36

Proposed acquisition of Lonmin 14 December 2017

Proposed

acquisition of

Lonmin

14 December 2017

www.sibanyestillwater.com

Forward looking StatementsThis Presentation contains forward-looking statements within the meaning of the “safe harbour” provisions of the United States

Private Securities Litigation Reform Act of 1995. These forward-looking statements, including, among others, those relating to

Sibanye Gold Limited trading as Sibanye-Stillwater (“Sibanye-Stillwater”)’s and Lonmin Plc (“Lonmin”)’s financial positions, business

strategies, plans and objectives of management for future operations, are necessarily estimates reflecting the best judgment of the

senior management and directors of Sibanye-Stillwater and Lonmin. All statements other than statements of historical facts

included in this Presentation may be forward-looking statements. Forward-looking statements also often use words such as

“anticipate”, “believe”, “intend”, “estimate”, “expect” and words of similar meaning. By their nature, forward-looking statements

involve risk and uncertainty because they relate to future events and circumstances and should be considered in light of various

important factors, including those set forth in this disclaimer. Readers are cautioned not to place undue reliance on such

statements. The important factors that could cause Sibanye-Stillwater’s and Lonmin’s actual results, performance or achievements

to differ materially from those in the forward-looking statements include, among others, economic, business, political and social

conditions in the United Kingdom, South Africa, Zimbabwe and elsewhere; changes in assumptions underlying Sibanye-Stillwater’s

and Lonmin’s estimation of their current mineral reserves and resources; the ability to achieve potential synergies from the Offer; the

ability to achieve anticipated efficiencies and other cost savings in connection with past and future acquisitions, as well as at

existing operations; the success of Sibanye-Stillwater’s and Lonmin’s business strategy, exploration and development activities; the

ability of Sibanye-Stillwater and Lonmin to comply with requirements that they operate in a sustainable manner; changes in the

market price of gold, PGMs and/or uranium; the occurrence of hazards associated with underground and surface gold, PGMs and

uranium mining; the occurrence of labour disruptions and industrial action; the availability, terms and deployment of capital or

credit; changes in relevant government regulations, particularly environmental, tax, health and safety regulations and new

legislation affecting water, mining, mineral rights and business ownership, including any interpretations thereof which may be

subject to dispute; the outcome and consequence of any potential or pending litigation or regulatory proceedings or other

environmental, health and safety issues; power disruptions, constraints and cost increases; supply chain shortages and increases in

the price of production inputs; fluctuations in exchange rates, currency devaluations, inflation and other macro-economic

monetary policies; the occurrence of temporary stoppages of mines for safety incidents and unplanned maintenance; their ability

to hire and retain senior management or sufficient technically skilled employees, as well as their ability to achieve sufficient

representation of historically disadvantaged South Africans’ in management positions; failure of information technology and

communications systems; the adequacy of insurance coverage; any social unrest, sickness or natural or man-made disaster at

informal settlements in the vicinity of some of Sibanye-Stillwater’s operations; and the impact of HIV, tuberculosis and other

contagious diseases. These forward-looking statements speak only as of the date of this Presentation. Sibanye-Stillwater and Lonmin

expressly disclaim any obligation or undertaking to update or revise any forward-looking statement (except to the extent legally

required).

