22

Constanza Jacazio Senior Gas Analyst International Energy Agency Climate change and the shifting energy mix

Constanza Jacazio

Senior Gas Analyst

International Energy Agency

Climate change and the shifting energy mix

© OECD/IEA 2015 © OECD/IEA 2015

Costanza Jacazio,

Senior Gas analyst, IEA

November 2015

Natural gas in a sustainable energy system

© OECD/IEA 2015

The usual gas industry view is:

Coal to gas switch in power generation is a large and cost efficient climate policy option

Consequently we should raise the CO2 price to make gas competitive

Renewable targets/subsidies distort markets

In any case, gas is the ideal back up for renewables so it is needed anyway

© OECD/IEA 2015

Meanwhile views from the green community

Gas is a fossil fuel which will have to be phased out

Cheap gas risks locking out renewables

Earthquakes, methane leakage, water contamination - fracking is bad

“the utility death spiral” – with solar and batteries we will not need large energy companies anyway

© OECD/IEA 2015

EU and USA: the biggest gas consuming sector is not electricity

© OECD/IEA 2015

Industrial gas demand: a modern society without plastics and fertiliser?

© OECD/IEA 2015

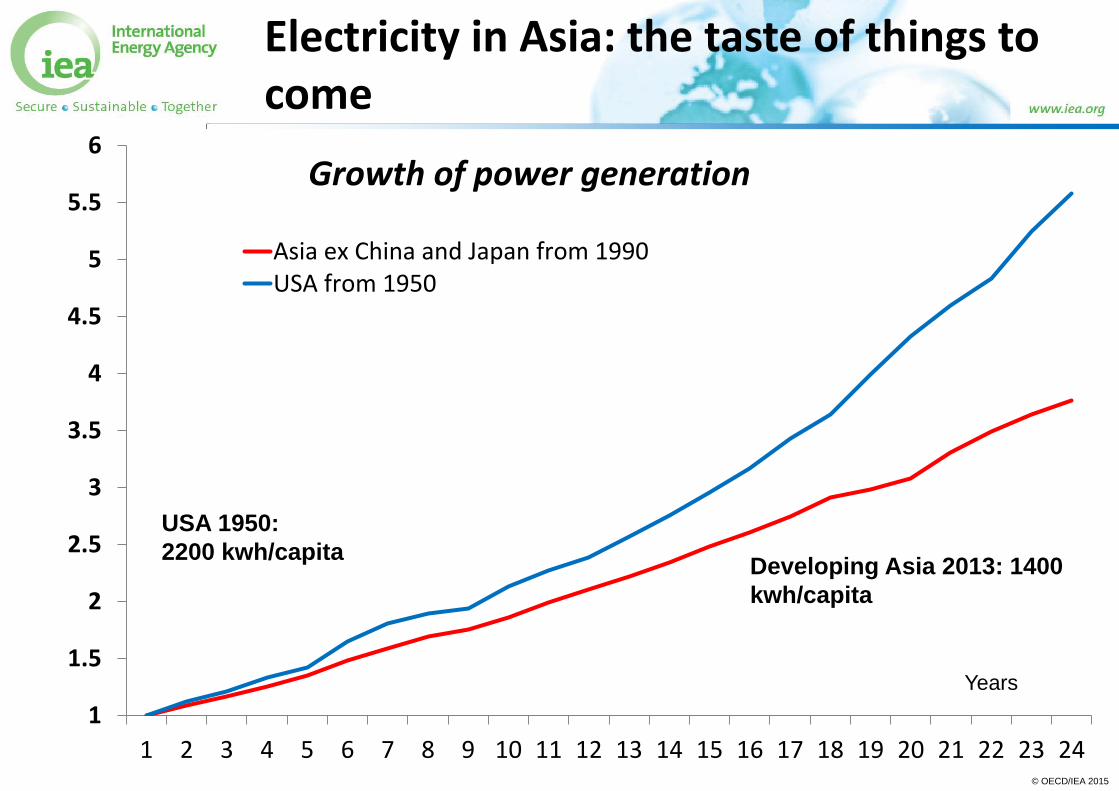

Electricity in Asia: the taste of things to come

1

1.5

2

2.5

3

3.5

4

4.5

5

5.5

6

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Asia ex China and Japan from 1990USA from 1950

