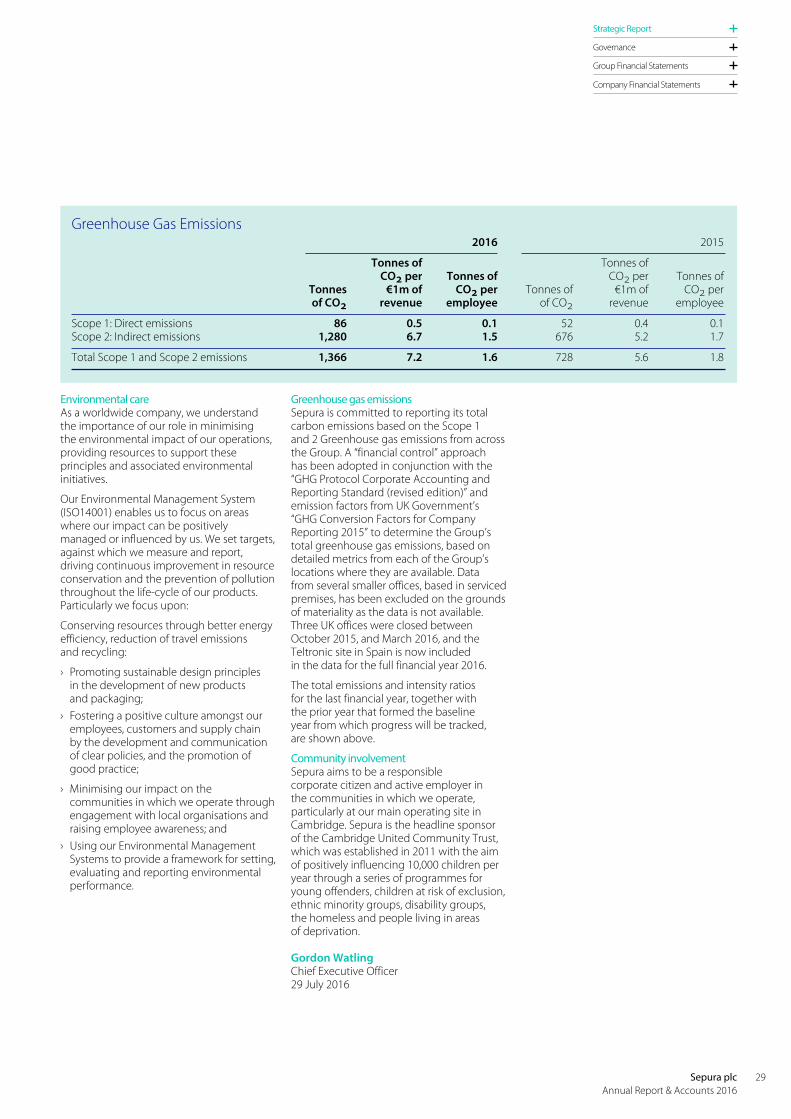

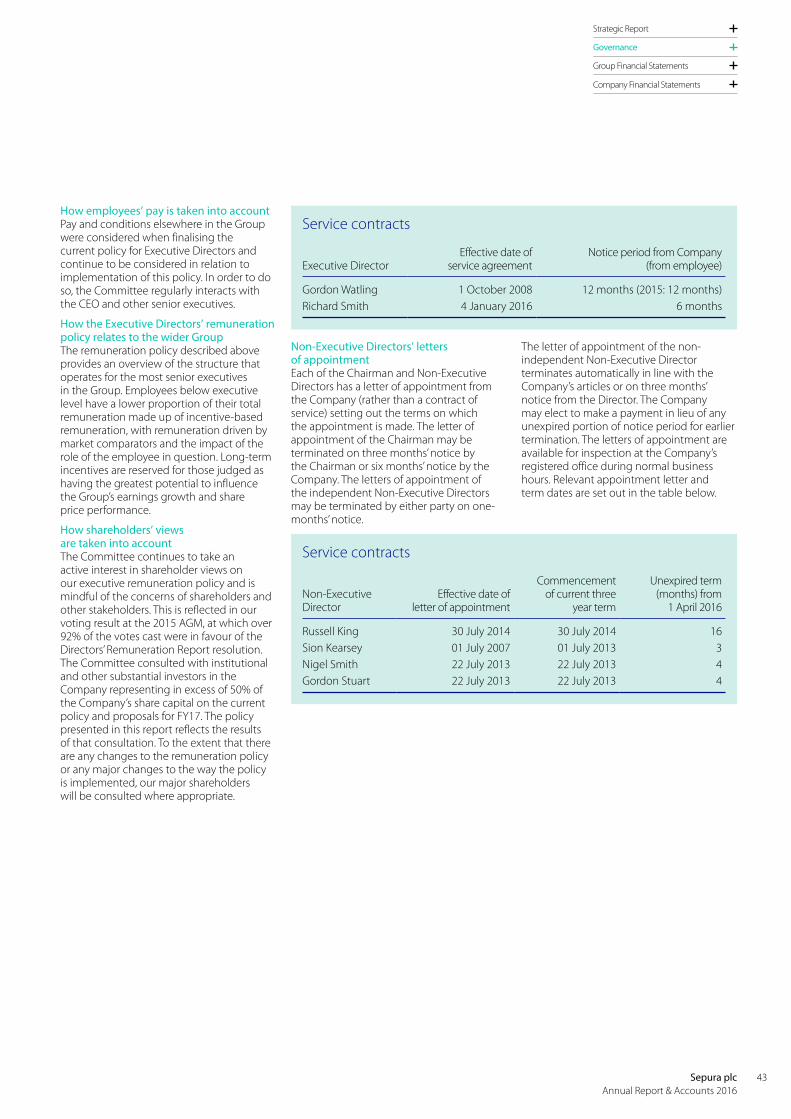

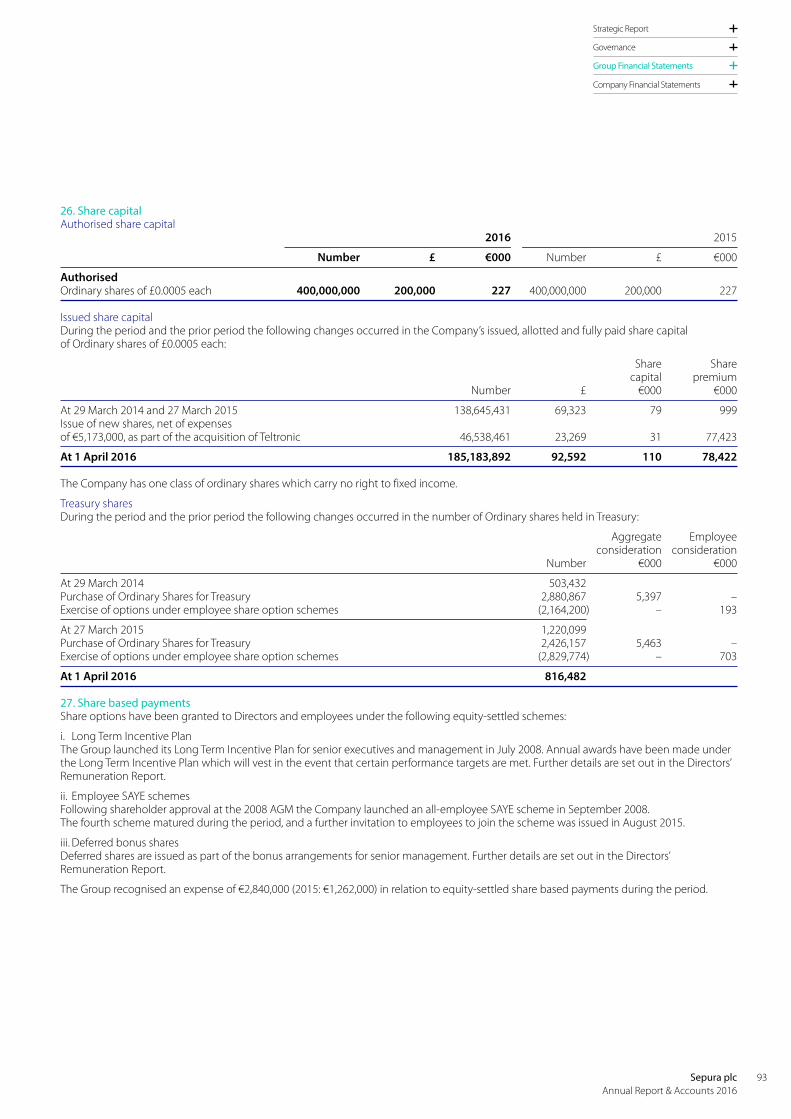

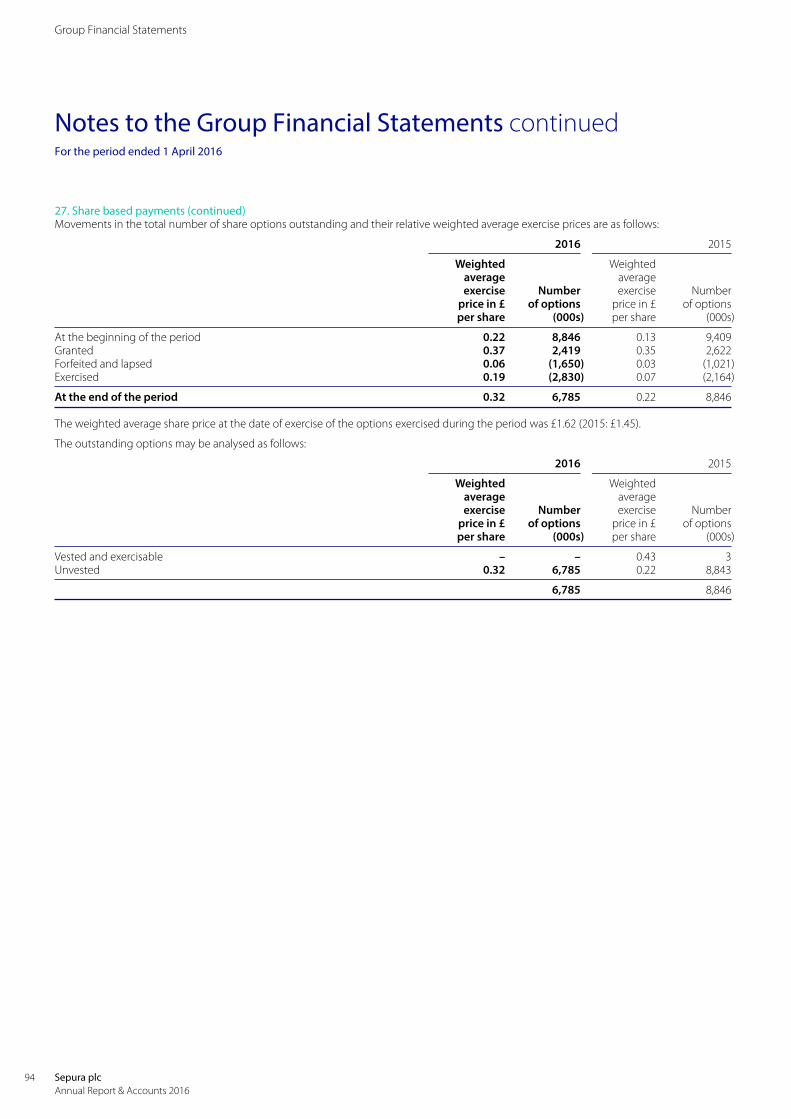

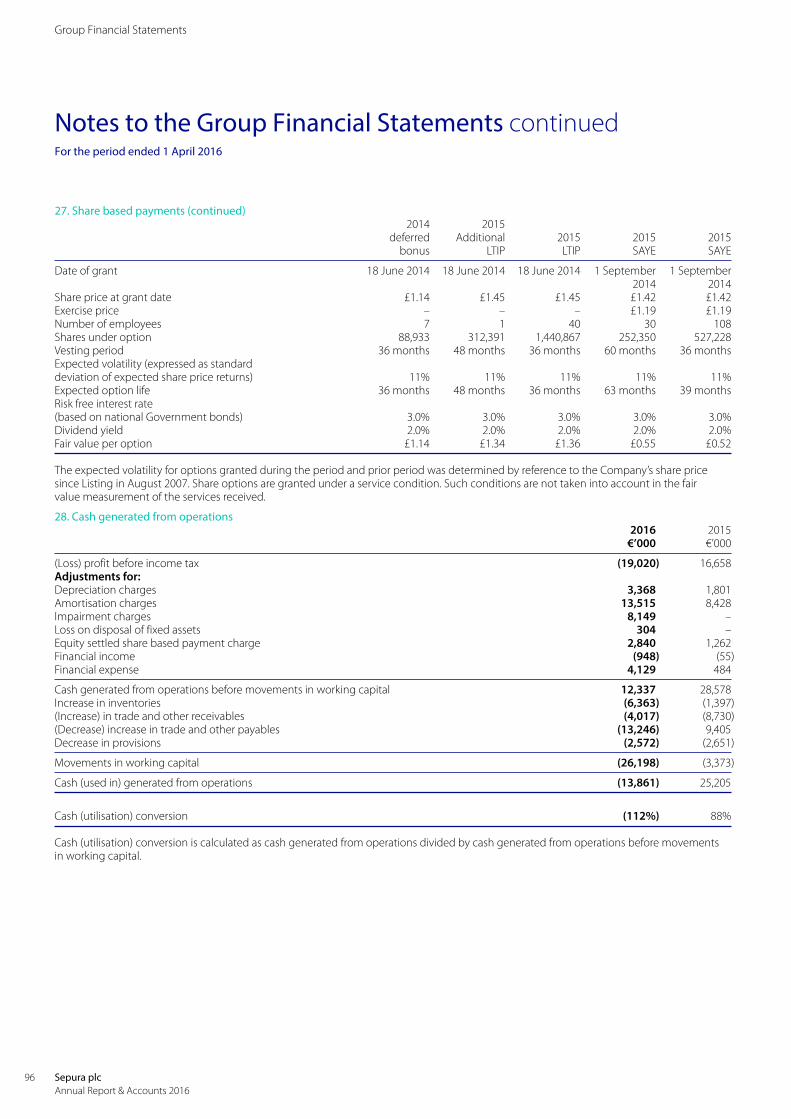

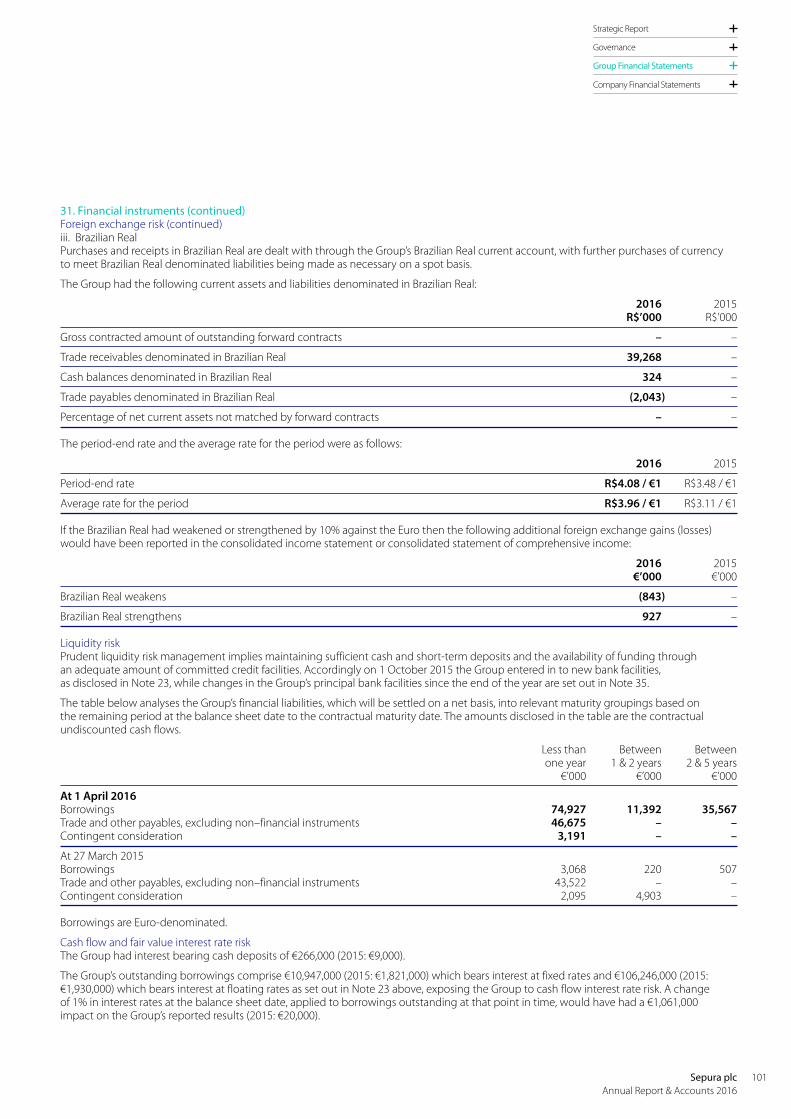

120

Sepura plc Annual Report & Accounts 2016 Tomorrow’ s communication today

Sepura plcAnnual Report & Accounts 2016

Tomorrow’s communication today

We are Sepura

Welcome

Sepura is a global leader in the design, development and supply of digital radio solutions, complementary accessories, support tools and devices.

On the coverSepura’s solutions deliver robust and reliable communications 24/7 in over 100 countries. We help our customers overcome the operational challenges that they face every day as they keep the public safe and secure.

Sepura plc Annual Report & Accounts 2016

Read more about our products on pages 12 to 13

Read more about how the industry is changing on pages 10 to 11

Read more about how we run our business on pages 8 to 9

Welcome

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Strategic ReportWelcome 01Where we do business 02What we’ve been up to 04Chairman’s Statement 06How do we run our business? 08How is the industry changing? 10What sets us apart? 12How are we performing? 14Operational Review 16Financial Review 20What challenges do we face? 23Corporate Social Responsibility 26

Governance Corporate Governance Report › Our Board and Senior Management 30 › Introduction from our Chairman 32

Report of the Audit Committee 36Directors’ Remuneration Report › Annual Statement 38 › Remuneration Policy Report 40 › Annual Report on Remuneration 45

Directors’ Report 52

