37

February 26 th , 2018 Cerved Information Solutions S.p.A. Results to 31 December 2017

0 73

132

0 128 142

109 189 255

191 191 191

0 103 188

16 159 189

221 221 221

92 188 210

February 26th, 2018

Cerved Information Solutions S.p.A.

Results to 31 December 2017

1

Disclaimer

This presentation and any materials distributed in connection herewith (together, the “Presentation”) do not constitute or form a part of, and should not be construed as, an offer for sale or subscription of or solicitation of any offer to purchase or subscribe for any securities, and neither this Presentation nor anything contained herein shall form the basis of, or be relied upon in connection with, or act as an inducement to enter into, any contract or commitment whatsoever. The information contained in this Presentation has not been independently verified and no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness, reasonableness or correctness of the information or opinions contained herein. None of Cerved Information Solutions S.p.A., its subsidiaries or any of their respective employees, advisers, representatives or affiliates shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this Presentation. The information contained in this Presentation is provided as at the date of this Presentation and is subject to change without notice.

Statements made in this Presentation may include forward-looking statements. These statements may be identified by the fact that they use words such as “anticipate”, “estimate”, “should”, “expect”, “guidance”, “project”, “intend”, “plan”, “believe”, and/or other words and terms of similar meaning in connection with, among other things, any discussion of results of operations, financial condition, liquidity, prospects, growth, strategies or developments in the industry in which we operate. Such statements are based on management’s current intentions, expectations or beliefs and involve inherent risks, assumptions and uncertainties, including factors that could delay, divert or change any of them. Forward-looking statements contained in this Presentation regarding trends or current activities should not be taken as a representation that such trends or activities will continue in the future. Actual outcomes, results and other future events may differ materially from those expressed or implied by the statements contained herein. Such differences may adversely affect the outcome and financial effects of the plans and events described herein and may result from, among other things, changes in economic, business, competitive, technological, strategic or regulatory factors and other factors affecting the business and operations of the company. Neither Cerved Information Solutions S.p.A. nor any of its affiliates is under any obligation, and each such entity expressly disclaims any such obligation, to update, revise or amend any forward-looking statements, whether as a result of new information, future events or otherwise. You should not place undue reliance on any such forward-looking statements, which speak only as of the date of this Presentation. It should be noted that past performance is not a guide to future performance. Please also note that interim results are not necessarily indicative of full-year results.

2

Today’s Presenters

Marco Nespolo – Chief Executive Officer

Giovanni Sartor – Chief Financial Officer

9 years at Cerved

9 years of TMT industry experience

Prior experience: Seves Group, Nylstar (RP-Snia JV), Eni, Heinz

Education: MBA from Eni University; Statistics and Economics degree from University of Padua

Pietro Masera – Head of Corporate Development & IR

5 years at Cerved

15 years of TMT industry experience

Prior experience: CVC, Deutsche Bank, Bankers Trust, UBS, SEAT

Education: degree in Economics and Business Administration from University of Bergamo

9 years at Cerved

13 years of TMT industry experience

Prior experience: Bain Capital, Bain & Company, Citibank

Education: degree in Business Administration from Bocconi University of Milan

3

Table of Contents

Highlights 1

Financial Review 3

Appendices 4

Business Review 2

4

Executive Summary

Macro Highlights

Continuing economic recovery in Italy albeit lagging European peers

Italian bank actions to address NPEs finally materialising in 2018

2017

Financial Results

Revenues +6.5% vs 2016, +5.6% organic

Adjusted EBITDA1) +4.0% vs 2016, +3.7% organic

Operating Cash Flow €142.6m in 2017, (1.0%) vs 2016

Adjusted Net Income €98.2m in 2017, +6.8% vs 2016

Leverage2) 2.5x LTM Adjusted EBITDA

Other

Dividends of €52.7m (+9.3%) proposed by the Board to the AGM

Group reorganization with mergers effective from March 2018

Investor Day II in June 2018 to provide new Strategic Outlook

On-boarding of more than €20bn of AuMs as a result of partnerships

closed and servicing contracts recently signed

Note: 1) Adjusted EBITDA excludes provisions of €0.7m related to the Long Term Incentive Plan in FY’16 and €1.8m in FY’17 2) Leverage excludes €18.0m cash-out occurred on January 2nd, 2018 for the acquisition of the BP Bari servicing platform

5

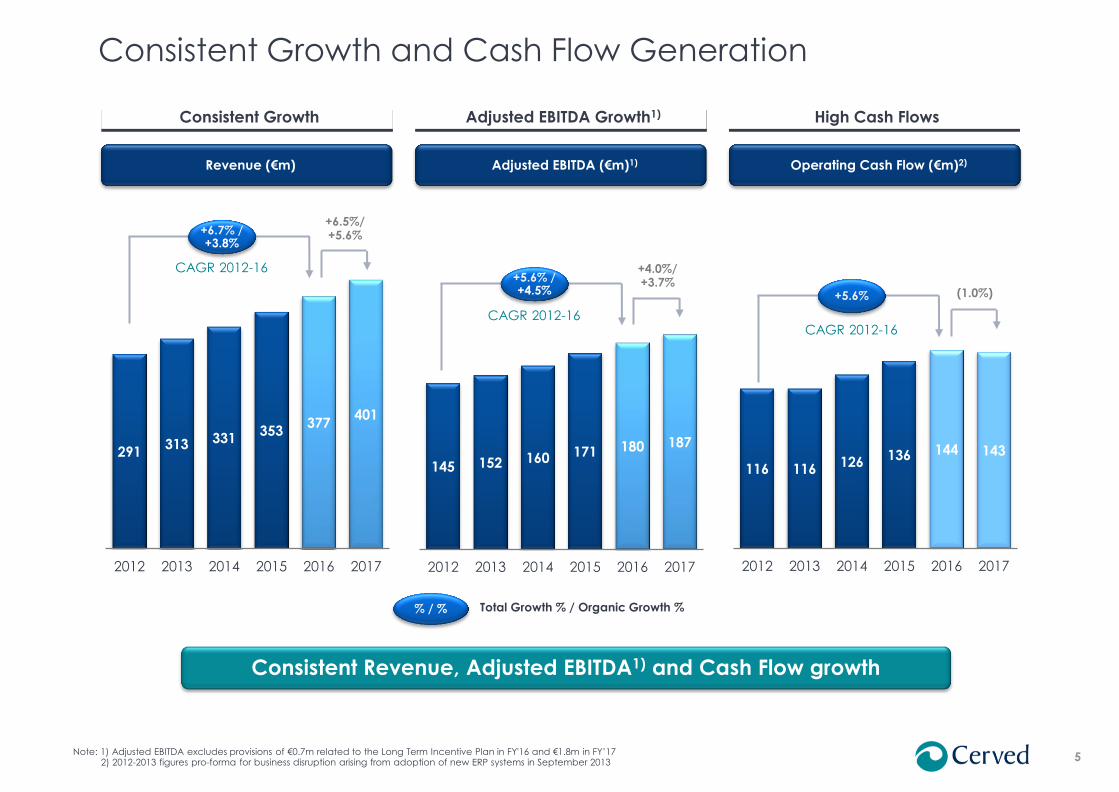

116 116 126

136 144 143

2012 2013 2014 2015 2016 2017

145 152 160 171 180 187

2012 2013 2014 2015 2016 2017

291 313 331

353 377

401

2012 2013 2014 2015 2016 2017

+6.5%/ +5.6%

Consistent Growth and Cash Flow Generation

Note: 1) Adjusted EBITDA excludes provisions of €0.7m related to the Long Term Incentive Plan in FY'16 and €1.8m in FY’17 2) 2012-2013 figures pro-forma for business disruption arising from adoption of new ERP systems in September 2013

Consistent Growth Adjusted EBITDA Growth1) High Cash Flows

Revenue (€m) Adjusted EBITDA (€m)1) Operating Cash Flow (€m)2)

