Private Labels and Retailer Profitability: Bilateral Bargaining in the Grocery Channel * Paul B. Ellickson a , Pianpian Kong b , and Mitchell J. Lovett a a Simon Business School, University of Rochester b School of Management, University at Buffalo, SUNY September 29, 2017 Abstract We examine the role of store branded “private label” products in determining bar- gaining outcomes between retailers and manufacturers in the single-serve brew-at-home coffee category. Exploiting a novel setting in which the dominant, single-serve technol- ogy was protected by a patent that prevented private label entry, we develop a struc- tural model of demand and supply-side bargaining and seek to quantify the impact of private labels on retailer profits. To quantify the benefits of private label introduction, we decompose their impact into the direct profits (from adding an additional product) and the bargaining benefit on branded products (from increasing retailer’s bargaining leverage), netting out the business stealing effects on incumbent branded products. We find that bargaining outcomes are driven primarily by bargaining leverage, while bargaining ability is relatively symmetric between retailer and manufacturer. More- over, the impact of bargaining leverage is substantial: increased bargaining leverage accounts for roughly 20% of the overall benefit of private label introduction, which is itself on the order of 10% of pre-introduction profits. Finally, we find that private labels are beneficial to all retailers, but some retailers gain much more than others. Keywords: Retail Grocery, Bargaining Models, Private Labels, Store Brands, De- mand Estimation. * We thank Guy Arie, Greg Crawford, Michaela Draganska, Ron Goettler, Paul Grieco and Ali Yu- rukoglu for valuable comments. We also thank seminar participants at Arizona State Carey, Duke Fuqua, Goethe Universitat, Houston, Northwestern Kellogg, Penn State economics, University of Rochester, Simon Business School, Yale SOM and the University of Zurich as well as attendees at INFORMS Marketing Science 2017, SICS 2017, and QME 2017 for helpful feedback. Send any correspondence to [email protected](Ellickson), [email protected](Lovett) or [email protected](Kong). 1

Transcript

Private Labels and Retailer Profitability:Bilateral Bargaining in the Grocery Channel∗

Paul B. Ellicksona, Pianpian Kongb, and Mitchell J. Lovetta

aSimon Business School, University of RochesterbSchool of Management, University at Buffalo, SUNY

September 29, 2017

Abstract

We examine the role of store branded “private label” products in determining bar-gaining outcomes between retailers and manufacturers in the single-serve brew-at-homecoffee category. Exploiting a novel setting in which the dominant, single-serve technol-ogy was protected by a patent that prevented private label entry, we develop a struc-tural model of demand and supply-side bargaining and seek to quantify the impact ofprivate labels on retailer profits. To quantify the benefits of private label introduction,we decompose their impact into the direct profits (from adding an additional product)and the bargaining benefit on branded products (from increasing retailer’s bargainingleverage), netting out the business stealing effects on incumbent branded products.We find that bargaining outcomes are driven primarily by bargaining leverage, whilebargaining ability is relatively symmetric between retailer and manufacturer. More-over, the impact of bargaining leverage is substantial: increased bargaining leverageaccounts for roughly 20% of the overall benefit of private label introduction, whichis itself on the order of 10% of pre-introduction profits. Finally, we find that privatelabels are beneficial to all retailers, but some retailers gain much more than others.

∗We thank Guy Arie, Greg Crawford, Michaela Draganska, Ron Goettler, Paul Grieco and Ali Yu-rukoglu for valuable comments. We also thank seminar participants at Arizona State Carey, DukeFuqua, Goethe Universitat, Houston, Northwestern Kellogg, Penn State economics, University of Rochester,Simon Business School, Yale SOM and the University of Zurich as well as attendees at INFORMSMarketing Science 2017, SICS 2017, and QME 2017 for helpful feedback. Send any correspondenceto [email protected] (Ellickson), [email protected] (Lovett) [email protected] (Kong).

1

1 Introduction

Private labels are an important source of retailer revenues and profits. They generated $98

billion in U.S. food and grocery sales in 2012, or 17.1% of total revenues (Schultz, 2012;

Nielsen Global Survey, 2012). The impact of private label brands on retailer category profits

can come directly from the private label sales themselves or indirectly through improved

negotiating positions with national brands. Direct profits increase because private labels can

attract new consumers or larger spending through lower prices; higher margins are another

benefit. Indirect profits arise because the store brand can play a strategic role in negotiations

with manufacturers and increase the retailers’ share of channel profits (Scott Morton and

Zettelmeyer, 2004). A private label improves the retailer’s bargaining position by reducing

the forgone profits if negotiations with manufacturers fail, generating a bargaining benefit

via more favorable margins on the competing branded products.1

In this paper, we measure the influence of private label entry on bargaining outcomes in

the single-cup brew-at-home coffee category and compare the size of the bargaining benefit to

that of the direct profit from simply adding more options. Our empirical analysis exploits a

unique setting in which the dominant branded product, Keurig/GMCR’s ‘K-Cup’ technology,

was patent protected, effectively preventing entry by private label coffee products prior to

patent expiration. Therefore, we are able to observe how retailers and manufacturers behave

both with and without competition from private label products, and isolate the factors that

change this conduct. Further, because our data contains many retailers, we observe variation

in the quality and positioning of the various private label brands. After the patent expiration,

this yields exogenous variation in the shock to negotiations that different retailers receive. To

leverage this unique source of variation, we build a model of consumer demand and supply-

side bargaining in the brew-at-home coffee category. We estimate the model using weekly,

chain-level data from 72 retail market areas. We then conduct counterfactual exercises

1A third benefit argued for store brands is store or store brand loyalty that increases traffic to the store.Our data limits our ability to speak to this potential benefit and so, beyond effects through changes in thedraw from the outside good, we do not claim to capture such benefits in this study.

2

that quantify the impact of private label products on bargaining outcomes, comparing the

bargaining benefit to the direct category expansion benefit of introducing private labels.

As noted above, our empirical strategy involves exploiting a unique setting that unfolded

in the brew-at-home coffee market over our sample period. A previously mature product

category, the brew-at-home coffee market was disrupted in the mid-to-late 2000s by a new

product offering: single-serving coffee pods. This new technology offered convenience, and

a standardized, high-quality brewing experience, to a growing segment of coffee connois-

seurs. While single-serve coffee had existed both in the U.S. and abroad for many years,

Keurig/GMCR was able to position itself as the de facto U.S. standard by offering a wide

range of sub-brands and licensed/partner products, alongside a design that was superior to

its rivals and much wider product distribution.2 Notably, since both the Keurig brewers

and K-Cup pods were patented, competitive entry (to this particular design) was effectively

foreclosed until late 2012, creating a unique “before and after experiment.” To exploit this

exclusion, we develop a structural model of demand and supply that can control for con-

founding factors in the competitive environment (e.g., cost changes, new product entries,

continued market expansion, and evolving substitution patterns) and reveal how private

labels shaped bargaining outcomes.

While providing a unique setting for analyzing private label competition, the single-

serve coffee category presents some challenges on the demand side. First, a central aspect

of the Keurig/GMCR strategy was brand variety, so it will be important to include the

full set of brands offered. Second, since this was a new product launch (that we observe

almost from inception), availability of K-Cup products was limited, especially in the early

hardware (i.e., the Keurig brewer). Consumers that did not own the brewer were not in the

market for single-cup pods. Ignoring these market features could lead to large biases in our

2Keurig/GMCR is also the “category captain” in many retailers, adding to its dominant position (Nijset al., 2013). The category captain coordinates with the retailer to manage the selection and display of agiven product category. It is typically one of the leading national brands.

3

demand estimates. Getting the demand system right is critical, as it drives all subsequent

inference. We address all three concerns by extending Bruno and Vilcassim (2008) and

developing a random-coefficient, discrete-choice demand system that accounts for availability

and machine ownership by simulating individual consumers and aggregating up to observed

shares (availability and ownership are tied to the data via aggregate moments of each). We

demonstrate that the model yields flexible substitution patterns that capture key market

features, including substitution between single-cup products and variation in the private

label brand equities.

Turning to the supply side, we must first recover wholesale prices, as these are not

observed in the data. To do so, we assume monopolist retailers and use the first order

conditions from the retailer’s profit maximization problem to solve for the wholesale prices

that rationalize retailer decisions (Bresnahan, 1987; Werden and Froeb, 1994). We find that

these recovered wholesale prices decline in the period after the patent expiration as one

would expect if the bargaining benefit were meaningful.

