30

Sec 195 TDS: Recent Case Studies Ameya Kunte, Taxsutra May 30, 2015 ICAI Pune – Direct Tax Refresher Courese

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | vincent-bruce-james |

| View: | 214 times |

| Download: | 1 times |

Sec 195 TDS: Recent Case Studies Ameya Kunte, TaxsutraMay 30, 2015

ICAI Pune – Direct Tax Refresher Courese

2

Contents1. Sec 206AA and Sec 195

2. Non-discrimination and TDS

3. Source rule on FTS payments (GVK)

4. Source rule on FTS payments (Luftansa)

5. Set-off – Constructive payment

6. Customer Discount = Interest

7. New Sec 195(1) explanation

8. Export Commission – not FTS (HC)

9. New Circular 3 on Sec 195 and Sec 40(a)

3

Sec 195 What does the section say ?

Any person responsible for paying to a non-resident, not being a company, or to a foreign company, any interest (not being interest referred to in section 194LB or section 194LC 1 or section 194LD) or any other sum chargeable under the provisions of this Act (not being income chargeable under the head “Salaries”) shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, deduct income-tax thereon at the rates in force

4

Recent Judicial Pronouncements

5

Sec 206AA 206AA. (1) Notwithstanding anything contained in any other provisions of this Act, any person entitled to receive any sum or income or amount, on which tax is deductible under Chapter XVIIB (hereafter referred to as deductee) shall furnish his Permanent Account Number to the person responsible for deducting such tax (hereafter referred to as deductor), failing which tax shall be deducted at the higher of the following rates, namely:—

(i) at the rate specified in the relevant provision of this Act; or

(ii) at the rate or rates in force; or

(iii) at the rate of twenty per cent.

1/3

6

Sec 206AA vs 90(2)

• DDIT vs. Serum Institute of India Limited [TS-158-ITAT-2015(PUN)]

• Pune ITAT ruled that Sec 206AA is not a charging section and the same can’t override Sec 90(2) of the Act.

• Provisions of Chapter XVII-B governing TDS not subordinate to Sec 90(2) and also cannot override provisions of Sec 4 and 5 of the IT Act .

• Also Sec 206AA is not charging section but is a part of procedural provisions dealing with collection and TDS

• Lower TDS as per DTAA applicable and not higher rate as per Sec 206AA on royalty and FTS payments to NR without PAN

2/3

7

Sec 206AA vs 90(2)

• Provisions of section 195 of the Act which casts a duty on the assessee to deduct tax at source on payments to a non-resident cannot be looked upon as a charging provision

• While arriving at the decision ITAT relied on SC rulings in Eli Lily & Co and GE India Technology Centre Pvt. Ltd and Azadi Bachao Andolan

• Bangalore ITAT: Bosch Ltd. [TS-904-ITAT-2012(Bang)] - Higher rate of 20% u/s 206AA not applicable for tax grossing-up u/s 195A, if TDS is borne by the Indian payerWrit before Karnataka HC :

• Sec 206AA is ultra vires the provisions of Sec 139A, Rule 114C and Sec 90

• Sec 206AA is only confined to 'furnishing' of PAN and not to 'obtaining' of PAN

3/3

8

Non-discrimination & TDS • Mitsubishi Corporation India Pvt. Ltd [TS-647-ITAT-2014(DEL)]

• Payment for purchase of goods from non-resident having Indian PE

• AO sought to invoke disallowance u/s 40(a)(i)(a) for failure to deduct tax at source

