Selected Topics in Robust Convex Optimization Arkadi Nemirovski School of Industrial and Systems Engineering Georgia Institute of Technology • Optimization programs with uncertain data and their Robust Counterparts • Tractability of Robust Counterparts • Robust Optimization and Chance Constraints

Transcript

Selected Topics in Robust ConvexOptimization

Arkadi Nemirovski

School of Industrial and Systems Engineering

Georgia Institute of Technology

• Optimization programs with uncertain data and theirRobust Counterparts

• Tractability of Robust Counterparts• Robust Optimization and Chance Constraints

• Optimization programs with uncertain data and theirRobust Counterparts

• Tractability of Robust Counterparts• Robust Optimization and Chance Constraints

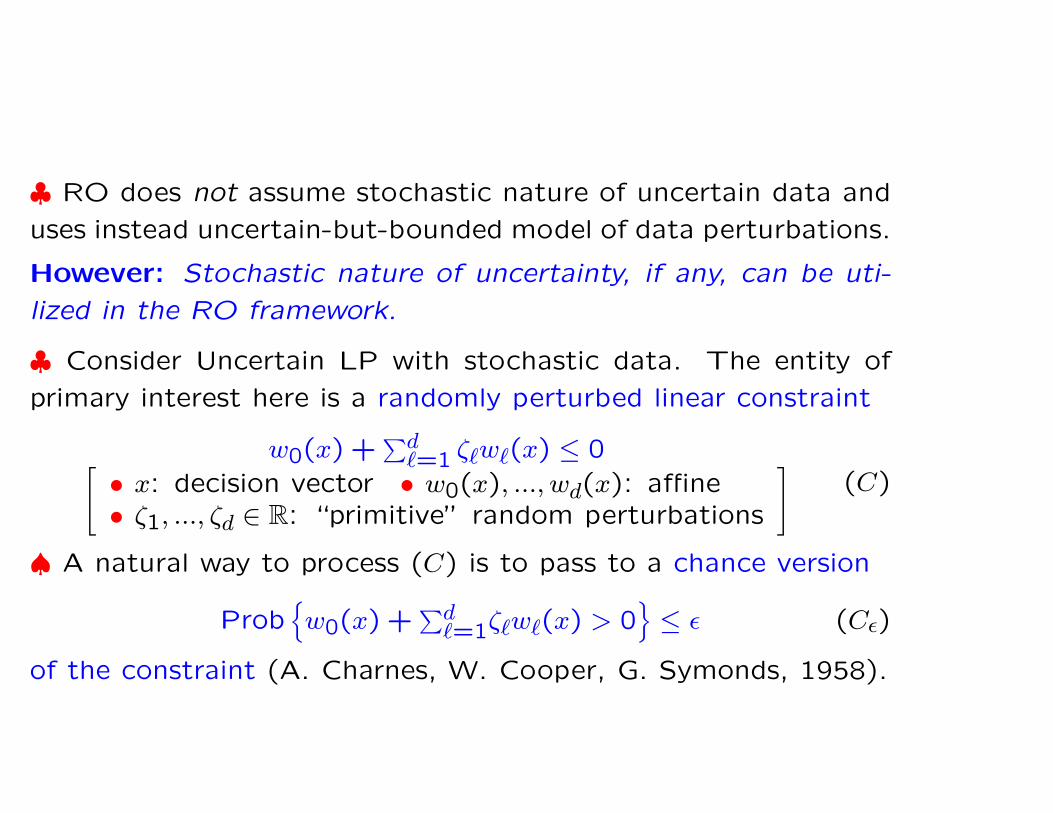

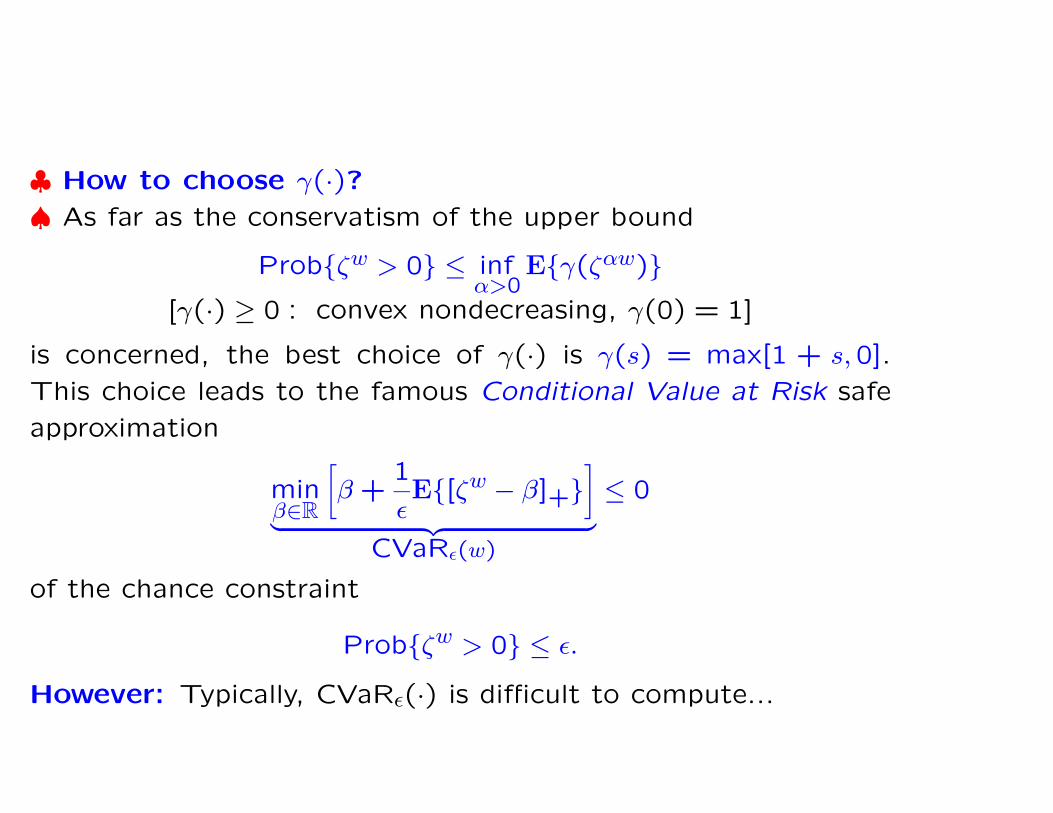

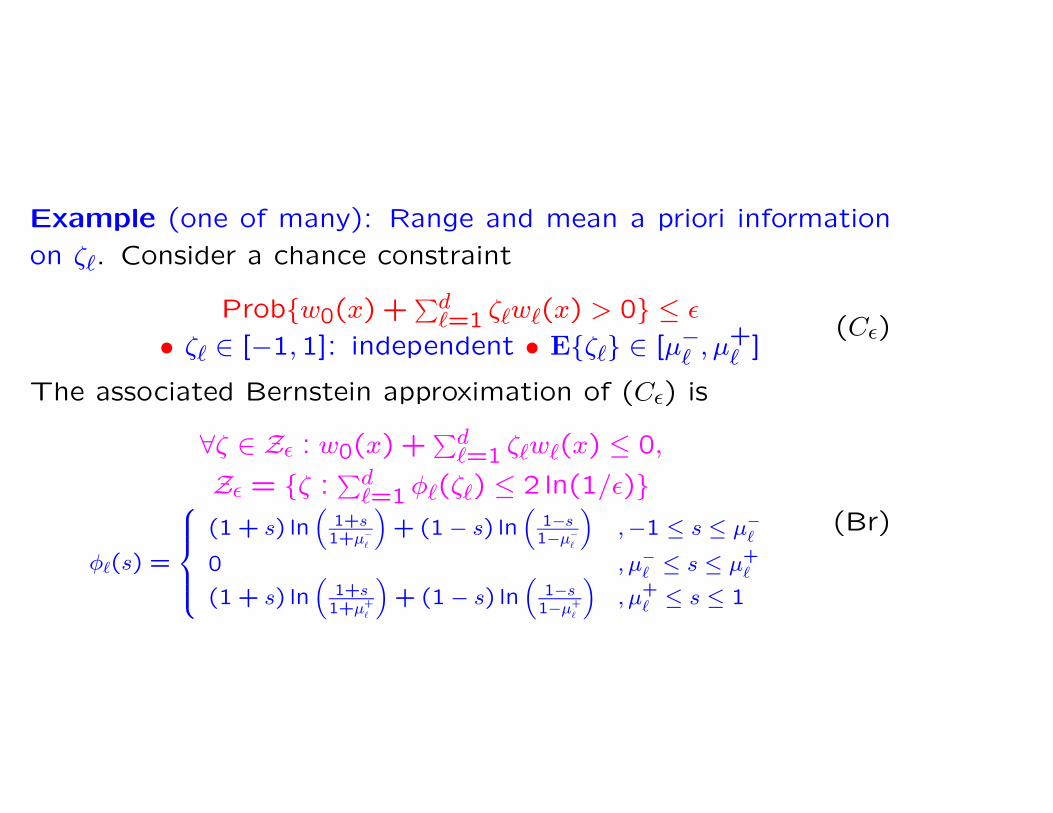

♣ Robust Optimization is a methodology for processing uncer-

tain optimization problems

minx

{f(x, ζ) : F (x, ζ) ∈ K}

• x ∈ Rn is the decision vector

• ζ ∈ Rd is the data (or data perturbation)

• f(x, ζ) : Rn × Rd → R and F (x, ζ) : Rn × Rd → Rm are given

functions, and K ⊂ Rm is a given set.

f(·, ·), F (·, ·),K form the structure of the uncertain problem.

♣ In contrast to Stochastic Programming, RO does not as-

sume stochastic nature of data ζ and uses instead uncertain-

but-bounded uncertainty model: ζ runs through a given (typi-

cally, compact) uncertainty set Z ⊂ Rd.

