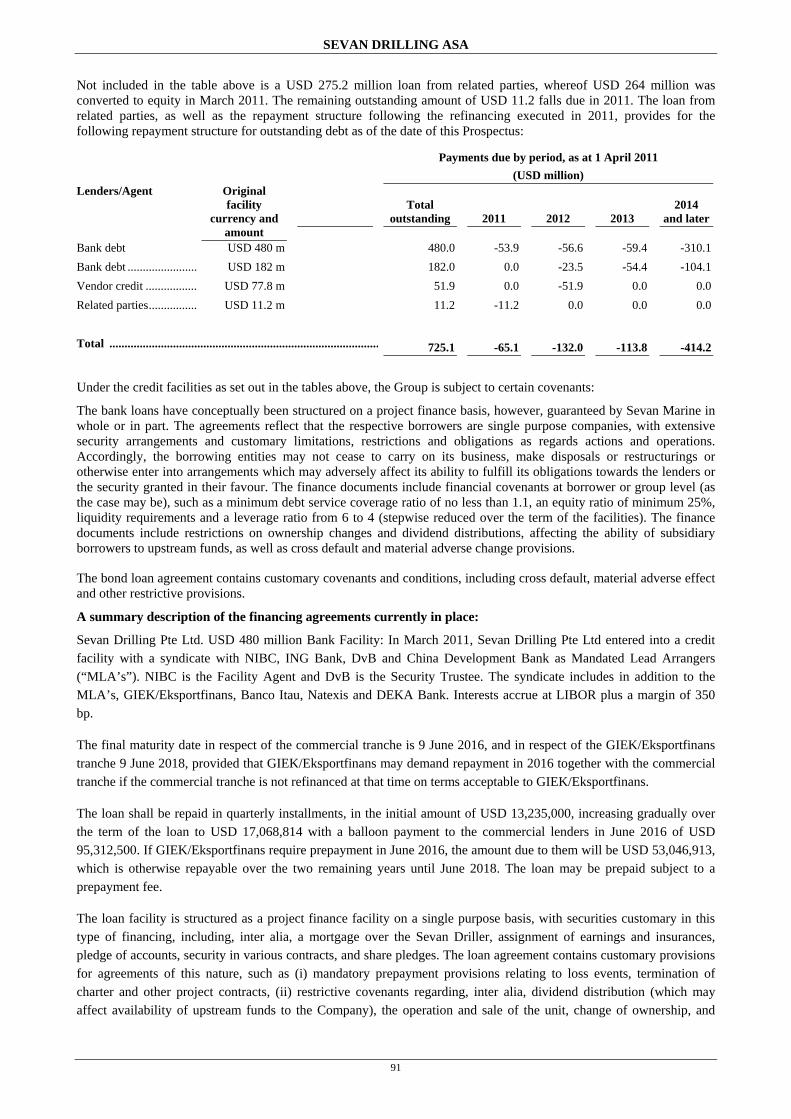

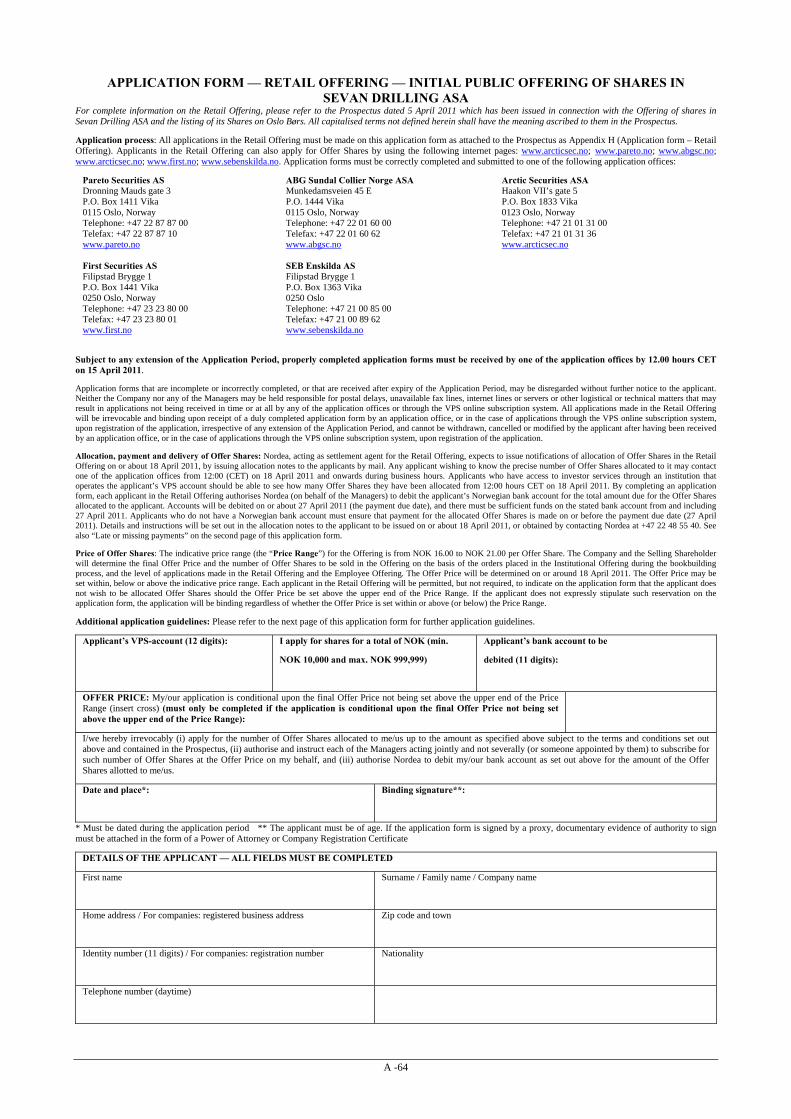

PROSPECTUS SEVAN DRILLING ASA (A public limited liability company organized under the laws of the Kingdom of Norway) Up to NOK 3.270 million initial public offering Indicative price range from NOK 16.00 to NOK 21.00 per Offer Share The information contained in this prospectus (the “Prospectus”) relates to the initial public offering and listing on Oslo Børs, or alternatively, Oslo Axess, of ordinary shares, each with a par value of NOK 1.00 (the “Shares”), in Sevan Drilling ASA (“Sevan Drilling” or the “Company”), a public limited liability company organized under the laws of Norway (taken together with its consolidated subsidiaries, the “Sevan Drilling Group” or the “Group”). The Company intends to effect a global offering of Shares (“the Offer Shares”) of up to NOK 3.270 million (~USD 595 million) (the “Offering”) by way of a combined secondary offering of existing shares in the Company held by Sevan Marine ASA (“Sevan Marine” or the “Selling Shareholder”) and a primary issuance of new shares in the Company. The Offering will comprise (i) an institutional offering to (a) institutional and professional investors in Norway, (b) institutional investors outside Norway and the United States, and (c) in the United States, to “qualified institutional buyers” (“QIBs”) as defined in, and in reliance on, Rule 144A (“Rule 144A”) under the United States Securities Act of 1933, as amended (the “US Securities Act”) (the “Institutional Offering”); and (ii) a retail offering to the public in Norway (the “Retail Offering”); and (iii) an employee offering to Eligible Employees (as defined herein) (the “Employee Offering”). All offers and sales outside the United States will be made in reliance on Regulation S (“Regulation S”) under the US Securities Act. The price of the Offer Shares (the “Offer Price”) will be fixed based on a bookbuilding period for the Institutional Offering (the “Bookbuilding Period”), which is expected to run from 09:00 hours (Central European Time, “CET”) on 5 April 2011 to 17:30 hours (CET) on 15 April 2011, whereas the application period for the Retail Offering and the Employee Offering (the “Application Period”) is expected to run from 09:00 hours (CET) on 5 April 2011 to 12:00 hours (CET) on 15 April 2011 The Selling Shareholder has granted the Managers (as defined below) an option to purchase, at the Offer Price, up to 13 million additional Shares (but not exceeding 10% of the number of Offer Shares initially allocated in the Offering) (the “Additional Shares”) to cover over-allotments in connection with the Offering and short positions, if any, exercisable within a 30-day period commencing at the time trading in the Shares on Oslo Børs (the “Over-Allotment Option”). The Over- Allotment Option will be effected by way of a further secondary sale of Existing Shares held by the Selling Shareholder, and may be exercised solely to cover over-allotments in connection with the Offering.. All Shares will be registered in the Norwegian Central Securities Depository (the “VPS”), and will be in book-entry form. All Shares will rank in parity with one another and carry one vote per Share. THE OFFER SHARES AND ADDITIONAL SHARES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE US SECURITIES ACT OR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OR OTHER JURISDICTION IN THE UNITED STATES, AND MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES EXCEPT TO QIBS IN RELIANCE ON THE EXEMPTION FROM THE REGISTRATION REQUIREMENTS OF THE US SECURITIES ACT PROVIDED BY RULE 144A, OR OUTSIDE THE UNITED STATES IN COMPLIANCE WITH REGULATION S. THIS PROSPECTUS HAS NOT BEEN APPROVED NOR REVIEWED BY THE US SECURITIES AND EXCHANGE COMMISSION AND IS NOT FOR GENERAL DISTRIBUTION IN THE UNITED STATES. FOR CERTAIN SELLING AND TRANSFER RESTRICTIONS SEE SECTION 6 “SELLING AND TRANSFER RESTRICTIONS”. Prior to the Offering, there has been no public trading market for the Shares. Sevan Drilling has applied for admission to trading of the Shares on Oslo Børs, and the listing application is expected to be approved by the Board of Directors of Oslo Børs on 27 April 2011. Completion of the Offering is conditional upon, inter alia, Oslo Børs approving the Company’s application for listing on Oslo Børs, or, alternatively, Oslo Axess. The payment due date for the Offer Shares is expected to be on or about 27 April 2011. The Offer Shares will be delivered through the facilities of the VPS. Trading in the Shares on Oslo Børs, or, alternatively, Oslo Axess, is expected to commence on or about 29 April 2011, under the trading symbol “SDRILL”. Global Coordinator Pareto Securities Joint Lead Managers and Joint Bookrunners Pareto Securities ABG Sundal Collier Arctic Securities First Securities ING Bank SEB Enskilda The date of this Prospectus is 5 April 2011

Transcript

PROSPECTUS

SEVAN DRILLING ASA (A public limited liability company organized under the laws of the Kingdom of Norway)

Up to NOK 3.270 million initial public offering Indicative price range from NOK 16.00 to NOK 21.00 per Offer Share

The information contained in this prospectus (the “Prospectus”) relates to the initial public offering and listing on Oslo Børs, or alternatively, Oslo Axess, of ordinary shares, each with a par value of NOK 1.00 (the “Shares”), in Sevan Drilling ASA (“Sevan Drilling” or the “Company”), a public limited liability company organized under the laws of Norway (taken together with its consolidated subsidiaries, the “Sevan Drilling Group” or the “Group”). The Company intends to effect a global offering of Shares (“the Offer Shares”) of up to NOK 3.270 million (~USD 595 million) (the “Offering”) by way of a combined secondary offering of existing shares in the Company held by Sevan Marine ASA (“Sevan Marine” or the “Selling Shareholder”) and a primary issuance of new shares in the Company. The Offering will comprise (i) an institutional offering to (a) institutional and professional investors in Norway, (b) institutional investors outside Norway and the United States, and (c) in the United States, to “qualified institutional buyers” (“QIBs”) as defined in, and in reliance on, Rule 144A (“Rule 144A”) under the United States Securities Act of 1933, as amended (the “US Securities Act”) (the “Institutional Offering”); and (ii) a retail offering to the public in Norway (the “Retail Offering”); and (iii) an employee offering to Eligible Employees (as defined herein) (the “Employee Offering”). All offers and sales outside the United States will be made in reliance on Regulation S (“Regulation S”) under the US Securities Act.

The price of the Offer Shares (the “Offer Price”) will be fixed based on a bookbuilding period for the Institutional Offering (the “Bookbuilding Period”), which is expected to run from 09:00 hours (Central European Time, “CET”) on 5 April 2011 to 17:30 hours (CET) on 15 April 2011, whereas the application period for the Retail Offering and the Employee Offering (the “Application Period”) is expected to run from 09:00 hours (CET) on 5 April 2011 to 12:00 hours (CET) on 15 April 2011

The Selling Shareholder has granted the Managers (as defined below) an option to purchase, at the Offer Price, up to 13 million additional Shares (but not exceeding 10% of the number of Offer Shares initially allocated in the Offering) (the “Additional Shares”) to cover over-allotments in connection with the Offering and short positions, if any, exercisable within a 30-day period commencing at the time trading in the Shares on Oslo Børs (the “Over-Allotment Option”). The Over-Allotment Option will be effected by way of a further secondary sale of Existing Shares held by the Selling Shareholder, and may be exercised solely to cover over-allotments in connection with the Offering..

All Shares will be registered in the Norwegian Central Securities Depository (the “VPS”), and will be in book-entry form. All Shares will rank in parity with one another and carry one vote per Share.

THE OFFER SHARES AND ADDITIONAL SHARES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE US SECURITIES ACT OR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OR OTHER JURISDICTION IN THE UNITED STATES, AND MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES EXCEPT TO QIBS IN RELIANCE ON THE EXEMPTION FROM THE REGISTRATION REQUIREMENTS OF THE US SECURITIES ACT PROVIDED BY RULE 144A, OR OUTSIDE THE UNITED STATES IN COMPLIANCE WITH REGULATION S.

THIS PROSPECTUS HAS NOT BEEN APPROVED NOR REVIEWED BY THE US SECURITIES AND EXCHANGE COMMISSION AND IS NOT FOR GENERAL DISTRIBUTION IN THE UNITED STATES. FOR CERTAIN SELLING AND TRANSFER RESTRICTIONS SEE SECTION 6 “SELLING AND TRANSFER RESTRICTIONS”.

Prior to the Offering, there has been no public trading market for the Shares. Sevan Drilling has applied for admission to trading of the Shares on Oslo Børs, and the listing application is expected to be approved by the Board of Directors of Oslo Børs on 27 April 2011. Completion of the Offering is conditional upon, inter alia, Oslo Børs approving the Company’s application for listing on Oslo Børs, or, alternatively, Oslo Axess.

The payment due date for the Offer Shares is expected to be on or about 27 April 2011. The Offer Shares will be delivered through the facilities of the VPS. Trading in the Shares on Oslo Børs, or, alternatively, Oslo Axess, is expected to commence on or about 29 April 2011, under the trading symbol “SDRILL”.

Global Coordinator Pareto Securities

Joint Lead Managers and Joint Bookrunners

Pareto Securities ABG Sundal Collier Arctic Securities First Securities ING Bank SEB Enskilda

The date of this Prospectus is 5 April 2011

IMPORTANT INFORMATION This Prospectus has been prepared to comply with the Norwegian Securities Trading Act of 29 June 2007 no. 75 (the “Norwegian Securities Trading Act”) and related secondary legislation, including the Commission Regulation (EC) no. 809/2004 implementing Directive 2003/71/EC of the European Parliament and of the Council of 4 November 2003 regarding information contained in prospectuses (the “Prospectus Directive”) as well as the format, incorporation by reference and publication of such prospectuses and dissemination of advertisements (hereafter “EC Regulation 809/2004”). This Prospectus has been prepared solely in the English language; however a Norwegian language summary is included in Section 18 “Norwegian Summary (Norsk Sammendrag)”. The Financial Supervisory Authority of Norway (Nw. Finanstilsynet) (the “Norwegian FSA”) has reviewed and approved this Prospectus in accordance with Sections 7-7 and 7-8 of the Norwegian Securities Trading Act.

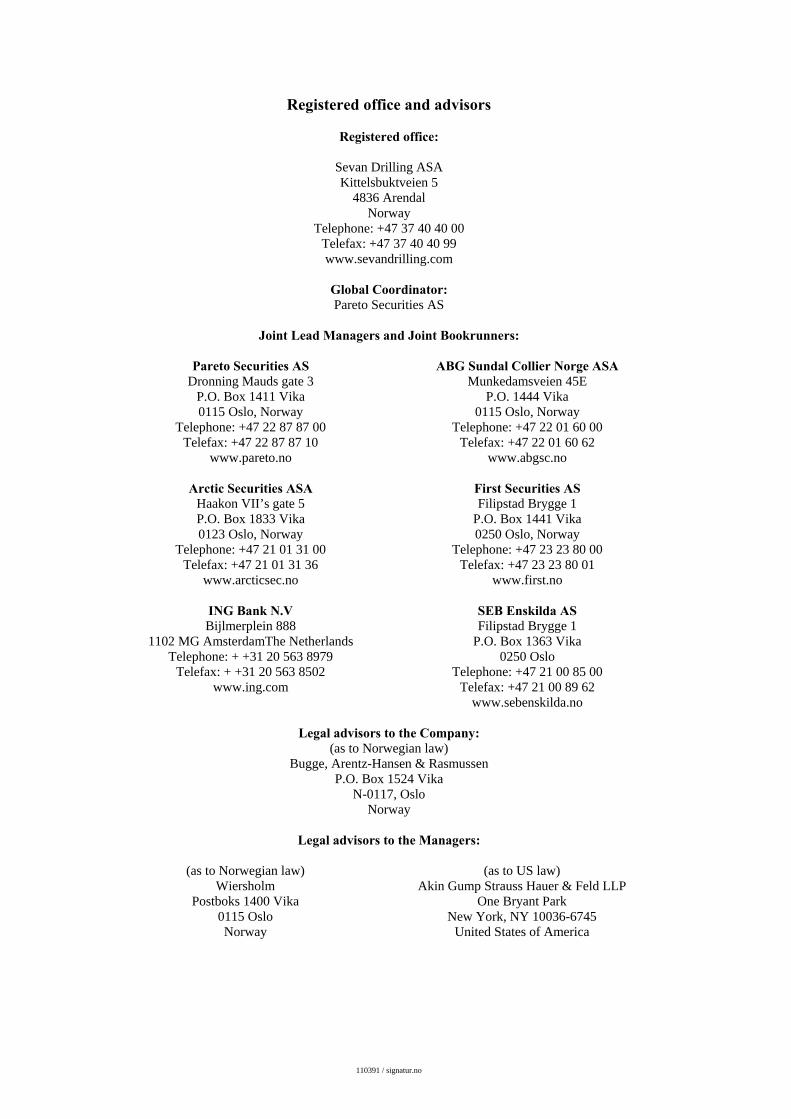

The Company and Sevan Marine have engaged Pareto Securities AS as Global Coordinator. Pareto Securities AS, ABG Sundal Collier Norge ASA, Arctic Securities ASA, First Securities AS, ING Bank N.V. and SEB Enskilda AS act as Joint Lead Managers and Joint Bookrunners for the Offering (together, the “Managers”).

