34

Roper Technologies, Inc. Q4 2015 Financial Results February 1, 2016

Roper Technologies, Inc.

Q4 2015 Financial Results February 1, 2016

Click to edit Master title style

A Diversified Growth Company

2

Safe Harbor Statement

The information provided in this presentation contains forward-looking statements within the meaning of the

federal securities laws. These forward-looking statements include, among others, statements regarding

operating results, the success of our internal operating plans, and the prospects for newly acquired businesses

to be integrated and contribute to future growth, profit and cash flow expectations. Forward-looking statements

may be indicated by words or phrases such as "anticipate," "estimate," "plans," "expects," "projects," "should,"

"will," "believes" or "intends" and similar words and phrases. These statements reflect management's current

beliefs and are not guarantees of future performance. They involve risks and uncertainties that could cause

actual results to differ materially from those contained in any forward-looking statement. Such risks and

uncertainties include our ability to integrate our acquisitions and realize expected synergies. We also face other

general risks, including our ability to realize cost savings from our operating initiatives, general economic

conditions, unfavorable changes in foreign exchange rates, difficulties associated with exports, risks associated

with our international operations, difficulties in making and integrating acquisitions, risks associated with newly

acquired businesses, increased product liability and insurance costs, increased warranty exposure, future

competition, changes in the supply of, or price for, parts and components, environmental compliance costs and

liabilities, risks and cost associated with asbestos related litigation and potential write-offs of our substantial

intangible assets, and risks associated with obtaining governmental approvals and maintaining regulatory

compliance for new and existing products. Important risks may be discussed in current and subsequent filings

with the SEC. You should not place undue reliance on any forward-looking statements. These statements speak

only as of the date they are made, and we undertake no obligation to update publicly any of them in light of new

information or future events.

We refer to certain non-GAAP financial measures in this presentation. Reconciliations of these non-GAAP

financial measures to the most directly comparable GAAP financial measures can be found within this

presentation.

