23

Baker & O’Brien, Inc. All rights reserved. OPIS 16 th Annual National Supply Summit Las Vegas, Nevada October 28, 2014 Refining America’s New Light Tight Oil (LTO) Production

Baker & O’Brien, Inc. All rights reserved.

OPIS 16th Annual National Supply Summit Las Vegas, Nevada October 28, 2014

Refining America’s New Light Tight Oil (LTO) Production

1

• Growing U.S. LTO Production

• The Industry’s Initial Response

• What Happens Next?

• How Will Refined Products and Intermediates be Impacted?

Note: This presentation assumes that current restrictions on crude oil exports will continue for at least the next several years, and does not address the pros/cons or

impacts of lifting or keeping those restrictions.

Overview

2

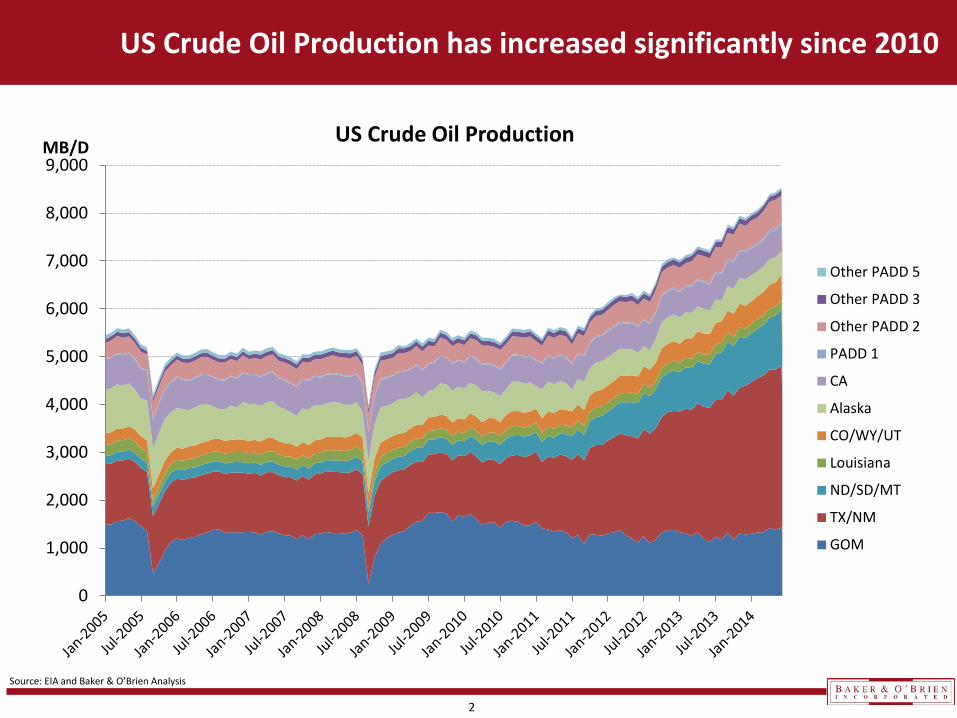

US Crude Oil Production has increased significantly since 2010

Source: EIA and Baker & O’Brien Analysis

US Crude Oil Production MB/D

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Other PADD 5

Other PADD 3

Other PADD 2

PADD 1

CA

Alaska

CO/WY/UT

Louisiana

ND/SD/MT

TX/NM

GOM

3

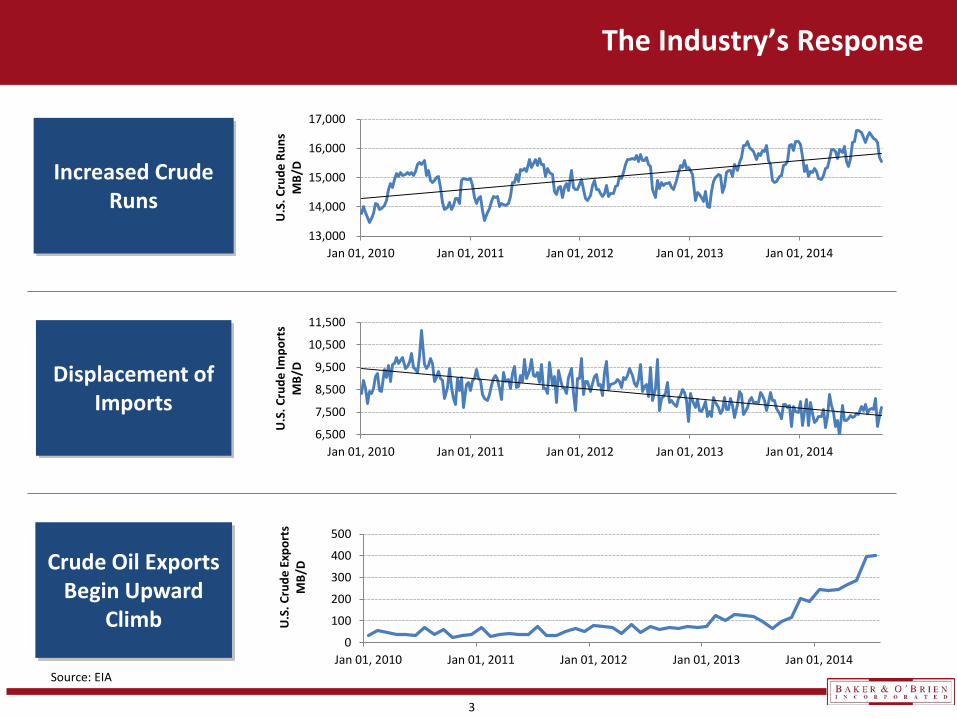

The Industry’s Response

Displacement of

Imports

Crude Oil Exports Begin Upward

Climb

Increased Crude Runs