Any reproduction or distribution of this Prospectus, in whole or in part, and any disclosure of its contents is prohibited.

This Prospectus and the terms and conditions of the Offering as set out herein shall be governed by and construed in accordance with Norwegian law. The courts of Norway, with Oslo as legal venue, shall have exclusive jurisdiction to settle any dispute which may arise out of or in connection with the Offering or this Prospectus.

4 notice to investors...................................................................................................................................... 26

5 The Offering .............................................................................................................................................. 29

6 Selling and Transfer Restrictions .............................................................................................................. 39

8 Company Description ................................................................................................................................ 63

9 Board of Directors, Management and Employees ..................................................................................... 75

10 Selected combined Financial INFORMATION ........................................................................................ 82

11 Operating and Financial Review ............................................................................................................... 86

12 Related Party Transactions ........................................................................................................................ 95

13 Dividends and Dividend Policy ................................................................................................................. 96

14 Description of the Shares and Share Capital ............................................................................................. 97

15 Securities Trading in Norway ................................................................................................................. 101

17 Additional Information ............................................................................................................................ 108

19 Definitions and Glossary ......................................................................................................................... 119

Appendix A: Articles of Association of Sevan Drilling ASA ................................................................... A-1 Appendix B: Audited Combined Accounts (IFRS) for the Sevan Drilling Group for the accounting

years 2010, 2009 and 2008 .................................................................................................. A-2 Appendix C: Audited historical financial information (NGAAP) for Sevan Drilling ASA for the

years ended 31 December 2010, 2009 and 2008 ............................................................... A-37 Appendix D: Application Form Employee Offering (English and Norwegian) ...................................... A-56 Appendix E: Application Form Retail Offering (English and Norwegian) ............................................ A-61

SEVAN DRILLING ASA

4

1 SUMMARY The following summary must be read as an introduction to the full text of this Prospectus, and is qualified in its entirety by, information presented in greater detail elsewhere in this Prospectus and the appendices hereto. This summary is not complete and does not contain all the information a potential investor should consider before investing in the Shares. Any investment decision relating to the Offering and an investment in the Shares should be based on the consideration of this Prospectus as a whole, including Section 2 “Risk Factors” and the Financial Statements included herein. Where a claim relating to the information contained in this Prospectus is brought before a court, a plaintiff investor might, under the national legislation of a Member State of the European Economic Area, have to bear the costs of translating this Prospectus before legal proceedings are initiated. No civil liability attaches to those persons who have prepared this summary, including any translations thereof, unless it is misleading, inaccurate or inconsistent when read together with other Sections of this Prospectus. For definitions of certain terms as used herein, see Section 19 “Definitions and Glossary”.

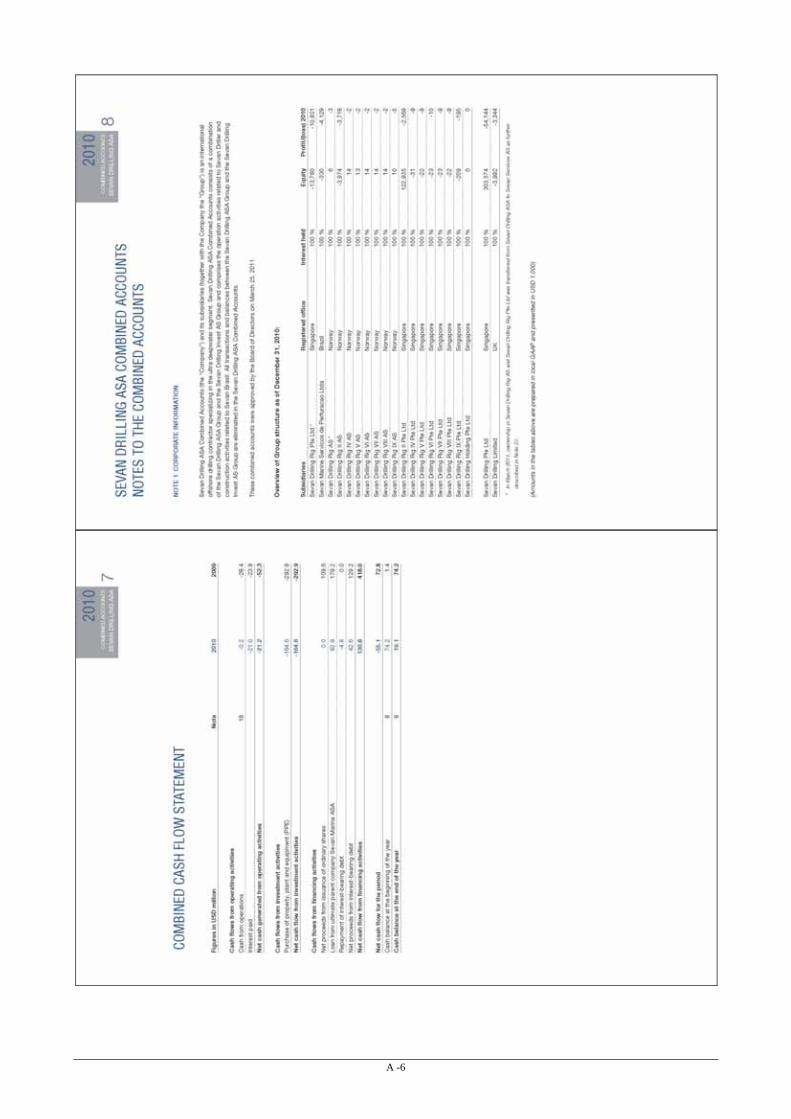

1.1 Introduction to Sevan Drilling Corporate information

Sevan Drilling was incorporated on 31 May 2006 as a public limited liability company. The Company is organized and existing under the laws of Norway in accordance with and pursuant to the Norwegian Public Limited Liability Companies Act. The Company’s registration number is 989 910 272.

According to section 2 of its articles of association, the Company’s head-quarters and registered office shall be in Stavanger. The Company is in the process of moving premises, but the current office is at Kittelsbuktveien 5, 4836 Arendal, Norway, telephone: +47 37 40 40 00 and telefax: +47 37 40 40 99. The Company’s website is www.sevandrilling.com.

Sevan Marine is as of the date of this Prospectus the sole shareholder in the Company.

Business overview

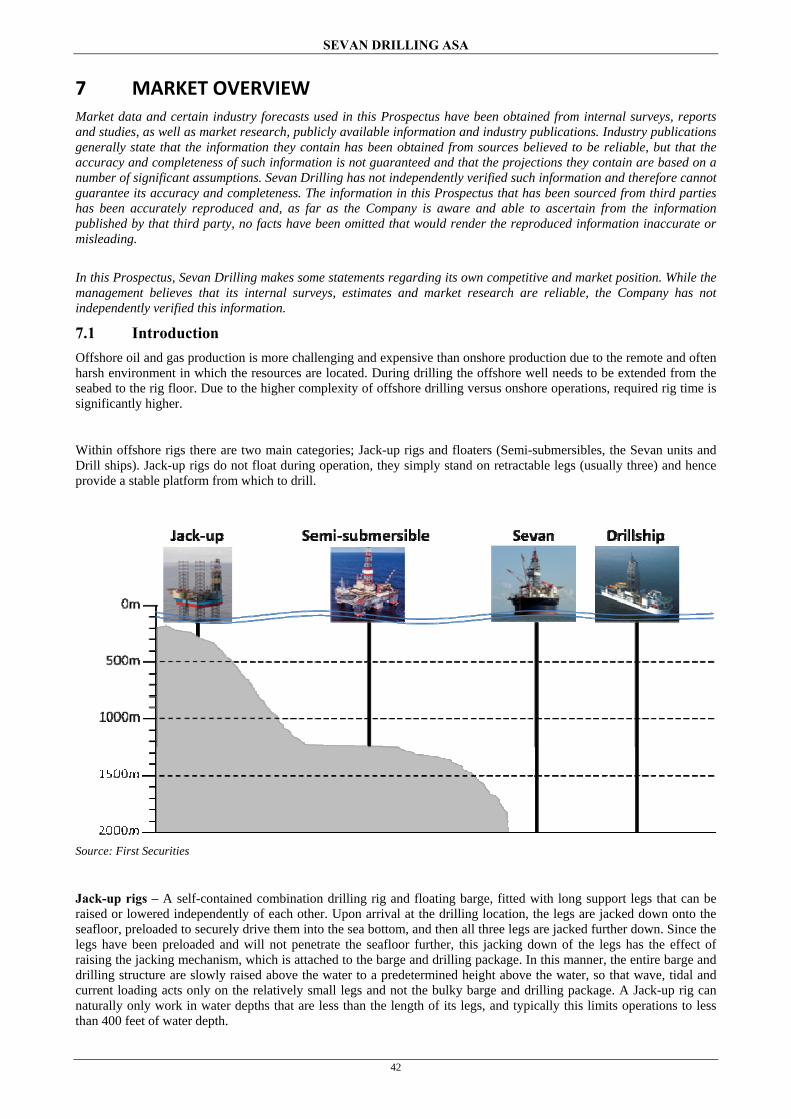

Sevan Marine has developed the cylinder shaped offshore floating unit (the “Sevan Unit”) based on the patented design and proprietary know-how held by Sevan Marine (the “Sevan Design”). Since 2001, Sevan Marine and its subsidiaries (the “Sevan Group”) have engaged in the design, building, owning and operation of units for floating production, storage and offloading of oil, as well as offshore drilling based its cylindrical design.

In February 2006, Sevan Marine announced its decision to pursue the development of ultra deepwater drilling units (the “Sevan Rig”) based on the Sevan Design as a separate business area within the Sevan Group. Since then, Sevan Drilling has become a fully integrated offshore drilling contractor with ownership of two ultra deepwater drilling units. The Company owns and operates Sevan Driller, which is one the world‘s most advanced, robust and “state-of-the-art” ultra deepwater drilling units. The Sevan Driller is of the Sevan 650 design and built for safe and efficient year-round operations in ultra deep waters worldwide. The Sevan Driller has been operating under a 6-year charter contract with Petrobras S.A (“Petrobras”) since June 2010 off the coast of Brazil. The second unit, the Sevan Brasil is under construction at the COSCO Qidong Shipyard, China (“COSCO”). The Sevan Brasil is also an ultra deepwater drilling unit of the Sevan 650 design, and is scheduled for delivery from the yard in the first quarter of 2012 and for commencement of a six-year charter contract with Petrobras in Brasil in the second quarter of 2012.

In March 2011, Sevan Drilling, through two wholly owned subsidiaries, entered into letters of intent with COSCO for the construction of two ultra deepwater drilling units, and options for two additional units of the same specifications, based on the Sevan 650 design. The Company estimates a price including project management, pre-delivery financing, capital spares, drilling tools and pre-operations) of approximately USD 525 million for each newbuild. The price for the two optional newbuilds will be the same, however, the price is subject to possible price adjustments for significant movements in exchange rates and prices of major equipment packages. Under the letters of intent, and provided binding construction contracts become effective as therein contemplated, the first firm newbuild shall be delivered in the fourth quarter of 2013, whereas the second firm newbuild shall be delivered in the second quarter of 2014. The first optional newbuild, assuming that the option is exercised (at the latest by first quarter 2012), shall be delivered in the fourth quarter of 2014, whereas the second optional newbuild, assuming that the option is exercised (at the latest by the third quarter of 2012), shall be delivered in the second quarter of 2015.

SEVAN DRILLING ASA

5

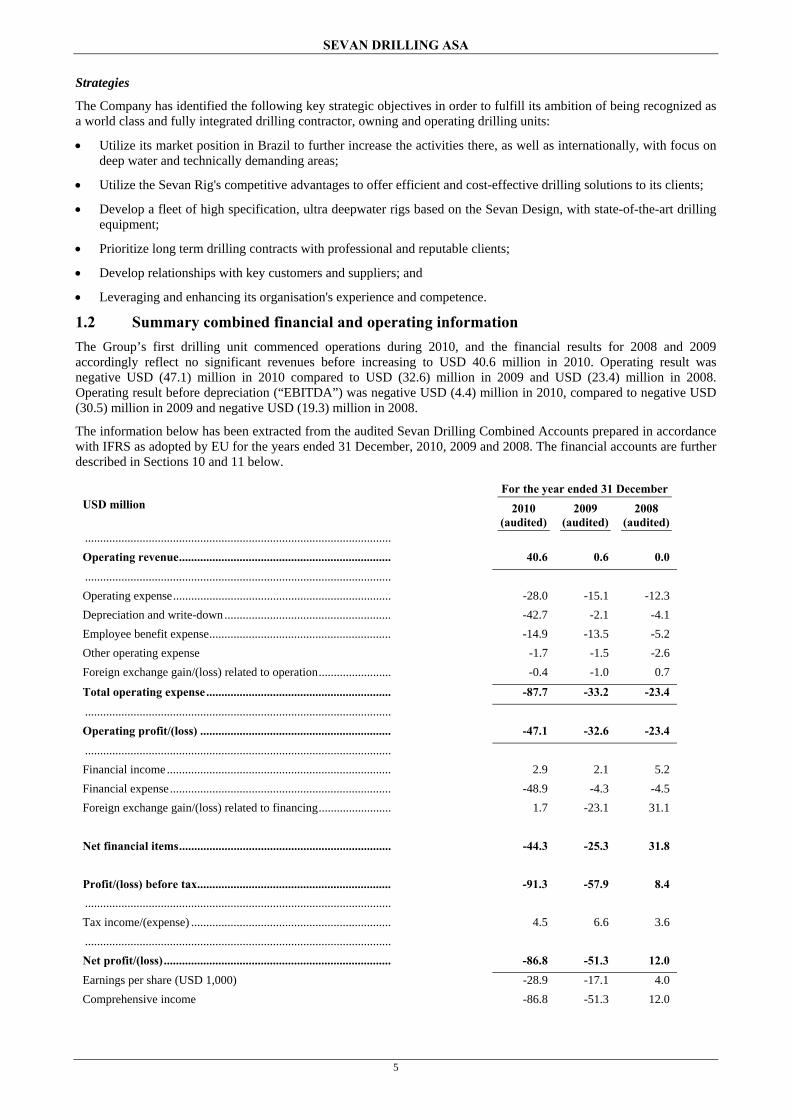

Strategies

The Company has identified the following key strategic objectives in order to fulfill its ambition of being recognized as a world class and fully integrated drilling contractor, owning and operating drilling units:

• Utilize its market position in Brazil to further increase the activities there, as well as internationally, with focus on deep water and technically demanding areas;

• Utilize the Sevan Rig's competitive advantages to offer efficient and cost-effective drilling solutions to its clients;

• Develop a fleet of high specification, ultra deepwater rigs based on the Sevan Design, with state-of-the-art drilling equipment;

• Prioritize long term drilling contracts with professional and reputable clients;

• Develop relationships with key customers and suppliers; and

• Leveraging and enhancing its organisation's experience and competence.

