60

Review 2012 | Protection & Indemnity Marine Insight Aon Risk Solutions

Review 2012 | Protection & Indemnity

Marine Insight Aon Risk Solutions

Contents.

Introduction 1

Mutual Clubs 7

P&I Comparative Data 35

P&I Club Market Reference 41

Specialist Markets 49

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Overall, the marine insurance market is basically flat, according to data from the Aon Global Risk Insight Platform (GRIP®), which provides fact-based insights into over USD80 billion of global flow. The position for the marine mutual protection and indemnity market is more complicated as a result of restrictions on competition under the International Group agreement.

Aon’s 2011 Review assessed the P&I market as being ‘increasingly cautious’ following a downturn in the clubs’ investments in the second half of the year due to a faltering in international markets. Nevertheless, the thirteen P&I clubs that make up the International Group all posted overall surpluses for the 2010/2011 year, aided by what were, in the end, reasonable investment returns with many of the clubs achieving record levels of free reserves.

Introduction.

1

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

One year laterTwelve months on, the lack of any meaningful

recovery in the global economy in particular in Europe

and North America has meant that international

investment markets remain volatile. As a result the

investment return generated across the board by the

13 International Group clubs for the 2011/12 year has

been rather modest, typically ranging between the

3% to 4% mark. The clubs’ expectation for the 2013

policy year is that it will produce a similar level of

investment income.

It is true that over recent years we have seen clubs

accumulate record levels of free reserves. In the past

this may have provided an opportunity for them to

ride out adverse policy years, the imminent advent of

Solvency II makes this a less viable option. Solvency

II’s stringent capital requirements will make it very

difficult for them to use their reserves to offset or

subsidise any unprofitable technical underwriting

results. Therefore, the anticipated continued lack of

any meaningful investment income means the clubs

will have to focus ever more on their technical

underwriting results to ensure they maintain

satisfactory levels of free reserves.

The 2012 P&I renewal saw a relatively consistent

approach on General Increases across all 13

International Group clubs, with the vast majority

opting for 5%. However, as our analysis in this

review highlights, the 2011/12 year has produced

a greater divergence in the overall financial results

of the various clubs when compared to those of

the last couple of years. As a result, at the 2013 P&I

renewal we may well also see greater divergence

across the International Group when it comes 2013

General Increases. The combination of an anticipated

continued lack of meaningful investment return for

the 2012/13 year and ever increasing regulatory

pressure not to erode levels of free reserves, means

there is a very real possibility that those clubs that

produced a negative technical underwriting result in

2011/12 will come under pressure to post General

Increases at the higher end of the scale. We would

not be surprised to see the range of General

Increases posted for the 2013 P&I renewal

ranging from 5% to 12.5%.

Intr

oduc

tion

2

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

3

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Intr

oduc

tion

Are we seeing the early signs of the ‘churn effect’?Much has been made over the years about the

potential impact the ‘churn effect’ may be having on

the P&I market.

Many of the International Group clubs have

experienced considerable growth in their entered

tonnage over the last 10 years following the explosion

in world tonnage during shipping’s boom years.

Where of course the rules under International Group

Agreement restrict competition between P&I clubs,

it is also known that on the few occasions where

‘genuine’ competition is allowed to operate within the

system it can be, and usually is, fierce.

As a result the delta between the premiums of those

vessels that have gone through several renewals

and ‘cycles’ of General Increases and newbuildings

that more recently have entered the P&I system has

steadily increased. However, with the shipping market

continuing to be gripped by the longest downturn

in recent memory, owners are scrapping older, less

effcient and higher premium tonnage.

And while of course it would be too simplistic

to explain any particular club’s recent technical

underwriting and overall financial result purely by

means of the ‘churn effect’, we believe it is important

to continue to keep a close eye on the relationship

between a club’s rate of growth and its technical

underwriting result. A combination of the ‘churn

effect’, lack of investments and technical

underwriting losses has the potential to

prolong and exacerbate any divergence in the

level General Increases beyond the 2013 P&I

renewals.

The challenge of the 2013 Group Reinsurance renewalAt the time of writing, it is a little too early to give

any accurate guidance on what the exact impact the

renewal of the International Group Excess of Loss

reinsurance contract will have on the individual vessel

rating categories. However, following the loss of the

Costa Concordia and significant deterioration in the

estimate of the RENA claim in the final weeks of the

2011/12 year, it is likely the reinsurance markets will

be looking for a sizable rise from the International

Group at renewal.

There may be a desire to pass on a

considerable share of any increase to the

passenger sector, however we believe that

when it comes to allocating any increase in

reinsurance costs to the individual vessel

categories, this should be done in an equitable

manner. One must not forget that twice in the

last 10 years the International Group has applied

significant increases to the reinsurance rates of

4

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

passenger vessels. Furthermore, up to January 2012,

the passenger sector had also performed extremely

well in terms of claims over the same 10 year period,

effectively maintaining a clean record in relation to

the International Group Excess of Loss reinsurance

programme. As a result, over the period passenger

vessels have made a very significant positive

contribution to the overall cost of the International

Group Reinsurance programme and there is merit

in the argument that an incident such as the

Costa Concordia had already been priced into the

reinsurance rates for passenger vessels.

Add to this the fact that the vast majority of the

Concordia’s total claim amount relates to the cost of

the removal of her wreck with other types of vessel

having also produced significant claims in relation to

this risk in recent years, an overly punitive increase in

reinsurance rates for the passenger sector would be

difficult to justify.

Primary war P&I liabilities – A challenge for the passenger shipping industryAt Aon the approaching implementation of the

EU Passenger Liability Regulation (PLR, being the

precursor to the 2002 Protocol to the Athens

Convention, which is not expected to be in force until

at least 2013) due to enter into force on 31 December

2012 is very much at the forefront of our minds.

The certification of terrorism liabilities is a necessary

requirement under the PLR and currently falls outside

of the primary P&I cover granted by the clubs. This

means that a ‘Blue Card’ type certificate will need to

be issued by insurers covering ground up war and

terrorism liabilities.

Aon would have hoped that the solution to

this certification requirement would be for the

International Group P&I clubs to write ground up war

and terrorism liabilities and therefore issue a single

‘Blue Card’ covering both standard P&I and war

P&I liabilities. Through the International Group, the

boards of all P&I clubs were asked to consider this

issue and while a number of clubs agreed with this

proposal, the required 75% majority of clubs under

the International Group Agreement has not been

achieved.

This had left passenger ship operators with a

challenge that the P&I insurance community is now

actively working to solve. At the time of writing there

are a couple of potential solutions being considered:

• Gard already has a vehicle by the name of Safeguard

in place which they utilise for issuing Bunker Blue

Cards for their fixed premium P&I clients. It is now

being investigated if this infrastructure can also be

adapted to also issue the necessary primary P&I war

risks certification as required under the PLR

5

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Intr

oduc

tion

• The UK War Club has confirmed that they will be

certifying passenger vessel members for primary war

P&I liabilities, in line with PLR requirements

• A panel of brokers, including Aon, have been invited

by the International Group to present a commercial

insurance or reinsurance solution. At the time of

writing, these proposals were in the process of being

analysed by the International Group with a further

update expected after the summer

• Those P&I clubs most affected by the PLR may

look at establishing a ‘mini pool’ arrangement for

primary war P&I liabilities allowing them to issue

the necessary certification to satisfy the relevant

authorities

European Commission investigation of The International Group is closed At the time of writing of our 2012 review the

European Commission announced that it would be

closing its review of the International Group which

began in 2010. The International Group states that:

‘Even though the European Commission has decided

to close its investigation, the International Group

plans to make some amendments to the IGA. The

International Group is finalising these and details will

be published in due course.‘

Aon will provide a further update and commentary on

the matter once details are released by means of one

of our regular marine publications.

VigilanceAon’s overall message leading up to the 2013 P&I

renewal and beyond to all parties concerned is one of

vigilance.

Individual clubs need to ensure they maintain a sound

financial position and collectively the International

Group clubs need to secure their position from a

reinsurance point of view.

Owners and operators need to make sure that they

partner with clubs that remain on a sound financial

footing while at the same time being in a position

to offer appropriate solutions to any new risks and

challenges that develop.

The challenge for the P&I community on the

whole leading up to the 2013 renewal is, for

there to continue to be in place a system

that covers all types of owners and operators

for their respective exposures effectively,

efficiently and economically.

Mutual Clubs.

7

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

American Club 8

Britannia 10

Gard 12

Japan Club 14

London Club 16

North of England 18

Shipowners Club 20

Skuld 22

Standard Club 24

Steamship Mutual 26

Swedish Club 28

UK P&I Club 30

West of England 32

Mut

ual C

lubs

Commentary on individual clubs has been supplied by the clubs themselves.

Balance sheet data includes combined P&I and FD&D figures if applicable

8

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

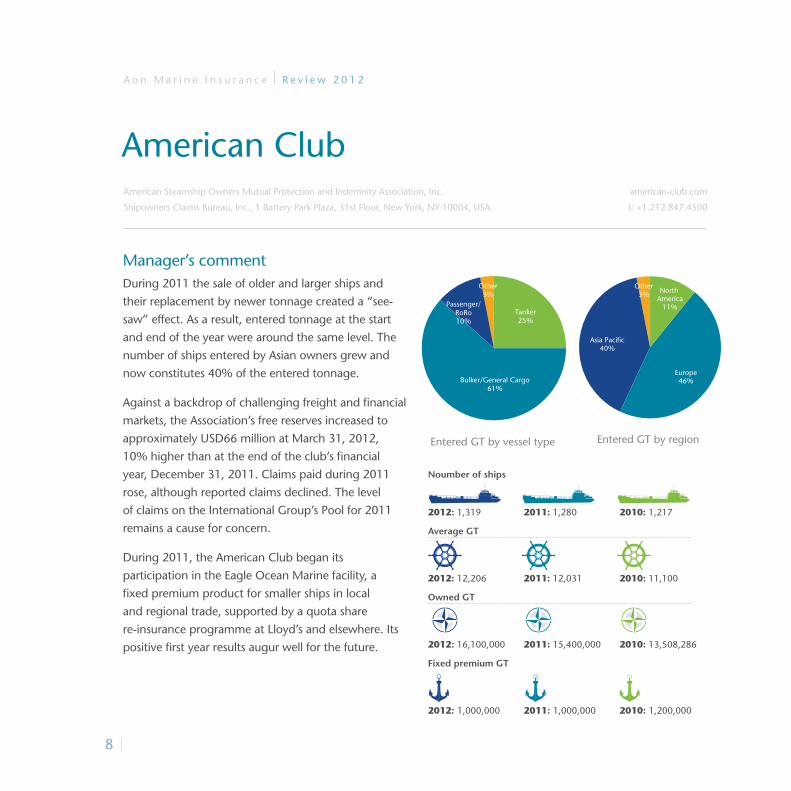

American Club

Manager’s commentDuring 2011 the sale of older and larger ships and

their replacement by newer tonnage created a “see-

saw” effect. As a result, entered tonnage at the start

and end of the year were around the same level. The

number of ships entered by Asian owners grew and

now constitutes 40% of the entered tonnage.

