1 REPORT OF THE CONTROLLER AND ACCOUNTANT-GENERAL (CAG) ON THE PUBLIC ACCOUNTS OF THE CONSOLIDATED FUND FOR THE YEAR ENDED 31ST DECEMBER, 2016 1 INTRODUCTION 1.1 Mandate Section 41(1)(b) of the Financial Administration Act, 2003 (Act 654)(FAA) (subsequently replaced by Section 81(1) of the Public Financial Management Act, 2016) and Regulation 191 of the Financial Administration Regulations, 2004 (LI 1802)(FAR) mandates the Controller and Accountant-General to prepare the Annual Public Accounts (Financial Statements) on the Consolidated Fund of the Republic of Ghana. The accounts is to be prepared within a period of three months after the end of the financial year or such other period as Parliament may by resolution determine and transmit same to the Auditor-General and the Minister for Finance (MoF). The Financial Statements are prepared on Government business based on the Appropriation Act for each financial year as required by Article 179 (2) (a) of the 1992 Constitution of the Republic of Ghana. In August 2016, the Public Financial Management Act, 2016 (Act 921) was promulgated to replace the Financial Administration Act, 2003 (Act 654) as the overarching law governing public financial management. 1.2 Components of the Financial Statements The financial statements of the Consolidated Fund comprise: A Statement of Receipts and Payments (with budget summary comparatives) A Statement of Revenue and Expenditure (with budget summary comparatives) A Balance Sheet A Cash Flow Statement Notes to the Accounts

Transcript

1

REPORT OF THE CONTROLLER AND ACCOUNTANT-GENERAL (CAG) ON THE PUBLIC

ACCOUNTS OF THE CONSOLIDATED FUND FOR THE YEAR ENDED 31ST DECEMBER,

2016

1 INTRODUCTION

1.1 Mandate

Section 41(1)(b) of the Financial Administration Act, 2003 (Act 654)(FAA) (subsequently replaced by

Section 81(1) of the Public Financial Management Act, 2016) and Regulation 191 of the Financial

Administration Regulations, 2004 (LI 1802)(FAR) mandates the Controller and Accountant-General to

prepare the Annual Public Accounts (Financial Statements) on the Consolidated Fund of the Republic of

Ghana. The accounts is to be prepared within a period of three months after the end of the financial year

or such other period as Parliament may by resolution determine and transmit same to the Auditor-General

and the Minister for Finance (MoF).

The Financial Statements are prepared on Government business based on the Appropriation Act for each

financial year as required by Article 179 (2) (a) of the 1992 Constitution of the Republic of Ghana.

In August 2016, the Public Financial Management Act, 2016 (Act 921) was promulgated to replace the

Financial Administration Act, 2003 (Act 654) as the overarching law governing public financial

management.

1.2 Components of the Financial Statements

The financial statements of the Consolidated Fund comprise:

A Statement of Receipts and Payments (with budget summary comparatives)

A Statement of Revenue and Expenditure (with budget summary comparatives)

A Balance Sheet

A Cash Flow Statement

Notes to the Accounts

2

1.3 Additional Statements

In line with Regulation 191 (d) of the FAR, a statement of transactions during the year and analysis

of the financial position at the end of the year for the following accounts are included in the financial

statements;

Public Debts

Deposits and Other Trust Monies

Securities of Government

Advances

Public loans (Receivables)

Equity Investments of the Consolidated Fund

Additional information comprising Summary Expenditure of MDAs by items and sectors are included

in the financial statements.

1.4 Scope of the financial statements

The preparation of the accounts was guided mainly by the FAA as the law in force for the greater part

of the year.

Section 81 (1) of the PFMA requires that CAG prepares the consolidated annual accounts of

Government, the accounts of the Contingency Fund and, the accounts on the Petroleum Funds.

As the structures for implementing the new law fully are still under development, the public accounts

produced by Controller and Accountant General for 2016 are on the Consolidated Fund only.

1.5 Basis of Accounting

The 2016 Financial Statements were prepared in accordance with the stated accounting policies on

public funds currently in use as indicated on pages 23 & 24 in the financial report. The CAGD is in

the process of applying IPSAS accrual basis in a progressive manner.

3

2.0 SYSTEM IMPROVEMENT

2.1 Payroll Management

Over the years CAGD, as part of the overall PFM reforms by Government, has undertaken various

measures to ensure that the Single Spine Pay Policy (SSPP), as implemented, is sustainable and that there

exists a credible system to manage Government payroll cost efficiently and effectively. In the regard

various initiatives were pursued during the year under review as follows;

2.1.1 Implementation of Electronic Salary Payment Voucher (ESPV) system

The Electronic Salary Payment Voucher (ESPV) system was vigorously pursued during the year as a

means of cleaning the payroll data to enhance the accuracy of the payroll cost.

