24

Prepared by Aon Benfield Analytics Rate Monitor Report and Quarterly U.S. Property & Casualty Profitability Analysis Fourth Quarter 2016

Prepared by Aon Benfield Analytics

Rate Monitor Report and Quarterly U.S. Property & Casualty Profitability Analysis Fourth Quarter 2016

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 2

Table of Contents

Section 1 Rate trends

Section 2 Quarterly performance metrics and analysis

Section 3 Year-To-Date (YTD) performance metrics and analysis

Section 4 Additional information

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 3

Rate Trends – 4th Quarter 2016

The pricing environment in the U.S. P&C commercial market is soft, but conditions vary based on territory, line of business and size of the account

− The commercial property market remains in a prolonged soft cycle, although the overall magnitude of rate decreases has continued to moderate

− Generally larger accounts are more competitive than smaller accounts, although middle market accounts are becoming more competitive (carriers reported rates flat to down 2%)

− There has been softening in terms and conditions in some lines of business

− Commercial casualty lines experiencing positive rate increases include cyber, commercial auto, general liability and umbrella

− However, rates in the aggregate are not moving directionally or in proportion to underlying long-term cost trends (higher severity trends were reported in commercial auto, excess casualty and medical malpractice)

Carriers reported rate increases in Homeowners of 2% on average, with exposure increases of up 3% - 5%

− Rate increases in Homeowners have been moderating for the past 2 years

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 4

Rate Trends – 4th Quarter 2016

Both commercial and personal auto liability rates increased for the third quarter in a row

− Carriers submitting rate increases are motivated by the increased frequency and severity of auto claims, which are partially fueled by a continued increase of miles driven, speeding and distracted driver claims

− Carriers expect rates in commercial and personal auto to increase in 2017, but there is uncertainly as to whether the rates will keep pace with long-term cost trends

− Some carriers expect the frequency of losses to decline in a few years due to safer vehicles, but severity is expected to remain elevated for the foreseeable future

Internationally rates remain under pressure and have been down more than U.S. rates except where material catastrophes have occurred, such as Canada

− Carriers stated that the most competitive lines remain marine, aviation and energy

− Overall, the reinsurance marketplace conditions remain challenging, although the pace of rate deterioration appears to be decelerating

Based on the rate indices, rate filings and carrier comments, the most competitive lines remain

– Energy, aviation and marine – Commercial property (particularly on the larger cat exposed accounts) – Construction

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 5

Aon Benfield Commercial Casualty Rate Indices

Most carriers state that commercial casualty rates have been flat to declining, but some lines of business are achieving rate increases

Commercial auto has been one line that has seen high single-digit rate increases

There has been an uptick in demand for cyber – Carriers are reporting single digit rate

increases in cyber, but the increases are less than in prior quarters

Carriers reported that overall rates in general liability and umbrella are up marginally for the year

Workers compensation has experienced an increase in competition with some carriers reporting rate decreases in the mid single digit range

In professional lines, several carriers reported that overall rates declined 2%, with D&O rates down as much as 4%

Standard: Chubb Limited., American International Group, Inc., Hartford Financial Services Group, Inc., Travelers Companies Inc., XL Group plc, W.R. Berkley Corporation and CNA Financial Corporation Specialty: Arch Capital Group Ltd, Allied World Assurance Company Holdings, AG, Markel Corporation, RLI Corp., W.R. Berkley Corporation and CNA Financial Corporation. Some groups report a Commercial Line rate change which includes both property and casualty.

Source: Aon Benfield Inc.

