50

Contents Sectoral Trends: Performance of the primary and secondary sectors of the South African economy – statistical update 3 rd Quarter 2014 Department of Research and Information

Contents

Sectoral Trends: Performance of the primary and secondary sectors

of the South African economy – statistical update

3rd Quarter 2014

Department of Research and Information

Contents

Highlights 1

Performance of the primary and secondary sectors

Physical volume of production 6

Production capacity utilisation 6

Employment 7

Remuneration 7

Exports 8

Imports 8

Selected trade trends (excluding trade with BLNS)

Trade balance 9

Major traded products 9

Composition of trade 9

Regional trade 9

Trade trends with major regions or regional blocs 10

Performance of the primary and secondary sub-sectors: statistical synopsis

Agriculture, forestry and fishing 12

Total mining 13

- Coal mining 14

- Gold and uranium mining 15

- PGM mining 16

- Iron ore mining 17

- Other mining 18

Total manufacturing 19

- Food 20

- Beverages 21

- Textiles 22

- Wearing apparel 23

- Leather and leather products 24

- Footwear 25

- Wood and wood products 26

- Paper and paper products 27

- Printing, publishing and recorded media 28

- Coke and refined petroleum products 29

- Basic chemicals 30

- Other chemicals and man-made fibres 31

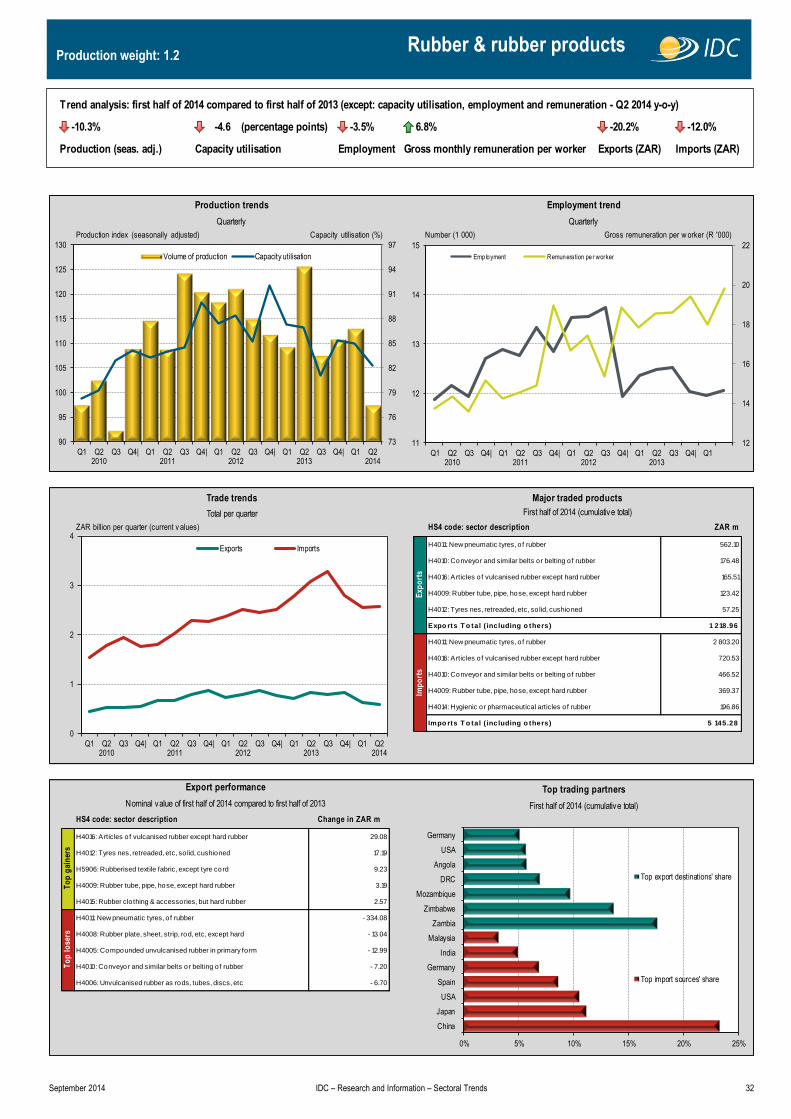

