37

BBVA Research – Colombia Outlook 2Q19 / 1 Colombia Outlook 2Q19 April 2019

BBVA Research – Colombia Outlook 2Q19 / 1

Colombia Outlook2Q19

April 2019

Global activity has continued moderating, with a particularly weak performance in exports and industrial sectors. A series of

factors have contributed to activity weakening, especially:

i) structural deceleration of the Chinese economy; ii) protectionism; iii) Uncertainty in Europe related to brexit and the

automotive sector; and iv) the cyclical moderation in the US economy. We expect global growth in 2019 and 2020 of 3.4%.

Central Banks will be more cautious in their hiking cycles in this new scenario and will help to reduce global volatility.

Internal demand, though leading growth in Colombia, will continue showing significant differences within its components.

Investment will accelerate thanks to machinery and equipment. Building construction will be limited in 2019, but will

accelerate in 2020. Civil Works will be very dynamic in 2019, but not as much in 2020 due to the political cycle of regional

governments. On the other hand, private consumption will grow in 2019 and 2020 at similar rates as observed in 2018,

given that a weak consumer confidence and the deterioration of the labor market reduce the capacity of consumption

acceleration. Finally, public expenditure will progressively decelerate.

Inflation will remain close to 3,0% in 2019 and 2020. With activity recovering slowly, controlled inflation will allow the

Central Bank to delay its interest rate hiking cycle further down in 2019, and achieve its neutral level of 4,75% in early

2020. However, Banco de la Republica will remain vigilant of the reasons behind the deterioration of the current account

deficit this year, explained more by investment than consumption, and the mid term structural fiscal adjustment needed.

Key Messages

BBVA Research – Colombia Outlook 2Q19 / 2

BBVA Research – Colombia Outlook 2Q19 / 3

Content

01

02

Global growth remains weak and monetary policy will be cautious

Internal demand boosts economic growth in Colombia

03 Slow recovery and low inflation delay interest rate move for the Central Bank

BBVA Research – Colombia Outlook 2Q19 / 4

01Global growth remains weak and monetary

policy will be cautious

BBVA Research – Colombia Outlook 2Q19 / 5

0.4

0.6

0.8

1.0

1.2

Ma

r-1

4

Se

p-1

4

Ma

r-1

5

Se

p-1

5

Ma

r-1

6

Sep-1

6

Ma

r-1

7

Se

p-1

7

Ma

r-1

8

Se

p-1

8

Ma

r-1

9CI 20% CI 40%

CI 60% Current

Period average Jun-11 to Dec-18 Trend

World GDP growth(Forecasts based on BBVA-GAIN % QoQ)

Source: BBVA Research

Global GDP has moderated more than expected

Global growth has slowed due to China's structural moderation, high uncertainty in Europe, trade protectionism and the cyclical slowdown in the US

A slight improvement is possible in the short, but activity will remain less dynamic than in previous years

BBVA Research – Colombia Outlook 2Q19 / 6

Weak exports and investment, but private consumption

remains relatively robust

World Exports(Thousands of dollars)

PMIs(Level)

Source: BBVA Research based on IMF data Source: BBVA Research based on IHS Markit data