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%20

09, Q

420

10, Q

120

10, Q

220

10, Q

320

10, Q

420

11, Q

120

11, Q

220

11, Q

320

11, Q

420

12, Q

120

12, Q

220

12, Q

320

12, Q

420

13, Q

120

13, Q

220

13, Q

320

13, Q

420

14, Q

120

14, Q

220

14, Q

320

14, Q

420

15, Q

120

15, Q

220

15, Q

320

15, Q

420

16, Q

120

16, Q

220

16, Q

320

16, Q

4

Rat

e C

hang

e

All Co. Avg

Specialty Co. Avg

Standard Co. Avg

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 6

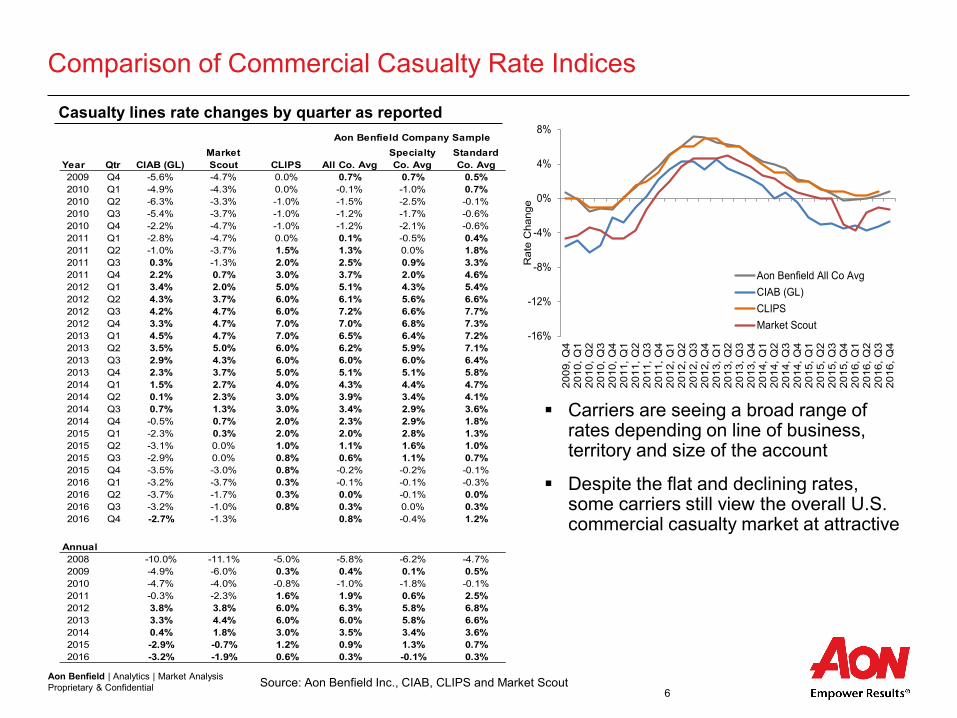

Comparison of Commercial Casualty Rate Indices Casualty lines rate changes by quarter as reported

Source: Aon Benfield Inc., CIAB, CLIPS and Market Scout

Carriers are seeing a broad range of rates depending on line of business, territory and size of the account

Despite the flat and declining rates, some carriers still view the overall U.S. commercial casualty market at attractive

Aon Benfield Company Sample

Year Qtr CIAB (GL)Market Scout CLIPS All Co. Avg

Specialty Co. Avg

Standard Co. Avg

2009 Q4 -5.6% -4.7% 0.0% 0.7% 0.7% 0.5%2010 Q1 -4.9% -4.3% 0.0% -0.1% -1.0% 0.7%2010 Q2 -6.3% -3.3% -1.0% -1.5% -2.5% -0.1%2010 Q3 -5.4% -3.7% -1.0% -1.2% -1.7% -0.6%2010 Q4 -2.2% -4.7% -1.0% -1.2% -2.1% -0.6%2011 Q1 -2.8% -4.7% 0.0% 0.1% -0.5% 0.4%2011 Q2 -1.0% -3.7% 1.5% 1.3% 0.0% 1.8%2011 Q3 0.3% -1.3% 2.0% 2.5% 0.9% 3.3%2011 Q4 2.2% 0.7% 3.0% 3.7% 2.0% 4.6%2012 Q1 3.4% 2.0% 5.0% 5.1% 4.3% 5.4%2012 Q2 4.3% 3.7% 6.0% 6.1% 5.6% 6.6%2012 Q3 4.2% 4.7% 6.0% 7.2% 6.6% 7.7%2012 Q4 3.3% 4.7% 7.0% 7.0% 6.8% 7.3%2013 Q1 4.5% 4.7% 7.0% 6.5% 6.4% 7.2%2013 Q2 3.5% 5.0% 6.0% 6.2% 5.9% 7.1%2013 Q3 2.9% 4.3% 6.0% 6.0% 6.0% 6.4%2013 Q4 2.3% 3.7% 5.0% 5.1% 5.1% 5.8%2014 Q1 1.5% 2.7% 4.0% 4.3% 4.4% 4.7%2014 Q2 0.1% 2.3% 3.0% 3.9% 3.4% 4.1%2014 Q3 0.7% 1.3% 3.0% 3.4% 2.9% 3.6%2014 Q4 -0.5% 0.7% 2.0% 2.3% 2.9% 1.8%2015 Q1 -2.3% 0.3% 2.0% 2.0% 2.8% 1.3%2015 Q2 -3.1% 0.0% 1.0% 1.1% 1.6% 1.0%2015 Q3 -2.9% 0.0% 0.8% 0.6% 1.1% 0.7%2015 Q4 -3.5% -3.0% 0.8% -0.2% -0.2% -0.1%2016 Q1 -3.2% -3.7% 0.3% -0.1% -0.1% -0.3%2016 Q2 -3.7% -1.7% 0.3% 0.0% -0.1% 0.0%2016 Q3 -3.2% -1.0% 0.8% 0.3% 0.0% 0.3%2016 Q4 -2.7% -1.3% 0.8% -0.4% 1.2%

Annual2008 -10.0% -11.1% -5.0% -5.8% -6.2% -4.7%2009 -4.9% -6.0% 0.3% 0.4% 0.1% 0.5%2010 -4.7% -4.0% -0.8% -1.0% -1.8% -0.1%2011 -0.3% -2.3% 1.6% 1.9% 0.6% 2.5%2012 3.8% 3.8% 6.0% 6.3% 5.8% 6.8%2013 3.3% 4.4% 6.0% 6.0% 5.8% 6.6%2014 0.4% 1.8% 3.0% 3.5% 3.4% 3.6%2015 -2.9% -0.7% 1.2% 0.9% 1.3% 0.7%2016 -3.2% -1.9% 0.6% 0.3% -0.1% 0.3%

