The Shale Gas Investment Guide is a magazine about Europe's unconventional oil and gas markets. This issue is about the United Kingdom UK and the cover story is about Frances Morris Jones, Anna McMaster and Victoria Merton, three professionals at work in the UK. Andrew CEO of iGas concludes with an piece about Europe's gas markets.

GUIDE S HALE GAS investment WINTER 2014 KEEP CALM AND FRACK ON th ACREAGE IS UP FOR GRABS IN THE UK, AS HOPES FOR A SHALE GAS BOOM HIT A HIGH. UK LICENSING ROUND WHO’S WHO: EU | REPUTATION IS EVERYTHING | ANDREW AUSTIN, IGAS | MARCELLUS BOOMING USA $32 | $30CAD | POLAND 100 PLN + VAT | EU €25 | UK £20

Transcript

sh

al

e g

as

inv

es

tm

en

t g

uid

e

win

te

r 2

014

Guide

Shale GaS investmentwinter 2014

KeeP CALMAnd FrAck On

thAcreAge is up FOr grAbs in the uk,

As hOpes FOr A shAle gAs bOOm hit A high.

uK liCensing rOund

who’s who: eU | rePUtAtion is everything | Andrew AUstin, igAs | MArCeLLUs BooMing

UsA $32 | $30CAd | PoLAnd 100 PLn + vAt | eU €25 | UK £20

Please visit our booth 32 at Shale Gas Europe 2013 in Warsaw!

p / 2 4 UKFOCUS• Turning Point, 2015• Fit for Purpose?• UK, the New Poland• Tough Road Ahead• Fracking’s Material Challenge• Hutton Energy• Reputation is Everything• Here comes the sun

p / 5 0 PrivateEquityinShortSupply

p / 5 4PGNiG: Down to Earth

p / 5 6Strategic Water

p / 6 4GlobalUpdate:EnemiesofNewOrder

p / 6 8Best technologies

p / 7 0Small-scale LNG

p / 7 2Release Gas, trap CO2

p / 7 4WHO’SWHO:EU

p / 9 4SERVICES DIRECTORY

p / 1 1 4Wellhead:AndrewAustin,IGas

CO

NT

EN

TS

110

PolandShaleCoalition

EUMarketUpdate

64GlobalUpdate

8 | Shale Ga S Inve S tm ent GuIde | winter 2014

Shifting Paradigm

B y w o j c i e c h k o ś ć

The hopes for a quick change that European shale gas might bring about have given way to a more sober view that the change will rather come at a pace typical for the oil and gas industry, which is slow.

opinion

With an easier permitting regime and land-owners profitting from whatever oil and gas companies could find on their land, it still took three decades for shale gas to transform America’s energy mix.

As shale gas plays like the Marcellus are far from depletion and technological advances allow frackers to go back to wells thought spent, gas from shales is going to flow. It is

now estimated that by 2025, the US will pro-duce more energy at home than it wi l l need, for the first time in close to 60 years.

The European op-erators look at the US as a country of refer-ence and never miss an opportunity to say what they would give for the EU to let go of procedures and the traditional govern-ment, rather than private, ownership of

mineral resources. But they are looking at the US, which is after a long period of develop-ment, while Europe is only just beginning.

The early excitement about the European - mostly Polish, now also British - shale gas was an effect of the rather unsophisticated applica-tion of knowledge about unconventionals

exploration amassed in America. The disap-pointment was then inevitable because Polish and UK shales are very different from US ones.

Those companies that have not given in yet, like San Leon Energy or Orlen Upstream, are now pretty open about the necessity to fine-tune fracking technology in order to tailor it to Polish geology.

They are also frank that it is going to take time. It might be a little less time in the UK, where the key shale play, the Bowland, is ten times thicker than the US’s Barnett and stretches along a mere 200 kilometers from West to East Midlands. This, according to market insiders, should bring answers to key questions sooner than in Poland.

There exists some pressure, however, to prove the European shale gas acreage sooner rather than later, as the chief supplier of many EU member states, Russia, has fallen out of favor with Europe, following its slow-motion inva-sion of Ukraine.

Given the EU’s most recent climate and en-ergy targets - 40 percent cut in emissions, 27 percent share of renewables in the mix, 30 percent improvement in energy efficiency - domestically produced natural gas could come in handy as a means to reduce the cost of en-ergy imports, while Europe marches toward decarbonization of its economy. An immediate leap to renewables seems unlikely at the mo-ment. Let gas - despite its fossil fuel credentials - play a role while it is still possible.

An immediate leap to renewables seems

unlikely at the moment. Let gas -

despite its fossil fuel credentials - play a

role while it is still possible

w w w.cle antechpol and.com | 9

EDiToR in CHiEFwojcIech KoSc

pUBLiSHERparKer Snyder

ART DiRECToRŁuK aSz ma zureK

ConCEpT DESignpaIGe weIr

pRinCipAL AnALYSTpIotr wdowInSKI

CoMMUniCATionSGabor chodKowSKI- GyurIcS

CopY EDiToRSmarynIa KruK, jo harper

HiRED! MAnAging EDiToRjan w ypIjewSKI

HiRED! WRiTERSr adeK budzowSKI, hubert K aron, pIotr lewandowSKI, edy ta Stopyr a , Gordon waSIlewSKI, dawId wIer zbIcKI

WRiTERSpaul Garret t In memorIam

nIlIma choudhury (london), Gabor chodKowSKI- GyurIcS, rhodrI davIeS (buenoS aIreS), davId GacS (buenoS aIreS), tIm GoSlInG (moScow, praGue), andrew hobbS (perth), mIrona hrItcu (buchareSt),

lInaS jeGelIvIcIuS ( vIlnIuS), StanISŁaw Koczot, jaKub Koczot, julIuSz Kowalcz yK, Ian lewIS (london), Sar a lIchwa (london), zuz anna marchant (london), nIKolay marchenKo (SofIa), jerIn mathew (banGalore),

wu mInG (beIjInG), nIchol aS newman (london), GreG penfold (cape town), Sonja van renSSen (bruSSelS), claudIa perez rIvaS (tex aS), Graham StacK (KIev ), domInIc SwIre (beIjInG), alIce trudelle (Quebec),

Gordon waSIlewSKI, jude webber (mexIco cIt y )

EXpERT ConTRiBUToRSolGa andrIenKo-bentz, jaceK cIborSKI, pIotr dobrowolSKI, florence Geny, GrzeGorz KuS,

drew leIfheIt, eva-marIa macIazeK, paweŁ poprawa, elena revutSKaya, wojcIech SŁowInSKI

gUEST CoLUMniSTSfr anK maIo, K athryn z. Kl aber, K amleSh parmar, andrew auStIn

KEY pHoTogRApHYlou denIm, Km r atSchK a , Konr ad SIeron, Sz ymon SzczeSnIaK

DTpma zureK Gr afIK a , www. ma zureKGr afIK a .pl

pRinTERdruK arnIa beltr anI, www.druK arnIabeltr anI.pl, Kr aKów,

DiSTRiBUTiontm medIa , al. jana pawŁ a II 61/239, 00 -117, warSaw

SUBSCRipTionthe Shale GaS InveStment GuIde IS prInted two tImeS a year. the maGazIne IS dIrect maIled to all lIcenSed

operatorS for unconventIonal oIl and GaS In the eu-28. to SubScrIbe, wrIte to [email protected].

pUBLiSHERcleantech pol and llc , ul. Krucz a 51/31, 00 - 022 warSaw, pol and

Guide

Shale GaS investment ma

st

he

ad

´

´

´

´

´‘

.

10 | Shale Ga S Inve S tm ent GuIde | winter 2013

To become a partner for the magazine, please contact

the publisher

CommercialpartnersThe American Chamber

of Commerce (AmCham) is a business organization that serves and promotes its member companies.

AmCham fosters positive relationships with the government

and promotes the free market spirit. www.amcham.com.pl

Cleantech poland is a consultancy for oil and gas

providing representation services. Cleantech Poland publishes the

Shale Gas Investment Guide and the magazine Cleantech.

www.cleantechpoland.com

poland Shale Coalition is an industry organization open to anyone. The Poland Shale Coalition, founded in 2013, aims at education

and outreach. Founding members of the Poland Shale Coalition receive

outreach in their concessions.www.shalecoalition.pl

DTZ is a property services company,

providing occupiers and investors with end-to-end property solutions, global and local market knowledge,

forecasting and trend analysis.www.dtz.pl

pwCPwC provides oil and gas companies with services in assurance, advisory

and tax & legal. A global services company, PwC has been in Poland

for 20 years and counts many of the largest oil and gas

companies as clients. www.pwc.pl

SSWSSW provides comprehensive tax and legal advisory services. SSW, whose main practice areas are energy and natural resources, advises investors on the business implications of the

government’s proposed changes to oil and gas laws.

www.ssw.pl

nutech is a U.S. based global oilfield

consultancy providing reservoir optimization and evaluation

services including optimization of existing wells.

www.nutechenergy.com

HAYSis the world’s leading company in

recruiting qualified, professional and skilled workforce. Hays Energy team is dedicated to serve energy, oil and gas; since its launch in 2007, the team has

covered 200 placements for middle and top management functions.

www.hays.pl

CH RoBinSonC.H. Robinson is one of the world’s

largest third party logistics (3PL) providers offering multimodal

transportation services and logistics solutions.

www.chrobinson.com

Risk to ReputationRisk to Reputation is an enterprise

risk consultancy for oil and gas that provides actionable and measurable

advice to senior management to hedge against unexpected outcomes.

For years, we support our clients with knowledge and market experience by providingbusiness advisory, tax and legal advisory, audit and accounting consultancy. We are happy to talk with you about the needs of your business.