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

Jan-1

6

Ma

r-1

6

Ma

y-16

Jul-1

6

Sep

-16

Nov-1

6

Jan-1

7

Ma

r-1

7

Ma

y-17

Jul-1

7

Sep

-17

Nov-1

7

Jan-1

8

Ma

r-1

8

Ma

y-18

Jul-1

8

Sep

-18

Nov-1

8Nominal exports

Trend

50

51

52

53

54

55

56

57

58

Jan-1

7

Ma

r-1

7

Ma

y-17

Jul-1

7

Sep

-17

Nov-1

7

Jan-1

8

Ma

r-1

8

Ma

y-18

Jul-1

8

Sep

-18

Nov-1

8

Jan-1

9

Global Manufacturing PMI

Global Services PMI

BBVA Research – Colombia Outlook 2Q19 / 7

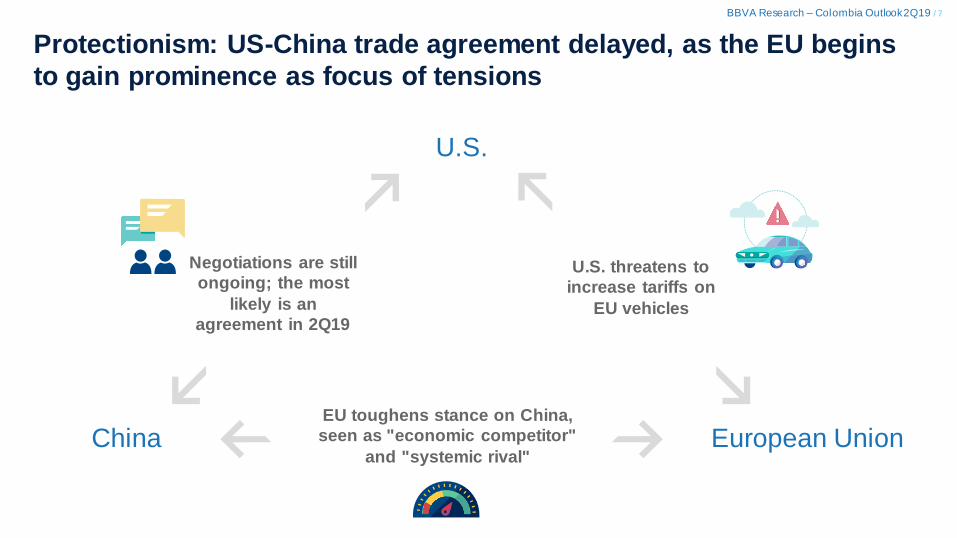

Protectionism: US-China trade agreement delayed, as the EU begins

to gain prominence as focus of tensions

U.S.

China European Union

Negotiations are still

ongoing; the most

likely is an

agreement in 2Q19

U.S. threatens to

increase tariffs on

EU vehicles

EU toughens stance on China,

seen as "economic competitor"

and "systemic rival"

BBVA Research – Colombia Outlook 2Q19 / 8

Growth moderation has caused a shift in monetary policy in the US

and the Eurozone, and new stimuli in China

Fed

Long pause in the

rate hike, but there

could be a hike by the

end of the year

The normalization

(reduction) of the

balance sheet will

end earlier than

expected (September

2019)

Latam and other

emerging countries

There is room for a more

dovish monetary policy

BCE

Postponement

of monetary

normalization

Lower interest

rates for longer

and additional

liquidity

China

Additional monetary

stimulus: RRR and

lending rate reductions

in 2019

Increase in public

deficit, to 2.8% of GDP

in 2019

Tax cuts (2% of GDP)

BBVA Research – Colombia Outlook 2Q19 / 9

Action by central banks and an absence of "accidents" would

enable global growth to soft-land

More signs of global

slowdown

New stimulus

policies

01Protectionism An US-China trade agreement is still likely, despite the delay

02Brexit:Greater uncertainty, for a longer time

03

Financial markets: volatility constrained by central banks’ measures

Assumption on the evolution of the global outlook: no “accidents”

04Oil:Price moderation following the recent upturn

Global growth soft-lands

BBVA Research – Colombia Outlook 2Q19 / 10

Without "accidents", global growth will decelerate gradually

Sube

Se mantiene

BajaSource: BBVA Research

1,0 1,3

Eurozona

2019 2020

2019 2020

3.4 3.4

World

Latam

2019 2020

1.7 2.3

2019 2020

1.4 2.2

Mexico

China

2019 2020

6.0 5.8

US

2019

2.52020

2.0

BBVA Research – Colombia Outlook 2Q19 / 11

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2.00

2.25

2.50

2.75

3.00

3.25

3.50

Dec-1

6

Fe

b-1

7

Apr-

17

Jun-1

7

Aug

-17

Oct-

17

Dec-1

7

Fe

b-1

8

Apr-

18

Jun-1

8

Aug

-18

Oct-

18

Dec-1

8

Fe

b-1

9

10Y US 10Y EZ

Markets: long-term yields excessively low due to cyclical risk and “safe

haven” effect , with volatility limited by central banks' dovish tone

Sovereign debt yields(%)

Equity indexes and Volatility (VIX)(Base 100 in Jan-15 and %)

Source: BBVA Research based on Haver data

8

13

18

23

28

33

38

43

70

80

90

100

110

120

130

140

150

Jan-1

5

Apr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

Apr-

17

Jul-1

7

Oct-

17

Jan-1

8

Apr-

18

Jul-1

8

Oct-

18

Jan-1

9

VIX (rhs) S&P Eurostoxx

Source: BBVA Research based on Haver data

BBVA Research – Colombia Outlook 2Q19 / 12

Volatility reduced in emerging economies, due to a moderation in the

expectation of interest rate hikes by CB and higher commodity prices.

