Page 1

NEW YORK | LONDON | DUBAI | MUMBAI | BANGALORE WWW.IBSINTELLIGENCE.COM

A CEDAR GROUP BUSINESS

SALES LEAGUE TABLE REPORT 2021

DEFINITIVE LANDSCAPE OF

BANKWIDE, RETAIL BANKING,

WHOLESALE BANKING, WEALTH

MANAGEMENT AND NEW SLT AREAS

ANALYSIS OF LEADERSHIP CLUB,

SLT SPECIAL AWARDS AND SLT

LEADERBOARD

Page 2

EEurope/ UKBerkeley Square House, Berkeley Square, London W1J6BD, UK, +44 (0) 207 887 7850

Middle East | DubaiP O Box 501807Building 3, Office 203, Dubai Internet City, Dubai, UAE

America | New York 250 Park Avenue, 7th Floor, New York, NY 10177, USA +1 212 5726314

Asia | Mumbai201 Tower A, Peninsula Business Park,Senapati Bapat Marg,Lower Parel, Mumbai 400013, India + 91 22 6171 98

Asia | BangaloreWeWork, Salarpuria Symbiosis Arekere, Begur HobliBannerghatta Road,Bengaluru, KA 560076, India

ABOUT IBS INTELLIGENCE

Established in 1991, UK headquartered IBS Intelligence is the world’s most trusted source ofFinancial Technology News, Research & Advisory. IBSI’s Sales League Table is considered theglobal industry barometer ranking leading banking technology suppliers. It’s research reportscomprehensively cover global suppliers across all Banking Technology & FinTech systems, isalso distributed by Thomson Reuters, Bloomberg and S&P Capital IQ. Its Innovation Lab atDubai brings banks and suppliers together with an opportunity to access the Middle Eastopportunity and to test & experience global FinTech products within the region.

Reach out to us today to learn how we can meet your Financial Technology needs, and addvalue to your business at [email protected]

For more information, visit www.ibsintelligence.com

OFFICES

ABOUT CEDAR MANAGEMENT CONSULTING

Cedar is a leading global consulting, research and analytics firm with network offices in 16countries, 500 professionals and over 1000 clients. Since 1985, its team has been assistingclients in the area of strategy, process, strategic human capital, and business technology. As ageneral management consulting firm, it is able to assist clients across these areas in anintegrated fashion – from formulation to execution. Its business intelligence unit CypressAnalytica provides innovative analytic solutions across industry sectors.

Reach out to us for queries at [email protected]

For more information, visit www.cedar-consulting.com/

© IBS Intelligence, 202 . All rights reserved. No part of this report may be copied, photocopied,reproduced, translated or reduced to any electronic medium or machine-readable form, in wholeor in part, without prior written consent of IBS Intelligence. Any other reproduction in any formwithout the permission of IBS Intelligence is prohibited. All materials contained in this documentare protected by United Kingdom copyright law and may not be reproduced, distributed,transmitted, displayed, published or broadcast without prior permission of IBS Intelligence.

Page 3

1

Contents List of Figures............................................................................................................................................................. 4

List of Tables .............................................................................................................................................................. 5

1.0 Introduction ........................................................................................................................................................ 6

1.1 IBSI Sales League Table Analysis – BackOffice Systems ....................................................................................... 7

1.2 IBSI SLT 2021 – BackOffice System | Quarterly Trends ....................................................................................... 8

1.3 IBSI SLT 2021 – BackOffice System | Hosted vs Licensed .................................................................................... 9

2.0 IBS Intelligence Annual Global Sales League Table | 2021 .............................................................................. 10

3.0 IBSI Sales League Table Analysis ....................................................................................................................... 16

4.0 BankWide .......................................................................................................................................................... 17

4.1 BankWide – Universal Banking | Core ............................................................................................................... 17

4.1.1 Market Trends ............................................................................................................................................ 17

4.1.2 Universal Banking | Core | Sales League Table .......................................................................................... 18

4.2 BankWide – Risk Management & Compliance Management ............................................................................ 20

4.2.1 Market Trends ............................................................................................................................................ 20

4.2.2 Risk Management | Sales League Table ..................................................................................................... 21

4.2.3 Compliance Management | Sales League Table ......................................................................................... 23

4.3 BankWide – CRM .............................................................................................................................................. 25

4.3.1 Market Trends ............................................................................................................................................ 25

4.3.2 CRM | Sales League Table........................................................................................................................... 26

5.0 Retail Banking ................................................................................................................................................... 27

5.1 Retail Banking – Retail Banking | Core .............................................................................................................. 27

5.1.1 Market Trends ............................................................................................................................................ 27

5.1.2 Retail Banking | Core | Sales League Table ................................................................................................ 28

5.2 Retail Banking – Lending | Retail ....................................................................................................................... 30

5.2.1 Market Trends ............................................................................................................................................ 30

5.2.2 Lending | Retail | Sales League Table ......................................................................................................... 30

5.3 Retail Banking – Digital Banking & Channels ..................................................................................................... 32

5.3.1 Market Trends ............................................................................................................................................ 32

5.3.2 Digital Banking & Channels | Sales League Table ....................................................................................... 33

5.4 Retail Banking – Payments | Retail .................................................................................................................... 35

5.4.1 Market Trends ............................................................................................................................................ 35

5.4.2 Payments | Retail | Sales League Table ..................................................................................................... 35

6.0 Wholesale Banking ............................................................................................................................................ 36

6.1 Wholesale Banking – Payments | Wholesale .................................................................................................... 36

6.1.1. Market Trends ........................................................................................................................................... 36

Page 4

2

6.1.2 Payments | Wholesale | Sales League Table .............................................................................................. 37

6.2 Wholesale Banking – Lending | Corporate ........................................................................................................ 38

6.2.1 Market Trends ............................................................................................................................................ 38

6.2.2 Lending | Corporate | Sales League Table ................................................................................................. 38

6.3 Wholesale Banking – Wholesale Banking | Treasury & Capital Market ............................................................ 39

6.3.1 Market Trends ............................................................................................................................................ 39

6.3.2 Wholesale Banking | Treasury & Capital Markets | Sales League Table .................................................... 41

6.4 Wholesale Banking – Wholesale Banking | Transaction Banking ...................................................................... 42

6.4.1 Market Trends ............................................................................................................................................ 42

6.4.2 Wholesale Banking | Transaction Banking | Sales League Table ............................................................... 42

7.0 Wealth Management ........................................................................................................................................ 44

7.1 Wealth Management – Private Banking & Wealth Management ..................................................................... 44

7.1.1 Market Trends ............................................................................................................................................ 44

7.1.2 Private Banking & Wealth Management | Sales League Table .................................................................. 45

7.2 Wealth Management – Investment & Fund Management ............................................................................... 46

7.2.1 Market Trends ............................................................................................................................................ 46

7.2.2 Investment & Fund Management | Sales League Table ............................................................................. 47

8.0 New SLT Areas ................................................................................................................................................... 48

8.1 Conversational Banking ..................................................................................................................................... 48

8.1.1 Market Trends ............................................................................................................................................ 48

8.1.2 Conversational Banking | Sales League Table ............................................................................................ 48

8.2 New SLT Areas – DataWarehouse & Business Intelligence ............................................................................... 49

8.2.1 Market Trends ............................................................................................................................................ 49

8.2.2 DataWarehouse & Business Intelligence | Sales League Table .................................................................. 49

8.3 New SLT Areas – InsurTech ................................................................................................................................ 50

8.3.1 Market Trends ............................................................................................................................................ 50

8.3.2 InsurTech | Sales League Table .................................................................................................................. 50

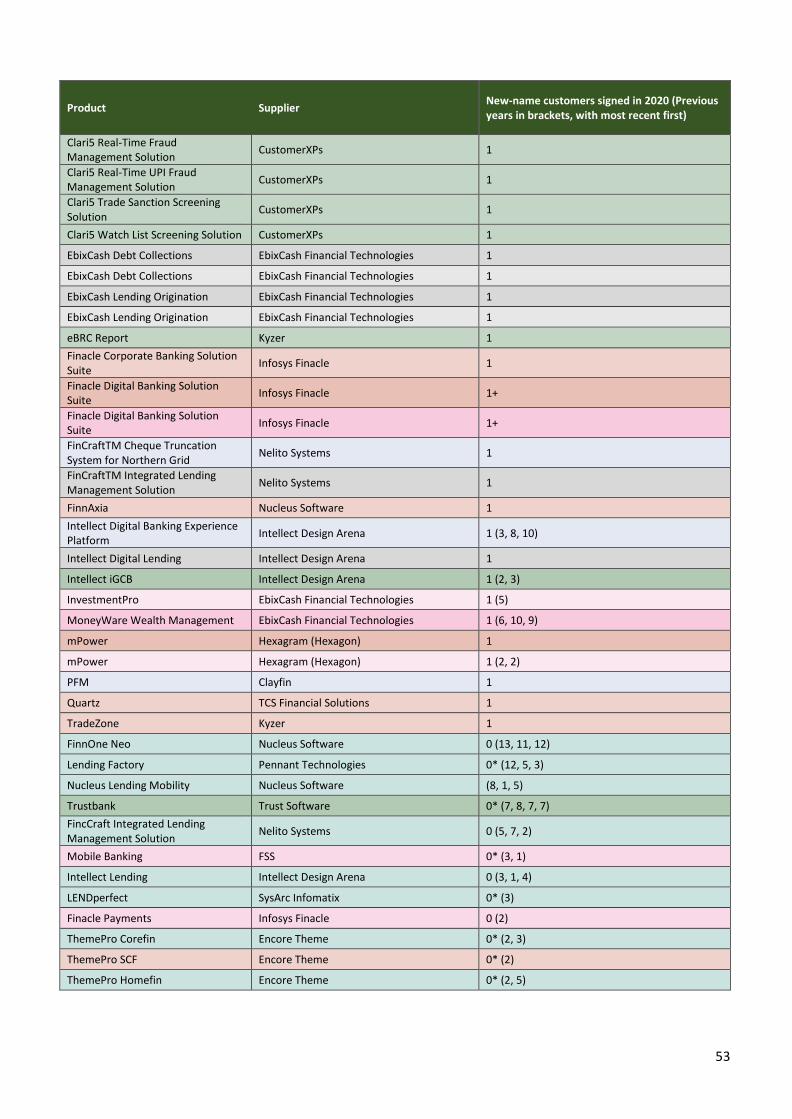

9.0 IBSI SLT 2021 – Domestic Sales League Table | India ...................................................................................... 51

9.1 Market Trends ............................................................................................................................................... 51

9.2 Domestic Sales League Table | India ............................................................................................................. 52

10.0 IBSI SLT 2021 – Domestic Sales League Table | USA ...................................................................................... 56

10.1 Market Trends ............................................................................................................................................. 56

10.2 Domestic Sales League Table | USA ............................................................................................................ 58

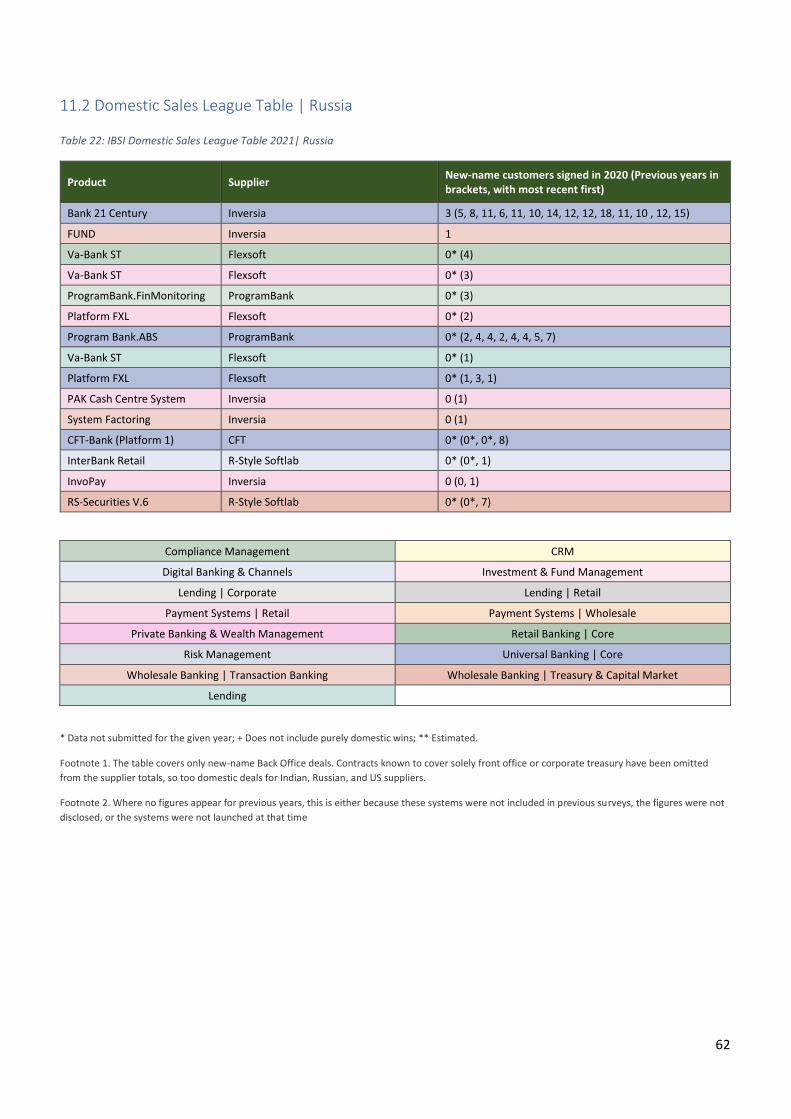

11.0 IBSI SLT 2021 – Domestic Sales League Table | Russia .................................................................................. 61

11.1 Market Trends ............................................................................................................................................. 61

11.2 Domestic Sales League Table | Russia ......................................................................................................... 62

