Quotas and Voting Shares in the IMF: Theory Mart´ ın Gonzalez-Eiras Universidad de San Andr´ es * May 15, 2008 Abstract Member countries of the International Monetary Fund (IMF) contribute to a pool of resources that is later used to extend credits. A member’s quota, its share in the IMF capital, determines not only the required financial contribution but also its voting weight and influence on policy. Heterogeneity among members in terms of population, wealth, and integration to international markets has recently produced a debate about the methods used for quota determination, that so far led to the approval in April 2008 of a partial reform in the quota system. With the aim of contributing to this debate, I address the question of the optimal determination of voting weights in the IMF. To this effect I adapt the model of Barber`a and Jackson (2006) of optimal voting rules in a heterogeneous union. The model predicts that member states’ votes be weighted according to their share in world exports, income per capita, and the level of foreign reserves. Voting thresholds should increase with the importance of international finance positions relative to trade flows, and with the importance of moral hazard inefficiencies associated with IMF lending. 1 Introduction The International Monetary Fund (IMF) is a financial institution founded in 1944 with the main purpose of assisting members facing temporary balance of payments problems. From an initial membership of 44 states, today almost all the countries in the world participate in it. Members of the IMF do not have equal power. They contribute a quota subscription of financial resources, and this quota is the basis for determining voting power. Historically, quota allocations have been based mainly on economic size and external trade volume. Heterogeneity among members in terms of population, wealth, and integration to international markets has recently produced a debate about the methods * Vito Dumas 284, B1644BID Victoria, Pcia. Buenos Aires, Argentina. E-mail: [email protected]. I want to thank Andr´ es Drenik for research assistance, and Lawrence Broz, John Hassler, Enrique Kawa- mura, Dirk Niepelt, Torsten Persson, Mart´ ın Rossi, James Vreeland, and conference participants at IIES Stockholm University, Universidad de San Andr´ es, PEIO meeting (Monte Verit´ a 2008), and Workshop on Global Interdependence (Barcelona 2008) for comments. All errors are mine. 1

Transcript

Quotas and Voting Shares in the IMF: Theory

Martın Gonzalez-EirasUniversidad de San Andres∗

May 15, 2008

Abstract

Member countries of the International Monetary Fund (IMF) contribute to apool of resources that is later used to extend credits. A member’s quota, its sharein the IMF capital, determines not only the required financial contribution but alsoits voting weight and influence on policy. Heterogeneity among members in terms ofpopulation, wealth, and integration to international markets has recently produceda debate about the methods used for quota determination, that so far led to theapproval in April 2008 of a partial reform in the quota system. With the aim ofcontributing to this debate, I address the question of the optimal determination ofvoting weights in the IMF. To this effect I adapt the model of Barbera and Jackson(2006) of optimal voting rules in a heterogeneous union. The model predicts thatmember states’ votes be weighted according to their share in world exports, incomeper capita, and the level of foreign reserves. Voting thresholds should increase withthe importance of international finance positions relative to trade flows, and withthe importance of moral hazard inefficiencies associated with IMF lending.

1 Introduction

The International Monetary Fund (IMF) is a financial institution founded in 1944 withthe main purpose of assisting members facing temporary balance of payments problems.From an initial membership of 44 states, today almost all the countries in the worldparticipate in it. Members of the IMF do not have equal power. They contribute a quotasubscription of financial resources, and this quota is the basis for determining votingpower. Historically, quota allocations have been based mainly on economic size andexternal trade volume. Heterogeneity among members in terms of population, wealth, andintegration to international markets has recently produced a debate about the methods

∗Vito Dumas 284, B1644BID Victoria, Pcia. Buenos Aires, Argentina. E-mail: [email protected]. Iwant to thank Andres Drenik for research assistance, and Lawrence Broz, John Hassler, Enrique Kawa-mura, Dirk Niepelt, Torsten Persson, Martın Rossi, James Vreeland, and conference participants at IIESStockholm University, Universidad de San Andres, PEIO meeting (Monte Verita 2008), and Workshopon Global Interdependence (Barcelona 2008) for comments. All errors are mine.

1

used for quota determination. In response to this, and also in the face of mountingcriticism from academics and policymakers, the IMF embarked in September 2005 on alarge-scale program of modernization. Salient among its objectives was governance reform,including adjusting quota shares to “reflect better the relative weight of members in theworld economy”. In April 2008, a reform proposal representing a step in this directionwas approved.

In the past decade there have been many reform proposals that focused on differentaspects of IMF governance. Buira (2005), among others, calls for using PPP measuresof GDP in the current quota formulas as a way to increase participation of developingcountries and thus improve the Fund’s “legitimacy”. This suggestion was the subjectof heated debate, and eventually incorporated in the reform proposal approved in 2008.Vaubel (2005) identifies as a problem the separation between the ultimate principals andthe IMF executive directors, Woods (2005) calls for an increase in accountability, some-thing that Frey and Stutzer (2006) suggest can be achieved through citizen participationin decision making. Bird and Rowlands (2005) suggest reforming the quota system argu-ing that the post-Bretton Woods IMF has made the use of quotas for the simultaneousdetermination of contributions, access and voting rights untenable. To the best of myknowledge, none of these, and other, reform proposals has been founded on a model ofexpected utility maximization.

I derive a micro-founded model to study the optimality of the quota system. Thisrelates to several issues. First, determining under what assumptions a quota system isindeed optimal. This is a relevant question considering that some reform proposals (O’neilland Peleg (2000) and Rapkin and Strand (2006) for example) call for a double majoritysystem for votes in the IMF. To answer this question I will first characterize the optimalvoting rule and then see when this can be represented by a weighted voting rule as usedin the IMF. The second issue relates to the determination of members’ voting weights.The third issue is the optimal determination of total quotas, and thus how the volume ofIMF financial resources should relate to the conditions of the world economy.

Having the IMF as an institution in which each member has a representative whovotes on behalf of the citizens of her country, I adapt Barbera and Jackson (2006) modelof optimal voting rules. Votes at the IMF take place over two alternatives: whether ornot to bailout a member country in crisis.1 An optimal voting rule seeks to maximizea welfare function that takes into account the utilities of all citizens represented in theIMF. I show that, under certain assumptions, an optimal voting rule consists of a weightfor each country’s vote and a threshold that indicates how large the total weight of votescast in favor of a bailout must be in order to implement the policy.

When making a decision for a particular vote, members of the IMF weight the benefitsand costs that a bailout would have on their citizens. Benefits are assumed to relate totrade linkages, and costs are assumed to originate from moral hazard inefficiencies affectingnet factor income from abroad. When benefits outweigh costs a country will vote in favorof a bailout, and when the costs are larger than the benefits, the country will oppose abailout. Votes are weighted by the ex-ante average intensity of preferences of citizens with

1The formalization generalizes in a straightforward way to cases in which a number of member countriesface a crisis simultaneously and the decision is whether to assist all of them, a subset of them, or none.

