42

Retail Markets Today & Tomorrow In Ireland & the UK August 2011 Growing the success of Irish food & horticulture

1SCB Partners for Board Bia, In Confidence

Retail Markets Today & TomorrowIn Ireland & the UK

August 2011

Growing the success of Irish food & horticulture

2SCB Partners for Board Bia, In Confidence

Background & Research Objectives• ReportObjectives 3• Methodology 4

1. State of the Grocery Retail Industry• SummaryOverview 5• FoodRetailSalesProjections 5• ConvergenceofIrishandUKRetailMarkets 6• Mergers&AcquisitionsintheRetailSector 6• GroceryRetailFormatGrowth 7• ChallengeswithinUKandIrishRetailMarkets 9• HowIrishFoodisPerceivedattheMoment 10

2. Retailer Expansion Plans• SummaryOverview 11• ExpansionPlans 12• MajorConvenienceExpansion 13• InternationalExpansion 14

3. Technologies for Channel Expansion• SummaryOverview 15• DevelopedOnlineShoppingExperience 16• MCommerce 17• MergerofDigital&PhysicalWorld 19• NewTechnology 20

4. Trends in Promotions• SummaryOverview 21• RetailerPromotions 21

5. Private Label vs Branded• SummaryOverview 23• PrivateLabelDevelopments 23

6. Retailer Perspective on Best-In-Class Products•SummaryOverview 26• Best-In-ClassFormulation 27• Best-In-ClassPackaging 29• Best-In-ClassPositioning 31

7. Supply Chain Advancements• SummaryOverview 32• RetailerSupplyChainOverview 33• SustainableDistribution 34• Logistics 35• Rationalisation 36

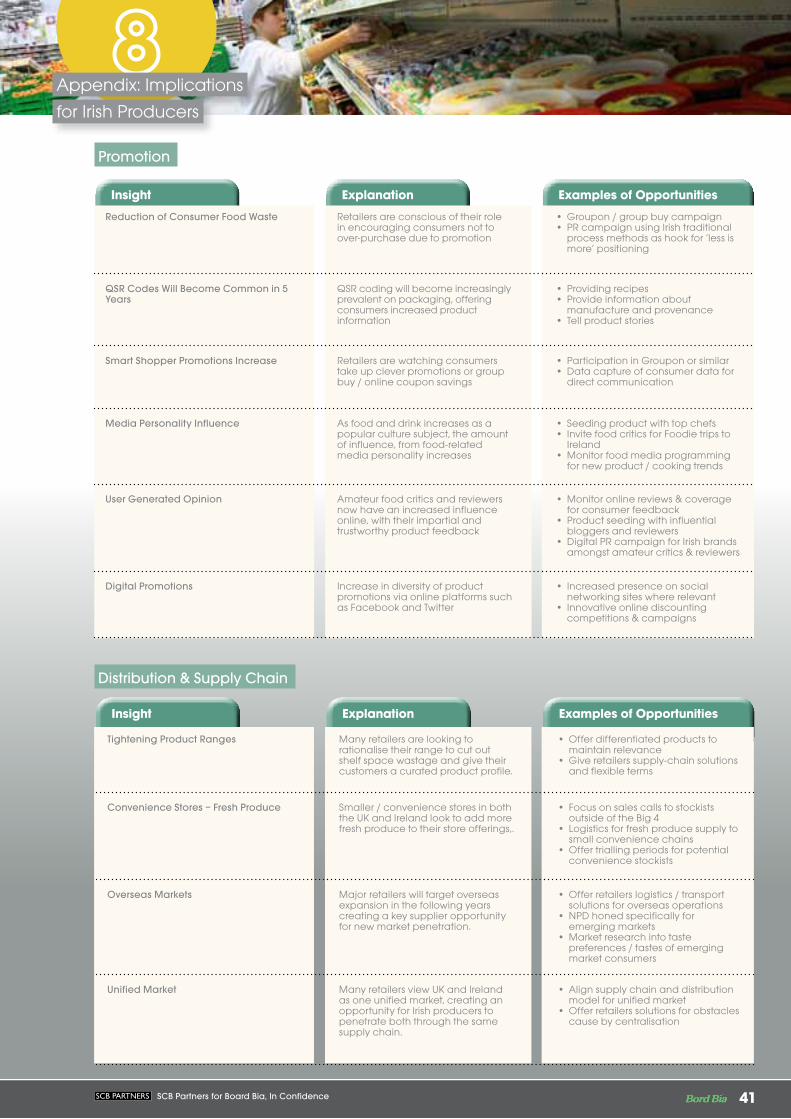

8. Appendix: Implications for Irish Producers• SummaryOverview 37• FoodforThought 37

CONTENTS

3SCB Partners for Board Bia, In Confidence

BACKGROUND&RESEARCHOBJECTIVES

Report ObjectivesRetailersinIrelandandtheUKareessentialtothesuccessofIrishfoodandbeveragesuppliers.InordertohelpdrivefuturecompetitiveadvantagefortheIrishfoodandbeverageindustry,adeepunderstandingofthekeygroceryretailtrendsandchangingretaildynamicsisrequiredtoprepareforthefuture.

Theobjectiveofthisreportistoanswerthequestion“What does the future hold for the Irish and UK Retail Landscape?”

Thisreportprovidesanin-depthforecastofthefoodandbeverageretailenvironmentinIrelandandtheUKinthenext3–5yearsandprovidescriticalinsightsintohowIrishproducerscanachievecompetitiveadvantage.Thereportprovides:

• Avision and understandingofthegroceryretailenvironmentandexpectedchanges

• Expansion,contractionorconsolidationofretailersandtheeffect on Irish suppliers

• Drivers, scenarios and conditionsthatwillimpactontheretailenvironment

• Strategiesthattraditionalretailersanddiscountershaveinplacetodevelopgrowth

• Supplychainimplicationsforretailers

• OpportunitiesforIrishretailerstoexpandtheirshareofshelfinretailers in Ireland and the UK

ReportOverviewRetail Markets Today and Tomorrow in Ireland and UK This report provides a detailed projection of a series of key trends that will materially impact Irish food and drinks suppliers. The report illuminates developments in the following areas over the next 3-5 years and is structured as follows:

2

3

State of

the Grocery

Retail

Industry

Retailer

Expansion

Plans

Technologies

for Channel

Expansion

Supply Chain

Advancements

Implications for

Irish Producers

4

5CurrencyusedisusingexchangerateatMay2011of1=$1.42,1=£0.87

1

Retailer

Perspective

on Product

Innovation

Trends in

Promotions

6

7

8

Private

Label vs.

Branded

4SCB Partners for Board Bia, In Confidence

Thereportwasdevelopedusingacombinationofsecondarydeskresearchandprimaryqualitativeresearch.

Secondary Desk Research Duringthedeskresearchphaseavarietyofpublicationsweresourcedandanalysed.Rigorousanalysisofsocio,politicalandeconomicdatafromreportsandwhitepapersfromgovernments,researchinstitutionsandannualreportsfromkeyretailsectororganisationswasconducted.Thesearereferencedbelow:

Selected Bibliography: Desk Research

• BuildingonSuccess,IGD• FullYearResults2010/2011,Marks & Spencer• PathwaysforGrowth,Bord Bia• WhereBritainShops2010,Verdict• UKFood&GroceryRetailers2010,Verdict• FoodRetailing,November2010,Mintel• FoodHarvest2020,Dept.ofAgriculture,Fisheries and Food• EuropeanFoodRetail,Barclays Capital• UKRetailFutures2012:Food&Grocery,Verdict• UKe-RetailGroceryRetailers2010,Verdict• FutureofRetail2010,PSFK• RetailIndustryGlobalReport2010, IMAP Retail• SustainabilityTrendsinEuropeanRetail,2009,Forum for the Future• RetailFutures,Forum for the Future• Food2030,Defra• UKFoodIndustry2010,Keynote

• UKMarketForecasts:FoodCatering&DrinkMarket2010,Keynote• PlanetRetail2010• AnualReport2010Tesco

Selected Qualitative InterviewsAspartofthequalitativeresearch,keyfiguresintheretailandfoodsectorsofIrelandandUKwereinterviewedfortheirinsights.Interviewswereconductedwithhigh-rankingtradebodyrepresentatives,CEOsoffoodretailersanddistributors,foodsectoracademicsandjournalistsaswellasproduct-innovationexperts,FMCGindustryexpertsandpackagingexperts.SCBconductedacombinationoftelephoneandface-to-faceinterviewsfromover30organisations.Eachinterviewlastedbetween15–60minutes.Abreakdownoftheprofileofrespondentsisillustratedinthetablebelow.

Theinterviewswereconductedwithexecutivesfromadiverserangeoforganisationsincluding:

• AlliedIrishBank• AngloBeefProcessors• AssociationofConvenienceStores• Barclays• CheckOutMagazine• DawnsMeats• Flahavans• IrishDairyBoard• Jeraboams• KepakFoods• Marks&Spencer

Profile Breakdown of Respondent

Type of RespondenT no. of InTeRvIews

FoodRetailers 15

Media 2

Producers 7

Financial 3

Other 7

About SCB PartnersThisreporthasbeenproducedbySCBPartners;aninternationaltrend-basedmarketinginsightsconsultancyspecialisinginprovidingcriticalbusinesslearningsforsomeoftheworld’smajorbluechipcompanies.SCBspecialisesinconsumerinsights,researchanalysis,innovations,marketingandbrandstrategies.

• Musgrave• OneStopConvenienceStores• Partridges• PlanetOrganic• RetailExcellenceIreland• RGDataIreland• TennantandRuttle• Tesco• TrinityCollege• Utilyx• Waitrose

4SCB Partners for Board Bia, In Confidence

Background&ResearchObjectives

Methodology

5SCB Partners for Board Bia, In Confidence

STATEOFTHEGROCERYRETAILINDUSTRY

Summary OverviewBoththeIrishandtheUKretailmarketsarebothsettoexpandin3-5yearstime,withIrishfoodretailgrowingatanaverageof1%ayearandUKfoodretailgrowingatanaverage2.8%peryearthrough2014.ThegroceryretailindustryinIrelandisexpectedtoreturntopreviousgrowthlevelsastheIrisheconomyrecovers,whiletheUKwillexpandatasteadyrate.

AdegreeofconvergenceoftheIrishandtheUKretailmarketsisexpected,asretailerslooktostreamlinecostsandcreateareasofmutualbenefit.

InIreland,theenvironmenthasbeendifficultfordomesticproducers.Suchconvergence,asUKretailerssuchasTescomovetowardsitsUKsupplynetworkwillcompoundthisunlesstheproducersareactiveintheirbusinesstothebrandagainstUKsuppliers.

AsintheUK,mergeractivityismorelikelytobeintheareaofacquisitiontoexpandintotheconveniencesector.

FoodRetailSalesProjectionsTotalIrishfoodretailsalesinIrelandhaverecentlybeenindecline,fromahighof11,398millionin2007decliningto10,370millionin2010.However,sales’projectionsto2014lookpositive,withgrowthof3.91%projectedtobeachievedby2014-creatingnewopportunitiesforIrishproducers.