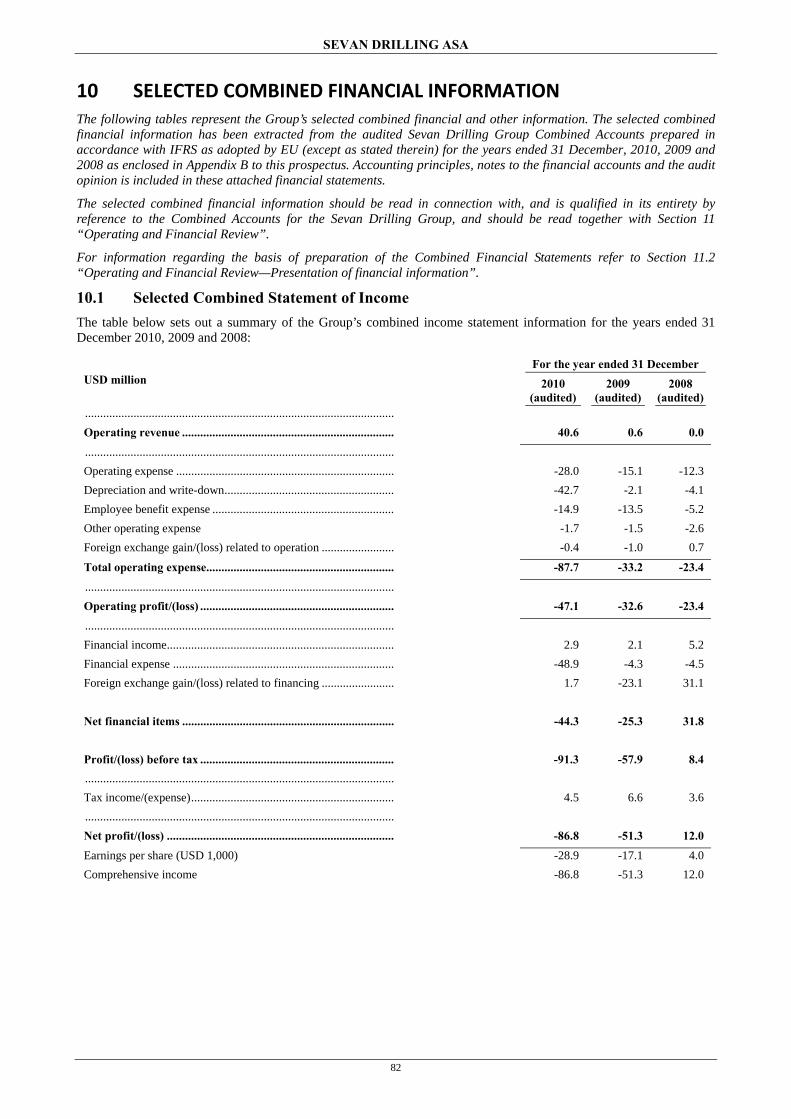

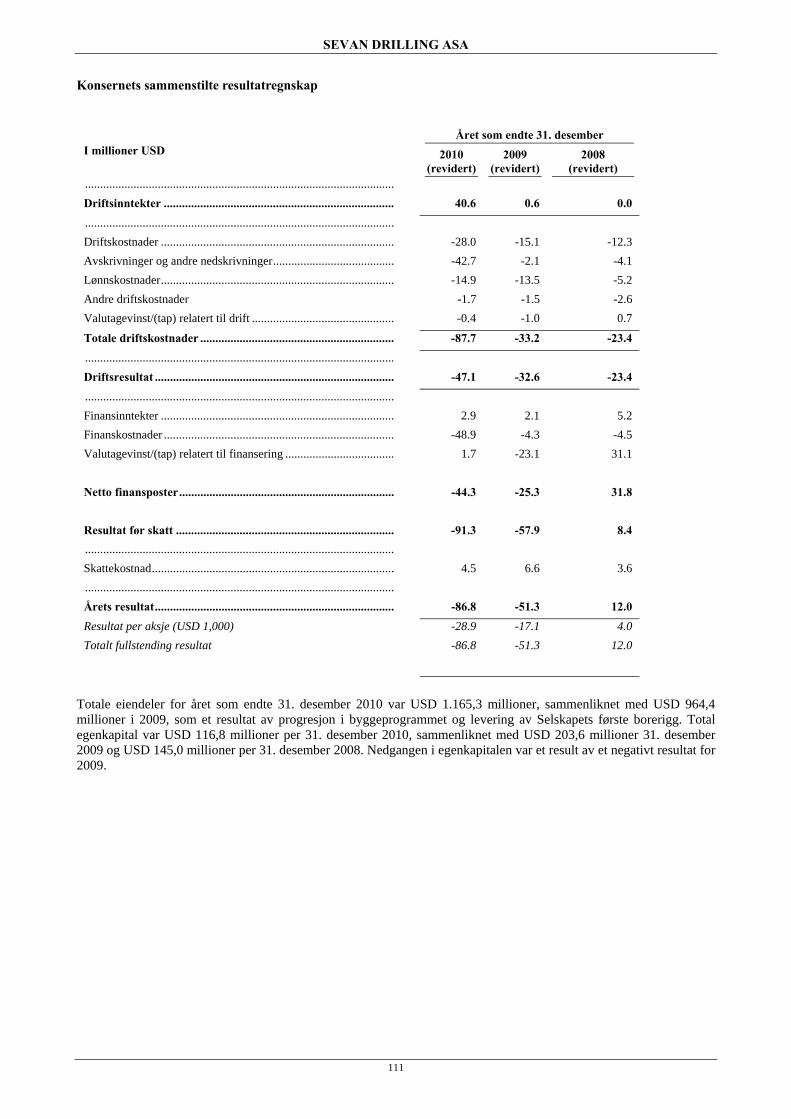

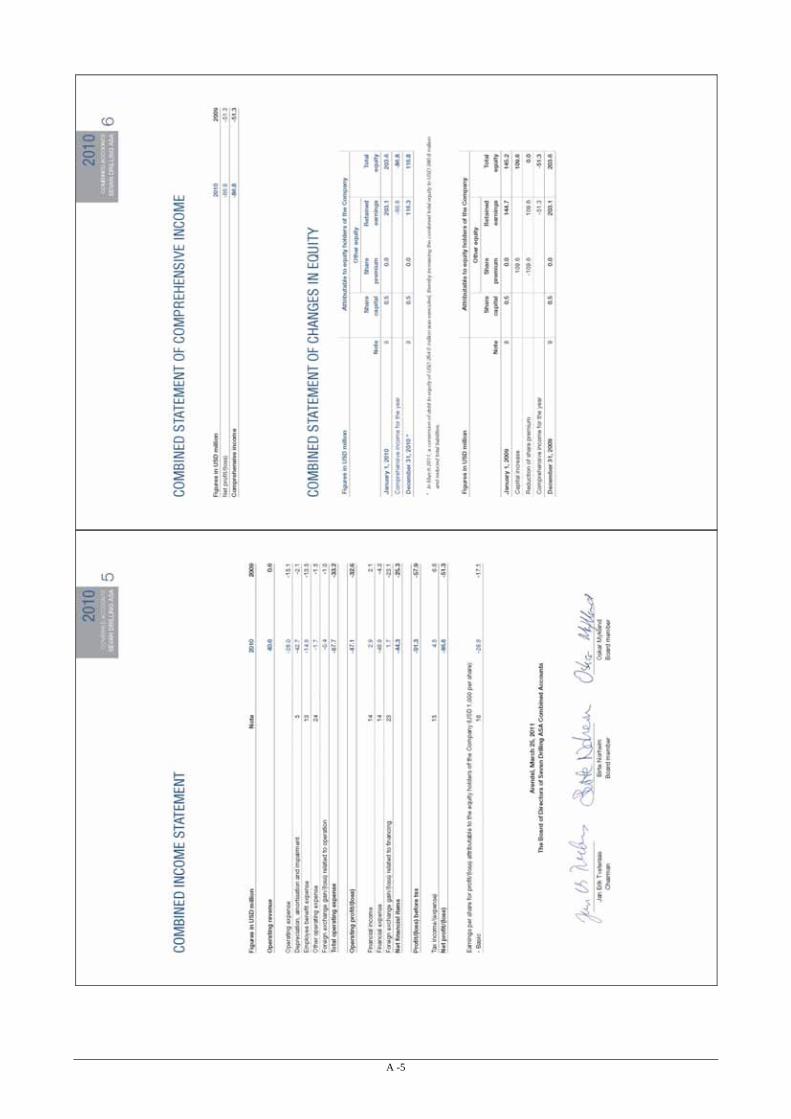

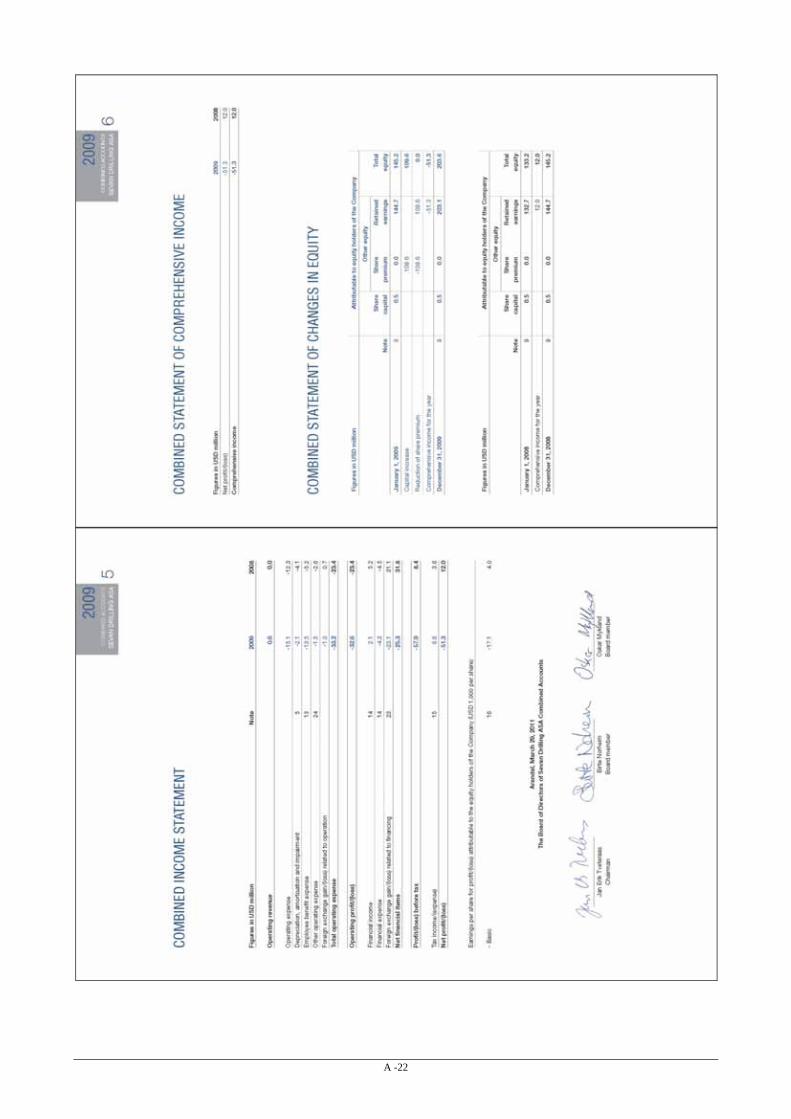

1.2 Summary combined financial and operating information The Group’s first drilling unit commenced operations during 2010, and the financial results for 2008 and 2009 accordingly reflect no significant revenues before increasing to USD 40.6 million in 2010. Operating result was negative USD (47.1) million in 2010 compared to USD (32.6) million in 2009 and USD (23.4) million in 2008. Operating result before depreciation (“EBITDA”) was negative USD (4.4) million in 2010, compared to negative USD (30.5) million in 2009 and negative USD (19.3) million in 2008.

The information below has been extracted from the audited Sevan Drilling Combined Accounts prepared in accordance with IFRS as adopted by EU for the years ended 31 December, 2010, 2009 and 2008. The financial accounts are further described in Sections 10 and 11 below.

Total operating expense ............................................................. -87.7 -33.2 -23.4 ..................................................................................................... Operating profit/(loss) ............................................................... -47.1 -32.6 -23.4 ..................................................................................................... Financial income .......................................................................... 2.9 2.1 5.2 Financial expense ......................................................................... -48.9 -4.3 -4.5 Foreign exchange gain/(loss) related to financing ........................

1.7 -23.1 31.1

Net financial items ......................................................................

-44.3 -25.3 31.8

Profit/(loss) before tax ................................................................ -91.3 -57.9 8.4 ..................................................................................................... Tax income/(expense) .................................................................. 4.5 6.6 3.6 ..................................................................................................... Net profit/(loss) ........................................................................... -86.8 -51.3 12.0 Earnings per share (USD 1,000) Comprehensive income

