SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED SMMT, the ‘S’ symbol and the ‘Driving the motor industry’ brandline are trademarks of SMMT Ltd Production Outlook and Economic Forecast Update Webinar Robert Baker, Chief Economist, SMMT Ian Henry, Director, AutoAnalysis John Leech, Partner, KPMG 26 September 2013

Transcript

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED SMMT, the ‘S’ symbol and the ‘Driving the motor

industry’ brandline are trademarks of SMMT Ltd

Production Outlook and Economic Forecast Update Webinar Robert Baker, Chief Economist, SMMT

Ian Henry, Director, AutoAnalysis

John Leech, Partner, KPMG

26 September 2013

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 2

• During presentations (14:00 – 14:30) everyone will be muted so that only

the presenters will be heard.

• The presentation will be followed by a Q&A session. Click on the hand

symbol to show that you have a question.

• If you are experiencing any technical problems please call 0207 344

1611 or 07793 773391

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 3

Robert Baker

SMMT

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 4

UK Economy & Automotive - key themes

• UK Economy on the move again – constraints on the domestic economy ease and policy pressed from all angles

• European economy stabilises after euroland’s immediate integrity (if not cohesion) is clarified by ECB

• UK automotive shows restructuring with growth (for cars) for other vehicle types market and sector trends are more varied; the pick-up in home demand may be well timed to extend the run on car sales and lift confidence for CVs

• Auto Europe’s refocusing is keyed-in; restructuring with growth reset in EC still a (competitive & capacity and confidence and credit) major challenge. May be a long-haul

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 5

UK Developments since Q2 2013 (1)

• UK GDP growth up, firm and stable over two quarters;

more growth expected, so confidence & durable recovery

hopes lifted too; consumers and construction quickest off

the mark

• UK new car sales volumes up substantially and stable near

2.2mn; more growth potential probable, so short - medium

term forecasts raised modestly and may go higher

• More varied trends CV markets, but volumes up from

recession lows; despite modest relapses of 2012 volumes

stable, yet trucks set for E5/E6 uncertainty and Green Bus

Fund underpinned (new AFV) bus demand

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 6

UK Developments since Q2 2013 (2):

• Europe’s new car and CV markets poised to stabilise; many economies weak & disjointed; long time to full recovery

• UK Automotive Sector Strategy for partnership growth unveiled. A very long term 20/30 year vision, but notable medium term spending commitments. And so too on Action on Roads and 2015/16’s Transport capital spend plans

• Bank’s new management gives reassurances on ultra loose money policies; but borrow responsibly and invest wisely. HMT’s beefs-up its communications on positive policies enabling private-led growth, while anchored to a path, if not exact timing & mix, of its 2010 fiscal consolidation plans

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 7

UK GDP growth slow at first then firmer ahead, by 2015

percen

tag

e c

han

ge -

sam

e q

uarte

r p

revio

us y

ear

UK GDP growth quarterly - cash & real - 2008 to 2013: 2013 to 2014F Forecasts Oxford Econ (Jul 13)

UK GDP, cash value at market prices

real GDP market prices

OE Fore - Jul 2013 (real)

OE Fore - Jul 2013 (cash)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 8

UK new car forecasts to 2014; (Jul 13) rolling years

SMMT - Forecast High - Projection Low - Projection

Forecast (Jul 2013)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 11

UK trucks recovered (E5/E6) trend ahead unclear rolling years

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

25

30

35

40

45

50

55 T

ho

usan

ds

UK Trucks 3.5T+ registrations - outlook to 2015/16P

Trucks =>3.5T: quarter growth S1 (right axis)

Trucks =>3.5T: quarter growth S2 (right axis)

Trucks=>3.5T: rolling year total S1 (left axis)

Trucks=>3.5T: rolling year total S2 (left axis)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 12