2

respect to the choice they make. If the tally of weighted votes in favor of the bailout islarger than the one against it the bailout is approved. Thus, votes are determined by the“externalities” that a given bailout have on the welfare of other members, and financialaid is approved only if the average positive effects dominate the negative ones.

To determine how a crisis abroad affects the welfare of a member country’s citizens,I use a static model of aggregate demand and have the foreign crisis triggering a realexchange rate shock to each member’s current account due to trade linkages with thecrisis country. The direct effect are proportional to the size of trade with the crisiscountry as exports to it would decrease, and imports from it increase. Since a countrycan dampen the effect that a crisis abroad has on its real exchange rate through the useof international reserves, the welfare impact would be decreasing in the stock of foreignreserves held. Under the assumption that the marginal utility of income is decreasing,welfare effects are larger for poorer countries.

The model predicts that the IMF would be more likely to provide assistance to bigger,more open countries. I test this prediction using the same dataset that Barro and Lee(2005) use to study the effect of IMF programs on economic performance. While they findthat size measured by GDP is a strong predictor of the probability of being bailed out bythe IMF, adding trade flows makes the influence of GDP to be statistically insignificant.Another prediction of the model is that voting thresholds should be increasing in theimportance of capital flows relative to trade flows. An extension that allows the possibilitythat financial aid from the IMF has moral hazard effects on members policies indicatesthat the threshold of votes needed to approve a bailout should be increasing in the severityof the moral hazard problem.

The remainder of the paper is structured as follows. Section 2 summarizes the historyand salient features of the IMF governance, while section 3 reviews the quota reform ap-proved in April 2008. Section 4 describes the model, and some regression results. Section5 discusses quota distribution according to the theoretical model. Section 6 concludes.

2 The IMF

Since its foundation, the IMF has made efforts “to foster global monetary cooperation,secure financial stability, facilitate international trade, promote high employment andsustainable economic growth, and reduce poverty”. But the roles it has played havechanged since the fall of the system which has brought the IMF into life: the BrettonWoods Agreement. Before 1973, the IMF was basically focused on developed countries:from 1947 to 1967 they have represented almost 70% of the total amount of resourceswithdrawn. After the liberation of the world exchange rate regime in 1973, the mainusers of the IMF resources shifted from developed countries to emerging economies inAfrica and Latin America with balance of payments crisis. This has widened the alreadydivergent preferences between more or less developed countries on policy issues, and thedisagreement over how this preferences are to be aggregated into collective decisions.

Decisions in the IMF are made by weighted majority of votes. The power structure isorganized in the following way: the Board of Governors, which possesses all the powers

3

of the Fund, is composed by representatives from all member countries. Each countryinitially received 250 basic votes plus one additional vote for each hundred-thousandSpecial Drawing Rights (SDRs) that it possesses. The basic votes were a compromisesolution intended to reconcile the principle of sovereign equality with the fact of widepower asymmetries among members. The ratio of basic votes to total votes increasedfirst, as new countries joined the IMF, reaching a historic high of 15.6% in 1958. Totalquota increases thereof made this ratio decrease to roughly 2%, while the quota reformapproved in April 2008 increased basic votes and introduced a mechanism to stabilizetheir number at 5.5% of total votes.2 While initially there was a single formula for thecalculation of quotas, in the early 1960s a complex multi-formula method was devisedto determine quotas on the basis of GDP, exports and imports, variability of exportreceipts and reserves. While this allowed differing weights for the calculation of quotasfor developed and developing countries, there was a significant loss of transparency. For awhile ten formulas were used, later to be replaced by five, a system that was in place up tothe reform of 2008 that returned to a single formula. There is no rationale for using theseand not other variables, nor for the weights attached to them in the mentioned formulas.In fact it appears that the formulas, as well as actual quotas, which in some cases divergesignificantly from the calculated ones, are biased to produce a political outcome close tothe one desired by the most powerful members of the IMF.3 One of the objectives of thereform of 2008 is to increase the credibility of the IMF by increasing the transparency ofthe quota determination process, and by realigning actual quotas with calculated ones.

The Board of Governors can delegate certain decisions to the Board of ExecutiveDirectors, which is composed of one representative from each of the five members of theFund having the largest quotas plus 19 other representatives, some of whom represent acertain subgroup of countries. Thus, each Executive Director has the number of votesequal to the sum of votes of the countries it represents. In this way, when the Boardof Directors vote, there is at the beginning a first meeting in which each subgroup ofcountries determines how their representative will vote. Then, the Board of ExecutiveDirectors meets and cast their vote. There are two different majority rules and theiruse depends on the issue being discussed at the moment. The first one, which requiresa 70% majority, is used for issues of procedure (decisions involving matters of policyand operations) and the second one, which requires an 85% majority, is used for issuesof substance (for example, constitutional revisions or changes in quotas). An importantobservation of these majority rules and voting system is that the United States is the onlycountry who retains a veto power since it possesses more than 15% of the total quotas.

The quota system serves several functions, which creates the possibility of conflict,as pointed by Bird and Rowlands (2005). A members quota defines four aspects of therelationship between the member country and the IMF: first, the amount of financialresources that members contributes to the Fund; second, the amount of resources thatthey can draw from the IMF; third, their voting power in institutional decision making,and finally, the members share of SDR allocations. Related to the question of how are

2Section 3 will review in more detail the quota reform approved in April 2008.3Mikesell (1944) acknowledges that the original Bretton Woods formula used to assign quotas among

the first 44 members of the IMF were built with the objective to match a desired outcome.

4

quotas determined, since its foundation, the IMF recognized that as it was going tomake large disbursements of scarce financial resources, their decisions would have to belegally binding rather than merely advisory. More egalitarian decision methods, say a one-country, one-vote rule, would not be acceptable to the major powers that contribute thebulk of the IMFs resources. Accordingly, a scheme was devised by which each nationalmember of the IMF has a quota that roughly equates its voting power to its financialsubscription to the organization.4

General Quota Reviews are typically undertaken at five-year intervals with the ob-jective of adjusting to changes in members’ relative position in the world economy, aswell as to accommodate new members. Each quota increase is divided at the discretionof the Board into an equiproportional and selective components. The former is akin toan expansion of capital, simply extending proportionally the existing quotas, while thelatter tends to shift the new quotas towards the calculated ones. Since historically theequiproportional component has averaged 70% of the quota increases, there has been asignificant status quo in the distribution of power in the IMF.