Growth of power generation

Developing Asia 2013: 1400

kwh/capita

USA 1950:

2200 kwh/capita

Years

© OECD/IEA 2015

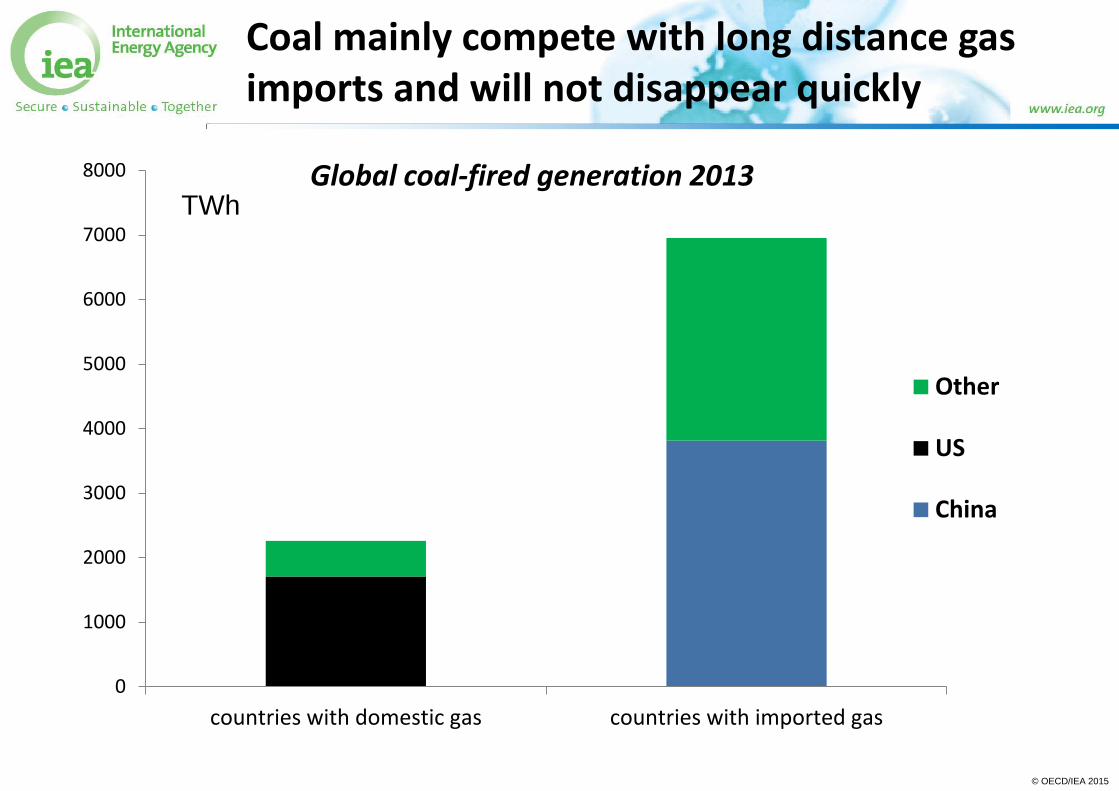

Coal mainly compete with long distance gas imports and will not disappear quickly

0

1000

2000

3000

4000

5000

6000

7000

8000

countries with domestic gas countries with imported gas

Other

US

China

Global coal-fired generation 2013 TWh

© OECD/IEA 2015

60 $/MWh

Is LNG still competitive with wind and solar?

