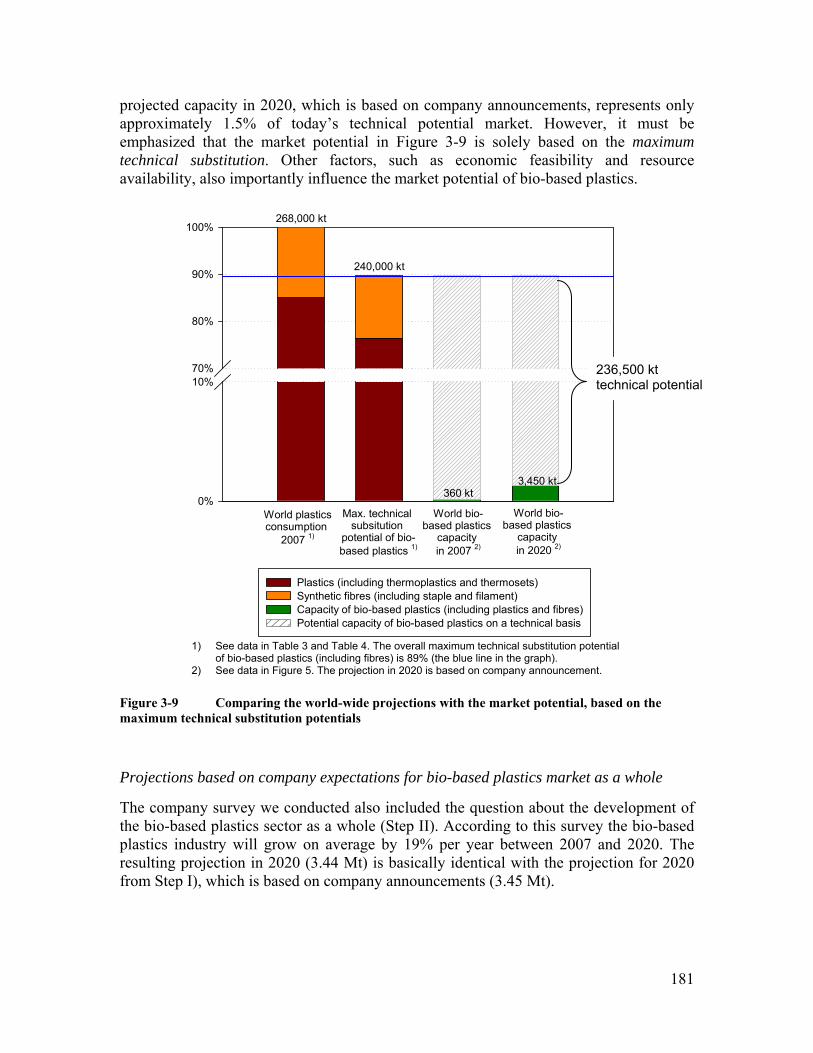

Product overview and market projection of emerging bio-based plastics PRO-BIP 2009 Final report June 2009 Li Shen 1 , Juliane Haufe, Martin K. Patel 2 Group Science, Technology and Society (STS) Copernicus Institute for Sustainable Development and Innovation Utrecht University www.chem.uu.nl/nws www.copernicus.uu.nl commissioned by European Polysaccharide Network of Excellence (EPNOE, www.epnoe.eu ) and European Bioplastics (www.europeanbioplastics.org ) Utrecht The Netherlands Contact authors: Email: 1 [email protected]2 [email protected]Heidelberglaan 2, 3584CS Utrecht, The Netherlands Phone: +31-30-253-7600 Fax: +31-30-253-7601

Transcript

Product overview and market projection of emerging bio-based plastics

PRO-BIP 2009

Final report

June 2009

Li Shen1, Juliane Haufe, Martin K. Patel2

Group Science, Technology and Society (STS)

Copernicus Institute for Sustainable Development and Innovation Utrecht University

www.chem.uu.nl/nws www.copernicus.uu.nl

commissioned by

European Polysaccharide Network of Excellence (EPNOE, www.epnoe.eu) and

European Bioplastics (www.europeanbioplastics.org)

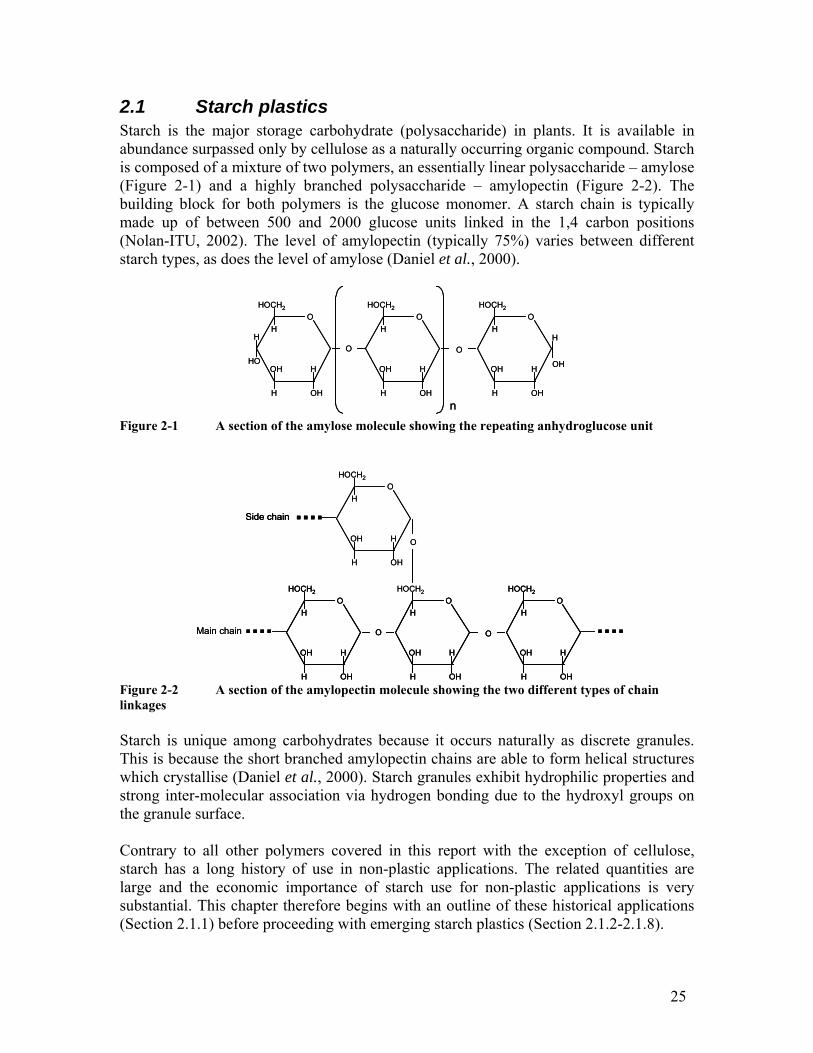

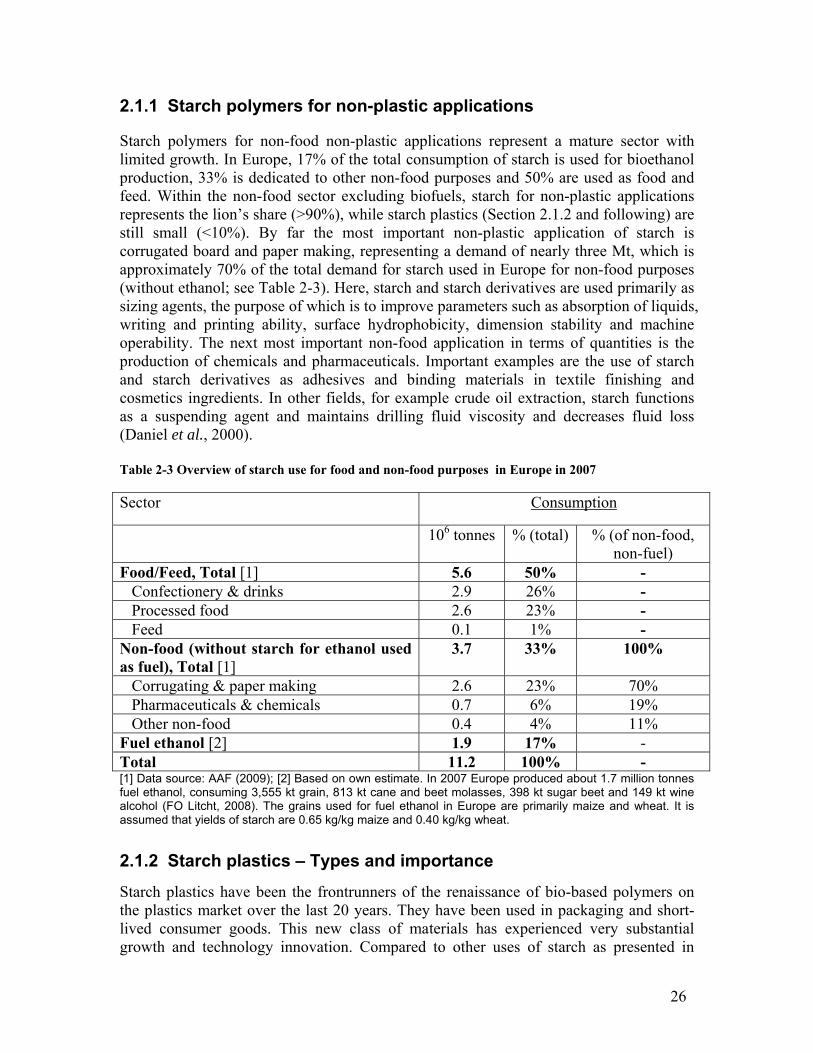

Polymers abound in nature. Wood, leaves, fruits, seeds and animal furs all contain natural polymers. Bio-based polymers have been used for food, furniture and clothing for thousands of years. The first artificial thermoplastic polymer “celluloid” was invented in the 1860s. Since then, numerous new compounds derived from renewable resources have been developed. However, many of the inventions related to bio-based polymers made in the 1930s and 1940s remained at the laboratory stage and were never used for commercial production. The main reason was the discovery of crude oil and its large-scale industrial use for synthetic polymers since the 1950s. Today, public concern about the environment, climate change and limited fossil fuel resources are important drivers for governments, companies and scientists to find alternatives to crude oil. Bio-based plastics may offer important contributions by reducing the dependence on fossil fuels and the related environmental impacts. In the past two decades bio-based plastics have experienced a renaissance. Many new polymers from renewable feedstocks were developed. For example, starch, i.e. a naturally occurring polymer, was re-discovered as plastic material. Other examples are PLA that can be produced via lactic acid from fermentable sugar and PHAs which can be produced from vegetable oil next to other bio-based feedstocks. The developments in the past five years in emerging bio-based plastics are spectacular from a technological point of view. Many old processes have been revisited, such as the chemical dehydration of ethanol which leads to ethylene, an important intermediate chemical which can be subsequently converted into polyethylene (PE), polyvinyl chloride (PVC) and other plastics. Moreover, recent technology breakthroughs substantially improved the properties of novel bio-based plastics, such as heat-resistance of PLA, enabling a much wider range of applications. For numerous types of plastics, first-of-its-kind industrial plants were recently set up and the optimization of these plants is ongoing. Hence, we are at the very beginning of the learning curve. Some of the plant capacities are still rather small when compared to petrochemical plants (e.g. the capacity of Tianan’s PHA plant is only 2 kt), but others are very sizable (e.g. Dow-Crystalsev’s bio-based PE plant will have a capacity of 350 kt). With growing demand for bio-based plastics, it is probably just a matter of time until turn-key plants with large capacities will be commercially available for more bio-based plastics, thereby allowing substantially accelerated growth. The subject of this study is bio-based plastics. In this report, bio-based plastics are defined as man-made or man-processed organic macromolecules derived from biological resources and for plastic and fibre applications (without paper and board).1 The bio-based plastics investigated in this study include starch plastic, cellulose polymers 1 In this report, the term “bioplastics” is avoided due to its ambiguity: it is sometimes used for plastics that are bio-based and sometimes for plastics that are biodegradable (including those representatives that are made form fossil instead of renewable resources).

ii

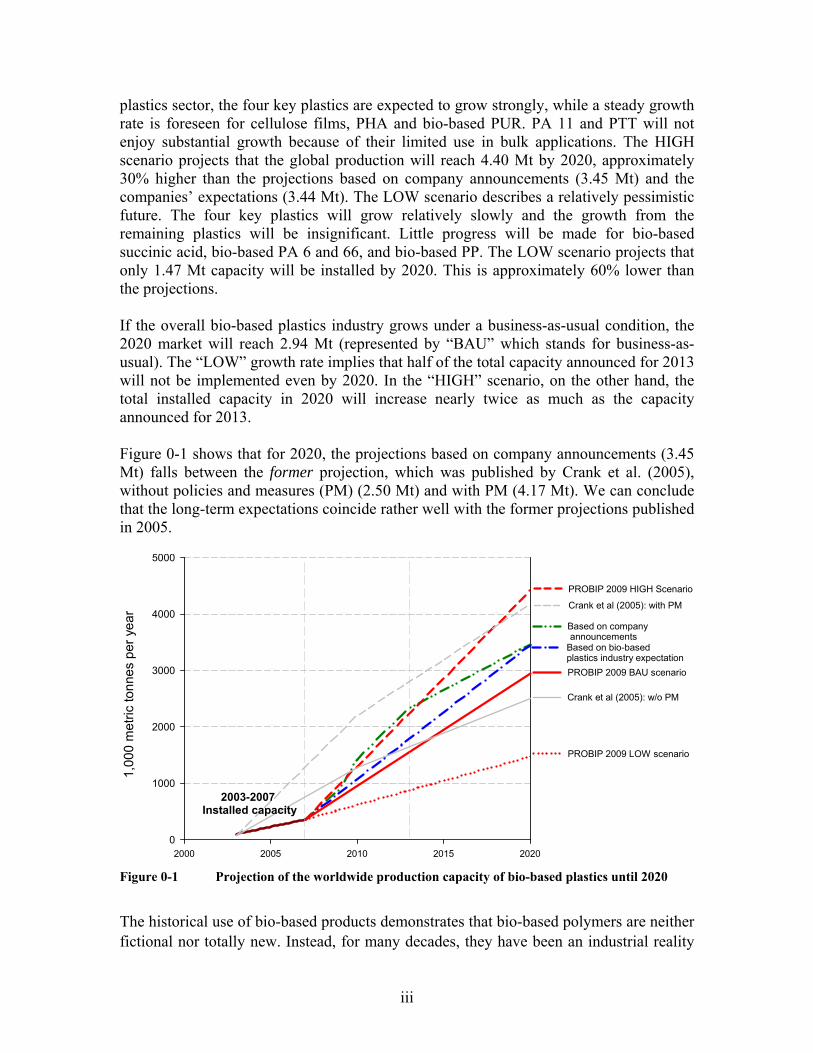

and plastics, PLA (polylactic acid), PTT (polytrimethylene terephthalate), PA (polyamides), PHA (polyhydroxyalkanoates), PE (polyethylene), PVC (polyvinylchloride), and other polyesters (e.g. PBT [polybutylene terephthalate], PBS [polybutylene succiniate], PET [polyethylene terephthalate] and PEIT [polyehthylene-co-isosorbite terephthalate]), PUR (polyurethane) and thermosets (e.g. epoxy resins). For each of these plastics, we present the bio-based production routes, material properties, technical substitution potentials, applications today and tomorrow, emerging producers and wherever possible, costs. This study estimates the global capacity of emerging bio-based plastics at 0.36 Mt (million metric tonnes) by the end of 2007. This is approximately 0.3% of the worldwide production of all plastics (dominated by petrochemical plastics). The current production capacity of bio-based plastics is even smaller compared to “conventional bioproducts”: they represent only 2% of the global production of established bio-polymers (20 Mt; comprising cellulose polymers, alkyd resins and non-food starch without starch for fuel ethanol) and only 0.1% of the world paper and board production. However, the market of emerging bio-based plastics has been experiencing rapid growth. From 2003 to the end of 2007, the global average annual growth rate was 38%. In Europe, the annual growth rate was as high as 48% in the same period. The total maximum technical substitution potential of bio-based polymers replacing their petrochemical counterparts is estimated at 270 Mt, or 90% of the total polymers (including fibres) that were consumed in 2007 worldwide. It will not be possible to exploit this technical substitution potential in the short to medium term. The main reasons are economic barriers (especially production costs and capital availability), technical challenges in scale-up, the short-term availability of bio-based feedstocks and the need for the plastics conversion sector to adapt to the new plastics. Nevertheless, this exercise shows that, from a technical point of view, there are very large opportunities for the replacement of petrochemical by bio-based plastics. As shown in Figure 0-1, the worldwide capacity of bio-based plastics, according to company announcements, will increase from 0.36 Mt in 2007 to 2.33 Mt in 2013 and to 3.45 Mt in 2020. This is equivalent to average annual growth rates of 37% between 2007 and 2013 and 6% between 2013 and 2020. In 2007, the most important products in terms of production volumes were starch plastics (0.15 Mt) and PLA (0.15 Mt). Based on the company announcements it is projected that the most important representatives by 2020 will be starch plastics (1.3 Mt), PLA (0.8 Mt), bio-based PE (0.6 Mt) and PHA (0.4 Mt). Figure 0-1 also shows three PROBIP 2009 scenarios (denoted as “BAU”, “HIGH” and “LOW”). These scenarios are based on expected influencing factors, namely, technical barriers, bulk applications, cost and raw material supply security. The BAU scenario assumes a steady growth of the four key plastics (i.e. starch plastics, PLA, bio-based PE and bio-based epoxy resin) and a modest growth for cellulose films, PHA and bio-based PUR. The BAU projection results in a global production capacity of approximately 3 Mt for 2020. The HIGH scenario shows a fast growing bio-based

iii

plastics sector, the four key plastics are expected to grow strongly, while a steady growth rate is foreseen for cellulose films, PHA and bio-based PUR. PA 11 and PTT will not enjoy substantial growth because of their limited use in bulk applications. The HIGH scenario projects that the global production will reach 4.40 Mt by 2020, approximately 30% higher than the projections based on company announcements (3.45 Mt) and the companies’ expectations (3.44 Mt). The LOW scenario describes a relatively pessimistic future. The four key plastics will grow relatively slowly and the growth from the remaining plastics will be insignificant. Little progress will be made for bio-based succinic acid, bio-based PA 6 and 66, and bio-based PP. The LOW scenario projects that only 1.47 Mt capacity will be installed by 2020. This is approximately 60% lower than the projections. If the overall bio-based plastics industry grows under a business-as-usual condition, the 2020 market will reach 2.94 Mt (represented by “BAU” which stands for business-as-usual). The “LOW” growth rate implies that half of the total capacity announced for 2013 will not be implemented even by 2020. In the “HIGH” scenario, on the other hand, the total installed capacity in 2020 will increase nearly twice as much as the capacity announced for 2013. Figure 0-1 shows that for 2020, the projections based on company announcements (3.45 Mt) falls between the former projection, which was published by Crank et al. (2005), without policies and measures (PM) (2.50 Mt) and with PM (4.17 Mt). We can conclude that the long-term expectations coincide rather well with the former projections published in 2005.