B y P i o t r W d o W i ń s k i P r i n c i Pa l a n a lys t c l e a n t e c h P o l a n d

E X P E R T V I E W

w w w.cle antechpol and.com | 13

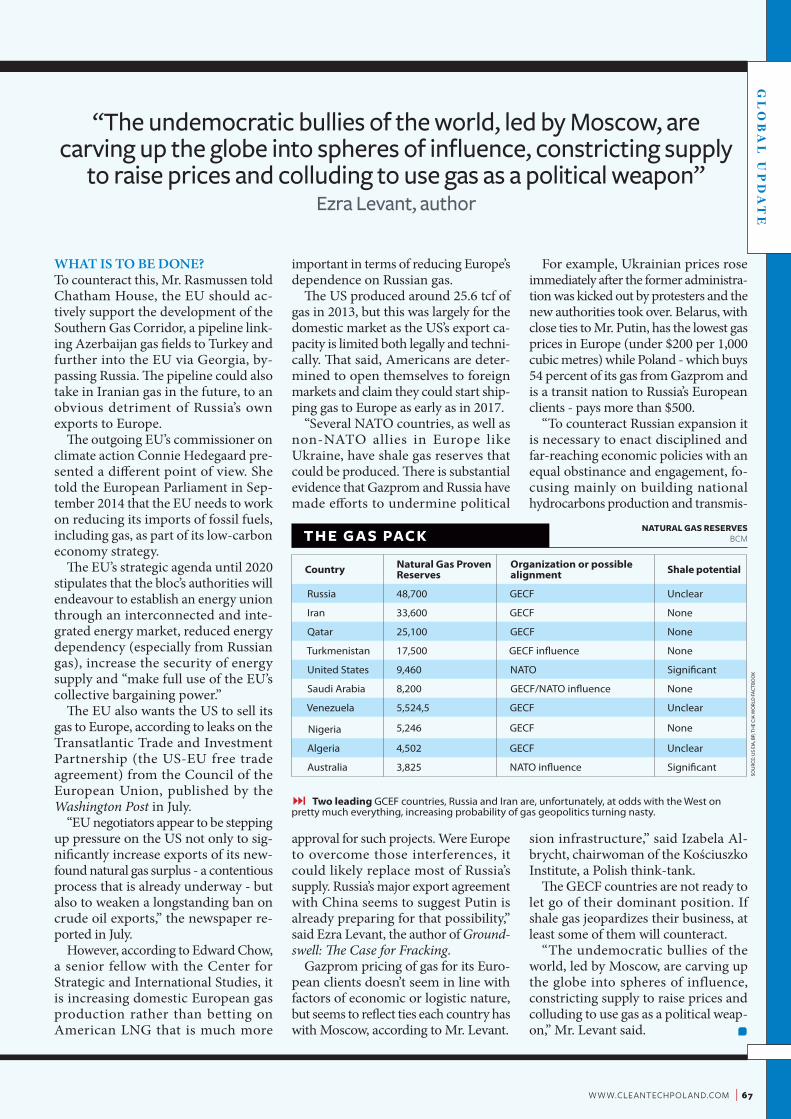

Source: cleantech Poland reSearch* TC - total concessions, NW - new wells (Q3, 2014)For detailed information about country specifics, please see "who's who section" on the page 74

M o s T a C T I V E E X P lo R E R sunconventional eu28 oil and Gas

BY COMPANY

� on top of the unimpressive pace of exploration in Europe to date, there lies a political question: what direction will the new European Commission (in office since November 1) give the EU in terms of development of its energy mix? The Commission will definitely want to address the issue of some €400bn that the bloc pays each year for energy imports, much of it for gas.

For years, we support our clients with knowledge and market experience by providingbusiness advisory, tax and legal advisory, audit and accounting consultancy. We are happy to talk with you about the needs of your business.

� Over the last half year, the number of European unconventional oil and gas wells drilled has increased, although the market in general is sluggish. The current hot spot is the UK: all eyes are on the upcoming results of the 14th onshore licensing round, expected to boost shale gas exploration on the back of esti-mated good geology in the Bowland play. Exploration in Poland is on-going but has been fading of late. On the other hand, Denmark will see its first shale gas well by Q1 2015, drilled by Total E&P Denmark and state-owned Danish North Sea Fund. Elsewhere in Europe, shale gas is hardly in favor with authorities, whom have a decisive say in getting exploration off the ground, as typically governments own the rights to mineral resources. The Netherlands and Ireland have both put a temporary ban on fracking ahead of further research, delaying decisions on drilling permits for unconventional oil and gas. Germany has introduced rigorous rules to regulate unconventional oil and gas that include a ban on coal bed methane and shale gas drilling up to 3000 meters deep until 2021. Bulgaria, France, Luxembourg and the Canton of Fribourg in Switzerland are also keeping moratoria on exploratory drilling. Exploration is stumbling in Northern Ire-land and Spain. In Poland, 3Legs Resources has decided to give up on its Baltic concessions after disappointing results from a production test at the Lublewo LEP-1ST1H well. San Leon Energy and ConocoPhillips continue to say publicly that they will continue works on their concessions. Other active operators are BNK Petroleum, Chevron and state-controlled PGNiG and Orlen Upstream.

company change in conc. Q1 - Q3 2014 country tc* nW*

iGas ↑ (+31) UK 38 1

egdon resources ↑ (+12) UK 23 -

Palomar natural resources ↑ (+3) PL 0 -

ineos ↑ (+2) UK 0 1

GdF suez sa ↑ (+25%) in 12 conc. DE, UK 16 2

conocoPhillips ↑ (+30%) in 3 conc. PL 3 -

total e&P uk ltd ↑ (+40%) in 2 conc(+50%) in 1 UK 0 -

aB igrene - SE 25 1

Gripen oil & Gas - SE 21 1

orlen upstream - PL 9 1

hutton energy - PL 3 -

BasF - Wintershall - DE 9 -

shesa - ES 5 -

total e&P denmark Bv - DK 2 -

nordsøfonden - DK - -

ascent resources - SK 1 -

cuadrilla resources ↓ (-1) PL, UK, NL 8 -

chevron ↓ (-1) PL, RO, (LT) 9 1

exxonMobil ↓ (-2) DE, (PL) 20 -

3legs resources Plc ↓ (-3) PL 3 -

PGniG ↓ (-4) PL 16 3

Bnk Petroleum inc ↓ (-5) PL, ES, (DE) 10 -

Petrolinvest ↓ (-6) PL 9 -

san leon energy Plc ↓ (-10) PL, ES, (DE), (SK) 26 -

dart energy ↓ (-31) UK 31 3

14 | shale Ga s Inve s tm ent GuIde | WINTER 2013 | shale Ga s Inve s tm ent GuIde | sUMMER 2013

T

I Ind c a t r soGuide

Shale GaS investment

14 | shale Ga s Inve s tm ent GuIde | WINTER 2014

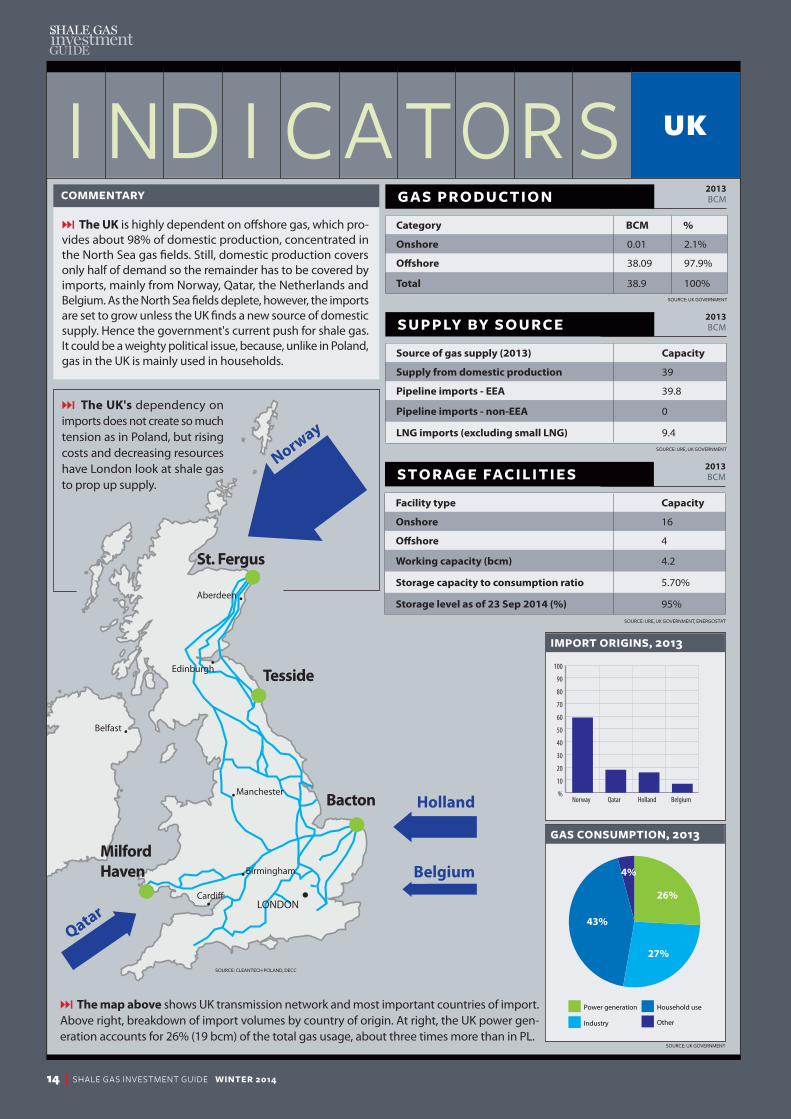

UK

� the uk is highly dependent on offshore gas, which pro-vides about 98% of domestic production, concentrated in the North Sea gas fields. Still, domestic production covers only half of demand so the remainder has to be covered by imports, mainly from Norway, Qatar, the Netherlands and Belgium. As the North Sea fields deplete, however, the imports are set to grow unless the UK finds a new source of domestic supply. Hence the government's current push for shale gas. It could be a weighty political issue, because, unlike in Poland, gas in the UK is mainly used in households.

CoMMENTaRy

PL-SK

PL-DE Lasów

PL-DE Mallnow(reverse)

PL-CZ

LNG Świnoujście

Cardi�

Belfast

59%

Edinburgh

Manchester

Birmingham

LONDON

Aberdeen

Łódź

Poznań

Wrocław

Rzeszów

Olsztyn

Gdańsk

Szczecin

WARSZAWA

Lublin

Bydgoszcz

KatowiceKraków

St. Fergus

Tesside

Bacton

MilfordHaven

Norway

Norway

Holland

Belgium

Qatar

Germany

Czech Rep.

existing

planned

Russia& CentralAsia

g a s P R o D U C T I o N

category BcM %

onshore 0.01 2.1%

offshore 38.09 97.9%

total 38.9 100%Source: uK Government

s U P P ly by s o U R C E2013 BCM

source of gas supply (2013) capacity

supply from domestic production 39

Pipeline imports - eea 39.8

Pipeline imports - non-eea 0

lnG imports (excluding small lnG) 9.4Source: ure, uK Government

s T o R a g E fa C I l I T I E s2013 BCM

Facility type capacity

onshore 16

offshore 4

Working capacity (bcm) 4.2

storage capacity to consumption ratio 5.70%

storage level as of 23 sep 2014 (%) 95%Source: ure, uK Government, enerGoStat

7%

47%25%

21%

26%

27%

43%

4%

Other

Household use

Industry

Power generation

Other

Household use

Industry

Power generation

gas CoNsUMPTIoN, 2013

Source: uK Government

� the map above shows UK transmission network and most important countries of import. Above right, breakdown of import volumes by country of origin. At right, the UK power gen-eration accounts for 26% (19 bcm) of the total gas usage, about three times more than in PL.

