Structural deficit under 0,5 % of GDP, excepted in case of special circumstances for countries with public debt superior to 60 % of GDP

Public debt have to be reduced by 1/20 each year. Countries under excess deficit procedure have to make “sufficient efforts”

4

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Fiscal surveillance

• Transposition of the new European rules on fiscal governance:

Implementation of the Fiscal compact: independent fiscal institutions must be in charge in charge of checking compliance with fiscal rules at national level

Anticipation of the “Two Pack” ’s provision: independent macroeconomic forecasts” means macroeconomic forecasts produced or endorsed by independent bodies

5

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Organisational Framework (1)

• In France, several options were originally considered:

Creating an ad hoc authority, but possibly costly for public finances and credibility has to be built ab initio

Broadening the missions of the Court of Auditors (Cour des comptes): it is endowed with a strong reputational capital, but confusion may appear as regard its ex ante and ex post roles. As well, its legitimacy as a forecasting institution might have have been weak

6

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Organisational Framework (2)

• An intermediate solution: creating an “independent body attached to the Court of Auditors”

A new body associated with the Court of Auditors and chaired by the Head of the Court (Didier Migaud, former head of the Budget Committee in Parliament)

However independent from the Court : its members come from diverse origins, it benefits from its own financial resources, as well as its own staff

7

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Organisational Framework (3)

• Court of Auditors and HCPF have different but complementary roles :

Court of Auditors : an ex post surveillance role. For instance: • Monitoring the implementation of Budget Laws and Social Security

Budget Laws

• Signing off the the State accounts and the Social Security accounts

• Issuing reports on the situation and outlook of public finances (in February and in June)

HCPF : an ex ante surveillance role, in delivering an opinion on a set of public finance texts.

• Attaching the High Council to the Court means: Preserving an institutional coherence between both IFIs

Creating financial and human synergies between the institutions

Ensuring the independence of the new body

8

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

The Court of Auditors

And

Fiscal Surveillance

9

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

History of the Court of Auditors

• One of the oldest public institution of the State, an emanation of the « curia regis » (the king’s court, in the Middle Ages).

• Article 15 of the French Declaration of Human Rights sets out that: « Society has the right to ask any public official to account for its administration »

• The law of 16 September 1807 established the present-day Court of Auditors.

10

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

The « Westminster model »:

The SAI is connected to Parliament.

The « executive model » :

The SAI is connected to the

Executive.

The « equidistant » model:

The SAI is equidistant from

Parliament and from the

Government

SAI Government

Parliament

SAI

Government Parliament

SAI

Government

Parliament

The Supreme Audit Institutions’ models: 3 patterns with a lot of possible variants

11

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

The Court’s equidistance The Court assists Parliament and the Government : it is

not at the disposal of Parliament more than it is at the disposal of Government.

The Court’s equidistance has been confirmed by a decision of the Constitutional Council in 2001 : « the Court of accounts is an administrative jurisdiction ; […] the Constitution ensures its independence from the legislative and from the executive. »

The Court of Auditors carries out some works at the request of Parliament but it remains free to decide on its program : in 2001, the Constitutional Council censored a sentence mentioning that the Court should communicate its draft program to the Parliament’s finance committees for advice.

12

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

A strengthened constitutional mission of assistance to the Government and to

Parliament

• Art. 47-2 of the Constitution :

« The Court of Auditors assists the Parliament in controlling

Government’s action. It assists the Parliament and the Government in

controlling the enforcement of finance laws and the implementation

of laws on the financing of Social Security as well as for the

assessment of public policies. It contributes to inform the citizens

through its public reports.»

