Tax Facts February 2016/2017 Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains, subject to certain exclusions. Non-residents are taxable on South African source income and capital gains only. Income Tax Individuals and special trusts Rate of tax Taxable income Rate of tax - years of assessment ending 28 Feb 2017 R0 – R188,000 18% of each R1 R188,001 – R293,600 R33,840 + 26% of each R above R188,000 R293,601 – R406,400 R61,296 + 31% of each R above R293,600 R406,401 – R550,100 R96,264 + 36% of each R above R406,400 R550,101 – R701,300 R147,996 + 39% of each R above R550,100 R701,301 and above R206,964 + 41% of each R above R701,300 Taxable income Rate of tax - years of assessment ending 29 Feb 2016 R0 – R181,900 18% of each R1 R181,901 – R284,100 R32,742 + 26% of each R above R181,900 R284,101 – R393,200 R59,314 + 31% of each R above R284,100 R393,201 – R550,100 R93,135 + 36% of each R above R393,200 R550,101 – R701,300 R149,619 + 39% of each R above R550,100 R701,301 and above R208,587 + 41% of each R above R701,300

Transcript

Tax Facts February 2016/2017

Residence basis of taxationSouth Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains, subject to certain exclusions. Non-residents are taxable on South African source income and capital gains only.

Income Tax

Individuals and special trusts

Rate of tax

Taxable income Rate of tax - years of assessment ending 28 Feb 2017

R0 – R188,000 18% of each R1

R188,001 – R293,600 R33,840 + 26% of each R above R188,000

R293,601 – R406,400 R61,296 + 31% of each R above R293,600

R406,401 – R550,100 R96,264 + 36% of each R above R406,400

R550,101 – R701,300 R147,996 + 39% of each R above R550,100

R701,301 and above R206,964 + 41% of each R above R701,300

Taxable income Rate of tax - years of assessment ending 29 Feb 2016

R0 – R181,900 18% of each R1

R181,901 – R284,100 R32,742 + 26% of each R above R181,900

R284,101 – R393,200 R59,314 + 31% of each R above R284,100

R393,201 – R550,100 R93,135 + 36% of each R above R393,200

R550,101 – R701,300 R149,619 + 39% of each R above R550,100

R701,301 and above R208,587 + 41% of each R above R701,300

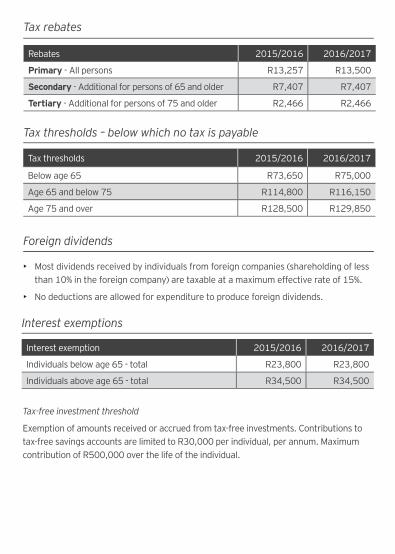

Rebates 2015/2016 2016/2017

Primary - All persons R13,257 R13,500

Secondary - Additional for persons of 65 and older R7,407 R7,407

Tertiary - Additional for persons of 75 and older R2,466 R2,466

Tax rebates

Tax thresholds 2015/2016 2016/2017

Below age 65 R73,650 R75,000

Age 65 and below 75 R114,800 R116,150

Age 75 and over R128,500 R129,850

Interest exemption 2015/2016 2016/2017

Individuals below age 65 - total R23,800 R23,800

Individuals above age 65 - total R34,500 R34,500

Tax thresholds – below which no tax is payable

Interest exemptions

Foreign dividends

• Most dividends received by individuals from foreign companies (shareholding of less than 10% in the foreign company) are taxable at a maximum effective rate of 15%.

• No deductions are allowed for expenditure to produce foreign dividends.

Tax-free investment threshold

Exemption of amounts received or accrued from tax-free investments. Contributions to tax-free savings accounts are limited to R30,000 per individual, per annum. Maximum contribution of R500,000 over the life of the individual.

