Selected Topics in Robust ConvexOptimization

Arkadi Nemirovski

School of Industrial and Systems Engineering

Georgia Institute of Technology

• Optimization programs with uncertain data and theirRobust Counterparts

• Tractability of Robust Counterparts• Robust Optimization and Chance Constraints

• Optimization programs with uncertain data and theirRobust Counterparts

• Tractability of Robust Counterparts• Robust Optimization and Chance Constraints

♣ Robust Optimization is a methodology for processing uncer-

tain optimization problems

minx

{f(x, ζ) : F (x, ζ) ∈ K}

• x ∈ Rn is the decision vector

• ζ ∈ Rd is the data (or data perturbation)

• f(x, ζ) : Rn × Rd → R and F (x, ζ) : Rn × Rd → Rm are given

functions, and K ⊂ Rm is a given set.

f(·, ·), F (·, ·),K form the structure of the uncertain problem.

♣ In contrast to Stochastic Programming, RO does not as-

sume stochastic nature of data ζ and uses instead uncertain-

but-bounded uncertainty model: ζ runs through a given (typi-

cally, compact) uncertainty set Z ⊂ Rd.

♣ RO, people:

• 1973: A.L. Soyster (LP)

• 1997: P. Kouvelis & G. Yu (IP)

• 1997 –:L. El Ghaoui & H. Lebret & F. OustryA. Ben-Tal & A. Nemirovski

}

(CP)

• 2000 –: E. Adida, A. Atamturk, A. Beck, D. Bertsi-

mas, C. Bhattacharyya, H.-G. Bock, S. Boyd, G. Calafiore,

M. Diehl, Y. Eldar, E. Erdogan, L. Grate, E. Guslitzer,

B. Golany, D. Goldfarb, C. Hol, G. Iyengar, M. Jor-

dan, E. Kostina, O. Kostyukova, G. Lanckriet, A. Nilim,

M. Sim, D. Pachamanova, C. Roos, C. Schrerer, A. Sood,

A. Thiele, J.-Ph. Vial, M. Zhang,...

♠ RO, applications:• Structural/Circuit/Network Design • Control • Signal

Processing • Machine Learning • Portfolio Optimization

• Inventory...

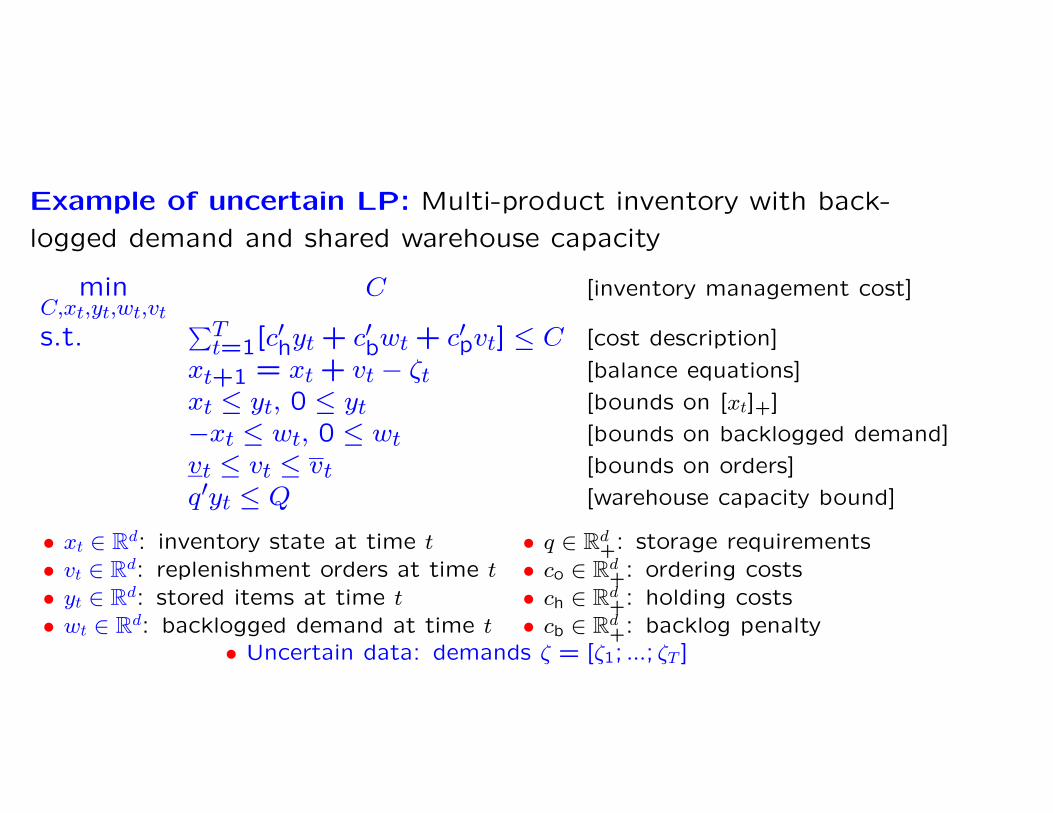

Example of uncertain LP: Multi-product inventory with back-

logged demand and shared warehouse capacity

minC,xt,yt,wt,vt

C [inventory management cost]

s.t.∑T

t=1[c′hyt + c′bwt + c′pvt] ≤ C [cost description]

xt+1 = xt + vt − ζt [balance equations]

xt ≤ yt, 0 ≤ yt [bounds on [xt]+]

−xt ≤ wt, 0 ≤ wt [bounds on backlogged demand]

vt ≤ vt ≤ vt [bounds on orders]

q′yt ≤ Q [warehouse capacity bound]

• xt ∈ Rd: inventory state at time t • q ∈ Rd+: storage requirements

• vt ∈ Rd: replenishment orders at time t • co ∈ Rd+: ordering costs

• yt ∈ Rd: stored items at time t • ch ∈ Rd+: holding costs

• wt ∈ Rd: backlogged demand at time t • cb ∈ Rd+: backlog penalty

• Uncertain data: demands ζ = [ζ1; ...; ζT ]

{

minx

{f(x, ζ) : F (x, ζ) ∈ K} : ζ ∈ Z}

(Unc)

Assume that our “decision environment” is such that

• All decisions xj should be made before ζ “reveals itself”

and thus should be independent of ζ

• The constraints are “hard”: their violations cannot be

tolerated

• We intend to take full care of all data ζ ∈ Z and do not

care what happens when ζ 6∈ Z.

Under these assumptions, seemingly the only meaningful way to

process (Unc) is to solve the Robust Counterpart

mint,x

{t : ∀ζ ∈ Z : f(x, ζ) ≤ t, F (x, ζ) ∈ K} (RC)

of the uncertain problem.

