26

docuformas.mx Docuformas Corporate Presentation 2018

docuformas.mx

Docuformas

Corporate Presentation 2018

docuformas.mx

Disclaimer

This document may contain certain forward-looking statements. These statements are non-historical facts, and they are based on the current vision of the Management ofDocuformas S.A.P.I. de C.V. for future economic circumstances, the conditions of theindustry, the performance of the Company and its financial results. The terms "anticipated","believe", "estimate", "expect", "plan" and other similar terms related to the Company, aresolely intended to identify estimates or predictions. The statements relating to theimplementation of the main operational and financial strategies and plans of investment ofequity, the direction of future operations and the factors or trends that affect the financialcondition, the liquidity or the operating results of the Company are examples of suchstatements. Such statements reflect the current expectations of the management and aresubject to various risks and uncertainties. There is no guarantee that the expected events,trends or results will occur. The statements are based on several suppositions and factors,including economic general conditions and market conditions, industry conditions andvarious factors of operation. Any change in such suppositions or factors may cause theactual results to differ from expectations.

All figures are expressed in Mexican Pesos ($) unless otherwise stated, and were preparedin accordance with the requirements from the National Banking and Securities Commission(CNBV). Figures for year ended 2015, 2016 and 2017 were assessed by independentauditors Galaz, Yamazaki, Ruiz Urquiza, S.C. (Members of Deloitte Touche TohmatsuLimited).

2

docuformas.mx

Docuformas’ Key Milestones

Docuformas acquires ARG, a leasing company specialized in transportation , creating the #2 biggest independent leasing player in Mexico.

Initial integration of the ARG acquisition.

Docuformas acquires ICI, expanding into the real estate lending business, and finalizes the ARG integration.

Docuformas taps international markets, issuing U.S. $150 million senior notes with 9.25% coupons.

1996 2006 2008 2010 2012 2014 2015 2016 2017 2018

Docuformas isfounded by AdamWiaktor with afocus on Xeroxleasing equipment.

Docuformas taps local capital markets, becoming the first mid-sized company to issue local debt in the Mexican Market.

Colony Capital(formerly Aureos) invests in Docuformas.

Docuformas issues structured public debt secured by its receivables.

Master Franchise Agreement is signed with Liquid Capital Corp and Liquid Capital Mexico is born.

Colony Capital and Alta Growth Capital invest U.S. $27 million in Docuformas. Counterparty rating increment to “BB-”

3

docuformas.mx

Docuformas at a Glance

• Leading independent leasing company in

Mexico, providing specialized financing

including leases, loans and factoring.

• Experienced management team, focused on

profitable growth, robust risk management and

compliance with high governance standards

• We target the rapidly growing and under-banked SME segment.

• Tailored products to finance specializedproductive assets.

• Personalized assessment and quick responsetime to clients.

Competitive Advantages:

1

2

3

Portfolio Breakdown

4

85%

14%1% Leasing Portfolio

Credit & FactoringPortfolio

Services Portfolio

Key Financial Indicators 2016 2017 12M18

R O A A 4.6% 2.5% 2.4%

R O A E 29.2% 18.4% 14.8%

Financial Debt / Stockholders´ Equity 4.3x 5.6x 3.7x

Net Financial Debt / Stockholders´ Equity 3.7x 3.9x 2.9x

Capitalization (SE/TA) 15.1% 13.0% 19.0%

Stockholder' Equity/ Total Portfolio 17.1% 17.2% 24.0%

Leasing Portfolio / Total Portfolio 78.6% 91.8% 85.3%

Total Portfolio / Financial Debt 1.4x 1.0x 1.1x

Total Portfolio / Net Financial Debt 1.6x 1.5x 1.5x

Current Assets/ Current Liabilities 1.1x 2.9x 2.3x

Financial Debt (MXN$mm) 2,856 4,443 5,178

Net Financial Debt (MXN$mm) 2,427 3,135 3,957

docuformas.mx

Leading and Established Leasing Specialist

A differentiated and established platform

The industry is characterized by "barriers to scaling"rather than “barriers to entry”, where players' lack ofaccess to financing stands out.

23 years of experience meeting the needs of SMEs in Mexico.

Tailor-made systems and technology.

Mix of third-party and in-house IT solutions.

Robust and efficient origination and collections processes.

Purchasing power with equipment manufacturers, dealers and suppliers.

Access to multiple, reliable and competitive funding sources.

Focus on employee developmentthrough constant training systems.

7. Highly experienced team

6. Consistent revenue growth & profitability

2. Rapid origination

5. Prudent leverage policy

4. Efficient operating platform

1. Diverse product strategy

3. Diversified portfolio

docuformas.mx 5

docuformas.mx

Corporate Structure and recent Capital Injection

Shareholder Prior New

Adam Wiaktor 67.9% 14.5%

Aureos Latin America Fund I and Fondo Aureos Colombia

32.1%

Alta Growth Capital Fund 35.7%

CKD (Colony Capital) 24.9%

Abraaj Thames B.V. (The Abraaj Group)

24.9%

Total 100% 100%

New investment previously reported of US $27million was completed during the 3th and 4thquarter 2018.