- Rubber products 32

- Plastic products 33

- Glass and glass products 34

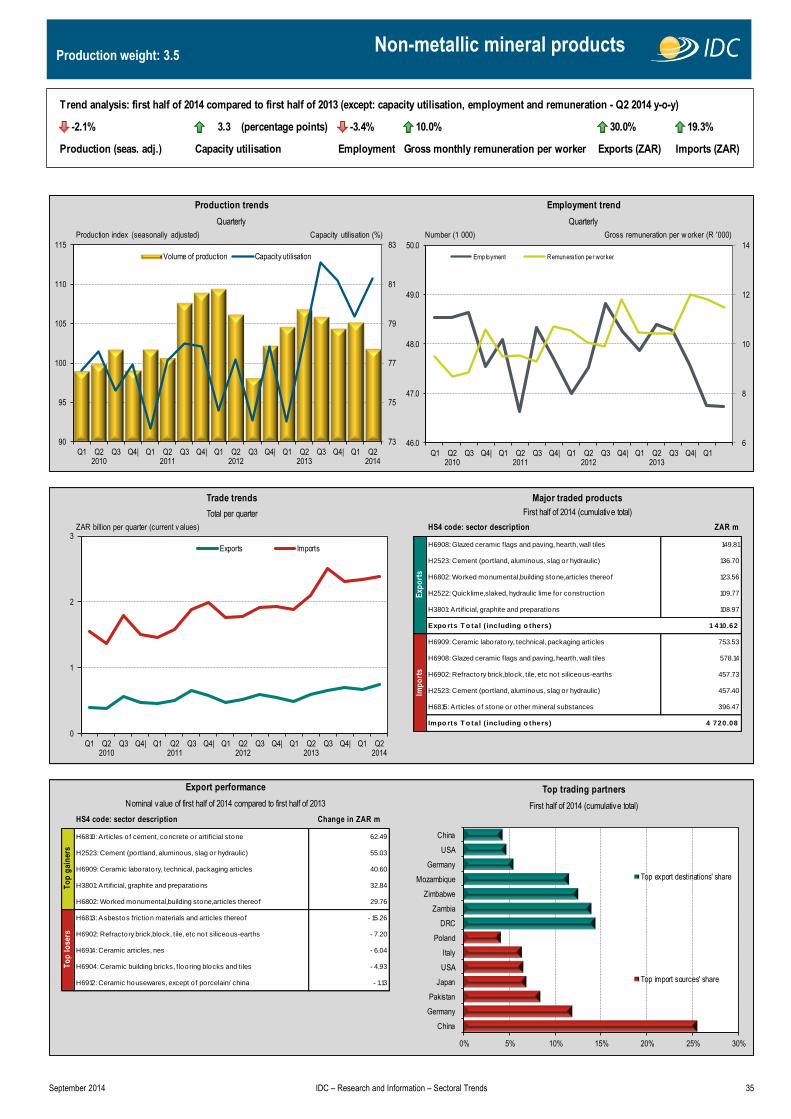

- Non-metallic mineral products 35

- Basic iron and steel 36

- Basic non-ferrous metallic products 37

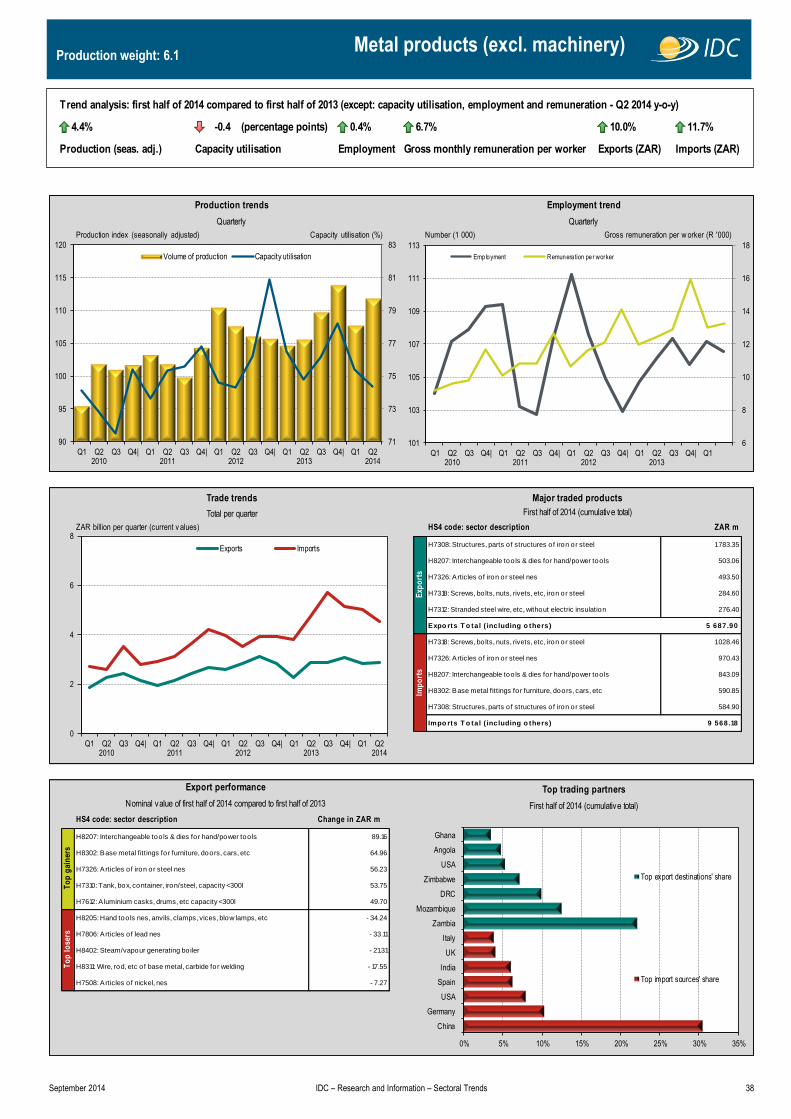

- Metal products excluding machinery 38

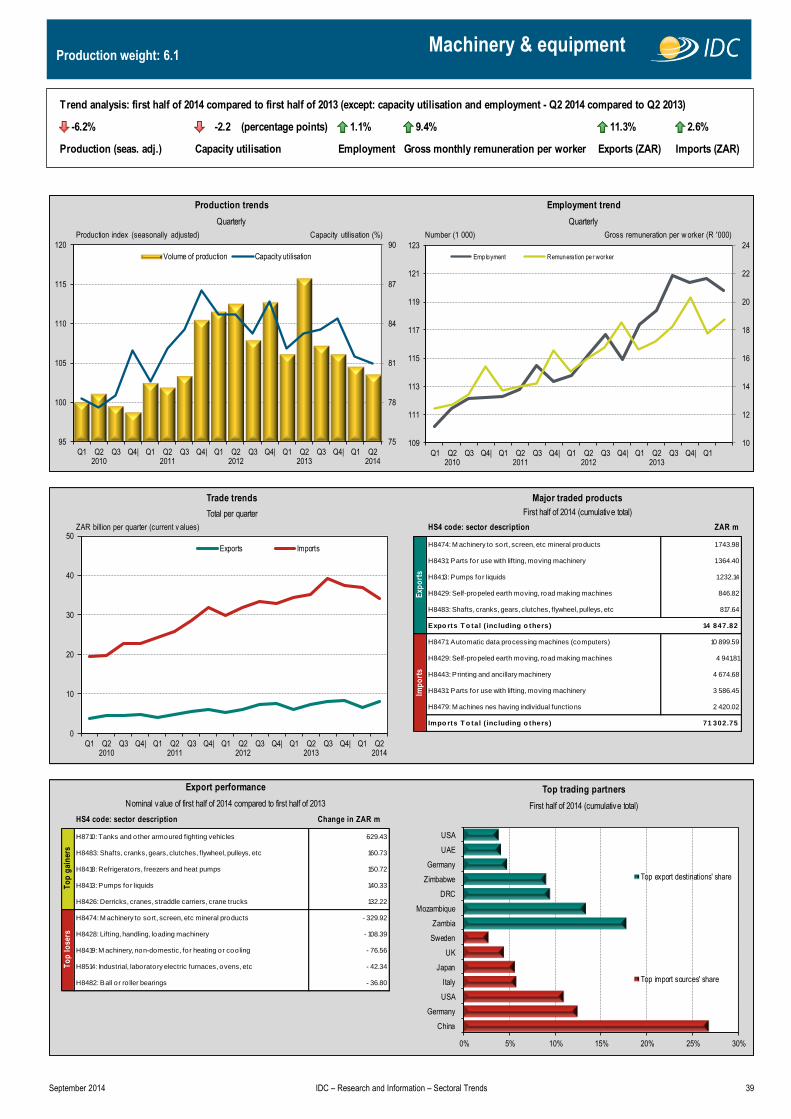

- Machinery and equipment 39

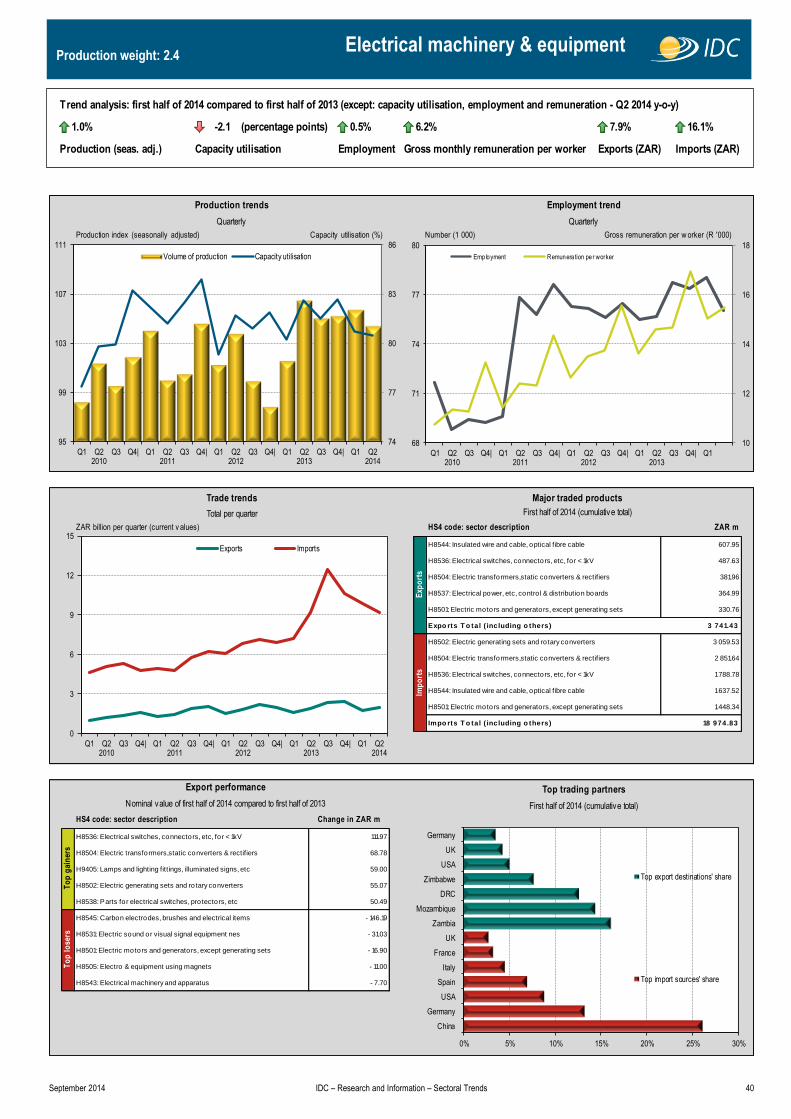

- Electrical machinery 40

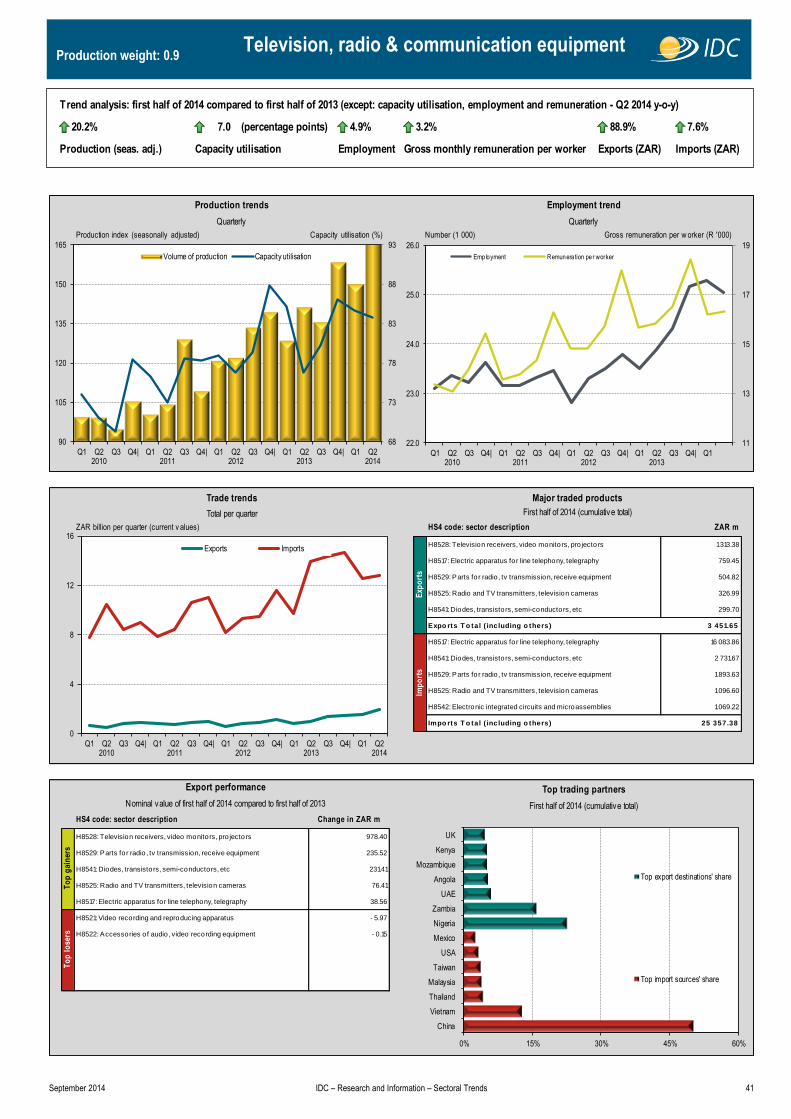

- Television, radio and communication equipment 41

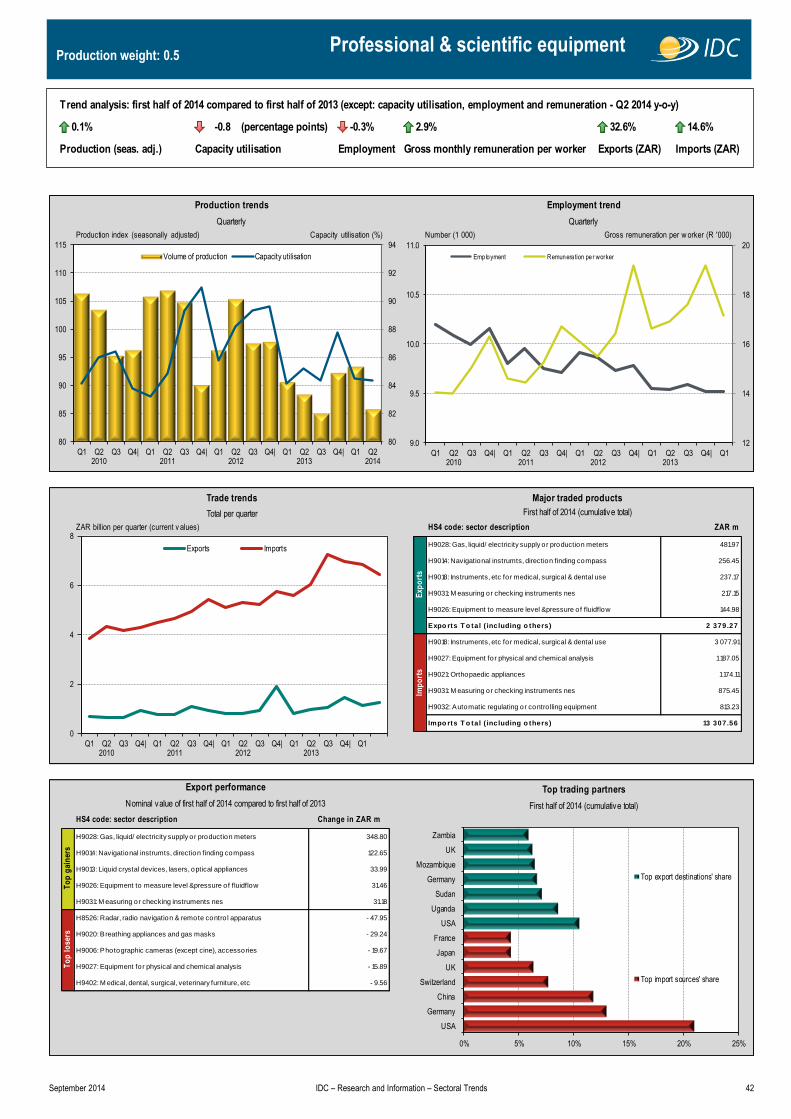

- Professional and scientific equipment 42

- Motor vehicles, parts and accessories 43

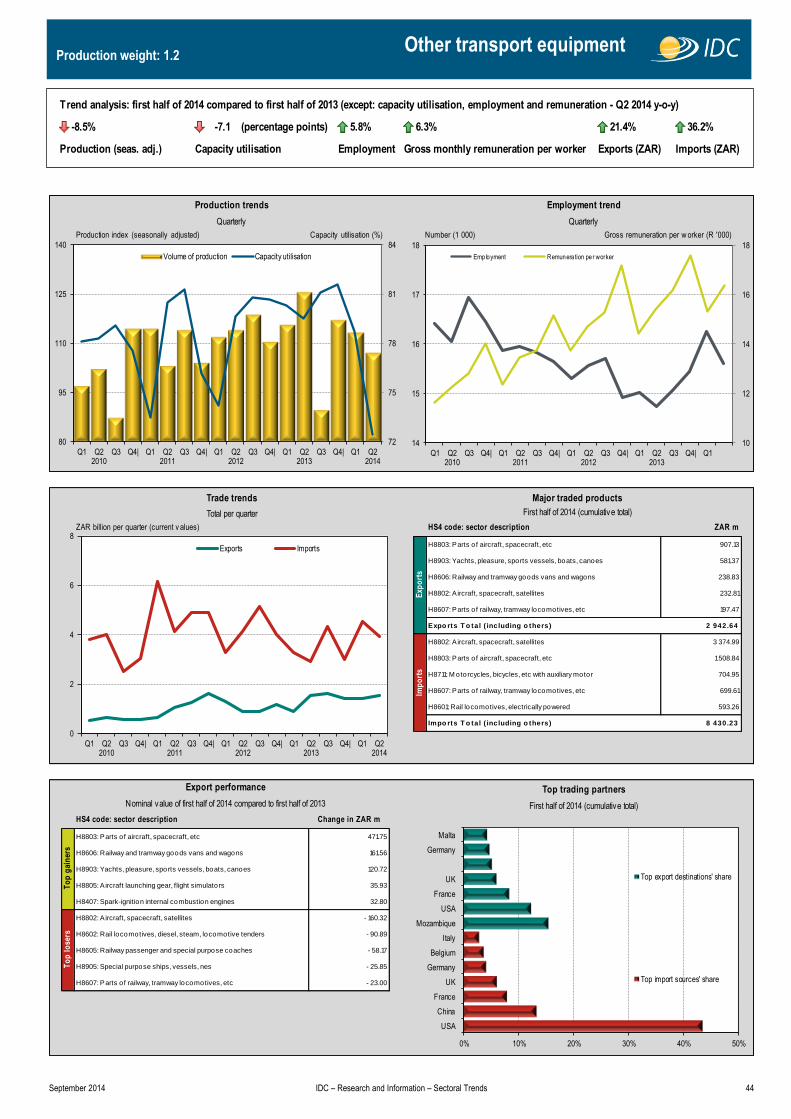

- Other transport equipment 44

- Furniture 45

- Other manufacturing 46

Acronyms, notes and data sources 47

September 2014 IDC – Research and Information – Sectoral Trends 1

Highlights

Value added (agriculture sector) and physical volume of production (mining and manufacturing

sectors)

Valued added by the agriculture, forestry and fishing sector benefitted from favourable weather

conditions early in the first semester of 2014, with good rain in the major maize growing areas. This

resulted in 3.3% growth in real terms relative to the corresponding period in 2013 (refer to Figure 1 on

page 6), mainly due to higher output of field crops and livestock.