-28.9 -86.8

-17.1 -51.3

4.0 12.0

SEVAN DRILLING ASA

6

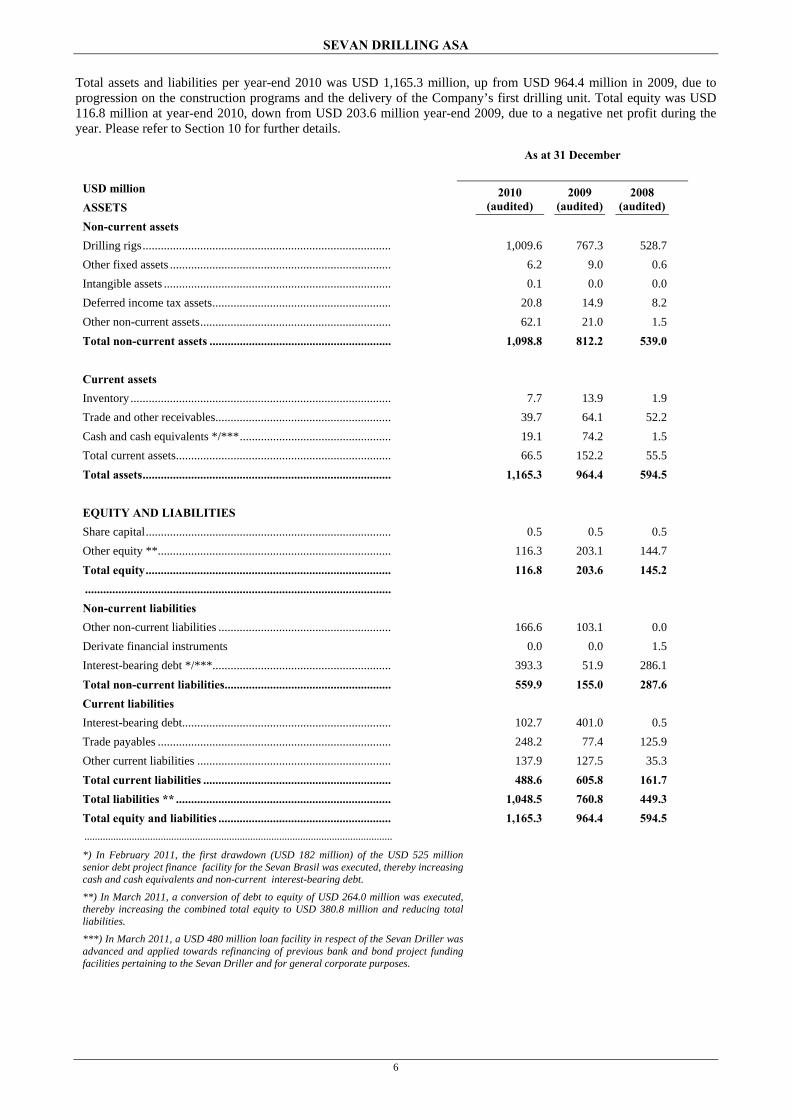

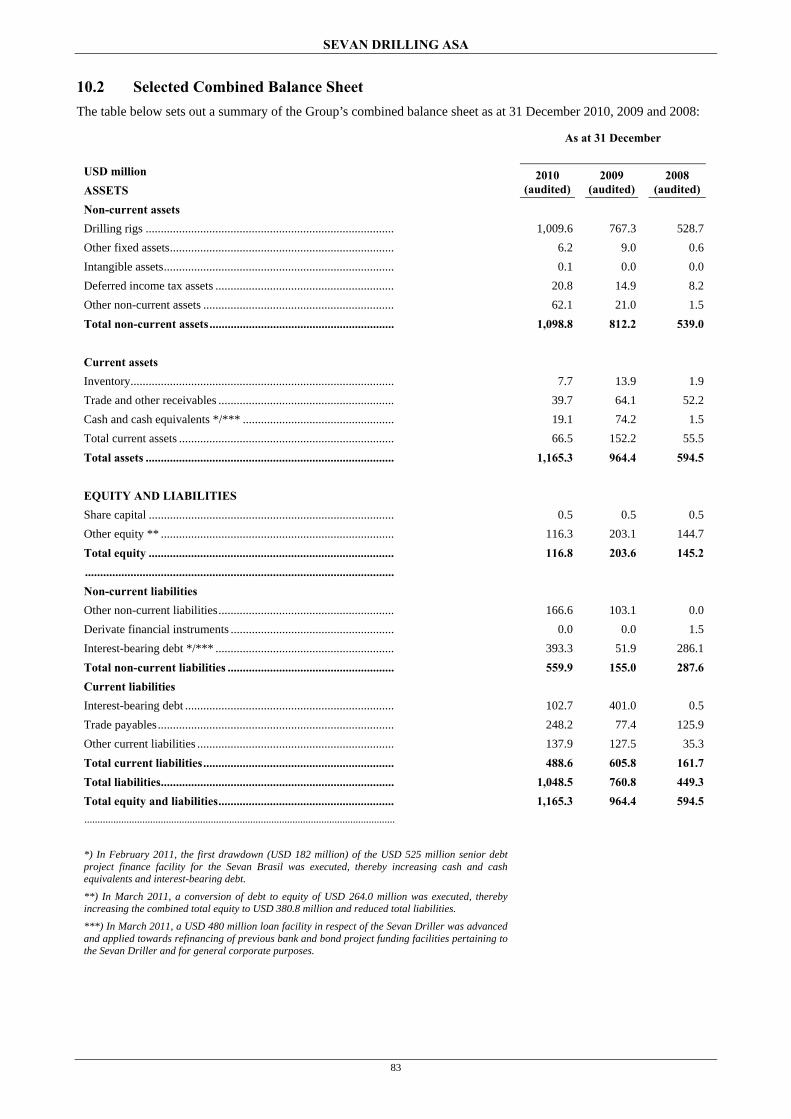

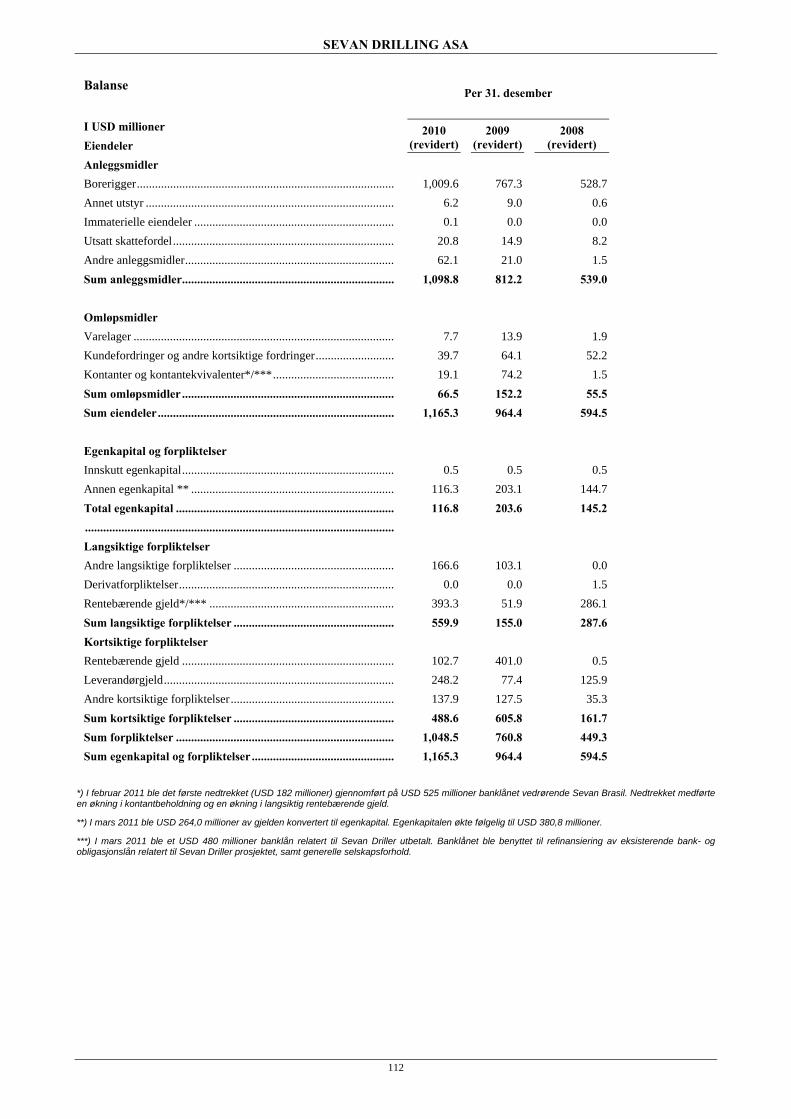

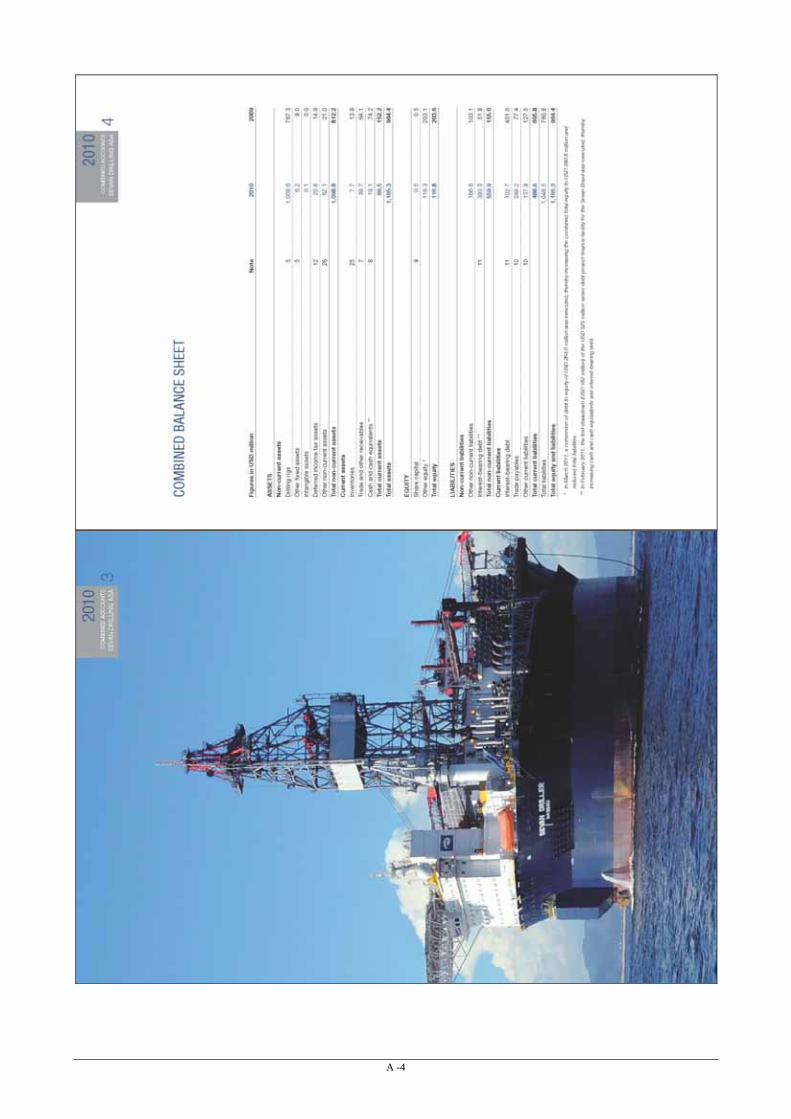

Total assets and liabilities per year-end 2010 was USD 1,165.3 million, up from USD 964.4 million in 2009, due to progression on the construction programs and the delivery of the Company’s first drilling unit. Total equity was USD 116.8 million at year-end 2010, down from USD 203.6 million year-end 2009, due to a negative net profit during the year. Please refer to Section 10 for further details.

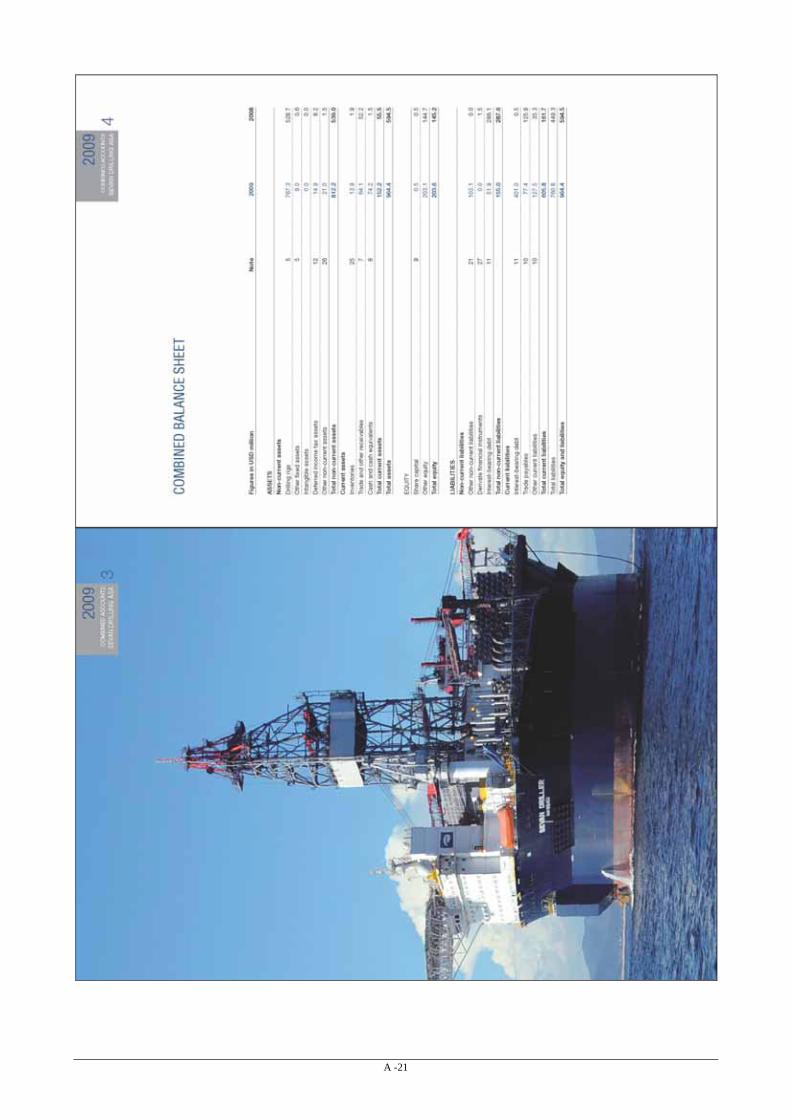

As at 31 December

USD million ASSETS Non-current assets

2010 (audited)

2009 (audited)

2008 (audited)

Drilling rigs .................................................................................. 1,009.6 767.3 528.7 Other fixed assets ......................................................................... 6.2 9.0 0.6 Intangible assets ........................................................................... 0.1 0.0 0.0 Deferred income tax assets ........................................................... 20.8 14.9 8.2 Other non-current assets ............................................................... 62.1 21.0 1.5 Total non-current assets ............................................................ Current assets

1,098.8 812.2 539.0

Inventory ...................................................................................... 7.7 13.9 1.9 Trade and other receivables .......................................................... 39.7 64.1 52.2 Cash and cash equivalents */*** .................................................. 19.1 74.2 1.5 Total current assets ....................................................................... 66.5 152.2 55.5 Total assets .................................................................................. EQUITY AND LIABILITIES

1,165.3 964.4 594.5

Share capital ................................................................................. 0.5 0.5 0.5 Other equity **............................................................................. 116.3 203.1 144.7 Total equity ................................................................................. 116.8 203.6 145.2 ..................................................................................................... Non-current liabilities

Other non-current liabilities ......................................................... 166.6 103.1 0.0 Derivate financial instruments 0.0 0.0 1.5 Interest-bearing debt */*** ........................................................... 393.3 51.9 286.1 Total non-current liabilities ....................................................... Current liabilities

559.9 155.0 287.6

Interest-bearing debt..................................................................... 102.7 401.0 0.5 Trade payables ............................................................................. 248.2 77.4 125.9 Other current liabilities ................................................................ 137.9 127.5 35.3 Total current liabilities .............................................................. 488.6 605.8 161.7 Total liabilities ** ....................................................................... 1,048.5 760.8 449.3 Total equity and liabilities ......................................................... 1,165.3 964.4 594.5 .....................................................................................................................

*) In February 2011, the first drawdown (USD 182 million) of the USD 525 million senior debt project finance facility for the Sevan Brasil was executed, thereby increasing cash and cash equivalents and non-current interest-bearing debt.

**) In March 2011, a conversion of debt to equity of USD 264.0 million was executed, thereby increasing the combined total equity to USD 380.8 million and reducing total liabilities.

***) In March 2011, a USD 480 million loan facility in respect of the Sevan Driller was advanced and applied towards refinancing of previous bank and bond project funding facilities pertaining to the Sevan Driller and for general corporate purposes.

SEVAN DRILLING ASA

7

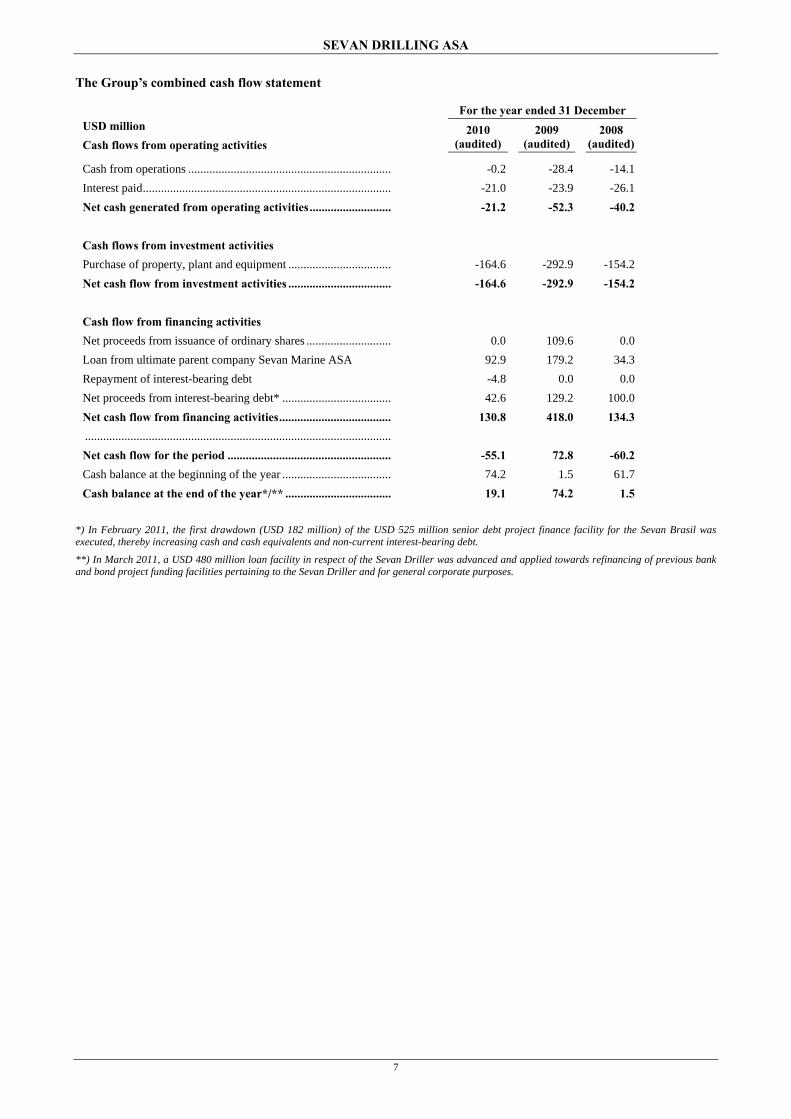

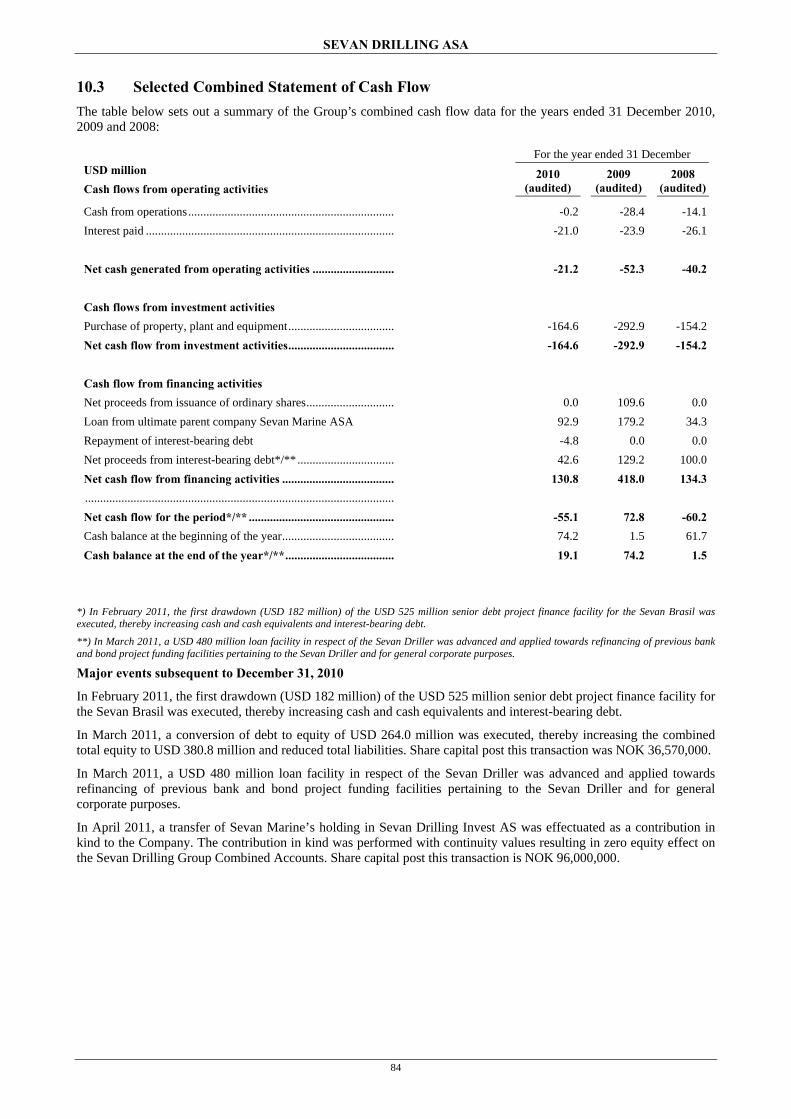

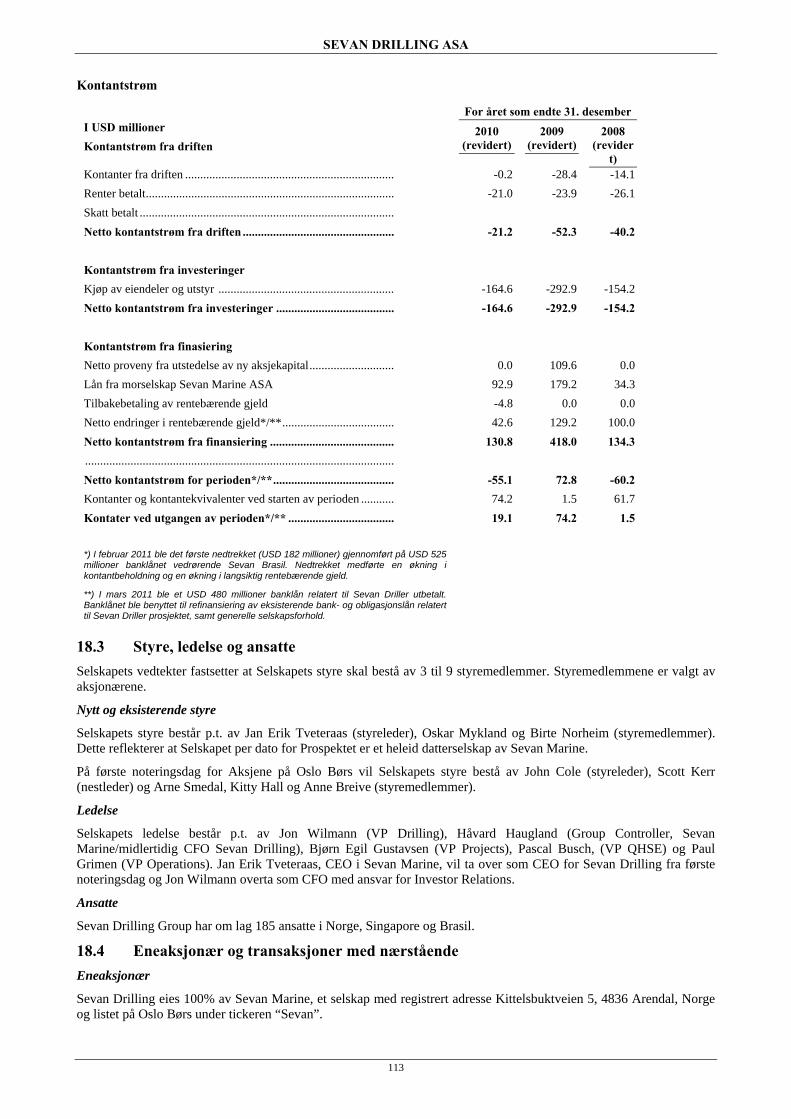

The Group’s combined cash flow statement

For the year ended 31 December USD million Cash flows from operating activities

2010 (audited)

2009 (audited)

2008 (audited)

Cash from operations ................................................................... -0.2 -28.4 -14.1 Interest paid .................................................................................. -21.0 -23.9 -26.1 Net cash generated from operating activities ........................... Cash flows from investment activities

-21.2 -52.3 -40.2

Purchase of property, plant and equipment .................................. -164.6 -292.9 -154.2 Net cash flow from investment activities .................................. Cash flow from financing activities

-164.6 -292.9 -154.2

Net proceeds from issuance of ordinary shares ............................ 0.0 109.6 0.0 Loan from ultimate parent company Sevan Marine ASA 92.9 179.2 34.3 Repayment of interest-bearing debt -4.8 0.0 0.0 Net proceeds from interest-bearing debt* .................................... 42.6 129.2 100.0 Net cash flow from financing activities ..................................... 130.8 418.0 134.3 ..................................................................................................... Net cash flow for the period ...................................................... -55.1 72.8 -60.2 Cash balance at the beginning of the year .................................... 74.2 1.5 61.7 Cash balance at the end of the year*/** ................................... 19.1 74.2 1.5

*) In February 2011, the first drawdown (USD 182 million) of the USD 525 million senior debt project finance facility for the Sevan Brasil was executed, thereby increasing cash and cash equivalents and non-current interest-bearing debt.

