Page 1

COVER PAGE

ROLE OF COST CONTROL STRATEGY IN ACHIEVING COORPORATE

SURVIVAL AND GROWTH A CASE STUDY OF NIGERIA BREWERY, ENUGU

BY

GLORIA CLEMENT

PGD/NOU142853270

RESEARCH WORK SUBMITTED FOR THE AWARD OF POSTGRADUATE

DIPLOMA IN BUSINESS ADMISTRATION TO THE SCHOOL OF MANAGEMENT

SCIENCE, NATIONAL OPEN UNIVERSITY OF NIGERIA

CENTRAL AREA STUDY CENTRE, ABUJA

SEPTEMBER, 2015.

Page 2

TITLE PAGE

ROLE OF COST CONTROL STRATEGY IN ACHIEVING COORPORATE

SURVIVAL AND GROWTH

(A CASE STUDY OF NIGERIA BREWERY ENUGU STATE)

BY

GLORIA CLEMENT

PGD/NOU142853270

A PROJECT SUBMITTED TO THE SCHOOL OF MANAGEMENT SCIENCE

NATIONAL OPEN UNIVERSITY OF NIGERIA, ABUJA STUDY CENTRE,

IN PARTIAL FULFILMENT OF THE AWARD OF POST GRADUATE DEGREE

(PGD) IN BUSINESS ADMINISTRATION.

SEPTEMBER, 2015.

i

Page 3

DECLARATION

I declare that this project has been written by me and that is a record of my own research

work. To best of my knowledge and believe, it has not been previously presented in any form

whatsoever in any applications for Postgraduate Diploma in Business Administration.

All source of information collected and materials used have been dully acknowledged by

means of references and bibliography

-------------------------------------- ------------------------------------

Gloria Clement Date

ii

Page 4

APPROVAL

This Project titled “The Role of cost control Strategy In Achieving Corporate

SurvivalandGrowth Using Nigeria Brewery Enugu as a Case Study” has been accepted as

meeting the regulations governing the award of Postgraduate Diploma (PGD) in Business

Administration of National Open University of Nigeria and is accepted for its contribution to

knowledge and literary appreciation

…………………………………. ……….. ……….

Olisekebe, Valentine Ike (Mr)Date

(Supervisor)

……………………….. …………………

External Examiner Date

……………………….. …………………

Dean of School Date

………………………... ..………………...

Dean Postgraduate School Date

iii

Page 5

DEDICATION

This project work is dedicated to Almighty God, for his protection and guidance throughout

this project work and my study in the time spent in order to pursue a Postgraduate Diploma,

to my family for their supports, both in kind and financially. You all occupy a special part of

my hearts; thank you.

iv

Page 6

ACKNOWLEDGEMENT

First and foremost, I thank God Almighty, who gave me the privilege and opportunity to

write this project work. My appreciation goes to my able supervisor Mr Olisekebe, Valentine

Ikewho patiently read through and gave me all necessary correction, may God b less you in

your entire endeavour (Amen).

I will like to acknowledge my parents and siblings who through their continuous financial

support, encouragement and prays kept me going throughout these program, thank you so

much.

I will like to acknowledge also my friends as well as my well-wishers for their support.

v

Page 7

TABLE OF CONTENTS

Cover page i

Title Page ii

Certification iii

Approval iv

Dedication v

Acknowledgement vi

Table of Content vii

List of Tables viii

Abstract ix

CHAPTER ONE

1.1 Background of the study 1

1.2 Statement of the problem 3

1.3 Objective of the study 3

1.4 Research questions 4

1.5 Significance of the study 4

1.6 Statement of Hypothesis 5

1.7 Scope and Delimitation of the study 6

1.8 Scope of the study 6

1.9 Definition of term 6

CHAPTER TWO

LITERATURE REVIEW

2.1 Historic background of Nigeria Brewery, Enugu 10

2.2 Conceptual framework 13

2.3 Theoretical framework 26

vi

Page 8

2.4 Review of current literature 37

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Design of the study 46

3.2 Population 45

3.3 Sample size 46

3.4 Sampling Techniques 47

3.5 Research Instrument 48

3.6 Instrument Validation 49

3.7 Reliability of the instrument 49

3.8 Source of data collection 50

3.9 Method of data collection 50

CHAPTER FOUR

PRESENTATION AND DATA ANALYSIS

4.1 Data analysis, Findings & Discussion 55

4.2 Test of Hypothesis 64

4.3 Discussion of the Findings 73

CHAPTER FIVE

SUMMARY, CONCLUSION AND RECOMMENDATION

5.1 Summary of the Findings 76

5.2 Conclusion 77

5.3 Recommendation 77

5.4 Proposal for further Studies 79

Reference 79

vii

Page 9

LIST OF TABLES

Table 2.2: Life method of inventory valuation 25

Table 2.4: Basis for direct labour cost 34

Table 2.5: Basis of labour hours 35

Table 2.6: Basis of machine hours 35

Table 3.1: Questionnaire distribution 48

Table 4.1: Questionnaire distribution 55

Table 4.2: Effect of physical control material theft 56

Table 4.3: Physical control in limiting wastage 56

Table 4.4: Effectiveness of cost control 57

Table 4.5: Information concerning material 57

Table 4.6: Effectiveness utilization of materials 58

Table 4.7: Cordial relations among heads of departments 58

Table 4.8: Consultation among heads in decision making 59

Table 4.9: Interdependency between workers 59

Table 4.10: Effect of co-ordination among cost centres 60

Table 4.11: Head involvement in budget preparation 60

Table 4.12: Supervision and implementation of budget 61

Table 4.13: Realizing objectives through the elimination of unnecessary cost 61

Table 4.14: Improvement in material handling through costs reduction techniques 61

Table 4.15: Cost reduction on profit planning 62

Table 4.17: Cost reduction in allocation of resources 63

Table 4.18: Effect of cost control on growth and profitability 63

Table 4.19: Test of hypothesis 64

viii

Page 10

ABSTRACT

These studies reveal the role of cost control strategy in achieving corporate survival and

growth a case study of Nigeria brewery Enugu state), Nigeria. The purpose of this research

paper is to examine the importance of cost control and the various cost control method used

and their impact on the survival of Nigeria brewery Enugu state. Used primary and

secondary data sources. The primary data were obtained using a structure questionnaire

which was administered to 30 randomly selected staff as well as discussion with some

targeted staff of Nigeria Brewery, Enugu State of Nigeria. The scoring on the questionnaire

was done using a five point Likert scale. The secondary data sources comprised of journal

articles, books, newspaper articles, company financial reports and internet. The student t -test

statistic and comparative percentage were used to test the hypothesis and the significance

level was α=0.01. This research discovered that 93.3% of the respondents were of the view

that cost control has greatly helped in boosting profitability in the company and 6.7%

disagreed. the cost reduction techniques adopted by the company are significantly adequate

for the achievement of companies’ objective .The study revealed that the problem of

manufacturing company is the high cost of overhead incurred in the company. These costs

are getting out of what the company could bear. This research recommended that The

companies should also make effort to improve its research and development unit to adapt to

local raw materials; a good budgeting process should also be put in place to control cost;

Just – in – Time (JIT) techniques should be employed to meet production and sales

requirement in Nigeria Brewery.

ix

Page 11

CHAPTER ONE

INTRODUCTION

1.1BACKGROUND OF THE STUDY

The word “cost” can be viewed in various ways. When it is considered in the noun form, “it

is the amount of the expenditure whether actual or notional incurred on, or attributable to a

given thing or activity.”In a relation to the research topic, cost can be defined as a term

providing service. It represents the monetary measurement of material, labour and overhead

used.

Control on the other hand is defined “as the process d assuring that plans are carried out in

such a way that objectives are attained:, control is also “ensuring that the cost to be incurred

on the total activity and various parts of it are kept under check and also that the quantum and

quality of activity are kept up to the mark” (Osisoma, 1996) Moore) 2001) says: To control,

you set goals, make plan, start to carry them out. Through control you try to guide things in

the direction you want them to go and hopefully you arrive at your goals.