Source: EIA

13,000

14,000

15,000

16,000

17,000

Jan 01, 2010 Jan 01, 2011 Jan 01, 2012 Jan 01, 2013 Jan 01, 2014

U.S

. Cru

de R

uns

MB/

D

6,500

7,500

8,500

9,500

10,500

11,500

Jan 01, 2010 Jan 01, 2011 Jan 01, 2012 Jan 01, 2013 Jan 01, 2014

U.S

. Cru

de Im

port

s M

B/D

0

100

200

300

400

500

Jan 01, 2010 Jan 01, 2011 Jan 01, 2012 Jan 01, 2013 Jan 01, 2014

U.S

. Cru

de E

xpor

ts

MB/

D

4

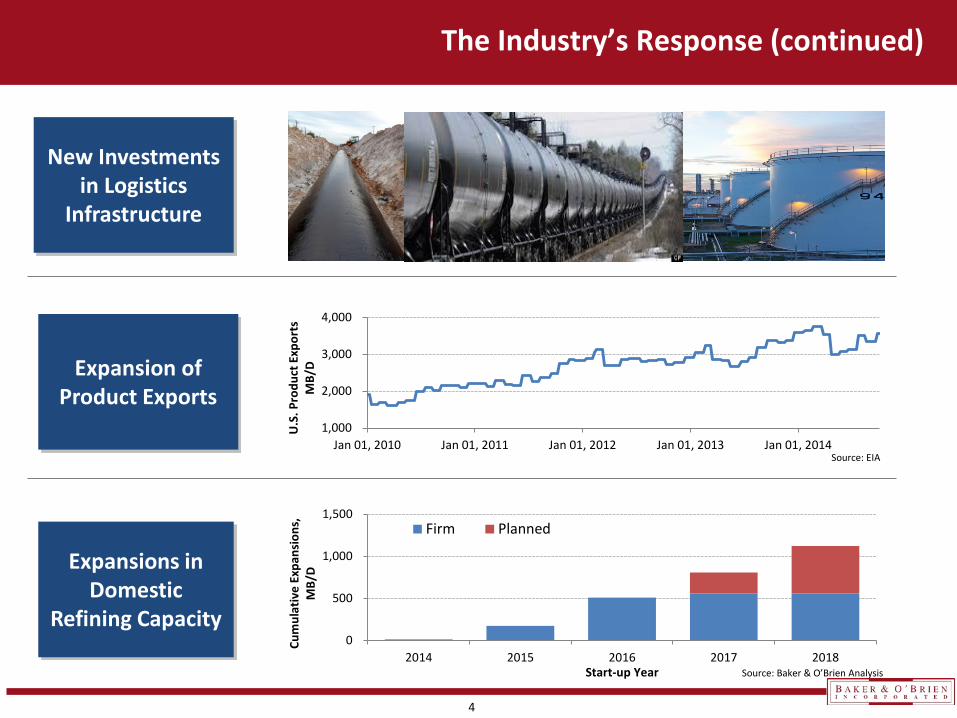

The Industry’s Response (continued)

Expansions in Domestic

Refining Capacity

New Investments in Logistics

Infrastructure

Expansion of Product Exports

Source: EIA

1,000

2,000

3,000

4,000

Jan 01, 2010 Jan 01, 2011 Jan 01, 2012 Jan 01, 2013 Jan 01, 2014

U.S

. Pro

duct

Exp

orts

M

B/D

0

500

1,000

1,500

2014 2015 2016 2017 2018

Cum

ulat

ive

Expa

nsio

ns,

MB/

D

Start-up Year

Firm Planned

Source: Baker & O’Brien Analysis

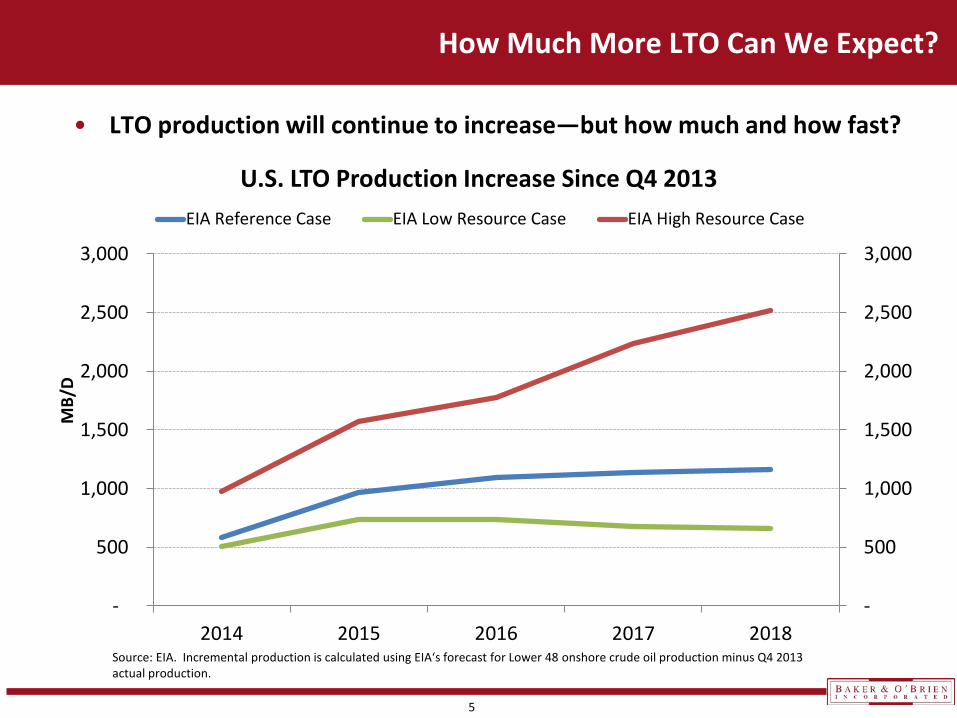

5

• LTO production will continue to increase—but how much and how fast?

How Much More LTO Can We Expect?

Source: EIA. Incremental production is calculated using EIA‘s forecast for Lower 48 onshore crude oil production minus Q4 2013 actual production.

