26

RUCHIRA PAPERS LIMITED Investor Presentation July 2018

RUCHIRA PAPERS LIMITEDInvestor Presentation July 2018

Company Overview

Business Overview

Tabl

e of

Con

tent

s

2

Industry Overview

Financial Overview

Tabl

e of

Con

tent

s

Company Overview

3

About Us

Incorporated in 1980.We take great pride in

creating a quality range of‘Tree-Free’ papers for

writing, high-volume printand packaging

Writing & Printing paperfinds its applications in printing andstationery, comprising note books,

writing & publishing material, spiralnotebooks, greeting cards, coloring

books, colored copier paper, billbooks, dairies and calendars etc

Facilities located in HimachalPradesh for manufacturing ofKraft Paper and Writing and

Printing Paper

One of the Largest manufacturers of‘Kraft’ and ‘Writing & Printing’

paper in Northern India fromAgro Residue

Kraft paper contributed 43% torevenues in 2017-18

4

Writing & Printing paperfinds its applications in printing andstationery, comprising note books,

writing & publishing material, spiralnotebooks, greeting cards, coloring

books, colored copier paper, billbooks, dairies and calendars etc

Kraft paper finds its application inmanufacturing of corrugated boxes,

cartons and other packaging material

WPP contributed 57% torevenues in 2017-18

PAT growing at 25.77% CAGR

A low debt company withDebt to Equity ratio at

0.21x

Pan India presence through strongnetwork of distributors and dealers

Our Journey

2007-08:LaunchedWriting &Printing paperproduction in2008

Productionincreased byde-bottleneckingat variousintervals postfrom 2008 oncontinuousbasis

2015-16:Certified forFSC chain ofcustody byRainforestAlliance

2017-18: a)ImplementedModernizationand De-bottleneckingprogrammeeb) AnnouncedGreenfieldproject forWriting andPrinting Paperat ChamkaurSahib, Punjab,

5

Incorporatedin 1980

1983-CommencedCommercialproduction ofKraft Paperwith 2310 TPA

1992-1994 :PM-2 installedformanufacturingof Kraft Paperandproductioncapabilityincreased to21000 TPA

2006-07:Came up withan IPO and gotlisted on BSE& NSE.

2007-08:LaunchedWriting &Printing paperproduction in2008

Productionincreased byde-bottleneckingat variousintervals postfrom 2008 oncontinuousbasis

2015-16:Certified forFSC chain ofcustody byRainforestAlliance

2017-18: a)ImplementedModernizationand De-bottleneckingprogrammeeb) AnnouncedGreenfieldproject forWriting andPrinting Paperat ChamkaurSahib, Punjab,

Management Team

•Subhash Chander Garg, aged 76 years, is Law graduate and hasexpertise in field of taxation. He is one of the Promoters of RuchiraPapers Limited and has been looking after the affairs of the companyas a Whole Time Director. He has been looking after the Taxation,Marketing and Sales functions of Ruchira Papers Limited since itsinception and has acquired rich marketing experience.

Mr. Subhash ChanderGarg

(Co-Chairman & Whole TimeDirector)

•Jatinder Singh, aged 64 years, is an Engineering Graduate fromPunjab University. He is one of the Promoters of Ruchira PapersLimited and has been looking after the affairs of the company as aWhole Time Director. Over the years, he has acquired deep insightinto the working of Paper Industry. He has been looking afterthe Finance, Administration and Raw Material Procurement of thecompany.

Mr. Jatinder Singh(Chairman & Whole Time

Director)

6

•Subhash Chander Garg, aged 76 years, is Law graduate and hasexpertise in field of taxation. He is one of the Promoters of RuchiraPapers Limited and has been looking after the affairs of the companyas a Whole Time Director. He has been looking after the Taxation,Marketing and Sales functions of Ruchira Papers Limited since itsinception and has acquired rich marketing experience.

Mr. Subhash ChanderGarg

(Co-Chairman & Whole TimeDirector)

•Umesh Chander Garg, aged 69 years is a Graduate and has beenassociated with Ruchira Papers Limited right from the conceptualstage. He is controlling day-to-day affairs of the Company as theManaging Director. He has been the key man in the selection ofvarious machineries and all expansion projects were executed underhis guidance. He has been looking after the Production, Maintenanceand Technical aspects of the company.