Mr. Adam Wiaktor continues as CEO ofDocuformas as well as a member of the Boardof Directors

35.7%

Corporate Structure

Adam Wiaktor

Docuformas, S.A.P.I. de C.V.

Analistas de Recursos Gobales, S.A.P.I. de C.V.

Rentas y Remolques de México, S.A.P.I. de C.V.

Inversiones y Colocaciones Inmobiliarias, S.A.P.I. de C.V.

14.6%49.8%

99.9%

99.9%

99.9%

Colony Capital funds

Alta Growth Capital funds

6

docuformas.mx

Well-Designed and Flexible Product Offering•

Leasing

Capital• Product lease with option to purchase

at the end of the term. 24-36 months

MXN $1-40mm

Equipment• Product lease without option to

purchase at end of the term.

Real Estate• Sale and lease back of real estate

assets.

5-7 years

MXN $15-60mm

Renting• Equipment leasing with supplies,

service and maintentance.

12-36 months

MXN $1-10mm

Factoring• Discounting A/R and provision of

vendor-financing and revolving credit lines.

30-60 days

MXN $1-20mm

Financing

Cash • Secured and unsecured cash loans as

non-asset-based lending.24-36 months

MXN $1-40mmEquipment

• Purchase and resale or lease of equipment with financing. Equipment serves as collateral.

7

docuformas.mx

Underserved Mexican SME Market

Characteristics of our clients

• Underbanked.

• Not price sensitive.

• Receptive to good service, including:

Approval speed.

Flexibility around customized solutions.

• Drawn to:

Simpler documentation.

No covenants.

Tax shield provided by lease payments.

Note:Sourced from INEGI & CNBVSourced from worldbank.org

97.4%

12.9%

2.6%

87.1%

% of entities % of loansSME Other

Underserved Mexican SMEs

SME entities (% of entities in 2015) and SME loan participation (% of loans in 2016)

1

Financing the Mexican SMEs is an attractive opportunity with significant growth potential.

8

docuformas.mx

Leasing portfolio (% of 2016 GDP)

Underserved Mexican SMEs

Underpenetrated financial system

Opportunity for financing, particularly in the leasing space

192.7%

112.1%62.2% 47.2% 36.2% 35.0%

Domestic credit to the private sector (% of 2016 GDP)

8.5%

2.4% 2.0% 1.7%0.7% 0.2%

Why are SME clients underbanked?

Banks are not set up to cater to SMEs' needs.

Banks have heavy fixed cost structures that make SMEs unattractive clients due to smaller “ticket size”.

Banks' reputational and legal risk burden makes KYC* requirements onerous.

Banks have stricter reserve and capitalization requirements.

Note:KYC: “know your customer”Sourced from INEGI & CNBVSourced from worldbank.org

9

docuformas.mx

Powerful and Effective Go-to-Market Model

Geographic reach extends beyond physical presence

Portfolio Presence

Presence in 30 states, over 93% of the

country.

Client knowledge drives credit quality and recurring business

Salesperson responsibilities:

Clients per Business Unit is limited to 30, and potential credit risks are spotted early on through communication with clients at least once a month.

Incentive-based compensation.

~60% of lease approval cases correspond to recurring clients.

Adversity to government risk through geographic diversification.