13

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

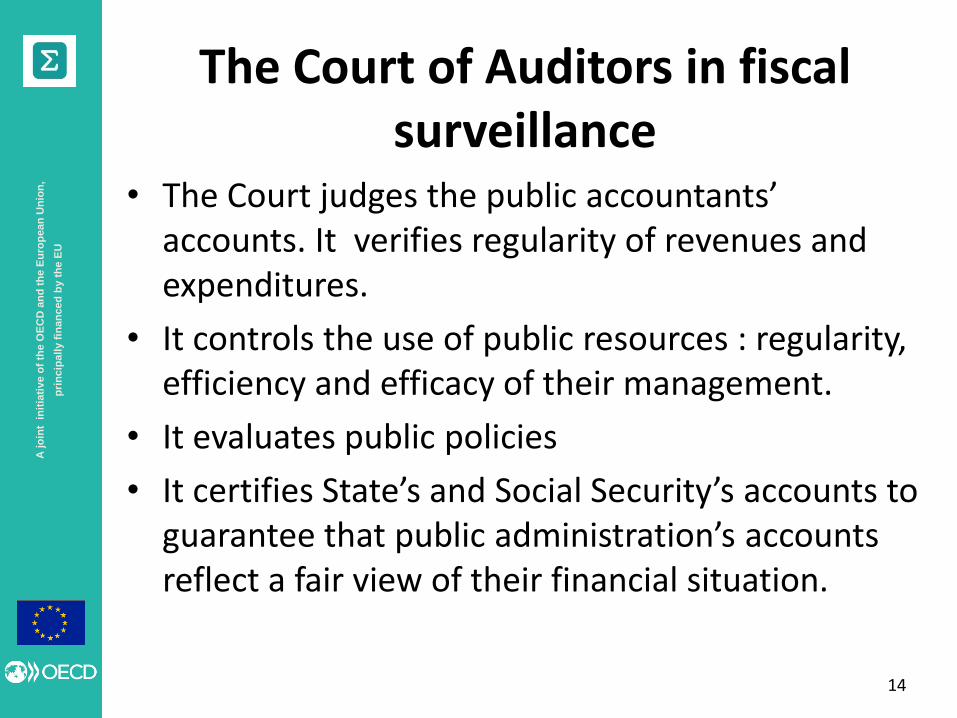

The Court of Auditors in fiscal surveillance

• The Court judges the public accountants’ accounts. It verifies regularity of revenues and expenditures.

• It controls the use of public resources : regularity, efficiency and efficacy of their management.

• It evaluates public policies

• It certifies State’s and Social Security’s accounts to guarantee that public administration’s accounts reflect a fair view of their financial situation.

14

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Reports in accordance with the 2001 Constitutional bylaw on budget (« LOLF »)

• Report on the fiscal balance and enforcement of budget act

• Report on the situation and outlook of public finance

• Annual audit opinions on the State’s account and social security account (« certification »)

• Reports on Social Security

• Other assistance missions : Assistance for evaluation and audit missions for finance

committees (Art. 58-1 of the LOLF)

Enquiries requested by the finance and social affairs committees of both Parliamentary assemblies (Art. 58-2 of the LOLF)

15

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Report on the fiscal balance and enforcement of budget act

• each chamber controls the expenditures of the ministries under its competencies and these reports are on-line

• The report is a synthesis of these controls

• Part 1: government deficit/surplus, compared with last year’s, with initial budget act, with public finance programing bill.

• Part 2: fiscal and non fiscal receipts and tax expenditures : comparison with last year’s, with the initial budget act. Analyse of the causes of differences: Intrinsic evolution Elasticity of fiscal receipts to GDP growth New fiscal measures

16

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Report on the fiscal balance and enforcement of finance laws

• Part 3: Government expenditures : Wage bill and pension scheme Debt interest expenditures Operating expenditures Capital expenditures In this part, we analyse the respect of government expenditures norms : - “0 in real terms” : all government expenditures - “0 in nominal terms”: all government expenditures except interest and pension expenditures

• Part 4: overall assessment : Regularity : conformity to Constitutional bylaw on budget act :

unity, universality and annularity Performance review Sustainability

17

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Global assessment of fiscal surveillance by the Court of Auditors

• An in-depth analysis with a high reputational capital

• Which prevents government to bypassing to the constitutional bylaw on budget

• But :

each year, recurrent critics, for instance :

• respects of norms

• sincerity of the receipts forecasts

• Quality of expenditures programming.

