts receivable.

ACCTS RECEIVABLE

Beg. BalCredit salesRecovery

10,000100,000

40095,200

2,800400

Cash collectionsWrite-offsCash collection

$12,000

John Wiley & Sons Canada, Ltd. ©2011

43

Gross receivables 12,000

AFDA (1,390)

Net receivables $ 10,610

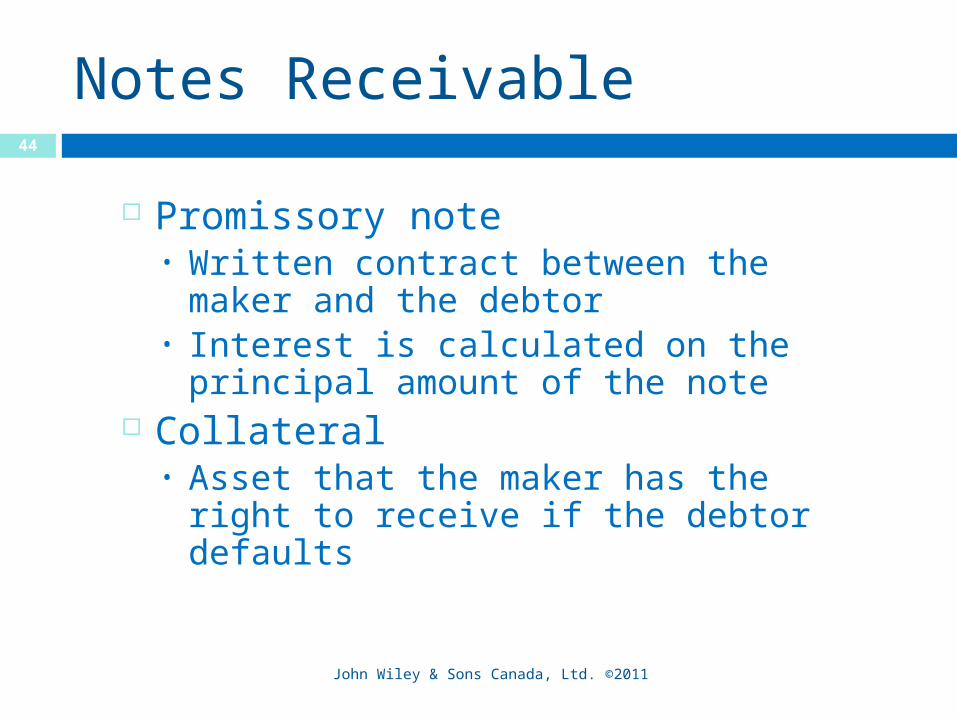

Notes Receivable

John Wiley & Sons Canada, Ltd. ©2011

Promissory note• Written contract between the maker

and the debtor• Interest is calculated on the principal

amount of the note Collateral

• Asset that the maker has the right to receive if the debtor defaults

44

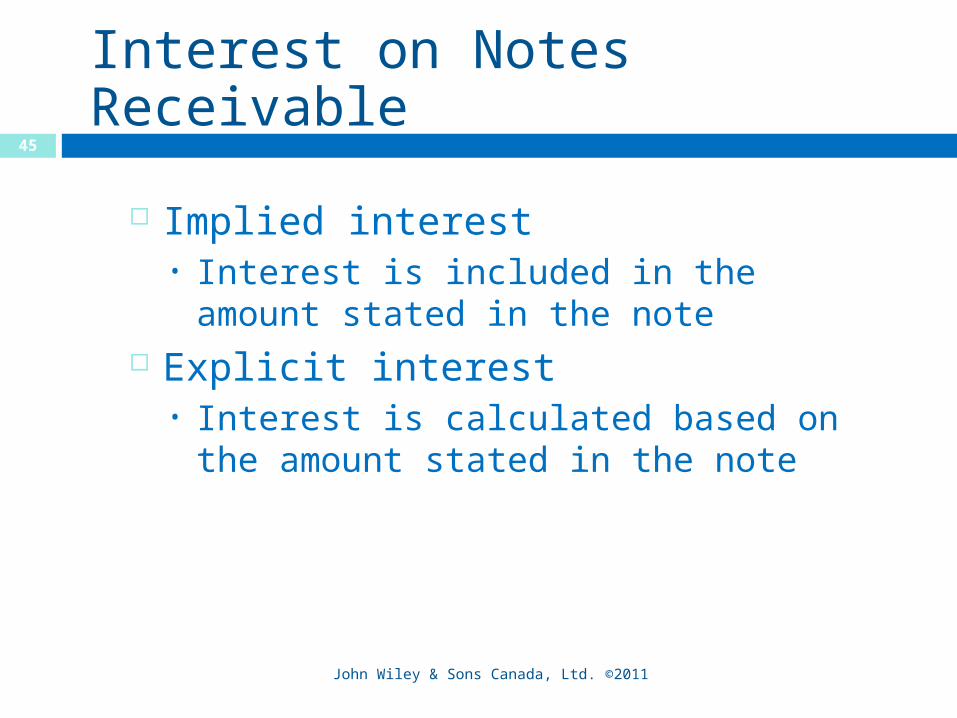

Interest on Notes Receivable

John Wiley & Sons Canada, Ltd. ©2011

Implied interest• Interest is included in the amount

stated in the note Explicit interest