CDS in Latam(Index Jan 2017=100)

Source: BBVA Research with Bloomberg data

Risk levels of emerging countries are very heterogeneussince some countries have to solve their internal and external imbalances

The realization of lower growth forecasts in develop countries and the expected fall in oil prices, could raise risk premium in emerging countries by year end.

50

100

150

200

Jan-1

8

Feb

-18

Ma

r-1

8

Apr-

18

Ma

y-1

8

Jun-1

8

Jul-1

8

Aug-1

8

Sep-1

8

Oct-

18

No

v-1

8

De

c-1

8

Jan-1

9

Feb

-19

Ma

r-1

9

Apr-

19

Brazil Colombia Chile Mexico Peru

BBVA Research – Colombia Outlook 2Q19 / 13

Oil markets: as expected, supply adjustments provided support to

prices in 1Q19, which will likely move down from now onwards

Brent oil prices(USD per barrel, end-of-period)

Production cuts have driven oil prices up (65 dollars per barrel, on average, in 1Q19)

We maintain prospects for lower prices in 2H19 and 2020, on slower economic growth and rising US supply

The lower global demand will also favor a drop in copper prices, although we have revised our forecasts slightly up, mainly due to supply disruptions

In the case of soybeans, we have revised our forecasts slightly upwards, but we continue to expect prices to recover moving forward

50

61

71

62

55

0

10

20

30

40

50

60

70

80

2016 2017 2018 2019 (f) 2020 (f)

Current Previous

Source: BBVA Research based on Haver data

BBVA Research – Colombia Outlook 2Q19 / 14

Global risks: increasing fears about a recession in the US and in the

Eurozone, in spite of central banks’ broader support

Source: BBVA Research

Recession: high

Protectionism: high

Fed’s exit: significantly lower

Recession: on the rise

• Brexit

• Italy

• Surge of Eurosceptic forces in the European Parliament

Protectionism: on the rise

ECB’s exit: significantly lower

Disorderly deleveraging : relatively higher

Protectionism: high

EE.UU.

EZ

-S

ho

rt-t

erm

pro

babilit

y +

- Severity +

CHN

Financial vulnerabilities can amplify the severity of the risks

BBVA Research – Colombia Outlook 2Q19 / 15

02Internal demand boosts economic growth in Colombia

BBVA Research – Colombia Outlook 2Q19 / 16

Recent indicators signal that private consumption will grow in 2019

at a similar rate than in 2018

Consumption leading indicators(Annual variation, %)

Source: BBVA Research, with DANE, ANDI and Fenalco data. * To January for retail sales and imports. To February for employment. And to March for vehicles

5,9

-0,1

-3,5

1,7

6,8

14,7

3,8

-0,9

5,6

10,4

5,6

1,4

9,0

16,1

22,1

0,0

3,3

5,4

0,6 0,8

-5

0

5

10

15

20

25

Retail sales Consumption imports Car sales Employment

1Q18 2Q18 3Q18 4Q18 1Q19*

BBVA Research – Colombia Outlook 2Q19 / 17

Employment growth, in low levels relative to previous periods,

accounts for expected consumption growth stability

Labor market: employment, supply and unemployment(Annual average. growth %y/y and rate in % of LF)

Source: BBVA Research, DANE data

Job creation rate has reduced below the growth of labor supply. As a result, unemployment rate has increased in recent quarters

Lower job creation could stall consumption acceleration

-2

0

2

4

6

8

10

12

14

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Jan-1

5

Jan-1

6

Jan-1

7

Jan-1

8

Jan-1

9Unemployment rate Employment growth

Labor supply growth

BBVA Research – Colombia Outlook 2Q19 / 18

Consumer confidence remains negative due to weak country

assesment. But it has been low for a while ¿structural change?