-16%

-12%

-8%

-4%

0%

4%

8%

2009

, Q4

2010

, Q1

2010

, Q2

2010

, Q3

2010

, Q4

2011

, Q1

2011

, Q2

2011

, Q3

2011

, Q4

2012

, Q1

2012

, Q2

2012

, Q3

2012

, Q4

2013

, Q1

2013

, Q2

2013

, Q3

2013

, Q4

2014

, Q1

2014

, Q2

2014

, Q3

2014

, Q4

2015

, Q1

2015

, Q2

2015

, Q3

2015

, Q4

2016

, Q1

2016

, Q2

2016

, Q3

2016

, Q4

Rat

e C

hang

e

Aon Benfield All Co AvgCIAB (GL)CLIPSMarket Scout

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 7

U.S. National Average Rate Change

Source: Aon’s National Casualty Quarterly Rate Report

The Aon National Rate Index captured rate increases in workers compensation, GL commercial auto, GL, workers compensation and umbrella

This contrasts with several carriers reporting casualty rates down in workers compensation and flat in most other commercial casualty lines

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2014

, Q1

2014

, Q2

2014

, Q3

2014

, Q4

2015

, Q1

2015

, Q2

2015

, Q3

2015

, Q4

2016

, Q1

2016

, Q2

2016

, Q3

2016

, Q4

Auto Liab

WC

Excess WC

GL

Lead Umbrella

Total Umbrella / ExcessLiab

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 8

Year QtrMarket Scout

(Personal Lines)Aon Benfield (HO-

only)2010 Q4 -- 6.4%2011 Q1 -- 6.4%2011 Q2 -- 6.0%2011 Q3 -- 6.4%2011 Q4 -- 6.8%2012 Q1 1.7% 6.7%2012 Q2 1.7% 6.8%2012 Q3 2.7% 6.9%2012 Q4 3.7% 7.4%2013 Q1 3.7% 7.6%2013 Q2 3.7% 6.8%2013 Q3 3.3% 6.9%2013 Q4 3.0% 6.3%2014 Q1 2.3% 5.7%2014 Q2 3.3% 5.3%2014 Q3 3.0% 4.1%2014 Q4 2.7% 3.6%2015 Q1 2.0% 3.7%2015 Q2 1.0% 2.6%2015 Q3 1.7% 3.1%2015 Q4 -0.7% 2.7%2016 Q1 -0.7% 2.4%2016 Q2 1.0% 2.2%2016 Q3 0.7% 2.3%2016 Q4 1.3% 2.0%

Annual2012 2.4% 7.4%2013 3.4% 6.3%2014 2.8% 3.6%2015 1.0% 2.7%2016 0.6% 2.0%

Personal Lines Rate Indices

Personal lines rate changes by quarter as reported

Rates in personal lines continue to increase, although the increases in homeowners rates continue to moderate

Personal auto has experienced an increase in severity and frequency in recent accident years

Carriers are expecting the positive rate momentum in personal lines to continue in 2017

Source: The Aon Benfield Homeowners rate index is based on approved rate filings for the top twenty insurance groups in each state.

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

201

0,

4Q

201

1,

1Q

201

1,

2Q

201

1,

3Q

201

1,

4Q

201

2,

1Q

201

2,

2Q

201

2,

3Q

201

2,

4Q

201

3,

1Q

201

3,

2Q

201

3,

3Q

201

3,

4Q

201

4,

1Q

201

4,

2Q

201

4,

3Q

201

4,

4Q

201

5,

1Q

201

5,

2Q

201

5,

3Q

201

5,

4Q

201

6,

1Q

201

6,

2Q

201

6,

3Q

201

6,

4Q

Rate

Change

Aon Benfield All Co Avg (HO only - Filed)Market Scout Barometer (Personal Lines)