From the definitions given above, cost control can define as the procedure and measures by

which the cost of carrying out an activity is kept under check. The aim is to ensure that costs

do not exceed to a certain level.

The use of effective cost control strategy cannot be over emphasized. Not only does it not

affect the individuals but, it also affect the whole economy of the nation business

organizations in both public and private sectors of the Nigerian economy have intentably

been facing adverse economic conditions. The by-product of the adverse economic

environment has been a considerable reduction in corporate profits. The concomitant effects

of the poor profit level have been retrenchments, abrupt closure of companies and parastatals

retirement with or without benefits or gratuities pay. Cut compulsory leave and so on.

1

Page 12

Reasons for these have been the remarkable increase in the cost of running business in the

country.

There are the foreign exchange problems with consequent lack of imported raw materials to

keep many manufacturing plants functional, even where the firms get the foreign exchange

market (FEM), it will not be enough to get the required quantity of raw materials to produce

at full capacity. A country faced with these problems has to find a solution to them.

Ogunlana (1993) also noted saying: “Nigeria is passing through a different period.

Everything possible must be done by everyone in a position to assist the economy in making

a guide recovering”. it at this point that the effective cost control strategies come to focus.

Its importance has just been recently recognized. It is therefore the deplorable situation

facing most business organization that many firms are now taking positive steps to adopt

effective cost control strategies to eliminate wastes, increase profitability and achieve higher

profitability and growth. It is not necessarily axiomatic that rising prices means rising costs,

effective cost control ensure the efficient use of resources. To effect this in a manufacturing

firm. Improvements in technologies are very helpful, but these alone are not sufficient. As

such, management of business organization has devices various strategies to supplement for

the technological inadequacy. Jobs are now timed and standards set. Cheaper and alternative

raw materials are now sought for to produce the same standards and quality of products.

Budgets have also been found as good cost control resources. In many organizations a

committee is set up under supervision of the chief Accountant with other department heads,

each charged with the responsibility of the overall cost control strategy, standards set should

be compared with actual order to correct variances that may emanate. Development in profit

should also be improved so as to ensure growth in organization.

2

Page 13

It based on the above background that the researcher intends to examine the role of cost

control strategies in achieving corporate survival and growth manufacturing organizations.

1.2 STATEMENT OF THE PROBLEM

In Nigeria, it has been observed the most business organization do not effectively control

their cost and problems have become more compounded since the advent of economic

recession in 1977.

The problem of being unable to adopt effective cost control strategies to reduce waste to an

acceptable level and improve upon profits, indeed; these problems demand immediate

solutions. Costs of operation an organization could be effectively controlled in order to

achieve maximum productivity and profitability. Effective cost control strategy involves

identifying the various systematic approaches for controlling cost so as to avoid the

occurrence of under utilization or over utilization of resources. The problems that impose the

proper control of costs by individual such as the personnel management, the cost accountant

and each departmental head and workers of the organization. The remunerations as ways of

motivation for all the individuals who helped in controlling costs accomplish the

organizational objective of higher profits and growth.

1.3 OBJECTIVES OF THE STUDY

The objectives of this study are:-

i. To ascertain out whether a typical Nigerian business undertake an effective cost

control strategy.

ii. To find out where the strategy minimizes total costs of operations with required

increase in profitability and growth.

3

Page 14

iii. To examine the nature of the strategy and its effect on profitability and growth of the

organization.

iv. To identify the roles played by the committee of cost organization.

1.4 RESEARCH QUESTIONS

In the course of the study some pertinent questions were asked and frank efforts were made

to address them, the questions thus include:

(i) What role does cost control have in preparation of growth and profitability in life

breweries?

(ii) What are the effective implementation and realization of full benefit of cost control?

(iii) What are the cost reductions adopted by the company?

1.5 SIGNIFICANCE OF THE STUDY

The study is necessitated by the obvious need for business organizations to plan for the

proper control of their costs through efficient handling of raw materials, equipments, spare

parts and payrolls, especially in this period of economic recession in Nigeria

To appreciate the vital role which effective cost control strategy plays in an organization’s

profit level, growth and existence. The significance of this study is to ensure that this vital

input to production is properly planned and optimally utilized for the achievement of

organization goals and objectives.

This study is useful to all levels of management in the manufacturing business especially

those in the strategic positions. Workers in non-managerial positions will also benefit from

this study, since they too will have to be involved at one point or the other by assisting in

controlling various departments.

4

Page 15

This study may also be useful to academics; it will provide lecturers, students and researchers

with data information to update their knowledge in matters concerning cost control.

Finally, the government, shareholders and potential investors will find this study very useful

in issues concerning control.

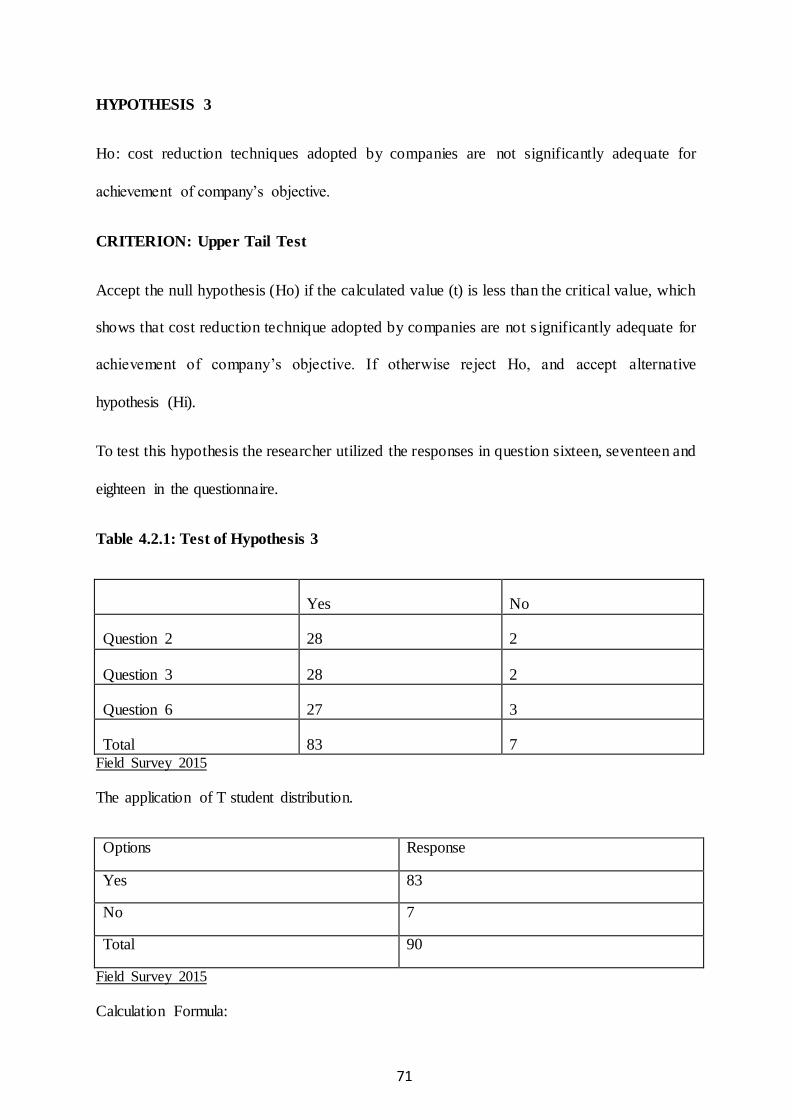

1.6 STATEMENT OF HYPOTHESES

In order to carry out this study successfully the following hypotheses were formulated:

i. Ho: The cost control process existence has no significant impact on growth and

profitability of the organizations.

Hi: The cost control process existence has significant impact on growth and profitability

of manufacturing organizations.

ii. Ho: There is no significant co-ordination among the different cost centers within the

company for effective implementation and realization of full benefit of costs control.