FoodretailsalesintheUKareexpectedtoachieveCAGRof2.8%overthenext4years.FoodretailsalesintheUKfor2010wereestimatedat129,260million,andarepredictedtoreach144,511millionby2014.

Republic of Ireland United Kingdom

value Index % Annual Change value Index % Annual

Change2007 11,398m 116 9.4% 112,229m 87 4.3%

2008 11,204m 114 -1.7% 118,877m 92 5.9%

2009 10,602m 108 -5.37% 128,107m 99 7.8%

2010 (est) 10,370m 106 -2.18% 129,260m 100 0.9%

2011 (fore) 10,392m 106 .2% 131,392m 102 1.6%

2012 (proj) 10,492m 107 .96% 134,668m 104 2.5%

2013 (proj) 10,728m 110 2.25% 137,807m 107 2.3%

2014 (proj) 10,776m 110 .44% 141,183m 109 2.5%

2015 (proj) 10,823m 111 .44% 144,511m 112 2.4%

All Food Retail Sales 2007 - 2015

“As today, retailers will need to provideextraordinary good value. Whatever

happens to the economy, people are still going be in the market for a treat,

but only at the right price.” Head of food – Major Multiple

“The concept of the weekly grocery shop is ‘past its sell by date. The

younger generation are performing the shopping equivalent of grazing and want more ready-made or easier to eat

food than ever before.”Academic, Trinity College

Source: Mintel 2010

6SCB Partners for Board Bia, In Confidence

StateofTheGroceryRetailIndustry

ConvergenceofIrishandUK Retail MarketsTheculturalandcommercialtiesbetweenIrelandandtheUKstretchbackcenturies,andthenextfiveyearswillsee increasing convergence of the two marketsfromtheperspectiveofmajorplayerswithinthegrocerysector,withagrowingnumberusingasingular UK and Irish strategy.

Today,theUKisIreland’slargestsingletradingpartner,accountingfor13.4bnofIrishexports(16%oftotal)and13.7bnofIreland’simports(30%oftotal).UKtradewithIrelandexceedsthetotalUKtradewithBrazil,Russia,IndiaandChinaandat£2.4bn;the Irish market consumes more UK produced food and drink than any other country.Theeconomicfiguresthenpointtothelogicofgreaterconvergence.

Buy British, Buy Local“BuyBritish”campaignshavebenefitedIrelandoverothercountriesintheEuropeanContinent.Whilethe“BuyBritish”campaignsintheUKhavehadconsiderablesuccessinsteeringconsumerspendingtowardshome-producedfoods,many UK consumers view Irish food to be practically local,allowingIrishproducersasizable advantage over importsfromContinentalcompetitors.

Thereisapotentialparadoxforsuppliersprovidingproducewithprovenanceandquality.ThisusuallyhasapricepointattachedtoitwhichcouldmakesuchproducehardtocompetewithotherUKproducedfoodsbeingsoldunder“BuyBritish”banners.CombinethiswithdownwardpricepressurefromthemajorUKretailers,andIrishproducerswillneedtoplancarefullytheirstrategyandpricing.Irishsupplierswillneedamethodtoovercomethepowerofthemultiples.Suppliers should play a very powerful role in the future of Irish exports-focusingonvalueandnotjustpricewillbepre-requisile.

Impact of TescoTheimpactofTesco(whichcurrentlycommands35%ortheIrishretailmarket)cannotbeunderestimated.TescoislookingtosynergiseproductofferingsbetweentheUKandIreland;supplierswillbeforcedtofollowsuit.

Advancementsinlogisticsandsupplychaintechnologywillallowcompaniestohaveonemainoffice,onesupplychainandoneproductstreamwhichservicebothcountries.

Thisstreamliningposesbothopportunitiesandchallengesforfoodproducers.ViewingtheUKaspartoftheIrishmarketmeansIrishproducerswillhavea65-millionstrongmarketofconsumerstosellto.However,thedominationoftheUKretailsectorbytheBigFoursupermarketsandtheirpropensitytostockfewerproductsacrossalloftheirstoresmeansthattogainafootholdintheenlargedmarket,thescale of Irish food production not only needs to be expanded but also differentiated.Beingregardedaslocalin“BuyBritish”campaignsinUKstoresmaynotbeenoughtocompensateforUKretailerssellingmoreUKproduceinIrishstores.Atpresent,theriskofnotgainingafootholdintheUKmarketisthatTesco’sproductsynergieswillcutIrishproducersoutofTesco’sshareofthedomesticmarket.IfWalmartweretoentertheIrishmarket,theycouldbeexpectedtobeatleastasaggressiveasTescointermsofrangesynergiesbetweenthetwocountries.

Mergers&AcquisitionsinRetailThedegreeofconsolidationintheIrishandUKretailsectors,aswellascompetitionlaw,indicatethattherewillbelimited merger and acquisition activity in either Irish or the UK markets in the next 3-5 years.Weakerindependentretailers,forexample,arethemostlikelytakeovercandidates.

Mature MarketsBoththeIrishandUKretailmarketsareconsideredverymature,andthus,growthintheretailsectorsisunlikelytooutstripthatofthewidereconomy.Moreover,bothmarketsaredominatedbyalimitednumberofhighlyentrenchedplayers.Takentogether,thesefactorsmeananyM&Awouldbeveryexpensive,followedbyslowgrowth.Combiningthisfactwiththeuncertaineconomicoutlookmakesitclearthatneither the Irish nor UK markets represent obviously good investment opportunities in the short to medium term.

Competition LawIt is unlikely thatcompetitionregulatorswouldgivethego-ahead for further consolidation in the retail sector given that 80% of the Irish and UK markets are already controlled by each country’s respective Big Four.

Theonlyscenariolikelytoaltertheabovedynamicisifaretailerwerestrugglingfinancially.Insuchasituation,thereducedcostofatakeovermightrenderthefirmanattractiveproposition,whilecompetitionauthoritieswouldlikelywaivethemergerthroughinordertoprotectjobs.ThemodelhereistheLloydsTSB/HBOSbankingmergerof2008which,undernormalcircumstanceswouldnothavebeenclearedbyauthoritiesbutinordertoprotectjobswasallowedtoproceed.

M&A RumoursDuetomaturemarketsandcompetitionlawM&Aactivityislimited.In both UK and Ireland, the key reason for acquisition would be for larger retailers to expand into the convenience sector.

Iceland: Icelandistheonlysupermarketchainwithanimmediatelyuncertainfuture.Thischilledfoodschainis67%ownedbythetroubledIcelandicbankLandsbanki,whichinturnisownedbytheIcelandicgovernment.AsofFebruary2011,Landsbankihassignalleditsintentiontosellitsstakeinthefrozenfoodsretailer.AsofMay2011,Momsanshadshowninterestinacquiringthestakeasawayofacquiringpropertytoenterintotheconveniencesector.Icelandhas682outlets,makingitasmallplayerrelativetothecompetition.Largerrivalsmightspypotentialefficiencysavingsthroughintegrationintoalargersupplyanddistributionchain,butitismorelikelytoremainanindependentchain.

Nisa: ThefutureofsymbolgroupNisaisalsouncertain.AnalystsareparticularlyinterestedtoseewhetherCostcutter’snewownerBibbyLinerenewsitsordercontractwithNisain2014,whenthepresentarrangementends.WereBibbyLinetotakeitsbusinesselsewhere,Nisawouldlose40%ofitsturnoveratstroke.ItisbelievedthereisagoodchanceofthishappeningafterNisaawardedDHLaseven-yeardistributioncontractinsteadofBibbyLine.

Dunnes:InIreland,therehasbeenmuchspeculationaboutthefutureofDunnes.Atthetimeofwritingdespiteongoingconcernsaboutthefutureofthisretailer,therearenospecificandcredibletakeoverrumours.

7SCB Partners for Board Bia, In Confidence

GroceryRetailFormatGrowth

TheUKfoodandgroceryspendwasvaluedat173.42bnin2010,representing52.7%oftotalretailsales.By2015,the total UK food and grocery spendisestimatedtoreach210.11bn,withaverageannualgrowth projected to be 3.9%, offering large growth potential for Irish producersexportingintotheUK.

Nearly 50% of this growthwillcomefromtheconvenience and online channels alone,withconvenienceinparticularbeingthebattlegroundbetweenthemajorretailersoverthenextfiveyears.Asthemajorretailerspursueexpansionswithstoreenlargementsandnewopeningstheywillcontinuetogainmarketsharefromindependentandspecialityretailers.Furthermore,onlineretailisexpectedtodoubleinvaluefrom5.52bnin2010to10.93bnby2015.

In Ireland, the retail format breakdown is similar to the UK by category, with the exception of hypermarkets.AsplanningpermissionismuchstricterinIrelandthanintheUK,thehypermarketformatislessprevalent.TheothermajordifferencebetweentheUKandIrelandistheproportionofindependentstoresthatdominateIreland’sconveniencesector.Whileconveniencewillgrow,theshareheldbyindependentsisdeclining.

Irish and UK producers will be expected to create products and packing sizes designedforchannel-specificneedsandthedifferentstore formats.

Source: IGD Research, 2010

UK Grocery Retail91,509 Stores191.3m sq ft

£150.8bn

Convenience Retailing48,289 Stores

53.5m sq ft • £32.1bn

Co-ops2,448 Stores •4.8m sq ft • £3.8bn

Co-ops1,402 Stores • 11.9m sq ft • £6.3bn

Symbol Groups16,072 Stores • 19.2m sq ft • £12.1bn

Discounters1,240 Stores • 11.2m sq ft • £6.4bn

Non Affiliated20,351 Stores • 18.1m sq ft • £6.9bn

Co-ops104 Stores • 0.9m sq ft • £0.6bn

Forecourts6,506 Stores • 5.5m sq ft • £4.3bn

Hypermarkets, Supermarkets & Superstores

7,970 Stores109.1m sq ft • £107.8bn

Traditional Retail35,250 Stores

28.7m sq ft • £6.1bn

Online£4.8bn

Multiples2,912 Stores • 5.9m sq ft • £5.0bn

Multiples5,224 Stores • 85.1m sq ft • £94.5bn

Breakdown of Grocery Retail Formats in the UK

SupermarketsOfatotal91,509foodretailstoresintheUK,7,970oftheseareclassifiedassupermarkets,hypermarketsorsuperstores.Rangingbetween3,000and60,000sqft,theselargeformatstoresrepresentapproximately2/3oftotalfoodretailsales(amountingto124billionin2010)andthusdecreasingthenumberofviableretailpartnersforIrishexporters.

Despiterepresentingthegreatestportionofsales,theavailablespacerequiredtoopenstoresofsuchsizeisfiniteandthereforesuchlargestoreformatswillnotbetheprimaryavenueforexpansioninthefuture.Majorretailerswillcompeteforplanningcommissionrightstobuildinthelimitednumberofspaceswheresuchlargestoresarepossible,andfocusonenlargingtheirexistingsupermarkets.

AtthemomentdiscountersAldiandLidlareexpandingtheirpresenceintheIrishmarketandgrowing.