**) In March 2011, a USD 480 million loan facility in respect of the Sevan Driller was advanced and applied towards refinancing of previous bank and bond project funding facilities pertaining to the Sevan Driller and for general corporate purposes.

SEVAN DRILLING ASA

8

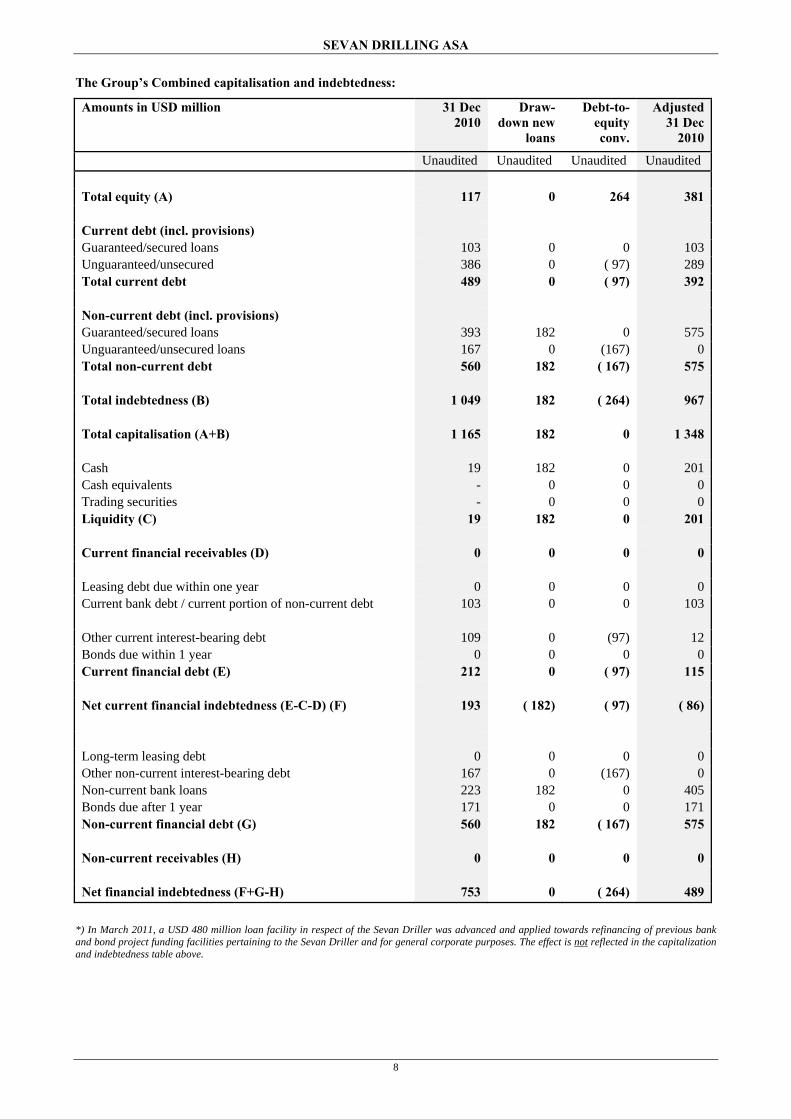

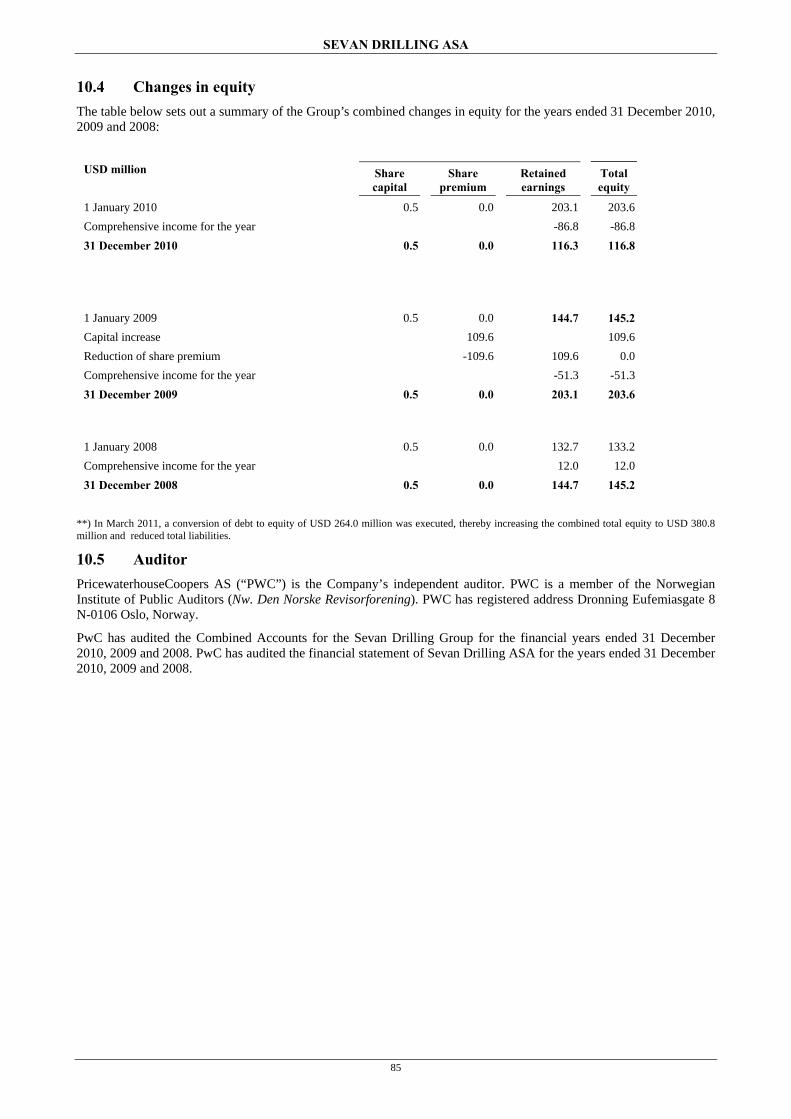

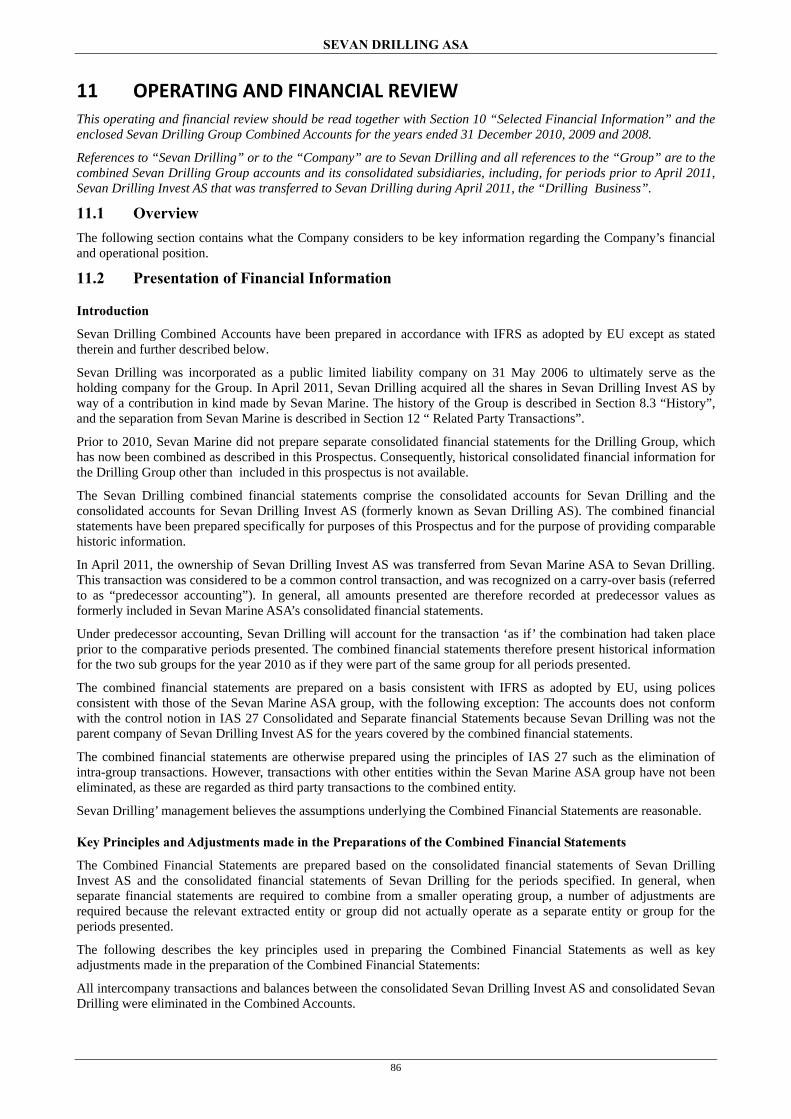

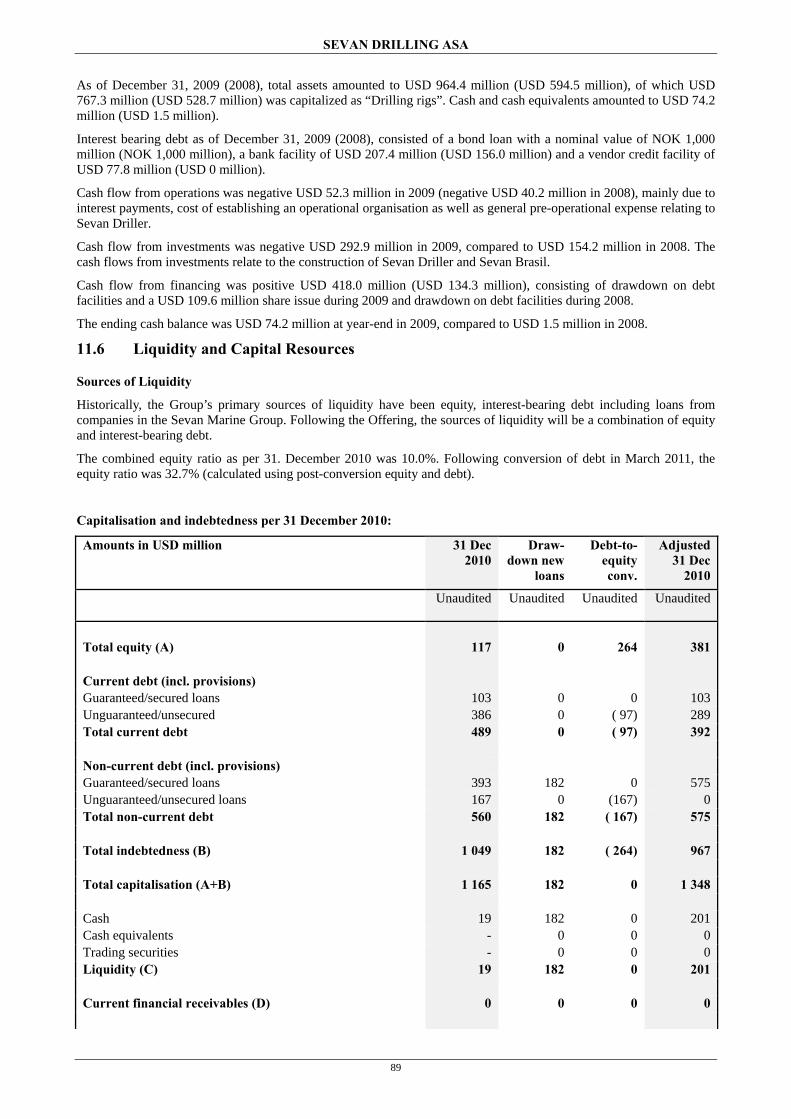

The Group’s Combined capitalisation and indebtedness:

Amounts in USD million 31 Dec 2010

Draw-down new

loans

Debt-to-equity conv.

Adjusted 31 Dec

2010

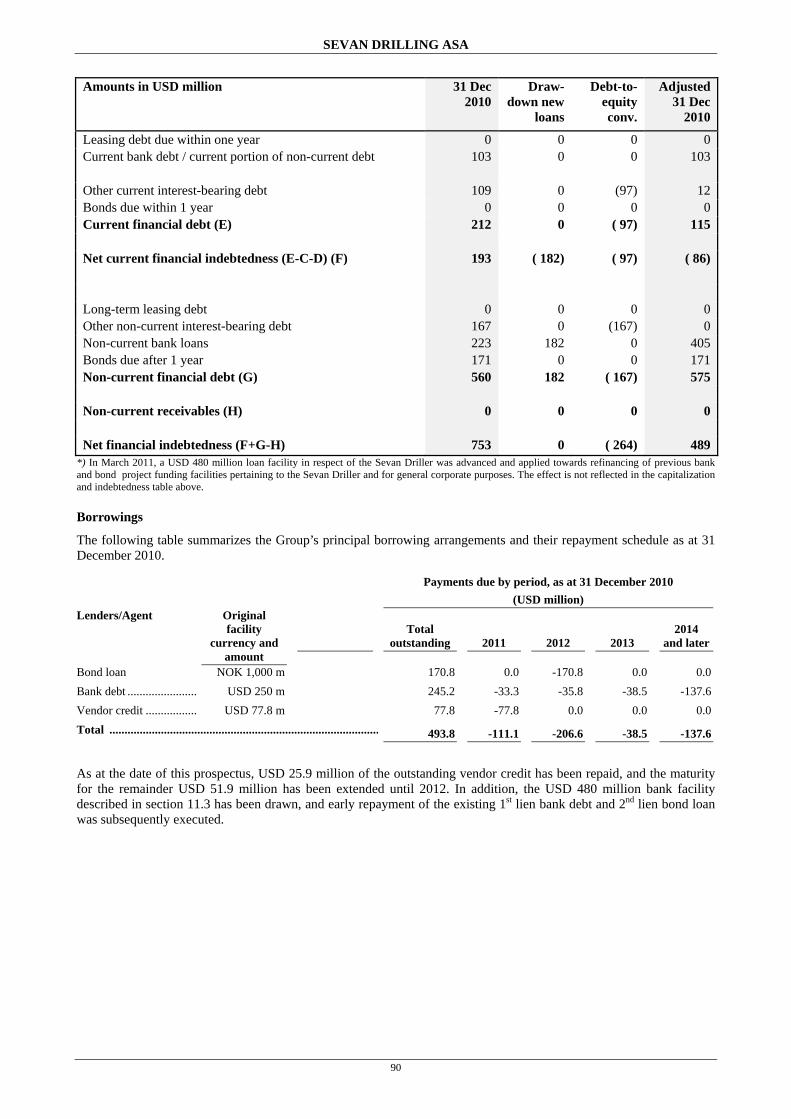

Unaudited Unaudited Unaudited Unaudited Total equity (A) 117 0 264 381 Current debt (incl. provisions) Guaranteed/secured loans 103 0 0 103Unguaranteed/unsecured 386 0 ( 97) 289Total current debt 489 0 ( 97) 392 Non-current debt (incl. provisions) Guaranteed/secured loans 393 182 0 575Unguaranteed/unsecured loans 167 0 (167) 0Total non-current debt 560 182 ( 167) 575 Total indebtedness (B) 1 049 182 ( 264) 967 Total capitalisation (A+B) 1 165 182 0 1 348 Cash 19 182 0 201Cash equivalents - 0 0 0Trading securities - 0 0 0Liquidity (C) 19 182 0 201 Current financial receivables (D) 0 0 0 0 Leasing debt due within one year 0 0 0 0Current bank debt / current portion of non-current debt 103 0 0 103

Other current interest-bearing debt 109 0 (97) 12Bonds due within 1 year 0 0 0 0Current financial debt (E) 212 0 ( 97) 115 Net current financial indebtedness (E-C-D) (F) 193 ( 182) ( 97) ( 86)

*) In March 2011, a USD 480 million loan facility in respect of the Sevan Driller was advanced and applied towards refinancing of previous bank and bond project funding facilities pertaining to the Sevan Driller and for general corporate purposes. The effect is not reflected in the capitalization and indebtedness table above.