Consistent Revenue, Adjusted EBITDA1) and Cash Flow growth

% / % Total Growth % / Organic Growth %

+6.7% / +3.8%

CAGR 2012-16 +4.0%/ +3.7% +5.6% /

+4.5%

CAGR 2012-16

(1.0%) +5.6%

CAGR 2012-16

6

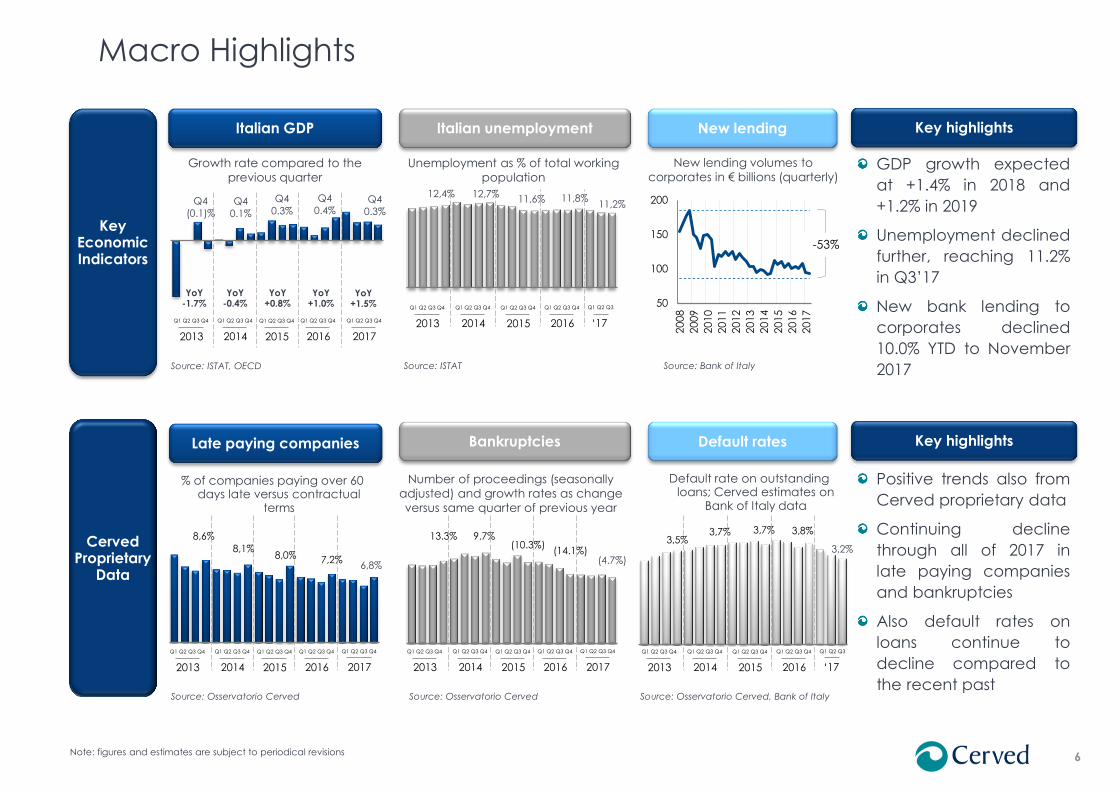

Macro Highlights

Note: figures and estimates are subject to periodical revisions

Key Economic Indicators

Cerved Proprietary

Data

GDP growth expected

at +1.4% in 2018 and

+1.2% in 2019

Unemployment declined

further, reaching 11.2%

in Q3’17

New bank lending to

corporates declined

10.0% YTD to November

2017

Positive trends also from

Cerved proprietary data

Continuing decline

through all of 2017 in

late paying companies

and bankruptcies

Also default rates on

loans continue to

decline compared to

the recent past

Key highlights

Key highlights

Source: Bank of Italy

12,4% 12,7% 11,6% 11,8%

11,2%

8,6%

8,1% 8,0% 7,2%

6,8%

Italian unemployment Italian GDP New lending

% of companies paying over 60 days late versus contractual

terms

Number of proceedings (seasonally

adjusted) and growth rates as change

versus same quarter of previous year

Growth rate compared to the

previous quarter

New lending volumes to

corporates in € billions (quarterly)

Late paying companies Bankruptcies Default rates

Default rate on outstanding loans; Cerved estimates on

Bank of Italy data

Source: Osservatorio Cerved

50

100

150

200

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

13.3% 9.7% (10.3%)

(14.1%) (4.7%)

Source: Osservatorio Cerved

3,5% 3,7% 3,7% 3,8%

3,2%

Source: Osservatorio Cerved, Bank of Italy

Q4

(0.1)%

Q4

0.1%

Q4

0.3%

Q4

0.4% Q4

0.3%

Source: ISTAT, OECD

YoY +0.8%

YoY -0.4%

YoY -1.7%

Source: ISTAT

-53%

YoY +1.0%

Unemployment as % of total working

population

Q1 Q2 Q3 Q4

2013

Q1 Q2 Q3 Q4

2014

Q1 Q2 Q3 Q4

2015

Q1 Q2 Q3 Q4

2016

Q1 Q2 Q3 Q4

2013

Q1 Q2 Q3 Q4

2014

Q1 Q2 Q3 Q4

2015

Q1 Q2 Q3 Q4

2016 ‘17

Q1 Q2 Q3

Q1 Q2 Q3 Q4

2013

Q1 Q2 Q3 Q4

2014

Q1 Q2 Q3 Q4

2015

Q1 Q2 Q3 Q4

2016 ‘17

Q1 Q2 Q3 Q1 Q2 Q3 Q4

2013

Q1 Q2 Q3 Q4

2014

Q1 Q2 Q3 Q4

2015

Q1 Q2 Q3 Q4

2016

YoY +1.5%

Q1 Q2 Q3 Q4

2017

Q1 Q2 Q3 Q4

2017

Q1 Q2 Q3 Q4

2013

Q1 Q2 Q3 Q4

2014

Q1 Q2 Q3 Q4

2015

Q1 Q2 Q3 Q4

2016

Q1 Q2 Q3 Q4

2017

7

Highlights 1

Table of Contents

Business Review 2

Financial Review 3

Appendices 4

8

Total

Snapshot of 2017 Divisional Results

Credit Info

Financial Inst.

Credit Info

Corporate

Credit Management

Marketing Solutions

127 129

148 157

+2.2%

+5.7%

+11.7%

+16.1%

+6.5% (+5.6% organic)

+2.0%

+13.2%

+14.0%

+4.0% (+3.7% organic)

8 9

24 28

21 25

85 95

F.I.: double-digit growth in appraisals, up-

selling and new customer acquisition in BI

Corporate: launch of new products and

continuing focus on sales force effectiveness

which positively impacted consumption

EBITDA: minor margin compression mainly due

to strong growth in lower-margin segments

Revenues: met targets despite limited NPL

portfolio intake during 2017, re-scoping of the

remarketing segment

EBITDA: minor margin accretion due to mix

effect and operational improvements

Revenues: PayClick full-year consolidation

and strong trajectory, softer growth in the

legacy business

EBITDA: margin uplift in legacy business

compensating dilution from PayClick

consolidation

Drivers Adjusted EBITDA1) Revenues Area

147 150

Consolidated and divisional figures in line with company strategic outlook 2016-2018

Note: 1) Adjusted EBITDA excludes provisions of €1.8m related to the Long Term Incentive Plan

+4.1%

9

Business Review – Topics

Operational and Strategic Update for 2017 and Key Actions for 2018

Business

Corporate

Credit Information – Financial Institutions

Credit Information – Corporate

Credit Management

Marketing Solutions

Capital Structure

Investor Relations

Mergers & Acquisitions

10

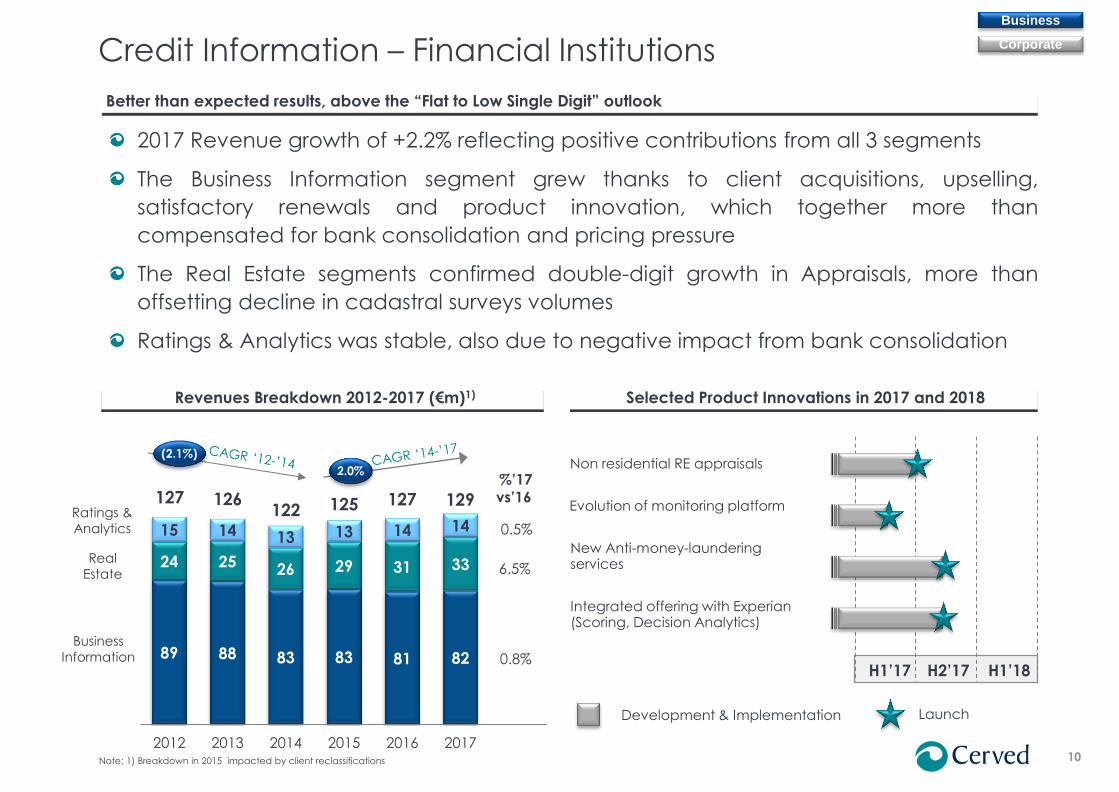

2017 Revenue growth of +2.2% reflecting positive contributions from all 3 segments

The Business Information segment grew thanks to client acquisitions, upselling,

satisfactory renewals and product innovation, which together more than

compensated for bank consolidation and pricing pressure

The Real Estate segments confirmed double-digit growth in Appraisals, more than

offsetting decline in cadastral surveys volumes

Ratings & Analytics was stable, also due to negative impact from bank consolidation

Credit Information – Financial Institutions

Better than expected results, above the “Flat to Low Single Digit” outlook

Business

Corporate

Revenues Breakdown 2012-2017 (€m)1) Selected innovation and product expansion initiatives

89 88 83 83 81 82

24 25 26 29 31 33

15 14 13 13 14 14

2012 2013 2014 2015 2016 2017

127 126 122 125 127

0.8%

%’17

vs’16

6.5%

0.5%

2.0%

(2.1%)

Note: 1) Breakdown in 2015 impacted by client reclassifications

Business

Information

Real

Estate

Ratings &

Analytics

129

H2’17 H1’18 H1’17

Non residential RE appraisals

Evolution of monitoring platform

New Anti-money-laundering services

Integrated offering with Experian (Scoring, Decision Analytics)