Consumer confidence(Balance of answers)

Source: BBVA Research, Fedesarrollo data

Propensity to by durable goods and homes(Balance of answers)

22

-6 -5

95

-10-4

9

-27-28

-8 -11

-29-24

28

9 813

94 6

-40

-30

-20

-10

0

10

20

30

40

Avg

.11-1

4

Avg

.15-1

7

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

*

Avg

.11-1

4

Avg

.15-1

7

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

*

Avg

.11-1

4

Avg

.15-1

7

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19*

Consumerconfidence

Countryassessment

Householdassessment

-50

-40

-30

-20

-10

0

10

20

30

40

50

Feb

-11

Oct-

11

Jun-1

2

Fe

b-1

3

Oct-

13

Jun-1

4

Fe

b-1

5

Oct-

15

Jun-1

6

Feb

-17

Oct-

17

Jun-1

8

Feb

-19

Durable goods Home

BBVA Research – Colombia Outlook 2Q19 / 19

On the other hand, leading indicators related to investment in

machinery and equipment show a favorable dynamic

Investment leading indicators(Annual variation, %)

Source: BBVA Research, DANE, XM and La Galería Inmobiliaria data. * Imports and industrial production as of January. Energy demand in February. House sales to March

3,7

0,12,6

-5,2

9,1

4,92,8

-2,8

7,4

3,5 4,12,6

25,2

3,1 3,7

12,410,1

3,04,5

-7,2-12

-7

-2

3

8

13

18

23

28

Capital goods imports Industrial production Energy demand Housing sales

1Q18 2Q18 3Q18 4Q18 1Q19*

BBVA Research – Colombia Outlook 2Q19 / 20

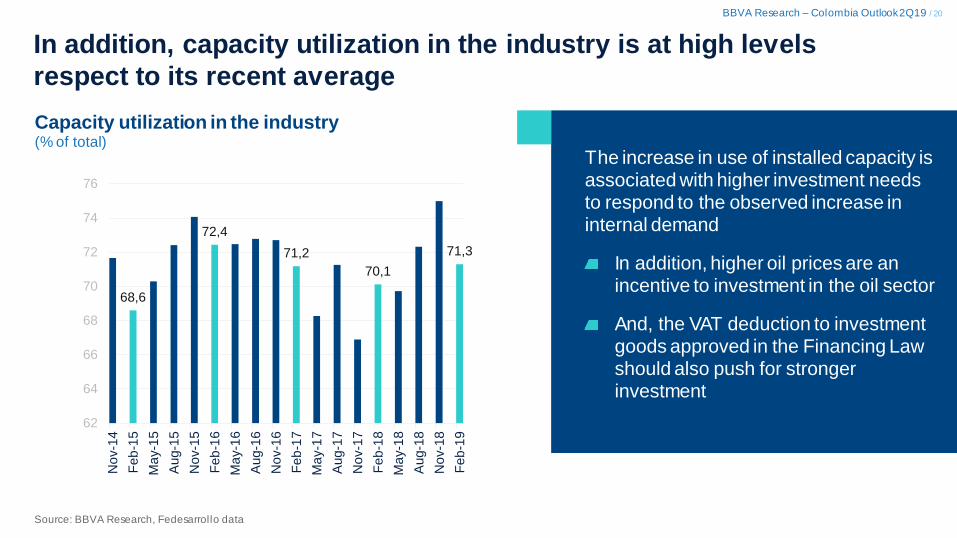

In addition, capacity utilization in the industry is at high levels

respect to its recent average

Capacity utilization in the industry(% of total)

Source: BBVA Research, Fedesarrollo data

The increase in use of installed capacity is associated with higher investment needs to respond to the observed increase in internal demand

In addition, higher oil prices are an incentive to investment in the oil sector

And, the VAT deduction to investment goods approved in the Financing Law should also push for stronger investment

68,6

72,4

71,2

70,1

71,3

62

64

66

68

70

72

74

76

No

v-1

4

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

Ma

y-1

8

Aug-1

8

No

v-1

8

Feb

-19

BBVA Research – Colombia Outlook 2Q19 / 21

Private consumption will boost total consumption from the end of

2019 and investment in machinery and equipment total investment

Final consumption: private and public(Annual variation, %)

Source: BBVA Research, DANE data

Total investment(Annual variation, %)

4,6

3,1

1,6

2,1

3,5 3,43,6

4,7 4,9

1,8

3,8

5,9

4,1

2,9

0

1

2

3

4

5

6

7

20

14

20

15

20

16

20

17

20

18

20

19 (

f)

20

20 (

f)