On Europe’s Growth Path and Prospects Source: Oxford Economics Jul/Aug 2013

Real GDP %

growth y/y

2004-2008

% pa

2009 2012 2013 2014 2014-2017

% pa

Germany 2.0 -5.1 0.9 0.4 1.6 1.6

France 1.8 -3.1 0.0 -0.1 0.7 1.2

Italy 1.1 -5.5 -2.4 -1.9 0.1 1.1

Spain 3.1 -3.7 -1.4 -1.5 0.4 1.2

Euro Area 2.1 -4.4 -0.5 -0.6 0.9 1.4

UK 2.4 -5.2 0.2 1.2 2.0 2.5

Russia

Turkey

4.0

5.0

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 13

On Europe’s New Car Registration Volumes Source: ACEA cars in millions

Region/states 2007 2009 2012 2013 : 12mth Aug

(as index 2007=100)

EC (27) 15.57 14.16 12.05 11.63 (75)

Euro Zone 11.62 11.11 8.94 8.41 (72)

UK 2.4 1.99 2.05 2.18 (91)

F/D/I/E/UK (5) 11.73 11.22 9.13 8.89 (76)

I/E/PT/GR/IE (5) 4.78 3.55 2.34 2.22 (46)

I & E 4.11 3.12 2.10 1.99 (48)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 14

On Europe’s CV Registration Volumes Source: ACEA all CVs in millions

Region/states 2007 2009 2012 2013 – 12mth Jun

(as index 2007=100)

EC (27) 2.58 1.59 1.78 1.71 (75)

Euro Zone 1.88 1.22 1.30 1.24 (72)

UK 0.39 0.22 0.28 0.29 (91)

F/D/I/NL/E/S/UK 1.97 1.27 1.45 1.4 (76)

I/E/PT/GR/IE 0.75 0.38 0.36 0.34 (46)

I & E 0.60 0.31 0.32 0.31 (52)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 15

On Europe’s trucks 16t+ registration volumes Source: ACEA all CVs in 000s

Region/states 2007 2009 2012 2013 – 12mth Jun

EC (27) 312 157 217 204 (65)

Euro Zone 226 118 150 139 (62)

UK *29 19 29 28 (96)

F/D/I/NL/E/S/UK 223 124 160 150 (67)

I/E/PT/GR/IE (5) 71 25 28 26 (37)

I & E 62 21 25 24 (38)

*: UK 2008=35.1

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 16

On Europe’s Vehicle Production Volumes Source: OICA e.o.e: vehicles in millions

Region/states 2007 2009 2012 2013 : 12mth Jun

(as index 2007=100)

EC (27) 19.72 15.25 16.23 15.86 (80)

Euro Zone 17.60 14.00 14.49 14.12 (80)

UK 1.75 1.09 1.58 1.58 (90)

D 6.21 5.21 5.65 5.64 (91)

I/E/PT (3) 4.35 3.09 2.81 2.87 (66)

Russia

Turkey

1.66

1.10

0.72

0.87

2.23

1.07

2.22 (133)

1.08 (98)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 17

UK economy & CV markets – concluding perspectives

On the UK economic outlook for 2013/14

• Real GDP growth up, outlook positive and supportive;