Group Financial StatementsIndependent Auditors’ Report to the Members of Sepura Plc 56Consolidated Income Statement 64Consolidated Statement of Comprehensive Income 65Consolidated Statement of Changes in Equity 65Consolidated Balance Sheet 66Consolidated Statement of Cash Flows 67Notes to the Group Financial Statements 68

Company Financial StatementsIndependent Auditors’ Report to the Members of Sepura plc 103Company Balance Sheet 105Company Statement of Changes in Equity 106Notes to the Parent Company Financial Statements 107

Shareholder Information 114Contact Details and Advisers 115Financial Calendar 2016/17 116

“Sepura’s 2016 Annual Report sets out the strategy of the Group, including the markets in which the Group operates, and how the Group addresses those markets through product innovation and customer service.

It also presents the Group’s results for the year, explaining progress towards our long-term goals and setting out the challenges for the year ahead. I hope that you find it informative, and I look forward to reporting further progress in 2017.”Russell KingChairman

Our purpose

To help our customers overcome their operational challenges.

Our plan

To design, develop and supply the best possible solutions and products to both win new customers and then efficiently service their operational needs.

Our ambition

To build on our success as a world leading supplier of TETRA solutions, by expanding into more markets.

01Sepura plc Annual Report & Accounts 2016

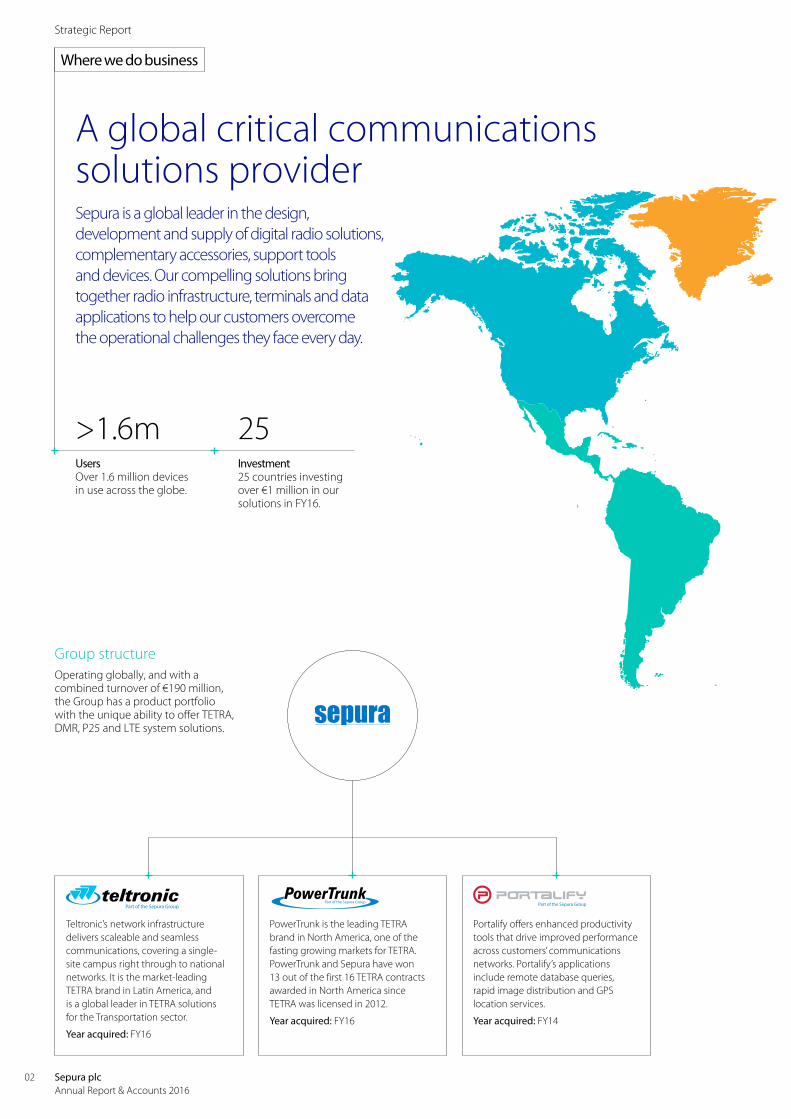

Where we do business

A global critical communications solutions providerSepura is a global leader in the design, development and supply of digital radio solutions, complementary accessories, support tools and devices. Our compelling solutions bring together radio infrastructure, terminals and data applications to help our customers overcome the operational challenges they face every day.