These inferred wholesale prices are then the focus of our bargaining model. We assume

that retailers and manufacturers bargain over linear contracts that determine these “transfer

prices.” Following the recent literature, we model the retailer-manufacturer vertical contract-

ing relationship as a ‘Nash in Nash’ bargain, focused on determining the wholesale price that

effectively splits the gains from trade. Using the inferred wholesale prices, we recover the

bargaining power (ability) parameters and manufacturer cost parameters that rationalize

the data. To do so, we compute both the profits that each party achieves under agreement

and the profits that would obtain should they fail to reach agreement. The observed whole-

sale prices maximize the Nash product, as indexed by the power parameters. Private label

products provide a key source of variation in the disagreement payoffs that define the gains

from trade.

To estimate this bargaining model, we modify the empirical approach developed by

Grennan (2013), which allows us to recover separate bargaining parameters for each re-

4

tailer/manufacturer pair. We find that bargaining ability is quite symmetric between re-

tailers and manufacturers and also does not change significantly after the patent expiration

(private label entry). Thus, we find that bargaining outcomes are driven primarily by the

shift in bargaining leverage (position) that private labels create. We then conduct coun-

terfactual exercises that quantify their impact bargaining outcomes. The impact of the

change in bargaining leverage is substantial: bargaining benefits account for roughly 20%

of the overall benefit of private label introduction, which is itself on the order of 10% of

pre-introduction profits. We find that private labels are beneficial to all retailers, but some

retailers gain much more than others. The size of the gain increases with the quality of the

adjacent private label, suggesting that success in one category can be leveraged in others.

Our research relates to several streams of literature in both marketing and economics.

First, we contribute to the literature on private labels, which includes seminal papers by Hoch

and Banerji (1993) and Dhar and Hoch (1997) that identified and cataloged the determinants

of private label success, and sought to explain why their penetration varied across retailers.

Hansen et al. (2006) investigate whether consumer tastes for store brands are correlated

across categories, or are driven more by category-specific factors. They find strong evidence of

the former relative to the latter. Sayman et al. (2002) study how private labels are positioned

vis-a-vis national brands, and Scott Morton and Zettelmeyer (2004) show how private labels

allow the retailer to carry closer substitutes to national brands than otherwise and that this

arises because of the incentives national brands face in negotiating with retailers.

A few papers have studied questions more directly related to the bargaining benefit of

private labels per se. Pauwels and Srinivasan (2004) examine the impact of store brand

entry on the relative margins of retailers and suppliers, as well as their role in shifting

consumer demand. They examine four categories in the Dominick’s Finer Foods retail chain

and find that retailer margins improve, but that category sales only rarely expand upon

store brand entry. Similarly using Dominick’s data on the oats category, Chintagunta et al.

(2002) empirically analyze how private labels change conduct in the channel, as well as

5

how this conduct translates through to retailer pricing decisions. They find that post entry

manufacturers’ accommodate so that Dominick’s average weekly margin increased by around

3%, but that consumers tastes do not change post entry. Meza and Sudhir (2010) again use

Dominick’s data, but for the breakfast cereal market, and examine how private labels affect

bargaining power, and ask whether and how retailers can use prices to strategically influence

this negotiation. They find that bargaining power increases as evidenced by lower wholesale

prices on imitated national brands, but that strategic pricing is less clearly evidenced in

the data. We add to this literature along three key dimensions. First, our setting lets

exploit the patent expiration to evaluate behavior with and without exogenous private label

exclusion. Second, we implement a full bargaining model specification that allows us to

generate counterfactuals to investigate the causal effects of private labels and isolate the

bargaining component of the private label benefit. Third, we expand the investigation from

a single retailer to 54 different retailer banners and 72 different retail market areas, allowing

us to describe the distribution of private label bargaining and category expansion benefits

across varying private label brand qualities.

Our bargaining model draws upon the theoretical literature on bilateral Nash bargaining

(Nash, 1950; Rubinstein, 1982), which includes the theoretical development of the ‘Nash in

Nash’ bargaining solution for most applied work by Horn and Wolinsky (1988) and recent

developments by Collard-Wexler et al. (2014). In doing so, we contribute to the growing

stream of empirical literature on bargaining models, which includes papers by Misra and

Mohanty (2006), Ho (2009), Draganska et al. (2010), Crawford and Yurukoglu (2012), Gren-

nan (2013), Ho and Lee (2013), Gowrisankaran et al. (2014), and Crawford et al. (2015).

This work is also related to a broader empirical literature on vertical contracting, which in-

cludes important contributions by Villas-Boas (2007) and Bonnet and Dubois (2010), among

several others. Two papers in this literature on manufacturer-retailer relationships speak di-

rectly to the coffee market. Noton and Elberg (2016) model bargaining between retailers and

manufacturers in the Chilean market for instant and ground coffee, focusing on the impact of

6

supplier size on the split of channel profits. Contrary to conventional wisdom, they find that

small suppliers often attain shares of the channel surplus on par with the largest supplier.

In the paper most closely related to ours, Draganska et al. (2010) empirically model the bar-

gaining problem between retailers and manufactures in the German market for ground coffee,

seeking to quantify the sources of heterogeneous bargaining power and determine whether

they have shifted over time. They find that store brand entry, per se, does not increase

bargaining power, but that store brands positioned closer to national brands tend to have

stronger bargaining power. They also find that bargaining positioning has little impact on

profits.

Our contribution to the broader bargaining literature goes well beyond a new application

of the model. Our unique setting of the patent expiration allows a test of sorts of the

bargaining model itself. Specifically, we are able to evaluate how well the model captures the

way private labels shift bargaining position as compared to needing to capture the change

in bargaining outcomes through bargaining power (ability), a shift that seems unlikely to

actually occur at the point of the patent expiration. We find that indeed the bargaining model

can capture the change through bargaining position with changes in the average bargaining

power before versus after the patent expiration being very small and insignificant. This

provides new evidence that bargaining models can capture fundamental aspects of supply

behavior under even large exogenous shifts in the supply arrangements.

The paper is organized as follows. In section 2, we describe the data used in our empirical

study and provide an overview of the at home coffee market and the role of the single serve

(K-Cup) segment in driving its expansion. The model and estimation are described in section

3. We present the results of our estimation in section 4 and conduct counterfactual exercises

in section 5. Section 6 concludes.

7

2 Data and Setting

The data are drawn from IRI’s point of sale (POS) database for the period January 2008 to

March 2014. The data cover 72 U.S. retailer-market areas (RMAs) and include 54 distinct

retail banners (e.g. Safeway, Kroger). Retailer-market areas are geographic trading areas

defined by IRI together with the retailer, and roughly correspond to retailer divisions. Re-

tailer divisions are usually organized around regional distribution centers, which typically

serve up to a few hundred individual stores. The data we have access to contain information

only about the retailer and not other competing retailers in the market area.

For each RMA, we observe weekly, SKU-level data on sales, price per serving and mer-

chandising variables, each aggregated up from the individual store level to the RMA. In

addition, we observe the standard volume (ACV) weighted product distribution measure,

our key proxy for product availability at the RMA-level. Rather than working with individ-

ual SKUs, we aggregate up to the segment-brand level, so that, for example, all Starbuck’s

K-Cup SKUs (e.g. Dark Sumatra, Breakfast Blend) are rolled up to a single choice. Note

that this is done by segment, so that, for example, Starbucks premium drip coffee (whole bean

and ground) is treated as a separate product from the Starbucks K-Cup offering. We include

four coffee segments: instant (e.g. Nescafe), main (e.g. Folgers), premium (e.g. Starbucks)

and single-cup (e.g. Keurig). The four segments are vertically differentiated, with instant

and main offering the cheapest alternatives and single-cup the costliest. In the single-cup

category in particular, Keurig operates a number of sub-brands with common pricing and

promotion schedules. In the analysis we have aggregated these to a single “Keurig” brand