� the uk's dependency on imports does not create so much tension as in Poland, but rising costs and decreasing resources have London look at shale gas to prop up supply.

2013 BCM

Source: cleantech Poland, decc

w w w.cle antechpol and.com | 15w w w.cle antechpol and.com | 15

I Ind c a t r soGuide

Shale GaS investment

w w w.cle antechpol and.com | 15

� Poland is only slightly more dependent on gas imports than the UK, but the problem is that it is dependent on a historic enemy Russia, which has been viewed as unreliable political and business partner of late, following the crisis it instigated in Ukraine. In 2013, the country gas production covered approximately 30% of domestic demand. No less than a revolution in the supply structure might be on the cards, however. Poland wants to diversify supplies using an LNG terminal (7.5 bcm capacity), coming online in 2015, that will take gas under a signed contract with Qatar. Poland also hopes to develop its estimated 350-780 tcm of shale gas.

CoMMENTaRy

PL

g a s P R o D U C T I o N 2013 BCM

category BcM %

onshore 5.48 99.7%

offshore 0.02 0.3%

total 5.5 100%Source: PGniG, ure

s U P P ly by s o U R C E2013 BCM

source of gas supply (2013) capacity

supply from domestic production 4.4

Pipeline imports - eea 2.6

Pipeline imports - non-eea 11.87

lnG imports (excluding small lnG) 0Source: PGniG, ure

s T o R a g E fa C I l I T I E s2013 BCM

Facility type capacity

onshore 7

offshore 0

Working capacity (bcm) 2.5

storage capacity to consumption ratio 15.72%

storage level as of 23 sep 2014 (%) 99%Source: PGniG, ure

PL-SK

PL-DE Lasów

PL-DE Mallnow(reverse)

PL-CZ

LNG Świnoujście

Cardi�

Belfast

59%

Edinburgh

Manchester

Birmingham

LONDON

Aberdeen

Łódź

Poznań

Wrocław

Rzeszów

Olsztyn

Gdańsk

Szczecin

WARSZAWA

Lublin

Bydgoszcz

KatowiceKraków

St. Fergus

Tesside

Bacton

MilfordHaven

Norway

Norway

Holland

Belgium

Qatar

Germany

Czech Rep.

existing

planned

Russia& CentralAsia

7%

47%25%

21%

26%

27%

43%

4%

Other

Household use

Industry

Power generation

Other

Household use

Industry

Power generation

gas CoNsUMPTIoN, 2013

Source: PGniG, PGi

� in coal-reliant Poland, only 7% (1 bcm) of gas is used for power generation (left). Above left, breakdown of gas imports by country of origin. The map shows Poland's transmission network, existing/planned gas entry points, and LNG terminal in Świnoujście (operational from 2015).

� since april 2014, Po-land has been able to get gas from Germany (even though gas is Russian by origin) via a so-called real reverse mechanism, allow-ing Poland to pump gas via the Yamal pipeline.

Source: Pwc elaboration baSed on GaS inFraStructure euroPe

16 | shale Ga s Inve s tm ent GuIde | WINTER 201316 | shale Ga s Inve s tm ent GuIde | WINTER 2014

I Ind c a t r soGuide

Shale GaS investment

� During the hearings for the candi-date to the post of Energy Union Com-missioner, Maroš sefcovic, a lot was said about the EU’s dependence on energy imports, including gas. little talk, however, focused on one of the possible ways to reduce gas imports, that is, its extraction from European shales. What kind of policy from the new European Commission towards shale gas would you like to see?As we know, policy is first of all based on setting up an objective, which, in

the case of shale gas, will mean launch-ing its industrial production, and secondly on considering the most ef-fective methods leading to that goal. In the past, lobby groups in the Euro-pean Parliament did a lot to discour-age member states from unconven-tional natural gas resources. It seems, however, that the new commission will leave these issues at the discretion of member states, providing of course that they maintain EU environmental standards, both during exploration and future production. However, we must bear in mind that what we cur-rently know about shale gas in Poland does not provide much ground for consideration of shale gas resources as a factor in on Poland’s long-term gas import plans.

Complete studies are needed on Pol-ish geology and then economic analy-ses. And this is what I would like the future policy of the new European Commission to be.

� How do you think the gas market in Europe is going to change once t h e f l o a t i n g l N g t e r m i n a l i n Klaipeda and the lNg terminal in swinoujscie start operating? Will this enable the baltic countries and Poland to become less dependent on gazprom or will it rather be a argument for price reductions in purchasing gas from the Russian company?Liquefied gas, both from floating and at stationary LNG terminals, is always more expensive due to the technology

– first it is compressed, and then de-compressed. Besides, there are the costs of transporting LNG to countries that contract it. The possibility of us-ing imported LNG will definitely in-crease energy security, especially of the Baltic countries. But will this in-crease economic competitiveness? I am afraid it will not. I also fear it will not result in a price reduction of gas purchased from Russia. And it is en-ergy prices that determine, for the time being at least, competitiveness, not only in Poland but in the whole of the European Union on global mar-kets.

� How do you assess the EU emis-sions reduction target adopted at the end of october?These EU regulatory objectives mean a further tightening of the EU’s climate policy, or the reduction of carbon emissions, by at least 40 percent with 1990 as the baseline year, an increase in renewables’ share by at least 27 percent and an increase in energy ef-ficiency of up to 30 percent. The emis-sions reduction objective in the case of Poland, where GDP is below 60 percent of the EU average, will mean that the power industry will still be allowed to use free emission allow-ances. After 2020, however, it will account for no more than 40 percent of allowances verified after backload-ing has kicked in, which per account balance will necessitate the need to purchase allowances and potentially result in rising electricity prices.

E X P E R T I N T E R V I E W

sGiG speaks to Prof. adam Gierek, Mem-ber of the european Parliament for so-cialists and democrats and a member of the parliamentary committee of indus-try, research and energy. the eP has re-cently green-lighted the new european commission under the presidency of for-mer prime minister of luxembourg Jean-claude Juncker. the Juncker commis-sion, it appears, will attach great importance to the issues of european en-ergy, with the creation of a new portfolio for the commission’s vice president for energy union. the idea of the energy union is to make the eu a unified voice in issues such as energy imports, gas in particular, and to make the 28-country bloc’s effort to use less energy more ef-fective.

P r o F . a d a M G i e r e k

MEP, Group of the Progressive Alliance of Socialists and Democrats

“lobby groups did a lot to discourage member states from unconventional natural

gas resources. it seems, however, that the new commission will leave these issues at the

discretion of member states”

EU

w w w.cle antechpol and.com | 17w w w.cle antechpol and.com | 17

I Ind c a t r soGuide

Shale GaS investment

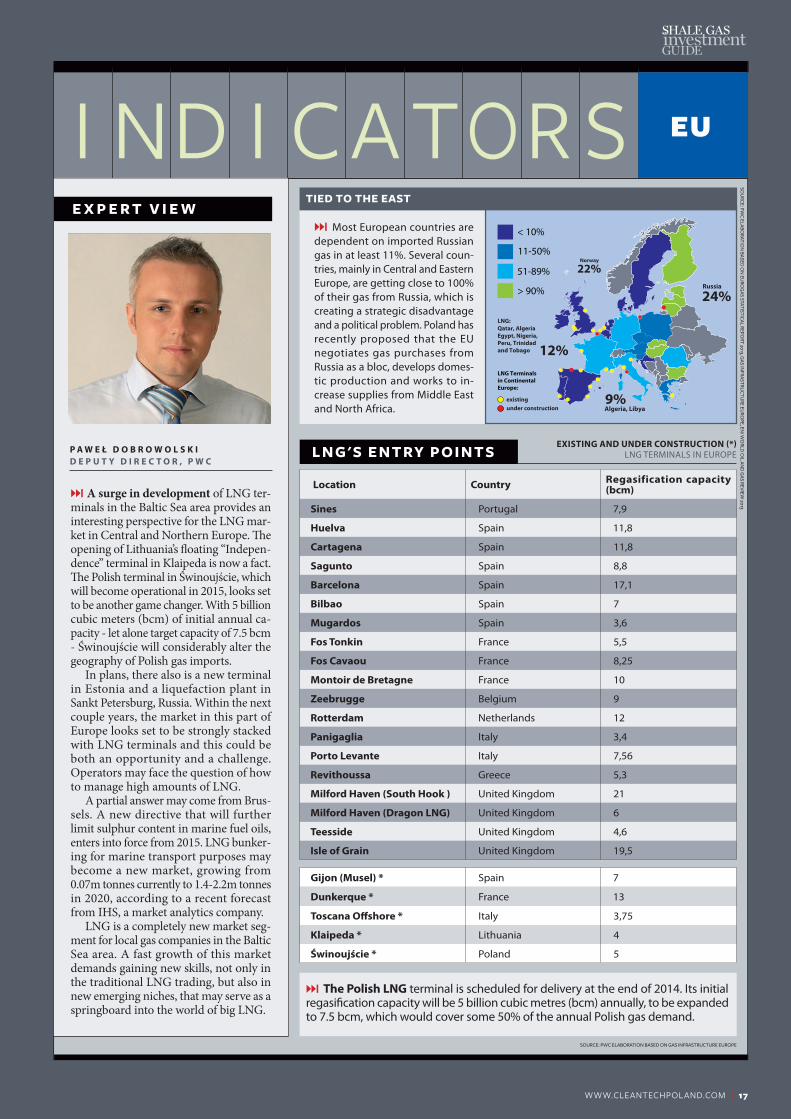

� A surge in development of LNG ter-minals in the Baltic Sea area provides an interesting perspective for the LNG mar-ket in Central and Northern Europe. The opening of Lithuania’s floating “Indepen-dence” terminal in Klaipeda is now a fact. The Polish terminal in Świnoujście, which will become operational in 2015, looks set to be another game changer. With 5 billion cubic meters (bcm) of initial annual ca-pacity - let alone target capacity of 7.5 bcm - Świnoujście will considerably alter the geography of Polish gas imports. In plans, there also is a new terminal in Estonia and a liquefaction plant in Sankt Petersburg, Russia. Within the next couple years, the market in this part of Europe looks set to be strongly stacked with LNG terminals and this could be both an opportunity and a challenge. Operators may face the question of how to manage high amounts of LNG. A partial answer may come from Brus-sels. A new directive that will further limit sulphur content in marine fuel oils, enters into force from 2015. LNG bunker-ing for marine transport purposes may become a new market, growing from 0.07m tonnes currently to 1.4-2.2m tonnes in 2020, according to a recent forecast from IHS, a market analytics company. LNG is a completely new market seg-ment for local gas companies in the Baltic Sea area. A fast growth of this market demands gaining new skills, not only in the traditional LNG trading, but also in new emerging niches, that may serve as a springboard into the world of big LNG.