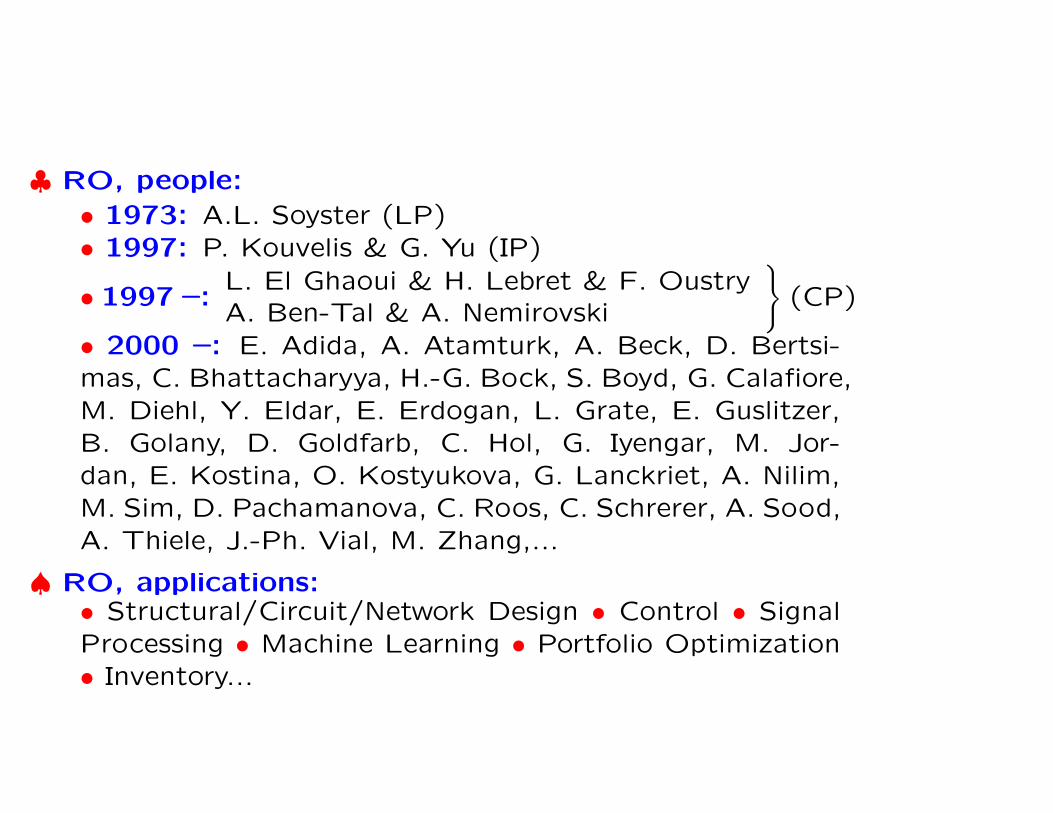

♣ RO, people:

• 1973: A.L. Soyster (LP)

• 1997: P. Kouvelis & G. Yu (IP)

• 1997 –:L. El Ghaoui & H. Lebret & F. OustryA. Ben-Tal & A. Nemirovski

}

(CP)