Group structureOperating globally, and with a combined turnover of €190 million, the Group has a product portfolio with the unique ability to offer TETRA, DMR, P25 and LTE system solutions.

Teltronic’s network infrastructure delivers scaleable and seamless communications, covering a single-site campus right through to national networks. It is the market-leading TETRA brand in Latin America, and is a global leader in TETRA solutions for the Transportation sector.

Year acquired: FY16

PowerTrunk is the leading TETRA brand in North America, one of the fasting growing markets for TETRA. PowerTrunk and Sepura have won 13 out of the first 16 TETRA contracts awarded in North America since TETRA was licensed in 2012.

Year acquired: FY16

Portalify offers enhanced productivity tools that drive improved performance across customers’ communications networks. Portalify’s applications include remote database queries, rapid image distribution and GPS location services.

Year acquired: FY14

UsersOver 1.6 million devices in use across the globe.

Investment25 countries investing over €1 million in our solutions in FY16.

>1.6m 25

Strategic Report

02 Sepura plc Annual Report & Accounts 2016

Designing solutions Our deep expertise and experience enables us to combine terminals, systems and applications into solutions that address the operational challenges facing our customers.

Systems

DevicesWe provide a comprehensive portfolio of hand-held and vehicle radios that address the operational requirements of the most demanding users and environments.

Our network infrastructure delivers scaleable and seamless communications, covering a single-site campus right through to national networks.

Read more about our products on pages 12 to 13

Segments Description Revenue

Our international reach

Northern Europe › 68,000 radios for German

public safety

› Market leader in Germany, TETRA's largest market

› Eastern European order for > 5,000 ATEX radios

SEMEA › 63,000 radios to Saudi Arabia

› Multiple Teltronic network deployments across the Middle East

› First significant Portalify contract, in Sub-Saharan Africa

Latin America › Multiple Teltronic network

deployments across Brazil

› State-wide network for Sergipe in Brazil

› Further success in Mexico

APAC › Softer demand from Australian

extractive industries

› Teltronic network deployments across SE Asia

› Managed service contract with Singapore oil facility

UK&I › Market-leader in TETRA's

most mature market

› Increasing number of commercial opportunities

North America › 1,000 terminals delivered to Toronto

Transit for deployment on Sepura infrastructure

› Canadian utility contract signed in October 2015

› New York transportation contract awarded in February 2016

Revenue by customer location

34% Northern Europe

32% SEMEA

18% Latin America

7% APAC

6% UK&I

3% North America

€65.0m

€124.7m

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

03Sepura plc Annual Report & Accounts 2016

Strategic Report

Sepura supplies Subsea 7 North Sea Spoolbase

Sepura, in conjunction with 1-2-3 Communication AS, has supplied TETRA terminals to the Subsea 7 North Sea Spoolbase in Vigra, Norway. The complete system comprises TETRA infrastructure, Sepura STP9000 hand-portable radios and a dispatcher solution.

Sepura launch revolutionary picture messaging solution; from control room to the field

Sepura has launched a new feature-enhanced version of its revolutionary IMAGE application, which allows the transfer of pictures from a control room to the mobile devices of field personnel.

Bavarian fire brigades choose Sepura

Two prestigious contracts have been awarded to Sepura's long-standing German partner, Selectric GmbH, for the supply of more than 6,000 TETRA radios to fire brigades in the regions of Straubing and Passau.

August 2015

August 2015 October 2015

Sepura completes the acquisition of Teltronic

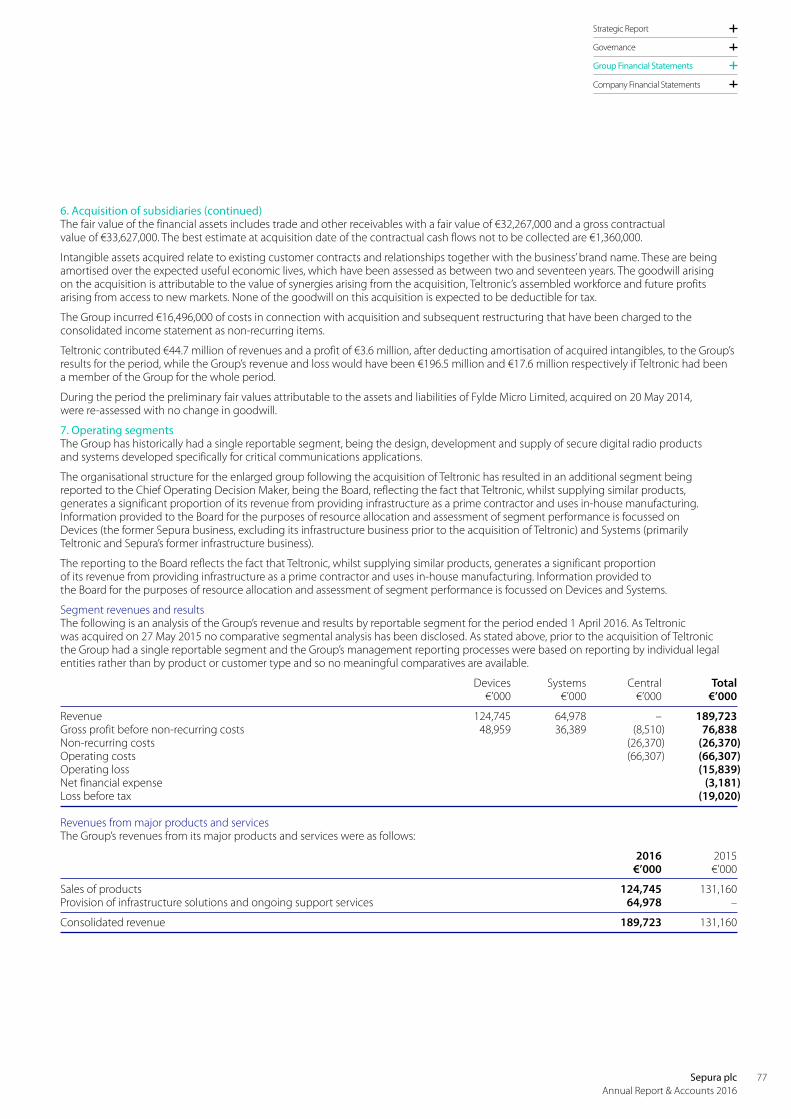

Sepura announced the acquisition of Spanish PMR company Teltronic, with its complementary product offering and strong brands in Latin and North America. Further details are set out on vvv in Note 6 to the consolidated financial statements.

May 2015

What we've been up to

Our year in review

During the year we have secured significant projects across the globe.

04 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Teltronic provides security-boosting TETRA-LTE solution for Bilbao Metro

The President of the Basque Country, Iñigo Urkullu, has inaugurated the latest phase of Teltronic's security-boosting communications network for Bilbao Metro, deployed in conjunction with ITELAZPI, operators of the Basque Country's regional communications network.

Sepura increases commitment to APAC region

Sepura has enhanced its operations in the Asia-Pacific region by investing in new prestigious offices in both Malaysia and Australia.

Teltronic selected for Qatar’s first tram system

Teltronic, part of the Sepura Group, has been chosen to provide a radio communications solution for Qatar's first tram system, part of the country's ambitious Education City project.

November 2015

“We are delighted that this project has had such a positive start.”

Ricardo Lizundia, TETRA Systems Manager at ITELAZPI

Sepura ships the SC20

First orders of the SC20 series, Sepura’s new flagship hand-portable radios were shipped in February. The SC20 series hand-portable radio is the first product to utilise Sepura's "Next Generation" platform and is resilient, intelligent and durable, providing intuitive operation and outstanding performance.

February 2016

March 2016

October 2015

05Sepura plc Annual Report & Accounts 2016

Strategic Report

Chairman’s Statement

Overview2016 was a year of considerable change and challenge as Sepura continued its transformation into a global supplier of critical communications solutions. The strategic acquisition of Teltronic, in May 2015, significantly expanded the Group’s geographical footprint in Latin America and enabled the Group to capitalise on further exciting early opportunities for TETRA in North America.

The core TETRA business delivered a record number of devices, the multi-year development programme on the Group’s “Next Generation” platform was completed and the UK offices were consolidated into new headquarters near Cambridge.

At the same time, the Group’s financial performance was adversely and materially impacted by a number of factors that have been, or are being, addressed.

The Group saw signs of softening in several important markets. The UK continues to be affected by uncertainty over the transition to the Emergency Services Network. Oil and gas markets in Russia and Australia remain subdued and weakness in the Brazilian economy is impacting ongoing projects.

Separately, the Group’s DMR and Applications businesses have not grown as rapidly as expected, and the strengthening Dollar has increased product costs. These factors, combined with two significant opportunities that did not close as expected at the end of the financial year, adversely affected adjusted EBITDA for the year. However, the Group was able to close the year with a record order backlog of €75 million.

Purchasing inventory for these delayed projects, slower than expected receipts from customers who have previously paid to terms, and additional costs associated with the acquisition and integration of Teltronic, contributed to a much larger than anticipated closing net debt position of €119.4 million.

Capital structureOn 27 April 2016 as a result of this higher than expected debt position, the Group announced it was in discussion with its debt providers and major shareholders concerning its level of indebtedness.

On 27 June 2016 the Group announced the Capital Raise which will reduce leverage and, in conjunction with amendments made to its main banking facilities, provide working capital for the Group as it continues to grow.

The Group has raised gross proceeds of approximately £65.0 million by way of a firm placing and placing and open offer of, in aggregate, 185,714,285 new ordinary shares at an offer price of 35 pence per new ordinary share. 124,258,224 new ordinary shares were issued through the firm placing and 61,456,061 new ordinary shares were issued through the placing and open offer on the basis of 1 new ordinary share for every 3 existing ordinary shares.

Management actionsIn conjunction with the review of the Group’s capital structure, Richard Smith, who joined the Board as Chief Financial Officer in January, is leading a comprehensive programme to drive operational improvement and strengthen cash management. The Group’s business model has also been reviewed in order to shorten the Group’s working capital cycle.