Example: To build the RC of the Inventory problem, we use

balance equations to eliminate the states and pass to the RC of

the resulting inequality constrained problem, thus arriving at

minC,yt,wt,vt

C

s.t.

∑Tt=1[c

′hyt + c′bwt + c′pvt] ≤ C

x1 +∑t−1

τ=1[vτ − ζτ ] ≤ yt, 0 ≤ yt

−x1 − ∑t−1τ=1[xτ − ζτ ] ≤ wt, 0 ≤ wt

vt ≤ vt ≤ vt, q′yt ≤ Q

∀ζ ∈ Z(RC)

Note: When Z is a computationally tractable convex set, the

semi-infinite problem (RC) is computationally tractable. E.g.,

when Z is polyhedral: Z = {ζ : ∃u : Pζ + Qu + r ≥ 0}, RC can

be converted into an explicit LP program of sizes polynomial in

T, d and the sizes of the representation of Z.

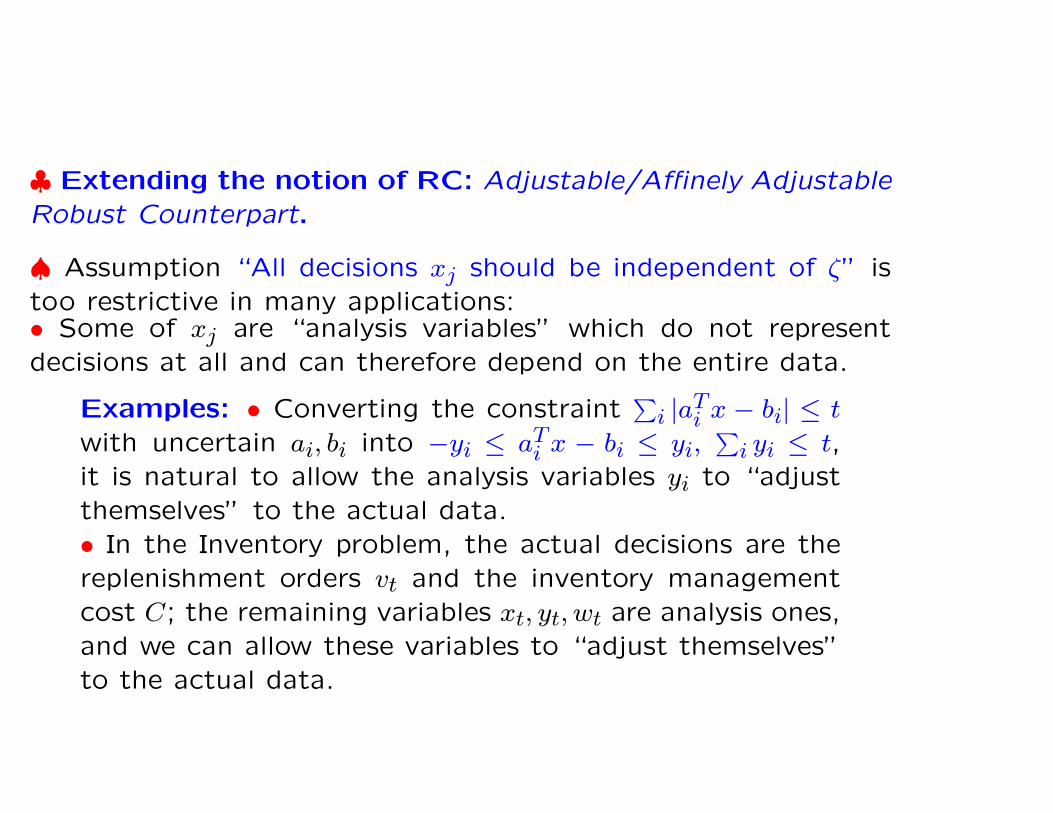

♣ Extending the notion of RC: Adjustable/Affinely Adjustable

Robust Counterpart.

♠ Assumption “All decisions xj should be independent of ζ” is

too restrictive in many applications:• Some of xj are “analysis variables” which do not represent

decisions at all and can therefore depend on the entire data.

Examples: • Converting the constraint∑

i |aTi x − bi| ≤ t

with uncertain ai, bi into −yi ≤ aTi x − bi ≤ yi,

∑

i yi ≤ t,

it is natural to allow the analysis variables yi to “adjust

themselves” to the actual data.

• In the Inventory problem, the actual decisions are the

replenishment orders vt and the inventory management

cost C; the remaining variables xt, yt, wt are analysis ones,

and we can allow these variables to “adjust themselves”

to the actual data.

• In dynamical decision-making, some of the decisions xj should

be made when the actual data becomes partially known and thus

can depend on the corresponding portions of the data

Example: In the Inventory problem with uncertain de-

mand, replenishment orders vt of day t usually can depend

on the actual demands at days 1, ..., t − 1.

♣ To account for adjustability, we allow for every xj to depend

on a prescribed portion Pjζ of ζ: xj = Xj(Pjζ), thus arriving at

Adjustable Robust Counterpart

mint,{Xj(·)}n

j=1

{t : ∀ζ ∈ Z : f(X(ζ), ζ) ≤ t, F (X(ζ), ζ) ∈ K}

[X(ζ) = {Xj(Pjζ)}](ARC)

Note: ARC is infinite-dimensional and thus is typically heavily

computationally intractable. Seemingly the only applicable tech-

nique is Dynamic Programming ⇒“curse of dimensionality”

♣ To overcome, to some extent, intractability of ARC, we re-

strict the decision rules to be affine: Xj(Pjζ) = ξ0j + ξTj Pjζ, thus

arriving at the Affinely Adjustable Robust Counterpart

mint,{ξ0j ,ξj}n

j=1

{t : ∀ζ ∈ Z : f(X(ζ), ζ) ≤ t, F (X(ζ), ζ) ∈ K}

[X(ζ) = {ξ0j + ξTj Pjζ}n

j=1](AARC)

Example: The only “actual decisions” in the Inventory problemare orders vt. Assume that vt can depend on the precedingdemands ζt−1 = [ζ1; ...; ζt−1]. To build the AARC, we• introduce linear decision rules for the orders vt = v0

t + Vtζt−1

• make xt, yt, wt affine functions of ζ:xt = x0t + Xtζ, yt = y0

t +Ytζ, wt = w0

t + Wtζ, thus ending up with

minC,v0

t ,Vt,...,w0t ,Wt

C

s.t.