Mr. Umesh ChanderGarg

(Managing Director)

•Mr. Vipin Gupta, aged 48 Years is working as professional Whole TimeDirector With the Company. He is heading the Finance and Accounts ofthe Company. He is associated with the Company for the past 26Years.. He is a Post Graduate in Commerce.

Mr. Vipin Gupta(CFO & Whole Time

Director)

Competitive Advantage

Diversified ProductPortfolio

Ruchira Papers hasdiversified into better

product mix across Kraftpaper and Writing &

Printing paper

Ruchira Papers hasdiversified into better

product mix across Kraftpaper and Writing &

Printing paper

Dedicated Workforce

The Company has a highlydedicated , skilled and

efficient employee base of1014

The Company has a highlydedicated , skilled and

efficient employee base of1014

Strong relations withCustomers and

suppliers

Understanding customerneeds, emerging trends

and accordingly providingproducts to customers isthe prime responsibility

Understanding customerneeds, emerging trends

and accordingly providingproducts to customers isthe prime responsibility

Strategic Location &PAN India Presence

Plant is located inHimachal Pradesh and

well connected to stateand national highways

Plant is located inHimachal Pradesh and

well connected to stateand national highways

Robust Balance sheet

Ruchira’s debt to equityratio is the modest in

the industry

Ruchira’s debt to equityratio is the modest in

the industry

7

Diversification helps de-risking of business in theevent of any volatility in

demand and prices

Diversification helps de-risking of business in theevent of any volatility in

demand and prices

Ruchira Papers providesextensive training to its

employees on skillbuilding

Ruchira Papers providesextensive training to its

employees on skillbuilding

Strong relations withsuppliers keeps the flow

of operations smooth

Strong relations withsuppliers keeps the flow

of operations smooth

The Company has a PANIndia distribution network

to market its products

The Company has a PANIndia distribution network

to market its products

Ruchira is comfortablyplaced in terms of short

term liquidity

Ruchira is comfortablyplaced in terms of short

term liquidity

Awards & Recognitions

Udyog Ratna Award by Himachal Pradeshin 2005 FSC Certificate (Forest Stewardship Council) from

Rain Forest Alliance, New York, USA ISO 9001 : 2015

8

Udyog Ratna Award by Himachal Pradeshin 2005 FSC Certificate (Forest Stewardship Council) from

Rain Forest Alliance, New York, USA ISO 9001 : 2015

Appreciation Award from Himachal PradeshCorrugated Box Manufactures Association in the

year 2009

Certificate of Excellencefrom INC 500 in 2013

Business Overview

9

Our Products

Manufactured by using agricultural residues, such as wheat straw, Baggase,sarkanda (80%-85%),Softwood Pulp (4% -5%) and other materials (10%-15%)

Writing and Printing paper is used in the fabrication of note books and writing &publishing material; coloured paper is used in the fabrication of spiral notebooks,wedding cards, shade cards, children’s colouring books, coloured copier paperand bill books

Contributed 57% of total revenues generated in FY2018 Writing and Printing paper brands are ‘Tarang’. ‘Safeda’, ‘Kora’, ‘Savera’, ‘Karigar’,

‘Gehua’, ‘Mela’, ‘Pahari

Writing & Printing Paper

10

Manufactured by using agriculture residues, such as Bagasse, wheat straw,sarkanda (50%-55%) and indigenous and imported waste paper(45% -50%)

Used in the packaging industry especially in making corrugated boxes / cartons andother packaging requirements

Special features of the Company’s Kraft Paper are the load bearing capacity andtensile strength, which make it suitable for corrugated packing applications.

Contributed 43% to the revenue in FY2018 Kraft paper brands include ‘Multani’, ‘Maati’, ‘Khadi’. Also manufactures special tube grade paper known as DTY and POY.

Kraft Paper

Plant Location & Capabilities

• Plant located at Kala Amb, in District Sirmaur of Himachal Pradesh

and well connected to state and national highways

• For Writing Paper & Printing unit the Company has set up 8.1 MW

Power Co-generation plant for captive purpose to get

uninterrupted power supply for its operations.

• The Company has set up ‘Chemical Recovery Plant’ for process of

black liquor generated during the process for captive consumption.