Onshore wind

SA

52 $/MWh

US

48 $/MWh

China

80 - 100 $/MWh

Brazil

54 $/MWh

Turkey

73 $/MWh

Germany

67-100 $/MWh

Ireland

69 $/MWh

Australia

65 $/MWh

UK

120 $/MWh

India

88 $/MWh

Chile

89 $/MWh

85 $/MWh

US

~75 $/MWh

Utility PV

SA

65 $/MWh

Brazil

81 $/MWh

Dubai

<60 $/MWh

UK

120 $/MWh

Recent long-term remuneration contract prices (e.g. auctions or FITs)

Combination of technology cost reduction, better resources, appropriate regulatory framework attracting financing

Long-term PPAs and price competition effective drivers

Egypt

41 $/MWh

© OECD/IEA 2015

Electrification in Asia without coal?

0

1

2

3

4

5

India, Indonesia, Vietnam Malaysia

15 times EU wind and solar or 6 times EU gas imports from Russia

Per capita electricity supply, Mwh/year

© OECD/IEA 2015

Integration of renewables: innovation in the “software” of clean energy

Better forecasting algorithms

Close to real time operation

Improved grid monitoring and TSO collaboration

System friendly renewables

© OECD/IEA 2015

Very large capacity with very low load factors

0

100

200

300

400

500

600

700

800

capacity, GW generation, Twh

© OECD/IEA 2015

Does cheap gas kill renewable investment?

© OECD/IEA 2015

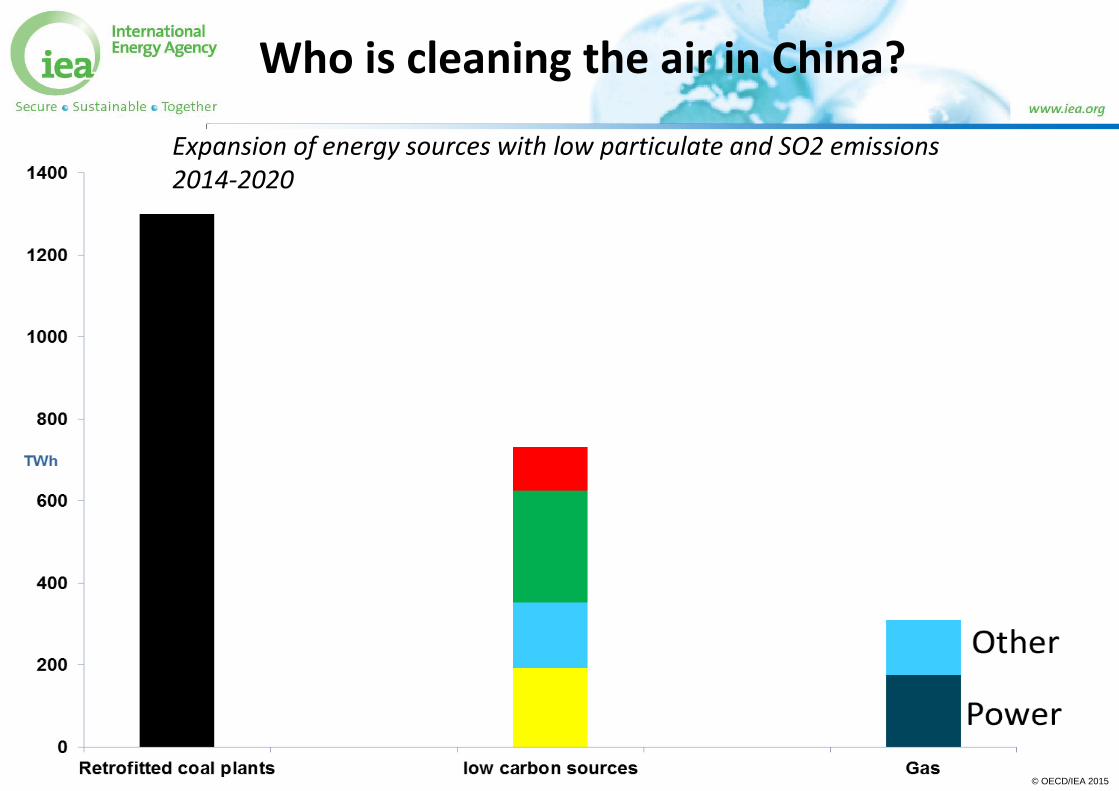

Who is cleaning the air in China?