• Invoking of non-discrimination article under the treaty

1/3

9

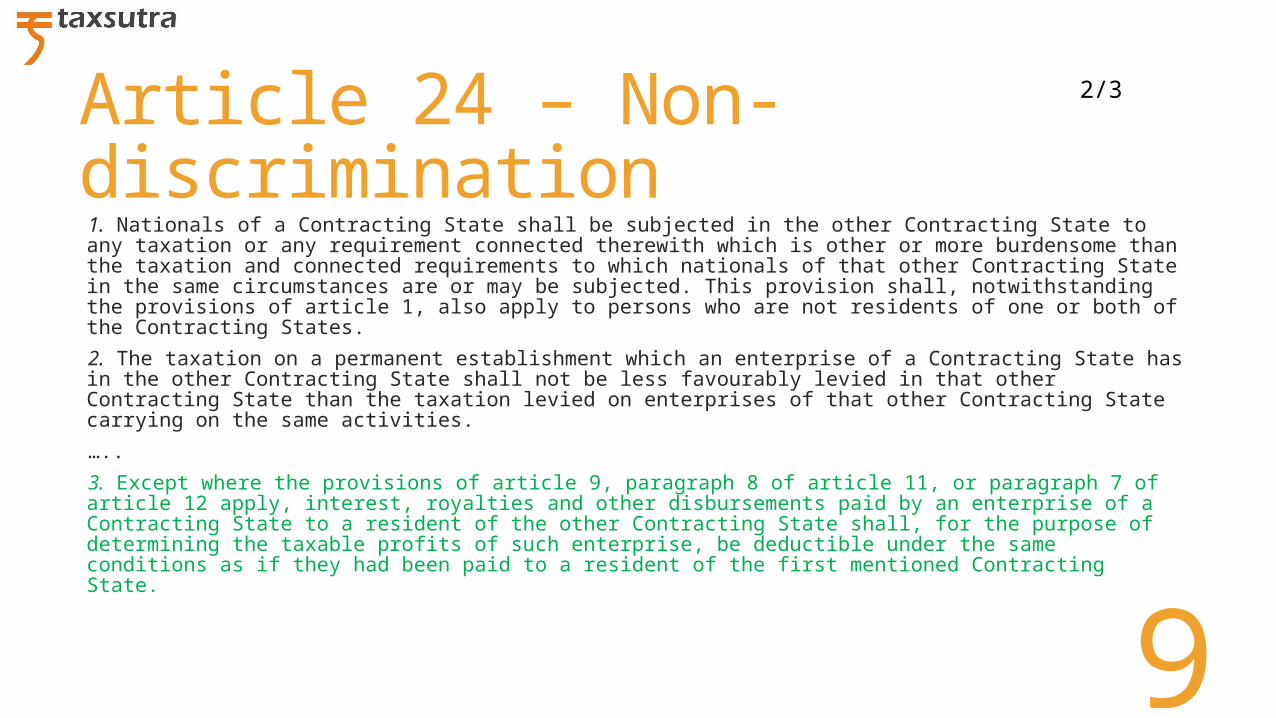

Article 24 – Non-discrimination 1. Nationals of a Contracting State shall be subjected in the other Contracting State to any taxation or any requirement connected therewith which is other or more burdensome than the taxation and connected requirements to which nationals of that other Contracting State in the same circumstances are or may be subjected. This provision shall, notwithstanding the provisions of article 1, also apply to persons who are not residents of one or both of the Contracting States.

2. The taxation on a permanent establishment which an enterprise of a Contracting State has in the other Contracting State shall not be less favourably levied in that other Contracting State than the taxation levied on enterprises of that other Contracting State carrying on the same activities.

…..

3. Except where the provisions of article 9, paragraph 8 of article 11, or paragraph 7 of article 12 apply, interest, royalties and other disbursements paid by an enterprise of a Contracting State to a resident of the other Contracting State shall, for the purpose of determining the taxable profits of such enterprise, be deductible under the same conditions as if they had been paid to a resident of the first mentioned Contracting State.

2/3

10

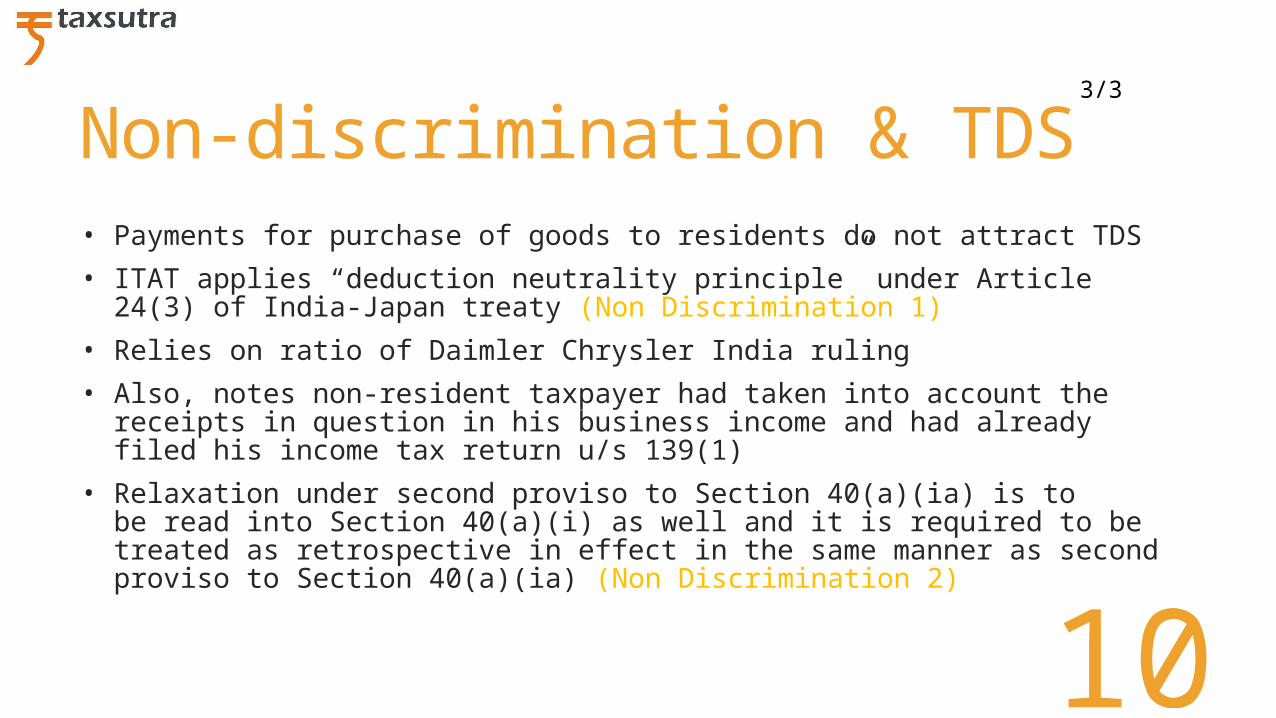

Non-discrimination & TDS • Payments for purchase of goods to residents do not attract TDS

