16

Schwab Intelligent Portfolios. ® Investing has changed forever.

Schwab Intelligent Portfolios.®

Investing has changed forever.

Technology that will change the way you invest.

Schwab Intelligent Portfolios® is an automated investment advisory

service that builds, monitors, and rebalances your portfolio—so you

don’t have to. And Schwab Intelligent Portfolios doesn’t charge

advisory fees, commissions, or account service fees.

See the back cover of this brochure for important information about rebalancing and how we make money.

A sophisticated and diversified asset allocation.• Portfolios are made up of low-cost exchange-traded funds (ETFs).

• No advisory fees, no commissions, and no account service fees are charged.

The portfolio below is an illustrative example. Your specific portfolio will be based on your stated individual goals and risk profile.

See the back cover of this brochure for important information about how we make money.

My Portfolio

$118,004

Commodities

Stocks

Cash

Fixed Income

Cash 9% Commodities 5% Fixed Income 21% Stocks 65%

Cash 9% Precious Metals 5% Corporate Bonds 1%Securitized Bonds 3%

Int’l Developed Bonds 2%

High Yield Bonds 8%

Emerging Bonds 7%

U.S. Large Company Stocks 8%

U.S. Large Fundamental 11%U.S. Small Company Stocks 4%

U.S. Small Fundamental 7%Int’l Large Company Stocks 5%Int’l Large Fundamental 8%Int’l Small Company Stocks 3%

Int’l Small Fundamental 5%Int’l Emerging Markets 4%Int’l Emerging Fundamental 5%U.S. REITs 3%Int’l REITs 2%

We’ll build you a sophisticated and diversified portfolio.

To build and manage your portfolio, Schwab Intelligent Portfolios® uses

an advanced algorithm and the professional insights of the Charles

Schwab Investment Advisory, Inc. (CSIA) team. You will get a diversified

portfolio composed of low-cost exchange-traded funds (ETFs)—all

handpicked by the CSIA team.

Portfolios include up to 20 asset classes across stocks, fixed income,

real estate, and commodities, as well as an FDIC-insured cash

component—so they’re truly diversified. After the ETFs are chosen, the

experts at CSIA monitor their performance on an ongoing basis to make

sure the ETFs continue to provide consistency and diversity.

Get started at intelligent.schwab.com

8.0% 9.0% 10.0% 11.0% 12.0% 13.0%

Rebalancing can lower risk.This example demonstrates how a diversified portfolio’s volatility can increase if it is left to drift with the market ups and downs.

Portfolio VolatilityHypothetical Moderate Asset Allocation

• Rebalanced

• Never rebalanced

Risk (Annualized standard deviation)

You’ll stay on track with automatic rebalancing.

With any portfolio, natural market fluctuations increase and decrease

the value of some of your holdings, causing your asset allocation to stray

from its target. When that happens, it’s time to rebalance by buying

underweight and selling overweight asset classes.

Rebalancing is critical to successful investing. Schwab Intelligent

Portfolios® monitors your portfolio with daily check-ins and

automatically rebalances across up to 20 asset classes, working to

keep your investments consistent with your selected risk profile, which

may help with investment growth and reduced volatility over time.

Risk is based on the standard deviation of a hypothetical moderate asset allocation (35% large-cap stocks, 15% international stocks, 10% small-cap stocks, 35% bonds, and 5% cash investments), rebalanced annually, from 1970 to 2013. Portfolio volatility (as measured by standard deviation) estimates are based on market indexes representing these asset classes. The example is hypothetical and provided for illustrative purposes only. It is not intended to represent a specific investment product. Source: Schwab Center for Financial Research, with data from Morningstar, Inc. See the back cover of this brochure for more information about the market indexes used.

Get started at intelligent.schwab.com

Hypothetical example is for illustrative purposes only and is not intended to represent a specific investment product.

