10

Page 1 Retirement Planning Toolkit Planning a Financially Secure Retirement

Page 1

Retirement Planning ToolkitPlanning a Financially Secure Retirement

Page 2

OverviewThe purpose of this guide is to provide a framework to help you to plan for your retirement.

Retirement is one of life’s major personal and financial life events and planning in advance is vital. Our role is to help you to achieve and enjoy a financially secure retirement.

This guide is divided into the following 3 steps:

1. Assessing your needs.2. Reviewing your options.3. Implementing & evaluating

your retirement plan.

We help you to plan for a financially secure retirement by:

k Reviewing and evaluating your existing financial affairs.

k Assessing your financial needs in retire-ment.

k Developing a tax-efficient plan to help you to achieve a financially secure retirement.

k Recommending suitable savings accounts, investment options, Approved Retirement Funds and annuities for you, as appropri-ate.

k Providing you with ongoing expert finan-cial advice and assistance during your retirement.

Page 3

1 Assessing Your NeedsThe key to a financially secure and carefree retirement is having enough regular income to meet your ongoing lifestyle costs. So, how much do you need in retirement?

k The first stage is to review your existing lifestyle expenses. Our checklist at the end of this guide will help you to compile your lifestyle expenses.

k You may need to add an extra amount to allow for additional expenses that may arise, such as medical costs, extra holidays, more travel, etc.

k The next step is to review your financial costs and obligations, such as loan repayments and life insurance costs.

k Ideally, you should aim to be debt-free by the time you retire, and you may need to consider a debt management strategy in order to ensure that your debts are cleared in a structured and affordable manner.

k Most likely you will not require life insurance when you retire, unless life insurance is required for any remaining loans or for inheritance tax purposes.

Allowing for inflation (of say 2% or 3% per year), you should then estimate the future values of your lifestyle costs, and your future financial costs at your preferred retirement date.Next, you should list out and review your existing assets, liabilities and likely sources of income in retirement, such as your savings and investments, private/public sector pension plans, and your entitlement to the state pension.

When you have listed out the current values of your assets and liabilities, you should then estimate the future values of your assets and liabilities, and your future income levels that you can reasonably expect at your preferred retirement date. You should consider:

k A prudent rate of growth to be applied to your existing savings and investments in order to estimate their future val-ues.

k Amortising any existing loans in order to estimate the future loan balances. Note that interest rates are currently at historically low levels and are likely to rise at some stage

Page 4

in the future, so future interest rates may impact on your future loan balances, and may impact on your ability to clear your loans.

k The level of income that your savings and investments can realistically provide at your preferred retirement date and during your retirement, for example deposit interest on your cash deposits, dividend income, rental income, etc.

k Your entitlement to the state pension and other state benefits in retirement, including en-titlements for spouse/partner. You may need to contact the Department of Social Protec-tion in order to determine your entitlements. In addition, if you have worked abroad, you should check your entitlements to a state pension based on the time you have worked in other countries.

k The future values of your private/public sector pen-sion plans and the level of income in retirement that your pension plans can realistically provide. Annui-ty rates are currently at low levels, due to low interest rates and bond yields, and future annuity rates may be higher than current annuity rates.

Note: an annuity provides a secure regular pension income for life in exchange for an upfront lump sum payable from an accumulated value in a pension plan.

“Annuity rates are currently at low levels, due to low interest rates and bond yields, and future annuity rates may be higher than current annuity rates.”

At the end of this first step, you should have a clear picture of how much you need in retirement, an estimate of the future values of your assets and liabilities at your preferred retirement date, and an idea of the amount of income that you can reasonably expect from your assets and pension plans during your retirement.