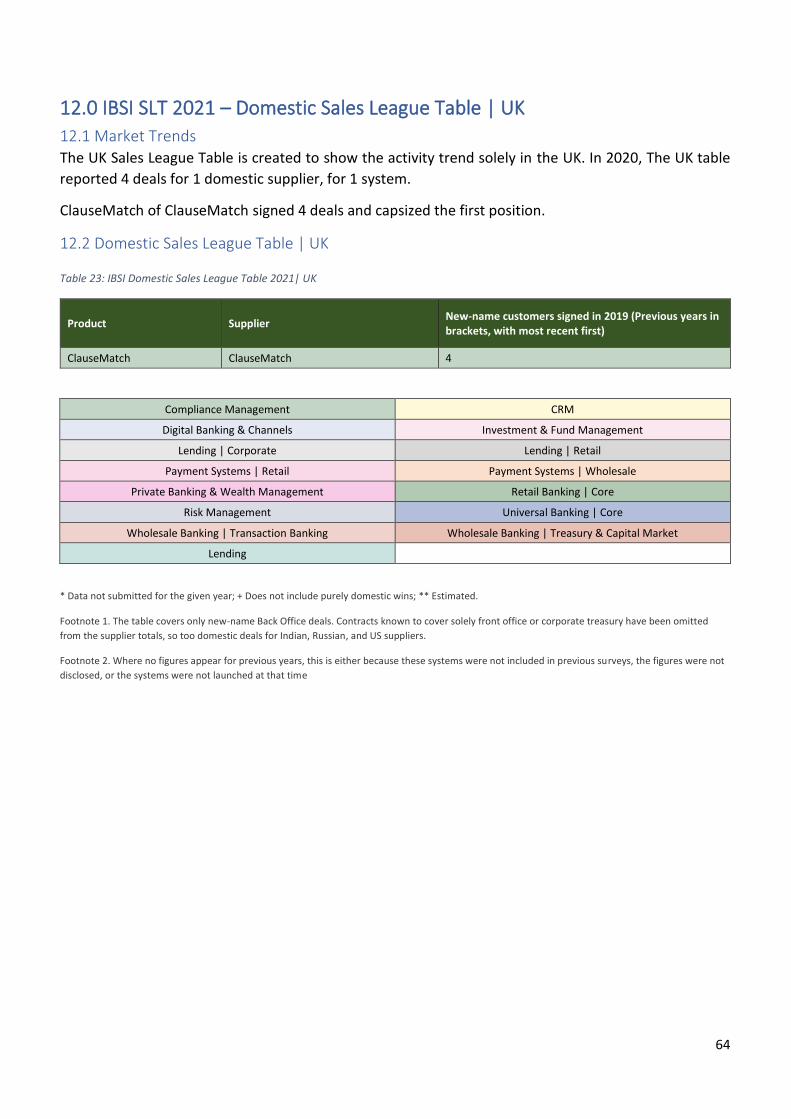

12.0 IBSI SLT 2021 – Domestic Sales League Table | UK ........................................................................................ 64

Page 5

3

12.1 Market Trends ............................................................................................................................................. 64

12.2 Domestic Sales League Table | UK .............................................................................................................. 64

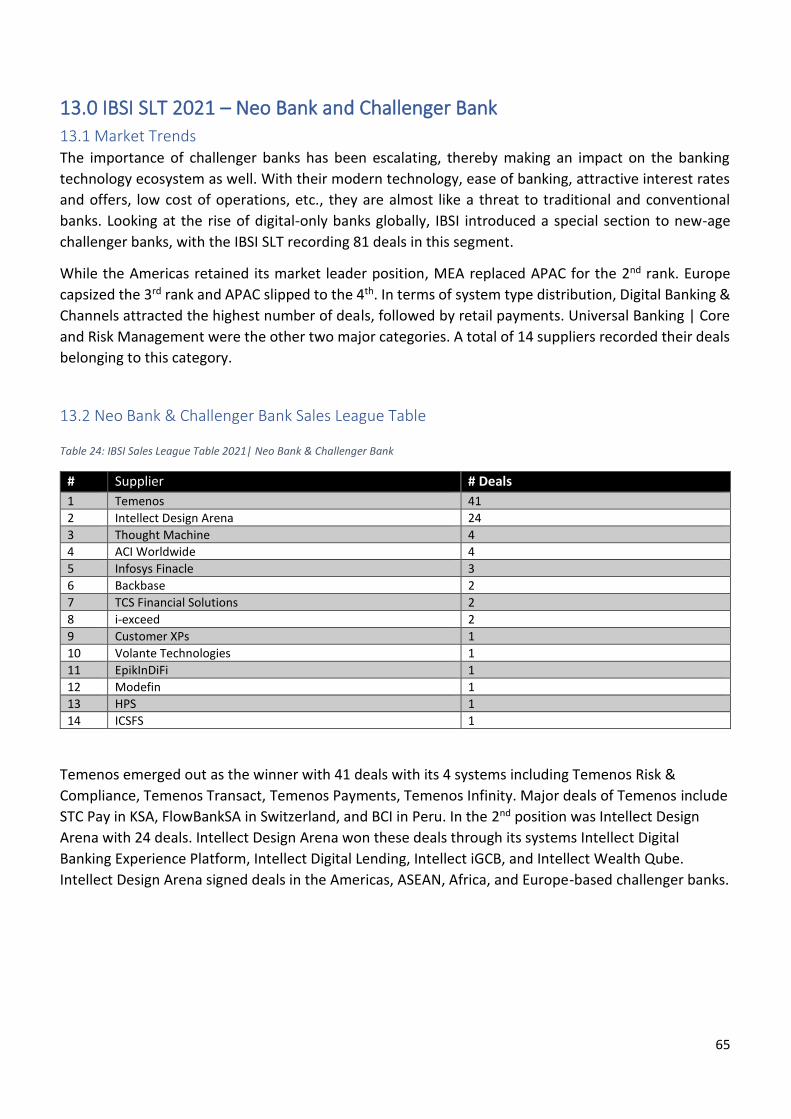

13.0 IBSI SLT 2021 – Neo Bank and Challenger Bank ............................................................................................. 65

13.1 Market Trends ............................................................................................................................................. 65

13.2 Neo Bank & Challenger Bank Sales League Table ........................................................................................ 65

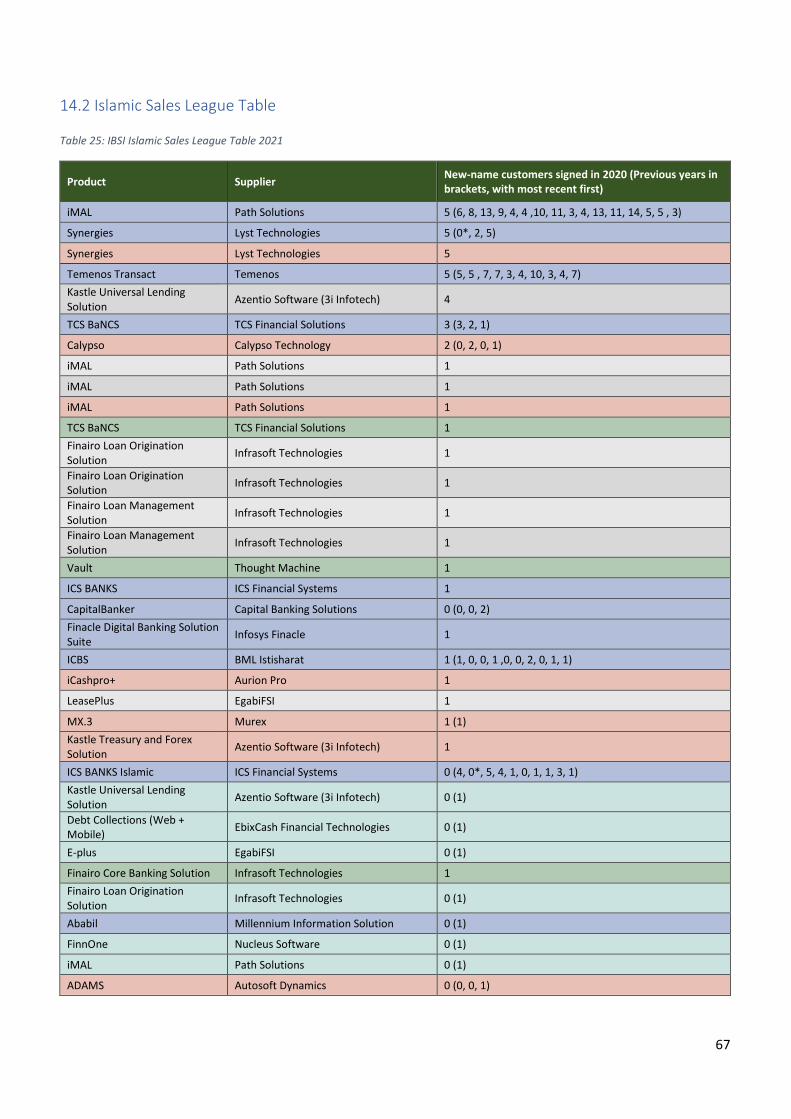

14.0 IBSI SLT 2021 – Islamic Sales League Table .................................................................................................... 66

14.1 Market Trends ............................................................................................................................................. 66

14.2 Islamic Sales League Table ........................................................................................................................... 67

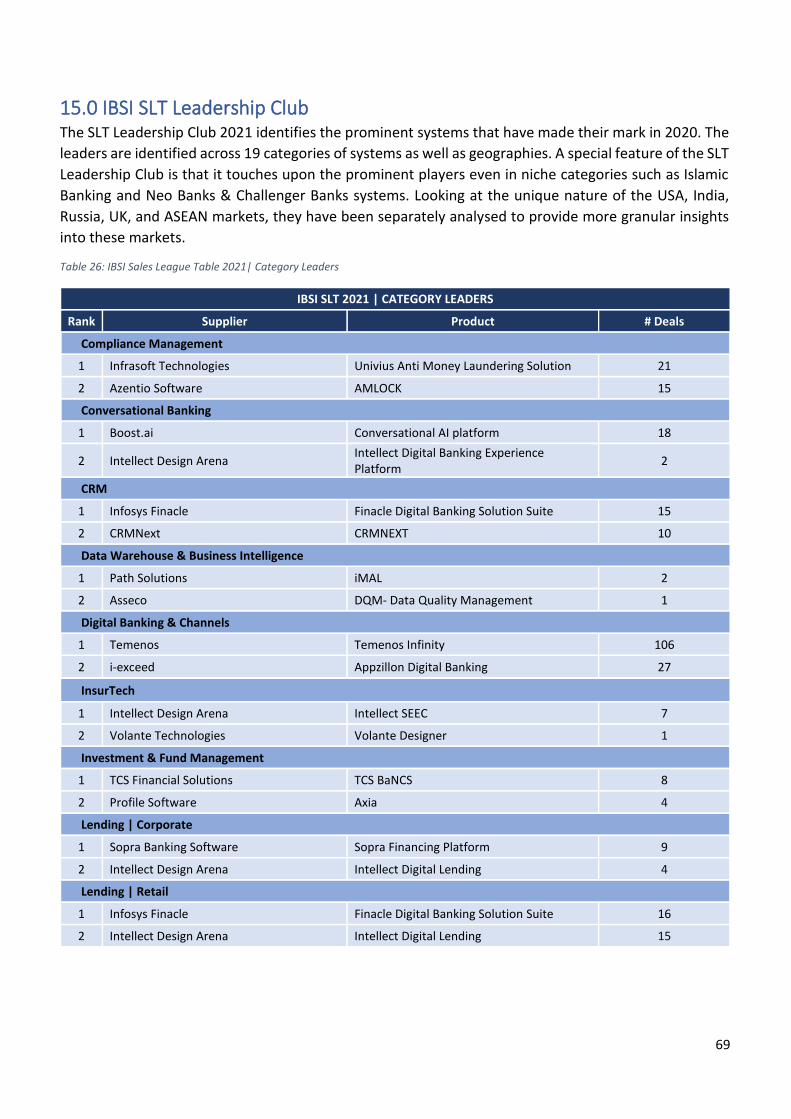

15.0 IBSI SLT Leadership Club ................................................................................................................................. 69

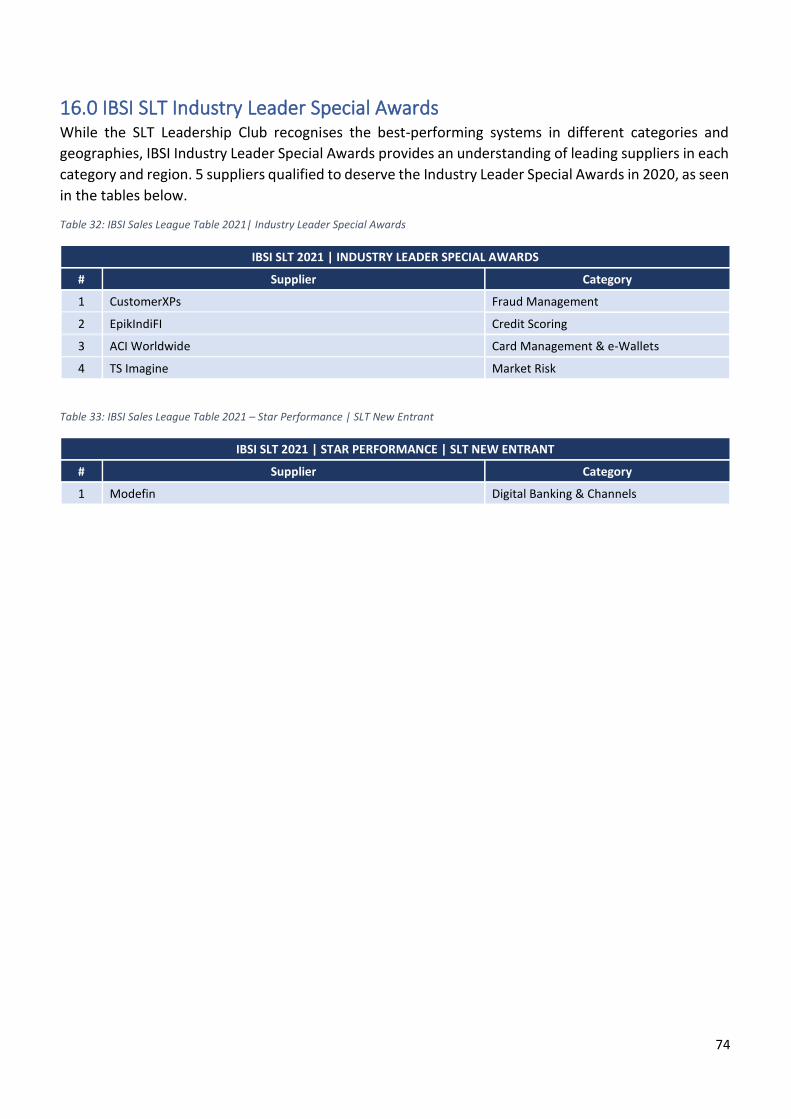

16.0 IBSI SLT Industry Leader Special Awards ........................................................................................................ 74

17.0 IBSI SLT LeaderBoard ...................................................................................................................................... 75

17.1 Universal Banking | Core ............................................................................................................................. 75

17.2 Retail Banking | Core ................................................................................................................................... 76

17.3 Wholesale Banking ...................................................................................................................................... 77

17.4 Private Banking & Wealth Management ..................................................................................................... 78

17.5 Lending......................................................................................................................................................... 79

17.6 Digital Banking & Channels .......................................................................................................................... 80