The adverse effects of the protracted strike in the platinum group metals (PGM) mining sub-sector were

reflected in the 27.8% contraction (year-on-year) in its physical volume of production in the first half of

2014, with its large weighting impacting negatively on the performance of the overall mining sector. The

‘other mining’ sub-sector (including manganese ore, chrome ore, nickel, copper, building materials and

diamonds) and iron ore mining reported solid increases in production volumes in the opening half of the

year, although output of manganese, iron ore and, to a lesser extent, chrome ore tapered off towards the

end of the period. Nonetheless, on a cumulative basis over the six-month period, manganese and nickel

production was substantially higher relative to the corresponding period in 2013, posting increases of

approximately 27.3% and 14.6%, respectively, while diamond production was 17.6% higher. Output of

coal (-0.8% year-on-year) and copper (-0.1%) was marginally lower in the first semester of 2014, and

the downward trend in gold production continued unabated.

The physical volume of production in the broad manufacturing sector remained unaltered in the opening

half of 2014 relative to the corresponding period in 2013. Major segments of the manufacturing sector

continued to face difficult trading conditions in key external markets, particularly in Europe.

Domestically, demand conditions deteriorated due to the spill-over effects of the industrial action

induced production stoppages in platinum mining during the first five months of 2014, as well as

weakening household demand for consumption goods. Manufacturing sub-sectors with strong linkages

to mining activity, such as machinery and equipment, ‘other transport equipment’, ‘other chemicals’ and

rubber products reported lower production volumes. Sub-sectors that recorded substantially higher

output levels included television, radio and communication equipment; leather and leather products; and

coke and refined petroleum products.

Utilisation of production capacity in manufacturing

Despite flat overall production volumes, the broad manufacturing sector reported a marginal increase in

the utilisation of its production capacity in the second quarter of 2014 relative to the same period a year

earlier, as illustrated in Figure 2 on page 6. This may be indicative of a slight loss of production capacity.

September 2014 IDC – Research and Information – Sectoral Trends 2

Highlights

The higher output levels posted by the television, radio and communication equipment sub-sector and

the coke and refined petroleum products sub-sector were confirmed by a higher utilisation of their

production capacity in the year to the second quarter of 2014.

In contrast, the furniture sub-sector continued to experience difficult operating conditions as reflected by

lower production volumes, and yet also reduced spare capacity, possibly indicating a decline in its

production capacity over the past year.

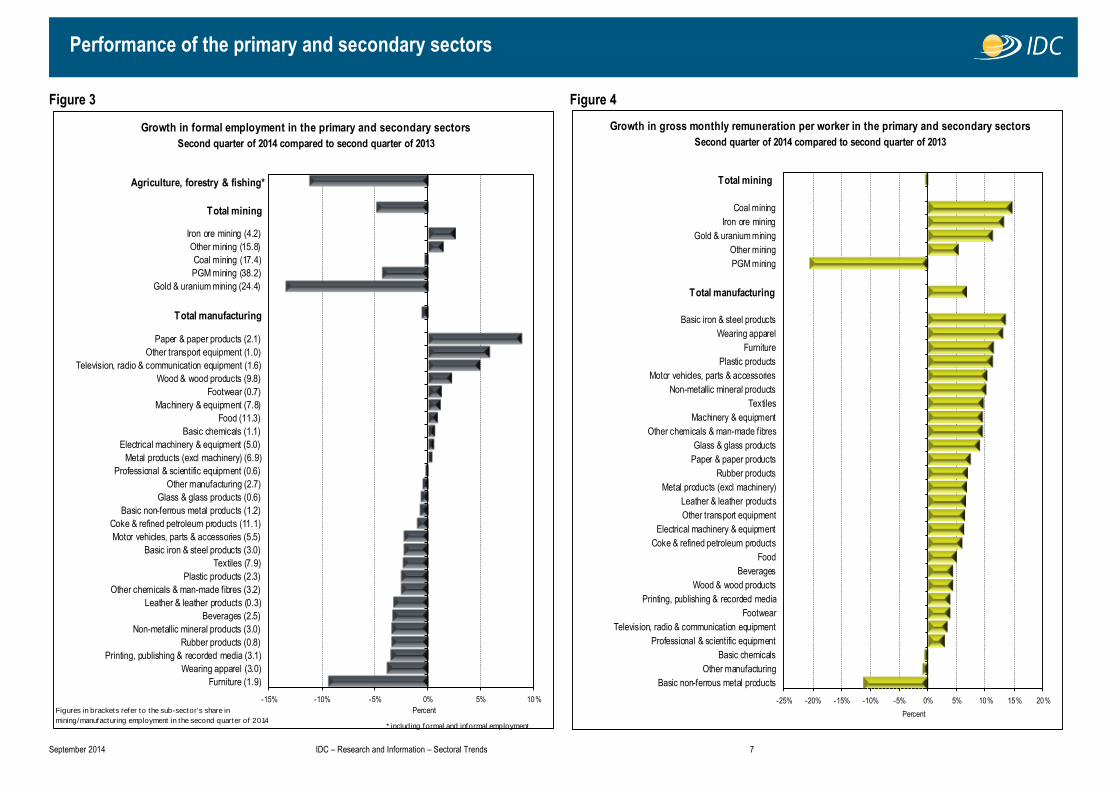

Employment

Employment levels in the agriculture, forestry and fishing sector declined by 83 000, or 11.2% of the

sector’s total employment, in the second quarter of 2014 compared to the same quarter in 2013 (refer to

Figure 3 on page 7). The contraction in employment since the first quarter of 2013, when the most

recent peak was recorded, amounted to 105 000 job losses. This adverse trend may be partly explained

by the sharp increase in the sector’s minimum wage during the latter part of 2013, which may have

reinforced its mechanisation drive.

Mining sector employment fell by approximately 25 000, or 4.9% of the total, in the year to the second

quarter of 2014. The majority of the job losses were attributable to the gold mining (-18 188) and

platinum group metals mining (-8 309) sub-sectors. The contraction reported in the gold mining sub-

sector was mainly due to a lower number of permanent employees, whilst the platinum group metals

mining sub-sector reduced the use of contract employees as the five-month long strike drew to a close

at the end of the second quarter of 2014.

Employment in the broad manufacturing sector declined by 9 000 in the second quarter of 2014 relative

to the levels reported a year earlier. The following sub-sectors recorded the largest job losses: furniture

(-3 104 jobs); textiles (-3 060); and motor vehicles, parts and accessories (-2 006). The wood and wood

products sub-sector as well as the paper and paper products sub-sector, in turn, reported substantial

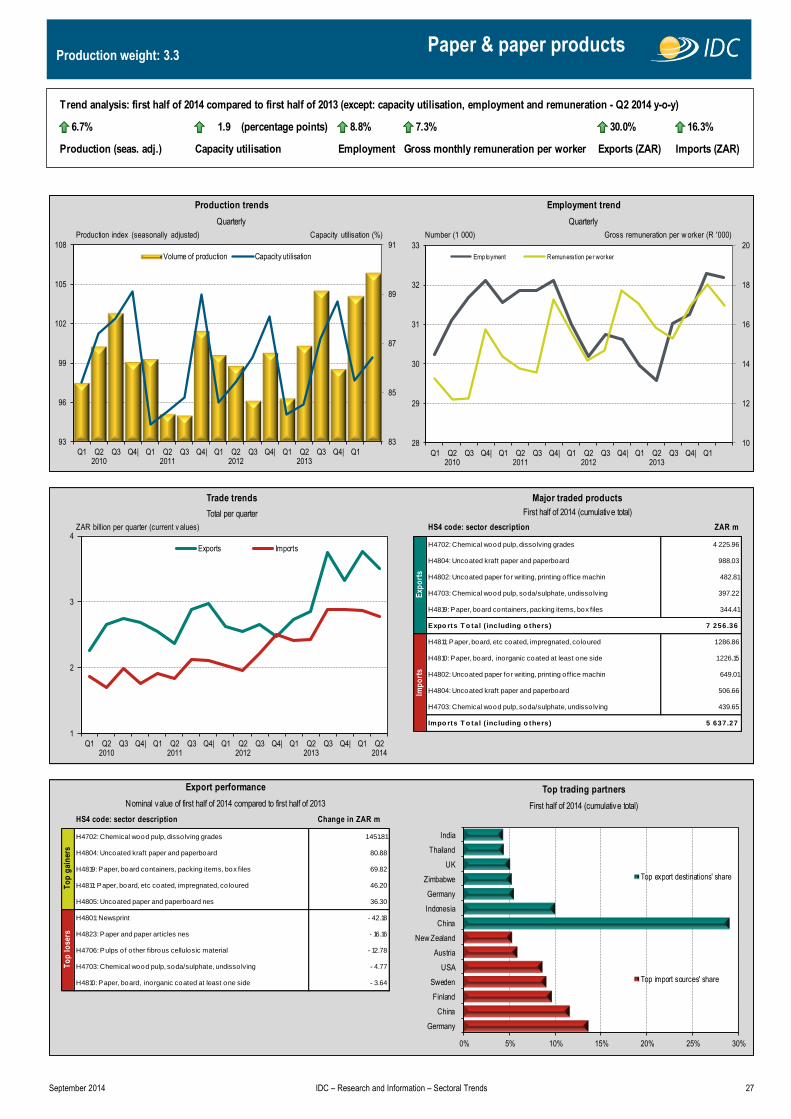

employment gains in the order of 3 336 and 2 612 additional jobs, respectively.

Further employment losses are expected in the overall manufacturing sector in the third quarter of 2014

considering the generally difficult trading conditions and above inflation wage increases settled upon in

segments of the sector at the end of a month-long strike.

Worker remuneration in mining and manufacturing

Gross remuneration per worker in the mining sector was clearly affected by protracted strike activity in

its platinum mining segment, as it declined by 0.5% over the 12-month period up to the second quarter

September 2014 IDC – Research and Information – Sectoral Trends 3

Highlights

of 2014 (refer to Figure 4 on page 7). Due to the ‘no-work-no-pay’ principle, the average remuneration

per worker in the platinum group metals mining sub-sector fell by 20.5% over this period.