E X P E R T V I E W

P a W e Ł d o B r o W o l s k i d e P u t y d i r e c t o r , P W c

location country regasification capacity (bcm)

sines Portugal 7,9

huelva Spain 11,8

cartagena Spain 11,8

sagunto Spain 8,8

Barcelona Spain 17,1

Bilbao Spain 7

Mugardos Spain 3,6

Fos tonkin France 5,5

Fos cavaou France 8,25

Montoir de Bretagne France 10

Zeebrugge Belgium 9

rotterdam Netherlands 12

Panigaglia Italy 3,4

Porto levante Italy 7,56

revithoussa Greece 5,3

Milford haven (south hook ) United Kingdom 21

Milford haven (dragon lnG) United Kingdom 6

teesside United Kingdom 4,6

isle of Grain United Kingdom 19,5

Gijon (Musel) * Spain 7

dunkerque * France 13

toscana offshore * Italy 3,75

klaipeda * Lithuania 4

Świnoujście * Poland 5

> 90%

51-89%

< 10%

11-50%

existingunder construction

LNG Terminalsin ContinentalEurope:

Algeria, Libya9%

Russia

24%

Norway

22%

12%

LNG:Qatar, AlgeriaEgypt, Nigeria, Peru, Trinidad and Tobago

Sou

rce: Pw

c elabo

ration

baSed o

n eu

roG

aS StatiStical rePo

rt 2013, GaS in

FraStruc

ture eu

roPe, en

i wo

rld o

il and

GaS review

2013

Source: Pwc elaboration baSed on GaS inFraStructure euroPe

l N g ' s E N T Ry P o I N T seXistinG and under construction (*)

LNG TERMINALS IN EUROPE

� Most European countries are dependent on imported Russian gas in at least 11%. Several coun-tries, mainly in Central and Eastern Europe, are getting close to 100% of their gas from Russia, which is creating a strategic disadvantage and a political problem. Poland has recently proposed that the EU negotiates gas purchases from Russia as a bloc, develops domes-tic production and works to in-crease supplies from Middle East and North Africa.

TIED To THE EasT

� the Polish lnG terminal is scheduled for delivery at the end of 2014. Its initial regasification capacity will be 5 billion cubic metres (bcm) annually, to be expanded to 7.5 bcm, which would cover some 50% of the annual Polish gas demand.

EUEU

18 | shale Ga s Inve s tm ent GuIde | WINTER 2013 | shale Ga s Inve s tm ent GuIde | sUMMER 2013

I Ind c a t r soGuide

Shale GaS investment

18 | shale Ga s Inve s tm ent GuIde | WINTER 2014

E X P E R T V I E W

olGa andrienko-BentZ director, enerGy GrouP, PWc ukraine

� Oil and gas sector in Ukraine is on the verge of an incredible transformation. Integration into European networks, upgrade to the modern standards and overall market liberalization open tre-mendous opportunities. With almost 20% share in total EU-28 gas storage capacities and accounting for 17% of Europe’s gas consumption with its transportation capacity, Ukraine is bound to play an important role in the region. On the other hand, the country faces a very difficult challenge of increasing its energy efficiency as well as finding ways to assure energy independence. Both are interdependent, geopolitical pressures providing for additional stimulus to

urgently starting closing the 30-40% energy efficiency gap, which has hardly been tackled during the last 20 years. The government has launched an am-bitious reform program, including har-monization of the national legislation with the EU norms, reforming the pricing system, introducing market principles, reforming the national oil and gas com-pany Naftohaz, improving the indepen-dence of the regulatory authority, as well as modernization of Ukraine’s gas trans-portation system. The success of this transformation depends on political will of the Ukrai-nian government, as well as coordi-nated and consistent efforts of interna-tional community.

Changes to the Geological and Mining Act – practical consequences for exploration and mining companies

The conference that the mining sector has been waiting for

Warsaw, 13th - 14th January 2015

Details:

www.ssw.pl

reklama Górnictwo.indd 3 2014-11-07 13:55:13

elena revutskaya senior consultant, PWc ukraine

� ukraine has 12 under-ground gas storage facilities, with total active capacity of about 31 bcm. Storages and system of trunk pipelines are operated by Ukrtransgaz, a 100% state-owned entity. Total EU-28 natural gas stocks are 78.2 bcm and Ukrainian stocks are 15.9 bcm as of November 2014.

UKRaINE aND THE EURoPEaN gas sECToR

Ukraine

Other EU-28

Italy

France

Germany

15

16

17

18

19

20

21

22

23

24

25

2014**2013*20122011201020092008

17%

17%

12%

23%

Russia Ukraine Europe

Transit and export to Ukraine

111 bcm

Transit

86 bcm

Reverse 2bcm

Transit through other countries 76.4bcm

Poland

29%

3%

� ukraine has Europe's third biggest storage capacity, behind Germany and Italy.

Ukraine

Other EU-28

Italy

France

Germany

15

16

17

18

19

20

21

22

23

24

25

2014**2013*20122011201020092008

17%

17%

12%

23%

Russia Ukraine Europe

Transit and export to Ukraine

111 bcm

Transit

86 bcm

Reverse 2bcm

Transit through other countries 76.4bcm

Poland

29%

3%

sToRagE CaPaCITy Vs EU-28 gas TRaNsIT RUssIa-EU, % of UKRaINE CoNsUMPTIoN

� europe receives approximately 50% of its Russian gas importa via Ukraine. It was 80% before Nord Stream began operational.

Source: GaS inFraStructure euroPe eia, miniStry oF Fuel and enerGy oF uKraine, euroStat, euroGaS. * - the amount oF GaS conSumPtion waS taKen From euroGaS data(data For eu 28 and Switzerland) , **- the amount oF GaS conSumPtion waS ForecaSted by euroGaS (data For eu 28 and Switzerland). the value oF tranSit throuGh

� russian natural gas export to Ukraine decreased by 3.6 bcm to 16.1 bcm in the first nine months of 2014 in comparison with the same period of 2013. In 2014 Ukrtransgaz and Eustream agreed on reverse supplies of gas to Ukraine at a rate of up to 8 billion cubic meters per year. Ukraine is developing reverse routes of gas supplies from Hungary, Poland, Slovakia and Romania. Opening all four routes will allow Ukraine to in-crease annual gas deliveries to 25 billion cubic meters.

bETWEEN RoCK aND a HaRD PlaCE?

Ukraine

Other EU-28

Italy

France

Germany

15

16

17

18

19

20

21

22

23

24

25

2014**2013*20122011201020092008

17%

17%

12%

23%

Russia Ukraine Europe

Transit and export to Ukraine

111 bcm

Transit

86 bcm

Reverse 2bcm

Transit through other countries 76.4bcm

Poland

29%

3%

Source: britiSh Petroleum StatiStical review oF world enerGy June 2014, GazProm materialS, miniStry oF Fuel and enerGy oF uKraine

UA

Changes to the Geological and Mining Act – practical consequences for exploration and mining companies

The conference that the mining sector has been waiting for

Warsaw, 13th - 14th January 2015

Details:

www.ssw.pl

reklama Górnictwo.indd 3 2014-11-07 13:55:13

gas TRaNsIT RUssIa-EU, % of UKRaINE CoNsUMPTIoN

20 | Shale Ga S Inve S tm ent GuIde | winter 2014

June 24/14

rasmussen: Russia diRects shale dissent

FACE

BOO

KMan for hire

June 14/14

German government proposes fracking restrictions June 18/14

FTS International and Sinopec to develop China shale gas

June 26/14

Greece, Spain, Denmark join Europe’s

shale gas effort

t nr e d I nG

June 30/14

NY court upholds state fracking ban

Former Secretary General oF nato, Anders Fogh Rasmussen, accused Russia of supporting anti-fracking movements so as to maintain Europe’s chief gas supplier. “I have met allies who can report that Russia, as part of their sophisticated information and disinfor-mation operations, engaged actively with so-called non-governmental organisations - environmental organisa-tions working against shale gas - to maintain European dependence on imported Russian gas,” Mr. Rasmussen said at London’s Chatham House, a foreign affairs think-tank, the UK press reported. Anti-fracking protests helped stop shale gas exploration in various European countries such as France, Germany or Bulgaria.

Green activists denied Mr. Rasmussen’s revelations and demanded that he either proved his statement or issued an apology. “The European authorities have published several studies demonstrating high risks involved in the fracking industry—as have leading scientists around the world. Does Mr. Rasmussen believe that these institutions and individuals are all Russian dupes?” a group of envi-ronmental organizations said in a letter.

w w w.cle antechpol and.com | 21

July 10/14

exxon mobil, TPao to unlock tuRkish gas

phO

tOpi

n

turkey delights

July 21/14

Mexico lifts ban on foreign shale gas

investment

July 28/14

UK 14th O&G licensing round starts

July 21/14

China sTarTs Fuling Field commeRcial e&p

wiK

ipEd

iA

daily output on the rise

Tr

en

di

ng

exxon mobil announced that the Turkish government approved an agreement between its local affiliate and the national oil company Türkiye Petrolleri Anonim Ortaklığı (TPAO) to explore two deepwater blocks in the Black Sea, signed back in 2008. Further talks are pending about joint prospecting in the region of Thrace and in southeastern part of the country.

The agreement concerns a combined area of about 30,000 km2 including deepwater prospects in the Black Sea at depths reaching 2,000 meters. Exxon Mobil will be the operator and will earn a 50% inter-est in acreage in question.

“TPAO and ExxonMobil will be working closely to-gether to assess the potential of these blocks. I believe that we will find commercial quantities of oil and gas,” said TPAO President and CEO Mehmet Uysal.