Expansion of energy sources with low particulate and SO2 emissions 2014-2020

© OECD/IEA 2015

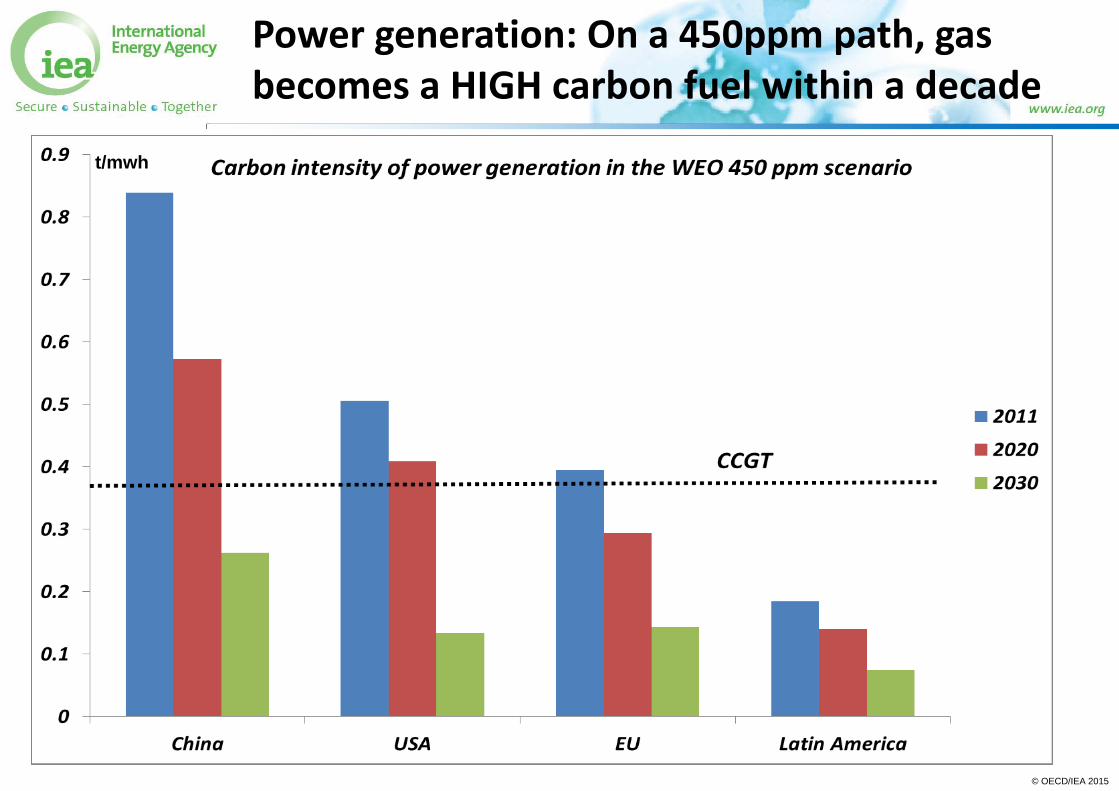

Power generation: On a 450ppm path, gas becomes a HIGH carbon fuel within a decade