2000 2005 2010 2015 2020

1,00

0 m

etric

tonn

es p

er y

ear

0

1000

2000

3000

4000

5000

2003-2007 Installed capacity

Based on company announcementsBased on bio-based plastics industry expectation

PROBIP 2009 BAU scenario

PROBIP 2009 LOW scenario

PROBIP 2009 HIGH Scenario

Crank et al (2005): w/o PM

Crank et al (2005): with PM

Figure 0-1 Projection of the worldwide production capacity of bio-based plastics until 2020

The historical use of bio-based products demonstrates that bio-based polymers are neither fictional nor totally new. Instead, for many decades, they have been an industrial reality

iv

on a million-tonne-scale. Today, the combined volume of these non-food and non-plastics applications of starch and man-made cellulose fibres is 55 times larger than the total of all new bio-based polymers (approx. 20 Mt versus approx. 0.35 Mt in 2007). The new bio-based polymers may reach this level in 20-30 years from now. The use of starch for paper production only amounts to 2.6 Mt and is hence still six times larger than today’s worldwide production of bio-based plastics. This demonstrates that the production of bio-based products at very large scale is not unprecedented. First-in-kind production of bio-based plastics in large industrial plants should be seen as a large-scale experimental phase in which the strengths and weaknesses of the various bio-based plastics and their production routes become apparent. The experience gained must then be taken into account when the production reaches the steep phase of the S-curve. It will hence take more than two decades from now until meaningful benefits such as CO2 emission reduction will be achieved at the macro level. On the other hand, the advantages of the slow substitution of petrochemical plastics are that technological lock-in can be more easily avoided and that an optimized portfolio of processes can be implemented ensuring maximum environmental benefits at lowest possible costs and minimum social backlash. To conclude, several factors clearly speak for bio-based plastics. These are the limited and therefore uncertain supply with fossil fuels (especially oil and gas), the related economic aspects, environmental considerations (especially savings of non-renewable energy and greenhouse gas abatement), innovation offering new opportunities (technical, employment etc.) and rejuvenation in all steps from chemical research to the final product and waste management. Challenges that need to be successfully addressed in the next years and decades are the lower material performance of some bio-based polymers, their relatively high cost for production and processing and the need to minimize agricultural land use and forests, thereby also avoiding competition with food production and adverse effects on biodiversity and other environmental impacts.

v

Preliminary remarks

Bio-based plastics are in their infancy. There are success stories and very promising developments, but failures and serious problems also exist. This report attempts to give the full picture and to draw fair conclusions.

Given the still early stage of development of bio-based plastics the information basis used in this report may be less complete than for analyses on mature materials (here: conventional plastics). The quality of the information used and presented differs by chapter:

Most of the information given in Chapter 2 can be considered as solid. This applies to both the description of the production process and the material properties. To a lesser extent, it applies to the expected developments in cost structure and selling price. The estimation of maximum technical substitution potential at the end of the chapter should be considered as indicative only.

The projections for future production volumes of bio-based plastics, which are presented in Chapter 3, are subject to large uncertainty. To account for this difficulty, various scenarios are distinguished.

In Chapter 4, the authors attempt to summarise the results, to present a balanced discussion and to draw sound conclusions for the key decision makers, i.e. for policy makers and for companies. Before making use of any results in this report the reader should, however, be aware of the underlying limitations intrinsic in the techno-economic assessment – and especially concerning the projections. This report is based on information on commercialised and emerging bio-based plastics. Other bio-based plastics which are currently in an earlier phase of R&D can be taken into account only partly and only in an aggregated manner, even though some of them might be produced on a respectable scale towards the end of the projection period of this report (year 2020). Bio-based chemicals that are not used for plastics production (e.g. solvents, lubricants and surfactants and other intermediates and final products) are outside the scope of this report; if they develop favourably, this could reinforce also the growth of bio-based polymers.

vi

Acknowledgements

We herewith thank European Bioplastics (www.europeanbioplastics.org) and European Polysaccharide Network of Excellence (EPNOE, www.epnoe.org) who funded this study. In particular, the commitment of Dr. Patrick Navard (EPNOE), Dr. Harald Käb (European Bioplastics) and Mr. Jöran Reske (European Bioplastics) made it possible that this study could be prepared. We thank all experts who have contributed to this report by providing information about their products and processes. Particular thanks are addressed to Dr. Danuta Ciechanska (IWCH, Poland), Michel Geuskens (Rodenberg, Netherlands), Diether Hesse (Telles, USA), Francesco Degli Innocenti (Novamont, Italy), Isao Inomata (JapanBioPlastics Association, Japan), Frits de Jong (BIOP, Germany), Dr. Joseph V. Kurian (DuPont, USA), Guillaume Le (Arkema, France), Dr. Jim Lunt (Tianan, China), Yasuhiro Miki (Kaneka, Japan), Laurent Massacrier (Limagrain, France), Antonio Morschbacker (Braskem, Brazil), Dr. Hans van der Pol (PURAC, Netherlands), Dr. Jan Ravenstijn (DSM, Netherlands), Reichert Ruud (PURAC, Netherlands), Frederic Scheer (Cereplast, USA), Harald Schmidt (Biotec, Germany), Andy Sweeteman (Innovia, UK), Erwin Vink (NatureWorks LLC, USA) and Dr. Sicco de Vos (PURAC, Netherlands). We give special thanks to Christiaan Bolck, Jacco van Haveren and Jan van Dam (all Wageningen UR, Agrotechnology and Food Innovations), for their valuabale suggestions and contributions.

vii

Table of contents

Executive summary.............................................................................................................. i Preliminary remarks............................................................................................................ v Acknowledgements............................................................................................................ vi Table of contents............................................................................................................... vii List of Figures .................................................................................................................... ix List of Tables ..................................................................................................................... xi 1. Introduction................................................................................................................. 1

The plastics sector in perspective and its dynamics........................................................ 4 Bio-based plastics as new option .................................................................................... 8 Objectives and scope of this report............................................................................... 10 Structure of the report ................................................................................................... 12

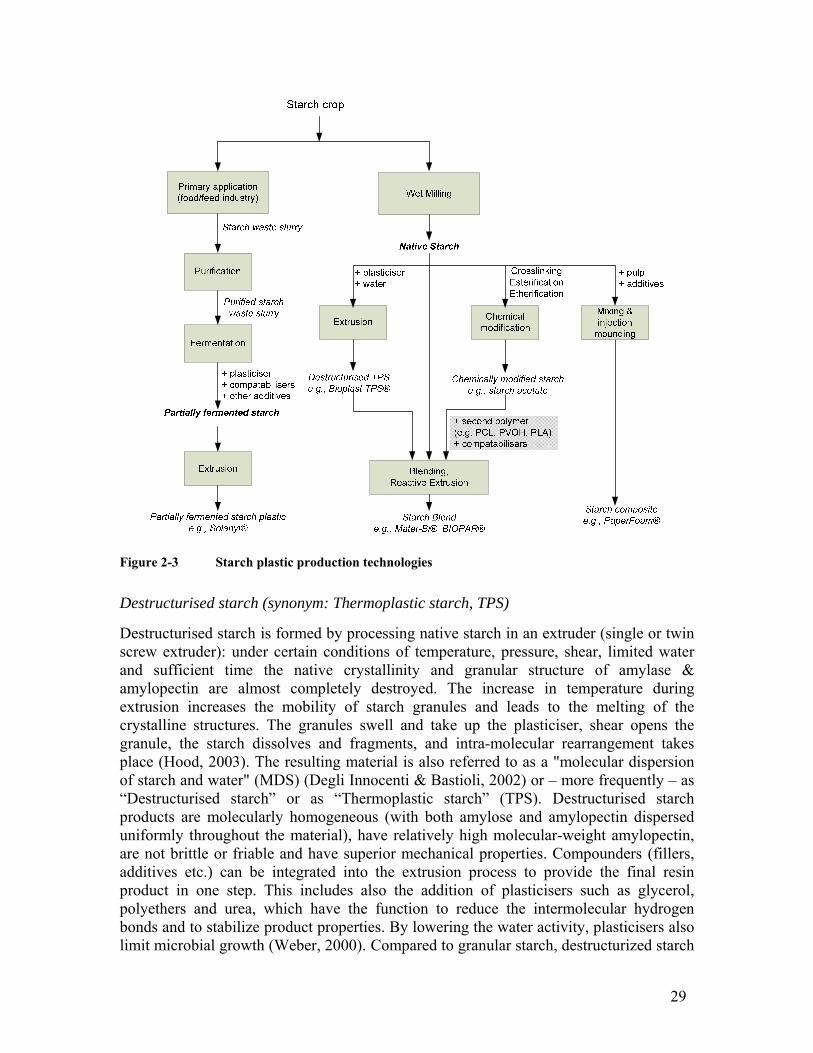

2.1.1 Starch polymers for non-plastic applications............................................ 26 2.1.2 Starch plastics – Types and importance.................................................... 26 2.1.3 Production of starch plastics ..................................................................... 27 2.1.4 Properties .................................................................................................. 34 2.1.5 Technical substitution potential ................................................................ 36 2.1.6 Applications today and tomorrow............................................................. 36 2.1.7 Current and emerging producers............................................................... 38 2.1.8 Expected developments in cost structure and selling price ...................... 41

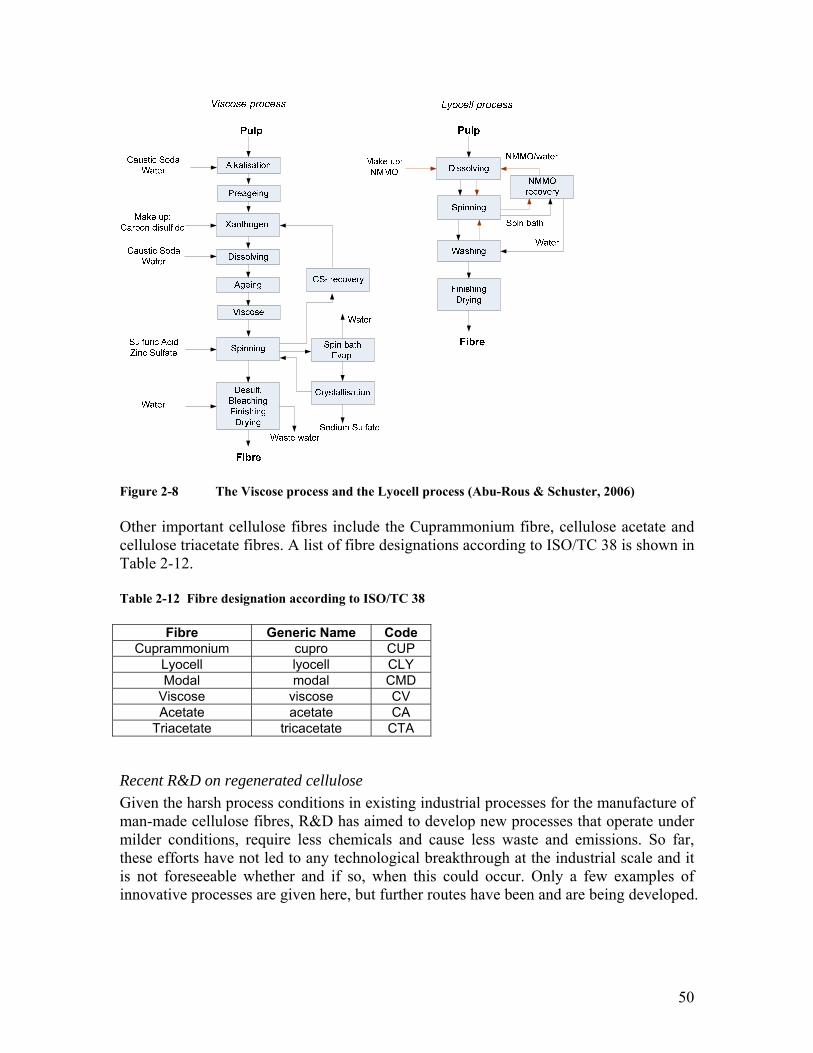

2.2 Cellulosic polymers .......................................................................................... 43 2.1.1 Cellulosic polymers for non-plastic applications...................................... 44 2.1.2 Cellulosic plastics (including fibres) – Types and importance................. 45 2.2.3 Production of cellulose plastics (including fibres).................................... 48 2.2.4 Properties .................................................................................................. 52 2.2.5 Technical substitution potential ................................................................ 54 2.2.6 Applications today and tomorrow............................................................. 54 2.2.7 Current and emerging producers............................................................... 55 2.2.8 Expected developments in cost structure and selling price ...................... 56

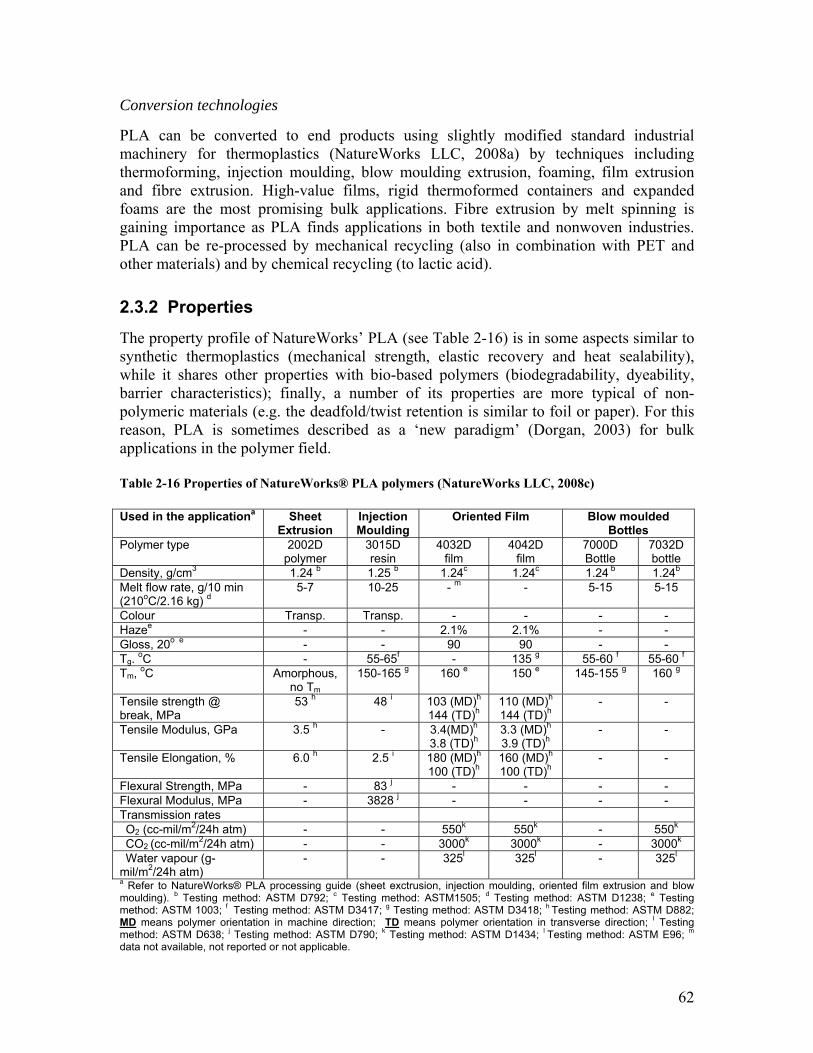

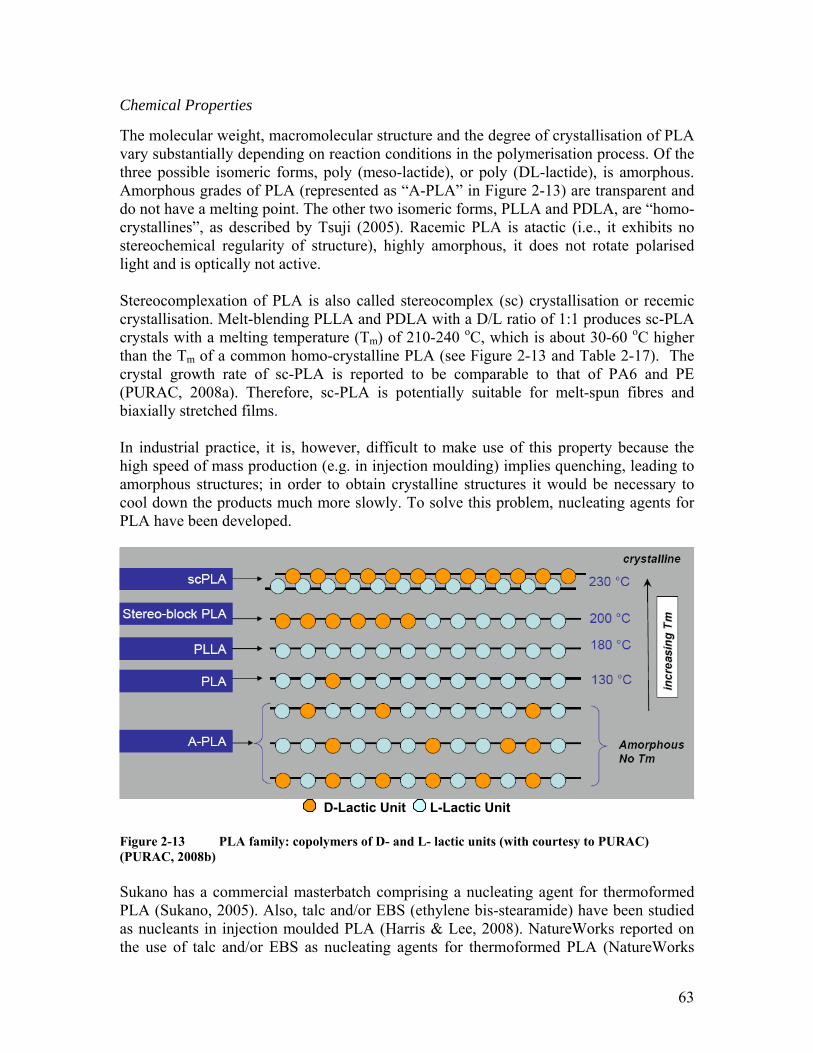

2.3 Polylactic acid (PLA)........................................................................................ 57 2.3.1 Production of PLA .................................................................................... 58 2.3.2 Properties .................................................................................................. 62 2.3.3 Technical substitution potential ................................................................ 67 2.3.4 Applications today and tomorrow............................................................. 68 2.3.5 Current and emerging producers............................................................... 71 2.3.6 Expected developments in cost structure and selling price ...................... 73