Private consumption Public consumption

-10

-5

0

5

10

15

20

14

20

15

20

16

20

17

20

18

20

19 (

f)

20

20 (

f)

Total investment Other investment*

Investment in construction

BBVA Research – Colombia Outlook 2Q19 / 22

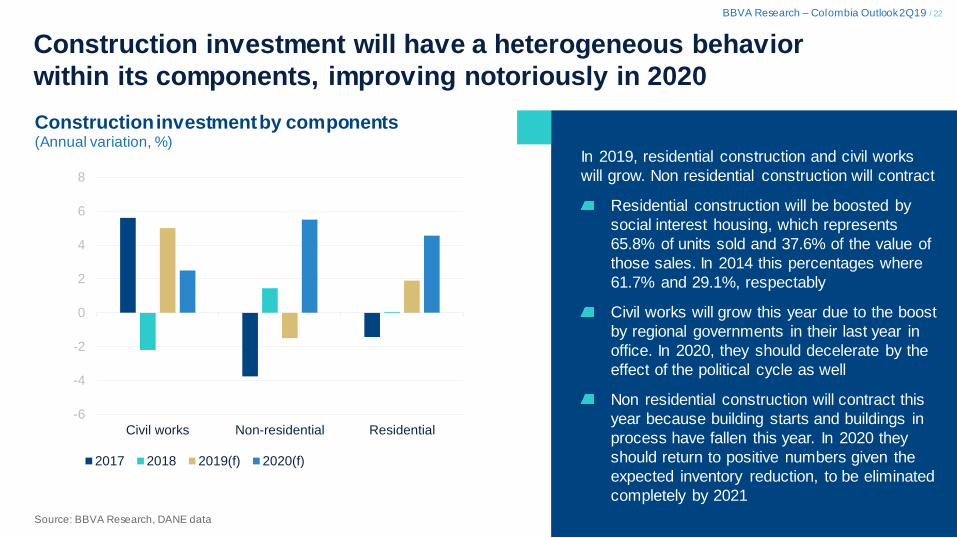

Construction investment will have a heterogeneous behavior

within its components, improving notoriously in 2020

Construction investment by components(Annual variation, %)

Source: BBVA Research, DANE data

In 2019, residential construction and civil works

will grow. Non residential construction will contract

Residential construction will be boosted by

social interest housing, which represents

65.8% of units sold and 37.6% of the value of

those sales. In 2014 this percentages where

61.7% and 29.1%, respectably

Civil works will grow this year due to the boost

by regional governments in their last year in

office. In 2020, they should decelerate by the

effect of the political cycle as well

Non residential construction will contract this

year because building starts and buildings in

process have fallen this year. In 2020 they

should return to positive numbers given the

expected inventory reduction, to be eliminated

completely by 2021

-6

-4

-2

0

2

4

6

8

Civil works Non-residential Residential

2017 2018 2019(f) 2020(f)

BBVA Research – Colombia Outlook 2Q19 / 23

Negative contribution by non residential construction is driven

by a fall in work in process since the end of last year

Construction under process(Million of sq. meters, end of year)

Source: BBVA Research, DANE data

Between December 2017 and 2018, work in process fell by 15%. Given this, construction culmination will be limited this year by the reduction of sq. meters in process

In particular, residential work in process fell by 12% and non residential fell by 22%

0

5

10

15

20

25

30

35

Dec-14 Dec-15 Dec-16 Dec-17 Dec-18

Residential Non - residential Total buildings

BBVA Research – Colombia Outlook 2Q19 / 24

Total investment will increase its contribution to growth. While

public expenditure will reduce it slowly

GDP Growth and contributions(Annual variation, contribution to the growth rate, %)

Source: BBVA Research, DANE data

Private consumption remains as the most relevant component in GDP, more for its contribution than for its dynamics, despite the expected acceleration of Investment

In 2020, investment will contribute with a point of growth, highest contribution since 2014

External demand, will continue to reduce growth, given that the expected dynamic of imports is higher than the expected behavior of imports

1,4

2,73,0

3,3

-1

0

1

2

3

4

2017 2018 2019(f) 2020(f)

External demand Private consumption

Public consumption Investment in construction

Investment without construction GDP

BBVA Research – Colombia Outlook 2Q19 / 25

03Slow recovery and low inflation delay

interest rate move for Banco de la Republica

BBVA Research – Colombia Outlook 2Q19 / 26

Headline inflation will be close to the 3.0% Central Bank target, despite

the recent upward pressure in administered and food prices

Headline and core inflation(Annual variation, %)