Hi: There is significant co-ordination among the different cost centers within the

company for effective implementation and realization of full benefit of costs

control.

iii. Ho: The cost reduction techniques adopted by the companies are not significantly

adequate for achieving company’s objectives.

Hi: The cost reduction techniques adopted by the companies are significantly adequate

for achieving company’s objectives.

5

Page 16

1.7 SCOPE & DELIMITATION OF THE STUDY

This study is limited to cost control in manufacturing industries and as such, it does not

extend other aspects of cost nor does it extend to other sectors of the economy.

In Nigeria, there are many manufacturing organizations registered with Manufactures

Association of Nigeria (MAN). Knowing that cost control is a broad area, the scope of this

study will be restricted to Nigeria Brewery Enugu.

In studying the organizations, the researcher will look at the effectiveness of the existing cost

control scheme and the role it plays in achieving survival and growth in the organizations.

1.8 LIMITATION OF THE STUDY

The general population of this study is all manufacturing firms in the country. This is because

the result of the research will be applied to them but due to the difficulty in having access to

this general population, the researcher chose the specific population to be the significant

staffs of Nigeria Brewery Enugu who are knowledgeable in the subject of the study. These

are about thirty-eight (38) in number that were selected from the accounts and finance

departments and among staff in change of store in the company.

Time Factor: it was one of the major setbacks encountered in carrying out this research. The

researcher has to allocate the limited time she has between her studies and this project work.

Financial problems: Research is capital intensive in nature. The cost of obtaining materials

for the study, the cost of transportation, typing cyclostyling etc: are all capital intensive.

1.9 DEFINITION OF TERMS

According to Ojo (p107) definition of terms used in social sciences research is operational

“words are defined as they are used by the researcher”. This means that the researcher used

certain definition of the terms in the study may be different from ordinary dictionary

meanings.

6

Page 17

ROLE: this is a prescribed or expected behavior associated with a particular position or

status in a group or organization.

COST: cost denotes the amount of money that a company spends on the creation or

production of goods and services. It does not include make-up for profit.

CONTROL: this is to test or verify (a scientific experiment) by a parallel experiment or

other standard of comparison.

COST CONTROL: Cost control is the control of all items of expenditure by regular and

frequent comparison of actual expenditure with predetermined standard or budgets, so the

undesirable trends from stand can be detected and corrected at an early stage.

STRATEGY: this is a plan of action designed to achieve a long – term or overall aim.

ACHIEVING: this is to accomplish a goal or to do something you set out to do. it also bring

about a desired result; succeed.

COOPERATE: this is to work or act together or jointly for a common purpose or benefit.

SURVIVAL: this is an object or practice that has continued to exist from earlier time.

GROWTH: this is the development from a lower or simpler to a higher or more complex

form; evolution.

7

Page 18

REFERENCE

• Argyris;. C. (1975) Human problem with Budgets Canada

Harvard Business Review Vol.2 No.4

• Anyanwu, B.E (1995) The Concept of internal Auditing,

Owerri: SEB publishing Ltd.

• Evans, D. F (2003) Flexible Budgetary Control and Standard Costs. Dallas Texas Mac

Donald and Evans Ltd.

• Garrison, R.H(1979) Management Accounting U.S.A:

Business publications Ltd.

• Gillespie .C. (2004). Standard and Direct Costing; New

Zealand: Pitman Publishing Inc.

• Harper H.M. (1982) Cost and Management Accounting;

London Mac Donald and Evans Ltd.

• Kohler, Eric L (1975), A Dictionary for Accountants Englewood Cliff presence Hail

publishers.

• Moore Franklin G. (2001) The Hand Book of Budgetary Control. U.K Graham

publishers.

• Morrison A .E (1981) Storage and Control of Stock.

London: Pitman publishing Ltd.

8

Page 19

• Obiagwu, F. A (1981) Budgetary for Effective Operation.

Owerri SEB publishers Ltd.

• Oliver Stanley (1975) Accountants Guide to Management Technique USA: Gower

Presshand ‘book

• Osisioma B.C (1996) Studies in Accountancy; Text and readings, Enugu New ages

publishers.

• Pandely I.M. (1985) Financial Management; New Delli:

Vikas publishing House.

9

Page 20

CHAPTER TWO

REVIEW OF LITERATURE

2.1 HISTORIC BACKGROUND OF NIGERIA BREWERY (ENUGU, ENUGU STATE)

Nigerian Breweries Plc, Enugu State Branch (Ama Brewery) is located at Amaeke Ngwo

near 9th Mile Corner in Enugu State. it is the sixth branch of Nigerian Brewery Plc in

Nigeria and it was commissioned in the year 2003. The site covers a total area of

approximately 100 hectares. Ama Brewery is designed with the best cutting edge

technology and world-class standard processes. The company has a production capacity of 3

million hectoliters per annum.

Nigeria Breweries Plc and Heineken International jointly owe the company. It is a beverage

company designed for the production of three brands of beer lagers namely; Star, Gulder and

Heineken, and two brands of soft drink namely; Amstel malta and Maltina, which

are successfully in production.

The company is made up of several departments which are controlled by heads of

departments (HODs) who in turn are summarily headed by brewery manager. He oversees the

general activities of the company.

DIFFERENT DEPARTMENTS AND THEIR FUNCTIONS

A. Support and development: This department is generally responsible for the welfare

and communications in the brewery. This department is the main administrative in the

company since they head decision-making. This department is headed by the

support and development manager and he is assisted by the human resource manager

that is principally involved with employee welfare and the information and

communication manager that is involved with the computer systems operation in the

brewery.

10

Page 21

B. Finance Department: This department is headed by the regional finance manager and

takes care of the company’s finance which is the fundamental tool for problem-

solving. This department provides the information for the company to attract investors,

establish lines of credit and plan for the future. They also pay workers’ salary. The

management and financial accountants assist the manager.

C. Logistics Department: This department is responsible for the stocktaking and

distribution of products to the public. They take care of the means of distribution of

their products and the sales of the products. This department is headed by the regional

logistics manager, and assisted by the middle manager.

D. Quality Assurance Unit: This department is in charge of maintaining the standard

quality of the inputs (raw materials) and outputs (products) of the company. This

department is headed by the total quality manager who is assisted by several analysts.

E. Production Department/Brew House: This department is the largest department and

is involved in the actual beverage making process. The brew house is designed for the

production of 12 brews per day and is automatically controlled from a central control

room and every activity from grains intake to storage is automatically carried out. This

department is headed by the production manager brewing, whom several swift

managers, operators and technicians, assist.

F. Packaging and Engineering Department: This is the second largest department as it

incorporates all packaging, engineering, waste disposal, maintenance and mechanical

processes in the brewery. It is headed by the Packaging and Engineering Manager and

is assisted by middle manager, technicians and operators

11

Page 22

Abbreviations:

S&DM___________ Support And Development Manager

HRM ___________ Human Resource Manager

HIN _____________ Head Industrial Nurse

ICM______________ Information Communication Manager

RFM ____________ Regional Finance Manager

MA______________ Management Accountant

FA ______________ Finance Accountant

RLM ____________ Regional Logistics Manager

LOM ____________ Logistics Operation Manager

SK______________ Store Keeper

TQM ___________ Total Quality Manager

PMB ___________ Production Manager Brewing

SMB____________ Shift Manager Brewing

BOP/BTE______ Packaging And Engineering Manager

PEM ___________ Engineering Development Manager

12

Page 23

MM____________ Maintenance Manager

SMP___________ Shift Manager Packaging

SPM___________ Spare Parts Manager

AM____________ Automation Manager

EUT___________ Engineers In Charge Of Utilities

TPM__________ Total Preventive Manager

PRM___________ Public Relation Manager

2.2 CONCEPTUAL FRAMEWORK

Costs are analyzed in order to provide information that will assist the measurement of control of

expenditure. Behaviorally, cost may be classified under controllable and non-controllable costs.