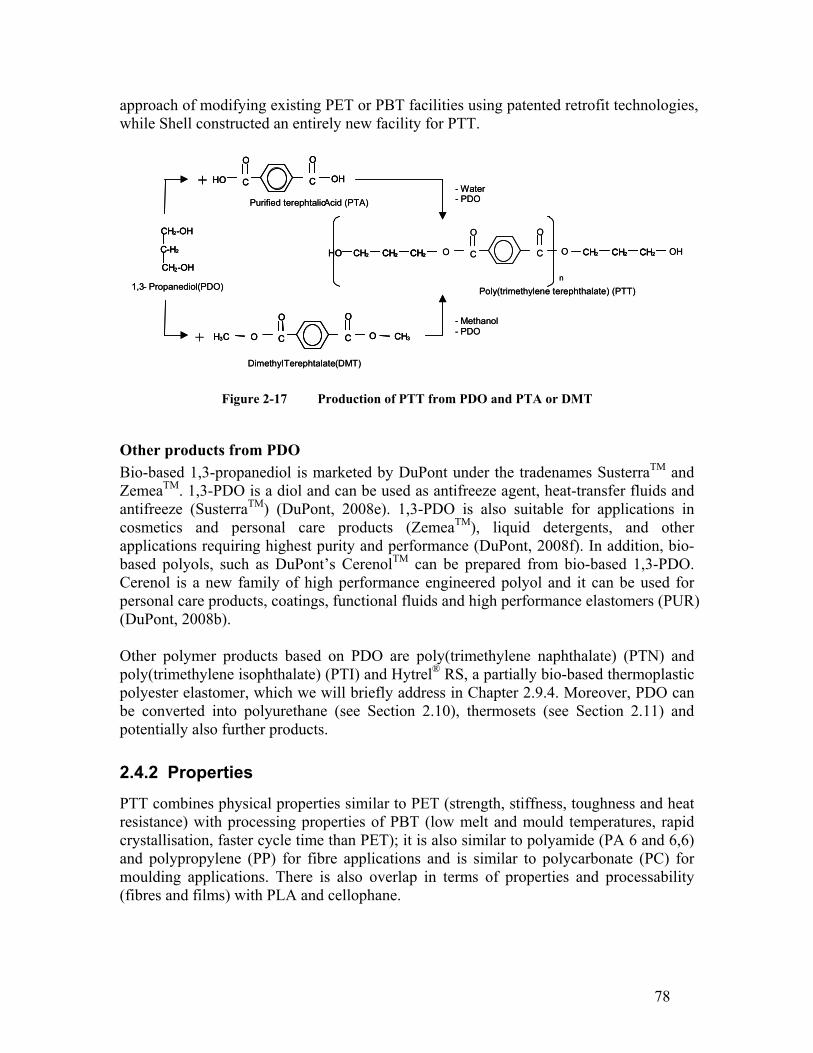

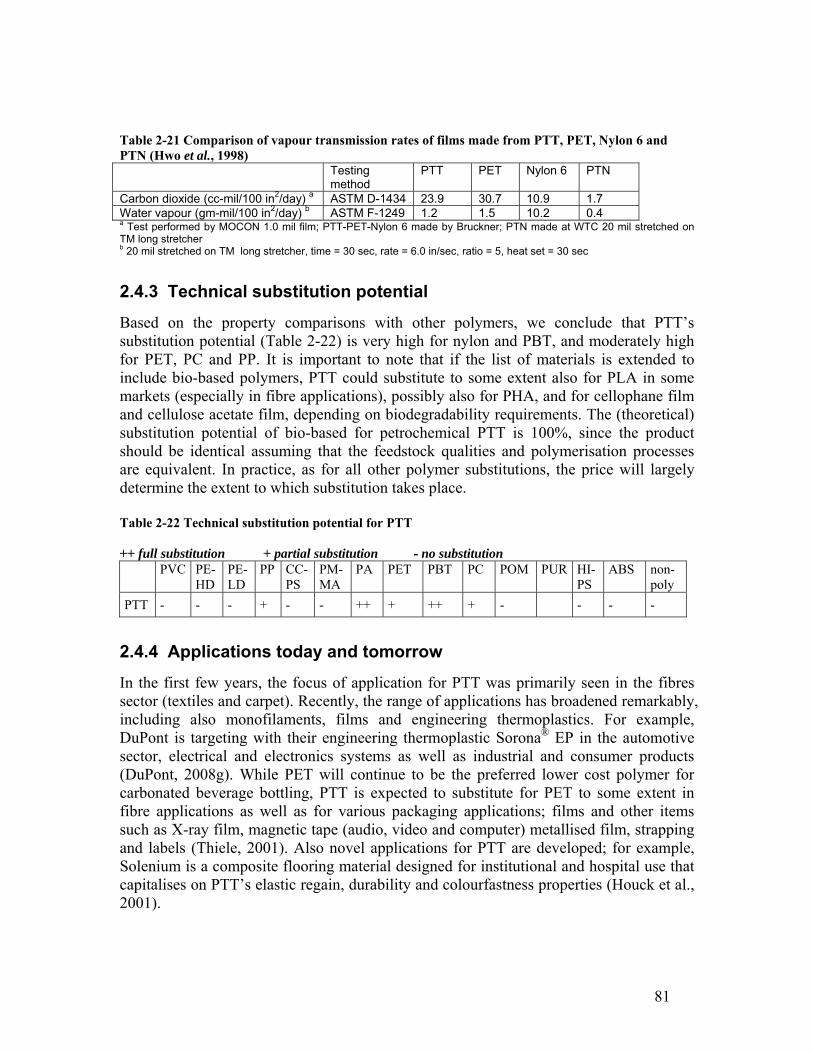

2.4 PTT from bio-based PDO ................................................................................. 75 2.4.1 Production................................................................................................. 76 2.4.2 Properties .................................................................................................. 78 2.4.3 Technical substitution potential ................................................................ 81 2.4.4 Applications today and tomorrow............................................................. 81

viii

2.4.5 Current and emerging producers............................................................... 82 2.4.6 Expected developments in cost structure and selling price ...................... 82

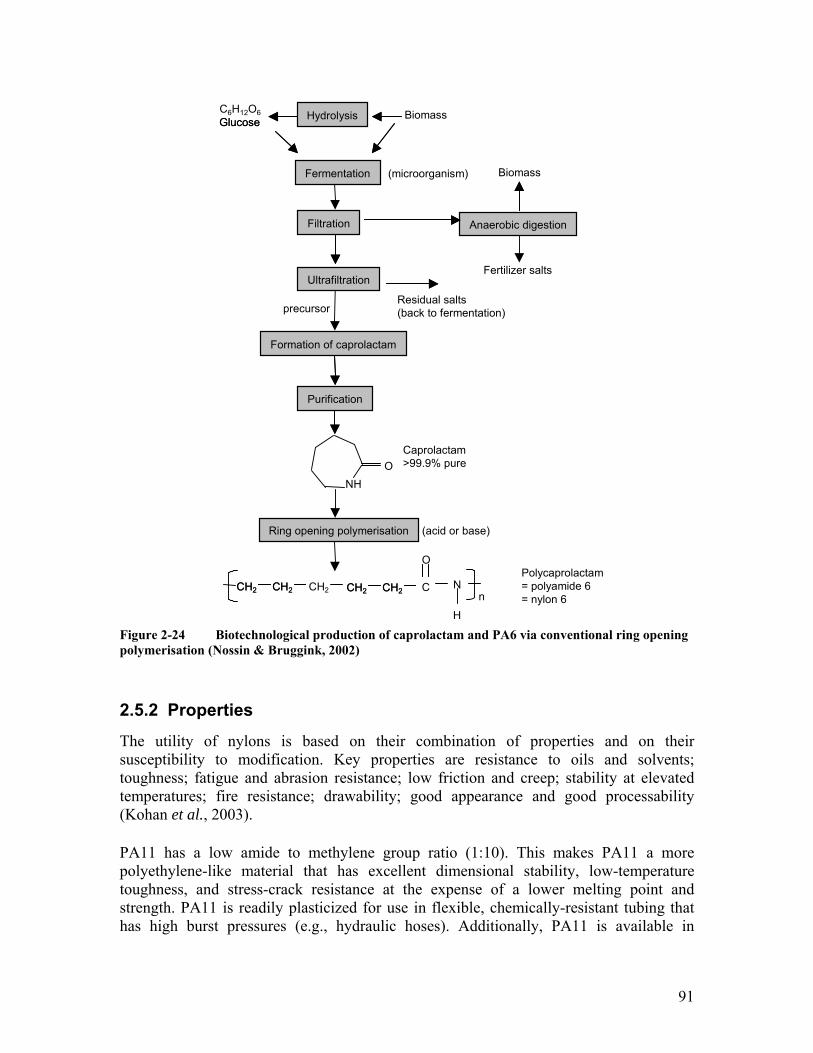

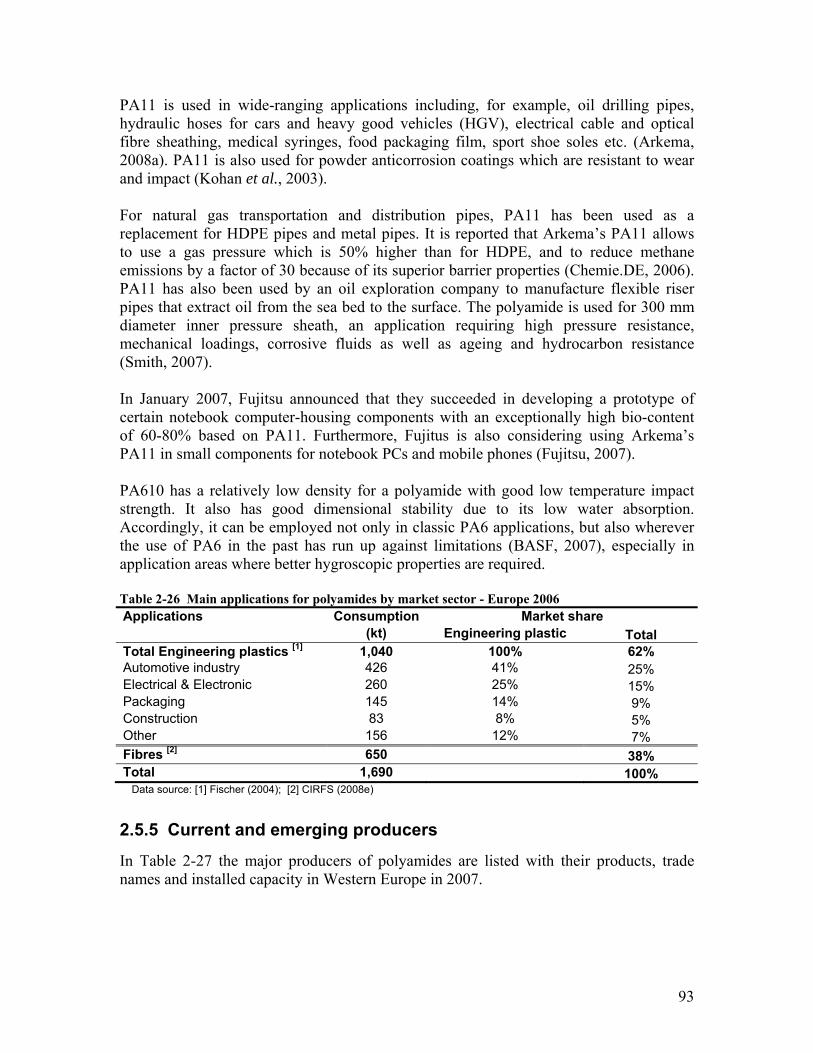

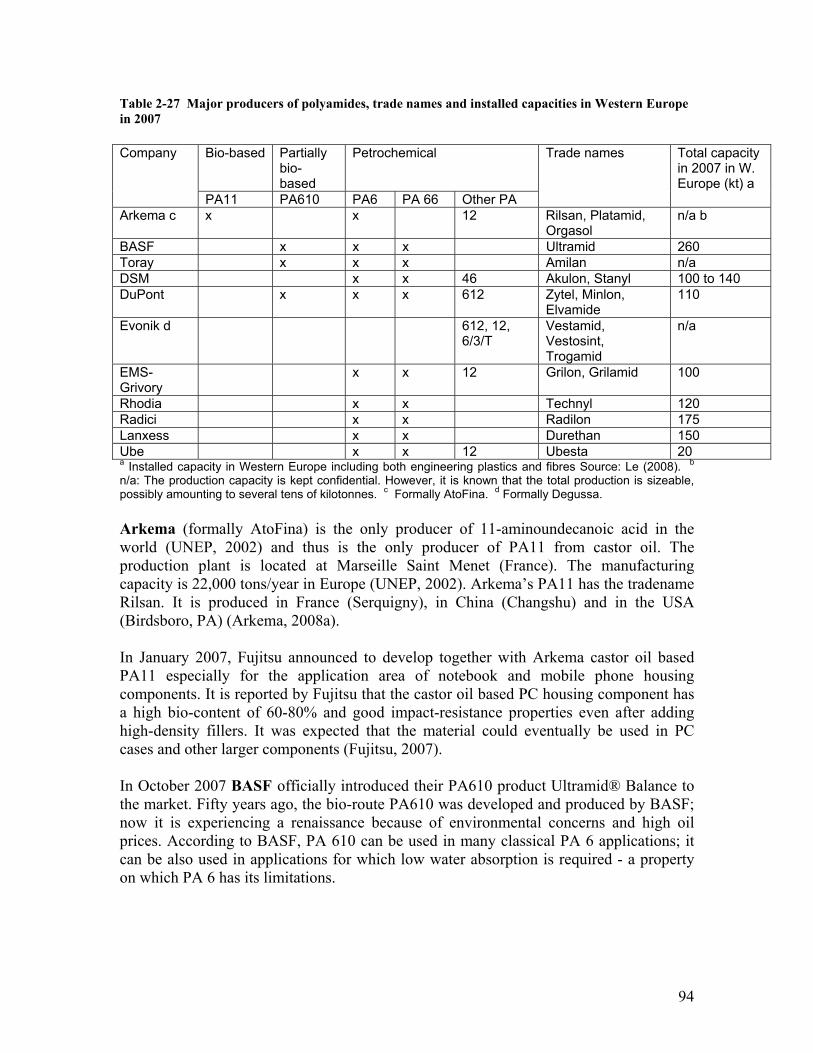

2.5 Bio-based polyamides (nylon) .......................................................................... 85 2.5.1 Production of bio-based polyamides......................................................... 86 2.5.2 Properties .................................................................................................. 91 2.5.3 Technical substitution potential ................................................................ 92 2.5.4 Applications today and tomorrow............................................................. 92 2.5.5 Current and emerging producers............................................................... 93 2.5.6 Expected developments in cost structure and selling price ...................... 95