3 April 2008 Reform of Quota and Voice

In March 2008 year the Executive Board presented a reform package of its quota systemthat a month later was approved by the Board of Governors. The proposal was thefinal product of extensive discussions at the Executive Board along the guidelines set inthe Fund’s Annual Meeting in Singapore in September 2006, and aimed at realigningmembers quota shares with their relative economic weight. The participation and voiceof low-income countries was enhanced through a substantial increase in the number ofbasic votes, and a mechanism that will maintain the ratio of basic votes to total votesconstant in the future. Furthermore, the IMF will seek to make quotas and voting sharesmore responsive to changes in economic realities in future General Quota Reviews.

A salient characteristic of the reform is that quotas are once again calculated using asimple formula. This improves the transparency of governance at the IMF and helps inbetter reflecting the members’ relative position in the global economy. In coming up withthis formula the Board has taken into account a number of restrictions, which include themultiplicity of roles that quotas have, that they be based on available data, and that theybe politically feasible. The new formula proposed includes four economic variables, GDP,openness, variability and reserves, expressed in shares of global totals. The weightedaverage is then compressed in order to reduce dispersion in calculated quota shares,

ICQ = (0.5Y + 0.3CC + 0.15V + 0.05R)k

were ICQ is the intermediate calculated quota share, Y is a weighted average of GDPconverted at market exchange rates and PPP exchange rates averaged over a three yearperiod. The weight on market-based GDP is 60%. CC is the annual average of the sum ofcurrent payments and current receipts for a five year period. V is the variability of current

4The presence of basic votes introduces a wedge between financial subscription and voting power,which is significant specially for less developed countries.

5

receipts and net capital flows, measured as a standard deviation from the centered three-year trend over a thirteen year period. R is the average over a year of official reserves,and k = 0.95 is a compression factor. Calculated quotas are obtained after rescaling thesum of ICQ to 100.

The computation of GDP both at market rates and at PPP rates reflects a compromisebetween the position of developing countries which supported the later as a better estimateof the relative volume of goods and services produce by their economies, and the positionof developed countries which see market rate GDP as the relevant indicator, particularlyas a measure of the contributive power of members. The compression factor is an artifactto moderate the dispersion of calculated quotas. Given the limitation of the new quotaformula in enhancing the voice of emerging economies, a tripling of basic votes was decided,a measure that increases vote share beyond quota share for less developed nations. Theinclusion of PPP GDP and the compression factor were one of the more controversialaspects of the reform proposal and the Executive Board has decided to include them inthe formula for a period of 20 years. At the end of this period the argument for retainingthese components would be reviewed. The quota formula only calculates the relativequota of IMF members. Total quota determination continues to be discretionally decidedat General Quota Reviews.

4 Model

There are n countries in the IMF, which are heterogeneous in terms of population, wealth,and integration to the world economy. Country i has a population of pi citizens, all ofwhom derive the same utility u(ci) from per capita consumption ci. It is known that,with some probability, a subset of the member countries will suffer a negative balance ofpayments shock, in which case a decision will have to be made on whether to financiallyassist the affected country, or countries. For ease of exposition I will assume that only onecountry, country j, might experience a balance of payments shock, and later show thatthe analysis extends to a multi-country crisis. A state of the world is then a descriptionof members’ preferences on whether to assist or not country j. Without loss of generalityutilities can be normalized to zero if the status quo prevails and no assistance is provided,and preferences are then denoted by a vector ~u(j) ∈ Rn with element u(j)i ≡ uij beingthe utility of a representative agent in country i if country j is bailed out.5

After a shock takes place, each country’s representative will decide to vote for a bailoutor not, based on whether the utility of a bailout is positive or negative for that country’scitizens. Thus the representative’s voting behavior can be represented by a functionhi : R −→ {b, nb}, which maps the preferences of citizens into a vote. The notationhi(uij) = b indicates that the representative of country i votes in favor of a bailout. Thisindicates that uij > 0, and equivalently a no bail out vote, hi(uij) = nb, indicates thatuij < 0.

In a second stage, the votes of the representatives are aggregated according to a voting

5Thus uij ≡ u(cbi ) − u(cnb

i ) were the superscripts differentiate consumption when country j is bailedout or not.

6

rule. Let v : Rn −→ {0, 12, 1} denote the outcome of this two-stage voting procedure as

a function of the state of the world, ~u(j). Here v(~u(j)) = 1 indicates that a bailout isapproved, v(~u(j)) = 0 means that country j will not be assisted, and v(~u(j)) = 1

2denotes

a tie that will be resolved by the toss of a coin.Let an efficient voting rule be one that maximizes the expected social welfare function

among the class of feasible voting rules.6 The social welfare function is given by theexpected total utility, giving equal weight to any citizen of the IMF, independent of thecountry of residence. Therefore I will consider voting rules that maximize the followingwelfare function:

E

[∑i

v(~u(j))piuij

]

were the expectation is taken over the distribution of balance of payments shocks, givenby µ(·), affecting any subgroup of the countries in the IMF. It will be initially assumedthat the probability and severity of a crisis in country j, characterized by distributionfunction, is independent of the policies it follows, i.e. that v(·) has no effect on µ(·). Iwill later lift this assumption, and study how the optimal rule is determined when theexpectation of a bailout affects countries policies and thus the probability distribution ofbalance of payments shocks.

Three alternatives for the informational content of votes, and contingency of the vot-ing rule v(·) on them will be considered. The first case is one in which the underlyingpreferences, uij are publicly observed (or correctly inferred from the state of nature). Inthis case it is trivial to see that the optimal voting rule is determined by,

vE(u) =

1 if∑

i uij > 0,0 if

∑i uij = 0,

12

if∑

i uij < 0.

Of more interest is the case in which a country’s vote does not perfectly indicate theintensity of preferences for a given choice. For this case consider the following voting rule,proposed by Barbera and Jackson (2006). For each country, and for each possible state,two weights are assigned, one when the country votes in favor of bailing out country j,and another for votes against this. For the former we have,

wbij = piE[uij|uij > 0, j]

Therefore the weight assigned to country i is proportional to the total expected welfareof its citizens when a bail-out of country j is indeed their preferred policy. Similarly, theweight assigned to country i when it votes against the bail-out is given by,

wnbij = −piE[uij|uij < 0, j]

The efficient voting rule vE(u) is then defined by,

v(~u(j)) =

1 if∑

i:hi(~u(j))=b wbij >

∑i:hi(~u(j))=nb wnb

ij ,

0 if∑

i:hi(~u(j))=b wbij <

∑i:hi(~u(j))=nb wnb

ij ,12

if∑

i:hi(~u(j))=b wbij =

∑i:hi(~u(j))=nb wnb

ij .

6These are voting rules that depend only on the information obtained by the votes of the representa-tives.

7

Proposition 1. If preferences are independent across countries (meaning that one coun-try’s utility for a given alternative does not depend on the full profile of votes of the restof the countries), then a voting rule is efficient if and only if it is equivalent up to ties tovE.