Irishdatanotavailable

StateofTheGroceryRetailIndustry

8SCB Partners for Board Bia, In Confidence

ConvenienceGenerating35.5bninsalesinthe12monthstoApril2010,theconveniencechannelnowrepresents20.5%ofthetotal UKfoodandgrocerymarket.With predicted growth rate of 5.8% over the next five years, convenience is growing considerably faster than the retail market as a whole,andwillrepresent25%oftheUKgroceryandfoodmarketby2016.Irish exporters that tailor their products to the needs of convenience retail (via NPD, packaging and logistics) will benefit. In3-5yearsconvenienceformatswillgrowtakingsharefromsupermarketsforthefollowingreasons:

• Growingconsumerneedforquick,easy-accessshops• Retailerfocusonconveniencesites,duetoplanningpermission

restrictionsandfinitesuperstorespaces• Consumersincreasinglyshiftingthe‘weeklyshop’online

As major retailers focus on smaller formats, the big four will continue to take sales from independents, forcing these smaller retailers out of the market.Notably,growthinconvenienceisoccurringinthefaceofstoreclosures:asofApril2010therewere48,410conveniencestoresintheUK,representingadecreaseof0.5%overtheprevious12months.Asthemultiplescontinuetoexpandaggressivelyintothechannelwithsophisticatedlarger-sizedconveniencestores,itispredictedthattheabsolutenumberofoverallstoreswillcontinuetodecrease.

Over1,000newconveniencemultiplesareforecasttohaveopenedbyApril2015anditispredictedthatthenon-affiliatedindependentswillsuffermost,withtheirstorenumbersalreadydeclining5%yearonyeartoApril2010.Amongstaffiliatedindependents,thebuyingpoweroftheirsymbolgroupsoffersreasonableinsulationagainstcompetitionfromthemultiples,whiledespitetheUSPofindependentforecourtstheirstorenumberscontinuetodeclineduetocompetitionfrombothsupermarketsandsymbolgroups.

It is worth noting, however, that even as their store numbers continue to fall, non-affiliated independents still account for 41.3% of all UK convenience stores in 2011,andwithsalesof7.8bntheywillremainanimportantpartoftheretailmix.These retailers offer small and new Irish producers further opportunities,astheytrytokeeptherangeandqualityoftheirstockcompetitivewiththelikesofTescoExpressandSainsbury’sLocal.

OnlineOnline grocery retailing in the UK is projected to double in valuefrom5.5bnto10.9bnin2015fuelledbytechnologicaldevelopments,greaterconsumerconfidenceinonlineretailgenerallyandsignificantimprovementsindelivery/collectionmethodsandaccuracy.

Althoughonlinesalesrepresentedonly 2% of total grocery sales in the UK in 2008, it is predicted that by 2015 this will increase to 5.4%.Currentlymostpopularamongstyoungerconsumers,familiesandmoreaffluentconsumers,onlineshoppingwillbecomeincreasinglywidespreadamongthemainstreampopulation.

In Ireland, online grocery retail is currently held back by a relatively low broadband penetration and logistic issues.HoweverkeymarketplayerssuchasTescoarekeentoexpandtheironlineoperationsinIrelandoverthenext5years.

Big 4 Planning Applications 2010

Glasgow:64(+36)

Cleveland:59(+52)

Sheffield:74(+58)Nottingham:82(+70)

Birmingham:104(+85)Cardiff:

64(+44)Bristol:

76(+57)

2010

0-10

11-20

21-30

31-40

41-50

50+

Expansionofthebigfoursupermarketscontinueswith577planningapplicationsapprovedamongstthembetween2008and2010.Tescoistheleaderinnewstoreopeningswith392approvals,whileLondonistheleadingdestinationwith110newopeningsplanned.

Specialty 1

SpecialtyretailersintheUKrepresented8.0%ofthemarketshareinfoodretailin2009,includinggreengrocers,butchers,fishmongers,farmshops,gourmetshopsanddepartmentstorefoodhalls.1

However,asmajorretailersfocusonexpandingtheirpremiumown-brandofferingsaswellasstockingluxuryitemstoencouragecustomerup-sell,theyareexpectedtofurtherconsolidatethemarketandgainfurthersharepercentage.

One area of growth for specialty retailers is an increased consumer interestinlocalsuppliersasaconsequenceofthetrend for localisation.

1BasedonDatamonitorwhichusesadifferentclassificationsystemtoIGD

StateofTheGroceryRetailIndustry

9SCB Partners for Board Bia, In Confidence

ChallengeswithintheUK and Irish Retail MarketsConsumer SpendingThe ongoing recession both in Europe and internationally continues to impact consumer spending levels in relation to food and has been particularly evident in the ongoing shift to value offerings.

Whileanyturnaroundinconsumerfoodpricesiswelcome,theongoingpromotionalpressuresonmanufacturersasretailersseektomaintainmarketsharecontinuedtoimpactonaveragereturnsacrossmostcategoriesduring2010.Withglobalfoodcommoditypricesincreasingstronglyoverrecentmonths,it is expected that consumer prices are likely to come under renewed pressure to increase in 2011.

Changing Consumer Trends The perception of ‘value’ has changed amongst UK and Irish consumers,largelyduetotherecentrecessionandincreasingstrengthofprivatelabelbrands.Consumers have been content to down trade to lower-priced brands,oftenstoreeconomyranges,safeintheknowledgethattheycanfindhigh-qualityproduceinthevalueendofthemarket.

Brand loyalty has diminished somewhat, as consumers sought more for their money,althoughnotsimplythecheapestoption.Irish producers can reposition their product portfolios where necessary to address this issue and exploit areas for growth.

• Someconsumershaveneededtodrasticallyreducetheirgroceryspend,andhavelookedforthelowestpossiblepricesforfoodanddrink.

• Forothers,thepriorityhasbeenmoreaboutcontrollingspendthroughmakingtrade-offs;foregoingindulgentspendonfoodanddrink.

• Consumershavenowcometoexpectdeals.Theyaremuchmoresavvyandawareandlookfor(andexpect)value,eveninpremiumproductsandranges.

UK Retail Demand FoodsectorsalesfortheUKretailmarketsareexpectedtobeconsiderablymorestablethaninIrelandandfollowalinearpathuntil2015.

However,therearestillconcernsaboutthestateoftheconsumerpositionintheUK.WhiletheUKmarketisgrowing,severalfactorsarehamperinggrowthrate:

• Wagesgrowthisaveragingunder2%,whileinflation(theRPI)isapproaching5%.Thismeansincomesarebeingsqueezedalready.Consumershavefinancedgrowthinspendingbysavingless.

• TheVATincreaseto20%fromJanuary2011

• Thefrontloadingofspendingcutstothefirsttwoyearsofthecurrentparliament

• Theinevitableriseininterestratesandhowthiswillimpacthouseownersalreadysqueezedduetotheabovereasons.

StateofTheGroceryRetailIndustry

FindingsfromBordBia’s‘FeelingthePinch’reportsummarisesprevailingconsumerbehaviourintimesofeconomicuncertainty.

10SCB Partners for Board Bia, In Confidence

Building on the Power of Irish ProvenanceIntheIrishandUKmarkets,thereputationofIrishproduceandbrandsremainsstrongandisassociatedwithtrustedqualityandhighstandardsincategories.‘BuyIrish’positioninghasprovenextremelypopularintheIrishmarket,buttheopportunityremainstodifferentiatetheprovenanceofIrishdairy,meatandfreshproduceintheUKfurther.

IrishproducershavetheopportunitytoraisetheidentityofIrishproductsintheUKandbeyond,throughemphasising the traditional production techniquesassociatedwiththecountry.

Irish personality Building

TheperceptionofIrishfood,especiallydairy,meatandfreshproduce,intheUKisofsafe,high-qualityfood.Irishbrandscouldfurtherbuildonthisbyadding a clear personality and narrativetocomplementtheseattributes.Mediapersonalities,suchascelebritychefsorrespectedfoodcritics,andchampionsofIrishproducewouldhelpIrishfoodformastrongeridentity.SuchpersonalitybuildingwillleadtoproducebecomingaspirationalforsomeUKconsumers.

Regional provenance

Whilemanyproducersdotalkaboutprovenancetoadegree,thereisroomforthemtobemorespecificandbeevenmoreconfidentaboutthe‘personality’ofthemeat,dairyorfreshproducetheyareselling.Forexample,inFrance,SpainandItalyitiscommontoreferencetheregionatleastasprominentlyasthecountryandthishelpstounderpinthesemarketsasdiverseculinarynations.Ultimately,consumersfinditeasiertoassociatelambwiththehillyfieldsofConnaughtthansimplywith‘Ireland’.AlreadyIrish beef is, in some instances, being referred to as Irish Angus or Irish Hereford and this does give the meat increased identity. Added personality would come, for example, by giving information about the producers themselves; the farm, the family, history of the herd or breed, or variety and benefits of fruit and vegetables being sold.

StateofTheGroceryRetailIndustry

HowIrishFoodisPerceivedAttheMomentInbothIrelandandtheUK, the reputation of Irish produce is a strong one synonymous with high standards, good quality and trustworthiness.Usingthispositionasafoundation,thereissignificantpotentialforIrishproducerstobuildanevenstronger brand around Irish food and drink by adding a more distinctive Identity beyond being Irish.

Insights from Ireland InIrelanditself,notsurprisingly,domesticretailersareinvariablypositiveaboutIrishproducebutthereisabeliefthatsupplierscandomoretobuild their brand around the provenance of their produce. Simply stating that the produce is either local or Irish will not always be sufficient.Moreinformationaboutthelocalityofwherethefoodisproducedandpackagedcanonlystrengthenbrands.FromtheIrishconsumerstandpoint,clarity around the definition of what local means will be important.Aslargernon-domesticretailersstartsellingproducelabelled‘locallymade‘thispotentiallycouldmeanit’sproducedintheUK.So a very clear labelling of regional provenance will be vital

HavingsuchanapproachtobrandingandlabellingwillalsohelpIrishproducerswithretailersandconsumersintheUK.UKretailersnowregularlyemphasisetheregionalprovenanceofproductsduetothesaturationofthe‘BuyBritish’banner,andtheincreasingknowledgeshownbycustomers.By adopting a branding approach that taps into regional aspects, Irish produce will become more aspirational amongst UK consumers and will also differentiate it from other ‘local’ produce.Differentiationofproduce,toallowitstandoutfromthecompetitionwillbeessential.

Insights from the UKThe national Irish brand does have considerable advantage over other non-UK produced food owing to the natural affinity UK consumers have with Irish culture.SuppliersneedtocontinuetobuildonthesepositiveassociationsandassetsthroughinnovationandNPD,whilecontinuingtoemphasisetheIrishbrandpersonality.

UKretailersperceiveIrishproducetobequasi-local,respectable,safeandofhighquality,butwithouttherobust‘personality’asgarneredbythelikesofFrenchorItalianfoodanddrink.This puts Irish suppliers in a strong position to be able to build upon the ‘face’ of Irish produce–againemphasisingthekeymarketcharacteristicsandregionalassetswhenpitchingforexportopportunities.A strong PR campaign and media seeding of Irish produce would without doubt help this process.