• 2000 –: E. Adida, A. Atamturk, A. Beck, D. Bertsi-

mas, C. Bhattacharyya, H.-G. Bock, S. Boyd, G. Calafiore,

M. Diehl, Y. Eldar, E. Erdogan, L. Grate, E. Guslitzer,

B. Golany, D. Goldfarb, C. Hol, G. Iyengar, M. Jor-

dan, E. Kostina, O. Kostyukova, G. Lanckriet, A. Nilim,

M. Sim, D. Pachamanova, C. Roos, C. Schrerer, A. Sood,

A. Thiele, J.-Ph. Vial, M. Zhang,...

♠ RO, applications:• Structural/Circuit/Network Design • Control • Signal

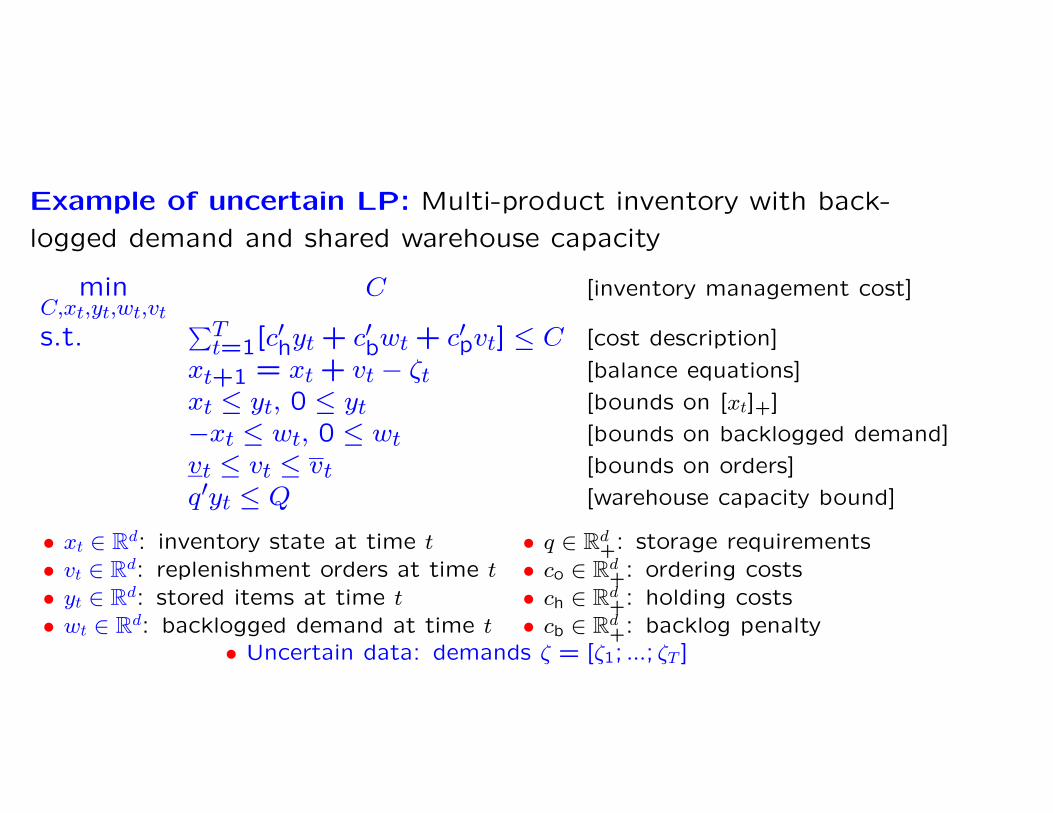

Example of uncertain LP: Multi-product inventory with back-

logged demand and shared warehouse capacity

minC,xt,yt,wt,vt

C [inventory management cost]

s.t.∑T

t=1[c′hyt + c′bwt + c′pvt] ≤ C [cost description]

xt+1 = xt + vt − ζt [balance equations]

xt ≤ yt, 0 ≤ yt [bounds on [xt]+]

−xt ≤ wt, 0 ≤ wt [bounds on backlogged demand]

vt ≤ vt ≤ vt [bounds on orders]

q′yt ≤ Q [warehouse capacity bound]

• xt ∈ Rd: inventory state at time t • q ∈ Rd+: storage requirements

• vt ∈ Rd: replenishment orders at time t • co ∈ Rd+: ordering costs

• yt ∈ Rd: stored items at time t • ch ∈ Rd+: holding costs

• wt ∈ Rd: backlogged demand at time t • cb ∈ Rd+: backlog penalty

• Uncertain data: demands ζ = [ζ1; ...; ζT ]

{

minx

{f(x, ζ) : F (x, ζ) ∈ K} : ζ ∈ Z}

(Unc)

Assume that our “decision environment” is such that

• All decisions xj should be made before ζ “reveals itself”

and thus should be independent of ζ

• The constraints are “hard”: their violations cannot be

tolerated

• We intend to take full care of all data ζ ∈ Z and do not

care what happens when ζ 6∈ Z.

Under these assumptions, seemingly the only meaningful way to

process (Unc) is to solve the Robust Counterpart

mint,x

{t : ∀ζ ∈ Z : f(x, ζ) ≤ t, F (x, ζ) ∈ K} (RC)

of the uncertain problem.

Example: To build the RC of the Inventory problem, we use

balance equations to eliminate the states and pass to the RC of

the resulting inequality constrained problem, thus arriving at

minC,yt,wt,vt

C

s.t.

∑Tt=1[c

′hyt + c′bwt + c′pvt] ≤ C

x1 +∑t−1

τ=1[vτ − ζτ ] ≤ yt, 0 ≤ yt

−x1 − ∑t−1τ=1[xτ − ζτ ] ≤ wt, 0 ≤ wt

vt ≤ vt ≤ vt, q′yt ≤ Q

∀ζ ∈ Z(RC)

Note: When Z is a computationally tractable convex set, the

semi-infinite problem (RC) is computationally tractable. E.g.,

when Z is polyhedral: Z = {ζ : ∃u : Pζ + Qu + r ≥ 0}, RC can

be converted into an explicit LP program of sizes polynomial in

T, d and the sizes of the representation of Z.