Against a backdrop of challenging freight and financial

markets, the Association’s free reserves increased to

approximately USD66 million at March 31, 2012,

10% higher than at the end of the club’s financial

year, December 31, 2011. Claims paid during 2011

rose, although reported claims declined. The level

of claims on the International Group’s Pool for 2011

remains a cause for concern.

During 2011, the American Club began its

participation in the Eagle Ocean Marine facility, a

fixed premium product for smaller ships in local

and regional trade, supported by a quota share

re-insurance programme at Lloyd’s and elsewhere. Its

positive first year results augur well for the future.

Entered GT by vessel type

Other3%

Passenger/RoRo10%

Bulker/General Cargo61%

Tanker25%

Entered GT by region

Other3%

Asia Pacific40%

Europe46%

North America

11%

American Steamship Owners Mutual Protection and Indemnity Association, Inc.

Shipowners Claims Bureau, Inc., 1 Battery Park Plaza, 31st Floor, New York, NY 10004, USA

american-club.com

t: +1.212.847.4500

Ships and GT

Noumber of ships

2012: 1,319 2011: 1,280 2010: 1,217

Average GT

2012: 12,206 2011: 12,031 2010: 11,100

Owned GT

2012: 16,100,000 2011: 15,400,000 2010: 13,508,286

Fixed premium GT

2012: 1,000,000 2011: 1,000,000 2010: 1,200,000

9

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

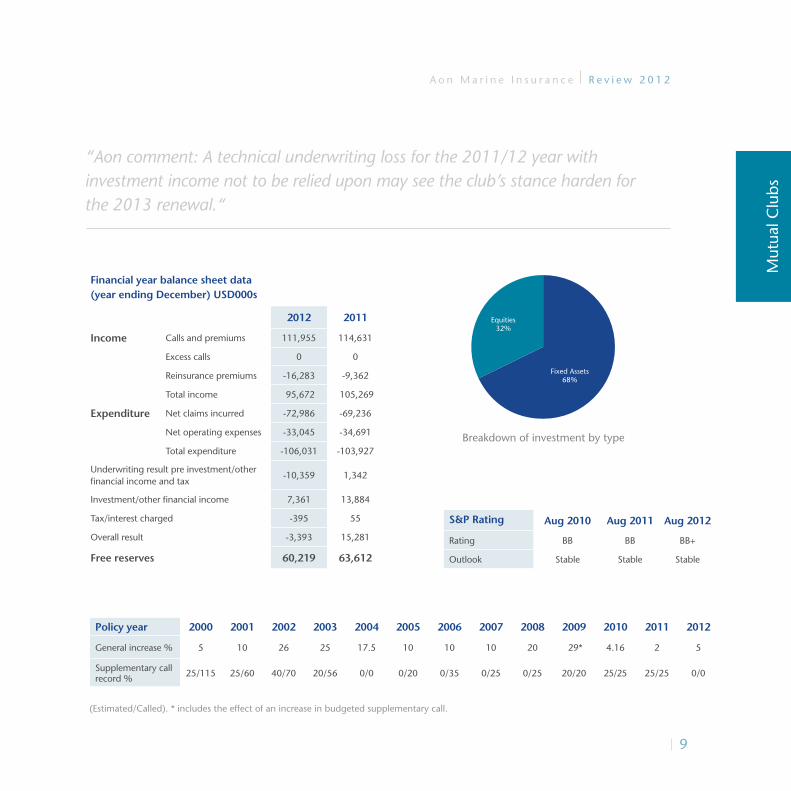

Policy year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

General increase % 5 10 26 25 17.5 10 10 10 20 29* 4.16 2 5

Supplementary call record % 25/115 25/60 40/70 20/56 0/0 0/20 0/35 0/25 0/25 20/20 25/25 25/25 0/0

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating BB BB BB+

Outlook Stable Stable Stable

Financial year balance sheet data (year ending December) USD000s

2012 2011

Income Calls and premiums 111,955 114,631

Excess calls 0 0

Reinsurance premiums -16,283 -9,362

Total income 95,672 105,269

Expenditure Net claims incurred -72,986 -69,236

Net operating expenses -33,045 -34,691

Total expenditure -106,031 -103,927

Underwriting result pre investment/other financial income and tax

-10,359 1,342

Investment/other financial income 7,361 13,884

Tax/interest charged -395 55

Overall result -3,393 15,281

Free reserves 60,219 63,612

“Aon comment: A technical underwriting loss for the 2011/12 year with investment income not to be relied upon may see the club’s stance harden for the 2013 renewal.“

Breakdown of investment by type

Equities32%

Fixed Assets68%

Mut

ual C

lubs

10

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Manager’s commentWe have had a positive underwriting result and an

investment return that was better than expected.

Despite strong growth in owned tonnage – there was

a net gain of 7.5 million GT during the year – calls

and premiums for the year were slightly lower than

2010/11. This reflected reduced chartered tonnage

and a decision to waive half of the outstanding

deferred call for the 2009/10 policy year, amounting

to some USD12.8 million. To achieve such a solid

financial result having waived part of the deferred

call is a real achievement and the result of the

Association’s sound financial strategy.

P&I Claims have continued the upward trend seen

over recent years, and although there have been none

from Britannia ships, the cost of the pool claims has

also been high with two large high profile casualties.

Nevertheless, favourable development of claims in

earlier policy years offset this adverse experience and

the overall cost of P&I claims for the year was only

USD14.2 million higher than last year.

Number of ships

2012: 2,951 2011: 2,820 2010: 2,879

Average GT

2012: 37,648 2011: 36,525 2010: 34,040

Owned GT

2012: 111,100,000 2011: 103,000,000 2010: 98,000,000

Fixed premium GT

2012: 28,900,000 2011: 36,000,000 2010: 40,000,000

Entered GT by vessel type

Other1%

Container25%

Bulker/General Cargo36%

Tanker38%

Entered GT by region

Other1%

Asia Pacific53%

Europe39%

Americas7%

BritanniaThe Britannia Steam Ship Insurance Association Limited

45 King William Street, London, EC4R 9AN, UK

britanniapandi.com

t +44 (0)20 7407 3588

11

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Breakdown of investment by type

Cash19%

Equities16%

Bonds65%

Breakdown of investment by type

Cash19%

Equities16%

Bonds65%

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 0 10 28.8* 15 8.5 7.5 2.5 5 23.8* 12.5 5 5 5

Supplementary call record % 25/25 25/25 40/40 40/40 40/30 40/30 30/30 30/30 40/40 40/32.5 40/40 40/40 40/40

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating A A A

Outlook N/A N/A N/A

Type of rating Pi Pi Pi

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 281,772 298,482

Excess calls 0 0

Reinsurance premiums -63,681 -74,468

Total income 218,091 224,014

Expenditure Net claims incurred -209,634 -201,818

Net operating expenses -29,389 -27,877

Total expenditure -239,023 -229,695

Underwriting result pre investment/other financial income and tax

-20,932 -5,681

Investment/other financial income 39,531 59,611

Tax/interest charged -2,830 -1,115

Overall result 15,769 52,815

Free reserves excluding Boudicca 290,677 274,908

Free reserves including Boudicca 460,977 454,108

Mut

ual C

lubs

“Aon comment: The club continues to justify its reputation as one of the most financial stable clubs in the International Group, underlining their confidence by returning half the deferred call for 2009/10“

12

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Gard

Manager’s commentDespite ongoing low levels of global economic activity,

Gard has delivered strong underwriting results for

the last three years, and for the 2010 policy year P&I

recorded a combined ratio net (CRN) of 99%. However,

the claims picture is beginning to change – with rising

levels driven by increasing cargo values and deteriorating

exchange rate movements.

Gard is, relative to the market, in a very strong position

both in terms of technical underwriting performance

and financial strength, and this is attracting new business

both from existing and new Members. The run up to

the 20 February renewal saw good results, with some

particular highlights. There was a good renewal in Japan

where medium and smaller shipowners have been

looking for alternatives outside the local market, and

who see Gard as a good partner for the future. We also

saw ongoing development in Germany, Greece, France,

North America and Norway.

Assuranceforeningen Gard

Gard AS, Kittelsbuktveien 31, NO-4836 Arendal, Servicebox 600, NO-4809 Arendal, Norway

gard.no

t +47 37 01 91 00

Ships and GT

Number of ships

2012: 5,700 2011: 5,300 2010: 5,100

Average GT

2012: 25,754 2011: 24,528 2010: 21,268

Owned GT

2012: 146,800,000 2011: 130,000,000 2010: 119,100,000

Fixed premium GT

2012: 57,500,000 2011: 51,000,000 2010: 52,000,000

Entered GT by vessel type

MobileOffshore

10%Other14%

Passenger2%

Container17% Bulker/General

Cargo25%

Tanker32%

Entered GT by region

Asia Pacific22%

Europe68%

Americas10%

13

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Mut

ual C

lubs

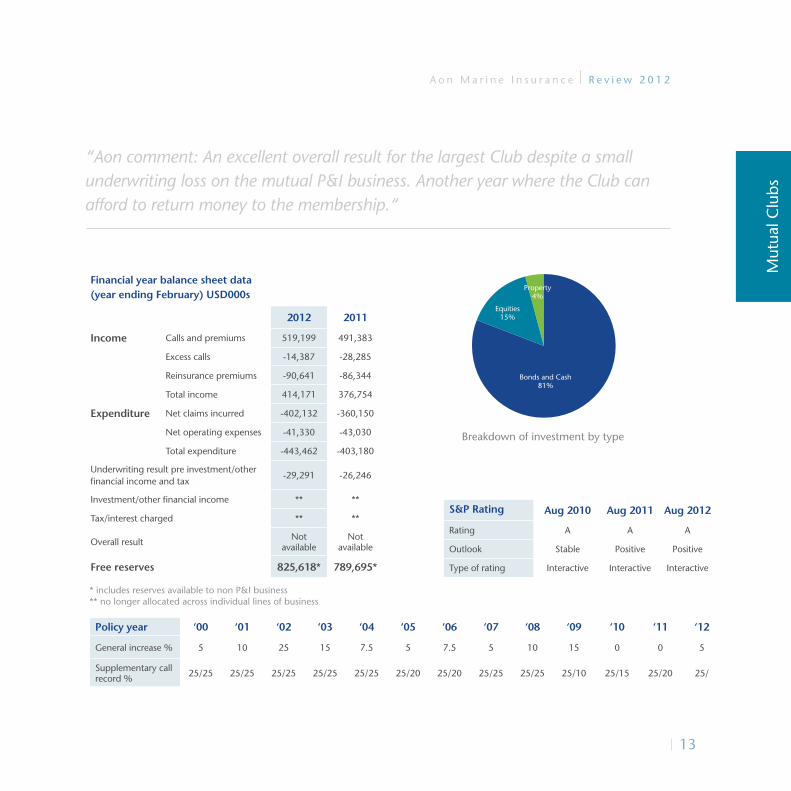

“Aon comment: An excellent overall result for the largest Club despite a small underwriting loss on the mutual P&I business. Another year where the Club can afford to return money to the membership.“