Selected Product Innovations in 2017 and 2018

Development & Implementation Launch

11

4,2% 5,8%

5,1% 6,7%

Lost

Clients

Existing

Clients

New

Clients

Y-o-Y

Consumption

Note: 1) Consumption of points and services in 2017 compared to 2016 for Credit Information products by c. 20k corporate clients

2017 Revenue growth of +5.7% reflected the positive contribution of new product

launches and continuous effort of sales force excellence

Very strong Q4 (+9.3%) which compensated for the weak Q3 (+0.4%), in part due to

delays in the finalization of specific projects with large accounts

Product innovation and commercial effort on excellence remain a key area of focus in

2018

Credit Information – Corporates

Revenues on the high end of expectations of “Mid Single Digit Growth”

Business

Corporate

Consumption of Credit Information Points & Services 2017 vs 2016 1) Selected Product Innovations in 2017 and 2018

H2’17 H1’18 H1’17

Cerved Credit Suite

New Payline Decision systems

Industry-specific solutions & value propositions

New Foreign Report platform

Development & Implementation Launch

Integration of Credit Collection features into Credit Info platforms (Payline Collection & Credit Collection Score)

12

33%

Work-out

47%

Legal

Services

12%

Asset

Remark'ng

9%

2017 Revenue growth of +11.7%, with all segments performing in double-digit territory,

exception made for remarketing which is being re-scoped (eg. yacht business)

During 2017 AuMs almost doubled with the Barclays deal while NPLs growth was below

expectations due to delay in major portfolios’ transactions

Higher margins in 2017 mainly driven by business mix and operational improvements

Current focus on finalizing partnerships with Quaestio, BMPS and BP Bari, and on-

boarding new portfolios for more than €20bn

Significant recruiting effort on-going to support AuMs growth

Revenues in line with expectations despite limited new NPL portfolio intakes impacting 2017

Evolution of AuMs in 2015-2017 (€bn) Revenues Breakdown 2017PF1)

Credit Management Business

Corporate

Receivables &

Performing Loans

(33%)

NPL-related

activities

(67%)

12,0 13,3

11,0

1,7 1,0

25,1

FY'15 FY'16 Barclays New

Portfolios

Other Net

Changes

FY'17

Notes: Receivables under management of €0.7bn, €0.6bn and €0.8bn in 2015, 2016 and 2017; FY’17 excludes AuMs from BPB transaction Note: 1) partnership with Barclays considered on a full year basis

13

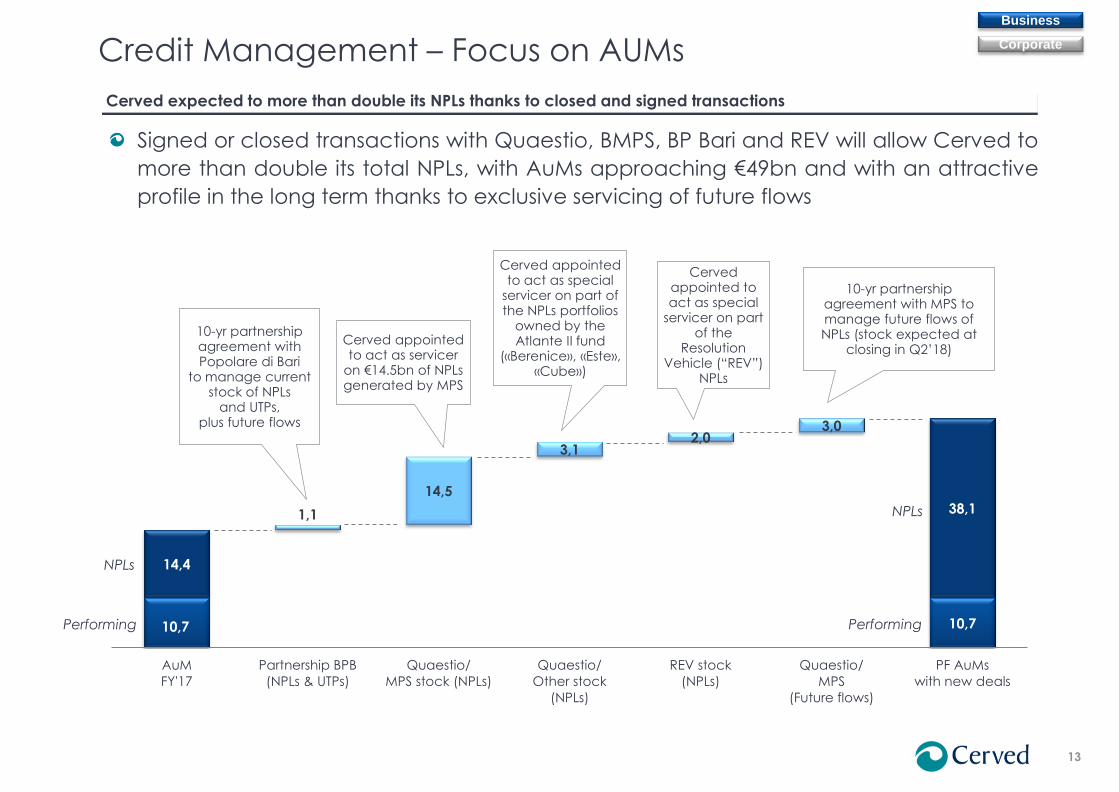

10,7 10,7

14,4

38,1 1,1

14,5

3,1 2,0

3,0

AuM

FY'17

Partnership BPB

(NPLs & UTPs)

Quaestio/

MPS stock (NPLs)

Quaestio/

Other stock

(NPLs)

REV stock

(NPLs)

Quaestio/

MPS

(Future flows)

PF AuMs

with new deals

Credit Management – Focus on AUMs Business

Corporate

Signed or closed transactions with Quaestio, BMPS, BP Bari and REV will allow Cerved to

more than double its total NPLs, with AuMs approaching €49bn and with an attractive

profile in the long term thanks to exclusive servicing of future flows

Cerved expected to more than double its NPLs thanks to closed and signed transactions

10-yr partnership agreement with Popolare di Bari

to manage current stock of NPLs

and UTPs, plus future flows

Cerved appointed to act as servicer

on €14.5bn of NPLs generated by MPS

10-yr partnership agreement with MPS to manage future flows of NPLs (stock expected at

closing in Q2’18)

Cerved appointed to act as special

servicer on part of the NPLs portfolios

owned by the Atlante II fund

(«Berenice», «Este», «Cube»)

Cerved appointed to act as special

servicer on part of the

Resolution Vehicle (“REV”)

NPLs

NPLs

Performing

NPLs

Performing

14

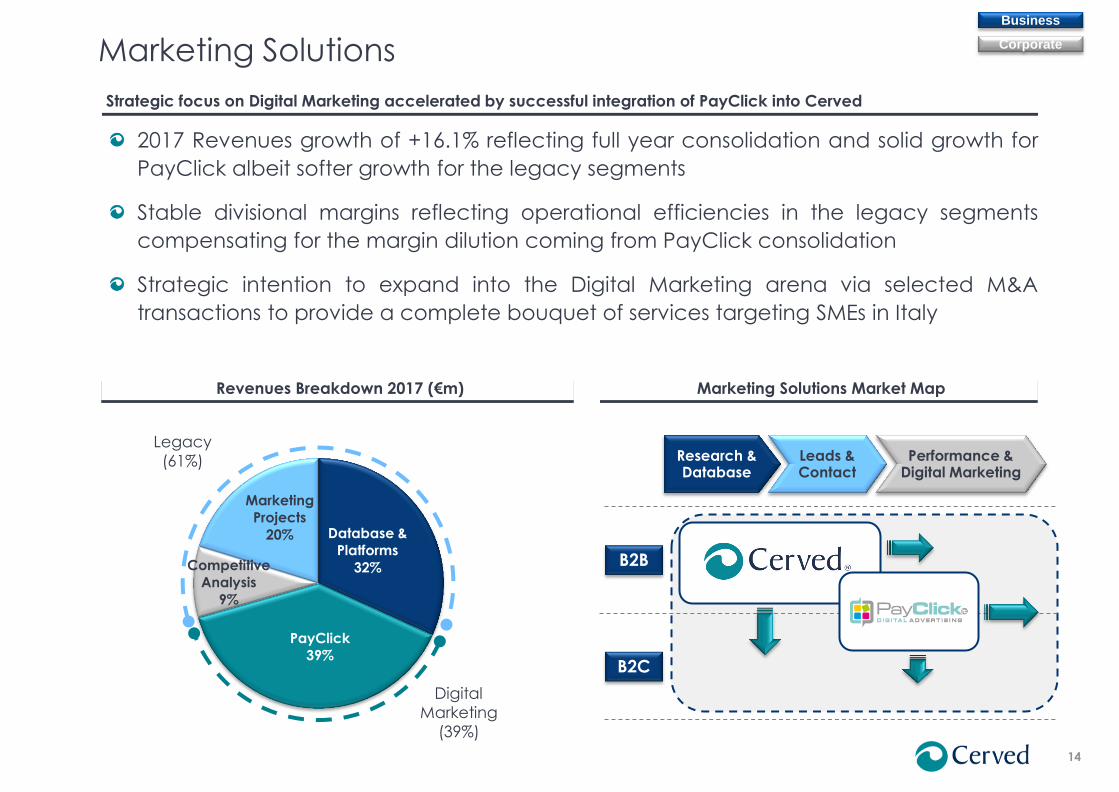

Marketing Solutions Market Map Revenues Breakdown 2017 (€m)

Marketing Solutions

Strategic focus on Digital Marketing accelerated by successful integration of PayClick into Cerved