∑

t≤T [c′h[y0t + Ytζ] + c′b[wt + Wtζ] + c′p[v

0t + Vtζt−1]] ≤ C

x0t+1 + Xt+1ζ = x0

t + Xtζ + v0t + Vtζt−1 − ζt

x0t + Xtζ ≤ y0

t + Ytζ, 0 ≤ y0t + Ytζ

−[x0t + Xtζ] ≤ w0

t + Wtζ, 0 ≤ w0t + Wtζ

vt ≤ v0t + Vtζt−1 ≤ vt, q′[y0

t + Ytζ] ≤ Q

∀ζ ∈ Z

(AARC)Note: The AARC of the Inventory problem is computationallytractable provided that Z is so. E.g., when Z is a polyhedral set,(AARC) is equivalent to an explicit LP program.

Example (continued): Consider single-product Inventory with

N = 10 and a box uncertainty set: (1 − ρ)ζn ≤ ζ ≤ (1 + ρ)ζn.

Here the ARC is well within the grasp of Dynamic Programming.

♣ How large are the gaps in the chain Opt(ARC) ≤ Opt(AARC) ≤Opt(RC) ?

• We built a sample of 768 Inventory problems with uncertainty

of 10% – 50% by picking at random cost coefficients, storage

capacity and nominal demand trajectory ζn and subsequent fil-

tering out problems with infeasible ARC’s.

♠ It turns out that Opt(ARC) = Opt(AARC) in every one of

these 768 problems!

Note: This phenomenon disappears when passing from minimiz-

ing the worst-case inventory management cost to minimizing the

average of this cost.

♠ Opt(RC) was typically essentially worse than Opt(ARC) =

Opt(AARC):

Range of Opt(RC)

Opt(ARC)1 (1,2] (2,10] (10,1000] ∞

Frequency in the sample 38% 23% 14% 11% 15%

♣ In the RO context, affine decision rules not necessarily are

bad!

• Optimization programs with uncertain data and theirRobust Counterparts

• Tractability of Robust Counterparts• Robust Optimization and Chance Constraints

♣ Robust Counterparts of uncertain problem are semi-infinite

programs and thus can be intractable even when all instances of

the uncertain problem are easy to solve.⇒ When Robust Counterparts are computationally tractable?

What to do if it is not the case?

♠ We focus on uncertain affinely perturbed LP/CQP/SDP prob-

lems{

minx

{

cTζ x + dζ : Ai

ζx + biζ ∈ Ki, i = 1, ..., m

}

: ζ ∈ Z}

with fixed recourse:

• cζ, dζ, Aiζ, b

iζ: affine in ζ

• Fixed recourse [automatically valid for the RC]: All coeffi-

cients of the adjustable variables xj (those with Pj 6= 0) are

certain (i.e., independent of ζ).

• Ki: nonnegative rays/Lorentz cones/semidefinite cones (un-

certain LP, CQP, SDP, respectively).

♠ We always assume that Z is given by a strictly feasible semidef-

inite representation

Z = {ζ : ∃u : P(ζ, u) � 0}(P(·): affine in (ζ, u)).

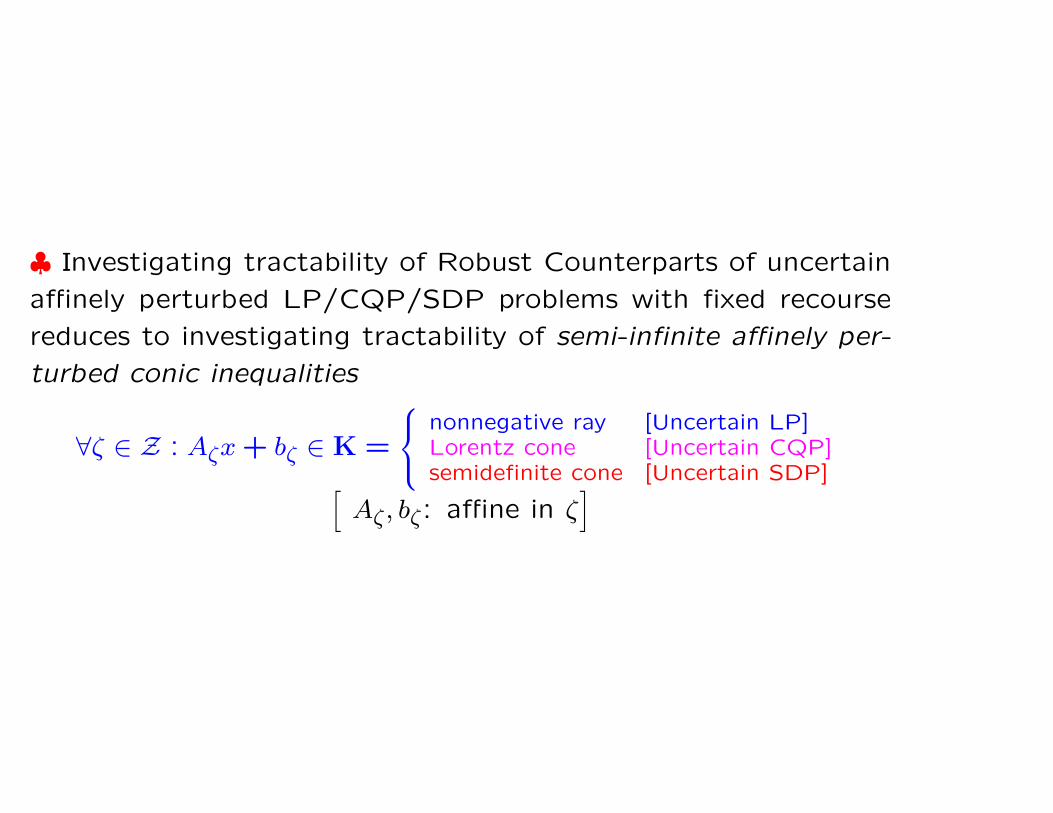

♣ Investigating tractability of Robust Counterparts of uncertain

affinely perturbed LP/CQP/SDP problems with fixed recourse

reduces to investigating tractability of semi-infinite affinely per-

turbed conic inequalities

∀ζ ∈ Z : Aζx + bζ ∈ K =

nonnegative ray [Uncertain LP]Lorentz cone [Uncertain CQP]semidefinite cone [Uncertain SDP]

[

Aζ, bζ: affine in ζ]

♣ Tractability of a semi-infinite affinely perturbed conic inequal-

ity

∀ζ ∈ Z : Aζx + bζ ∈ K

depends on the tradeoff between the geometries of K and Z –

the more complicated is Z, the simpler should be K.