Kohler defined controllable costs as cost that varies with volume, efficiency and choices is less

than a proportionate manner with management determination and generally are known as

Variable Costs. Example is any cost which may be directly regulated at a particular level of

management authority.

Non-Controlled Costs are defined as:

1. Cost that do not fluctuate with volume

2. Any cost allocated to but not incurred by an operating unit, often not identified with the

supplied goods and services.

Beninger (1976) recognizes that controllable costs are subject to modification and change at a

particular level of management, while uncontrollable cost are not, But Horngren (1987) in his

own view noted that “all cost are controllable to some degree and by somebody over the long

run, those that are controllable are subject to various degrees, of influence’.

Generally, three types of factory costs are incurred in manufacturing companies

13

Page 24

1. Direct material: which is any raw material that is identifiable component of the finishes

product. For example nitrate which is used in the manufacture of Coca-Cola soft drink

2. Direct labour: which is the amount of wages earned by workers who are actually

engaged in transforming the materials its raw material states to a finishes product. Direct

materials and indirect labour comprise the prime cost of a product.

3. Factory overhead: which are indirect labour and other factory overhead. Indirect costs

comprise; factory overhead, selling overhead, distribution overhead and administrative

overhead.

In processing industries, direct labour and factory overhead costs are sometimes referred to as”

Conversion cost”.

The three (3) types of costs discussed above will give the total costs.

2.2.1 COST CONTROL, REDUCTION AND VALUES ANALYSIS

Cost control is adherence to standards; cost reduction is a challenge to the standards

themselves. In other words cost reduction is a further step to cost control. It involves such

measures and procedures by which cost per unit of quantity produced will be lower than

previously.

The aim of cost control must be cost reduction while the aim of cost reduction is to see

whether there is any possibility of bringing about a saving in the cost incurred-materials,

labour and overheads. To reduce cost, requires a, constant appraisal of the whole company

and not just production processes.

Value analysis is a special type of cost reduction. Olive Stanley defines it as “a systematic

inter disciplinary examination of design and other factors affecting the cost of production in

14

Page 25

order to desire a means of achieving the specified purposes, most economically at a required

standard of quantity and reliability”.

Its main objectives are to ascertain the appropriate cost for the appropriate performance.

2.2.2 ASPECT OF EFFECTIVE COST CONTROL

Effective cost control has two aspects; operational control and accounting control. Operational

Control: In a small enterprise, the manger can control cost through personal observation and

supervision of operations. As the business grows, such personal control is delegated too little

supervision. When the business continues to grow, a point is reached when such to control will

no longer be relied upon to keep waste, idleness, inefficiency and other cost contained,

consequently, it then becomes necessary to supplement operational control with accounting

control.

Accounting Control: This requires creating system of records which will analyze costs, account

for them and supply current pertinent reports to reveal how those who are responsible for costs

are discharging their responsibilities.

2.2.3 CONCEPTS OF PROBABILITY AND GROWTH

Accountants use the term profit in a number of ways, for instance profit is the excess of

revenue over cost, and it may qualify as the gross profit, net profit, pre4ax profit etc.

One can also define profit as simply the difference between revenue and cost which arises

because some firms are more efficient than others. Profitability therefore, is the measures of

returns on the resources or capital employed by the organization while growth is the rate of

development in the organization.

Nature and theories of profit

15

Page 26

Brigham and Pappas (1980) recognize four theories of profit which are “Frictional theory and

innovation theory”.

1. Frictional theory: This look at profit from the return of capital viewpoint; it save that return

on capital that would induce people to save and invest their money in business enterprises is

the normal profit. It goes further to say that normal profit is not steady due to frictions in the

economy, which may cause profit to fall below or rise above normal pro fits

2. The Monetary Theory: This suggests that due to some factory such as possession and

discovery of unique resources, innovations, patent rights, copyrights etc. some firms are

placed in the unique and monopoly situation which makes them to manipulate production and

price there by making abnormal profits.

3. The Compensatory or Functional Theory: These views profits are arising as compensation

for efficient and effective management and for undertaking the risks or mvesurLg n an

enterprise.

4. The Innovation Theory: It looks at profit as payment or compensation to successful

inventions of new things or ways of doing things

Factors That Affect Profitability and Growth: Since making of profit involves cost and

revenue, any factor that reduces costs, increase profit vice visa. The factors that affect

profitability and growth mostly in business organization are;

1. Fluctuation in economic Trend: firms are in business to minimize their costs and

optimize their revenues. An economy may experience such economic fluctuations as

depression, and this in turn influence business activities.

2. Changes in population and fashion

16

Page 27

3. The introduction of a new technique: Technology facilities production, it helps to reduce

unit costs, thereby increasing profitability, of the organization.

4. Demand and price.

5. Managerial skill: a prudent, resourceful efficient and innovative management is one that

is able to organize its operations such that costs are minimized and profits optimized.

Organization Role of Profit in a Business

Profits are indispensable in the life of any business organization, it aids business growth. It

increases the capital of the owners of the business. This is because part of the profits may be

ploughed back to: enhance the expansion of the business. Increase scale of production and

finance some other profit yielding projects. In a corporation, the shareholders receive their

share of profits only after dividends have been declared and the profits retained and ploughed

back.

The formula used in dividend declaration is

Po = ∑Dt/(Cl-1L)t

t= 1

where:

Po = Current price

Dt = expected dividend

K = discount rate

17

Page 28

= Indication that the fin is a going concern and there is no foreseeable termination daLe on

the stock. Source: (dames C. Van House, Financial management and policy, 6th ed Engle

wood cliff: prentice —Hall international Inc. 983, P.64).

Profit is indispensable for the growth of business as highlighted. It is therefore advisable for

business undertake those ventures that would maximize their profits and minimize those costs

without fraud or deception. Some of these would include the employment of capable and

efficient managers, proper and prudent employment of the resources available to the

organizations, making sure that enough finance is available to implement most of the projects

of the organization, making available modem equipment of production, which would increase

output and reduce limit cost of the products.

The aim of the measure is to reduce costs and increase revenues. The business organization

marketing, finance and administrative departments to ensure that co-ordination and efficiency

are achieved. In conclusion, the entire story is ensuring the adoption of effective costs control

measures to increase profitability and growth of a business organization.

2.2.4 MATERIAL INVETORY CONTROL

Effective control of material costs involves both operational and accounting control. From the

operational point of view, physical and procedural safeguards should be provided for materials

and supplies, physical facilities should be provide which will protect materials and supplies from

damage or deterioration and make them inaccessible to those unauthorized to do so. In addition,

specific employees should be more responsible for the purchasing receipt, inspection care and

disposition of materials and supplies.

Thus responsibilities of material control will be divided among purchasing, receiving and

inspection, production and service department personnel.

18

Page 29

Accounting control of material costs will be effected for by providing:

a. Forms for recording the requisitioning, ordering purchasing, receiving and inspecting.

b. Issuing and handling of direct and indirect materials.

c. Written procedures of all materials handling

d. Written authorization from persons in the company who are entrusted with phase of the

material acquisition and consumption.

e. A system or reports to reflect material cost performance in respect of such factors as

Usage, Waste, spoilage, Shrinkage and variances from established price and quantity

standards.

f. Written inventory taking procedure and component supervision of accounting and evaluation

inventories.

g. Logical, consistent policies or costing materials issue to production or service departments,

and for presentation of inventories.

2.2.5 THE PURCHASING FUNCTION

The control of material costs should begin with the requisitioning of materials and only few

responsible persons such as the departmental supervisors should be authorized to requisite

materials, and such authorization should be clearly defined in accounting and procedures manual.

In such cases, the authority to requisite production materials and factory supplies will be

confined to production materials and factory supplies will be confined to production control

department.

The Important Steps in Initiating Purchases are:

a. Need for materials.

b. Requisition for materials raised

c. Order prepared and placed

d. Materials they received from supplies.

19

Page 30

e. The material tested and inspected, certified perfect and are received or rejected for

valid reasons.

f. Goods received notes and the materials stored

g. Invoices passed for payment in the account section.

h. Appropriate accounting entries made in the costing and financial book.