Exxon Mobil is also interested in exploring Thrace and the southeastern Dadas shale formation, estimated to potentially hold 1.3 trillion cubic meters of gas, where TPAO has drilled some wells in cooperation with Shell.

china’S miniStry oF land and reSourceS said last week that the Fuling field, China’s first large shale gas play, contained proven reserves of nearly 107 billion cubic metres of gas. The ministry’s announce-ment is considered an official launch of Fuling’s com-mercial development.

In June, the field’s operator, Chinese state owned oil and gas company Sinopec reached a daily output of 3.2 million cubic metres from 29 test wells. The company also stated that the gas contains as much as 98% methane, with low levels of carbon dioxide and no hydrogen sulphide.

China is eager to mirror the US shale boom, but indus-try experts warn that Fuling’s success might not be easily replicated elsewhere in the country. Fuling is considered to posses some of most favourable geological conditions in a country where drilling in other locations proved to have been complex and costly.

aug 6/14

Surge in Polish drilling activity: 3Legs, San Leon,

Orlen

aug 8/14

China halves 2020

shale gas output

estimate

22 | Shale Ga S Inve S tm ent GuIde | winter 2014

3leGS reSourceS said that it would give up on their three concessions in the Baltic Basin in northern Poland, following lower than anticipated natural gas flow rates on the Lublewo LEP-1ST1H lateral well. “In view of the results to date of the Lublewo LEP1-ST1H well, which it considers to be at sub-commercial levels, and the further time needed to complete the remainder of the testing phase on the well when the prospects of a more successful outcome appear remote, the Com-pany has concluded that it would be in the best interests of its shareholders to exercise its option to withdraw from the three western Baltic Basin concessions,” 3Legs announced in a release on September 17.

According to 3Legs, the Lublewo well has produced at an average rate of 396 mscf/d natural gas and 157 b/d of light oil. “While it had been hoped that early hydrocarbon production rates might improve substan-tially as the well continued to flow back frac fluid, this has not yet occurred.”

Opp

pw

Man in the arena

sep 9/14

US fracking sand demand outpaces supply

sep 18/14

Argentina overhauls O&G law

t nr e d I nG

sep 17/14

Casing, CemenTing Risk to acquiFeRs

ClE

An

tEC

h p

OlA

nd

Blame at the top

neither horizontal drillinG nor hydraulic fracturing of shale deposits is responsible for drinking water contamination, according to a study led by Thom-as Darrah of the Ohio State University, published in the “Proceedings of the National Academy of Sciences”. Analysis of eight clusters of contaminated wells in Penn-sylvania and Texas showed that the source of the problem was faulty casing and cementing of the wells.

“These results appear to rule out the migration of meth-ane up into drinking water aquifers from depth because of horizontal drilling or hydraulic fracturing,” said Avner Vengosh, professor of geochemistry and water quality at Duke University. Using noble gas and hydrocarbon trac-ers, researchers identified and distinguished between signatures of naturally occurring methane and stray gas contamination from shale drill sites. Researchers analyzed gas content in 113 drinking-water wells and one natural methane seep in the Marcellus shale in Pennsylvania, and in 20 wells in the Barnett shale in Texas.

sep 23/14

Exxon Mobil halts activity in Russian Arctic sep 2914

UK changes trespass law to enable access to drilling sites

sep 17/14

3legs resourCes gives up Baltic acReage

w w w.cle antechpol and.com | 23

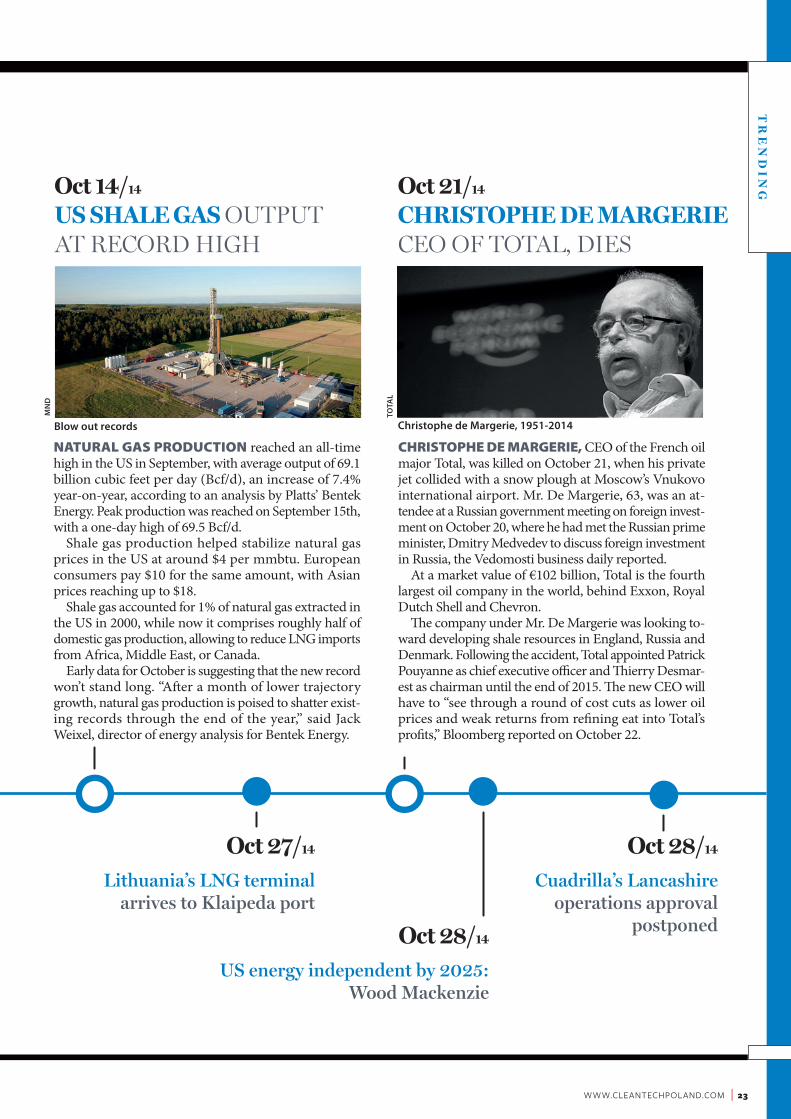

oct 28/14

US energy independent by 2025: Wood Mackenzie

oct 28/14

Cuadrilla’s Lancashire operations approval

postponed

oct 27/14

Lithuania’s LNG terminal arrives to Klaipeda port

Tr

en

di

ngoct 21/14

ChrisToPhe de margerie ceo oF total, dies

chriStophe de marGerie, CEO of the French oil major Total, was killed on October 21, when his private jet collided with a snow plough at Moscow’s Vnukovo international airport. Mr. De Margerie, 63, was an at-tendee at a Russian government meeting on foreign invest-ment on October 20, where he had met the Russian prime minister, Dmitry Medvedev to discuss foreign investment in Russia, the Vedomosti business daily reported.

At a market value of €102 billion, Total is the fourth largest oil company in the world, behind Exxon, Royal Dutch Shell and Chevron.

The company under Mr. De Margerie was looking to-ward developing shale resources in England, Russia and Denmark. Following the accident, Total appointed Patrick Pouyanne as chief executive officer and Thierry Desmar-est as chairman until the end of 2015. The new CEO will have to “see through a round of cost cuts as lower oil prices and weak returns from refining eat into Total’s profits,” Bloomberg reported on October 22.

Mn

d

Blow out records

oct 14/14

us shale gas output at RecoRd high

natural GaS production reached an all-time high in the US in September, with average output of 69.1 billion cubic feet per day (Bcf/d), an increase of 7.4% year-on-year, according to an analysis by Platts’ Bentek Energy. Peak production was reached on September 15th, with a one-day high of 69.5 Bcf/d.

Shale gas production helped stabilize natural gas prices in the US at around $4 per mmbtu. European consumers pay $10 for the same amount, with Asian prices reaching up to $18.

Shale gas accounted for 1% of natural gas extracted in the US in 2000, while now it comprises roughly half of domestic gas production, allowing to reduce LNG imports from Africa, Middle East, or Canada.

Early data for October is suggesting that the new record won’t stand long. “After a month of lower trajectory growth, natural gas production is poised to shatter exist-ing records through the end of the year,” said Jack Weixel, director of energy analysis for Bentek Energy.

tOtA

l

Christophe de Margerie, 1951-2014

24 | Shale Ga S Inve S tm ent GuIde | Summer 2014

w w w.cle antechpol and.com | 25

l Operations update p.26

l Licensing and permitting p.30

l UK, the new Poland p.32

l The 14th licensing round: tough road ahead p.34

l Fracking’s material challenge p.36

l Geology overview p.38

l Profile: Hutton Energy p.40

l Interview: Tom Vesey, Risk to Reputation p.42

l Feature: Here comes the sun p.44

CONTENTS

The UK is the new Poland. Not just because of the immigration from the central European

country. As the enthusiasm for shale gas in Poland seems to be waning, the super-thick

British shales start to fuel the imagination - and the protesters.

Keep Calmand

Frack On

U K F O C U S

26 | Shale Ga S Inve S tm ent GuIde | WINTer 2014

The UK is one of the few Euro-pean countries in which investors have high expectations that shale

gas exploration could be a commercial success by 2020.

British-owned Cuadrilla Resources, an independent pioneer of fracking in the UK, is one of 19 companies cur-rently racing to get British shale gas flowing, alongside French-owned oil and gas major Total and the Swiss-based chemicals company INEOS, which owns a refinery at Grangemouth, where it needs new sources of gas to convert into synthetic ethanol, ethyl-ene, propylene and polymers: polyeth-ylene and polypropylene. It is such companies that are expected to give exploration the kick that seems to have been lost in Poland, where drilling is going forward, but not yet with very promising results.

Asked about shale gas, the UK front-runners of the industry are still very wary about what they want to reveal. “It’s still very early days in this country. We don’t know yet if the American experience will happen here. A whole

lot more work needs to be done by the industry in exploration before we can say for sure,” said Andy Houldsworth of Cuadrilla Resources.

There is not much doubt that Mr. Houldsworth’s view that a lot more work is needed to be done is correct. According to Wood Mackenzie, a UK energy consultant company, merely six wells targeting shale plays in the UK have been drilled to date.

The UK Onshore Oil and Gas (UKOOG), an industry association, reported in July 2014 that current spending on fracking exploration can be counted in the tens of millions of pounds. Extracting oil from UK’s de-clining North Sea fields, which some claim shale gas will replace one day, will cost £14 billion this year alone.