♣ “Trivial case”: Scenario-generated uncertainty set

Theorem. The RC/AARC of an uncertain affinely perturbed

LP/CQP/SDP problem{

minx

{

cTζ x + dζ : Ai

ζx + biζ ∈ Ki, i = 1, ..., m

}

: ζ ∈ Z}

with fixed recourse and with scenario-generated uncertainty set

Z = Conv{ζ1, ..., ζN} is computationally tractable.

♣ “Solvable case”: Uncertain LP

Theorem. The RC/AARC of uncertain affinely perturbed LP

problem{

minx

{

cTζ x + dζ : Ai

ζx + biζ ∈ Ki, i = 1, ..., m

}

: ζ ∈ Z}

[Ki : given by explicit lists of linear inequalities]

with fixed recourse is computationally tractable. With Z given by

a strictly feasible LP/CQP/SDP representation, the RC/AARC

is an explicit LP/CQP/SDP program of sizes polynomial in the

size of instances and the size of the representation of the uncer-

tainty set.

♣ Aside of a number of highly specific particular cases, semi-

infinite conic quadratic/linear matrix inequalities are computa-

tionally intractable. Whenever it is the case, a natural course

of actions in the RO context is to replace an intractable semi-

infinite conic inequality with its safe tractable approximation.

Definition. Consider a semi-infinite conic inequality

∀ζ ∈ Z : Aζx + bζ ∈ K (C)

and let 0 ∈ Z. We embed (C) into the parametric family of

semi-infinite conic inequalities

∀(ζ ∈ ρZ) : Aζx + bζ ∈ K (Cρ)

(ρ ≥ 0: uncertainty level).

A system of convex constraints (Sρ) in variables x and additional

variables u is called a safe tractable approximation of (Cρ) tight

within factor ϑ ≥ 1, if

• [tractability] The constraints in (Sρ) are efficiently computable

• [safety] Whenever x can be extended to a feasible solution of

(Sρ), x is feasible for (Cρ)

• [tightness] Whenever x cannot be extended to a feasible solu-

tion of (Sρ), x is not feasible for (Cϑρ).

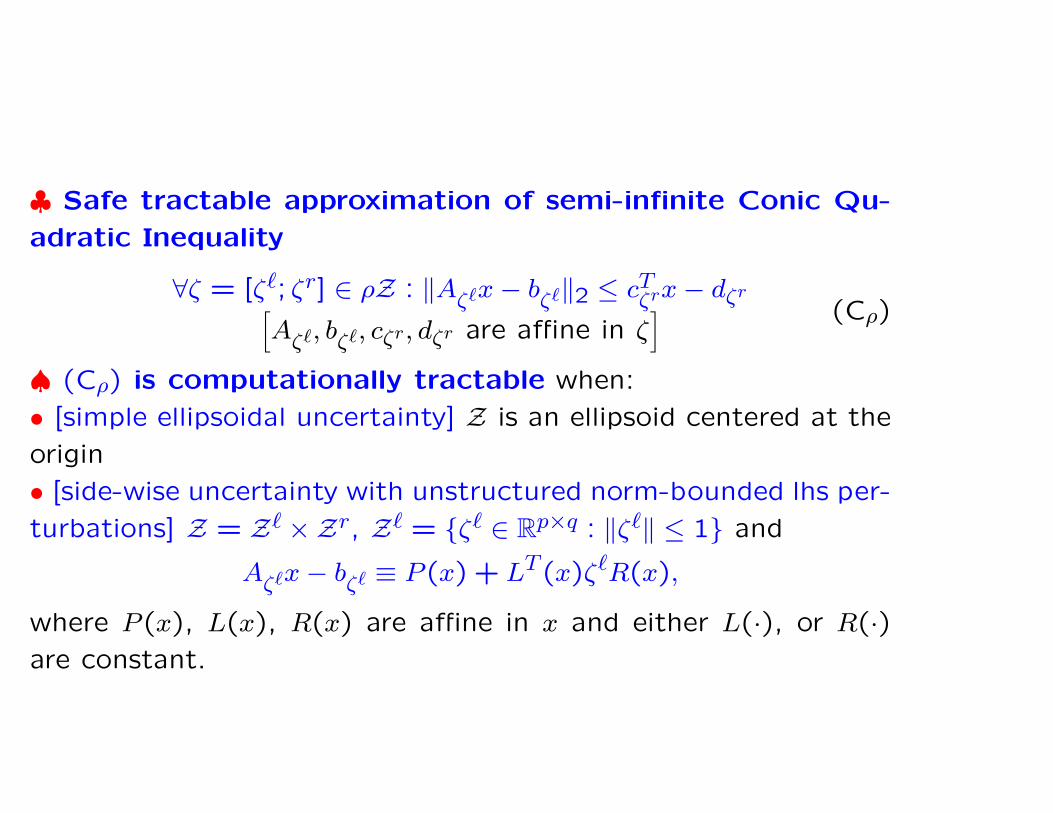

♣ Safe tractable approximation of semi-infinite Conic Qu-

adratic Inequality

∀ζ = [ζ`; ζr] ∈ ρZ : ‖Aζ`x − bζ`‖2 ≤ cTζrx − dζr

[

Aζ`, bζ`, cζr, dζr are affine in ζ] (Cρ)

♠ (Cρ) is computationally tractable when:

• [simple ellipsoidal uncertainty] Z is an ellipsoid centered at the

origin

• [side-wise uncertainty with unstructured norm-bounded lhs per-

turbations] Z = Z` ×Zr, Z` = {ζ` ∈ Rp×q : ‖ζ`‖ ≤ 1} and

Aζ`x − bζ` ≡ P (x) + LT (x)ζ`R(x),

where P (x), L(x), R(x) are affine in x and either L(·), or R(·)are constant.

Example: The semi-infinite Least Squares inequality

∀(ζ ∈ Rp×q, ‖ζ‖ ≤ ρ) : ‖

[

[An, bn] + LT ζR]

[x; 1]‖2 ≤ t (Cρ)

admits exact SDP representation

tI − λLTL Anx + bn

λI ρR[x; 1]

[Anx + bn]T ρ[R[x; 1]]T t

� 0 (Sρ)

in variables t, x, λ: (t, x) is feasible for (Cρ) iff it can be extended

to a feasible solution to (Sρ).

∀ζ = [ζ`; ζr] ∈ ρZ : ‖Aζ`x − bζ`‖2 ≤ cTζrx − dζr (Cρ)

♠ (Cρ) admits tight tractable safe approximation when the

uncertainty is side-wise: Z = Z` ×Zr and

• [∩-ellipsoidal lhs perturbation set]

Z` = {ζ` : [ζ`]TQjζ` ≤ 1, 1 ≤ j ≤ M} with Qj � 0,

∑

j Qj � 0

⇒(Cρ) admits an explicit safe SDP approximation tight within

the factor ϑ = O(1)√

lnM .