11SCB Partners for Board Bia, In Confidence 11SCB Partners for Board Bia, In Confidence

RetailerExpansionPlans“The multiples are encouraging people

to switch to private label and consumers are far more receptive to

this given the economic backdrop. The pressure on branded manufacturers

will only continue.”Md – Major producer

“Supermarkets based outside of the city provide ‘destination’ shopping

for the average consumer – a once a week trip. Convenience stores have the appeal of being local however

tend to be expensive so a combination of convenience and a reputation for

value will create a new dominant force in the retail market in Ireland.”

Brand Manager – Major producer

“Tesco or Sainsbury convenience stores stock half as many lines as

independent convenience, so there will have to be significant

rationalisation amongst the independents.”

Ceo – Trade Body

Summary OverviewRetailersareprojectingconsiderablegrowthoverthenextfiveyearsheavilydrivenbythemultiples,withtheirparticularfocusonconvenienceandonlinechannels.Inaddition,themajorityofmajorretailersarelookingoverseas,eithertocapturegrowthinemergingmarkets,ortoevaluatere-enteringContinentalEuropeanmarkets.

Changingconsumerlifestyleswillrequiremoreconvenienceoptions,soretailerswillreacttothistrendbyopeningmoresmallerandaccessiblebranches.Irishsuppliersandproducerswillneedtoprioritisethesetrendsinrelationtotheirproductandpackagingstrategies.Althoughinternationalmarketsarealreadyastrongsourceofrevenueforsomemajorfoodretailers,thistrendslookssettocontinue.KeyUKplayerswillcontinueaggressiveexpansionabroad(especiallyinemergingeconomiessuchasChinaandIndia),andothermorecautiousretailerswillconsiderre-enteringforeignmarkets.

IrishproducersmustlooktoexploiteverypotentialexportopportunityofferedbyUKretailers,suchastailoringproductstonewmarketsorinvestinginlogisticsthataccommodatethelongdistanceexportofgoodstothelikesofChinaandIndia.Thoseproducerswithstrongrelationshipsarelikelytobenefit,growingwiththeretailers.

AugmentedReality

12SCB Partners for Board Bia, In Confidence

ExpansionPlansWithfoodretailers’salesexpectedtoreach166.2billionby2015in the UK alone, competition for market share amongst the key players is intense.Majorretailerswillcontinuetomakegainsfromsmallerchainsandindependentsthroughstoreenlargementsandopeningsinnewareas.In the UK the key battle for space will be played out in the convenience format market, with Irish producers able to tailor their NPD to the specific needs of the convenience sector.Consumerspendinginthissectorwillincreaseat5.8%peryearcomparedto3.9%ingroceryretailgenerally.Internationally,emergingmarketssuchasIndiaandChinawillbecomekeytargetsforexpansionasretailersseektodiversifytheirportfolioandincreasegrowthrates.

Major Multiples Domestic ExpansionFoodretailspendingintheUKisexpectedtogrowatanaverageannualrateof3.9%overthenextfiveyears,reachingatotalof210billionby2015.The major retailers are meeting this demand through store enlargements and new branches,withthebigfourtargetingacombined5millionsquarefeetofnewspaceperyear,equallingonestoreperworkingday.Althoughhypermarkets,supermarketsandsuperstoresaccountfor2/3ofgroceryretailprofit,finitegeographicspace,planningpermissionrestrictionsandcommunitybacklasharemakingsuchlargerformatsdifficulttopursue.With intensifying competition for space in an increasingly saturated market, retailers are being forced to look for new solutions.

Inadditiontotheconveniencesector, the lunchtime sandwich market is also poised to become a new battle ground for the major supermarkets withMorrisonsandAsdaalsoconsideringsmallerformatstorestofollowtheSainsbury’sFreshKitchenroll-out.openits4thlargestbranchinNewtonMearnsthisyear.

Tesco

Sainsbury’s

Asda

Morrisons

Somerfield

Waitrose

Where the Big Retailers Dominate

source: CACI Market Report

• Tesco: Withamajorinternationalpushexpectedinthenextfewyears,Tesco’snationalsalesareexpectedtoaccountforasmallerpercentageofprofits.Butwithplanstoopen2.4millionsqftin2011,amountingto292newstores,theretailerismaintainingasteadypaceofgrowthinIrelandandtheUKnonetheless.InIreland,Tescohasfacedatoughcoupleofyearsbolsteringits“Irish”salesthroughitspresenceinNorthernIreland,closetotheborder.

• Waitrose: Asurgeof250newbranchopeningsisplannedfor2011,followedbyanadditional40peryearupto2015.Scotlandrepresentsasignificantfocusfortheretailer,whichwillopenits4thlargestbranchinNewtonMearnsthisyear.

• Asda: Asda’srecentacquisitionofNettorepresentsamajornewfocusforthecompanyonsmallerstoreformats,andmuchofitsexpansioninthenearfuturewillfocusonthedevelopmentoftheseoutlets.Nevertheless,planstobuildeighty20,000squarefootsupermarketsby2015indicatethatAsdawillcontinuetodevelopthelargerformatstoresforwhichitisbestknown.ThoughmuchdiscussionhasbeenmadeinrecentyearsaboutexpansionintotheIrishmarket,noofficialplansarecurrentlyacknowledgedbyAsda.

• Iceland: AfterclosingallofitsIrishbranchesin2005,Icelandisplanningtore-establishitselfwithamarketpresenceinIrelandwith40newstoresby2014.

• Sainsbury’s: Bylate2011Sainsbury’shopestoincreaseitsgrossspaceby15%,withaparticularfocusoncarbonneutralexpansionsandgreenerstoreformatsthatreduceenergyconsumption.TheretailerisalsotestingasandwichshopformatnamedFreshKitchen,forpotentialroll-outacross200UKsites.

• Morrison’s: Expansionplansfocusonthesmallconveniencestoreformatoflessthan3,000ft,withatotaltargetof1.5millionsquarefeetofnewspaceby2013.IthasalsoexpressedinterestinacquiringastakeinIceland.

RetailerExpansionPlans

42%

6%2%

Extra

Superstore

Express

Metro

Homeplus

Sainsbury’sNewFreshKitchenFormat

13SCB Partners for Board Bia, In Confidence

Major Convenience ExpansionTheUK’sconveniencesectorwill grow faster than grocery retail in general,andwilltotal36.9billioninfiveyearsaccordingtorecentindustrystudies.Changingconsumerlifestylesaredriving retailers to increase their number of smaller, accessible branches. Irish producers will need to prioritise these trends in relation to NPD and packaging strategies.

However,asthenumberofsmallerindependentchainsfallsduetoacquisitionsbymultiples,buy-outopportunitiesforthemultipleswilldiminish.Overthenextfiveyearsmultiplestoopennewstoresonsitesnotalreadyhousingconveniencestores.

Contributing Factors To Growth of Convenience In Next 5 Years

Contractioninthenumberofindependentconveniencestoresinoperation

Increasingpresenceof‘Big4’retailersandotherbrandsinthesector

Growingfuelpriceswillencourageshopperstowalkratherthandrivetostores

Rapidexpansionofnewentrants(largelymaingroceryretailplayers)helpingtoreduceoveralldecline

Workingmothers’needforconvenienceoptionstobalanceworkcommitmentswithfamilyneeds

On-the-gobreakfast,atdesklunch,andsnackstoreplacemissed home meals

Increaseof‘top-up’shoppingtripstosupplementprimary(oftenweekly)groceryvisitoronlineshop

Operatorsfromoutsidethesectordevelopingbroaderconveniencebasedformats/offerings

Urbanisation,populationdensityincitiesandincreaseduseofpublictransportation

Improvementoftheconvenienceoffering,presentingconsumerswithviableconveniencealternativestosuperstores

Centra: IrishconvenienceretailchainCentraplanstoadd17newstoresandover500newjobstoitsnetworkin2011,inaninvestmentworth23m.

SPAR Ireland: SparIreland’sgrowthisexpectedtocontinueto500storesbytheendof2011.In2010therewerebothstoreclosuresand22newopeningsthatamountedtoatotalof460stores.ThereisoptimismthattheSparchainwillsoonreachthe500markshouldtheIrisheconomystabilise.

Waitrose:PremiumgrocerWaitrose’sgentleexpansionintotheconveniencesectorhasseentheopeningofahandfulof

LittleWaitrosestoresacrosstheUK,inLondon,ManchesterandCambridge.Another37

locationsareexpectedtoopenoverthenextyear.

Sainsbury’s:TheUK’sthirdgroceryretailerisuppingitsconvenienceportfoliobyaddinga

further75storesbytheendofthe2010/11financialyear,withanother100+plannedfortherestoftheyear.Thisexpansionwillfocusparticularlyinthe

northandwestwhereSainsbury’sisunder-represented.ItsFreshKitchensandwichformatwill

alsoenticefurtherconvenienceshoppers.

Asda:TherecentacquisitionofNettowillresultinanewstoreformatakintoaTesco

MetroorSainsbury’sCentral,whichwillallowAsdatomoveintosmallermarkettowns.

RetailerExpansionPlans

14SCB Partners for Board Bia, In Confidence

International ExpansionInternationalmarketsarealreadyastrongsourceofrevenueforsomemajorfoodretailers,andthefutureislikelytoseecontinuationofthistrend.Irish producers must look to exploit every potential export opportunity offered by UK retailers, such as tailoring products to new markets or investing in logistics that accommodate the long distance export of goods to the likes of China and India.

• Tesco:Withastrongpresenceonthreecontinents,Tescoleadsthewayinglobalexpansion.Internationalsalesaccountfor22%ofthegroup’sprofit,withexpectationsthatthiswillreach43%by2015.WithitshighestrevenuecomingfromSouthKorea,ThailandandIreland,TescoseesAsiaasalong-terminvestmentandwillcontinuetoexpanditsnumberofstoresthere.InChinaspecifically,Tesco’sapproachinvolvesbuildingbespokeshoppingmallsoutsidethemaincitiesandfittingthemwithhypermarkets.PlansforthefutureincludeexpansionintoIndia,withitsfirstcashandcarrystoreopeningin2011.TescoholdspositionsinseveralprofitablemarketsinEasternEuropefromwhichitislikelytoexpandintoneighbouringcountries,includingHungary,Slovakia,PolandandtheCzechRepublic.

*RevenuesaresalesexcludingVAT

Us

£349m*

UK

38,558m*

Asia

£8,432m*

europe

£8,695m*

*RevenuesaresalesexcludingVATsource: TescoAnnualReport2010

• Sainsbury’s: RecentmarketvisitstoShanghaiandpublicstatementsofinterestregardingIndiaindicatethatSainsbury’swillalsobejoiningthebattleforAsia.PastfailuresinforeignmarketssuchastheU.S.havedeterredSainsbury’sfrominternationalexpansionuntilrecently,butstrongmarketperformancehasledtorenewedinterest.

• Waitrose: WithtwostoresinU.A.EandonerecentlyopenedinBahrain,physicalinternationalpresenceislimitedtotheMiddleEast.Waitroseisinfiltratingothermarketsthroughitsproducts,developingrecognizedbrandstatusinplacessuchastheU.S.andCanadathroughcooperationwithotherstockists.

• Asda: Asdaiscurrentlyinvestigatingthedevelopmentofsixnewprivatelabelbrandsspecificallyforinternationalcirculation,andalreadyhastheperfectlaunchplatformthroughparentcompanyWalmart.Currentlytherearenoplanstoexpandphysicallywithnewforeignstores,withafocusonnationalgrowth.