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 9

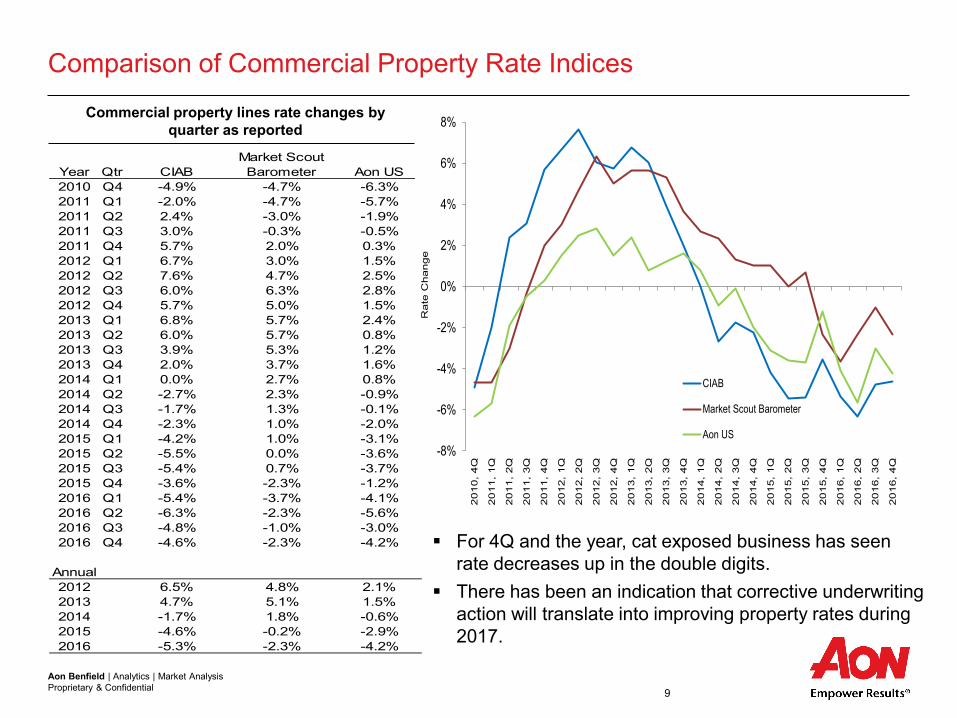

Year Qtr CIAB Market Scout Barometer Aon US

2010 Q4 -4.9% -4.7% -6.3%2011 Q1 -2.0% -4.7% -5.7%2011 Q2 2.4% -3.0% -1.9%2011 Q3 3.0% -0.3% -0.5%2011 Q4 5.7% 2.0% 0.3%2012 Q1 6.7% 3.0% 1.5%2012 Q2 7.6% 4.7% 2.5%2012 Q3 6.0% 6.3% 2.8%2012 Q4 5.7% 5.0% 1.5%2013 Q1 6.8% 5.7% 2.4%2013 Q2 6.0% 5.7% 0.8%2013 Q3 3.9% 5.3% 1.2%2013 Q4 2.0% 3.7% 1.6%2014 Q1 0.0% 2.7% 0.8%2014 Q2 -2.7% 2.3% -0.9%2014 Q3 -1.7% 1.3% -0.1%2014 Q4 -2.3% 1.0% -2.0%2015 Q1 -4.2% 1.0% -3.1%2015 Q2 -5.5% 0.0% -3.6%2015 Q3 -5.4% 0.7% -3.7%2015 Q4 -3.6% -2.3% -1.2%2016 Q1 -5.4% -3.7% -4.1%2016 Q2 -6.3% -2.3% -5.6%2016 Q3 -4.8% -1.0% -3.0%2016 Q4 -4.6% -2.3% -4.2%

Annual2012 6.5% 4.8% 2.1%2013 4.7% 5.1% 1.5%2014 -1.7% 1.8% -0.6%2015 -4.6% -0.2% -2.9%2016 -5.3% -2.3% -4.2%

Comparison of Commercial Property Rate Indices

Commercial property lines rate changes by quarter as reported

For 4Q and the year, cat exposed business has seen rate decreases up in the double digits.

There has been an indication that corrective underwriting action will translate into improving property rates during 2017.