-

500

1,000

1,500

2,000

2,500

3,000

-

500

1,000

1,500

2,000

2,500

3,000

2014 2015 2016 2017 2018

MB/

D

U.S. LTO Production Increase Since Q4 2013 EIA Reference Case EIA Low Resource Case EIA High Resource Case

6

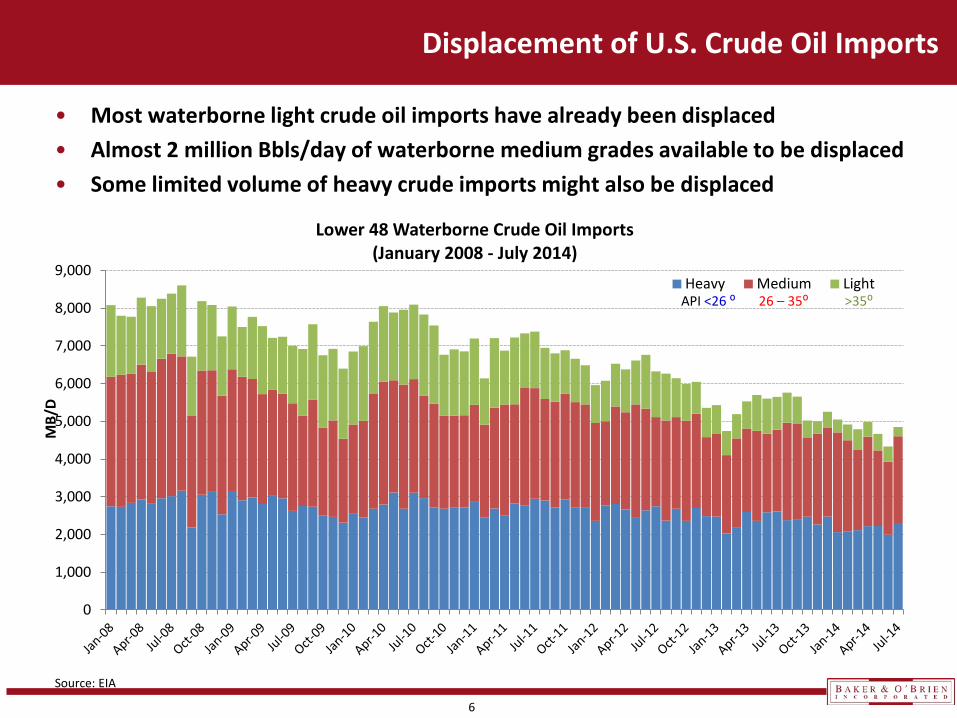

Displacement of U.S. Crude Oil Imports

• Most waterborne light crude oil imports have already been displaced • Almost 2 million Bbls/day of waterborne medium grades available to be displaced • Some limited volume of heavy crude imports might also be displaced

Source: EIA

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

MB/

D

Lower 48 Waterborne Crude Oil Imports (January 2008 - July 2014)

Heavy Medium Light API <26 ⁰ 26 – 35⁰ >35⁰

7

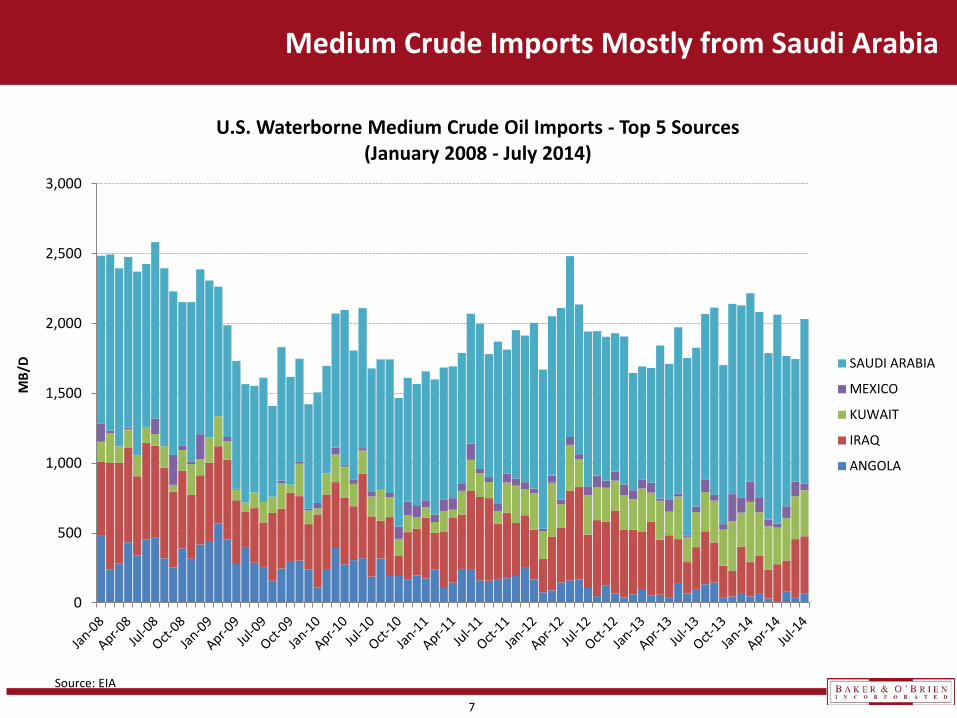

Medium Crude Imports Mostly from Saudi Arabia

0

500

1,000

1,500

2,000

2,500

3,000

MB/

D

U.S. Waterborne Medium Crude Oil Imports - Top 5 Sources (January 2008 - July 2014)

SAUDI ARABIA

MEXICO

KUWAIT

IRAQ

ANGOLA

Source: EIA

8

• As part of announced refining expansions, we can expect some “capacity creep” in ability to run more LTO.

• Since most waterborne light crude imports have been displaced, medium grades are likely to be backed out.

• West Coast LTO runs will slowly be increased as logistics bottlenecks are overcome.

• More stabilized condensates will be exported as a result of recent regulatory finding.

What Can the Industry do Next?