• Marks & Spencer:AstrategyprioritizinginternationalexpansionisunderwayatMarks&Spencer,withIndiaandChinaatthecoreoffuturegrowth.Theretailerisalsolikelytore-openstoresincontinentalEuropeafterhavingfailedinthatmarketadecadeago.

Diversificationissettobealeadingtrend,asglobalchainsmoveintokeyareasandnewretailersjointheraceforforeignexpansion.ChinaandIndiapresentthemselvesastwokeytargetsforpotentialgrowth,withhighlevelsofinvestmentandconsumersseekingtoemulateWesternlifestyle.Asretailersexpandinternationally,producerswithstrongrelationshipsarelikelytobenefit,growingwiththeretailers.

Tesco Around The World

TOP 10 GLOBAL GROCERY MARKETS

800

700

600

500

400

300

200

100

€ BILLIO

N

US

704

bn

China3

77 b

n

Franc

e2

37 b

n

Japan

342

bn

Ind

ia 2

19 b

n

UK

216

bn

Germ

any

173

bn

Italy

146

bn

Russia1

33 b

n

Mexico1

29 b

n

US

734

bn

China6

09 b

n

Ind

ia 3

21 b

n

Japan

397

bn

Franc

e2

36 b

n

Russia2

14 b

n

Brazil2

13 b

n

UK

196

bn

Germ

any

184

bn

ITa

ly 1

50 b

n

2006 2010 (Forecast) 2014 (Forecast)

source: IGDGlobalRetailingReport2010

China8

75 b

n

US

857

bn

Japan

414

bn

Ind

ia 5

15 b

n

Russia3

70 b

n

Brazil3

27 b

n

Franc

e2

62 b

n

UK

223

bn

Germ

any

193

bn

Ind

on

esi

a 1

92 b

n

900

RetailerExpansionPlans

15SCB Partners for Board Bia, In Confidence

Groupon

DebenhamsOnlineTV

Summary OverviewRetailerswillseektotakeadvantageoftheincreasedconsumerinterestintheconvenienceofonlineshopping,aswellasimprovedconnectivityavailabletoconsumersthroughsmartphoneapplicationsandmoreengagingonlineexperiences.Asconsumers’trustofonlineformatsdevelops,retailerswilllookforwaystoamplifyconsumerspendviatheironlineandmobileplatformsaswellasremainvisibleandrelevantintheircustomers’day-to-daylives.

Thegrowthofbroadband,mobilecommerceandrelatedapplicationsaswellasuseofsocialnetworksandcrowdshoppingsiteswillenableretailersknowmoreaboutcustomers.Ofequalimportancewillbetheabilityforcustomerstohaveaccesstoallsortsofinformationaboutretailersandtheproductstheystockandsell.Thesenewchannelsofpurchasinganddialoguewillmeanastutesupplierscanselldirecttoitscustomers.Thegrowthofmobileappsmeansthatcustomerswillusetheirmobilesintheshopsandbasepurchasingdecisionsonresultsgeneratedbytheapps.

Homedeliveryfromm-commerceoronlineshoppingwillcontinuetogrowinpopularitywhichmeansthattheretailerswillcontinuetoevolvethelogisticsinthesupplychaintodeliverbest-in-classorderfulfillment.Atthesametime,Irishproducers,willneedtoincreaseefficiencyintheirsupplychaintobeapplicableforonlineretailplatforms

Instores,theautomationtrendofthepastfewyearswillcontinuetostrengthen,particularlyintheconveniencechannel,asretailerslooktocutdownonoverheadsandstreamlinethepayingprocess.

TechnologiesforChannelExpansion

“Social media will be increasingly important. Consumers are very tribal. Sites such as mysupermarket.com and other review sites will become easier

to access consumer reviews while shopping.”

Business planning Manager – Major Retailer

“Internet shopping is growing steadily, but many obstacles still remain. Logistics

for home delivery are poor in Ireland – especially as most homes have dual-earners and therefore delivery window

is small.”Ceo – Trade Body

“Our view is that online is going to come far more into play, whether it be via home delivery or pick up. We see neighborhood stores becoming more

important as people mix their purchase habits between big supermarkets and small neighborhood stores. We see that

as a channel for growth.”Commercial director – supplier

16SCB Partners for Board Bia, In Confidence

Developed Online Shopping ExperienceTheUKaccountedfor30%ofallEuropeanonlinesalesin2010,andisexpectedtogrowby14%in2011.Brands using social networks and crowd shopping sites (such as Groupon) to provide shoppers with special offers, are not only increasing revenue from advertising and click through, but also learning more about their customers via data capture.Thustheycanexpandtheirrelationshipandloyaltywithconsumers.ThisisatrendthatIrishbrandsandproducers(especiallysmallornewcompanies)canutilisetogaincompetitiveadvantage,andtoincreasebrandloyalty.

Onlineshoppingpioneersinclude:

• Groupon: AmericansuccessstoryGrouponhastakentheUKbystorm.Thecouponsitehassavedits50millionusers851millioninitsfirsttwoyearsthroughproductdiscounts.Customersgetheavilydiscounteddealsattheirlocalrestaurantsandshops,andthelocalmerchantsgetaninfluxofnewcustomers.ThisformatcouldsuitnewIrishbrandslookingtoincreaseawarenessamongstconsumers.

• Makro: WholesalerMakrohada‘TweetaPrice’campaign,allowingcustomersonTwittertodecidethepriceofselectedproducts.Thediscountappliedwasdeterminedbythenumberofre-tweetsthateachproductgot.

• Debenhams: Themulti-productretailerintroduceditsownonlineTVformatthatcanbealsoviewedviasmartphonesandYouTube.Byusingthewebsite’sclickandbuysystem,viewerscanpurchaseitemsfeaturedonthechannelastheywatch.

• Superquinn: TheIrishretailersignedadealwithperformancemarketingcompanyTradeDoublerinlate2010tostrengthenitsonlinebusinessin2011andbeyond.

• Mysupermarket.com: Onlinecomparisonwebsitessuchasmysupermarket.comgivecustomersinstantaccesstopriceandcontentcomparisonsandareanexcellentplatformforswitchingbrandsorretailers,bolsteredbydesignatedpagesfortopoffersandpersonalisedrecommendationsfollowingregularuse.

• M&S Social Media Success: Marks&Spencerhasthelargesttwitterfollowingamongstmajorfoodretailers,andoverthreetimesasmanyFacebookfansassecondplaceSainsbury’s.Regularupdatesfromthecompanyengagecustomersina2-wayconversationandhelptopublicisepromotionstakingplaceinstore.

• TV Shopping Channels: QVChassourcedlocally-producedproductsforsomeprogrammes.Forexample,FraserDohertytheyoungfounderofSuperJamappearedonthechannel.QVClooksforfoodproductsthatareuniqueandhaveastorybehindthem.

Both suppliers and retailers will have to adapt all new channels of purchasing and dialogue with customers. Prices will be increasingly transparent and thus competitive.

Therewillbeopportunitiesformarketing:astutesupplierswillbeabletoselldirecttoconsumers.

As Ireland develops its broadband infrastructure Irish products need to get up to speed with all new technologies so that they can take advantage of the benefits afforded. UK retailers and their established suppliers have had some time advantage.

TechnologiesforChannelExpansion

MySupermarket

SuperQuinn

17SCB Partners for Board Bia, In Confidence

M-CommerceThoughstillinitsinfancy,thefutureofdigitalshoppingisquicklybecomingacollectionofmobileretail,peer-to-peerlending,storedvaluecards,micro-philanthropyandprivatecurrencies.

•M-Commerce sales in the UK are expected to more than double in the next three years.In2009,2%oftheBritishpopulationusedtheirmobiletoshoponline,whileapproximatelyonethirdhadinternetontheirmobiledevice.(Source:GlobalMobileandM-CommerceTrends2011,Reportlinker.)

•75% of online retailers currently have a mobile strategy.By2015,thenumbershouldincreaseevenmore.AsmarketsinEuropeandtheMiddleEastoutpacetheUS,e-commercewillshiftitsmarketalignmenttofocusondifferentgeographies. (Source:ABIResearch,2010.)

•Asthenumberoftangibleproductsalesincreasethroughm-commerce,2015shouldseenumbersmovebeyond20%from6%especiallyasmobileinterfaceslikeeBay’s‘app’takehold.(Source:MobileMarketingAssociation,2010.)

Dozensofsmartphoneapplications(suchasGoogleShopper)willallowconsumerstolookupaproductbyscanningitortypinginthebarcode.Theappthenreturnsalistofpricesforthesameitematnearbystoresorthroughonlineretailers.

Retailers will need to ensure that they enable the shopper to make purchases whenever and wherever they want, which means mobile site optimisation and mobile commerce channels cannot be ignored.

ConsequentlyIrish producers will need to ensure that the pricing and product information of their products on these sites are correct (wronginformationmayleadaconsumertooptforacompetitorbrand)andthattheyhavethecustomerservicesupportinplace.

TechnologiesforChannelExpansion

GPSstorelocators,barcodescanners,loyaltypointsandshoppinglistsareallnowbecomingstandardfeaturesonretailers’apps,andeBayhasrecentlylaunchedafashionappwhichusesaugmentedreality.In the coming years, grocery sector retailers will use this technology to encourage sales by offering product and cooking suggestions via barcodes, product compatibility, and flash promotions.

• Amazon: Amazonrecentlyannouncedthatitsmobilecommercerevenuereached1.15billioninthelast12months(worldwide)andpredictedtherewillcomeatimewhenallretailerswillhavewebsitesthatareoptimisedformobileuse.

• Tesco: TheUK’sfirsttransactionalbarcodescannerfortheiPhonewaslaunchedbyTescoattheendof2010,enablingshopperstoscananygroceryitemandaddittoahomedeliveryorderinstantly.

• Marks & Spencer:Theretailerenteredthemobilee-commercemarketattheendof2010viaanewmobilesiteratherthananapp.Thenewsite(currentlyrestrictedtoclothing,homewareandtechnology)isexpectedtocovergrocerypurchasesaswellifthelaunchprovessuccessful.

• Sainsbury / Nectar: Sainsburycurrentlyhastwoappsonthemarket.TheSainsbury’sappincludesastorelocator,alistofdealsinstore,newsandpersonalisedoffers.TheNectarappisintendedforpeoplewhoshopinSainsbury’sandHomebaseandprovidesaccesstooffersformoreloyaltypoints.

• Waitrose: MuchliketheSainsbury’soffering,thisfreebrandappalsoprovidesshopperswithrecipesuggestionsandcross-sellingproductopportunities.

18SCB Partners for Board Bia, In Confidence

Implications1. Producerswillneedtokeepapacewithtechnologytrends

asbroadbandpenetrationanduseofmobileinternetincreasesinIreland.UKsuppliershavehadmorerecentexperienceofthis;assomeretailerslooktoconvergesupplychains,Irishsupplierswillneedtobeabletocompeteonthisfrontandbepreparedfornewrequirementsaroundpackagingandlabellingforexample.