Companies and Trusts

Rate of tax

Years of assessment ending between1 Apr 2015 and31 Mar 2016

Years of assessment ending between1 Apr 2016 and31 Mar 2017

Income tax

Company (resident and non- resident and personal service provider)

28% 28%

Gold mining, oil and gas, and long-term insurance companies are subject to special rules

Small business corporation (individual shareholders; gross income may not exceed R20m; investment income limited to 20% of gross income)

Sliding scale reaching 28% above taxable income of R550,000

Sliding scale reaching 28% above taxable income of R550,000

Micro business (may elect to be taxed on gross turnover on cash receipts only, limited record-keeping and submissions to SARS are required)

Turnover may not exceed R1m p.a. Sliding scale reaching 3% above turnover of R750,000

Turnover may not exceed R1m p.a. Sliding scale reaching 3% above turnover of R750,000

Trusts (excluding special trusts including personal service provider)

41% 41%

Withholding tax (subject to double taxation agreement)

Dividends tax 15% 15%

Interest paid to a non-resident 15% 15%

Royalties paid to a non-resident 15% 15%

Services fees paid to a non-resident

N/A N/A

Tax allowances

Manufacturing plant & machinery (section 12C)

40%: 20%: 20%: 20% 40%: 20%: 20%: 20%

Renewable energy assets (section 12B)

50%: 30%: 20% 50%: 30%: 20%

Commercial buildings (section 13quin)

5% 5%

Special tax allowance provisions apply to the capital expenditure of specific industries, e.g. mining, oil and gas extraction, farming, hoteliers, ship owners and toll road operators. Moveable assets which do not fall within the above categories qualify for varying rates set out in Interpretation Note 47 [section 11(e)].

Capital gains tax (CGT)

Events that trigger a disposal include a sale, donation, exchange, loss, death and emigration.

Exclusions

• Annual reduction of R40,000 for individuals and special trusts.

• Exclusion of R300,000 for the year of death.

• R2 million exemption on capital gain or capital loss on disposal of primary residence.

• Most personal (private, non-business) use assets and retirement benefits.

• Payments to original holders of long-term insurance policies.

• Small business exclusion (where a person is over 55 years old) of R1,8 million when a small business with a market value not exceeding R10 million is disposed of.

A portion of the net capital gain on the disposal of an asset is included in taxable income, according to a specific inclusion rate:

Taxpayer Inclusion rate Income tax rate Effective CGT rate

Individuals and special trusts 40% 0% - 41% 0% - 16,4%

Company (including non-resident company)

80% 28% 22,4%

Trusts 80% 41% 32,8%

Allowances and fringe benefits

Provisional tax

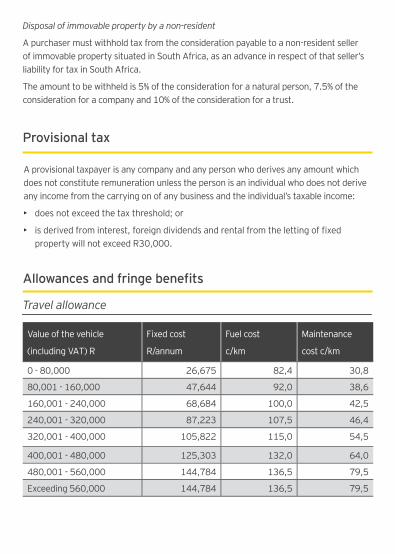

Value of the vehicle

(including VAT) R

Fixed cost

R/annum

Fuel cost

c/km

Maintenance

cost c/km

0 - 80,000 26,675 82,4 30,8

80,001 - 160,000 47,644 92,0 38,6

160,001 - 240,000 68,684 100,0 42,5

240,001 - 320,000 87,223 107,5 46,4

320,001 - 400,000 105,822 115,0 54,5

400,001 - 480,000 125,303 132,0 64,0

480,001 - 560,000 144,784 136,5 79,5

Exceeding 560,000 144,784 136,5 79,5

Travel allowance

A provisional taxpayer is any company and any person who derives any amount which does not constitute remuneration unless the person is an individual who does not derive any income from the carrying on of any business and the individual’s taxable income:

• does not exceed the tax threshold; or

• is derived from interest, foreign dividends and rental from the letting of fixed property will not exceed R30,000.