17.7 Payments ..................................................................................................................................................... 81

18.0 Conclusion ....................................................................................................................................................... 83

Page 6

4

List of Figures Figure 1: Total BackOffice System Sales: 2016-2020 ................................................................................................. 7

Figure 2: BackOffice System | Quarterly Trend for 2020 .......................................................................................... 8

Figure 3: BackOffice System | Hosted vs Licensed Trend for 2020 ........................................................................... 9

Figure 4: IBSI Sales League Table Analysis ............................................................................................................... 16

Figure 5: Market Trend for Universal Banking | Core: Geographic Break-up ......................................................... 17

Figure 6: Universal Banking | Core: Deals by Supplier 2016 – 2020 ....................................................................... 19

Figure 7: Market Trend for Risk & Compliance: Geographic Break-up ................................................................... 20

Figure 8: 2020 Deals Analysis – Risk Management .................................................................................................. 22

Figure 9: 2020 Deals Analysis – Compliance Management ..................................................................................... 24

Figure 10: Market Trend for CRM: Geographic Break-up ........................................................................................ 25

Figure 11: CRM: Deals by Supplier 2016 – 2020 ...................................................................................................... 26

Figure 12: Market Trend for Retail Banking | Core: Geographic Break-up ............................................................. 27

Figure 13: Retail Banking | Core: Deals by Supplier 2016 – 2020 ........................................................................... 29

Figure 14: 2020 Deals Analysis – Lending | Retail ................................................................................................... 31

Figure 15: Digital Banking & Channels: Deals by Supplier 2016 – 2020 .................................................................. 34

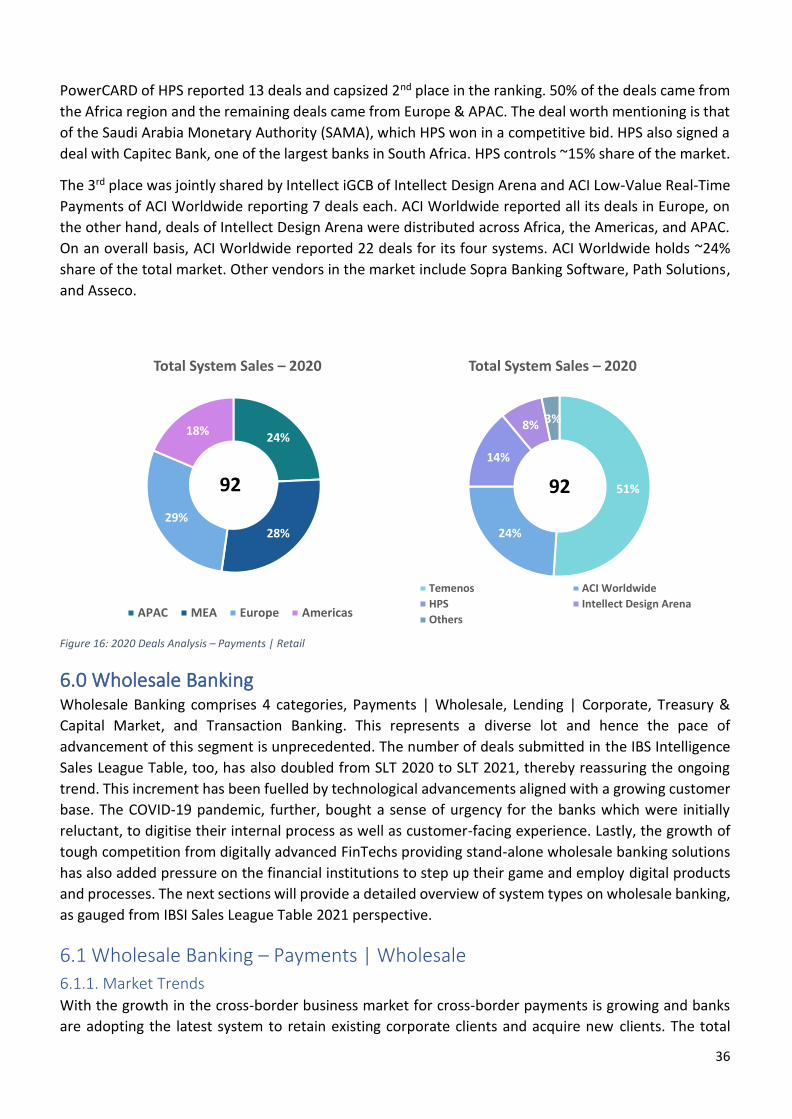

Figure 16: 2020 Deals Analysis – Payments | Retail ................................................................................................ 36

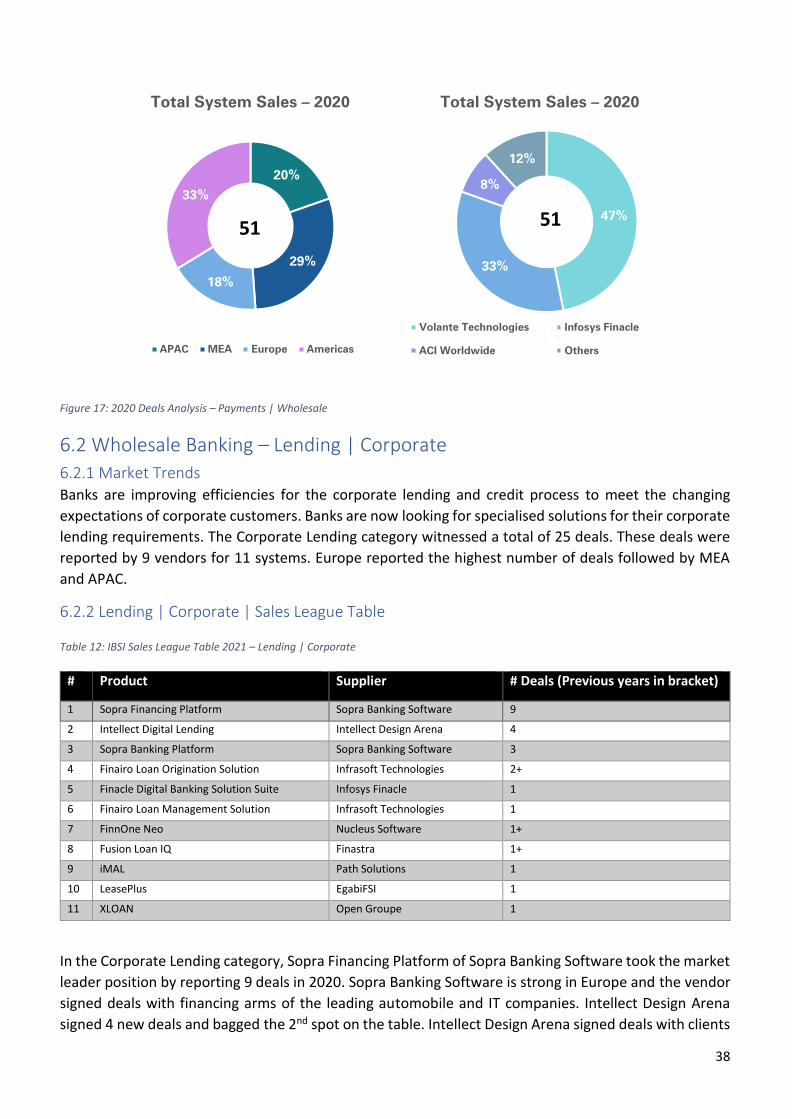

Figure 17: 2020 Deals Analysis – Payments | Wholesale ........................................................................................ 38

Figure 18: 2020 Deals Analysis – Lending | Corporate ............................................................................................ 39

Figure 19: 5-year Market Trend for Wholesale Banking | Treasury & Capital Markets: Geographic Break-up ...... 40

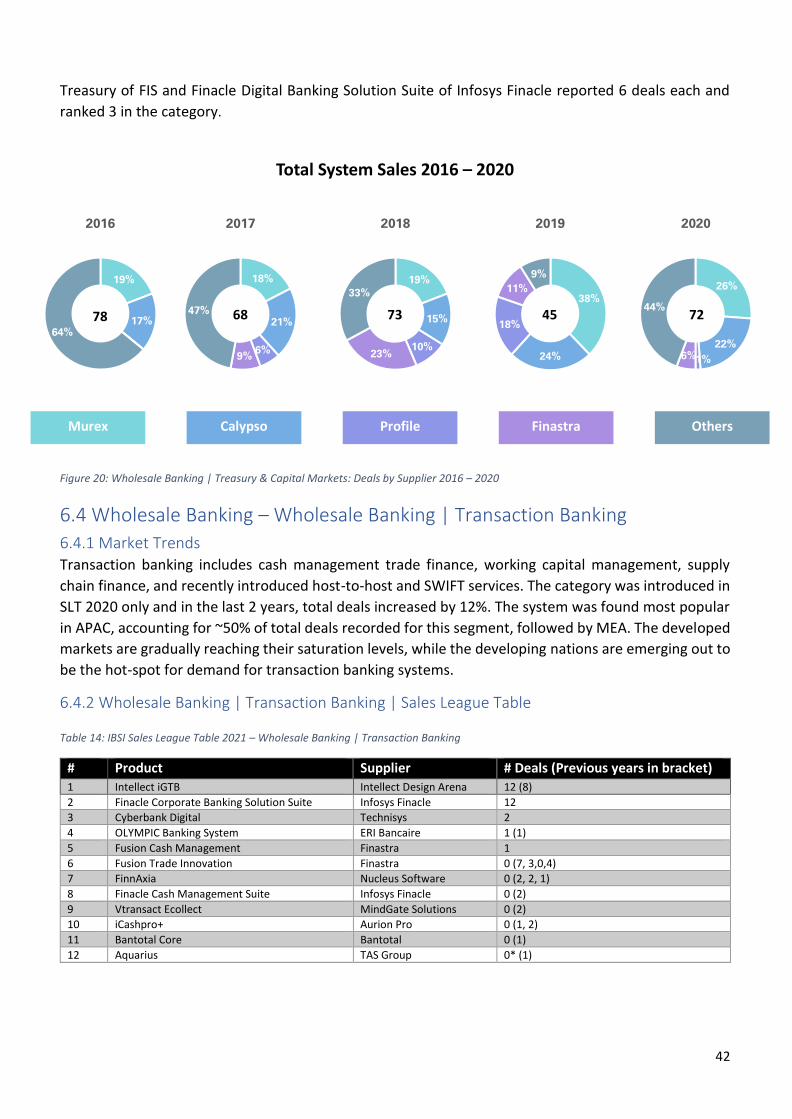

Figure 20: Wholesale Banking | Treasury & Capital Markets: Deals by Supplier 2016 – 2020 ............................... 42

Figure 21: 2020 Deals Analysis – Wholesale Banking | Transaction Banking .......................................................... 43

Figure 22: Market Trend for Private Banking & Wealth Management: Geographic Break-up ............................... 44

Figure 23: Private Banking & Wealth Management: Deals by Supplier 2016 – 2020 ............................................. 45

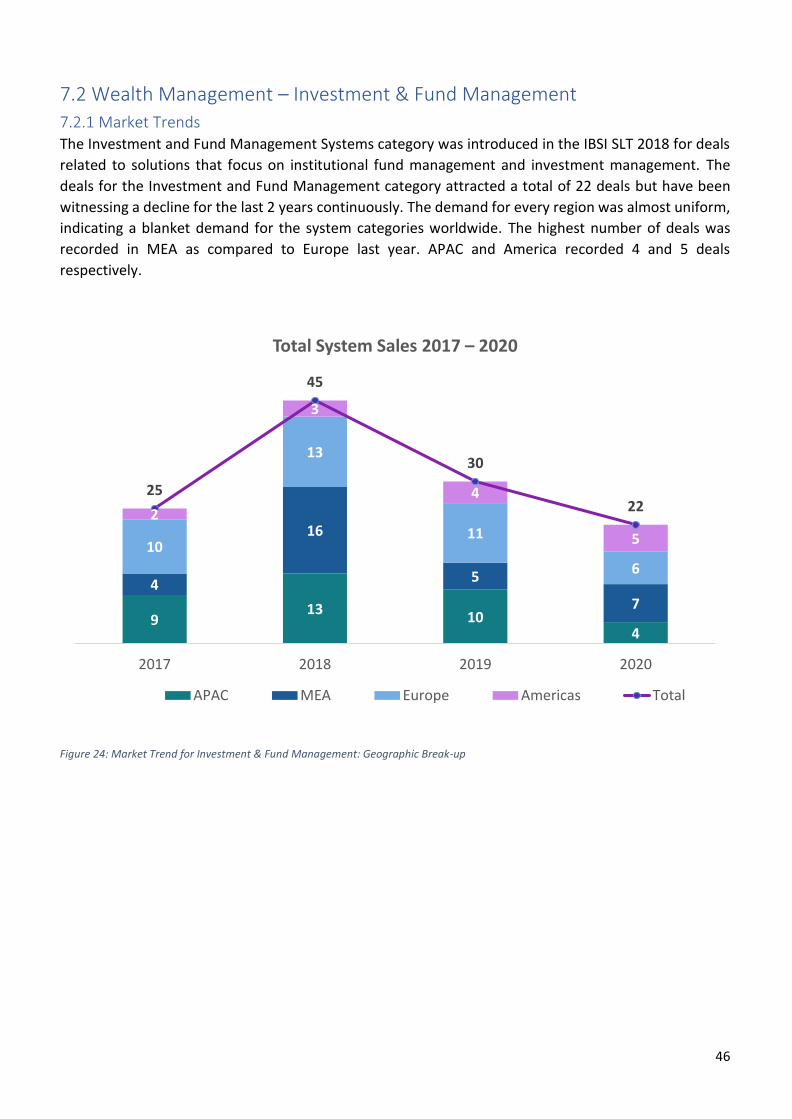

Figure 24: Market Trend for Investment & Fund Management: Geographic Break-up .......................................... 46

Figure 25: Private Banking & Wealth Management: Deals by Supplier 2016 – 2020 ............................................. 47

Figure 26: 2020 Deals Analysis – Conversational Banking ....................................................................................... 48

Figure 27: 2020 Deals Analysis – DataWarehouse & Business Intelligence ............................................................ 49

Figure 28: 2020 Deals Analysis – InsurTech ............................................................................................................. 50

Figure 29: Market Trend for Domestic Sales League Table | India ......................................................................... 51