2. Irishproducerswillhavetothinkcarefullyabouthowtheycancapitaliseonnewopportunitiespresentedbytechdevelopmentsandtheimplicationsthiscouldhaveontheirownproductionandsupplycapabilities.

TechnologiesforChannelExpansion

Rise of Food & Beverage AppsIntheIrishandUKgrocerysectors,potentiallytransformativeappsarealreadyspreading,mostoriginatingfromtheUS.Theseapplicationsarestillintheirformativestage,but have the potential to change the way consumers think about food and shopping over the coming five years.Consumersaretakingthesetechnologiesintotheretailenvironmentandbasingpurchasing

Good Guide TheGoodGuideprovidesshopperswithethicalratingsforthousandsofproducts.Thesearebasedonalonglistofhealth,environmentalandsocialcriteriausinginformationinthepublicdomain.

ScanavertThisallowsconsumerstosettheirowndietarypreferencesincludingallergies.Itthenwarnsthemifaproductisincompatiblewiththesesettingswhileshopping.

AUGByscanningthebarcodewiththeAUGApp,shopperscanfindhowfartheproducthastravelledtoreachthestore,theidentityoftheprimaryproducer,whethertheingredientsareinseasonandahistoricalrecordofprices.

CNET Scan and Shop Allowsyoutoscanaproductbarcode,accessuserreviews,comparepricesfromvariousretailersandorderonline.

Smart Phone Apps:

3.Giventhetransparencythattheinternetandmobilecommerceaffords,suppliersneedtobeawarethatexistingandpotentialcustomerswillexpecttobeabletoaccessaccurateinformationaboutproduce,ingredients,ecocredentials,pricingetc,allatthetouchofabutton.

4.Whileretailersareactivelyusingsocialmediaandappstoengagecustomers,Irishproducersmustactivelyconsiderhowtheycanusethesechannelstobuildtheirownbrandsandfollowing.

decisionsonresultsgeneratedbytheapps.Thoughmanyfoodappsarepreoccupiedwithrecipesandfinediningreviews,some offer very specific information liable to influence decisions made while shopping.Examplesshowingpracticalusesfornewfoodapptechnologyareshownbelow:

19SCB Partners for Board Bia, In Confidence

• Dairy Crest: Chilleddairyfoodsupplier,DairyCrest,hasimplementedParagonSoftwareSystemstohelpcentraliseitsUKdeliveryscheduling.Theautomatedroutingtechnologymakesforbettertransportplanning,transforminglogisticoperationsfromatraditionalmethodofstock-baseddeliveriestoaweb-basedcollaborativeplanningmodel.

• Waitrose: Transactionsmadeonlineathomeoratworkcanthenbecollectedfromtheretaileravoidingthein-storeexperience.Waitrosehasrolledouttheconceptto21newstores.

• Boots: In2011,Bootsisplanningtoopenadrivethroughnewstoreforfoodofferingsandpharmacyitems.

• In Store Digital Order: Asdaistotrialtheuseofin-storeorderinginthreeofitsstores(Bradford,GlasshoughtonandHyde).Customerswillbeabletoordergoodsfromanin-storedisplayoranonlinecatalogue,withproductsthendispatchedfromawarehousespaceonsite.TheCo-operativeisnowcombininghomedeliverywiththelatesttouchscreentechnologyviadigitaltouchscreenkiosksthatallowconsumerstoefficientlyselectadeliverytimeinstoreastheydotheirshopping.

Merger of Digital and Physical WorldRetailershavetoquicklyrespondtotheever-growingpopularityinhomedeliveryasthepreferredchoiceofshoppingfortime-poorconsumers.Logistics in the supply chain are being adapted to cope and deliver best-in-class order fulfilment operations. This expectation will also be passed on to Irish producers, who will need to increase efficiency in their supply chain to be applicable for online retail platforms.

Retailersareexpandingwithnewdepotsdedicatedtohomeshoppingpicking,andalternativecollectionoptionsarebeingofferedtotheconsumersuchasClick&Collectandin-storedigitalordering.

Examplesofrecentleadersinclude:

• Asda: Asda’sexpansionplansinhomeshoppingarematerialisingwiththeopeningofasecondsiteinNorthLondon,dedicatedtohomeshoppingdistribution.Asdaisextendingitsreachbydiversifyingitsofferingstoincludebetterorderingonline,pickingupinstorefacilitiesandefficienthomedelivery.Theirnewsitewillhelptofacilitatetheseservices.

Asda’sdedicatedHomeShoppingCentreinMorley,nearLeeds.Productsorderedonlinearepickedby500Asdaemployeesandplacedintotesreadyfordelivery.Twoconveyorsystemsof45metreseachuseacombinationofhorizontalandinclinedbeltconveyors,rollerconveyorsandpoweredbends.

• Tesco: Thefirstquarterof2011willseethecompletionofTesco’slatestdistributioncentreinNorthLondon.The23minvestmentwillhelptheUK’sNo1supermarkettoserviceitsdot.comandconveniencebusinesses.Tescoisalsotriallinga‘DriveThruClick&Collect’servicewhereshoppershavetheirgroceriesputintotheircarbootforthemfora2.3charge,andisplanningtooffercollectionfromitsvastnetworkofconveniencestores.

Single Channel Multi-Channel Cross-Channel Omni-Channel

• Customersexperienceasingletypeoftouch-point.

• Retailershaveasingletypeoftouchpoint.

• Customerseesmultipletouch-pointsaspartofthesamebrand.

• Retailershavea‘singleviewofthecustomer’butoperateinfunctionalsilos.

• Customerseesmultipletouch-pointsactingindependently.

• Retailer’schannelknowledgeandoperationsexistintechnicalandfunctionalsilos.

• Customersexperienceabrand,notachannelwithinabrand.

• Retailersleveragetheir‘singleviewofthecustomer’incoordinatedandstrategicways.

The Legacy The Reality The Aspiration The Ideal

TechnologiesforChannelExpansion

Evolution of Customer / Retailer Touch Points

20SCB Partners for Board Bia, In Confidence

New TechnologyRetailerswillcontinuetoslowlyupgradetheirtechnologyoffering,withhandheldITdevicesandvideotouchpointsfindingtheirwayin-storeoverthenextfiveyears.

The automation trend of the past few years will continue to strengthen, particularly in the convenience channel,asretailerslooktocutdownonoverheadsandstreamlinethepayingprocessasmuchaspossibleforcustomersthroughgreaterimplementationofself-servicecheckoutandmobilepoint-of-salesystems.

In-Store Technology Handheld TechnologyOverthenextfiveyearshandheldITdeviceswillincreasinglybeusedbyretailstafftobetterservicetheneedsofcustomersaswellasbycustomersthemselves.

Video TouchpointsRetailersareusingthenewestinterfacetechnology,suchasmulti-touchtoprovidefixedinformationpointsinstore.Thesepointscanprovidefloorplansandotherinformationinaninteractivewayforconsumers.

Self CheckoutsUSPizzeriaUNOhasimplementedmobileselfcheckoutsintheirrestaurants,allowingdinerstoplaceordersandpaysimultaneouslyminimizingwaitingtimeandmakingordersmoreaccurate.

Unmanned Kiosks: Wine KioskConceptstoresarecurrentlytestingnewformsofautomatedfoodandbeveragevending,completewithconciergeadvicethatprovidesrecommendationsbasedondiningmenus.

Personal TechnologySpontaneous OffersTesco’sfutureclubcardwillinstantlygiveshoppersspecialdiscounts,whichappearonthecard,basedonauser’spreviousbasketsandshoppinglists.

Location-Based ServicesLocation-basedserviceshavebecomeevenmorepowerfulwhentheycombinepersonalisedandpermission-basedreal-timenotificationsforrewardsatlocalestablishments.

Mobile PaymentSmartPhoneswillcontainindividualbankdetailsandcreditcardinformationinasingledevice,allowingconsumerstostreamlinetheirwallets.

Augmented RealityMobileaugmentedrealityappsareincreasinginpopularity,theincreasedinterestwillleadtonearly1.4billionworldwidedownloadsby2015.

Future Retail FormatsExperts Utility StoresNewformatswillblendtraditionalconvenienceshoppingwithcasualdiningcountersthatprovidefresh,ready-to-consumefoodandbeverages,ensuringspeedandqualityarenolongermutuallyexclusive.

Hydroponics Withanincreaseindemandfromtheconsumerforfresher,morelocalandsustainableproduceitisunsurprisingthathydroponicscouldplayamajorpartinthelookandfeeloffuturesupermarkets.

Ocado Future Fridge Forecastingthepotentialforfridgestoevolveintosomethingtrulycerebral,offeringpredictive,fullyautomatedshoppingalteringthewayweshopandeatforever.

TechnologiesforChannelExpansion

21SCB Partners for Board Bia, In Confidence

Summary OverviewRetailerswillincreasinglyusecustomisedpromotionsandincentives,basedonconsumerdatafromloyaltycardsandonlineshopping,enablingretailerstogainvaluableconsumerprofilinginsights.Influentialmediapersonalities;includingcelebritychefs,amateurbutinfluentialfoodcritics,bloggersandothers,willimpactinitialstore-stockingdecisions;theymayalsodeveloppromotionalpartnershipsandrelationshipswithretailers.

TrendsinPromotions“About 18 months ago Flahavans made

a very conscious shift to dial up their Irish, locally sourced pedigree. They

are 95% sourced locally.”Marketing director – food Body

“Producer’s marketing campaign. They need to have a launch campaign and ongoing communications. It is a factor when we take a product – it helps, but

it’s not essential.”Marketing director – food Retailer

Retailer Promotions Retailerscontinuetocreate new promotions and incentives (loyaltycards,collaborationswithlifestylebrands,prizes)withwhichtomaintain consumer loyalty while also gaining invaluable consumer profiling insights. This gives Irish producers the opportunity to provide retail partners with promotions, such as discounted products or brand relevant prices.

Retailersarealsofindingnewwaystotapintonewfoodanddrinktrendscomingfromthemedia,whilealsoutilisingtheseincreasinglyinfluentialmediapersonalities;fromcelebritychefsallthewaythroughtoamateurbutinfluentialfoodcritics/bloggers. Irish brands also have the opportunity to gain insight from these new sources, and to seed product and favour amongst key personalities.

22SCB Partners for Board Bia, In Confidence

Promotionswillremainamajorcomponentofhowretailersprovidevaluetotheconsumer.Overthenextfiveyears,promotionswillbemoreandmoreaggressiveasretailersgrapplewiththenatureofamaturemarketwithlittleabove-inflationgrowth.Brandbundlingandco-promotionsaswellastriedandtestedstrategiessuchascouponsandloyalty-cardschemeswillbekeycomponentsofretailers’promotionalofferings.

ExamplesofRetailerPromotions:

• Tesco: Tescohasofferedapromotiononlightbulbs,wherebyeachsaleofenergy-savingbulbscanbeconvertedintoairmilesthroughtheClubcardrewards’programme.

• Loyalty Card Schemes: TheBigClubcardVoucherExchangepromotionfromTescooffersClubcardholdersthechancetoredeemtheirpointsatdoublevalue.Itrecentlycontributedtoan18%increaseinvoucherredemptioncomparedwiththepreviousyear.