Page 5

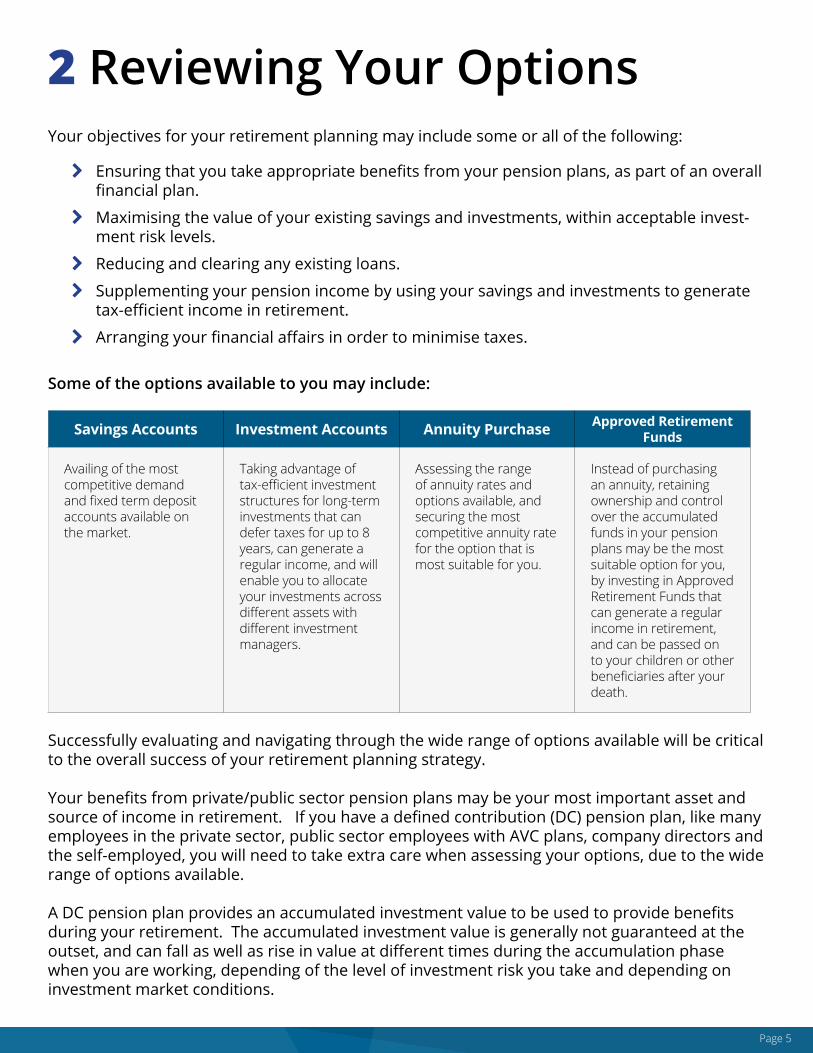

2 Reviewing Your Options Your objectives for your retirement planning may include some or all of the following:

k Ensuring that you take appropriate benefits from your pension plans, as part of an overall financial plan.

k Maximising the value of your existing savings and investments, within acceptable invest-ment risk levels.

k Reducing and clearing any existing loans.

k Supplementing your pension income by using your savings and investments to generate tax-efficient income in retirement.

k Arranging your financial affairs in order to minimise taxes.

Some of the options available to you may include:

Savings Accounts Investment Accounts Annuity Purchase Approved Retirement Funds

Availing of the most competitive demand and fixed term deposit accounts available on the market.

Taking advantage of tax-efficient investment structures for long-term investments that can defer taxes for up to 8 years, can generate a regular income, and will enable you to allocate your investments across different assets with different investment managers.

Assessing the range of annuity rates and options available, and securing the most competitive annuity rate for the option that is most suitable for you.

Instead of purchasing an annuity, retaining ownership and control over the accumulated funds in your pension plans may be the most suitable option for you, by investing in Approved Retirement Funds that can generate a regular income in retirement, and can be passed on to your children or other beneficiaries after your death.

Successfully evaluating and navigating through the wide range of options available will be critical to the overall success of your retirement planning strategy.

Your benefits from private/public sector pension plans may be your most important asset and source of income in retirement. If you have a defined contribution (DC) pension plan, like many employees in the private sector, public sector employees with AVC plans, company directors and the self-employed, you will need to take extra care when assessing your options, due to the wide range of options available.

A DC pension plan provides an accumulated investment value to be used to provide benefits during your retirement. The accumulated investment value is generally not guaranteed at the outset, and can fall as well as rise in value at different times during the accumulation phase when you are working, depending of the level of investment risk you take and depending on investment market conditions.