Breakdown of investment by type

Property4%

Equities15%

Bonds and Cash81%

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 5 10 25 15 7.5 5 7.5 5 10 15 0 0 5

Supplementary call record % 25/25 25/25 25/25 25/25 25/25 25/20 25/20 25/25 25/25 25/10 25/15 25/20 25/

* includes reserves available to non P&I business** no longer allocated across individual lines of business

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating A A A

Outlook Stable Positive Positive

Type of rating Interactive Interactive Interactive

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 519,199 491,383

Excess calls -14,387 -28,285

Reinsurance premiums -90,641 -86,344

Total income 414,171 376,754

Expenditure Net claims incurred -402,132 -360,150

Net operating expenses -41,330 -43,030

Total expenditure -443,462 -403,180

Underwriting result pre investment/other financial income and tax

-29,291 -26,246

Investment/other financial income ** **

Tax/interest charged ** **

Overall result Not available

Not available

Free reserves 825,618* 789,695*

14

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Japan Club

Manager’s commentMost of our members experienced tight financial

conditions and plunged into the red due to soaring fuel

costs and value of the yen. In addition, the Great East

Japan Earthquake and floods in Thailand had no small

effect on the continuous poor economic performance

in Japan.

In the circumstance, there was a continuous increase

of newly built vessels entered with the Association.

However, there was a decrease in the number and

tonnage of vessels entered at renewal. The overall

tonnage entered with the Association decreased to 90.49

million gross tons, which represents a decrease of 2.25

million gross tons when compared to the last year.

While the increased tendency of claims has continued,

we have steadily improved our financial strength with

our reserves increasing by USD9 million to USD167

million. In addition, we have earned a BBB credit rating

with a stable outlook from Standard & Poor’s.

Japan Shipowners’ Mutual P&I Association

2-15-14 Nihonbashi-Ningyocho, Chuoh-ku, Tokyo 103-0013, Japan

piclub.or.jp

t +81 33 662 7401

Ships and GT

Number of ships

2012: 2,449 2011: 2,558 2010: 2,699

Average GT

2012: 35,627 2011: 34,805 2010: 32,697

Owned GT

2012: 87,250,000 2011: 89,030,000 2010: 88,250,000

Fixed premium GT

2012: 2,610,000 2011: 2,890,000 2010: 3,300,000

Entered GT by vessel type

Other18%

Container10%

Bulker/General Cargo58%

Tanker15%

Entered GT by region

Americas65%

Europe3%

Asia Pacific19%

Others13%

15

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Mut

ual C

lubs

“Aon comment: A difficult year saw the Japan Club ask members for a 10% unbudgeted Supplementary Call. The Club also announced plans for a UK Club style subordinated loan. “

Breakdown of investment by type

Fixed Income,44%

Bonds 32%

Cash24%

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 0 10 0 10 0 0 0 10 20 12.5 12.5 10 3

Supplementary call record % 20/20 20/10 20/20 30/10 30/30 30/30 30/60 30/30 30/30 40/40 40/50 40/40 40/40

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating BBB BBB BBB

Outlook n/a n/a Stable

Type of rating pi pi Interactive

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 259,865 281,753

Excess calls 0 0

Reinsurance premiums -46,228 -49,652

Total income 213,637 232,101

Expenditure Net claims incurred -180,390 -183,179

Net operating expenses -27,505 -27,439

Total expenditure -207,895 -210,618

Underwriting result pre investment/other financial income and tax

5,742 21,483

Investment/other financial income -1,877 -13,375

Tax/interest charged -6,027 -638

Overall result 3,865 8,108

Free reserves 166,949 157,827

16

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

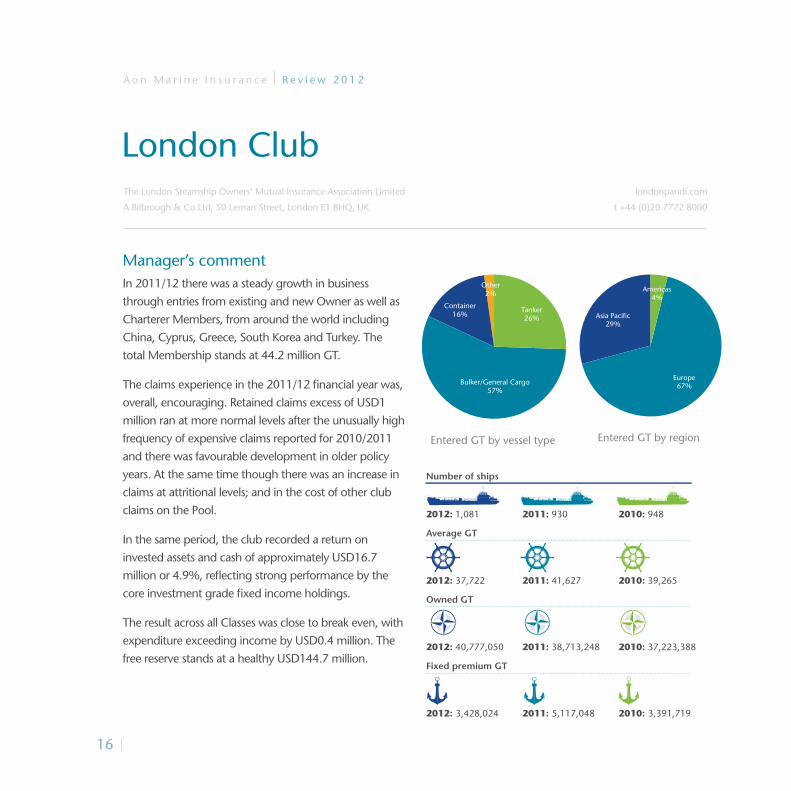

London Club

Manager’s commentIn 2011/12 there was a steady growth in business

through entries from existing and new Owner as well as

Charterer Members, from around the world including

China, Cyprus, Greece, South Korea and Turkey. The

total Membership stands at 44.2 million GT.

The claims experience in the 2011/12 financial year was,

overall, encouraging. Retained claims excess of USD1

million ran at more normal levels after the unusually high

frequency of expensive claims reported for 2010/2011

and there was favourable development in older policy

years. At the same time though there was an increase in

claims at attritional levels; and in the cost of other club

claims on the Pool.

In the same period, the club recorded a return on

invested assets and cash of approximately USD16.7

million or 4.9%, reflecting strong performance by the

core investment grade fixed income holdings.

The result across all Classes was close to break even, with

expenditure exceeding income by USD0.4 million. The

free reserve stands at a healthy USD144.7 million.

Number of ships

2012: 1,081 2011: 930 2010: 948

Average GT

2012: 37,722 2011: 41,627 2010: 39,265

Owned GT

2012: 40,777,050 2011: 38,713,248 2010: 37,223,388

Fixed premium GT

2012: 3,428,024 2011: 5,117,048 2010: 3,391,719

Entered GT by vessel type

Other2%

Container16%

Bulker/General Cargo57%

Tanker26%

The London Steamship Owners’ Mutual Insurance Association Limited

A Bilbrough & Co Ltd, 50 Leman Street, London E1 8HQ, UK

londonpandi.com

t +44 (0)20 7772 8000

Entered GT by region

Asia Pacific29%

Europe67%

Americas4%

17

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Breakdown of investment by type

Other2%

Equities9%

Cash21%

Fixed Income69%

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 5 10 27.5 25 15 12.5 12.5 7.5 17.5 15 5 5 5

Supplementary call record % 40/40 40/40 40/40 40/40 40/40 40/40 40/89 40/89 40/75 40/40 0/0 0/0 0/0

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating BBB BBB BBB

Outlook Stable Stable Stable

Type of rating Pi Pi Pi

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 109,190 113,224

Excess calls 0 0

Reinsurance premiums -21,216 -22,549

Total income 87,974 90,675

Expenditure Net claims incurred -93,338 -101,118

Net operating expenses -11,367 -11,021

Total expenditure -104,705 -112,139

Underwriting result pre investment/other financial income and tax

-16,731 -21,464

Investment/other financial income 16,484 25,199

Tax/interest charged -154 -91

Overall result -401 3,644

Free reserves 144,669 145,070

Mut

ual C

lubs

“Aon comment: An improved underwriting performance resulting primarily from a good claims year. Work still needs to be done to improve the technical underwriting result further.“

18

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

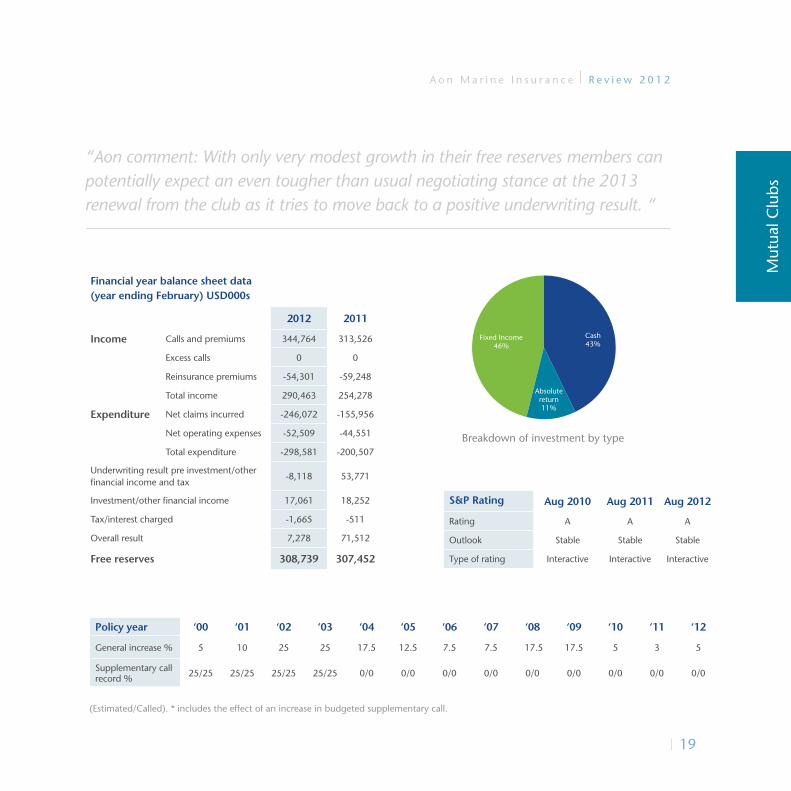

North of England

Manager’s CommentNorth produced an overall surplus of USD1.6 million,

leading to a third consecutive annual increase in free

reserves to USD314.0 million. The combined ratio was

only slightly above breakeven at 101.8%, and the club

continues to reserve all claims at a very conservative 95%

confidence level.