Disclaimer

2

www.sibanyestillwater.com

1. Introduction

2. Transaction overview

3. Transaction rationale

a. Lonmin transaction rationale

b. Sibanye-Stillwater transaction rationale

4. Conclusion

5. Appendix

Contents

3

Introduction

4

www.sibanyestillwater.com

Transaction is aligned with our vision…

5Sibanye-Stillwater cares

SUPERIOR VALUE CREATION

FOR ALL OUR STAKEHOLDERS

Through mining our mult i -commodity

resources in a safe and healthy

environment

www.sibanyestillwater.com

6

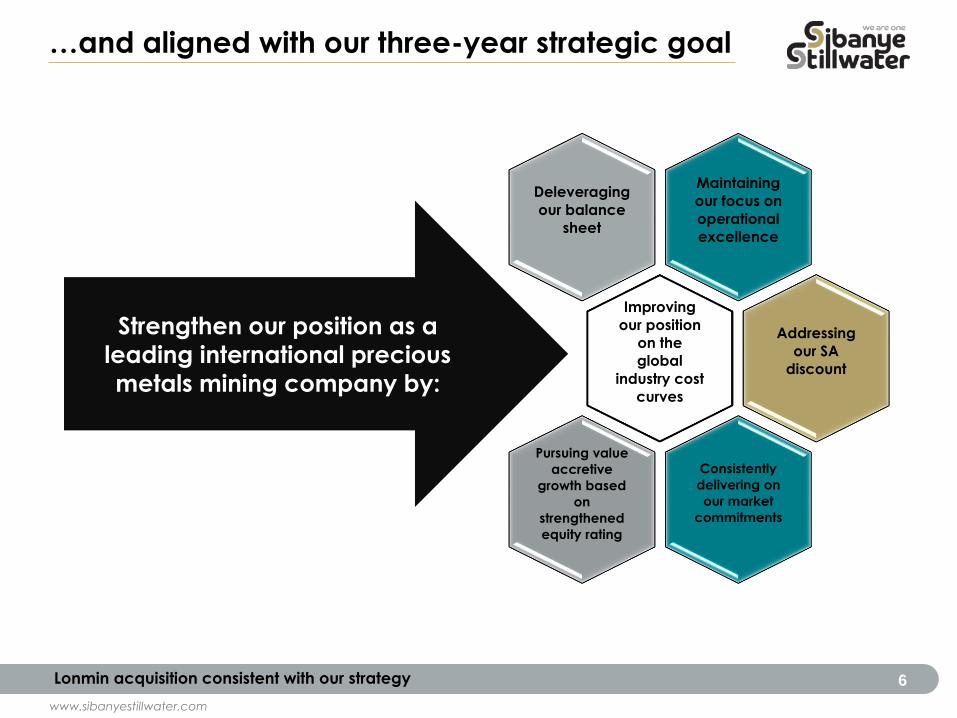

…and aligned with our three-year strategic goal

Lonmin acquisition consistent with our strategy

Maintaining

our focus on

operational

excellence

Deleveraging

our balance

sheet

Improving

our position

on the

global

industry cost

curves

Addressing

our SA

discount

Consistently

delivering on

our market

commitments

Pursuing value

accretive

growth based

on

strengthened

equity rating

Strengthen our position as a

leading international precious

metals mining company by:

www.sibanyestillwater.com

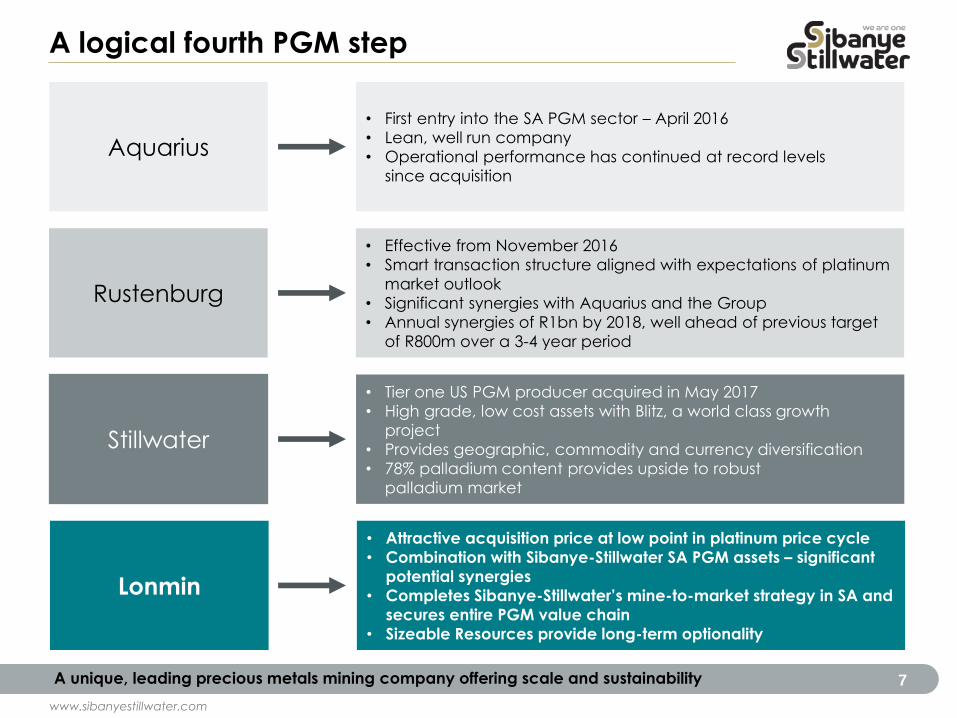

A logical fourth PGM step

7

Aquarius

Rustenburg

Stillwater

Lonmin

• First entry into the SA PGM sector – April 2016

• Lean, well run company

• Operational performance has continued at record levels

since acquisition

• Effective from November 2016

• Smart transaction structure aligned with expectations of platinum

market outlook

• Significant synergies with Aquarius and the Group

• Annual synergies of R1bn by 2018, well ahead of previous target

of R800m over a 3-4 year period

• Tier one US PGM producer acquired in May 2017

• High grade, low cost assets with Blitz, a world class growth

project

• Provides geographic, commodity and currency diversification

• 78% palladium content provides upside to robust

palladium market

• Attractive acquisition price at low point in platinum price cycle

• Combination with Sibanye-Stillwater SA PGM assets – significant

potential synergies

• Completes Sibanye-Stillwater’s mine-to-market strategy in SA and

secures entire PGM value chain

• Sizeable Resources provide long-term optionality

A unique, leading precious metals mining company offering scale and sustainability

www.sibanyestillwater.com

A leading precious metals mining company

8

0.2

0.3

0.6

0.7

1.4

1.6

2.0

RBPlats

Northam

Norilsk²

Lonmin

Impala

Sibanye-Stillwater

(post-transaction)³

Amplats¹

2016A platinum

production (moz)

0.1

0.1

0.3

0.9

1.3

1.3

2.6

RBPlats

Northam

Lonmin

Impala

Amplats¹

Sibanye-Stillwater

(post-transaction) ³

Norilsk²

2016A palladium

production (moz)

1.5

1.7

2.0

2.1

2.4

2.8

2.9

3.6

3.8

5.2

5.5

Sibanye-Stillwater

Agnico-Eagle

Polyus

Gold Fields

Newcrest

Kinross

Gold Corp

AngloGold

Sibanye-Stillwater

(post-transaction)

Newmont

Barrick

2016A gold and gold

equivalents

production (moz)

3,4

Sibanye-Stillwater global PGM ranking Sibanye-Stillwater global gold ranking

Lonmin’s contribution to Sibanye-Stillwater

Positioned globally as a leading precious metals producer

Source: Company filings

Note:

1. Exclusive of Rustenburg Mine

2. Includes PGM by-products only

3. Rustenburg + Aquarius + Stillwater + Lonmin. Rustenburg, Kroondal, Platinum Mile and Mimosa as of FY16, per public disclosure. Figures include Blitz at full ramp-up

4. Sibanye –Stillwater gold equivalents included

www.sibanyestillwater.com

Manageable liquidity position

9

($ 305)

($ 225)

$ 175

$ 435 $ 480 $ 444 $ 537

($ 800)

($ 600)

($ 400)

($ 200)

$ 0

$ 200

$ 400

$ 600

2017 2018 2019 2020 2021 2022 2023 2024 2025

Pro-Forma¹ Liquidity and Debt Maturity Ladder - US$ millions

Cash (incl GBF) Available Facilities USD RCF ($350m) ZAR RCF (R6bn)

2022 Bonds ($500m) 2023 Convertible ($450m) 2025 Bonds ($550m)

Note: Sibanye-Stillwater figures as at 30 June 2017

¹ Pro-forma assumes Lonmin is acquired at a net debt neutral position

• Our priority is the deleveraging of our balance sheet

– Current net debt/EBITDA of 2.6x targeting 1.0x in the medium term

– All share consideration for Lonmin will not add debt to the balance sheet

• Anticipated that Lonmin will settle their current debt facilities prior to closing

with own cash

Primary focus on deleveraging – conserving cash

Transaction overview

10

www.sibanyestillwater.com

• Sibanye-Stillwater to acquire 100%

of Lonmin

• All share consideration:

– Share exchange ratio of 0.967

– At closing prices on 13 December 2017 this equates to a 35% premium

– Based on the 30 day VWAP of Sibanye-Stillwater this values each Lonmin share at 100p or a 41% premium to the Lonmin 30 day VWAP, equates to aggregate value of R5.15 billion (GBP 285 million)

– Lonmin Shareholders will receive approximately 11.3 % of pro-forma market cap

• Subject to various conditions

precedent

• No break or cancellation fee

• Should Sibanye-Stillwater

shareholders not approve the

transaction, agreement in principle

to discuss asset acquisition

A logical value accretive transaction

Transaction overview

11

1. Northam

2. Anglo America

Platinum

3. Siyanda Resources

4. Sedibelo Platinum

5. Wesizwe Platinum

6. Royal Bafokeng

Platinum

7. Impala Platinum

8. Eastern Platinum

Sibanye-Stillwater

Lonmin

12

3

2

4

6

Western Bushveld

Joint Venture

Pandora Joint

Venture

7

7

66

5

10

18

www.sibanyestillwater.com

Transaction subject to, inter-alia, the following conditions:

• Lonmin shareholder approval following all regulatory approvals (>75% by value

and majority in number of shares present and voting)

• Certain competition and regulatory approvals in relevant jurisdictions 1

• No cancellation of any prospecting or mining right held by Lonmin, pursuant to

Section 47 of the MPRDA having a material adverse effect 2

• Sibanye-Stillwater shareholder approval following all regulatory approvals

(>50% of shares present and voting)

Key conditions precedent

12

Note:

1. Including South Africa, the United Kingdom or possibly the European Union

2. Subject to Panel confirmation

A smart transaction structure

www.sibanyestillwater.com

Indicative milestones to closing

13

Target completion in

H2 2018

Announcement of transaction – 14 December, 2017

Lonmin shareholder approval and court meeting – H2 2018

Competition clearance obtained – H2 2018

Lonmin publish annual financial statements – January, 2018

The approval of the scheme by the court

Sibanye-Stillwater shareholder approval – H2 2018

A smart transaction structure

Transaction rationale

14

www.sibanyestillwater.com

Lonmin – transaction rationale

15Bongekile Ngqulunga

Lonmin Head of Precious

Metals Refinery

www.sibanyestillwater.com

16

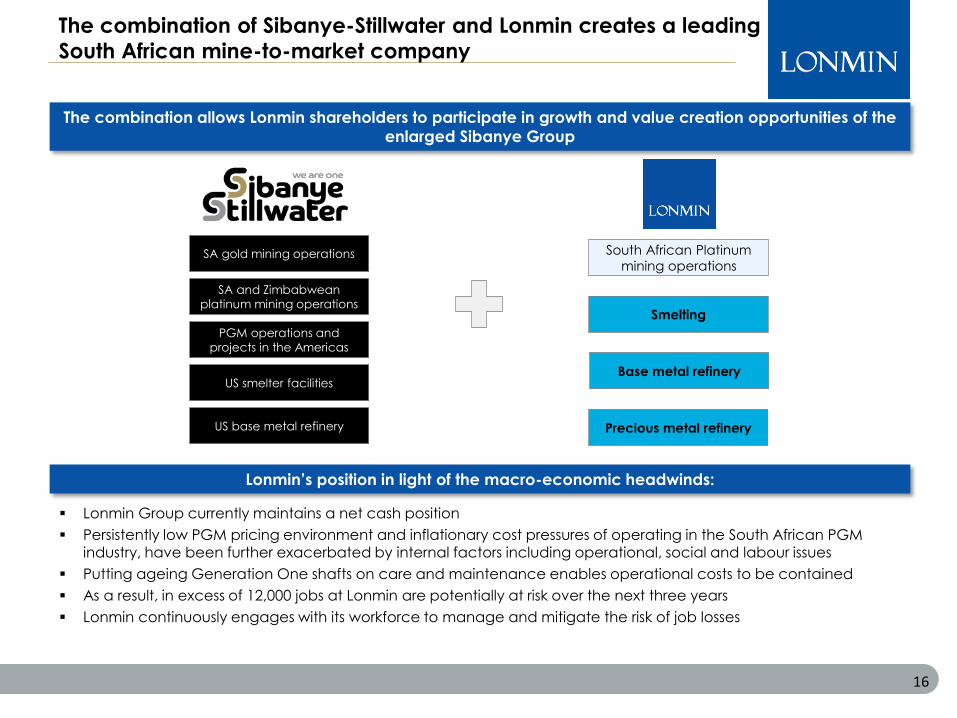

The combination allows Lonmin shareholders to participate in growth and value creation opportunities of the

enlarged Sibanye Group

SA gold mining operations

SA and Zimbabwean

platinum mining operations

PGM operations and

projects in the Americas

US smelter facilities

US base metal refinery

South African Platinum

mining operations

Smelting

Base metal refinery

Precious metal refinery

Lonmin Group currently maintains a net cash position

Persistently low PGM pricing environment and inflationary cost pressures of operating in the South African PGM

industry, have been further exacerbated by internal factors including operational, social and labour issues

Putting ageing Generation One shafts on care and maintenance enables operational costs to be contained

As a result, in excess of 12,000 jobs at Lonmin are potentially at risk over the next three years

Lonmin continuously engages with its workforce to manage and mitigate the risk of job losses

Lonmin’s position in light of the macro-economic headwinds:

The combination of Sibanye-Stillwater and Lonmin creates a leading

South African mine-to-market company

www.sibanyestillwater.com

“ We believe that this Offer is in the best interests of Lonmin, Lonmin

Shareholders and all other stakeholders. Lonmin has an enviable mine to

market business with great mining assets, projects and process

technology and resilient workforce. Despite this, Lonmin continues to be

hamstrung by liquidity concerns. The combination with Sibanye-Stillwater

therefore provides a stronger platform for Lonmin shareholders and other

stakeholders to benefit from the long-term upside potential of an enlarged and geographically diversified Sibanye-Stillwater group. We

therefore unanimously recommend this Offer to our shareholders.” Ben

Magara – Chief Executive Officer

17

Lonmin CEO message

Sibanye-Stillwater

rationale

18

www.sibanyestillwater.com

• Sibanye-Stillwater anticipates that the transaction is NAV accretive on closing and earnings and cash flow accretive on a per share basis from 2021, once synergies begin to be realised in full and once related one-off costs have been incurred

• Detailed due diligence confirms significant synergies between Sibanye-Stillwater and Lonmin’s contiguous PGM assets

• Acquiring downstream processing business with a replacement value significantly higher than acquisition cost

• Enhanced scale facilitates greater operational flexibility and more effective allocation of capital

• Sizeable PGM Resources with potential upside from advanced brownfield projects and greenfield project pipeline

4%

29%

3%

6%

58%

Pro forma Mineral Reserves

4E Moz

Kroondal

Rustenburg

Mimosa

Tailings

Lonmin

Value accretive transaction with upside

Sibanye-Stillwater rationale

19

3%

27%

2%

8%

1%

59%

Pro forma Mineral Resources

4E Moz

Kroondal

Rustenburg

Mimosa

Projects

Tailings

Lonmin

Total

54.9moz

Total

307.1moz

1

Note:

1. Mineral Reserves and resources 4E attributable. Source: Companies’ 2016 Reserve and Resources statements

www.sibanyestillwater.com

Attractive acquisition at low point in price cycle

20

Lonmin: Afriore

Mvela: Booysendal &

Northam

Nkwe: Garatau/Tubatse

Anooraq: Bokoni

Jubilee: Tjate Project

Platmin: Sedibelo West

Anglo: AnooraqZambezi: Northam

Hebei: Eastplats

Sibanye-Stillwater:

Aquarius

Sibanye-Stillwater:

Rustenburg

Lonmin: Pandora

Northam: Tumela

Northam: Eland

RBPlats: Maseve

Implats: Waterberg

Sibanye-Stillwater:

Lonmin

0

5

10

15

20

0 100 200 300 400 500 600 700

De

al va

lue

(U

S$/R

eso

urc

e o

z)

Deal value (US$m)

Historic SA PGM transactions

A sizeable resource base at a compelling price

Source: Various companies’ disclosures

Note: Bubble size represents PGM Resources

www.sibanyestillwater.com

Marikana mines overview

21

Source: Lonmin 2017 Interim Results Presentation

SC =Shaft Capacity

DWL = Deepest Working Level

www.sibanyestillwater.com

• Significant capital investment required to maintain flat production profile

– Substantial capital hump

• Decommissioning of generation one shafts, which are coming to the end of

their lives, results in an expected retrenchment of approximately 12 600

employees over the next 3 years

Challenging financial requirements under current economic conditions

Lonmin production and capex profile

22

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

202

9

203

0

203

1

203

2

203

3

203

4

203

5

203

6

203

7

4E P

GM

ou

nc

es

Lonmin LoM - 4E PGM ounces in concentrate

K3 Saffy Rowland E3

4B K4 W1 E1

E2 Hossy Newman BTT

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

202

9

203

0

203

1

203

2

203

3

203

4

203

5

203

6

203

7

R m

illio

n

Lonmin LoM - Total capital by category (real terms)

Total Mining Capex Total Conc. Capex

Total S&R Capex Total Other Capex

Source: Lonmin’s company information

Note:

1. Numbers include contractors

www.sibanyestillwater.com

Affordable mining plan with optionality

Sibanye-Stillwater revised operational plan

23

• Revised mining plan developed after detailed due diligence

• Plan suitable for current economic and market conditions

– “Lower for longer” plan

• Conservative plan not contingent on expenditure of project capital thereby

ensuring affordability

• Generation one shafts to be put on care and maintenance as per Lonmin plan

• Flexibility to delay Mining project capital

– Optionality to significantly extend operating life in a higher PGM price environment