Business

Corporate

2017 Revenues growth of +16.1% reflecting full year consolidation and solid growth for

PayClick albeit softer growth for the legacy segments

Stable divisional margins reflecting operational efficiencies in the legacy segments

compensating for the margin dilution coming from PayClick consolidation

Strategic intention to expand into the Digital Marketing arena via selected M&A

transactions to provide a complete bouquet of services targeting SMEs in Italy

Database &

Platforms

32%

PayClick

39%

Competitive

Analysis

9%

Marketing

Projects

20%

Research & Database

Performance & Digital Marketing

Leads & Contact

B2B

B2C

Legacy

(61%)

Digital

Marketing

(39%)

15

Net Debt Bridge Quarterly Leverage 2016 vs 2017

Capital Structure

Strong cash flow generation provides strong support for M&A strategy, dividend payout and deleverage

Deleverage to 2.5x at year-end 2017 (2.6x proforma for BP Bari transaction) confirms

Cerved’s strong cash generation capabilities

Board of Directors proposed dividend of €52.7m (+9.3% vs €48.2m paid in May 2016)

equating to 53.6% of 2017 Adjusted Net Income

Residual leverage capacity to 3.0x long-term target to be retained for M&A, share

buybacks and interest savings (25 bps savings under 2.85x)

Completed i) extension of €200m of TLB to end 2023 (from Jan 2022), ii) reduction of

margins, iii) removal of security package and iv) switch of TLA from amortizing to bullet

Corporate

Business

523

474

(143)

16 22

48 2 4

Ne

t D

eb

t

20

16

Op

. C

ash

Flo

w

Ca

sh-In

tere

sts

Ca

sh-T

axe

s

Ne

t d

ivid

en

ds

M&

A

No

n-R

ec

. &

Oth

er

ite

ms

Ne

t D

eb

t

20

17

3,1x 3,2x

3,1x

2,9x 2,8x 2,8x

2,7x

2,5x

Q1

'16

Q2

'16

Q3

'16

Q4

'16

Q1

'17

Q2

'17

Q3

'17

Q4

'17

Margin Ratchet

2.85x

Note: Q4 leverage excludes €18.0m cash-out occurred on January 2nd 2018 for the acquisition of the BP Bari servicing platform

16

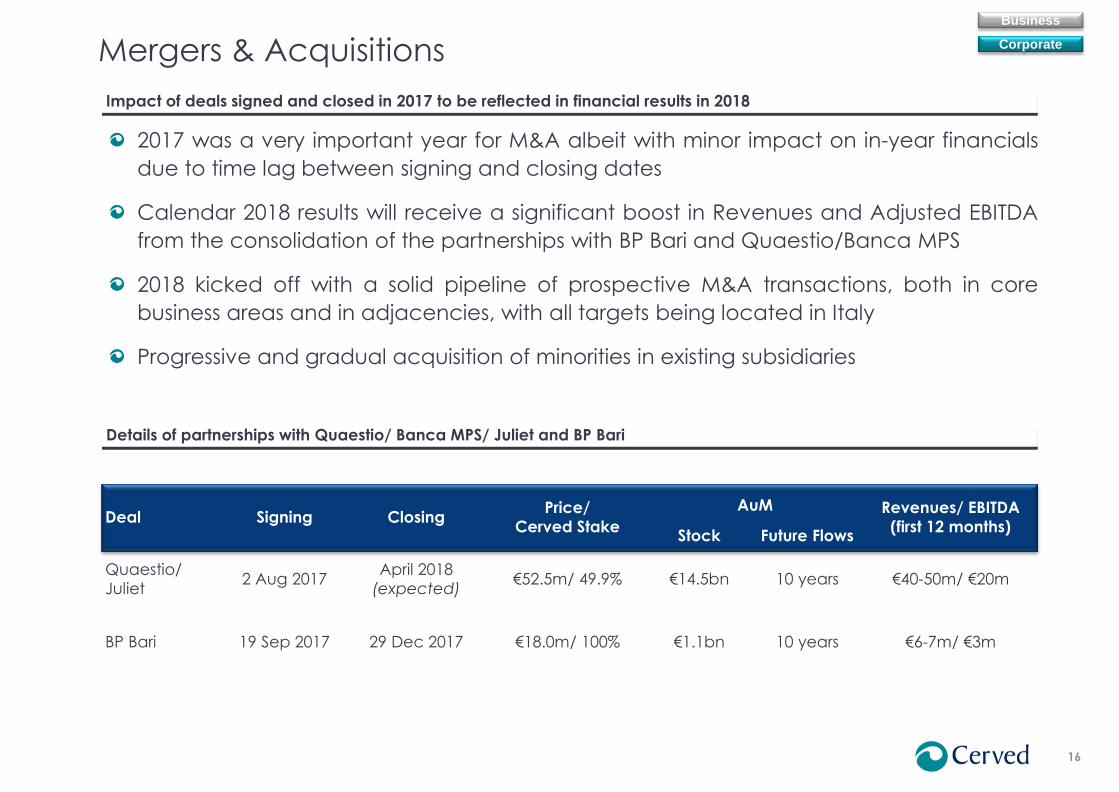

Deal Signing Closing Price/

Cerved Stake

AuM Revenues/ EBITDA

(first 12 months) Stock Future Flows

Quaestio/

Juliet 2 Aug 2017

April 2018

(expected) €52.5m/ 49.9% €14.5bn 10 years €40-50m/ €20m

BP Bari 19 Sep 2017 29 Dec 2017 €18.0m/ 100% €1.1bn 10 years €6-7m/ €3m

Details of partnerships with Quaestio/ Banca MPS/ Juliet and BP Bari

Mergers & Acquisitions

Impact of deals signed and closed in 2017 to be reflected in financial results in 2018

2017 was a very important year for M&A albeit with minor impact on in-year financials

due to time lag between signing and closing dates

Calendar 2018 results will receive a significant boost in Revenues and Adjusted EBITDA

from the consolidation of the partnerships with BP Bari and Quaestio/Banca MPS

2018 kicked off with a solid pipeline of prospective M&A transactions, both in core

business areas and in adjacencies, with all targets being located in Italy

Progressive and gradual acquisition of minorities in existing subsidiaries

Corporate

Business

17

Date Event Venue

Feb 27-28 Roadshow (Mediobanca) London

Mar 28 Equity Conference (HSBC) Paris

Apr 9 Annual General Meeting – Cerved Milan

Apr tbd Roadshow (Equita SIM) Switzerland

May 3 Mid-Small Cap Conf. (GS) London

May 7 Q1 2018 Results – Cerved Conf call

May 16-17 Italian Equity Conference (Kepler) Milan

Jun tbd Investor Day 2018 – Cerved London &

Milan

Jun 26 Business Services Conference (GS) London

Jun 27 CEO Conference (Mediobanca) Milan

Jul 30 H1 2018 Results – Cerved Conf call

Date Event Venue

Aug 1-3 US Roadshow (tbd) NY & Boston

Sep 5 Industrial Day (Borsa Italiana) Milan

Sep 12 Mid-Small Caps (JPM) London

Sep 28 Italian Conference (JPM) Milan

Oct tbd Roadshow (Kepler) Scandinavia

Oct 29 9M 2018 Results – Cerved Conf call

Nov 28 Mid Cap Conference (Exane) London

Nov-Dec Roadshow (tbd) Benelux

Nov-Dec Roadshow (tbd) Paris &

Frankfurt

Financial Calendar and Tentative Conferences and Roadshows in 2018

Investor Relations

Continued focus on providing clearer and insightful information to the financial community

Investor Relations team and capabilities reinforced in light of MiFid II regulation and

continuing effort to improve visibility of Cerved within the financial community

Investor Day II to be hosted in London in June, with a follow-up event in Cerved’s

headquarters in Milan to offer a more granular look into Cerved’s products and

services range (exact dates to be defined)

Corporate

Business

18

Highlights 1

Table of Contents

Appendices 4

Business Review 2

Financial Review 3

19

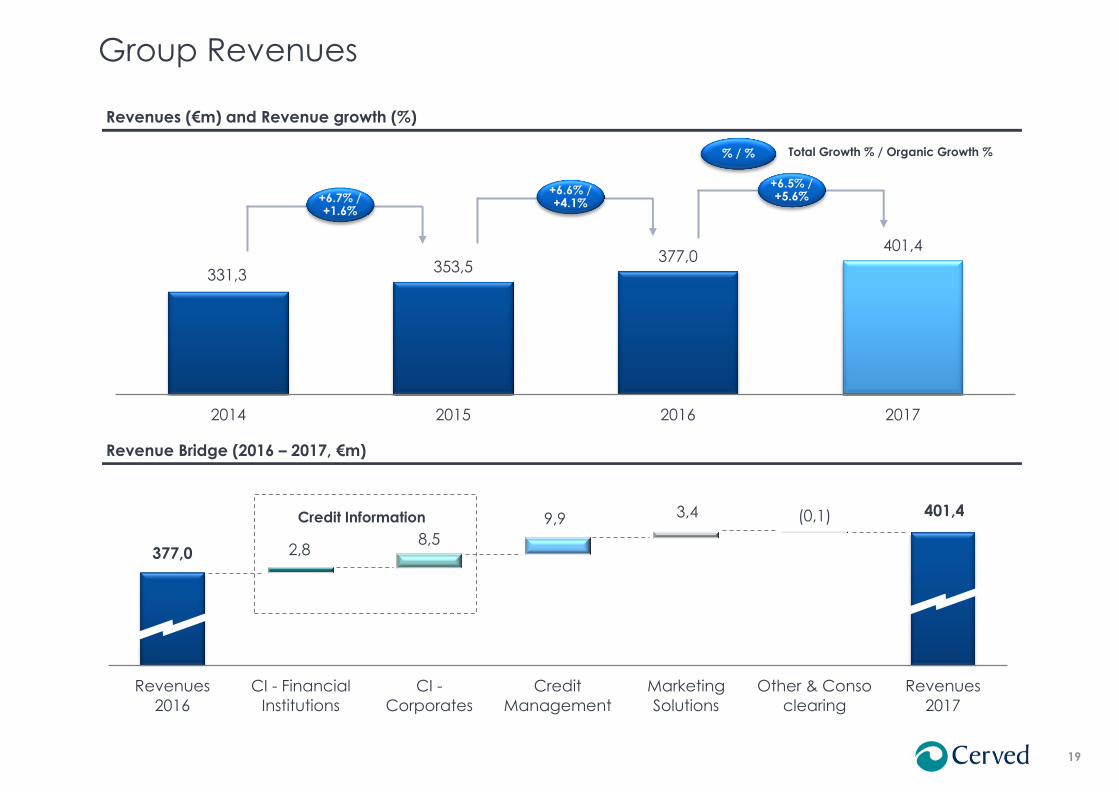

Group Revenues

Revenue Bridge (2016 – 2017, €m)