CollectionProcess

OriginationRelationshipManagement

10

docuformas.mx

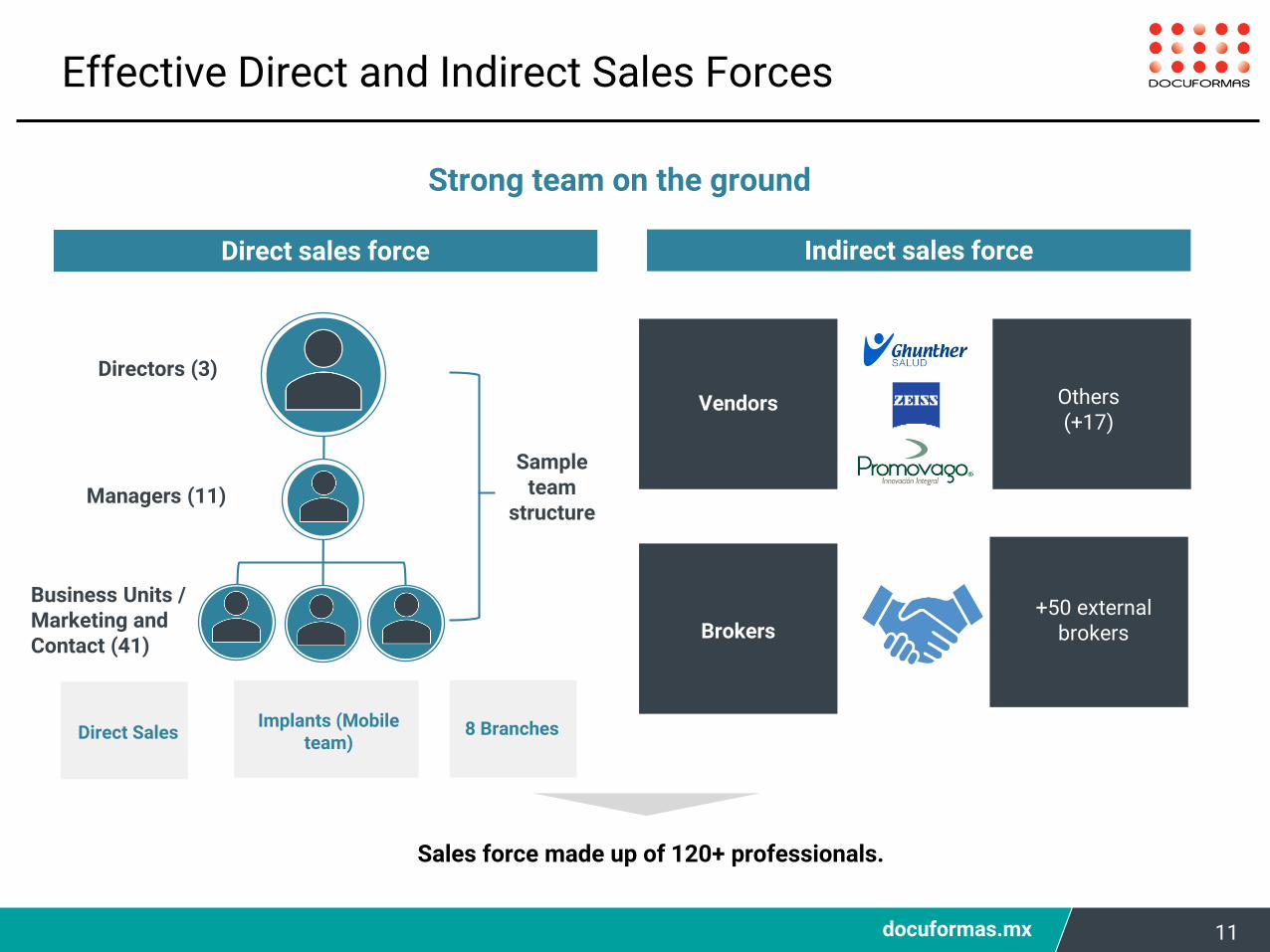

Effective Direct and Indirect Sales Forces

Sales force made up of 120+ professionals.

Others (+17)

+50 external brokers

Indirect Sales Force

Vendors

Brokers

Indirect sales forceDirect sales force

Strong team on the ground

Directors (3)

Managers (11)

Business Units / Marketing and Contact (41)