An ex-post analysis • Only a few weeks between the closing of State’s accounts and

the publishing of the report

• Parliament don’t pay enough attention to the execution of the budget

18

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

The High Council of

Public Finances

And

Fiscal Surveillance

19

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Over-optimistic forecast as a rationale for setting up an IFI in France

20

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Legal framework of public finances programming and monitoring

• French constitution, article 34 : « the multiannual guidelines for public finances shall be established by Planning Laws. They shall contribute to achieving the objective of balanced accounts for public administrations.”

• Constitution bylaw of December, 17th 2012 on planning and governance of public finances : Defines the content of multiannual planning budget laws Adds an introductory article on general government balance in all

budget laws Creates an independent fiscal council implements the automatic correction mechanism

• Multiannual planning budget laws defines : Medium term growth assumptions Public finances trajectory Fiscal rules : spending limits or objectives and rules for revenues

and tax expenditures

21

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

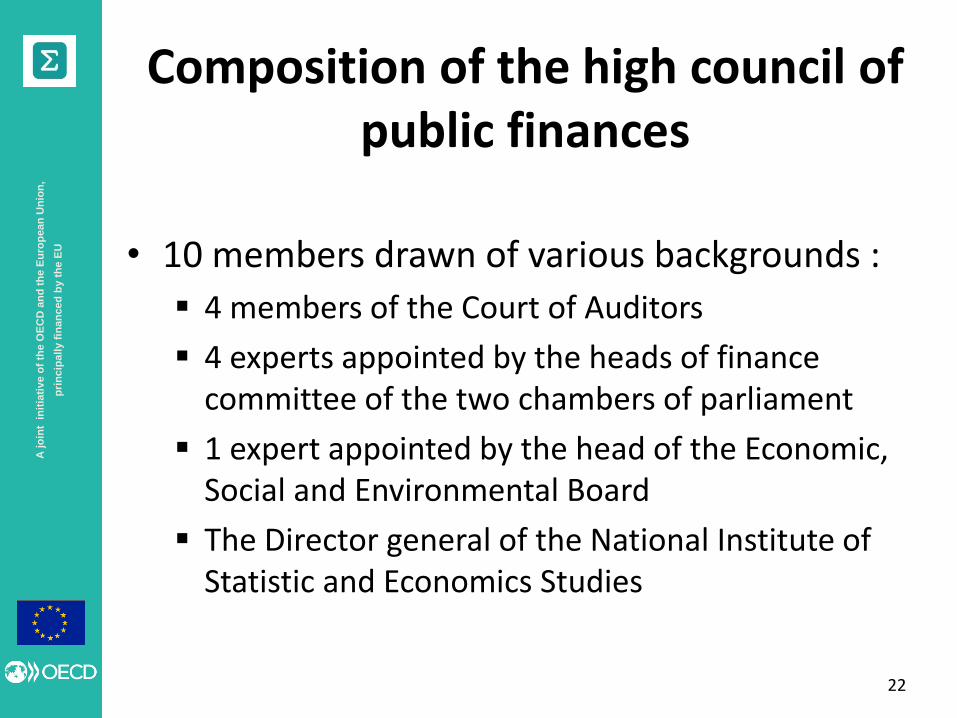

Composition of the high council of public finances

• 10 members drawn of various backgrounds :

4 members of the Court of Auditors

4 experts appointed by the heads of finance committee of the two chambers of parliament

1 expert appointed by the head of the Economic, Social and Environmental Board

The Director general of the National Institute of Statistic and Economics Studies

22

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

The HCPF – an independent body

• HCPF is chaired by the head of the Court of Auditors

• Mandates cannot be renewed (5 years) nor revoked

• Members cannot hold elected office

• Members have to submit a declaration of interests

• The HCFP cannot receive or solicit any instruction from the Government or any other organisations

• Permanent Secretariat but part-time staffers Secretary General 2 Deputies (from the Court of Auditors) : 1 economist, 1 public

finance expert 2 Senior Economists (originally from OECD and French Treasury) 1 Assistant

• Budget : 800.000 € and back office provided by the Court of Auditors

23

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Mandate of the HCPF (1)