Revenues (€m) and Revenue growth (%)

331,3 353,5

377,0 401,4

2014 2015 2016 2017

377,0

401,4

2,8 8,5

9,9 3,4 (0,1)

Revenues

2016

CI - Financial

Institutions

CI -

Corporates

Credit

Management

Marketing

Solutions

Other & Conso

clearing

Revenues

2017

Credit Information

% / % Total Growth % / Organic Growth %

+6.5% / +5.6% +6.7% /

+1.6%

+6.6% / +4.1%

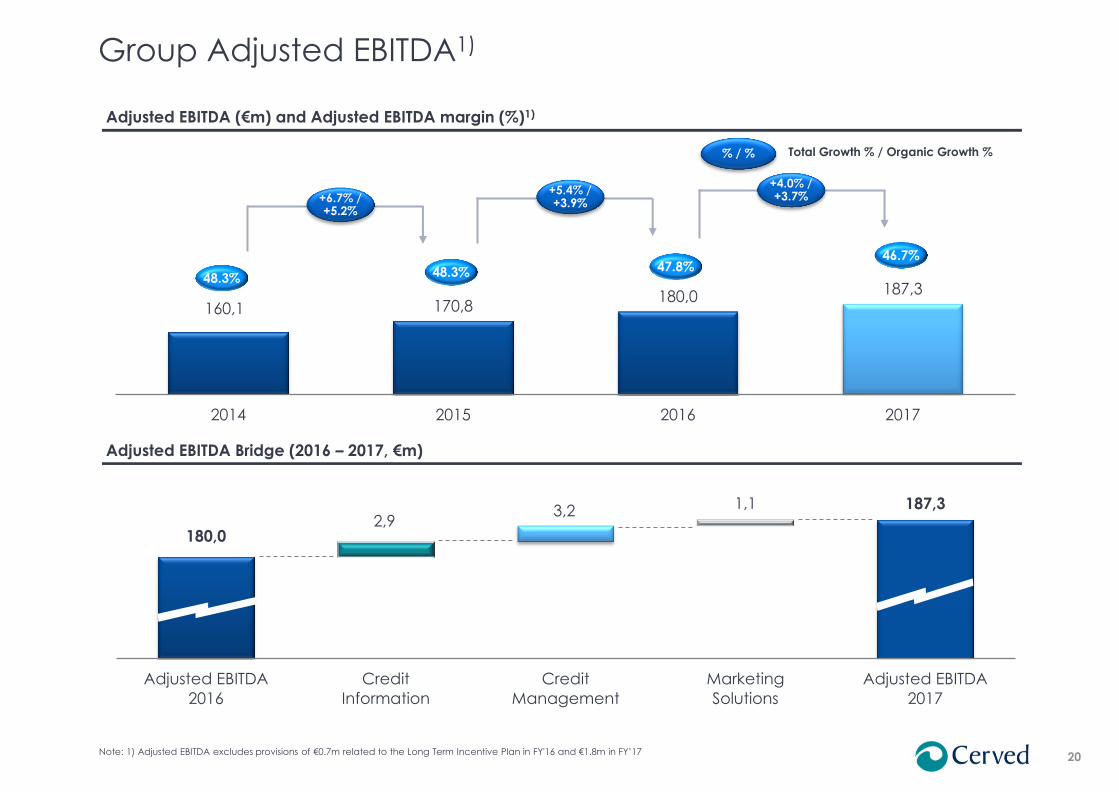

20

180,0

187,3 2,9

3,2 1,1

Adjusted EBITDA

2016

Credit

Information

Credit

Management

Marketing

Solutions

Adjusted EBITDA

2017

160,1 170,8 180,0 187,3

2014 2015 2016 2017

Group Adjusted EBITDA1)

Adjusted EBITDA Bridge (2016 – 2017, €m)

Adjusted EBITDA (€m) and Adjusted EBITDA margin (%)1)

48.3% 48.3%

% / % Total Growth % / Organic Growth %

46.7% 47.8%

+6.7% / +5.2%

+4.0% / +3.7%

Note: 1) Adjusted EBITDA excludes provisions of €0.7m related to the Long Term Incentive Plan in FY'16 and €1.8m in FY’17

+5.4% / +3.9%

21

53,3 75,0 84,7 94,6

2014 2015 2016 2017

Note: 1) Breakdown between Corporates and Financial Institutions could be slightly different from past figures due to the reclassification of some clients within segments 2) Adjusted EBITDA excludes provisions of €0.7m related to the Long Term Incentive Plan in FY'16 and €1.8m in FY’17

Group Divisional Performance

Credit Information Credit Management Marketing Solutions

122,0 125,4 126,6 129,4

142,7 141,7 148,1 156,5

264,7 267,1 274,7 286,0

2014 2015 2016 2017

Re

ve

nu

e

Ad

just

ed

EB

ITD

A2)

142,1 145,4 147,5 150,4

2014 2015 2016 2017

11,2

19,5 24,4

27,6

2014 2015 2016 2017

14,7 13,8 21,1

24,5

2014 2015 2016 2017

6,8 5,9 8,2 9,3

2014 2015 2016 2017

45.9% 42.7%

21.0%

26.0%

53.7% 54.4% 53.7%

Fin. Inst.

Corp.

% YoY Growth % Adjusted EBITDA margin % % CAGR

37.9%

29.2% 52.6%

%

28.8%

38.7%

1)

+14.0%

+9.9%

CAGR ‘14-16

+13.2%

+47.8%

CAGR ‘14-16

+1.9%

CAGR ‘14-16

+2.0%

+16.1%

+19.7%

CAGR ‘14-16

+11.7%

+26.1%

CAGR ‘14-16

+1.9%

CAGR ‘14-16

+4.1%

22

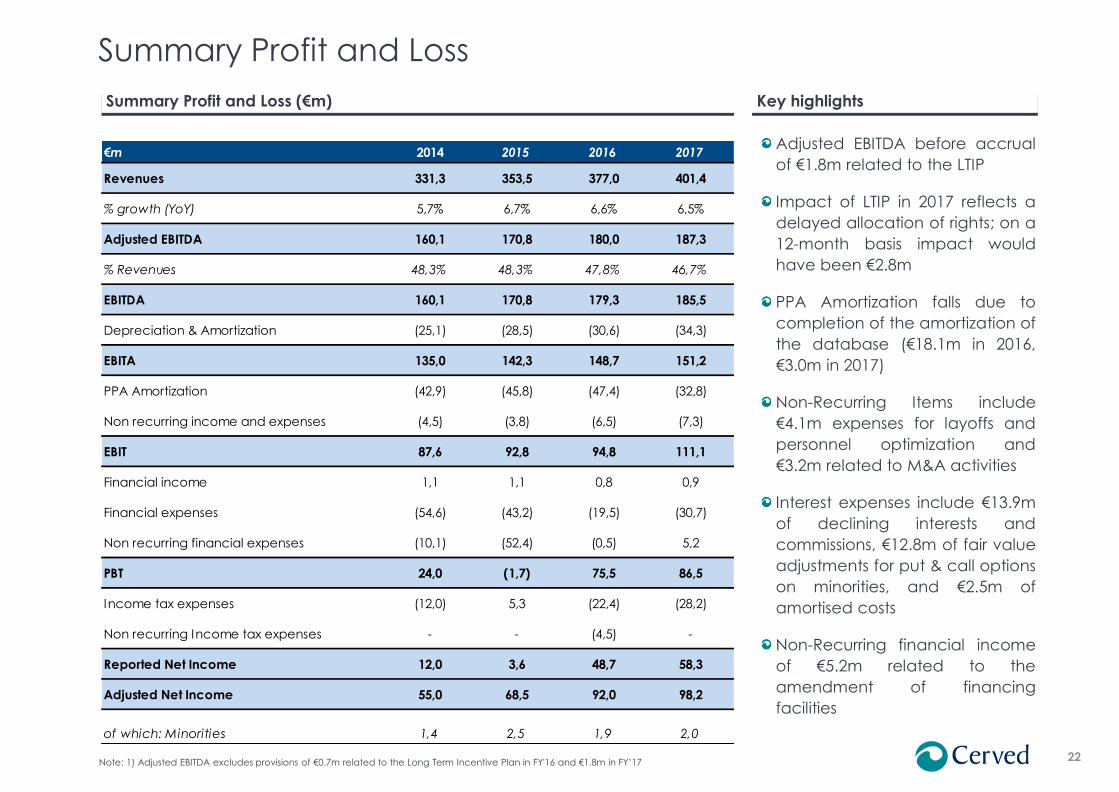

€m 2014 2015 2016 2017

Revenues 331,3 353,5 377,0 401,4

% growth (YoY) 5,7% 6,7% 6,6% 6,5%

Adjusted EBITDA 160,1 170,8 180,0 187,3

% Revenues 48,3% 48,3% 47,8% 46,7%

EBITDA 160,1 170,8 179,3 185,5

Depreciation & Amortization (25,1) (28,5) (30,6) (34,3)