• The Company ‘s water requirement is sourced from ground water

through tube-wells.

11

• Plant located at Kala Amb, in District Sirmaur of Himachal Pradesh

and well connected to state and national highways

• For Writing Paper & Printing unit the Company has set up 8.1 MW

Power Co-generation plant for captive purpose to get

uninterrupted power supply for its operations.

• The Company has set up ‘Chemical Recovery Plant’ for process of

black liquor generated during the process for captive consumption.

• The Company ‘s water requirement is sourced from ground water

through tube-wells.

4970

6

4772

2

5402

1

5202

8 6642

6

6800

0

4079

1

4142

5

4338

7

4707

4

5053

1

4742

5

9049

7

8914

7

9740

8

9910

2 1169

57

1154

25

0

20000

40000

60000

80000

100000

120000

140000

FY13 FY14 FY15 FY16 FY17 FY18

In M

etric

Ton

nes

Kraft Writing Total

Production (In MT)

Industry Overview

12

Industry Highlights

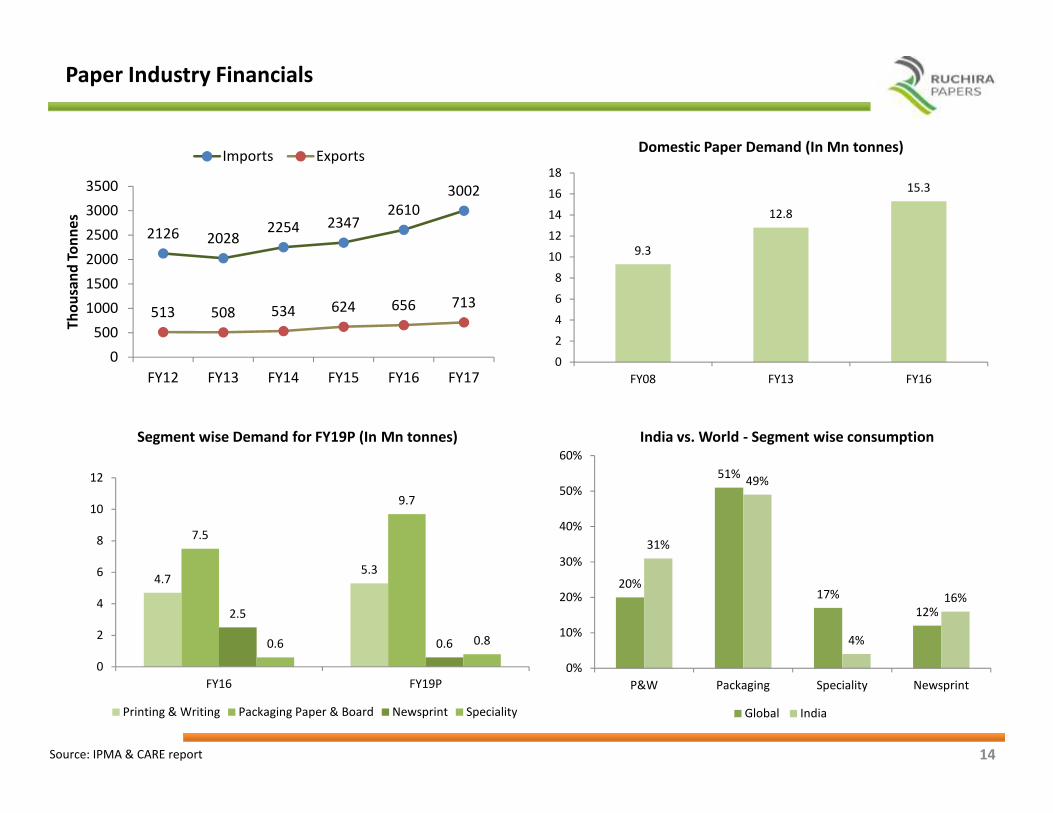

The domestic demand of paper in India has been growing at a CAGR of 6.6% and is likely to touch 18.5 million tonnes in 2018-19.

Of which, Printing and Writing segment demand is expected to grow at a CAGR of 4.2% and reach 5.3 million tonnes in FY19. ThePackaging Paper and Board segment is expected to grow at a CAGR of 8.9% and reach 9.7 million tonnes in FY19.