Page 6

(2) Lump Sum & Annuity Option

Lump sum, based on length of service, of up to 1.5 times “final salary” is withdrawn from the DC

pension plan+

Balance (excluding any AVC funds) must be used to purchase an annuity

This option is not available for self-employed pension plans

(3) Lump Sum & ARF / AMRF Option

Lump sum up to 25% of the value of the DC pension plan is

withdrawn

+ Balance invested in an Approved (Minimum)

Retirement Fund (ARF/AMRF)

(1) Annuity Option

The entire accumulated value in the DC pension plan is paid upfront in

return for a guaranteed regular pension income

payable throughout your life

Under options (2) and (3), the tax treatment of the lump sum is as follows:

k The maximum tax-free lump sum from all pension plans is €200,000.

k The portion of any lump sum amounts (if any) between €200,000 and €575,000 is subject to tax at the standard rate (currently 20%).

k The portion of any lump sum amounts (if any) above €575,000 is subject to tax at the margin-al rate (currently ) and the Universal Social Charge, and PRSI if applicable.

These limits apply to all lump sums paid since 7 December 2005. The applicable tax is deducted at source by the pension plan provider.

All withdrawals from an ARF/AMRF are treated as income for income tax purposes and the value in an ARF and/or in an AMRF can be used to purchase an annuity at any stage.

A withdrawal of % of an ARF value is deemed to occur from the year turning age 61 onwards and is taxed as income.

In the event of death, the value in an ARF/AMRF can pass to a spouse’s ARF/AMRF or to the estate.

A summary of the typical options for taking retirementbenefits from a DC pension plan (not a DB pension plan) is as follows:

A defined benefit (DB) pension plan generally provides a fixed level of benefits at retirement, based on the length of time that you are an active member of the plan, provided that the DB pension plan has the resources to pay the benefits and maintain the payment of the benefits during retirement.

ARF = Approved Retirement FundAMRF = Approved Minimum Retirement Fund

Page 7

Unless certain conditions are met, under Option (3) on the previous page, at least €63,500 must be invested in an Approved Minimum Retirement Fund, with no access to the capital until at least age 75.

An example under Option (3), based on a DC pension plan value of €300,000 at retirement, is as follows:

Tax-free Cash 25%

€75,000

Pension Plan Value

€300,000

Trf. to ARF/AMRF

75%

€225,000

ARF

€161,500

• Withdrawals can be made as required• All withdrawals taxed as income• Withdrawal of % per annum deemed

to occur from the year turning age 61 onwards and taxed as income

• Value in an ARF can be used to purchase an annuity at any stage.

• No access to original capital until age 75• At age 75, AMRF becomes an ARF• Growth on capital can be withdrawn as

income if required• All withdrawals taxed as income• Value in an AMRF can be used to

purchase an annuity at any stage

AMRF

€63,500

ARF = Approved Retirement FundAMRF = Approved Minimum Retirement Fund

Page 8

3 Implementing & Evaluating Your Retirement Plan When you have decided on the options for your retirement plan, the next stage is the imple-mentation of your plan, and evaluation of the plan over time.

You will need to select specific financial products from the vast range of financial products available on the market. Before selecting specific financial products from financial providers, such as banks and life insurance companies, the following should be considered:

k General pedigree, reputation and track record of the financial provider.

k Size and financial strength of the provider.

k Initial and ongoing charges for the financial product, and how these charges compare with competitor products.

k Range of options provided within the financial product, such as the investment options available and access to leading international investment managers.

k Efficiency and effectiveness of the administration and support services for the financial product, and the ease of access to up-to-date information for you, including online ac-cess, mobile applications, etc.

k Tax treatment of the income/gains generated by the financial product.

Over time, you will need to keep your plan on track, and most long-term plans need some al-terations and adjustments to take account of potential changes to your circumstances, chang-es in general market condition, and other changes that can occur from time-to-time.

Page 9

LIFESTYLE EXPENSES CHECKLIST

Self

Annual Amount

Spouse/Partner(if separate costs)Annual Amount

Food & Drink & Household:

Clothing:

Entertainment:

Holidays & Travel:

Electricity:

Gas/Oil:

Telephone:

Water Charges:

TV/Digital/Broadband, etc:

Property Maintenance:

Property Insurance:

Property Tax:

Motor Tax & Insurance:

Motor Fuel & Maintenance:

Club Subscriptions:

Medical/Dental Costs:

Health Insurance:

Other Expenses:

Totals:

Page 10

Need Expert Advicefor Financial Decisions?

Request a Consultation