The investment return for the year was 2.76% and

although satisfactory in view of the low risk nature of the

investment portfolio, this was still lower than originally

anticipated. In addition the club’s office headquarters in

Newcastle were subject to a building revaluation charge

of USD7.5 million, which reflects the current weak

commercial property market in the UK.

During the year to 20 February 2012 and subsequently,

the club’s membership has continued to grow steadily

and owned tonnage has now increased to 125 million

GT, and together with estimated chartered entries of 45

million GT, this takes the total entered tonnage in the

club to around 170 million GT.

North of England P&I Association Limited

The Quayside, Newcastle Upon Tyne, NE1 3DU, UK

nepia.com

t +44 (0)191 232 5221

Entered GT by vessel type

Other12%

Passenger1%

Container23%

Bulker/General Cargo34%

Tanker30%

Entered GT by region

Other12%

Asia Pacific26%

Europe49%

Americas13%

Number of ships

2012: 4,000 2011: 3,665 2010: 3,075

Average GT

2012: 30,750 2011: 28,377 2010: 26,992

Owned GT

2012: 123,000,000 2011: 104,000,000 2010: 83,000,000

Fixed premium GT

2012: 40,000,000 2011: 39,000,000 2010: 28,000,000

19

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 5 10 25 25 17.5 12.5 7.5 7.5 17.5 17.5 5 3 5

Supplementary call record % 25/25 25/25 25/25 25/25 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating A A A

Outlook Stable Stable Stable

Type of rating Interactive Interactive Interactive

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 344,764 313,526

Excess calls 0 0

Reinsurance premiums -54,301 -59,248

Total income 290,463 254,278

Expenditure Net claims incurred -246,072 -155,956

Net operating expenses -52,509 -44,551

Total expenditure -298,581 -200,507

Underwriting result pre investment/other financial income and tax

-8,118 53,771

Investment/other financial income 17,061 18,252

Tax/interest charged -1,665 -511

Overall result 7,278 71,512

Free reserves 308,739 307,452

Mut

ual C

lubs

“Aon comment: With only very modest growth in their free reserves members can potentially expect an even tougher than usual negotiating stance at the 2013 renewal from the club as it tries to move back to a positive underwriting result. “

Breakdown of investment by type

Fixed Income46%

Absolutereturn11%

Cash43%

20

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Entered GT by region

Other18.33%

Asia Pacific50.78%

Europe18.81%

Americas12.07%

Shipowners Club

Manager’s CommentThe Shipowners’ Club produced a strong set of results

with increased gross written premium at USD209.7

million, up 6.5% on last year. Growth was the underlying

theme throughout, with the total number of Members

up by 5.3% to 5,922, entered vessels up 8.1% to

31,341, and gross tonnage rising 11.2% to 19.8 million.

Shipowners’ financial security was also reinforced by a

growth in free reserves to USD234.5 million, resulting in

total funds of USD502 million, up 16.5% on the previous

year.

Shipowners was also pleased with its strong technical

performance. The overall surplus of USD46.5 million

consisted of an underwriting surplus up 13% on the

preceding year, at USD28.6 million and an investment

return of USD18.9 million, before taxation. The

underwriting result represented a combined ratio of

84.9%, in line with the previous year, and the investment

result produced a 4.85% return on capital.

The Shipowners’ Mutual Protection and Indemnity Association

St Clare House, 30-33 Minories, London EC3N 1BP, UK

shipownersclub.com

t +44 (0)20 7488 0911

Entered GT by vessel type

Yachts3.5%

Offshore14.6%

Barges18.8%

Harbour30%

Fishing12.2%

Passenger11.8%

Bulker/General Cargo4.9%

Tanker4.2%

Ships and GT

Number of ships

2012: 31,341 2011: 30,602 2010: 28,227

Average GT

2012: 632 2011: 593 2010: 588

Owned GT

2012: 19,792,065 2011: 18,151,077 2010: 16,583,272

Fixed premium GT

2012: N/A 2011: N/A 2010: N/A

21

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Breakdown of investment by type

Fixed interest investments

75%

Equity investments

25%

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 0 0 20 15 0 0 0 5 15 10 5 0 0

Supplementary call record % 25/0 25/0 25/0 25/0 25/0 25/0 25/0 25/0 25/0 10/0 10/0 10/0 10/0

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating BBB BBB BBB

Outlook N/A N/A N/A

Type of rating Pi Pi Pi

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 209,689 196,815

Excess calls 0 0

Reinsurance premiums -19,927 -22,998

Total income 189,762 173,817

Expenditure Net claims incurred -118,172 -107,150

Net operating expenses -43,030 -40,510

Total expenditure -161,202 -147,660

Underwriting result pre investment/other financial income and tax

28,560 26,157

Investment/other financial income 18,903 27,648

Tax/interest charged -917 -931

Overall result 46,546 52,874

Free reserves 234,460 187,914

Mut

ual C

lubs“Aon comment: Another excellent result for the small ship specialists. Expect to see

the S&P ‘A’ rating return soon.“

22

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Skuld

Manager’s commentSkuld is a strong world leading marine insurance

provider with focus on innovation, financial strength

and talented staff. For 9 consecutive years, Skuld

is the only P&I Club with a positive underwriting

result – creating reliability and predictability for the

members and clients. No general increase and no

supplementary calls.

Through diversification Skuld is able to provide all

products in the marine insurance: Protection and

Indemnity for shipowners, liability covers for charterers,

defence insurance and a wide range of additional covers.

The specialized team in Skuld Offshore provides contract

reviews and bespoke covers for offshore liability. Skuld

1897, a syndicate at Lloyd’s, offers marine and energy

covers, as well as cargo and additional marine liabilities.

Worldwide offices cover virtually every time zone

and are manned by dedicated and professional staff

representing over 20 nationalities and thus many cultural

backgrounds as well as a wide variety of legal, nautical

and technical expertise.

Assuranceforeningen SKULD

(Gjensidig), Ruseløkkvn. 26, 0251 Oslo, Norway

skuld.com

t +47 22 00 22 00

Entered GT by vessel type

Other2%

Passenger2%

Container10%

Bulker/General Cargo40%

Tanker45%

Entered GT by vessel type

Other2%

Passenger2%

Container10%

Bulker/General Cargo40%

Tanker45%

Entered GT by region

Other2%

Asia Pacific20%

Europe68%

Americas11%

Number of ships

2012: 3,792 2011: 3,688 2010: 3,860

Average GT

2012: 18,434 2011: 17,226 2010: 14,264

Owned GT

2012: 69,900,000 2011: 63,530,385 2010: 55,060,102

Fixed premium GT

2012: N/A 2011: N/A 2010: 42,389,547

23

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Breakdown of investment by type

Alternative investments

3%

Commodities1%

Equities15%

Fixed income72%

Cash9%

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 0 10 30 25 15 7.5 5 2.5 7.5 15 5 N/A N/A

Supplementary call record % 20/65 20/20 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating A- A- A

Outlook Stable Positive Stable

Type of rating Interactive Interactive Interactive

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 299,971 272,429

Excess calls 0 0

Reinsurance premiums -38,482 -32,312

Total income 261,489 240,117

Expenditure Net claims incurred -193,722 -165,054

Net operating expenses -56,109 -44,455

Total expenditure -249,831 -209,509

Underwriting result pre investment/other financial income and tax

11,658 30,608

Investment/other financial income 14,802 37,043

Tax/interest charged -2,106 -3,029

Overall result 24,353 64,622

Free reserves 291,429 266,436

Mut

ual C

lubs“Aon comment: Another solid overall financial result for the club. Skuld’s ability to

consistently deliver positive technical underwriting surpluses is very noteworthy“

24

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Entered GT by region

Other10%

Asia Pacific22%

Europe52%

Americas16%

Standard Club

Manager’s commentThis has been both an eventful year and one of

consolidation. The Standard Club remains very well

placed to continue to provide members with the service

and security that they need.

Although the underwriting has been challenging, we are

reporting another overall surplus, so that the financial

security that the club provides to its members is stronger

than ever.

The year also saw an internal consolidation of the club

into fewer underwriting entities, a change that has

enabled more effective use of capital and reduced

compliance costs.

Number of ships

2012: 7,511 2011: 7,257 2010: 6,890

Average GT

2012: 17,080 2011: 16,537 2010: 15,084

Owned GT

2012: 96,000,000 2011: 86,000,000 2010: 76,000,000

Fixed premium GT

2012: 29,000,000 2011: 37,000,000 2010: 39,000,000

The Standard Steamship Owners’ P&I Association (Bermuda) Limited

12/13 Essex Street, London WC2R 3AA, UK

standard-club.com

t +44 (0)20 3320 8888

Entered GT by vessel type

Tanker28%

Passenger & Ferry

6%Other3%

Offshore13%

Dry Bulk24%

Container & General Cargo

27%

25

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Breakdown of investment by type

Cash14%

Gold1%

Alternativeassets3%

Equities17%

Bonds64%

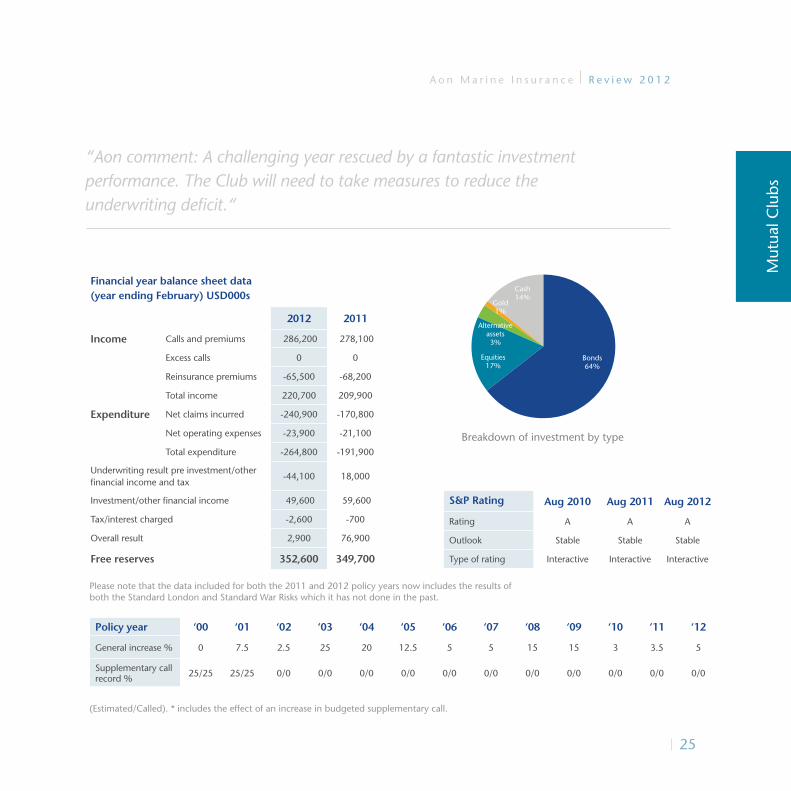

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 0 7.5 2.5 25 20 12.5 5 5 15 15 3 3.5 5

Supplementary call record % 25/25 25/25 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating A A A

Outlook Stable Stable Stable

Type of rating Interactive Interactive Interactive

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 286,200 278,100

Excess calls 0 0

Reinsurance premiums -65,500 -68,200

Total income 220,700 209,900

Expenditure Net claims incurred -240,900 -170,800

Net operating expenses -23,900 -21,100

Total expenditure -264,800 -191,900

Underwriting result pre investment/other financial income and tax

-44,100 18,000

Investment/other financial income 49,600 59,600

Tax/interest charged -2,600 -700

Overall result 2,900 76,900

Free reserves 352,600 349,700

Mut

ual C

lubs

“Aon comment: A challenging year rescued by a fantastic investment performance. The Club will need to take measures to reduce the underwriting deficit.“

Please note that the data included for both the 2011 and 2012 policy years now includes the results of both the Standard London and Standard War Risks which it has not done in the past.