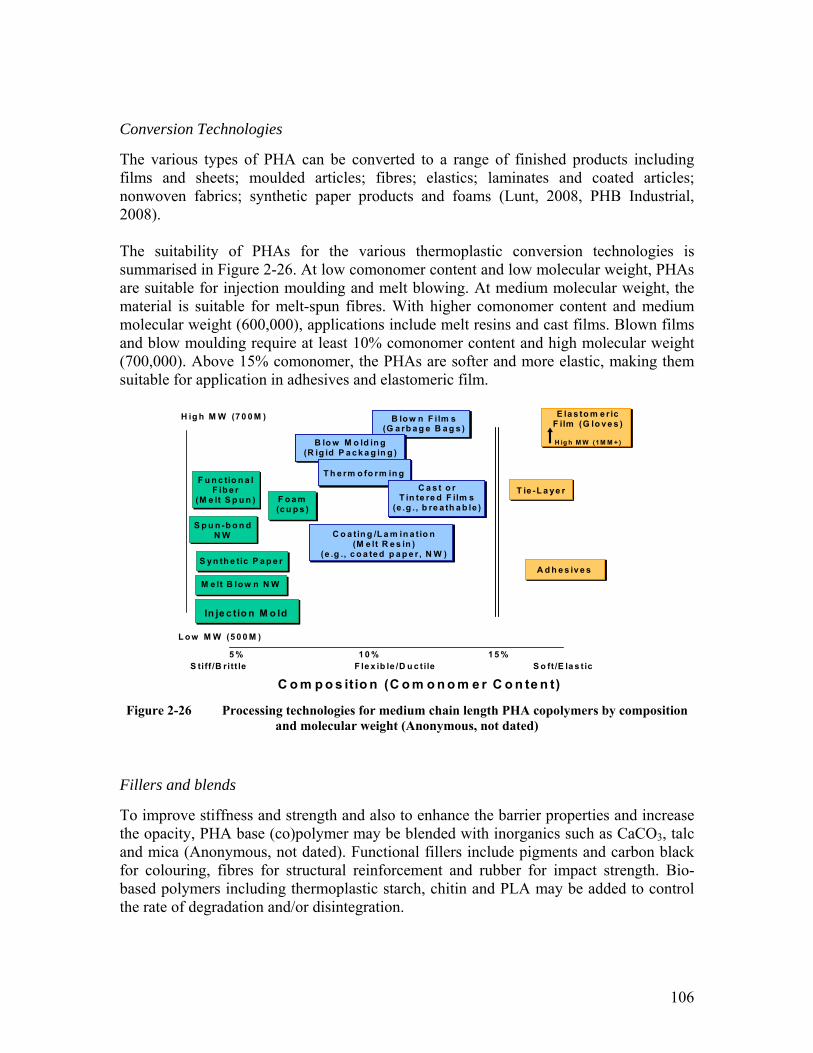

2.6 Polyhydroxyalkanoates (PHAs)........................................................................ 97 2.6.1 Production of PHAs ................................................................................ 100 2.6.2 Properties ................................................................................................ 102 2.6.3 Technical substitution potential .............................................................. 107 2.6.4 Applications today and tomorrow........................................................... 108 2.6.5 Current and emerging producers............................................................. 108 2.6.6 Expected developments in cost structure and selling price .................... 111

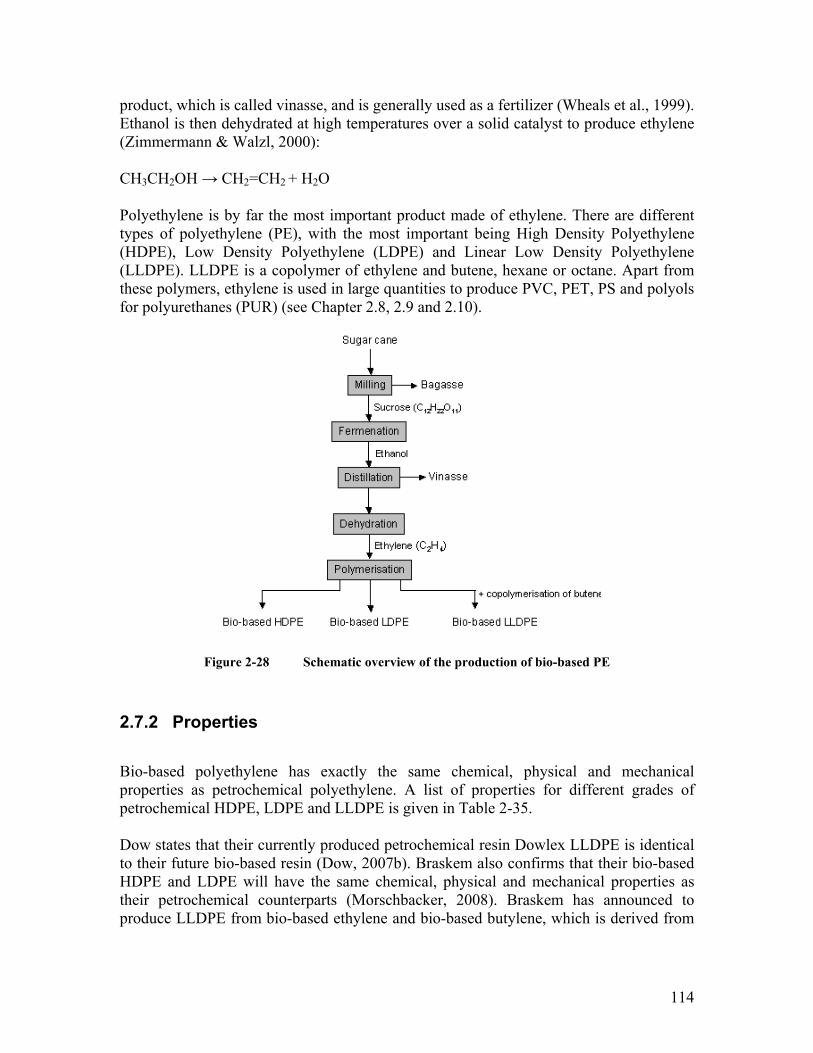

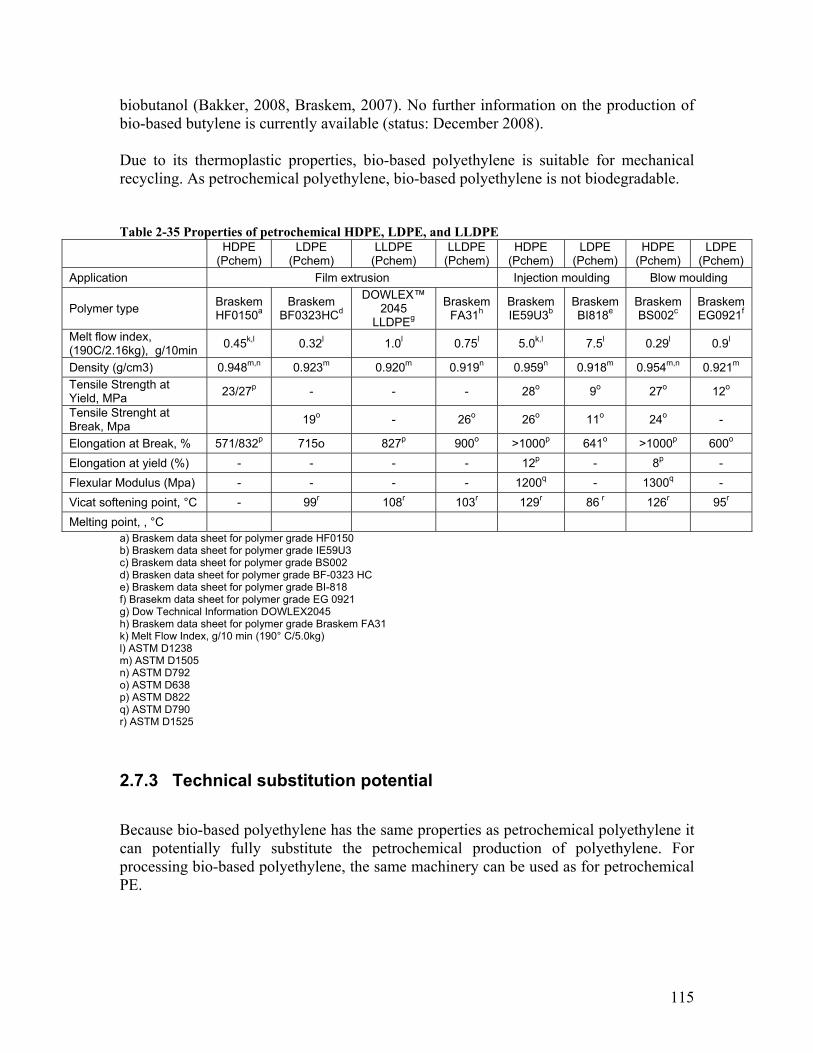

2.7 Bio-based polyethylene (PE) ......................................................................... 113 2.7.1 Production.............................................................................................. 113 2.7.2 Properties ............................................................................................... 114 2.7.3 Technical substitution potential ............................................................. 115 2.7.4 Applications today and tomorrow.......................................................... 116 2.7.5 Current and emerging producers............................................................ 116 2.7.6 Expected developments in cost structure and selling price .................... 117

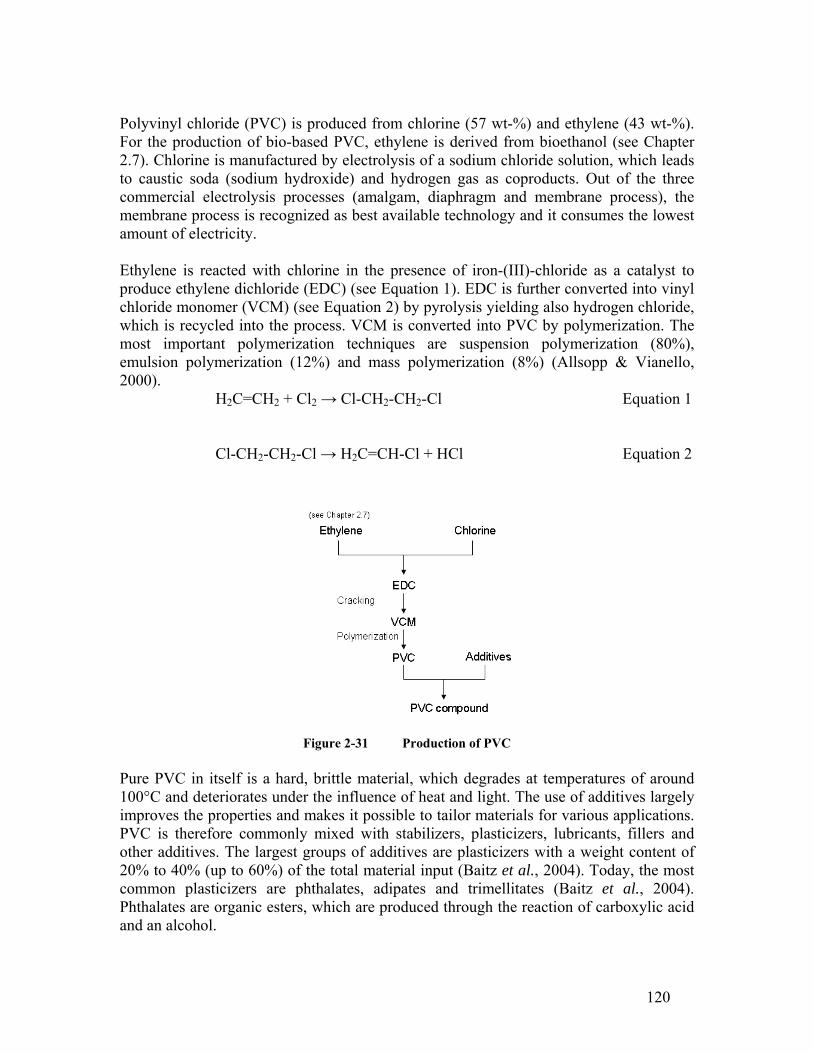

2.8 Polyvinyl chloride (PVC) from bio-based PE ............................................... 119 2.8.1 Production............................................................................................... 119 2.8.2 Properties ............................................................................................... 121 2.8.3 Technical substitution potential ............................................................. 121 2.8.4 Applications today and tomorrow........................................................... 122 2.8.5 Current and emerging producers............................................................. 122 2.8.6 Expected developments in cost structure and selling price ................... 123

2.9 Other emerging bio-based thermoplastics ...................................................... 125 2.9.1 PBT from bio-based BDO ...................................................................... 128 2.9.2 PBS from bio-based succinic acid .......................................................... 131 2.9.3 Bio-based polyethylene terephthalate (PET) .......................................... 134 2.9.4 Polyethylene isosorbide therephthalate (PEIT) ...................................... 137 2.9.5 Further polyesters based on PDO ........................................................... 139

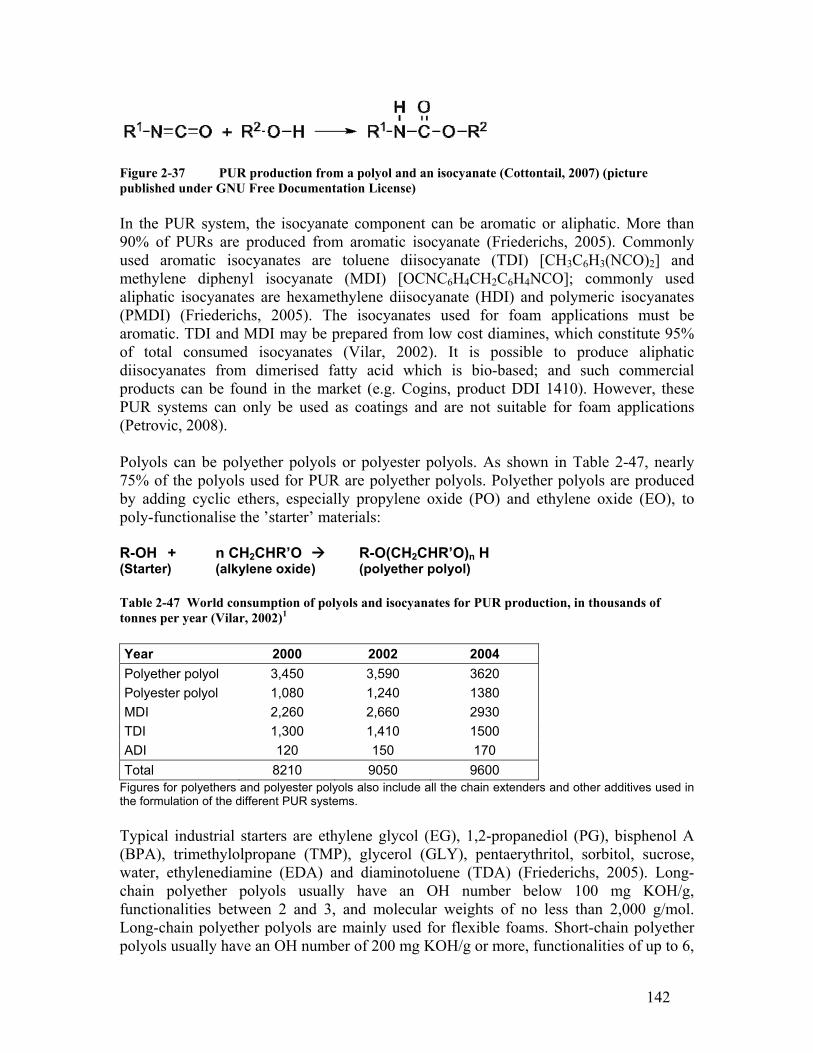

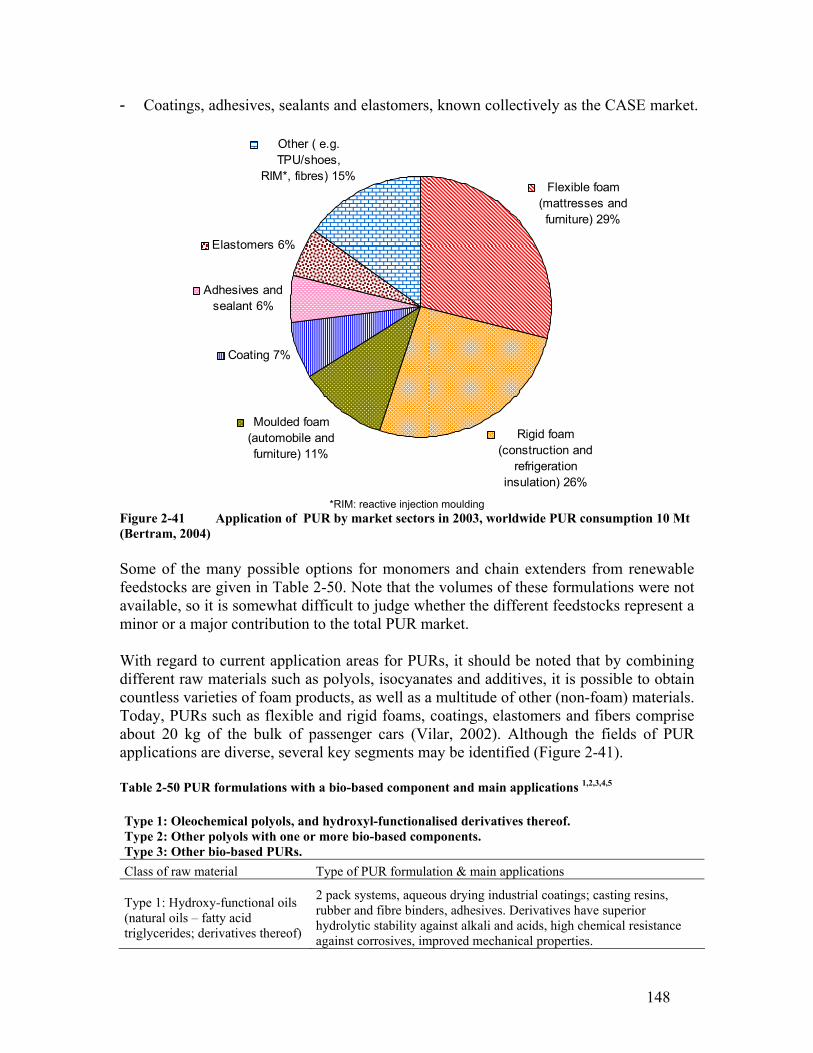

2.10 Polyurethane (PUR) from bio-based polyols.................................................. 141 2.10.1 Production of PUR.................................................................................. 141 2.10.2 Properties ................................................................................................ 146 2.10.3 Technical substitution potential .............................................................. 147 2.10.4 Applications today and tomorrow........................................................... 147 2.10.5 Current and emerging producers............................................................. 149 2.10.6 Expected developments in cost structure and selling price .................... 153

2.11.3 Thermosets based on propylene glycol (1,2 propanediol) ...................... 160 2.11.4 Thermosets based on PDO (1,3 propanediol) ......................................... 161 2.11.5 Other products......................................................................................... 161