Click to edit Master title style

A Diversified Growth Company

3

Reg. G Disclosure

Today’s Conference Call Will Discuss Income Statement

Results Primarily on an Adjusted (Non-GAAP) Basis. The Q4

2015 Adjusted Results Exclude the Following Items:

(1) Gain on Sale of Abel Pumps, Offset by Impairment

Charge on Minority Investment

(2) Purchase Accounting Adjustment to Acquired Deferred

Revenue

(3) Acquisition-Related Inventory Step-Up Charge

See Appendix for Reconciliation from GAAP to Adjusted Results

Click to edit Master title style

A Diversified Growth Company

4

Roper Conference Call

» Q4 and FY Enterprise Financial Results

» Segment Detail & Outlook

» Q1 and FY 2016 Guidance

» Q&A

5

Q4 Enterprise Results

Q4 2015 Enterprise Highlights

6

Good Execution; Disciplined Capital Deployment

» Revenue: $948M, Flat to Last Year

– Organic (4%), FX Headwind (2%), Acquisitions/Divestitures +6%

– Declines in Industrial and Energy Segments

– Strong Growth in Medical and RF Technology Segments

» Gross Margin +190 Bps to 61.8%

» EBITDA Margin +60 Bps to 35.9%

» EBITDA +2% to $341M

» Free Cash Flow +3% to $261M; 140% Conversion

» Completed $900M Bond Issuance in December

» Deployed over $700M in Acquisitions; Abel Sale Completed

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

Click to edit Master title style

A Diversified Growth Company

7

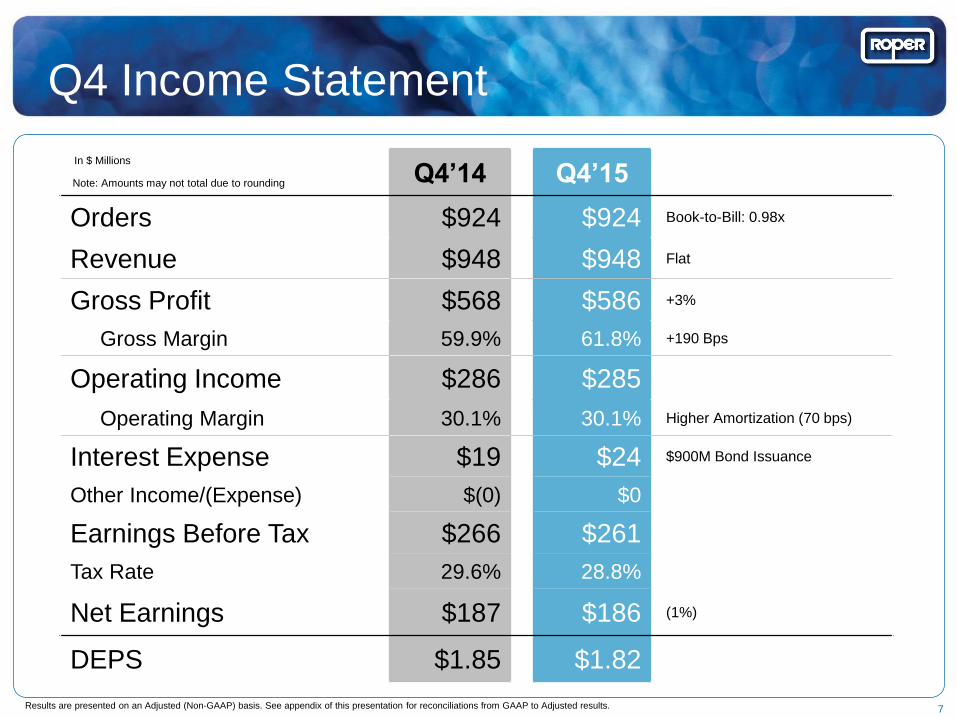

Q4 Income Statement

Q4’14 Q4’15

Orders $924 $924 Book-to-Bill: 0.98x

Revenue $948 $948 Flat

Gross Profit $568 $586 +3%

Gross Margin 59.9% 61.8% +190 Bps

Operating Income $286 $285

Operating Margin 30.1% 30.1% Higher Amortization (70 bps)

Interest Expense $19 $24 $900M Bond Issuance

Other Income/(Expense) $(0) $0

Earnings Before Tax $266 $261

Tax Rate 29.6% 28.8%

Net Earnings $187 $186 (1%)

DEPS $1.85 $1.82

In $ Millions

Note: Amounts may not total due to rounding

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

8

Full Year Enterprise Results

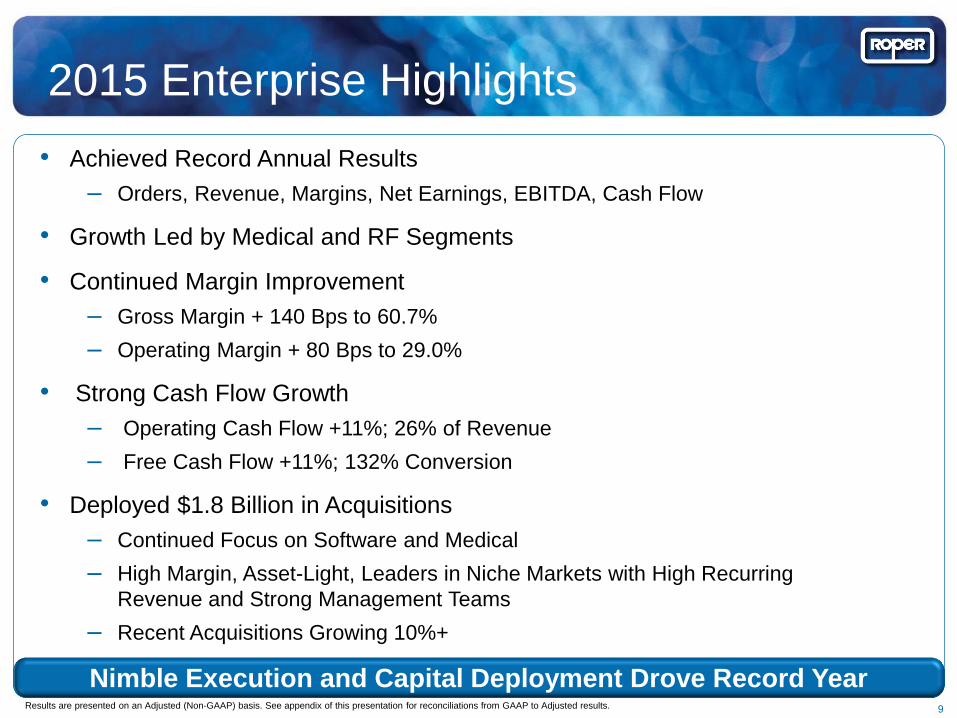

2015 Enterprise Highlights

9

Nimble Execution and Capital Deployment Drove Record Year Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

• Achieved Record Annual Results

‒ Orders, Revenue, Margins, Net Earnings, EBITDA, Cash Flow

• Growth Led by Medical and RF Segments

• Continued Margin Improvement

– Gross Margin + 140 Bps to 60.7%

– Operating Margin + 80 Bps to 29.0%

• Strong Cash Flow Growth

‒ Operating Cash Flow +11%; 26% of Revenue

‒ Free Cash Flow +11%; 132% Conversion

• Deployed $1.8 Billion in Acquisitions

‒ Continued Focus on Software and Medical

‒ High Margin, Asset-Light, Leaders in Niche Markets with High Recurring

Revenue and Strong Management Teams

‒ Recent Acquisitions Growing 10%+

2015 Full Year Revenue Bridge

Strong Execution Despite FX and Energy Market Declines 10

In $ Millions

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

3,300

3,400

3,500

3,600

3,700

3,800

3,900

$3,552

+ 56

+ 39

+ 157

(35)

(104)

(72)

$3,593

Foreign

Exchange

Industrial

Segment

Organic

Energy

Segment

Organic

RF

Segment

Organic

Medical

Segment

Organic

Acquisitions /

Divestitures

2014

Revenue

2015

Revenue

Growth

Before

Impact of

FX

+7% (3%) (3%)