26

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Entered GT by region

Other7%

Asia Pacific38%

Europe31%

Americas24%

Steamship Mutual

Manager’s commentIn the difficult economic environment the financial

performance of the club over the past year has been

satisfactory. The capital position remains strong and

stable, albeit with a marginal reduction in free reserves,

some 2%, mainly due to a small deterioration in back

year estimates.

Tonnage increased to a total entered tonnage of 92

million. A very few fleets left or reduced their entry at

the renewal, mostly because agreement could not be

reached when the record suggested that an increase in

premium was necessary.

It is always unfortunate to see business leaving the

club but sound underwriting and equity between the

membership must have priority.

Number of ships

2012: 9,327 2011: 9,035 2010: 7,780

Average GT

2012: 6,712 2011: 6,397 2010: 6,787

Owned GT

2012: 62,600,000 2011: 57,800,000 2010: 52,800,000

Fixed premium GT

2012: 30,000,000 2011: 34,000,000 2010: 30,000,000

The Steamship Mutual Underwriting Association (Bermuda) Limited

Aquatical House, 39 Bell Lane, London E1 7LU, UK

simsl.com

t +44 (0)20 7247 5490

Entered GT by vessel type

Other4%

Passenger13%

Container17%

Bulker/General Cargo45%

Tanker22%

27

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Breakdown of investment by type

Equities3%

Property1%

AlternativeInvestments

7%

CorporateBonds15%

Cash & Deposits

17%

Government Bonds56%

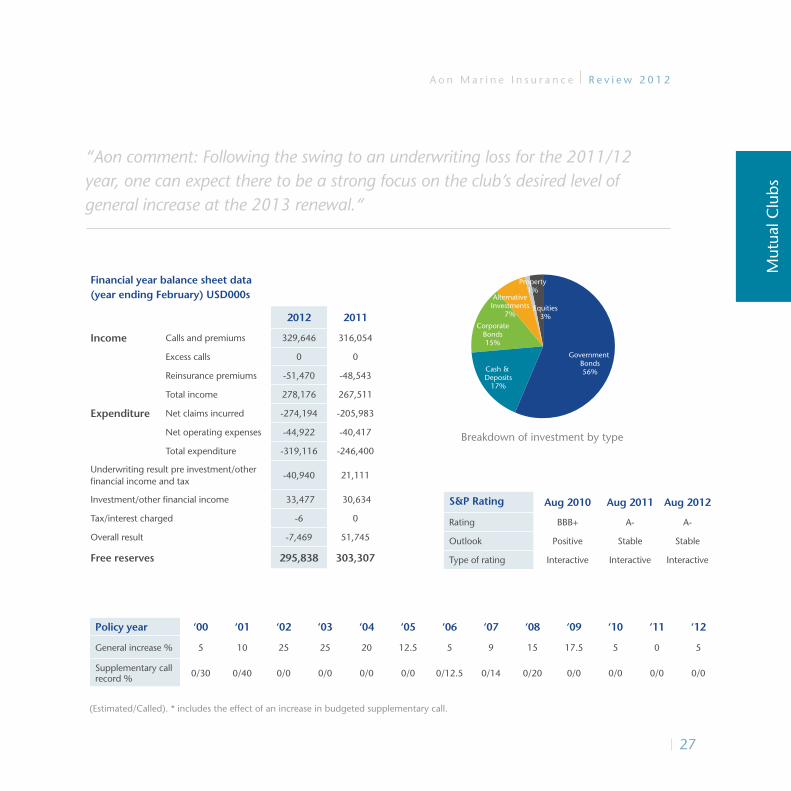

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 5 10 25 25 20 12.5 5 9 15 17.5 5 0 5

Supplementary call record % 0/30 0/40 0/0 0/0 0/0 0/0 0/12.5 0/14 0/20 0/0 0/0 0/0 0/0

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating BBB+ A- A-

Outlook Positive Stable Stable

Type of rating Interactive Interactive Interactive

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 329,646 316,054

Excess calls 0 0

Reinsurance premiums -51,470 -48,543

Total income 278,176 267,511

Expenditure Net claims incurred -274,194 -205,983

Net operating expenses -44,922 -40,417

Total expenditure -319,116 -246,400

Underwriting result pre investment/other financial income and tax

-40,940 21,111

Investment/other financial income 33,477 30,634

Tax/interest charged -6 0

Overall result -7,469 51,745

Free reserves 295,838 303,307

Mut

ual C

lubs

“Aon comment: Following the swing to an underwriting loss for the 2011/12 year, one can expect there to be a strong focus on the club’s desired level of general increase at the 2013 renewal.“

28

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Entered GT by region

Other2%

Asia Pacific34%

Europe64%

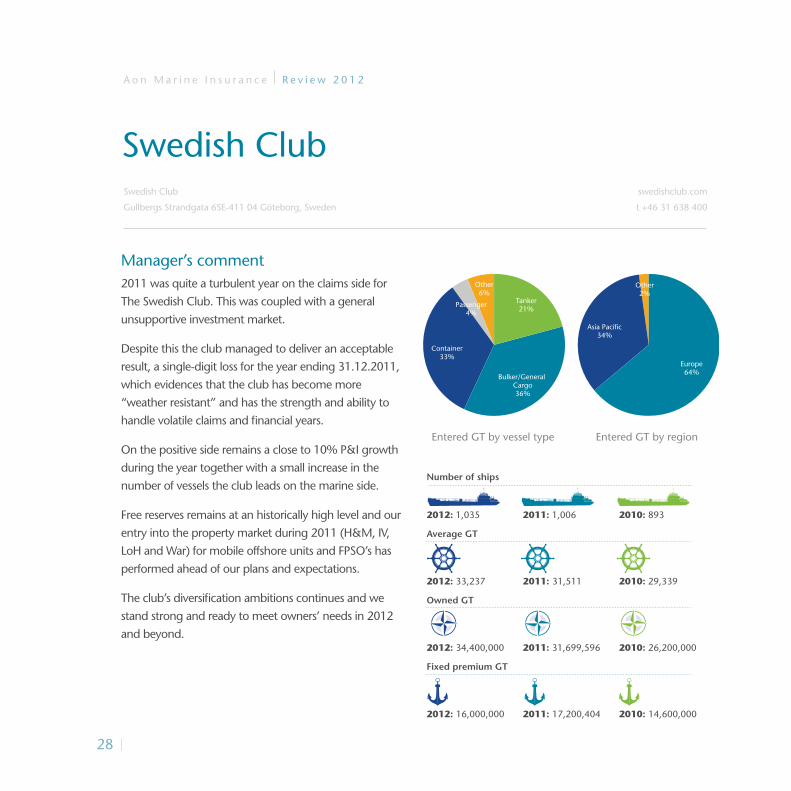

Manager’s comment2011 was quite a turbulent year on the claims side for

The Swedish Club. This was coupled with a general

unsupportive investment market.

Despite this the club managed to deliver an acceptable

result, a single-digit loss for the year ending 31.12.2011,

which evidences that the club has become more

“weather resistant” and has the strength and ability to

handle volatile claims and financial years.

On the positive side remains a close to 10% P&I growth

during the year together with a small increase in the

number of vessels the club leads on the marine side.

Free reserves remains at an historically high level and our

entry into the property market during 2011 (H&M, IV,

LoH and War) for mobile offshore units and FPSO’s has

performed ahead of our plans and expectations.

The club’s diversification ambitions continues and we

stand strong and ready to meet owners’ needs in 2012

and beyond.

Swedish Club

Number of ships

2012: 1,035 2011: 1,006 2010: 893

Average GT

2012: 33,237 2011: 31,511 2010: 29,339

Owned GT

2012: 34,400,000 2011: 31,699,596 2010: 26,200,000

Fixed premium GT

2012: 16,000,000 2011: 17,200,404 2010: 14,600,000

Swedish Club

Gullbergs Strandgata 6SE-411 04 Göteborg, Sweden

swedishclub.com

t +46 31 638 400

Entered GT by vessel type

Other6%

Passenger4%

Container33%

Bulker/General Cargo36%

Tanker21%

29

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Breakdown of investment by type

Equities20%

Bonds and Cash80%

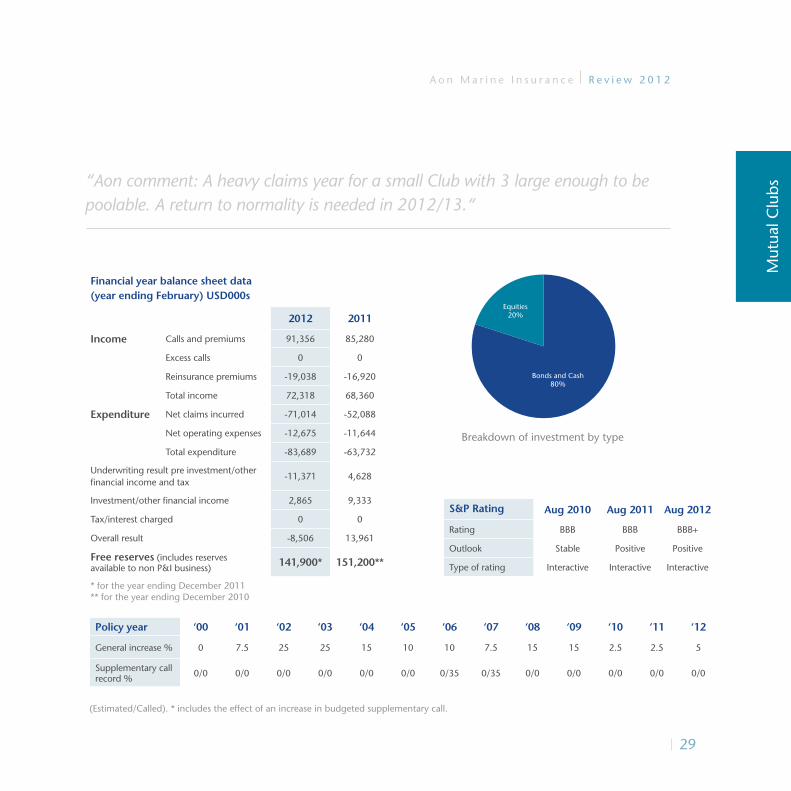

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 0 7.5 25 25 15 10 10 7.5 15 15 2.5 2.5 5