consistent if not steady; and to 2.5% y/y by 1H 2015

• Consumer inflation sticky, subdued for now near 2.5%

• Restructuring a long-haul; investment…to be continued

• Growth in real earnings and wages expected

On the new Car and CV sectors in 2013/14

• Stable UK TIVs; more growth possible near term

• Unsure on stable, steady and sustainable growth in EC

• Issues on capacity EC/UK; anchor relevance of 2007’s

level of new vehicle demand levels and shifting mix

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 18

Ian Henry

AutoAnalysis

Data prepared by Ian Henry

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 19

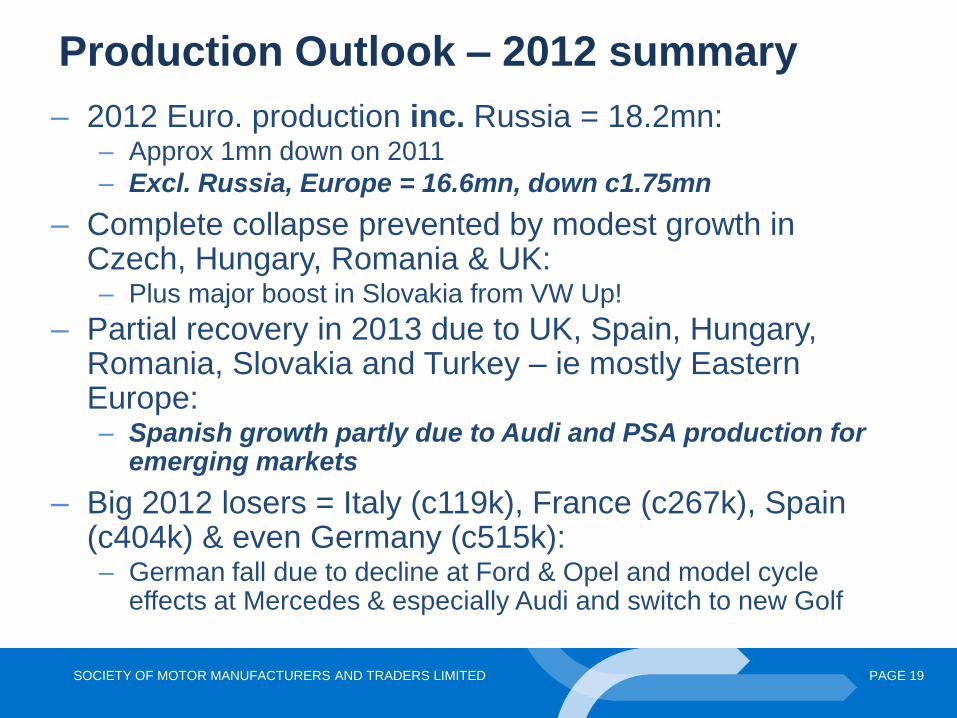

Production Outlook – 2012 summary

– 2012 Euro. production inc. Russia = 18.2mn: – Approx 1mn down on 2011

– Excl. Russia, Europe = 16.6mn, down c1.75mn

– Complete collapse prevented by modest growth in Czech, Hungary, Romania & UK: – Plus major boost in Slovakia from VW Up!

– Partial recovery in 2013 due to UK, Spain, Hungary, Romania, Slovakia and Turkey – ie mostly Eastern Europe: – Spanish growth partly due to Audi and PSA production for

emerging markets

– Big 2012 losers = Italy (c119k), France (c267k), Spain (c404k) & even Germany (c515k): – German fall due to decline at Ford & Opel and model cycle

effects at Mercedes & especially Audi and switch to new Golf

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 20

Production Outlook: “best case” recovery

highlights

– Germany will recover: – By 2018 it will back above 2007 level, but not quite at 2011’s somewhat

artificial peak

– Long-term losers … by 2018: – France could be c33%/962k down on 2007 – even allowing for

Renault’s renewed commitment to French production

– Italy down 28%/343k and Spain c17%/478k on 2007 – even allowing for Fiat’s reorganisation of production and Renault’s proposed

expansion in Spain and commitment of VW and PSA to Spain

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 23

Possible that situation could be much worse, if decline in European sales continues …

– The widening gap between Blue and Pink lines highlights the importance of Russian production to Europe’s total

– A further fall in 2013 would suggest that in the best case scenario (Yellow) in 2017-8 would be only slightly better than 2008 – and it raises issue of Europe not recovering to 2007 peak for some time, if at all

– Continued decline in 2014 will not only delay long-term recovery, but also risks market settling down at much reduced volumes: Europe needs to consider implications of scenarios 5 & 6

– If long run European production excl. Russia is c16.5mn upa or worse (as in scenario 6), we do not believe current industry structure is sustainable

European Production Excl. Russia - Worst Scenarios

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 24

Structural change at the volume VMs in response to falling sales & production volumes…