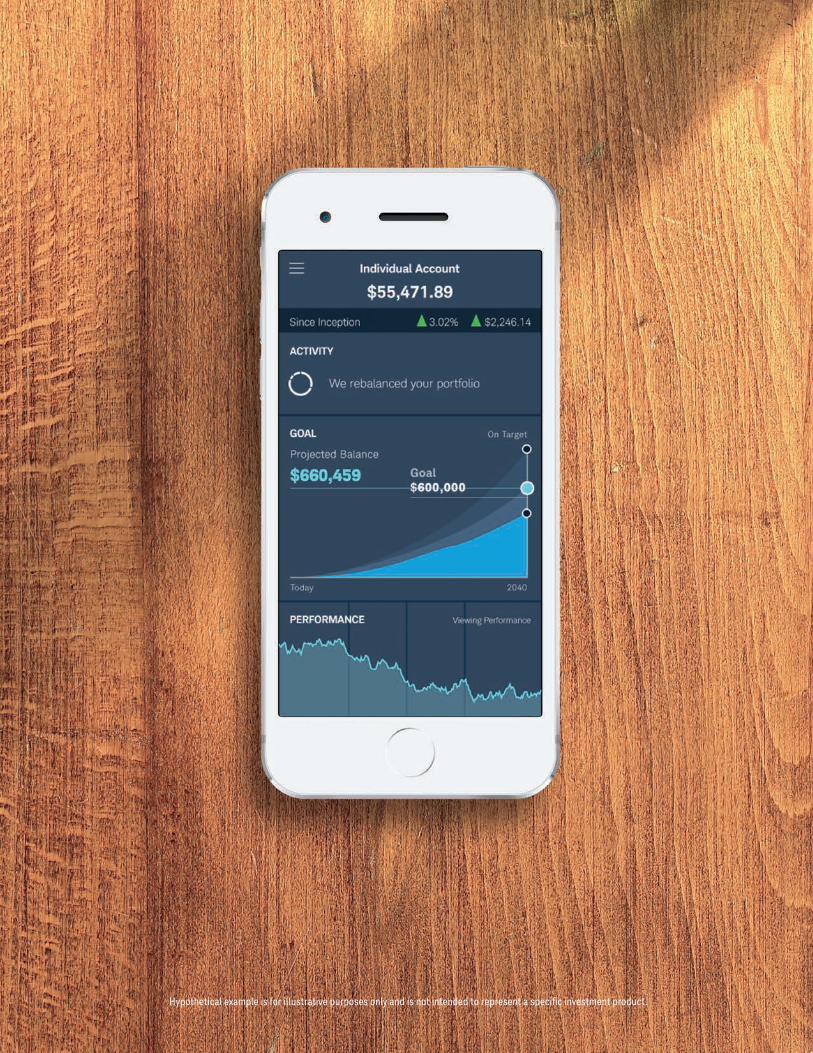

We’ll help you set, track and work toward achieving your financial goals.

Investing can be a challenge. It takes time to study the market, choose

the right investments, and stay on top of your long-term goals. Schwab

Intelligent Portfolios® Goal Tracker can help you get on course and

stay there.

Looking for income in retirement? Schwab Intelligent Portfolios makes it

easy to set and adjust a target withdrawal amount to help you achieve a

sustainable income stream based on your stated goals.

Get started at intelligent.schwab.com

There is no guarantee the intended goal, or the duration of future withdrawals associated with those goals, will be reached, and changes to inputs and other assumptions may affect your potential to reach the intended goal. In addition, the projections and other information you will see here about the likelihood of various outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. The projections are based on estimates intended to be representative of the selected portfolio. The output of this tool may vary with each use and over time. The tool does not consider the specific securities or other assets held by you. This tool provides analysis based upon your inputs but makes additional assumptions detailed in the Goal Tracker white paper (schwab.com/goalwhitepaper).

Hypothetical example is for illustrative purposes only and is not intended to represent a specific investment product.

$150,000

$140,000

$130,000

$120,000

$110,000

$100,000

$90,000

$80,000

$70,000

$60,000

Acc

ount

Val

ue

2008 2009 2010 2011 2012 2013 2014 2015

Tax-Loss Harvesting

No Tax-Loss Harvesting

Tax-loss harvesting can improve your returns.

Source: Charles Schwab Investment Advisory. This example is hypothetical and for illustrative purposes only. It is not intended to represent a specific investment product. It is not tax advice, and each investor is strongly encouraged to consult his or her own tax advisor about the utility of tax-loss harvesting. The example is based on a hypothetical $100,000 moderate risk portfolio held in a taxable account. Daily ETF returns were used when available. When not available, returns were backfilled with the underlying index. When the underlying index was unavailable, the strategic benchmark returns were used. A 39.6% federal tax rate was assumed on ordinary income and short-term capital gains and no allowance was made for state taxes. Tax-loss harvesting opportunities were checked for all asset classes. The losses being captured had to be greater than a set threshold before the trade was made. At the end of every calendar year, the tax savings were reinvested in the portfolio. The tax savings are equal to the assumed tax rate multiplied by the amount of ordinary income offset by losses captured through the program. The amount of ordinary income that may be offset by losses is limited to $3,000, or the amount of losses captured plus any tax-loss carryforwards, whichever is smaller. The hypothetical example shown resulted in $10,617 of realized losses that could potentially carry forward to future calendar years. There was no rebalancing assumed in the hypothetical portfolio. The example assumes that there are no capital gains from any other portfolio. The example does not consider the potential future sale of replacement assets, which could result in higher capital gains than would be the case without tax-loss harvesting. See back cover of this brochure for additional important information about tax-loss harvesting and the example provided.