Saffy RowlandK3 E3 4B K4

NewmanW1 E1 E2 Hossy BTT

Lonmin LoM 4E PGM ounces in concentrate

Concentrator capex Smelter and refinery capexMining capex

Other capex New furnace capex Total LoM Capex

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

2018 2021 2024 2027 2030 2033 2036

4E P

GM

ou

nc

es

Revised plan - adjusted 4E PGM ounces

in concentrate

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2018 2021 2024 2027 2030 2033 2036

R m

illio

n

Revised capital by category compared to Lonmin

plan (Real terms)

Source: Lonmin’s company information and due diligence performed by Sibanye-Stillwater

www.sibanyestillwater.com

Revised plan designed to ensure viability of operations

Restructuring

24

As at 30 September* 2017 Actual 2018 2019 2020 Cumulative

Total employees 32 512 28 812 23 512 19 912

Head count reduction -3 700 -5 300 -3 600 -12 600

* Numbers quoted include contractors

¹ Exclude additional smelter and refinery personnel required for the additional furnace in the Sibanye-Stillwater plan

• Planned retrenchment of approximately 12 600* employees over the next

three years primarily as a result of generation one shafts reaching the end of

their reserves

• The Sibanye-Stillwater revised business plan could affect a further 890¹ people

• The revised Sibanye-Stillwater plan is a base case for viability under current

market conditions

• Subject to S189 consultations, the possible retrenchments are anticipated to be

phased over a three-year period

Lonmin plan (before the transaction)

www.sibanyestillwater.com

Average processing synergies from 2021 to 2032 of approximately R550m per annum

Processing considerations

25

• Ability to treat Rustenburg

concentrate in Lonmin

processing facilities from 2021

• Synergy benefit of treating own

concentrate through owned

facilities

• Optimising capacity positively

impacts processing unit costs

• Allows for better mine planning

flexibility enhancing profitable

mining mix

• Potential to build DC ARC

furnace (approximate capital

cost of R1bn) to cater for total

Rustenburg concentrate

– Other potential solutions also being investigated

-

100 000

200 000

300 000

400 000

500 000

-

100 000

200 000

300 000

400 000

500 000

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

Ton

ne

s o

f C

on

cen

trat

e

Concentrate by Source

Sibanye-Stillwater Concentrate tonnes Lonmin Concentrate produced tonnes

-

200 000

400 000

600 000

800 000

1000 000

1200 000

1400 000

1600 000

1800 000

2000 000

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

4E

oz

in c

on

c /

4E

oz

pro

du

ced

4E PGM oz by Source

Lonmin 4E contained in conc Sibanye-Stillwater 4E Produced

www.sibanyestillwater.com

Long-term benefits of mine-to-market model in SA

26Creating an integrated long life mining and processing complex on the Western Limb

• One of only 3 fully integrated South

African PGM producers

• Scale allows for optimisation of

processing facilities, reducing unit

costs

• Reduced processing costs of

Rustenburg production from 2021

www.sibanyestillwater.com

Clear cost benefits realised at Kroondal and Rustenburg operations from integration with Sibanye-Stillwater

PGM all-in cost curves 2016 - 2017

27

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

20 000

Co

st R

/Oz

Two

riv

ers

Mo

toto

lo

Ea

st B

ou

lde

r

Stillw

ate

r

Zim

pla

ts

Kro

on

da

l

Un

ion

Ma

rula

Mo

dik

wa

Am

an

de

lbu

lt

Mo

ga

lakw

en

a

Lon

min

Mim

osa

Bo

oyse

nd

al

Ru

ste

nb

urg

Imp

ala

Bo

sch

ko

pp

ie

Un

ki

Zo

nd

ere

ind

e

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

20 000

Co

st R

/Oz

Two

riv

ers

Ea

st B

ou

lde

rStillw

ate

r

Mo

toto

lo

Kro

on

da

l

Zim

pla

ts

Ru

ste

nb

urg

Mo

ga

lakw

en

a

Mo

dik

wa

Mim

osa

Un

ion

Lon

min

Am

an

de

lbu

lt

Un

ki

Bo

oyse

nd

al

Imp

ala

Bo

sch

ko

pp

ie

Zo

nd

ere

ind

e

Ma

rula

Avg. basket price R12,128/ounce (6E)Avg. all-in costs = R12,589/ounce (6E)

Avg. basket price R12,699/ounce (6E)Avg. all-in costs = R12,277/ounce (6E)

Source: Company reports, Citi Research,

Note:

1. Includes cash costs, all capex exploration, corporate costs, cash taxes and other operating costs

2. Excluding base metal credits

3. Mines acquired by Sibanye-Stillwater in the Aquarius acquisition include Kroondal and Mimosa

Jun-16 all-in costs1 chart, by mine (R/6E ounce)2

Jun-17 all-in costs1 chart, by mine (R/6E ounce)2

Sibanye-Stillwater mines Lonmin Other PGM mines

www.sibanyestillwater.com

• Overhead costs (R730m per annum by 2021)

– Corporate office rationalisation (closing

the London office and delisting)

– Regional shared services

– Operational (mining) services

– One-off R80m cost required to achieve

these synergies

• Processing synergies

– Differential cost benefits of R780m by

2021 and an average of approximately

R550 per annum from 2021

– Approximately R1bn of capex required

for the purchase of a new furnace

Quantified synergies 1 Incremental synergy potential 2

• Ability to mine through existing mine boundaries

• Optimal use of surface infrastructure

• Optimising the mining mix

• Prioritisation of projects and new growth capital

• Capital reorganisation in line with new consolidated regional plan

Material synergies with Lonmin operations

28

Pre-tax synergies of approx. R1.5bn per annum by 2021

Note:

1. For overhead synergies, total savings anticipated when fully implemented in FY21; varies per toll agreement production

throughput for processing synergies with average calculated between 2021 and 2032

2. Synergies which are unquantifiable at this point in time

Average annual pre–tax synergies of approximately R1.3bn from 2021 – ensuring operational viability

www.sibanyestillwater.com

• Potential to retain more jobs in the

longer term

• Continued delivery of benefits for

employees, communities and other

stakeholders

• Greater stability for the Rustenburg

regional economy

• Positive for the South African fiscus

All stakeholders to benefit over the longer term

Broader stakeholder benefits

29

Conclusion

30

www.sibanyestillwater.com

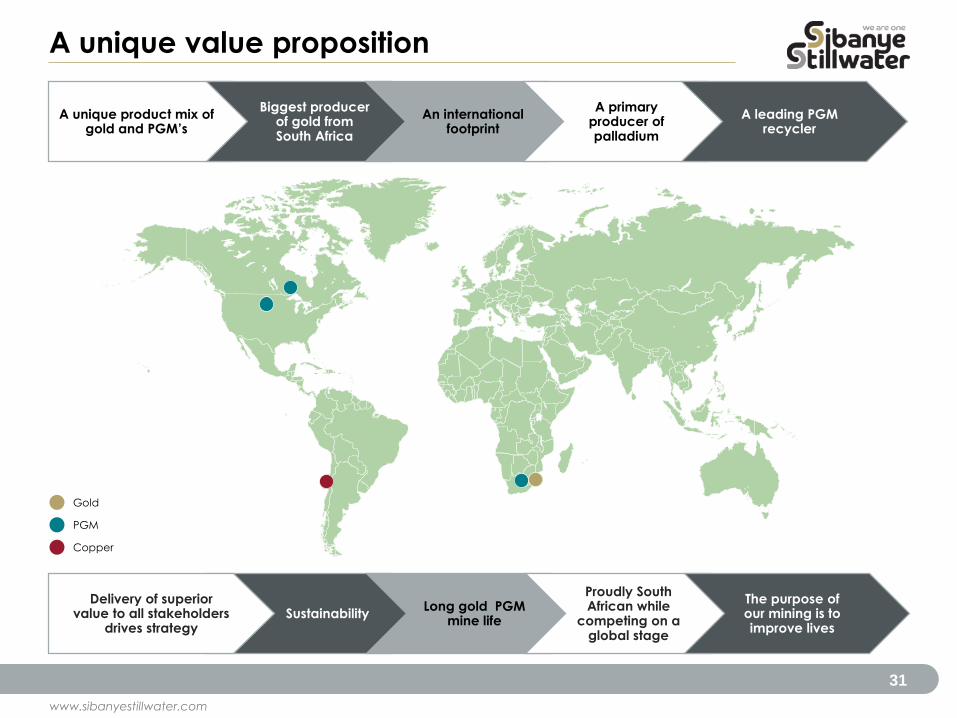

A unique value proposition

31

A unique product mix of gold and PGM’s

Biggest producer of gold from South Africa

An international footprint

A primary producer of palladium

A leading PGM recycler

Sustainability Long gold PGM

mine life

Proudly South African while

competing on a global stage

The purpose of our mining is to improve lives

Delivery of superior value to all stakeholders

drives strategy

Gold

PGM

Copper

Contacts

James Wellsted/ Henrika Ninham

Tel:+27(0)83 453 4014/ +27(0)72 448 5910

Website: www.sibanyestillwater.com

32

Appendix

33

www.sibanyestillwater.com

Transaction summary

34

Consideration

• Under the terms of the Offer, each Lonmin shareholder will be entitled to receive:

• for each Lonmin Share 0.967 New Sibanye-Stillwater Shares

• Based on the 30 trading day volume weighted average price of R18.67 of Sibanye-Stillwater shares for the period ended 13 December 2017 (being the last business day prior to the date of this announcement)*, the offer values each Lonmin share at 100.0 pence and values the existing issued ordinary share capital of Lonmin at approximately £285 million and represents

a premium of approximately:

• 57 per cent. to the closing price per Lonmin share of 63.8 pence on 13 December 2017; and

• 41 per cent. to the 30 trading day volume weighted average price per Lonmin share for the period ended 13 December 2017 of 71.1 pence.

• The exchange ratio of the offer has been determined using the 30 trading day volume

weighted average price for Sibanye-Stillwater to smooth out the daily movements.

• Based on the closing price of R16.11 of a Sibanye-Stillwater share on 13 December 2017*, the offer values each Lonmin share at 86.3 pence and represents a premium of approximately 35 per cent. to the closing price per Lonmin share of 63.8 pence on 13 December 2017.

• Following completion of the acquisition, Lonmin shareholders will hold approximately 11.3 per cent. of the enlarged Sibanye-Stillwater group

Source: Factset as of 13 December 2017

* The exchange rate on that date being R18.056:£1

www.sibanyestillwater.com

Transaction summary (continued)

35

Directors’ recommendationsand irrevocable undertakings

• The Lonmin Directors intend unanimously to recommend that Lonmin shareholders vote in favour of the scheme at the court meeting and the resolutions to be proposed at the Lonmingeneral meeting

• The Lonmin Directors have irrevocably undertaken to Sibanye-Stillwater to do in respect of their own beneficial shareholdings in Lonmin representing approximately 0.026698 per cent. of the existing issued ordinary share capital of Lonmin

Shareholderapproval

• Sibanye-Stillwater shareholder approval in relation to the issue of the new Sibanye-Stillwater shares to Lonmin shareholders in accordance with the Sibanye-Stillwater Memorandum of Incorporation supported by more than 50 percent of the voting rights exercised on the ordinary resolution at the Sibanye-Stillwater shareholder meeting

• Lonmin shareholder approval

• a majority in number of the Lonmin shareholders who are present and vote (and are entitled to vote), whether in person or by proxy, at the court meeting and who represent 75 per cent. in value of the Lonmin Shares voted by those Lonmin shareholders

• the resolutions required to implement the Scheme being duly passed by the requisite majority or majorities of votes cast at the Lonmin general meeting

Required key regulatory approvals*

• Certain competition and regulatory approvals (including in South Africa and the United Kingdom (or the European Union, in case a referral is made to the European Commission pursuant to Article 22 of the Council Regulation (EC) 139/2004) being obtained

License condition

• There is no cancellation of any prospecting right or mining right held by Lonmin pursuant to Section 47 of the MPRDA where such cancellation is material, and if such a cancellation has occurred it has not been: (i) withdrawn, lifted or revoked in writing by the Minister; or (ii) set aside, nullified or otherwise suspended by the order of a court of competent jurisdiction, within 15 business days of such cancellation (or, if earlier, by the date scheduled for the court hearing to approve the scheme).

*Refer to www.sibanyestillwater.com/investors/transactions/lonmin for announcement with full details on the required regulatory and other approvals

www.sibanyestillwater.com

Overview of Lonmin PGM operations

36

95%

3% 2%

Mineral Reserves 4E Moz 1

Marikana

Pandora JV

Tailings Dams

64%

16%

9%

7%3%1%

Mineral Resources 4E Moz 1

Marikana

Akanani

Limpopo

Pandora JV

Limpopo

Loskop JV

Western Limb Assets:• Marikana Mine• Pandora Mine

Total

31.7 Moz

Total

180.6 Moz

0.52

0.24

0.01

0.08

0.12

0.03

Refined 6E PGMS 2

Platinum

Palladium

Gold

Rhodium

Ruthenium

Iridium

Total

1.32 Moz

Eastern Limb Assets:• Limpopo & Loskop

Northern Limb Assets:• Akanani Project

Note:

1. Mineral Reserves and resources 4E attributable. Source: 2016 Reserve and Resources statement

2. Total refined PGMS 2017 - Fourth Quarter and Full Year 2017 Production Report and Business Update