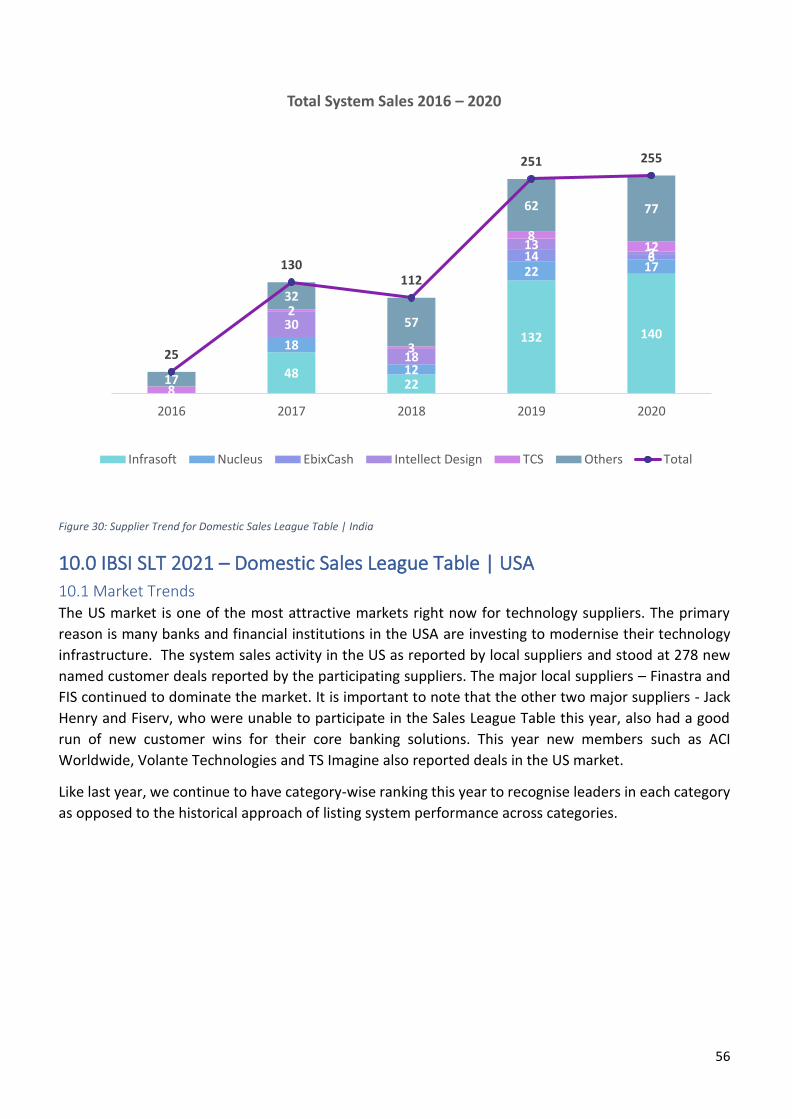

Figure 30: Supplier Trend for Domestic Sales League Table | India ........................................................................ 56

Figure 31: Market Trend for Domestic Sales League Table | USA ........................................................................... 57

Figure 32: Supplier Trend for Domestic Sales League Table | USA ......................................................................... 60

Figure 33: Market Trend for Domestic Sales League Table | Russia ....................................................................... 61

Figure 34: Supplier Trend for Domestic Sales League Table | Russia ...................................................................... 63

Figure 35: Supplier Trends for Islamic Sales League Table ...................................................................................... 66

Figure 36: IBSI LeaderBoard – Universal Banking | Core ......................................................................................... 75

Figure 37: IBSI LeaderBoard – Retail Banking | Core ............................................................................................... 76

Figure 38: IBSI LeaderBoard – Wholesale Banking .................................................................................................. 77

Figure 39: IBSI LeaderBoard – Private Banking & Wealth Management ................................................................. 78

Figure 40: IBSI LeaderBoard – Lending .................................................................................................................... 79

Figure 41: IBSI LeaderBoard – Digital Banking & Channels ..................................................................................... 80

Figure 42: IBSI LeaderBoard – Payments ................................................................................................................. 81

Figure 43: IBSI LeaderBoard – Risk & Compliance ................................................................................................... 82

Page 7

5

List of Tables Table 1: IBSI Sales League Table 2021 | Annual Global Sales League Table ............................................................ 10

Table 2: Categories in IBSI SLT 2021 ........................................................................................................................ 15

Table 3: IBSI Sales League Table 2021 – Universal Banking | Core ......................................................................... 18

Table 4: IBSI Sales League Table 2021 – Risk Management .................................................................................... 21

Table 5: IBSI Sales League Table 2021 – Compliance Management ........................................................................ 23

Table 6: IBSI Sales League Table 2021 – CRM .......................................................................................................... 26

Table 7: IBSI Sales League Table 2021 – Retail Banking | Core ............................................................................... 28

Table 8: IBSI Sales League Table 2021 – Lending | Retail ........................................................................................ 30

Table 9: IBSI Sales League Table 2021 – Digital Banking & Channels ...................................................................... 33

Table 10: IBSI Sales League Table 2021 – Payments | Retail ................................................................................... 35

Table 11: IBSI Sales League Table 2021 – Payments | Wholesale ........................................................................... 37

Table 12: IBSI Sales League Table 2021 – Lending | Corporate ............................................................................... 38

Table 13: IBSI Sales League Table 2021 – Wholesale Banking | Treasury & Capital Markets ................................. 41

Table 14: IBSI Sales League Table 2021 – Wholesale Banking | Transaction Banking ............................................ 42

Table 15: IBSI Sales League Table 2021 – Private Banking & Wealth Management ............................................... 45

Table 16: IBSI Sales League Table 2021 – Investment & Fund Management .......................................................... 47

Table 17: IBSI Sales League Table 2021 – Conversational Banking ......................................................................... 48

Table 18: IBSI Sales League Table 2021 – DataWarehouse & Business Intelligence ............................................... 49

Table 19: IBSI Sales League Table 2021 – InsurTech ................................................................................................ 50

Table 20: IBSI Domestic Sales League Table 2021| India ........................................................................................ 52

Table 21: IBSI Domestic Sales League Table 2021| USA .......................................................................................... 58

Table 22: IBSI Domestic Sales League Table 2021| Russia ...................................................................................... 62

Table 23: IBSI Domestic Sales League Table 2021| UK ............................................................................................ 64

Table 24: IBSI Sales League Table 2021| Neo Bank & Challenger Bank .................................................................. 65

Table 25: IBSI Islamic Sales League Table 2021 ....................................................................................................... 67

Table 26: IBSI Sales League Table 2021| Category Leaders .................................................................................... 69

Table 27: IBSI Sales League Table 2021| Neo Banks & Challenger Banks ............................................................... 71

Table 28: IBSI Sales League Table 2021| Regional Leaders ..................................................................................... 71

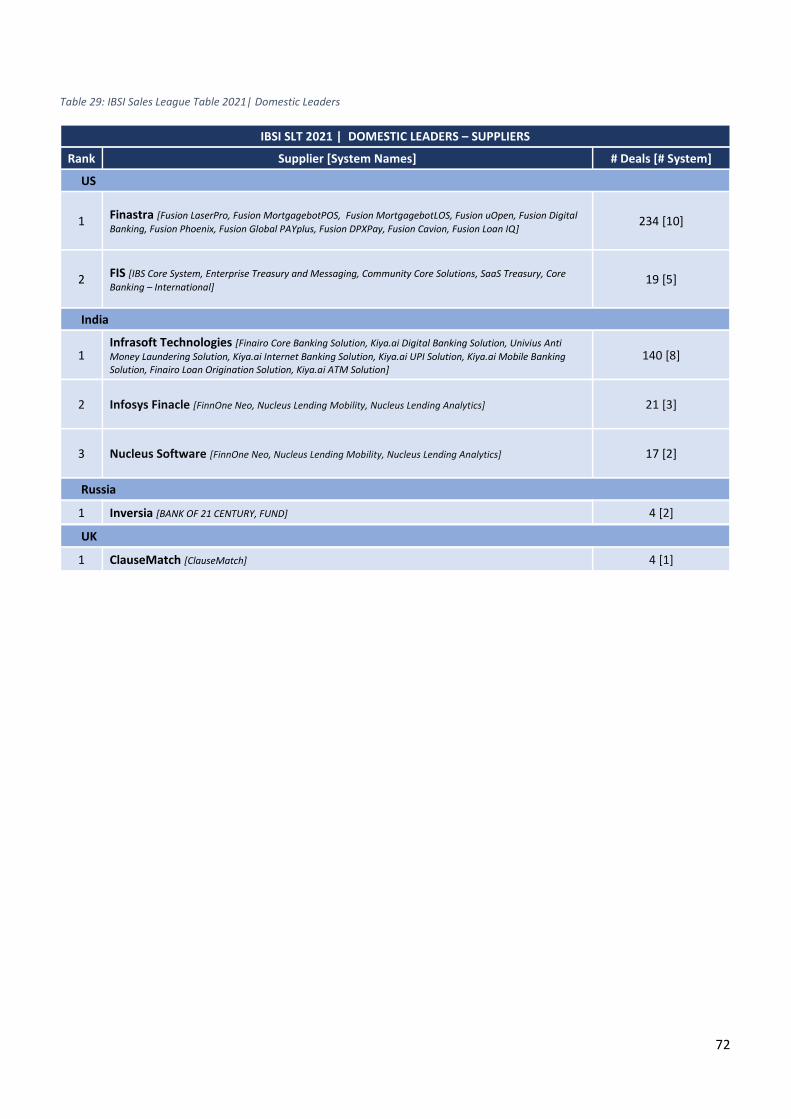

Table 29: IBSI Sales League Table 2021| Domestic Leaders .................................................................................... 72

Table 30: IBSI Sales League Table 2021 – Global Leadership | Product Breadth .................................................... 73

Table 31: IBSI Sales League Table 2021 – Global Leadership | Geographic Spread ................................................ 73

Table 32: IBSI Sales League Table 2021| Industry Leader Special Awards .............................................................. 74

Table 33: IBSI Sales League Table 2021 – Star Performance | SLT New Entrant ..................................................... 74

Page 8

6

1.0 Introduction

IBS Intelligence has been reviewing the conventional and new-age banking systems selections on a year-by-year basis for the last 20 years. The iconic IBSI Sales League Table (SLT) has been a barometer for measuring supplier performance across hundreds of system selection engagements that are carried out across the globe.

To ensure that reporting is consistent and comparable across systems and geographies, the SLT excludes license renewals as well as extensions to the current license (new geography, new functionality, etc.) and is restricted to the pre-defined categories – i.e., the core and back-office systems that are addressed across Universal, Wholesale (Transaction and Treasury & Capital Market), Retail, Private and Lending (Retail and Corporate) system categories, and systems falling in the Digital Banking Channels, Payments (Retail and Wholesale), Risk Management, Compliance Management, Investment & Fund Management, InsurTech, Conversational Banking, Datawarehouse & Business Intelligence, and CRM categories. The SLT is limited to financial institution sales and is compiled annually from submissions made from each supplier, which are independently verified. Key to note here is that the Sales League Table does not distinguish between large and small deals, considering these have more to do with the volume of the deals won during the year across system types and geographies and are not a function of value. The domestic deals of the US, India, UK, and Russia have also been excluded from the Global Sales League Table for apparent reasons. They have been represented separately in the Domestic Sales League Tables.

IBSI has been pioneering the Annual Sales League Table, which has come to be recognised as the barometer for measuring the sales performance of global suppliers, across all back-office systems. The data collated over time has allowed IBSI to compare each year’s banking systems market performance and analyse trends across years both in terms of system sales and geographic focus. The analysis constitutes the industry’s only real picture of who has been buying what and where; and would seem to be particularly useful when you delve into the detail. This is the key purpose of this report. Comparisons can be made over time, by supplier, geography, type, and size of the institution. It is a single-point repository to compare performance from a global perspective.

The Sales League Table Report is developed based on the details submitted by over 60 suppliers who are ranked on the SLT, which also captures the details of their wins.

Page 9

7

1.1 IBSI Sales League Table Analysis – BackOffice Systems Core Banking continues to remain at the heart of the bank, the general focus on technology investments

has shifted towards specialized solutions that help a bank enhance its market presence rapidly and

improve overall customer experience. A monolithic universal banking system is a thing of the past, and

the general strategy adopted by most banks is to opt for the best-of-breed solution for each of their

business area. This was evident in the new customer deal activity reported for the conventional back-

office system categories during the last 2 years.

The total volume of global new-name customer deals for BackOffice categories continued to grow in

2019 & 2020. The total deal count stood at 425 in 2020, recording a strong growth from 360 deals

reported in 2019. While the overall number of deals for Universal Banking is stable but deals in Lending

Systems and Wholesale Banking are fuelling the overall market. As banks are going for the best-of-breed

specialised solution, the market witnessed growth in overall deals in Retail Banking as well.

Deal submissions to the IBSI Sales League Table 2021 reminded us that conventional back-office systems

such as retail banking systems, treasury, lending, wealth management systems, and of course, the all-

encompassing universal banking systems are growing. Moreover, with 425 deals, 2020 reported the

highest number of new deals in the last 5 years. Retail Banking systems came up as the shining star as

total deals in this space grew by more than 50% as compared to 2019. Retail Banking system suppliers

reported 58 new customer deals in 2020 as compared to 38 new customer deals in 2019. Private Banking

systems reported a decline in the total number of deals, while overall deals in Universal Banking

remained stable.

Figure 1: Total BackOffice System Sales: 2016-2020

* Lending includes 2 Categories – Lending | Corporate and Lending | Retail

* Private includes 2 Categories – Private Banking & Wealth Management and Investment & Fund Management

* Wholesale includes 2 Categories – Wholesale Banking | Transaction Banking and Wholesale Banking | Treasury & Capital Market

Universal Retail Wholesale Lending Private

48%

21%

5%

15%

12%

2016

43%

19%

10%

13%

14%

2017

32%

22%10%

14%

21%

2018

32%

19%11%

24%

14%

2019

362 350 328 360

27%

24%14%

25%

11%

2020

425

Total BackOffice System Sales 2016 – 2020

Page 10

8

1.2 IBSI SLT 2021 – BackOffice System | Quarterly Trends

Figure 2: BackOffice System | Quarterly Trend for 2020

The trend in terms of the volume of overall deal activity for the year remained the same as last year,

with the fourth quarter being particularly active as compared to the other quarters. At the region level,

the fourth quarter was the most active period for the APAC and contributed to ~39% of the total deals

of the year. In Europe, ~40% of the total deals were recorded in the fourth quarter while for others, the

percentage remained ~30% for the same period.

While the fourth quarter was consistently the most active period for all regions, it is interesting to note

that in MEA, the third quarter was equally active with many of the large banking deals getting signed in

the third quarter.

In APAC region second quarter of the year was also active as the second quarter is the financial year-end

in many Asian countries and banks spend their budgets during that time.