Sample team

structure

Direct SalesImplants (Mobile

team)8 Branches

11

docuformas.mx

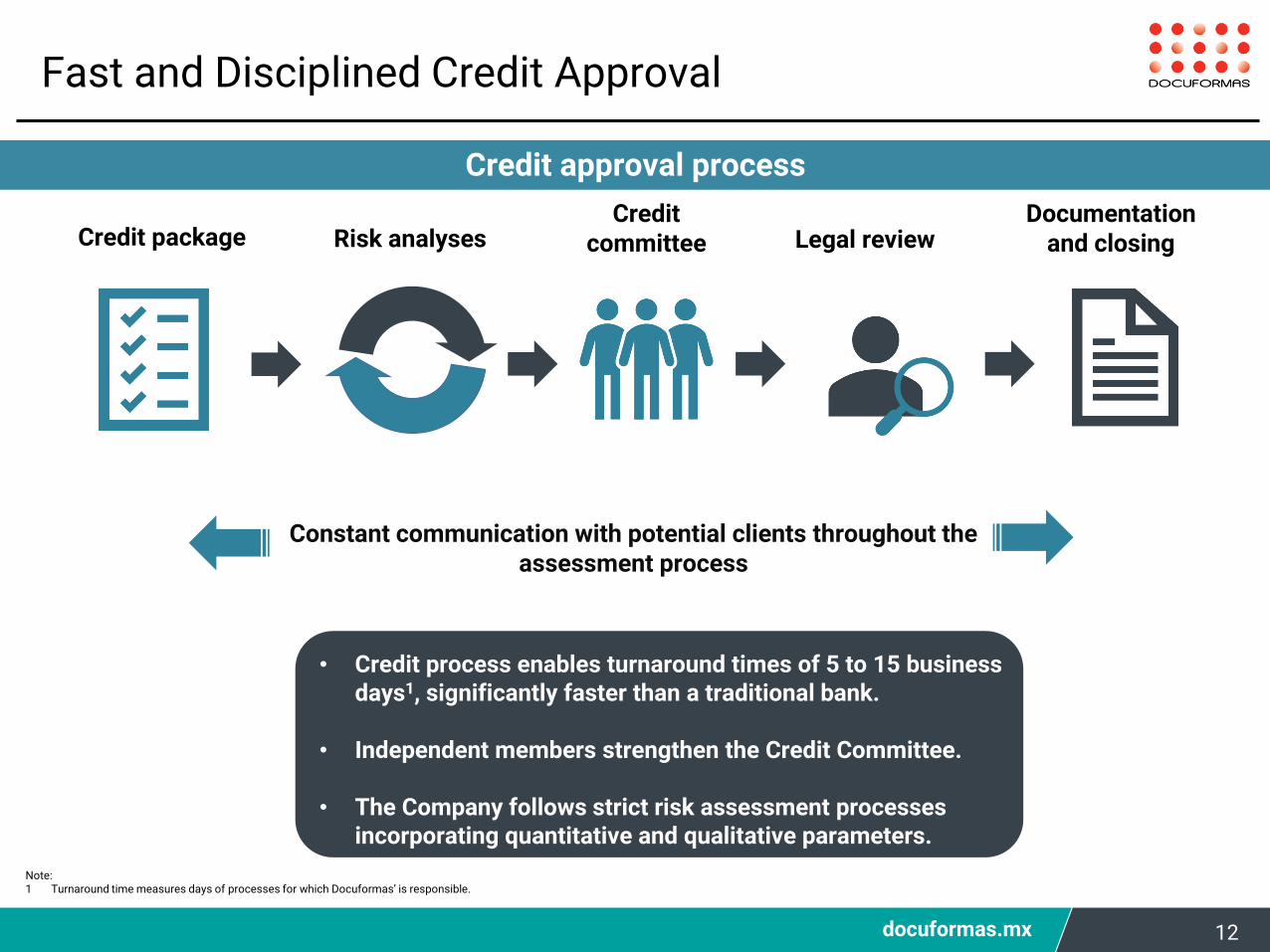

Fast and Disciplined Credit Approval

Credit approval process

Note:1 Turnaround time measures days of processes for which Docuformas’ is responsible.

Credit package Risk analysesCredit

committee Legal reviewDocumentation

and closing

Constant communication with potential clients throughout the assessment process

• Credit process enables turnaround times of 5 to 15 business days1, significantly faster than a traditional bank.

• Independent members strengthen the Credit Committee.

• The Company follows strict risk assessment processes incorporating quantitative and qualitative parameters.

12

docuformas.mx

Efficient Collection Process

The collection process is greatly facilitated by Docuformas maintaining ownership of leased assets.

Invoice Current Past dueNon-performing/ repossession

Automatically generated on the 5th day of every month

(<30 days) (31 to 90 days) (>90 days)

Contracts are marked as non-performing

Invoice Generation.

Payment received by the end of the month.

No payment received by the end of the

month.

Payment or revised payment schedule

negotiation.

Failure to pay within 90 days of receiving

invoice.

Payment or revised payment schedule

negotiation.

Repossession, re-lease or sale after

120 days.

3

?

3

?

3

?

Variable compensation structure incentivizes successful collection.

Constant dialogue enables Business Units to spot credit

risks early on.Negotiations are facilitated by

pledged assets & guarantees as well as legal action and

repossession. Assets generally have strong secondary markets.

Business units are responsible for the collection process and are in constant communication with clients.

13

docuformas.mx

933 1,005

1,414

2016 2017 2018

Origination and Top-Line Growth

Top-line expansion

Strong portfolio growth

Portfolio (MX$mm)

Note:1 Run-off is defined as the minimum contracted payments that were expected to come due as of the end of the previous period (See Notes 7, 8 and 9 of the Audited Financial Statements).2 Net origination is defined as portfolio originated and acquired throughout the year, net of run-off from portfolio originated within that year.

Total revenues (MX$mm)

14

Consistent top line growth year over year since its inception ,due to:

Specific target market Competitive go to market strategy

Strong corporate practices Experienced management

3,648

1,396

1,631 3,883

1,856

2,603 4,630

1,927

3,086 5,789

2015 Run-off¹ Origination² 2016 Run-off¹ Origination² 2017 Run-off¹ Origination² 12M18

docuformas.mx

531

396 466

25.4%

20.5%19.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

-

100

200

300

400

500

600

2016 2017 12M18

Gross Profit OPEX as % of revenues

Solid Gross Profit Growth with Positive Bottom-Line

ProfitabilityImproving EfficiencyMXN$mm

15

MXN$mm

181

132

162

2016 2017 12M18

docuformas.mx

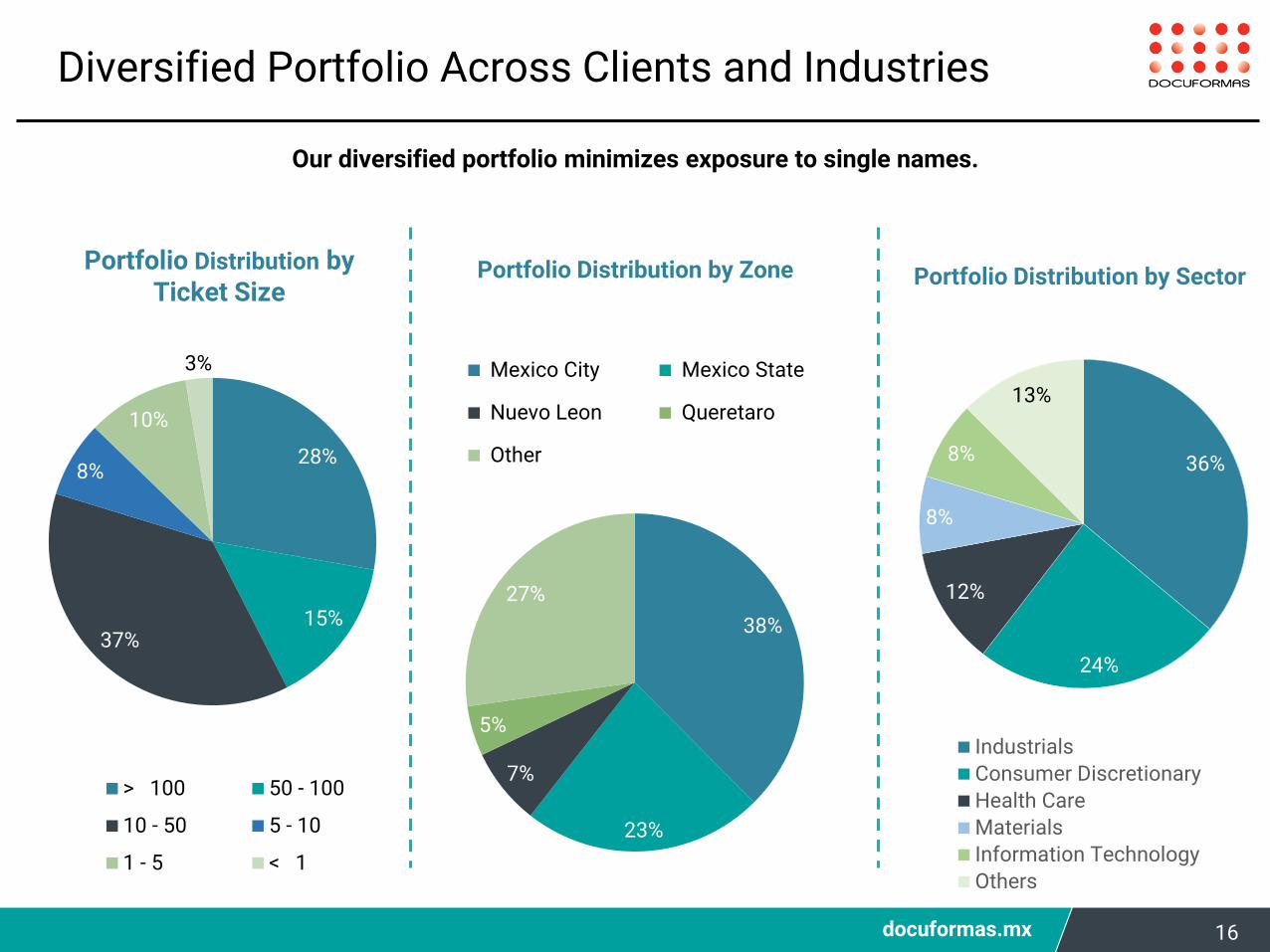

36%

24%

12%

8%

8%

13%

Industrials

Consumer Discretionary

Health Care

Materials

Information Technology

Others

38%

23%

7%

5%

27%

Mexico City Mexico State

Nuevo Leon Queretaro

Other28%

15%37%

8%

10%

3%

> 100 50 - 100

10 - 50 5 - 10

1 - 5 < 1

Diversified Portfolio Across Clients and Industries

Our diversified portfolio minimizes exposure to single names.