• ITAT applies “deduction neutrality principle” under Article 24(3) of India-Japan treaty (Non Discrimination 1)

• Relies on ratio of Daimler Chrysler India ruling

• Also, notes non-resident taxpayer had taken into account the receipts in question in his business income and had already filed his income tax return u/s 139(1)

• Relaxation under second proviso to Section 40(a)(ia) is to be read into Section 40(a)(i) as well and it is required to be treated as retrospective in effect in the same manner as second proviso to Section 40(a)(ia) (Non Discrimination 2)

3/3

11

Source rule on FTS payments (GVK)• GVK Industries Ltd & Anr Vs ITO [TS-61-SC-2015]

• Payment of ‘success fee’ to a Swiss co., acting as a ‘financial advisor’ to GVK Industries Ltd. ('assessee')

• Financial structure, alternate sources of borrowings within and outside India, assessment of export credit rating agencies, loan negotiation & documentation with lenders

• Money was raised in India and abroad by assesse based on Swiss company’s services

• SC Constitution Bench rules on powers of the Parliament to rule the law having extra-territorial application – nexus with India theory laid down

1/3

12

Source rule on FTS payments (GVK)• Explains Source versus Residence concept of taxation

• Source based taxation is 'accepted' & 'applied' in international tax law and that ".. source rule is in consonance with the nexus theory and does not fall foul of the said doctrine on the ground of extra-territorial operation..”

• FTS = Technical, managerial or consultancy services

• Consultancy means giving professional advice or services in a specialized field

• Swiss co. acted as a consultant, “It had the skill, acumen and knowledge in the specialized field i.e. preparation of a scheme for required finances and to tie-up required loans”

2/3

13

Source rule on FTS payments (GVK)• Quotes AAR ruling [(1999) 242 ITR 280] = Consultancy includes

advisory whether or not expertise in technology is required to perform it

• Delhi HC decision in Bharti Cellular Limited (2009) 319 ITR 139] = It is obvious that the service of consultancy also necessarily entails human intervention. The consultant, who provides the consultancy service, has to be a human being. A machine cannot be regarded as a consultant.

• Success fees in the nature of consultancy and taxable in India • The case did not discuss India-Switzerland DTAA

• No business connection in India u/s 9(1)(i)