9

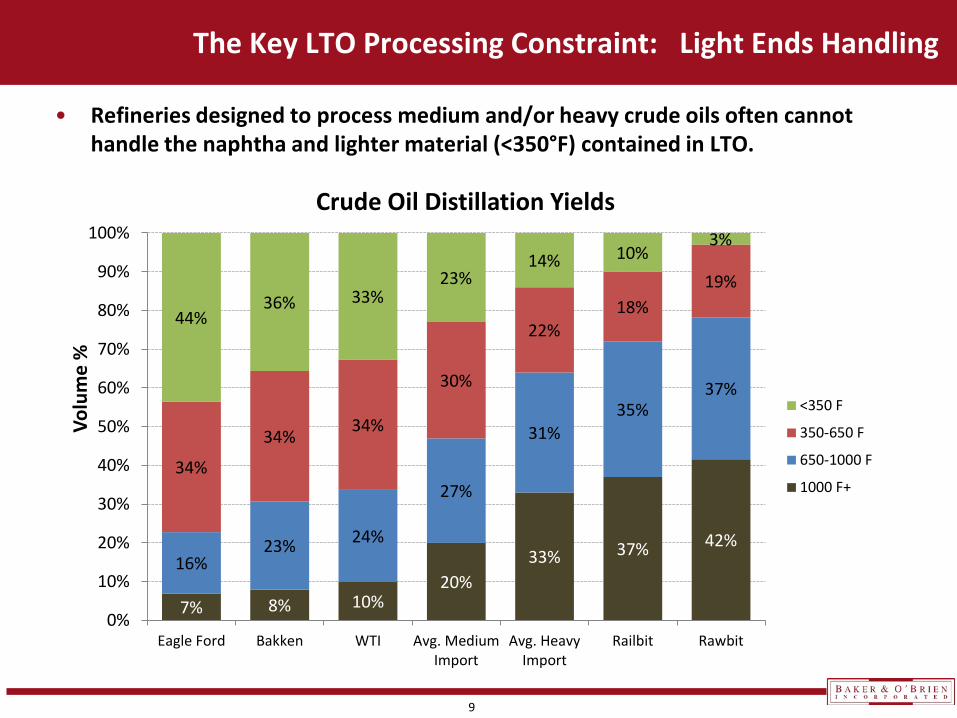

The Key LTO Processing Constraint: Light Ends Handling

• Refineries designed to process medium and/or heavy crude oils often cannot handle the naphtha and lighter material (<350°F) contained in LTO.

7% 8% 10% 20%

33% 37% 42% 16%

23% 24%

27%

31% 35%

37%

34%

34% 34%

30%

22% 18%

19%

44% 36% 33%

23% 14% 10%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Eagle Ford Bakken WTI Avg. MediumImport

Avg. HeavyImport

Railbit Rawbit

Crude Oil Distillation Yields

<350 F

350-650 F

650-1000 F

1000 F+

Volu

me

%

10

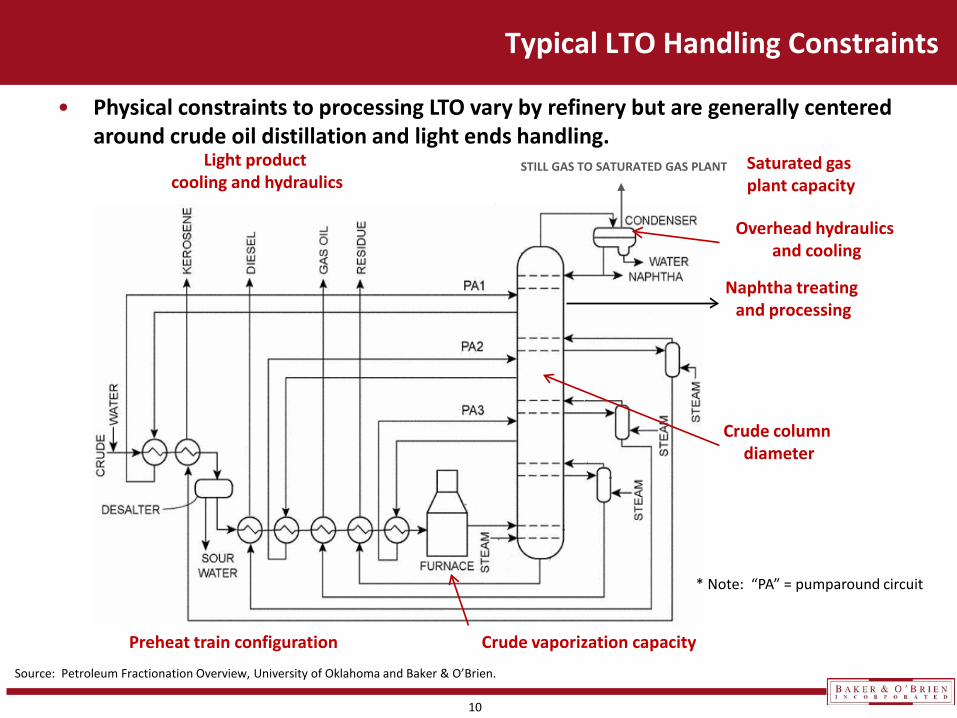

Typical LTO Handling Constraints

STILL GAS TO SATURATED GAS PLANT

Crude vaporization capacity

Saturated gas plant capacity

Light product cooling and hydraulics

Crude column diameter

Overhead hydraulics and cooling

Naphtha treating and processing

Preheat train configuration

Source: Petroleum Fractionation Overview, University of Oklahoma and Baker & O’Brien.

• Physical constraints to processing LTO vary by refinery but are generally centered around crude oil distillation and light ends handling.

* Note: “PA” = pumparound circuit

11

• Direct substitution of medium crude with LTO: – Refiners would generally need to sacrifice some throughput in order to

substitute light for medium without some additional investment.

Options for Replacing Medium Crude Oil with LTO

• LTO/heavy blends can substitute for some medium grade imports:

– Advantages: Enables refiners to maintain crude throughput and keep downstream units full.