t/mwh

© OECD/IEA 2015

Supply security concerns

Conflict with potential

gas supply security

implications

Gas production or

infrastructure

affected by conflict

or terrorism

© OECD/IEA 2015

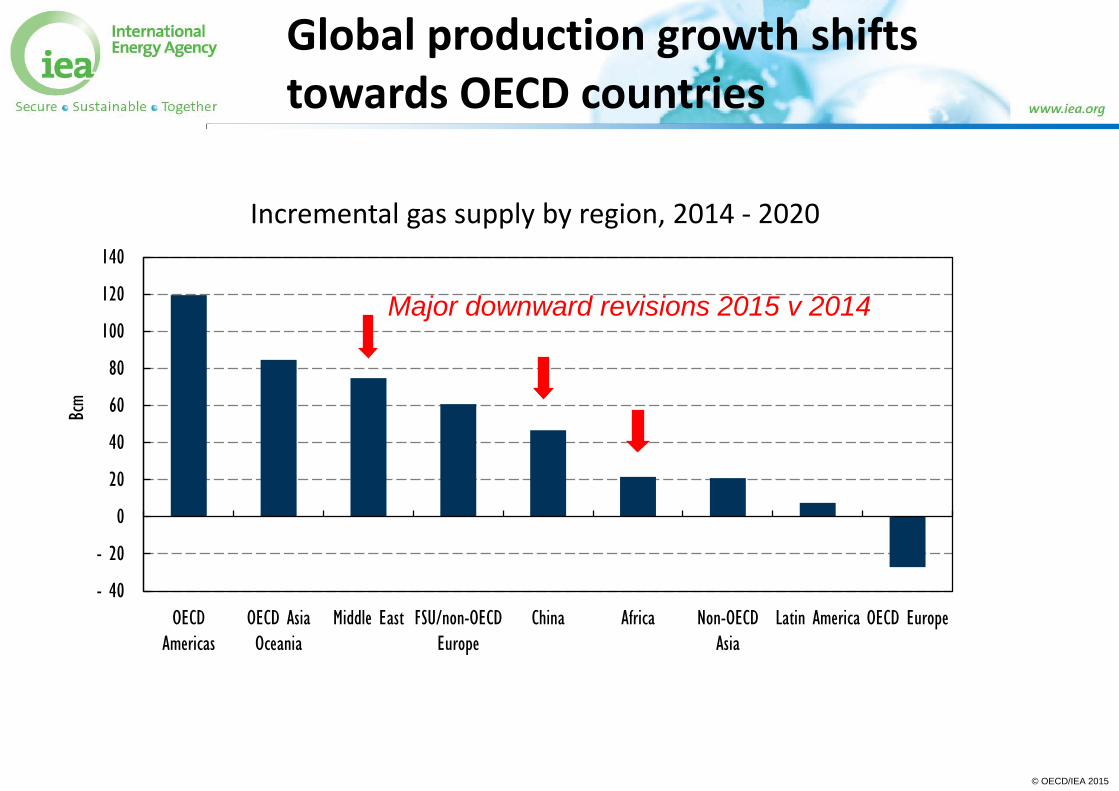

Global production growth shifts towards OECD countries

Incremental gas supply by region, 2014 - 2020

- 40

- 20

0

20

40

60

80

100

120

140

OECD

Americas

OECD Asia

Oceania

Middle East FSU/non-OECD

Europe

China Africa Non-OECD

Asia

Latin America OECD Europe

Bcm

Major downward revisions 2015 v 2014

© OECD/IEA 2015

Resilient production turns North America into a major exporter

Marcellus

Cost deflation

Technological progress

Access to capital

© OECD/IEA 2015

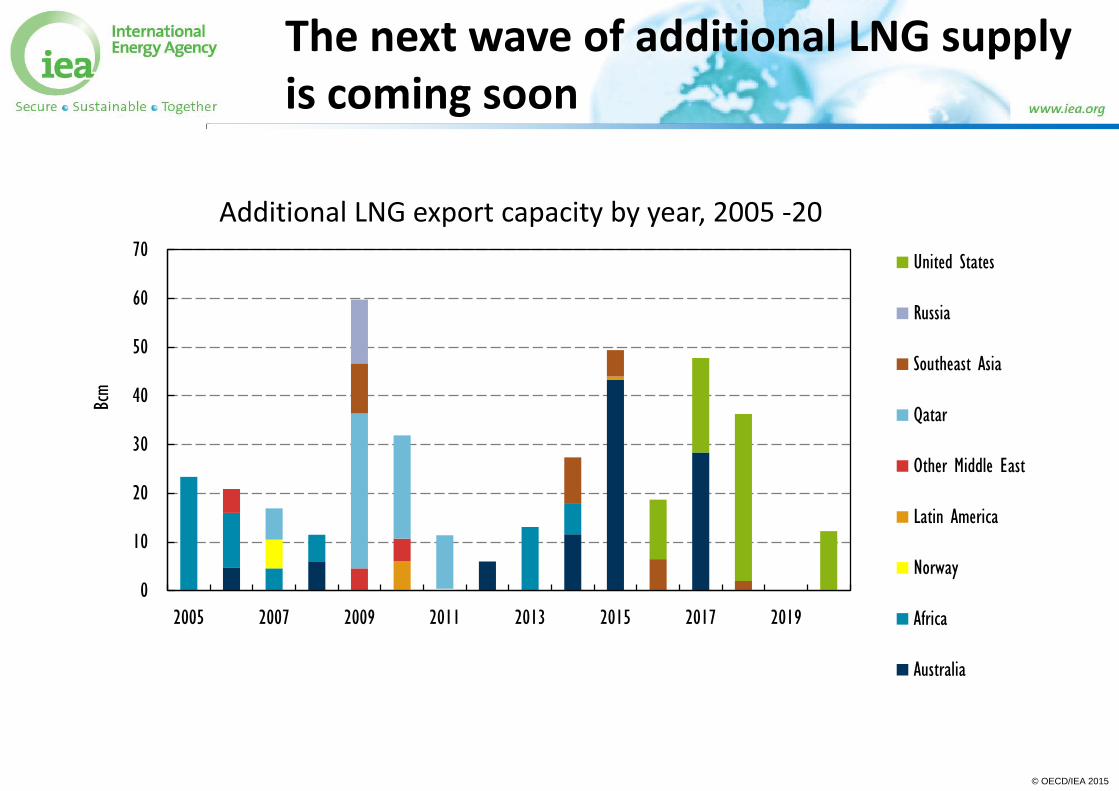

The next wave of additional LNG supply is coming soon

Additional LNG export capacity by year, 2005 -20

0

10

20

30

40

50

60

70

2005 2007 2009 2011 2013 2015 2017 2019

Bcm

United States

Russia

Southeast Asia

Qatar

Other Middle East

Latin America

Norway

Africa

Australia

© OECD/IEA 2015

Methane leakage can move gas from solution to part of the problem

0

200

400

600

800

1000

1200

1400

coal gas

worst case leakage best case leakage

combustion

kg/MWh

Greenhouse gas emissions from power generation

Use the footer function to insert the presentation title and date here

This document is for investment professionals only and should not be relied upon by private investors.

This document has been approved by Sarasin & Partners LLP of Juxon House, 100 St Paul’s Churchyard, London, EC4M 8BU, a limited liability

partnership registered in England & Wales with registered number OC329859 which is authorised and regulated by the Financial Conduct Authority