• HCPF is required to deliver an opinion on a set of public finance texts : Public Finance Programming Bills

Initial and amending Budget Laws and Social Security Budget Bills

Stability programs provided to EU Commission and Council

• The missions of the HCPF revolve around 3 axes: Examining the soundness of macroeconomic forecasts and

potential growth estimates on which drat finance texts are based

Analysing ex ante the consistency of annual fiscal forecast set by Budget Bills with the multiannual structural balance targets

Identifying ex post “significant observed deviation” arising from comparisons between past year budget implementation and the multiannual guidelines on structural balance set in the Programming Laws

24

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Mandate of the HCPF (2)

• The issues on which the HCPF has to deliver an opinion are precisely defined: Macroeconomic forecasts or assumptions (draft budget, stability

and growth program, multiannual planning law)

Potential growth (multiannual planning law)

Consistency of draft budget and annual fiscal targets with the multi-year structural balance path

Identifying ex post “significant observed deviations” from the adjustment path

• the law is silent on the form and content of the opinion: It says only “the High Council delivers an opinion on

“macroeconomic forecasts, consistency of draft budget, potential growth…”

It is up to the council to decide form and content

25

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Mandate of HCPF (3)

• The HCPF provides an opinion on the macro economic forecasts made by the Government: Advisory role: no validation nor coproduction of forecasts. The

making of macroeconomic forecasts lies entirely with the Government

Importance of the critical risk assessment undertaken by the High Council

Benchmarking with forecasts made by other bodies (institute for economic research, international organisations…)

• The HCPF provides an assessment on the potential growth hypothesis from the Government Establishing its own analysis is necessary for estimating the output

gap and recovery scenarios which are subject to considerable uncertainty

26

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Mandate of the HCPF (4)

• The HCPF considers the consistency of annual objectives set by finance bills in comparison to multi-year structural balance trajectory: Multiannual guidelines on structural balance

Soundness of receipts and expenditures projections

• The HCPF plays a major role in triggering the correction mechanism in: Delivering an opinion about possible “significant observed

deviation” between the budget turnout and the multiannual guidelines on structural balance

Delivering an opinion on the corrective actions taken by the Government in its next opinion on initial budget bill

providing a public assessment on the occurrence of “exceptional circumstances” as agreed in the SGPFP

27

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Relationship with Parliament and Government

• Parliament is closely involved in the process: The Chairman of the High Council can be heard at any time at the

request of the Finance Committee of both Chambers

Opinions are systematically handed over to Parliament

• Opinion from the High Council are not binding for the Government: The High Council is an advisory body

Nevertheless, given the publicity and media attention attached to HCFP’s opinions, the Government runs a reputational risk if it chooses to disregard them

The Constitutional Council takes into account HCFP’s opinions in its constitutional check of budget bills (“sincerity”)

28

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

First reactions

• The High council is now an important institutional actor of public finances

• Good press coverage in France : the High Council is well identified in the institutional framework

• Building European and international credibility: European Commission (working document DBP review, 11/2013):

“The HCFP is an independent authority by law”

IMF (article IV consultation 2013): “the first two opinions issued by the newly created council attest to its independence and professionalism”

OECD (Economic Survey 2013): “Members of the Cour des comptes will play a leading role in (the) council, ensuring its independence. (…) The success of the new institutional framework will depend on how much weight will be given to the council’s evaluations” 29

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

First working year (2013)

• The High council was set up in mid-March 2013 after all members were appointed

• It delivered its first opinion on 15 April 2013 on the economic forecasts of 2013-2017 Stability Program

• 3 other opinions in 2013: On the automatic correction mechanism (May, 29th)

On initial budget bill (September 25th)

On amending budget bill (November)

30

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Second working year (2014)

• 6 opinions : Assessing macroeconomic forecasts of 2014-2019

Stability Program

Analysing ex ante the consistency with structural balance trajectory (draft budget, amending budget)

Identifying ex post “significant deviations

Assessing potential GDP estimates (Programing public finance bill)

Output gap and potential growth

31

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Opinion on the programming budget bill for