Outstanding Margins

Continued Margin Expansion

Full Year Gross Margin

11

Full Year EBITDA Margin

58.6% 59.3%

60.7%

+210 Bps

2014 2015 2013

+180 Bps

32.8% 33.8%

34.6%

2013 2014 2015

In $ Millions

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

Compounding Cash Flow

We Believe Cash is the Best Measure of Performance

Full Year Operating Cash Flow

In $ Millions

$840

$929

12

2014 2015

» Q4 Operating Cash Flow: $269M

• 145% Conversion

» Q4 Free Cash Flow: $261M

• 3% Increase

• 27% of Revenue

» Full Year Free Cash Flow: $893M

• 11% Increase

• 132% Conversion

Notes: Free Cash Flow = Operating Cash Flow – Capital Expenditures; Conversion Calculated Using Adjusted Net Income

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

+ 11%

Strong Financial Position

13

$900M Bond Issuance; Revolver Upsized; Ample Liquidity

12/31/14 12/31/15

Cash $610 $779

Undrawn Revolver $1,500 $1,670

Gross Debt $2,214 $3,289

Net Debt $1,604 $2,510

Shareholders’ Equity $4,755 $5,299

TTM EBITDA $1,201 $1,245

Net Debt-to-EBITDA (TTM)

1.3x

2.0x

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

In $ Millions

14

Segment Detail & Outlook

Energy Ind Tech RF Medical

$183 $234

$376

$556

$588

$745

$1,037

$1,223

* Excludes

Corporate

Expenses

EBITDA

Margin 31% 31% 36% 45%

2015 Segment Results

Excellent Segment Margins; Medical and RF ~70% of EBITDA

In $ Millions

15 Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

Revenue

EBITDA*

Click to edit Master title style

A Diversified Growth Company

16

Medical Solutions

($M) Q4’15 V to PY

Revenue $324 +12%

Op Profit $118 +16%

OP Margin 36.6% +110 bps

* Excludes Corporate Expenses

Q4 2015

FY 2016

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

• Organic Revenue +3%, Acq. +12%, FX (3%)

• 2014 Acquisitions – SHP and IPA – Each Delivered

Double Digit Growth in Their First Organic Quarter

• Verathon Strong on New Product Sales

• Northern Digital Continued Excellent Year with Strong

Revenue Growth and Record Backlog

• Atlas Medical Integration with Sunquest On Track

• Expect Mid Single Digit Organic Growth

• Segment Organic Growth Strengthens Throughout the Year

‒ Sunquest New Software Releases in Second Half

‒ 2015 Acquisitions (Strata, Data Innovations and

SoftWriters) Become Organic in Q2

• Verathon and Northern Digital Drive Medical Device Growth

• CliniSys Acquisition Closed on January 7th; European

Hospital Laboratory Software Provider

Medical % of

Roper 2015 EBITDA*

* Excludes Corporate Expenses

41% 41%

Click to edit Master title style

A Diversified Growth Company

17

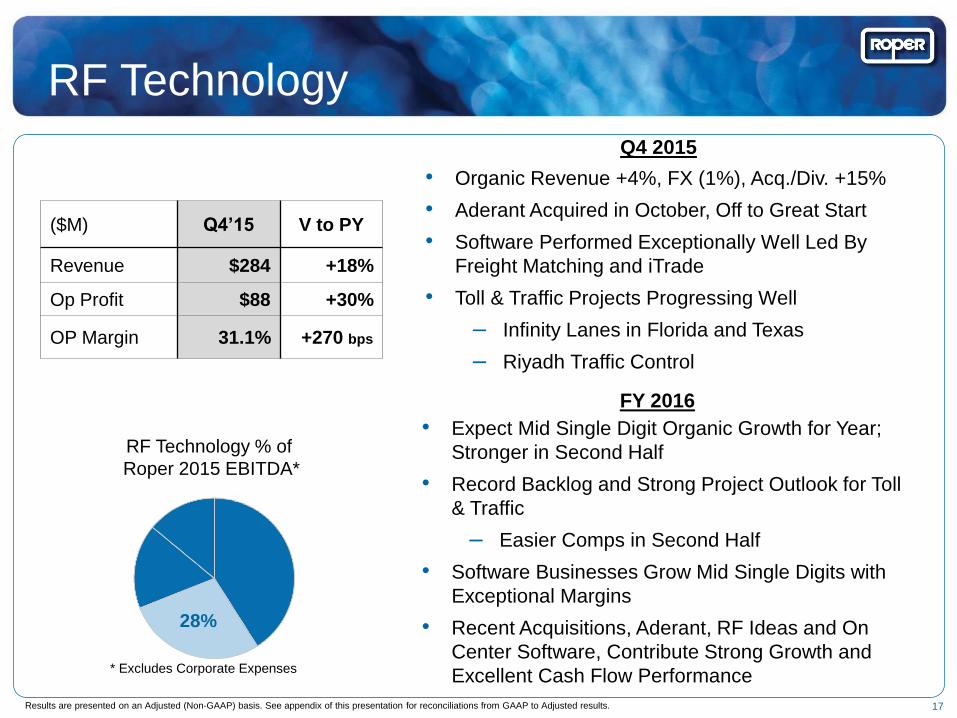

RF Technology

• Organic Revenue +4%, FX (1%), Acq./Div. +15%

• Aderant Acquired in October, Off to Great Start

• Software Performed Exceptionally Well Led By

Freight Matching and iTrade

• Toll & Traffic Projects Progressing Well

‒ Infinity Lanes in Florida and Texas

‒ Riyadh Traffic Control

($M) Q4’15 V to PY

Revenue $284 +18%

Op Profit $88 +30%

OP Margin 31.1% +270 bps

Q4 2015

FY 2016

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

• Expect Mid Single Digit Organic Growth for Year;