This result is Theorem 1 in Barbera and Jackson (2006) and the proof is in theirappendix.

It could be possible that for political reasons the voting rule can not be made contingenton the identity of the crisis country. Ex-ante some potential members of the IMF mightfeel unfairly treated by such a tailor-made governance structure and would not decideto join the organization. In that case it makes sense to consider what is the optimalvoting rule when the rule must satisfy an additional restriction, mainly that it can not becontingent on the state of the world. If we redefine the above voting rule correspondinglywe get that each country is assigned the following weights when voting in favor or againsta bail-out, irrespective of who is in need of financial assistance,

wbi = piE[uij|uij > 0] (1)

wnbi = piE[uij|uij < 0] (2)

where now expectations are taken ex-ante over the joint probability distribution of thelikelihood and severity of a crisis in country j and over the effect this has on prefer-ences of citizens in country i. The efficient voting rule is defined as before replacing thecorresponding weights in the summations. As we are now considering a non-contingentvoting rule we can assume wlog that ex-post the intensity of preferences, uij, are publiclyobserved. This simplifies the calculation of the weights wb

i and wnbi .

Under this rule, weights are affected by the intensity of preferences inside a countryfor the alternatives, as captured by the values of uij. Thus countries that on average caremore intensely about a bailout decision should be given more weight than countries thatare less affected by the outcome. In their work, Barbera and Jackson consider an abstractdecision between two alternatives and therefore have no reason for heterogeneity amongmembers’ intensity of preferences. They thus give every citizen of the union the samepossible utilities, of plus one or minus one. Given the nature of the problem studied hereI introduce more structure about countries’ preferences and the extent to which a shockin country j affects a representative citizen in country i.

To relate the intensity of preferences, uij, to fundamentals I assume CRRA preferences(with coefficient of risk aversion θ) over per capita consumption ci,

u(ci) =1

1− θc1−θi .

I assume a static model of aggregate demand in an open economy where aggregate incomeis given by aggregate demand, Yi, plus net factor income from abroad, Zi. Aggregatedemand is given by consumption, investment, and net exports. The following behavioralrelations characterize the components of aggregate income, were for simplicity subindex

8

i has been suppressed,

C = C0 + C1(Y + Z(ε)) I = I0 (3)

NX(ε) = X(ε)− εM(ε), X ′(ε) > 0, M ′(ε) < 0 (4)

Z(ε) = rF − r∗F ∗ = (rF )(ε)− (r∗F ∗)(ε). (5)

where C is consumption, I investment, NX are net exports of goods and services (Xbeing exports and M imports), F and F ∗ are foreign assets and liabilities, r and r∗ arethe, possibly different, interest rate charged and paid on those foreign positions, and ε isthe real exchange rate. The equilibrium relations for aggregate demand and consumptionare,

Y =1

1− C1

(C0 + I0 + C1Z(ε) + NX(ε)) (6)

Y = m (Y0 + C1Z(ε) + NX(ε)) (7)

C = mC1

(C0 + Z(ε) + NX(ε),

)(8)

where m is the multiplier of aggregate demand to external shocks. As Fischer (1999) pointsout, a bailout prevents the overshooting of real exchange rate depreciation in country j.Thus a bailout produces a relative appreciation of the real exchange rate in country j,αj = −∆εj

εj> 0.7 Under the assumption that the Marshall-Lerner condition holds, a

currency depreciation, ∆εε

, has a positive effect on net exports of,

(εX,ε + εM,ε − 1)(X + εM)

2

∆ε

ε≡ a(X + εM)

∆ε

ε

were it is assumed that trade is balanced (i.e. X = εM = X+εM2

), and I will assume thatthe elasticities characterizing the response of net exports, represented by parameter a, arethe same for all countries. Thus, the effect of a bailout in country j on net exports incountry i is given by,

∆NXi = a(Xi + εiMi)−εj

εi

dεi

dεj

αj (9)

a(Xi + εiMi)Xij + εiMij∑k Xik + εiMik

αj (10)

aαj(Xij + εiMij) (11)

were in the first expression, ∆εi

εi=

−εj

εi

dεi

dεj

−∆εj

εj=

−εj

εi

dεi

dεjαj, and

−εj

εi

dεi

dεjis the impact of

a real exchange rate appreciation in country j on the real exchange rate in country i.This effect is assumed to be proportional to the fraction of bilateral trade between bothcountries, as reflected in the second expression.

A bailout of country j has also negative effects in country i. It increases expectedmoral hazard problems on all financial relations between country i and the rest of the

7Therefore, αj is a measure of the magnitude of the balance of payment shock in country j, since adeeper crisis would cause a larger deviation in the real exchange rate if the status quo prevails.

9

world, and thus has a negative impact on net factor income from abroad, Zi.8 Income

received from foreign assets held by citizens in country i, riFi experiences a reduction inexpected principal recovery, and income paid to foreigners holding domestic assets, r∗i F

∗i

increases due to risk premia. This effect is modeled to take the form,

∆Zi = −δmi

∑

k

(Fik + F ∗ik)

thus δmi measures the percentage impact that a bailout has on income derived fromfinancial positions. With the notation |F | ≡ F + F ∗, and with consumption per capitagiven by c ≡ C

pwe have

uij = ∆u(ci) = c−θi ∆ci = c−θ

i miC1i(∆NXi + ∆Zi)

pi

(12)

uij = c−θi miC1i

(αa(Xij + εiMij)− δ

∑k |Fik|

pi

)(13)

were c−θi is the marginal utility of consumption for country i, a term that reflects that

poorer countries are, ceteris paribus, more affected by a crisis abroad. The model there-fore assumes that the positive effects for country i when country j is bailed-out arisefrom trade links between countries i and j. Negative effects are proportional to financialrelations between country i and the rest of the world. According to this representationfor preferences, a country would be more likely to support a bailout of another countryin crisis when it has strong trade relations with this country. And it is less likely to votefor a bail-out the more financially integrated it is with the rest of the world.

Next we will make assumptions on the structure of trade flows between countries iand j and on the size of financial relations that a country has with the rest of the world.These take the form,

Xij + εiMij = (Xi + εiMi)Xj + εjMj

dij(∑

k Xk + εkMk)(14)

|Fi| = b(Xi + εiMi) (15)

were dij is proportional to the distance between countries i and j and tries to capture“gravity” effects. Thus I assume that trade between two countries is proportional to theirvolume of trade and inversely proportional to their distance, and that financial positionsare proportional to trade flows. The first assumption is made since it has been provedempirically that bilateral trade decreases with the distance between trading countries.With respect to the second assumption, it can be verified that there is indeed a strongcorrelation between both variables in the data at any given point in time.9

8In reality this negative effect should affect future net factor income but for simplicity I abstract ofintertemporal considerations in the model.