Figure: PURCHASING PROCEDURE

NB:

G.R.N = Good Receive Note

L.P.O = local purchasing Order

The receiving department is responsible for running, checking and testing or inspecting

materials. Definite procedures should be established, physical control of materials received,

and a receiving report should be provided to verify receipts.

2.2.6 ACCOUNTABILITY FOR MATERIALS

The store department is charged with accountability for materials, including raw materials,

parts, supplies and scrap through the receiving reports and returned materials report. In the

materials against misappropriate or damage they should maintain constant watch over the

goods.

Buyer

Factory engineer

Suplies

Inspector

G.R.N Invoice

Reguisition

Chegues

Order L.P.O

Inspector Accountantoffice

G.R.N Invoice

Invoice G.R.N

Invoice G.R.N

Reguisition

20

Page 31

If the materials have been requisitioned in excess of actual needs, the excess amount should

be returned to the store department and procedures should be provided for controlling and

accounting for such returns. The store department should again be charged for the materials

and the department which returned them should be received from accounting for these

materials. The transfer of accountability and the reserves flow of cost can be document

through the use of material returned tickets

2.2.7 INVENTORY CONTROL

Pandey (1985) defines inventories as “stock of product a company is manufacturing for sales

and the components that make up the product”.

Plorison (1981) also defined it as “the means by which materials of the correct quantity and

quality is made available as and when required with due regard to economy in storage and

ordering costs, purchase prices and working capital”

Inventories exist in the form of raw materials, work- in-progress, and finished goods,

materials and work- in- progress inventories form more than 70% of any product cost and as

such the purchaser must buy what is right at right quality and quantity. However, Gillespie

(2004) recognizes that a company that neglects the management of inventories is only

jeopardizing its long-run profits ability and many fail ultimately”

In carrying out an efficient and effective control of inventories, the following decisions come

to mind;

a. How much to order?

b. when to order?

In approaching these two decisions, management feels somewhat ambivalent. Pressures, is to

order huge lot or quantity so as to minimize ordering cost. The order pressure is to order

small lot, so as to minimize carrying costs. If pushed too far, either of the courses of action

21

Page 32

will have unfavorable effect on profit but by using certain tool from operation research, we

can arrive at a model

for deriving economic Order Quantity (EOQ) is the point at which the ordering cost equals

the carrying (holding) cost as shown in figure 2 below.

Total point

Cost Low point

Stockholding cost

Ordering cost

EOQ Order size

Fig.2 EOQ MODEL

Ordering Cost: Includes the cost incurred in the requisitioning, purchase ordering

transporting, receiving inspecting and storing.

Carrying cost: Are costs incurred in holding a given level of inventory. They include storage

costs Insurance, Taxes, cost of deterioration and obsolescence etc.

Mathematically, EOQ= 2ac / Ip

Where:

22

Page 33

a = annual demand

c = ordering cost

p = price of inventory

I = an expression of 1% inventory holding cost.

For a period, the total ordinary cost is simply the number of orders for that period multiplied

by the cost per order. While the total carrying cost is the average number of units of inventory

for the period times of the carrying cost per unit.

Illustration= If a manufacturing company purchased raw

Materials from outside supplies at 17.10 per order.

Total annual need = N18O0.

Total ordering cost per order processed in N30 and the desired annual return on inventory

investment 15% of

N17.1O EOQ for the company can be calculated using the

Formula above

EOQ = 2ac/ip = (2x1800x30)/ip = 205units

Number of order will therefore be;

EOQ = 1800/205 = 8.8times

2.2.8 INVENTORY VALUATION METHODS

When the materials requisition have been honored by the storekeeper and have been noted on

the bin cards, they are passed to the cost officers. At this stage a price is inserted upon the

material requisitions and this is to give the total cost of the issue, which has been made to the

23

Page 34

job or process in the factor. C.J. Walker recommends the following valuation methods in a

manufacturing company. Actual Cost, F’IFO, LIFO, AVCO Market price and standards cost.

Some of these methods are explained below;

FIRST IN FIRST OUT (FIFO)

1. FIFO is a costing method widely used in valuing inventories. The method assumes

that materials flow from stores to production in the same chronological order as they

were produced; first purchases are issued out first.

Supposing Coca-Cola Bottling Company’s card for the month of June was as follows.

Quantity Price (N)

June 2 100 7.00

June 6 150 8.00

June 10 200 8.50

June 13 200 8.975

June 18 150 --

THEIR INVENTORIES CAN BE VALUED USING LIFO

VALUATION METHOD

Date Receipts

Qty Up(N) Value Qty Up(N) Values Qty Up(N) value

June 2 100 7.00 700 100 7.00 700

June 6 150 8.00 1200 250 7.8 1900

June 10 200 8.5 1700 450 8.5 3600

June 13 200 8.975 1795 650 8.975 5395

June 18 150 7.8 1100 500 4295

(100x7)

(50x8)

Field Survey 2015

24

Page 35

LAST IN FIRST OUT

Thus method assumes that the prices of last material that comes in is the price of issue unit

that quantity is exhausted, using the same illustration of coca-cola bottling company

valuation of inventories

Would appear as in table 2.2.

Table 2.2 life method of inventory valuation

Date Receipts

Qty Up(N) Value Qty Up(N) Values Qty Up(N) value

June 2 100 7.00 700 100 7.00 700

June 6 150 8.00 1200 250 7.8 1900

June 10 200 8.5 1700 450 8.5 3600

June 13 200 8.975 1795 650 8.975 5395

June 18 150 8.975 1346 500 8.098 4049

AVERAGE COST (AVCO) METHOD

Where a material is purchased at different prices, it seems logical to regard cost of a unit of

such material as the average of all the units’ purchases. This method tends to smoothen out

the fluctuations in prices and it favours the accountants. Using the same illustration, valuation

using AVCO method is as follow in table 2.4

Date Receipts

Qty Up

(N)

Value Qty Up

(N)

Values Qty Up

(N)

value

June 2 100 7.00 700 100 7.00 700

June 6 150 8.00 1200 250 7.8 1900

June 10 200 8.5 1700 450 8.5 3600

June 13 200 8.975 1795 650 8.975 5395

June 18 150 8.3 1245 500 4150

Field Survey 2015

Field Survey 2015

25

Page 36

2.3 THEORETICAL FRAMEWORK

Without manpower, it would be impossible to produce or distribute goods and services, and

thus impossible for the business to exists or achieve its objective. To buttress this, it is the

human resources that combine factors or ideas to produce the products and. services which

are economic products, which the consumer will be willing to buy with his hard earned cash

or currency.

The objective of planning, and control labour cost is therefore trying to ensure that the firm

receive optimum services at optimum cost from the people it employ in producing,

distributing products and services.

Labour costs involved both rational and accounting control.

Operational controls of labour costs involve Job analysis, job classification and the

recruiting, hiring and training of qualified personnel. It also involves the appointment of

supervisors with responsibility of clearly defined area of labour cost and necessary authority

to maintain control over labour utilization. Accounting control is achieved by development of

forms and records, and the preparation of various reports on:

a. The efficiency of utilization of labour

b. The effects of ways incentives

c. The share of labour in the total products of the enterprise.

ENTERPRISE

Labour control is meaningful only when it can be measured in number of persons employed

or man hours, units’ workers, capital asses, tools and equipments in monetary units.

26

Page 37

Approaches ofLabour Control

Labour control starts from selection of employees. The line manager supplies all information

needed as regards the selection to the personnel department. In some companies the personnel

manager does the work of finding suitable workers. In such a situation, if there is any

mistake, the personnel officer is blamed for making joint effort of line manager is required in

selection of employees. The requirements for employee’s selection are;

1. Physical requirements such as sex, eyesight, etc.

2. Mental or psychological requirements such as intelligence.

3 Training requirements such technical qualification and experiences.

Whenever the right person is selected there should be greater efficiency with minimum costs.