Stronger in Second Half

• Record Backlog and Strong Project Outlook for Toll

& Traffic

‒ Easier Comps in Second Half

• Software Businesses Grow Mid Single Digits with

Exceptional Margins

• Recent Acquisitions, Aderant, RF Ideas and On

Center Software, Contribute Strong Growth and

Excellent Cash Flow Performance * Excludes Corporate Expenses

27%

RF Technology % of

Roper 2015 EBITDA*

28%

Click to edit Master title style

A Diversified Growth Company

18

Industrial Technology

• Organic Revenue (8%), FX (3%), Divest. (6%)

• Completed Abel Divestiture

• Neptune Grew Double Digits in the U.S.; Toronto

Project Completion Headwind Remains

• Continued Declines in Upstream Oil & Gas

• Expect Low Single Digit Organic Growth for Segment

‒ Upstream O&G Declines 30% (~$20M)

‒ Neptune U.S. Growth Continues and Toronto

Headwind Eases After Q1

‒ Low Single Digit Growth in Other End Markets

($M) Q4’15 V to PY

Revenue $182 (17)%

Op Profit $52 (24)%

OP Margin 28.7% (270) bps

Industrial Technology % of

Roper 2015 EBITDA*

* Excludes Corporate Expenses

20%

Q4 2015

FY 2016

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

17%

17%

Click to edit Master title style

A Diversified Growth Company

• Organic Revenue (17%), FX (4%)

• Q4 Seasonal Improvement Less Than Expected

• Reduced Backlogs in Oil & Gas Project Businesses

• Strong Growth in Zetec Nuclear Business

• Operating Margin Still Impressive at 32.7%

Energy Systems & Controls

19

($M) Q4’15 V to PY

Revenue $158 (21)%

Op Profit $52 (28)%

OP Margin 32.7% (340) bps

Q4 2015

FY 2016

• Expect High Single Digit Organic Decline for Segment

‒ Oil & Gas Remains Weak, Down (~15%)

‒ Project Activity Continues to Decline; Large

Impact to Compressor Controls

‒ Modest Growth in Other Areas Led By Nuclear

and Industrial Markets

* Excludes Corporate Expenses

14%

Energy % of

Roper 2015 EBITDA*

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

20

2016 Guidance

2016 Revenue Outlook

Total Revenue Up 8 - 10%; Organic Revenue Up 2 - 4% 21

In $ Millions

Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

$3,593

+8 - 10%

Foreign

Exchange

Industrial

Segment

Energy

Segment

RF

Segment

Medical

Segment

Completed

Acquisitions /

Divestitures

2015

Revenue

2016

Revenue

Growth

Before

Impact of

FX

+MSD

Organic

+MSD

Organic

+LSD

Organic

(HSD)

Organic

Note: Excludes Future

Acquisitions

Click to edit Master title style

A Diversified Growth Company

22

2016 Guidance Established

» Full Year Operating Cash Flow ~ $1.0B

» Full Year Adjusted DEPS: $6.85 – $7.15

• Key Assumptions:

– Revenue Growth: 8 – 10% ; Organic 2 – 4%, Comps ease after Q1

– Non-Cash Amortization +$30M to $195M

– Interest Expense +$25M to $109M

– Tax Rate 30.0% - 30.5%

– Excludes Future Acquisitions or Divestitures

» Q1 Adjusted DEPS: $1.42 – $1.47

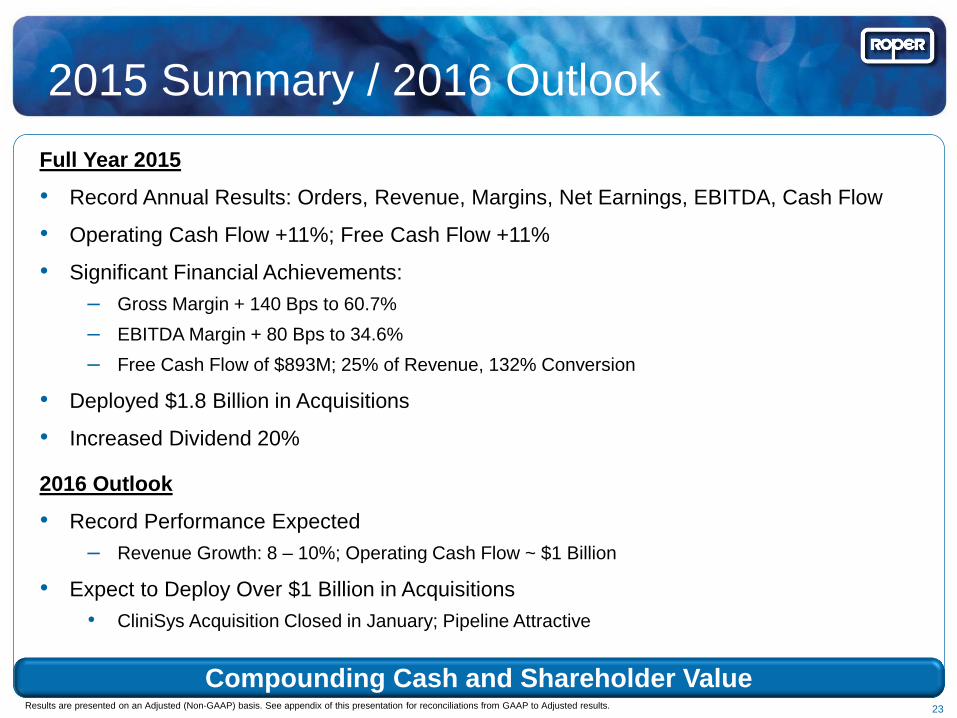

2015 Summary / 2016 Outlook

23

Compounding Cash and Shareholder Value Results are presented on an Adjusted (Non-GAAP) basis. See appendix of this presentation for reconciliations from GAAP to Adjusted results.

Full Year 2015

• Record Annual Results: Orders, Revenue, Margins, Net Earnings, EBITDA, Cash Flow

• Operating Cash Flow +11%; Free Cash Flow +11%

• Significant Financial Achievements:

– Gross Margin + 140 Bps to 60.7%

– EBITDA Margin + 80 Bps to 34.6%

– Free Cash Flow of $893M; 25% of Revenue, 132% Conversion

• Deployed $1.8 Billion in Acquisitions

• Increased Dividend 20%

2016 Outlook

• Record Performance Expected

‒ Revenue Growth: 8 – 10%; Operating Cash Flow ~ $1 Billion

• Expect to Deploy Over $1 Billion in Acquisitions

• CliniSys Acquisition Closed in January; Pipeline Attractive

24

Appendix

Click to edit Master title style

A Diversified Growth Company

25

Reconciliations I

Q4 2015 Revenue Growth

Reconciliation

Industrial

Technology

Energy

Systems &

Controls

Medical &

Scientific

Imaging

RF

Technology Roper

Organic Growth (8)% (17)% 3% 4% (4)%

Acquisitions/Divestitures (6)% - 12% 15% 6%

Foreign Exchange (3)% (4)% (3)% (1)% (2)%

Rounding - - - - -

Total Revenue Growth (17)% (21)% 12% 18% -

Q4 2015 Orders Growth

Reconciliation

Industrial

Technology

Energy

Systems &

Controls

Medical &

Scientific

Imaging

RF

Technology Roper

Organic Growth (4)% (28)% 7% (3)% (6)%

Acquisitions/Divestitures (4)% - 15% 17% 8%

Foreign Exchange (4)% (3)% (3)% (1)% (3)%

Rounding 1% - - - 1%

Total Orders Growth (11)% (31)% 19% 13% -

Click to edit Master title style

A Diversified Growth Company

26

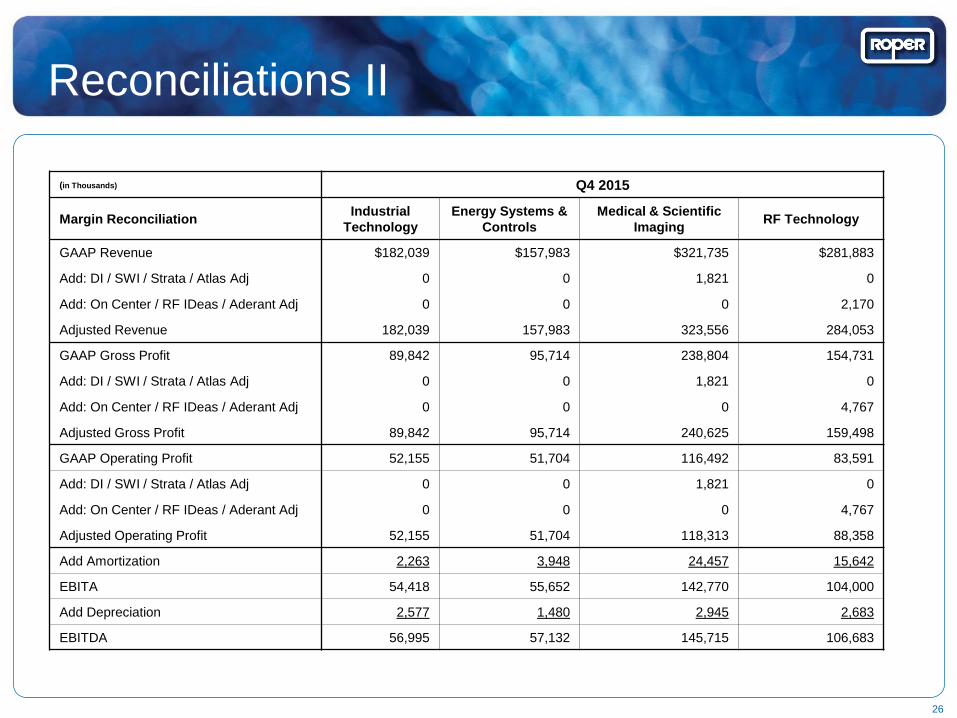

Reconciliations II

(in Thousands) Q4 2015

Margin Reconciliation Industrial

Technology

Energy Systems &

Controls

Medical & Scientific

Imaging RF Technology

GAAP Revenue $182,039 $157,983 $321,735 $281,883

Add: DI / SWI / Strata / Atlas Adj 0 0 1,821 0

Add: On Center / RF IDeas / Aderant Adj 0 0 0 2,170

Adjusted Revenue 182,039 157,983 323,556 284,053

GAAP Gross Profit 89,842 95,714 238,804 154,731

Add: DI / SWI / Strata / Atlas Adj 0 0 1,821 0

Add: On Center / RF IDeas / Aderant Adj 0 0 0 4,767

Adjusted Gross Profit 89,842 95,714 240,625 159,498

GAAP Operating Profit 52,155 51,704 116,492 83,591

Add: DI / SWI / Strata / Atlas Adj 0 0 1,821 0

Add: On Center / RF IDeas / Aderant Adj 0 0 0 4,767

Adjusted Operating Profit 52,155 51,704 118,313 88,358

Add Amortization 2,263 3,948 24,457 15,642

EBITA 54,418 55,652 142,770 104,000

Add Depreciation 2,577 1,480 2,945 2,683

EBITDA 56,995 57,132 145,715 106,683

Click to edit Master title style

A Diversified Growth Company

27

Reconciliations III

(in Thousands) Q4 2014

Margin Reconciliation Industrial

Technology

Energy Systems &

Controls

Medical & Scientific

Imaging RF Technology

GAAP Revenue $219,642 $200,009 $286,410 $240,084

Add: SHP Purchase Accounting

Adjustment to Acquired Deferred Revenue 0 0 1,204 0

Add: FoodLink Purchase Accounting

Adjustment to Acquired Deferred Revenue 0 0 0 180

Adjusted Revenue 219,642 200,009 287,614 240,264

GAAP Operating Profit 69,056 72,177 100,488 67,994

Add: SHP Purchase Accounting

Adjustment to Acquired Deferred Revenue 0 0 1,204 0

Add: FoodLink Purchase Accounting

Adjustment to Acquired Deferred Revenue 0 0 0 180

Add: IPA Acquisition Related Inventory

Step-up Charge 0 0 425 0

Adjusted Operating Profit 69,056 72,177 102,117 68,174

Add Amortization 2,266 4,289 21,150 11,510

EBITA 71,322 76,466 123,267 79,684

Add Depreciation 2,953 1,563 3,071 2,722

EBITDA 74,275 78,029 126,338 82,406

Click to edit Master title style

A Diversified Growth Company

28

Reconciliations IV

(in Thousands) Full Year 2015

Margin Reconciliation Industrial

Technology

Energy Systems &

Controls

Medical & Scientific

Imaging RF Technology

GAAP Revenue $745,381 $587,745 $1,215,318 $1,033,951

Add: SHP / DI / SWI / Strata / Atlas Adj 0 0 7,831 0

Add: FL / On Center / RF IDeas / Aderant Adj 0 0 0 2,786

Adjusted Revenue 745,381 587,745 1,223,149 1,036,737

GAAP Gross Profit 370,894 341,372 899,775 552,605

Add: SHP / DI / SWI / Strata / Atlas Adj 0 0 7,831 0

Add: FL / On Center / RF IDeas / Aderant Adj 0 0 0 7,346

Adjusted Gross Profit 370,894 341,372 907,606 559,951

GAAP Operating Profit 214,538 162,128 441,931 312,112

Add: SHP / DI / SWI / Strata / Atlas Adj 0 0 7,831 0

Add: FL / On Center / RF IDeas / Aderant Adj 0 0 0 7,346

Adjusted Operating Profit 214,538 162,128 449,762 319,458

Add Amortization 9,044 16,158 94,433 46,441

EBITA 223,582 178,286 544,195 365,899

Add Depreciation 10,868 5,096 11,495 10,436

EBITDA 234,450 183,382 555,690 376,335

Click to edit Master title style

A Diversified Growth Company

29

Reconciliations V

(in Thousands) Full Year 2014

Margin Reconciliation Industrial

Technology

Energy Systems &

Controls

Medical & Scientific

Imaging RF Technology

GAAP Revenue $827,145 $691,813 $1,080,309 $950,227

Add: SHP / IPA Adjustments 0 0 1,970 0

Add: FoodLink Adjustments 0 0 0 360

Adjusted Revenue 827,145 691,813 1,082,279 950,587

GAAP Gross Profit 417,568 403,287 779,407 501,637

Add: SHP / IPA Adjustments 0 0 2,819 0

Add: FoodLink Adjustments 0 0 0 360

Adjusted Gross Profit 417,568 403,287 782,226 501,997

GAAP Operating Profit 247,596 203,021 375,867 271,177

Add: SHP / IPA Adjustments 0 0 2,819 0

Add: FoodLink Adjustments 0 0 0 360

Adjusted Operating Profit 247,596 203,021 378,686 271,537

Add Amortization 9,085 17,614 81,841 47,854

EBITA 256,681 220,635 460,527 319,391

Add Depreciation 12,050 5,667 11,842 10,848

EBITDA 268,731 226,302 472,369 330,239

Click to edit Master title style

A Diversified Growth Company

30

Reconciliations VI

(All Numbers are In Thousands)