EBITA 135,0 142,3 148,7 151,2

PPA Amortization (42,9) (45,8) (47,4) (32,8)

Non recurring income and expenses (4,5) (3,8) (6,5) (7,3)

EBIT 87,6 92,8 94,8 111,1

Financial income 1,1 1,1 0,8 0,9

Financial expenses (54,6) (43,2) (19,5) (30,7)

Non recurring financial expenses (10,1) (52,4) (0,5) 5,2

PBT 24,0 (1,7) 75,5 86,5

Income tax expenses (12,0) 5,3 (22,4) (28,2)

Non recurring Income tax expenses - - (4,5) -

Reported Net Income 12,0 3,6 48,7 58,3

Adjusted Net Income 55,0 68,5 92,0 98,2

of which: Minorities 1,4 2,5 1,9 2,0

Adjusted EBITDA before accrual

of €1.8m related to the LTIP

Impact of LTIP in 2017 reflects a

delayed allocation of rights; on a

12-month basis impact would

have been €2.8m

PPA Amortization falls due to

completion of the amortization of

the database (€18.1m in 2016,

€3.0m in 2017)

Non-Recurring Items include

€4.1m expenses for layoffs and

personnel optimization and

€3.2m related to M&A activities

Interest expenses include €13.9m

of declining interests and

commissions, €12.8m of fair value

adjustments for put & call options

on minorities, and €2.5m of

amortised costs

Non-Recurring financial income

of €5.2m related to the

amendment of financing

facilities

Summary Profit and Loss (€m)

Summary Profit and Loss

Key highlights

Note: 1) Adjusted EBITDA excludes provisions of €0.7m related to the Long Term Incentive Plan in FY'16 and €1.8m in FY’17

23

Net Working Capital reached

12.5% of Revenues in 2017

compared to 10.8% in 2016

Trade Receivables increased by

€7.0m mainly due to the

sustained growth in the Credit

Management division, albeit

declined from 41.1% to 40.3% as

a percentage of Revenues

Trade Payables increased by

€7.5m reflecting the impact of

higher costs and revised supplier

management terms

Reduction of €9.6m in Deferred

Revenues largely attributable to

the Corporate division, and

reflecting customer mix (large

corporate clients less linked to

prepaid points) and gap

between consumption and sales

of prepaid points

0,7 2,0 1,7 2,0

145,3 139,8 154,9

161,9

(32,4) (30,0) (38,5) (46,0)

(73,3) (74,0) (77,3) (67,7)

40,4 37,8 40,9 50,2

2014 2015 2016 2017

Inventories Trade receivables Trade payables

Deferred revenues Net Working Capital

Net Working Capital

11.7%

Net Working Capital (€m)

NWC as % of Revenues 1) %

10.7% 10.8% 12.5%

Note: 1) NWC/Revenues based on pro-forma Revenues for the previous 12 months

Key highlights

24

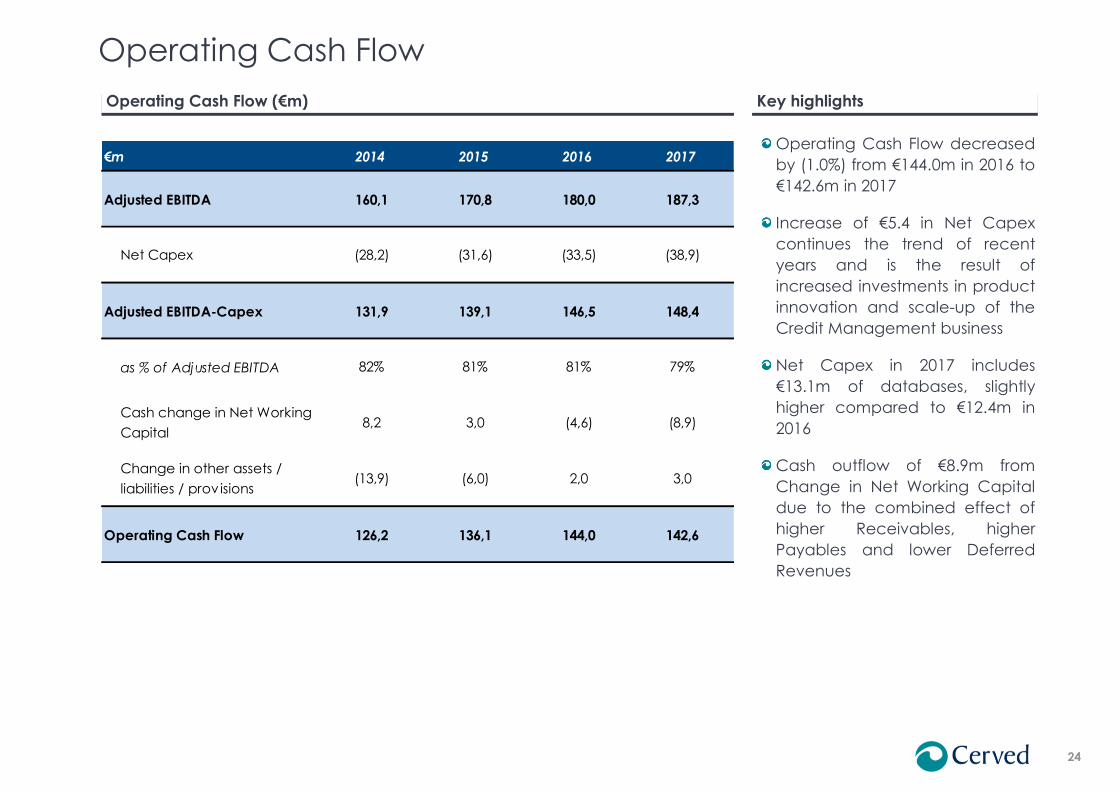

€m 2014 2015 2016 2017

Adjusted EBITDA 160,1 170,8 180,0 187,3

Net Capex (28,2) (31,6) (33,5) (38,9)

Adjusted EBITDA-Capex 131,9 139,1 146,5 148,4

as % of Adjusted EBITDA 82% 81% 81% 79%

Cash change in Net Working

Capital8,2 3,0 (4,6) (8,9)

Change in other assets /

liabilities / provisions(13,9) (6,0) 2,0 3,0

Operating Cash Flow 126,2 136,1 144,0 142,6

Operating Cash Flow decreased

by (1.0%) from €144.0m in 2016 to

€142.6m in 2017

Increase of €5.4 in Net Capex

continues the trend of recent

years and is the result of

increased investments in product

innovation and scale-up of the

Credit Management business

Net Capex in 2017 includes

€13.1m of databases, slightly

higher compared to €12.4m in

2016

Cash outflow of €8.9m from

Change in Net Working Capital

due to the combined effect of

higher Receivables, higher

Payables and lower Deferred

Revenues

Operating Cash Flow (€m)

Operating Cash Flow

Key highlights

25

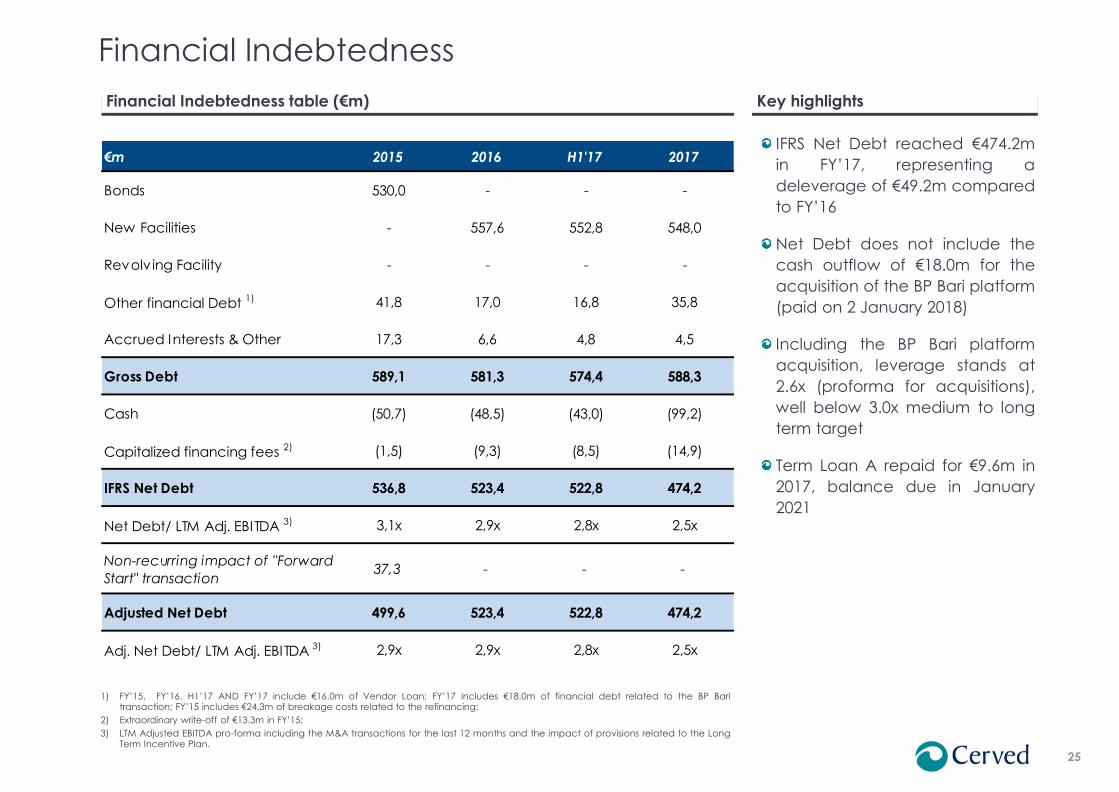

€m 2015 2016 H1'17 2017

Bonds 530,0 - - -

New Facilities - 557,6 552,8 548,0

Revolv ing Facility - - - -

Other financial Debt 1) 41,8 17,0 16,8 35,8

Accrued Interests & Other 17,3 6,6 4,8 4,5

Gross Debt 589,1 581,3 574,4 588,3

Cash (50,7) (48,5) (43,0) (99,2)