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

20

10,

4Q

20

11,

1Q

20

11,

2Q

20

11,

3Q

20

11,

4Q

20

12,

1Q

20

12,

2Q

20

12,

3Q

20

12,

4Q

20

13,

1Q

20

13,

2Q

20

13,

3Q

20

13,

4Q

20

14,

1Q

20

14,

2Q

20

14,

3Q

20

14,

4Q

20

15,

1Q

20

15,

2Q

20

15,

3Q

20

15,

4Q

20

16,

1Q

20

16,

2Q

20

16,

3Q

20

16,

4Q

Rate

Change

CIAB

Market Scout Barometer

Aon US

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 10

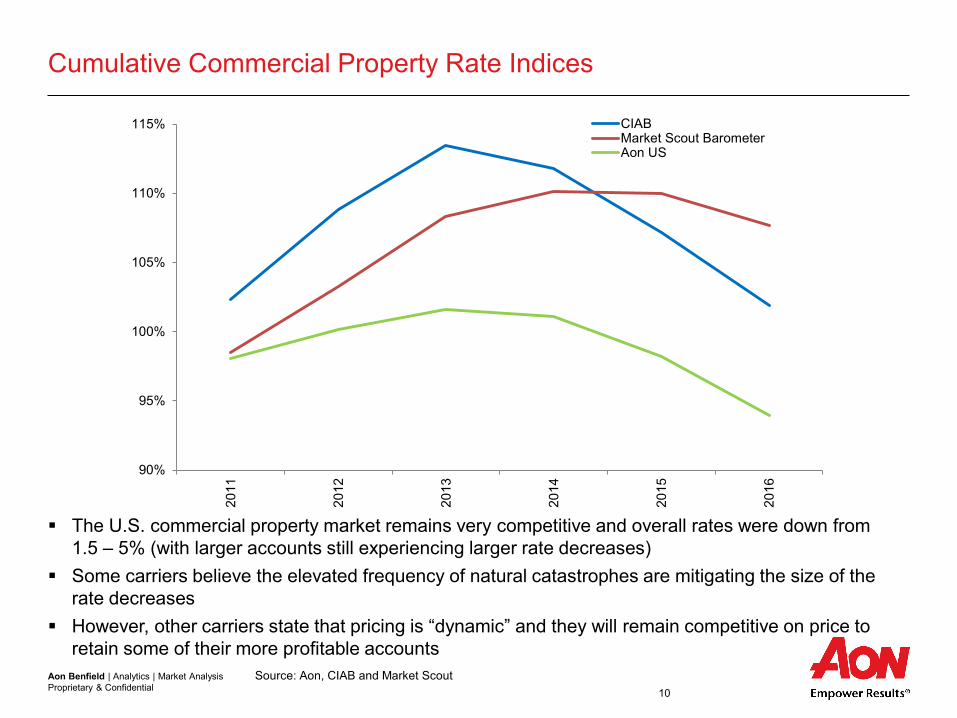

Cumulative Commercial Property Rate Indices

The U.S. commercial property market remains very competitive and overall rates were down from 1.5 – 5% (with larger accounts still experiencing larger rate decreases)

Some carriers believe the elevated frequency of natural catastrophes are mitigating the size of the rate decreases

However, other carriers state that pricing is “dynamic” and they will remain competitive on price to retain some of their more profitable accounts

Source: Aon, CIAB and Market Scout

90%

95%

100%

105%

110%

115%

2011

2012

2013

2014

2015

2016

CIABMarket Scout BarometerAon US

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 11

Table of Contents

Section 1 Rate trends

Section 2 Quarterly performance metrics and analysis

Section 3 Year-To-Date (YTD) performance metrics and analysis

Section 4 Additional information

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 12

4Q 2016 Profitability Observations

Catastrophe losses for most groups were elevated, fueled by Hurricane Matthew

Overall reserves redundancies were lower, as there was a significant amount of reserve strengthening by some groups in commercial and personal auto, workers compensation, A&E as well as lines in run-off

Earned premiums increased overall, fueled by acquisitions

Overall this led to an 4.4 pp increase in the combined ratio (to 97.8%) and a 2.3% decrease in ROE (to 6.6%)

– Just over half of the P&C groups beat their initial quarterly consensus earnings estimates groups, which was on par with 4Q 2015

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 13

YTD 4Q 2016 Profitability Observations

2016 Year-to date results mirrored the fourth quarter results

– Catastrophe losses were elevated, due to Hurricane Matthew, the Fort McMurray wildfire, flooding in the gulf area as well as an increase in wind and hail losses

– Reserve redundancies decreased from 3.9% to 2.6%

– Earned premiums increased from 2.2% to 3.9%

Investment results were mixed, with most groups reporting increases, but a few groups reporting sharp declines

Total equity (excluding Berkshire) decreased 1.5%

– Driven by share buybacks and dividends of $31B, offset by net income of $23B and unrealized gains of $2B

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 14

Miss Beat

% Beat EPS

Target

0% 20% 40% 60% 80% 100%

Large Cap (6)

Commercial (7)

Personal (9)

Specialty (13)

Small Cap Specialty (7)

Reinsurance (9)

Industry (51) 53

44

57

46

67

43

27

4

4

6

6

3

4

24

5

3

7

3

4

2 67

4Q 2016 Actual vs. Estimated EPS by Sector

Note: There are 54 insurance and reinsurance groups included in this report. However, an EPS estimate was not available for 3 groups. The number next to each sector represents the number of groups in that sector. “Miss” or “Beat” refers to the number of groups that did not meet (Miss) or exceeded (Beat) the consensus EPS estimate.

Missed Target Est. Beat Target Est.