2014-2019 - September 2014 (1)

• Potential output scenario: HCPF notes that the Government has chosen to use the European

Commission’s estimates of potential output

It underscores the inherent weakness of output gap estimates, especially given the uncertainty surrounding the magnitude of output losses stemming from the economic crisis

It explains that overstated output gap would lead to a deeper structural deficit all along the programming period

HCPF considers that estimate potential growth presented by the Government (1% for 2014-2015, about 1.2% on average for 2016-2019) is an acceptable hypothesis

• Macroeconomic scenario HCFP considers that the Government macroeconomic scenario is more

realistic than macroeconomic scenario presented in the latest Stability programme (April 2014)

But it relies on too favourable assumptions, especially with respect to international environment and investment 32

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Opinion on the programming budget bill for

2014-2019 - September 2014 (2)

• Public finance scenario: HCPF notes that the public finance trajectory in the programming budget

bill is not consistent with the commitments undertaken by France, which is currently under an excessive deficit procedure, in the Stability programme of April 2014

The structural adjustment for years 2014, 2015 and 2016 is clearly less than that provided by said commitments

Consequently, and given the worsened economic situation, the nominal deficit remains above 4% of GDP and the deficit target under 3% is postponed to 2017

The medium term objective (MTO), revised downwards to -0.4% of GDP, has been postponed again to the end of programming period (2019)

Even if this new trajectory is less ambitious than the previous one, complying with it would require a strong slowdown of public expenditure. In view of the announced measures to date, the HCPF highlights a risk of deviation with respect to the trajectory towards the MTO

33

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Opinion on budget bill for 2015

September 2014 (1)

• The HCPF considers that the Government’s growth forecast of 0.4% for 2014 is realistic

• It considers that the Government’s forecast of 1% for 2015 is optimistic It requires a quick and lasting recovery, which is not supported by latest

short-term indicators

Macroeconomic forecasts suffer from some weakness regarding the dynamism of the international environment and domestic demand

• The HCPF underscores that the government has not attempted to correct the “significant deviation” (1.5 point of GDP) between the structural deficit in 2013 and the programming budget law for 2012-2017, still a valid reference

• Given the context of weak growth and low inflation, the HCPF underscores that postponing the structural adjustment again could put the public debt trajectory at risk 34

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Opinion on budget bill for 2015

September 2014 (2)

• The HCPF welcomes the efforts for reducing public expenditures since 2011

• Nevertheless, given the measures presented by the Government to date, the HCPF reckons that the expected public expenditures growth for 2015 (1.1% in nominal terms), and therefore the structural adjustment target (0.2%) for 2015, may not be achieved.

35

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Opinion on the stability programme 2015-

2018 - April 2015

• The HCPF considers that the Government growth forecast of 1% in 2015, unchanged since the budget bill for 2015, is now prudent, thanks to a more favourable environment resulting from strong falls in both the oil price and the euro. Inflation and wage forecasts have been judiciously revised downwards

• The HCPF considers that the growth forecasts for the years 2016 to 2018 are prudent, despite the financial risks. They are meant to ensure the credibility of the nominal trajectory of public balances.

• Nevertheless, the HCPF regrets that the potential growth forecast, whose estimation is highly uncertain, has already been increased, only a few months after the adoption of the programming budget law. This review automatically increase the level of structural adjustment notified to the EU commission, without any change in fiscal ou revenues measures. It makes the split between the cyclical and the structural components of public balance difficult to estimate and makes it harder to analyse fiscal policy

36

A j

oin

t i

nit

iati

ve o

f th

e O

EC

D a

nd

th

e E

uro

pe

an

Un

ion

,

pri

nc

ipall

y f

ina

nced

by t

he

EU

Global assessment of fiscal surveillance by the HCPF

• A particularly difficult job :

Very short delays to give an opinion

Highly risky : economic forecasting is as difficult as astrology

• Government forecasts are now more realistic, even especially cautious

• But :

Some tricky measures (for instance the review of potential growth in stability programme)

The correction mechanism is partly inefficient, because budget laws are annual and have the same juridical status than multiannual programming laws