Against the backdrop of declining employment at the broad sector level, gross remuneration per worker

in manufacturing increased by 7.4% in the year to the second quarter of 2014. At the sub-sector level,

the highest rates of increase were reported by the coke and refined petroleum as well as the ‘other

chemicals’ industries.

Trade balance (excl. BLNS)

South Africa’s external trade (excluding trade with Botswana, Lesotho, Namibia and Swaziland, also

known as the BLNS countries within the Southern African Customs Union) in the opening semester of

2014 was severely affected by the production stoppages associated with industrial action over the first

five months of the year, as well as by weaker global demand, especially in commodities markets. Import

demand, particularly for mineral products (mostly crude oil and refined petroleum and related products),

remained strong. The balance of trade recorded a cumulative deficit of R108.5 billion, representing a

26% increase on the R86.1 billion deficit reported in the first half of 2013 (refer to page 9).

The trade surplus with European countries outside of the European Union (EU) narrowed to R2.2 billion

in the opening semester of 2014, from R7.4 billion a year earlier. In contrast, the trade deficit with the EU

came in at R48.8 billion, compared to R58.3 billion in the first half of 2013.

A sharp increase in imports from the Middle East worsened South Africa’s trade deficit with this region

over the first six months of 2014 to almost R50 billion, from R35 billion in the corresponding period a

year earlier.

South Africa’s trade surplus with the rest of the African continent (excluding BLNS) remained almost

unchanged at R19.5 billion over the reporting period.

Exports (excl. BLNS)

South Africa’s merchandise exports (excluding exports to BLNS countries) totalled R403.4 billion in the

first semester of 2014, representing an 8.4% increase relative to the corresponding period in 2013, as

illustrated in Figure 5 on page 8.

Exports of the agriculture, forestry & fishing sector increased by 7.6% over this period, having benefitted

from a substantial rise in exports of edible fruits (such as citrus fruit, grapes, stone fruit, etc.). Exports of

maize, apples and groundnuts fell sharply over the period.

September 2014 IDC – Research and Information – Sectoral Trends 4

Highlights

The value of mining related exports declined marginally in the opening semester of 2014 on a year-on-

year basis. The exports of the gold mining sub-sector fell by R6.4 billion, while those of the PGMs mining

sub-sector were R3.7 billion lower. The stronger export performance of ores, especially manganese

(+R2.7 billion) and iron (+R1.3 billion), in conjunction with coal (+R1.3 billion) limited the impact of lower

precious metals’ exports.

Manufacturing exports increased by 16.2% in the first half of 2014 relative to the corresponding period a

year earlier. Iron and steel exports made a substantial contribution as these increased by R13.2 billion

over this period. Higher output levels in the television, radio and communications equipment supported

an 88.9% increase in the value its exports, the best performance of all manufacturing sub-sectors, albeit

off a very low base.

Asia remained the largest regional market for South Africa’s exports in the first semester of 2014. Mining

products dominated the export basket destined for this region, specifically iron ore, coal, non-ferrous

metals and PGMs. Iron and steel exports were also significant, with China, Japan and India as key Asian

destinations.

Although Asia remained the leading export destination, exports to the EU were the largest contributors to

the 9% year-on-year growth in overall exports in the first half of 2014. The export basket destined for EU

markets was dominated by basic iron and steel, PGMs, motor vehicles, parts and accessories for motor

vehicles, as well as cereals and other agricultural products. Germany, the United Kingdom, the

Netherlands and Belgium were the principal contributors to the growth in South Africa’s exports to the

EU over this period.

The rest of the African continent has become an increasingly important market for locally-produced

goods, accounting for approximately 18.7%, or R75.6 billion, of South Africa’s overall merchandise

export basket (excluding trade with BLNS countries). Importantly, the export basket destined for African

markets consists largely of manufactured goods and is quite diversified, comprising items such as

machinery and equipment (e.g. mining and agricultural machinery); transport equipment (including motor

vehicles and parts); base metals and fabricated metal products; chemicals; as well as processed food.

The decline in exports destined for the North American Free Trade Agreement (NAFTA) region was

mainly attributable to lower exports of spun and woven textiles.

Imports (excl. BLNS)

Merchandise imports (excluding imports from BLNS countries) during the first semester of 2014

amounted to R511.9 billion, representing an increase of 11.7% from the value recorded over the

corresponding period in 2013, as illustrated in Figure 6 on page 8.

September 2014 IDC – Research and Information – Sectoral Trends 5

Highlights

The value of imports of agricultural, forestry and fishing products increased by 36.4% over this period,

largely due to imports of oil seed (R920 million higher, or 188%) and cereals (R854 million higher, or

46%).

Mining imports similarly rose by 36.7%, driven mainly by increased imports of crude oil, which expanded

by R25.6 billion, and PGM ores (which increased by 641% year-on-year, or R1.1 billion) to cater for

insufficient domestic supply due to production stoppages.

Imports of manufactured goods increased by 5.9% in the year to the first semester of 2014, with import

demand for parts and accessories of motor vehicles, electric motors, generators and transformers, motor

vehicles, as well as for office, accounting and computing machinery rising sharply. Demand for imported

iron and steel products, in turn, fell 20.4% over this period.

Asia remained South Africa’s largest source of imported products, mostly supplying petroleum products,

motor vehicle parts and accessories, as well as television and radio transmitters, line telephony. China,

India, Japan, Thailand and Singapore were the most prominent sources of these imports.

The substantial growth in imports from the Middle East recorded in the first half of 2014 on a year-on-

year basis was attributable to sharply higher crude oil imports (R12.6 billion higher, or 36.4%) and some

refined petroleum imports (R1.5 billion higher, or 29.8%), sourced largely from Saudi Arabia and, to a

lesser extent, the United Arab Emirates and Kuwait.

September 2014 IDC – Research and Information – Sectoral Trends 6

Performance of the primary and secondary sectors

Figure 1 Figure 2

Growth in physical volume of production in the primary and secondary sectors

Average for the first half of 2014 compared to average for the first half of 2013 (Seasonally adjusted)

* Real value add

Figures in brackets refer to the sub-sector's percentage

share in mining/manufacturing product ion in the second quarter of 2014

-30% -20% -10% 0% 10% 20%

Glass & glass products (0.9)

Rubber products (1.2)

Other transport equipment (1.2)

Machinery & equipment (6.1)

Printing, publishing & recorded media (3.6)

Wearing apparel (1.1)

Other chemicals & man-made fibres (7.1)

Furniture (1.1)

Textiles (1.2)

Non-metallic mineral products (3.5)

Plastic products (3.1)

Footwear (0.4)

Basic non-ferrous metal products (3.5)

Professional & scientific equipment (0.5)

Motor vehicles, parts & accessories (7.4)

Beverages (6.4)

Electrical machinery & equipment (2.4)

Food (17.4)

Basic iron & steel products (4.7)

Basic chemicals (4.8)

Wood & wood products (2.6)

Metal products (excl machinery) (6.1)

Paper & paper products (3.3)

Other manufacturing (3.0)

Coke & refined petroleum products (6.3)

Leather & leather products (0.2)

Television, radio & communication equipment (0.9)

PGM mining (24.6)

Gold & uranium mining (17.7)

Coal mining (23.7)

Iron ore mining (14.4)

Other mining (19.6)

Percent

Agriculture, forestry & fishing *

Total mining

Agriculture, forestry & fishing *

Total mining

Total manufacturing

Manufacturing: Change in the utilisation of production capacity

Total manufacturing (81.6)

Second quarter of 2014 compared to second quarter of 2013

Figures in brackets refer to the sub-sector's average capacity

ut ilisat ion in the second quarter of 2014

-10 -8 -6 -4 -2 0 2 4 6 8

Footwear (84.5)

Other transport equipment (72.4)

Motor vehicles, parts & accessories (80.2)

Glass & glass products (80.2)

Rubber products (82.3)

Wearing apparel (77.6)

Basic iron & steel products (77.8)

Food (80.0)

Machinery & equipment (81.0)

Electrical machinery & equipment (80.5)

Other manufacturing (75.0)

Plastic products (83.2)

Wood & wood products (82.7)

Professional & scientific equipment (84.4)

Basic chemicals (86.1)

Printing, publishing & recorded media (76.8)

Textiles (69.1)

Metal products (excl machinery) (74.4)

Basic non-ferrous metal products (80.8)

Beverages (82.6)

Paper & paper products (86.4)

Leather & leather products (69.9)

Other chemicals & man-made fibres (83.0)

Non-metallic mineral products (81.3)

Furniture (89.9)

Coke & refined petroleum products (81.1)

Television, radio & communication equipment (83.8)

Percentage points

September 2014 IDC – Research and Information – Sectoral Trends 7

Performance of the primary and secondary sectors

Figure 3 Figure 4

* including formal and informal employment

Growth in formal employment in the primary and secondary sectors

Second quarter of 2014 compared to second quarter of 2013

Figures in brackets refer to the sub-sector's share in

mining/manufacturing employment in the second quarter of 2014

-15% -10% -5% 0% 5% 10%

Furniture (1.9)

Wearing apparel (3.0)

Printing, publishing & recorded media (3.1)

Rubber products (0.8)

Non-metallic mineral products (3.0)

Beverages (2.5)

Leather & leather products (0.3)

Other chemicals & man-made fibres (3.2)

Plastic products (2.3)

Textiles (7.9)

Basic iron & steel products (3.0)

Motor vehicles, parts & accessories (5.5)

Coke & refined petroleum products (11.1)

Basic non-ferrous metal products (1.2)

Glass & glass products (0.6)

Other manufacturing (2.7)

Professional & scientific equipment (0.6)

Metal products (excl machinery) (6.9)

Electrical machinery & equipment (5.0)

Basic chemicals (1.1)

Food (11.3)

Machinery & equipment (7.8)

Footwear (0.7)

Wood & wood products (9.8)

Television, radio & communication equipment (1.6)

Other transport equipment (1.0)

Paper & paper products (2.1)

Gold & uranium mining (24.4)

PGM mining (38.2)

Coal mining (17.4)

Other mining (15.8)

Iron ore mining (4.2)

Percent

Agriculture, forestry & fishing*

Total mining

Total manufacturing

Growth in gross monthly remuneration per worker in the primary and secondary sectors

Second quarter of 2014 compared to second quarter of 2013

-25% -20% -15% -10% -5% 0% 5% 10% 15% 20%

Basic non-ferrous metal products

Other manufacturing

Basic chemicals

Professional & scientific equipment

Television, radio & communication equipment

Footwear

Printing, publishing & recorded media

Wood & wood products

Beverages

Food

Coke & refined petroleum products

Electrical machinery & equipment

Other transport equipment

Leather & leather products

Metal products (excl machinery)

Rubber products

Paper & paper products

Glass & glass products

Other chemicals & man-made fibres

Machinery & equipment

Textiles

Non-metallic mineral products

Motor vehicles, parts & accessories

Plastic products

Furniture

Wearing apparel

Basic iron & steel products

PGM mining

Other mining

Gold & uranium mining

Iron ore mining

Coal mining

Percent

Total manufacturing

Total mining

September 2014 IDC – Research and Information – Sectoral Trends 8

Performance of the primary and secondary sectors

Figure 5 Figure 6

First half of 2014 (cumulative total) compared to First half of 2013 (cumulative total)

Growth in the value of imports (excl. imports from BLNS) in the primary and secondary sectors

Figures in brackets refer to the sub-sector's percentage

share in mining/manufacturing imports in Q2 of 2014

-30% -20% -10% 0% 10% 20% 30% 40%

Basic iron & steel products (2.1)

Printing, publishing & recorded media (0.3)

Rubber products (1.3)

Coke & refined petroleum products (7.8)

Machinery & equipment (17.8)