2.1.2 Implementation of New Recruitment Policy

Government’s net freeze policy on new employment into the Public Service was pursued during the year.

With the exception of Ghana Education Service and Ghana Health Service which were allowed to make

new recruitments in respect of completed trainees during the year, all other Public Service institutions

were only allowed to make replacement of vacancies.

2.1.3 Migration of GES Payroll from IPPD3 to IPPD2

To achieve harmonisation of payroll cost for budgetary control and effective reporting, CAGD embarked

on the migration of GES payroll from IPPD3 to IPPD2 Oracle system. The core objective of this migration

policy was to pave way for full integration of payroll cost into the GIFMIS financials and HRMIS

implementation. The migration process has been successfully completed.

2.1.4 E-Payslip

The Nationwide rollout of E-Pay-slip which was completed in 2015. Since the implementation of this

system all the 507,118 employees on the payroll have registered on the E-Pay-slip platform as at

December 2016. This has enabled public service workers have easy access to their salary information.

4

2.2 REVENUE AND CASH MANAGEMENT

As part of Government’s cash management reforms initiative, the Controller and Accountant General’s

Department is implementing the Treasury Single Account (TSA) as stipulated in section 46 of the Public

Financial Management Act, 2016 (Act 921). The implementation involves:

The Rationalization of Government bank accounts to ensure that Government operates with an

optimal number of bank accounts. This has led to the closure of 5,110 accounts whilst 1,236 are

being reviewed.

The Bank Account Tracking (B-Tracking) platform is being deployed to all MDAs/MMDAs.

This will allow for real-time visibility of all their bank accounts with commercial banks for

effective monitoring. As a result of the deployment of the B-Tracking platform at CAGD, the

Controller and Accountant-General began investing government bank balances held by the

commercial banks from May 2016. As at 31st December, 2016, a total income if

GH₵49.15million had been generated.

Investment of Government cash balances using B-Tracking Call Account Management (B-

CAM) platform.

3.0 PUBLIC FINANCIAL MANAGEMENT REFORM

Following the re-launch of BPEMS as GIFMIS in 2009, Ghana’s Public Financial Management Reforms

have achieved significant improvements in the areas of accounting and business processes, commitment

control, and timeliness in financial reporting.

3.1 During the year, the CAGD completed the upgrade of the Financials and the Payroll modules and

the rollout of the Human Resource Management Information System (HRMIS).

The coverage of GIFMIS was expanded to capture and track transactions related to the IGFs, SFs and

Donor Funds.

Specifically,

Fifty (50) IGF sites were activated or declared live as at end of December 2016

One (1) Statutory Fund (Energy Fund) went live as at December 2016

5

Four (4) Donor Funds projects went live in 2016.

A total of 736 staff from selected MDAs were trained and equipped with computers to

facilitate their work.

GIFMIS functionality was rolled out to seventeen (17) MMDAs.

The HRMIS project completed the establishment registers for the nine pilot MDAs

workforce (covering about 111,000 staff) and the rollout of the HRMIS core application

including employee cost management as well as the establishment and profile

management to six (6) pilot MDAs.

3.2 Promulgation of the Public Financial Management Act, 2016 (Act 921)

In August 2016, the Public Financial Management Act, 2016 (Act 921) was promulgated as the

overarching law governing public financial management.

The Act is to further strengthen public financial management, promote fiscal discipline and help

consolidate existing laws to regulate public financial management in Ghana to promote transparency and

accountability in the use of public funds.

The Law repealed, among others, the Financial Administration Act, 2003 (Act 654), Section 16(8) of the

Internal Audit Agency Act, 2003,(Act 658) and Section 30 of the Audit Service Act, 2000 (Act 584) both

of which related to the formation and operations of Audit Reports Implementation Committees (ARIC).

The Regulations supporting the implementation of this law is yet to be completed and the law provides

that regulations relating to the repealed enactments shall continue to be in force with the necessary

modification until such time that they are revoked by regulations under the new Act.

4 HIGHLIGHTS OF 2016 FINANCIAL PERFORMANCE

2016 Appropriation

The amounts appropriated for Government business and reflected in these Financial Statements were

regulated by the Appropriation Act 2016, Act 901. Payments made were based on warrants issued

on the authority of the Minister for Finance and was within the Appropriation of GH¢50,109.85

million.