Supplementary call record % 0/0 0/0 0/0 0/0 0/0 0/0 0/35 0/35 0/0 0/0 0/0 0/0 0/0

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating BBB BBB BBB+

Outlook Stable Positive Positive

Type of rating Interactive Interactive Interactive

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 91,356 85,280

Excess calls 0 0

Reinsurance premiums -19,038 -16,920

Total income 72,318 68,360

Expenditure Net claims incurred -71,014 -52,088

Net operating expenses -12,675 -11,644

Total expenditure -83,689 -63,732

Underwriting result pre investment/other financial income and tax

-11,371 4,628

Investment/other financial income 2,865 9,333

Tax/interest charged 0 0

Overall result -8,506 13,961

Free reserves (includes reserves available to non P&I business) 141,900* 151,200**

* for the year ending December 2011 ** for the year ending December 2010

Mut

ual C

lubs“Aon comment: A heavy claims year for a small Club with 3 large enough to be

poolable. A return to normality is needed in 2012/13.“

30

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Entered GT by region

Asia Pacific37%

Europe51%

Americas12%

UK P&I Club

Manager’s comment

Good result in difficult times

This year we report another operating surplus, USD11

million, further increasing the club’s free reserves and

capital to USD486 million. This level of capital puts our

club’s financial strength at the top level of its peer group

in the P&I sector.

Continuing improvement in the claims reserves on the

more recent policy years and early indications that 2011

will be a low claims year contrasts with results elsewhere

in the market adversely affected by an increase in claims

and volatile investment returns.

Our Board is determined that the UK Club should

be the leading shipowner controlled provider of P&I

insurance and other services. That commitment is the

guiding principle for everything we do. Whether it is the

competitive insurance and services we provide to our

members worldwide or the strengthening of the club’s

capital position which has become absolutely essential

for any insurance provider in the modern regulatory

environment.

The United Kingdom Mutual Ship Assurance Association (Bermuda) Limited

Thomas Miller P&I Ltd, 90 Fenchurch Street, London, EC3M 4ST, UK

ukpandi.com

t +44 (0)20 7283 4646

Entered GT by vessel type

Other18%

Passenger4%

Container14%

Bulker/General Cargo34%

Tanker30%

Number of ships

2012: 3,346 2011: 3,400 2010: 3,416

Average GT

2012: 33,473 2011: 30,882 2010: 31,177

Owned GT

2012: 112,000,000 2011: 105,000,000 2010: 106,500,000

Fixed premium GT

2012: 80,000,000 2011: 80,000,000 2010: 70,000,000

31

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Breakdown of investment by type

Absolute return funds

11.15%Equities10.31%

Cash11.15%

Fixed interest68.31%

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 0 7.5 20 25 17.5 12.5 12.5 7.5 17.5 12.5 5 5 3

Supplementary call record % 0/0 0/0 0/0 0/0 0/0 0/0 0/20 0/25 0/20 0/0 0/0 0/0 0/0

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating A- A- A-

Outlook Stable Stable Stable

Type of rating Interactive Interactive Interactive

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 360,540 364,651

Excess calls 0 140

Reinsurance premiums -70,685 -70,218

Total income 289,855 294,573

Expenditure Net claims incurred -237,754 -250,428

Net operating expenses -42,109 -40,621

Total expenditure -279,863 -291,049

Underwriting result pre investment/other financial income and tax

9,992 3,524

Investment/other financial income 10,214 69,509

Tax/interest charged -9,627 -10,416

Overall result 10,939 62,617

Free reserves including Hybrid capital 485,777 477,855

Free reserves excluding Hybrid capital 386,459 378,993

Mut

ual C

lubs“Aon comment: The growth in free reserves fuelled by a positive underwriting

result puts the club in a strong position for the 2013 renewal. “

32

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Entered GT by region

Other8%

Asia Pacific39%

Europe46%

Americas7%

West of England

Manager’s commentThe highlights of the club’s financial performance to

20 February 2012 are the lowest level of claims from

the club’s own members for many years, a free reserve

of USD179.3 million – broadly unchanged from that

of a year ago and a significantly lower combined ratio

of 108.7%. Together they represent a sound platform

for steady growth in the club’s capital position and

overall financial strength in the longer term.

Measures taken at the start of last year to reduce

the club’s exposure to members’ claims through

more selective underwriting and continuation of the

enhanced claims reserving processes established at

the end of 2009, are now feeding through into the

club’s overall financial performance.

External factors in the form of unusually large Pool

claims reported by other clubs for 2011 and volatile

financial markets resulting in a lower than usual

investment return prevented growth in the club’s

free reserve.

Number of ships

2012: 3,030 2011: 3,091 2010: 3,458

Average GT

2012: 16,799 2011: 15,852 2010: 15,124

Owned GT

2012: 50,900,000 2011: 49,000,000 2010: 52,300,000

Fixed premium GT

2012: 15,000,000 2011: 20,000,000 2010: 16,500,000

Number of ships

2012: 3,030 2011: 3,091 2010: 3,458

Average GT

2012: 16,799 2011: 15,852 2010: 15,124

Owned GT

2012: 50,900,000 2011: 49,000,000 2010: 52,300,000

Fixed premium GT

2012: 15,000,000 2011: 20,000,000 2010: 16,500,000

West of England Ship Owners Mutual Insurance Association (Luxembourg)

Tower Bridge Court, 226 Tower Bridge Road, London, SE1 2UP, UK

westpandi.com

t +44 (0)20 7716 6000

Entered GT by vessel type

Other2%

Passenger3%

Container17%

Bulker/General Cargo53%

Tanker25%

33

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Breakdown of investment by type

Equities15%

Absolute Return11%

Fixed income57%

Cash17%

Policy year ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

General increase % 5 5 10 25 15 12.5 12.5 5 15 19.2* 5 5 5

Supplementary call record % 50/50 20/20 20/20 20/20 20/35 20/35 20/55 20/55 20/65 30/30 30/30 30/30 30/30

(Estimated/Called). * includes the effect of an increase in budgeted supplementary call.

S&P Rating Aug 2010 Aug 2011 Aug 2012

Rating BBB BBB BB

Outlook N/A N/A N/A

Type of rating Pi Pi Pi

Financial year balance sheet data (year ending February) USD000s

2012 2011

Income Calls and premiums 211,551 243,167

Excess calls 0 0

Reinsurance premiums -33,008 -39,831

Total income 178,543 203,336

Expenditure Net claims incurred -157,595 -204,473

Net operating expenses -36,492 -35,532

Total expenditure -194,087 -240,005

Underwriting result pre investment/other financial income and tax

-15,544 -36,669

Investment/other financial income 11,250 54,307

Tax/interest charged 986 -4,083

Overall result -3,308 13,555

Free reserves 179,356 182,664

Mut

ual C

lubs

“Aon comment: The Club continues to improve the underwriting performance showing they are heading in the right direction. The improvements need to continue going forward.“

P&I Comparative Data.

35

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Free Reserves/Net Call Income 37

Net Claims/Net Call Income 37

Underwriting Result/Net Call Income 38

Overall Result/Net Call Income 38

Gross Call/GT 39

Net Claims/GT 39

P&I C

ompa

rativ

e D

ata

36

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Traditionally the popular method of comparing the

financial health of clubs has been to generate key

performance indicators around GT, call income, claims

and reserves. Although we have used GT as part of

our analysis, we do not consider it the most useful

constant.

A club with a high USD per GT ratio is not necessarily

an expensive or conservative club; one with a low

figure, likewise, is not necessarily competitive as GT

does not give any allowance for the type of vessels

within the club nor the individual retentions or loss

records they may carry. We have always said that

since premium is the underwriter’s assessment of risk

it is more valid to use annual call income to generate

comparative analytical data. Over the last few years

a number of clubs have made excess calls to cover a

shortfall in their finances and a couple of others have

called less than their originally estimated deferred calls.

Variations from the estimated total call tend to be rare

and give a distorted view of a club’s financial position.

We therefore do not include these adjustments in

analysis and use the original estimated total call for

comparisons. Conversely, free reserves will continue to

benefit year on year from the effects of an excess call,

and therefore have not been adjusted.

Our analysis is based on financial year dataFree Reserves/Net Call Income

Free reserves shown as a percentage of net annual

call income.

Net Claims/Net Call Income

Total incurred losses shown as a percentage of net

annual call income.

Underwriting Result/Net Call Income

Underwriting profit/loss calculated before investment

and other financial income has been taken into

account shown as a percentage of net call income.

Overall Result/Net Call Income

Underwriting profit/loss after investment and other

financial income has been taken into account shown

as a percentage of net call income.

Gross Call/GT

Total gross call income shown as USD per total GT

entered for owners’ risks.

Net Claims/GT

Total incurred losses shown as USD per total GT

entered for owners’ risks.

Notes1. Total incurred losses include paid and outstanding claims, provision

for incurred but not reported losses, net of reinsurance recoveries.2. Net annual call income excludes the cost of reinsurance and the

product of an excess call.3. UK Club free reserves include ‘Hybrid’ capital.4. The reduction in Gard’s 2010/11and 2011/12 deferred call has

been reinstated.

P&I Comparative Data

5. American Club’s ratios are in respect of the years 12 months at 1st December 2010 and 2011.

37

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

P&I C

ompa

rativ

e D

ata

Free reserves/Net call income

Amer

ican

Brita

nnia

Gard

Japan

Lond

onNor

th

Shipo

wners

Skuld

Stan

dard

Stea

msh

ip

Swed

ish UKW

est

2012 2011

0

50

100

150

200

250

Amer

ican

Brita

nnia

Gard

Japan

Lond

onNor

th

Shipo

wners

Skuld

Stan

dard

Stea

msh

ip

Swed

ish UKW

est

2012 2011

0

50

100

150

200

250

Net claims/Net call income

Amer

ican

Brita

nnia

Gard

Japan

Lond

onNor

th

Shipo

wners

Skuld

Stan

dard

Stea

msh

ip

Swed

ish UKW

est

2012 2011

0

50

100

150

Net call income reflects the club’s assessment of current and future risk.