• Sainsbury’s & Comic Relief:FortheannualcharitydriveRedNoseDay,Sainsbury’sisthesolefoodretailerstockistoftherednoses,andthusfeaturesprominentlyinassociatedTV,printpromotionsandcelebritylaunches.

TrendsinPromotions

The New InfluencersRetailbuyerscontinuetolooktofoodwriters,celebritychefs,bloggersandconsumerforumstokeepabreastofconsumerfoodtrends.Asconsumersalsolooktotheseinfluencersfortipsontastytreats,recipesandingredients,retailersandsuppliersmustalignwithconsumerinterestsandinfluences.

ExamplesofNewInfluencers:

• Olive Oil: Between1990and2010therehasbeena300%increaseinoliveoilimportsintheUK.Akeydriver,apartfromhealthbenefits,hasbeentheheavyuseofoliveoilbycelebritychefsontelevision.

• Food Programming: Between1990and2010therehasbeena7,000%increaseinthehoursoffoodprogrammingontelevision.

• Big Fish Fight Week: AiredonChannel4intheUKoveraweek,thisseriesofprogrammesfeaturingJamieOliver,HestonBlumenthalandGordonRamsaywasresponsiblefor:aweek-on-week45%increaseinsalesofsardines,coley,browncrab,whitingandspratsatTesco,Marks&Spencer’slargesteverweeklyfishturnoveranda167%increaseinthesaleofpollock(shownintheprogrammeasanalternativetocod)atSainsbury’s.

• Jamie Oliver: Thecelebritychef’s2008programmeFowlDinnerswasanuncompromisinglookattheBritishpoultryindustryandwascreditedwitha50%increaseinsalesoffree-rangeandorganicchickenacrosstheUK.

23SCB Partners for Board Bia, In Confidence

Private Label DevelopmentsThebattlebetweenprivate label and brands is intensifying as private label ranges have continued to increase market share overthepastyears.Ithasprovedparticularlysuccessfulduringtherecessionasconsumersdowntrade,coincidingwithretailersde-stockingsomethirdpartylineswhileinvestinginthefurtherdevelopmentoftheirownbrands.Duringtherecession,tradingdownwithinstoreratherthanswitchingbrandsbecamepopularasconsumerslookedforlowerpricesandqualityguarantees.

PrivateLabelvs.Branded

Summary OverviewGrowthinprivatelabelwillslowintheUKoverthenextfiveyearsafteradecadeofhugegrowth.Despitethis,newprivatelabel‘brands’willcontinuetoappear,andretailerswillseektoexpandprivatelabelofferingintootherareasthroughtheuseofco-brandingandexclusivityarrangements.

“The multiples are encouraging people to switch to private label and consumers are far more receptive to

this given the economic backdrop. The pressure on branded manufacturers

will only continue.”Md – Major producer

“This will continue to increase and will see many manufacturers looking

to supply private labels instead of creating their own branded goods.

Private labels are no longer a cheap option and have become trusted (and

cheaper) brands in themselves.”Business planning Manager – Major

Retailer

“Tesco is encouraging people to switch to private label and consumers are far more receptive to switching from

proprietary to retailer brands given the economic backdrop. There is a lot of pressure on branded manufacturers

now and this will only continue.”Commercial director - supplier

100,00090,00080,00070,00060,00050,00040,00030,00020,00010,000

2009 2010 2011 2012 2013

• Grocery Market • Own Label Market

104,298 106,385 109,044 112,317103,267

49,78846,470 48,082 51,796 53,912

CurrentPrices(€m)

own Label Market by value at Current prices

200,000

WaitroseLuxuryBiscuits

Sainsbury’sBeGoodToYourange

Source:KeynoteMarketForecasts:FoodCateringandDrinkMarketFocus-2009

24SCB Partners for Board Bia, In Confidence

PrivateLabelvs.Branded

Europe is the largest market for private label products globally. WithinEurope,theUnitedKingdomisthelargestprivatelabelmarketbysize,followedbyGermany.Private label penetration in the United Kingdom is forecast to well exceed 40% in 2011.

MostUKretailerscontinuetoemployabasic-middle-beststrategywiththeirprivatelabelranges,andthesameconsumerislikelytobuyfromallthreetierrangesdependingontheirneeds.However,thesuccessofprivatelabelsintheUnitedKingdomcanbepartiallygaugedbythefactthatconsumers are revelling in ‘premium’ private label categories.Privatelabelshaveconsistentlyemergedontopintermsofqualityandconsumerstodayassociateprivatelabelswithinnovationandtrustworthyquality.

AnotherimportantsuccessfactorhasbeenthedynamismandinnovationofUKretailers.Facedwithintensecompetitionfromotherplayers,theyhavecontinuouslyre-inventedtheirranges,andmodifiedproductstosuitchangingconsumerdemands.

Source:KeynoteMarketForecasts:FoodCateringandDrinkMarketFocus-2009

50

40

30

20

10

0

-10

Oct2008 Nov2008 Dec2008 Jan2009 Feb2009

• Budget • Premium • Standard

sales GrowthOwn Label food ranges, by quality tier (%)

Sainsbury’s Taste the Difference Sainsbury’s,facedwithincreasedcompetitionfromTesco,changeditsprivatelabelimagefrom‘lowprice’to‘premiumquality.TheTastetheDifferencerangewasrecentlythesubjectofthesupermarket’slargestproductlaunchtodate,ledbyasuccessfulcampaignfeaturingbrandambassadorJamieOliverthatcontributedtoa2.9%increaseinsales.

Sainsbury’s Bistro Range Anewlineofrestaurant-qualitypremiumreadymealslaunchedin2010undertheTastetheDifferencelabel,featuringstarters,mainsanddessertsfor2diners.

Chef Neil Nugent TheMichelin-starredchefheadedseveralaward-winningrestaurantsbeforemovingontoworkatAsda,Sainsbury’sandWaitrose,andhasrecentlybeenhiredbyMorrison’store-vampitsownlabelproductsaheadofananticipatedre-launch.

Tesco Own Brand Price Drop Forthefirsttimesince2007,Tesco’snewchiefexecutivehasinitiatedacross-the-storepricereductionsoneverythingfrombasicstotheTescoFinestrange,anindicationthatthefutureofTesco’sownlabelisprice-focused.

25SCB Partners for Board Bia, In Confidence

Exclusive Deals Suppliersandretailerswillincreasinglyhavetheopportunitytoenterintoexclusivityrelationships,wherebyproducer-brandedproductsaresoldexclusivelyinanoutletwithnoretailerbranding.The result is defacto private labels without the prominent branding of the retailer, which can be off-putting to some consumerswhotendtofavourabrandedproduct.Furthermoretheproducerhastheopportunitytoretainandbuilditsownbrand.Exclusivityagreementsmaylastfrom2-5yearstypically.

Examplesinclude:

Canus Goats Milk SoapWholeFoodssignedanexclusivedealinMay2011withCanusGoat’sMilkSoapandwillbeginstockingits‘GrabandGo’productsinbulkacrossthePacificNorthwestandSouthwestinAmerica.ThepartnershipallowsWholeFoodstosetupsoapdisplayswhereconsumersselectfromseveralflavoursofunpackagedsoapsandputthemintoCanusbrandedbags.

Champney’s Spa ProductsFrom2004-2011Champney’sSpaProductshadanexclusivedealwithSainsbury’sbutfrom2011ithasforgedanewexclusivepartnershipwithBoots,joiningBootsotherexclusiveluxuryspaproduct,Sanctuary.

Oatmeal of AlfordSmallScottishoatmanufacturerOatmealofAlfordrecentlywentonsaleexclusivelyinthreeWaitrosestoresinScotlandandisalsoavailableonline.

StabiliserTM BeefAsmallgroupofYorkshirefarmersknownasBeefImprovementGroupsignedapartnershipin2010withMorrisonstosupplymeatfromanewtypeofsustainablebeefcow,calledtheStabiliserTM.

Co-Branding Co-brandinginwhicharetailers’brandisappliedalongsidethatoftheproducers.Thisisoftendoneinthecontextofonexclusivedeal.

Examplesinclude:

Davidstow CheddarThisco-brandedcheeseisuniquetoWaitroseandprominentlydisplaysitsexclusiverelationshiponthefrontofthepacket.

Heston Blumenthal’s Hidden Orange Christmas PuddingHestonBlumenthalcreatedanexclusiveChristmasPuddinginpartnershipwithWaitroseforChristmas2010thatincludedawholecandiedorangeinthecentre.TheproductwassopopularitsoldoutinstoresandcouldbefoundoneBayforupwardsof80.5.

Louis Chaurey ChampagneChampagnebrandproducedentirelywiththebrandingofaregularchampagnebottle.TheonlymentionofM&Scomesinthesmallprintwhichreads‘ProducedforM&S’.

Duchy Originals from Waitrose English RaspberriesThisbrandincorporatestheWaitrosenameintotheexistingdesignoftheDuchyOriginals,creatingasubtlepartnershipbasedontheirexclusivityagreement.

Marks & Spencer Oakham© ChickensMarks&SpenceristheonlystockistofOakham©chickens,aslower-growingbreedthatcomefromdedicatedUKfarms.EveryMarks&SpencerpackagethatcarriesOakhamprominentlydisplaysthelabelonitspackaging.

PrivateLabelvs.Branded

26SCB Partners for Board Bia, In Confidence

RetailerPerspectiveonBest-In-ClassProducts

“It is going to be increasingly important to have products which are tailored to one

or two person families which will be cooked on the evening of purchase.”

Marketing director – Major Multiple

“Shelf-ready packaging is one area we feel our suppliers can improve upon”Marketing director – Major Multiple

“People want to cook but they remain time sensitive so they want ready meals that you have to prepare yourself, but which

have all the ingredients already selected and measured in one easy packet.”

Head of strategy & Business planning - Major Multiple

Summary Overview For Irish producers to grow market share and gain store shelf, an awareness of existing and future retail trends is an obvious pre-requisite. What is perhaps less clear is interpreting how each of these will impact a particular product or supplier. What retailers have made clear is that they expect suppliers to renovate and develop new products at the same time that they themselves are changing to enhance efficiencies and take into account areas of social and eco responsibility. So the environment is potentially pretty dynamic.

Manyconsumertrendsevolveslowlyandmanyofthethingsthatconsumersandretailersarelookingforfromsuppliersarealreadybeingconsidered,andindeedadoptedbyfoodproducers.

Whiletherewillbeanunderlyingawarenessoftrendsinformulation,packagingandpositioning,suppliersneedtoconstantlyreviewandupdateandnotesubtlechangesthatarehappening.Supplierswillalsoneedtoreviewtrendsinthecontextofthedifferentmarketstheyarelookingtoenter,aseachcountrywillhaveadoptedtrendstodifferentdegreesandofcoursehavetheirown.

Whatfollowsareexamplesofinterestingproductsthathavetappedintoongoingconsumerneedsaroundformulation,packagingandpositioning.