Capitalized financing fees 2) (1,5) (9,3) (8,5) (14,9)

IFRS Net Debt 536,8 523,4 522,8 474,2

Net Debt/ LTM Adj. EBITDA 3) 3,1x 2,9x 2,8x 2,5x

Non-recurring impact of "Forward

Start" transaction37,3 - - -

Adjusted Net Debt 499,6 523,4 522,8 474,2

Adj. Net Debt/ LTM Adj. EBITDA 3) 2,9x 2,9x 2,8x 2,5x

Financial Indebtedness

Financial Indebtedness table (€m)

1) FY’15, FY’16, H1’17 AND FY’17 include €16.0m of Vendor Loan; FY’17 includes €18.0m of financial debt related to the BP Bari transaction; FY’15 includes €24.3m of breakage costs related to the refinancing;

2) Extraordinary write-off of €13.3m in FY’15;

3) LTM Adjusted EBITDA pro-forma including the M&A transactions for the last 12 months and the impact of provisions related to the Long Term Incentive Plan.

Key highlights

IFRS Net Debt reached €474.2m

in FY’17, representing a

deleverage of €49.2m compared

to FY’16

Net Debt does not include the

cash outflow of €18.0m for the

acquisition of the BP Bari platform

(paid on 2 January 2018)

Including the BP Bari platform

acquisition, leverage stands at

2.6x (proforma for acquisitions),

well below 3.0x medium to long

term target

Term Loan A repaid for €9.6m in

2017, balance due in January

2021

26

Appendices 4

Highlights 1

Table of Contents

Financial Review 3

Business Review 2

0 73

132

0 128 142

109 189 255

191 191 191

0 103 188

16 159 189

221 221 221

92 188 210

27

129,4

156,5 24,5

94,6

Revenues PF FY’17

(€ and % Group)

Credit Information

Corporate Financial Institution

+3.1% +21.1% +18.5% +2.0%

39%

23%

6%

32%

Credit Management Marketing Solutions

Scope of Business

Growth FY ’17 vs’16

CAGR % ‘14-’17

Products and services sold to financial institutions and corporations to assess the solvency, creditworthiness and financial

condition of commercial counterparties and clients

Based on Italy’s largest and most comprehensive database on corporates

Market analysis, lead generation and

performance marketing products and services arising

from Cerved’s database

Servicing of all types of performing,

NPLs and problematic receivables on behalf

of banks, investors, finance companies,

utilities and corporates

+5.7% +11.7% +16.1% +2.2%

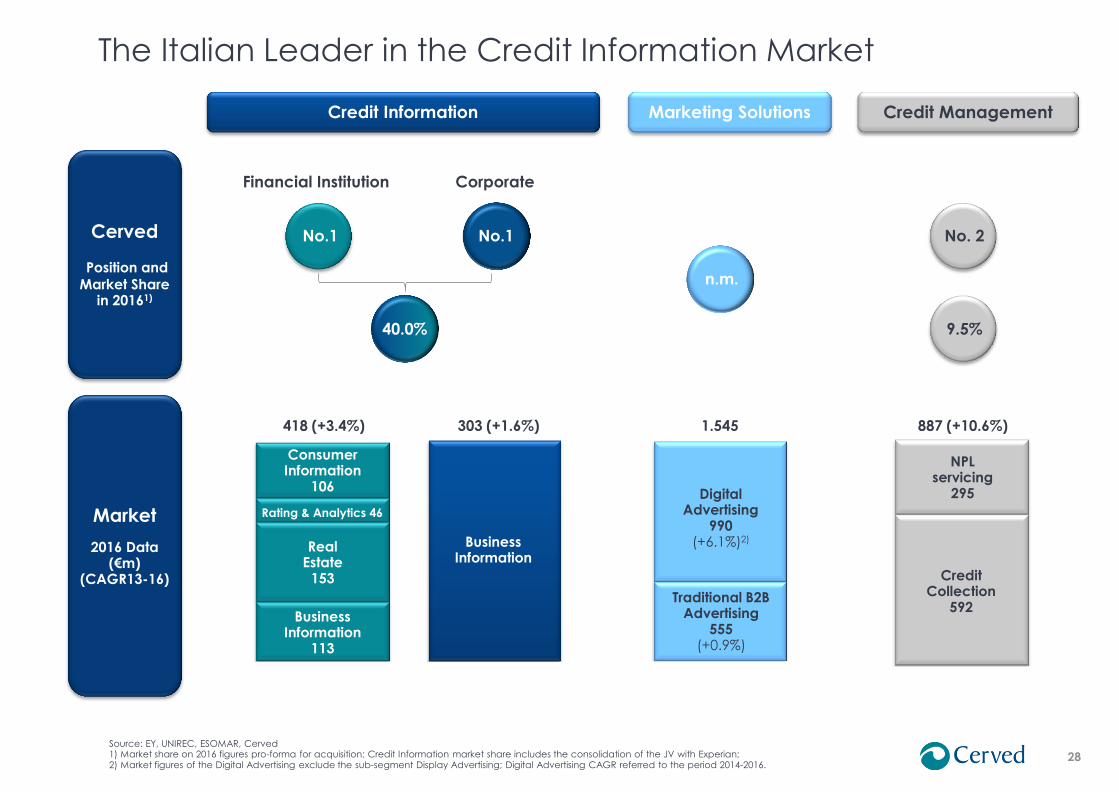

The Italian Leader in the Credit Information Market

Note: figures includes intercompanies

Key Drivers

Pricing pressure

Cross-selling

New bank lending

Underpenetration

Industrial production

Credit checks

Growth of NPLs

Bank outsourcing

Collection levels

Cross-selling

Consolidation

Product innovation

0 73

132

0 128 142

109 189 255

191 191 191

0 103 188

16 159 189

221 221 221

92 188 210

28

2% 42%

303 (+1.6%)

Business Information

1.545 887 (+10.6%)

Cerved

Position and

Market Share in 20161)

418 (+3.4%)

l% 40.0% 9.5%

n.m.

No.1 No. 2 No.1

Market

2016 Data (€m)

(CAGR13-16)

NPL servicing

295

Credit Collection

592 Business

Information 113

Rating & Analytics 46

Real Estate

153

Consumer Information

106

Source: EY, UNIREC, ESOMAR, Cerved 1) Market share on 2016 figures pro-forma for acquisition; Credit Information market share includes the consolidation of the JV with Experian; 2) Market figures of the Digital Advertising exclude the sub-segment Display Advertising; Digital Advertising CAGR referred to the period 2014-2016.

Corporate Financial Institution

Credit Information Marketing Solutions

The Italian Leader in the Credit Information Market

Credit Management

Digital Advertising

990 (+6.1%)2)

Traditional B2B Advertising

555 (+0.9%)

29

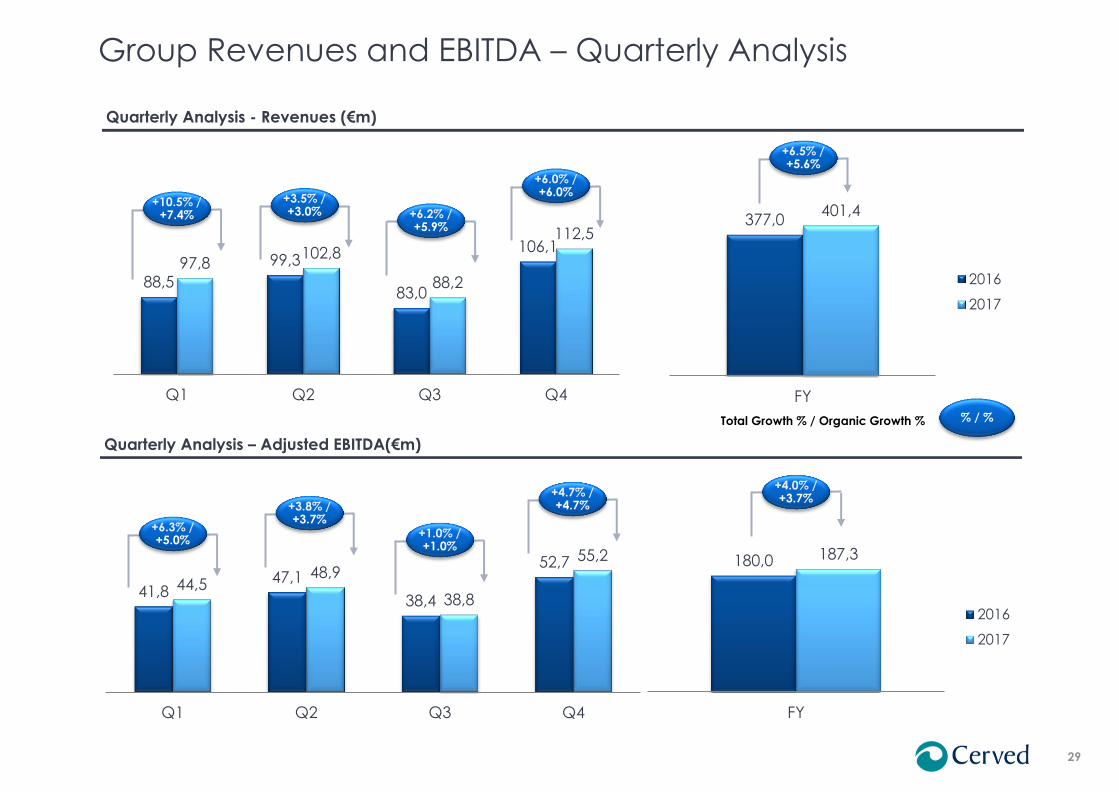

Group Revenues and EBITDA – Quarterly Analysis

180,0 187,3

FY

2016

2017

377,0 401,4

FY

2016

2017

Quarterly Analysis - Revenues (€m)