– Challenges: Blending exact substitute for medium grades Asphaltene precipitation issues Crude oil blending facilities Availability of heavy crude oil Possible high acid (TAN) constraints

12

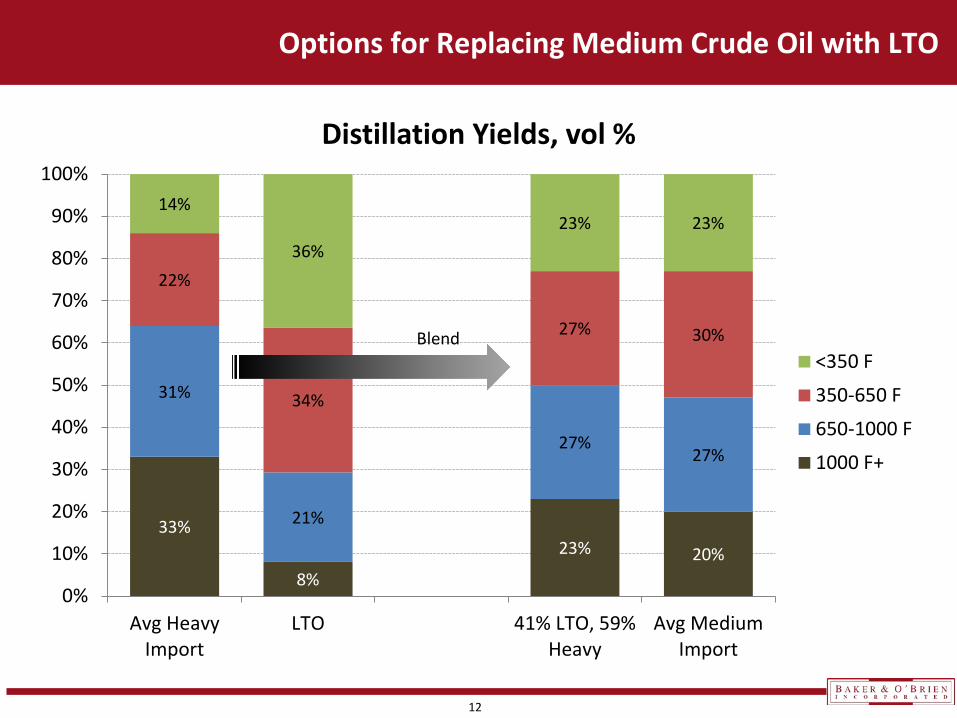

Options for Replacing Medium Crude Oil with LTO

33%

8%

23% 20%

31%

21%

27% 27%

22%

34%

27% 30%

14%

36% 23% 23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Avg HeavyImport

LTO 41% LTO, 59%Heavy

Avg MediumImport

Distillation Yields, vol %

<350 F

350-650 F

650-1000 F

1000 F+

Blend

13

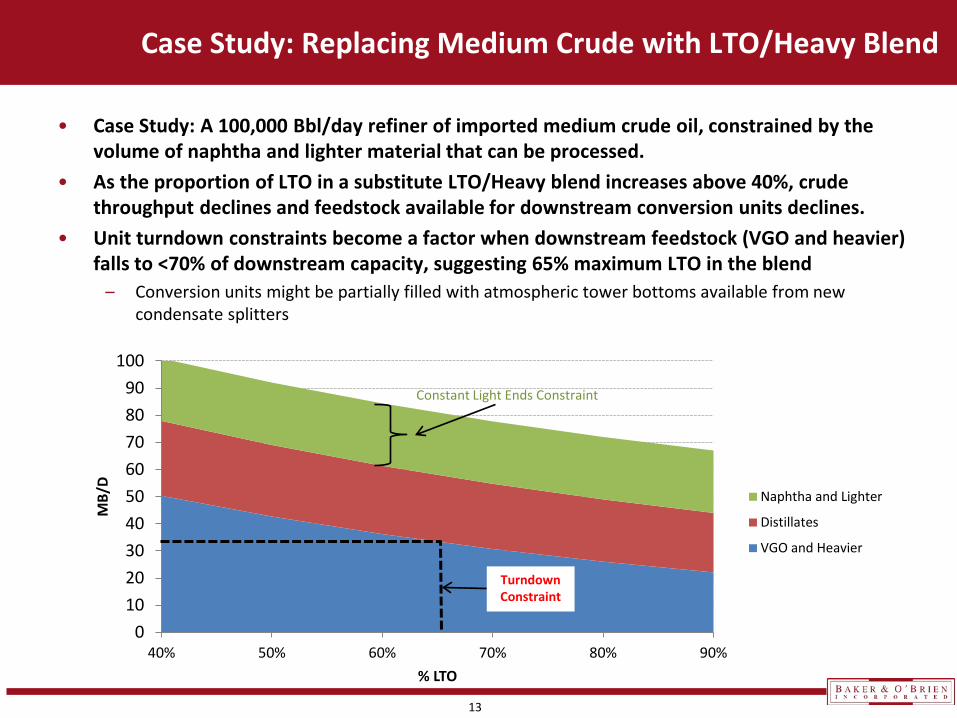

• Case Study: A 100,000 Bbl/day refiner of imported medium crude oil, constrained by the volume of naphtha and lighter material that can be processed.

• As the proportion of LTO in a substitute LTO/Heavy blend increases above 40%, crude throughput declines and feedstock available for downstream conversion units declines.