Source: BBVA Research, DANE data

Inflation by type of expenditure (Annual variation, %)

3,21

2,40

3,26

2,0

2,5

3,0

3,5

4,0

4,5

5,0

5,5

6,0

Ma

r-1

7

Ma

y-1

7

Jul-1

7

Sep-1

7

No

v-1

7

Jan-1

8

Ma

r-1

8

Ma

y-1

8

Jul-1

8

Sep-1

8

No

v-1

8

Jan-1

9

Ma

r-1

9

Headline

Non food non administered prices CPI

Non food CPI

6,34

3,29

0,94

3,27

0

1

2

3

4

5

6

7

Feb

-18

Ma

r-1

8

Apr-

18

Ma

y-1

8

Jun-1

8

Jul-1

8

Aug-1

8

Sep-1

8

Oct-

18

No

v-1

8

De

c-1

8

Jan-1

9

Feb

-19

Ma

r-1

9

Administered prices Non Tradables

Tradables Food

BBVA Research – Colombia Outlook 2Q19 / 27

Food prices continue to pressure this years result, but core inflation

will continue reducing allowing for headline inflation to end at 3,0%

Source: BBVA Research, DANE data

Headline and core inflation(Annual variation, %)

Shocks revived by inflation at the beginning of the year seem transitory and are already moderating

In the first quarter, food inflation accelerated marginally by the decisions of reducing crops to prevent the effects of “el Niño” and by energy costs driven by a reduction in the levels of water reservoirs

We believe this shocks are transitory and inflation will return to its previous trend soon

-1

0

1

2

3

4

5

De

c-1

7

Feb

-18

Apr-

18

Jun-1

8

Aug-1

8

Oct-

18

De

c-1

8

Feb

-19

Apr-

19

Jun-1

9

Aug-1

9

Oct-

19

De

c-1

9

Fe

b-2

0

Apr-

20

Jun-2

0

Aug-2

0

Oct-

20

De

c-2

0

Headline Core Food Target Range

(f)

BBVA Research – Colombia Outlook 2Q19 / 28

The exchange rate within a relatively narrow range will help to reduce

transmission effects on inflation in 2019 and 2020

Exchange rate(pesos per dollar)

* Corresponds to year-end data.

Source: BBVA Research projections and Banrep data

The exchange rate will face opposing forces that

will restrain its net upward and downward

movements (though maintaining significant

volatility) within a narrow range

Brent oil prices, though high currently, will

reduce gradually to USD62 per barrel at the

end of 2019 and to USD55 per barrel in

2020. This will be a factor that pushes the

exchange rate upward, and that also explains

part of the deterioration of the external

balance

At the same time, lower expected interest

rates and volatility in developed countries,

due to more cautious central banks, will

cushion part of the preceding effect

2.951 2.956

3.141

3.088

2500

2600

2700

2800

2900

3000

3100

3200

3300

Jan-1

7

Apr-

17

Jul-1

7

Oct-

17

Jan-1

8

Apr-

18

Jul-1

8

Oct-

18

Jan-1

9

Apr-

19

Jul-1

9

Oct-

19

Jan-2

0

Apr-

20

Jul-2

0

Oct-

20

BBVA Research – Colombia Outlook 2Q19 / 29

In a context of moderate growth and low inflation, the economy will

experience a higher external deficit

Current account deficit and its financing(% of GDP. With no additional financing resources to accumulate IR***)

Source BBVA Research with Banrep data. *Portfolio investment and debt flows,

mainly;**Foreign direct investment; *** International reserves

The deterioration of the external deficit will be

explained more by investment than consumption,

even though in the latter, one ought to be vigilant

of the fiscal consolidation and consequently on

public expenditure. The external financing will be

also relevant

If the external deficit (external financing) is

used more for investment, as in 2019 and

2020, rather than what happened in 2018,

boosted by consumption, the Central Bank

may be less worrisome of such deficit

On the other hand, between 2014-2015 and

2018-2020 foreign direct investment will not

be enough to fully finance the external deficit

and some alternative resources are needed,

such as capital of debt inflows. This fact in a

more complex financial world may lead to a

source of risks that should be monitored

4,2 4,04,9

4,4

3,3 3,7 3,7

0,92,3

0,50,6 0,3

5,2

6,3

4,3

3,3

3,84,3

4,0

0

1

2

3

4

5

6

7

20

14

20

15

20

16

20

17

20

18

20

19(f

)