Furthermore, the rate of turnover should be at a reasonable level. Also excessive cost relating

to training and recruitment are avoided.

A. Induction Training

After selection, induction follows, that is an attempt should be made to introduced each

employee to what the company makes, how the particular department contributes to the end-

product, the organization of the business, the names of the mangers, foreman and

supervisors and any matter which affect him personally such as collection of wages, names of

trade union official, rules regarding overtime working cards details of social activities, as

activities standard output, cost per unit and the importance of controlling cost including the

correct procedures for checking on and off jobs, are all vital matters.

27

Page 38

B. Absenteeism, Lateness and Overtime

Batty recognizes that “if the right man is selected and trained for a particular job, this reduces

cost, provided a careful which is maintained on the performance of the works”.

As a general rule, the wage selection or personnel section keeps records of absenteeism or

late. The foreman should be aware of lateness or absence of work immediately they occur.

With this maintained in a firm effective labour control will be achieved at all times because

employees will now know that they are being monitored and this will improved their

behavior to work. Good performance should attract immediate record, and consistently bad

performance should attract necessary disincentive.

Another area to be watched carefully is overtime, It has to regulation otherwise some workers

will abandon their normal work in order to do them during overtime, thereby causing

additional costs. Limits should impose on normal working hours, above which no worker is

allowed to exceed. Control can be affected by stipulating that departmental managers must

authorizes all overtime if standard costing is employed, any normal overtime will usually be

included in the standard cost. If additional overtime is worked, the cost would reveal in

labour various.

C. Use of time sheet in labour control

Labour cost can be controlled through the use of time sheet. This requires the recording of the

time a job is started and when the same job is completed. In this regard, a hypothetical unit

representing the amount of work to be done in a given hour is established as a standard

performance.

In an organization, where time keeping is done by distinct department, it takes care of

1. Overseeing the arrival and departure of workers.

28

Page 39

2. Maintaining records of how workers spend plant time.

Control of the first item involving total hours on job is commonly reflected by the use of

clock cards. They contain space for an industrial employee’s names, his number, his duty for

the week, that is whether on morning or afternoon duty, arrival and departure times. The

cards are designed to be inserted into a time clock that wills in-print the time of each such

insertion. A time clock is usually placed inside each entrance to officers or departments with

an accompanying rack for holding the clock cards of all employees which use that particular

entrance. When an employee enters his work area in the morning, he takes his card from the

rack, inserts it in the clock and returns it to the rack. When he leaves for lunch, it will clock

out and again clock in after lunch, with a final clock out at the end of the day. This card

shows whether he was late and how many time he spent in the plant.

D. Labour Wastes and it control

Labour wastes can occur in the form of idleness, non- supervision of the worker force,

exercise tea-break and late arrival or early dismissal on workers part: Idleness manifest in

three principal areas namely: idleness of personnel, idleness of facilities and idle space.

Personnel idleness reflects in a plant incomplete utilization of its labour force.

The causes are:

1. Insufficient work for certain employees.

2. The seasonal nature of a company’s

3. Sickness and injuries

4. Labour management disagreements

5. Absenteeism and tiredness.

29

Page 40

The type of waste can be minimized by job analysis, time and motion studies and preparation

of intelligent job description. On the other hand, idle facilities may exist when workers are

unable to use existing productive facilities because of:

1. Material shortage.

2. Breakdown of equipment

3. Unavailability of equipment

4. Absence of inspectors

Accounting to control of idleness must start with records for accumulating the cost time of

man and facilities. Employee’s time reports should show directly the amount of idle time

daily and their immediate supervisors should report such idleness. Based on this,daily weekly

reports summarizing such idleness and its cost should be prepare and presented to

departmental supervisors.

Factors That Affect Worker Productivity

The factors that commonly affect workers productivity are the work condition, time keeping,

and the light at the work place, healthy welfare, contented workforce and transport fare.

To solve these problems Obiagwu (1981) outlined some concept that can be used to enhance

workers productivity. These are:

Work humanization, Job environment quantity of working life job content, and factory

conditions like the development of team work approach to tasks in order to surmount the

problems of boredom, the introduction of flexible time to provide the individual work with a

great sense of control and better working condition.

30

Page 41

In addition to the above, Anyanwu (1995) also recognizes job enlargement, job rotation and

redesign and redesign incentives scheme and Fringe Benefits Incentive Scheme: Moore

(2001) use the ten-n “Incentives to describe wage payment plans which tie wages directly or

indirectly to productivity standards”.

In developing a good wage incentive, the company must ensure that;

1. The work contents are accurately measured to obtain full confidence on the work.

2. The schemes are fair and just to both the employer and the employee.

3. The workers are paid in direct proportion to the individual effort rather than as a

group

4. The scheme is simple in operation so that the workers can calculate their wages

easily.

5. The scheme gives the worker a guaranteed minimum wage.

6. The scheme has a reasonable degree of performance, and contains as much incentives

for slow and fast works.

Companies are entitled to any of these types of incentive scheme;

• Individual scheme

• Group scheme

• Factory-wide productivity scheme

• Profit sharing plans.

All these incentives tend to make the workers earnings more reasonable and intact Fringe

Benefits: Fringe benefits represent an extra Income, Additional security more desirable

31

Page 42

working conditions that require no additional effort. They are some of the free or subsidized

services offered by gain onthe part of the employees, as without such services, the employees

would have to pay for themselves. These include; free market services, transport, housing,

food subsidized lunch or luncheon vouchers, recreational services, other fringe benefit may

include paid public and annual holidays, contribution towards sickness benefits, redundancy

a’ company provident funds and pension schemes.

The rationale behind this is to reduce cost or just to maintain costs within limit, even though

this may lead to greater pay packet. On the other hand, the work facilities are better utilized,

hence the workers know that for every effort they make, they will be rewarded.

In conclusion, economic revival required greater creativity in our approach to manpower

development and utilization. We must therefore harness and effectively manage our human

resources for economic survival.

2.3.1 OVERHEAD COST ANALYSIS AND CONTROL

Operational and. accounting controls are employed in the control of overhead costs.

Overhead can he classified into’

Variable and fixed overhead costs, while the former varies with the level of activity, the later

does not. In other words, fixed cost is stable and predictable while variable cost is unstable

and unpredictable, always up and down.

These are the conceptions of various authors in the field of cost accounting, hut the researcher

felt that since controllability is relative to both time horizon and the management

responsibility area under considerations, it will be erroneous to agree with these authors that

variable cost are controllable while fixed cost are uncontrollable.

In support of this Anyanwu (1995) noted that “fixed cost can be conducted to variable cost”.

32

Page 43

2.3.2 Overhead Application Basis

A reasonable basis for applying estimated overhead to job are established by relating

overhead to other factors of production. In practice, the overhead of a producing department

are commonly related to one of the following production factors identified by Helper (1982):

Direct material cost

• Direct labour cost

• Prime cost

• Direct labour hours

• Machine hours

• Unit of production. An illustration:

The Obi and Sons Co showed the following information for the year 1997.

Direct material 42,200

Direct wage cost 40,000

Direct labour hours 10,000 hours

Machine hour operated 20,000 hours

Overhead applicable to the shop 50,000

The one batch of Co2 made this during the period, incurred the following costs;

Material 400

Labour 800

33

Page 44

Direct hour 220

Machine hours 1,000

An account for Co2 of the overhead costs can be absorbed using any of the control basis

mentioned above.

Solution:

Direct labour = 5000/10,000 = 0.5x220 =N110

Direct wage cost = 5000/40,000 = 0.125 x 800 =N100

Machine hour operated 5000/20,000 = 0.25X 1000 = N250.

Table 2.4: Basis for Direct Labour Cost.

N N

Material 400 Overhead cost

Labour 800 Control A/C 1300

Overhead 100

Total 1300 1300

Direct labour hours 200

Machine hours 1,000

An account for Co2 of the overhead costs can be absorbed using any of the control basis

mentioned above:

Solution:

Field Survey 2015

34

Page 45

Direct labour = 5000/10,000 = 0.5 x 220 = N110

Direct wage cost = 5000/40,000 = 0.125 x 800 = N100

Machine hours operated = 5000/20,000 = 0.25x100 = N250

Table 2.4: Basis of Direct Labour Cost.