Furniture (0.6)

Food (5.0)

Motor vehicles, parts & accessories (19.0)

Television, radio & communication equipment (6.3)

Beverages (0.6)

Other chemicals & man-made fibres (7.7)

Footwear (1.1)

Metal products (excl machinery) (2.4)

Basic non-ferrous metal products (2.0)

Wearing apparel (2.2)

Plastic products (1.5)

Leather & leather products (0.4)

Wood & wood products (0.5)

Glass & glass products (0.3)

Basic chemicals (5.3)

Professional & scientific equipment (3.3)

Other manufacturing (1.4)

Textiles (1.5)

Electrical machinery & equipment (4.7)

Paper & paper products (1.4)

Non-metallic mineral products (1.2)

Other transport equipment (2.1)

Gold & uranium mining (0.0)

Iron ore mining (0.3)

Coal mining (1.4)

Other mining (97.0)

PGM mining (1.3)

Percent

Agriculture, forestry & fishing

Total mining

Total manufacturing

-72.8%

641.4%

Growth in the value of exports (excl. exports to BLNS) in the primary and secondary sectors

First half of 2014 (cumulative total) compared to First half of 2013 (cumulative total)

Figures in brackets refer to the sub-sector's percentage

share in mining/manufacturing exports in Q2 of 2014

-40% -20% 0% 20% 40% 60% 80% 100%

Rubber products (0.6)

Other manufacturing (5.8)

Motor vehicles, parts & accessories (20.2)

Glass & glass products (0.3)

Beverages (2.5)

Coke & refined petroleum products (4.5)

Electrical machinery & equipment (1.7)

Wearing apparel (0.2)

Metal products (excl machinery) (2.6)

Printing, publishing & recorded media (0.2)

Machinery & equipment (6.7)

Basic non-ferrous metal products (5.8)

Furniture (0.7)

Basic chemicals (8.6)

Plastic products (0.9)

Other transport equipment (1.3)

Textiles (0.8)

Other chemicals & man-made fibres (4.8)

Footwear (0.1)

Paper & paper products (3.3)

Non-metallic mineral products (0.6)

Professional & scientific equipment (1.1)

Food (6.6)

Wood & wood products (0.9)

Basic iron & steel products (17.1)

Leather & leather products (0.5)

Television, radio & communication equipment (1.6)

Gold & uranium mining (16.4)

PGM mining (20.2)

Iron ore mining (24.2)

Coal mining (17.0)

Other mining (22.2)

Percent

Agriculture, forestry & fishing

Total mining

Total manufacturing

September 2014 IDC – Research and Information – Sectoral Trends 9

Selected trade trends (excluding trade with BLNS)

-300

-200

-100

0

100

200

300

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

SA trade balance

Imports Exports Trade balance

ZAR billion per quarter (current v alues)

0

25

50

75

100

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

SA exports by broad economic classification

Capital goods Consumption goods

Intermediate goods Raw materials

ZAR billion per quarter (current v alues)

0

25

50

75

100

125

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

SA imports by broad economic classification

Capital goods Consumption goods

Intermediate goods Raw materials

ZAR billion per quarter (current v alues)

HS2 code ZAR m

H71: Natural or cultured pearls, precious stones and metals 69 083.21

H26: Ores, slag and ash 66 166.37

H27: Coal, petroleum and petroleum products 39 346.39

H72: Iron and steel 39 078.05

H87: Vehicles, parts and accessories 32 720.99

Exports Total (including others) 403 391.19

H27: Coal, petroleum and petroleum products 128 112.10

H84: Machinery and equipment, mechanical appliances 69 596.10

H85: Electrical machinery and electronic equipment 48 123.04

H87: Vehicles, parts and accessories 44 573.27

H98: Original equipment components for the motor vehicle industry 32 712.23

Imports Total (including others) 511 859.90

Imp

ort

s

Major traded productsFirst half of 2014 (cumulative total)

Ex

po

rts

SA trade per regionFirst half of 2014 (cumulative total)

0% 5% 10% 15% 20% 25% 30% 35% 40%

Oceania

Europe (excl. EU)

Other Americas

NAFTA

Africa

Middle East

EU

Asia

Oceania

Other Americas

Europe (excl. EU)

Middle East

NAFTA

Africa

EU

Asia

Share of exports

Share of imports

SA trade growth by region

First half of 2014 (cumulative total) compared to first half of 2013 (cumulative total)

-30% -20% -10% 0% 10% 20% 30% 40% 50%

Oceania

Other Americas

EU

Europe (excl. EU)

NAFTA

Asia

Africa

Middle East

Europe (excl. EU)

Other Americas

Oceania

NAFTA

Asia

Africa

Middle East

EU

Export growth

Import growth

September 2014 IDC – Research and Information – Sectoral Trends 10

Trade trends with major regions or regional blocs

First half of 2014 (cumulative total)

SA trade balance with the EU Top traded product categories:

First half of 2014 (cumulative total)

First half of 2014 (cumulative total)

SA trade balance with Asia

SA trade balance with the Middle East Top traded product categories:

Top traded product categories:

SA trade balance with Africa (excl. trade with BLNS) Top traded product categories:

First half of 2014 (cumulative total)

-40

-30

-20

-10

0

10

20

30

40

50

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Imports Exports Trade balance

ZAR billion per quarter (current v alues)

0% 20% 40% 60% 80% 100%

Other goods

Wearing apparel; excl. fur apparel

Basic precious & non-ferrous metals

Petroleum refineries & synthesisers

Agriculture (cereals & other crops)

Crude oil mining

Other goods

Mining & construction machinery

Agriculture (cereals & other crops)

Petroleum refineries & synthesisers

Basic iron & steel

Motor vehicles

Share ofexports

Share ofimports

-120

-100

-80

-60

-40

-20

0

20

40

60

80

100

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Imports Exports Trade balance

ZAR billion per quarter (current v alues)

0% 15% 30% 45% 60% 75%

Other goods

Office, accounting & computing…

Motor vehicles

TV & radio transmitters, line telephony

Motor vehicle parts & accessories

Petroleum refineries & synthesisers

Other goods

Platinum group metal mining

Basic iron & steel

Mining of non-ferrous metal ores

Coal mining

Iron ore mining

Share ofexports

Share ofimports

-90

-75

-60

-45

-30

-15

0

15

30

45

60

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Imports Exports Trade balance

ZAR billion per quarter (current v alues)

0% 15% 30% 45% 60% 75%

Other goods

Petroleum refineries & synthesisers

Other chemical products, nec.

Medicinal chemicals

Motor vehicles

Motor vehicle parts & accessories

Other goods

Agriculture (cereals & other crops)

Motor vehicles

Motor vehicle parts & accessories

Platinum group metal mining

Basic iron & steel

Share ofexports

Share ofimports

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Imports Exports Trade balance

ZAR billion per quarter (current v alues)

0% 15% 30% 45% 60% 75%

Other goods

Plastics in primary form

Fertilisers & nitrogen compounds

Basic chemicals

Petroleum refineries & synthesisers

Crude oil mining

Other goods

Basic precious & non-ferrous metals

Basic iron & steel

Agriculture (cereals & other crops)

Coal mining

Diamond mining

Share ofexports

Share ofimports

September 2014 IDC – Research and Information – Sectoral Trends 11

Trade trends with major regions or regional blocs

SA trade balance with Oceania Top traded product categories:

First half of 2014 (cumulative total)

First half of 2014 (cumulative total)

First half of 2014 (cumulative total)

First half of 2014 (cumulative total)

SA trade balance with Nafta Top traded product categories:

SA trade balance with the Americas (excluding Nafta) Top traded product categories:

SA trade balance with Europe (excluding the EU) Top traded product categories:

-6

-4

-2

0

2

4

6

8

10

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Imports Exports Trade balance

ZAR billion per quarter (current v alues)

0% 15% 30% 45% 60%

Other goods

Medical & surgical equipment, etc.

Basic precious & non-ferrous metals

Watches & clocks

Medicinal chemicals

Agriculture (cereals & other crops)

Other goods

Motor vehicles

Agriculture (cereals & other crops)

Mining of non-ferrous metal ores

Basic precious & non-ferrous metals

Platinum group metal mining

Shareofexports

Shareofimports

-25

-20

-15

-10

-5

0

5

10

15

20

25

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Imports Exports Trade balance

ZAR billion per quarter (current v alues)

0% 15% 30% 45% 60% 75%

Other goods

Other chemical products, nec.

Mining & construction machinery

Motor vehicle parts & accessories

Aircraft & spacecraft

Motor vehicles

Other goods

Mining of non-ferrous metal ores

Basic chemicals

Platinum group metal mining

Basic iron & steel

Motor vehicles

Share ofexports

Share ofimports

-8

-6

-4

-2

0

2

4

6

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Imports Exports Trade balance

ZAR billion per quarter (current v alues)

0% 15% 30% 45% 60%

Other goods

Sugar refining

Agriculture (cereals & other crops)

Slaughtering, processing of meat

Vegetable & animal oils & fats

Motor vehicle parts & accessories

Other goods

Plastics in primary form

Basic chemicals

Motor vehicle parts & accessories

Coal mining

Basic iron & steel

Share ofexports

Share ofimports

-5

-4

-3

-2

-1

0

1

2

3

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Imports Exports Trade balance

ZAR billion per quarter (current v alues)

0% 15% 30% 45% 60%

Other goods

Mining & construction machinery

Pulp, paper & paperboard

Agriculture (cereals & other crops)

Coal mining

Basic precious & non-ferrous metals

Other goods

Mining & construction machinery

Basic iron & steel

Mining of non-ferrous metal ores

Basic chemicals

Motor vehicles

Share ofexports

Share ofimports

September 2014 IDC – Research and Information – Sectoral Trends 12

Production weight: 100 Agriculture, forestry and fishing

Real v alue added index (seasonally adjusted)

ZAR billion per quarter (current v alues) HS2 code: sector description ZAR m

H08: Edible fruit, nuts, peel o f citrus fruit, melons 14 763.00

H10: Cereals 2 182.08

H51: Wool, animal hair, horsehair yarn and fabric thereof 1 398.60

H12: Oil seed, o leagic fruits, grain, seed, fruit, etc 675.08

H07: Edible vegetables and certain roots and tubers 588.87

Expo rts T o tal ( including o thers) 21 059.66

H10: Cereals 2 697.95

H12: Oil seed, o leagic fruits, grain, seed, fruit, etc 1 411.48

H09: Coffee, tea, mate and spices 904.46

H40: Rubber and articles thereof 637.96

H24: Tobacco and manufactured tobacco substitutes 630.38

Impo rts T o tal ( including o thers) 8 042.49

HS2 code: sector description Change in ZAR m

H08: Edible fruit, nuts, peel o f citrus fruit, melons 2 008.61

H12: Oil seed, o leagic fruits, grain, seed, fruit, etc 212.83

H07: Edible vegetables and certain roots and tubers 128.36

H03: Fish, crustaceans, molluscs, aquatic invertebrates nes 85.54

H09: Coffee, tea, mate and spices 57.89

H10: Cereals -1 203.24

H51: Wool, animal hair, horsehair yarn and fabric thereof - 46.16

H24: Tobacco and manufactured tobacco substitutes - 4.62

H52: Cotton, yarn and woven fabric - 3.12

H40: Rubber and articles thereof - 0.65

First half of 2014 (cumulative total)

Export performance

Nominal value of first half of 2014 compared to first half of 2013

Quarterly

Real value added trend

Trade trends

Total per quarter

Top trading partners

First half of 2014 (cumulative total)

Employment trend

Quarterly

Number (1 000)