Tax-loss harvesting can reduce the impact of taxes on your net

returns from investment.

Here’s how it works:

• Generally, when you sell a security for a profit, such as when your

portfolio is rebalanced, it can generate a taxable gain.

• With tax-loss harvesting, securities that have lost value are sold.

This can help offset a limited amount of ordinary income and/or

gains elsewhere in your portfolio, and so reduce your taxes.

• When a security is sold for tax-loss harvesting, it is replaced by

a similar security to keep your allocation on track.

Example:

Without Tax-Loss Harvesting With Tax-Loss Harvesting

Gain: $10,000

Tax rate: 15%

Tax due: $1,500

Gain: $10,000

Loss: ($5,000)

Net gain: $5,000

Tax rate: 15%

Tax due: $750

In turn, tax savings can improve your returns over time, because more of your assets stay invested. The chart below illustrates how tax-loss

harvesting could have affected your account value from 2008 through 2015, based on a hypothetical moderate risk portfolio. The actual benefit of

tax-loss harvesting will vary from year to year and from investor to investor. For example: There may be fewer losses to harvest in years where

markets are consistently rising; an investor’s personal tax circumstances may mitigate or eliminate the benefit of tax-loss harvesting; and the

future sale of replacement assets may result in higher capital gains than otherwise would be the case.

We can automaticallyharvest losses to help offset taxes on gains.

One of the most effective tools for offsetting investment-related taxes is

tax-loss harvesting: selling a security that’s lost value in order to offset the

gain on another security, and then replacing the sold security with a similar

security to keep your portfolio allocation on target.

Tax-loss harvesting can be a complicated and time-consuming strategy,

so for a long time it was only available to the wealthiest investors. But now,

with a Schwab Intelligent Portfolios® account of $50,000 or more, tax-loss

harvesting can be handled automatically once you enroll in this service.