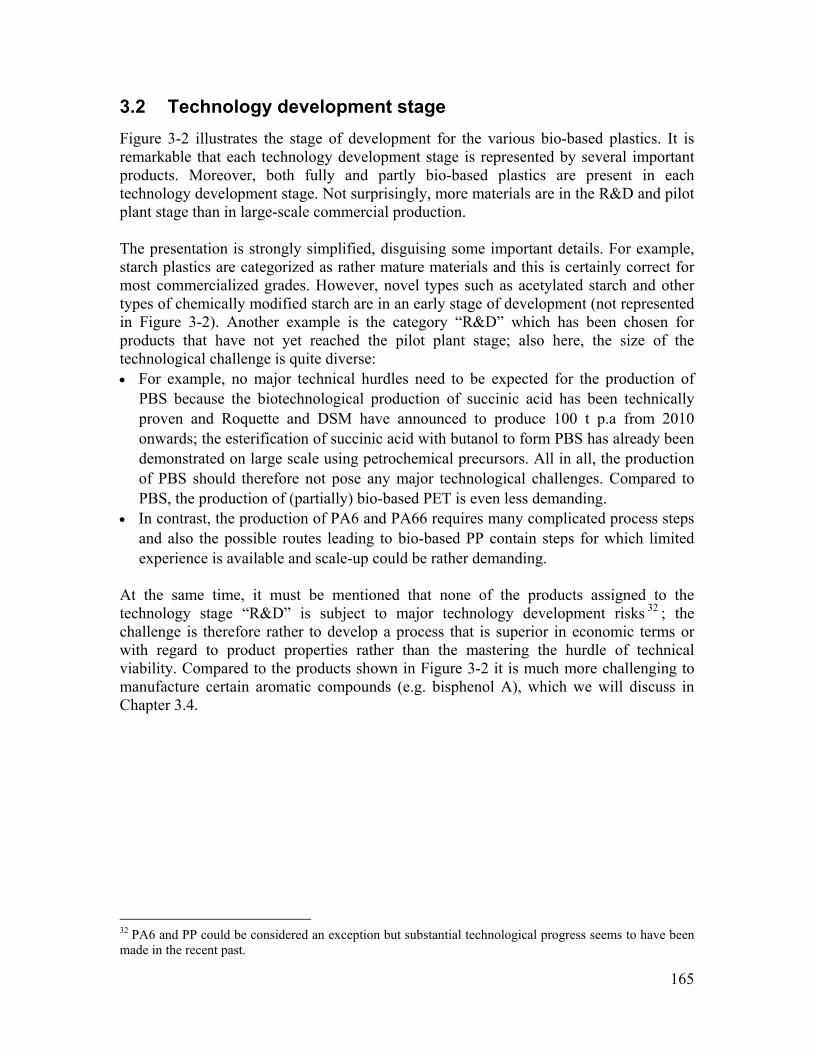

3. Scenarios for markets of bio-based plastics............................................................ 163 3.1 Production volumes and technology level today ............................................ 163 3.2 Technology development stage....................................................................... 165 3.3 Maximum technical substitution potential...................................................... 167 3.4 Further substitution potentials for the longer term ......................................... 171 3.5 Determining factors for the speed of implementation .................................... 175 3.6 Market projections for bio-based polymers .................................................... 177

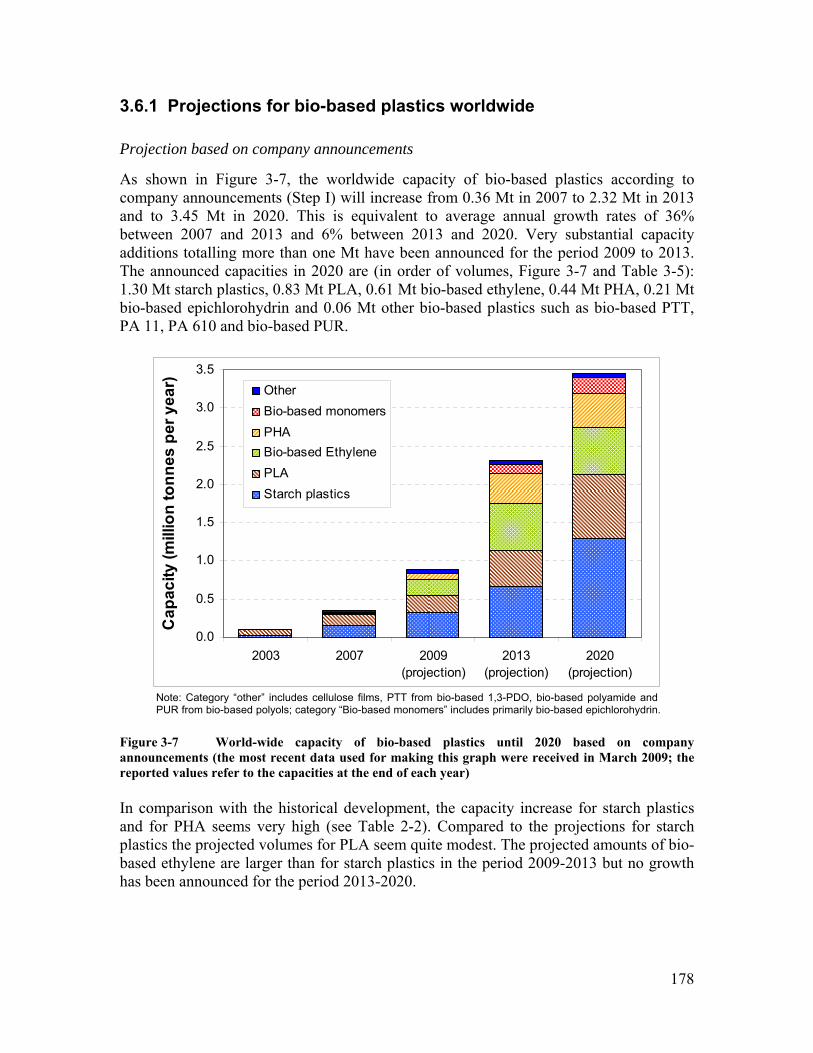

3.6.1 Projections for bio-based plastics worldwide ......................................... 178 3.6.2 Projections for bio-based plastics in Europe........................................... 187 3.6.3 Discussion on the credibility of the projections and comparison with other studies ................................................................................................................. 190

4. Discussion and conclusions .................................................................................... 193 Literature......................................................................................................................... 197 Appendix: List of abbreviations ............................................................................... 226

List of Figures

Figure 0-1 Projection of the worldwide production capacity of bio-based plastics until 2020 .................................................................................................................... iii Figure 1-1 World biomass production (left) and biomass utilised by human (right) ... 1 Figure 1-2 Comparing the global production of paper& board (values for 2006), mature bio-products (values for 2006) and emerging bio-based plastics (values for 2007)2 Figure 1-3 EU-27 production of bulk materials in 2004 (in brackets: values in EU-27 in 2004; 920 Mt in total) (See references in footnote to Figure 1-5).................................. 4 Figure 1-4 World-wide and European production of plastics since 1950 in thousand metric tonnes (PlasticsEurope, 2007) ................................................................................. 5 Figure 1-5 Share of bulk materials used in EU-27 in metric tonnes ............................ 6 Figure 1-6 Worldwide production of synthetic polymers 2006 (PlasticsEurope, 2007) ..................................................................................................................... 7 Figure 1-7 Thermoplastics demand by resin types 2006 (PlasticsEurope, 2007)........ 7 Figure 1-8 Current and emerging (partially) bio-based plastics and their biodegradability (the abbreviations used will be explained in Chapter 2)........................ 10 Figure 2-1. A section of the amylose molecule showing the repeating anhydroglucose unit

............................................................................................................................... 25 Figure 2-2 A section of the amylopectin molecule showing the two different types of chain linkages ................................................................................................................... 25 Figure 2-3 Starch plastic production technologies ..................................................... 29 Figure 2-4 A scheme for synthesizing reactive starch blends (Kalambur & Rizvi, 2006) ................................................................................................................... 33 Figure 2-5 The structure of cellulose.......................................................................... 43

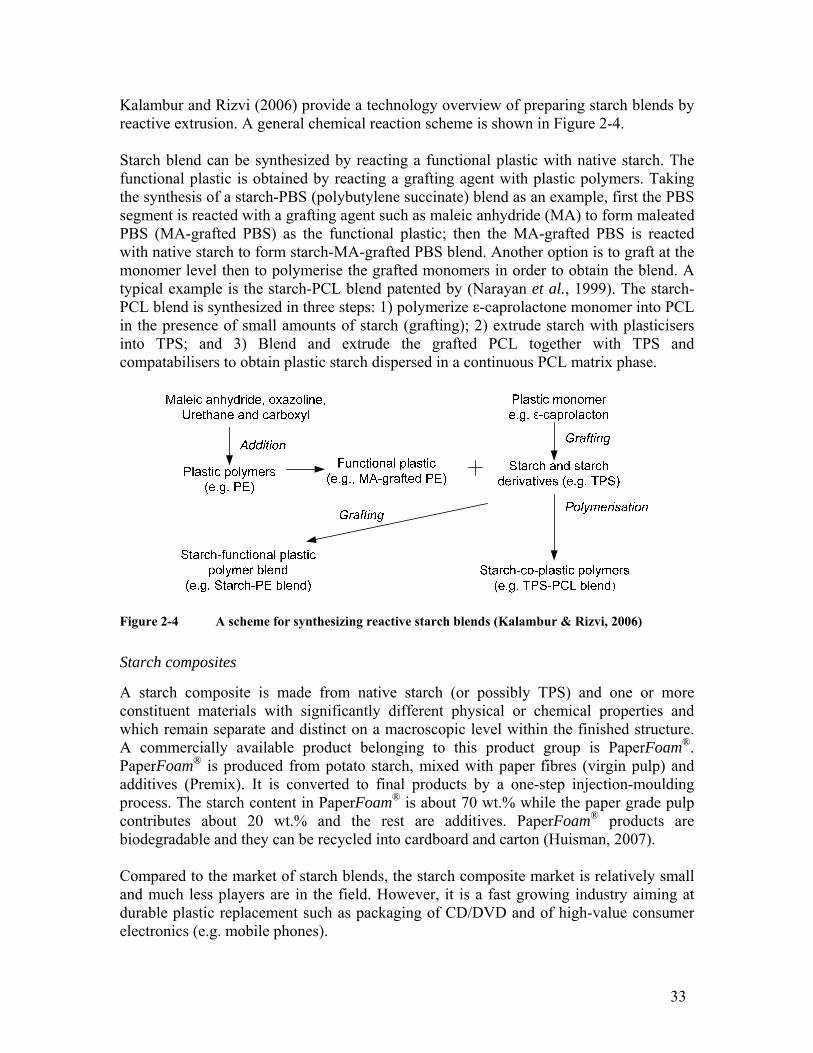

x

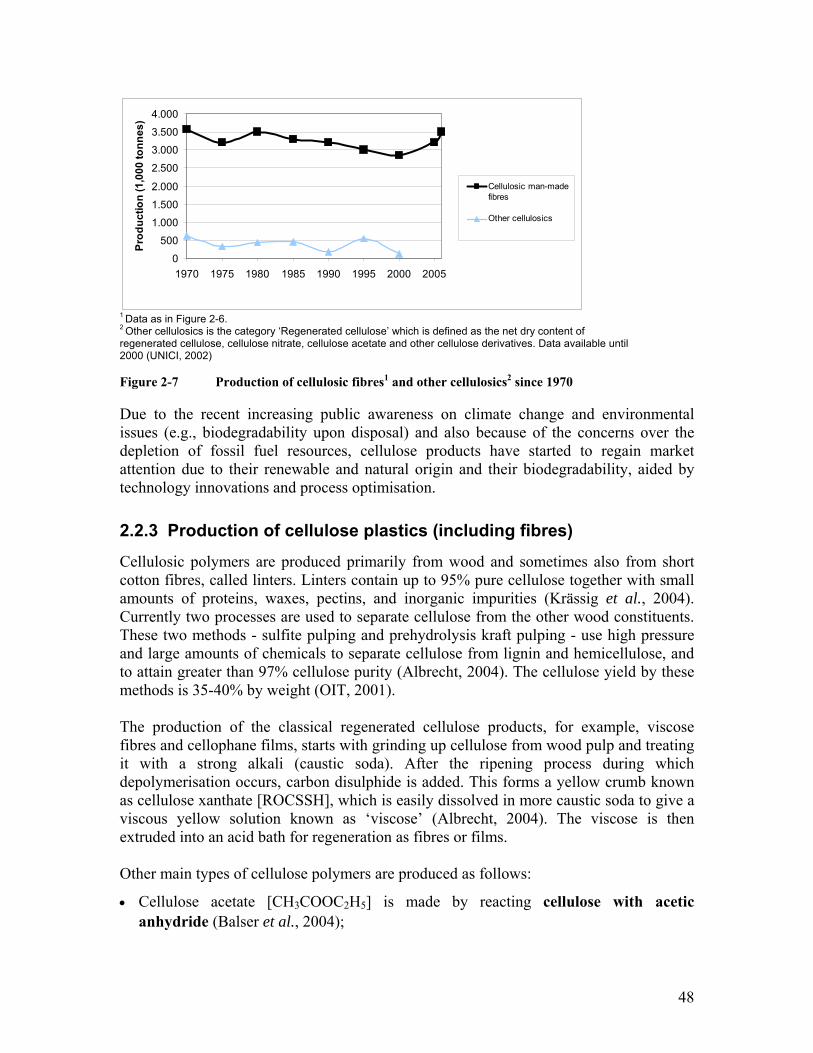

Figure 2-6 World fibre production 1920-2006 (Albrecht, 2004, Bachinger, 2006, EFS, 2006, IVE, 2007, USDA, 2006)........................................................................................ 46 Figure 2-7 Production of cellulosic fibres1 and other cellulosics2 since 1970 ........... 48 Figure 2-8 The Viscose process and the Lyocell process (Abu-Rous & Schuster, 2006) ................................................................................................................... 50 Figure 2-9 PLA molecule ........................................................................................... 57 Figure 2-10 Production of PLA from biomass ............................................................. 60 Figure 2-11 Stereocomplexation between PLLA and PDLA: enantiomeric PLA-based polymer blends (Tsuji, 2005), reprinted with permissions by Dr. Tsuji and Wiley-VCH Verlag GmbH & Co. KGaA.............................................................................................. 61 Figure 2-12 Crystal structure of PLA stereocomplex (Tsuji, 2005), reprinted with permissions by Dr. Tsuji and Wiley-VCH Verlag GmbH & Co. KGaA.......................... 61 Figure 2-13 PLA family: copolymers of D- and L- lactic units (with courtesy to PURAC) (PURAC, 2008b).............................................................................................. 63 Figure 2-14 Polytrimethylene terephthalate (PTT) molecule....................................... 75 Figure 2-15 Fermentation route to PDO....................................................................... 76 Figure 2-16 Conversion of glycerol to propylene glycols via the thermo-chemical route according to Chamiand et al. (2004) ....................................................................... 77 Figure 2-17 Production of PTT from PDO and PTA or DMT ..................................... 78 Figure 2-18 Production of x-aminoundecanoic acid from castor oil (Ogunniyi, 2006) (reprint with permission from Elsevier)............................................................................ 87 Figure 2-19 Production of sebacic acid from castor oil (Ogunniyi, 2006) (reprint with permission from Elsevier)................................................................................................. 88 Figure 2-20 Conventional route to adipic acid (Heine, 2000) ...................................... 88 Figure 2-21 Biotechnological production of adipic acid (Heine, 2000)....................... 89 Figure 2-22 Nylon 66 from adipic acid and diamine: conventional step polymerization by means of the carbonyl addition/elimination reaction................................................... 89 Figure 2-23 Production of azelaic acid and conventional step polymerization to PA69 (standard route incorporating the renewable feedstock oleic acid) (Höfer et al., 1997, Zahardis & Petrucci, 2007) ............................................................................................... 90 Figure 2-24 Biotechnological production of caprolactam and PA6 via conventional ring opening polymerisation (Nossin & Bruggink, 2002) ................................................ 91 Figure 2-25 PHA molecule........................................................................................... 97 Figure 2-26 Processing technologies for medium chain length PHA copolymers by composition and molecular weight (Anonymous, not dated) ......................................... 106 Figure 2-27 Building block of polyethylene (PE) ..................................................... 113 Figure 2-28 Schematic overview of the production of bio-based PE........................ 114 Figure 2-29 Polyolefin (PE, PP) demand in Western Europe 2006 (PlasticsEurope, 2007) ................................................................................................................. 116 Figure 2-30 Building block of polyvinyl chloride ethylene PVC molecule.............. 119 Figure 2-31 Production of PVC................................................................................. 120 Figure 2-32 PBT molecule.......................................................................................... 128 Figure 2-33 Applications of PBT in Europe 2006 (Eipper, 2007) ............................ 130 Figure 2-34 PBS molecule.......................................................................................... 132 Figure 2-35 PET molecule......................................................................................... 135 Figure 2-36 Use of PET applications in Western Europe (Glenz, 2004) .................. 137

xi

Figure 2-37 PUR production from a polyol and an isocyanate (Cottontail, 2007) (picture published under GNU Free Documentation License) ....................................... 142 Figure 2-38 Common plant oils (polyols and polyol precursors) (Clark, 2001) ........ 144 Figure 2-39 Epoxidation and ring opening of plant oil to obtain a polyol (Clark, 2001). ................................................................................................................. 145 Figure 2-40 Transesterification of castor oil with glycerine to produce a mixture of polyols with higher functionality (Vilar, 2002) .............................................................. 146 Figure 2-41 Application of PUR by market sectors in 2003, worldwide PUR consumption 10 Mt (Bertram, 2004) .............................................................................. 148 Figure 2-42 Soybean-based polyols and intermediate prices 2000 – December 2005, North America Market (Martin, 2006) ........................................................................... 153 Figure 2-43 Conversion of glycerol into epichlorohydrin according to the Solvay EpicerolTM process .......................................................................................................... 158 Figure 2-44 Production of DGEBA from epichlorohydrin and bisphenol A ............. 158 Figure 3-1 Capacity of emerging bio-based plastics by regions, 2003 and 2007 164 Figure 3-2 Development stage of main emerging bio-based material types ............ 166 Figure 3-3 Plastics consumption by end use application in Europe for 2007 (Simon & Schnieders, 2009) (courtesy PlasticsEurope).................................................................. 167 Figure 3-4 Use of benzene, toluene and xylene (BTX) for the production of plastics (estimated based on Weiss et al., (2007) and Patel et al., (1999)) .................................. 172 Figure 3-5 Highly selective depolymerization of lignin to products that preserve the lignin monomer structure (Bozell et al., 2007), reprinted with permission from PNNL 172 Figure 3-6 Production of 2,5-furan dicarboxylic acid (FDCA) from fructose via HMF ................................................................................................................. 173 Figure 3-7 World-wide capacity of bio-based plastics until 2020 based on company announcements (the most recent data used for making this graph were received in March 2009; the reported values refer to the capacities at the end of each year) ...................... 178 Figure 3-8 Breakdown of worldwide capacity of bio-based plastics by region in 2020 according to company announcements (the most recent data used for making this graph were received in March 2009) ........................................................................................ 180 Figure 3-9 Comparing the world-wide projections with the market potential, based on the maximum technical substitution potentials............................................................... 181 Figure 3-10 Projection of the worldwide production capacity of bio-based plastics until 2020 ................................................................................................................. 187 Figure 3-11 European capacity development of bio-based plastics until 2020 according to company announcements............................................................................................ 188 Figure 3-12 Projection of the European production capacity of bio-based plastics until 2020 ................................................................................................................. 189