• Unit turndown constraints become a factor when downstream feedstock (VGO and heavier) falls to <70% of downstream capacity, suggesting 65% maximum LTO in the blend

– Conversion units might be partially filled with atmospheric tower bottoms available from new condensate splitters

Case Study: Replacing Medium Crude with LTO/Heavy Blend

0102030405060708090

100

40% 50% 60% 70% 80% 90%

MB/

D

% LTO

Naphtha and Lighter

Distillates

VGO and Heavier

Constant Light Ends Constraint

Turndown Constraint

14

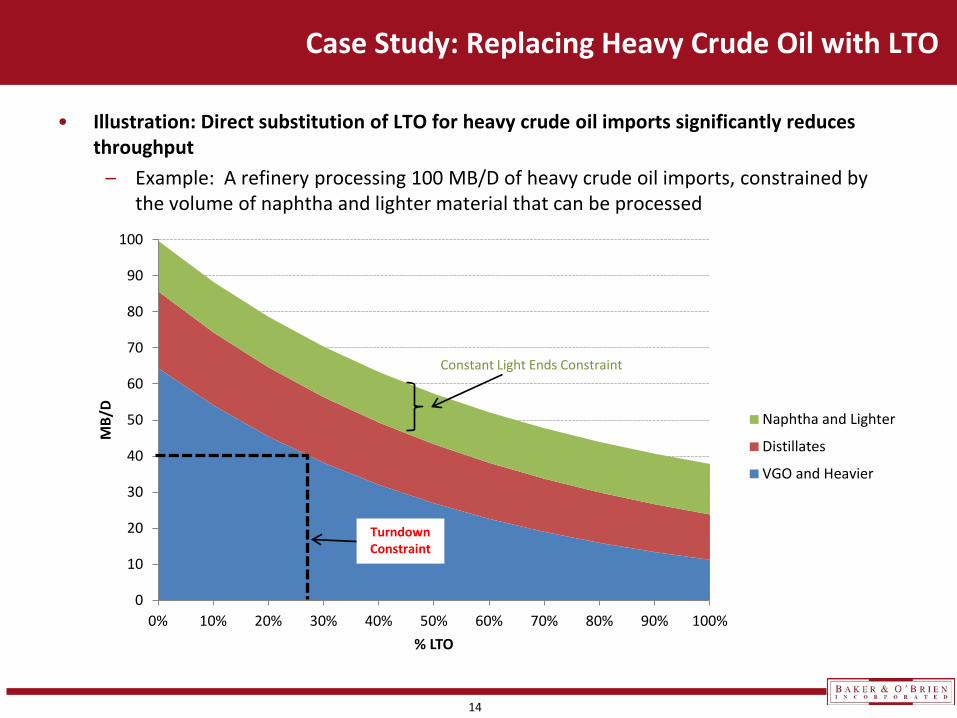

• Illustration: Direct substitution of LTO for heavy crude oil imports significantly reduces throughput

– Example: A refinery processing 100 MB/D of heavy crude oil imports, constrained by the volume of naphtha and lighter material that can be processed

Case Study: Replacing Heavy Crude Oil with LTO

0

10

20

30

40

50

60

70

80

90

100

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

MB/

D

% LTO

Naphtha and Lighter

Distillates

VGO and Heavier

Constant Light Ends Constraint

Turndown Constraint

15

• Direct substitution of LTO for heavy crude imports obviously has turndown limitations. This turndown limit could be alleviated by blends of LTO and bitumen.

Alternative for Replacing Heavy Crude Oil with LTO

• Blends of LTO with Canadian “rawbit” or “railbit” (10-25% diluent) could substitute for some heavy crude imports:

– Advantages: Similar to that for displacement of medium grades – Challenges:

Getting the right blend Asphaltene precipitation Crude blending facilities Availability of rawbit and railbit Possible high acid (TAN) constraints.

16

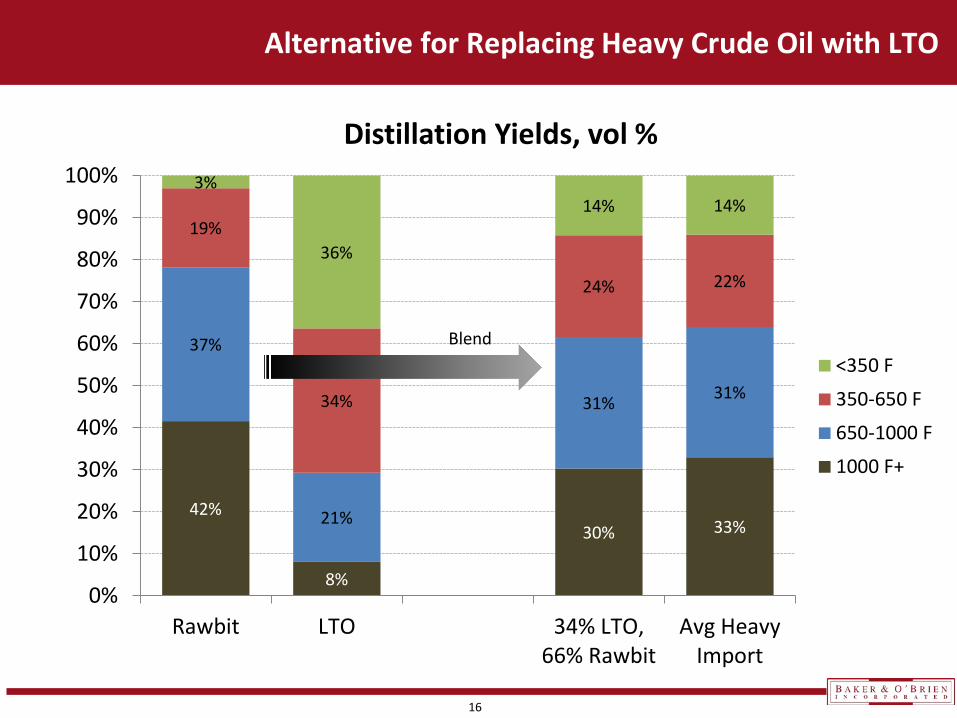

Alternative for Replacing Heavy Crude Oil with LTO

42%

8%

30% 33%

37%

21%

31% 31%

19%

34%

24% 22%

3%

36%

14% 14%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rawbit LTO 34% LTO,66% Rawbit