Get started at intelligent.schwab.com

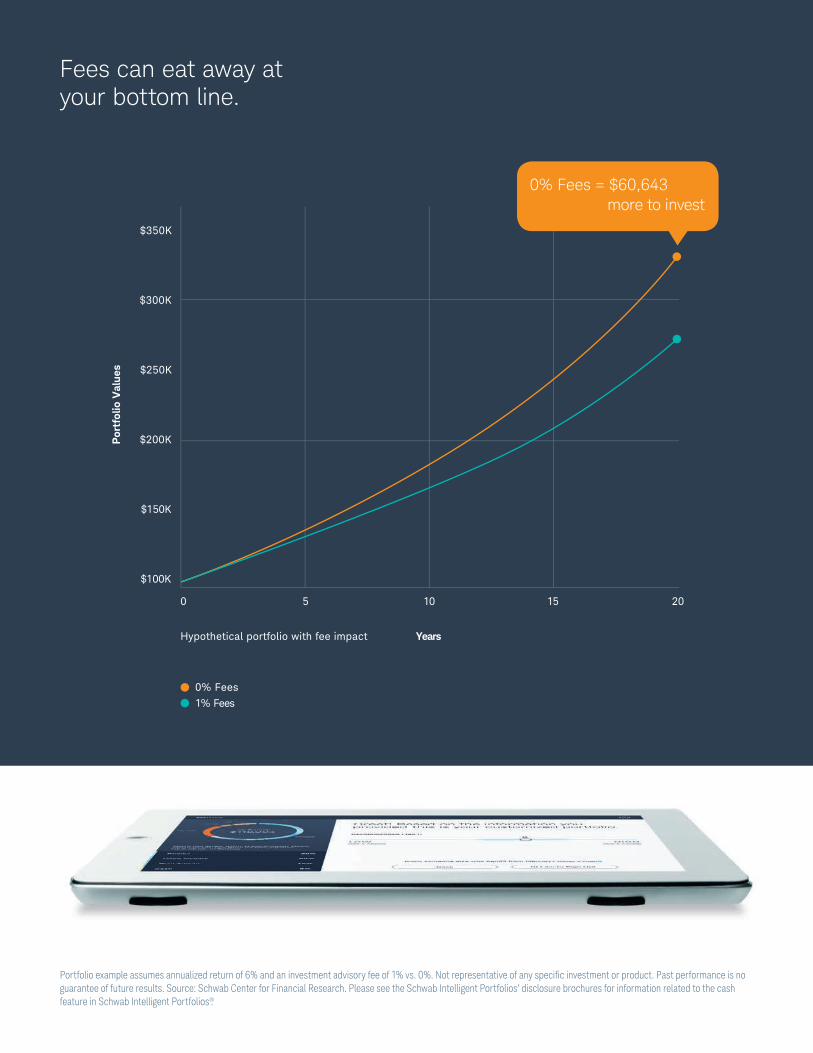

No advisory fees, account service fees, or commissions. Period.

Fees matter. Over time, even small fees can make a big dent in your

bottom line. No matter how much you earn on your investments, what

matters is what you get to keep.

Some investment advisory services charge annual advisory fees of

around 1% of your portfolio, or even more. It doesn’t sound like a lot,

but it can really add up. That’s why Schwab Intelligent Portfolios®

charges no advisory fees, no commissions, and no account service

fees—leaving you with more of your money to invest.

Get started at intelligent.schwab.com

How we make our money: Schwab Intelligent Portfolios charges no advisory fees. Schwab affiliates do earn revenue from the underlying assets in Schwab Intelligent Portfolios accounts. This revenue comes from providing advisory and other services to Schwab ETFs® and providing services relating to certain third-party ETFs that can be selected for the portfolio, and from the cash feature on the accounts. Revenue may also be received from the market centers where ETF trade orders are routed for execution.

$350K

$300K

$250K

$200K

$150K

$100K

Por

tfol

io V

alue

s

0 5 10 15 20

0% Fees

1% Fees

Hypothetical portfolio with fee impact Years

0% Fees = $60,643more to invest

Fees can eat away at your bottom line.

Portfolio example assumes annualized return of 6% and an investment advisory fee of 1% vs. 0%. Not representative of any specific investment or product. Past performance is no guarantee of future results. Source: Schwab Center for Financial Research. Please see the Schwab Intelligent Portfolios’ disclosure brochures for information related to the cash feature in Schwab Intelligent Portfolios®.

Enrolling is quick and easy. And when you contact us, we’ll answer 24/7.

You can get started with as little as $5,000 to invest. You begin by

going online and answering 12 straightforward questions about your

goals, time horizon, and appetite for risk. Then Schwab Intelligent

Portfolios® recommends a portfolio, based on your responses, that’s

designed to achieve your target investment allocation. From there,

it’s easy to sign up and fund your account.

We make monitoring your progress and managing your account

just as easy. All your portfolio information is at your fingertips,

whether you’re on your desktop or mobile device. Anytime you

have questions, you can talk to a Schwab investment professional.

We’re here 24 hours a day, 7 days a week, 365 days a year, at

1-855-694-5208 or via online chat.

Schwab investment professionals are employees of Charles Schwab & Co., Inc.

Get started: Enroll at intelligent.schwab.com.

Indexes used for rebalancing of hypothetical moderate asset allocation: U.S. large-cap stocks: S&P 500® Index. U.S. small-cap stocks: Russell 2000® Index; the Center for Research in Security Prices (CRSP) 6—8 Index was used prior to 1979. International stocks: MSCI EAFE® Net of Taxes. Bonds: Barclays U.S. Aggregate Bond Index; the Ibbotson Intermediate-Term Government Bond Index was used prior to 1976. Cash equivalents: Citigroup 3-Month U.S. Treasury Bill Index; the Ibbotson U.S. 30-day Treasury Bill Index was used prior to 1978. Indexes are unmanaged, do not incur fees and expenses, and cannot be invested in directly.