• [structured norm-bounded lhs perturbations]

Z` = {ζ` = {ζ`j}J

j=1 : ζ`j ∈ R

pj×qj : ‖ζ`j‖ ≤ 1}

Aζ`x − bζ` ≡ P (x) +∑

j LTj (x)ζ`

jRj(x)

where P (x), Lj(x), Rj(x) are affine in x and for every j either

Lj(·), or Rj(·) are constant.

⇒(Cρ) admits an explicit safe SDP approximation tight within

the factor ϑ = π2.

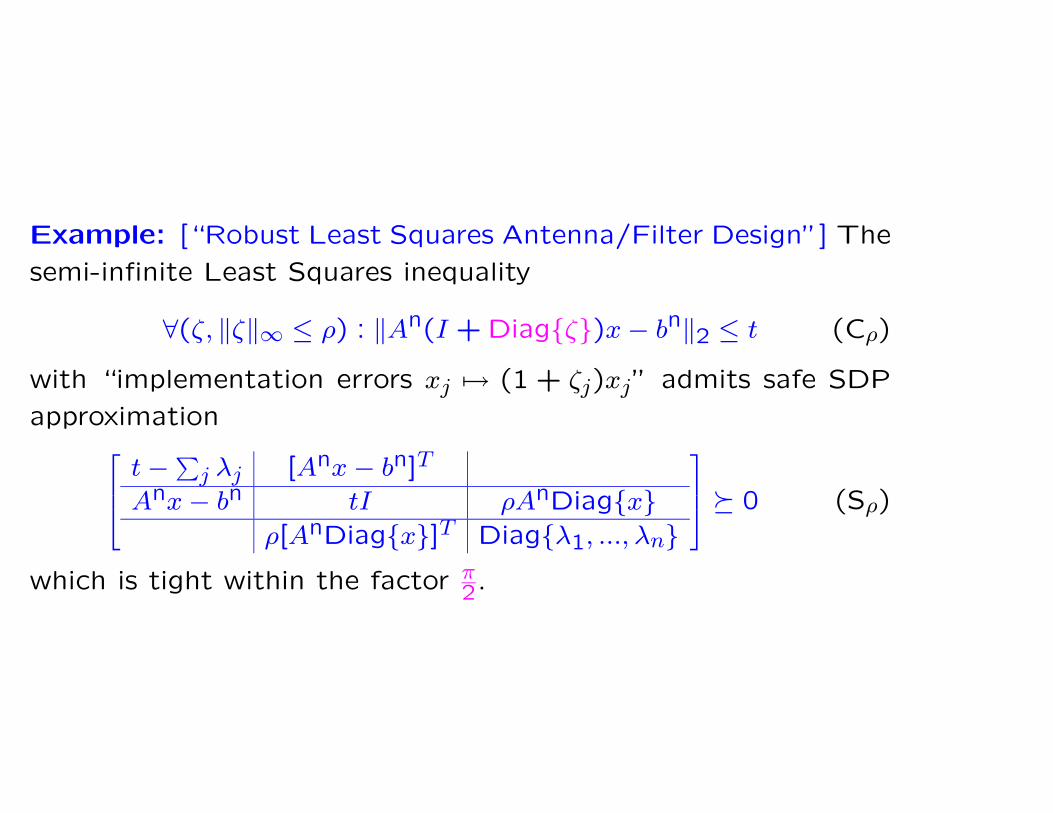

Example: [“Robust Least Squares Antenna/Filter Design”] The

semi-infinite Least Squares inequality

∀(ζ, ‖ζ‖∞ ≤ ρ) : ‖An(I + Diag{ζ})x − bn‖2 ≤ t (Cρ)

with “implementation errors xj 7→ (1 + ζj)xj” admits safe SDP

approximation

t − ∑

j λj [Anx − bn]T

Anx − bn tI ρAnDiag{x}ρ[AnDiag{x}]T Diag{λ1, ..., λn}

� 0 (Sρ)

which is tight within the factor π2.

♣ Safe tractable approximation of semi-infinite Linear Ma-

trix Inequality

∀(ζ ∈ ρZ) : Aζ(x) � 0[

Aζ(x) : bi-affine in x, ζ] (Cρ)

♠ Aside of scenario-generated uncertainty set, the only known

case when (Cρ) admits a tight tractable approximation is the

case of structured norm-bounded uncertainty:

Z = {ζ = {ζj}Mj=1 : ζj ∈ R

pj×pj , ‖ζj‖ ≤ 1, ζj = ξjI, j ∈ J}Aζ(x) = An(x) +

∑

j

[

LTj ζjRj(x) + RT

j (x)ζTj Lj

]

[

An(x),Rj(x) are affine in x]

Theorem. The semi-infinite LMI

∀(

{ζj}Mj=1‖ζj‖ ≤ ρ ∀j, ζj = ξjIpj , j ∈ J

)

:

An(x) +∑

j

[

LTj ζjRj(x) + RT

j (x)ζTj Lj

]

� 0(Cρ)

with structured norm-bounded uncertainty admits a safe tractable

SDP approximation. The tightness factor ϑ of this approxima-

tion depends solely on the largest size of the scalar perturbation

blocks

µ =

{

1, J = ∅maxj∈J pj, J 6= ∅

and does not exceed ϑ(µ), where ϑ(·) is a universal function such

that ϑ(1) = π2, ϑ(2) = 2, ϑ(k) ≤ π

√k. In the case of M = 1 (single

perturbation block), the approximation is exact: ϑ = 1.

Applications in: Robust Structural Design, Lyapunov Stability

Analysis/Synthesis under interval uncertainty, etc.