• Interest is calculated based on the amount stated in the note

45

Interest on Notes Receivable

Short-term notes receivable• Simple interest calculations

Long-term notes receivable• Compound interest calculations

John Wiley & Sons Canada, Ltd. ©2011

46

Simple Interest Formula

John Wiley & Sons Canada, Ltd. ©2011

Interest = Principal x Interest Rate x Time

Principal - amount borrowed

Interest Rate - stated as a yearly amount

Time - stated as a fraction of year

47

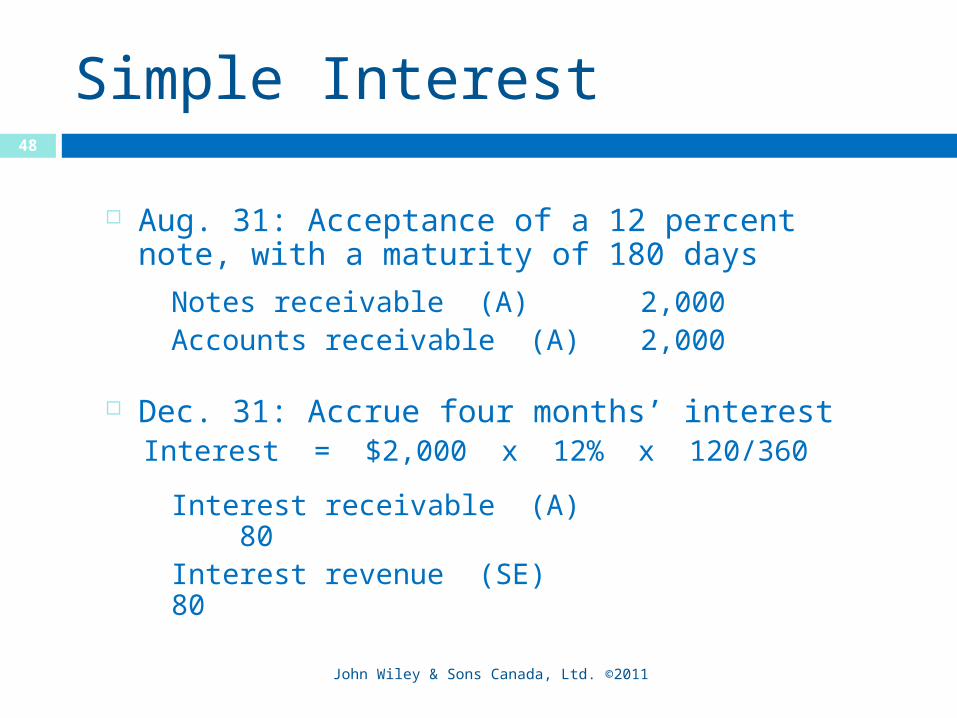

Simple Interest

John Wiley & Sons Canada, Ltd. ©2011

Aug. 31: Acceptance of a 12 percent note, with a maturity of 180 days

Notes receivable (A) 2,000Accounts receivable (A)

2,000

Dec. 31: Accrue four months’ interestInterest = $2,000 x 12% x 120/360

Interest receivable (A) 80Interest revenue (SE)