3/3

14

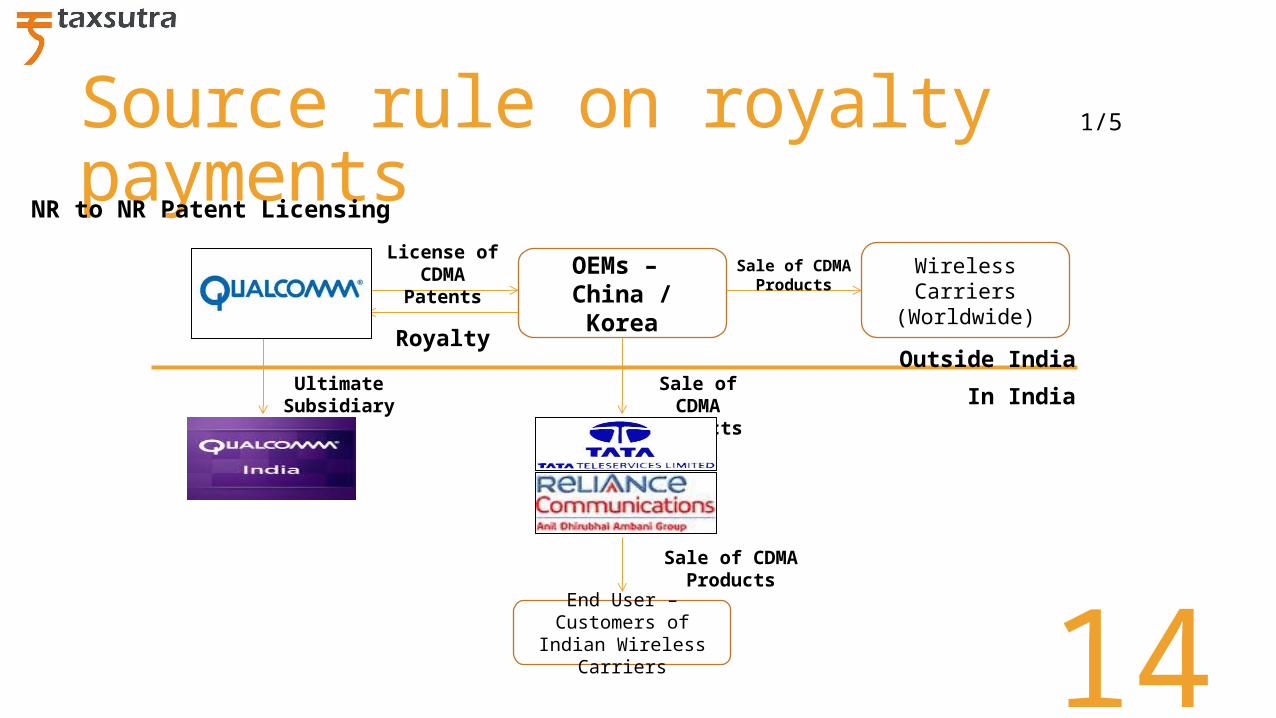

Source rule on royalty payments

OEMs – China / Korea

Wireless Carriers

(Worldwide)

Outside India

In India

License of CDMA

Patents

Sale of CDMA

Products

Royalty

Ultimate Subsidiary

Sale of CDMA

Products

End User – Customers of Indian

Wireless Carriers

Sale of CDMA Products

1/5

NR to NR Patent Licensing

15

Royalty - Sec 9(1)(vi) Sec 9(1)(vi) :

The following incomes shall be deemed to accrue or arise in India :

(vi) income by way of royalty payable by—

(a) the Government ; or

(b) a person who is a resident, except where the royalty is payable in respect of any right, property or information used or services utilised for the purposes of a business or profession carried on by such person outside India or for the purposes of making or earning any income from any source outside India ; or

(c) a person who is a non-resident, where the royalty is payable in respect of any right, property or information used or services utilised for the purposes of a business or profession carried on by such person in India or for the purposes of making or earning any income from any source in India

2/5

16

Source rule on royalty payments• Qualcomm Incorporated vs ADIT [TS-70-ITAT-2015(DEL)]

• Delhi ITAT ruled on taxability of royalty received by assessee (Qualcomm Incorporated, a US co.) from foreign Original Equipment Manufacturers (‘OEMs’) on sale of CDMA technology-enabled handsets & equipment to Reliance & Tata group in India

• The actual controversy, was whether the royalty paid will be taxable in the tax jurisdiction in which the handsets are manufactured, i.e. the situs of manufacture of handsets, or in the tax jurisdiction where the handsets are used, i.e. the situs of use of handsets

• Interpretation of Sec 9(1)(vi)(c)

3/5

17

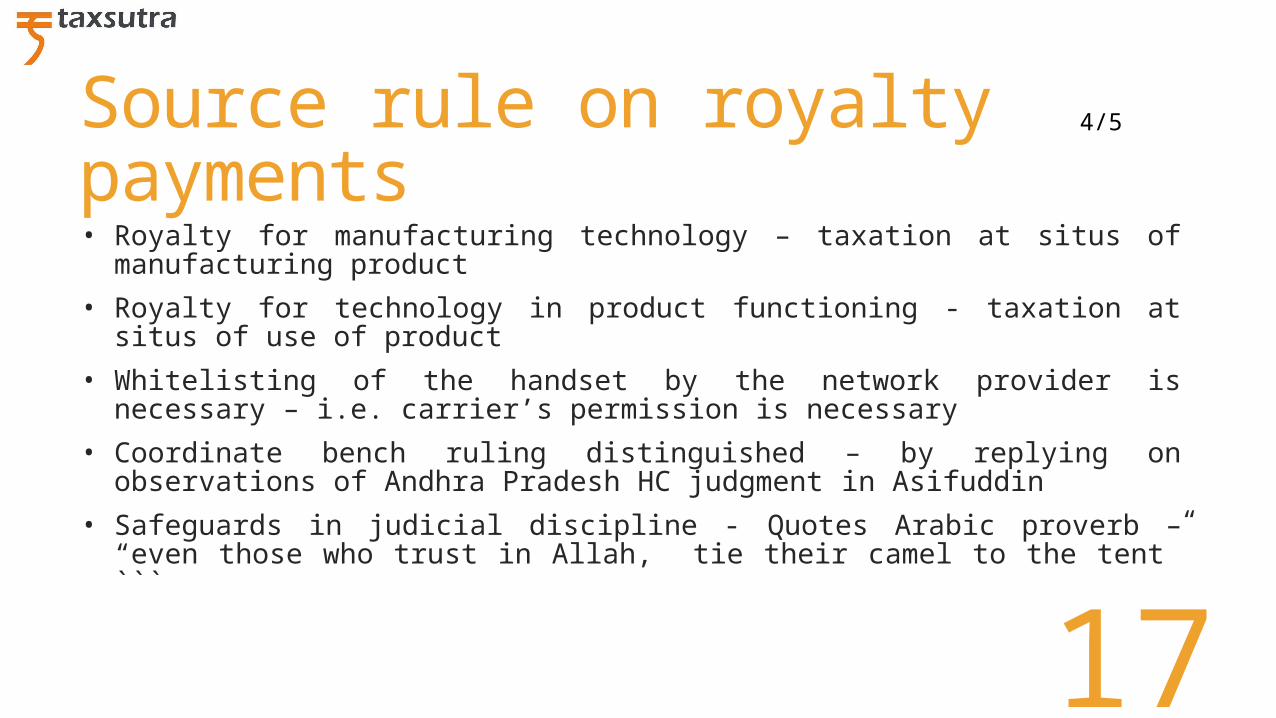

Source rule on royalty payments• Royalty for manufacturing technology – taxation at situs of

manufacturing product

• Royalty for technology in product functioning - taxation at situs of use of product