with firm reference number 475111 and passported under MiFID to provide investment services in the Republic of Ireland.

Please note that the value of shares and the income from them can fall as well as rise and you may not get back the amount originally

invested. This can be as a result of market movements and also of variations in the exchange rates between currencies.

All details in this document are provided for marketing and information purposes only and should not be misinterpreted as investment advice or

taxation advice. This document is not an offer or recommendation to buy or sell shares in the fund. You should not act or rely on this document but

should seek independent advice and verification in relation to its contents. Neither Sarasin & Partners LLP nor any other member of Bank J. Safra

Sarasin Ltd. accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any

part of its contents. The views expressed in this document are those of Sarasin & Partners LLP and these are subject to change without notice.

Where the data in this document comes partially from third party sources the accuracy, completeness or correctness of the information contained in

this publication is not guaranteed, and third party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability

in connection with third party data.

© 2015 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners

LLP. Please contact [email protected].

Important Information

Use the footer function to insert the presentation title and date here

Sarasin & Partners LLP

Juxon House

100 St. Paul’s Churchyard

London EC4M 8BU

T: +44 (0)20 7038 7000

F: +44 (0)20 7038 6850

www.sarasinandpartners.com

![PDF Energy Analyst 27[1].04.10-Presentation Final](https://static.documents.pub/doc/80x56/577d344c1a28ab3a6b8d8315/pdf-energy-analyst-2710410-presentation-final.jpg)