N N

Material 400 Overhead cost _

Labour 800 Control A/C 1300

Overhead 100 _

Total 1300 1300

Table 2.5: Basis of Labour Hours.

N N

Material 400 Overhead cost

Labour 800 Control A/C 1310

Overhead 110

Total 1310 1310

Table 2.6 Basis of Machine Hours.

N N

Material 400 Overhead cost

Labour 800 Control A/C 1300

Overhead 100

Total 1300 1300

Field Survey 2015

Field Survey 2015

Field Survey 2015

35

Page 46

The factory overhead control account is a general ledger cost of control account from the

above illustration; the company is favored with direct costs basis absorption.

2.3.3 WORKING CAPITAL MANAGEMENT AND CONTROL

This is another area in the cost control.

Van Horn’s (1990) describes working capital management as “involving the administration

of current assets and current liabilities”.

Current assets include assets such as cash, marketable securities, and receivables arid

inventories.

In this study, the researcher’s attention will be directed toward cash and inventory aspect of

working capital. Inventory management control had already been discussed. Therefore the

researcher will base his discussion in cash management. Cash are required as - cash balance

in hand, bank balances, short-term deposit and other near cash items.

j.m Keynes (1985) identified three basic motives for holding cash are;

1. Transaction motive: This is the need to hold cash for meeting payment arising in the

ordinary course of business

2. Precautionary motive: relates to holding of cash to meet unexpected contingencies.

3. Speculative motive: relates to the holding of cash to take advantage of expected

business opportunities.

Excess cash involves greater liquidity for idle assets, although this may involve little risks

and less profitability, as the excess cash are not channels into investment. On the other hand,

maximum availability of cash will ensure prompt payment for transactions, which is capable

of attracting cash discount, and this in effect will reduce unit cost of a firm‘s product when

36

Page 47

the excess are channeled into investment. This will attract more profits and some element of

work. Firms are therefore advised to make efficient use of their cash.

2.4 REVIEW OF CURRENT LITERATURE

According to Trevor (1979) “cost control is the control of expenditure within pre-determined

levels”

Eric (19Th) defined it as “the employment of management devices in the performance of any

operations so that re-establishment objectives of quality, quantity and time may be attained at

the lowest possible out lay for goods and services’.

Breech (1980) sees cost control as “the control of all terms of expenditure by regular and

frequent comparison of actual expenditure with predetermined standards for budget, so that

undesirable trends away from standard can be detected and corrected at early stage’.

According to Allan R. Drebin and Harold Bierman (1995) cost control considers what should

be and what corrective action should be taken when costs are excessive”,

From the foregoing, one can say that cost control is a continuous activity aimed at improving

efficiency and quality by ensuring that the right resources are provided, and only directing

anticipated levels, it is also concerned with understanding how and why costs change. Cost is

concerned with the setting of performance standard and monitoring of actual results against

these standards.

And finally, it is concerned with people’s attitude and motivation when handling money that

is not their own cost control will be meaningless unless constant attempts are made in

reducing the costs.

37

Page 48

In any organization, cost control will be best achieved when the following measures are

taken:

1. Cost standard are predetermined

2. The actual costs are ascertained

3. Comparisons are made between the two above

4. Variances are established, analysis and reported upon.

5. Executive actions necessary are taken to ensure that exceptions of deviations are

brought back on course.

A budget is a quantitative economic plan in respect of a period of time. Evans (2003) defined

budget and control as a system of controlling costs which includes the preparation of budget,

co-coordinating the departments, establishing responsibilities, comparing actual performance

with that budgeted and acting upon results to achieve maximum profitability”.

Certain fundamental principles can he outlined from these definitions and these are:

1. You establish a plan or target of performance which co-ordinates all the activities of

the business.

2. Record the actual performance.

3. Compare the actual performance with that planned.

4. Calculate the differences of variances and analyze the reasons for them.

5. Act immediately, if necessary to remedy the sit action.

One can say that budgetary control is an embodiment of planning and control process with

feedback concept. An illustration of this inter-relationship is presented in figure 2.4

38

Page 49

PLANNING PROCESS CONTROL PROCESS

Goals

Objective

Management

decision

Budgets

Feedback for fut

Fig. 2.4 Planning and Control Process

Source: management accounting: a decision emphasis by Don T Decoster and

EldenL.Sehafer)

The budget is not only expression of management plans but also basis of comparison with

actual results in the central process. The latter function being performed with the aid of

budgetary control reports. To make the budgetary control system effective, the organization

should:

Monitor actual activity and measure

actual results

Compare actual results with plan

identifying significant deviation

Investigation significant from deviation plans

Take corrective action

39

Page 50

1. Create budget centers

2. Introduce adequate accounting records

3. Prepare instruction in techniques

4. Prepare organization chart with defined responsibility.

5. Set the work of the budget committee.

6. Define the budget periods, the key factors and level of activity.

The most vital of all these is the preparation of an organization chart. The starting point in

designing and establishing a budgeting control system is to define responsibilities. This may

be best achieved through the preparation of a organization chart which will defines the

functional responsibilities of each member of company and his relationship to other

members. The organization chart will depend on the nature and size of the company but a

simplified sample is given in figure 2.5, this time depicting budget responsibilities

40

Page 51

Chief Executive

Buyer Sale manager Production

manager

Accountant

Purchases Sale, selling

and

distribution

costs

production

Figure 2.5. Organizational Chart of Budgetary Control

Responsibility for setting standard

Standard Costing: Is the system of cost accounting, which makes use of predetermined

standard cost relating to each element of cost control techniques which involves the following

steps:

1. Predetermination of the standard costs.

2. Recording of actual cost incurred.

3. Recoding of actual with standard costs

Budget Officer

Production cost Admin.

Cost cash master capital

expenditure

Plant utilization

41

Page 52

4. Obtaining the cost variances, which are analyzed so the inefficiency may be quickly

brought to the notice of the person responsible for them.

5. Reporting to management, so that appropriate action can he taken.

His action is the important of effective cost control. F hypothetical case is given below to

illustrate what face been discussed so far.

Fig. 2.6 production cost budget report to management for period: Three months to 31stJuly

2013

Variance

Budget Actual adversefavourable

N N N N

Direct materials

Product A 6,000 6,000 600 -

Product B 9,000 9,000 • -

Product C 3,000 2,850 • 150

Direct Labour - -

Product A 10,500 10,800 300 -

Product B 10,500 10,200 • 300

Product C 40,500 4,600 150 -

Production material 11 -

Product A 2,400 2,469 69 -

Product B 3,000 2,913 - 87

Product C 1,200 1,239 39 -

Total 50,100 50,721 1,158 537

Field Survey 2015

42

Page 53

With the above variance, whether adverse or favorable, management would now be in the

position to determine:

1. Where the variance occurred (material, labour and overhead)

2. What was responsible and

3. Why it happened.

43

Page 54

REFERENCES

• Batterseby Albert (1980) A Guide to stock control

London: Pitman Publishing Ltd.

• Black., Chapin. and miller (1975) Principles of Accounting

3rd Edition USA: CBS College publishing.

• Brigham and papas (1976) Management Economics

London: Dryden Press.

• Breech, E. F. L. (1980) The Principles and Practice of Management London:

Longmanpublishers.

• Earnest L.N (1976) Variance Accounting, London:Prentice —Hall Press inc

• Evans, D. F (2003) Flexible Budgetary Control and Standard Costs. Dallas Texas Mac

Donald and Evans Ltd.

• Garrison, R.H(1979) Management Accounting U.S.A:

Business publications Ltd.

• Gillespie .C. (2004). Standard and Direct Costing; New

Zealand: Pitman Publishing Inc.

• Harper H.M. (1982) Cost and Management Accounting;

London Mac Donald and Evans Ltd.