In spite of the sustained growth witnessed by the industry, the per capita paper consumption in India stands at a little over 13 kg which iswell below the global average of 57 kg and significantly below 200 kg in North America. This gap is a clear indication of the huge growthopportunity that lies ahead for the paper sector in India.

As per IPMA’s (Indian Paper Mills Association) estimates, this industry contributes approximately Rs 4,500 crore to the exchequer andprovides employment to over 5 lakh people across approximately 750 paper mills.

13

India's share of the Global PaperMarket

229

74

13

57

0

50

100

150

200

250

US China India World

Per Capita Consumption of Paper (kg)

20%

51%

17%12%

31%

49%

4%

16%

P&W Packaging Speciality Newsprint

World

India

India vs. World - Segment wise consumption

4%

96%

India Global

Source: IPMA & CARE report

Paper Industry Financials

2126 20282254 2347

26103002

513 508 534 624 656 713

0500

100015002000250030003500

FY12 FY13 FY14 FY15 FY16 FY17

Thou

sand

Tonn

es

Imports Exports

9.3

12.8

15.3

02468

1012141618

FY08 FY13 FY16

Domestic Paper Demand (In Mn tonnes)

14

4.75.3

7.5

9.7

2.5

0.60.6 0.8

0

2

4

6

8

10

12

FY16 FY19P

Printing & Writing Packaging Paper & Board Newsprint Speciality

Segment wise Demand for FY19P (In Mn tonnes)

20%

51%

17%12%

31%

49%

4%

16%

0%

10%

20%

30%

40%

50%

60%

P&W Packaging Speciality Newsprint

Global India

India vs. World - Segment wise consumption

Source: IPMA & CARE report

Demand Drivers-Indian Paper Industry

DemandDrivers

Rising incomelevels. Growing

per capitaexpenditure

Govt. boost to theeducation sector

& increasingliteracy rate

Rising circulation

Increase in the number of colleges and institutions, risingenrolment numbers, rising literacy (continuedgovernment spending on education through the SarvaShiksha Abhiyan) is expected to lead to an increasedexpenditure on textbooks, notebooks and other assortedpaper products thereby driving demand.

The per capita personal disposable income surged from Rs73,476 in FY12 to Rs. 1,19,296 in FY17 at a CAGR of 10.2%.Also, the per capita private final consumption expendituretoo rose from Rs 40,250 in FY12 to Rs.68,049 in FY17 at aCAGR of 11.1%. The growth in country’s per capita GDP inturn has increased the disposable income of the populaceultimately driving the country’s consumption.

15

DemandDrivers

Rapid urbanizationand increased

consumption byearning

population

Requirement ofbetter qualitypackaging of

FMCG productsmarketed through

organized retail

Aspirations of higher income, higher standard of living etc.has drawn more and more people from villages to settle intowns and cities. This transition from rural to urban areashas led to an increase in the demand. Earning populationshas grown from 55.4% to 66.2% which will driveconsumption going forward

As per the Audit Bureau of Circulation (ABC), thecirculation of print media reached 62 million copies a dayin 2016, implying a 10 year CAGR of nearly 5%.

Packaging needs of industries such as FMCG,Pharmaceuticals, Food & beverages, textiles etc. hasshown consistent growth over the last few years whichhas led to increased demand for packaging paper.

Source: Annual report & CARE report

Key Challenges-Indian Paper Industry

• Inadequate availability of rawmaterial domestically possesses amajor constraint for the IndianPaper Industry

• Dependence on imports of pulp,wastepaper and even pulpwood tomeet their raw material needs andoften have to pay premium whichimpacts profitability

• On account of cheaper imports thedomestic industry has facedchallenges in pricing its products.

• With FTAs and lower costs, importsare expected to continuechallenging the domestic industryin the medium term

Competitionfrom

imports

Access toquality and

costcompetitiveraw material

16

• Indian Paper Industry is largelyfragmented and is prone to usingoutdated technology

• Usage of outdated technology,both the raw material as well aspower consumption is higher ascompared to a modern paper mill

• Adverse changes in climate canaffect the business operations

• The paper industry market isextremely volatile and issusceptible to risks that arise fromchanges in demand, price,competition, customers, suppliersand raw materials.