The tax-loss harvesting example in this brochure is intended to illustrate the possible benefits of reinvesting federal income tax savings, if the portfolio weights associated with a hypothetical portfolio of moderate risk held in a taxable account had been in existence and employed for the period specified, and does not reflect actual results. The hypothetical example is designed to allow investors to understand and evaluate the application of tax-loss harvesting to a portfolio by seeing the potential benefits from federal income tax savings that may have occurred during a certain time period. While the hypothetical results reflect the general application of tax-loss harvesting, they have certain limitations and should not be considered indicative of future results by any client. In particular, the example results do not reflect actual federal income tax savings in an actual account, so there is no guarantee that, in fact, an actual account would have achieved the results shown. Moreover, the potential federal income tax savings do not reflect investments outside the program that could impact the utilization or realization of such savings. The hypothetical example results also assume that federal income tax rates would have remained static over the period. Index returns were used when ETFs in the portfolios were not in existence. Hypothetical fees were not applied to index returns to simulate ETF net of fees performance, and therefore, the federal income tax savings would have been higher had actual simulated ETF fees been applied in the hypothetical portfolios. The simulation used total return data. For purposes of estimating hypothetical historical federal income tax savings, the portfolio weights associated with a hypothetical portfolio of moderate risk were assumed to be static throughout history. In reality, the portfolio allocation is likely to change over time.

The tax-loss harvesting example is based on a hypothetical moderate risk portfolio using the following asset allocation and strategic benchmarks: 15% U.S. large company stocks, 9% U.S. small company stocks, 11% int’l developed large company stocks, 7% int’l developed small company stocks, 7% int’l emerging market stocks, 3% U.S. REITs, 2% int’l REITs, 2% U.S. Treasuries, 3% U.S. investment-grade corporate bonds, 7% U.S. securitized bonds, 1% U.S. inflation-protected bonds, 4% int’l developed country bonds, 8% U.S. corporate high-yield bonds, 4% int’l emerging market bonds, 5% gold and other precious metals, and 12% cash investments.

Disclosures:

Tax-loss harvesting is available for clients with invested assets of $50,000 or more in their Schwab Intelligent Portfolios® account. Clients must enroll to receive this service. Please be aware that the ability to realize significant tax benefits from tax-loss harvesting depends upon a variety of factors, and no assurance can be offered that a particular investor will in fact realize significant tax benefits.

How we make our money: Schwab Intelligent Portfolios charges no advisory fees. Schwab affiliates do earn revenue from the underlying assets in Schwab Intelligent Portfolios accounts. This revenue comes from providing advisory and other services to Schwab ETFs® and providing services relating to certain third-party ETFs that can be selected for the portfolio, and from the cash feature on the accounts. Revenue may also be received from the market centers where ETF trade orders are routed for execution.

The cash allocation in Schwab Intelligent Portfolios will be accomplished through enrollment in the Schwab Intelligent Portfolios Sweep Program (“Sweep Program”), a program sponsored by Schwab. By enrolling in Schwab Intelligent Portfolios, clients consent to having the free credit balances in their Schwab Intelligent Portfolios brokerage accounts swept to deposit accounts at Charles Schwab Bank through the Sweep Program. Charles Schwab Bank is an FDIC-insured depository institution affiliated with Schwab and CSIA. Deposit balances held in the Sweep Program at Schwab Bank are eligible for FDIC insurance up to allowable limits.

Schwab Intelligent Portfolios is designed to monitor a client’s portfolio on a daily basis and will also automatically rebalance as needed to keep the portfolio consistent with the client’s selected risk profile unless such rebalancing may not be in the best interest of the client. Trading may not take place daily.

Please read the Schwab Intelligent Portfolios’ disclosure brochures, available at intelligent.schwab.com/disclosurebrochure, for important information, pricing, and disclosures relating to Schwab Intelligent Portfolios.

Schwab Intelligent Portfolios® is made available through Charles Schwab & Co., Inc. (“Schwab”), a dually-registered investment adviser and broker dealer. Portfolio management services are provided by Charles Schwab Investment Advisory, Inc. (“CSIA”). Schwab and CSIA are affiliates and subsidiaries of The Charles Schwab Corporation.

Charles Schwab & Co., Inc. and Charles Schwab Bank are separate but affiliated companies and subsidiaries of The Charles Schwab Corporation. Brokerage products, including the Schwab One® brokerage account, are offered by Charles Schwab & Co., Inc., Member SIPC. Deposit and lending products are offered by Charles Schwab Bank, Member FDIC and an Equal Housing Lender.

©2018 Charles Schwab & Co., Inc. All rights reserved. CC1843534 (0418-85SS) MKT85007FM-06 (05/18) 00210834

Brokerage Products: Not FDIC-Insured • No Bank Guarantee • May Lose Value