• Optimization programs with uncertain data and theirRobust Counterparts

• Tractability of Robust Counterparts• Robust Optimization and Chance Constraints

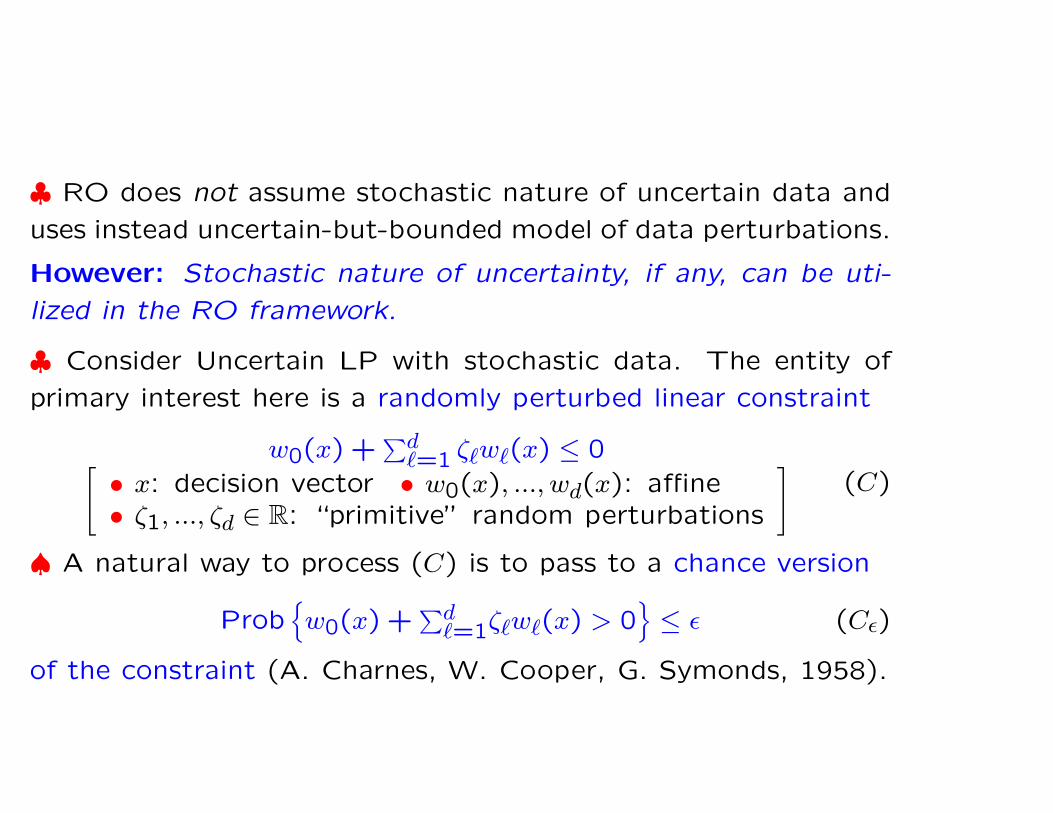

♣ RO does not assume stochastic nature of uncertain data and

uses instead uncertain-but-bounded model of data perturbations.

However: Stochastic nature of uncertainty, if any, can be uti-

lized in the RO framework.

♣ Consider Uncertain LP with stochastic data. The entity of

primary interest here is a randomly perturbed linear constraint

w0(x) +∑d

`=1 ζ`w`(x) ≤ 0[

• x: decision vector • w0(x), ..., wd(x): affine• ζ1, ..., ζd ∈ R: “primitive” random perturbations

]

(C)

♠ A natural way to process (C) is to pass to a chance version

Prob{

w0(x) +∑d

`=1ζ`w`(x) > 0}

≤ ε (Cε)

of the constraint (A. Charnes, W. Cooper, G. Symonds, 1958).

π(w) ≡ Prob{ζw ≡ w0 +∑d

`=1 ζ`w` > 0} ≤ ε (Cε)

♠ There exists significant literature on chance constraints (T.

Badics, D. Dentcheva, A. Dupacova, L. Miller, A. Prekopa, A.

Ruszczynski, B. Vizvari, H. Wagner,...)

However: In general, (Cε) is difficult to process:

• In many cases, the feasible set of a chance constraint is non-

convex;

• Even when convex, the feasible set of (Cε) can be “computa-

tionally intractable”:

When ζ ∼ Uniform([0,1]d), π(w) is quasi-convex (C. Lagoa et al.,

2005). However, unless P=NP, it is impossible to compute π(w)

with accuracy δ > 0 in time polynomial in d, total binary length of

(rational) w and ln(1/δ) [L. Khachiyan, 1989].

π(w) ≡ Prob{ζw ≡ w0 +∑d

`=1 ζ`w` > 0} ≤ ε (Cε)

♣ When (Cε) “as it is” is difficult to process, one can look

for a safe tractable approximation of (Cε) – a computationally

tractable convex set Wε such that

Wε ⊂ {w : π(w) ≤ ε} (∗)♠ A way to build a safe tractable approximation of (Cε):

Take a convex function γ : R → R with lims→−∞

γ(s) = 0,

γ(0) = 1 and set Γ(w) = E {γ(ζw)} .Note: π(w) ≤ Γ(αw) ∀α > 0 and Γ(·) is convex, whence

the set Wε = cl {w : ∃α > 0 : Γ(αw) ≤ ε} is convex and

satisfies (∗).

⇒Whenever Γ(·) is efficiently computable, Wε is a safe tractable

approximation of (Cε).

γ(·) : R → R+, γ(0) = 1 : convex, lims→−∞

γ(s) = 0

⇒ Γ(w) ≥ E

{

γ(

w0 +∑d

`=1 ζ`w`

)}

: convex

⇒ Wε ≡ cl {w : ∃α > 0 : Γ(αw) ≤ ε}⊂{w : Prob{ζw > 0} ≤ ε}Note: Wε is a closed convex cone such that

Wε = {w ∈ Rd+1 : w0 +

∑d

`=1ζ`w` ≤ 0 ∀ζ ∈ Zε}

for an appropriate convex compact set Zε.

⇒The safe approximation w(x) ∈ Wε of the chance constraint

Prob{w0(x) +∑d

`=1 ζ`w`(x) > 0} ≤ ε

is nothing but the Robust Counterpart

∀ζ ∈ Zε : w0(x) + ζ1w1(x) + ... + ζdwd(x) ≤ 0

of the uncertain affinely perturbed linear constraint

w0(x) + ζ1w1(x) + ... + ζdwd(x) ≤ 0

with properly defined perturbation set Zε.