• Whitelisting of the handset by the network provider is necessary – i.e. carrier’s permission is necessary

• Coordinate bench ruling distinguished – by replying on observations of Andhra Pradesh HC judgment in Asifuddin

• Safeguards in judicial discipline - Quotes Arabic proverb – “even those who trust in Allah, tie their camel to the tent” ```

4/5

18

Source rule on royalty payments• Situs for use of patent – place where patent is used a decisive

factor rather than location of the payer

• Tribunal- “When an OEM is making an India specific product and when that assessee is carrying out a part of his business activities in India, it cannot be said that the assessee is not carrying on business, even if not manufacturing, in India.”

• CDMA – Code Division Multiple Access

• SIM – Subscriber Identity Module

5/5

19

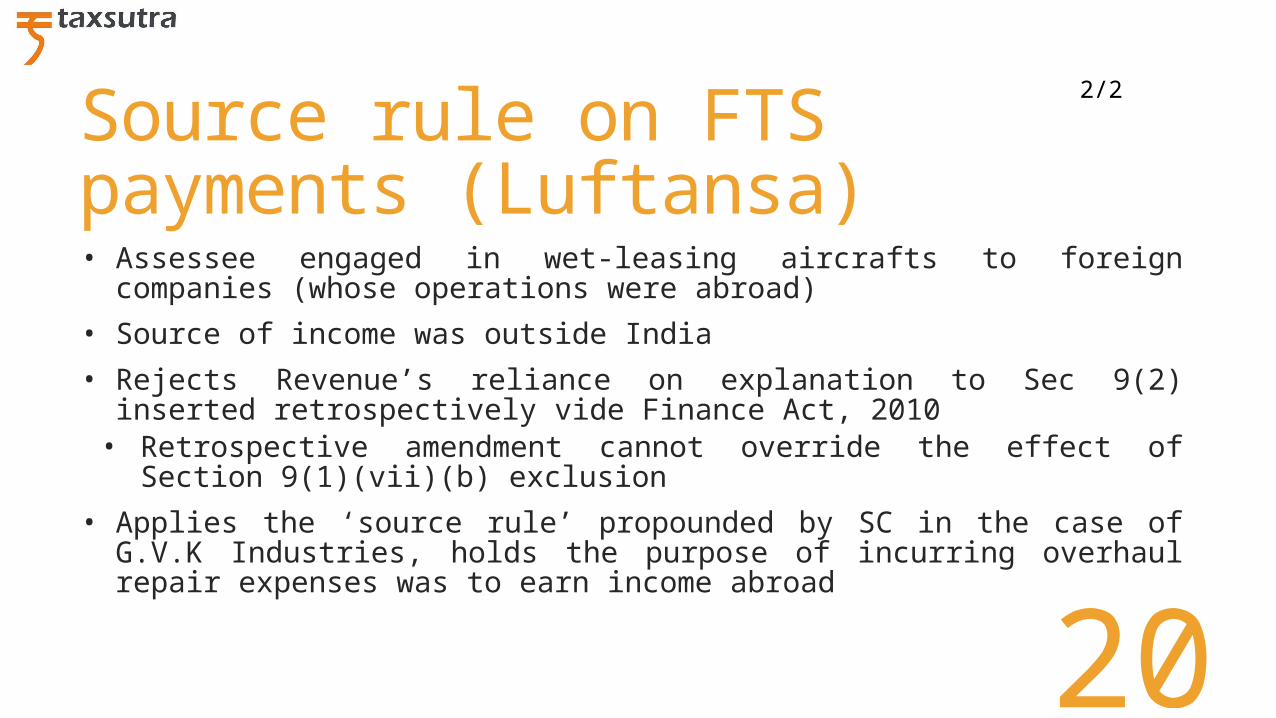

Source rule on FTS payments (Luftansa)• Lufthansa Cargo India [TS-299-HC-2015(DEL)]

• Luftanasa Cargo paid to a German co. for carrying out overhaul repairs to aircrafts

• Luftanasa Cargo engaged in wet-leasing of aircrafts to foreign companies

• Assessee was obliged to maintain the aircraft in flying condition, in accordance with DGCA guidelines to possess a valid airworthiness certificate, hence it entered into overhaul agreement with a German co.