Free reserves are the club’s safety net if past and future liabilities exceed the club’s assessment.

The greater the ratio between free reserve and net call income the greater the club’s safety net. This ratio should be viewed in conjunction with chart ‘Underwriting result/net call income’ as the more positive the underwriting result the less critical the free reserve to net call ratio.

Net call income reflects the club’s assessment of current and future risk.

Net claims are the club’s actual current exposure (and a guide to future exposure).

The lower the ratio between net claims and net call income the more favourable the underlying underwriting position.

38

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Underwriting result/Net call income

Amer

ican

Brita

nnia

Gard

Japan

Lond

onNor

th

Shipo

wners

Skuld

Stan

dard

Stea

msh

ip

Swed

ish UKW

est

2012 2011

-25

-20

-15

-10

-5

0

5

10

15

20

25

Overall result/Net call income

Amer

ican

Brita

nnia

Gard

Japan

Lond

onNor

th

Shipo

wners

Skuld

Stan

dard

Stea

msh

ip

Swed

ish UKW

est

2012 2011

-15

-10

-5

0

5

10

15

20

25

30

35

40

Net call income reflects the club’s assessment of current and future risk.

Underwriting result is the actual product of the current net claims and operating costs to net call income.

The greater the ratio between underwriting result and net call income the greater the likelihood of a surplus.

Net call income reflects the club’s assessment of current and future risk.

Overall result is the actual product of the current net claims and operating costs to net call income, investment income and exchange loss/gains.

The greater the ratio between overall result and net call income the greater the likelihood of a surplus but this may also indicate a greater than average sensitivity to investment performance.

39

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

P&I C

ompa

rativ

e D

ata

Gross call/GT

Amer

ican

Brita

nnia

Gard

Japan

Lond

onNor

th

Shipo

wners

Skuld

Stan

dard

Stea

msh

ip

Swed

ish UKW

est

2012 2011

0

2

4

6

8

10

12

Net claims/GT

Amer

ican

Brita

nnia

Gard

Japan

Lond

onNor

th

Shipo

wners

Skuld

Stan

dard

Stea

msh

ip

Swed

ish UKW

est

2012 2011

0

1

2

3

4

5

6

Gross call income reflects the club’s total income (inclusive of group reinsurance costs) as an assessment of current and future risk.

Total entered GT is a measure of the size of the club, but provides no indication of current or future risk.

The ratio can give some assessment of the club’s membership risk profile.

Net claims are the club’s actual current exposure (and a guide to future exposure).

Total entered GT is a measure of the size of the club, but provides no indication of current or future risk.

The ratio can give an assessment of the club’s current membership risk profile.

The greater the ratio between the indicators in the above two charts the greater the likelihood of a surplus.

P&I Club Market Reference.

41

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

2012 Policy Year Mutual Reinsurance Structure 42

P&I Class Supplementary Call History 46

P&I Class General Increase History 47

P&I C

lub

Mar

ket

Refe

renc

e

42

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

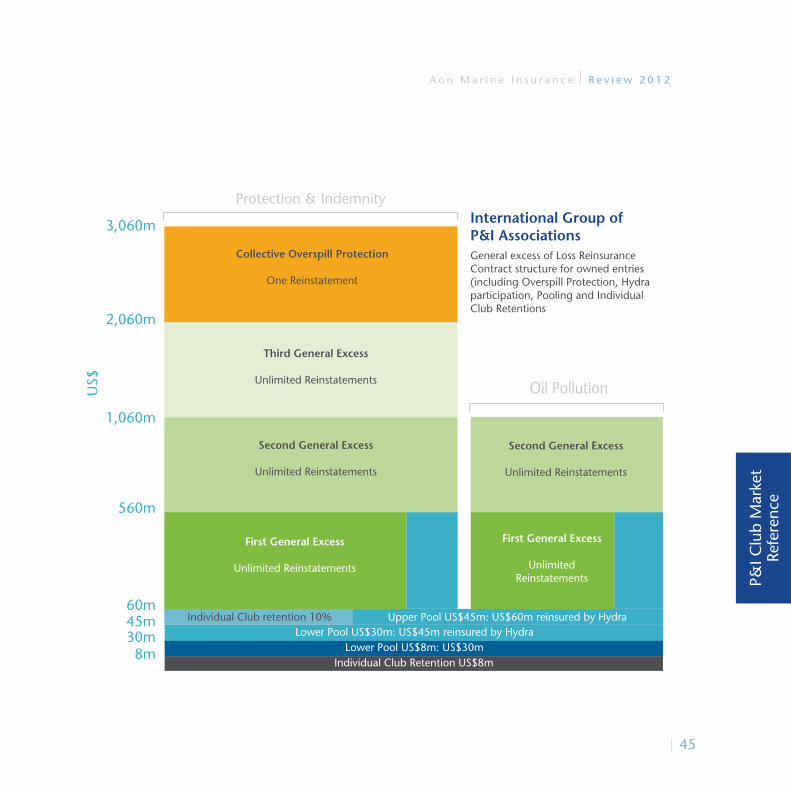

Pooling and structureFor the 2012/13 year the individual club retention

figure remained unchanged at USD8 million with the

Pool limit unchanged at USD60 million with Hydra,

the Group’s captive, participating in the Group’s upper

pool which is currently USD30 million.

There was one amendment to the Pool retention

structure whereby any club that brings a large claim

to the Pool will now bear a 10% retention within the

layer USD15 million excess of USD45 million, with the

balance being apportioned between all Group Clubs.

Claims that exceed the overall limit of the Group’s

excess reinsurance contract, including the reinsured

overspill layer, are then be pooled among the Group

Clubs.

The overall limit for this overspill remains unchanged

at 2.5% of the limitation funds under the 1976

Limitation Convention for all mutual ships entered in

the Group Clubs.

2012 Policy Year Mutual Reinsurance Structure

43

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

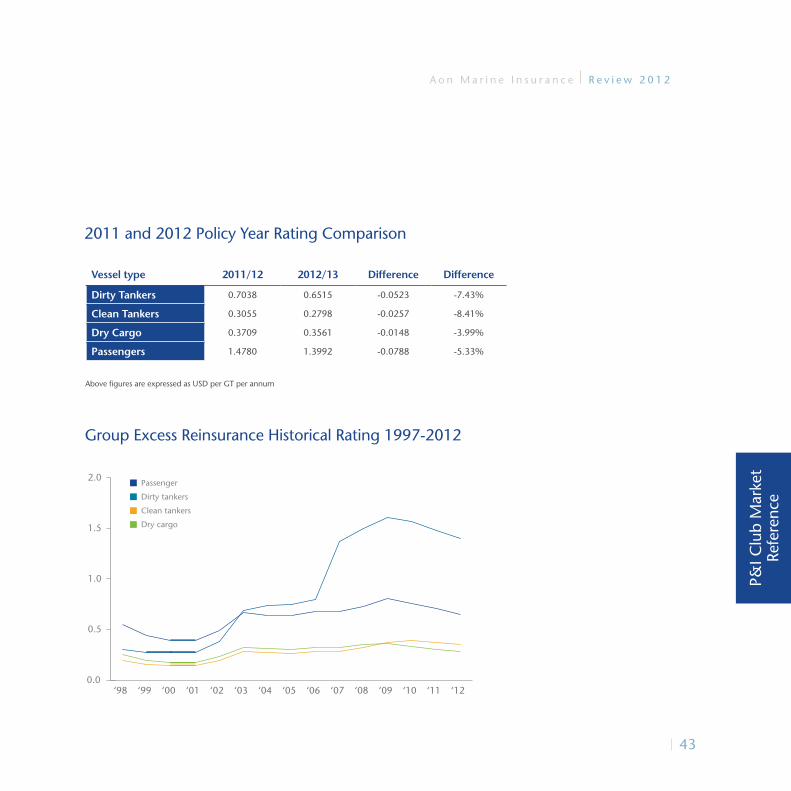

2011 and 2012 Policy Year Rating Comparison

Vessel type 2011/12 2012/13 Difference Difference

Dirty Tankers 0.7038 0.6515 -0.0523 -7.43%

Clean Tankers 0.3055 0.2798 -0.0257 -8.41%

Dry Cargo 0.3709 0.3561 -0.0148 -3.99%

Passengers 1.4780 1.3992 -0.0788 -5.33%

Above figures are expressed as USD per GT per annum

Group Excess Reinsurance Historical Rating 1997-2012

P&I C

lub

Mar

ket

Refe

renc

e

‘98 ‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12

Passenger

Dirty tankers

Clean tankers

Dry cargo

0.0

0.5

1.0

1.5

2.0

44

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Excess of LossThe International Group’s excess of loss reinsurance

programme was severely impacted by two major

losses by the end of the 2011 policy year.

Whereas the record had been showing signs of

improvement over the previous years, the enormity of

these incidents had a detrimental effect on the overall

loss record and although rating for 2012 had already

been published, an additional premium was paid

by the group to its reinsurers in order to finalise the

contract renewal.

The contract was renewed for the 2012/13 year on

a similar structure to the previous year with only one

slight variation in the pooling arrangement.

Historically separate rating categories, determined by

vessel types, have been utilised to allocate premium

and this format continued for the 2012/13 year with

downward variations in the individual rating categories

as shown opposite:

45

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

P&I C

lub

Mar

ket

Refe

renc

e

3,060m

Protection & Indemnity

Oil Pollution

2,060m

1,060m

560m

60m45m30m8m

International Group of P&I AssociationsGeneral excess of Loss Reinsurance Contract structure for owned entries (including Overspill Protection, Hydra participation, Pooling and Individual Club Retentions

Collective Overspill Protection

One Reinstatement

Third General Excess

Unlimited Reinstatements

Second General Excess

Unlimited Reinstatements

Second General Excess

Unlimited Reinstatements

First General Excess

Unlimited Reinstatements

Individual Club retention 10% Upper Pool US$45m: US$60m reinsured by HydraLower Pool US$30m: US$45m reinsured by Hydra

Lower Pool US$8m: US$30mIndividual Club Retention US$8m

First General Excess

UnlimitedReinstatements

US$

46

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

P&I Class Supplementary Call History

Policy year 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13

American Club 25/60 40/70 20/56 0/0 0/20 0/35 0/30 0/25 20/20 25/25 25/25 0/0

Britannia 25/25 40/40 40/40 40/30 40/30 30/30 30/30 40/40 40/32.5 40/40 40/40 40/40

Gard 25/25 25/25 25/25 25/25 25/20 25/20 25/25 25/25 25/10 25/15 25/20 25/25

Japan Club 20/10 20/20 30/10 30/30 30/30 30/60 30/30 30/30 40/40 40/50 40/40 40/40

London Steamship 40/40 40/40 40/40 40/40 40/40 40/89 40/89 40/75 40/40 0/0 0/0 0/0

North of England 25/25 25/25 25/25 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0

Shipowners 25/0 25/0 25/0 25/0 25/0 25/0 25/0 25/0 10/0 10/0 10/0 10/0

Skuld 20/20 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0

Standard 25/25 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0 0/0

Steamship 0/40 0/0 0/0 0/0 0/0 0/12.5 0/14 0/20 0/0 0/0 0/0 0/0

Swedish 0/0 0/0 0/0 0/0 0/0 0/35 0/35 0/0 0/0 0/0 0/0 0/0

UK 0/0 0/0 0/0 0/0 0/0 0/20 0/25 0/20 0/0 0/0 0/0 0/0

West of England 20/20 20/20 20/20 20/35 20/35 20/55 20/55 20/65 30/30 30/30 30/30 30/30

Original estimate/actual or current estimate as percentage of advance call/estimated total call as applicable.