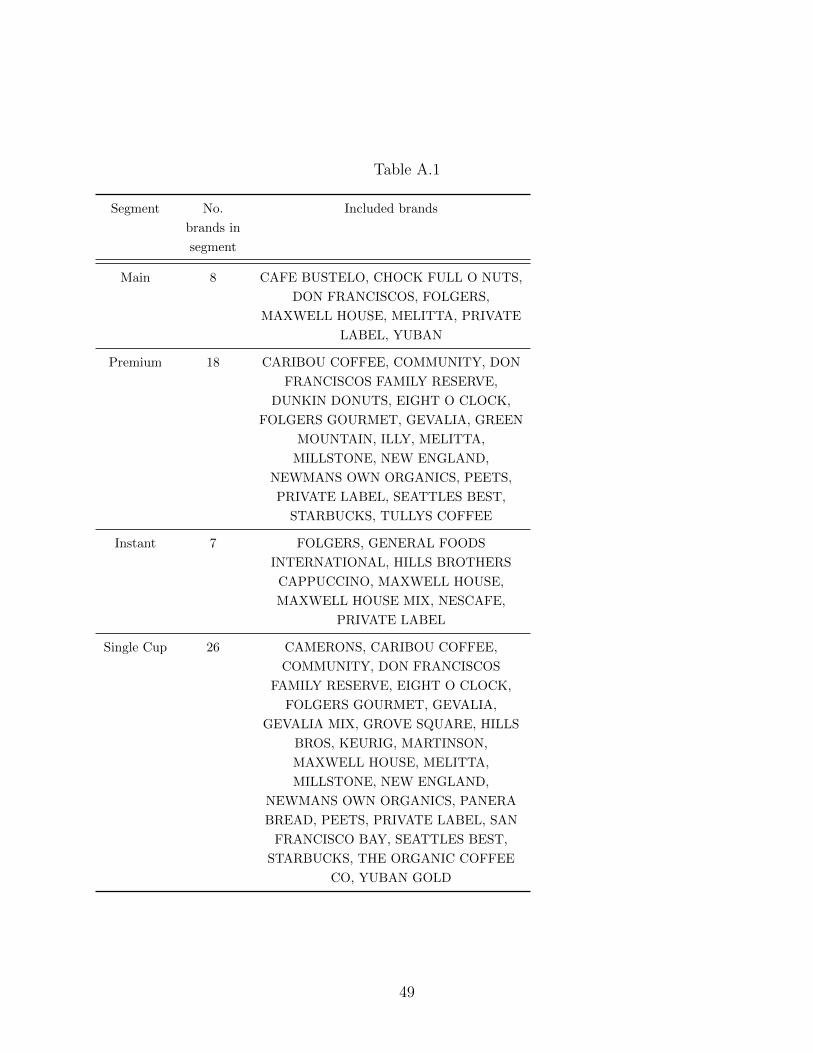

for K-cups. Details of the brand aggregation and the segment definitions are in appendix A.

In addition to the aggregate POS data, we include cross-tabulations drawn from the

IRI individual panelist data. We use the panelist cross-tabs in two ways. First, the panel

provides an estimate of the number of shoppers in each RMA. We use this to construct our

measure of market size. We define the size of the market to be the number of shoppers times

the number of days per week (7) times a scaling factor related to per capita coffee purchase

8

in that RMA, which we obtain from the average daily coffee purchases in that market per

shopper. Second, we develop a proxy for the installed base of K-Cup machine owners. We

extract K-Cup penetration data that reports, at the yearly level, the percent of shoppers (in

each RMA) who have consumed K-Cup coffee products in the previous 12 months. We then

use these yearly values from the panelist data to impute weekly observations of installed

base at the RMA-weekly level. The details of this imputation are available in appendix B.

Finally, we obtain information on coffee bean commodity prices from the International

Coffee Organization (http://www.ico.org). These bean prices are available at the monthly

level for the four primary coffee bean types: Colombian milds, other milds, Brazilian naturals,

and Robustas. The prices are in US cents per pound, which we convert to US dollars per

pound for our analysis. The prices for all the bean types, except for the Robustas, are closely

correlated. The Robustas are priced slightly lower than the other bean types. During the

observation period, the bean prices increase and then fall, with the peak prices occurring in

early 2011. We use these bean prices as an input to the manufacturing costs. In addition,

we categorize the brands into Keurig relationships and vertical positions. Table 1 presents

the brands included in each of the ownership and vertical positioning categories. Note these

definitions are valid for the period we study. Some brands that are indicated as third party

later partnered with Keurig (e.g., Peets).

Type Brands

Owned KeurigLicensee Caribou Coffee, Eight O’Clock, Newman’s Own OrganicsPartner Folgers Gourmet, Millstone, Seattle’s Best, StarbucksValue Offering Camerons, Eight O’Clock, Grove Square, Private Label, San Francisco BayPremium Offering Gevalia Mix, Peets, Seattle’s Best, Starbucks

Table 1: Cost Function Variable Definitions

Our final sample is selected to include RMA-week-segment-brand cases with a reasonable

level of distribution. Details of the sample construction are presented in appendix A.

9

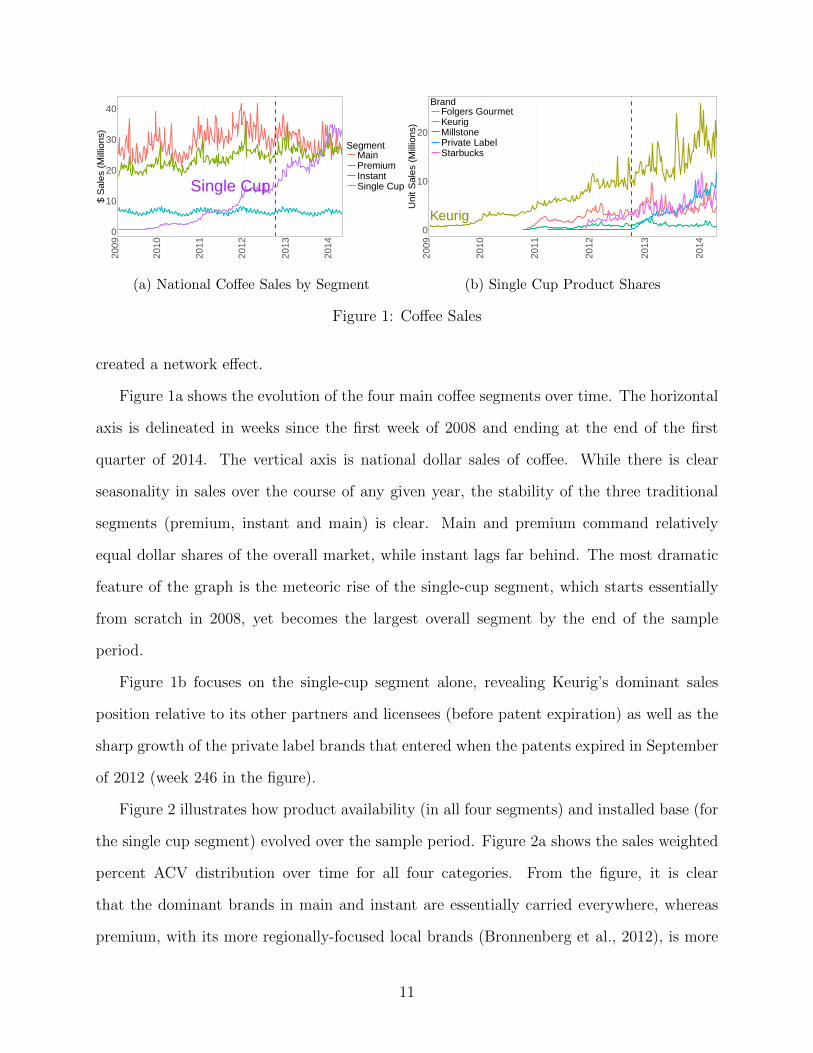

2.1 The Brew-At-Home Coffee Market

The previously mature category of coffee for ‘at home’ brewing was disrupted in the mid to

late 2000s by the creation and expansion of the single serving ‘K-Cup’ technology pioneered

by Keurig and Green Mountain Coffee Roasters (GMCR). While a variety of single serve

coffee technologies have existed in the U.S. for quite some time (primarily in the commercial

office setting), they did not achieve widespread adoption in the at-home market until Keurig

effectively created the de facto standard with its proprietary K-Cup technology.3 Keurig

started by focusing on the commercial office market, utilizing a direct sales force distribu-

tion system that relied on partnerships with five primary coffee roasters, who also handled

the production and distribution of the cups. They shifted focus to the much larger at-home

market in the early 2000s, at which point GMCR acquired Keurig (they had earlier been

separate companies) and brought the main coffee roasters in house as well. The popularity

of the Keurig system leveraged the growing demand for premium coffee resulting from the

rapid expansion of Starbucks cafes and other premium coffee shops in the U.S. throughout

the 1990s, which also drove the growth of the premium ground and whole bean segment

in the grocery channel in the late 1990s and early 2000s. The Keurig system offered the

convenience of a ‘mess-free’ single-serve brewing experience, while standardizing the quality

of the delivered coffee (by precisely controlling the portion size, brewing time and temper-

ature). A key factor in their positioning strategy was the wide array of flavors, styles and

brands they offered, which GMCR achieved through an aggressive licensing and partnership

strategy with household brands. This positioning differentiated GMCR’s K-Cups from com-

peting single-serve products like Senseo, Flavia and Tassimo. Moreover, by becoming the de

facto standard for single-serve at-home brewing, they were effectively the only single-cup op-

tion available (in wide distribution) at grocery stores, mass merchandisers and clubs, which

3In Europe, the capsule-based single-cup espresso brewing system developed by Nespresso has becomethe standard there. Nespresso machines are available in the U.S. as well, but have had more limited successin this market than Keurig due to their focus on espresso-based beverages and their far more limited capsuledistribution, which is still primarily through online sites.