Major traded products

Exp

ort

s

To

p g

ain

ers

Imp

ort

s

To

p l

ose

rs

110

115

120

125

130

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Real value added

0

3

6

9

12

15

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 5% 10% 15% 20%

Russia

USA

Brazil

Romania

Australia

Zambia

India

Netherlands

UK

UAE

China

Hong Kong

Zimbabwe

Russia

Top export destinations' share

Top import sources' share

600

640

680

720

760

800

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

3.3% -- (percentage points) -9.8% -- 7.6% 36.4%

Real value added (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 13

Production weight: 100 Total mining

Production index (seasonally adjusted)

ZAR billion per quarter (current v alues) HS2 code: sector description ZAR m

H71: Natural or cultured pearls, precious stones and metals 65 009.56

H26: Ores, slag and ash 64 253.34

H27: Coal, petro leum and petro leum products 27 085.63

H25: Salt, sulphur, earth, stone, plaster, lime and cement 1 817.08

Expo rts T o tal ( including o thers) 158 165.61

H27: Coal, petro leum and petro leum products 95 407.43

H71: Natural or cultured pearls, precious stones and metals 3 507.31

H25: Salt, sulphur, earth, stone, plaster, lime and cement 938.24

H26: Ores, slag and ash 878.21

Impo rts T o tal ( including o thers) 100 731.19

HS2 code: sector description Change in ZAR m

H26: Ores, slag and ash 9 357.95

H27: Coal, petro leum and petro leum products 3 240.50

H25: Salt, sulphur, earth, stone, plaster, lime and cement 670.82

H71: Natural or cultured pearls, precious stones and metals -11 845.14

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)

87

89

91

93

95

97

99

101

103

105

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Volume of production

15

25

35

45

55

65

75

85

95

105

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 10% 20% 30% 40% 50%

Saudi Arabia

Nigeria

Angola

Ghana

UAE

Mozambique

Gabon

China

Japan

India

Netherlands

USA

UK

Switzerland

Top export destinations' share

Top import sources' share

8

10

12

14

16

18

20

480

490

500

510

520

530

540

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Employment Remunera tion per worker

-2.6% -- (percentage points) -4.9% -0.5% -1.3% 36.7%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 14

Production weight: 23.7 Coal mining

Production index (seasonally adjusted)

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H2701: Coal, briquettes, ovoids etc, made from coal 26 932.13

H2703: Peat (including peat litter) 0.61

H2702: Lignite, except jet 0.06

0.00

Expo rts T o tal ( including o thers) 26 932.80

H2701: Coal, briquettes, ovoids etc, made from coal 1 380.60

H2703: Peat (including peat litter) 22.71

Impo rts T o tal ( including o thers) 1 403.32

HS4 code: sector description Change in ZAR m

H2701: Coal, briquettes, ovoids etc, made from coal 1 268.61

H2703: Peat (including peat litter) 0.21

H2702: Lignite, except jet 0.04

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)

90

93

96

99

102

105

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Volume of production

0

4

8

12

16

20

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 10% 20% 30% 40% 50%

Australia

Mozambique

USA

Russia

New Zealand

Vietnam

Netherlands

India

Netherlands

China

Pakistan

Taiwan

UAE

Israel

Top export destinations' share

Top import sources' share

15

16

17

18

19

20

70

75

80

85

90

95

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Employment Remunera tion per worker

-0.8% -- (percentage points) -0.4% 14.5% 4.9% 24.2%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 15

Production weight: 17.7 Gold and uranium mining

Production index (seasonally adjusted)

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H7108: Gold, unwrought, semi-manufactured, etc 25 867.38

Expo rts T o tal ( including o thers) 25 867.38

H7108: Gold, unwrought, semi-manufactured, etc 1.25

Impo rts T o tal ( including o thers) 1.25

HS4 code: sector description Change in ZAR m

H7108: Gold, unwrought, semi-manufactured, etc -6 387.50

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)

50

60

70

80

90

100

110

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Volume of production

0

5

10

15

20

25

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 5% 10% 15% 20% 25% 30% 35%

Vietnam

Germany

USA

South Korea

Greece

UK

Italy

Top export destinations' share

Top import sources' share

7

9

11

13

15

17

19

110

120

130

140

150

160

170

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Employment Remunera tion per worker

Gold export destinations are classified as unallocated

-3.1% -- (percentage points) -13.4% 11.1% -19.8% -72.8%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 16

Production weight: 24.6 PGM mining

Production index (seasonally adjusted)

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H7110: P latinum, unwrought, semi-manufactured 31 897.91

H7111: M etals, clad with platinum, semi-manufactured 21.47

Expo rts T o tal ( including o thers) 31 919.38

H7110: P latinum, unwrought, semi-manufactured 1 284.01

H7111: M etals, clad with platinum, semi-manufactured 0.08

Impo rts T o tal ( including o thers) 1 284.09

HS4 code: sector description Change in ZAR m

H7111: M etals, clad with platinum, semi-manufactured 5.10

H7110: P latinum, unwrought, semi-manufactured -3 721.06

Imp

ort

s

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

s

50

60

70

80

90

100

110

120

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Volume of production

0

5

10

15

20

25

30

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 5% 10% 15% 20% 25% 30%

UK

Germany

Switzerland

USA

Gabon

South Korea

Taiwan

Japan

UK

USA

Switzerland

Hong Kong

Germany

China

Top export destinations' share

Top import sources' share

59.3%

11

13

15

17

19

175

185

195

205

215

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Employment Remunera tion per worker

-27.8% -- (percentage points) -4.3% -20.5% -10.4% 641.4%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 17

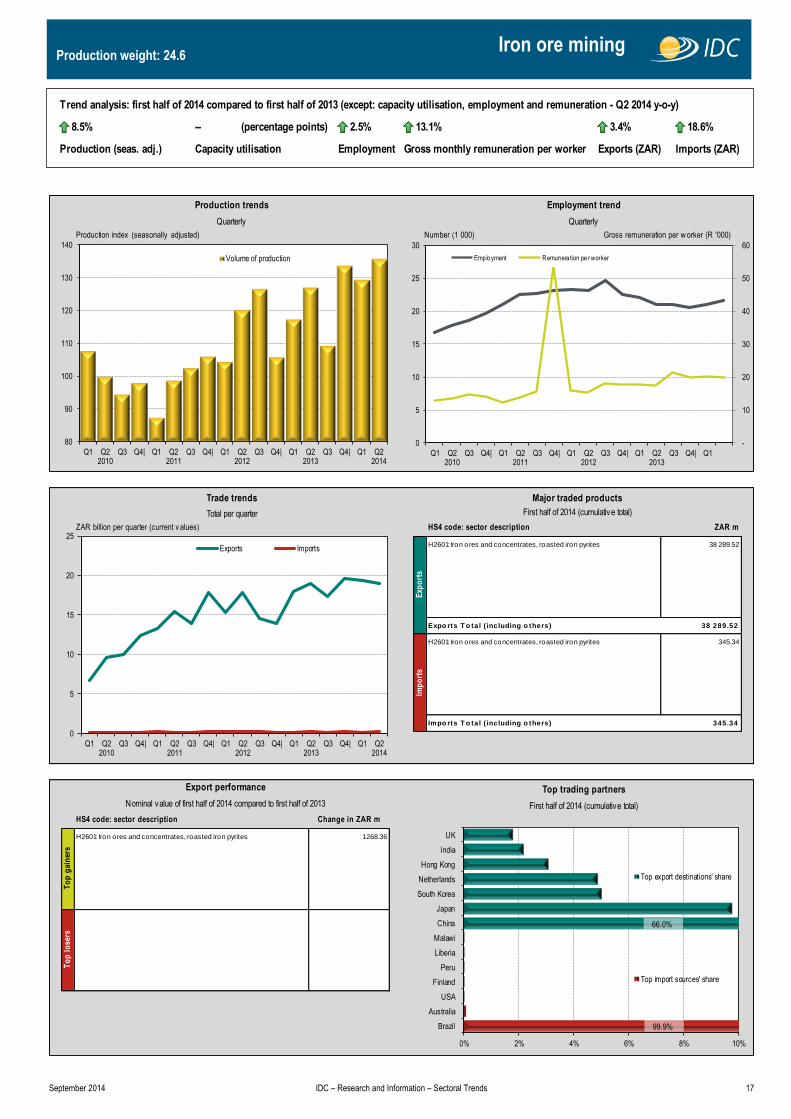

Production weight: 24.6 Iron ore mining

Production index (seasonally adjusted)

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H2601: Iron ores and concentrates, roasted iron pyrites 38 289.52

Expo rts T o tal ( including o thers) 38 289.52

H2601: Iron ores and concentrates, roasted iron pyrites 345.34

Impo rts T o tal ( including o thers) 345.34

HS4 code: sector description Change in ZAR m

H2601: Iron ores and concentrates, roasted iron pyrites 1 268.36

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)

80

90

100

110

120

130

140

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Volume of production

0

5

10

15

20

25

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 2% 4% 6% 8% 10%

Brazil

Australia

USA

Finland

Peru

Liberia

Malawi

China

Japan

South Korea

Netherlands

Hong Kong

India

UK

Top export destinations' share

Top import sources' share

99.9%

66.0%

-

10

20

30

40

50

60

0

5

10

15

20

25

30

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Employment Remunera tion per worker

8.5% -- (percentage points) 2.5% 13.1% 3.4% 18.6%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 18

Production weight: 19.6 Other mining

Production index (seasonally adjusted)

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H2602: M anganese ores, iron ores >20% M anganese 9 684.60

H7102: Diamonds, not mounted or set 7 200.15

H2610: Chromium ores and concentrates 5 755.60

H2614: Titanium ores and concentrates 2 891.49

H2603: Copper ores and concentrates 2 715.99

Expo rts T o tal ( including o thers) 35 156.53

H2709: Petro leum oils, o ils from bituminous minerals, crude 92 302.03

H7102: Diamonds, not mounted or set 2 211.04

H2711: Petro leum gases & other gaseous hydrocarbons 1 701.34

H2503: Sulphur, except sublimated, precipitated, co llo idal 518.51

H2519: Natural magnesium carbonate, magnesium oxide 154.04

Impo rts T o tal ( including o thers) 97 697.19

HS4 code: sector description Change in ZAR m

H2602: M anganese ores, iron ores >20% M anganese 2 744.95

H7102: Diamonds, not mounted or set 1 445.42

H2603: Copper ores and concentrates 1 015.18

H2617: Ores and concentrates, nes 894.79

H2616: Precious metal ores and concentrates 548.48

H2610: Chromium ores and concentrates - 696.00

H2615: Niobium tantalum vanadium zirconium ores, etc - 540.39

H2607: Lead ores and concentrates - 352.13

H7106: Silver, unwrought or semi-manufactured, etc - 41.35

H2608: Zinc ores and concentrates - 32.75

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)

80

85

90

95

100

105

110

115

120

125

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Volume of production

0

10

20

30

40

50

60

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 10% 20% 30% 40% 50%

Saudi Arabia

Nigeria

Angola

Ghana

UAE

Mozambique

Gabon

China

Belgium

USA

India

Finland

UAE

Israel

Top export destinations' share

Top import sources' share

9

11

13

15

17

19

60

65

70

75

80

85

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Employment Remunera tion per worker

14.1% -- (percentage points) 1.4% 5.2% 18.8% 35.6%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 19