Q1

▪ Temenos signs deal with KSA based STC Pay. STC Pay is a digital secure wallet designed to offer optimal level of speed and convenience to its customers

▪ Azentino Software wins deals with KSA based National Finance House and Murabaha Marina Financing Company for Lending | Retail

▪ EpikInDiFi signs deal with Australia based Goulburn Murray Credit Union Cooperative Ltd, which caters to local communities

19%

Q2 ▪ Thought Machine signs deals with

Monese, a UK based challenger bank

▪ Open Groupe wins deal with France based Initiative Ile de France

19%

Q3

▪ Intellect Design Arena wins Wholesale Banking deal with First Abu Dhabi Bank, the largest bank in the United Arab Emirates

▪ Sopra Banking Software wins deal with Advans Cameroun of France

▪ Avaloq wins major Private Banking & Wealth Management deal with Degroof Petercamof Belgium

27%

Q4 ▪ TCS wins a Universal Banking |

Core deal with Bitcoin Suisse of Switzerland

▪ MIMICS, Inc wins Private Banking & Wealth Management deal with Home Mortgage Bank Trinidad

35%

Page 11

9

1.3 IBSI SLT 2021 – BackOffice System | Hosted vs Licensed

Figure 3: BackOffice System | Hosted vs Licensed Trend for 2020

The percentage of conventional banking system deals hosted on the cloud increased to 34% of total

conventional deals as compared to 30% in 2019. Most of the cloud-based installations were in Europe

followed by APAC and the Americas. Out of the total cloud-based installations, ~66% of installations were

in APAC and Europe, while the share of the Americas and the MEA stood at ~23% and ~11% respectively.

It is interesting to note that Universal Core Banking solutions accounted for more than 30% of total

hosted deals, while Lending accounted for ~30% of total hosted deals.

This trend reflects the growing number of challenger banks which operate with cloud-native technology

infrastructure.

284 283 266 245 260

77 6762 109

134

0

50

100

150

200

250

300

350

400

2016 2017 2018 2019 2020

Hosted vs Licensed 2016 – 2020

Licensed Hosted

60%

60%

87%

78%

66%

40%

40%

13%

22%

34%

0% 20% 40% 60% 80% 100%

Private

Lending

Wholesale

Retail

Universal

Hosted vs Licensed in 2020 by Category

Licensed Hosted

Page 12

10

2.0 IBS Intelligence Annual Global Sales League Table | 2021 Table 1: IBSI Sales League Table 2021 | Annual Global Sales League Table

Product Supplier New-name customers signed in 2020 (Previous years in brackets, with most recent first)

Temenos Transact Temenos 48 (51, 43, 45, 43,34, 37, 35, 34, 27, 38, 40, 40, 44, 40, 32, 28, 24, 32, 36, 42, 34, 33, 19, 15, 10, 29, 7, 9)

MX.3 Murex 19 (17, 14, 12, 15, 11, 12, 9, 8, 9, 7, 11, 12, 15, 5)

Intellect iGCB Intellect Design Arena 18+ (14+, 7+)

Finacle Digital Banking Solution Suite Infosys Finacle 17+

Calypso Calypso Technology 16 (11, 11, 14, 13, 15, 14, 9, 14, 12, 19, 15, 14, 22, 14, 15, 8, 6, 7, 2, 3, 1)

Finacle Digital Banking Solution Suite Infosys Finacle 16+

Intellect Digital Lending Intellect Design Arena 15+

Sopra Banking Platform Sopra Banking Software 13

Lend.Ezee EpikInDiFi 11+

TCS BaNCS TCS Financial Solutions 11+ (15+, 13+, 18+, 17+, 11, 8+ ,8, 9+, 13+, 13+, 17+, 23, 31, 25, 14, 8 , 6*, 9, 10, 10, 6, 8, 6, 9, 5)

Sopra Financing Platform Sopra Banking Software 9

Avaloq Banking Software Avaloq 6 (7, 3, 3, 2, 5, 8 ,4, 9, 3, 7, 3, 5, 6, 4, 5, 1, 5 , 2, 1, 7)

COBIS Cobiscorp 6 (0, 3)

Finacle Digital Banking Solution Suite Infosys Finacle 6+

Kastle Universal Lending Solution Azentino Software (3i Infotech) 6 (5+)

SaaS Treasury FIS 6+

Vault Thought Machine 6 (1)

Enterprise Treasury and Messaging FIS 5+

iMAL Path Solutions 5 (6, 7, 13, 9, 4, 4 ,10, 11, 3, 4, 13, 11, 14, 5, 5 , 3)

Synergies Lyst Technologies 5 (0*, 2, 5)

Synergies Lyst Technologies 5

Intellect Digital Lending Intellect Design Arena 4

Intellect Treasury Intellect Design Arena 4

Mortgage plus EgabiFSI 4

Bantotal Internet Banking Bantotal 3

BX CBP Bankware Global 3 (1, 1, 2)

BX PF Bankware Global 3

ConsumerPlus EgabiFSI 3

Core Banking - International FIS 3+

Cyberbank Core Technisys 3

Intellect Wealth Qube Intellect Design Arena 3

Loxon Collection System Loxon 3 (3, 0, 2)

PowerBanker Capital Banking Solutions 3 (3, 0, 1)

Prospero Wealth Management Finartis 3 (3, 4)

Quartz TCS Financial Solutions 3

Sopra Banking Platform Sopra Banking Software 3

Sopra Banking Platform Sopra Banking Software 3

ANT – Audit Objectway 2

Bantotal Core Bantotal 2 (2, 5, 3, 2, 5, 3 ,5, 3, 5)

CapitalBanker Capital Banking Solutions 2 (2, 0, 3, 0*, 1, 2 ,2, 3, 4, 3)

Page 13

11

Product Supplier New-name customers signed in 2020 (Previous years in brackets, with most recent first)

CapitalPrivate Capital Banking Solutions 2 (0, 2, 4)

EbixCash Debt Collections EbixCash Financial Technologies 2+

EbixCash Lending Management EbixCash Financial Technologies 2

EbixCash Lending Origination EbixCash Financial Technologies 2+

Finairo Loan Origination Solution Infrasoft Technologies 2+

Finairo Loan Origination Solution Infrasoft Technologies 2+

FinnOne Neo Nucleus Software 2+ (8+, 6+, 7+, 5, 3 ,8, 7, 14, 27, 13, 17, 16, 17, 11, 9)

Fusion Kondor Finastra 2 (4)

Fusion Summit Finastra 2

ICBS BML Istisharat 2 (3, 2, 2, 1, 4, 1 ,3, 1, 3, 3, 6, 6, 5, 5, 3, 4, 3, 2, 3, 5, 3, 4)

ICS BANKS ICS Financial Systems 2 (1, 0*, 7, 9, 3, 0, 5, 4, 5, 5, 8, 6, 10, 11)

Sopra Financing Platform Sopra Banking Software 2

TCS BaNCS TCS Financial Solutions 2

Acumen-net Profile Software 1 (6, 7, 4)

Avaloq Banking Software Avaloq 1

Avaloq Banking Software Avaloq 1 (0, 0, 1)

Axia Profile Software 1 (1, 2, 0, 1)

BankPLus EgabiFSI 1

BANQIN Bank Genie 1

Bantotal Core Bantotal 1

Bantotal Internet Banking Bantotal 1

Bantotal Digital Onboarding Bantotal 1

Blenderpay TM Blender 1

CapitalBanker Capital Banking Solutions 1

CapitalBanker Capital Banking Solutions 1

Cyberbank Core + Digital Technisys 1

Cyberbank Digital Technisys 1 (1)

Eximius PMS Objectway 1 (2)

Finacle Digital Banking Solution Suite Infosys Finacle 1

Finacle Digital Banking Solution Suite Infosys Finacle 1+

Finairo Loan Management Solution Infrasoft Technologies 1

Finairo Loan Management Solution Infrasoft Technologies 1

Finairo Microfinance Solution Infrasoft Technologies 1

FinnOne Neo Nucleus Software 1+

FinnOne Nucleus Software 1

FMS.next Profile Software 1

Fusion CreditQuest Finastra 1 (2+, 1)

Fusion Essence Finastra 1 (5, 2, 4, 5, 4, 3 ,2, 2, 4, 6, 1, 2)

Fusion Loan IQ Finastra 1+

Fusion Phoenix Finastra 1+

Helios Objectway 1

iCashpro+ Aurion Pro 1

ICBS BML Istisharat 1

iMAL Path Solutions 1

Page 14

12

Product Supplier New-name customers signed in 2020 (Previous years in brackets, with most recent first)

iMAL Path Solutions 1

iMAL Path Solutions 1

Kastle Treasury and Forex Solution Azentino Software (3i Infotech) 1+

LeasePlus EgabiFSI 1

LFI – Latam FIS 1

MicrofinancePLus EgabiFSI 1 (0, 4)

MIMICS Financial Software MIMICS, Inc 1

MoneyWare Wealth Management EbixCash Financial Technologies 1+ (1+, 3+, 4, 18, 7)

OLYMPIC Banking System ERI Bancaire 1

OLYMPIC Banking System ERI Bancaire 1

Standalone crypto assets platform Avaloq 1

XLOAN Open Groupe 1

Sopra Financing Platform Sopra Banking Software 0 (11, 13, 12, 14)

Finacle Core Banking Infosys Finacle 0 (10+, 13+, 15+, 17+, 16, 9, 9, 14+, 12+, 8+, 14+, 14, 13, 3*, 13, 14, 9, 8, 11, 9, 2)

Sopra Banking Platform Sopra Banking Software 0 (10, 0, 6, 10, 4, 2 ,2, 5, 2, 7, 3, 4, 3, 7, 3, 5, 2, 5, 1, 1, 3)

Fusion LenderComm Finastra 0 (7)

Intellect Lending Intellect Design Arena 0 (7+, 3, 7+, 10, 5, 3 ,0, 1, 2, 2, 0, 2, 3, 4)

Systematics FIS 0 (7+, 3, 0+, 1+, 0, 0 ,0, 0, 0, 0, 1, 1, 0+, 0, 2, 1, 8, 7, 7, 0*)

Nucleus Lending Mobility Nucleus Software 0 (6+, 2)

E-plus EgabiFSI 0 (5)

Close Servicing Davinci 0* (4)

Fusion Markets Finastra 0 (4, 4, 0*, 2, 5, 3, 4, 5, 3, 7, 9, 19, 25, 15, 8)

ICS BANKS Islamic ICS Financial Systems 0 (4)

OLYMPIC Banking System ERI Bancaire 0 (4, 1, 3, 2, 2, 3 ,1, 2, 3, 3, 5, 2, 9, 7, 4, 6, 3, 14, 18, 18, 24, 23, 25)

Debt Collection EbixCash Financial Technologies 0 (3)

Finacle Treasury Infosys Finacle 0 (3+, 2)

Finairo Loan Origination Solution Infrasoft Technologies 0 (3+, 6+)

AutoCREDIT Autosoft Dynamics 0 (2)

Axia Profile Software 0 (2)

Close Origination Davinci 0* (2)

Finacle Origination Infosys Finacle 0 (2)

Finairo Microfinance Solution Infrasoft Technologies 0 (2)

Finairo Core Banking Solution Infrasoft Technologies 0 (2+, 0*, 0, 1)

FinCraft Core Banking Solution Nelito Systems 0 (2, 1, 1)

FincCraft Integrated Lending Management Solution

Nelito Systems 0 (2+)

Fusion Equation Finastra 0 (2, 1)

Profile Core System FIS 0 (2, 4, 0+, 0+, 0, 2 ,3, 5, 4, 3, 4, 5, 8, 3, 2, 1, 2, 5, 4, 12*)

Vanguard (Loan Orignation Platform) EpikInDiFi 0 (2+)

ADAMS Premium Autosoft Dynamics 0 (1, 1, 1)

COBIS Retail Cobiscorp 0 (1, 3, 3, 9, 0, 0 ,3, 1, 1, 2)

Retail & Corporate Lending Origination EbixCash Financial Technologies 0 (1)

Finacle Wealth Management Solution Infosys Finacle 0 (1, 4)

Page 15

13

Product Supplier New-name customers signed in 2020 (Previous years in brackets, with most recent first)

FinXEdge Collect Infosys Finacle 0 (1)

Fusion MortgagebotPOS Finastra 0 (1+)

Fusion Opics Finastra 0 (1, 8, 5, 7, 3, 1 ,4, 6, 18, 5, 15, 11, 11, 6, 6, 8, 14, 8, 25, 25, 15, 25, 24, 9, 8, 7, 5)

Bankway Core System FIS 0 (1+)

Core 24 Core System FIS 0 (1, 1)

Ababil Millennium Information Solution

0 (1)

MIMICS Core Processing System MIMICS, Inc 0 (1)

F-Lease Open Groupe 0 (1)

Marylease Open Groupe 0 (1)

iMAL Path Solutions 0 (1, 1)

SAB AT Sopra Banking Software 0 (1, 1, 2, 5, 2, 2 ,8, 7, 2, 2, 6, 2, 7, 6, 8)

LENDperfect SysArc Infomatix 0* (1+)

Cyberbank Core Technisys 0 (1, 2, 2, 0*, 0, 0 ,1*, 1*)

Pennant Lending Factory Pennant Technologies 0* (0+, 0+, 1)

Abanks Grupo ASI 0 (0, 0*, 0*, 5)

Altimis Objectway 0 (0, 0, 0, 1)

Ambit Quantum FIS 0 (0, 0, 5+, 11, 8, 10, 9, 7, 8, 8, 8, 15, 5, 9, 1*, 14, 6, 19, 6)

AutoBANKER Premium (formerly Autobanker II)

Autosoft Dynamics 0 (0, 1, 1, 0*, 0, 1 ,2, 3, 1, 1, 0, 0, 0, 0, 1, 2, 1, 1)

Avaloq Banking Suite Avaloq 0 (0, 1)

OLYMPIC Banking System ERI Bancaire 0 (0, 1)

Bank 21 Century Inversia 0 (0, 0+, 0+, 5+, 11, 10,14,12,12,18,11,10,12,15)

Bantotal Microfinance Bantotal (0, 1, 0*, 1)

BX CBP Bankware Global (0, 2)

CashTrea Credence Analytics 0 (0*, 0+, 3)

COBIS Sales & Service Suite Cobiscorp 0 (0, 2)

CorePlus Probanx 0* (0*, 7, 8, 0*, 4, 2)

e-IBS Datapro 0 (0*, 0*, 2, 5, 3, 6 ,7, 1, 2, 8, 6)

Ethix International Turnkey Systems (ITS)

0* (0*, 3, 0*, 4, 0*, 5 ,1, 4, 3)

Eximius Objectway 0 (0, 4, 2, 3)

Extend Objectway 0 (0, 0, 1)

Finacle Liquidity Management solution Infosys Finacle 0 (0, 1)

Finairo Lending Management Solution Infrasoft Technologies 0 (0, 6+)