List of Tables

Table 2-1 Overview of currently most important groups and types of bio-based plastics........................................................................................................................................... 14

xii

Table 2-2 Current and potential large volume producers of bio-based, or potentially bio-based and/or biodegradable plastics (1/8)......................................................................... 16 Table 2-3 Overview of starch use for food and non-food purposes in Europe in 2007... 26 Table 2-4 Properties and uses of various chemical modified corn starch (Daniel et al., 2000) ................................................................................................................................. 30 Table 2-5 Common NON-bio-based and biodegradable co-polymers used in starch blends........................................................................................................................................... 32 Table 2-6 Biodegradability and bio-content of starch blends........................................... 32 Table 2-7 Properties of selected starch plastics ............................................................... 35 Table 2-8 Technical substitution potential for starch plastics (the table below gives the views of the companies questioned) ................................................................................. 36 Table 2-9 Main applications for starch blends – share of interviewed company’s total production by market sector (scope: EU27+CH+NORD+EU candidate countries) ........ 38 Table 2-10 Major producers of starch plastics, products, trade names and capacities ..... 39 Table 2-11 Major fields of application in which the individual product groups of cellulose ethers are used (Thielking & Schmidt, 2006).................................................... 45 Table 2-12 Fibre designation according to ISO/TC 38.................................................... 50 Table 2-13 Mechanical, thermal and water retention properties of selected staple fibres 52 Table 2-14 Mechanical, thermal, and permeability properties of selected films (Schmitz & Janocha, 2002) .............................................................................................................. 53 Table 2-15 Major producers of man-made cellulose fibres, cellulose acetate and other cellulose esters .................................................................................................................. 55 Table 2-16 Properties of NatureWorks® PLA polymers (NatureWorks LLC, 2008c) .... 62 Table 2-17 Thermal properties of amorphous versus crystalline and stereocomplex PLA (with courtesy to PURAC (2008b) ................................................................................... 65 Table 2-18 Technical substitution potential for PLA according to interviews with experts from NatureWorks and PURAC. ...................................................................................... 68 Table 2-19 Main applications for PLA – share of interviewed companies, total production by market sector.............................................................................................. 69 Table 2-20 Properties of polymers from potentially bio-based monomers and selected other polymers used in engineering thermoplastics, films and fibre applications............ 80 Table 2-21 Comparison of vapour transmission rates of films made from PTT, PET, Nylon 6 and PTN (Hwo et al., 1998)................................................................................ 81 Table 2-22 Technical substitution potential for PTT........................................................ 81 Table 2-23 Feedstocks costs for PTT production from PTA and PDO ........................... 83 Table 2-24 Commercially available bio-based polyamides and potential bio-based polyamides ........................................................................................................................ 86 Table 2-25 Material properties of unmodified nylon polymers a..................................... 92 Table 2-26 Main applications for polyamides by market sector - Europe 2006.............. 93 Table 2-27 Major producers of polyamides, trade names and installed capacities in Western Europe in 2007.................................................................................................... 94 Table 2-28 Structures of Polyhydroxyalkanoates (PHAs)................................................ 98 Table 2-29 Commercially interesting PHAs and recent commercialisation development........................................................................................................................................... 99 Table 2-30 Comparing PHA polymers with common plastics in properties (Sudesh et al., 2000) ............................................................................................................................... 102

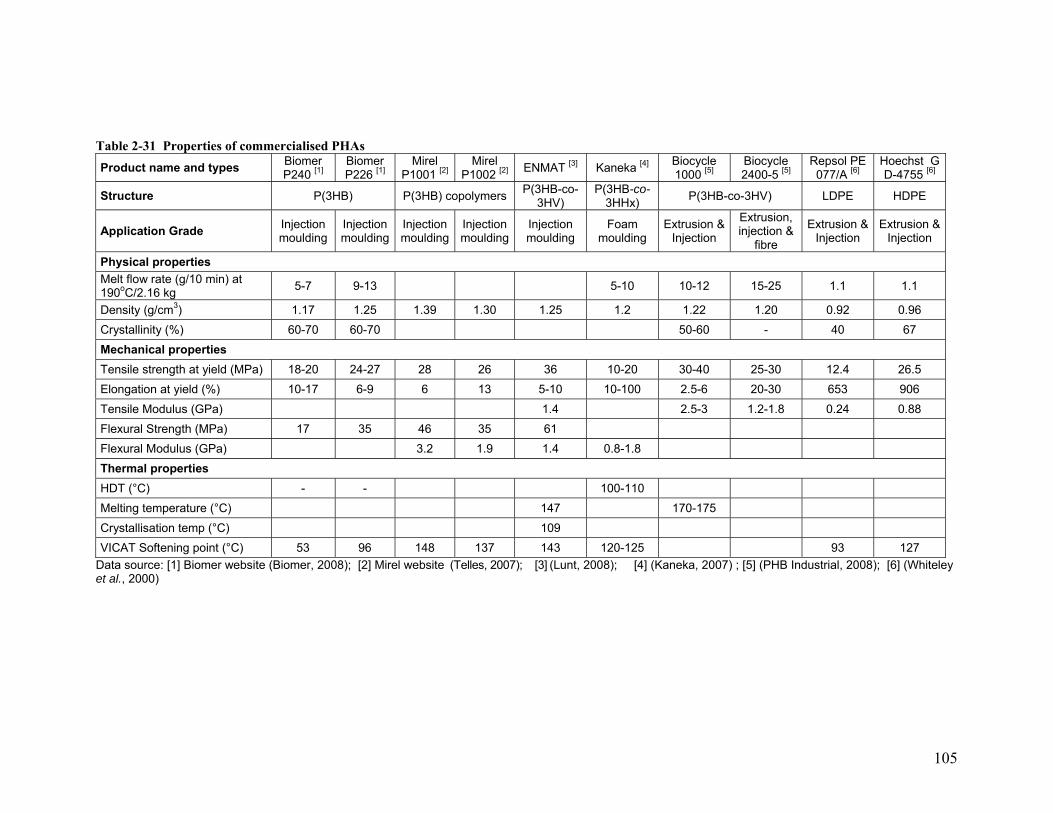

xiii

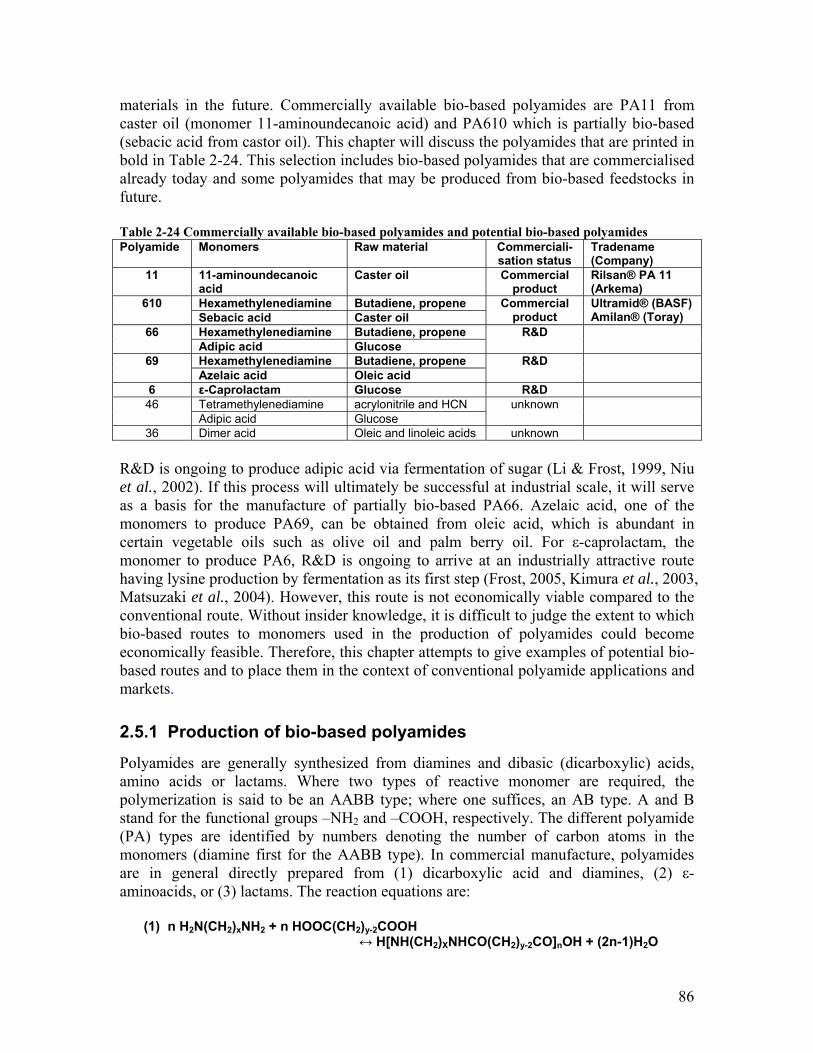

Table 2-31 Properties of commercialised PHAs............................................................ 105 Table 2-32 Technical substitution potential for PHAs according to interviews with experts from Telles and Kaneka. .................................................................................... 107 Table 2-33 Application of PHAs today and tomorrow (Kaneka, 2008, Telles, 2008) .. 108 Table 2-34 Producers of PHAs, current and future capacities........................................ 109 Table 2-35 Properties of petrochemical HDPE, LDPE, and LLDPE ............................. 115 Table 2-36 Main applications for LDPE/LLDPE and HDPE, total demand by market sector in Germany (Consultic, 2004) .............................................................................. 116 Table 2-37 Typical properties of rigid petrochemical PVC (Allsopp & Vianello, 2000)......................................................................................................................................... 121 Table 2-38 Typical properties of flexible petrochemical PVC (Allsopp & Vianello, 2000)......................................................................................................................................... 121 Table 2-39 Main applications for PVC (Plinke et al., 2000) .......................................... 122 Table 2-40 PVC production for construction industry in Western Europe 1999 (ECVM, 2001) ............................................................................................................................... 122 Table 2-41 Polyesters from bio-based or potential bio-based monomer (polymers which will be discussed in more detail in the text below are printed in bold letters)................ 126 Table 2-42 Major producers of PBT (Eipper, 2007)...................................................... 131 Table 2-43 Main applications for PBS and PBSA – share of interviewed company’s1 total production by market sector (scope: global)2 ......................................................... 133 Table 2-44 Properties of petrochemical PET standard grade ........................................ 136 Table 2-45 Share of PET production by market sector in Germany, excluding PET fibre production (Consultic, 2004) .......................................................................................... 136 Table 2-46 Renewable content of commercial available bio-based polyols and PURs 141 Table 2-47 World consumption of polyols and isocyanates for PUR production, in thousands of tonnes per year (Vilar, 2002)1.................................................................... 142 Table 2-48 Properties and uses of polyether polyols (Friederichs, 2005, Petrovic, 2008)......................................................................................................................................... 143 Table 2-49 Bio-based polyols for PUR production ....................................................... 144 Table 2-50 PUR formulations with a bio-based component and main applications 1,2,3,4,5

......................................................................................................................................... 148 Table 2-51 Raw material, trade names and major producers of bio-based polyols and PUR................................................................................................................................. 149 Table 2-52 Overview of the most important thermosets made from petrochemical feedstock ......................................................................................................................... 155 Table 3-1 Technical substitution potential of bio-based polymers (plastics) in Western

Europe (plastic applications excluding fibres and non-plastics)......................... 168 Table 3-2 Technical substitution potential bio-based fibres in Western Europe (without natural bio-based fibres such as cotton).......................................................................... 168 Table 3-3 Worldwide technical substitution potential of bio-based polymers (plastics) (plastic applications including thermoplastics and thermosets, excluding fibres).......... 169 Table 3-4 Worldwide technical substitution potential of bio-based man-made fibres in the world (both staple fibres and filament)........................................................................... 170 Table 3-5 World-wide shares of bio-based plastics by types and major players in 2020 according to company announcements ........................................................................... 179

xiv

Table 3-6 Categorization of bio-based plastics into the categories ”Biodegradable” and “Nondegradable” (based on a simple 60:40 assumption for starch plastics, see text), according to company announcements, worldwide 2020................................................ 180 Table 3-7 Influencing factors and expected growth in the three scenarios for bio-based plastics until 2020 ........................................................................................................... 185 Table 3-8 World-wide production capacity of bio-based plastics until 2020 – comparison of old and new projections.............................................................................................. 187 Table 3-9 Shares of bio-based plastics by types in Europe 2020 based on company announcements................................................................................................................ 188 Table 3-10 European production capacity of bio-based plastics until 2020 – comparison of old and new projections.............................................................................................. 189 Table 3-11 Total production of bio-based plastics in the scenarios “BAU”, LOW” AND “HIGH” in Europe .......................................................................................................... 191

1

1. Introduction

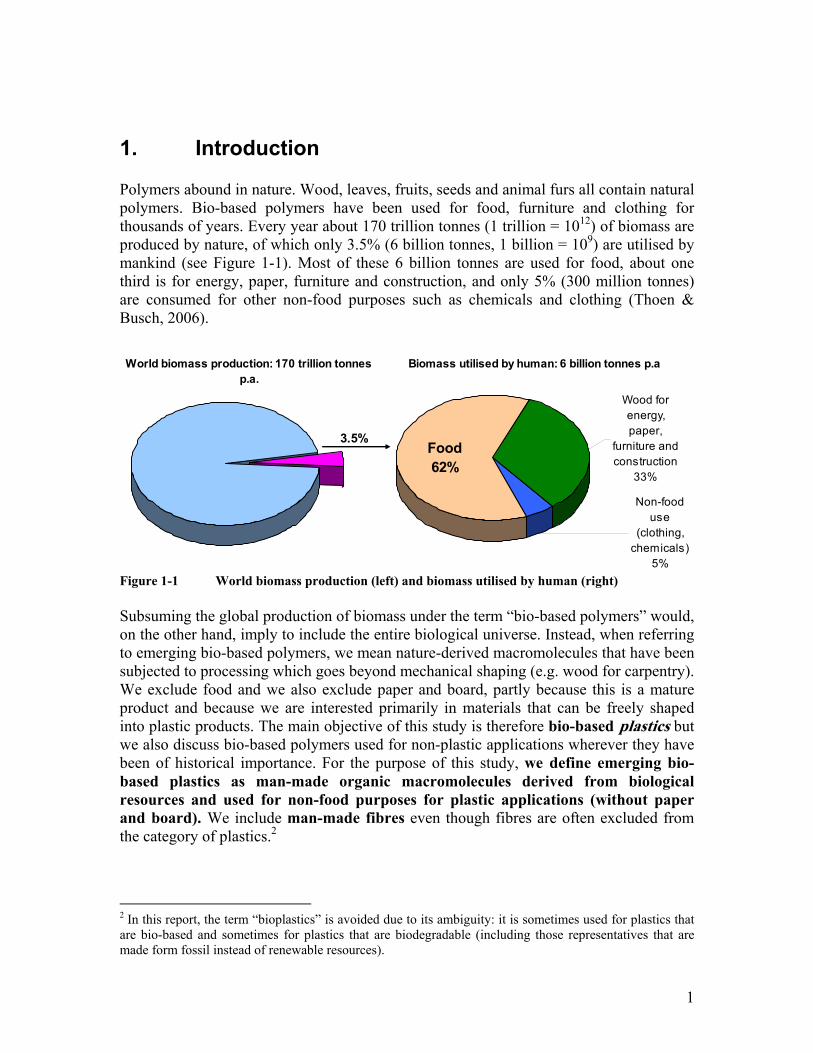

Polymers abound in nature. Wood, leaves, fruits, seeds and animal furs all contain natural polymers. Bio-based polymers have been used for food, furniture and clothing for thousands of years. Every year about 170 trillion tonnes (1 trillion = 1012) of biomass are produced by nature, of which only 3.5% (6 billion tonnes, 1 billion = 109) are utilised by mankind (see Figure 1-1). Most of these 6 billion tonnes are used for food, about one third is for energy, paper, furniture and construction, and only 5% (300 million tonnes) are consumed for other non-food purposes such as chemicals and clothing (Thoen & Busch, 2006).

World biomass production: 170 trillion tonnes p.a.