Technology

Climatechange riskand Market

risk

Financial Overview

17

Quarterly Highlights

110.92

118.7

107.33

100102104106108110112114116118120

Q1FY19 Q1FY18 Q4FY18

*Revenue from Operations (Rs. In cr)

19.6322.51

12.97

0

5

10

15

20

25

Q1FY19 Q1FY18 Q4FY18

EBIDTA (Rs. In cr)

* Net of Excise

18

14.76

18.13

8.90

0

5

10

15

20

Q1FY19 Q1FY18 Q4FY18

PBT (Rs. In cr)

9.66

11.81

6.14

0

2

4

6

8

10

12

14

Q1FY19 Q1FY18 Q4FY18

PAT (Rs. In cr)

* Net of Excise

Q1FY19 Performance Highlights

Q1FY19 Performance Overview

• Revenue from operations stood at Rs. 110.92 cr;

• EBIDTA at Rs. 19.63 cr; EBIDTA margins stood at

Rs. 17.69 %

• PAT at Rs. 9.66 cr; PAT margins stood at Rs.

8.71%

• EPS stood at Rs. 4.30

Net Sales Realization:WPP: NSR was Rs. 55766/- PMT.

Kraft Paper: NSR was Rs. 25435/- PMT

Production highlights:WPP: Production during Q1FY19 was12392 MT.

Kraft Paper: Production during Q1FY19was 17785 MT

19

• Revenue from operations stood at Rs. 110.92 cr;

• EBIDTA at Rs. 19.63 cr; EBIDTA margins stood at

Rs. 17.69 %

• PAT at Rs. 9.66 cr; PAT margins stood at Rs.

8.71%

• EPS stood at Rs. 4.30

Net Sales Realization:WPP: NSR was Rs. 55766/- PMT.

Kraft Paper: NSR was Rs. 25435/- PMT

Commenting on the financial performance of the company Mr. Jatinder Singh, Chairman & Whole TimeDirector, Ruchira Papers Limited, said, “We are back on the track after the successful implementation ofmodernization programme undertaken during Q4 of FY18. Further in Kraft paper unit we have stabilizedour capabilities to manufacture the products which we had proposed during implementation ofmodernization and upgradation programme and have received good response for these value addedproducts manufactured by us. The quality of product of paper has been accepted in the market. We arehopeful to get the same reflected in topline and bottom-line of Q2 of FY19 onwards. It was a toughquarter no doubt however with value additions successfully implemented we are well on track”

Revenue Break-up & Margins

15.24%

11.40%

13.10%

15.33%

16.57%

7.68%8.50%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

200

250

300

350

400

450

500

Perc

enta

ge (%

)

Rs. I

n cr

ore

61.9

5%

58.8

1%

62.3

5%

62.1

9%

57.8

3%30.00%

40.00%

50.00%

60.00%

70.00%

Perc

enta

ge (%

)

20

320.13 346.56 362.58 417.1 447.6

4.77%

3.70%

5.37%

0.00%

2.00%

4.00%

6.00%

0

50

100

150

200

FY14 FY15 FY16 FY17 FY18

Perc

enta

ge (%

)

Rs. I

n cr

ore

Total Revenue EBIDTA Margins (%) PAT Margins (%)61

.95%

58.8

1%

62.3

5%

62.1

9%

57.8

3%

38.0

5%

41.1

9%

37.6

5%

37.8

1%

42.1

7%

0.00%

10.00%

20.00%

FY14 FY15 FY16 FY17 FY18

Perc

enta

ge (%

)

WPP (% of Revenue) Kraft Paper (% of Revenue)

Financial Performance

15.28 12.8319.47

32.0538.24

05

1015202530354045

FY14 FY15 FY16 FY17 FY18

PAT (Rs. In cr)

321.93 347.92 363.73418.10 451.35

050

100150200250300350400450500

FY14 FY15 FY16 FY17 FY18

Total Income (Rs. In cr)

21

25.42 20.4431.77

46.4458.31

0

10

20

30

40

50

60

70

FY14 FY15 FY16 FY17 FY18

PBT (Rs. In cr)

48.7939.82

47.4863.96

74.17

0

10

20

30

40

50

60

70

80

FY14 FY15 FY16 FY17 FY18

EBIDTA (Rs. In cr)