16

Portfolio Distribution by Ticket Size

Portfolio Distribution by Zone Portfolio Distribution by Sector

docuformas.mx

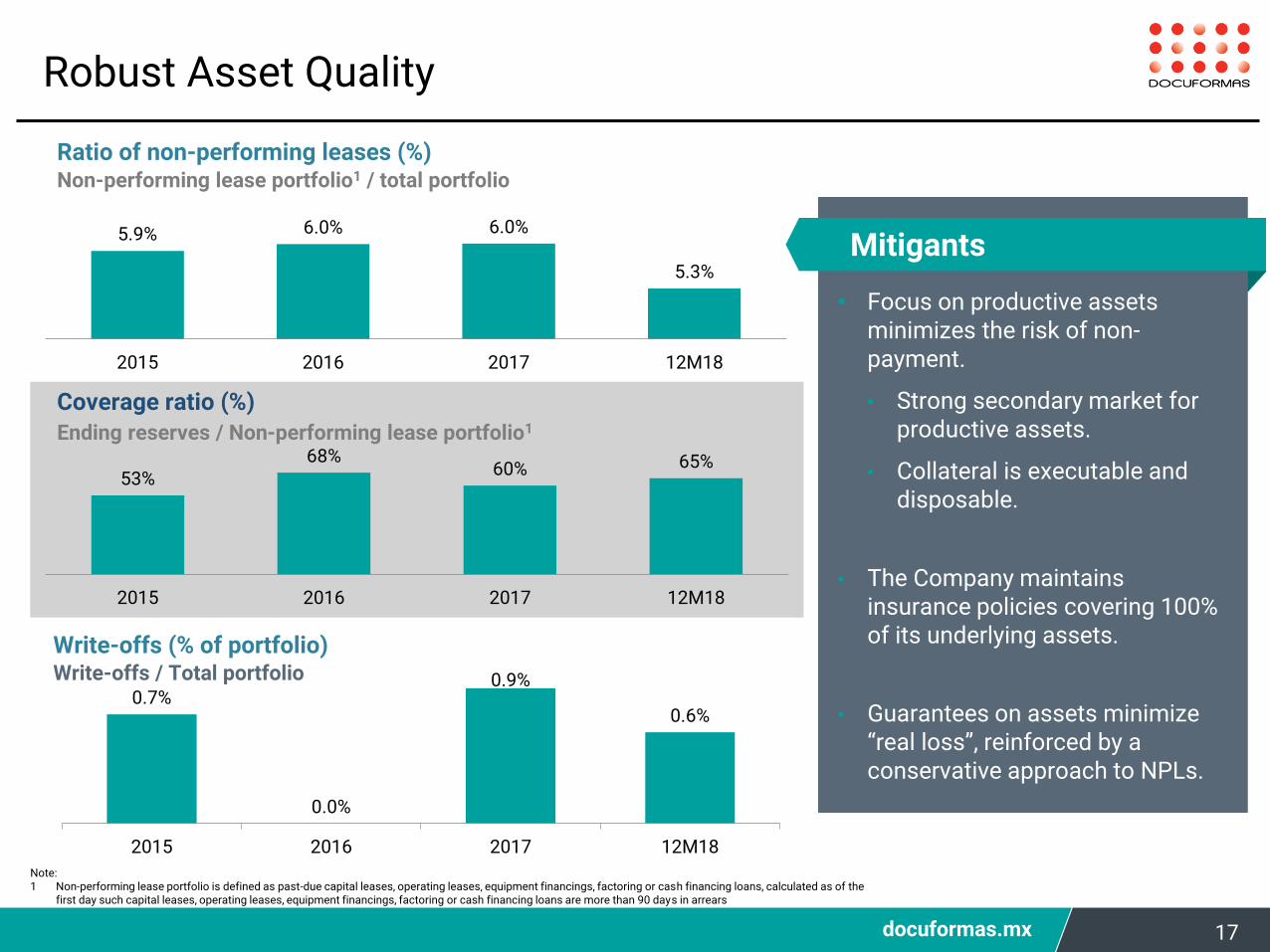

Robust Asset Quality

Ratio of non-performing leases (%)Non-performing lease portfolio1 / total portfolio

Coverage ratio (%)

Ending reserves / Non-performing lease portfolio1

Write-offs (% of portfolio)Write-offs / Total portfolio

Note: 1 Non-performing lease portfolio is defined as past-due capital leases, operating leases, equipment financings, factoring or cash financing loans, calculated as of the

first day such capital leases, operating leases, equipment financings, factoring or cash financing loans are more than 90 days in arrears

• Focus on productive assets minimizes the risk of non-payment.

• Strong secondary market for productive assets.

• Collateral is executable and disposable.

• The Company maintains insurance policies covering 100% of its underlying assets.

• Guarantees on assets minimize “real loss”, reinforced by a conservative approach to NPLs.

Mitigants

17

5.9% 6.0% 6.0%

5.3%

2015 2016 2017 12M18

53%68%

60% 65%

2015 2016 2017 12M18

0.7%

0.0%

0.9%

0.6%

2015 2016 2017 12M18

docuformas.mx

Strong Balance Sheet

Ample Capitalization

Disciplined Leverage

(Total stockholders equity / assets)

(Total financial debt / total shareholders equity)