Biomass utilised by human: 6 billion tonnes p.a

Wood for energy, paper,

furniture and construction

33%

Non-food use

(clothing, chemicals)

5%

Food62%

3.5%

Figure 1-1 World biomass production (left) and biomass utilised by human (right) Subsuming the global production of biomass under the term “bio-based polymers” would, on the other hand, imply to include the entire biological universe. Instead, when referring to emerging bio-based polymers, we mean nature-derived macromolecules that have been subjected to processing which goes beyond mechanical shaping (e.g. wood for carpentry). We exclude food and we also exclude paper and board, partly because this is a mature product and because we are interested primarily in materials that can be freely shaped into plastic products. The main objective of this study is therefore bio-based plastics but we also discuss bio-based polymers used for non-plastic applications wherever they have been of historical importance. For the purpose of this study, we define emerging bio-based plastics as man-made organic macromolecules derived from biological resources and used for non-food purposes for plastic applications (without paper and board). We include man-made fibres even though fibres are often excluded from the category of plastics.2

2 In this report, the term “bioplastics” is avoided due to its ambiguity: it is sometimes used for plastics that are bio-based and sometimes for plastics that are biodegradable (including those representatives that are made form fossil instead of renewable resources).

2

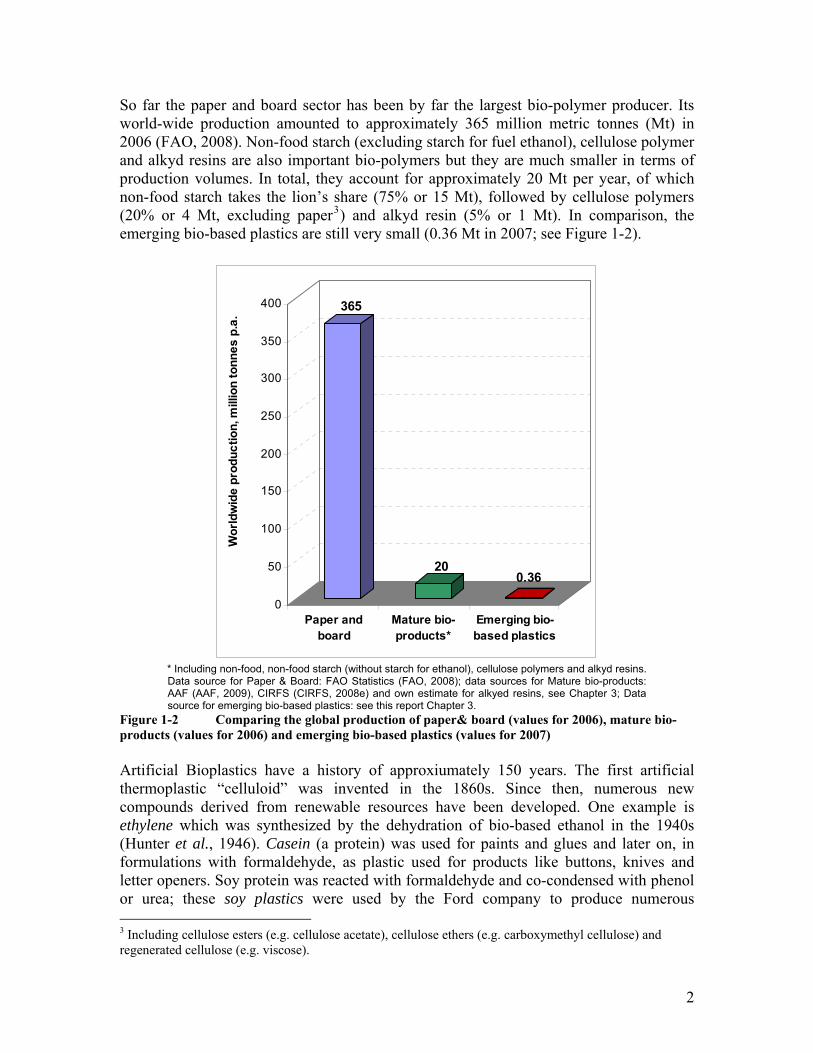

So far the paper and board sector has been by far the largest bio-polymer producer. Its world-wide production amounted to approximately 365 million metric tonnes (Mt) in 2006 (FAO, 2008). Non-food starch (excluding starch for fuel ethanol), cellulose polymer and alkyd resins are also important bio-polymers but they are much smaller in terms of production volumes. In total, they account for approximately 20 Mt per year, of which non-food starch takes the lion’s share (75% or 15 Mt), followed by cellulose polymers (20% or 4 Mt, excluding paper3) and alkyd resin (5% or 1 Mt). In comparison, the emerging bio-based plastics are still very small (0.36 Mt in 2007; see Figure 1-2).

365

200.36

0

50

100

150

200

250

300

350

400

Paper andboard

Mature bio-products*

Emerging bio-based plastics

Wo

rld

wid

e p

rod

uc

tio

n, m

illio

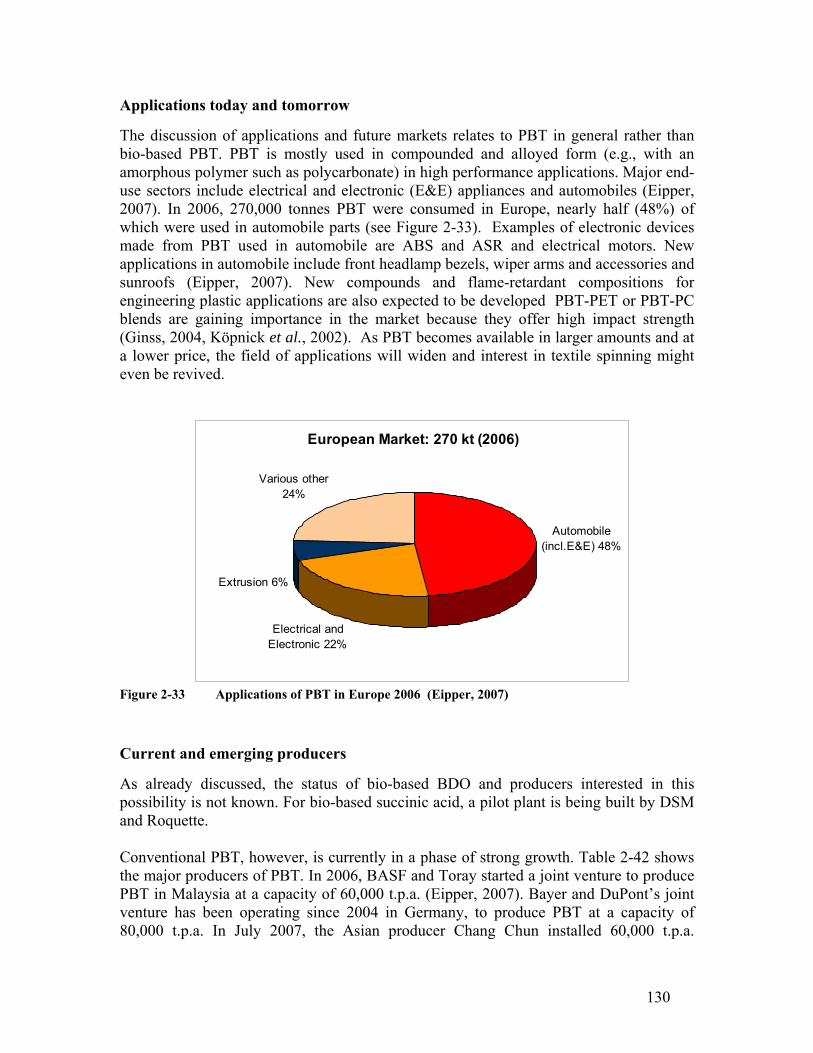

n t

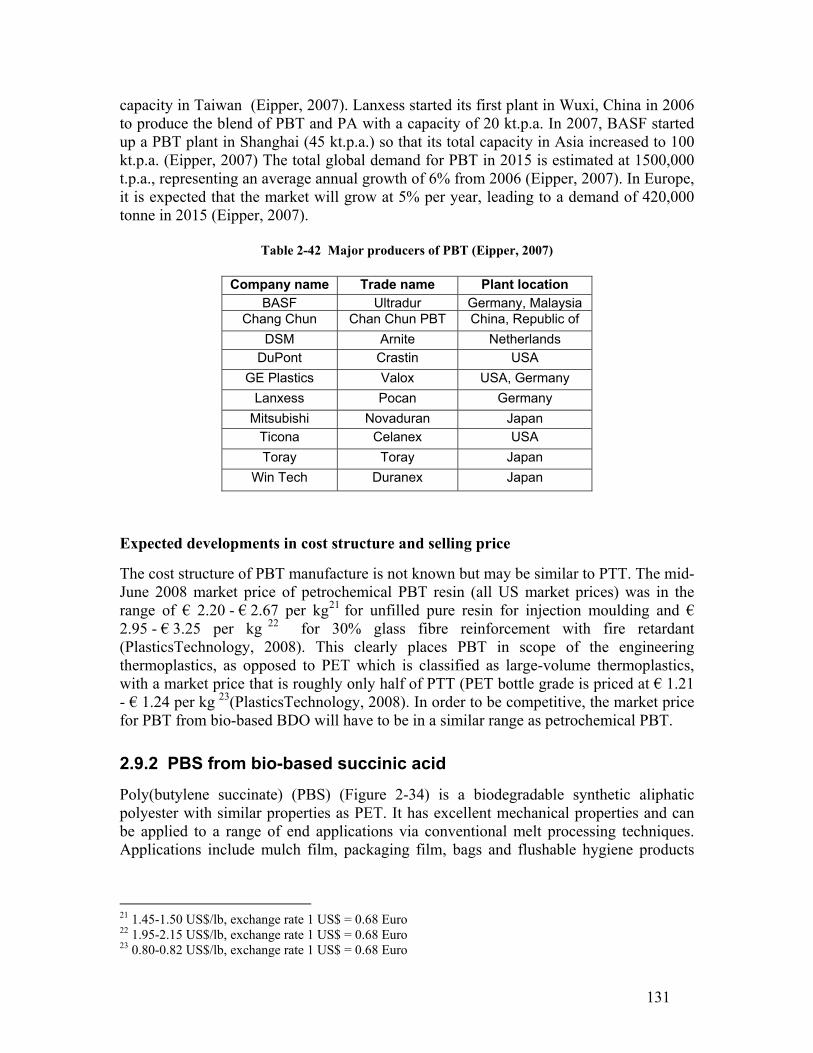

on

ne

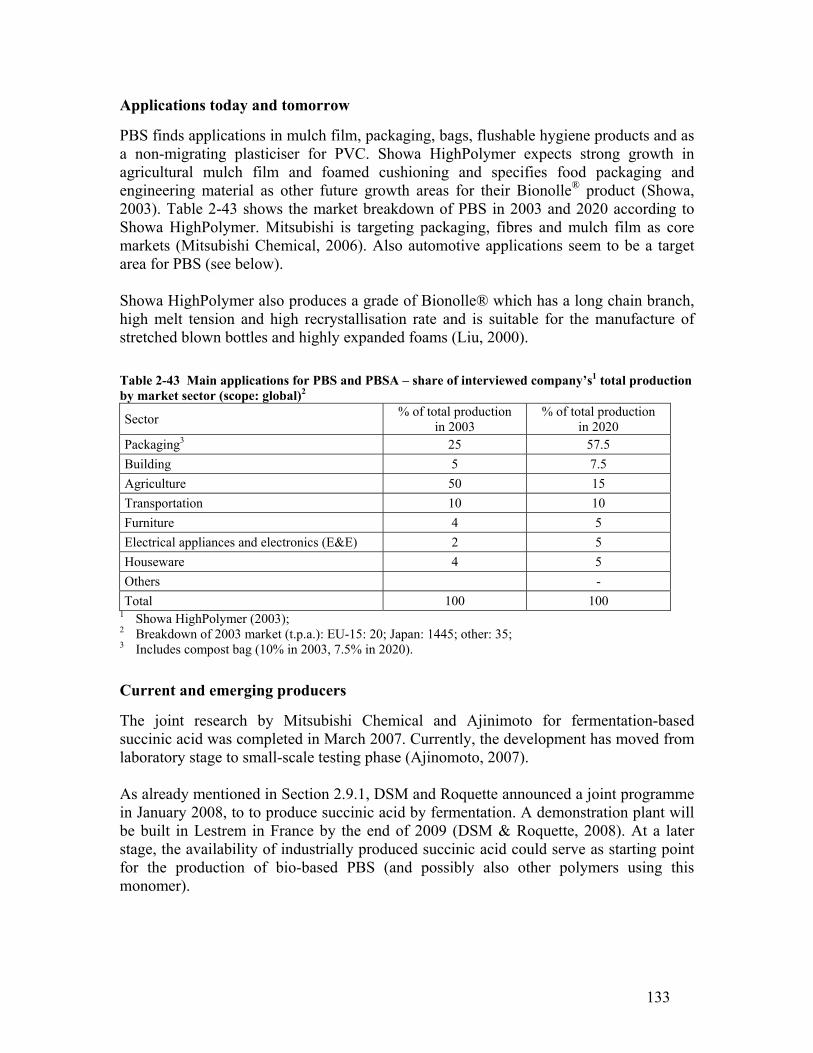

s p

.a.

* Including non-food, non-food starch (without starch for ethanol), cellulose polymers and alkyd resins. Data source for Paper & Board: FAO Statistics (FAO, 2008); data sources for Mature bio-products: AAF (AAF, 2009), CIRFS (CIRFS, 2008e) and own estimate for alkyed resins, see Chapter 3; Data source for emerging bio-based plastics: see this report Chapter 3.

Figure 1-2 Comparing the global production of paper& board (values for 2006), mature bio-products (values for 2006) and emerging bio-based plastics (values for 2007) Artificial Bioplastics have a history of approxiumately 150 years. The first artificial thermoplastic “celluloid” was invented in the 1860s. Since then, numerous new compounds derived from renewable resources have been developed. One example is ethylene which was synthesized by the dehydration of bio-based ethanol in the 1940s (Hunter et al., 1946). Casein (a protein) was used for paints and glues and later on, in formulations with formaldehyde, as plastic used for products like buttons, knives and letter openers. Soy protein was reacted with formaldehyde and co-condensed with phenol or urea; these soy plastics were used by the Ford company to produce numerous 3 Including cellulose esters (e.g. cellulose acetate), cellulose ethers (e.g. carboxymethyl cellulose) and regenerated cellulose (e.g. viscose).

3

automotive parts such as steering wheels, glove-box doors and interior trim (Stevens, 2002). Shellac is produced by extraction of the natural polymer excreted by the shell louse (Coccus lacca or Laccifer lacca) and was used for paints and varnish next to small solid articles (Fiebach & Grimm, 2000, 2002). Also regenerated cellulose, e.g. in the form of cellophane film and man-made cellulose fibres, were developed in those times and have been used in a wide range of applications, for example apparel, food (e.g. for sausages) and non-plastics (e.g. varnishes) (see also Chapter 2). However, many of these inventions in the 1930s and 1940s stayed in laboratory and were never used for commercial production. The main reason was the discovery of crude oil and its large-scale industrial use for synthetic polymers since the 1950s. Some products, e.g. man-made cellulose fibres, defended their position but did not succeed to grow at the rate of the newly emerging petrochemical products. Other products, especially non-plastics such as starch derivatives used as paper and textile auxiliaries, enjoyed a long period of growth and nowadays represent mature product areas. The oil price shocks of the 1970s led to renewed interest in the possibilities offered by non-petrochemical feedstock. However, this did little more than temporarily slow down the pace of growth in petrochemical polymers. Based on some first attempts in the 1980s, interest rose again in the 1990s4 and broad attention has been paid to bio-based chemistry in general and bio-based plastics in particular since the early 2000s. One of the main drivers especially in the 1990s was the goal to provide the market with plastics that are biodegradable, in order to solve the problem of rapidly increasingly amounts of waste and limited landfill capacities. While, in densely populated industrialized countries with limited landfill capacity, waste is nowadays primarily disposed off in municipal solid waste incineration (MSWI) plants, plastic waste management remains an issue especially in developing countries. Plastics are also increasingly polluting the sea, with the most prominent example being the so-called Great Pacific Garbage Patch in the central North Pacific Ocean (Day et al., 1988, Moore, 2003, Moore et al., 2001). There, plastic debris has been accumulating to an estimated size of 700 000 km2 to 15 million km2 resulting in large-scale marine pollution (La Canna, 2008, Moore et al., 2001). The fact that the area lies in international waters, makes the accumulation of plastic debris an urgent issue to be tackled on an international scale. Currently neither individual countries, community of states nor intergovernmental bodies are taking the initiative or responsibility to solve the problem (Didde, 2008). Biodegradable plastics can be manufactured not only from bio-based feedstock but also from petrochemical raw materials. But bio-based plastics, defined here as plastics that are fully or partially produced from renewable raw materials, have played a more important

4 Among the first attempts in the 1980s, simple products such as pure thermoplastic starch and starch/polyolefin blends were introduced. Due to the incomplete biodegradability of starch/polyolefin blends, these products had a negative impact on the public attitude towards biodegradable polymers and they damaged the image of the companies involved. It took many years to repair this damage, which was achieved largely by introduction and wide acceptance of more advanced copolymers consisting of thermoplastic starch and biodegradable petrochemical copolymers. This stage was reached in the 1990s.

4

role in the domain of biodegradable plastics. These developments have also been a stimulus for R&D on application areas where degradability is not a necessity (e.g. automotive applications of the biodegradable plastic polylactic acid, PLA) and on bio-based plastics which are not biodegradable (e.g. bio-based polyethylene). These bio-based durable plastics have gained much impetus in the last few years and are now one of the driving forces for the use of bio-based feedstock in plastics manufacture, next to the feature of biodegradability.

The plastics sector in perspective and its dynamics In order to understand better the size of the challenge of replacing petrochemical by bio-based plastics, we discuss first the dimension of the plastics industry in comparison with other bulk materials, the main types of polymers and the dynamics of plastics production to date. We refer here to the polymer industry in its current state, which is dominated by petrochemical polymers (see Chapter 3.1). Compared to other bulk materials, plastics are newcomers. They have been used in substantial quantities for only five to seven decades. In contrast, wood and clay have been used since the existence of mankind, glass for 5500 years, steel for 3500 years, paper for 1900 years, cement for 180 years and pure aluminium for 120 years. In high-income countries, plastics have overtaken aluminium and glass in terms of quantities used (mass) and now account for 6% of the total amount of bulk materials (see Figure 1-3).