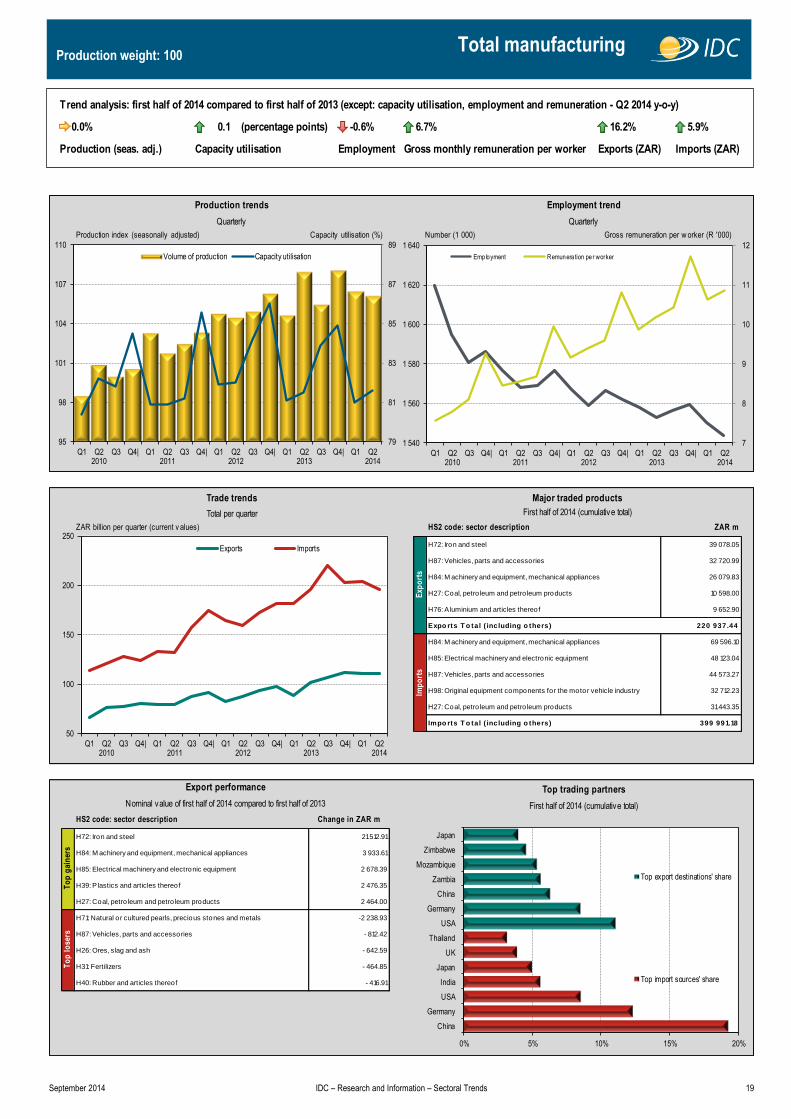

Production weight: 100 Total manufacturing

ZAR billion per quarter (current v alues) HS2 code: sector description ZAR m

H72: Iron and steel 39 078.05

H87: Vehicles, parts and accessories 32 720.99

H84: M achinery and equipment, mechanical appliances 26 079.83

H27: Coal, petro leum and petro leum products 10 598.00

H76: A luminium and articles thereof 9 652.90

Expo rts T o tal ( including o thers) 220 937.44

H84: M achinery and equipment, mechanical appliances 69 596.10

H85: Electrical machinery and electronic equipment 48 123.04

H87: Vehicles, parts and accessories 44 573.27

H98: Original equipment components for the motor vehicle industry 32 712.23

H27: Coal, petro leum and petro leum products 31 443.35

Impo rts T o tal ( including o thers) 399 991.18

HS2 code: sector description Change in ZAR m

H72: Iron and steel 21 512.91

H84: M achinery and equipment, mechanical appliances 3 933.61

H85: Electrical machinery and electronic equipment 2 678.39

H39: P lastics and articles thereof 2 476.35

H27: Coal, petro leum and petro leum products 2 464.00

H71: Natural or cultured pearls, precious stones and metals -2 238.93

H87: Vehicles, parts and accessories - 812.42

H26: Ores, slag and ash - 642.59

H31: Fertilizers - 464.85

H40: Rubber and articles thereof - 416.91

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)Production index (seasonally adjusted) Capacity utilisation (%)

79

81

83

85

87

89

95

98

101

104

107

110

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Volume of production Capacity utilisation

50

100

150

200

250

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 5% 10% 15% 20%

China

Germany

USA

India

Japan

UK

Thailand

USA

Germany

China

Zambia

Mozambique

Zimbabwe

Japan

Top export destinations' share

Top import sources' share

7

8

9

10

11

12

1 540

1 560

1 580

1 600

1 620

1 640

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Employment Remunera tion per worker

0.0% 0.1 (percentage points) -0.6% 6.7% 16.2% 5.9%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 20

Production weight: 17.4 Food

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H1701: Solid cane/ beet sugar & chemically pure sucrose 1 580.90

H2009: Fruit and vegetable juices, not fermented/ spirited 1 207.64

H2008: Fruit, edible plant parts nes, prepared/preserved 1 057.24

H2106: Food preparations, nes 858.80

H0303: Fish, frozen, whole 790.65

Expo rts T o tal ( including o thers) 14 663.10

H0207: M eat, edible offal o f domestic poultry 1 993.64

H1006: Rice 1 814.49

H1511: Palm o il and its fractions, not chemically modified 1 677.66

H2304: Soya-bean o il-cake and other so lid residues 1 612.47

H2106: Food preparations, nes 987.59

Impo rts T o tal ( including o thers) 19 910.37

HS4 code: sector description Change in ZAR m

H1701: Solid cane/ beet sugar & chemically pure sucrose 686.05

H2301: Flour etc of meat, fish or o ffal for animal feed 303.20

H2009: Fruit and vegetable juices, not fermented/ spirited 300.64

H0303: Fish, frozen, whole 238.49

H2106: Food preparations, nes 231.92

H1512: Safflower, sunflower & cotton-seed o il, fractions - 36.95

H1104: Worked cereal grains except flour, groat, meal,etc - 24.70

H1702: Sugars nes, lactose, fructose, glucose etc - 15.70

H1101: Wheat or meslin flour - 12.69

H3505: Dextrins, o ther modified starches, starch glues - 10.08

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)Production index (seasonally adjusted) Capacity utilisation (%)

74

76

78

80

82

84

86

88

85

90

95

100

105

110

115

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Volume of production Capacity utilisation

2

5

8

11

14

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 3% 6% 9% 12% 15%

Argentina

Thailand

Netherlands

Indonesia

Brazil

China

Germany

Zimbabwe

Mozambique

Angola

Zambia

Italy

China

Japan

Top export destinations' share

Top import sources' share

5

7

9

11

13

165

170

175

180

185

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Employment Remunera tion per worker

2.3% -2.7 (percentage points) 0.9% 4.9% 33.7% 3.9%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 21

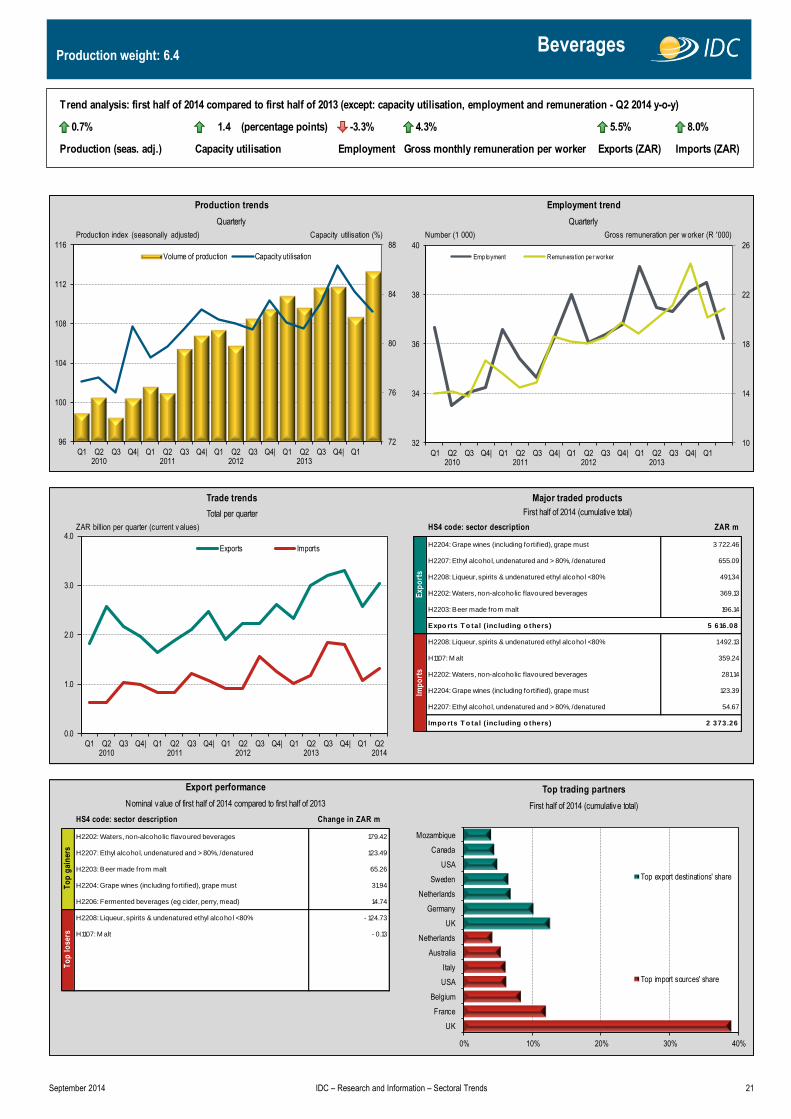

Production weight: 6.4 Beverages

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H2204: Grape wines (including fortified), grape must 3 722.46

H2207: Ethyl alcohol, undenatured and > 80%, /denatured 655.09

H2208: Liqueur, spirits & undenatured ethyl alcohol <80% 491.34

H2202: Waters, non-alcoholic flavoured beverages 369.13

H2203: Beer made from malt 196.14

Expo rts T o tal ( including o thers) 5 616.08

H2208: Liqueur, spirits & undenatured ethyl alcohol <80% 1 492.13

H1107: M alt 359.24

H2202: Waters, non-alcoholic flavoured beverages 281.14

H2204: Grape wines (including fortified), grape must 123.39

H2207: Ethyl alcohol, undenatured and > 80%, /denatured 54.67

Impo rts T o tal ( including o thers) 2 373.26

HS4 code: sector description Change in ZAR m

H2202: Waters, non-alcoholic flavoured beverages 179.42

H2207: Ethyl alcohol, undenatured and > 80%, /denatured 123.49

H2203: Beer made from malt 65.26

H2204: Grape wines (including fortified), grape must 31.94

H2206: Fermented beverages (eg cider, perry, mead) 14.74

H2208: Liqueur, spirits & undenatured ethyl alcohol <80% - 124.73

H1107: M alt - 0.13

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)Production index (seasonally adjusted) Capacity utilisation (%)

72

76

80

84

88

96

100

104

108

112

116

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Volume of production Capacity utilisation

0.0

1.0

2.0

3.0

4.0

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 10% 20% 30% 40%

UK

France

Belgium

USA

Italy

Australia

Netherlands

UK

Germany

Netherlands

Sweden

USA

Canada

Mozambique

Top export destinations' share

Top import sources' share

10

14

18

22

26

32

34

36

38

40

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Employment Remunera tion per worker

0.7% 1.4 (percentage points) -3.3% 4.3% 5.5% 8.0%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 22

Production weight: 1.2 Textiles

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H5105: Wool and animal hair, carded or combed 467.70