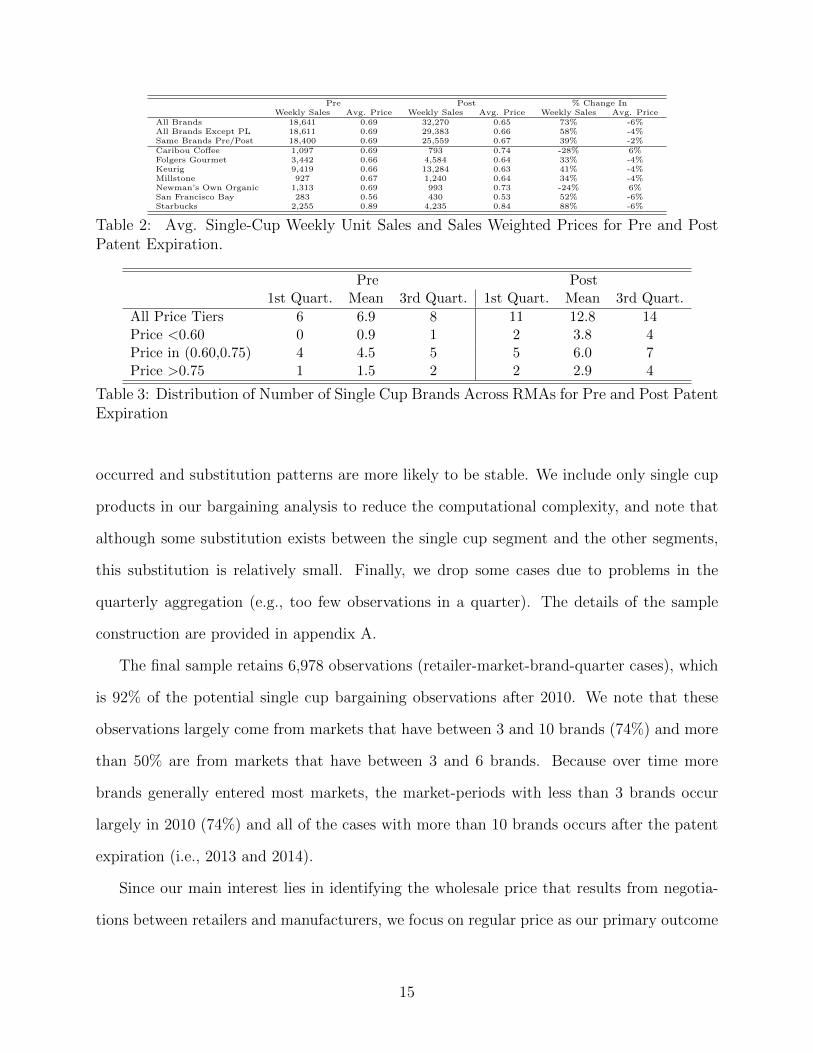

Table 3: Distribution of Number of Single Cup Brands Across RMAs for Pre and Post PatentExpiration

occurred and substitution patterns are more likely to be stable. We include only single cup

products in our bargaining analysis to reduce the computational complexity, and note that

although some substitution exists between the single cup segment and the other segments,

this substitution is relatively small. Finally, we drop some cases due to problems in the

quarterly aggregation (e.g., too few observations in a quarter). The details of the sample

construction are provided in appendix A.

The final sample retains 6,978 observations (retailer-market-brand-quarter cases), which

is 92% of the potential single cup bargaining observations after 2010. We note that these

observations largely come from markets that have between 3 and 10 brands (74%) and more

than 50% are from markets that have between 3 and 6 brands. Because over time more

brands generally entered most markets, the market-periods with less than 3 brands occur

largely in 2010 (74%) and all of the cases with more than 10 brands occurs after the patent

expiration (i.e., 2013 and 2014).

Since our main interest lies in identifying the wholesale price that results from negotia-

tions between retailers and manufacturers, we focus on regular price as our primary outcome

15

variable.4 The POS data do not distinguish between regular and promotional prices, so we

proxy for the regular “shelf” price by computing the 90th moving quantile of quarterly prices

and treating this as the regular price. The remaining measures are constructed as averages.

Figure 3b shows the regular price series for the leading brand in each of the three primary

segments (single-cup, premium and main). There is a single price series for each retailer

(RMA) in each category. Although we focus on bargaining in the single-cup segment, we

show the regular prices for the other segments as a benchmark, for instance, to capture the

influence of common cost factors on retail coffee prices. From this figure we can ascertain

three facts. First, the figure depicts the clear vertical separation of the segments. Second,

retailers’ prices vary a reasonable amount. Third, by comparing across segments, we are

able to see that prices in the single cup segment decreased after patent expiration (quarter

19 in the figure, corresponding to the vertical line) more than the other segments. Moreover,

single cup prices continue to fall for the remainder of the sample, as additional private label

and independent (e.g. non-Kuerig-affiliated) brands continue to enter the market.5

3 Model and Estimation

On the demand side, we specify a relatively standard discrete choice, random coefficient

model of consumer demand (aggregated to the market share level) using the framework

developed by Berry et al. (1995). To accommodate the rapid expansion of the single-cup

segment (particularly the limited early distribution/availability in many grocery chains) and

also to account for the costly hardware requirement of owning a Keurig brewer, we employ

methods developed by Bruno and Vilcassim (2008) to simulate consumers with choice sets

that are consistent with these market features.

4See Nijs et al. (2010) on the role of manufacturer trade promotions.5Using a difference-in-difference analysis between the single-cup segment and the other segments for the

pre- versus post-patent expiration periods and including controls for time trends, quarter of year dummiesand RMA fixed effects, we find that the interaction representing the diff-in-diff for the immediate decreasefrom quarter 19 to 20 is significant (coef=-0.034, se=0.006, n=432), and so is the total decrease in the postpatent expiration (coef=-0.024, se=0.003, n=2592).

16

(a) Private Label Entry Timing(b) Regular Prices of Leading Brand

Figure 3: Descriptive Results

On the supply side, we assume that retailers set monopoly prices at the retail level

(abstracting away from retailer to retailer competition).6 Using the first order conditions

(FOCs) of the monopoly pricing problem, we then ‘back out’ the implied marginal costs

the retailer pays for each coffee product (Werden and Froeb (1994); Nevo (2000a)). These

costs are assumed to be the wholesale prices charged by manufacturers to the retailers that

carry their products. Note that we do not have any additional data on the wholesale prices

themselves. For all products carried by a given retailer, we assume that these wholesale prices

are negotiated via the ‘Nash in Nash’ bilateral bargaining (with passive beliefs) protocol

proposed by Horn and Wolinsky (1988). In particular, we assume that the parties bargain

bilaterally over a purely linear transfer price, enforcing the assumption that firms do not

believe that other contracts will be renegotiated should they fail to reach agreement in

this bargain. Note that we are directly ruling out the existence of more complex nonlinear

contracts, slotting fees, quantity discounts or full-line forcing arrangements that may be

6Given our full estimation set-up, this is not as restrictive as it might seem. We include six-month productintercepts for all products, so that the outside good is effectively able to change every half year. Hence, theonly cross-store effects we do not capture with our demand system are short term price promotions andmerchandizing. Of course, the monopolist assumption ignores strategic interaction among retailers.

17

empirically relevant (O’Brien and Shaffer, 2005).7

3.1 Demand Model and Estimation

We assume that consumers are in the market for coffee every week, though we set the market

size to account for the population of coffee drinkers and the number of cups they drink per

week. Consumer i is characterized by a vector of taste parameters which includes price

sensitivity and segment specific tastes, as well as a vector of local product availabilities,

ait, and an ownership indicator for the hardware required for the Keurig system, mit. The

hardware and availability variables determine which products are in the current choice set

of a given consumer, as will be precisely detailed below. For consumer i in market r at time

t, the utility for product j (segment-brand) is then given by

uijrt = αilog (pjrt) + γitXjrt + ξjrt + εijrt (1)

The individual level utilities are defined as follows: αi

γit

=

α

γt

+ vi (2)

where v is assumed to be distributed multivariate normal with mean zero and diagonal

covariance matrix, and, as typical in structural demand estimation, we assume the εijrt are

distributed according to a type-I extreme value error distribution. Following Nevo (2001),

utility can be re-written parsimoniously as uijrt = δjrt + µijrt + εijrt. The first term, δjrt ≡

αlog (pjrt) + γtXjrt + ξjrt, represents the common component of utility that is shared by all

individuals, while the two remaining terms, µijrt and εijrt are heterogeneous across them.

The µijrt is simply vi

(log (pjrt) , Xjrt

)′, in which vi are often referred to as the ‘nonlinear

7Although these are admittedly strong assumptions (albeit ones that are maintained throughout almostthe entire empirical bargaining literature), we have some ability to test their restrictiveness by focusing onthe small set of firms (e.g. Wegmans) that publicly and categorically refuse to enter into such arrangements.