9From the EWN II dataset collected by Lane and Milesi-Ferretti (2006). Their figure 4 shows thatfor aggregate numbers the trade in assets increased at a faster rate in industrialized countries thanin emerging markets since the late 1980s. Country level data cross-section regressions, with five-yearaverages, show a strong correlation between external assets and liabilities and product trade throughouttheir whole sample period, 1970-2004. The assumption of proportionality is crucial to collapse weightsto a single variable and obtaining a simple weighted formula, as shown below.

10

An important caveat is that this formulation would imply that any country j thatexperiences a shock would have the same effects on other countries mutual net factorincome from abroad (for example between i and k). Although it might seem more reason-able to assume that the effects of a shock are increasing with the crisis country economicsize, or the magnitude of its balance of payments shock, what matters for the result isthat the positive, trade-related, effects be more sensible to scale factors than the negativeeffects related to net factor income. It is for simplicity that the latter are assumed to beindependent of the characteristics of a given bailout package.10

With this formulation all countries i such that uij > 0 would vote in favor of bailingout country j when in crisis. An inspection of country preferences shows that i wouldbail out all countries j such that,

αjaXj + εjMj

dij(∑

k Xk + εkMk)> δb

were I have assumed that model parameters a, and δ are the same across countries. Thus,countries experiencing a significant imbalance (high α) are more likely to be assisted, anda bailout will have more support among neighbors of the country experiencing the shock.Big, open, countries would be more likely to be bailed out than small, closed, ones. Ofcourse it must be recognized that during a crisis country j, regardless of its size, would voteto bail itself out. But this trivial, symmetry-breaking, vote becomes negligible in the limitof an infinite number of countries, all of atomistic size, assumption made henceforth.11

Under this assumption, and having the probability that a country experiences a balanceof payments shock, µ(α, q, y,~t), i.e. as a function of its participation in world trade,

measured with respect to average trade volume, q ≡ (Xj+Mj)

E[X+εM ], its income per capita, y,

and its location in the world, given by ~t. With the distance between countries i and jgiven by dij = |~ti − ~tj| ≡ ρ, and with ψ∗ ≡ δb

awe have,

wbi = c−θ

i miC1i(Xi + εiMi)

∫

~t

∫ α

0

∫ ∞

ρψ∗α

∫ y

0

(αaq

ρ− δb) µ(α, q, y,~t) dy dq dα d~t

wnbi = −c−θ

i miC1i(Xi + εiMi)

∫

~t

∫ α

0

∫ ρψ∗α

0

∫ y

0

(αaq

ρ− δb) µ(α, q, y,~t) dy dq dα d~t

where α is the maximum balance of payments shock that a country can experience, andy the maximum possible income per-capita. We impose now an homogeneous distribu-tions of countries around the globe, and independence of the structure of shocks with thegeographical distribution of countries, i.e. µ(α, q, y,~t) = µ(α, q, y). Under these assump-tions, the integrals in the previous expressions are independent of country i, and we have

thatwnb

i

wbi≡ γ is constant for all countries. Here γ measures a bias towards the status

quo (there is more intensity in preferences towards the status quo if γ > 1). This is the

10Remember also that the negative effect relates to future income, and not contemporaneous effects onasset prices directly due to the bailout.

11Similar results would be found if the voting rule excludes from the vote the country that is requestingfinancial assistance.

11

same formulation with a bias factor that Barbera and Jackson (2006) assume in order toderive the result that an optimal voting rule is efficient if and only if it is equivalent to aweighted voting rule (their Corollary 1). Under these assumptions therefore it would notbe optimal to have a double majority system for votes in the IMF as advocated in somereform proposals.12 In this case the optimal weights are:

w∗i = wb

i

and the threshold for approving a bailout is

γ∑

i w∗i

1 + γ

The threshold of votes is increasing in the bias γ and thus we can see how it is affectedby structural parameters, such as the importance of international financial investmentsrelative to trade flows, b, or the distribution of crisis probabilities across countries, µ(·),which affects the integrals of wb

i and wnbi . In particular we mentioned in Section 2 that

before the fall of the Bretton Woods system the IMF worked like a credit union assistingmainly developed countries, afterwards switching to an asymmetric arrangement of netcreditor developed countries and net borrower emerging countries. This means that in thepost Bretton Woods world the density distribution µ(·) changed, shifting mass from thefirst integral above to the second one, reducing wb

i and increasing wnbi , thus increasing γ,

and therefore the optimal vote threshold. An increase in b, the size of financial positionsrelative to trade flows, would also lead to an increase in γ. This can be observed in thedata using gross external positions (from Lane and Milesi-Ferretti (2006)) and trade data.This prediction is consistent with the evolution of decision making at the IMF. There hasbeen an increase both in the largest required supermajority (from 80% to 85%, in 1969),and in the number of decisions requiring supermajorities (from originally 9 to more than50 currently).13

Structural parameters also affect the total quota subscription under the optimal votingrule. This is given by

∑i w

bi , and accordingly should increase proportionally to trade when

the structural parameters are unaffected. But if the density distribution µ(·) changes,shifting mass from the first integral above to the second one reducing wb

i , the ratio oftotal quota subscription to world trade would decrease. This behavior has been observedin the data for the post Bretton Woods period.

With respect to the possibility of a multi-country crisis, remember that a bailout’snegative effects are assumed to be independent of the size of the country being bailedout. Thus the negative effects would be the same independently of how many countriesare assisted by the IMF. Therefore the criteria to decide whether to help the countriessuffering the balance of payments shock is the same as if all of them were lumped intoa larger country. Notice how this gives incentives to small countries to distort domestic

12For example see O’neill and Peleg (2000) and Rapkin and Strand (2006).13It should be noted that the majority for a bailout decision remains at 70% of weighted votes. But

other procedural decisions that indirectly relate to country programs saw their majority requirementsincrease.

12

policy with the objective of increasing the correlation of their balance of payments shockswith those of bigger economies, thus increasing the chances of a bailout when one isneeded.