ON THE GROUNDCurrently, the bulk of company activ-ity is focused on conducting further geological research in preparation for identifying promising test drilling sites. Companies are also busy preparing and submitting planning applications to

Shale gas operations in the UK are poised to recover in 2015 from the lull they have been in since the infamous seismic event on a Cuadrilla Resources site in 2011.

B y N i C h O l a S N e w m a N i N l O N d O N

Turning point, 2015O p e r a t i O N S U p d a t e

local authorities (see also p. 30). This seems to be the current state of play for the small independents, big companies and newcomer INEOS.

“Earlier this year, we submitted plan-ning applications for two exploratory sites located within our Bowland Basin licence area. We are planning to drill, hydraulically fracture and test the flow of gas from up to four exploration wells on each of the sites, one at Roseacre Wood and the other at Preston New Road over the next year,” said Mr. Houldsworth.

At least eight shale exploration com-panies are undertaking site preparation at prospective wells, including indepen-dents like privately owned Cuadrilla Resources and publicly listed IGas En-ergy, with the latter committed to drill and carry out flow tests at its licensed sites in the east Midlands and north west England.

In addition, Celtique Energie has an-nounced plans to start well site prepara-tions at its Broadford Bridge-1 well site in West Sussex in order to drill in win-ter 2014 or spring 2015 (see table, p.28).

w w w.cle antechpol and.com | 27

UK

fo

cU

s

Two significant developments at gov-ernmental level promise to speed up exploration and drilling from next year. Firstly, the government is in the process of devising an attractive package of tax and regulations governing fracking. For instance, in 2013, the UK Treasury devised early-stage tax concessions for the shale industry.

Secondly, new laws are being de-signed to accommodate shale gas ex-ploration. Horizontal drilling and fracking will in part supersede the Tres-pass Laws. Before the next general election in May 2015, new legislation will be passed to allow companies drill-ing below 300 metres for oil and gas to have easier access under landowners’ property.

“[The government] has streamlined and simplified regulations and intro-duced the most competitive tax regime in Europe for shale gas, while maintain-ing robust environmental safeguards and making sure there is more informa-tion going to local communities,” the UK Minister of State for Energy Mat-thew Hancock MP said.

SEISMIC SURVEYSUnderpinning investor interest and much of the current exploration and

evaluation of licensed blocks are inde-pendent survey reports released by the British Geological Survey and Depart-ment of Energy and Climate Change.

The latest survey, dated June 2014 and covering the Midland Valley of Scotland,

estimated total-in-place-shale gas at between 1.40 trillion cubic metres (tcm) and 3.81 tcm.

A survey of the Bowland-Hodder basin in Lancashire, dated 2013, esti-mated 24-68 tcm (upper and lower units)

of shale gas, making this almost on a par with gas-in-place estimations for the Marcellus formation.

At company level, however, little seis-mic activity is currently underway. Nei-ther Cuadrilla Resources nor INEOS are going forward with any major seismic programs. This is likely to change in 2015. “Seismic will be one tool that our team will use in all exploration activity, to bet-ter understand the basin, to aid in iden-tifying the best geological location for exploration drilling, coring and ap-praisal,” said Hannah Brandstaetter, INEOS’ spokeswoman.

OBSTACLESIn general, the industry’s and govern-ment efforts to communicate and make the case for shale are far from successful.

The DECC public opinion tracker on attitudes towards fracking reported in August 2014 that public support and opposition is even at 24% each, while 47% said they neither supported nor op-posed fracking.

“Misinformation is a real obstacle to this technology. Getting the facts about safe on-shore gas extraction across to people will be a significant challenge,” said Ms. Brandstaetter. She adds that INEOS has hired some of the world’s

“Misinformation is a real obstacle to this technology. Getting

the facts about safe on-shore gas extraction across to people will be a

significant challenge”Hannah Brandstaetter,

INEOS

PHO

TOPI

N

28 | Shale Ga S Inve S tm ent GuIde | WINTer 2014

leading shale gas experts to make sure the gas can be safely extracted in an environ-mentally responsible way.

Given the lack of public support, it is not surprising that fracking companies are failing to gain planning permission to drill, hydraulically fracture and test wells. This is due to local politicians on the plan-ning approval committee who see grant-ing approval as a politically difficult.

“Cuadrilla and the industry as a whole, must keep on communicating, at local and national levels. It’s vital that the gen-eral public fully understands the potential benefits associated with UK shale gas, such as jobs, energy security and tax revenues,” said Mr. Houldsworth.

That said, a September 2014 paper from Professor Sarah O’Hara from the Univer-sity of Nottingham, published findings on the general public’s attitudes towards shale gas, a result of a series of surveys carried out from March 2012 to Septem-ber 2014 (see chart).

“The public was asked whether shale gas extraction in the UK should be allowed, a question intended to capture

people’s “all-things considered” judge-ment on shale,” wrote Professor O’Hara’s team.

In July 13, before the Balcombe pro-tests, which were widely reported and saw protesters forcibly removed from a Cuadrilla site, the survey revealed 58.3% in favor of shale gas extraction and 18.8% against.

Post-Balcombe, there was a decline “yes” and an increase in “no” respons-es that continued until May 2014 when the number of people who believe shale gas extraction should be allowed fell below 50%.

In September 2014 the differential between the “yes” and “no” camps in-creased slightly to +21% and may indicate

PHO

TOPI

N

location Operator plans

Belcoo near Enniskillen in Fermanagh, Northern Ireland Tamboran Resources Exploration well

Crawberry Hill in Yorkshire, England Rathlin Energy Well tests

East Sussex, England Cuadrilla Plans to drill

Glynneath in South Wales UK Methane Drill one shale gas well

Maesteg, Bridgend in South Wales Coastal Oil & Gas Ltd Drill for core samples

Maesteg, Bridgend in South Wales UK Methane Drill one shale gas well

Preston New Road near Little Plumpton in Lancashire, England Cuadrilla Well tests

South Sussex, England IGAS Plans to drill

West Newton in Yorkshire, England Rathlin Energy Well tests

West Sussex, England Celtique Energie/Magellan Plans to drill

w h e r e S h a l e t h e y d r i l l wOrK plaNS

SOURCE: BBC 2014, DECC 2014, THE TElEGRAPH 2014, WAlES ON lINE 2014

w w w.cle antechpol and.com | 29

that the Balcombe effect has bottomed out, the researchers noted.

Adding a significant financial induce-ment such as INEOS’s recent announce-ment of a £2.5 billion shale gas giveaway might win greater public acceptance. “This is a game changer for Britain’s shale gas industry. Giving 6% of revenues to those living above Britain’s shale gas

developments means the rewards will be fairly shared,” said Jim Radcliffe, INEOS’s Chairman in September 2014.

NEWCOMERS BOOST POTENTIALINEOS is one of the new companies that have signed up to test the UK’s potential for shale gas, potentially creating a snowball effect of more operators jumping on the exploration bandwagon and, possibly later, pro-duction.

Apart from INEOS, these compa-nies include one of the world’s super majors, Total, and the French power generator and energy trader GDF Suez, both of which farmed-in into existing license blocks earlier in 2014.

INEOS claims they are committed to British shale. “We have established

INEOS Upstream, where we have operational, commercial and techni-cal support from Dan Steward, Kent Bowker and Nick Steinberger, who were the senior team at Mitchell En-ergy in the Barnett Shale and who pioneered the geological and petro-leum engineering as well as fracture stimulation work that achieved the

successful commercial production of sas from the Barnett,” Ms. Brandstaet-ter said.

Ms. Brandstaetter adds that the company is keen to move forward with mergers and acquisitions, and licence applications. INEOS com-pleted one deal in August 2014, which is the purchase of 51% of the shale section in the PEDL 133 license block in Midland Valley in Scotland from BG Group.

Earlier in 2014, Total announced plans to invest at least $21m (£12.7m) in the UK shale gas industry. Total has already agreed with UK energy firm IGas Energy to buy a 40% share in two shale gas exploration licences in Lincolnshire.

In addition, in October 2013,

France’s GDF Suez delivered a major vote of confidence in the nascent industry by buying a 25% stake in 13 UK exploration licences owned by Australian independent Dart Energy, holder of one of the largest acreage positions in Britain.

Following the deal, John McGold-rick, Dart chief executive, told Bloomberg that “the level of interest in UK unconventional gas is growing almost daily.”

LICENSING ROUNDIn order to boost onshore drilling for oil and gas, including gas from shales, the UK government launched on 28 July 2014 the 14th onshore licensing round for a large swathe of England and Scotland including the Bowland Shale in the north of England and the Midland Valley in Scotland, two shale gas plays seen as promising in Britain (see p. 34).

The licensing round closed on October 28, but, according to Nick Grealy, a shale gas advocate, the new picture of interest - if any - in British shale gas is not seen arriving any time soon.

“The government may announce some general figures about December but the full information won’t be there until early 2015,” Mr. Grealy said.

That said, both leaders in explora-tion Cuadrilla as well as newcomers from INEOS have confirmed that they have their eyes set on applying for new acreage. “At the moment it is more or less likely that we will apply for licenses in the 14th round,” Ms. Brandstaetter said in early October.

“We are carefully assessing the ex-ploration acreage included in the 14th round, whilst maintaining our im-mediate focus on securing planning consents for our proposed shale gas exploration sites in Lancashire,” said Mr. Houldsworth.

UK

fo

cU

s

“The level of interest in UK unconventional gas is growing almost daily”

John McGoldrick, Dart Energy, for Bloomberg

poll: Should Shale gaS exTracTIoN IN The uk be alloWed?

0

10

20

30

40

50

60

Jan 12 Mar 13 Jul 13 Sep 13 Jan 14 May 14 Sep 14

Yes

No

Don’t know

Ukraine

OtherEU28

Italy

France

Germany

� the public has consistently favored drilling for shale gas over the last three yearsin the UK

SOU

RCE:

UN

IvER

SITy

Of

NO

TTIN

GH

AM

30 | Shale Ga S Inve S tm ent GuIde | WINTER 2014

Permitting for shale exploration in the UK is a multi-step process involving national government and local councils. There’s what it takes.

B y N i l i m a C h o u d h u r y i N l o N d o N

Fit for Purpose?l i C E N S i N G & P E r m i T T i N G

Over the last 30 years, more than 2,000 wells have been drilled onshore in the UK, although only

around 200 have been hydraulically fractured.

In 2013, the British Geological Sur-vey (BGS) in association with the government’s Department of Energy and Climate Change (DECC) esti-mated that there may be up to 2,281 trillion cubic feet of shale gas in one major basin, Bowland-Hodder, alone.