Excess Supplementary Call

Reduced Supplementary Call

Open Year

47

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Policy year 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

American 10 26 25 17.5 10 10 10 20 29 4.16 2 5

Britannia 10 28.8 15 8.5 7.5 2.5 5 23.8 12.5 5 5 5

Gard 10 25 15 7.5 5 7.5 5 10 15 0 0 5

Japan 0 0 10 0 0 0 10 20 21.1 12.5 10 3

London 10 27.5 25 15 12.5 12.5 7.5 17.5 15 5 5 5

North 10 25 25 17.5 12.5 7.5 7.5 17.5 17.5 5 3 5

Shipowners 0 20 15 0 0 0 5 15 10 5 0 0

Skuld 10 30 25 15 7.5 5 2.5 7.5 15 5 n/a n/a

Standard 7.5 2.5 25 20 12.5 5 5 15 15 3 3.5 5

Steamship 10 25 25 20 12.5 5 9 15 17.5 5 0 5

Swedish 7.5 25 25 15 10 10 7.5 15 15 2.5 2.5 5

UK 7.5 20 25 17.5 12.5 12.5 7.5 17.5 12.5 5 5 3

West 5 10 25 15 12.5 12.5 5 15 19.2 5 5 5

average 7.5 20.4 21.5 13 8.8 6.9 6.7 16.1 16.5 4.8 3.4 4.3

P&I Class General Increase History

Percentage of advance call/estimated total call as applicable including any change in budgeted supplementary

call estimate.

P&I C

lub

Mar

ket

Refe

renc

e

Specialist Markets.The International Group of P&I Clubs has traditionally provided P&I cover for around 90% of the world’s ocean-going tonnage. However the fixed premium market continues to offer some credible options particularly in the smaller vessel division. Over the coming months there are expected to be significant developments in this sector of the P&I market with some new and interesting entrants emerging supported by some internationally recognised security. However in this review we have concentrated on the larger and more established fixed premium P&I providers to date.

49

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

British Marine 50

Eagle Ocean Marine 51

Hydor 52

Navigators 53

Osprey 54

RaetsMarine 55

Spec

ialis

t M

arke

ts

Commentary on individual insurers has been supplied by the insurers themselves.

50

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

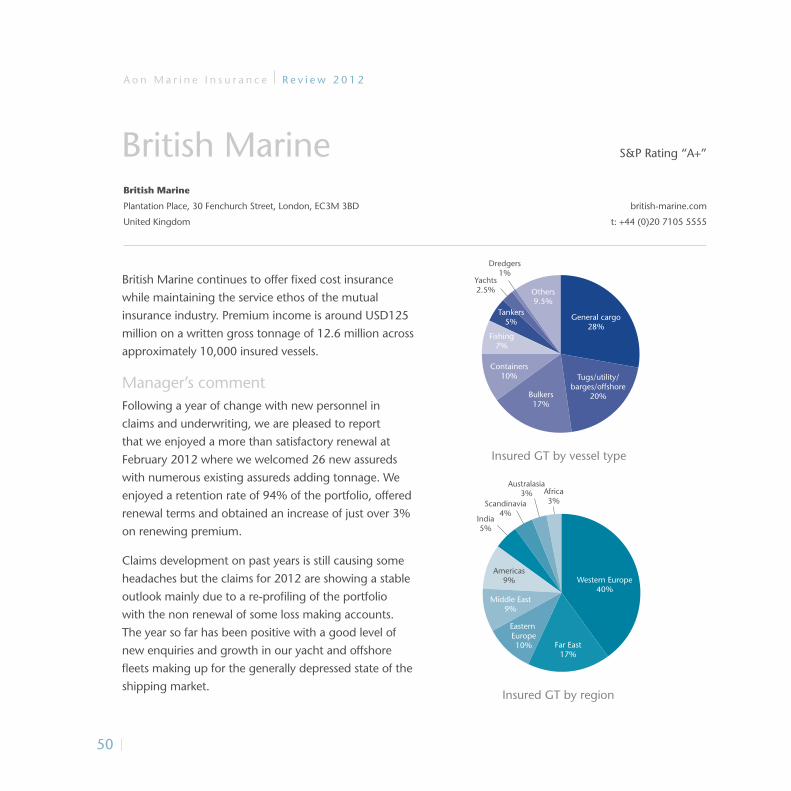

British Marine continues to offer fixed cost insurance

while maintaining the service ethos of the mutual

insurance industry. Premium income is around USD125

million on a written gross tonnage of 12.6 million across

approximately 10,000 insured vessels.

Manager’s commentFollowing a year of change with new personnel in

claims and underwriting, we are pleased to report

that we enjoyed a more than satisfactory renewal at

February 2012 where we welcomed 26 new assureds

with numerous existing assureds adding tonnage. We

enjoyed a retention rate of 94% of the portfolio, offered

renewal terms and obtained an increase of just over 3%

on renewing premium.

Claims development on past years is still causing some

headaches but the claims for 2012 are showing a stable

outlook mainly due to a re-profiling of the portfolio

with the non renewal of some loss making accounts.

The year so far has been positive with a good level of

new enquiries and growth in our yacht and offshore

fleets making up for the generally depressed state of the

shipping market.

British Marine

Western Europe40%

Far East17%

Eastern Europe10%

Middle East9%

Americas9%

India5%

Africa3%Scandinavia

4%

Australasia3%

Insured GT by region

British Marine

Plantation Place, 30 Fenchurch Street, London, EC3M 3BD

United Kingdom

british-marine.com

t: +44 (0)20 7105 5555

General cargo28%

Tugs/utility/barges/offshore

20%Bulkers17%

Containers10%

Fishing7%

Tankers5%

Others9.5%

Yachts2.5%

Dredgers1%

Insured GT by vessel type

S&P Rating “A+”

51

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Eagle Ocean Marine

A relatively recent entrant into the fixed premium

market the facility, operated by Eagle Ocean Agencies,

offers full P&I, and FD&D cover with security is

provided by the American Club. Policy limits up to

USD25 million for P&I and USD2 million for FD&D

with a further layer for P&I risks of USD25 million

excess of the primary layer available with Lloyd’s and

company security. Eagle Ocean’s annual premium

income is approximately USD5million with 125 vessels

at risk for a total gross tonnage of just under 500,000.

Manager’s commentEagle Ocean Marine provides attentive, sensibly priced

Protection and Indemnity and Defence insurance

to the operators of smaller vessels for whom a fixed

premium rather than a mutual product is the natural

choice. Eagle Ocean Marine seeks to distinguish itself

from its competitors by linking American Club security

backed by an extensive reinsurance programme

at Lloyd’s and in Germany with a breadth of service,

depth of expertise and speed of response

second-to-none in the industry.

Eagle Ocean Marine

c/o Eagle Ocean Agencies, Inc., One Battery Park Plaza - 31st Floor, New York, NY 10004

United States

Spec

ialis

t M

arke

ts

Asia50%

Europe9%

Americas5%

ROW34%

Insured GT by region

Tank42%

Tug & Barge4%Bulk

15%

General29%

Others2%

Insured GT by vessel type

S&P Rating “BB+”

eagleoceanmarine.com

t: +1 212 847 4600

52

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Hydor

Another relatively new entrant into the market

having been in operation since 2012. With security

consisting of 100% Lloyd’s syndicates, Hydor currently

writes a premium income of around USD5million in

premium over 306 vessels on a total gross tonnage of

approximately 2.2 million.

Manager’s commentHydor is a Managing General Agent and writes 100%

of risks on behalf of various Lloyd’s syndicates. Brit

Syndicate 2987 fronts 100% up to USD25 million with

excess layers up to USD500 million underwritten by

17 Lloyd’s syndicates.

The current portfolio is geographically diverse with

largest entries from Norway and Germany. Growth

during the year is international and Hydor now sees

more business coming through London and local

producers globally. Hydor is able to write all kind

of vessels up to 10,000 GT and for Charterers P&I/

FDD, there is no GT limitation. Hydor is focused on

sustainable growth and quality shipping companies.

Hydor

Rådhusgata 25, Oslo

Norway

hydor.no

t: +47 2241 5000

Norway33%

Others12%

Americas6%

Germany13%

Greece9%

Russia6%

MiddleEast6%

Denmark6%

Turkey5%

Greenland4%

Insured GT by region

General cargo27%

Offshore15%

Tank12%

Multipurpose11%

Ferry8%

Bulk7%

Ro/Ro7%

Fishing6%

Tug4%

Others3%

Insured GT by vessel type

S&P Rating “A+”

53

A o n M a r i n e I n s u r a n c e R e v i e w 2 0 1 2

Spec

ialis

t M

arke

ts

Navigators

Being part of a large international marine insurer,

Navigators P&I is in an advantageous position of being

able to offer overall marine packages to include P&I for

operators involved in other types of marine activities.

Insuring around 2.2 million gross tons comprising

1,700 vessels, the estimated premium income of

Navigators is approximately USD22.5 million.

Manager’s commentNavigators P&I provides the unrivalled expertise

necessary to protect against or minimise disruption

to operation of their commercial ships and promptly

delivers funds to indemnify them in event of loss they

have become liable/pay to others arising from such

shipping operations. We continue to offer a USD50

million limit with an option to increase this to USD100

million in selective circumstances. We continue to

concentrate on vessels not exceeding 10,000 GT and

that do not trade trans-Atlantic or trans-Pacific have a

global network, a wide range of competence within

P&I with authority to settle claims. The main claims

handlers and lawyers are based in London.

Navigators P&I

7th floor, 2 Minster Court, Mincing Lane, London EC3R 7BB

United Kingdom

navg.com

t: +44 (0)20 7220 6900

Europe37%

Asia24%

Africa5%Middle

East9%

Mexico &CentralAmerica

10%