18

parameters’ and Xjrt is the subset of variables in Xjrt that have random coefficients. We

note that in our setting Xjrt contains product-six-month fixed effects and month-in-year time

effects for each RMA, along with a coefficient for percent ACV display.8. For the non-linear

parameters, we include a random coefficient on log(pjrt), and coefficients on the Xjrt, which

contains segment dummies.

The availability and Keurig machine ownership variables constrain choices by excluding

or including options from the consumer’s choice set. The availability vector contains a

binary variable for each time period for each product. These variables take the values 1 or

0, indicating whether the product is available for that consumer in that week. The machine

ownership variable, mi has elements for each week, for each individual, taking values 1 if the

individual owns the machine and 0 otherwise. When mit = 0, the availability for all single-

cup products are then set to 0; we denote this modified availability vector ait. Note that

none of these variables are observed to us, but will instead be simulated from the aggregate

distribution, from which we are able to extract moments.

We normalize the outside good utility to 0, so that the individual probability of purchase

can then be computed as

sijrt =aijrte

δjrt+µijrt

1 +∑

k aikrteδkrt+µikrt

. (3)

Estimation proceeds via the generalized method of moments (GMM) as described by

Nevo (2000b) with the main distinction being the additional simulation over the availability

and ownership terms (based on Bruno and Vilcassim (2008) and Tenn and Yun (2008)). To

help identify the nonlinear parameters (associated with price and tastes for each segment),

we use the instrumenting strategy proposed by Gandhi and Houde (2015), which generalizes

and extends the methods originally suggested by Bresnahan et al. (1997). Note that we

are not instrumenting for price; we treat prices as conditionally exogenous given the large

number of time-varying product dummies already included in the demand system.9 The

8Recall that distribution and hardware ownership are handled directly in the simulation and do notappear as variables in Xjrt

9In fact, we have commodity coffee cost data, but once including the large number of time-varying

19

instruments that we do include are needed here to identify the nonlinear parameters that

characterize the consumer heterogeneity. The design of these instruments is intended to

capture how isolated a product is in product space, which should, in principle, give it more

market power. The particular instruments we employ are 1) the number of brands in a set

of price-difference bins, 2) the number of brands in the various price-difference bins within

the product’s own segment, and 3) the sum of the price differences in the product’s own

segment. In addition, we include the full cross of the average segment prices by the segment

identities.

3.2 Supply Model

The supply model has two stages. In the first stage, the retailer and manufacturer bargain

over the wholesale prices. In the second stage the retailer sets retail prices given these

wholesale prices. This timing corresponds to the idea that negotiations over wholesale prices

occur relatively infrequently compared to retailers’ opportunities to adjust retail prices. In

our discussion of the supply-side model, we begin with the retailer profits and retail pricing

decisions and then turn to the bargaining model.

3.2.1 Retailer Profits and Retail Pricing Decisions

The retailer profits and pricing problem is a relatively standard multi-product problem (e.g.

Goldfarb et al. (2009)). For the set of products carried by the retailer r in period t, mrt, the

retailer profits are given by

Πmrtr (·) =

∑j∈mrt

(prjt − wrjt) smrtrjt (prjt)Mrt, (4)

where Mrt is the size of the market and smrtrjt are the shares for product j in retailer r at

time t when consumers face as the feasible choice options all products in the set of products

dummies, the cost instruments have relatively little explanatory power. Note that later we use these costvariables as cost index variables in the cost function.

20

mrt. Note that this set of products may be smaller for specific consumers because of lacking

hardware ownership or distribution.

The optimal retail price decisions take wholesale prices as given and follow standard

monopolist retailer price setting (see, e.g., Nevo (2000a)). The optimal pricing policy in

matrix format are, p = w+Ω(p)−1s(p), where Ω(p) is the relevant matrix of share derivatives.

Note also that we can solve directly for wholesale prices as w = p − Ω(p)−1s(p), which is

how in our empirical analysis we recover wholesale prices from retail prices. The bargaining

model that we discuss next takes the retail pricing policy as given.

3.2.2 ‘Nash in Nash’ Bargaining

The negotiation between manufacturer and retailer over wholesale prices is formulated as a

‘Nash in Nash’ bargaining problem. In this problem, each manufacturer and retailer pair

bargain over each of the brands’ wholesale prices. These bilateral bargains occur simultane-

ously and without knowledge of the other bargains, but with the participants maintaining

passive beliefs regarding the outcomes of those bargains. Note that renegotiation is ruled

out here, which greatly reduces the computational complexity of the problem.

A central quantity of interest in the bargaining outcomes are the disagreement payoffs,

which determine the outside option of each participant in the bargain (and therefore the

strength of their bargaining position). As discussed above, the retailer’s disagreement payoff

is the profit obtained excluding from the product set the manufacturer’s product that is being

negotiated. This disagreement payoff reflects how much of the demand would be diverted

to other products, how the retailer would adjust the prices, and what the margins of those

products would then be. For the manufacturer, we assume that bargaining takes place

separately for each brand, so the disagreement payoff is the profit made by the manufacturer

(from that retailer) for the remaining brands (with the passive beliefs implying that the

wholesale prices of those remaining products would not change).

Note that we formulate these bargains as brand specific, so that a given manufacturer

21

bargains with the retailer separately for each brand within their portfolio, taking the other

bargains as given.10 We allow separate bargains for the multiple market areas of a retailer

in order to be consistent with the demand estimation as geographies vary in preferences and

substitution patterns even within a retail banner. We note that our estimates reveal that

the few banners with multiple RMAs (e.g., Kroger, Safeway) largely have similar bargaining

power estimates that are not statistically significant above the expected rate for multiple

hypothesis tests.

The Nash product for the bilateral bargaining game between manufacturer f and retailer

r over brand k is represented as a function of the wholesale price involved in the current

bargain, wr,kt, as well as the remaining wholesale prices, wr,−kt, which are assumed known

under the passive beliefs assumption. The relevant Nash product is given by

(ΠJrtr (wr,kt, wr,−kt)− ΠJrt−k

r (wr,−kt))βrkt (ΠJrt

f (wr,kt, wr,−kt)− ΠJrt−kf (wr,−kt)

)1−βrkt(5)

where βrkt ∈ 0, 1 is the bargaining power of the retailer and Πmh (wr,kt, wr,−kt) represents

the profits for player h ∈ Retailer = r, Manufacturer = f and for retailer product set

m, which is specific to time period t. These retailer product sets are Jrt, denoting the full

set of products available in retailer r, Jrt − k, denoting the same set less brand k. The

corresponding manufacturer product sets are frt, denoting the set of products in retailer r

owned by firm f , which includes brand k, and frt−k, denoting the set of products in retailer

r owned by firm f , excluding brand k. Note that the profit functions Πmh (·) take as retail

prices the optimal prices for the given product set given the wholesale prices. As a result,

the retail prices differ under agreement and disagreement.

This bargaining model has at its extreme values of βrkt specific supply models (see ap-

pendix D for details). In particular, if βrkt = 1 for all k brands in a given retailer r and

10Note that an alternative would be for the manufacturer to bargain over all products in their portfolioat once. With our model set-up, this alternative would imply that the retailers would be forced to carry allor none of the brands in the manufacturer’s product set. In practice, we in fact observe retailers carryingsubsets of the products and find the current assumption preferable. A similar argument (and assumption)is made in Grennan (2013), for similar reasons.

22

period t, then the equilibrium behavior coincides with the monopolist retailer that sets

wholesale prices equal to the manufacturers’ marginal costs, which is the fully-coordinated

channel outcome and equivalent prices to the non-linear contracting case that solves the

double-marginalization problem via including a fixed transfer fee in the contract between

manufacturer and retailer. In contrast, if βrkt = 0 for all k brands, then manufacturers offer

(linear) wholesale prices accounting for the competing manufacturers and the fact that the

retailer sets prices after them. In this sense, the model nests some important supply-side

models that are commonly used in the empirical and theoretical literatures (see Iyer and

Villas-Boas (2003) for a related discussion with a different utility function).11

3.2.3 Manufacturer Profits

We now specify manufacturer profits including two modifications to the standard multi-

product form to fit our empirical setting. As a starting point, we define manufacturer profits

in retailer r and period t with retailer product setmrt and manufacturer product set frt ⊂ mrt

are given by

Πmrtf (·) =

∑j∈frt

(wrjt − crjt) smrtrjt (prjt)Mrt, (6)

where crjt is the manufacturer’s marginal cost of production. This marginal cost is a func-

tion of variables Xc,rjt and parameters θc. In our setting, we use a linear cost function,

crjt = Xc,rjtθc. We allow costs to vary as a function of the relationship that each brand

has with Keurig (either owned, licensed, partnered, or unlicensed, which serves as the ex-

cluded category), the brand’s vertical positioning in quality space (either a premium or value

offering, which correspond to the highest priced and lowest priced product types), as well

as commodity prices for the primary coffee beans used to produce at-home packaged coffee

products (Colombian milds).12

11Under the assumption of monopoly retailers, in our empirical analysis, we find that the data rejectβrkt = 1, offering some evidence that with our monopolist retailer set-up non-linear contracts are notconsistent with the data. Relatedly, Iyer and Villas-Boas (2003) with a different model set-up from ours findthat non-linear contracts are not optimal when bargaining is possible.