27SCB Partners for Board Bia, In Confidence

need for variety: Consumersarealwaysonthelookoutfornewfoodstotry–newflavoursandtextures,andgenerallysomethingfreshandintriguing.Retailersarelookingfornewproductideas,newstylesofeating,exoticingredientsandprocessingtechniques.Specialtysalts,buttersandflavouredmeatsareontherise.

scan swedish Meatballs: Haveuntilnowlimitedtheirproductlinetoretainauthenticityasthe‘originalSwedishmeatballs’,advertisingarecipedatingbacktothe1800s.Yetnowthecompanyislookingintoexpandingintoarangeofmeatballstomeetconsumerdemandforvariation.

vogel Bread: HasbecomefamousforitsqualityanditsdiverseingredientselectionsuchasFlaxSeedandSoyabread,offeringuparefreshingalternativetobrownandwhite.

Healthy:Retailerswillcontinuethedrivetowardsfoodswithincreasedwellbeingbenefits,harnessingconsumers’growingfood-relatedhealthawarenessandgovernmentsponsoredinitiatives,suchaslowsugar,lowsaltandlowfat.Otherhealthareasincludefunctionalfoods,proteinorvitamin-enrichedanddiseaseprevention.

Cherrygood: ThefirstcherryjuicedrinkintheUKprominentlyfeaturesitshealthbenefitsinallmarketing.

Holme farm: Theirvenisonisstockedinmajorsupermarketsandadvertisedasanaturallylowfatmeat,‘fullofgoodness’,fromnaturally-raiseddeerthatgrazefreely.

Good4U:Healthfoodbrandthatspecializesinreadytoeatbeansproutsandshootshasjustlaunchedtheirfirstflavorof‘smartshots’,afunctionalenergydrinkmadeofwheatgrass,appleandlimethatisbeingtrialedinstoresinDublin.

Longer shelf Life products:Consumersarelookingforlongershelf-lifeproducts;equally,retailersarekeentoextendthetimethattheycanleaveproductonshelf.Additivesandprocessesthatextendshelflifeareofinterest.

AvtarHanda,aprofessorofhorticultureatPerdueUniversity,foundthataddingayeastgeneincreasesproductionofacompoundthatslowsaginganddelaysmicrobialdecayintomatoes.

CargillhasdevelopedafoodprocessingtechnologytocreateFressure™freshgroundbeefpatties,whichhavedoubletheshelflifeoftraditionalfreshburgers.

organic & natural: Thespotlightonorganic,naturalingredientsandfarmingprocessessuchasforagingforfruit,vegetablesandherbs,isgainingmomentum,championedbyculinarypersonalitiesandreflectingthetrendforareturntoallthings‘natural’.

natoora: Aspecialistonlinenaturalfoodgrocerthatstocksaselectionofforagedseasonalproduce.

organic Avenue:Containsraw,unprocessed,organicfruitswhichimprovethehealthofcustomers.

Ready to Go foods: Thesefactorshavealsoseenanincreaseindemandforcontrolled,manageable,completefoods,asconsumerslookforall-in-onesolutionswithmultipleflavourcombinations.Whatwillbethenewcerealbar?

Little dish:Aseriesofreadymealsforyoungchildrenthatfocuson

classic‘home-stlye’dishessuchasfishpie,pastabolognese,cottagepie,andpastawithpeas.

nescafé:Newcoffeeinapouchexperience,givingcustomersasingularhelpingcontaining,milk,coffeeandsugarforone.

The Bitterball:ThistraditionalDutchsnackhasbeenrevolutionizedbyChefThor,takingonnewflavoursandbringingitintothe21stcentury.

RetailerPerspectiveonBest-In-ClassProducts

Best-In-Class:FormulationRetailersareconstantlyonthelookoutfornewproductsthatanswertochangingconsumerlifestylesandbringoriginalandexcitingproductideastoretailshelves.

Whiletheseareasmaynotbenewtheexampleshereprovideinsightintowhatretailersconsidertobebest-in-class.

• Healthy• Organic & Natural• Fine Dining at Home• Hero Ingredients• Need for Variety

• Longer Shelf Life Products• Ready to Go Foods• Snack Foods• Technology

28SCB Partners for Board Bia, In Confidence

fine dining at Home: ‘Stayingin’isthenew‘goingout’,asconsumershonetheircookingskills,hostdinnerpartiesandcreaterestaurantexperiencesathome.Retailerslookingforspecialityfoods,‘restaurantstyletake-away’diningoptionsthatgivethemashareofthe‘dining’market.

Mark & spencer:TheM&Sdining-inexperienceprovidesagourmetmealandwinefortwofor£10.

Tesco: The‘RestaurantCollection’offersconsumersdishestheywouldstruggletoconcoctthemselveseveniftheyhadthetime.

scratch: Scratchreadymealsaremarketedas‘Propercooking.Properquick’forpeoplewithlittletimewhostilldesirethehome-cookedexperience,includingalltheingredientsnecessary,evenherbs,seasoning,oliveoilandwhitewine.

snack foods: Consumersarelookingfornewsnackfoodoptions,fromallcategories.

Twix fino: Notpositionedaslighteroption;TwixFinoallowssnackingindulgencewithlessfatandcalories,freefromthestigmaofbeinga‘dietbrand’

savoury Crackers:Shiftingthereputationofthericecakefromthatofablandsnackfortheweightconscious;Kalloisdiversifyingtheirpalettewithnewflavours.

Marmite Cheese Bites :On-the-gosnackfood,singleportionmarmite-flavouredcheddarcirclestounwrap.

Hero Ingredients:Specificingredientsarebeingglorified,asproductshighlightauniqueingredient,withthefinestonesstandingouttobecomebrandsintheirownright.Consumersarealsolookingforingredientreduction–productswithlessthan5ingredients.

Bordier Butter: Jean-YvesBordier’sbutterfromSaint-MaloinFranceiswidelyregardedasthefinestbutterintheworld.

nielsen Massey:Makesarangeofvanillasdependingontheoriginofthebean,includingMadagascaran,Mexican,Indonesian&Tahitian,andhasinformationonitswebsiteonthespecificculinaryuseofeachparticulartype.

Technology: Anytechnologythatbringsaconsumerbenefitorretailerefficiencyisofinteresttotheretailer.

Minus 8: Named after the freezingconditions in which the grapes are hand-pickedand pressed, Minus 8 is traditionally slow fermented from extraordinary wine. The process makes for a syrupy mellowness that is the perfect complement to tenderloin, foie gras or ice cream.

Refuel & Repair: Thissportsrecoveryready-to-usebeverageisahighproteindrinkfeaturingProdietFluidtechnology.Thisallowsthedrinktoincorporatehigherlevelsofproteininitwithoutincreasingitsviscosity,aidingrehydration.

RetailerPerspectiveonBest-In-ClassProducts

Best-In-Class:Formulation(continued)

29SCB Partners for Board Bia, In Confidence

Artisan packaging: WithBordBia’sguidance,smallproducerscanusetheirsizeastheirUSP,emphasisingthelocal,artisannatureoftheirbrandandproductportfoliofromappropriatelydesignedpackagingandlabelling

Goat Island pepper sauce: Thecapsealribbonaswellasaproductiondateribbon,givestheimpressionthatitisbrewedandstoredinanartisanenvironment.

Glenrothes scotch whiskey: Usingahandwrittenlookforthetastingnotesonitslabelsandasimplecorrugatedcardboardouter-casingemphasisesthehandmadeartisanqualityofthewhiskey.

Transparency: Packagingwithproductvisibility,includingwindows,smallerlabels,andclearmaterials.Labellingwillbecleanerandmoreneutralinappearance,witheasytounderstandingredients’lists.

supermarket chain Migros: hasusedtransparencyinaneyecatchingwaywithitspackagingofIrishAngusfillet.Thetextureofthequalitybeefbecomesadesignfeature.

Innocent: ThefruitjuicemakerhasmadetheUSPoftheir‘VegPot’mealsthatonlythreeingredientsareused.

packaging Modernization:Newmaterial,freshdesigns,progressive,customizedorinteractivepackagingsolutionsareexploredasstandoutpackagingformatsthatdifferfromthenorm.

306 paper Bottle: Thisisanenvironmentallyfriendlysolutiontotheproblemofresalableplasticbottles.Itisthefirsttotallyrecyclablepapercontainermadefrom100%renewableresources.

wdaru’s Mnum:ThisJapanaeseteacompany’splayfulinteractivepackaginghasmadetheteaacultproductinJapan.

eco & sustainability:Majorretailers,viatheircommitmenttocorporateandsocialresponsibility,areleadingthedriveforsustainablepackaging.Retailerswilllooktocollaboratewithproducersreducepackaginganduserecycledandbiodegradablematerials.

Boxed water: 90%ofthecontainerismadefromrenewableresourcesandalsopromotestheirenvironmentalpositionontheexterior. steve’s leaves:Baggedsaladleavesadvertisedas‘onlywashedinspringwater’,thataregrownbynaturefriendlyfarmersthatbuildwildlifehabitats.‘Steve’hasaPhDinwatercress.

Labelling evolution:LabelsarelikelytoevolveasQSRcodesbecomethenorm,governmenthealthlabellingrequirementsincrease,andotherelementshavetotakeuplabelsurfacearea.

Meat Labelling:TheEUismakingapushforclearerfoodlabellingrulesonmeat,toallowconsumerstoidentifyexactlywherethefoodtheyhavepurchasedhascomefrom.

QR Codes:ThewineindustryhasembracedQRCodesontheirlabelsasatooltoenhancethebuyingexperience;frommakingrecommendationstoofferingpromotions.

RetailerPerspectiveonBest-In-ClassProducts

Thesameconsumerneedsthatdriveformulationtrendswillencouragepackaginginnovation.Packagingisamechanictoconveytrust,authenticity,varietyandenhanceconvenience.Retailerstakealead,aheadoftheconsumer,ingreen/sustainabilityissuesandlookingforpackagingsolutionsthatimproveefficiencies.

Whiletheseareasmaynotbenewtheexampleshereprovideinsightintowhatretailersconsidertobebest-in-class.

• Transparency• Eco & Sustainability• Extending Shelflife• On-the-Go• Artisan Packaging

• Packaging Modernization• Labelling Evolution• Retailer Friendly Packaging• Packaging Reduction

Best-In-Class:Packaging

30SCB Partners for Board Bia, In Confidence

extending shelf-life:Thedrivetowardsgreaterchilledfoodscreatesaneedforpackagingmaterialswhichhelptomaintainfreshness.Retailersareincreasinglylookingforpackagingwhichboostsshelflifeofproductssuchasmeatanddairy.

McCains: A1mmwide‘IntegritySeal’isdesignedtoreducemanufacturingcosts,cutdownonfoodwastageandprolongingfreshnessandshelflife.

Tesco fresh and naked:UsesanewpackagingtechnologycalledBioptima,whichisfullybiodegradeablewhilealsohelpingpreventsaladfromdryingout.

Retailer friendly packaging:Suppliershavetomakesuretheirpackagingworkswithintheaimsofdifferentretailers’CSRprogramtmes(inrelationtopackagereductionandsustainability),andareshelfreadyforallin-storerequirements.

smurfit Kappa Machine systems: Producesshelf-readypackagingfordairy,cerealsandotherindustries.

sainsbury: SuppliersarenowprovidingretailerssuchasSainsbury’swithbrandedmulti-packcartonsdesignedtostackandsitonshelveseasilytherebymaximizingspaceandaidingstorageandstockcontrol.