The Group’s focus will narrow to those markets and geographies where it is clear market leader and there are more immediate cash generating opportunities. It will continue to invest in markets such as North America, while significantly reducing activity in early-stage markets which require long-term investment before generating acceptable returns.

As part of this focus, the Group has now withdrawn from DMR in order to concentrate its resources on the more attractive opportunities for TETRA in the Transportation and North American markets.

At the forefront of digital radio technology

Russell KingChairman

The Group’s focus will narrow to those markets and geographies where it is clear market leader and there are more immediate cash generating opportunities.

06 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

The Board are taking action to improve revenue visibility and shorten the Group’s working capital cycle by reducing the revenue weighting to the final quarter of each financial year. This will reduce inventory levels and alleviate pressure to offer discounts or extended credit to customers to secure business at this critical time of year.

The Group will also reduce its credit exposure in emerging markets by only accepting business with lower levels of credit risk.

OutlookThese actions will result in some revenue being recognised later than previously expected. However, the Group will benefit substantially from the related working capital improvements.

In the light of the Group’s recent financial performance and the Capital Raising, the Board is not recommending a final dividend and will suspend dividend payments until it is appropriate for distributions to be resumed.

2016 has been a particularly challenging year for Sepura. The Board believes that the Capital Raising and revised banking arrangements will strengthen the Group’s capital structure and, in conjunction with the management team’s actions to improve working capital efficiency and expand margins, will reduce the Group’s net debt to EBITDA ratio towards the Board’s medium term target of 1.5x.

The Group closed the year with an order backlog of €75 million which did not include the two contracts which slipped from FY16. The strong pipeline of opportunities now totals €420 million. While it is expected that the management changes implemented will help with seasonality in the medium term, for FY17 the Board still expects that revenue will be weighted towards the second half of the financial year.

With an improved business model and robust capital structure, the Board is confident that the Group will be well placed to exploit its leading position in a number of fast growing global markets.

Russell KingChairman29 July 2016

2016 Financial performance › Group revenue €189.7 million (2015: €131.2 million)

– €44.7 million contribution from Teltronic

– 250,000 devices shipped, up 15% on FY15 (217,000)

– Record order backlog of €75 million

› Adjusted EBITDA1 €16.5 million (2015: €17.0 million)

› Adjusted operating profit1 €12.4 million (2015: €15.0 million)

› Pretax loss €19.0 million (2015: profit €16.7 million)

› Closing net debt €119.4 million (2015: €1.1 million)

– Net debt increase as a result of Teltronic acquisition and working capital

2017 Outlook › Capital structure revised to strengthen balance sheet

– Firm Placing, and Placing and Open Offer (the “Capital Raising”) raised gross proceeds of £65 million

– Debt facilities amended in conjunction with the Capital Raising

– No final dividend recommended (interim dividend paid of 0.79 pence per share)

› Management actions taken to revise business model - impacting FY17 financial performance

– Focus on geographies and verticals with market leadership

– Cost reduction programme well advanced

– Improve working capital efficiency and increased focus on cash generation

› Growth drivers intact

– Long-term structural drivers remain in Professional Mobile Radio (“PMR”) market through the transition to digital

– Transportation and North America remain growth areas

– Teltronic acquisition enhancing growth in key markets

Read more about our Key Performance Indicators on pages 14 to 15

1 The calculation of adjusted operating profit and IFRS operating profit are set out in Notes 8 and 15 respectively to the consolidated financial statements.

Unless otherwise stated, all comparative figures exclude the impact of the acquisition of Teltronic SAU that was completed during the period.

07Sepura plc Annual Report & Accounts 2016

Strategic Report

How do we run our business?

A framework for long-term growthOur vision is to establish Sepura as a global leader in the supply of digital communication systems.

Our strategy is designed to deliver sustainable growth, reduced risk and long term financial performance.

Design Outsource

Sell

Maintain

Refresh

Our business model

We continuously enhance our product and service offering to ensure that we have a broad portfolio of market-leading solutions. We have invested over €200 million in research and development, enabling us to secure a competitive advantage by being first supplier in our markets to offer GPS and Gateway and Repeater functionality, together with a wide range of other innovative product features and functions.

We outsource the manufacture of our products to world-class Contract Electronics Manufacturers, who offer a flexible and scaleable supply that meets our customers’ demand profile. We work closely with our supply chain to improve the design of our products, and to reduce costs and lead-times.

We sell direct in the UK, and have exclusive partnerships with a global network of dedicated PMR distributors, each of which is a specialist in their particular geography or market vertical. We work closely with them to target key opportunities, combining their local knowledge and relationships with our product expertise to create a compelling and cost-effective solution for end-users.

In conjunction with our local partners we support our installed base through additional accessories to meet users’ evolving operational needs together with the provision of warranty and repair services as required.

Customers typically replace fleets of devices after 5-7 years, accessing new features and functionality.

08 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Our strategic priorities

Developing a broad portfolio of market-leading solutions Innovation drives the digital PMR market as users operate in extremely challenging environments, such as mines and factories, and so require increasingly rugged and robust devices. Products must have an operational life of between five to seven years and withstand shock and dust or water ingress.

Users also require a wide ecosystems of accessories and tools that help them address their evolving operational challenges, and are therefore looking at emerging technologies such as 4G/“LTE” to deliver broadband data as well as traditional voice communications.

› We have invested over €200 million over the last 10 years

in research and development, and the Group currently employs over 300 R&D personnel dedicated to helping our customers succeed.

› Our investment has enabled us to secure a competitive advantage by being the first supplier in our markets with improved products and critical functionality, together with a wide range of other innovative product features and functions.

› For example, during the year the Group launched the SC20, the first product to utilise Sepura’s “Next Generation” platform and incorporate a high speed data bearer, making it the first TETRA hand-portable which can claim to be LTE data ready.

› Our broad portfolio of market-leading products ensures

we can support our customers as their needs evolve during the life of their network.

› We carefully select our local partners, based on their expertise and local knowledge, to ensure that they can provide the highest possible levels of customer service.

› The result is a demonstrable track record of customer retention and the repeat business that flows from establishing Sepura as our customers’ supplier of choice.

› Our broad portfolio of market-leading products that

includes solutions tailored for high-growth markets, such as our Transportation solutions.

› Our long-term relationships with the right partners who help us identify local trends and country-specific requirements that are incorporated into our product development roadmap.

› Our global presence, comprehensive market understanding and thought-leadership ensures we are at the forefront of the PMR analogue to digital migration.

Targeting high growth opportunitiesNot every vertical within the PMR market is growing at the same rate. While public-safety users constitute the largest vertical, many national digital PMR networks are now in place. The current wave of new networks is driven by commercial users, especially in the Transportation vertical and in North America.

We are continually identifying complementary high-growth opportunities within the PMR market which can be addressed by our core competencies and:

› grow our geographical footprint › broaden our product portfolio › enter new market verticals › offer a range of PMR standards.

Building long-term customer relationshipsA typical PMR network will be operational for at least 20 years. In addition to the initial capital purchase of infrastructure, applications and terminals, customers require regular supplies of batteries and other ancillaries which generate strong recurring revenues over the lifetime of the network, or require additional software licences as the number of end users on a network increases.

The challenge Our response

09Sepura plc Annual Report & Accounts 2016

Strategic Report

How is the industry changing?

The PMR market today

The PMR market today is fast paced and challenging, with key trends such as innovation and regulation driving the migration to digital PMR.

Key trendsIdentifying opportunities for growth.

Professional Mobile Radio Digital PMR market growth

Terminal installed base (m)

0

10

20

30

40

50Analogue

Digital

11 1513 1712 1614 18 19

InnovationDigital PMR technologies offer users additional benefits over analogue and alternative technologies including

RegulationsGovernments are mandating an “analogue to digital migration” as they are for other markets such as television and radio, as they need

Commercial driversAnalogue components are becoming obsolete and expensive to maintain, while Digital PMR offers users

› Instantaneous group communication › Enterprise-class accessory ecosystem › Location tracking and automated

database queries

› Increased spectrum efficiency › Interoperability across user groups

and agencies › Enhanced security and functionality

› Low cost of ownership › Rugged and robust products that

operate in the harshest environments › Productivity tools that maximise

return on investment

Professional Mobile Radio (PMR) is the term used to describe the form of two-way radio communications used by many public safety and commercial organisations around the world. As at 31 December 2015 an estimated 44.4 million PMR users were communicating over PMR radio networks, generally through two-way radios that are either carried by individuals or installed in vehicles or control rooms. Organisations that utilise PMR networks generally operate over a wide geographical area with multiple users co-ordinated from a central control room and so require instant communication between individuals or pre-defined user groups.

Estimated PMR users communicating over PMR radio networks as at 31 December 2015.

Estimated total PMR market value by 2017.

44.4m

$16.5bn

10 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Our solution

Our response is to offer a broad portfolio of innovative products supported by exceptional customer service.

UKAll 43 police forces in England and Wales

Supplier of over 99% of covert radios in the UK

Exclusive supplier to the Department of Health

GermanyLargest TETRA market with c. 560,000 registered public safety users

97% of the country now covered

68,000 public safety radios delivered in FY16

GlobalIn 2016, international revenues went up by 58% to €178 million

25 countries generated over €1 million of revenue (2015: 21 countries)

Major market leadersWe are the market-leader in over 30 countries.

Addressing a growing market

Sepura devices in use world-wide (m)

0

0.2

0.4

0.6

0.8

1.2

1.4

1.0

1.6

07 1109 1308 12100503 0604 14 15 16

#1 supplier public safety worldwide

#1 supplier all users EMEA

Sepura spun out, focused

on TETRA

Transforming Sepura into a robust and diversified businessCreating a robust and diversified business by responding to our marketplace.

Strengthening our core business › Maintaining terminal product leadership › Delivering operating cashflow

Expanding across the value chain › Launching our ATEX portfolio › Creating solutions including infrastructure › Developing our applications capability

Expanding into adjacent PMR standards › Leveraging Teltronic’s P25 portfolio › Developing a multi-standard capable

platform

Expanding into adjacent market sectors Leveraging ATEX, infrastructure and applications › Expanding into North America

1

2

3

4

Our strategic acquisitions over the past 5 years

3T › May 2012 › Infrastructure capability

Portalify › July 2013 › Software applications

capability

Fylde › May 2014 › Enhances DMR offering

Teltronic › May 2015 › Increases geographical

presence, including PowerTrunk in North America

› Expands product portfolio

11Sepura plc Annual Report & Accounts 2016

Strategic Report

What sets us apart?

Our market leading productsWe help our customers overcome their operational challenges by offering a complete radio solution.

User organisations include: › Public safety › Transportation › Utilities › Government › Military › PAMR › Commercial & industrial › Oil & gas

TETRA

Why invest in digital radio solutions?