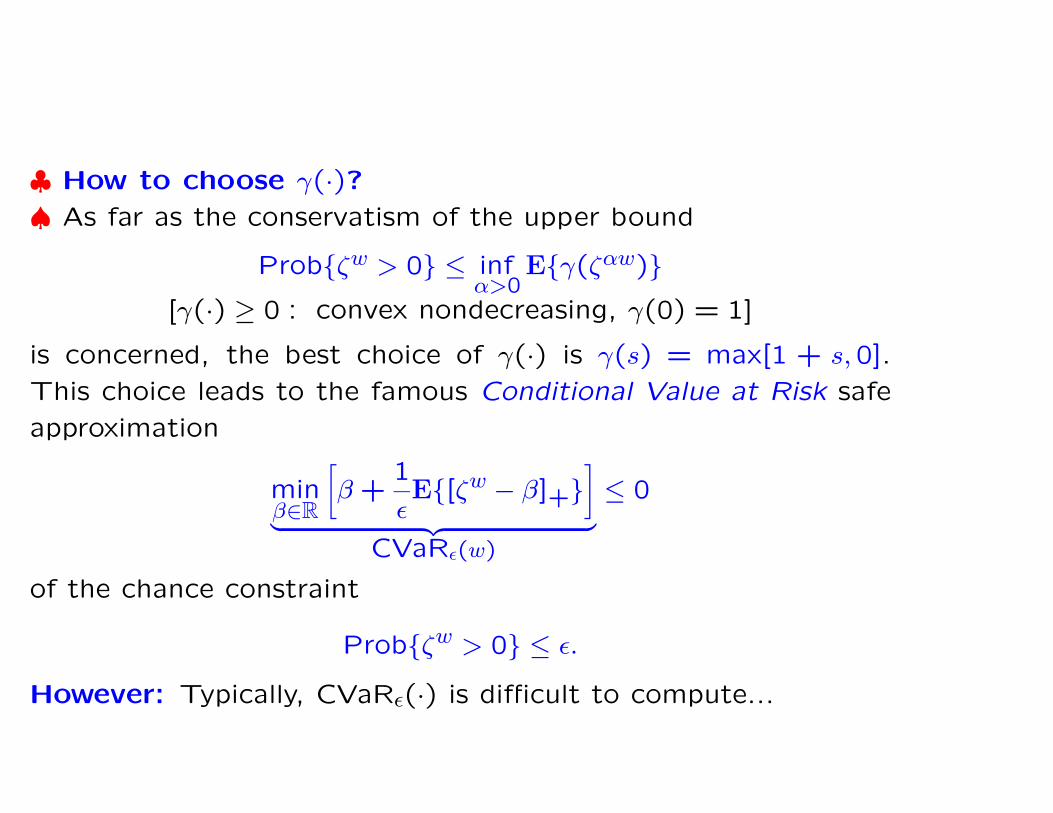

♣ How to choose γ(·)?♠ As far as the conservatism of the upper bound

Prob{ζw > 0} ≤ infα>0

E{γ(ζαw)}[γ(·) ≥ 0 : convex nondecreasing, γ(0) = 1]

is concerned, the best choice of γ(·) is γ(s) = max[1 + s,0].

This choice leads to the famous Conditional Value at Risk safe

approximation

minβ∈R

[

β +1

εE{[ζw − β]+}

]

︸ ︷︷ ︸

CVaRε(w)

≤ 0

of the chance constraint

Prob{ζw > 0} ≤ ε.

However: Typically, CVaRε(·) is difficult to compute...

♣ Ensuring computability: Bernstein approximation [Pin-

ter, 1989; Nem.&Shapiro, 2005]

Observation: Consider a chance constraint

Prob{w0 +∑d

`=1 ζ`w` > 0} ≤ ε (Cε)

and assume that

• ζ1, ..., ζd are independent

• We are smart enough to build efficiently computable

convex bounds Φ`(r) ≥ ln(

E{erζ`})

on the logarithmic

moment-generating functions of ζ`, ` = 1, ..., d.

Choosing γ(s) = es, one can set

Γ(w) = exp{w0 +∑d

`=1 Φ`(w`)}thus arriving at a tractable safe approximation of (Cε).

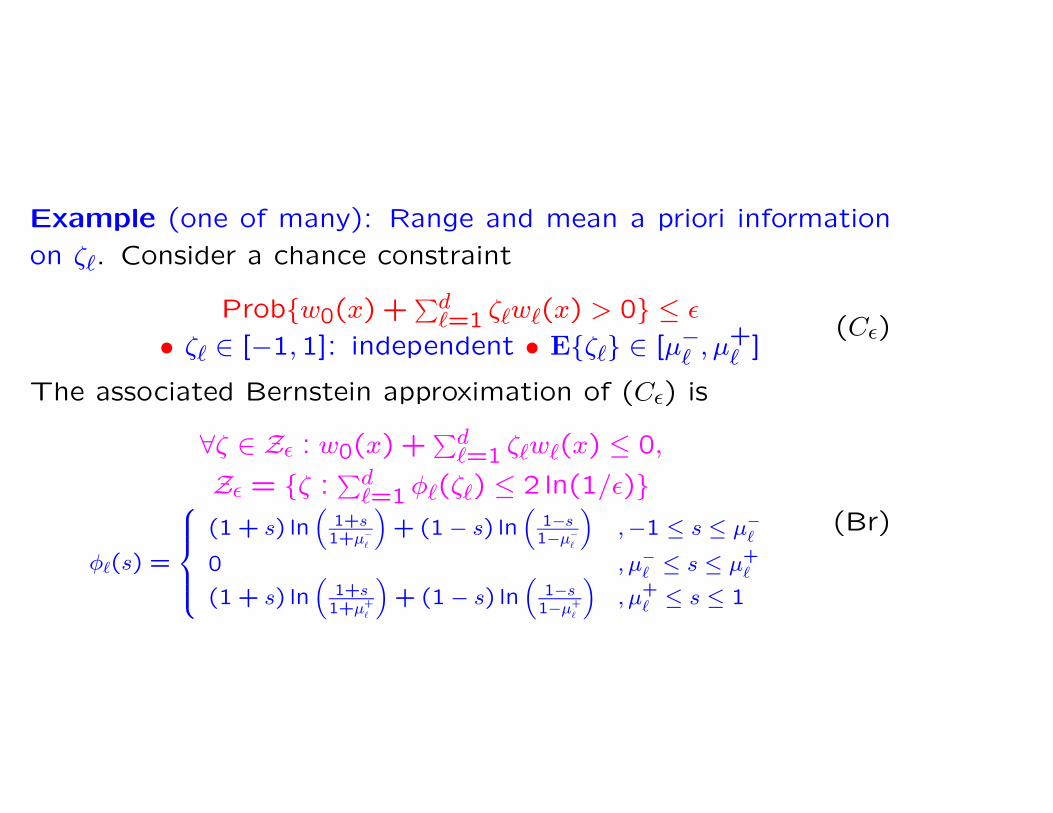

Example (one of many): Range and mean a priori information

on ζ`. Consider a chance constraint

Prob{w0(x) +∑d

`=1 ζ`w`(x) > 0} ≤ ε

• ζ` ∈ [−1,1]: independent • E{ζ`} ∈ [µ−` , µ+

` ](Cε)

The associated Bernstein approximation of (Cε) is

∀ζ ∈ Zε : w0(x) +∑d

`=1 ζ`w`(x) ≤ 0,

Zε = {ζ :∑d

`=1 φ`(ζ`) ≤ 2 ln(1/ε)}

φ`(s) =

(1 + s) ln(

1+s1+µ−

`

)