SEVAN DRILLING ASA

9

Major events subsequent to December 31, 2010

In February 2011, the Sevan Drilling Group made a drawdown of USD 182 million under the USD 525 million construction financing facility for the Sevan Brasil as described in Sections 11.3 and 12.

In March 2011, conversions of debt to Sevan Marine amounting to USD 264 million was effected, thereby increasing the equity ratio to approximately 32% following the conversion.

In April 2011, a transfer of Sevan Marine’s holding in Sevan Drilling Invest AS (formerly Sevan Drilling AS) AS was effected as a contribution in kind to the Company. The contribution in kind was performed with continuity values resulting in zero equity effect on the Sevan Drilling Group Combined Accounts.

In March 2011, a USD 480 million loan facility in respect of the Sevan Driller was advanced and applied towards refinancing of previous bank and bond project funding facilities pertaining to the Sevan Driller and for general corporate purposes.

Trends

Except as otherwise disclosed in this Prospectus, the draw-down of new loans (described in Section 1.2), the share capital increase (described in Section 1.2) and the announcement of the planned Offering (described in Section 1.7), there have been no significant changes in the financial or trading position of the Group since the date of its latest financial information included in this Prospectus.

1.3 Board of Directors, senior management and employees The Company’s Articles of Association provide that the Board of Directors shall consist of 3 to 9 Directors. The Directors are elected by the shareholders.

New and current Board of Directors

The Company’s Board of Directors currently consists of Jan Erik Tveteraas (Chairman), Oskar Mykland and Birte Norheim (Board members), reflecting that as at the date of this Prospectus, the Company is a wholly-owned subsidiary of Sevan Marine.

As of the first day of trading of the Shares on Oslo Børs, the Company’s Board of Directors will consist of Jon C. Cole (Chairman), Scott I. Kerr (Deputy Chairman), Arne Smedal, Kitty Hall and Anne Breive (Board members). In addition, by such date two directors nominated by the employees will have been elected.

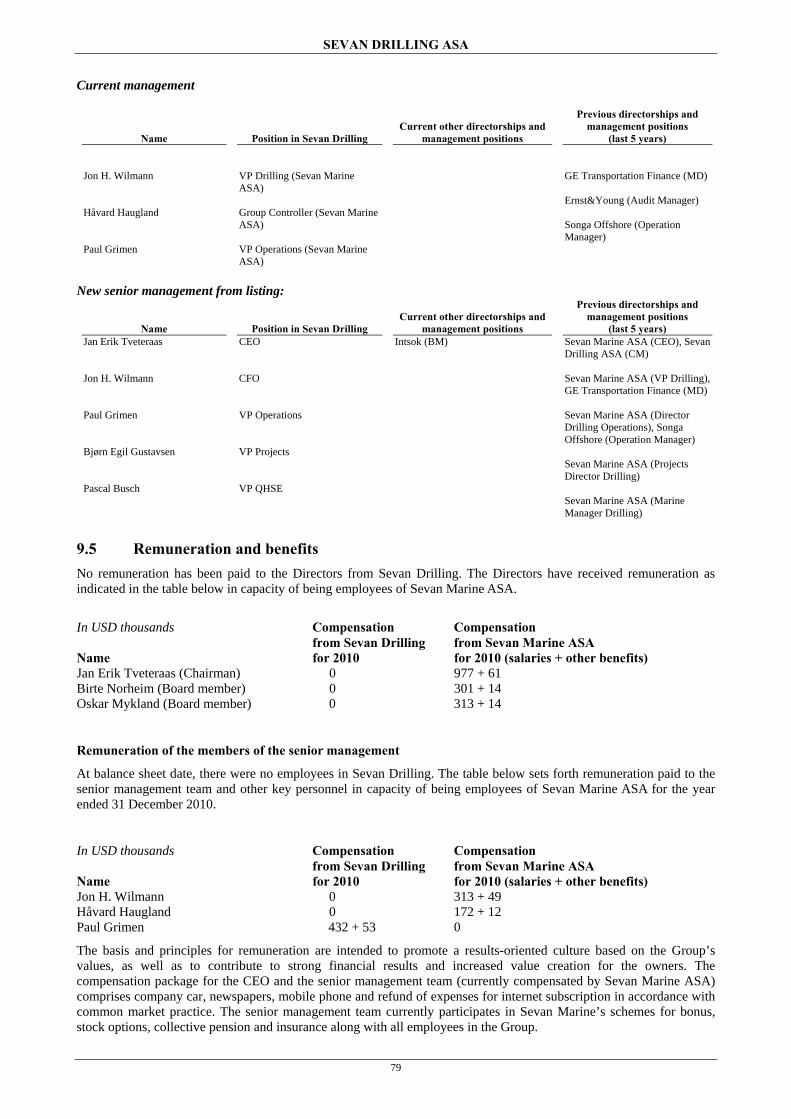

Senior management

The senior management of the Company currently consists of Jon H. Wilmann (VP Drilling), Håvard Haugland (Group Controller, Sevan Marine/Interim CFO, Sevan Drilling) and Paul Grimen (VP Operations).

As of the first day of trading of the Shares on Oslo Børs, Jan Erik Tveteraas will have been appointed CEO, and Jon H. Wilmann will have been appointed CFO, with IR responsibility as part of the job description. Bjørn Egil Gustavsen (VP Projects) and Pascal Busch (VP QHSE) will supplement the senior management team, together with Mr. Grimen. The Norwegian employees will be employed by the Company’s wholly-owned subsidiary Sevan Drilling Management AS, which will provide services under a management agreement.

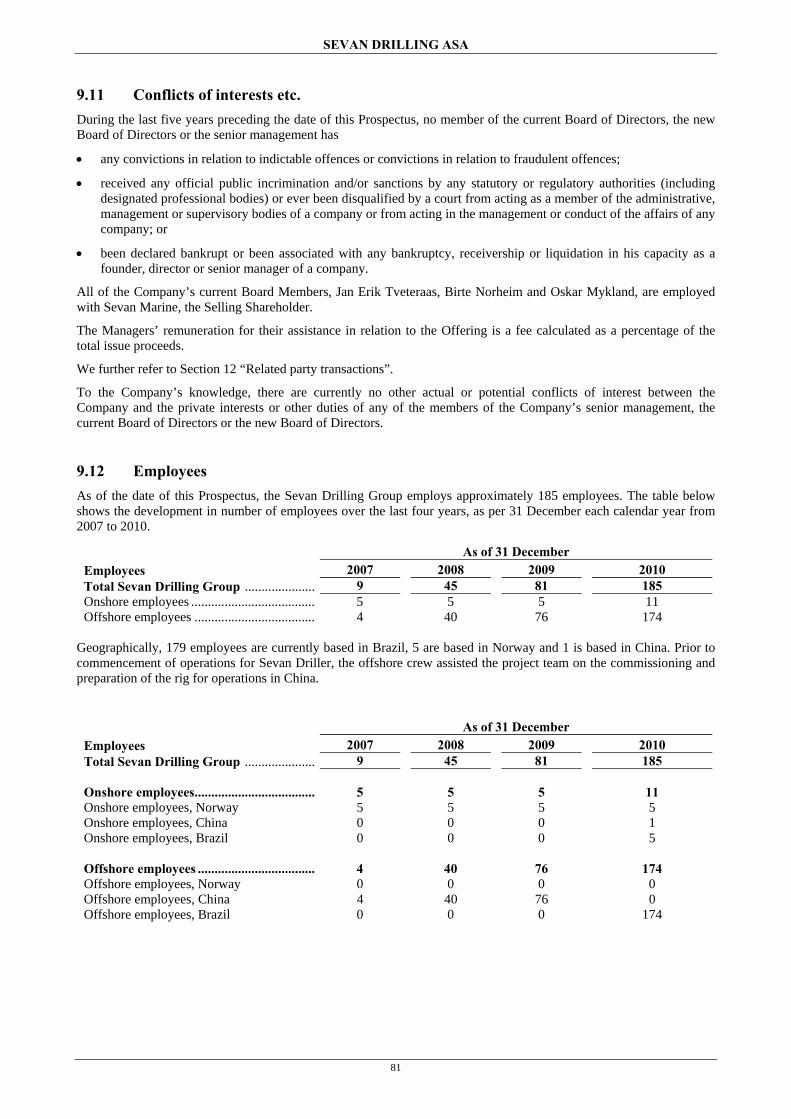

Employees

The Sevan Drilling Group employs approximately 185 employees in Norway, Singapore and Brazil.

1.4 Sole shareholder and related party transactions Sole shareholder

Sevan Drilling is 100% owned by Sevan Marine, a company with registered address at Kittelsbuktveien 5, 4836 Arendal, Norway, and listed on the Oslo Stock Exchange with ticker “Sevan”.

Related party transactions

The Group has in the period covered by the Financial Statements included herein been subject to various related party transactions with Sevan Marine and companies in which Sevan Marine exerts considerable influence. For further information of the Group’s related party transactions, see Section 12 “Related Party Transactions” below in this Prospectus.

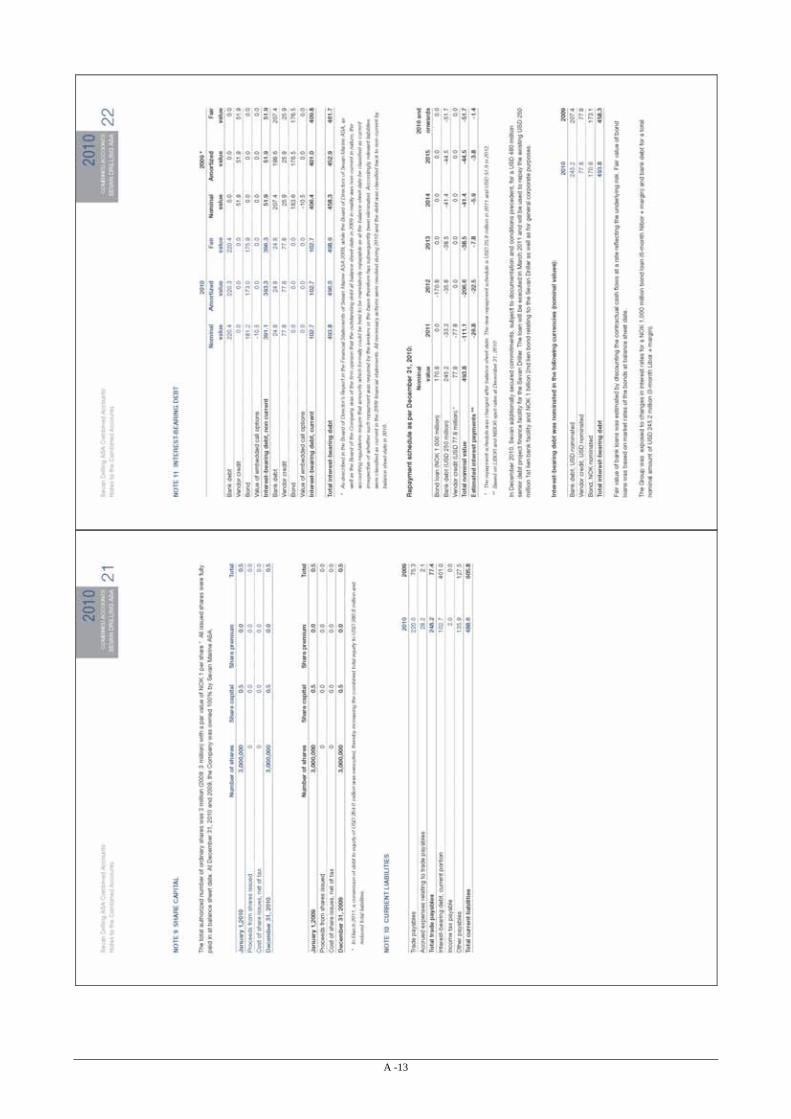

1.5 Share capital As at the date of this Prospectus, the Company’s share capital is NOK 96,000,000, divided into 96,000,000 Shares, each Share with a par value of NOK 1.00. All Shares in the Company are of the same class and vested with equal rights in all respects. The Shares have all been validly issued and are fully paid.

SEVAN DRILLING ASA

10

1.6 Articles of association The Articles of Association of the Company (or a translation from Norwegian thereof) are included as Appendix A to this Prospectus.

1.7 Summary of the Offering The following table summarizes, and provides certain indicative key dates for, the Offering.

The Offering .............................................. The Offering is an offering of up to NOK 3,270 million (~USD 595 million) through an offering of a number of Shares to be determined in conjunction with determination of the final Offer Price, consisting of an Institutional Offering, a Retail Offering, and an Employee Offering. The Offering comprises between 92 million and 120 million new Shares (the “New Shares”) offered and issued by the Company and 64 million existing Shares (the “Existing Shares”) to be sold by the Selling Shareholder, thus aggregating a total of between 156 million and 184 million Offer Shares, excluding any Additional Shares.

Institutional Offering ................................. In the Institutional Offering, Offer Shares are being offered to institutional investors and professional investors in Norway and outside Norway and the United States in reliance on Regulation S under the US Securities Act, and in the United States to a limited number of QIBs in reliance on Rule 144A under the US Securities Act, subject to a lower limit per order of NOK 1,000,000.

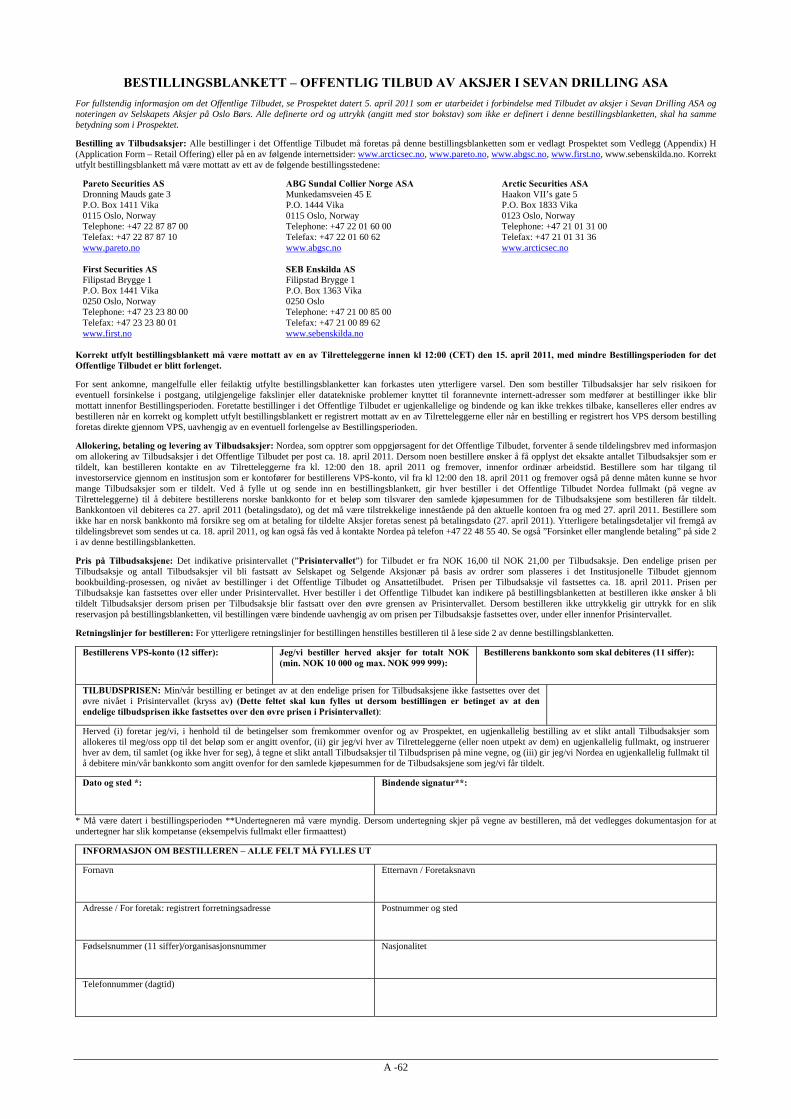

Retail Offering .......................................... In the Retail Offering, Offer Shares are being offered to the public in Norway subject to a lower limit per application of an amount of NOK 10,000 and an upper limit per application of an amount of NOK 999,999 for each investor.