Reliable Communications are “mission critical“ and so users prefer their own network rather than relying on a shared or third-party network which may suffer degradation of service if too many users are accessing the network at the same time.

Robust Users operate in extremely challenging environments, such as mines and factories, and so require rugged and robust devices that can withstand shock and dust or water ingress, with an operational life of between five to seven years. Users also typically wear protective clothing and so require devices that can be operated without removing, for example, gloves or helmets.

Secure Private, encrypted networks reduce the risk that third parties eavesdrop on sensitive communications.

Group communications Users need to communicate simultaneously with multiple individuals without the need to dial, or the delay associated with establishing a connection on a commercial mobile cellular system.

Low cost of ownership Without monthly services fees, PMR radios offer a significantly lower total cost of ownership when compared directly to smartphones and other cellular connected devices.

Enhanced worker safety For scenarios where worker safety is critical, the always-on capabilities of PMR radios are invaluable.

Improved battery life and management A major requirement for business-critical communication solutions is a strong all-shift battery.

Better audio quality The level of ambient noise can render many mobile communications devices ineffective. The voice quality on PMR digital radios is enhanced by sophisticated software algorithms and background noise suppression.

Value adding features and functionality PMR radios offer additional integrated features such as GPS, text messaging and location tracking.

Enterprise-class accessory ecosystem Providing a variety of accessories, PMR radios offer a broad accessory portfolio closely aligned with enterprise use cases and target applications.

12 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Systems

Terminals

Applications

Productivity applicationsImage MessagingMessageQuery

Command & controlSICS-NET DispatchSICS-NET VisualiseSICS-DTT

Resource managementLocate-ServerLocateRadio Manager 2STProtect

Radio applicationsShort Data ApplicationsVirtual ConsoleWAPStop & Search

Network managementNetwork Management System

SecurityCDTCMCSKMS

Hand-portable radiosSC20 SeriesSTP8X SeriesSTP9000 SeriesSRH Series

Mobile radiosSRG3900HBCHBC2

Covert radiosSRC3300

Fleet managementRadio Manager 2

ModemSRB

AccessoriesSTP AccessoriesSRH3900 AccessoriesSTP8X AccessoriesSRG Accessories

Radio accessSoloFR400

Network coreeXtras FTS100eXtras FTG64 GatewaysCentral RecorderSecurity Management

Command & controlSICS-NET DispatchSICS-NET VisualiseSICS-DTT

Network managementNetwork Management System

Productivity applicationsImage MessagingMessageQuery

DispatchEmergency 112

Resource managementLocate-ServerLocateSTProtect

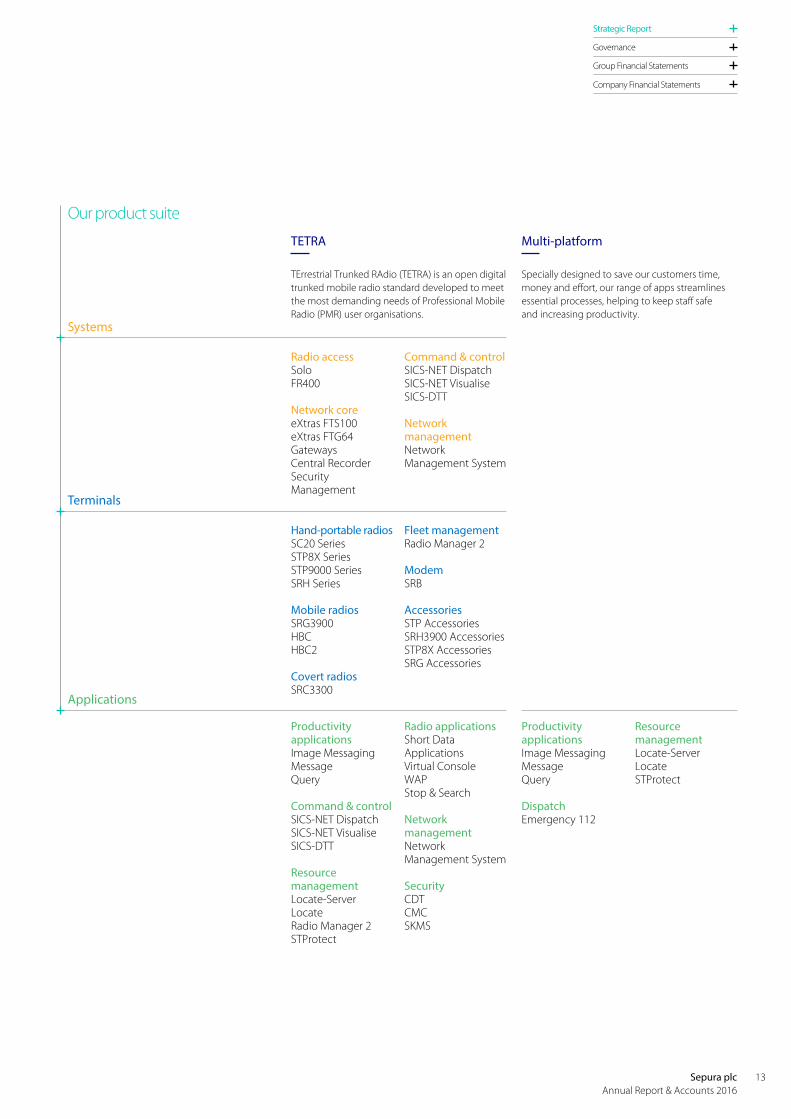

TErrestrial Trunked RAdio (TETRA) is an open digital trunked mobile radio standard developed to meet the most demanding needs of Professional Mobile Radio (PMR) user organisations.

Specially designed to save our customers time, money and effort, our range of apps streamlines essential processes, helping to keep staff safe and increasing productivity.

TETRA Multi-platform

Our product suite

13Sepura plc Annual Report & Accounts 2016

Strategic Report

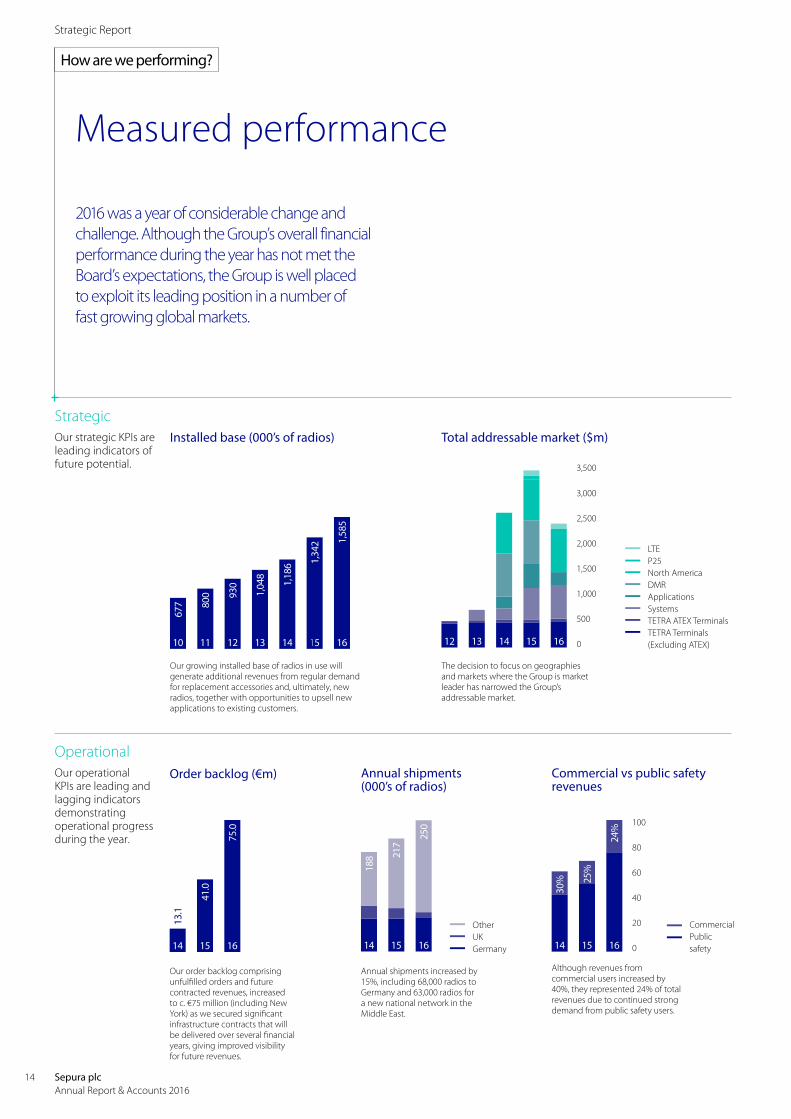

Installed base (000’s of radios)

StrategicOur strategic KPIs are leading indicators of future potential.

Our growing installed base of radios in use will generate additional revenues from regular demand for replacement accessories and, ultimately, new radios, together with opportunities to upsell new applications to existing customers.

The decision to focus on geographies and markets where the Group is market leader has narrowed the Group’s addressable market.

OperationalOur operational KPIs are leading and lagging indicators demonstrating operational progress during the year.

Order backlog (€m)

Although revenues from commercial users increased by 40%, they represented 24% of total revenues due to continued strong demand from public safety users.

Our order backlog comprising unfulfilled orders and future contracted revenues, increased to c. €75 million (including New York) as we secured significant infrastructure contracts that will be delivered over several financial years, giving improved visibility for future revenues.

Annual shipments (000’s of radios)

Annual shipments increased by 15%, including 68,000 radios to Germany and 63,000 radios for a new national network in the Middle East.

Commercial vs public safety revenues

How are we performing?

Measured performance

20

0

60

100

40

80

Total addressable market ($m)

14 1515

3,000

500

0

1,500

2,500

1,000

2,000

3,500

12 13 14 15 16

1616

24%

25%

30%

250

217

14

188

16

75.0

15

41.0

14

13.1

16

1,58

5

15

1,34

2

14

1,18

6

13

1,04

8

12

930

11

800

10

677

Other UK Germany

Commercial Public

safety

LTE P25 North America DMR Applications Systems TETRA ATEX Terminals TETRA Terminals

(Excluding ATEX)

2016 was a year of considerable change and challenge. Although the Group’s overall financial performance during the year has not met the Board’s expectations, the Group is well placed to exploit its leading position in a number of fast growing global markets.

14 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

1 The calculations of adjusted operating margin and adjusted diluted EPS, together with an explanation of why they are relevant measures, are set out in Notes 8 and 15 to the consolidated financial statements respectively

2 Calculated as cash generated from (or used by)operations divided by cash generated from (or used by) operations before movements in working capital

Revenue (€m)

Adjusted diluted EPS (¢)1

Adjusted operating margin1

Dividends per share (p)

Cash conversion (utilisation)2

FinancialOur financial KPIs are lagging indicators showing the financial result of our operational performance.