+ (1 − s) ln(

1−s1−µ−

`

)

,−1 ≤ s ≤ µ−`

0 , µ−` ≤ s ≤ µ+

`

(1 + s) ln(

1+s1+µ+

`

)

+ (1 − s) ln(

1−s1−µ+

`

)

, µ+` ≤ s ≤ 1

(Br)

∀ζ ∈ Zε : w0(x) +∑d

`=1 ζ`w`(x) ≤ 0,

Zε = {ζ :∑d

`=1 φ`(ζ`) ≤ 2 ln(1/ε)}, φ`(s) = ...︸ ︷︷ ︸

“Entropy uncertainty”, Nem.&Shapiro, 2006

(Br) ⇔ Explicit CP

⇓Prob{w0(x) +

∑d`=1 ζ`w`(x) > 0} ≤ ε (Cε)

• ζ` ∈ [−1,1]: independent • E{ζ`} ∈ [µ−` , µ+

` ]

♠ (Br) can be further safely approximated by

∀ζ ∈ Z+ε : w0(x) +

∑

` ζ`w`(x) ≤ 0

Z+ε = {‖ζ‖∞ ≤ 1}⋂

[

{‖ζ‖2 ≤√

2 ln(1/ε)}+{µ− ≤ ζ ≤ µ+}

]

︸ ︷︷ ︸

“Ball-Box uncertainty”, Ben-Tal & Nem., 2000

(BB) ⇔ Explicit CQP

∀ζ ∈ Z+ε : w0(x) +

∑

` ζ`w`(x) ≤ 0

Z+ε = {‖ζ‖∞ ≤ 1}⋂

[

{‖ζ‖2 ≤√

2 ln(1/ε)}+{µ− ≤ ζ ≤ µ+}

](BB) ⇔ Explicit CQP

⇓∀ζ ∈ Zε : w0(x) +

∑d`=1 ζ`w`(x) ≤ 0,

Zε = {ζ :∑d

`=1 φ`(ζ`) ≤ 2 ln(1/ε)}, φ`(s) = ...(Br) ⇔ Explicit CP

⇓Prob{w0(x) +

∑d`=1 ζ`w`(x) > 0} ≤ ε (Cε)

• ζ` ∈ [−1,1]: independent • E{ζ`} ∈ [µ−` , µ+

` ]

♠ (BB) is further safely approximated by

∀ζ ∈ Z++ε : w0(x) +

∑

` ζ`w`(x) ≤ 0

Z++ε = {‖ζ‖∞ ≤ 1}

⋂[

{‖ζ‖1 ≤√

2d ln(1/ε)}+{µ− ≤ ζ ≤ µ+}

]

︸ ︷︷ ︸

“Budgeted uncertainty”, Bertsimas & Sim, 2003

(Bd) ⇔ Explicit LP

∀ζ ∈ Z : w0(x) +∑d

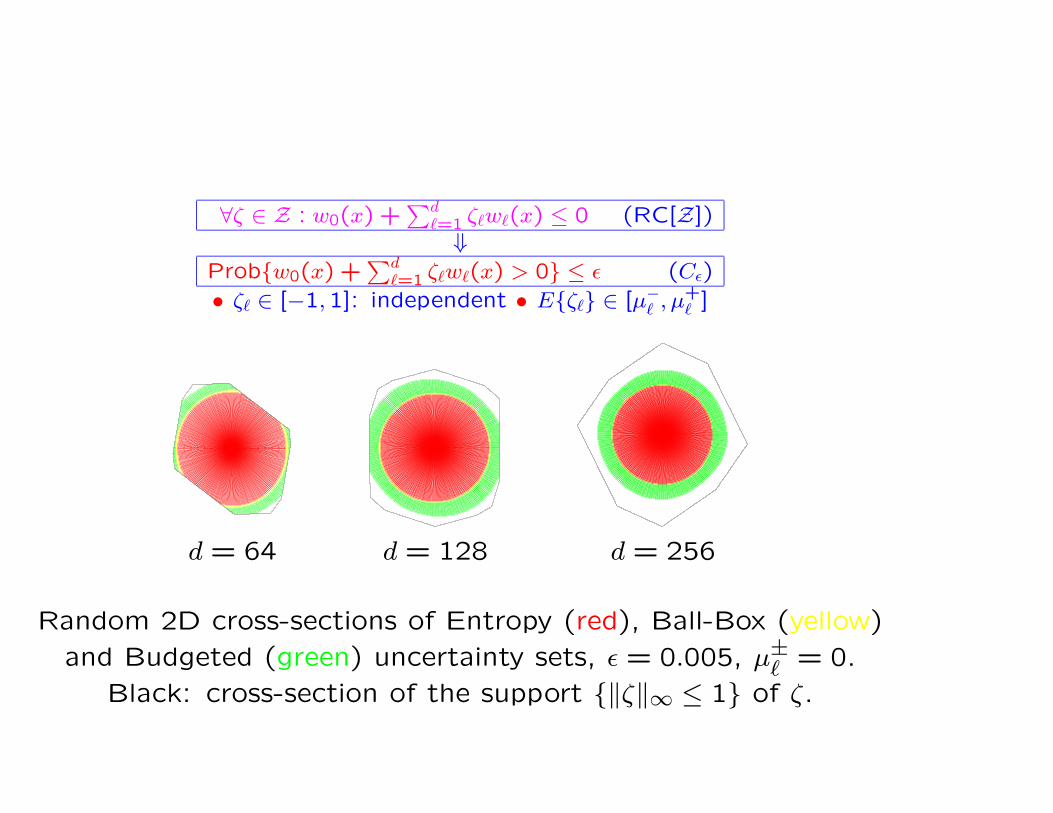

`=1 ζ`w`(x) ≤ 0 (RC[Z])⇓

Prob{w0(x) +∑d

`=1 ζ`w`(x) > 0} ≤ ε (Cε)

• ζ` ∈ [−1,1]: independent • E{ζ`} ∈ [µ−` , µ+

` ]

d = 64 d = 128 d = 256

Random 2D cross-sections of Entropy (red), Ball-Box (yellow)

and Budgeted (green) uncertainty sets, ε = 0.005, µ±` = 0.

Black: cross-section of the support {‖ζ‖∞ ≤ 1} of ζ.

![Selected topics in robust convex optimizationnemirovs/MP_SelectedRO_2008.pdfSelected topics in robust convex optimization 127 Signal processing and estimation [4,29,33].1 It would](https://static.documents.pub/doc/80x56/603e905b21cf823451262378/selected-topics-in-robust-convex-nemirovsmpselectedro2008pdf-selected-topics.jpg)