18

15.1%13.0%

19.0%

2016 2017 12M18

Capitalization Ratio

4.3x5.6x

3.7x

2016 2017 12M18

Leverage Ratio

Financial Debt

docuformas.mx

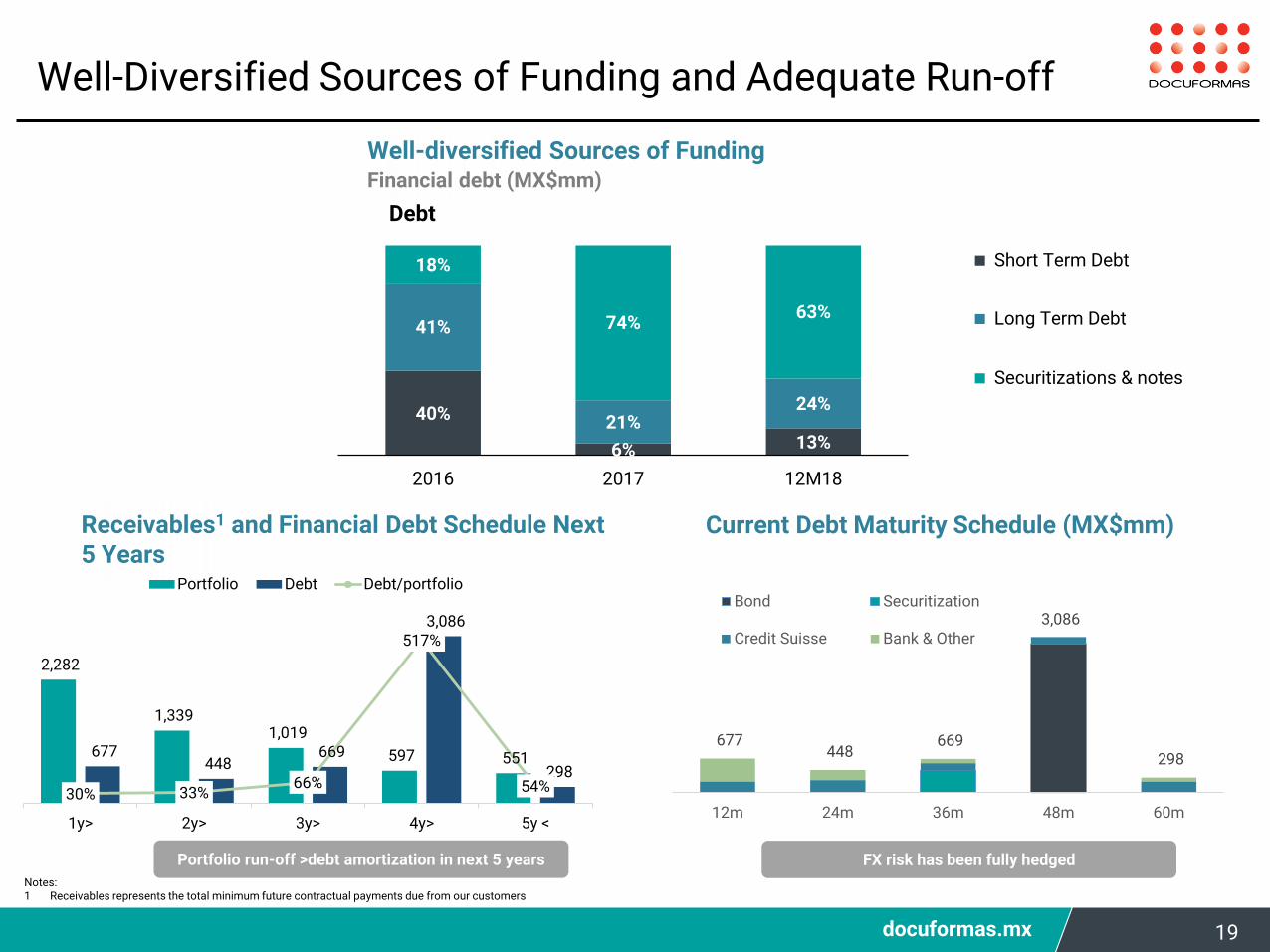

Well-Diversified Sources of Funding and Adequate Run-off

Current Debt Maturity Schedule (MX$mm)

FX risk has been fully hedged

Notes:1 Receivables represents the total minimum future contractual payments due from our customers

Receivables1 and Financial Debt Schedule Next 5 Years

Portfolio run-off >debt amortization in next 5 years

Well-diversified Sources of FundingFinancial debt (MX$mm)

19

40%

6% 13%

41%

21%24%

18%

74%63%

2016 2017 12M18

Debt

Short Term Debt

Long Term Debt

Securitizations & notes

2,282

1,339 1,019

597 551 677 448

669

3,086

298

30% 33%66%

517%

54%0%

100%

200%

300%

400%

500%

600%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

1y> 2y> 3y> 4y> 5y <

Portfolio Debt Debt/portfolio

677 448

669

3,086

298

12m 24m 36m 48m 60m

Bond Securitization

Credit Suisse Bank & Other

docuformas.mx

4.4%

3.5%

2.3% 2.5%

2015 2016 2017 12M18

High Levels of Operational Efficiency

Workforce has been optimized following the ARG acquisition

Strong levels of operational efficiency have historically been achieved

The sales force operates under a variable compensation structure

Headcount evolution (# of employees) Incentive-based compensation breakdown (%)

Administrative expenses / total assets (%) Efficiency ratio (%)1

Compensation structure aligns incentives

Business Units are in charge of collection process as well as origination

Constant dialogue improves credit risk

Note:1. Efficiency Ratio is defined as operating expenses divided by Gross Income

Collection 2/3

Origination 1/3

20

137101 90 77

75

7658

57

2015 2016 2017 12M18

Corporate Sales

48.9% 44.7%52.0%

59.0%

2015 2016 2017 12M18*

docuformas.mx

Experienced Management - Strong Corporate Governance

Highly qualified Board of Directors

Strong Corporate Governance practices

Management team with more than 12 years of experience on average.

The board of directors is comprised of 8 members.

Robust corporate governance gives Docuformas an edge versus its peers.

Miguel ÁngelOlea Sisniega

Eduardo Cortina Murrieta

Experienced Management Team

Name PositionYears of

ExperienceYears at

Docuformas

Se

nio

r M

an

ag

em

en

t

Adam P. Wiaktor

Chief Executive Officer 33 23

Alejandro Monzó

Deputy CEO 20 1

Hector Esquivel

Chief Financial Officer 30 3

Eduardo Limón

Investor Relations Officer

27 12

Ricardo Vazquez

Human Resources Director

19 4

Gerardo Gutierrez

Chief Technology Officer 38 5

Alejandro Pacheco

Director of Credit 25 4

Patricia Barrera

General Counsel 18 4

Antonio Bañuelos

Structuring and Collections Director

21 12

GumersindoChavez

Procurement Officer 36 13

Erika Nuñez Process Director 16 5

Sales

Danilo Sarrelangue

Sales Director 22 19

Carlos Durán Sales Director 22 6

Name Position

Miguel Ángel Olea Sisniega President

Eduardo Cortina Murrieta Advisor Colony

Ignacio Gómez-Urquiza Advisor Colony

Erik Carlberg y González de la Vega Advisor Alta

Javier García-Teruel Ávila Advisor Alta

Alejandro Renteria Villagomez Advisor Alta

Adam Wiaktor Rynkiewicz Advisor

Miguel Ángel Noriega Cándano Independent Advisor

21

docuformas.mx

Investor Relations Contact Information

Contact Information

For more information visit

www.docuformas.mx

or contact:

Miranda Investor Relations

Ana María Ybarra Corcuera

+52 1 (55) 3660 4037

Eduardo Limón

Investors Relation Officer

+52 (55) 4324 3434

Ramón Barreda Barrera

Investors Relation Deputy Director

+52 (55) 5148 3600 / (55) 9178 6370

22

docuformas.mx 23

Financial Summary

docuformas.mx

Financial and Operating Summary

Key metrics and financial highlights

24

*In millions of pesos

Financials Metrics (in millions of pesos) 2016 2017 12M18Total Revenues 933 1,005 1,414 Cost of Revenues 402 609 948 Gross Profit 531 396 466 % 57% 39% 33%Operating Expenses 237 207 275 Net Income 181 132 162 % 19% 13% 11%

Operating Metrics (in millions of pesos) 2016 2017 12M18Total Portfolio 3,883 4,630 5,789 Leasing Portfolio 3,052 4,250 4,939 Credit & Factoring Portfolio 709 290 784 Services Portfolio 122 89 65 NPL 6.0% 6.0% 5.3%

Real Estate Portfolio 271 510 726 Total Portfolio including Real Estate 4,154 5,140 6,515

Financial Indicators 2016 2017 12M18R O A A 4.6% 2.5% 2.4%R O A E 29.2% 18.4% 14.8%Financial Debt / Stockholders´ Equity 4.3x 5.6x 3.7xNet Financial Debt / Stockholders´ Equity 3.7x 3.9x 2.9xCapitalization (SE/TA) 15.1% 13.0% 19.0%Stockholder' Equity/ Total Portfolio 17.1% 17.2% 24.0%Leasing Portfolio / Total Portfolio 78.6% 91.8% 85.3%Total Portfolio / Financial Debt 1.4x 1.0x 1.1xTotal Portfolio / Net Financial Debt 1.6x 1.5x 1.5xCurrent Assets/ Current Liabilities 1.1x 2.9x 2.3xFinancial Debt (MXN$mm) 2,856 4,443 5,178Net Financial Debt (MXN$mm) 2,427 3,135 3,957

docuformas.mx

Income Statement

25

REVENUES 2016 2017 12M18Interest on capital leases 558 563 675Equipment financing 170 296 546Operating leases 196 145 193Factoring 9 1 0Total income 933 1,005 1,414

COSTSInterest expense 214 351 511Equipment financing 88 151 344

Depreciation of assets under operating leases 100 107 93

Total costs 402 609 948

GROSS INCOME 531 396 466Selling expenses 22 17 25Administrative expenses 153 142 180Allowance for loan losses 63 48 70Operating expenses 237 207 275

OPERATING INCOME 293 189 191Other (income) expenses, net (0) (2) 9

Interest income (2) (88) (10)Interest expenses 50 58 49Net exchange loss (profit) 9 135 (5)

Valuation of derivative financial instruments (5) 10 (44)

Comprehensive financing result 52 115 (10)

INCOME BEFORE INCOME TAXES 242 76 192Income taxes 61 (56) 30NET INCOME 181 132 162

*In millions of pesos

docuformas.mx

Balance sheet*In millions of pesos

26

ASSETS 2016 2017 12M18

Current Assets

Cash and cash equivalents 429 1,308 1,221

Accounts receivable 1,545 1,115 1,277

Allowance for loan losses 0 164 198

Taxes due from 116 107 191

Sundry debtors 22 27 28

Related parties due from 19 3 37

Other assets 37 65 31

Inventory 0 0 11

Total current assets 2,168 2,789 2,994

Non-current assets

Property-furniture and equipment - net 651 870 1,059

Long-term receivable 1,300 2,131 2,899

Other assets 81 169 178

Derivative financial instruments 19 10 -2

Goodwill 164 163 163

Total non-current assets 2,215 3,343 4,297

Total assets 4,383 6,132 7,291

LIABILITIES 2016 2017 12M18

Current liabilities

Current portion of long-term debt 1,254 256 677

Accounts payable 94 163 33

Sundry creditors 283 381 551

Due to related parties 273 75 9

Income taxes and other taxes payable 49 94 29

Total current liabilities 1,953 969 1,299

Non-current liabilities

Long-term debt 1,602 4,187 4,501

Deferred income tax 165 181 181

Derivative financial instruments 0 0 -77

Total non-current liabilities 1,767 4,368 4,605

Total liabilities 3,720 5,337 5,904

STOCKHOLDERS' EQUITY & RESERVES

Capital stock & retained earnings 482 663 1,322

Valuation of derivative financial intstruments 0 0 -97

Current year net income 181 132 162

Total Stockholders' equity and reserves 663 795 1,387

Total liabilities and stockholders' equity and reserves 4,383 6,132 7,291

Capital stock & retained earnings 482 663 1,322