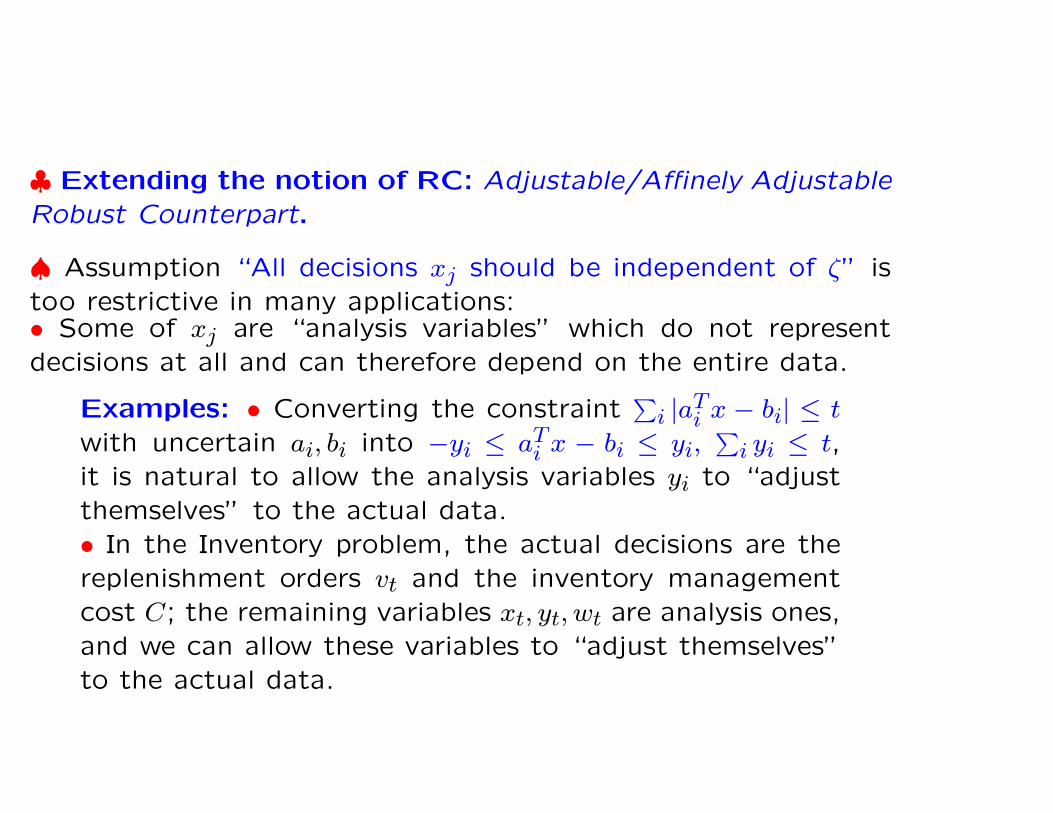

♣ Extending the notion of RC: Adjustable/Affinely Adjustable

Robust Counterpart.

♠ Assumption “All decisions xj should be independent of ζ” is

too restrictive in many applications:• Some of xj are “analysis variables” which do not represent

decisions at all and can therefore depend on the entire data.

Examples: • Converting the constraint∑

i |aTi x − bi| ≤ t

with uncertain ai, bi into −yi ≤ aTi x − bi ≤ yi,

∑

i yi ≤ t,

it is natural to allow the analysis variables yi to “adjust

themselves” to the actual data.

• In the Inventory problem, the actual decisions are the

replenishment orders vt and the inventory management

cost C; the remaining variables xt, yt, wt are analysis ones,

and we can allow these variables to “adjust themselves”

to the actual data.

• In dynamical decision-making, some of the decisions xj should

be made when the actual data becomes partially known and thus

can depend on the corresponding portions of the data

Example: In the Inventory problem with uncertain de-

mand, replenishment orders vt of day t usually can depend

on the actual demands at days 1, ..., t − 1.

♣ To account for adjustability, we allow for every xj to depend

on a prescribed portion Pjζ of ζ: xj = Xj(Pjζ), thus arriving at

Adjustable Robust Counterpart

mint,{Xj(·)}n

j=1

{t : ∀ζ ∈ Z : f(X(ζ), ζ) ≤ t, F (X(ζ), ζ) ∈ K}

[X(ζ) = {Xj(Pjζ)}](ARC)

Note: ARC is infinite-dimensional and thus is typically heavily

computationally intractable. Seemingly the only applicable tech-

nique is Dynamic Programming ⇒“curse of dimensionality”

♣ To overcome, to some extent, intractability of ARC, we re-

strict the decision rules to be affine: Xj(Pjζ) = ξ0j + ξTj Pjζ, thus

arriving at the Affinely Adjustable Robust Counterpart

mint,{ξ0j ,ξj}n

j=1

{t : ∀ζ ∈ Z : f(X(ζ), ζ) ≤ t, F (X(ζ), ζ) ∈ K}

[X(ζ) = {ξ0j + ξTj Pjζ}n

j=1](AARC)

Example: The only “actual decisions” in the Inventory problemare orders vt. Assume that vt can depend on the precedingdemands ζt−1 = [ζ1; ...; ζt−1]. To build the AARC, we• introduce linear decision rules for the orders vt = v0

t + Vtζt−1

• make xt, yt, wt affine functions of ζ:xt = x0t + Xtζ, yt = y0

t +Ytζ, wt = w0

t + Wtζ, thus ending up with

minC,v0

t ,Vt,...,w0t ,Wt

C

s.t.

∑

t≤T [c′h[y0t + Ytζ] + c′b[wt + Wtζ] + c′p[v

0t + Vtζt−1]] ≤ C

x0t+1 + Xt+1ζ = x0

t + Xtζ + v0t + Vtζt−1 − ζt

x0t + Xtζ ≤ y0

t + Ytζ, 0 ≤ y0t + Ytζ

−[x0t + Xtζ] ≤ w0

t + Wtζ, 0 ≤ w0t + Wtζ

vt ≤ v0t + Vtζt−1 ≤ vt, q′[y0

t + Ytζ] ≤ Q

∀ζ ∈ Z

(AARC)Note: The AARC of the Inventory problem is computationallytractable provided that Z is so. E.g., when Z is a polyhedral set,(AARC) is equivalent to an explicit LP program.

Example (continued): Consider single-product Inventory with

N = 10 and a box uncertainty set: (1 − ρ)ζn ≤ ζ ≤ (1 + ρ)ζn.

Here the ARC is well within the grasp of Dynamic Programming.

♣ How large are the gaps in the chain Opt(ARC) ≤ Opt(AARC) ≤Opt(RC) ?

• We built a sample of 768 Inventory problems with uncertainty

of 10% – 50% by picking at random cost coefficients, storage

capacity and nominal demand trajectory ζn and subsequent fil-

tering out problems with infeasible ARC’s.