12In fact, the different coffee bean commodity prices are highly correlated.

23

To this basic profit set up, we add two additional contractual details that are unique

to our setting. First, in both the pre- and post-patent periods, Keurig had partnering and

licensing relationships with many existing national brands. In the pre-patent period, this

was the primary legal avenue by which these national brands could enter the market.13 In the

post-patent period, any firm could enter and produce K-Cups on their own. In both cases,

these contractual relationships influence the bargaining outcomes through the construction

of the agreement and disagreement payoffs, which are detailed below. Second, some retailers

contracted directly with Keurig to produce their private label products, while others utilized

an independent third-party manufacturer. This also has important implications for the

bargaining leverage.

To address the first issue, we develop a representation of these contractual relation-

ships (partners and licensees) directly in the model. First, Keurig manufactures the K-Cup

products for their partners; Keurig’s partners take the product to market themselves (i.e.

negotiated directly with the retailers) and pay Keurig for accrued sales. Abstracting from the

details of these unobserved contracts, we model these contracts as offering revenue sharing

back to Keurig net of Keurig’s costs. Hence, while a given partner, say Starbucks, bargains

with the retailers directly in our framework, they must pay a fraction of the wholesale price

to Keurig. Correspondingly, when Keurig bargains for its wholesale prices (on the products

it owns), it considers the side payment it receives from its partners when constructing its

agreement and disagreement payoffs.

The modified profits for the partner brands are

ΠJrtf (·) =

∑j∈frt

(wrjt(1− κ)− crjt) sJrtrjt (prjt)Mrt, (7)

13In fact, there are several small manufacturers who apparently worked around the patent, but obtainedlimited penetration (e.g., San Francisco Bay and Grove Square).

24

where κ is the net revenue sharing paid to Keurig per unit. Keurig’s profit is then,

ΠJrtf (·) =

∑j∈frt

(wrjt − crjt) sJrtrjt (prjt)Mrt +∑j∈Jp,rt

wrjtκsJrtrjt (prjt)Mrt, (8)

where Jp,rt is the set of partner brands in retailer r in period t.

In addition to partners, Keurig also managed K-Cup products that held licensed brand

names. These licensee brands (e.g., Eight O’Clock and Newman’s Own Organic) are manu-

factured and brought to market by Keurig. Keurig pays a licensing fee back to the licensor

for each cup sold. In our model, these licensing fees appear as part of the costs (to Keurig)

for licensing brands.

The second contractual issue noted above concerns the manufacturing relationships for

the private label products (post-patent expiration). Note that private label brands are owned

by the retailer rather than the manufacturer, so that the retailer can choose amongst multiple

manufacturers for the purpose of producing the product. During our study time frame, the

set of coffee pod manufacturers was relatively limited. We abstract to two manufacturers–

Keurig and another player that has no national brands in the marketplace (a third party

manufacturer). For retailers that have Keurig as the manufacturer, the bargain is between

Keurig and the retailer, where that bargain internalizes all of the profits from Keurig’s other

products (i.e., Keurig’s own, licensing, and partner brands). In contrast, the third party

manufacturer has no other products that it internalizes (making its disagreement payoff zero

should it fail to reach agreement with the retailer).

3.3 FOCs of the Supply-side Bargain Problems

The solution to the aforementioned supply-side bargains requires solving for the optimal

wholesale prices that maximize the Nash product given in equation (5). To do so, we

differentiate (5) with respect to wr,kt. To simplify notation let Rfkt = ΠJrtr (wr,kt, wr,−kt) −

ΠJrt−kr (wr,−kt) and Frkt = ΠJrt

f (wr,kt, wr,−kt)− ΠJrt−kf (wr,−kt).

25

This leads to the following expression:

dRfkt

dwr,ktFrktβrkt +

dFrktdwr,kt

Rfkt (1− βrkt) = 0 (9)

Note that this first order condition is invariant to constant factors (as are Nash Products

in general). The full calculations for the derivatives included in equation (9) are presented

in Appendix E.

For our estimation, a different form of the FOC is useful. Dropping the r and t subscripts,

we can rewrite the FOC as

βk1− βk

= −dFk

dwkRk

FkdRk

dwk

. (10)

3.4 Econometric Errors and Estimation Procedure

Given this model set-up, we rewrite the bargaining power parameters, βrkt, as the ratio,

φrkt = βrkt1−βrkt

. Following Grennan (2013), we assume these to take the following form:

φrkt = φrk ∗ εrkt, (11)

where εrkt is referred to as the bargaining residual and represents the econometric error in

the model that we will interact with instruments during estimation.

To compute supply side parameter estimates, we use a non-linear generalized method of

moments procedure, where the moments are E (log(εrkt) ∗ Zrkt). We note that the econo-

metric error is calculated by substituting equation (10) into (11).

We separate the parameters into two groups–those corresponding to the marginal costs,

θc and those corresponding to the bargaining power parameters, θβ. We note that equation

(10) can be written as φrkt (θc), and equation (11) can be written as εrkt (φrkt (θc) , θβ). This

naturally gives rise to a simplified computational approach that is reminiscent of the BLP

inner-loop/outer-loop algorithm. Specifically, we use a non-linear optimization routine that

optimizes over the parameters θc. For any value of θc, we can calculate the (linear) parameters

26

θβ that minimize the objective function analytically. In this way, we concentrate these

parameters out, which allows us to include a large number of parameters in θβ. In our

setting, θβ includes one bargaining power parameter for each retailer-manufacturer brand

pair, leading to over 500 such pairs.

To illustrate how the actual estimation works, we first rewrite equation (10) (dropping

the subscripts for f , r, and t) as

φk = −dFk

dwk(θc)Rk

Fk (θc)dRk

dwk

. (12)

Calculating the βk at each iteration of the optimizer would be computationally challenging.

However, given the structure of the problem, and leveraging the information set of the

researcher, many of the computationally difficult quantities in equation (10) can be pre-

calculated. For these calculations, we take as given the w that we recover using the demand

estimates, regular prices (90th quantile of quarterly prices), and the monopolist retailer

pricing equations. As a result, of the quantities in equation (10), we can completely pre-

calculate the Rft anddRft

dwr,ft. Further, the quantities Frt and dFrt

dwr,ftcan be pre-calculated up

to the cost parameters θc.

Note that these pre-calculations involve several steps. First, to calculate the quantities

related to the retailer profits, we need to compute the disagreement payoffs. Because these

payoffs involve counterfactual sets of products, we need to solve for the optimal prices with

the reduced product set Jrt − k. Since we have assumed a monopolist retailer, this prob-

lem has a unique solution and we uncover it by successive approximation (e.g., see Judd

(1998)). Second, for each bargain, we need to simulate the shares for both the agreement

and disagreement product sets, as well as their prices. Third, for each agreement payoff, we

need to simulate the first and second derivatives of the shares. Finally, we need to compute

the solution to the system of total derivatives of optimal price by wholesale prices based on

equation (31) provided in Appendix E.

27

Once these pre-computations are complete, we proceed as follows:

1. Guess θc

2. Calculate φrkt (θc)

3. Calculate θβ and log(εrkt)

4. Calculate the GMM objective function

5. Use non-linear optimizer repeating steps 1 to 4

3.5 Identification and Instruments

We note that our model is in principle identified non-parametrically following the arguments

in Berry and Haile (2014). The main distinction is that in our case, we have transformed the

problem from having econometric errors in the costs to in the bargaining power parameters

following Grennan (2013). As discussed above, demand is identified assuming exogenous

prices (given our rich set of fixed effects) using the observed Xjrt and pjrt and a set of instru-

ments that identify the cross-product substitution patterns (i.e., the non-linear parameters)

as suggested by Gandhi and Houde (2015). Given this demand system, then for any given

model of supply, the cost function can be estimated assuming a cost index variable (coffee

bean commodity prices, in our case). This identification argument presumes a cost shock

as an econometric error, whereas we have transformed the errors into a bargaining power

parameter residual. To our understanding, this does not affect the logic of the identification

arguments. The bargaining power parameters are identified from variation in the demand

conditions (e.g., we use functions of brand equities) holding fixed the cost index variable and

equilibrium behaviors. In principle, this identification comes from holding the cost index

fixed and having a constant cost function over variation in demand conditions, which, in

essence, allows matching the observed equilibrium behaviors (i.e. prices) to the (same) best

fitting supply model (i.e., bargaining power parameters). Of course, these arguments from

28

Berry and Haile (2014) discuss non-parametric identification, whereas we impose a number of

parametric assumptions (e.g., restricting the set of supply models to the class of bargaining

models with monopolist retailers and with pairwise bargaining powers).