We delivered a fourth consecutive year of organic double-digit revenue growth, together with incremental revenues from Teltronic.

The reduced operating margin, together with additional interest on extra borrowings, resulted a reduction in adjusted EPS for the year.

Adjusted operating margin was adversely impacted by foreign exchange, high-volume/low-margin contracts and delays to significant contracts that were expected to be delivered in March 2016.

In the light of the Group’s recent financial performance and the recent new equity, the Board has not recommended a final dividend and so the dividend for the year is the same as the interim dividend already paid.

An expansion of working capital due to increased inventory purchased to satisfy delayed contracts, together with slower than expected receipts from customers, meant the group did not generate any operating cash during the year.

14

14 14

14

14

15

15 15

15

15 16

16

16 16

16

189.

77.

2

0.79

6.5%

(112

%)13

1.2

9.7

2.40

11.4

%

88%

116.

68.

4

2.00

10.7

%

101%

15Sepura plc Annual Report & Accounts 2016

Strategic Report

Operational Review

Shaping the future of digital communicationsThe Group now has an installed base of approximately 1.6 million TETRA devices in 120 countries, that generates a growing stream of recurring revenues as users refresh existing fleets and acquire accessories and applications to maximise the return on their investments in the Group’s technology.

Although the Group’s overall financial performance during the year has not met the Board’s expectations set earlier in the year, the Group reported a fourth consecutive year of double-digit growth in organic revenues as it continued to benefit from its leading position within the growing digital PMR market.

The acquisition of Teltronic SAU (“Teltronic”) during the year added additional scale, geographical reach and product capability that positions the Group for further success in its chosen markets.

The Group has also made significant investments in organic product development, premises, people and technology which are expected to deliver operational efficiencies and strengthen operating margins in future.

Long-term structural growth within the PMR marketThe world-wide PMR market continues to grow, with the estimated total spend by PMR users expected to reach $16.5 billion by 2017. Digital PMR technologies, such as those provided by the Group, currently account for an estimated 38% of the current 45 million PMR users today, with a further 11 million PMR users forecast to migrate to digital by 2019.

TETRA is a proven technology with an estimated 3.7 million users in over 100 countries at 31 December 2015. TETRA supports public safety users around the globe at critical moments where secure and effective communication helps to keep users and the public safe and secure.

While governments and public safety agencies were the principal early adopters of TETRA, increasing numbers of commercial organisations are now adopting TETRA for their own communication networks.

Transportation is the largest market for TETRA after public safety, with the demands arising from the mass movement of people sharing many of the requirements of public safety markets. Solutions for Transportation customers typically include a high infrastructure content including control rooms, signalling and telemetry applications and driver interfaces.

Sustained demand from TETRA devices marketsThe Group’s shipments of devices increased by 15% to 250,000 (2015: 217,000), reflecting further adoption of TETRA world-wide in emerging TETRA markets such as Saudi Arabia, where the Group delivered 63,000 devices under the contract secured last year.

The Group now has an installed base of approximately 1.6 million TETRA devices in 120 countries, that generates a growing stream of recurring revenues as users refresh existing fleets and acquire accessories and applications to maximise the return on their investments in the Group’s technology.

Volumes in Germany were up 5% to 68,000 (2015: 65,000) devices, reinforcing the Group’s market leadership in the world’s largest TETRA market. The initial deployment of the national TETRA network in Germany is nearing completion, and the contracted backlog at the end of the year was for 36,000 devices. The number of new users is expected to decrease in the coming year in line with the overall deployment plan while initial users are expected to commence their first refresh of devices.

The Group’s shipments of devices increased by 15% to 250,000 (2015: 217,000).

The estimated total spend by PMR users is expected to reach $16.5 billion by 2017.

+15%

$16.5bn

16 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Radios delivered(000's)

0

50

100

150

200

250

14 1615

250

217

188

17Sepura plc Annual Report & Accounts 2016

Strategic Report

“Teltronic has accelerated the delivery of the Group’s strategic objectives, and made a significant contribution to Sepura’s progress.”

Acquisition of TeltronicThe acquisition of Teltronic, a complementary Spanish PMR business, was completed in May 2015. Teltronic has accelerated the delivery of the Group’s strategic objectives, and made a significant contribution to Sepura’s progress:

› Scale – Teltronic contributed €44.7 million to revenues, and has a robust backlog of orders that improves revenue visibility.

› Global reach – Teltronic’s strong presence in both Latin and North America has significantly increased the geographical diversity of the Group’s business. Revenues from Latin America increased by 604% to €33.8 million (2015: €4.8 million), and revenues in North America by 227% to €7.2 million (€2.2 million).

North America remains at an early stage of development, but the Group continues to promote TETRA with commercial users, especially in the Transportation sector. This culminated in the decision by New York City Transit to deploy a Sepura TETRA network which will be delivered over the next three years.

› End-user diversity – Teltronic’s comprehensive Transportation portfolio secured further important contracts in addition to New York. It is now the Group’s largest commercial vertical, representing 10% of total revenues in FY16 (FY15: 7%).

› Product offering and technical breadth – In addition to its specialist Transportation products, Teltronic also enhances the Group’s product portfolio through its early stage LTE and P25 products.

Initial projects include integrating a mission-critical LTE network in the Canary Islands with its existing Teltronic TETRA network, reflecting a wider trend for the provision of broadband data over LTE in conjunction with established TETRA technology for voice communications.

› Synergies – The initial synergies forecast have been achieved. Synergies contributed €4 million of EBITDA compared to the €1.5 million originally forecast. Synergies are now expected to contribute €7 million of EBITDA in the current financial year.

Investment in products, premises and peopleThe Group has also invested in organic product development, with the completion of a multi-year development programme on its “Next Generation” platform. The first product to incorporate this platform is the SC20 radio, the first TETRA terminal to incorporate multi-bearer capabilities and thereby offer customers a flexible platform, which also has the ability to support both TETRA and emerging LTE technologies. Research & development remains critical to the future success of the Group and R&D expenditure represented approximately 12.8% of revenues for the period.

In January the Group completed the consolidation of its UK operations from four separate sites into its new headquarters in Cambridge. The new building will reduce operational expenditure and enhance productivity.

The Group has also strengthened its management team through the appointment of a new Chief Financial Officer, Chief Operating Officer, VP-Devices and VP-Marketing.

The initial benefits of these, and other investments made by the Group, are already being realised and are expected to make a significant contribution to Sepura’s future financial performance.

Operational Review continued

Teltronic contributed €44.7 million to revenues.

Revenues from Latin America increased by 604% to €33.8 million (2015: €4.8 million).

€44.7m

604%

18 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Business model reviewAfter four years of rapid growth a programme is underway to drive operational efficiencies, improve cash management and review certain aspects of the Group's standard terms of business which could shorten the working capital cycle.

In addition, the Board has undertaken a thorough review of the Group’s business model and explored ways of improving the cash generation of the business. The Board has determined to undertake the following measures:

› Improving sales phasing – the Group's revenue profile has historically been heavily weighted to the year-end, reducing visibility of earnings and necessitating increased inventory levels to support potential business. Reducing the Group's emphasis on year-end revenue by matching orders received from the Group's commercial partners to the delivery and payment schedules agreed with their end-users and placing restrictions on the approval of discounting arrangements and credit terms will provide better visibility of earnings and margin improvement;

› Aligning manufacturing timescales with customer delivery schedules – Teltronic has typically incurred certain costs relatively early in the contract period and recognised the associated revenues at that point. The Group intends to alter the Teltronic manufacturing process to manage working capital more effectively. As a result, product manufacturing will occur later in the contract period than is currently the case with a resultant impact on the timing of revenue being recognised. Aligning manufacturing timescales more closely to customer requirements will reduce stock holding and corresponding working capital requirements, shortening the Group's working capital cycle; and

› Reducing credit risk profile – active management of the Group's exposure of credit risk (including, where appropriate, aligning payment terms more closely to contract performance and/or product delivery and declining business until credit can be confirmed) will reduce exposure to delayed payment or non-payment of customer invoices.

While these initiatives will result in a one-off shift of revenue for the current financial year, the Group will benefit from working capital improvement and a better alignment of profitability to cash flows.

Withdrawal from DMRIn addition, the Board has undertaken a review of its DMR strategy. It now believes that it will not be possible to achieve further market penetration without significant additional investment. It has therefore decided to withdraw from the DMR market, instead allocating the Group’s resources to opportunities which are more immediately revenue and cash generative within the TETRA market, such as those within the North American region and the transportation sector.

Creating a more robust businessThe Board believes that, despite these measures having a one-off impact on short-term financial performance, they are in the best interests of the Group and will ensure a more robust business which delivers better visibility of revenue and improved cash conversion.

19Sepura plc Annual Report & Accounts 2016

Strategic Report

Financial Review

RevenueThe Group delivered revenues of €189.7 million, up 45% from last year’s €131.2 million and including a €44.7 million contribution from Teltronic. Organic revenues increased by 10%.

The total number of terminals shipped increased by 15% from 217,000 to 250,000.

Gross marginGross margin excluding non-recurring costs for the full year, was 40.5% (2015: 46.2%) while reported gross margin was 37.3% (2015: 46.2%). This reflected product and customer mix and the strengthening of the US Dollar compared to the Euro which increased product costs.

On a constant currency basis the gross margin for the year was 41.5% (2015: 46.2%). Gross margin excluding non-recurring costs strengthened as expected in H2 to 41.4% (H1: 39.5%) following the high-volume, low margin contracts delivered in H1.

Research and development costsGross expenditure on research and development increased by 30% to €21.8 million (2015: €16.8 million) following the acquisition of Teltronic, and represented 11% of revenues (2015: 13%).

Investment in research and development continued to focus on maintaining product leadership, with significant investment in the Group’s next generation platform of both terminals and infrastructure, culminating in the launch of the SC20 in May 2015.

Capitalised development expenditure represented 75% (2015: 78%) of related gross development spend. The related amortisation charge increased to €8.3 million (2015: €6.7 million) following the acquisition of Teltronic, the launch of the SC20 and a full year of amortisation of the Group’s investment in its DMR products.

Selling, marketing, distribution and administrative expensesSelling, marketing and distribution expenses, excluding non-recurring items, increased by 55% to €28.3 million (2015: €18.2 million), reflecting the additional sales resource acquired with Teltronic and investments made to expand the Group’s routes to market, especially in North America.

Administrative expenses, excluding the IFRS 2 share option cost, non-recurring items and the amortisation of acquired intangibles, increased to €16.7 million (2015: €10.7 million). The Teltronic acquisition accounted for 36% of this increase.

Foreign exchangeThe Group continues to be impacted by the volatility of both Euro/GBP and Euro/USD exchange rates. Adjusted operating profit on a constant currency basis, excluding the forecast impact of foreign exchange hedges, was €15.1 million, €2.7 million higher than that reported, after adjusting for the following items:

› Revenues would have been €1.3 million lower;

› Product costs would have been €3.0 million lower; and

› The Group’s unhedged Sterling operating costs would have been €1.0 million lower.