• Such services are ‘technical’ in nature

• However, services fell in exclusionary part of Sec 9(1)(vii)(b) (FTS not taxable in India where services are utilized for earning income from any source outside India)

1/2

20

Source rule on FTS payments (Luftansa)• Assessee engaged in wet-leasing aircrafts to foreign companies

(whose operations were abroad)

• Source of income was outside India

• Rejects Revenue’s reliance on explanation to Sec 9(2) inserted retrospectively vide Finance Act, 2010

• Retrospective amendment cannot override the effect of Section 9(1)(vii)(b) exclusion

• Applies the ‘source rule’ propounded by SC in the case of G.V.K Industries, holds the purpose of incurring overhaul repair expenses was to earn income abroad

2/2

21

Set-off – Constructive payment

• Right Tunnelling Co. Ltd. vs ADIT [TS-220-ITAT-2014(DEL)]

Thai Main Contractor

(non-resident)

Assessee – Thai Sub-Contractor

(non-resident)Machinery Hire charges due

Contract payment after adjusting machinery hire charges

Is Sec 195 TDS applicable?

1/2

22

Set-off – Constructive payment

• Assessee: Sec 195 was not attracted for the reason that the assessee was not “responsible to pay” hire charges, as the arrangement was such that contractor recovered the same from contract dues.

• Assessee: Intent and language of the provision did not take into account a situation where no actual payment was stipulated

• ITAT : “Just because certain obligations, terms & conditions etc. have been agreed to between the parties, it does not lead to a conclusion that there is no hirer and hiree relationship”

• Methods of settlement of accounts is of no consequence, adjustment of hire charges against contract dues amounts to ‘constructive payment’, liable to TDS

2/2

23

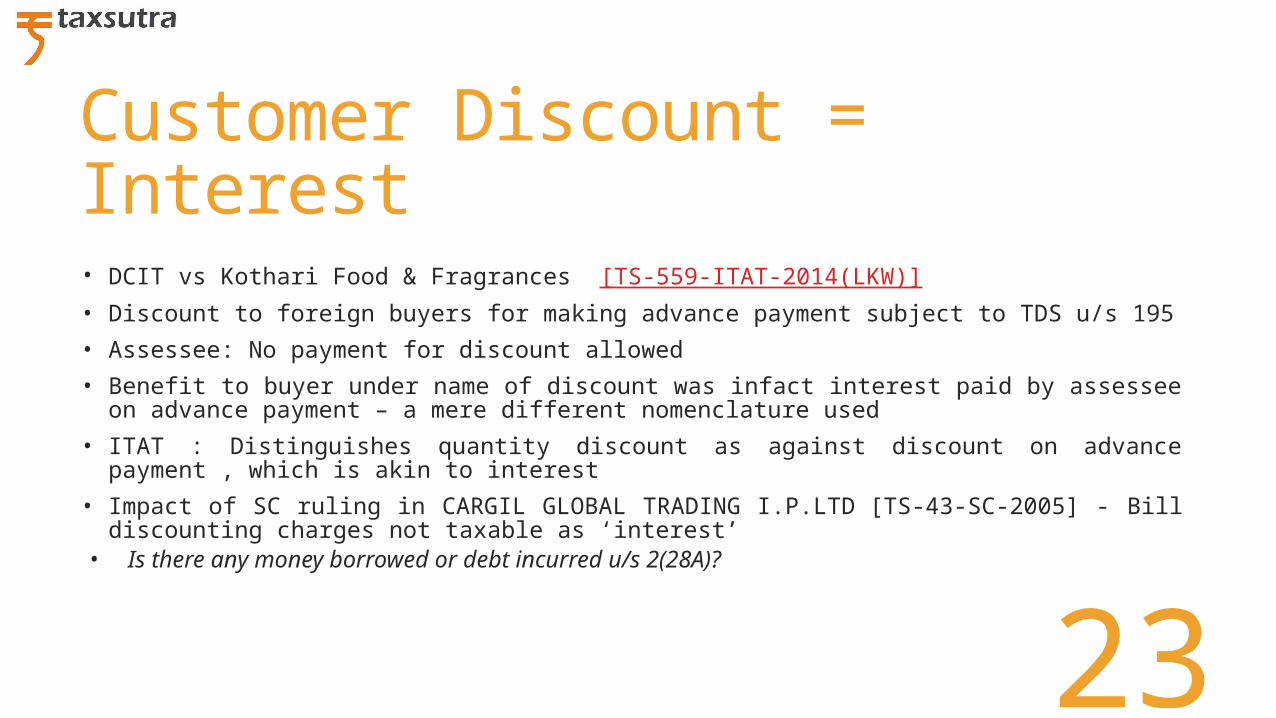

Customer Discount = Interest

• DCIT vs Kothari Food & Fragrances [TS-559-ITAT-2014(LKW)]

• Discount to foreign buyers for making advance payment subject to TDS u/s 195

• Assessee: No payment for discount allowed

• Benefit to buyer under name of discount was infact interest paid by assessee on advance payment – a mere different nomenclature used

• ITAT : Distinguishes quantity discount as against discount on advance payment , which is akin to interest

• Impact of SC ruling in CARGIL GLOBAL TRADING I.P.LTD [TS-43-SC-2005] - Bill discounting charges not taxable as ‘interest’

• Is there any money borrowed or debt incurred u/s 2(28A)?