Adjustments

Full Year

2015 GAAP

Purchase

Accounting

Adjustments to

Acquired

Deferred

Revenue

Purchase

Accounting

Adjustments to

Acquired

Inventory

Write-Down of

Investment

Gain on Sale of

Business

Full Year

2015

Adjusted

Net Sales $3,582,395 $10,617 - - - $3,593,012

Gross Profit $2,164,646 $10,617 $4,560 - - $2,179,823

Operating Profit $1,027,918 $10,617 $4,560 - - $1,043,095

Net Earnings $696,067 $6,901 $2,964 $6,193 $(33,431) $678,694

Taxes 306,278 3,716 1,596 3,335 $(37,429) 277,496

Interest 84,225 - - - - 84,225

Depreciation 38,185 - - - - 38,185

Amortization 166,076 - - - - 166,076

EBITDA $1,290,831 $10,617 $4,560 $9,528 $(70,860) $1,244,676

Full Year 2015 Reconciliation of GAAP to Adjusted; Revenue, Gross Profit, and EBITDA

(1) For the purchase accounting adjustments, the company used a 35% tax rate as these adjustments are US-based items and 35% is the statutory tax rate in the United States.

(2) For the write-down on investment adjustment, the company used a 35% tax rate as this adjustment was US-based and 35% is the statutory tax rate in the United States.

(3) For the Gain on Sale, the specific taxes due in regard to this transaction have been identified above.

Click to edit Master title style

A Diversified Growth Company

31

Reconciliations VII

(All Numbers are In Thousands)

Adjustments

Full Year

2014 GAAP

Purchase

Accounting

Adjustments to

Acquired

Deferred

Revenue

Purchase

Accounting

Adjustments to

Acquired

Inventory

Full Year

2014

Adjusted

Net Sales $3,549,494 $2,330 - $3,551,824

Gross Profit $2,101,899 $2,330 $849 $2,105,078

Operating Profit $999,473 $2,330 $849 $1,002,652

Net Earnings $646,033 $1,515 $552 $648,100

Taxes $275,423 815 297 276,535

Interest 78,637 - - 78,637

Depreciation 40,890 - - 40,890

Amortization 156,394 - - 156,394

EBITDA $1,197,377 $2,330 $849 $1,200,556

Full Year 2014 Reconciliation of GAAP to Adjusted; Revenue, Gross Profit, and EBITDA

(1) For the purchase accounting adjustments, the company used a 35% tax rate as these adjustments are US-based items and 35% is the statutory tax rate in the United States.

Click to edit Master title style

A Diversified Growth Company

32

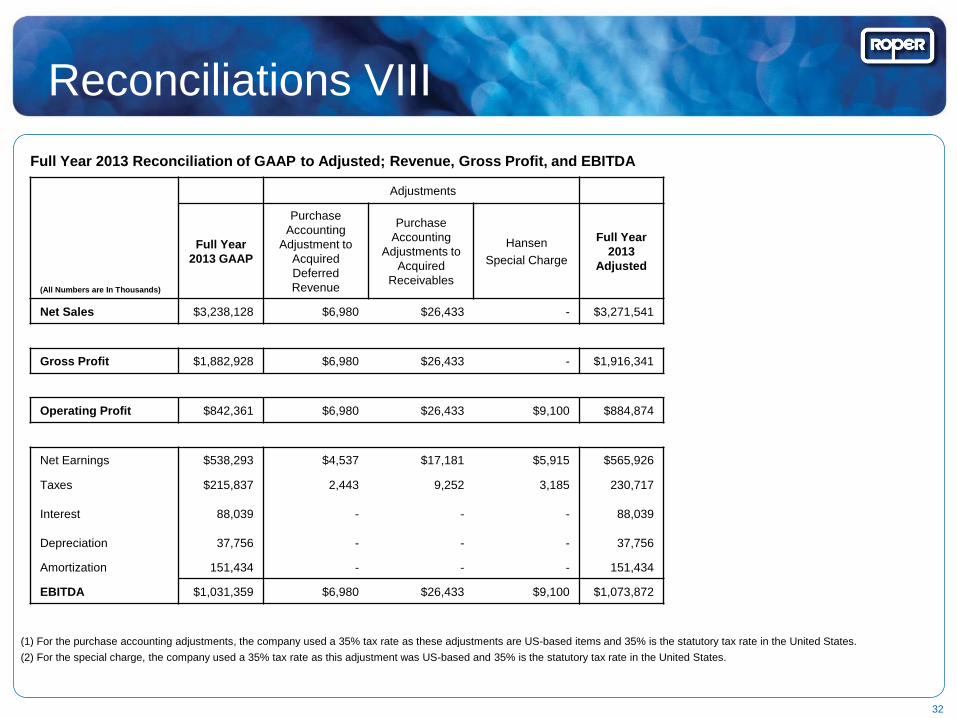

Reconciliations VIII

(All Numbers are In Thousands)