• Kohler, Eric L (1975), A Dictionary for Accountants Englewood Cliff presence Hail

44

Page 55

Publishers.

• Moore Franklin G. (2001) The Hand Book of Budgetary Control. U.K Graham Burn

publishers.

• Morrison A .E (1981) Storage and Control Of Stock.

London: Pitman publishing Ltd.

• Obiagwu, F. A (1981) Budgetary for Effective Operation.

Owerri SEB publishers Ltd.

• Oliver Stanley (1975) Accountants Guide to Management Technique USA: Gower

PressHand ‘book

• Osisioma B.C (1996) Studies in Accountancy; Text and readings, Enugu New ages

publishers.

• Strawser, B.F (1990) Financial Accountig. USA Dame Publishers Inc.

• Van Horns, James C, (1983) Fnancial Management and Policy 6th edition.

EnglewoodCliff; prentice.

45

Page 56

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 DESIGN OF THE STUDY

This research adopted a case study and survey approach. Data were collected from the firm

used as case study. The data collected were analyzed and the findings used to generalize all

firms in the manufacturing industry.

3.2 POPULATION

Population is the totality of the observation with which we are concerned. Population can be

finite or infinite. A finite population has a definite unit, it is infinite if it has no upper unit or

the number of units it contains is not known. It is also considered as a universe of data

consisting of data within special parameters and it can refer to a special group to be

measured. It is precisely defined in this research work. Since the research could not cover the

whole population, a sample of the population was selected to represent the entire population

consisting of the respondent and selected analysis in respect of the research work. The

population in this research work is to Nigeria Breweries, Enugu.

3.3 SAMPLE SIZE

According to Obasi (1997, p.57) the size of a sample is determined by the combination of

technical issue as well as human and financial consideration. The technical factor includes the

size of population. The level of precision desired and the level of variability of factors to be

estimated. The homogeneity of the population, the extent of prior knowledge about the

characteristics of the population, the rate at which the development is taking place in the area,

among other critical determinations that informs the sample size.

46

Page 57

It is important to mention that sample size is used in studies that involve a large population.

Samples are used for the following reasons:

- To adequately manipulate an enormous population to avoid errors due to the

calculation of large numbers.

- The desire to reduce the cost of producing questionnaire that will cover the

entire population in question.

To this end, a total of 38 respondents were administered with the questionnaire chosen from

the identified and selected population. However, only 30 questionnaires were dully

completed and returned to the source. The responses from the respondents as contained in

this research questionnaire were restricted to accommodate the independent and dependent

variables so as to relate the facts on how the financial institutions operate or been furthered

towards economic development.

3.4 SAMPLING TECHNIQUES

The researcher adopted the judgmental sampling technique to decide that the enforce specific

population be used as the sample since the population is small and finite. Thus the sample

size is 38 staff selected from the two companies used as cases study.

QUESTIONNAIRE DESIGN AND ADMINISTRATION

The questionnaire was carefully design to save some specific purposes. It was designed to

collect data on the role of cost control strategy in an organization and the impact of the

strategy in achieving corporate survival and growth of the organization

47

Page 58

The questions was addressed to the following categories of employees in the organization;

top management staff, accountants, junior staff and factory workers. Breakdown of the

pattern of response from the employees are shown in table3.1 below:

Table 3.1 questionnaire distribution

No. of questionnaire

Respondents Sent out received Percentage

Top management 12 10 26.3

Accountant 6 5 13.2

Junior staff 10 7 18.4

Factory workers 10 8 21.0

Total 38 30 78.9

From the table above, a total of thirty-eight (38) questionnaire were distributed to different

categories of workers and thirty (30) were returned representing 78.9%

3.5 RESEARCH INSTRUMENT

Research instrument is a means or item through which information or data will be elicited.

The main research instruments used in gathering the necessary information for the research

work are interview and questionnaire. These were well constructed and clearly worked for

easy understanding and to void errors commonly associated with this type of instruments

when used by some researchers. Ambiguous questions were carefully avoided so that

respondents would feel free and understand the questions being asked. The research work

also made used of anecdotal sources that is, the secondary sources.

Field Survey 2015

48

Page 59

3.6 INSTRUMENT VALIDATION

Validity as postulated by Tuckman (1978,p. 92) is concerned with measurement. It deals with

accuracy and effectiveness of the measuring instrument. Validity is the appropriateness of an

instrument in measuring what it tends to measure. The validity of a test is the extent to which

a test measures what is supposed to measure.

This research work was done by giving the draft questions to the teacher’s supervisor, in

which his comments were useful in establishing content validity of the instrument.

In the conclusion of the research questionnaire, the following steps were applied;

i. The determination of the information required

ii. Who were the respondents to answer the question

iii. Deciding on how to phrase the question

iv. Deciding on how to arrange the questionnaire

v. Deciding on how to administer the questionnaire

3.7 RELIABILTY OF THE INSTRUMENT

Reliability of a test instrument according to Ogbuoshi (2006, p. 91) is consistency of the test

in measuring whatever intends to measure. It involves the accuracy of both the process and

result of the measurement. Wherein, a measuring instrument is reliable if it provides the same

data when administered twice or more under the same/similar condition.

The question and interview are reliable because it has given the researcher the desired result.

The researchers tested the reliability of the instrument by using the same questionnaire to take

two separate measurements on the same population at different times. The correction between

the two instruments shows the reliability of the instrument.

49

Page 60

3.8 SOURCE OF DATA COLLECTION

The data for this study were obtained from two major sources- primary and secondary

sources of information.

The Primary Data: These are data obtained from the companies with the aid of some

prepared pieces of questionnaire.

Staff of the organizations directly answered the questionnaire. In addition oral interview were

conducted with some top- level managers, production managers and particularly the financial

accountants. Personal observation was also used.

The Secondary Data: These are data obtained from several sources; these include textbooks

on cost accounting, management accounting, personal management, finance, economics,

magazines, Journals and newspapers,

3.9 METHOD OF DATA ANALYSIS

The major statistical methods used for data analysis was T-students distribution analysis. A

simple percentage was also used m the preliminary stage of the analysis.

The T- students distribution is computed using the

Formula

t = (X-U) N

Where:

T = Calculated value

N Number of respondents

50

Page 61

X = Number of successes (yes)

U = Number of respondents multiplied by the assumed probability (NP)

= Standard deviation NP9

P = Is the same as 90% of confidence

Q = is the same as 10% level of error.

The procedure involved preparation of the T- student distribution are as follow:

1. Calculate t

2. Refer to the appropriate table for the desired significance level (which is 90% in the

research study) and find the value of that t. this value will be positive for upper tail

test and value negative for lower tail test.

3. Decision rule:

For upper and one tail test (tve), accept

Ho, if calculated value (t) is less than the t interval otherwise reject Ho if calculated t is

greater than the t internal.

The T student’s distribution has a relative frequency curve that is bell shaped as shown in

51

Page 62

Figure 3.1;

Lower tail test Upper tail test

-X +X

FIGURE 3.1 SKETCH OF T- STUDENTS DISTRIBUTION

52

Page 63

REFERENCES

• Argyris;. C. (1975) Human problem with Budgets Canada

Harvard Business Review Vol.2 No.4

• Anyanwu, B.E (1995) The Concept of internal Auditing,

Owerri: SEB publishing Ltd.

• Batterseby Albert (1980) A Guide to stock control

London: Pitman Publishing Ltd.

• Black, Chapin. and miller (1975) Principles of Accounting

3rd Edition USA: CBS College publishing.

• Brigham and papas (1976) Management Economics

London: Dryden Press.

• Breech, E. F. L. (1980) The Principles and Practice of Management London:

Longmanpublishers.

• Earnest L.N (1976) Variance Accounting, London:Prentice —Hall Press inc

• Evans, D. F (2003) Flexible Budgetary Control and Standard Costs. Dallas Texas Mac

Donald and Evans Ltd.

• Garrison, R.H(1979) Management Accounting U.S.A:Business publications Ltd.