24

New Sec 195(1) explanation• ACIT vs Vilas N Tamhankar [TS-726-ITAT-2014(Kol)]

• Payments made to Canadian resident for sales & marketing support outside India

• Services entirely rendered from outside India

• New Explanation 2 to Sec 195(1) - Sec 195 will apply irrespective of whether payee has a residence or place of business or business connection in India

• It would not disturb the law laid down in GE India and would not be of any consequence in present case when payee did not have any business connection / presence in India

• Explanation only seeks to remove the issue of determination of tax incidence on basis of whether payee is a tax resident in India from being a consideration for non-deduction of tax u/s195

25

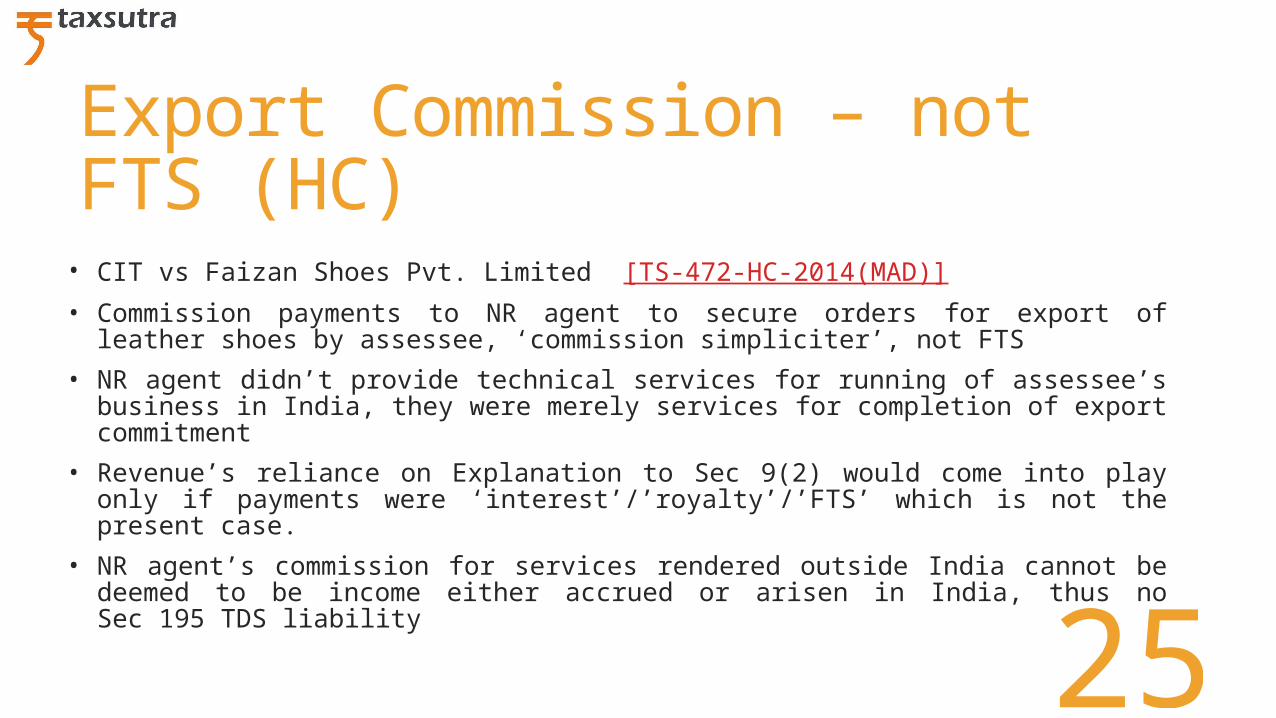

Export Commission – not FTS (HC)

• CIT vs Faizan Shoes Pvt. Limited [TS-472-HC-2014(MAD)]

• Commission payments to NR agent to secure orders for export of leather shoes by assessee, ‘commission simpliciter’, not FTS

• NR agent didn’t provide technical services for running of assessee’s business in India, they were merely services for completion of export commitment

• Revenue’s reliance on Explanation to Sec 9(2) would come into play only if payments were ‘interest’/’royalty’/’FTS’ which is not the present case.

• NR agent’s commission for services rendered outside India cannot be deemed to be income either accrued or arisen in India, thus no Sec 195 TDS liability

26

CBDT Circular 3/2015

• For disallowance of “other sum chargeable” u/s 40(a)(i) (other than royalty, FTS, etc), the basis would be “appropriate portion of the sum chargeable to tax”, and not the gross amount

• Disallowance u/s 40(a)(i) regarding ‘other sum chargeable’ is triggered when deductor fails to withhold taxes as per Sec 195

• Sec 40(a)(i) disallowance in case of a deductor is interlinked with the “sum chargeable under the Act” as mentioned u/s 195 for the purpose of TDS

• Disallowance amount shall be the same as determined by AO as per Instruction no. 2/2014 dated Feb 26, 2014 which had clarified that in cases on non-deduction of TDS u/s 195, AO to determine appropriate portion of sum chargeable to tax, to ascertain tax liability on which deductor shall be deemed as assessee in default u/s 201

27

Thank YouContact Details:

Email - [email protected]

Mobile - 9823038088

Views are personal. Presentation for academic discussion only.