♠ It turns out that Opt(ARC) = Opt(AARC) in every one of

these 768 problems!

Note: This phenomenon disappears when passing from minimiz-

ing the worst-case inventory management cost to minimizing the

average of this cost.

♠ Opt(RC) was typically essentially worse than Opt(ARC) =

Opt(AARC):

Range of Opt(RC)

Opt(ARC)1 (1,2] (2,10] (10,1000] ∞

Frequency in the sample 38% 23% 14% 11% 15%

♣ In the RO context, affine decision rules not necessarily are

bad!

• Optimization programs with uncertain data and theirRobust Counterparts

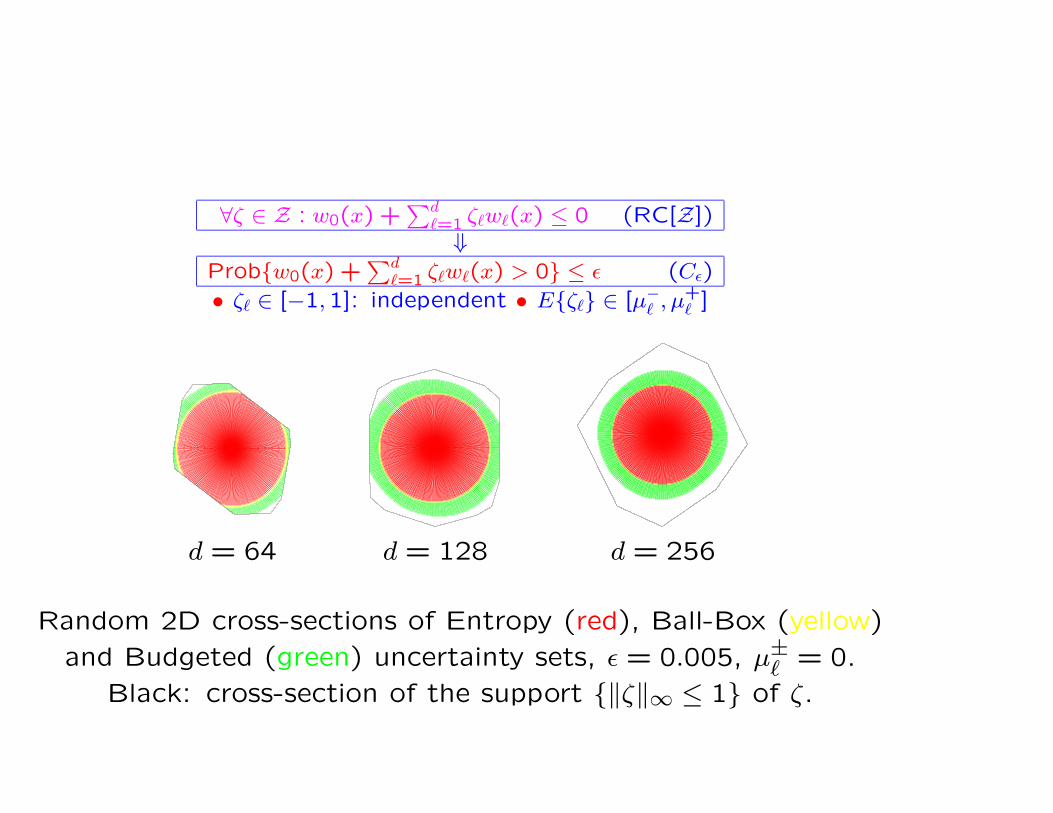

• Tractability of Robust Counterparts• Robust Optimization and Chance Constraints