The Group continues to use forward contracts to sell Euros and buy Sterling to meet Sterling expenses that can be forecast with sufficient certainty as to timing and value to qualify for hedge accounting. This provides certainty as to the future Euro reporting value of these costs to the Group for the next 12 months.

The average hedge rate for the period was €1.280 / £1, based on prevailing rates during the prior year, compared to €1.190 / £1 for the same period last year which were in turn based on prevailing rates 12 months previously. As a result the Group’s hedged Euro operating costs increased by 7% compared to the prior year.

The hedges outstanding at the end of the period covered £25.0 million (2015: £27.4 million) of forecast Sterling cash flows at rates ranging from €1.281 – €1.422 / £1 (2015: €1.233 – €1.354 / £1), and with a weighted average rate of €1.343 / £1 (2015: €1.274 / £1) compared to the spot rate at the end of the period of €1.25 / £1 (2015: €1.367/ £1). The translation of the Group’s hedged Sterling cost base into Euros in the coming year will therefore result in higher reported Euro costs than those reported for FY16.

Building on a strong base

Record revenues of €189.7 million (2015: €131.2 million).

€189.7m14 15 16

189.

7

131.

2

116.

6

Revenue(€m)

“The Group delivered revenues of €189.7 million, up 45% from last year’s €131.2 million and including a €44.7 million contribution from Teltronic. Organic revenues increased by 10%.

The total number of terminals shipped increased by 15% from 217,000 to 250,000.”

20 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Operating profitThe Group presents adjusted Earnings Before Interest, Tax, Depreciation and Amortisation (“EBITDA”) and adjusted operating profit as key performance measures in addition to the operating profit reported under IFRS. The Group considers that the exclusion of certain non-recurring or non-cash items provides an alternative measure of the underlying trading performance of the Group.

Adjusted EBITDA and adjusted operating profit were €16.5 million and €12.4 million (2015: €17 million and €15.0 million) respectively. EBITDA was €1.0 million (2015: €27.3 million) and the operating loss was €15.8 million (2015: operating profit of €17.1 million).

Non-recurring itemsThe Group has incurred a number of non-recurring items in the current period, totalling €26.6 million (2015: €1.2 million) and comprising:

› €6.6 million of costs, primarily professional fees, in connection with the acquisition of Teltronic – see Note 3

› €11.1 million of restructuring costs relating to the combined Group

› €1.5 million of costs incurred in association with the Firm Placing, Placing and Open Offer

› €9.4 million of non-cash impairment costs against the Group’s investment in the DMR market, including a provision of €3.8 million against inventory

› €0.3 million write off of debt issue costs for facilities replaced in the period

› €0.3 million provision against outstanding receivables from a customer in Greece

› €2.6 million credit for the net release of contingent consideration payable for the previous acquisitions of Fylde Micro Limited and Portalify Oy.

Non-recurring items in the prior period related to initial costs incurred in connection with the acquisition of Teltronic (€0.9 million), the acquisition of Fylde Micro Limited (€0.5 million) and subsequent restructuring (€0.4 million), together with a provision against outstanding receivables from a customer in Greece (€1.8 million) and a credit for the net release of contingent consideration of €2.4 million.

TaxationThe Group continued to benefit from tax relief on qualifying research and development expenditure and elected to participate in the R&D Enhanced Credit (“RDEC”) scheme whereby a proportion of the cash spend on R&D in the UK may be recovered from the government and is accounted for as a government grant within operating activities. €3.3 million was receivable under this scheme at the end of the year.

EPSAdjusted diluted earnings per share, based on expensing development costs as they are incurred and excluding non-recurring items, the IFRS 2 share option charge, associated National Insurance and the amortisation of acquired intangibles, was 7.2 € cents (2015: 9.7 € cents).

IFRS fully diluted loss per share was 6.1€ cents (2015: earnings per share of 10.8 € cents).

Cash flows and financingNet debt at the end of the period was €119.4 million (2015: €1.1 million), reflecting primarily the facilities put in place to fund the acquisition of Teltronic.

The Group also experienced an expansion of working capital due to the procurement of inventory for customer orders which were not received at the end of the period, together with slower than expected receipts from customers who have previously paid to terms.

Slower debtor collection is in part a function of the Group's broader geographic diversity with some emerging markets experiencing challenging economic conditions which have impacted cash flows.

As a result the Group has been subject to short term cash constraints and discussions with its debt providers which have resulted in a waiver of year end covenants and amendments to the Group’s main banking facilities, including a bridging facility being made available prior to the receipt of the proceeds of the Equity Raise.

“Investment in research and development continued to focus on maintaining product leadership, with significant investment in the Group’s next generation platform of both terminals and infrastructure, culminating in the launch of the SC20 in May 2015.”

An increase of 30% to €21.8 million (2015: €16.8 million).1 As calculated in Note 8 to the consolidated

financial statements

€21.8m14 15 16

21.8

16.8

16.7

R&D gross expenditure1

(€m)

21Sepura plc Annual Report & Accounts 2016

Strategic Report

Following these amendments to the Group’s banking facilities, the Board retains its medium term target of net debt to EBITDA of around 1.5x as the Group’s annual average.

Significant non-operating cash flows related to:

› €122.0 million (2015: €3.4 million) paid for acquisitions, including €120.8 million for Teltronic

› €16.4 million (2015: €13.1 million) spent on capitalised development costs

› €12.0 million (2015: €5.2 million) of other capital expenditure, including €6 million in relation to the Group’s new headquarters near Cambridge

› €5.2 million of interest and arrangement fees payable in respect of the Group’s new banking facilities

› €6.4 million (2015: €3.7 million) paid in relation to FY15 final dividend and FY16 interim dividend

› €5.4 million (2015: €5.4 million) purchasing shares for Treasury

› €0.7 million (2015: €0.2 million) received from employees exercising share options.

DividendsThe interim dividend already paid, was 0.79 pence per Ordinary Share (2015: 2.4 pence).

In view of the Capital Raising, the Board considers it appropriate to suspend the payment of dividends until further notice and will therefore not be recommending a final dividend in respect of the year.

The Board recognises that dividends are an important component of total shareholder returns and intends to resume dividend payments in the future once the financial position of the Group permits and subject to an appropriate level of dividend cover.

The balance sheetThe Group’s intangible assets increased from €66.6 million to €177.4 million primarily due to the acquisition of €116.9 million of intangibles with Teltronic, including €56.4 million of goodwill, and net capitalised R&D of €6.8 million.

The Group’s net assets increased from €84.6 million to €137.9 million, reflecting the additional equity raised during, and the result for, the period.

Share capitalThe Group purchased 2.4 million (2015: 2.9 million) shares to be held in Treasury in anticipation of future share option awards vesting, for total consideration of €5.5 million (2015: €5.4 million). 2.8 million (2015: 2.2 million) Treasury shares were utilised to settle options that vested and were exercised during the period, leaving 0.8 million (2015: 1.2 million) shares in Treasury at the end of the period.

A further invitation for eligible employees to participate in the Company’s SAYE scheme was issued in September, with options over 0.7 million (2015: 0.8 million) shares subsequently granted at an exercise price of 129 pence. Options were also granted to senior executives under the Company’s Long-Term Incentive Plan totalling 1.7 million shares (2015: 1.8 million). These will vest if targets relating to the period to 31 March 2018 are achieved.

Richard SmithChief Financial Officer29 July 2016

Intangible assets increased from €66.6 million to €177.4 million.

€177.4m14 15 16

177.

4

66.6

52.9

Intangible assets(€m)

Capitalised development costs increased from €13.1 million to €16.4 million.

€16.4m14 15 16

16.4

13.1

12.5

Capitalised development costs(€m)

Financial Review continued

22 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

What challenges do we face?

Clear and focussed strategy

The material strategic and operational risks and uncertainties facing the Group, their potential impact on our future performance, and how we manage them.

No change DownUp

Key to change in risk

Developing a broad portfolio of market-leading solutions

Building long-term customer relationships

Targeting high growth opportunities

Key to strategic link

Risk and impact Management strategy Change Strategic link

Technological changeOur revenue and profitability are affected by the extent to which there is increasing demand for, and development by our competitors of, additional products and product features. For example, the adoption of 4G/“LTE” for the delivery of broad-band data services to consumers has led some Public Safety agencies, including those in the UK, to explore the possibility of creating equivalent data networks, using either planned commercial networks or constructing their own 4G private networks. We make significant investments in new product development, and there can be no guarantee that we will be able to generate sufficient revenue to offset these development costs or to continue to make such investments. There are also associated risks relating to difficulties and delays in the development process of new products, and their acceptance by customers. If our competitors successfully launch new products or features which we are unable to match then we could lose market share with a corresponding impact on our future profitability and financial position.

Product innovationWhile the existing 4G standard does not contain the protocols necessary for voice traffic, or the call prioritisation and similar functions required by Public Safety agencies, we are investing in new product development to position the Group for the likely future deployment of LTE and our recently launched “Next Generation” SC20 products incorporate a high speed data bearer making it the first TETRA hand-portable which can claim to be LTE data ready. This is part of our ongoing programme of identifying customer needs, and potential competitor advances, to ensure that we maintain a portfolio of market leading products. We focus our development efforts on features which meet a market requirement and are likely to generate sufficient revenue to fund their development. We have established internal processes for prioritising and reviewing our development projects.

Reliance on key markets or customersA significant percentage of our revenue in each financial year is currently derived from a small number of end-user organisations, the majority of which are governmental organisations, in several key geographies.

The timing of orders from these customers is influenced by a number of factors, including governmental investment decisions which may be affected by changes in political and economic conditions. This makes accurate predictions of the timing of future revenues more difficult. In the event that there is a delay to either the tendering process or the placing of orders following a successful bid, then revenues may not be generated within the originally forecast timeframe, with a consequential impact on the profitability of the Group in any given period.

Growing our addressable marketThe Group’s focus on diversification will result in a reducing significance of individual contracts or customers relative to the Group’s total operations. Our addressable market has increased following the acquisition of Teltronic and we enter new markets. Furthermore, the increasing role of regular add-on and replacement business also helps to mitigate the impact of significant delays in securing new customers. However, the impact of significant contracts on half and full-year reported revenue remains a risk for the Group.

23Sepura plc Annual Report & Accounts 2016

Strategic Report

Risk and impact Management strategy Change Strategic link

Credit riskReliance on key markets or customers may also result in credit risk being concentrated within a small group of customers and default by a material customer could have a material impact on the Group’s results. Following the global expansion of the Group’s activities it now operates in countries and with customers that may give rise to higher credit risk exposure than that to which it has previously been exposed.