4.1 International Reserves

It is possible to add a role for international reserves in the basic model. The main reasonfor doing this is that the model emphasizes trade and finance links between countries asthe determinants of the intensity of preferences regarding the bail out decision of distressedcountries. And since a country that has a higher level of reserves is better prepared tobuffer the effects of an external shock, this should be reflected in its voting power. Withrespect to the positive effects of a bailout, a higher level of reserves in country i reducesthe impact of real exchange volatility in country j on the real exchange rate in country i.Thus the positive effect for country i of bailing out country j is reduced to,

aαj(Xij + εiMij)f(Ri)

were f(·) is a decreasing function of the level of international reserves R, and f(0) = 1.14

With respect to the negative effects of a bailout, a higher level of international reservesreduces the loss in net factor income from abroad as there is no loss in income receivedfrom foreign reserves. This should not be confused with the fact that holding a largershare of foreign assets as reserves leads to a reduction in income received from theseassets.15 What matters for the bail out decision is the change in this income due to thenegative effects a bailout has on financial positions. Thus the negative effect for countryi of bailing out any country is reduced to,

−δmi

∑

k

(Fik + F ∗ik)g(Ri)

were g(·) is a decreasing function of its argument and g(0) = 1. With this modification itis straightforward to derive the weights wb

i and wnbi that a country should receive when it

votes in favor or against a bailout. To guarantee that the integrals in those expressionsremain independent of country i, and thus to have a common bias factor γ, we need toimpose that g(·) = f(·). Under this assumption the result that a weighted voting rule isoptimal still holds. Now weights are given by,

w∗i = c−θ

i miC1i(Xi + εiMi)f(Ri)

∫

~t

∫ α

0

∫ ∞

ρψ∗α

∫ y

0

(αaq

ρ− δb) µ(α, q, y,~t) dy dq dα d~t

It should be noted that the model predicts that, controlling for other determinants, coun-tries having larger positions of foreign reserves should have less power in IMF decisionmaking. This contrasts with the fact that all past and present formulas for quota deter-mination in the IMF give a positive weight to reserves.

14Alternatively the argument of function f(·) could be the ratio of reserves to aggregate income, ortrade volume.

15The “optimal” level of international reserves might be affected by the cost of holding them, tradedagainst the benefits that having a large position of reserves has as a buffer against external shocks.

13

4.2 Moral Hazard

To be done.

4.3 Empirical Evidence

Since the weights are determined independently of the threshold (since they are indepen-dent of γ), we can use the actual distribution of quotas in the IMF in the postwar periodto test if it is “optimal”. We now proceed with this estimation.

4.4 Econometric Specification

It is almost straightforward to derive a regression equation to estimate the previous model.This structural econometric approach contrasts with typical analysis of the distribution ofquotas in the IMF that resort to a reduced-form aproach. A minor adjustment has to bedone in order to derive the regression equation. This is to include foreign reserves as anexplanatory variable. The reason to add this variable is that a country with more foreignreserves is in a better position to buffer an output slowdown associated with a currentaccount shock originated abroad.16 This intertemporal smoothing is not captured by thesimple static model, but since it could reduce the intensity of preference with respect tothe bailout decision, and thus the optimal weights, we should control for it.

Under the assumptions used to derive the optimal weights, namely that we consider thelimit of a large number of countries (to avoid symmetry breaking by a crisis country votingin favor of its own bailout), independence of shocks from the geographic distribution ofcountries, equality of multipliers, m, and structural parameters (a, and δ) the regressionequation to estimate is derived by taking logarithms in equation (16). This gives,

Although the model predicts that β1 = 1, it is not true that the multiplier is independentof trade openness. A more open country would have a smaller multiplier, and thereforea lower quota. Thus the coefficient of TRADE is expected to be positive but less thanone. We further expect β3 to be negative. If the social welfare function gives the sameweight to every individual irrespective of their country of citizenship, β2 would be negative,otherwise its sign is indeterminate.17 Further controls will be added to test for the validityof the model. I will discuss those cases as they show up.

16See, for example, Hviding, Nowak and Ricci (2004). They estimate that a halving of reserves increasesreal exchange rate volatility by 20%.

17Another reason why β3 > 0 is that quotas serve the double purpose of determining country rep-resentation and capital contributions to the IMF. It is reasonable to assume that the latter should beproportional to GDP. Incorporating this in an objective function balancing representation and contri-bution capacity the weights would be w∗i = wb

i yψi , were ψ > 0 measures the relative importance of

contribution capacity in the welfare function.

14

4.5 Data

The data set was obtained from the International Financial Statistics (IFS), and WorldDevelopment Indicators (WDI). The sample is an unbalanced panel of five-year-averageobservations (for example the observation for 1975 corresponds to the average of thecorresponding variable from 1975 to 1979) for 184 countries over the period 1960-2004.The main reason to use five-year averages is that quota revisions are infrequent, andhave taken place at roughly five-year intervals (the longest period without a revision wasbetween June 1990 and January 1998). Table 1 introduces the variables used in the mainregressions to determine the relative quota of the IMF member countries.

The dependent variable is the logarithm of the relative share of quotas, net of basicvotes, that a country has in the IMF, QUOTA.18 With respect to independent variables,the logarithm of the total trade volume, TRADE, comes from IFS data on exports andimports, measured in current USD. The logarithm of GDP per capita, GDPPC, is con-structed using GDP from IFS measured in current USD, and population data comingfrom WDI. Since this last variable should capture the intensity of preferences, it wouldbe more accurate to use PPP measurements of GDP. Due to a lack of data I instead useGDP measured in current USD. The logarithm of foreign reserves, RESERV ES, usesdata from IFS measured in current USD. Given that quota decisions are based on pastperformance I used one period lag of these regressors.

Further controls are used to test for the validity of the model. To this effect a numberof dummies are introduced: continental dummies for OECD, Latin America, Asia, Africa,and former communist countries. Other dummies differentiate countries based on whetherthey were early or more recent members of the IMF. As discussed in Section 2, there issome inertia in the adjustment of quotas, which could give more power to early members.I used a dummy, EARLY, for countries that were members of the IMF before 1960.Another distinction that I want to control for is whether the Bretton Woods agreement isin place or not. Given the fact that the IMF’s role changed after the collapse of the fixedexchange rates system in 1973, I use a dummy, AFTER, for periods after that date.

4.6 Results

We will first test the model prediction that the volume of trade is an important determi-nant of the likelihood that a country would be bailed out by the IMF. To this effect I willuse a probit regression used by Barro and Lee (2005) to estimate the importance of po-litical economy variables in determining the likelihood of an IMF loan program approval.In their paper Barro and Lee use U.N. voting patterns and bilateral trade to measurea country’s political and economic proximity with the United States and the three bigEuropean countries (France, Germany and the United Kingdom), together with quotashares and the number of nationals working at the IMF. They find that these politicaleconomy variables help to explain the probability and size of IMF loan programs. In their

18Besides the fact that there is no rationale in the model for basic votes, representation beyond thesebasic votes is what the model explains. Furthermore, as seen in Section 2, the relative importance ofbasic votes has declined to close to two per cent of total votes nowadays.

15

regressions they use a number of controls, in particular the logarithm of GDP. Amongother results, they find that bigger countries are more likely to get a loan approval.