FinCraft Enterprise Reporting Nelito Systems 0 (0, 0+, 0, 2)

FinCraft Lending Nelito Systems 0 (0, 0, 0+, 1)

Flexcube Oracle FSS 0* (0*, 0*, 0*, 0*, 28, 27, 15, 17+, 28, 32, 33+, 39+, 20**, 43, 37, 36)

FMS.next Profile Software 0 (0, 0, 1)

Fusion Post-Trade Finastra 0 (0, 2)

Horizon FIS 0 (0, 0+, 0+, 3+)

IBS FIS 0 (0, 0+, 0+, 1+)

iDeal Credence Analytics 0 (0*, 0+, 0+, 7+)

IMSplus Profile Software 0 (0, 0, 2, 5, 6, 1 ,1, 1, 2)

Integrity FIS 0 (0, 0, 3+, 1+)

Page 16

14

Product Supplier New-name customers signed in 2020 (Previous years in brackets, with most recent first)

Intellect Digital Core Intellect Design Arena 0 (0, 0+, 10+, 8)

Intellect DTB Intellect Design Arena 0 (0, 6)

Intellect Liquidity Management Intellect Design Arena 0 (0, 2, 4)

Intellect OneTREASURY Intellect Design Arena 0 (0, 0, 3)

Intellect Quantum Core Banking Intellect Design Arena 0 (0, 0, 1)

Intellect Wealth Management Intellect Design Arena 0 (0, 2, 1, 1, 0, 0 ,0, 1, 1, 1, 0, 4, 0, 3)

Loans Management SAP 0* (0*, 0*, 2, 0*, 9, 2 ,8, 7, 3, 8, 8, 15, 17, 7, 3, 4, 2)

Mercury FIS 0 (0, 0+, 1, 1)

PROFITS® Integrated Core Banking System Intrasoft International 0* (0, 2, 8, 0*, 1, 1 ,1, 3, 0, 0)

RS-Bank R-Style Softlab 0* (0*, 2)

SAP Inclusive Banking SAP 0* (0*, 0*, 1)

SAP Leasing SAP 0* (0*, 0*, 1)

SAP Transactional Banking SAP 0* (0*, 0*, 10)

SAP Treasury SAP 0* (0*, 0*, 4)

Smartlender Aurion Pro 0 (0, 3)

Sopra Banking Amplitude Sopra Banking Software 0 (0, 9, 3, 13, 11, 5 ,3, 3, 5, 5, 3, 6, 7, 9, 3, 7, 12, 9)

TrustBankCBS / Microfins Trust Software 0* (0+, 1+, 2+, 6+, 4, 3* ,2*, 2*, 2*)

Wealth in One Objectway 0 (0, 0, 1, 1)

Universal Banking | Core Private Banking & Wealth management

Wholesale Banking | Treasury & Capital Market Retail Banking | Core

Lending | Corporate Lending | Retail

Lending

* Data not submitted for the given year; + Does not include purely domestic wins; ** Estimated.

Footnote 1. The table covers only new-name Back Office deals. Contracts known to cover solely front office or corporate treasury have been omitted

from the supplier totals, so too domestic deals for Indian, Russian, and US suppliers.

Footnote 2. Where no figures appear for previous years, this is either because these systems were not included in previous surveys, the figures were not

disclosed, or the systems were not launched at that time.

Page 17

15

Table 2: Categories in IBSI SLT 2021

• Universal Banking | Core

• Risk Management

• Compliance Management

• CRM

BankWide

• Retail Banking | Core

• Lending | Retail

• Digital Banking & Channels

• Payments | Retail

Retail Banking

• Payments | Wholesale

• Lending | Corporate

• Treasury & Capital Market

• Transaction Banking

Wholesale Banking

• Private Banking & Wealth Management

• Investment & Fund Management

Wealth Management

• Conversational Banking

• Datawarehouse & Business Intelligence

• InsurTech

New SLT Areas

• India

• USA

• Russia

• UK

Domestic SLT

• Neo Bank & Challenger Bank

Neo Bank & Challenger Bank

• Islamic Banking

Islamic Banking

• Universal Banking | Core

• Retail Banking | Core

• Wholesale Banking

• Private Banking & Wealth Management

• Lending

• Digital Banking & Channels

• Payments

• Risk & Compliance Management

IBSI Sales League Table LeaderBoard

Page 18

16

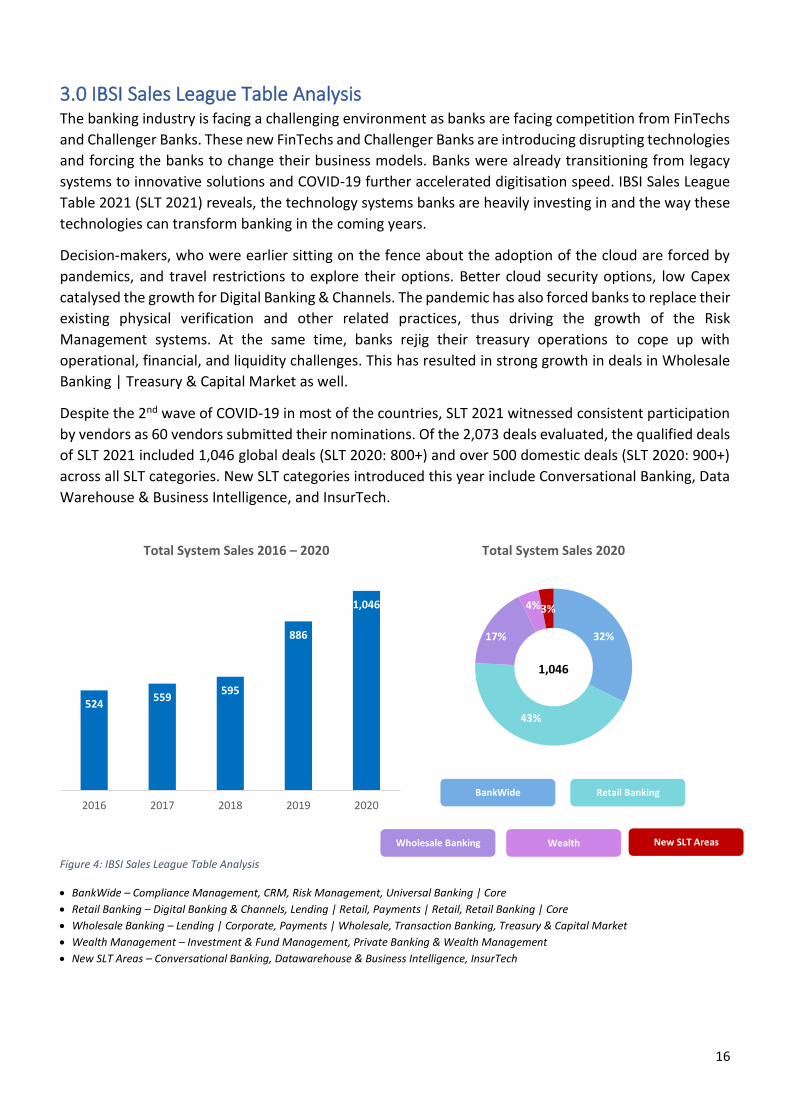

3.0 IBSI Sales League Table Analysis The banking industry is facing a challenging environment as banks are facing competition from FinTechs

and Challenger Banks. These new FinTechs and Challenger Banks are introducing disrupting technologies

and forcing the banks to change their business models. Banks were already transitioning from legacy

systems to innovative solutions and COVID-19 further accelerated digitisation speed. IBSI Sales League

Table 2021 (SLT 2021) reveals, the technology systems banks are heavily investing in and the way these

technologies can transform banking in the coming years.

Decision-makers, who were earlier sitting on the fence about the adoption of the cloud are forced by

pandemics, and travel restrictions to explore their options. Better cloud security options, low Capex

catalysed the growth for Digital Banking & Channels. The pandemic has also forced banks to replace their

existing physical verification and other related practices, thus driving the growth of the Risk

Management systems. At the same time, banks rejig their treasury operations to cope up with

operational, financial, and liquidity challenges. This has resulted in strong growth in deals in Wholesale

Banking | Treasury & Capital Market as well.

Despite the 2nd wave of COVID-19 in most of the countries, SLT 2021 witnessed consistent participation

by vendors as 60 vendors submitted their nominations. Of the 2,073 deals evaluated, the qualified deals

of SLT 2021 included 1,046 global deals (SLT 2020: 800+) and over 500 domestic deals (SLT 2020: 900+)

across all SLT categories. New SLT categories introduced this year include Conversational Banking, Data

Warehouse & Business Intelligence, and InsurTech.

Figure 4: IBSI Sales League Table Analysis

• BankWide – Compliance Management, CRM, Risk Management, Universal Banking | Core

• Retail Banking – Digital Banking & Channels, Lending | Retail, Payments | Retail, Retail Banking | Core

• Wholesale Banking – Lending | Corporate, Payments | Wholesale, Transaction Banking, Treasury & Capital Market

• Wealth Management – Investment & Fund Management, Private Banking & Wealth Management

• New SLT Areas – Conversational Banking, Datawarehouse & Business Intelligence, InsurTech

524559

595

886

1,046

2016 2017 2018 2019 2020

Total System Sales 2016 – 2020

32%

43%

17%

4%3%

Total System Sales 2020

1,046

BankWide Retail Banking

Wholesale Banking Wealth

Management

New SLT Areas

Page 19

17

4.0 BankWide BankWide includes 4 system categories and banks implement these systems to provide a wide variety of

comprehensive financial services, including those tailored to retail, commercial, and investment services

to their clients. BankWide includes legacy Universal Banking and Risk Management as well as new-age

digital and automation systems technologies like CRM and Compliance Management. The number of

deals signed in the BankWide increased from 255 in 2016 to 338 in 2020, clearly showing the importance

of the systems included in the category. Even in 2020, the category recorded a growth of 5% as compared

to 2019. While traditional categories like Universal Banking are stable in the new deals, new-age

technologies are driving the market. The next sections will provide a detailed overview of the system

types of BankWide, as analysed from IBSI Sales League Table 2021 perspective.

4.1 BankWide – Universal Banking | Core

4.1.1 Market Trends Universal Banking | Core is the backbone of every bank. In 2016 the total number of universal core

banking sold was 171, and the total number of deals declined during the next 2 years to 150 and 104.

This got us thinking, if the core is still the king, or if new-age technology taking over the marker gradually?

But the total number of deals posted growth in 2019 and remained stable in 2020. The trend in the

number of deals indicates that without keeping a strong core, the banks could not invest in newer digital

technologies.

In 2020, the developed markets in the Americas posted the highest growth indicating that banks in these

markets are upgrading their systems. Market in MEA region posted a decline because of COVID factor as

banks were spending judicially. APAC market recorded the highest number of deals and emerged as the

largest market for the category. The overall share of the APAC market is continuously growing and has

increased from ~26% in 2016 to ~31% in 2020.

Figure 5: Market Trend for Universal Banking | Core: Geographic Break-up

45 34 28 28 35

5955

48 45 34

3231

14 2920

35

30

1414

25

171

150

104116 114

2016 2017 2018 2019 2020

Total System Sales 2016 – 2020

APAC MEA Europe Americas Total

Page 20

18

4.1.2 Universal Banking | Core | Sales League Table

Table 3: IBSI Sales League Table 2021 – Universal Banking | Core

# Product Supplier # Deals (Previous years in bracket) 1 Temenos Transact Temenos 48 (51, 43, 45, 43,34, 37, 35, 34, 27, 38, 40, 40, 44, 40,

32, 28, 24, 32, 36, 42, 34, 33, 19, 15, 10, 29, 7, 9)

2 Finacle Digital Banking Solution Suite

Infosys Finacle 17+

3 TCS BaNCS TCS Financial Solutions 11+ (15+, 13+, 18+, 17+, 11, 8+ ,8, 9+, 13+, 13+, 17+, 23, 31, 25, 14, 8 , 6*, 9, 10, 10, 6, 8, 6, 9, 5)

4 COBIS Cobiscorp 6 (0, 3)

5 iMAL Path Solutions 5 (6, 7, 13, 9, 4, 4 ,10, 11, 3, 4, 13, 11, 14, 5, 5 , 3)

6 Synergies Lyst Technologies 5 (0*, 2, 5)

7 Bantotal Internet Banking Bantotal 3

8 PowerBanker Capital Banking Solutions 3 (3, 0, 1)

9 Quartz TCS Financial Solutions 3

10 CapitalBanker Capital Banking Solutions 2 (2, 0, 3, 0*, 1, 2 ,2, 3, 4, 3)

11 ICBS BML Istisharat 2 (3, 2, 2, 1, 4, 1 ,3, 1, 3, 3, 6, 6, 5, 5, 3, 4, 3, 2, 3, 5, 3, 4)

12 ICS BANKS ICS Financial Systems 2 (1, 0*, 7, 9, 3, 0, 5, 4, 5, 5, 8, 6, 10, 11)

13 Avaloq Banking Software Avaloq 1

14 BANQIN Bank Genie 1

15 Bantotal Digital Onboarding Bantotal 1

16 Finairo Microfinance Solution Infrasoft Technologies 1

17 FMS.next Profile Software 1

18 Fusion Essence Finastra 1 (5, 2, 4, 5, 4, 3 ,2, 2, 4, 6, 1, 2)

19 OLYMPIC Banking System ERI Bancaire 1

20 Finacle Core Banking Infosys Finacle 0 (10+, 13+, 15+, 17+, 16, 9, 9, 14+, 12+, 8+, 14+, 14, 13, 3*, 13, 14, 9, 8, 11, 9, 2)

21 Sopra Banking Platform Sopra Banking Software 0 (10, 0, 6, 10, 4, 2 ,2, 5, 2, 7, 3, 4, 3, 7, 3, 5, 2, 5, 1, 1, 3)

22 ICS BANKS Islamic ICS Financial Systems 0 (4)

23 Fusion Equation Finastra 0 (2, 1)

24 Ababil Millennium Information Solution

0 (1)

25 MIMICS Core Processing System MIMICS, Inc 0 (1)

26 SAB AT Sopra Banking Software 0 (1, 1, 2, 5, 2, 2 ,8, 7, 2, 2, 6, 2, 7, 6, 8)

27 Cyberbank Core Technisys 0 (1, 2, 2, 0*, 0, 0 ,1*, 1*)

28 Abanks Grupo ASI 0 (0, 0*, 0*, 5)

29 AutoBANKER Premium Autosoft Dynamics 0 (0, 1, 1, 0*, 0, 1 ,2, 3, 1, 1, 0, 0, 0, 0, 1, 2, 1, 1)

30 Bank 21 Century Inversia 0 (0, 0+, 0+, 5+, 11, 10,14,12,12,18,11,10,12,15)

31 e-IBS Datapro 0 (0*, 0*, 2, 5, 3, 6 ,7, 1, 2, 8, 6)