Aluminum1%

Plastics6%

Paper & board11%

Cement25%

Bricks & Tiles21%

Crude steel22%

Glass4%

Wood10%

Figure 1-3 EU-27 production of bulk materials in 2004 (in brackets: values in EU-27 in 2004; 920 Mt in total) (See references in footnote to Figure 1-5) The fact that plastics are in a comparatively early stage of their product life cycle explains the particularly high growth rates of plastics production worldwide. For example, plastics production in EU-27 grew by 4.6% p.a. between 1971 and 2006, while the total production of all bulk materials increased by 0.7% p.a. between 1971 and 2004. The world-wide growth rate of plastics is even higher, amounting to 5.9% between 1971 and 2006. In 2006, the global annual production of plastics amounted to 245 Mt (PlasticsEurope, 2007) (see Figure 1-4).

(200 Mt)

(60 Mt)

(90 Mt) (9 Mt)

(190 Mt)

(240 Mt)

(100 Mt)

(30 Mt)

5

0

50,000

100,000

150,000

200,000

250,000

300,000

1950

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Year

Th

ou

san

d m

etri

c to

nn

es

World

Europe

Figure 1-4 World-wide and European production of plastics since 1950 in thousand metric tonnes (PlasticsEurope, 2007) As a consequence of the outstanding growth rates for plastics, their share in the overall material mix of industrialized countries has been increasing at the expense of the other bulk materials (see Figure 1-5). This is partly a result of new needs, which can best be fulfilled by plastics (e.g., safety devices such as airbags, mulch films for agriculture and certain medical devices and implants). But to a large extent the increased market share of plastics is caused by material substitution. For example, glass has been substituted for polymers in consumer goods such as computer screens, plastics have made inroads into the traditional applications of glass and paper/board in packaging and they have replaced metals in many components of consumer goods (e.g. cameras, car bumpers) and buildings (window frames and insulation materials).

6

0

50,000

100,000

150,000

200,000

250,000

300,000

1950

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

Year

Th

ou

san

d m

etri

c to

nn

es

Aluminum Bricks & Tiles Cement Crude steel Glass

Paper & board Plastics Wood

Figure 1-5 Share of bulk materials used in EU-27 in metric tonnes Data sources: Aluminium: RIVM (2008) for the years 1960-1990, EAA (2008) for the years 1980-2006, USGS for the years 1991-2006; Paper & Board: FAO (2008) for the years 1970-2006; Bricks & Tiles: UNSD (2004), (2008) for the years 1970-2005; Plastics: Simon (2008); Cement: (2004) for the years 1970-2000, USGS (2008) for the years 2001-2005; Wood: FAO (2008); Crude steel: IISI (2008) for the years 1970-2007; Glass: CPIV (2008) for the years 1980-2006.

Of all polymers, two thirds are thermoplastics in the narrow sense of the word (see Figure 1-6). This excludes synthetic fibres (13%), which are produced from thermoplastic polymers (polyester, polyamide, acrylics and others). Polyurethanes and elastomers are - depending on the subtype - either thermoplastics or thermosets. The group “Other” in Figure 1-6 represents primarily thermosets and accounts for 14%. An estimated share of 10% of all polymers are used as non-plastics (e.g. as adhesives, coatings and auxiliaries), while the vast majority are plastics (i.e. shaped products). Within the category of thermoplastics, polyolefins represent more than 50% (Figure 1-6). Together with PVC (18%) they account for approximately 70%. If PET (7%) and PS/EPS (8%) are added, the total represents approximately 85% of all thermoplastics (these percentages and the values in Figure 1-6 are world-wide data but the breakdown is essentially identical for Western Europe according to PlasticsEurope (2007).

7

Polyurethanes4%

Elastomers4%

Fibers13%

Others14%

Thermoplastics 65%

Figure 1-6 Worldwide production of synthetic polymers 2007 (Simon & Schnieders, 2009)

There are major discrepancies in the level of plastics use across the world. According to PlasticsEurope (Simon & Schnieders, 2009), there is still a factor of three between the world average per capita demand of plastics (30 kg/cap/a) and the current Western European level (99 kg/cap/a). The current difference between the demand levels in Western European and in Middle/East African countries (10 kg/cap/a) amounts even to a factor of 10. In other words, 15% of the world population (including Western Europe, the NAFTA countries and Japan) account for 50% of the global plastics consumption. Considering the size of this gap, one can expect a long trajectory of sustained growth of polymer production and demand in the developing world. If, for example, in the long term (e.g. by the year 2050) the average world-wide per capita polymer demand would reach 90 kg p.a. (which was approximately the average value of Western and Central Europe in the year 2000), the world-wide production would increase from approximately

8

250 Mt today to more than 850 Mt, i.e. by a factor of 3.5 (assuming a population by 2050 of 9.5 billion (U.S. Census Bureau, 2008)). Whether or not such a development will occur, will depend on many factors, among them world economic growth and the affordability and supply security of resources. For fossil fuels and feedstock, the affordability and supply security clearly depend on geopolitical developments, oil production and processing capacities, the demand in developing countries and depletion-related supply shortages. These factors are reflected in the price levels of crude oil and natural gas, which are likely to strongly influence the further development of fossil fuel-based polymers. Another potentially important determining factor for the future of the polymer industry is the further course of climate policy.

Bio-based plastics as new option In the last few years, increasing (apparent) coupling of the prices of fossil fuels and agricultural products has been observed. There are different views about whether this is primarily a consequence of the use of biomass for energy purposes (primarily biofuels) or whether other reasons are equally or even more important (Banse et al., 2008). Among the other reasons quoted are droughts, increased energy and fertilizer prices, declining global stocks due to changed policies, the increased demand from the developing world and speculation. Until recently, the OECD and other reputable organizations assigned a modest influence to biofuels (Legg, 2008). However, a World Bank report released in July 2008 draws the conclusion, that the large increase in biofuels production in the EU and the USA is indeed the most important reason for the rising food grain prices (World Bank, 2008). The report admits that the empirical evidence is scarce but it agues that there is prevailing consensus among market analysts according to whom speculation is of subordinate importance (which other authors had identified as important factor). At the same time, the World Bank report projects decreasing food prices from 2009 onwards. This seems to be the expected consequence of the proposed action list, which includes – among other measures – “action in the US and Europe to ease subsidies, mandates and tariffs on bio-fuels that are derived from maize and oilseeds” (World Bank, 2008). A cautious conclusion may be that the use of bio-based feedstock in the chemical industry is not a guarantee for safeguarding a high growth potential, also because policies aimed at safe and affordable food supply are likely to be given more importance. The chemical industry can probably nevertheless reduce its business risks by extending its resource base through the use of bio-based feedstock. This is supported by the fact that the prices of agricultural commodities have increased by far less than those of crude oil.

Today, public concern about the environment, climate change and limited fossil fuel resources are important drivers for governments, companies and scientists to find alternatives to crude oil. Bio-based plastics may offer important contributions by reducing the dependence on fossil fuels and the related environmental impacts.

9

As shown earlier in Figure 1-7, 85% to 90% of today’s total plastics are standard plastics. Bio-based plastics will therefore be able to substantially reduce the chemical industry’s environmental footprint only if bio-based plastics manage to conquer a meaningful share of standard plastics. Bio-based plastics have a higher product value than biofuels (e.g. ethanol) but their product value is lower than for special and fine chemicals and pharmaceuticals. Also the value added created by bulk bio-based plastics will take an intermediate position. While the replacement by conventional bulk plastics may be a long-term goal, plastics applied for higher value applications are nevertheless of interest today because they could pave the way for bio-based bulk products. Therefore all materials that have the potential to be applied in large quantities from a technical point of view will be included in this report. There are three principal ways to produce bio-based plastics, i.e. i) to make use of natural polymers which may be modified but remain intact to a large

extent (e.g. starch plastics); ii) to produce bio-based monomers by fermentation or conventional chemistry (e.g. C1

chemistry) and to polymerize these monomers in a second step (e.g. polylactic acid); iii) to produce bio-based polymers directly in microorganisms or in genetically modified

crops. As we will show in this report, the first way is by far the most important, followed by the second; we are not aware of any meaningful quantities being produced according to the third pathway. Developing a new plastic and introducing it to the market is a major challenge because the newcomers must compete with the existing petrochemical plastic, for which the production and use has been optimized for decades and which are well known in the entire supply chain. Considering also that all of today’s standard bulk plastics were introduced to the market 50 and more years ago, some experts have expressed doubts about whether new plastics would have any chances to succeed in the marketplace (Lemstra, 2005). Further aspects that have been put forward as counterarguments are the competition from plastics producers from the Middle East (especially from the Arabic peninsula) and China and the low margins in plastics production. Although these factors cannot be denied, the investments made and announced for new bio-based plastics indicate that they have a potential to be produced on large scale and to revolutionize the existing production methods in the chemical industry. In the last few years it has become increasingly clear that a very broad range of plastics can be produced fully or partially from biomass and that these plastics can be tailored to be fully or partially biodegradable (see Figure 1-8). As we will see in Chapter 2, these opportunities are increasingly being exploited by entrepreneurs. There is hence no doubt anymore that new bio-based plastics can be successfully commercialized. As a consequence, the focus of attention has shifted and the types of concern have gradually changed over time. Since analogies are seen with biofuel production, which is clearly ahead of bio-based plastics in terms of the quantities produced, the main issues are the distortion of food markets, the land use requirements (for food versus feed versus materials, including bio-based

10

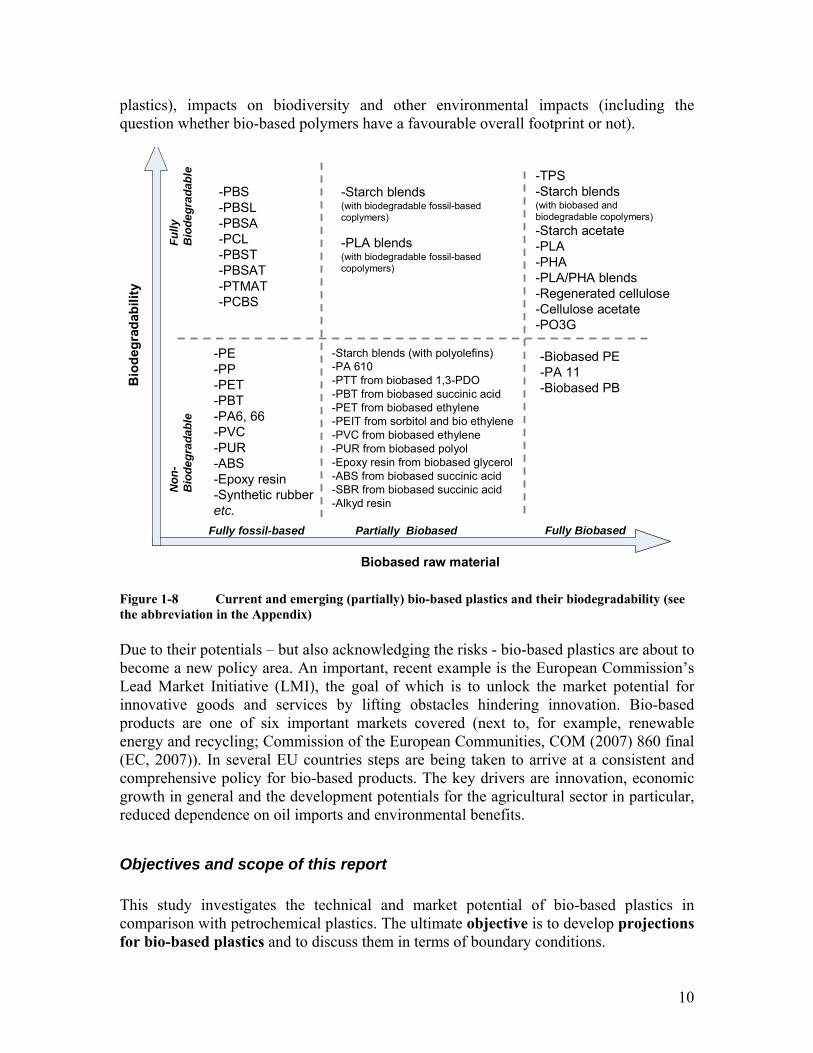

plastics), impacts on biodiversity and other environmental impacts (including the question whether bio-based polymers have a favourable overall footprint or not).

-Starch blends (with polyolefins)-PA 610-PTT from biobased 1,3-PDO-PBT from biobased succinic acid-PET from biobased ethylene-PEIT from sorbitol and bio ethylene-PVC from biobased ethylene-PUR from biobased polyol-Epoxy resin from biobased glycerol-ABS from biobased succinic acid-SBR from biobased succinic acid-Alkyd resin

Figure 1-8 Current and emerging (partially) bio-based plastics and their biodegradability (see the abbreviation in the Appendix) Due to their potentials – but also acknowledging the risks - bio-based plastics are about to become a new policy area. An important, recent example is the European Commission’s Lead Market Initiative (LMI), the goal of which is to unlock the market potential for innovative goods and services by lifting obstacles hindering innovation. Bio-based products are one of six important markets covered (next to, for example, renewable energy and recycling; Commission of the European Communities, COM (2007) 860 final (EC, 2007)). In several EU countries steps are being taken to arrive at a consistent and comprehensive policy for bio-based products. The key drivers are innovation, economic growth in general and the development potentials for the agricultural sector in particular, reduced dependence on oil imports and environmental benefits.

Objectives and scope of this report This study investigates the technical and market potential of bio-based plastics in comparison with petrochemical plastics. The ultimate objective is to develop projections for bio-based plastics and to discuss them in terms of boundary conditions.

11

The geographical scope of the study is, in first instance, Western Europe for the market projections. In addition, a global viewpoint will be taken in order to account for the global availability of technology and of many raw materials and in order to reflect global developments in production. The time horizon of this prospective study is the year 2020. The base years chosen for the analysis are 2003, 2007, 2013 and 2020. Relevant historical developments are studied both for bio-based and for petrochemical polymers. With regard to the type of products and their production the scope of this study can be further specified as follows:

The focus is on bio-based plastics and not on biodegradable plastics. Bio-based plastics can be, but are not necessarily, biodegradable. For example, starch plastics are generally biodegradable while bio-based polyethylene is not biodegradable. Moreover, several petrochemical (co-)polymers exist that are biodegradable. Biodegradability is therefore not a selection criterion for inclusion in this study.

Neither is the share of biogenic carbon in the product a selection criterion. As a consequence, both plastics with a high share of embodied biogenous carbon (max. 100%) and plastics with a low share are taken into account. The rationale behind this decision is that high shares of embodied biogenous carbon may lead to relatively high plastics prices, leading to a limited market volume and therefore limited environmental benefits. In contrast, allowing plastics with a lower content of renewable carbon to enter the market without restriction could offer more cost-effective solutions (greater environmental benefits at lower cost).

The primary interest of this study is the replacement of bulk petrochemical plastics by bio-based plastics that can also be produced at large scale. Since upscaling of production technology and the development of the market takes time, we include also materials which will first serve higher value applications but could be used for bulk applications in the medium to long term.

Natural fibres and natural fibre composites are - in general excluded - since this report focuses on the bio-based polymers used as polymer matrix. Starch composites are included where starch is used as polymer matrix. It should, however, be noted that the industrial use of natural fibres is growing and that the available environmental assessments show low environmental impacts compared to their synthetic counterparts (Deimling et al., 2007, Patel, 2008). This indicates also very interesting possibilities for combining natural fibres with bio-based polymers. To acknowledge these developments, we briefly address them in Chapter 2.2 (see Box 2-1).

Natural rubber (caoutchouc) is excluded because the production capacities (plantations) are limited and cannot be easily extended. Moreover, natural rubber is used in specific applications (e.g. tyres for airplanes and trucks) due to its outstanding

12

quality compared to synthetic rubber. To our knowledge there is so far no bio-based production process which could replace natural rubber.

Regarding the three principal ways to produce bio-based plastics we limit ourselves in this report to i) the use of natural polymers which may be modified but remain intact to a large

extent (e.g., starch polymers), ii) the production of bio-based monomers by fermentation or conventional chemistry

(e.g., C1 chemistry), followed by polymerization. We exclude bio-based polymers that are directly produced in microorganisms or in genetically modified crops (third pathway) because the large-scale application of this pathway seems rather unlikely from today’s perspective.5

The key selection criteria for the bio-based plastics covered by this study are the proximity to or the realization of commercialization but also the potential market volume. This means that plastics and plastics precursors that have been discussed in literature as potential bulk products but for which there are no evident signs of “take-off” are generally not included in this study (e.g., levulinic acid). Exceptions are made for technically feasible plastics with potentially very large market volumes.

To summarise, the approach taken in this study obviously results in some limitations which need to be taken into account in the interpretation phase (see also section “Preliminary remarks” at the beginning of the report). However, the analyses presented in the following do allow us to gain understanding of the potential of bio-based plastics in comparison with petrochemical plastics and to derive some conclusions for policy makers.

Structure of the report Apart from the introductory chapter (Chapter 1) this report is divided into three chapters. The main purpose of Chapter 2 is to provide an overview of the main types of bio-based polymers with regard to their chemical composition, their production, properties, the technical substitution potential, application areas, current and emerging producers and the product prices. In total, eleven polymers or polymer groups were studied based on in-depth literature research (printed publications, internet) and expert interviews. The overall goal of Chapter 3 is to develop projections for the production of bio-based polymers until 2020. As the first step, the influencing factors and boundary conditions for the future production and use of bio-based polymers are identified and discussed (Section 3.1-3.5). On this basis market projections are presented in Section 3.6. Chapter 4 finally draws overall conclusions about the prospects of bio-based plastics.

5 To our knowledge, the third pathway is currently only relevant for polyhydroxyalkanoates (PHA). Although commercialisation efforts are underway for PHA, bulk volume applications appear to be still many years off.

13