80

48

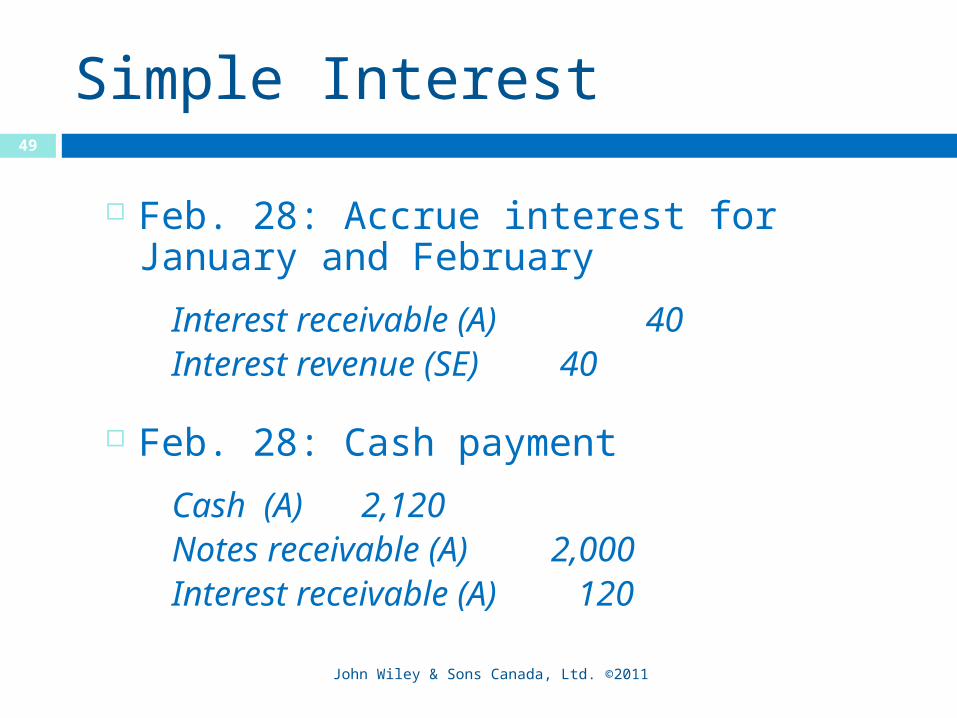

Simple Interest

John Wiley & Sons Canada, Ltd. ©2011

Feb. 28: Accrue interest for January and February

Interest receivable (A) 40Interest revenue (SE) 40

Feb. 28: Cash payment

Cash (A) 2,120Notes receivable (A) 2,000Interest receivable (A) 120

49

Short-Term Liquidity

John Wiley & Sons Canada, Ltd. ©2011

Liquidity• The ability to convert assets into cash to pay

liabilities• Measures

• Current ratio• Quick ratio

50

Evaluate the liquidity of Sony Corporation

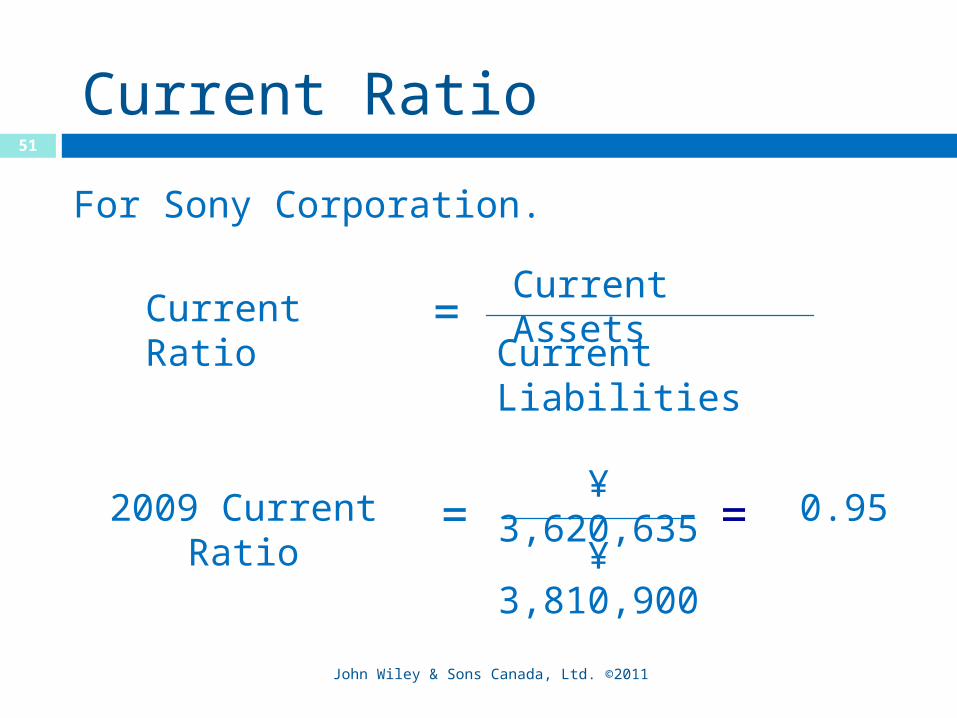

Current Ratio

John Wiley & Sons Canada, Ltd. ©2011

Current Ratio =Current Assets

Current Liabilities

2009 Current Ratio

=¥ 3,620,635

¥ 3,810,900

= 0.95

For Sony Corporation.

51

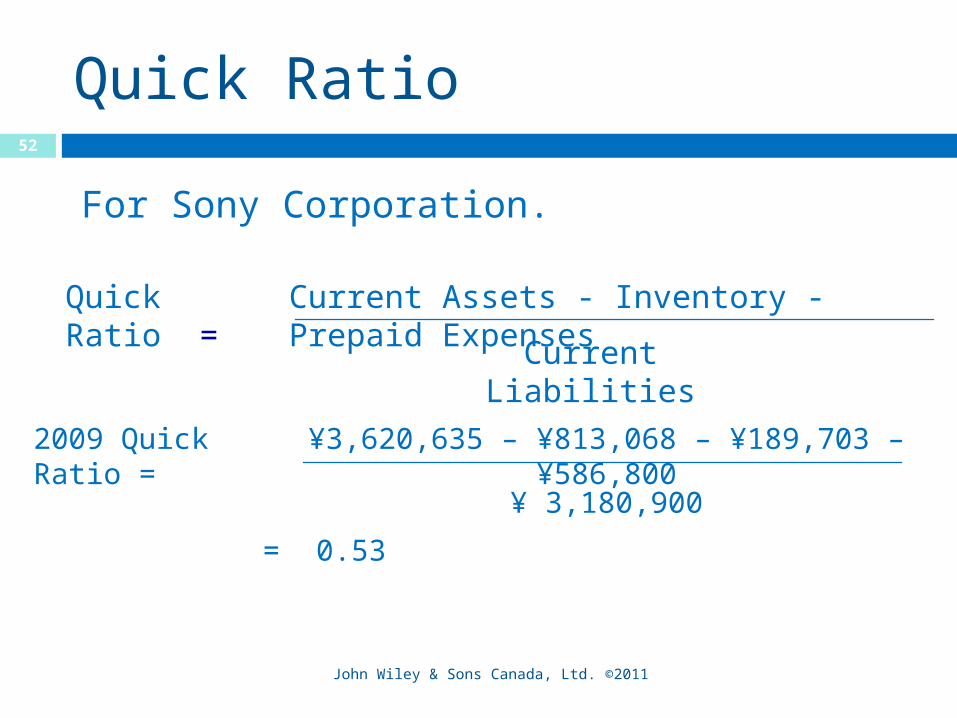

Quick Ratio

John Wiley & Sons Canada, Ltd. ©2011

Quick Ratio =

Current Assets - Inventory - Prepaid Expenses Current Liabilities

¥3,620,635 – ¥813,068 – ¥189,703 – ¥586,800

¥ 3,180,900

= 0.53

For Sony Corporation.

52

2009 Quick Ratio =

Accounts Receivable Turnover

John Wiley & Sons Canada, Ltd. ©2011

Accounts Receivable

Turnover Ratio

= Credit Sales

Average Accounts Receivable

Accounts Receivable Turnover for 2009 = ¥7,110,053

(¥853,454 + ¥1,090,285)/2

= 7.3

For Sony Corporation

Collection Period = 365

7.3= 50

days

53

Copyright © 2011 John Wiley & Sons Canada, Ltd. All rights reserved. Reproduction or translation of this work beyond that permitted by Access Copyright (The Canadian Copyright Licensing Agency) is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons Canada, Ltd. The purchaser may make back-up copies for his / her own use only and not for distribution or resale. The author and the publisher assume no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

Copyright54