EPS estimated vs. actual

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 15

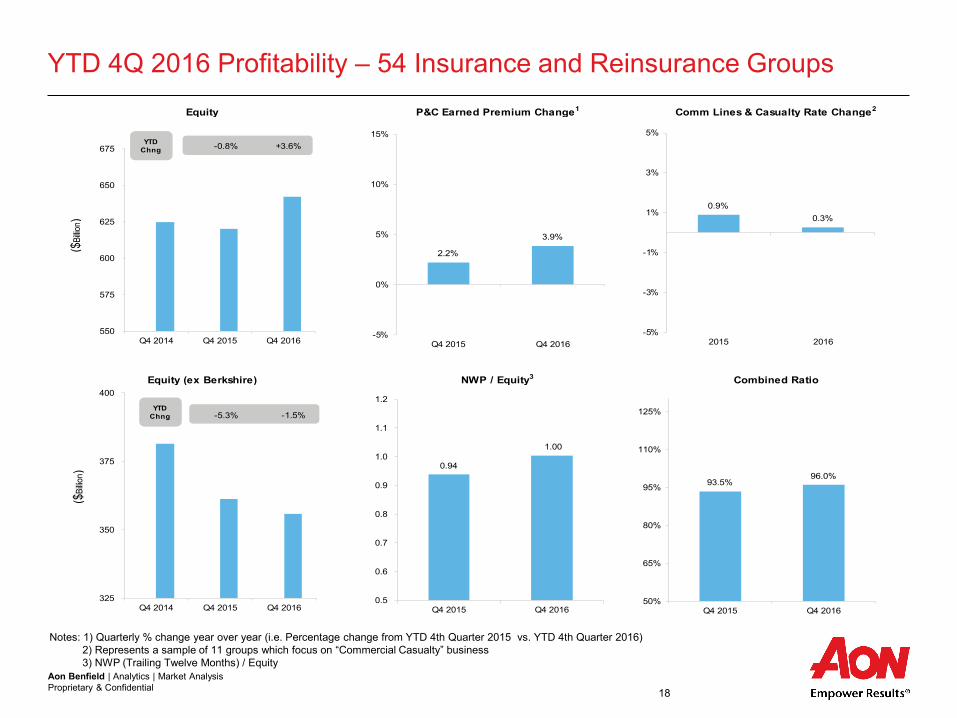

4Q 2016 Profitability – 54 Insurance and Reinsurance Groups

Notes: 1) Quarterly % change year over year (i.e. Percentage change from 4th Quarter 2015 vs. 4th Quarter 2016) 2) Represents a sample of 11 groups which focus on “Commercial Casualty” business 3) NWP (Trailing Twelve Months) / Equity

Equity (ex Berkshire)

Equity P&C Earned Premium Change¹

NWP / Equity3 Combined Ratio

Comm Lines & Casualty Rate Change2

+1.1% +1.9% +1.4% -0.9%

550

575

600

625

650

675

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

+1.1% +2.0% +0.7% -5.2%

300

325

350

375

400

425

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

QuarterChng

QuarterChng

0.970.95 0.94 0.94

1.00

0.5

0.6

0.7

0.8

0.9

1.0

1.1

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

3.8%

6.1%

3.8%

2.1%3.4%

-5%

0%

5%

10%

15%

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

93.4% 93.2%

98.9%

94.7%97.8%

50%

65%

80%

95%

110%

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

($Bi

llion)

-0.2% -0.1%

0.0%0.3%

0.8%

-5%

-3%

-1%

1%

3%

5%

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

($Bi

llion)

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 16

CY Quarter YOY Point Change

4Q 2016 Profitability – 54 Insurance and Reinsurance Groups

Note: CY Quarter = Current Year Quarter; YOY Point Change = Percentage point change from 4th Quarter 2015 vs. 4th Quarter 2016

Return on Equity P&C Earned Premium Change Combined Ratio

Reserve Development to Premium Catastrophe Losses to Premium Combined Ratio ex-Cat & Reserve Development

+1.4

+5.2

+2.5

+0.2

-4.7

-2.5

-0.7

50% 65% 80% 95% 110% 125%

SCSpec

Reins

Pers

Industry

Spec

Comm

LargeCap

+4.9

+1.9

+1.7

-2.3

-2.3

-3.7

-8.4

-15% -10% -5% 0% 5% 10% 15%

LargeCap

Pers

SCSpec

Spec

Industry

Comm

Reins

16.1%

-12.0%

+5.9

+4.5

+0.1

+4.3

+2.2

+1.8

-1.4

-10% -5% 0% 5% 10%

LargeCap

Comm

Pers

SCSpec

Industry

Spec

Reins

+6.8

+8.2

-1.9

+4.4

+4.4

+8.7

+0.7

50% 65% 80% 95% 110% 125%

LargeCap

SCSpec

Pers

Industry

Comm

Reins

Spec

-5% 0% 5% 10% 15%

SCSpec

Spec

Comm

Reins

Industry

LargeCap

Pers

+4.9

+2.0

+3.6

+2.5

+2.5

-4.4

+1.6

0% 2% 4% 6% 8% 10%

Reins

Industry

Spec

Comm

SCSpec

Pers

LargeCap

YOY Chng

YOY Chng

YOY Chng

YOY Chng

YOY Chng

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 17

Table of Contents

Section 1 Rate trends

Section 2 Quarterly performance metrics and analysis

Section 3 Year-To-Date (YTD) performance metrics and analysis

Section 4 Additional information

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 18

YTD 4Q 2016 Profitability – 54 Insurance and Reinsurance Groups

Notes: 1) Quarterly % change year over year (i.e. Percentage change from YTD 4th Quarter 2015 vs. YTD 4th Quarter 2016) 2) Represents a sample of 11 groups which focus on “Commercial Casualty” business 3) NWP (Trailing Twelve Months) / Equity

Equity P&C Earned Premium Change1

NWP / Equity3 Combined Ratio

Comm Lines & Casualty Rate Change2

Equity (ex Berkshire)