Disposal of immovable property by a non-resident

A purchaser must withhold tax from the consideration payable to a non-resident seller of immovable property situated in South Africa, as an advance in respect of that seller’s liability for tax in South Africa.

The amount to be withheld is 5% of the consideration for a natural person, 7.5% of the consideration for a company and 10% of the consideration for a trust.

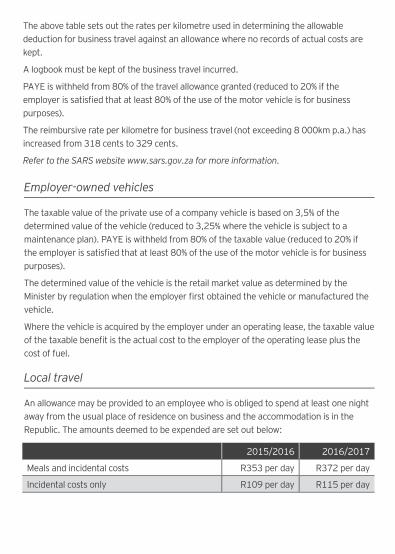

The above table sets out the rates per kilometre used in determining the allowable deduction for business travel against an allowance where no records of actual costs are kept.

A logbook must be kept of the business travel incurred.

PAYE is withheld from 80% of the travel allowance granted (reduced to 20% if the employer is satisfied that at least 80% of the use of the motor vehicle is for business purposes).

The reimbursive rate per kilometre for business travel (not exceeding 8 000km p.a.) has increased from 318 cents to 329 cents.

Refer to the SARS website www.sars.gov.za for more information.

Employer-owned vehicles

The taxable value of the private use of a company vehicle is based on 3,5% of the determined value of the vehicle (reduced to 3,25% where the vehicle is subject to a maintenance plan). PAYE is withheld from 80% of the taxable value (reduced to 20% if the employer is satisfied that at least 80% of the use of the motor vehicle is for business purposes).

The determined value of the vehicle is the retail market value as determined by the Minister by regulation when the employer first obtained the vehicle or manufactured the vehicle.

Where the vehicle is acquired by the employer under an operating lease, the taxable value of the taxable benefit is the actual cost to the employer of the operating lease plus the cost of fuel.

Local travel

An allowance may be provided to an employee who is obliged to spend at least one night away from the usual place of residence on business and the accommodation is in the Republic. The amounts deemed to be expended are set out below:

2015/2016 2016/2017

Meals and incidental costs R353 per day R372 per day

Incidental costs only R109 per day R115 per day

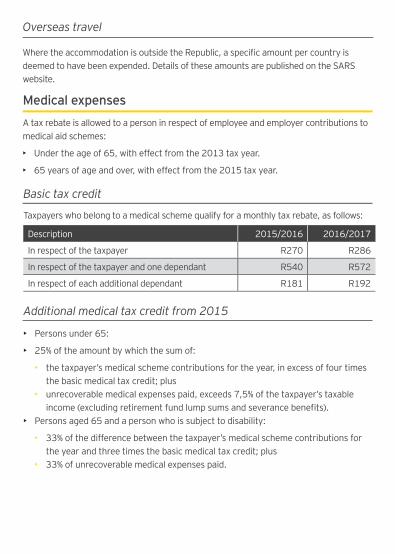

A tax rebate is allowed to a person in respect of employee and employer contributions to medical aid schemes:

• Under the age of 65, with effect from the 2013 tax year.

• 65 years of age and over, with effect from the 2015 tax year.

Taxpayers who belong to a medical scheme qualify for a monthly tax rebate, as follows:

• Persons under 65:

• 25% of the amount by which the sum of:

• the taxpayer’s medical scheme contributions for the year, in excess of four times the basic medical tax credit; plus

• unrecoverable medical expenses paid, exceeds 7,5% of the taxpayer’s taxable income (excluding retirement fund lump sums and severance benefits).

• Persons aged 65 and a person who is subject to disability:

• 33% of the difference between the taxpayer’s medical scheme contributions for the year and three times the basic medical tax credit; plus

• 33% of unrecoverable medical expenses paid.