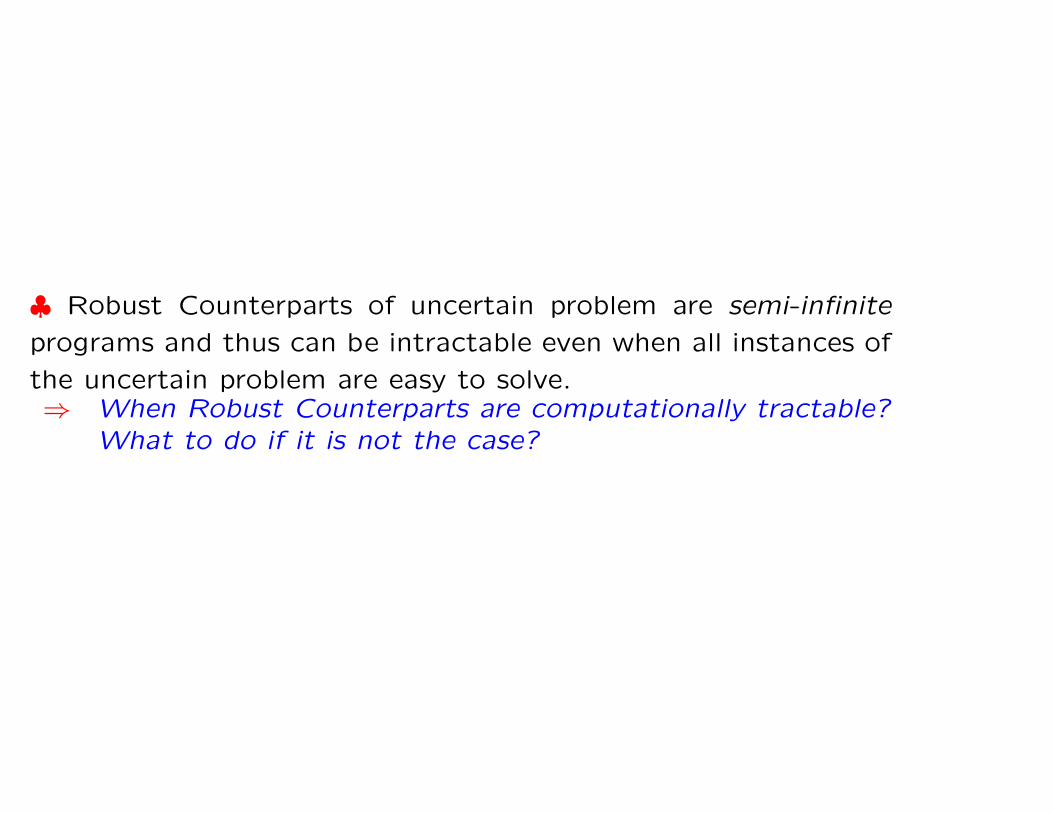

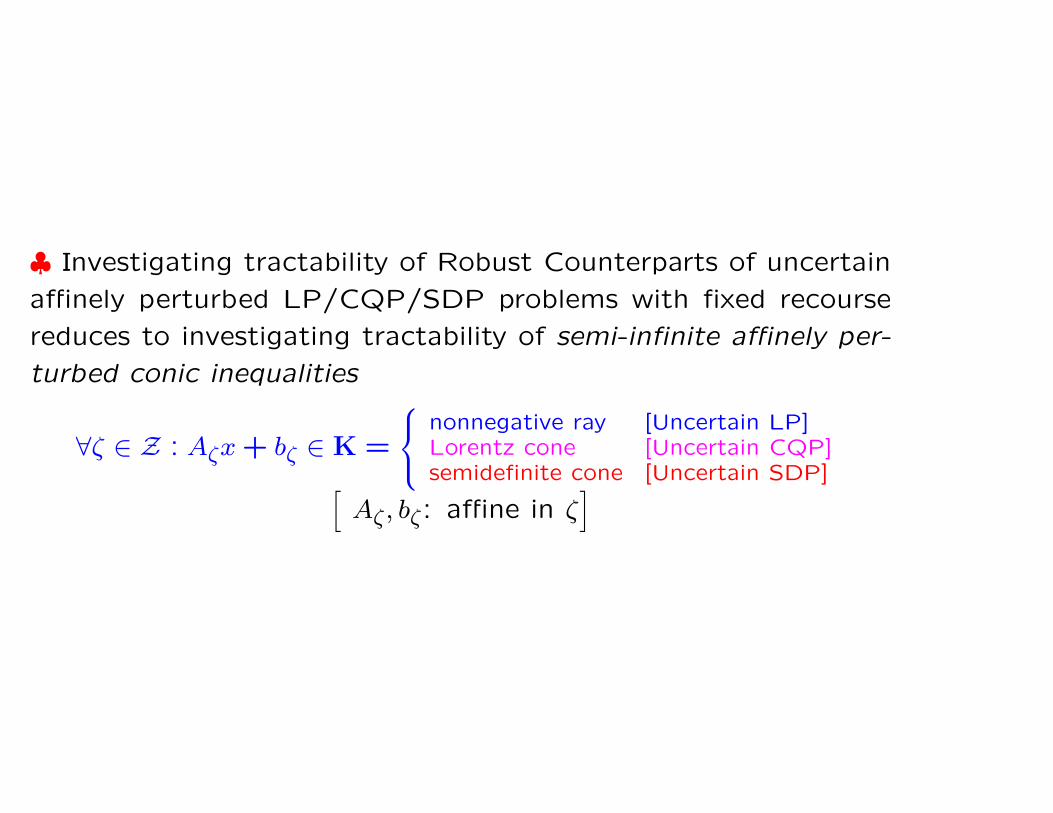

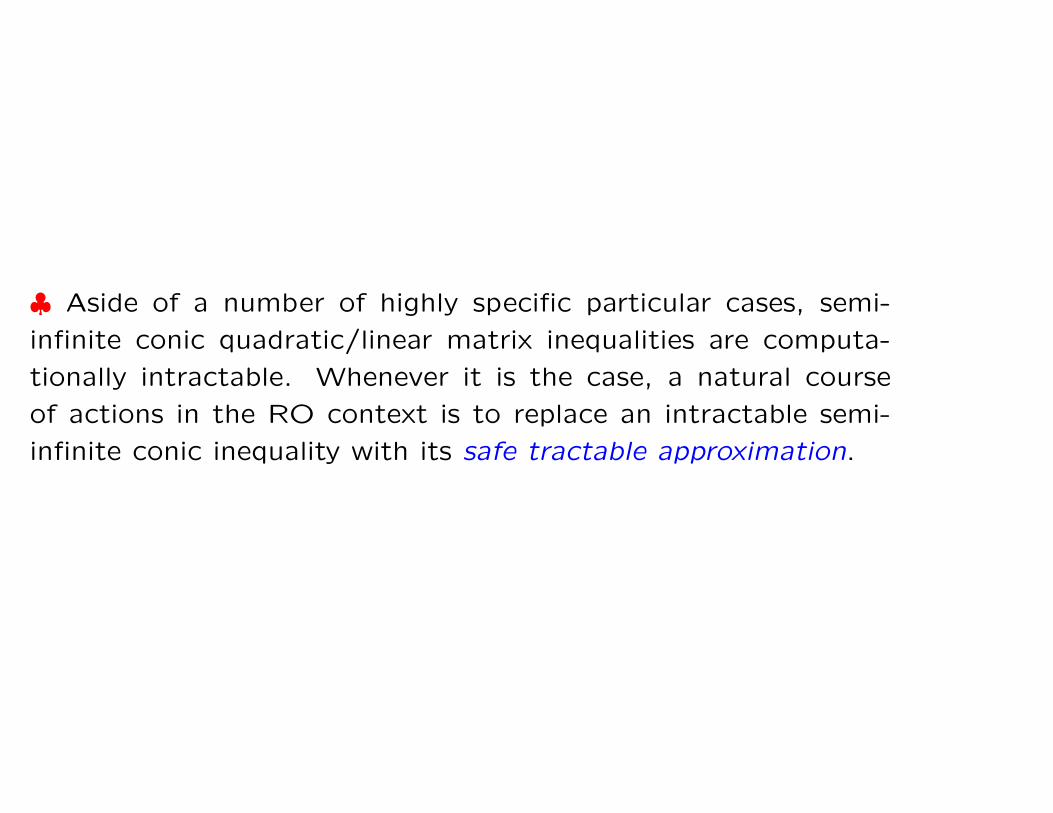

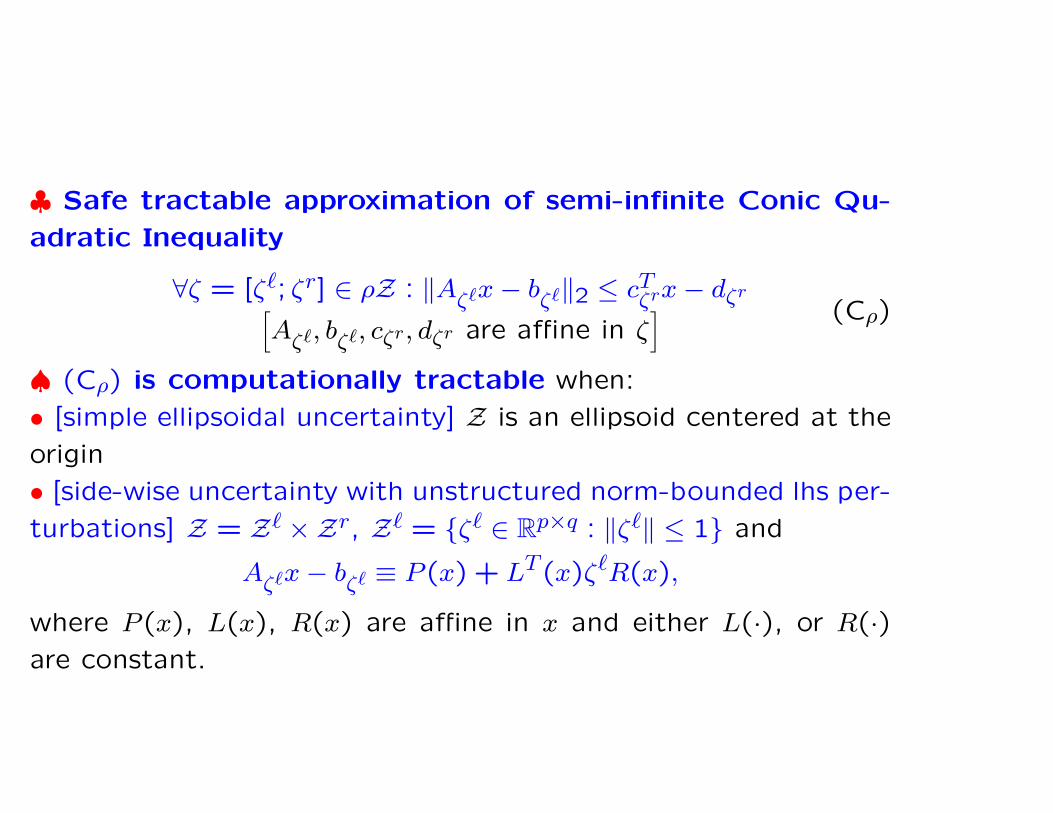

♣ Robust Counterparts of uncertain problem are semi-infinite

programs and thus can be intractable even when all instances of

the uncertain problem are easy to solve.⇒ When Robust Counterparts are computationally tractable?

What to do if it is not the case?

♠ We focus on uncertain affinely perturbed LP/CQP/SDP prob-

lems{

minx

{

cTζ x + dζ : Ai

ζx + biζ ∈ Ki, i = 1, ..., m

}

: ζ ∈ Z}

with fixed recourse:

• cζ, dζ, Aiζ, b

iζ: affine in ζ

• Fixed recourse [automatically valid for the RC]: All coeffi-

cients of the adjustable variables xj (those with Pj 6= 0) are