Avg HeavyImport

Distillation Yields, vol %

<350 F

350-650 F

650-1000 F

1000 F+

Blend

17

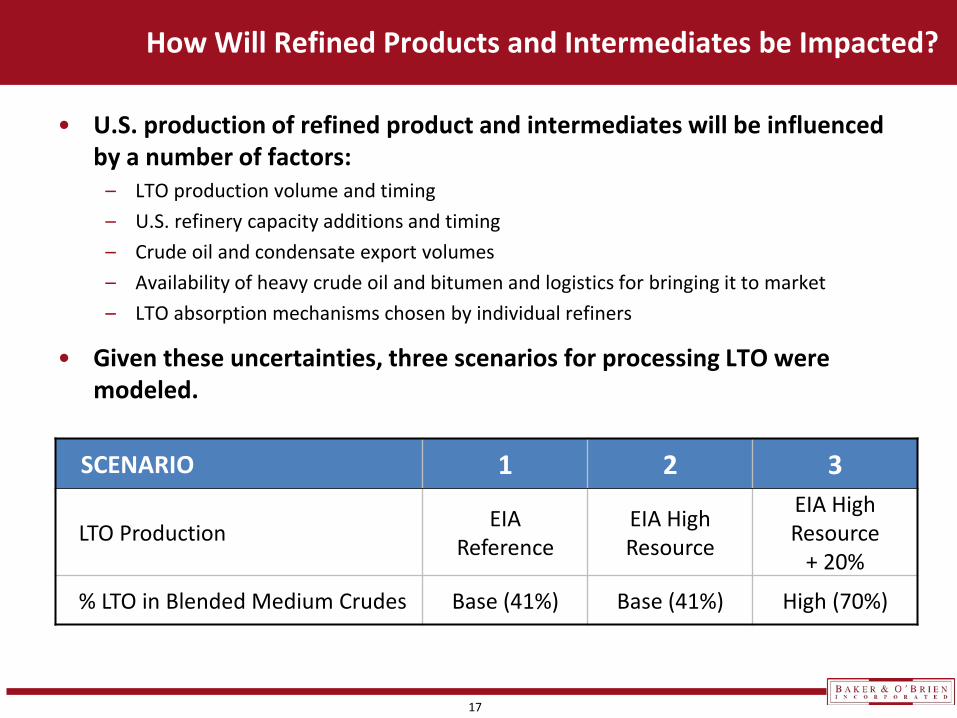

• U.S. production of refined product and intermediates will be influenced by a number of factors:

– LTO production volume and timing – U.S. refinery capacity additions and timing – Crude oil and condensate export volumes – Availability of heavy crude oil and bitumen and logistics for bringing it to market – LTO absorption mechanisms chosen by individual refiners

• Given these uncertainties, three scenarios for processing LTO were modeled.

How Will Refined Products and Intermediates be Impacted?

SCENARIO 1 2 3

LTO Production EIA Reference

EIA High Resource

EIA High Resource

+ 20%

% LTO in Blended Medium Crudes Base (41%) Base (41%) High (70%)

18

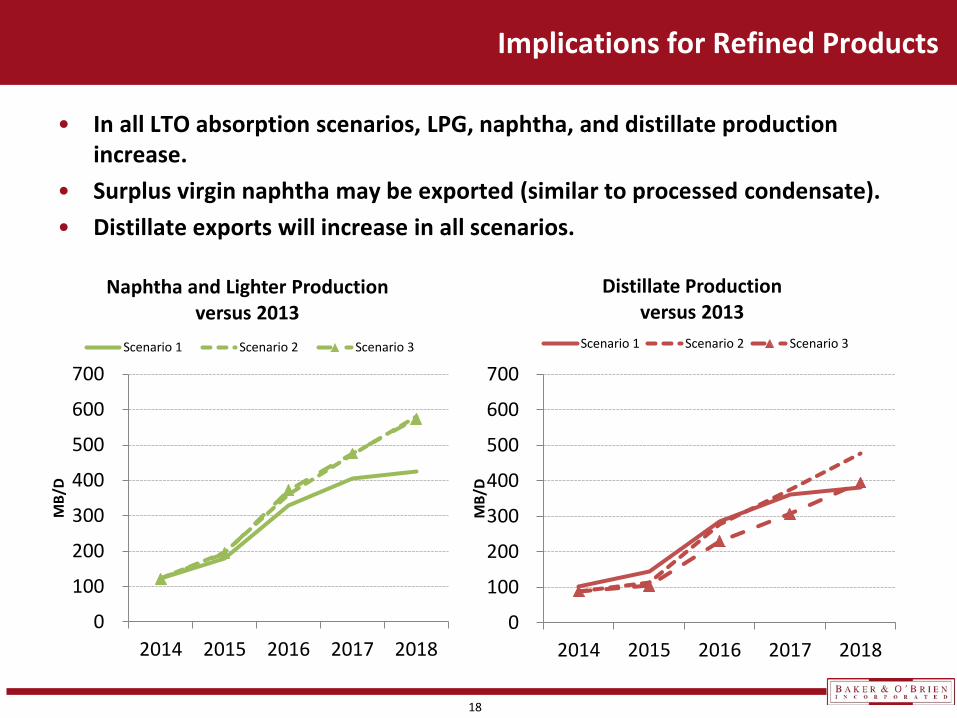

• In all LTO absorption scenarios, LPG, naphtha, and distillate production increase.

• Surplus virgin naphtha may be exported (similar to processed condensate). • Distillate exports will increase in all scenarios.