H5603: Nonwoven textiles, except felt 151.15

H9619: Sanitary towels and tampons, napkins and napkin liners for babies 146.83

H6306: Textile tarpaulin, sail, awning, tent, camping goods 133.92

H5101: Wool, not carded or combed 79.00

Expo rts T o tal ( including o thers) 1 815.71

H5407: Woven synth filament yarn, monofilament >67dtex 690.78

H9619: Sanitary towels and tampons, napkins and napkin liners for babies 655.87

H5603: Nonwoven textiles, except felt 491.09

H5513: Woven fabric>85% synt+cotn<170g/m2 unb/blchd 335.07

H6302: Bed, table, to ilet and kitchen linens 322.40

Impo rts T o tal ( including o thers) 6 198.05

HS4 code: sector description Change in ZAR m

H5105: Wool and animal hair, carded or combed 103.23

H9619: Sanitary towels and tampons, napkins and napkin liners for babies 71.34

H5603: Nonwoven textiles, except felt 36.74

H6305: Sacks& bags of a kind used for packing of goods 32.42

H5101: Wool, not carded or combed 21.17

H6306: Textile tarpaulin, sail, awning, tent, camping goods - 19.52

H5704: Carpets, floor coverings of felt, not tufted, flocked - 11.13

H5903: Fabric impregnated, coated/ covered with plastic - 6.33

H5407: Woven synth filament yarn, monofilament >67dtex - 5.87

H7019: Glass fibres, glass wool, and articles thereof - 4.87

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)Production index (seasonally adjusted) Capacity utilisation (%)

68

69

70

71

72

73

74

75

80

84

88

92

96

100

104

108

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Volume of production Capacity utilisation

0

1

2

3

4

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 10% 20% 30% 40%

China

Pakistan

India

Germany

Poland

Turkey

Hungary

Italy

Germany

Zambia

Zimbabwe

China

UK

Mozambique

Top export destinations' share

Top import sources' share

3

4

5

6

7

8

9

120

125

130

135

140

145

150

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Employment Remunera tion per worker

-3.0% -0.4 (percentage points) -2.4% 9.6% 22.1% 15.4%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 23

Production weight: 1.1 Wearing apparel

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H6203: M ens or boys suits, jackets, trousers, etc not knit 80.90

H6115: Panty hose, tights, hosiery nes, knit or crochet 41.46

H6103: M ens, boys suits,jackets,trousers, etc knit/crochet 37.85

H6211: Track suits, ski suits & swimwear, o ther garments 35.64

H6006: Other knitted or crocheted fabrics 35.17

Expo rts T o tal ( including o thers) 532.20

H6110: Jerseys, pullovers, cardigans, etc, knit or crochet 973.54

H6203: M ens or boys suits, jackets, trousers, etc not knit 910.92

H6109: T-shirts, singlets and other vests, knit or crochet 842.93

H6204: Woven female suits, jacket, dress, etc 742.43

H6104: Female suit, dress, skirt, etc, knit or crochet 413.63

Impo rts T o tal ( including o thers) 8 997.48

HS4 code: sector description Change in ZAR m

H6006: Other knitted or crocheted fabrics 15.29

H6103: M ens, boys suits,jackets,trousers, etc knit/crochet 9.82

H6211: Track suits, ski suits & swimwear, o ther garments 9.39

H6114: Garments, knit or crochet, nes 9.26

H6104: Female suit, dress, skirt, etc, knit or crochet 8.54

H6117: Clothing accessories or parts nes, knit or crochet - 14.04

H6206: Womens or girls' blouses, shirts and shirt-blouses - 4.40

H6201: Woven male overcoats, windjackets, etc - 3.25

H6205: M en's or boys' shirts - 2.60

H6110: Jerseys, pullovers, cardigans, etc, knit or crochet - 2.45

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)Production index (seasonally adjusted) Capacity utilisation (%)

73

76

79

82

85

88

85

90

95

100

105

110

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Volume of production Capacity utilisation

0

1

2

3

4

5

6

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 15% 30% 45% 60% 75%

China

Mauritius

Madagascar

India

Bangladesh

Vietnam

Indonesia

Mozambique

Zambia

USA

UK

Zimbabwe

DRC

Angola

Top export destinations' share

Top import sources' share

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

45

47

49

51

53

55

57

59

61

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Employment Remunera tion per worker

-3.8% -3.9 (percentage points) -3.9% 12.8% 9.9% 12.6%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 24

Production weight: 0.2 Leather & leather products

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H4104: Bovine/equine leather, no hair, not chamois, patent 618.92

H4107: Leather o f o ther animals, no hair, not chamois, etc 166.49

H4205: Articles of leather and composition leather, nes 121.70

H4106: Goat or kid skin leather, without hair 61.57

H4202: Trunks, suit-cases, camera cases, handbags, etc 46.02

Expo rts T o tal ( including o thers) 1 075.60

H4202: Trunks, suit-cases, camera cases, handbags, etc 955.84

H4107: Leather o f o ther animals, no hair, not chamois, etc 233.15

H4104: Bovine/equine leather, no hair, not chamois, patent 213.52

H4201: Saddlery and harness, o f any material 22.30

H4113: Composition leather, in slabs, sheets or strips 21.71

Impo rts T o tal ( including o thers) 1 500.74

HS4 code: sector description Change in ZAR m

H4104: Bovine/equine leather, no hair, not chamois, patent 206.42

H4107: Leather o f o ther animals, no hair, not chamois, etc 116.28

H4205: Articles of leather and composition leather, nes 57.85

H4202: Trunks, suit-cases, camera cases, handbags, etc 14.81

H4113: Composition leather, in slabs, sheets or strips 12.56

H4115: Composition leather, in slabs, sheets or strips - 1.74

H4114: Composition leather, in slabs, sheets or strips - 1.26

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)Production index (seasonally adjusted) Capacity utilisation (%)

60

64

68

72

76

80

80

90

100

110

120

130

140

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Volume of production Capacity utilisation

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 10% 20% 30% 40% 50% 60%

China

India

Brazil

Uruguay

Pakistan

Italy

Vietnam

Italy

China

Vietnam

Poland

Hong Kong

Hungary

Bulgaria

Top export destinations' share

Top import sources' share

5

6

7

8

9

3

4

5

6

7

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Employment Remunera tion per worker

14.1% 2.0 (percentage points) -3.2% 6.4% 64.6% 13.1%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 25

Production weight: 0.4 Footwear

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H6403: Footwear with uppers of leather 70.49

H6401: Waterproof footwear, rubber, plastic 41.87

H6402: Footwear, with outer so le, upper rubber or plastic 18.73

H6405: Footwear nes, so le not leather, rubber or plastic 15.81

H6404: Footwear with uppers of textile materials 13.24

Expo rts T o tal ( including o thers) 163.94

H6404: Footwear with uppers of textile materials 1 525.61

H6402: Footwear, with outer so le, upper rubber or plastic 1 482.64

H6403: Footwear with uppers of leather 1 141.40

H6406: Parts o f footwear, in-so les, heel cushion, etc 93.50

H6405: Footwear nes, so le not leather, rubber or plastic 76.94

Impo rts T o tal ( including o thers) 4 388.15

HS4 code: sector description Change in ZAR m

H6403: Footwear with uppers of leather 18.04

H6405: Footwear nes, so le not leather, rubber or plastic 6.05

H6402: Footwear, with outer so le, upper rubber or plastic 5.97

H6401: Waterproof footwear, rubber, plastic 4.28

H6404: Footwear with uppers of textile materials 1.15

H6406: Parts o f footwear, in-so les, heel cushion, etc - 0.08

Export performance Top trading partners

Nominal value of first half of 2014 compared to first half of 2013 First half of 2014 (cumulative total)

To

p g

ain

ers

To

p l

ose

rs

Trade trends Major traded products

Total per quarter First half of 2014 (cumulative total)

Exp

ort

sIm

po

rts

Production trends Employment trend

Quarterly Quarterly

Number (1 000) Gross remuneration per w orker (R '000)Production index (seasonally adjusted) Capacity utilisation (%)

84

86

88

90

92

94

85

90

95

100

105

110

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Volume of production Capacity utilisation

0

1

2

3

4

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1 Q22014

Exports Imports

0% 15% 30% 45% 60% 75%

China

Vietnam

Indonesia

Italy

India

Brazil

Thailand

Zambia

Zimbabwe

Mozambique

DRC

USA

Angola

Malawi

Top export destinations' share

Top import sources' share

4

5

6

7

8

9

7

8

9

10

11

12

Q1 Q22010

Q3 Q4| Q1 Q22011

Q3 Q4| Q1 Q22012

Q3 Q4| Q1 Q22013

Q3 Q4| Q1

Employment Remunera tion per worker

-2.0% -8.7 (percentage points) 1.2% 3.7% 27.5% 10.3%

Production (seas. adj.) Employment Gross monthly remuneration per worker Exports (ZAR) Imports (ZAR)

Trend analysis: first half of 2014 compared to first half of 2013 (except: capacity utilisation, employment and remuneration - Q2 2014 y-o-y)

Capacity utilisation

September 2014 IDC – Research and Information – Sectoral Trends 26

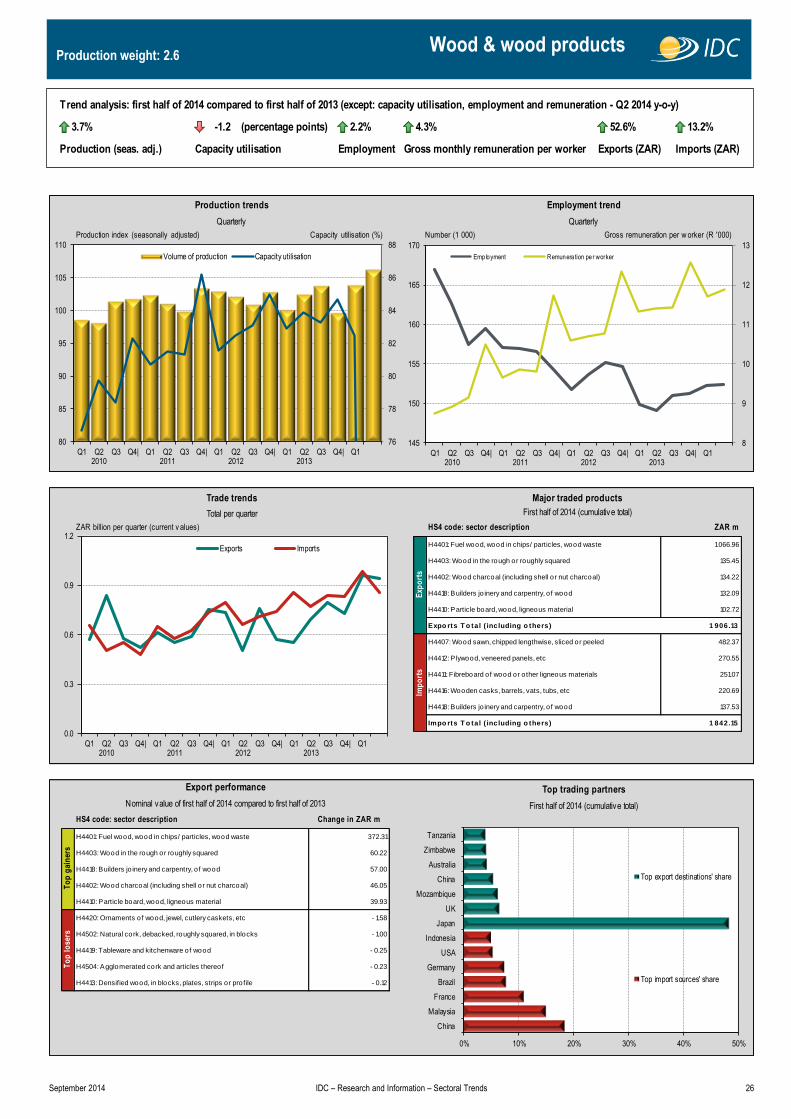

Production weight: 2.6 Wood & wood products

ZAR billion per quarter (current v alues) HS4 code: sector description ZAR m

H4401: Fuel wood, wood in chips/ particles, wood waste 1 066.96

H4403: Wood in the rough or roughly squared 135.45