-5.3% -1.5%

325

350

375

400

Q4 2014 Q4 2015 Q4 2016

-0.8% +3.6%

550

575

600

625

650

675

Q4 2014 Q4 2015 Q4 2016

YTD Chng

0.94

1.00

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Q4 2015 Q4 2016

2.2%

3.9%

-5%

0%

5%

10%

15%

Q4 2015 Q4 2016

93.5%96.0%

50%

65%

80%

95%

110%

125%

Q4 2015 Q4 2016

($Bi

llion)

YTD Chng

0.9%0.3%

-5%

-3%

-1%

1%

3%

5%

2015 2016

($Bi

llion)

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 19

CY Quarter YOY Point Change

YTD 4Q 2016 Profitability – 54 Insurance and Reinsurance Groups Return on Equity P&C Earned Premium Change Combined Ratio

Reserve Development to Premium Catastrophe Losses to Premium Combined Ratio ex-Cat & Reserve Development

+1.7

-1.3

+0.8

+0.3

+1.0

-0.3

+0.3

50% 65% 80% 95% 110% 125%

Pers

Spec

SCSpec

Industry

Reins

Comm

LargeCap

-0.3

+4.8

+3.6

+2.5

+2.0

+1.4

+3.5

50% 65% 80% 95% 110% 125%

Pers

SCSpec

LargeCap

Industry

Comm

Spec

Reins

+2.9

+0.4

-0.8

-1.1

-1.9

-3.3

-4.5

-15% -10% -5% 0% 5% 10% 15%

Spec

Pers

Industry

LargeCap

SCSpec

Reins

Comm

+1.7

+0.4

+2.3

+0.8

+1.3

+1.5

+0.8

-10% -5% 0% 5% 10%

LargeCap

Pers

SCSpec

Comm

Industry

Spec

Reins

-5% 0% 5% 10% 15%

Spec

SCSpec

LargeCap

Industry

Comm

Reins

Pers

+1.7

+1.5

-2.3

+1.7

+0.9

+1.6

+1.2

0% 2% 4% 6% 8% 10%

SCSpec

Comm

Pers

Reins

Industry

LargeCap

Spec

YOY Chng

YOY Chng

YOY Chng

YOY Chng

YOY Chng

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 20

Table of Contents

Section 1 Rate trends

Section 2 Quarterly performance metrics and analysis

Section 3 Year-To-Date (YTD) performance metrics and analysis

Section 4 Additional information

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 21

Objectives

A primary objective of this report is to provide an update on U.S. P&C rate trends

– Casualty rate trends are derived from a variety of public sources and represent Aon Benfield’s best estimate of casualty rate changes

– Casualty rate trends are also extracted from Aon’s National Casualty Quarterly Rate Report

– The Aon Benfield Homeowners rate index is based on approved rate filings for the top twenty insurance groups in each state

– The Aon Benfield rate change indices are compared to other rate change indices including: CIAB, CLIPS and Market Scout

– The Aon US Commercial Property index is taken from “Aon’s Global Risk Insight Platform” (GRIP)

– The report also provides insight into the profitability of the U.S. P&C Industry

– The U.S. P&C Industry is represented by 54 public insurance and reinsurance groups

– The groups are predominantly U.S. non-life and have been categorized into six sectors