Results are reported on Table 2. In the first column I reproduce the probit regression ofBarro and Lee, and in the second column TRADE is introduced replacing GDP . Resultsshow that countries with more trade volume are more likely to be assisted by the IMF.And putting together both GDP and TRADE results in GDP losing its explanatoryvalue while the coefficient on TRADE remains positive and statistically significant.19

Thus the evidence supports the result found in Section 3 that IMF members are morelikely to approve a bailout the larger is the volume of trade of the country experiencing abalance of payments crisis.

Next, I test the model predictions with respect to quota distribution. In table 3 wepresent the output of three OLS estimations for IMF relative quota QUOTA, measured inlogarithms. All regressions control for time effects. Column 1 includes lagged GDPPC,TRADE and RESERV ES; column 2 includes continental dummies and column 3 in-cludes a dummy for the countries that have entered the IMF before 1965. The objective ofthese regressions is to find evidence of systematic deviations from the theoretical model.

The coefficient for TRADE is significantly positive in all of the specifications, im-plying that a 1 percent increase in trade would increase the relative quota by 0.86%.The coefficient on GDPPC is negative and significant in all of the specifications. Theestimated coefficient implies that a 1 percent rise in the GDP per capita in the past fiveyears would reduce the relative quota by 0.24%. Finally, the estimated coefficient forRESERV ES indicates a positive and insignificant relationship.

The geographic controls indicate that there are certain regional characteristics thataffect their relative quota, implying that it is better to use other estimation mechanism,as fixed effect estimator. It is found that asian countries are underrepresented in IMFrelative to the theoretical predictions of the model. This fact has been pointed out byseveral authors, for example, by Rapkin and Strand (2003), and it shows that there areunobservable factors explaining the distribution of power in the IMF beyond those impliedby the model of Section 3. Countries that entered early in the IMF have a significantlylarger quota share than more recent members. This is further evidence of the violationof the exogeneity assumption of our main regression, and is not surprising given that,as mentioned in Section 2, equiproportional increases of quotas are very important inGeneral Quota Reviews.

To address the problem of unobserved explanatory variables I do a fixed effects estima-tion. Results are presented in table 4. Column 1, reports the basic regression with laggedTRADE, GDPPC and RESERV ES. Column 2, presents the same variables interactedwith the EARLY and AFTER binary variables used to discriminate the model fit be-tween early and more recent members of the IMF, and whether the fall of the BrettonWoods agreement changed the allocation of quotas among members.

In column 1, TRADE enters with positive sign and it is strongly significant, suggestingthat an increase of 1 percent would, holding other variables constant, increase the relativequota by 0.14%. Under the fixed effect estimation, the coefficient of RESERV ES is

19This third regression omits the political economy controls mentioned above. If they were included,both GDP and TRADE are not significant in explaining the probability of approval of an IMF program.

16

negative and significant but the reduction of the relative quota implied by an increaseof 1% of the reserves is just 0.026%. Finally, the estimated coefficient for GDPPC ispositive and significant. An increase of 1 percent would augment the relative quota by0.13%.

As mentioned, the main objective of the specification presented in column 2 is toinvestigate if the relationship found in the precedent paragraph is constant over time andover groups of countries. We find evidence that there were systematic differences betweenearly and late members in the IMF for the period before the fall of the Bretton Woodsagreement. For example, the coefficient on TRADE for early members of the IMF was0.09 percentage points larger than the one on late members (for which the coefficient was0.077). After 1975 there are no statistical differences in the coefficients of the regressorsbetween early and late members of the IMF.

5 Reform proposal

Having derived a theoretical formula for the distribution of voting power among IMFmembers, it seems natural to ask the question of what that distribution would look like,and how it compares with current quota shares. To do that I use the following relation:

wi = (Xi + Mi)y−θi RES−κ

were RES are international reserves. Imposing a coefficient of 1 on trade, I set κ = 0.18to keep the same relative importance of reserves to trade as in the regressions reportedbefore (0.018 ≈ 0.026

0.14). For the coefficient on GDP per capita I consider two cases, θ = 1

3

and θ = 23. This will show how sensitive the distribution of votes is to GDP per capita.

Results for the largest members in the IMF are reported in Table 5 for the period 1995-2000 for which there is more data available. The first column reports actual relativequotas, while in the second column I use an ad hoc specification dependent only on trade.Results are very sensitive to the specification on GDP per capita as can be seen from acomparison of columns 3 and 4. Considering that the power of rich developed countriesgets diluted as we increase θ, a politically feasible proposal could be the one in column 4that maintains the US veto power.

Significant outlier among the members with quota shares above one percentage pointare: Argentina, Saudi Arabia, Switzerland, and Venezuela among the countries overrepre-sented in the IMF, and China and Mexico among the underrepresented. It is worth notingthat under this rule, the total quota of these big members would only reduce slightly, from73.3% to 72.6%. Therefore there are no significant gains in representation for small, lessdeveloped countries.

6 Conclusions

I have derived a theoretical model for the optimal calculation of quotas among membersof the IMF. Under simplifying assumptions a simple weighted voting rule is the efficient

17

voting rule. Optimal weights are proportional to a country’s volume of trade. Givenparticipation in world trade, quotas decrease with per-capita income and with holdings offoreign reserves. Furthermore, the model helps to determine the total quota for the IMF,a decision that has always been discretionally determined at General Quota Review.

The model has implication for the reform proposals that have been presented to im-prove the legitimacy of the IMF (See for example Cottarelli (2005) and Rapkin and Strand(2006)). In particular under the assumptions of the model, there is no rationale for a dou-ble majority system as the “count and account” proposal of O’Neill and Peleg (2000).Further research will be aimed at developing a more sophisticated model of income andconsumption determination, incorporating intertemporal considerations, and moral haz-ard.

References

[1] Allegret, J. and P. Dulbecco, (2003), “The Governance of International Institutions-The IMF and the Evolution of the New International Financial Architecture-”. Eco-nomics for the future - Celebrating 100 years of Cambridge Economics. Cambridge(UK) 17-19, September 2003.

[2] Barro R. J. and J. Lee, (2005), “IMF programs: Who is chosen and what are theeffects?”, Journal of Monetary Economics, vol. 52, pages 1245-1269.

[3] Bernstein, E. (1968), “The International Monetary Fund”, International Organiza-tion, vol. 22(1), pages 131-151, Winter.

[4] Barbera S. and M. Jackson, (2006), “On the Weights of Nations: Assigning VotingWeights in a Heterogeneous Union”, Journal of Political Economy, Vol 114 No 2,pages 317-339.

[5] Bird, G. (1996), “The International Monetary Fund and Developing Countries: AReview of the Evidence and Policy Options”, International Organization, vol. 50(3),pages 477-511, Summer.

[6] Bird, G and Rowlands, (2006), “IMF quotas: Constructing an international organi-zation using inferior building blocks”, Review of International Organizations, Vol 1No 2, pages 153-171.