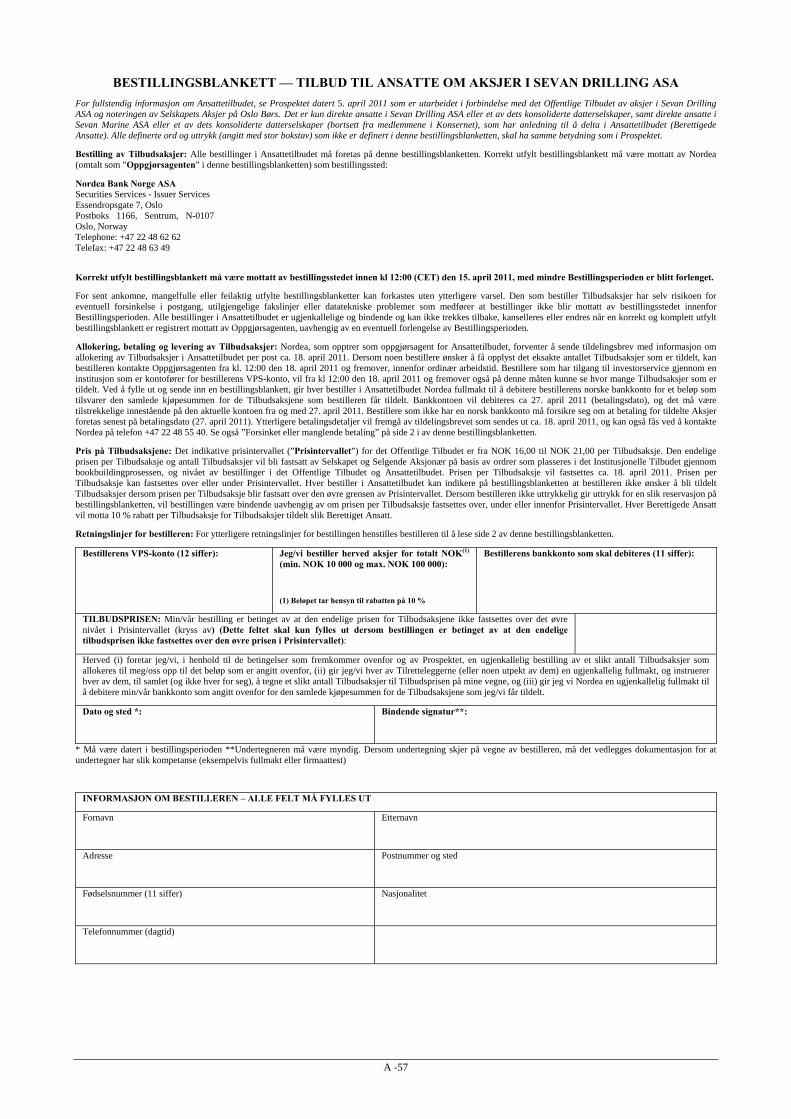

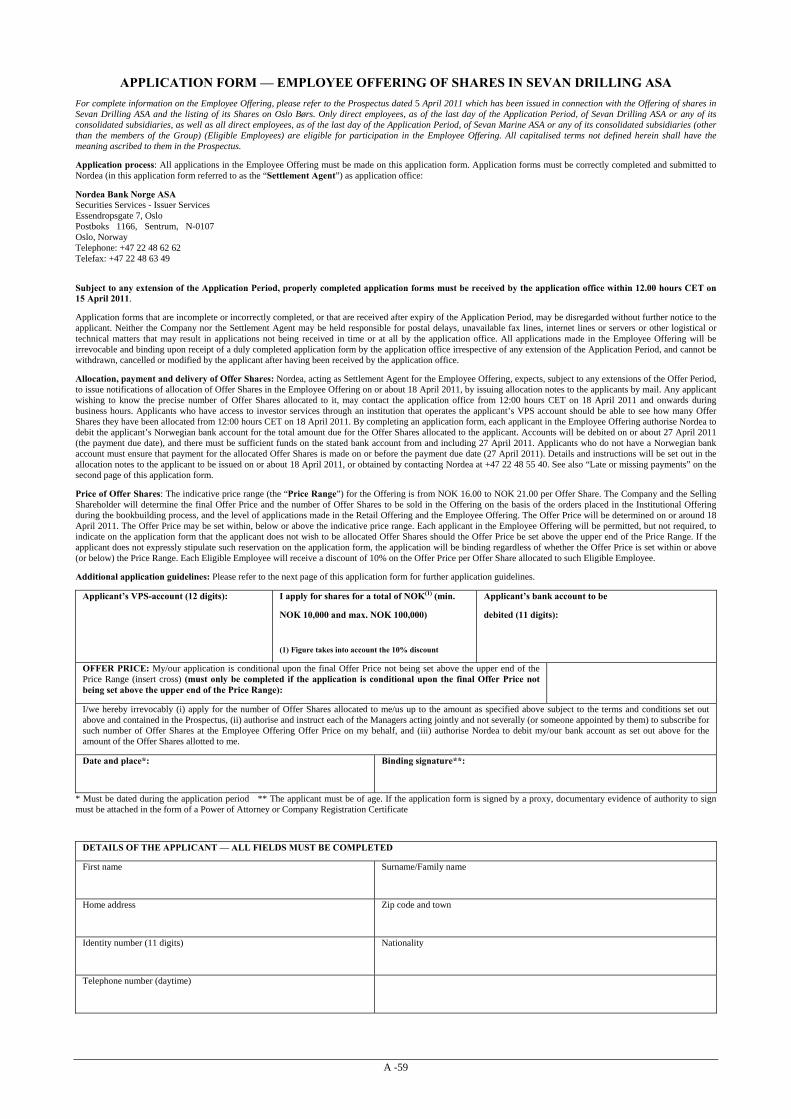

Employee Offering In the Employee Offering, Offer Shares are being offered to Eligible Employees (as defined herein), subject to a lower limit per application of an amount of NOK 10,000 and an upper limit per application of an amount of NOK 100,000 (in each case after deduction of the discount). Each Eligible Sevan Drilling Employee will receive a discount of 10% of the Offer Price per Offer Share allocated to such employee. For a brief description of the Norwegian tax effects of such discount, please see Section 16.3 below.

Additional Shares ...................................... The Selling Shareholder has granted the Managers an option to purchase, at the Offer Price, up to 13 million Additional Shares (but not exceeding 10% of the number of Offer Shares initially allocated in the Offering) to cover over-allotments in connection with the Offering and short positions, if any, exercisable within a 30-day period commencing at the time trading in the Shares on Oslo Børs.

Bookbuilding Period .................................. The Bookbuilding Period for the Institutional Offering is expected to take place from 09:00 hours (CET) on 5 April 2011 to 17:30 hours on 15 April 2011, subject to extensions.

Application Period ..................................... The period in which applications for Offer Shares will be accepted in the Retail Offering and the Employee Offering will last from 09:00 hours (CET) on 5 April 2011 to 12:00 hours (CET) on 15 April 2011, subject to extensions.

Indicative price range ................................ From NOK 16.00 to NOK 21.00 per Offer Share.

Notification of allocation ........................... On or about 18 April 2011.

Payment of Offer Shares ............................ On or about 27 April 2011.

Delivery of Offer Shares ............................ On or about 28 April 2011.

Admission to trading of the Shares ............ It is expected that trading in the Shares will commence on Oslo Børs on 29 April 2011.

Use of proceeds ......................................... The net proceeds from the offering of New Shares will be used (i) to finance the initial instalments equal to 20% of the contract price for the first two newbuilds at COSCO, (ii) working capital reserve for the newbuild rigs and (iii) for general corporate purposes.

SEVAN DRILLING ASA

11

Dilution ...................................................... Assuming sale of 168 million Offer Shares in the Offering (the number of Offer Shares to be issued at the mid-point of the indicative price range plus the 64 million Offer Shares offered by the Selling Shareholder (not including the sale of any Additional Shares)), Sevan Marine’s ownership in the Company will be reduced from 100% to approximately 16%.

Expenses .................................................... Sevan Drilling estimates that the total expenses in connection with the Offering (inclusive of commission payable by the Company to the Managers, but excluding any discretionary commission) and the listing of its Shares on Oslo Børs will amount to approximately NOK 120 million (of which the Company will cover NOK 75 million).

ISIN ........................................................... NO 001 0455793

Oslo Børs trading symbol ......................... The Shares are expected to trade under the trading symbol “SDRILL”.

1.8 Documents on display Copies of the following documents will be available for inspection at the Company’s registered office during normal business hours from Monday to Friday each week (except public holidays) for a period of twelve months from the date of this Prospectus:

• the Articles and Memorandum of Association of the Company;

• the Combined Accounts for Sevan Drilling Group, and the financial statements of the Sevan Drilling ASA as of and for years ended 31 December 2010, 2009 and 2008;

• all reports included or referred to in this Prospectus; and

• this Prospectus.

1.9 Advisors and auditors Advisors

Pareto Securities AS is engaged as Global Coordinator. Pareto Securities AS, ABG Sundal Collier Norge ASA, Arctic Securities ASA, First Securities AS, ING Bank N.V and SEB Enskilda AS act as Joint Lead Managers and Joint Bookrunners for the Offering.

Bugge, Arentz-Hansen & Rasmussen (BA-HR) has acted as legal advisor to the Company as to Norwegian law. Wiersholm has acted as Norwegian legal advisor to the Managers, and Akin Gump Strauss Hauer & Feld LLP has acted as the Managers’ US legal advisor in connection with the Offering. Deloitte has acted as financial due diligence advisor to the Managers.

Auditor

PricewaterhouseCoopers AS (“PwC”) is the Company’s independent auditor. PwC is a member of the Norwegian Institute of Public Auditors (Nw. Den Norske Revisorforening).

1.10 Summary of risk factors Investing in the Shares involves inherent risks. Before deciding whether or not to participate in the Offering, an investor should consider carefully all of the information set forth in this Prospectus, and in particular, the specific risk factors set out below. An investment in the Shares is suitable only for investors who understand the risk factors associated with this type of investment and who can afford a loss of all or part of the investment.

If any of the risks described below materialize, individually or together with other circumstances, they may have a material adverse effect on the Group’s business, financial condition, results of operations and cash flow, which may cause a decline in the value and trading price of the Shares that could result in a loss of all or part of any investment in the Shares.

The risks and uncertainties described below are not the only ones faced by the Group. Additional risks and uncertainties that the Company currently believes are immaterial, unlikely or that are not presently known to the Company may also have a material adverse effect on its business, financial condition, results of operations and cash flow.

The order in which the risks are presented below is not intended to provide an indication of the likelihood of their occurrence nor of their severity or significance. These risks should also be considered in connection with the cautionary statement regarding forward-looking information set forth in Section 4 below.

SEVAN DRILLING ASA

12

Risks relating to the industry in which the Group operates:

• The offshore contract drilling industry, which is capital intensive, is also cyclical, with volatile demand and day rates. The business, financial condition, and results of operations for drilling rig owners and operators depend on the level of activity in the offshore oil and gas industry, which is significantly affected by, among other things, volatile oil and gas prices and may be materially and adversely affected by a decline in offshore oil and gas exploration, development and production.

• Uncertainty relating to the development of the world economy may affect the oil price in general and/or reduce demand for drilling services or result in contract delays or cancellations.

• An over-supply of drilling units may lead to a reduction in dayrates, which are the amounts earned per day per drilling unit, which may materially impact the competition between and/or the profitability of rig owners.

• The market value of drilling units may decrease, which could cause rig owners to incur losses in case of sale of drilling rigs following a decline in their market values, and may result in lower day rates on subsequent charter contracts.

• Consolidation of suppliers may limit availability of supplies and services when needed, at an acceptable cost, or at all.

• Governmental laws and regulations could affect the operations of rig owners, increase their operating costs, reduce demand for drilling services and/or restrict the ability of rig owners to operate the drilling units or otherwise adversely affect their operational or financial condition.

• Rig owners may be subject to liability under environmental laws and regulations, which could have a material adverse effect on their results or operations and financial condition.

• The drilling s business involves numerous operating hazards.

• Rig owners may be subject to litigation that could have an adverse effect on their financial condition.

• Technology disputes involving rig owners, their suppliers or sub-suppliers could impact their operations or increase operating costs.

• Competition within the oilfield services industry is fierce and may adversely affect rig owners’ ability to market their services and/or secure profitable employment.

• Uncertainty relating to the development of the world economy may reduce demand for drilling services or result in contract delays or cancellations.

• The drilling units may, from time to time, operate in various jurisdictions exposing the relevant owners and operators to additional risks.

• Tax rules may change or new tax rules may be introduced, or the application of existing rules may change all of which could materially and adversely affect the profitability of the drilling business.

• Risk of war and/or terrorist attacks.

Risks relating to the Group:

• The Group currently has only one customer (Petrobras) and operates in one country only (Brazil).

• The letters of intent with COSCO for two newbuilds remain to be converted to firm and binding construction contracts, which depend, inter alia, on COSCO’s ability to secure pre-delivery financing on a ring-fenced basis relative to the contracting Sevan Drilling entities.

• If the letters of intent with COSCO for the two newbuilds result in binding and effective EPC contracts, the two new units will, initially, be without employment contracts and financing for 80% of the contract price. No assurance can be given that employment and financing can be obtained on acceptable terms, or at all, in time for scheduled delivery in fourth quarter 2013 and first quarter 2014, respectively. Additional equity financing may be necessary if bank financing is not secured by delivery of the newbuild rigs.

• The continued availability of the financing of the Sevan Brasil is conditional upon the unit being delivered by the yard no later than by 31 November 2012 and the acceptance by Petrobras of the unit under the charter contract no later than by 30 May 2013, failing which a mandatory prepayment event occurs.

• Certain existing guarantees, some of which contain financial covenants, provided by Sevan Marine in favour of lenders and certain other third parties will continue to be in effect until otherwise agreed with relevant beneficiaries, thus rendering Sevan Drilling dependent on the continued performance of Sevan Marine.

SEVAN DRILLING ASA

13

• The Group’s operating and maintenance costs will not necessarily fluctuate in proportion to changes in operating revenues.

• The Group’s future contracted revenue for its drilling units may not be ultimately realized.

• The Group’s offshore drilling contracts may be terminated early due to certain events.

• The Group may not be able to renew or obtain new and favourable contracts for drilling units whose contracts are expiring or are terminated, which could adversely affect the Group’s revenues and profitability.

• The Group’s newbuilding projects are subject to risks which could cause delays or cost overruns.

• The Company may not be able to successfully implement its strategies.

• The Group’s success depends on key members of its management team.

• Failure to obtain or retain highly skilled personnel could adversely affect the Group’s operations.

• Labour interruptions could disrupt the Group’s business.

• In order to execute the Company’s growth strategy, the Company may require additional equity and/or debt capital in the future, which may not be available.

• The Group’s existing or future debt arrangements could limit the Group’s liquidity and flexibility in obtaining additional financing, in pursuing other business opportunities or the Company’s ability to declare dividends to its shareholders.

• If the Group is unable to comply with the restrictions and the financial covenants in the agreements governing its indebtedness, there could be a default under the terms of these agreements, which could result in an acceleration of payment obligations in respect of financial indebtedness.

• Interest rate fluctuations could affect the Group’s profitability, earnings and cash flow.

• Fluctuations in exchange rates could result in financial losses for the Group.

• A change in tax laws or their application of any country in which the Group operates from time to time, or complex tax laws associated with international operations which the Group may undertake from time to time could result in a higher tax expense or a higher effective tax rate on the Group’s earnings.

• A loss of a major tax dispute or a successful tax challenge to the Group’s operating structure from time to time, intercompany pricing policies, the taxable presence of subsidiaries in certain countries or other disputes related to or challenges to the Group’s tax payments could result in a higher tax rate on the Group’s worldwide earnings, which could result in a significant negative impact on its earnings and cash flows from operations.

Risks relating to the Shares:

• The price of the Shares may fluctuate significantly.

• There is no existing market for the Shares, and a trading market that provides adequate liquidity may not develop.

• Future sales of Shares by the Company’s major shareholder or any of its primary insiders may depress the price of the Shares.

• Future issuances of Shares or other securities may dilute the holdings of shareholders and could materially affect the price of the Shares.

• Investors may not be able to exercise their voting rights for Shares registered in a nominee account.

• Investors in the United States may have difficulty enforcing any judgement obtained in the United States against the Company or its Directors or executive officers in Norway.

• The transfer of Shares is subject to restrictions under the securities laws of the United States and other jurisdictions.

• Shareholders outside of Norway are subject to exchange rate risk.

• The Company will have a major shareholder at completion of the Offering.

SEVAN DRILLING ASA

14

2 RISK FACTORS Investing in the Shares involves inherent risks. Before deciding whether or not to participate in the Offering, an investor should consider carefully all of the information set forth in this Prospectus, and in particular, the specific risk factors set out below. An investment in the Shares is suitable only for investors who understand the risk factors associated with this type of investment and who can afford a loss of all or part of the investment.

If any of the risks described below materialize, individually or together with other circumstances, they may have a material adverse effect on the Group’s business, financial condition, results of operations and cash flow, which may cause a decline in the value and trading price of the Shares that could result in a loss of all or part of any investment in the Shares.

The risks and uncertainties described below are not the only ones faced by the Group. Additional risks and uncertainties that the Company currently believes are immaterial, unlikely or that are not presently known to the Company, may also have a material adverse effect on its business, financial condition, results of operations and cash flow.

The order in which the risks are presented below is not intended to provide an indication of the likelihood of their occurrence nor of their severity or significance. These risks should also be considered in connection with the cautionary statement regarding forward-looking information set forth in Section 4.

2.1 Risks relating to the industry in which the Group operates The general level of activity in the offshore oil and gas industry depends on the oil price, which for various reasons is likely to vary over time

The drilling business in general, including the Group’s business depends on the level of activity in oil and gas exploration, as well as the identification and development of oil and gas reserves and production in offshore areas worldwide. The availability of quality drilling prospects, exploration success, relative production costs, the stage of reservoir development, political concerns and regulatory requirements all affect customers' levels of activity and drilling campaigns. Accordingly, oil and gas prices and market expectations of potential changes in these prices significantly affect the level of activity and demand for the Group’s drilling units.

Oil and gas prices are extremely volatile and are affected by numerous factors beyond the Group’s control, including, but not limited to, the following:

• worldwide demand for oil and gas;

• the cost of exploring for, developing, producing and delivering oil and gas;

• expectations regarding future energy prices;

• new or changed taxes on the exploration, production, sale, purchase or consumption of oil or petroleum products;

• the ability of the Organisation of Petroleum Exporting Countries (“OPEC”) to set and maintain production levels and impact pricing;

• the level of production in non-OPEC countries;

• government laws and regulations, including environmental protection laws and regulations;

• local and international political, economic and weather conditions;

• political and military conflicts in oil-producing and other countries; and

• the development and exploitation of alternative energy sources.