A summary report of the appropriation is for the financial year as below:

6

Table 1: 2016 Appropriation

YEAR 2016 2015

GH¢ (Millions) GH¢ (Millions)

Annual Appropriation 50,109.85 44,887.06

Appropriation Utilised (51,722.25)

(39.572.85)

Balance on Appropriation (1,612.40)

5,314.21

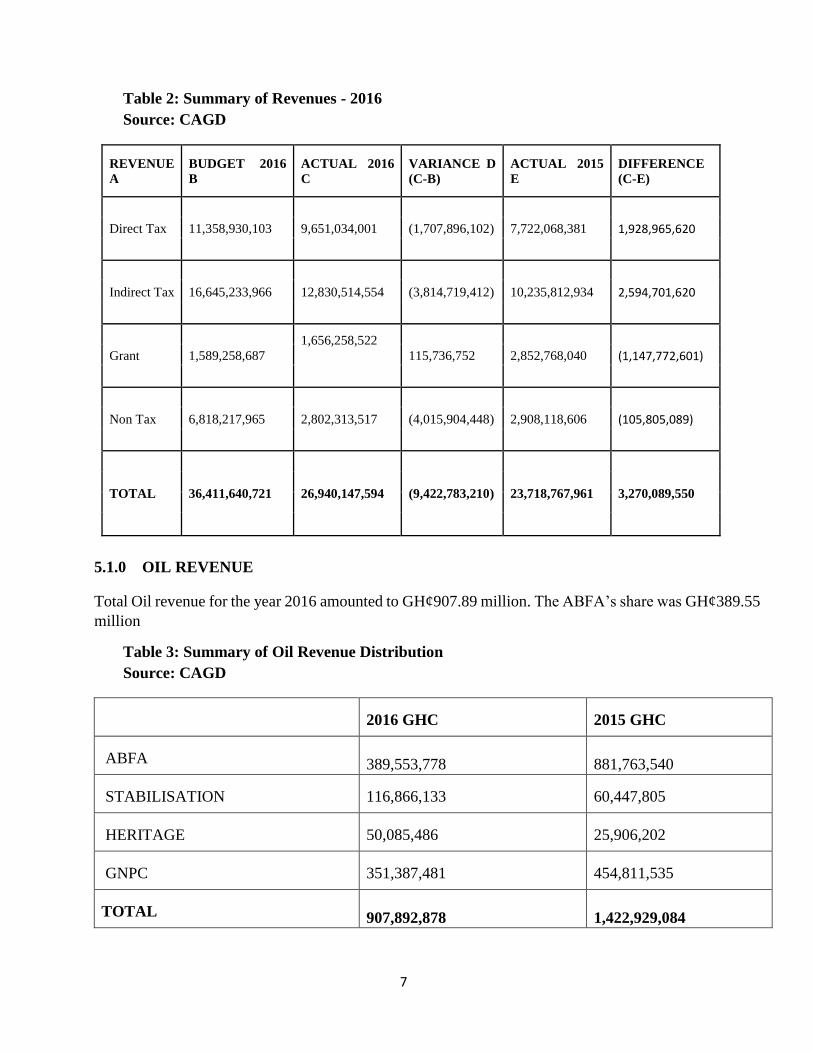

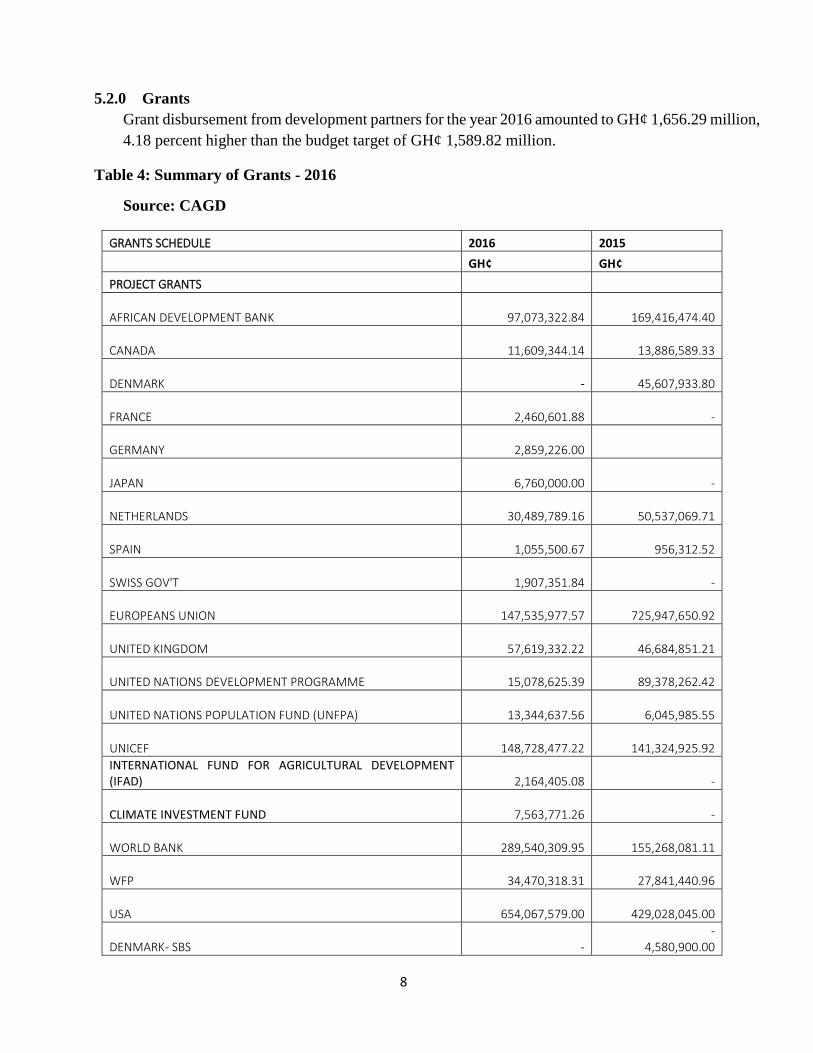

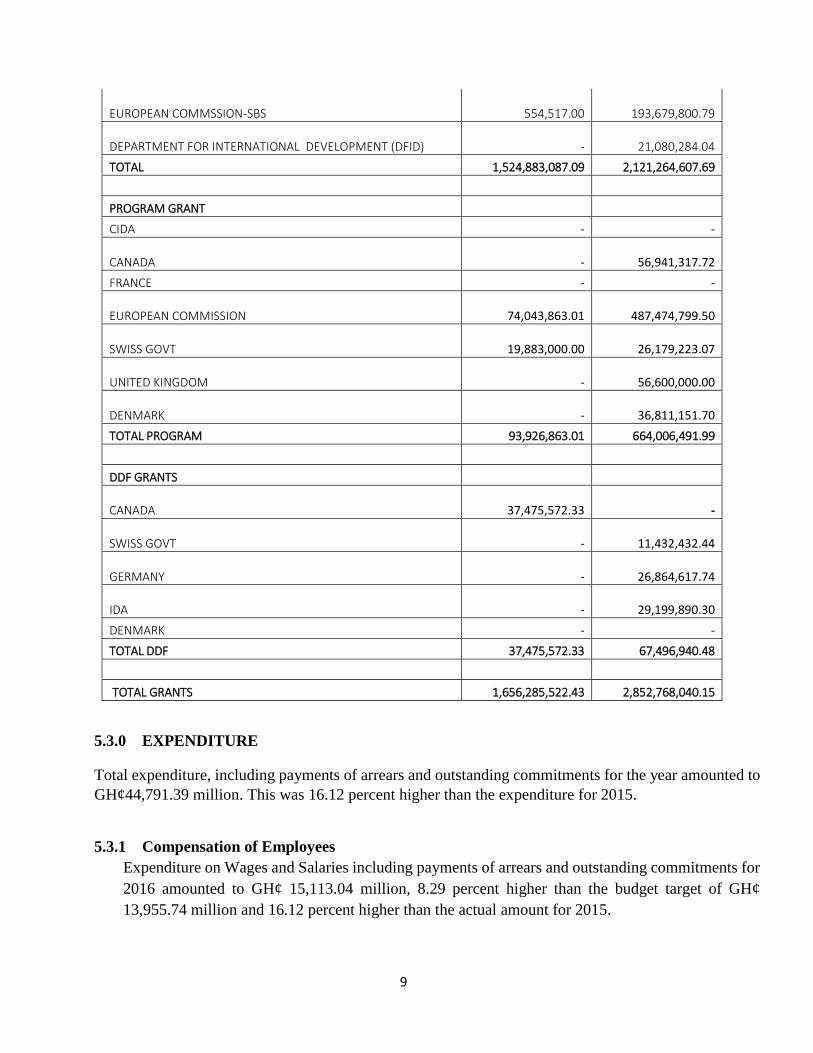

5 Revenue

Total revenue and grants for the year 2016 amounted to GH¢ 26.99 billion against a target of GH¢

36.41 billion. The shortfall was broadly attributable to the impact of the energy challenges on

household and firms and lower than anticipated petroleum receipts among others. Revenue

performance in 2016 was however an improvement of 13.79 percent over 2015.

7

Table 2: Summary of Revenues - 2016

Source: CAGD

REVENUE

A

BUDGET 2016

B

ACTUAL 2016

C

VARIANCE D

(C-B)

ACTUAL 2015

E

DIFFERENCE

(C-E)

Direct Tax 11,358,930,103 9,651,034,001 (1,707,896,102) 7,722,068,381 1,928,965,620