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 22

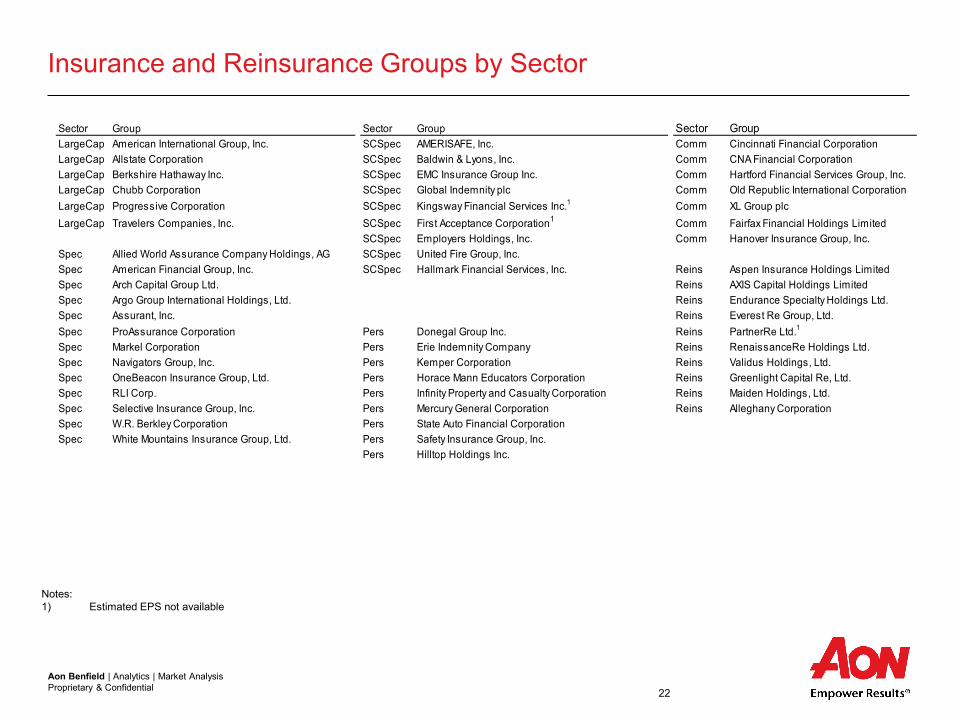

Insurance and Reinsurance Groups by Sector

Notes: 1) Estimated EPS not available

Sector Group Sector Group Sector GroupLargeCap American International Group, Inc. SCSpec AMERISAFE, Inc. Comm Cincinnati Financial CorporationLargeCap Allstate Corporation SCSpec Baldwin & Lyons, Inc. Comm CNA Financial CorporationLargeCap Berkshire Hathaway Inc. SCSpec EMC Insurance Group Inc. Comm Hartford Financial Services Group, Inc.LargeCap Chubb Corporation SCSpec Global Indemnity plc Comm Old Republic International CorporationLargeCap Progressive Corporation SCSpec Kingsway Financial Services Inc.1 Comm XL Group plcLargeCap Travelers Companies, Inc. SCSpec First Acceptance Corporation1 Comm Fairfax Financial Holdings Limited

SCSpec Employers Holdings, Inc. Comm Hanover Insurance Group, Inc.Spec Allied World Assurance Company Holdings, AG SCSpec United Fire Group, Inc.Spec American Financial Group, Inc. SCSpec Hallmark Financial Services, Inc. Reins Aspen Insurance Holdings LimitedSpec Arch Capital Group Ltd. Reins AXIS Capital Holdings LimitedSpec Argo Group International Holdings, Ltd. Reins Endurance Specialty Holdings Ltd.Spec Assurant, Inc. Reins Everest Re Group, Ltd.Spec ProAssurance Corporation Pers Donegal Group Inc. Reins PartnerRe Ltd.1

Spec Markel Corporation Pers Erie Indemnity Company Reins RenaissanceRe Holdings Ltd.Spec Navigators Group, Inc. Pers Kemper Corporation Reins Validus Holdings, Ltd.Spec OneBeacon Insurance Group, Ltd. Pers Horace Mann Educators Corporation Reins Greenlight Capital Re, Ltd.Spec RLI Corp. Pers Infinity Property and Casualty Corporation Reins Maiden Holdings, Ltd.Spec Selective Insurance Group, Inc. Pers Mercury General Corporation Reins Alleghany CorporationSpec W.R. Berkley Corporation Pers State Auto Financial CorporationSpec White Mountains Insurance Group, Ltd. Pers Safety Insurance Group, Inc.

Pers Hilltop Holdings Inc.

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 23

Contact Information

Greg Heerde Head of Americas Analytics Aon Benfield Analytic +1.312.381.5364 [email protected] Brian Alvers Head of Americas Actuarial Aon Benfield Analytics +1.312.381.5355 [email protected]

Tracy Hatlestad COO of Analytics Aon Benfield Analytics +65.6512.0244 [email protected] Mike McClane Market Analysis - Americas Aon Benfield Analytics +1.215.751.1596 [email protected]

National Casualty Quarterly Rate Indices All Other Aon Rate Indices Michael Gruetzmacher Chris Cortese +1.312.381.5364 +1.215.751.1595 [email protected] [email protected]

For information on Aon rate indices, please contact:

Aon Benfield | Analytics | Market Analysis Proprietary & Confidential 24

About Aon Benfield

Aon Benfield, a division of Aon plc (NYSE: AON), is the world’s leading reinsurance intermediary and full service capital advisor. We empower our clients to better understand, manage and transfer risk through innovative solutions and personalized access to all forms of global reinsurance capital across treaty, facultative and capital markets. As a trusted advocate, we deliver local reach to the world’s markets, an unparalleled investment in innovative analytics, including catastrophe management, actuarial and rating agency advisory. Through our professionals’ expertise and experience, we advise clients in making optimal capital choices that will empower results and improve operational effectiveness for their business. With more than 80 offices in 50 countries, our worldwide client base has access to the broadest portfolio of integrated capital solutions and services. To learn how Aon Benfield helps empower results, please visit aonbenfield.com.

© Aon Benfield Inc. 2017. This document is intended for general information purposes only and should not be construed as advice or opinions on any specific facts or circumstances. This analysis is based upon information from sources we consider to be reliable, however Aon Benfield does not warrant the accuracy of the data or calculations herein. The content of this document is made available on an “as is” basis, without warranty of any kind. Aon Benfield disclaims any legal liability to any person or organization for loss or damage caused by or resulting from any reliance placed on that content. Members of the Aon Benfield Analytics will be pleased to consult on any specific situations and to provide further information regarding the matters discussed herein.

Sources: Commercial Lines Insurance Pricing Survey (CLIPS), Council of Insurance Agents and Brokers (CIAB), Market Scout, SNL Financial, LC and Aon plc