Quarterly Analysis – Adjusted EBITDA(€m)

88,5

99,3

83,0

106,1 97,8

102,8

88,2

112,5

Q1 Q2 Q3 Q4

41,8 47,1

38,4

52,7

44,5 48,9

38,8

55,2

Q1 Q2 Q3 Q4

Total Growth % / Organic Growth % % / %

+10.5% / +7.4%

+3.5% / +3.0%

+6.5% / +5.6%

+6.3% / +5.0%

+3.8% / +3.7%

+4.0% / +3.7%

+6.2% / +5.9%

+1.0% / +1.0%

+6.0% / +6.0%

+4.7% / +4.7%

30

Credit Information – Revenues (€m)

Credit Information – Quarterly Analysis

68,6 70,9 60,9 74,3

274,7

71,7 73,0 62,1 79,2

286,0

Q1 Q2 Q3 Q4 FY

2016

2017

32,0 32,0 30,0 32,6

126,6

32,7 32,0 31,0 33,6

129,4

Q1 Q2 Q3 Q4 FY

Credit Information – Financial Institutions – Rev (€m)

36,6 38,9 30,9 41,7

148,1

39,0 40,9 31,1 45,6

156,5

Q1 Q2 Q3 Q4 FY

2016 2017

Credit Information – Corporate – Rev (€m)

36,9 37,4 31,5 41,6

147,5

38,3 39,5 31,1 41,6

150,4

Q1 Q2 Q3 Q4 FY

2016

2017

Credit Information – Adjusted EBITDA (€m)

+3.6% +5.6%

+4.4% +3.0% +2.0%

+2.1% +0.1%

+2.2%

+6.5% +5.3%

+0.4% +3.5%

+5.7%

+4.1%

(1.3%) (0.2%)

+2.0%

+6.6%

+9.3% +3.1%

31

Credit Mgmt and Marketing Solutions – Quarterly Analysis

1,1 2,0

1,6

3,4

8,2

1,7 2,0 1,7

3,9

9,3

EBITDA Q1 EBITDA Q2 EBITDA Q3 EBITDA Q4 EBITDA FY

2016

2017

3,8

7,6 5,3

7,7

24,4

4,5 7,4 6,0

9,8

27,6

EBITDA Q1 EBITDA Q2 EBITDA Q3 EBITDA Q4 EBITDA FY

2016

2017

17,4 23,9

18,3 25,1

84,7

21,5 24,5 22,0 26,7

94,6

Rev Q1 Rev Q2 Rev Q3 Rev Q4 Rev FY

3,1 5,7 4,7

7,6

21,1

5,6 6,4 5,0

7,5

24,5

Rev Q1 Rev Q2 Rev Q3 Rev Q4 Rev FY

Credit Management – Revenues and Adjusted EBITDA (€m)

Marketing Solutions – Revenues and Adjusted EBITDA (€m)

+23.3% +2.4%

+11.7%

+18.2%

(3.0%)

+26.8%

+79.8% +11.7%

+16.1%

+57.4% (2.8%)

+6.7%

+14.0%

+7.0%

+19.8% +13.3%

+13.2%

+6.5%

(0.8%)

+13.5%

32

€m 2014 2015 2016 2017

Total Revenues (including other income) 331,6 353,7 377,1 401,7

Cost of raw material and other materials (7,0) (8,3) (7,4) (7,1)

Cost of Serv ices (76,3) (78,9) (84,9) (98,5)

Personnel costs (73,7) (81,5) (91,7) (96,8)

Other operating costs (8,2) (8,5) (8,6) (8,7)

Impairment of receivables and other provisions (6,3) (5,7) (4,5) (3,2)

Adjusted EBITDA 160,1 170,8 180,0 187,3

Performance Share Plan - - (0,7) (1,8)

EBITDA 160,1 170,8 179,3 185,5

Depreciation & amortization (25,1) (28,5) (30,6) (34,3)

EBITA 135,0 142,3 148,7 151,2

PPA Amortization (42,9) (45,8) (47,4) (32,8)

Non-recurring Income and expenses (4,5) (3,8) (6,5) (7,3)

EBIT 87,6 92,8 94,8 111,1

PBT 24,0 (1,7) 75,5 86,5

Income tax expenses (12,0) 5,3 (22,4) (28,2)

Non-recurring Income tax expenses - - (4,5) -

Reported Net Income 12,0 3,6 48,7 58,3

Adjusted Net Income 55,0 68,5 92,0 98,2

of which: Minorities 1,4 2,5 1,9 2,0

Profit and Loss

Source: Company Information; for further details refer to Cerved Information Solutions S.p.A. Annual and Quarterly Reports

33

€m 2014 2015 2016 2017

Intangible assets 472,4 459,7 423,7 395,9

Goodwill 718,8 718,8 732,5 750,4

Tangible assets 17,3 16,4 19,8 20,6

Financial assets 14,9 8,3 8,7 9,0

Fixed assets 1.223,4 1.203,1 1.184,7 1.175,9

Inventories 0,7 2,0 1,7 2,0

Trade receivables 145,3 139,8 154,9 161,9

Trade payables (32,4) (30,0) (38,5) (46,0)

Deferred revenues (73,3) (74,0) (77,3) (67,7)

Net working capital 40,4 37,8 40,9 50,2

Other receivables 7,1 7,6 7,7 6,7

Other payables (26,1) (32,2) (53,9) (85,9)

Net corporate income tax items (18,8) (1,0) 0,3 (7,3)

Employees Leaving Indemnity (13,1) (12,5) (13,1) (13,3)

Provisions (11,1) (8,5) (7,3) (6,0)

Deferred taxes (1) (109,1) (88,7) (91,9) (90,0)

Net Invested Capital 1.092,7 1.105,6 1.067,4 1.030,3

IFRS Net Debt (2) 487,6 536,8 523,4 474,2

Group Equity 605,1 568,8 543,9 556,0

Total Sources 1.092,7 1.105,6 1.067,4 1.030,3

Balance Sheet

Source: Company Information; for further details refer to Cerved Information Solutions S.p.A. Annual and Quarterly Reports (1) Non cash item; (2) Net of capitalized financing fees

34

€m 2014 2015 2016 2017

Adjusted EBITDA 160,1 170,8 180,0 187,3

Net Capex (28,2) (31,6) (33,5) (38,9)

Adjusted EBITDA-Capex 131,9 139,1 146,5 148,4

as % of Adjusted EBITDA 82% 81% 81% 79%

Cash change in Net Working Capital 8,2 3,0 (4,6) (8,9)

Change in other assets / liabilities (13,9) (6,0) 2,0 3,0

Operating Cash Flow 126,2 136,1 144,0 142,6

Interests paid (51,7) (40,3) (29,2) (16,3)

Cash taxes (24,1) (40,2) (27,3) (22,5)

Non recurring items 1) (3,4) (3,2) (8,8) (9,2)

Cash Flow (before debt and equity movements) 46,9 52,3 78,7 94,6

Net Div idends 1,0 (40,1) (44,4) (47,8)

Acquisitions / deferred payments / earnout (20,9) (23,5) (27,9) (2,4)

IPO Capital Increase (net of IPO costs) 220,2 - - -

Other (0,1) (1,1) - -

IPO debt drawdown / (repayment) (254,5) - - -

"Forward-Start" Refinancing and "Amendment" - - (35,5) (2,9)

Net Cash Flow of the Period (7,5) (12,3) (29,1) 41,5

Cash Flow

Source: Company Information; for further details refer to Cerved Information Solutions S.p.A. Annual and Quarterly Reports (1) FY 2016 figure Includes €2.2m cash outflow for the new headquarters

35

€m 2014 2015 2016 2017

Reported Net Income 12,0 3,6 48,7 58,3

Non recurring income and expenses 4,5 3,8 6,5 7,3

Non recurring financial charges 10,1 52,4 0,5 (5,2)

Capitalized financing fees 3,4 2,9 2,2 2,5

PPA Amortization 42,9 45,8 47,4 32,8

IRS termination 1,0 - - -

Fair Value adjustment of options - - - 12,8

Fiscal Impact of above components (18,9) (28,4) (17,7) (10,4)

Adjustments 43,0 76,4 38,8 39,8

Impact of IRES change treatment - (11,5) - -

Non recurring income tax expenses - - 4,5 -

Adjusted Net Income 55,0 68,5 92,0 98,2

Adjusted Net Income Bridge

Source: Company Information; for further details refer to Cerved Information Solutions S.p.A. Annual and Quarterly Reports

Cerved Information Solutions S.p.A. Via dell’Unione Europea, 6A/6B –

20097 San Donato Milanese Tel. +39 02 77541

company.cerved.com

![Investment Outlook - AXYS Group · UBS: 6.70: Mkt Summary & Highlights ... [12% of TMT ex UTIN] closed unmoved WoW at Rs88.50, ... Investment Outlook ...](https://static.documents.pub/doc/80x56/5b0400ce7f8b9aba168cadf4/investment-outlook-axys-670-mkt-summary-highlights-12-of-tmt-ex-utin.jpg)