With the possibility of gaining access to such significant reserves and the financial returns that could be achieved from this, the government is streamlining its policies to meet the need for energy security and to move towards a low carbon economy with natural gas as a transition fuel on the road to renewable energy.

Still, the complexities and compli-cations of the UK regulatory system persist and are one of the elements behind the fact that the UK’s massive potential has not yet translated into a drilling frenzy.

“What we’ve seen before is small players that take bigger risks that go

and look for the stuff and then find it, develop it and look to sell out to the big players. The first really big player to enter by itself, which is very interesting, is a chemical company called INEOS,” said Dan Lewis, senior advisor on infrastructure policy at the Institute of Directors, an industry association.

LICENSES AND PERMITSFour major agencies are involved in regulating the oil and gas industry: the government’s Department of Energy and Climate Change (DECC), local councils represented by the Mineral Planning Authorities (MPA), the En-vironment Agency, an executive non-departmental public body, and the UK’s national independent watchdog, the Health and Safety Executive (HSE).

To complicate matters, the licence and permit process is not uniform throughout the UK, with many dif-ferences between England, Scotland and Wales.

In England the onshore oil and gas industry body, UK Onshore Operators Group (UKOOG), requires companies

to engage with local residents and other stakeholders before each of the three stages of operation and prior to submitting a planning application.

Operators will need to apply for a petroleum exploration and develop-ment licence from DECC, after which they will need to carry out an Envi-ronmental Risk Assessment.

At this stage, the UKOOG has com-mitted to providing £100,000 in com-munity benefits, per well-site, where fracking takes place.

Then operators are required to no-tify the Environment Agency and HSE of their intention to drill a wellhole and detail how they intend to protect water resources.

Land use planning permission is required from the Local Minerals Planning Authority, which can be a county council, for surface operations like the construction and operation of individual well-pads.

An Environmental Impact Assess-ment is then submitted to the MPA, which decides on the application fol-lowing talks with the statutory con-sultees and the local community and

w w w.cle antechpol and.com | 31

Fit for Purpose?

uk

fo

cu

s

imposes any planning conditions. Following the completion of the En-

vironmental Impact Assessment, an operator also needs to apply for envi-ronmental permits, which includes the

management and disposal of waste from drilling the borehole, mining waste and a permit for naturally occurring radio-active material for managing flow-back fluid and waste gases, issued by the Environmental Agency.

In order for DECC to then provide

final consent, operators will need to review available information on fault lines and monitor seismicity, conduct real time seismic monitoring during operations, submit a hydraulic stimula-

tion plan and monitor the growth in height of the fracture away from the borehole.

At production, the UKOOG requires companies to pay 1% of revenues to the local community. This could easily run into tens of thousands of pounds.

TIMESCALEMr. Lewis believes the UK will start to see the number of well pads dramati-cally increase within the next couple of years. “There’s quite a lot of political agreement behind the need to do this” (see p. 32).

However, he argues that where po-litical parties disagree is perhaps in terms of how quickly companies go from completing paperwork to production.

“What we have is a tiny system much more geared to big companies with big pockets and longer time horizons [but] currently between getting an explora-tion licence and getting gas to market you’re looking at a time lag of 6-8 years and what you want is four years or less,” said Mr. Lewis.

Of more immediate concern, accord-ing to Professor John Loughhead, Executive Director at the UK Energy Research Centre (UKERC), is the small number of onshore drilling rigs available in the UK, as opposed to thousands in the US.

“I do not believe there is a struc-tural problem with the system which means that inherent barriers exist due to regulatory or licensing require-ments,” said Professor Loughhead.

He does note however that as explo-ration is yet to be undertaken, the industry remains in the dark about how much gas is actually retrievable, and even how much the supply chain can handle.

“So the review of regulations and licensing is intended to ensure the system is fit for purpose – ensure the right reviews are undertaken that will provide the robust social, environ-mental and safety assurances needed, but to do so in an efficient way that does not create unnecessary barriers, i.e. those that provide no benefit to any involved party,” said Professor Loughhead.

“Currently between getting an exploration licence and getting gas to market you’re

looking at a time lag of 6-8 years and what you want is four years or less”

Dan Lewis, Institute of Directors

pho

topi

n

| Shale Ga S Inve S tm ent GuIde | winter 201432

You have been doing most of your fracking in Poland to date, but with Polish shale gas dynamics

going somewhat flat, is the UK now what you’re thinking more about?We have a business development posi-tion in the UK. We don’t do any ser-vices yet but we will be staging seismic services probably by January. We’re talking to four companies that have licenses in the UK and also to several others that are trying to acquire li-censes in the new licensing round.

What is the sentiment about shale gas in the British shale gas sector? Is the UK the new Poland now?There’s quite a bit of enthusiasm. The UK is more advanced in trying to pro-pel forward on shale gas. I’m still opti-mistic that we will have commercial shale gas in Poland, but there’s going to be a long delay because of the pipeline situation, as midstream does not exist in Poland. If you don’t have a pipeline close to your well, it’s a 3-4 year ordeal to get the well tied in. And that’s going to slow down production.

Does the UK have all that then?It does. Plus it’s a much easier process to tie a well in. The UK has a great in-

frastructure for household gas, more so than in Poland. There’s a lot more tie-in lines, most of the well pads will have pipelines within 20-30 feet, or 10 me-ters. The UK will get to production much, much faster than Poland.

Is it just developed midstream that gets UK operators and yourself ex-cited about UK shale gas?It’s no secret that when Cuadrilla drilled their first shale well almost four years ago, it would appear to have commer-

cial potential. There was a potential commercial gas flow from their well. They never announced production numbers, because the stimulation caused a small earthquake due to prox-imity of an active fault and things got stalled since then and it’s only now that everybody’s in a great rush again, with the government passing laws to im-prove the permitting situation, getting

new players in through the licensing round and so on.

Poland’s shale geology didn’t pan out to be so terrific. As a CEO of an oil-field services company, what can you infer about the UK geology?The Bowland shale has good TOCs, good permeability and other key pa-rameters. I think the way that commer-ciality will happen in the Bowland is much like it did in the Barnett [a major shale gas play in the US], where we had multiple shale layers separated by lime-stone and sandstone. The way you will drill in the UK, then, is that you will lay multiple laterals from the same well bore, so instead of 8 to 12 wells on a pad, you can multiply that times 4-5 so you’d get 32-40 wells to a pad. That’s an advantage from the standpoint of den-sity of well sites and well costs.

Would you expect that there will be a lot of interest in the 14th licensing round from UK and international players?For sure. Even the independents that are active already or the ones getting ready to go in are very well funded. There’s going to be a conscious effort to get in quickly.

i n t e r V i e w

Dennis McKee, founder and CEO of United Oilfied Services, is setting his sights on the UK market, where he thinks he can capitalize on Britain’s expected boom in demand for onshore services.

I n t e r v I e w b y w o j c I e c h K o ś ć

UK, the New Poland

Ma

rek

Cza

rneC

ki

“The UK will get to production much, much faster than

Poland”

w w w.cle antechpol and.com | 33

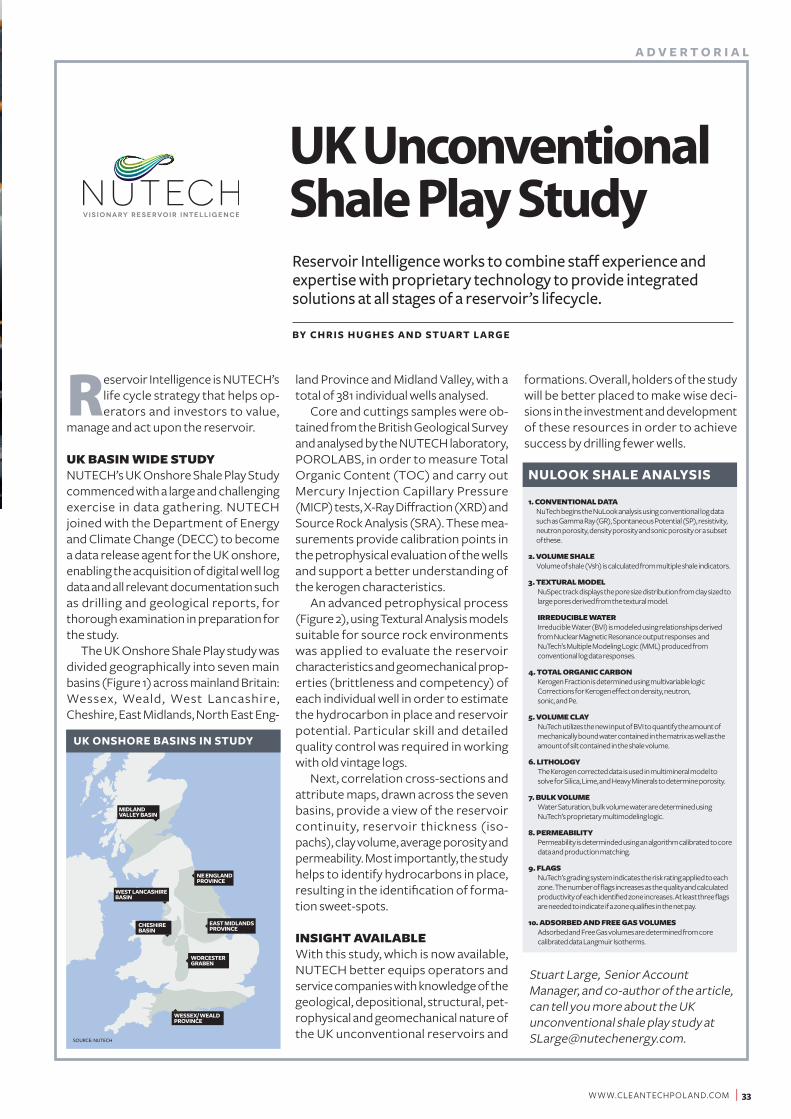

Reservoir Intelligence is nutech’s life cycle strategy that helps op-erators and investors to value,

manage and act upon the reservoir.