32 Ethix International Turnkey Systems (ITS)

0* (0*, 3, 0*, 4, 0*, 5 ,1, 4, 3)

33 Flexcube Oracle FSS 0* (0*, 0*, 0*, 0*, 28, 27, 15, 17+, 28, 32, 33+, 39+, 20**, 43, 37, 36)

34 Horizon FIS 0 (0, 0+, 0+, 3+)

35 IBS FIS 0 (0, 0+, 0+, 1+)

36 Mercury FIS 0 (0, 0+, 1, 1)

37 RS-Bank R-Style Softlab 0* (0*, 2)

38 SAP Transactional Banking SAP 0* (0*, 0*, 10)

39 Sopra Banking Amplitude Sopra Banking Software 0 (0, 9, 3, 13, 11, 5 ,3, 3, 5, 5, 3, 6, 7, 9, 3, 7, 12, 9)

Page 21

19

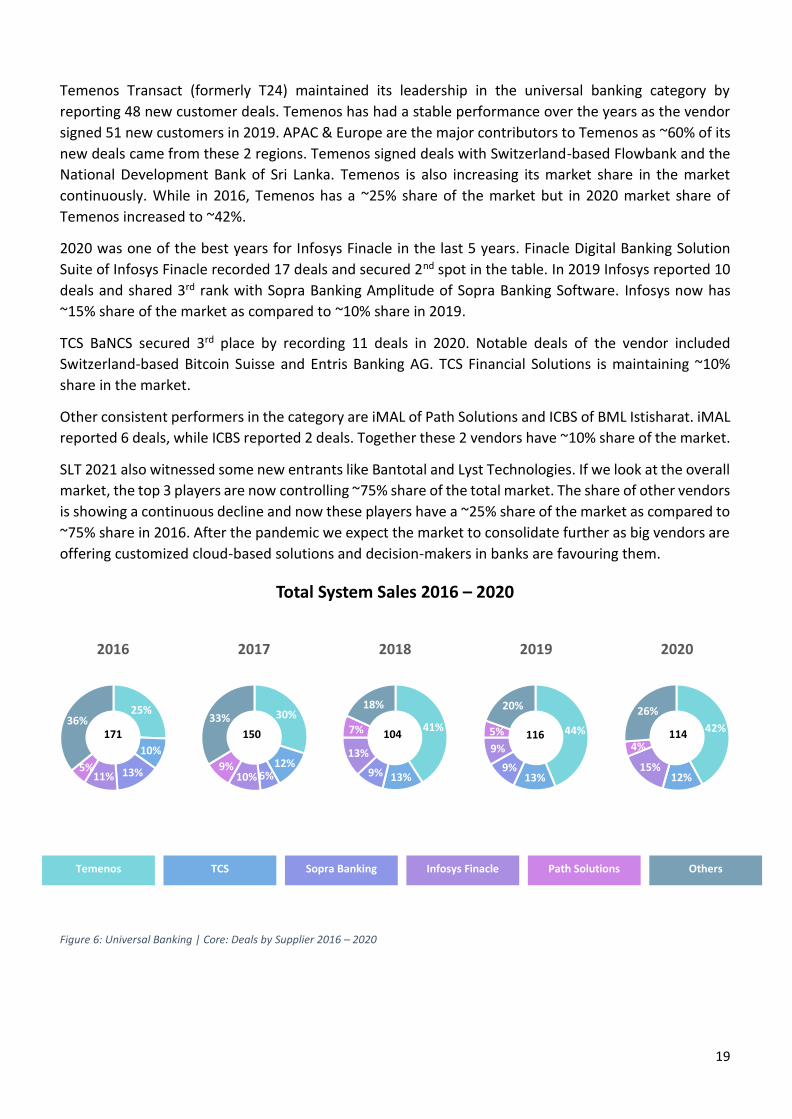

Temenos Transact (formerly T24) maintained its leadership in the universal banking category by

reporting 48 new customer deals. Temenos has had a stable performance over the years as the vendor

signed 51 new customers in 2019. APAC & Europe are the major contributors to Temenos as ~60% of its

new deals came from these 2 regions. Temenos signed deals with Switzerland-based Flowbank and the

National Development Bank of Sri Lanka. Temenos is also increasing its market share in the market

continuously. While in 2016, Temenos has a ~25% share of the market but in 2020 market share of

Temenos increased to ~42%.

2020 was one of the best years for Infosys Finacle in the last 5 years. Finacle Digital Banking Solution

Suite of Infosys Finacle recorded 17 deals and secured 2nd spot in the table. In 2019 Infosys reported 10

deals and shared 3rd rank with Sopra Banking Amplitude of Sopra Banking Software. Infosys now has

~15% share of the market as compared to ~10% share in 2019.

TCS BaNCS secured 3rd place by recording 11 deals in 2020. Notable deals of the vendor included

Switzerland-based Bitcoin Suisse and Entris Banking AG. TCS Financial Solutions is maintaining ~10%

share in the market.

Other consistent performers in the category are iMAL of Path Solutions and ICBS of BML Istisharat. iMAL

reported 6 deals, while ICBS reported 2 deals. Together these 2 vendors have ~10% share of the market.

SLT 2021 also witnessed some new entrants like Bantotal and Lyst Technologies. If we look at the overall

market, the top 3 players are now controlling ~75% share of the total market. The share of other vendors

is showing a continuous decline and now these players have a ~25% share of the market as compared to

~75% share in 2016. After the pandemic we expect the market to consolidate further as big vendors are

offering customized cloud-based solutions and decision-makers in banks are favouring them.

Figure 6: Universal Banking | Core: Deals by Supplier 2016 – 2020

Temenos Sopra Banking TCS Infosys Finacle Path Solutions

25%

10%

13%11%5%

36%

2016

30%

12%6%10%

9%

33%

2017

41%

13%9%

13%

7%

18%

2018

44%

13%9%

9%

5%

20%

2019

171 150 104 116

Others

42%

12%15%

4%

26%

2020

114

Total System Sales 2016 – 2020

Page 22

20

4.2 BankWide – Risk Management & Compliance Management

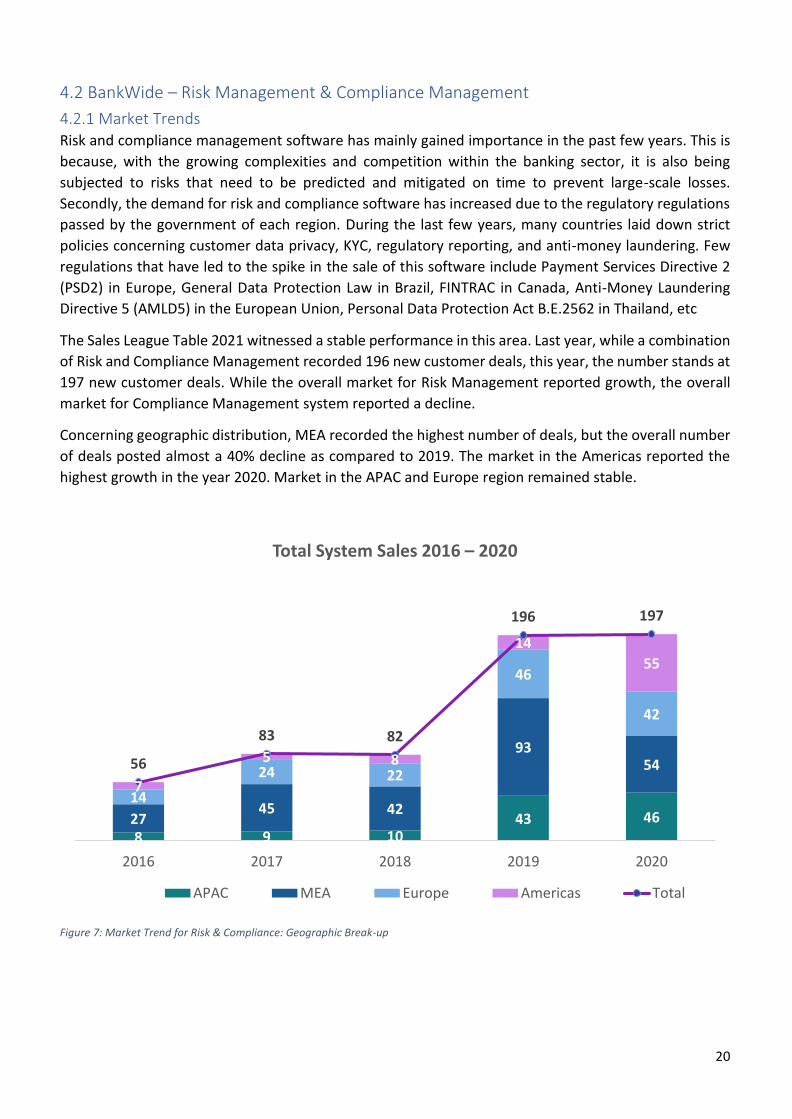

4.2.1 Market Trends Risk and compliance management software has mainly gained importance in the past few years. This is

because, with the growing complexities and competition within the banking sector, it is also being

subjected to risks that need to be predicted and mitigated on time to prevent large-scale losses.

Secondly, the demand for risk and compliance software has increased due to the regulatory regulations

passed by the government of each region. During the last few years, many countries laid down strict

policies concerning customer data privacy, KYC, regulatory reporting, and anti-money laundering. Few

regulations that have led to the spike in the sale of this software include Payment Services Directive 2

(PSD2) in Europe, General Data Protection Law in Brazil, FINTRAC in Canada, Anti-Money Laundering

Directive 5 (AMLD5) in the European Union, Personal Data Protection Act B.E.2562 in Thailand, etc

The Sales League Table 2021 witnessed a stable performance in this area. Last year, while a combination

of Risk and Compliance Management recorded 196 new customer deals, this year, the number stands at

197 new customer deals. While the overall market for Risk Management reported growth, the overall

market for Compliance Management system reported a decline.

Concerning geographic distribution, MEA recorded the highest number of deals, but the overall number

of deals posted almost a 40% decline as compared to 2019. The market in the Americas reported the

highest growth in the year 2020. Market in the APAC and Europe region remained stable.

Figure 7: Market Trend for Risk & Compliance: Geographic Break-up

8 9 1043 4627

45 42

9354

14

24 22

46

42

7

5 8

14

55

56

83 82

196 197

2016 2017 2018 2019 2020

Total System Sales 2016 – 2020

APAC MEA Europe Americas Total

Page 23

21

4.2.2 Risk Management | Sales League Table

Table 4: IBSI Sales League Table 2021 – Risk Management

# Product Supplier # Deals (Previous years in bracket) 1 Temenos Risk & Compliance Temenos 84 (53. 43, 27, 25)

2 Sopra Banking Platform Sopra Banking Software 16

3 Imagine Trading System TS Imagine 12

4 MX.3 Murex 11 (5, 0, 5, 5)

5 ACI Fraud Management ACI Worldwide 3

6 iMAL Path Solutions 2 (1, 0, 3)

7 Fusion Risk Finastra 1 (3, 1, 4, 1)

8 Kastle Integrated Risk Management Solution

Azentio Software (3i Infotech) 1

9 RiskAvert Profile Software 1 (1, 1)

10 Credit Risk Management Platform Actico 0 (4)

11 AXIS Asseco 0 (3)

12 Intellect Risk Management Intellect Design Arena 0 (3)

13 ACTICO Platform Actico 0 (3)

14 UP Payments Risk Management ACI Worldwide 0 (1)

15 SmartVista BPC Group 0* (1)

16 Loxon IFRS9 Calculation Engine Loxon 0 (1, 1, 2, 2)

The uncertainty in the business caused by COVID-19 changed the perception of risk management as a

function. Banks want to improve their decision-making capabilities through the intelligent use of internal

and external data. Banks are investing in technology to enhance their risk management capabilities to

face the new challenges in risk management and lately in crisis management.

The Sales League Table witnessed an overall rise in the number of deals in this area. This year Risk

Management reported 131 deals as compared to 80 deals in 2019. Category reported year-on-year

growth of 64%.

Temenos emerged as the winner with its Temenos Risk and Compliance system recording 84 deals as

compared to 53 deals in 2019. Americas contributed more than 50% of the total deals. APAC and Europe

were other major contributors. Temenos signed deals with Italy's newest challenger bank Flowe and KBC

Bank of Ireland. The Share of Temenos in the segment increased from ~44% in 2016 to ~64% in 2020.

Sopra Banking Platform of Sopra Banking Software reported 16 deals and secured second place in the

ranking. Most of the deals came from banks and financial institutions from Europe.

New entrant TS Imagine capsized ~9% share of the market and ranked 3rd in the table. Imagine Trading

System of TS Imagine reported 12 deals. Imagine Trading System not only offers UCITS compliance but

its robust VaR engine helps clients to monitor and control if an ETF is in danger of breaching NAV Limits.

Vendor secured deals from leading banks in Europe & APAC. MX.3 of Murex reported 11 deals, recording

a significant growth from 5 deals in 2019. Murex signed deals with banks in ASEAN and Middle East.

Murex is maintaining ~8% share in the market.

Page 24

22

Figure 8: 2020 Deals Analysis – Risk Management

21%

13%

29%

37%

Total System Sales – 2020

APAC MEA Europe Americas

131

64%12%

8%

1%1%14%

Total System Sales – 2020

Temenos Sopra Banking

Murex Profile Software

Finastra Others

131

Page 25

23

4.2.3 Compliance Management | Sales League Table

Table 5: IBSI Sales League Table 2021 – Compliance Management

# Product Supplier # Deals (Previous years in bracket)

1 Univius Anti Money Laundering Solution

Infrasoft Technologies 21 (58, 14, 10, 13)

2 AMLOCK Azentio Software (3i Infotech) 15 (11)

3 ClauseMatch ClauseMatch 6

4 Clari5 Real Time Anti-Money Laundering (AML) Solution

CustomerXPs 3 (2)

5 Clari5 Real Time Enterprise Fraud Management (EFM) Solution CustomerXPs 3 (2)

6 iMAL Path Solutions 3 (4)

7 RegulatoryPlus EgabiFSI 2

8 CCR.Ezee EpikInDiFi 2 (1)

9 Sopra Banking Platform Sopra Banking Software 2 (2)

10 AutoCOMPLIANCE Autosoft Dynamics 2 (2)

11 Intellect iGCB Intellect Design Arena 2

12 CapitalCompliance Capital Banking Solutions 1 (2, 2, 17)

13 Kyzer TFRS Kyzer 1

14 Clari5 Employee Fraud Monitoring and Prevention Solution

CustomerXPs 1

15 Clari5 Trade Finance Solution CustomerXPs 1

16 FATCA & CRS Asseco 1

17 Univius FATCA CRS Solution Infrasoft Technologies 0 (15)

18 Intellect Risk Management Intellect Design Arena 0 (6)

19 COBIS Inclusion Cobiscorp 0 (2)

20 EAGLE Asseco 0 (2)

21 TCS BaNCS TCS Financial Solutions 0 (2)

22 Univius Anti Fraud Solution Infrasoft Technologies 0 (2)

23 Clari5 Card Fraud Management System CustomerXPs 0 (1)

24 Fincraft IFRS Solution Nelito Systems 0 (1)

25 MoneyWare Asset Management EbixCash Financial Technologies 0 (1)

During the COVID-19 pandemic, most of the regulators across the globe revised existing liquidity lines to

ensure cash availability in the banking system and to support the economy. Some countries have

postponed the implementation of some regulatory requirements, as a result, deals in compliance

management declined.