Practically, we need (at least) as many moments in our supply-side estimation as pa-

rameters. The moments for the bargaining parameters, θβ, come from a matrix of dummy-

variables (i.e., the bargaining parameters are fixed effects). To estimate the cost function

parameters, θc, we need to address the fact that our bargaining power parameters are fixed

effects that absorb the variation for each RMA-brand pair. Identifying the parameter on

the coffee bean price parameter is trivially separated due to its time variation. However, a

subset of the cost variables are constant across time for subsets of brands (e.g., for premium

brands, owned brands), so that if used directly as instruments, these cost variables would

be perfectly collinear with the bargaining power parameters. To address this, we interact

the cost variables with functions of the brand equities estimated in the demand side model,

which reflect demand shifters and are time-varying. Specifically, we use the brand equities

themselves, exponentiated brand equities, and the exponentiated brand equities divided by

the sum of the exponentiated brand equities for the retailer. In principle, these instruments

trace out the bargaining residuals to be independent of the demand conditions for relevant

subsets of brands that should face the same costs. In other words, they enforce that the

costs be the same in expectation as the demand conditions change, which closely follows the

logic of the non-parametric identification of the supply interactions.

4 Empirical Results

In this section, we discuss results from the structural demand estimation and then the

structural supply model.

29

4.1 Demand Model Estimates

Table 4 presents parameter estimates for the main parameters of interest, namely those

relating to price and heterogeneous substitution effects. Recall that the model includes

many additional controls, which are not reported here for brevity. The price coefficient is

negative and significant and yields an average own price elasticity of -2.89. This own price

elasticity is in line with other CPG categories, and is very similar to estimates using this data

and simpler models that do not capture substitution between brands as well, including a log

shares-log price regression (-3.06) and a model with no heterogeneity or ACV and installed

base correction (-3.10). The model reveals substantial heterogeneity in tastes for three of the

segments, namely single-cup, main and instant, whereas tastes for the premium segment are

relatively homogeneous. The model reveals significant, but modest heterogeneity in price

sensitivity. This modest heterogeneity may be due to the presence of segment heterogeneity,

since these segments exhibit a sharp degree of vertical differentiation.

Variable Estimate Std. Err. Signif.Mean Price -3.006 (0.001) **SD Price 0.109 (0.022) **SD Main 1.472 (0.020) **SD Premium 0.012 (0.099)SD Instant 4.693 (0.028) **SD Single cup 1.218 (0.033) **

Table 4: Estimates of Non-linear parameters

Figure 4 shows how the ‘brand intercepts’ compare between private label products and

the leading national brand for each segment in each of the 72 RMAs. The figures contain the

average (over all of the six-month time periods) brand intercept estimates for the correspond-

ing brands in each RMA. To present these values on a single graph, each brand intercept is

normalized by subtracting the mean of it’s segment’s leading national brand intercept (i.e.,

the leading national brand’s mean intercept is zero). Looking first at figure 4a, we can see

that, while the median brand intercept of the leading national brand is greater than that

30

of the private label, the distributions do overlap, particularly in the premium and single-

cup segments. Figure 4b, which presents the same comparison, using differences instead of

levels, illustrates that the overlap is not simply due to common market shifts, but rather

due to some private labels achieving brand equity levels near those of the national brands.

This suggests that the products do share similar positions in vertical quality space (for at

least some retailers), and as a result, compete for the same consumers. Moreover, it also

demonstrates that there is heterogeneity (across retailers) in the degree to which they do so,

providing a source of useful variation for the supply-side bargaining problem. For instance,

for the single-cup segment, most of Safeway’s RMAs are towards the top, and Wegmans is

at the very top, whereas most Kroger RMAs are located in the middle of the distribution.

1 2 3 4 5 6 7 8

−4

−3

−2

−1

01

2

Avg

. Bra

nd In

terc

ept (

Less

NB

Mea

n)

1_PL vs. Folgers 2_PL vs. Starbucks 3_PL vs. Nescafe 4_PL vs. Keurig

(a) Private Labels vs. Nationals

1 2 3 4

−4

−3

−2

−1

0

Diff

in B

rand

Inte

rcep

t (P

L −

NB

)

1_PL vs. Folgers 2_PL vs. Starbucks 3_PL vs. Nescafe 4_PL vs. Keurig

(b) Differences

Figure 4: Private Label Brand Qualities

In addition to the variation in brand intercepts, our supply-side model builds on the sub-

stitution patterns captured in the demand model. In particular, our interest is in capturing

aspects of the vertical segmentation (along price dimensions) within the K-Cup segment. To

illustrate these substitution patterns, we present cross-price elasticities for a subset of brands

and RMAs for the private labels in Table 5. The pattern of cross-price elasticities is sensible

with brands that are positioned vertically close to one another (e.g., Eight O’Clock and San

Francisco Bay) having higher elasticities and brands positioned further apart (e.g., Eight

O’Clock and Starbucks) having lower elasticities. Private labels have meaningful variation

because of their price positions and brand equity (and the resultant market shares). As

31

examples, Giant Maryland is an upscale chain and has higher elasticity to Peet’s and lower

to San Francisco Bay, whereas Supervalu Shoppers and Albertsons both have lower quality

private labels, and so have lower elasticities to Peet’s. Finally, we mention that Wegmans

has a much higher private label share than most other private labels and as a result has

much higher cross-elasticities. This is consistent with Wegmans strong private label share

and positioning as a retailer.

Brand SF Bay 8 O Clock Folger’s Keurig Starbucks Peet’s

Giant Maryland 0.094 0.141 0.141 0.141 0.140 0.173Albertsons NA 0.114 0.109 0.109 0.108 0.083Supervalu Shoppers NA 0.122 0.133 0.135 0.134 0.094Wegmans 0.766 NA 0.764 0.765 0.762 0.762

Table 5: Cross-Price Elasticities for Select National and Private Label Brands. Rows arethe brand that lowers price and columns the brand that is impacted. NA indicates the brandis not available in that retailer

We next examine whether the basic implications of an improved bargaining position

are apparent in the wholesale prices we recover from the monopolist pricing assumption.

Specifically, we consider for the same brands as presented in Table 2 (those available at least

six months prior to the patent expiration) whether the wholesale prices decrease on average

in the four quarters after the patent expiration versus the four quarters before the expiration.

Table 6 presents the analysis.

The estimated differences are all negative except in two cases, Caribou Coffee and New-

man’s Own Organics, the same brands that were found in Table 2 to increase the retail prices

following the patent expiration, suggesting a shift upmarket. For the remaining brands, the

decreases are between 3% and 7% with the second largest difference being for Keurig, the

leading national brand. These results suggest that, consistent with past research (Meza and

32

Brand % ∆ in w Est. Change S.E. t-stat Obs. Pre Obs. Post

Newman’s Own Organics 3.3% 0.014 0.005 2.68 267 266San Francisco Bay -6.7% -0.021 0.008 -2.59 46 77Starbucks -3.3% -0.019 0.004 -4.34 200 279

Table 6: Percent and Level Changes in w for the year before versus after patent expirationfor brands available at least 6 months before the patent expiration

Sudhir, 2010), the improved bargaining leverage that the private label provides leads to lower

wholesale prices. Our supply-side estimation and analysis further calibrates the magnitude

of this bargaining benefit in the context of the value of the private brand.

4.2 Supply-side Estimates

The supply-side estimation aims to recover two different sets of parameters, θc, which con-

tains the parameters of the cost function, and θβ, which contains the bargaining power pa-

rameters (bargaining ratios) for each retailer-brand pair. We first discuss the cost parameter

estimates and then turn to the bargaining power parameters.

Table 7: Estimates of Cost Parameters- *: p-value<.01

Table 7 presents the point estimates for the full set of cost parameters. The constant

is 9.7 cents, suggesting a modest per-cup cost for single-cup coffee. We find that costs are

influenced by the product’s relationship with Keurig and the commodity prices for Colombian

33

Milds. The coffee beans increase costs approximately one and a half cents per 100 index

points. Keurig’s owned brands are more expensive and licensee brands less expensive than

the third party brands, whereas partner brands are no different in cost. Premium brands

(e.g., Starbucks) are significantly more costly than all other brands, whereas value brands

are not significantly different from mid-range brands in terms of cost. Overall, costs have

meaningful variation, with the standard deviation being 3.3 cents, the interquartile range

covering 4 cents, and the total range covering 12 cents. According to our cost function, coffee

bean commodity costs make up on average 22% of the total manufacturing costs. We note,

consistent with the more involved packaging and processing, this proportion of coffee bean

costs is much lower than the 50% proportion that is presumed in Noton and Elberg (2016)

for traditional (e.g., large cans of) coffee. The modest level of response by manufacturers to

costs is also consistent with the results of McShane et al. (2016), who found that pass-through

by retailers is quite limited.

