ALM for Life Insurers, 18–19 Sepetember 2013 AllianceBernstein.com Erik Vynckier Chief Investment Officer—Insurance (EMEA) Wien/Vienna 28 May 2015 Preparing the Buy-Side to Optimize Collateral 4 th Annual Collateral Management Forum

Transcript

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Erik Vynckier Chief Investment Officer—Insurance (EMEA)

Wien/Vienna 28 May 2015

Preparing the Buy-Side to Optimize Collateral4th Annual Collateral Management Forum

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

�Planning Liquidity with Potential Future Exposure

�High Performance Computation

�Operating Model: the Integrated Front-to-Back Office

8

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

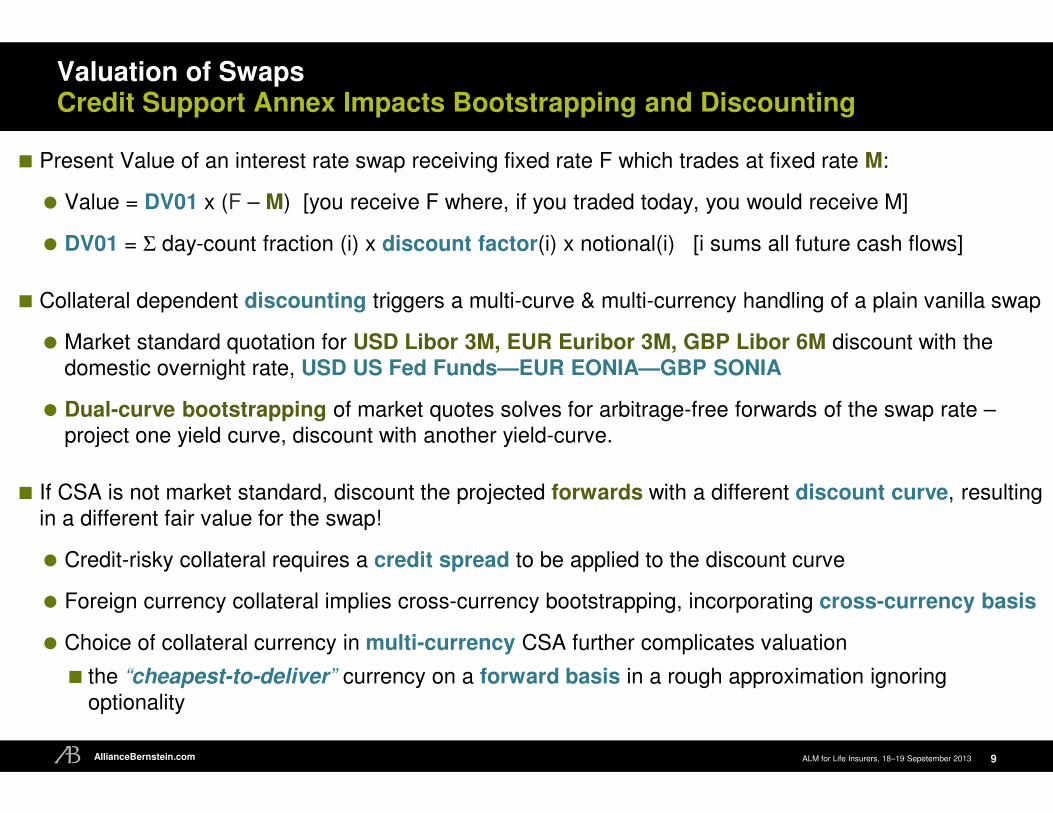

Valuation of SwapsCredit Support Annex Impacts Bootstrapping and Discounting

�Present Value of an interest rate swap receiving fixed rate F which trades at fixed rate M:

�Value = DV01 x (F – M) [you receive F where, if you traded today, you would receive M]

�DV01 = Σ day-count fraction (i) x discount factor(i) x notional(i) [i sums all future cash flows]

�Collateral dependent discounting triggers a multi-curve & multi-currency handling of a plain vanilla swap

�Market standard quotation for USD Libor 3M, EUR Euribor 3M, GBP Libor 6M discount with the

domestic overnight rate, USD US Fed Funds—EUR EONIA—GBP SONIA

�Dual-curve bootstrapping of market quotes solves for arbitrage-free forwards of the swap rate –project one yield curve, discount with another yield-curve.

� If CSA is not market standard, discount the projected forwards with a different discount curve, resulting

in a different fair value for the swap!

�Credit-risky collateral requires a credit spread to be applied to the discount curve

�Planning Liquidity with Potential Future Exposure

�High Performance Computation

�Operating Model: the Integrated Front-to-Back Office

23

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

New Operating Model for Investment Management

24

�Front-office needs to understand collateral and liquidity consequences of its investment

decisions

�Back-office not just an operation task but crucial input into asset allocation, asset-liability management, hedging best practices, reporting and compliance

�Collateral and liquidity management a critical input into overall balance sheet and capital

management of bank, insurer, pension fund

�Product Pricing and Product Development in Banking, Insurance and Pensions require

accurate liquidity pricing and sound collateral practices

�Position monitoring and liquidity analytics need to upgrade so as to accurately report & plan collateral & liquidity

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Read Up and Connect with Colleagues

25

�Clear Path Analysis study: “Collateral Management for Institutional Investors”

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Disclaimer

�This information is issued by AllianceBernstein Limited, 50 Berkeley Street, London W1J 8HA,

a company registered in England under company number 2551144. AllianceBernstein Limited is authorised and regulated in the UK by the Financial Conduct Authority (FCA – Reference

Number 147956). This information is directed at Professional Clients only. It is provided for informational purposes only and is not intended to be an offer or solicitation, or the basis for any

contract to purchase or sell any security, product or other instrument, or for AllianceBernstein to

enter into or arrange any type of transaction as a consequence of any information contained

herein. The views and opinions expressed in this document are based on AllianceBernstein's

internal forecasts and should not be relied upon as an indication of future market performance. Past performance is no guarantee of future returns. This information is not intended for public