Working with the right partnersThe Board has implemented policies that require appropriate credit checks on potential customers and customer orders are checked against pre-set requirements before acceptance. Formal credit control procedures are applied subsequent to invoicing customers, with letters of credit and payments in advance obtained where appropriate. Such rigorous procedures cannot completely mitigate credit risk, and the Group provides against significant overdue accounts where recoverability of the debt is considered sufficiently uncertain. The maximum exposure to credit risk is limited to the carrying value of trade and other receivables.

CompetitionThere is strong competition in the markets in which we operate, particularly in relation to government procurement tendering processes which rely on a combination of technical performance and price. A significant reduction in the prices we achieve for our products could have a material impact on the Group’s margins and profitability.

Investing in product leadershipThe Group’s ability to compete depends on its high-quality product range and its reputation for customer service as well as the ongoing programme of work to reduce product costs. The Board regularly reviews the level of investment in these areas in the light of changes in the competitive landscape, to ensure that the Group can continue to compete effectively.

Managing rapid growthThe rapid growth of our business may place a significant strain on our management, operational and financial resources, and those of our manufacturing and distribution partners. If we are unable to grow our business profitably, as a result of being unable to secure adequate resources or incurring excessive costs in doing so, then this could have a material adverse effect on our financial position.

Investing in operational excellenceThe Board is continually reviewing internal controls and processes, and hiring additional employees in critical areas of the business where necessary. During the year the Group implemented an integrated ERP system which enhances internal controls and delivers operational efficiencies. The Group has two primary sub-contract manufacturers, ensuring continuity of supply and providing flexibility in meeting additional demand for our products.

Managing working capitalA specific consequence of rapid growth could be a need to invest in additional working capital, either through holding extra inventory or offering extended credit terms to customers. If this additional working capital did not convert into cash on a timely basis, the Group might need to secure additional funding to meet its short-term cash requirements.

Securing adequate financingThe Board has undertaken the recent Capital Raise to strengthen the Group’s balance sheet and, in conjunction with the Group’s banking facilities, provide additional working capital for the Group as it continues to grow. The Board has also established regular reviews of the Group’s cash position and forecast cashflows to ensure adequate headroom is in place for the Group’s operational requirements.

What challenges do we face? continued

24 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Risk and impact Management strategy Change Strategic link

Foreign currencyThe Group has an international customer base and purchases products and services in a range of currencies. The reported revenues, costs, assets and liabilities of the Group are therefore affected by fluctuations in prevailing rates of exchange between these currencies. This affects comparisons of current year results to previous periods, where equivalent underlying transactions are reported at differing rates, and may affect future results if assets and liabilities are subject to revaluation over time.

Effective hedging of exchange rate exposuresThe Company’s presentational and functional currency is the Euro, reflecting the relative contribution of Euro-denominated revenues. The Board has implemented policies that require regular reviews of the Group’s forecast currency requirements, in conjunction with a rolling programme of monthly forward contracts to hedge forecast net cash flows in major currencies. Where these hedges are deemed to be effective any unrealised gains or losses on the hedges are recognised in equity rather than in the consolidated income statement, again reducing possible volatility in reported earnings arising from changes in exchange rates. Furthermore, following the acquisition of Teltronic the Group’s GBP revenues and costs are falling as a proportion of the Group’s overall activities while increasing USD revenues from the growing North American market provide a natural hedge against USD product costs.

Information securityThe Group regards information within the business as a key asset and recognises the risk and impact on the business of breaches to the integrity of information relating to the business.

Effective protection of information security and integrityThe Group has in place systems and processes for the classification and control of access to information within a number of elements of the business. The information security standard ISO27000 is a reference frame for all information security management systems and is the framework against which the Group manages information security.

Supply chain risk and product recallWe are dependent on outsourced electronic manufacturing companies for the manufacture of substantially all of our current products and on a small number of suppliers for key components. Any failure or inability of these companies to supply us could adversely affect our business. Our supply chain is complex, and the use of third-party suppliers and service providers could adversely affect our product quality, delivery schedules or customer satisfaction. Any of these could have an adverse effect on our financial results.

Monitor manufacturing and component supply chainThe Group mitigates supply chain risk by employing a number of supplier monitoring mechanisms and control measures which address business viability, production quality and component obsolescence. Automated and manual product testing is an integral part of all projects and manufacturing. In addition, all third party products undergo conformance testing and compliance checks.

Integration of acquired businessesOur future financial performance will reflect the results of acquired businesses, which will in turn be impacted by our ability to integrate such businesses into our current operations. If we are unable to retain key employees or exploit forecast synergies then we may be unable to deliver the forecast level of revenues, profitability and cash flows which could have an adverse effect on the financial results and position of the Group as a whole.

Protection from vendors, combined with detailed planning and executionPrior to any acquisition the Group undertakes detailed investigation and due diligence in conjunction with external advisors. Appropriate warranties and indemnities are obtained from the vendors against specific financial risks identified. Where appropriate, an element of consideration is deferred and will only be satisfied if the acquired business generates the forecast level of profitability on which the valuation of the business was based. Detailed integration plans are prepared, with specific risks identified and mitigation plans prepared, which set out detailed actions, responsibilities and timetables. We conduct regular reviews with the management of acquired entities to assess performance against these plans and take action accordingly.

25Sepura plc Annual Report & Accounts 2016

Strategic Report

Sepura's community involvement

Sepura is the headline sponsor of the Cambridge United Community Trust, which was established in 2011 with the aim of positively influencing 10,000 children per year through a series of programmes for young offenders, children at risk of exclusion, ethnic minority groups, disability groups, the homeless and people living in areas of deprivation.

Our highly active social committee coordinates company-wide social and sports events and supports and promotes charitable initiatives undertaken by individuals, teams or departments.

This is why the Board, led by the Chief Executive Officer, takes CSR seriously and is committed to advancing our related policies, systems and initiatives across all areas of the business as we continue to grow and mature. These areas primarily include ethical behaviour, concern for employee welfare, health and safety, care for the environment and community involvement.

We make considerable efforts to communicate effectively with all stakeholders who may have an interest in our CSR activities, including our shareholders, customers, suppliers, partners and employees. The Company’s website is one of the main routes for providing information to interested parties and providing us with constructive feedback.

Ethical behaviourIn support of our core values of integrity, excellence, care, teamwork and commitment, Sepura expects that its business around the world is always conducted to high ethical standards of practice and legal principles. To that end, all our employees and business partners are also expected to demonstrate high standards of professionalism and integrity at all times when conducting business on the Company’s behalf. This is indeed how we behave in practice.

A Code of Business Conduct and Ethics (including a whistle-blowing policy) covering the whole of the business and our various stakeholder interests is in place and is regularly reviewed and reiterated to staff and business partners.

Corporate Social Responsibility

Maintaining Long-Term Value

Sepura recognises that a positive approach to Corporate Social Responsibility (“CSR”) can have a positive contribution to its reputation and the ability to create and maintain long-term value for shareholders.

26 Sepura plc Annual Report & Accounts 2016

Strategic Report

Governance

Group Financial Statements

Company Financial Statements

Human rightsThe Group respects all human rights and conducts its business in adherence to all relevant government guidelines, and takes all practical steps to ensure that its products are not supplied to organisations that may use them to advance terrorism, internal repression or otherwise abuse human rights.

EmployeesAs a business driven largely by technical development and innovation, our main assets lie in the talents and skills of the people we employ. Consequently, we aim to attract, retain and motivate the highest calibre of employees, both technical and non-technical, by encouraging and rewarding high performance through competitive remuneration and incentive arrangements. Sepura continues to be an “Investor in People” accredited employer.

Acknowledging that an environment that fosters innovation and collaboration is critical to our success, efforts are made to identify and provide further learning, training and development opportunities for our employees. These are structured so as to align our organisational objectives with personal career aspirations. Formal performance reviews, including 360° appraisals, are conducted annually.

Similarly, the importance of two-way communication is recognised, particularly as it relates to the business and its performance. We actively encourage employee involvement through a Staff Council and keep employees regularly informed of the Group’s activities and performance through team briefings, direct access to managers and Directors at all levels and by interim and year-end presentations to all staff.

During the period, and with a view to encouraging share ownership amongst its employees, the Company issued another invitation to employees to join an all-employee ShareSave Scheme in the UK. This Scheme, which is HMRC approved, enables employees to purchase shares in Sepura through regular savings made over a three or five year period but at a discount of up to 20% on the share price as determined at the outset. The Company intends to make an annual invitation under this Scheme and will from time to time consider its extension to other countries in which it has established a major operating presence.

Equality and diversityThe split of staff by gender at the end of the period was as shown to the right. Sepura is committed to providing equality of opportunity to all existing and prospective employees without unlawful or unfair discrimination. In addition, we are supportive of the employment and advancement of disabled persons. The Group gives full and fair consideration to the applications for employment from disabled persons, having regard to their particular aptitudes and abilities. Appropriate arrangements are made for the continued employment and training, career development and promotion of disabled persons employed by the Group.

Health and safetyWe are committed to protecting the health and safety of our employees, and third parties who visit our sites, as well as having a positive influence on our supply chain throughout the world.

We are legally compliant and, where appropriate, work to exceed these requirements to provide safe working environments and a robust programme of occupational health management.

Gender diversity

DirectorsSenior Managers

Other Employees

64

12846 555

Male Female

27Sepura plc Annual Report & Accounts 2016

Strategic Report

Corporate Social Responsibility continued

It continues to be the Company’s policy to offer staff free influenza injections and additional policy and contingency plans are in place in the event of any pandemic virus impacting staff health and business continuity. Notable health and safety risks to the business continue to be fire, electrical faults, soldering, manual handling, work station use, driving and stress. Employee travel to high risk geographies, due to the expanding diversity of the Group’s customer base is an identified risk across the business and as such we ensure employees have access to guidance specific to the region they are travelling in; vaccinations and travel advisories for example. The statutory testing of all equipment and appliances is up to date for all Group offices. H&S induction and necessary training is mandatory for all employees and regular work station risk assessments are carried out together with any remedial action necessary. Occupational workplace and medical examinations are carried out across the Group in line with local legislation.

To support this ethos, we use a Health & Safety Management System (OHSAS18001 Teltronic S.A.U.) which identifies risks. These risks are continuously monitored and reviewed, then eliminated or reduced with control measures which are communicated to all relevant stakeholders.

During the period in the UK there were no accidents reportable under the Reportable Injuries, Diseases and Dangerous Occurrences Regulations 2013; there were 6 non-reportable accidents (2015: 3). In Spain there was 1 accident reportable under the Reportable Injuries, Diseases and Dangerous Occurrences Regulations and 4 non-reportable accidents. Health and Safety Committees meet regularly, with responsibility for controlling, directing and delegating responsibility to line management and functional heads for the practical day-to-day compliance with the Group’s Health and Safety Policy Statements, other operating procedures and relevant legislation. Appropriate training is also coordinated by this Committee, together with an ongoing awareness programme for all employees to help create and maintain a safe and healthy working environment. Health & Safety is included as part of the Group’s internal audit cycle with periodic audits also undertaken by external bodies.