Adjustments

Full Year

2013 GAAP

Purchase

Accounting

Adjustment to

Acquired

Deferred

Revenue

Purchase

Accounting

Adjustments to

Acquired

Receivables

Hansen

Special Charge

Full Year

2013

Adjusted

Net Sales $3,238,128 $6,980 $26,433 - $3,271,541

Gross Profit $1,882,928 $6,980 $26,433 - $1,916,341

Operating Profit $842,361 $6,980 $26,433 $9,100 $884,874

Net Earnings $538,293 $4,537 $17,181 $5,915 $565,926

Taxes $215,837 2,443 9,252 3,185 230,717

Interest 88,039 - - - 88,039

Depreciation 37,756 - - - 37,756

Amortization 151,434 - - - 151,434

EBITDA $1,031,359 $6,980 $26,433 $9,100 $1,073,872

Full Year 2013 Reconciliation of GAAP to Adjusted; Revenue, Gross Profit, and EBITDA

(1) For the purchase accounting adjustments, the company used a 35% tax rate as these adjustments are US-based items and 35% is the statutory tax rate in the United States.

(2) For the special charge, the company used a 35% tax rate as this adjustment was US-based and 35% is the statutory tax rate in the United States.

Click to edit Master title style

A Diversified Growth Company

33

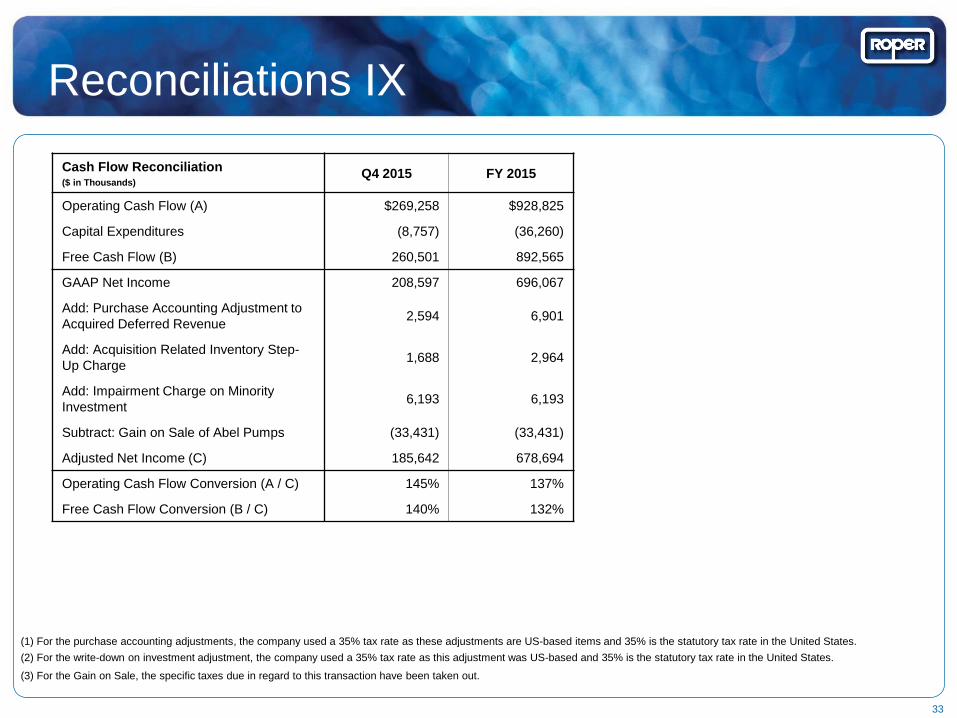

Reconciliations IX

Cash Flow Reconciliation ($ in Thousands)

Q4 2015 FY 2015

Operating Cash Flow (A) $269,258 $928,825

Capital Expenditures (8,757) (36,260)

Free Cash Flow (B) 260,501 892,565

GAAP Net Income 208,597 696,067

Add: Purchase Accounting Adjustment to

Acquired Deferred Revenue 2,594 6,901

Add: Acquisition Related Inventory Step-

Up Charge 1,688 2,964

Add: Impairment Charge on Minority

Investment 6,193 6,193

Subtract: Gain on Sale of Abel Pumps (33,431) (33,431)

Adjusted Net Income (C) 185,642 678,694

Operating Cash Flow Conversion (A / C) 145% 137%

Free Cash Flow Conversion (B / C) 140% 132%

(1) For the purchase accounting adjustments, the company used a 35% tax rate as these adjustments are US-based items and 35% is the statutory tax rate in the United States.

(2) For the write-down on investment adjustment, the company used a 35% tax rate as this adjustment was US-based and 35% is the statutory tax rate in the United States.

(3) For the Gain on Sale, the specific taxes due in regard to this transaction have been taken out.

Roper Technologies, Inc.