UK BASIN WIDE STUDY nutech’s uK onshore Shale play Study commenced with a large and challenging exercise in data gathering. nutech joined with the department of energy and climate change (decc) to become a data release agent for the uK onshore, enabling the acquisition of digital well log data and all relevant documentation such as drilling and geological reports, for thorough examination in preparation for the study.

the uK onshore Shale play study was divided geographically into seven main basins (Figure 1) across mainland Britain: wessex, weald, west lancashire, cheshire, east midlands, north east eng-

land province and midland valley, with a total of 381 individual wells analysed.

core and cuttings samples were ob-tained from the British Geological Survey and analysed by the nutech laboratory, poRolaBS, in order to measure total organic content (toc) and carry out mercury Injection capillary pressure (mIcp) tests, X-Ray diffraction (XRd) and Source Rock analysis (SRa). these mea-surements provide calibration points in the petrophysical evaluation of the wells and support a better understanding of the kerogen characteristics.

an advanced petrophysical process (Figure 2), using textural analysis models suitable for source rock environments was applied to evaluate the reservoir characteristics and geomechanical prop-erties (brittleness and competency) of each individual well in order to estimate the hydrocarbon in place and reservoir potential. particular skill and detailed quality control was required in working with old vintage logs.

next, correlation cross-sections and attribute maps, drawn across the seven basins, provide a view of the reservoir continuity, reservoir thickness (iso-pachs), clay volume, average porosity and permeability. most importantly, the study helps to identify hydrocarbons in place, resulting in the identification of forma-tion sweet-spots.

INSIghT AVAILABLE with this study, which is now available, nutech better equips operators and service companies with knowledge of the geological, depositional, structural, pet-rophysical and geomechanical nature of the uK unconventional reservoirs and

formations. overall, holders of the study will be better placed to make wise deci-sions in the investment and development of these resources in order to achieve success by drilling fewer wells.

By C H r i S H u g H e S a n d St ua rt L a rg e

Reservoir Intelligence works to combine staff experience and expertise with proprietary technology to provide integrated solutions at all stages of a reservoir’s lifecycle.

UK Unconventional Shale Play Study

1. CoNVENTIoNAL DATAnutech begins the nulook analysis using conventional log data such as Gamma Ray (GR), Spontaneous potential (Sp), resistivity, neutron porosity, density porosity and sonic porosity or a subset of these.

2. VoLUmE ShALE volume of shale (vsh) is calculated from multiple shale indicators.

3. TExTUrAL moDELnuSpec track displays the pore size distribution from clay sized to large pores derived from the textural model.

IrrEDUCIBLE WATErIrreducible water (BvI) is modeled using relationships derived from nuclear magnetic Resonance output responses and nutech’s multiple modeling logic (mml) produced from conventional log data responses.

4. ToTAL orgANIC CArBoNKerogen Fraction is determined using multivariable logic corrections for Kerogen effect on density, neutron, sonic, and pe.

5. VoLUmE CLAYnutech utilizes the new input of BvI to quantify the amount of mechanically bound water contained in the matrix as well as the amount of silt contained in the shale volume.

6. LIThoLogYthe Kerogen corrected data is used in multimineral model to solve for Silica, lime, and heavy minerals to determine porosity.

7. BULK VoLUmEwater Saturation, bulk volume water are determined using nutech’s proprietary multimodeling logic.

8. PErmEABILITYpermeability is determinded using an algorithm calibrated to core data and production matching.

9. FLAgSnutech’s grading system indicates the risk rating applied to each zone. the number of flags increases as the quality and calculated productivity of each identified zone increases. at least three flags are needed to indicate if a zone qualifies in the net pay.

10. ADSorBED AND FrEE gAS VoLUmESadsorbed and Free Gas volumes are determined from core calibrated data langmuir Isotherms.

nuLOOK SHaLe anaLySiS

MIDLANDVALLEY BASIN

NE ENGLAND PROVINCE

WEST LANCASHIREBASIN

EAST MIDLANDSPROVINCE

WORCESTERGRABEN

CHESHIREBASIN

WESSEX/ WEALDPROVINCE

uK OnSHOre BaSinS in Study

SOURCE: NUTECH

a d V e r t O r i a L

Stuart large, Senior account manager, and co-author of the article, can tell you more about the uK unconventional shale play study at [email protected].

| Shale Ga S Inve S tm ent GuIde | winter 201434

The UK governmenT, which is keen to find domestic supply to replace dwindling North Sea pro-

duction and offset rising imports, launched a 14th onshore licensing round earlier this year, primarily to boost shale gas exploration efforts. The results of the round, for which applica-tions were due by the end of October, will give an indication of the strength of interest in the shale gas sector beyond the pioneering minnows who dominate it at present.

“I’m sure this round of onshore li-censing will see some new players com-ing in,” said Ann-Marie Wilkinson, head of communications at IGas En-ergy, one of the leading players in the UK shale gas sector.

IGas, which will put in bids in the cur-rent licensing round with undisclosed

partners, is part of a consortium that has already agreed a deal with Total under which the French company will take a 40% interest in two shale gas exploration licences in central England, potentially investing up to $50 million. The agree-ment made Total the biggest oil and gas firm to invest in UK shale gas so far.

Another French firm, GDF Suez, has also agreed to invest in exploration for shale gas and coalbed methane with Australian firm Dart Energy. Dart was the target of a takeover bid by IGas, which went through in October to create the country’s largest shale gas firm in terms of acreage.

Much of the acreage covered by the GDF Suez/Dart agreement lies in northern England, which is considered to be one of the most promising early exploration targets.

SUPPORT CAN GROWReserve estimates by the British Geo-logical Survey for the Bowland shale formation of northwest England centre on a figure of around 1,300 trillion cubic feet of shale gas for that play alone, though there is little prospect of extract-ing anything like all of that. However, the industry is keen to point out that even if 10% of that amount could be produced, it would be enough to meet current UK demand for 50 years.

Despite the geological potential and strong backing for shale gas exploration from the Conservative government, doubts remain that large-scale invest-ment and know how from the industry’s big guns are about to flood in under the on-going licensing round or any time soon, given the opposition to hydraulic fracturing – or fracking – used in shale

U K ’ s L i c e n s i n g r o U n d

The UK’s fledgling drive to exploit its shale gas reserves has already become mired in controversy, raising the prospect that drilling programmes could be delayed for years by protests and red tape. With all the main political parties in favour of at least limited exploration, energy companies remain hopeful that the industry could move into a higher gear in the near future.

B y I a n L e w I s I n L o n d o n

Tough Road Ahead

pho

topi

n

w w w.cle antechpol and.com | 35

gas exploration and production. “The government has tried to set a

favourable set of fiscal terms and it is offering inducements to local commu-nities to accept development. But it is doing very little else to manage the incredible opposition to fracking. While that opposition remains, it is very dif-ficult to see any way forward,” said Professor Paul Stevens, a distinguished fellow at Chatham House, who has writ-ten reports on shale gas prospects for the London-based think tank.

A tracking survey published by the UK Department of Energy and Climate Change (DECC) in August showed public support for shale gas extraction standing at just 24%, compared to 29% three months earlier. Despite this, with 47% of that survey sample still unde-cided on the benefits of fracking, the industry argues that support could eas-ily grow, given the right circumstances.

We need to make shale gas explora-tion happen in a way that brings the public with us,” said IGas’ Wilkinson. “As a business we are very pro renew-ables, but the reality is that we need gas to complement it in the short-to-me-dium term,” she said.

However, Professor Stevens says that big energy firms, many of which have high profile stakes in other parts of the UK economy, will be wary of suffering reputational damage by becoming as-sociated with potentially unpopular shale developments that could be de-layed by high-profile, long-running court cases. The UK’s still ill-defined local and national legal frameworks for onshore shale drilling and tough envi-ronmental laws are unlikely to result in a speedy legal process.

DRIVING ITThe absence of major players does not necessarily preclude shale gas develop-ment – it certainly didn’t in the US, where it was the smaller companies that made all the early running, even with considerably less gas transportation infrastructure in place than would be the case in much of the UK.

The company most likely to kick start exploration in the Bowland shale is Cuadrilla Resources, which is planning to drill a series of wells there in coming months. Cuadrilla and others in the

sector are currently only allowed to carry out seismic tests and drill vertical exploration wells. They are not yet al-lowed to carry out fracking or flow tests.

It was a well fracked by Cuadrilla near Blackpool in the Bowland shale in 2011 that triggered an upsurge in pub-lic opposition to shale gas drilling, after it triggered minor earthquakes.

More recently, the postponement of Cuadrilla’s efforts to drill a vertical onshore oil well at Balcombe in Sussex, southern England on 2013 in the face of strong local protests reflected the potential for opposition to any drilling in rural areas, even when fracking is not involved. Meanwhile, in September 2014, an application by Celtique Ener-gie to drill within the South Downs National Park on England’s southern coast was turned down by the park’s governing authority.

The industry realises it needs to work hard, if it is to convince UK residents that fracking is safe and that it can bring

substantial economic benefits. As part of that effort, a report produced by EY for industry body UK Onshore Oil and Gas (UKOOG) earlier this year pro-duced some headline-grabbing figures. According to Getting ready for UK shale gas, a report from consultancy EY, UK shale gas development could attract some £33 billion of investment across the supply chain over 18 years and cre-ate around 64,000 jobs.

“With such benefits on offer, if explor-ers are allowed to increase exploration and they can obtain good flow rates from wells, then it should be much easier to obtain investment and gain public support. But we just don’t know what those flow rates are going to be yet,” said Corin Taylor, a senior adviser at UKOOG.

Associate Paul Gunn from interna-tional corporate law firm Eversheds adds that this round of onshore licens-ing will help improve the public image of operators, offering them a platform to demonstrate compliance with a regulatory system that is better tailored to their specific operations.

“It will be interesting to see what the appetite for new licenses has been fol-lowing the deadline for applications and the expected award of licences by DECC within the next 12 to 18 months,” said Mr. Gunn.

A ray of light for the industry was the announcement in August 2014 by INEOS, the owner of the Grangemouth petrochemicals plant on Scotland’s east coast, that it had acquired a 51% stake in a 329 sq km shale gas licence adjacent to its plant. Given the Grangemouth facility provides a ready market close at hand for any gas that is discovered, this could be readily converted into a com-mercially viable resource, potentially giving momentum to the sector.

Additional reporting by Nilima Choudhury.

UK

FO

CU

S

“If explorers are allowed to increase exploration and they can obtain good flow

rates, it should be much easier to obtain investment and gain public support”

Corin Taylor, UKOOG

Existing Onshore licences

Area Under Consideration

Current shale gas licences

UK’s Licensing geography

� Much of Britain could be subject to bids, but full details are set to emerge in 2015

36 | Shale Ga S Inve S tm ent GuIde | winter 2014

www.lmkr.com/geographix

®FIRST geology interpretation software on Windows

FIRST to incorporate workflows for unconventional plays

FIRST for seismic-inclusive geosteering

FIRST choice of shale operators

Realizing Your Unconventional Potential For 30 Years