[7] Buira, A. (2005), “The Bretton Woods Institutions: Governance without Legitimacy?in Ariel Buira, Reforming the Governance of the IMF and the World Bank (London:Anthem Press), 7-44.

[8] Cottarelli, C. (2005), “Efficiency and Legitimacy: Trade-offs in IMF Governance”,IMF Working Papers 05/107, IMF.

[9] Deutsche Bundesbank (2002), “Quotas and Voting Shares in the IMF”, MonthlyReport, September 2002, pages 63-77.

18

[10] Dreyer, J. and Schotter, A. (1978), “Power Relationships in the International Mone-tary Fund: The Consequences of Quota Changes”, Working Paper 78-06, C.V. StarrCenter for Applied Economics, New York University.

[11] Fischer, S. (1997), “Applied Economics in Action: IMF Programs”, American Eco-nomic Review, vol. 87(2), pages 23-27, May.

[12] Fischer, S. (1999), “On the Need for an International Lender of Last Resort”, Journalof Economic Perspectives, Vol. 13(4), pages 85-104, Fall.

[13] Hviding, K., M. Nowak, and L. Ricci, (2004), “Can Higher Reserves Help ReduceExchange Rate Volatility?”, IMF Working Papers 04/189, IMF.

[14] Knight, M. and J. Santaella, (1997), “Economic Determinants of IMF FinancialArrangements”, Journal of Development Economics, 54, pages 495-526.

[15] Lane, P. R. and G. M. Milesi-Ferretti, (2006), “The External Wealth of Nations MarkII: Revised and Extended Estimates of Foreign Assets and Liabilities, 1970-2004”,IMF Working Papers 06/69, IMF.

[16] Mikesell, R. (1994), “The Bretton Woods Debate: A Memoir”, ”Essays in Interna-tional Finance”, No 192, Princeton University

[17] ONeill, B. and Peleg, B. (2000), “Voting by Count and Account:Reconciling Power and Equality in International Organizations”(http://www.stanford.edu/ boneill/%26a.html).

[18] Rapkin, D. and Strand, J. (2003), “Is East Asia under-represented in the Interna-tional Monetary Fund?”, International Relations of the Asia-Pacific, vol. 3, pages1-28.

[19] Rapkin, D. and Strand, J. (2006), “Reforming the IMFs Weighted Voting System”,The World Economy, Vol. 29 (3), pages 305-324.

[20] Vaubel, R. (2006), “Principal-agent problems in international organizations”, Reviewof International Organizations, Vol 1 No 2, pages 125-138.

[21] Woods, N. (2005), “Making the IMF and the World Bank More Accountable, in ArielBuira, Reforming the Governance of the IMF and the World Bank (London: AnthemPress), 149-170.

19

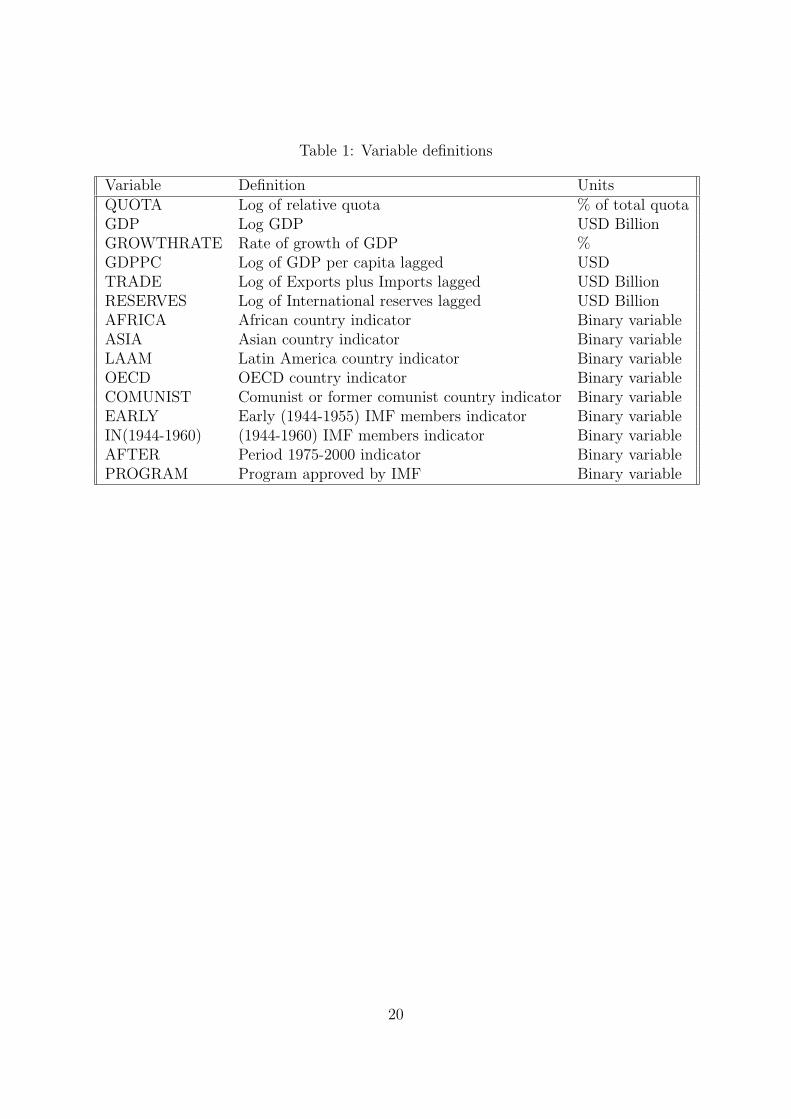

Table 1: Variable definitions

Variable Definition UnitsQUOTA Log of relative quota % of total quotaGDP Log GDP USD BillionGROWTHRATE Rate of growth of GDP %GDPPC Log of GDP per capita lagged USDTRADE Log of Exports plus Imports lagged USD BillionRESERVES Log of International reserves lagged USD BillionAFRICA African country indicator Binary variableASIA Asian country indicator Binary variableLAAM Latin America country indicator Binary variableOECD OECD country indicator Binary variableCOMUNIST Comunist or former comunist country indicator Binary variableEARLY Early (1944-1955) IMF members indicator Binary variableIN(1944-1960) (1944-1960) IMF members indicator Binary variableAFTER Period 1975-2000 indicator Binary variablePROGRAM Program approved by IMF Binary variable

![IFI Reform: IMF Reform [25] - G20 Research Group · 856 IMF Executive Board Approves Major Overhaul of Quotas and Governance, International Monetary Fund (Washington) 5 November 2010.](https://static.documents.pub/doc/80x56/5f5de81316c3b54ae1192971/ifi-reform-imf-reform-25-g20-research-group-856-imf-executive-board-approves.jpg)