– EU27 car markets fell in 2012 to 17-year low; latest 2013 figures

from ACEA show further decline in most markets, dampening

cautious optimism at Frankfurt

– Volume VMs’ European production falling significantly:

– 2007-2012: Fiat, Ford, Opel/Vauxhall, PSA and Renault combined

lost c3mn units’ production

– During same period total European production fell by 2.12mn: main

winners = Dacia, Hyundai-Kia and Volkswagen/Audi, plus Nissan

and JLR

– New order for VMs in Europe beginning to emerge …

– Volume brands facing long-run, structural decline in Europe as

value brands and premium marques continue to grow:

– Having lost c0.5mn units each over past six years, can the

volume VMs really recover?

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 25

Restructuring – and refocusing – now under way …

– Faced with continued and rising losses, Ford, GM & PSA have

announced plant closures

– Fiat is reallocating production between Italian factories: – Slimming down, but not yet closing plants

– Will bring production back from Mexico to Poland

– Optimistically, planning to use European factories as global export bases, for Fiat,

Alfa and Jeep brands … including Serbian and Turkish plants

– Renault reached union agreement on cost cutting: – increasing commitment to French & Spanish production

– adding Nissan car production to European portfolio …

– and increasing production in Turkey and Morocco largely for European markets

– GM & PSA established a defensive alliance, covering logistics,

purchasing and new models: – benefits not yet fully apparent, new models will not appear before 2016-7

– Will further cuts be required if demand/production falls again?

Remains probable that Fiat & Renault will need to cut further

into fixed cost base … PSA, Ford & GM deny they will cut

further in Europe …

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 26

Key issue: doubtful if export markets can be Europe’s saviour?

• German/UK premium and luxury brands have recently been very dependent on US and Chinese demand for recent growth

• To date, these markets have held up

• But European brands’ production in NAFTA and China is increasing, which will reduce how much non-EU export demand can be supplied by European production, especially at the volume brands

– VW group, Fiat, PSA, BMW and Mercedes all increasing capacity outside Europe, esp. in NAFTA, Brazil & China; JLR will soon be producing in China

– VW increasing production in Mexico, Audi building new plant in Mexico; BMW widening US production portfolio and building plant in Brazil

– Some moves may actually harm struggling European production sites:

• How far will Renault/Dacia production in Morocco impact on European factories’ output?

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 27

In conclusion … • Sustained production recovery unlikely before 2014, quite probably real

increase will not occur until 2015 – When recovery does come, revival will almost certainly be shallower and slower than post

2008-9 collapse …

• Possible that long-run European production volumes, excluding Russia could be well below 2007-2008 peaks

– Implications of this have not yet been fully worked out by the industry and authorities ….

• European vehicle production was not financially robust even in boom years

– How much longer can major VMs support European operations if losses continue?

– Ford, GM and PSA have started cutting back their European operations …

– GM remains very committed to Opel/Vauxhall, while Renault is raising investment in France and Spain: but will these moves really be sustainable?

• We expect further re-structuring and capacity cutbacks will be required: but when?

– A major European name could disappear by the end of the decade, if not before – Rising strength of Koreans & Nissan, and enduring appeal of German & UK premium brands

should not be underestimated – Pressure on the volume brands will increase and will be impossible to ignore – All this is without considering the impact of the Chinese who are now appearing on Europe’s

fringe …

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 28

The independent report produced for SMMT has been prepared on the basis of judgments made by AutoAnalysis, taking into account the information, opinion and insight from a range of industry, press and analyst sources available at the time of compiling this report. The views and projections contained in this report are those of the author, Ian Henry of AutoAnalysis. They do not represent an official SMMT view.

The full analysis report, exec summary and interactive maps are available from the SMMT Member Services website now at

www.smmt.co.uk/members-lounge/member-services. The 6 full reports a year are free for SMMT members and available at

£4,371 for non-members. If you have any questions about the content of the report or to enquire about purchasing a full year

subscription or individual reports, please contact us at [email protected] or call 0207 344 9265.