Description 2015/2016 2016/2017

In respect of the taxpayer R270 R286

In respect of the taxpayer and one dependant R540 R572

In respect of each additional dependant R181 R192

Medical expenses

Basic tax credit

Additional medical tax credit from 2015

Overseas travel

Where the accommodation is outside the Republic, a specific amount per country is deemed to have been expended. Details of these amounts are published on the SARS website.

Retirement fund lump sum withdrawal benefits

Retirement fund lump sum withdrawal benefits consist of lump sums from a pension, pension preservation, provident, provident preservation or retirement annuity fund on withdrawal (including assignment in terms of a divorce order).

Taxable income Rate of tax

R0 – R25,000 0% of taxable income

R25,001 – R660,000 18% of taxable income above R25,000

R660,001 – R990,000 R114,300 + 27% of taxable income above R660,000

R990,001 and above R203,400 + 36% of taxable income above R990,000

Effective 1 March 2016, employer contributions to pension, provident and retirement annuity funds are included in the individual’s taxable income as a taxable fringe benefit and deemed to be a contribution made by the individual.

The value of the fringe benefit in the case of:

• Defined contribution funds, is equal to the actual employer contribution.

• Funds other than defined contribution funds, is calculated in accordance with a formula.

Individuals are allowed to claim a deduction for contributions to a pension, provident and retirement annuity fund. The deduction is limited to the lesser of:

• R350,000; or

• 27,5% of the higher of ‘remuneration’ or ‘taxable income’.

Retirement funds

Taxable benefit in respect of employer contributions

Deduction in respect of contributions

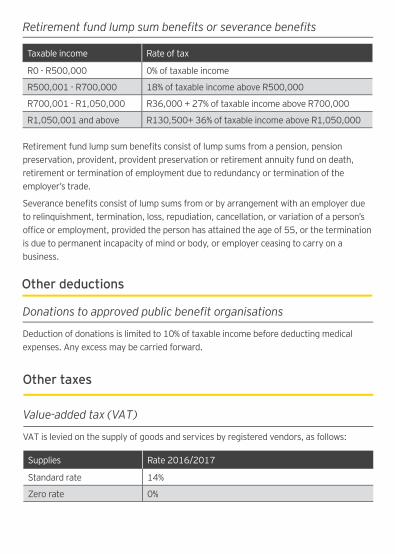

Value-added tax (VAT)

VAT is levied on the supply of goods and services by registered vendors, as follows:

Retirement fund lump sum benefits or severance benefits

Taxable income Rate of tax

R0 - R500,000 0% of taxable income

R500,001 - R700,000 18% of taxable income above R500,000

R700,001 - R1,050,000 R36,000 + 27% of taxable income above R700,000

R1,050,001 and above R130,500+ 36% of taxable income above R1,050,000

Retirement fund lump sum benefits consist of lump sums from a pension, pension preservation, provident, provident preservation or retirement annuity fund on death, retirement or termination of employment due to redundancy or termination of the employer’s trade.

Severance benefits consist of lump sums from or by arrangement with an employer due to relinquishment, termination, loss, repudiation, cancellation, or variation of a person’s office or employment, provided the person has attained the age of 55, or the termination is due to permanent incapacity of mind or body, or employer ceasing to carry on a business.

Other deductions

Donations to approved public benefit organisations

Deduction of donations is limited to 10% of taxable income before deducting medical expenses. Any excess may be carried forward.

Other taxes

Supplies Rate 2016/2017

Standard rate 14%

Zero rate 0%

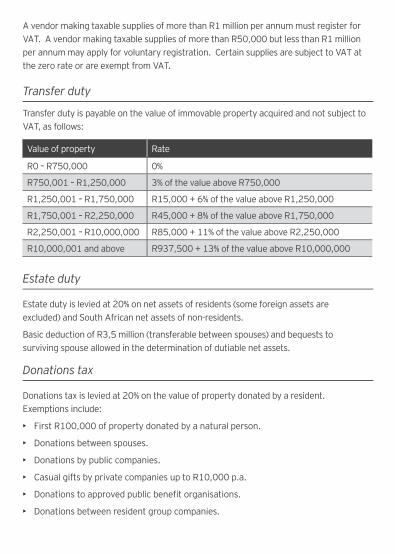

Value of property Rate

R0 – R750,000 0%

R750,001 – R1,250,000 3% of the value above R750,000

R1,250,001 – R1,750,000 R15,000 + 6% of the value above R1,250,000

R1,750,001 – R2,250,000 R45,000 + 8% of the value above R1,750,000

R2,250,001 – R10,000,000 R85,000 + 11% of the value above R2,250,000

R10,000,001 and above R937,500 + 13% of the value above R10,000,000

Estate duty

Transfer duty

Transfer duty is payable on the value of immovable property acquired and not subject to VAT, as follows:

Donations tax

Estate duty is levied at 20% on net assets of residents (some foreign assets are excluded) and South African net assets of non-residents.

Basic deduction of R3,5 million (transferable between spouses) and bequests to surviving spouse allowed in the determination of dutiable net assets.

A vendor making taxable supplies of more than R1 million per annum must register for VAT. A vendor making taxable supplies of more than R50,000 but less than R1 million per annum may apply for voluntary registration. Certain supplies are subject to VAT at the zero rate or are exempt from VAT.

Donations tax is levied at 20% on the value of property donated by a resident. Exemptions include:

• First R100,000 of property donated by a natural person.

• Donations between spouses.

• Donations by public companies.

• Casual gifts by private companies up to R10,000 p.a.

• Donations to approved public benefit organisations.

• Donations between resident group companies.

Skills Development Levy (SDL)

Securities Transfer Tax (STT)

Other

Unemployment Insurance Fund (UIF)

SDL is payable by employers to SARS at a rate of 1% of employees’ total remuneration. Employers paying annual remuneration of less than R500,000 are exempt from SDL.

STT is imposed at a rate of 0,25% on every transfer (including cancellation) of a security.

• General fuel levy increases by 30 cents per litre on 6 April 2016 (to R2,85 per litre of petrol and to R2,70 per litre of diesel)

• Excise duties on alcoholic beverages increase by between 6,7% and 8,5%

• Plastic bag levy increases from 6 cents to 8 cents per bag from 1 April 2016

• Incandescent globe tax increases from R4 to R6 per globe

• Tyre levy at R2,30 per kilogram to be introduced on 1 October 2016

• A tax on sugar sweetened beverages to be introduced on 1 April 2017

UIF is payable to SARS by employers and employees at a rate of 1% of the employees’ remuneration up to a threshold.

Employers not registered for PAYE or SDL purposes must pay the UIF contributions to the Unemployment Insurance Commissioner.

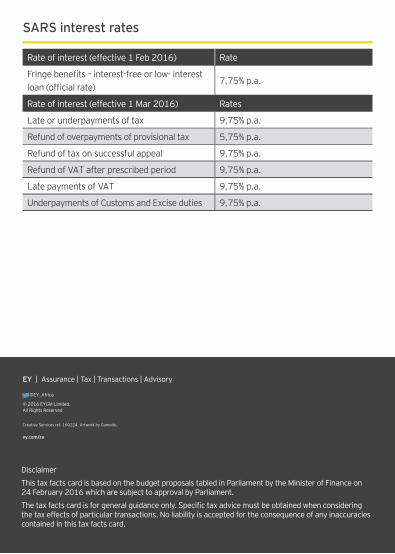

SARS interest rates

Rate of interest (effective 1 Feb 2016) Rate

Fringe benefits – interest-free or low- interest loan (official rate)

7,75% p.a.

Rate of interest (effective 1 Mar 2016) Rates

Late or underpayments of tax 9,75% p.a.

Refund of overpayments of provisional tax 5,75% p.a.

Refund of tax on successful appeal 9,75% p.a.

Refund of VAT after prescribed period 9,75% p.a.

Late payments of VAT 9,75% p.a.

Underpayments of Customs and Excise duties 9,75% p.a.

Disclaimer

This tax facts card is based on the budget proposals tabled in Parliament by the Minister of Finance on 24 February 2016 which are subject to approval by Parliament.

The tax facts card is for general guidance only. Specific tax advice must be obtained when considering the tax effects of particular transactions. No liability is accepted for the consequence of any inaccuracies contained in this tax facts card.