An over-supply of drilling units may lead to a reduction in day rates and/or lower utilization of drilling units

Significant increases in the prices for oil and gas have in the past resulted in a large number of construction orders being placed for newbuild rigs. Periods with very high oil prices could be followed by periods of sharp and sudden declines in oil and gas prices, which in turn result in declines in utilization and day rates, and an increase in the number of idle drilling units without long-term contracts.

The worldwide fleet of ultra deepwater and harsh environment drilling units (including the Sevan Driller and the Sevan Brasil) is currently estimated to consist of 85 units, according to data extracted from ODS Petrodata’s Rig Base. An additional 60 ultra deepwater units are reported to be under construction or on order with delivery scheduled prior to November 2013, which would bring the expected total fleet to 145 units by expiry of 2013. The strong growth in ultra deepwater units is due to the increased focus of oil companies on existing and new ultra deepwater regions for exploration and production, and the inability to upgrade or modify the existing mid-water fleet to undertake ultra deepwater and harsh environment drilling campaigns.

SEVAN DRILLING ASA

15

Lower utilization and day rates may adversely affect the value of drilling assets.

The market value of drilling units may decrease, and rig owners are exposed to potentially significant losses if they sell assets following a decline in market values or lower earnings if new charter contracts are signed at lower day rates.

If the offshore contract drilling industry suffers adverse developments in the future, the fair market value of drilling units may decline. The fair market value of the drilling units may increase or decrease depending on a number of factors, including:

• general economic and market conditions affecting the offshore contract drilling industry, including competition from other offshore contract drilling companies;

• types, sizes and ages of drilling units;

• supply and demand for drilling units;

• cost of newbuildings;

• prevailing level of drilling services contract day rates;

• the perceived efficiency, reliability and other competitive advantages or disadvantages of specific drilling designs and technology compared to alternative drilling solutions; the time required to build or deliver new units;

• government laws and regulations, including environmental protection laws and regulations and such laws becoming more stringent due to inter alia accidents such as the recent Deepwater Horizon accident; and

• technological advances.

Consolidation of suppliers may limit availability of supplies and services when needed, at an acceptable cost, or at all

Owners of drilling units generally rely on a significant supply by third parties of consumables, spare parts and equipment to operate, maintain, repair and upgrade its fleet of drilling units. During the last decade the number of available suppliers has been reduced, resulting in fewer alternatives for sourcing key supplies and services. In addition, certain key equipment used by drilling rig owners and operators is protected by patents and other intellectual property of its suppliers or other third parties. All of the foregoing may limit the availability of supplies and services when needed, at an acceptable cost, or at all. Cost increases, delays or unavailability could negatively impact the drilling industry at large and/or individual owners/operators of drilling units, and result in higher rig downtime due to delays in repair and maintenance.

Governmental laws and regulations could affect operations, increase operating costs, reduce demand for services from and restrict the ability of drilling rig owners to operate its drilling units or otherwise.

The drilling business is affected by governmental laws and regulations. The industry is dependent on demand for services from the oil and gas companies and, accordingly, is indirectly also affected by changing laws and regulations relating to the energy business in general. The laws and regulations affecting the drilling industry include, among others laws and regulations relating to;

• protection of the environment;

• quality, health and safety;

• import-export quotas, wage and price controls, imposition of trade barriers and other forms of government regulation and economic conditions;

• taxation.

The industry, including the Group and its customers are required to invest financial and managerial resources to comply with these laws and regulations. The future costs of complying with these laws and regulations cannot be predicted, and any new laws or regulations could materially increase the industry’s (including the Group’s) expenditures in the future. Existing laws or regulations or adoption of new laws or regulations limiting exploration or production activities by oil and gas companies or imposing more stringent restrictions on such activities could adversely affect the Group by increasing its operating costs, reducing the demand for its services and restricting its ability to operate drilling units.

The drilling business is subject to strict environmental laws and regulations with resulting potential exposure to liability and financial consequences for the Group

The drilling business is subject to environmental rules and regulations pursuant to international conventions and national legislation in relevant jurisdictions. Breach of these rules and regulations may result in fines, penalties and/or claims by authorities and customers. The operation of floating production and drilling units in offshore environments, entail inherent risk for pollution and resulting liability which could, potentially have a significant adverse effect on rig owners and operators, which may not be fully covered under contractual arrangements or insurances coverage.

SEVAN DRILLING ASA

16

Environmental laws and regulations have become more stringent in recent years, and may in some cases impose strict liability, rendering a person liable for environmental damage without regard to negligence. Such laws and regulations may expose rig owners and operators to liability resulting from acts or omissions by themselves or by relevant third parties. The application of legislative and/or regulatory requirements or the adoption of new requirements could have a material adverse effect on the financial position, results of operations or cash flows of affected industry players. Some degree of contractual indemnification pursuant to which clients agree to protect, hold harmless and indemnify against liability for pollution, well and environmental damage may be available to rig owners; however, there is no assurance that such indemnities are available or that, in the event of extensive pollution and environmental damage, the indemnifying party would have the financial capability to fulfill their contractual obligations. Also, these indemnities may be held to be unenforceable as a result of public policy or for other reasons. In addition, insurance cover may not be available or sufficient to cover relevant exposure.

The drilling business involves numerous operating hazards

Drilling operations are subject to hazards inherent in the drilling industry, such as blowouts, reservoir damage, loss of production, loss of well control, lost or stuck drill strings, equipment defects, craterings, fires, explosions and pollution. Contract drilling and well servicing require the use of heavy equipment and exposure to hazardous conditions, which may subject the owners and operators to liability claims by employees, customers and third parties. These hazards can cause personal injury or loss of life, severe damage to or destruction of property and equipment, pollution or environmental damage, claims by third parties or customers and suspension of operations. The operation of drilling units is also subject to hazards inherent in marine operations, either while on-site or during mobilization, such as capsizing, sinking, grounding, collision, damage from severe weather and marine life infestations. Operations may also be suspended because of machinery breakdowns, abnormal drilling and/or weather conditions, and failure of subcontractors to perform or supply goods or services, or personnel shortages.

Damage to the environment could also result from drilling operations, particularly through spillage of fuel, lubricants or other chemicals and substances used in drilling operations, or extensive uncontrolled fires. Owners and operators of drilling units may also be subject to property, environmental and other damage claims by oil and gas companies. Relevant insurance policies and contractual rights to indemnity may not adequately cover losses, and may not be customary or available at all. Pollution and environmental risks are generally not totally insurable.

The insurances coverage offered to drilling rig owners includes policy limits. As a result, they retain the risk for any losses in excess of these limits, which could be substantial. Also, industry players may decide to retain additional risk through self-insurance in the future.

If a significant accident or other event occurs and is not fully covered by insurance or any enforceable or recoverable indemnity from a client, it could significantly and adversely affect the financial position, results of operations or cash flows of the affected rig owner or operator.

Competition within the oilfield services industry is fierce and may adversely affect the industry players’ ability to market their services

The oilfield services industry is highly competitive and fragmented and includes several large companies that compete in the markets the Group serves, or will serve, as well as numerous small companies that compete with the Group on a local basis. The solidity and resources of the Group’s larger competitors could enable them to better withstand industry downturns, compete more effectively on the basis of technology and geographic scope, they may be favoured by clients due to better perceived reliability due to greater size and balance sheet, and they may beat the Company at recruiting and retaining skilled personnel. The Company believes the principal competitive factors in the market areas the Group serve are price, product and service quality, availability of crews and equipment and technical proficiency. The Group’s operations may be adversely affected if its current competitors or new market entrants introduce new products or services with better features, performance, prices or other characteristics than the Group’s products and services, or expand into service areas where the Group operates. Competitive pressures or other factors may also result in significant price competition, particularly during industry downturns, which could have a material adverse effect on the Group’s results of operations and financial condition. In addition, competition among oilfield services and equipment providers is affected by each provider’s reputation for solidity, safety, quality and technological innovation.

Uncertainty relating to the development of the world economy may reduce demand for drilling services or result in contract delays or cancellations

The drilling industry depends on its existing and prospective customers’ willingness and ability to make operating and capital expenditures to explore, develop and produce oil and gas. Demand for drilling units and services is particularly sensitive to oil price developments fluctuations in production levels, general demand and activity in the oil industry as well as exploration results. In such a volatile market, no assurance can be given as to the Company’s ability to successfully secure contracts and seize opportunities. A decrease in the oil price may have a material adverse impact on participants’ ability to secure attractive employment opportunities and, accordingly, adversely affect their financial condition. A high oil price may have a negative effect on the demand for petroleum products, which could, ultimately, have a negative impact on the demand for the industry’s products and services. Recent volatility in the world economy

SEVAN DRILLING ASA

17

has caused significant changes in the prices of oil and gas prices. Continued volatility may create uncertainty that can cause oil companies to cut spending budgets. Limitations on the availability of capital or higher costs of capital for financing expenditures, or the desire to preserve liquidity, may cause potential customers to make additional reductions in future capital budgets and outlays. Such adjustments could reduce demand for drilling services generally, and the Group’s products and services specifically, which could adversely affect its results of operations and cash flows.

The industry is generally fiercely competitive and specifically subject to continual and rapid technological developments

The deepwater drilling market is characterized by continual and rapid technological developments that have resulted in, and will likely continue to result in, substantial improvements in equipment functions and performance. As a result, the future success and profitability of industry participants will be dependent in part upon its ability to:

• improve existing services and related equipment;

• address the increasingly sophisticated needs of its customers; and

• anticipate changes in technology and industry standards and respond to technological developments on a timely basis.

If a rig owner such as the Group is not successful in acquiring new equipment or upgrading its existing equipment on a timely and cost-effective basis in response to technological developments or changes in standards in the industry, this could have a material adverse effect on such rig owner’s business.

Drilling operations are often international in scope and expose owners and operators to different formal challenges which may entail additional risks

Drilling activities in various jurisdictions and international operations involve additional risks, including risks of:

• terrorist acts, war, civil disturbances and piracy;

• seizure, nationalization or expropriation of property or equipment;

• political unrest;

• labour unrest and strikes;

• the inability to repatriate income or capital;

• complications associated with repairing and replacing equipment in remote locations;

• impositions of embargos;

• import-export quotas, wage and price controls, imposition of trade barriers and other forms of government regulation and economic conditions that are beyond the Group’s control;

• regulatory or financial requirements to comply with foreign bureaucratic actions; and

• changing taxation policies.

In addition, international contract drilling operations are subject to the various laws and regulations in relevant countries and jurisdictions, including laws and regulations relating to:

• the equipment requirements for operation of drilling units;

• repatriation of foreign earnings;

• oil and gas exploration and development;

• taxation of offshore earnings and the earnings of expatriate personnel;

• customs duties on the importation of drilling rigs and related equipment;

• requirements for local registration or ownership of drilling rigs by nationals of the country of operations; and

• the use and compensation of local employees and suppliers by foreign contractors.

Some foreign governments favour or effectively require (i) the awarding of drilling contracts to local contractors or to drilling rigs owned by their own citizens, (ii) the use of a local agent or (iii) foreign contractors to employ citizens of, or purchase supplies from, a particular jurisdiction. These practices may adversely affect foreign third parties’, such as the Group’s, ability to compete in those regions. It is difficult to predict what governmental regulations may be enacted in the future that could adversely affect the international drilling industry. Failure to comply with applicable laws and regulations, including those relating to sanctions and export restrictions, may subject the Group to criminal sanctions or civil remedies, including fines, denial of export privileges, injunctions or seizures of assets.

SEVAN DRILLING ASA

18

Risk of war, civil attacks, piracy, and terrorist attacks

Terrorist attacks have among other things caused instability in the world’s financial and commercial markets. This has in turn contributed to high levels of volatility in prices for among other things oil and gas. Even war, civil disturbances and/or piracy occurs from time to time in areas where drilling business is undertaken. Continuing instability for one or more of these reasons may cause further disruption to financial and commercial markets and contribute to even higher level of volatility in prices. In addition, acts of war, piracy or terrorism could limit or disrupt drilling operations, including disruptions from evacuation of personnel, cancellation of contracts or the loss of personnel or assets, and may significantly affect the drilling business in general and/or affected individual drilling rig owners/operators’ business and results of operations in the future.

2.2 Risks relating to the Group The Group currently relies heavily on one customer

The Group’s contract drilling business is subject to the risks associated with having a limited number of customers for its services. While the Group expects to enter into contracts with multiple clients in the years to come, as of the date of the Prospectus, Petrobras alone accounts for all of the Group’s future contracted revenues. While the Group enjoys a good relationship with Petrobras, it is also directly exposed to the results and financial condition of its sole customer for the time being, and, therefore, dependent on the continued success of Petrobras. The Group’s results of operations could be materially adversely affected if Petrobras were to fail to compensate the Group for it services, were to terminate the contracts (or any of them) with or without cause, fail to renew the existing contract or refuse to award new contracts to the Group and the Group is unable to enter into contracts with new customers at comparable dayrates.

The letters of intent with COSCO entail particular risk

The letters of intent with COSCO for two newbuilds remain to be converted to firm and binding construction contracts, which depend, inter alia, on COSCO’s ability to secure pre-delivery financing on a ring-fenced basis relative to the contracting Sevan Drilling entities.

If the letters of intent with COSCO results in final and binding contracts for construction of two additional units based on the Sevan 650 design, such projects will be commenced without any employment having been secured for the units upon delivery, and without financing in place for the instalments equal to 80% of the project price which is payable upon delivery, thus potentially exposing the 20% equity injected in the projects.

The financing of the Sevan Brasil is conditional

The continued availability of the financing of the Sevan Brasil is conditional upon the unit being delivered by the yard no later than by 31 November 2012 and the acceptance by Petrobras of the unit under the charter contract no later than by 30 May 2013, failing which a mandatory prepayment event occurs.

The Group has limited experience in operation of drilling rigs

The “Sevan Driller” has been in operation for 9 months only, so only limited experience from the operations of its drilling rigs has been gained. Because investors have limited historical operating and financial information on which to base the investment decision, the Company outlook must be considered in light of the risks, uncertainties and obstacles that it may face in an evolving and competitive market.

The Group’s operating and maintenance costs will not necessarily fluctuate in proportion to changes in operating revenues

The Group’s operating and maintenance costs will not necessarily fluctuate in proportion to changes in operating revenues. Operating revenues may fluctuate as a function of changes in supply and demand for contract drilling services, which in turn affect dayrates. In addition, equipment maintenance costs fluctuate depending upon the type of activity the unit is performing and the age and condition of the equipment. In connection with new assignments, the Group might incur expenses relating to preparation for operations under a new contract. The expenses may vary based on the scope and length of such required preparations and the duration of the firm contractual period over which such expenditures are amortized. In a situation where a drilling unit faces long idle periods, reductions in costs may not be immediate as some of the crew may be required to prepare drilling units for stacking and maintenance in the stacking period. Should drilling units be idle for a longer period, the Group may seek to redeploy crew members, who are not required to maintain the units, to active units to the extent possible. However, there can be no assurance that the Group will be successful in reducing its costs.

The Group’s future contracted revenue for its drilling units may not be ultimately realized

There may be uncertainty as to the duration of offshore charters due to extension and/or early cancellation options held by charterers, late delivery or deviation from contracted performance measures. Also, there may be off-hire periods during and between charters. The cancellation or postponement of one or more charters can have a major adverse impact on the earnings of drilling companies, including the Company. The Company may also suffer losses should

SEVAN DRILLING ASA

19

customers seek to renegotiate contracts during periods with depressed market conditions, or upon downtime, operational difficulties, safety related issues or if a unit becomes a total loss.

As of 31 December 2010, the future estimated contracted revenue for the Group’s drilling units, or contract drilling backlog, was approximately USD 1.9 billion under firm commitments, including bonus potential. The Group may not be able to perform under these contracts due to events beyond its control or due to default of the Group, and any of the Group’s customers may seek to cancel or renegotiate contracts for various reasons, including adverse conditions, or invoke suspension periods, at their discretion, resulting in lower dayrates. The Group’s inability or the inability of its customers to perform contractual obligations under these contracts may have a material adverse effect on the Group’s financial position, results of operations and cash flows.

The operation of drilling rigs requires effective maintenance routines and functioning equipment. Certain pieces of equipment are critical regarding the rigs’ performance of the drilling services as required in customer contracts. While efforts are made to continuously identify the need for critical spare parts and equipment, there is a risk of unpaid downtime resulting from the time needed to repair or replace equipment which may have a long delivery time should there not be readily available spares. In addition, downtime and suspension periods may be prolonged due to complications with repairing or replacing equipment as the drilling units may be situated in remote locations.

Risks relating to counterparties

The Company relies on timely delivery of goods and services by numerous vendors and suppliers, and the performance in full by the charterers of the Sevan units. Failure to perform or financial difficulties encountered by any such counterpart can adversely affect the financial and/or operational condition of the Company.

The Group’s offshore drilling contracts may be terminated early due to certain events

Under certain circumstances the Group’s existing or future contracts may permit a customer to terminate their contract early without the payment of any termination fee, as a result of non-performance, longer periods of downtime or impaired performance caused by equipment or operational issues, or sustained periods of downtime due to force majeure events. Many of these events are beyond the Group’s control. During periods of challenging market conditions, the Group may be subject to an increased risk of its clients seeking to repudiate their contracts, including through claims of non-performance. The ability of the Group’s customers from time to time to perform their obligations under their drilling contracts with the Group may also be negatively impacted by the prevailing uncertainty surrounding the development of the world economy and the credit markets. If the Group’s customers from time to time cancel their contracts with the Group, and the Group is unable to secure new contracts on a timely basis and on substantially similar terms, or if contracts are suspended for an extended period of time or if the Group’s contracts are renegotiated, it could adversely affect the Group’s financial position, results of operations or cash flows.