28

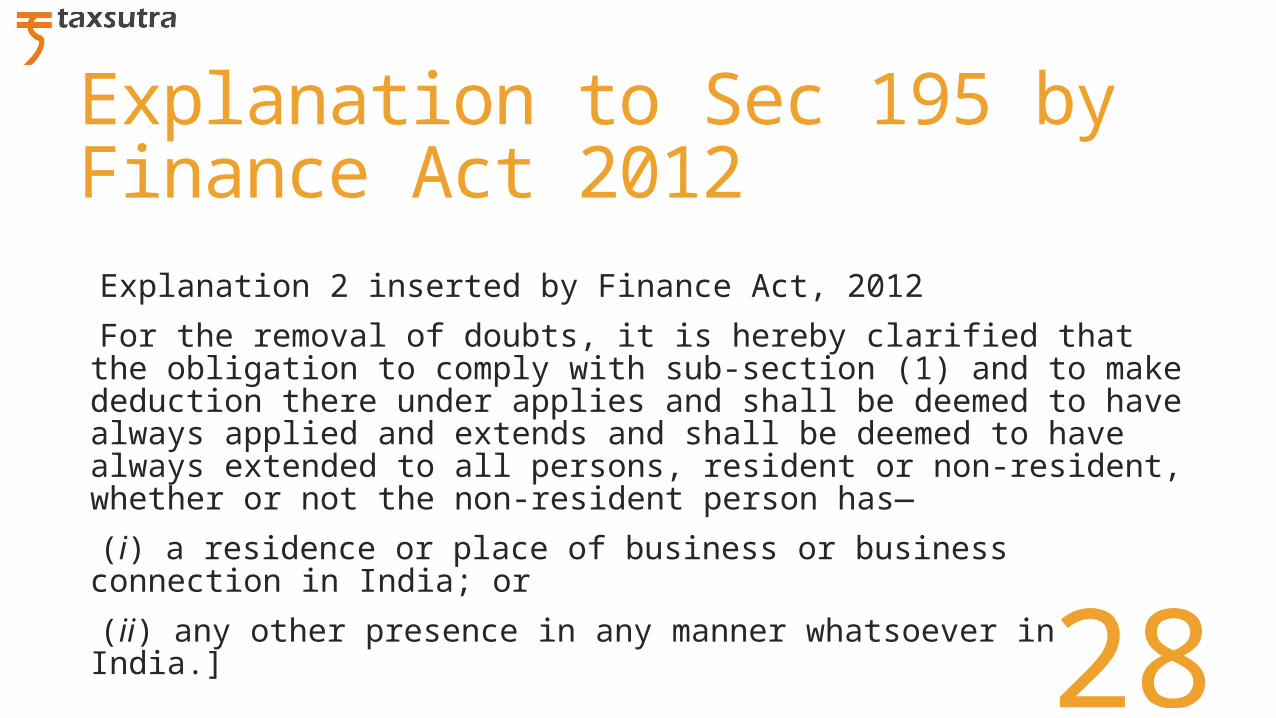

Explanation to Sec 195 by Finance Act 2012 Explanation 2 inserted by Finance Act, 2012

For the removal of doubts, it is hereby clarified that the obligation to comply with sub-section (1) and to make deduction there under applies and shall be deemed to have always applied and extends and shall be deemed to have always extended to all persons, resident or non-resident, whether or not the non-resident person has—

(i) a residence or place of business or business connection in India; or

(ii) any other presence in any manner whatsoever in India.]

29

Royalty - Sec 9(1)(vi) Sec 9(1)(vi) :

The following incomes shall be deemed to accrue or arise in India :

(vi) income by way of royalty payable by—

(a) the Government ; or

(b) a person who is a resident, except where the royalty is payable in respect of any right, property or information used or services utilised for the purposes of a business or profession carried on by such person outside India or for the purposes of making or earning any income from any source outside India ; or

(c) a person who is a non-resident, where the royalty is payable in respect of any right, property or information used or services utilised for the purposes of a business or profession carried on by such person in India or for the purposes of making or earning any income from any source in India

30

Fees for Technical Services : Sec 9(1)(vii)

Sec 9(1)(vii) :

The following incomes shall be deemed to accrue or arise in India :

(vii) income by way of fees for technical services payable by—

(a) the Government ; or

(b) a person who is a resident, except where the fees are payable in respect of services utilised in a business or profession carried on by such person outside India or for the purposes of making or earning any income from any source outside India ; or

(c) a person who is a non-resident, where the fees are payable in respect of services utilised in a business or profession carried on by such person in India or for the purposes of making or earning any income from any source in India