Implications for Refined Products

0

100

200

300

400

500

600

700

2014 2015 2016 2017 2018

MB/

D

Naphtha and Lighter Production versus 2013

Scenario 1 Scenario 2 Scenario 3

0

100

200

300

400

500

600

700

2014 2015 2016 2017 2018

MB/

D

Distillate Production versus 2013

Scenario 1 Scenario 2 Scenario 3

19

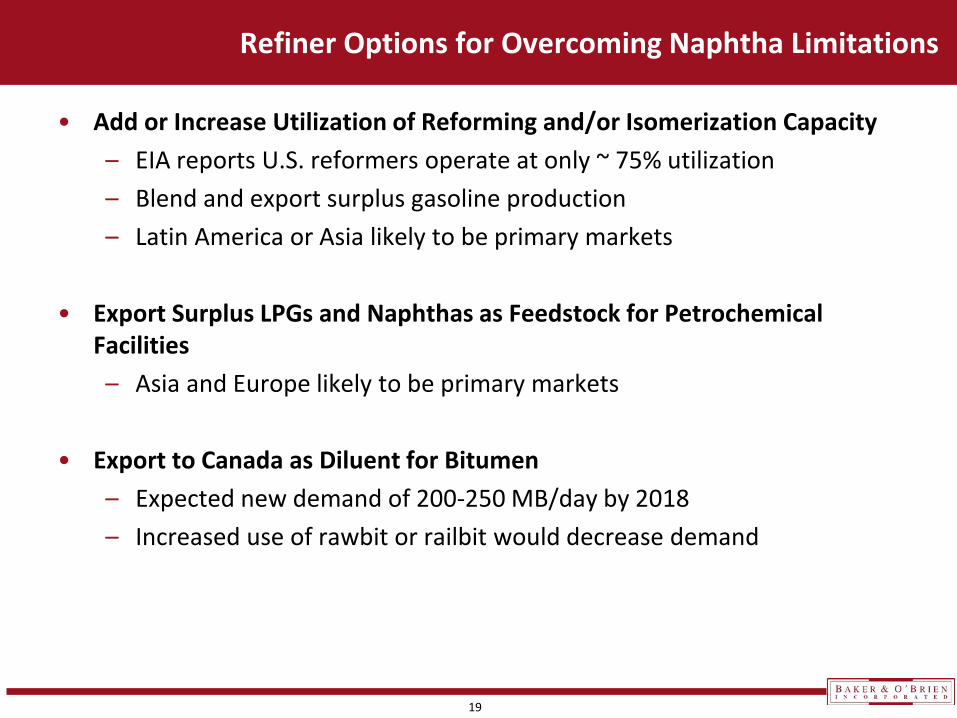

• Add or Increase Utilization of Reforming and/or Isomerization Capacity – EIA reports U.S. reformers operate at only ~ 75% utilization – Blend and export surplus gasoline production – Latin America or Asia likely to be primary markets

• Export Surplus LPGs and Naphthas as Feedstock for Petrochemical Facilities – Asia and Europe likely to be primary markets

• Export to Canada as Diluent for Bitumen – Expected new demand of 200-250 MB/day by 2018 – Increased use of rawbit or railbit would decrease demand

Refiner Options for Overcoming Naphtha Limitations

20

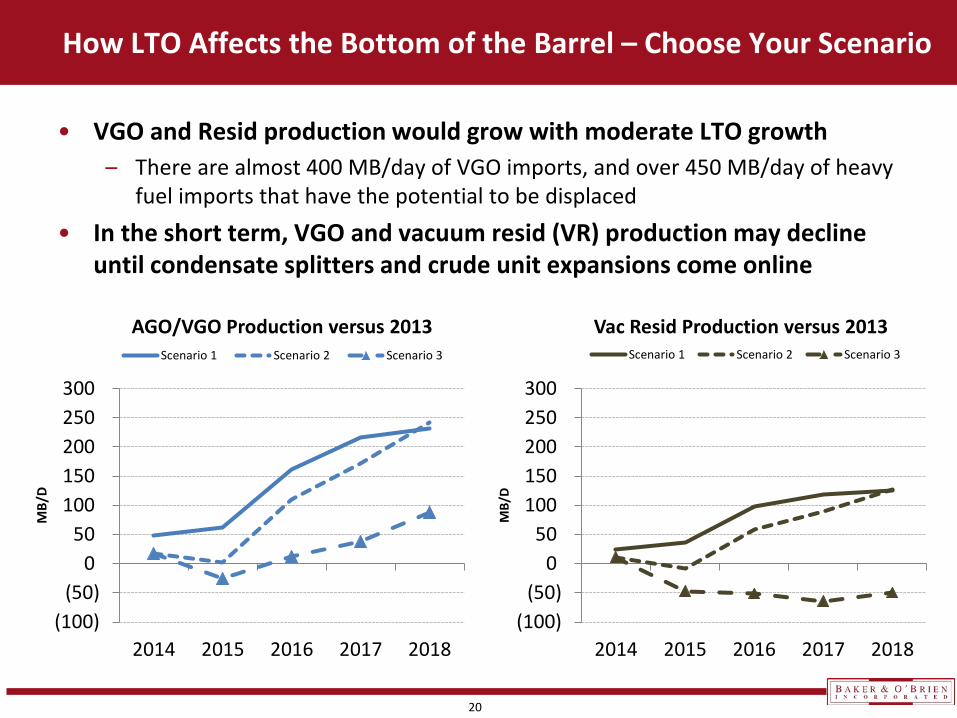

• VGO and Resid production would grow with moderate LTO growth

– There are almost 400 MB/day of VGO imports, and over 450 MB/day of heavy fuel imports that have the potential to be displaced

• In the short term, VGO and vacuum resid (VR) production may decline until condensate splitters and crude unit expansions come online

How LTO Affects the Bottom of the Barrel – Choose Your Scenario

(100)(50)

050

100150200250300

2014 2015 2016 2017 2018

MB/

D

AGO/VGO Production versus 2013 Scenario 1 Scenario 2 Scenario 3

(100)(50)

050

100150200250300

2014 2015 2016 2017 2018

MB/

D

Vac Resid Production versus 2013 Scenario 1 Scenario 2 Scenario 3

21

• US crude oil production has increased significantly since 2010 and is expected to continue to rise.

• Refiners can be expected to accelerate the displacement of medium and heavy crude imports.

• Refiners will exercise available short term and long term (capital) options for overcoming light ends limitations.

• Light virgin products will exhibit year-to-year increases, but heavy virgin intermediates could decline in the near term before rising.

• To the extent possible, refiners will blend LTO with heavier components to minimize turndown limitations.

Summary

22

Baker & O’Brien – Independent Energy Consultants

www.bakerobrien.com

Dallas Headquarters

12001 N. Central Expressway Suite 1200

Dallas, TX 75243 Phone: 1-214-368-7626

Fax: 1-214-368-0190

Houston Office

1333 West Loop South Suite 1350

Houston, TX 77027 Phone: 1-832-358-1453

Fax: 1-832-358-1498

London Office

146 Fleet Street Suite 2

London EC4A 2BU Phone: 44-20-7373-0925