The bargaining power (ability) parameters include a large number of parameters (over

500), one for each retailer-brand pair in the single-cup segment. The interquartile range of

the bargaining power is between 0.49 and 0.56, with a mean of 0.53 and a standard deviation

of 0.07. For the level of uncertainty estimated from the supply side, all of the estimates are

significantly different from both 0 and 1. Under the assumption of monopoly retailers, a

value of βrkt = 1 produces wholesale prices that are equivalent to those generated under

optimal non-linear contracts in this monopolist retailer setting (i.e., wholesale prices are set

to optimize the pairwise profits and a fixed transfer fee makes the retailer whole). Thus, we

find that the data reject the non-linear contract outcome in our setting.14 Further, we reject

that manufacturers are making take-it-or-leave-it offers to the retailers on linear wholesale

prices, which would be represented as a bargaining power of 0.

Most notably, only 19% of the bargaining power estimates are statistically different from

0.5, which would imply equal weight to the retailer and manufacturer. Overall, these esti-

14If retailers are, in fact, competitive, our model would be mis-specified so that our bargaining powerestimate less than 1 could still reflect some form of non-linear contracts.

34

mates suggest a large degree of homogeneity across both retailers and brands in how much

bargaining power their behavior reflects. Further, the retailer and the brands appear to

have similar levels of bargaining power, consistent with the original symmetric formulation

proposed by Nash (1950). This seems quite reasonable in our context, as the asymmetric

bargaining power itself is intended to reflect differences in patience, tolerance for risk and

the negotiating skills of each party. It is hard to see why these should vary across the two

sides in this setting, given that, in most cases, both parties are large, often publicly traded

corporations with extensive experience in this market. In this case, large variation in the

estimated bargaining parameters might suggest that our measures of bargaining leverage

were incomplete, and there were other sizable determinants of the bargaining outcomes left

unaccounted for. This does not appear to be the case here.

We also examine whether the bargaining power parameters change after patent expi-

ration. We estimate models where we allow the average βrkt to differ the year before the

quarter of the patent expiration (quarter 12 when most private label entry occurs) and the

year after. The mean difference for a model with common changes for all RMAs is -0.0025

(t-stat=-0.41). Further, allowing RMA-level differences in the change in bargaining power

reveals only an average change of -0.004 and only 9 RMAs having more than a 0.02 shift.

Even at 0.02 the change in percent profit increase is quite small.15. Thus, our findings sug-

gest that most of the variation in outcomes with versus without the private label is due to

changes in the bargaining leverage of the two parties rather than bargaining power (ability).

This bargaining leverage is determined by the nature of demand and the brand equities (in-

tercepts) for the products each retailer carries. In particular, for our investigation into the

influence of private brand entry on bargaining outcomes, the private brand equity should be

a central determinant. As noted in section 4.1, we find considerable variation in these brand

intercepts across RMAs.

15The absolute change in percentage profit increase from adding the private label for a shift in bargainingpower of -0.004 is 0.07% and the larger shift of 0.02 is -0.3%. These are very small changes compared towhat is observed as the direct change in profit from adding the private label.

35

5 Counterfactual Experiments

In this section, we use counterfactual simulations to isolate and explore the impact of private

label entry on bargaining outcomes. Recall that much was changing in the single-cup market

over this period. The market for K-Cup coffee was continuing to expand with machine

ownership, branded firms that were unaffiliated with Keurig were entering the market (post

patent expiration), while new affiliated brands were entering in both periods, and most

retailers were launching new private label products (just after patent expiration). To control

for these factors and focus directly on the impact of private label entry, we consider a period

immediately after patent expiration and construct counterfactual outcomes for scenarios

both with and without private label products.

In particular, for each RMA where a private label was actually introduced, we simulate

a counterfactual outcome in which the private label product is removed from the market.

We compute the equilibrium (bargained) wholesale prices, the corresponding optimal retail

prices, and the resulting market shares. These counterfactual values will be denoted with a

superscript CF . We then compare these to the “factual” bargained wholesale prices, optimal

retailer prices and equilibrium market shares, computed with the private label in the market

and denoted with a superscript F . Note that both constructs are simulations, with the

latter corresponding to the “treatment” that actually occurred (i.e. private label entry) and

the former corresponding to the counterfactual “control” condition. We present measures

that reflect both the impact of the private label presence and the proportion that is due to

bargaining benefits versus category expansion. We use percentage changes throughout to

maintain a common scale. In all cases, we consider a setting in which all retailers choose

to have their store brand manufactured by a third-party supplier, as this corresponds to a

case in which retailers have the strongest bargaining leverage. For the following analyses,

we consider all 65 RMAs having 338 RMA-period cases with a (factual) private label entry

as compared to a (counterfactual) market without the private label.

36

(a) Direct PL Profit as % of Profit w/o PL (b) Percent Increase in Segment Profit

5.1 Overall Impact of Private Label on Profits

We begin by quantifying the magnitude of the direct profits generated by the private label

products themselves. In particular, we examine how large the profits from the private labels

are in the single-cup segment, as a fraction of the total segment profits. These “direct

profits” are calculated as(pFPL − wFPL

)shFPL, where pFPL is the retail price of the private label

product, wFPL is the wholesales price the retailer pays to the manufacturer, and shFPL is the

equilibrium share of the PL product. To construct a percentage measure, we divide the

direct profit by the retailer profit from the single-cup segment (without the private label

in the market). The distribution of these percentages across retailers is displayed in figure

5a. Each observation underlying the density plot is an RMA-quarter. Note that retailers

vary quite substantially in this measure of direct profit from the private label. The median

retailer profits from the private label are 13% of the total segment profits without a private

label. Some firms earn considerably more, with Wegmans (which relies heavily on private

label products) holding the extreme position of around 120%. The Wegmans case shows

both the importance of the private label and that some markets had an under-provision of

product options prior to launching the private label. Overall, private labels constitute a

sizable fraction of the retailer profits.

Of course, the net contribution of private label introduction will be less than what is

captured in these direct profits, because this measure does not account for sales that are

37

diverted from the retailer’s other products. The net profit gain from introducing the private

label is presented in figure 5b, which shows the size of the percentage increase in overall

single-cup segment profits attributable to the introduction of a private label product. This

is calculated as the total retailer profit with the private label minus total retailer profit

without the private label divided by the total retailer profit without the private label. Note

that this calculation uses the same periods (i.e., not a before-after analysis). The lift is now

meaningfully smaller, though still quite large in magnitude. The median lift in overall profits

is 9.7%, with the extreme case of Wegmans at 93%. Private labels are a win for all retailers,

but some benefit substantially more than others.

5.2 Sources of Profit: Margin Improvement and Category Expan-

sion

We now consider how the profit gain is achieved. The private label can increase profit by

increasing the total category demand through the lower-priced product offering that draws

consumers away from the outside good and also can command a higher percentage margin.

Alternatively, the profit gain could come from increasing the margins of the existing products

without harming their sales too much.

Turning first to the total category expansion, we calculate the percentage increase in

singe-cup sales (out of total market size) with the private label versus without it. Figure 6a

indicates that the category expansion effect is quite large, increasing demand by an average

of 15%. This suggests there was pent-up demand for lower priced single-cup products and

that the private label satisfies a large segment of this unmet demand. Further, we also find

that (even) with the private label in the market, the average margin for the private labels

(52%) is higher than that of the leading national brand (47%). Note, however, that because

the category expansion arises largely due to the lower priced private label product, it is quite

possible that the average cents margin on product sold might actually fall.

We next examine how the margins on the national brands differ with versus without

38

(a) Percent Increase in Category DemandDue to PL

(b) Percent Increase in Margin on NationalBrands

the private label. In particular, we consider the margins the retailers are able to negotiate

with the national brands following the introduction of the private label product. Figure 6b

presents the density for the margin increase (on national brands) when the private label

is in the market versus the counterfactual outcome when the private label is absent. We

report this as a percentage of the counterfactual margin without the private label. While

the increase is relatively modest on average (2%) and most retailers see an increase of under

3%, again there is substantial heterogeneity, with some retailers achieving gains of 5% or

higher, some substantially less. This margin increase is part of the indirect benefit of private

label entry on the negotiations for the non-private label products.

5.3 Profit Decomposition and the Bargaining Benefit

We now evaluate the amount of profits arising from the bargaining benefit related to the

margin gain and category expansion. We first consider the category expansion. Category