Key Ratios

15.93%

12.19%

16.13%

20.98% 19.98%

23.91%

19.61%21.39%

25.15% 25.06%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

FY14 FY15 FY16 FY17 FY18

ROE ROCE

22

FY14 FY15 FY16 FY17 FY18

0.51

0.28 0.28

0.22 0.21

0

0.1

0.2

0.3

0.4

0.5

0.6

FY14 FY15 FY16 FY17 FY18

Debt to Equity

3.89 4.07

7.46

8.74

11.37

0.00

2.00

4.00

6.00

8.00

10.00

12.00

FY14 FY15 FY16 FY17 FY18

Interest Coverage ratio

Production Highlights

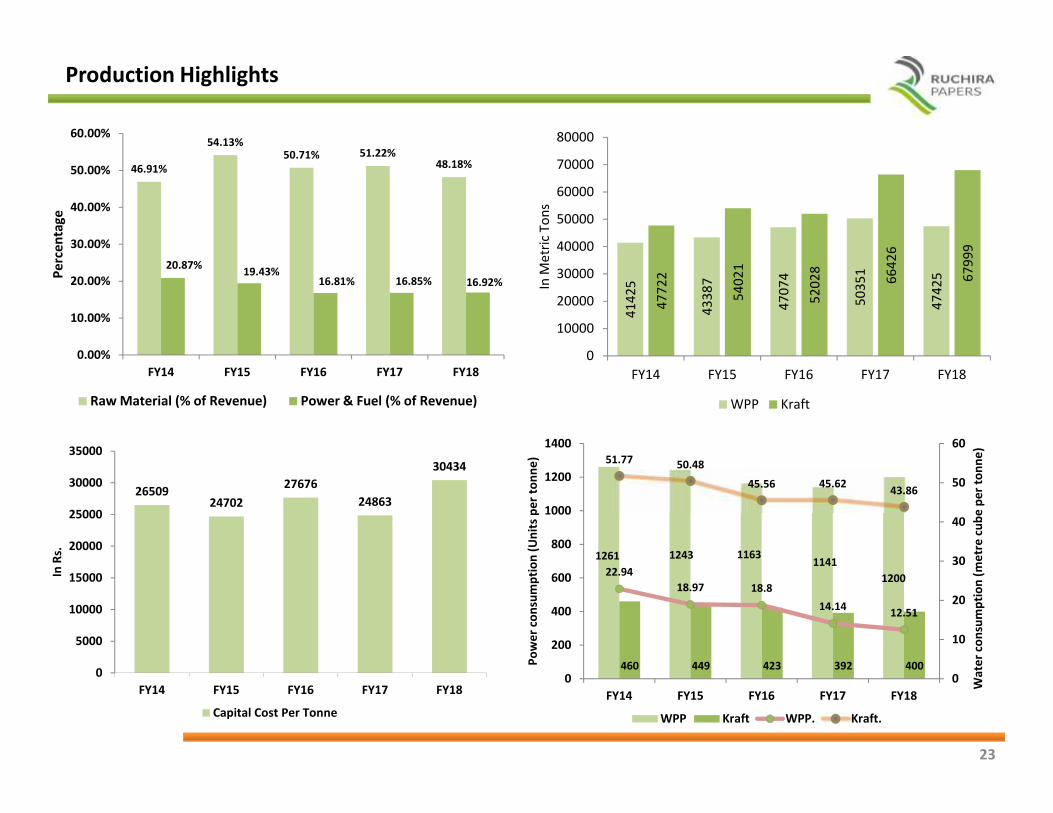

46.91%

54.13%50.71% 51.22%

48.18%

20.87% 19.43%16.81% 16.85% 16.92%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

FY14 FY15 FY16 FY17 FY18

Perc

enta

ge

Raw Material (% of Revenue) Power & Fuel (% of Revenue)

4142

5

4338

7

4707

4

5035

1

4742

5

4772

2

5402

1

5202

8

6642

6

6799

9

0

10000

20000

30000

40000

50000

60000

70000

80000

FY14 FY15 FY16 FY17 FY18

In M

etric

Ton

s

WPP Kraft

23

Raw Material (% of Revenue) Power & Fuel (% of Revenue) WPP Kraft

2650924702

2767624863

30434

0

5000

10000

15000

20000

25000

30000

35000

FY14 FY15 FY16 FY17 FY18

In R

s.