Univius Anti Money Laundering Solution of Infrasoft Technologies remained the market leader. The

vendor signed 21 new deals in the year across APAC and MEA and MEA contributing the most. In the

Middle East & Africa region, Infrasoft signed deals with leading banks in Kuwait & Qatar. In the ASEAN

vendor signed deals with leading banks in Cambodia. AMLOCK of Azentio Software was runner-up with

15 deals. The geographic spread of these deals is interesting as the maximum number of systems were

sold in the Middle East, followed by Africa and APAC. AMLOCK signed deals with the National Finance

House in KSA and J Trust Royal Bank Ltd in Cambodia. ClauseMatch signed 6 deals in 2020 and stood 3rd

in the ranking order. The vendor signed most of the deals in the Americas followed by APAC.

Page 26

24

Figure 9: 2020 Deals Analysis – Compliance Management

29%

56%

6%

9%

Total System Sales – 2020

APAC MEA Europe Americas

32%

23%12%

9%

5%

20%

Total System Sales – 2020

Infrasoft Technologies Azentio Software

CustomerXPs ClauseMatch

Path Solutions Otehrs

66 66

Page 27

25

4.3 BankWide – CRM

4.3.1 Market Trends Customer relationship management (CRM) is one of the most important tools in any customer-focused

industry. As banks implement CRM solutions for storing and analysing data of customers to meet their

revenues and exceeding customer expectations.

CRM category for the IBSI SLT 2021 witnessed 27 deals. The overall market in the category is quite stable

at 25 deals per year. APAC region is the market leader in the category with ~50% share of the market,

followed by the MEA region.

* 2019 – Participants in SLT didn’t report any deal in 2019

Figure 10: Market Trend for CRM: Geographic Break-up

15

7

2

12

8

5

5

11

1

9

11

4

1

325 25

8

27

2016 2017 2018 2019 2020

Total System Sales 2016 – 2020

APAC MEA Europe Americas Total

Page 28

26

4.3.2 CRM | Sales League Table

Table 6: IBSI Sales League Table 2021 – CRM

# Product Supplier # Deals (Previous years in bracket) 1 Finacle Digital Banking Solution Suite Infosys Finacle 15

2 CRMNEXT CRMNext 10 (0*, 6, 6)

3 CRM-SALES AND MARKETING Asseco 1

4 iMAL Path Solutions 1 (0, 0, 1)

5 MS CRM Platform Asseco 0 (0, 1)

6 Temenos Front Office (formerly Triple'A) Temenos 0 (0, 0, 0, 2)

7 SAP Hybris Sales Cloud SAP 0* (0*, 0*, 8)

8 Finacle CRM Infosys Finacle 0 (2, 1)

9 VeriTouch Veripark 0* (0*, 0*, 0*, 7)

10 Finacle Customer Information Infosys Finacle 0 (9, 0)

11 SAP CRM for Banking SAP 0* (0*, 0*, 3)

12 CRM Banking Edition CRMNext 0 (0*, 0, 0, 12)

13 Temenos Core Banking (formerly T24) Temenos 0 (0, 0, 0, 1)

14 Client Engage Objectway 0 (0, 0, 1, 0)

15 Temenos Front Office for PWM Temenos 0 (0, 0, 5, 0)

16 Intellect Wealth Intellect Design Arena 0 (0, 0, 0, 1)

17 Finacle Infosys Finacle 0 (0, 0, 0, 2)

18 MIMICS CRM System MIMICS, Inc 0 (0, 0, 1, 0)

Finacle Digital Banking Solution Suite of Infosys Finacle reported 15 deals and ranked first in the table.

Most of the deals came from the APAC region followed by Africa. Infosys Finacle signed deals with the

leading bank in South Pacific region and Co-Operative banks in Africa. Infosys has ~50% share in the

market and vendor is continuously growing its share in the market

CRMNEXT of CRMNext reported 10 deals and ranked second in the table. Most of the deals came from

the ASEAN region. Vendor signed deals with Krungsri Consumer Finance & Tesco Life Insurance Broker

Ltd of Thailand. CRMNEXT also signed deals with Clearview Federal Credit Union and Rbank in the USA.

CRMNEXT has ~40% share in the market.

Figure 11: CRM: Deals by Supplier 2016 – 2020

Infosys Finacle Path Solutions CRMNext Asseco Others

8%

48%

44%

2016

24%

4%

72%

2017

13%

75%

13%

2018

25 25 8 56%37%

4%4%

2020

27

Total System Sales 2016 – 2020

Page 29

27

5.0 Retail Banking Retail Banking includes 4 system categories and banks implement these systems to provide financial

services to individual customers. Retail Banking Systems help banks to automate for individual

consumers to manage their money, access credit, and securely deposit money. After the pandemic,

banks are ensuring that their customers can access their banking services without visiting the branches.

This has catalysed the growth of the Retail Banking System. During the 2020 overall Retail Banking

systems reported a total of 455 deals, a whopping 40% growth as compared to the year 2019. The next

sections will provide a detailed overview of the system types of Retail Banking, as analysed from IBSI

Sales League Table 2021 perspective.

5.1 Retail Banking – Retail Banking | Core

5.1.1 Market Trends Retail Banking deals have witnessed significant growth over the years from 2016–2020. The market for

Retail Banking System is growing continuously for the last 2 years. This rise in the number of deals can

be ascribed to the rapid advances in information technology, the evolving macroeconomic environment,

along various other micro-level demand and supply-side factors.

The year 2020 witnessed a sharp rise to 58 deals as compared to 38 deals in 2019. This can be mostly

attributed to the strong rise in deals in the Americas. Europe recorded the highest growth among all

regions. The number of deals in APAC declined from 18 deals in 2019 to 14 deals in 2020. The APAC

region is the only region that showed a decline. The MEA region also posted strong growth and total

deals increased from 9 deals in 2019 to 20 deals in 2020.

Figure 12: Market Trend for Retail Banking | Core: Geographic Break-up

9 7 918 14

7 8 5

9 18

2

1610

4

10

2

510

7

16

20

36 3438

58

2016 2017 2018 2019 2020

Total System Sales 2016 – 2020

APAC MEA Europe Americas Total

Page 30

28

5.1.2 Retail Banking | Core | Sales League Table

Table 7: IBSI Sales League Table 2021 – Retail Banking | Core

# Product Supplier # Deals (Previous years in bracket) 1 Intellect iGCB Intellect Design Arena 18+ (14+, 7+) 2 Sopra Banking Platform Sopra Banking Software 13 3 Vault Thought Machine 6 (1) 4 BX CBP Bankware Global 3 (1, 1, 2) 5 Core Banking - International FIS 3+ 6 Cyberbank Core Technisys 3 7 Bantotal Core Bantotal 2 (2, 5, 3, 2, 5, 3 ,5, 3, 5) 8 TCS BaNCS TCS Financial Solutions 2 9 Avaloq Banking Software Avaloq 1 (0, 0, 1) 10 BankPLus EgabiFSI 1 11 Bantotal Internet Banking Bantotal 1 12 CapitalBanker Capital Banking Solutions 1 13 Cyberbank Core + Digital Technisys 1 14 Cyberbank Digital Technisys 1 (1) 15 Fusion Phoenix Finastra 1+ 16 LFI - Latam FIS 1 17 Systematics FIS 0 (7+, 3, 0+, 1+, 0, 0 ,0, 0, 0, 0, 1, 1, 0+, 0, 2, 1, 8, 7, 7, 0*) 18 Finairo Microfinance Solution Infrasoft Technologies 0 (2) 19 Finairo Core Banking Solution Infrasoft Technologies 0 (2+, 0*, 0, 1) 20 FinCraft Core Banking Solution Nelito Systems 0 (2, 1, 1) 21 Profile Core System FIS 0 (2, 4, 0+, 0+, 0, 2 ,3, 5, 4, 3, 4, 5, 8, 3, 2, 1, 2, 5, 4, 12*) 22 COBIS Retail Cobiscorp 0 (1, 3, 3, 9, 0, 0 ,3, 1, 1, 2) 23 Bankway Core System FIS 0 (1+) 24 Core 24 Core System FIS 0 (1, 1) 25 OLYMPIC Banking System ERI Bancaire 0 (0, 1) 26 Bantotal Microfinance Bantotal (0, 1, 0*, 1) 27 CorePlus Probanx 0* (0*, 7, 8, 0*, 4, 2) 28 FinCraft Enterprise Reporting Nelito Systems 0 (0, 0+, 0, 2) 29 Intellect Digital Core Intellect Design Arena 0 (0, 0+, 10+, 8) 30 Intellect Quantum Core Banking Intellect Design Arena 0 (0, 0, 1) 31 PROFITS® Integrated Core

Banking System Intrasoft International 0* (0, 2, 8, 0*, 1, 1 ,1, 3, 0, 0)

32 TrustBankCBS / Microfins Trust Software 0* (0+, 1+, 2+, 6+, 4, 3* ,2*, 2*, 2*)

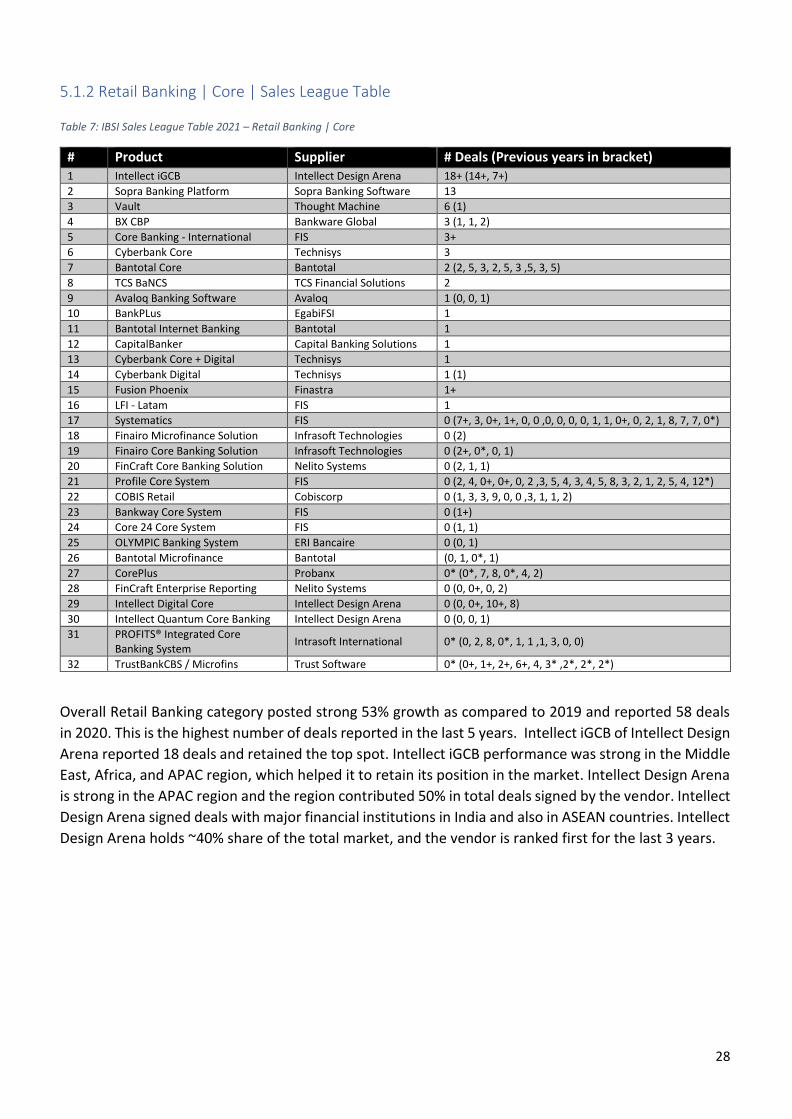

Overall Retail Banking category posted strong 53% growth as compared to 2019 and reported 58 deals

in 2020. This is the highest number of deals reported in the last 5 years. Intellect iGCB of Intellect Design

Arena reported 18 deals and retained the top spot. Intellect iGCB performance was strong in the Middle

East, Africa, and APAC region, which helped it to retain its position in the market. Intellect Design Arena

is strong in the APAC region and the region contributed 50% in total deals signed by the vendor. Intellect

Design Arena signed deals with major financial institutions in India and also in ASEAN countries. Intellect

Design Arena holds ~40% share of the total market, and the vendor is ranked first for the last 3 years.

Page 31

29

Sopra Banking Platform of Sopra Banking Software bagged 2nd position and reported 13 new deals in

2020. The vendor bagged most of the deals in the Africa region. Thought Machine, a provider of new-

age financial technology solutions reported 4 deals and ranked in 3rd place. Thought Machine signed

deals with challenger banks like Monese and Transfer Go. Bantotal and Nelito Systems are other

regular performers in the category.

Figure 13: Retail Banking | Core: Deals by Supplier 2016 – 2020

Intellect

Design Arena Bankware

Global FIS Bantotal

40%

5%5%

50%

2016

31%

6%8%

56%

2017

21%

24%

3%18%

35%

2018

37%

29%

3%5%

26%

2019

20 36 34 38

Others

31%

7%5%5%

52%

2020

58

Total System Sales 2016 – 2020

Page 32

30

5.2 Retail Banking – Lending | Retail

5.2.1 Market Trends Lending is rapidly emerging as a new focus area for banks as they look at implementing specialised

solutions to enhance the quality of their lending services to cater to corporate and retail customers.

Considering the growing importance of lending systems, IBSI introduced two separate categories to

depict lending systems - Lending | Corporate & Lending | Retail. The Lending | Retail category witnessed

a total of 83 deals with participation from 15 vendors. APAC and MEA region led the market by holding

~43% share each. Europe and the Americas combinedly control ~14% share of the market.

5.2.2 Lending | Retail | Sales League Table

Table 8: IBSI Sales League Table 2021 – Lending | Retail