Capital Cost Per Tonne

1261 1243 1163 11411200

460 449 423 392 400

22.9418.97 18.8

14.14 12.51

51.77 50.48

45.56 45.62 43.86

0

10

20

30

40

50

60

0

200

400

600

800

1000

1200

1400

FY14 FY15 FY16 FY17 FY18

Wat

er co

nsum

ptio

n (m

etre

cube

per

tonn

e)

Pow

er co

nsum

ptio

n (U

nits

per

tonn

e)

WPP Kraft WPP. Kraft.

Key Statics & Shareholding as on 30th June, 2018

Key Investors (%) holding

Non Institutions::Dolly Khanna 1.51

61.14%

37.96%

Shareholding (%)

24

Key Statistics As on 31st July, 2018CMP (Rs.) 117.70

Market Cap (Rs. In crore) 263.90

No. of outstanding shares(Crore) 2.24

Face Value 10.00BSE Code 532785NSE Code RUCHIRA

61.14%

0.90%

Promoter & Promoter Group Institutions Non- Institutions

Disclaimer

This presentation and the following discussion may contain “forward looking statements” byRuchira Papers Limited (“Ruchira” or “RPL” or the “Company”) that are not historical innature. These forward looking statements, which may include statements relating to futureresults of operations, financial condition, business prospects, plans and objectives are basedon the current beliefs, assumptions, expectations, estimates and projections of themanagement of RPL about the business, industry and markets in which RPL operates.

These statements are not guarantees of future performance and are subject to known andunknown risks, uncertainties and other factors, some of which are beyond RPL’s control anddifficult to predict, that could cause actual results, performance or achievements to differmaterially from those in the forward looking statements.

Such statements are not and should not be construed as a representation of futureperformance or achievements of RPL. In particular, such statements should not be regardedas a projection of future performance of RPL. It should be noted that the actual performanceor achievements of RPL may vary significantly from such statements.

25

This presentation and the following discussion may contain “forward looking statements” byRuchira Papers Limited (“Ruchira” or “RPL” or the “Company”) that are not historical innature. These forward looking statements, which may include statements relating to futureresults of operations, financial condition, business prospects, plans and objectives are basedon the current beliefs, assumptions, expectations, estimates and projections of themanagement of RPL about the business, industry and markets in which RPL operates.

These statements are not guarantees of future performance and are subject to known andunknown risks, uncertainties and other factors, some of which are beyond RPL’s control anddifficult to predict, that could cause actual results, performance or achievements to differmaterially from those in the forward looking statements.

Such statements are not and should not be construed as a representation of futureperformance or achievements of RPL. In particular, such statements should not be regardedas a projection of future performance of RPL. It should be noted that the actual performanceor achievements of RPL may vary significantly from such statements.

Contact Details

Ruchira Papers Ltd.Mr. Vipin Gupta(CFO & Executive Director)Email: [email protected];

Mr. Vishav Sethi(Company Secretary)Email: [email protected]

Website : www.ruchirapapers.com

Concept Public Relations India Ltd.Mr. Pratik PatilMobile: 8291510324Email: [email protected]

Ms. Ankita VermaMobile: 8898422588Email: [email protected]

Website : www.conceptpr.com

CONCEPT IR

26

Ruchira Papers Ltd.Mr. Vipin Gupta(CFO & Executive Director)Email: [email protected];

Mr. Vishav Sethi(Company Secretary)Email: [email protected]

Website : www.ruchirapapers.com

Concept Public Relations India Ltd.Mr. Pratik PatilMobile: 8291510324Email: [email protected]

Ms. Ankita VermaMobile: 8898422588Email: [email protected]

Website : www.conceptpr.com

![Untitled-1 []...SRI CHAMKAUR SAHIB, DISTT. ROOPNAGAR Under the management of Shiromani Gurdwara Parbandhak Committee Paste Photograph Gender Male Female (if female, whether single](https://static.documents.pub/doc/80x56/5e552fd9de89c0528b582b38/untitled-1-sri-chamkaur-sahib-distt-roopnagar-under-the-management-of.jpg)