20

20(f

)

FDI** Other necessary sources* Current account deficit

BBVA Research – Colombia Outlook 2Q19 / 30

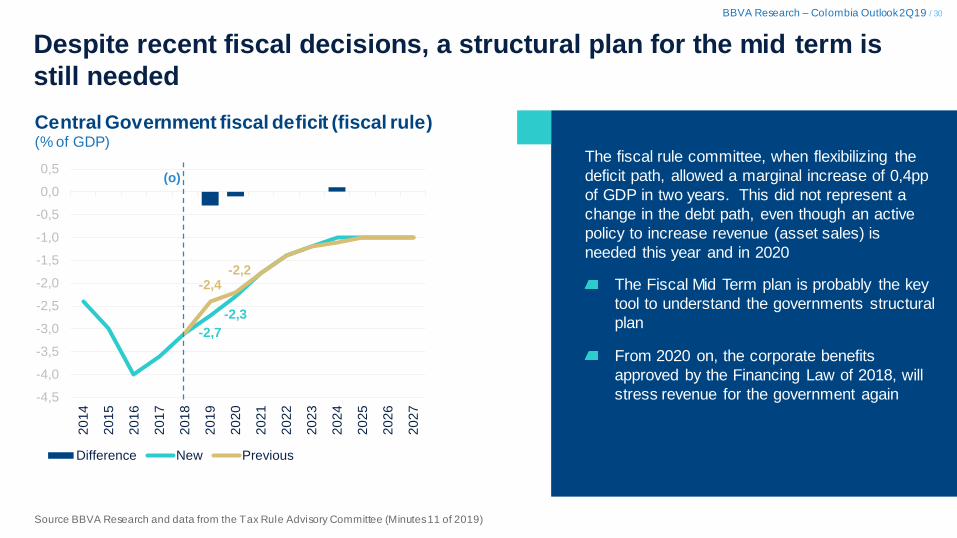

Despite recent fiscal decisions, a structural plan for the mid term is

still needed

Central Government fiscal deficit (fiscal rule)(% of GDP)

Source BBVA Research and data from the Tax Rule Advisory Committee (Minutes 11 of 2019)

The fiscal rule committee, when flexibilizing the

deficit path, allowed a marginal increase of 0,4pp

of GDP in two years. This did not represent a

change in the debt path, even though an active

policy to increase revenue (asset sales) is

needed this year and in 2020

The Fiscal Mid Term plan is probably the key

tool to understand the governments structural

plan

From 2020 on, the corporate benefits

approved by the Financing Law of 2018, will

stress revenue for the government again

-2,7

-2,3

-2,4-2,2

-4,5

-4,0

-3,5

-3,0

-2,5

-2,0

-1,5

-1,0

-0,5

0,0

0,5

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

Difference New Previous

(o)

BBVA Research – Colombia Outlook 2Q19 / 31

With low inflation, weak demand and a deteriorating external imbalance

(investment driven), BanRep can wait until year end to hike rates

BanRep policy interest rate(%)

Source: BBVA Research and Banrep data

In addition, lower interest rates in the world, credit growth around nominal GDP growth and low pressure by internal demand will allow the neutral interest rate to stand at 4.75%

In this context the Central Bank could increase its rate 25bp in the fourth quarter of 2019, with a downward bias towards remaining stable for the whole year. For 2020 we expect a new increase of 25bp, reaching 4.75%

3,0

3,5

4,0

4,5

5,0

5,5

6,0

6,5

7,0

7,5

8,0

Jan-1

5A

pr-

15

Jul-1

5O

ct-

15

Jan-1

6A

pr-

16

Jul-1

6O

ct-

16

Jan-1

7A

pr-

17

Jul-1

7O

ct-

17

Jan-1

8A

pr-

18

Jul-1

8O

ct-

18

Jan-1

9A

pr-

19

Jul-1

9O

ct-

19

Jan-2

0A

pr-

20

Jul-2

0O

ct-

20

(f)

Key Messages

Global activity has continued moderating, with a particularly weak performance in exports and industrial sectors. A series of

factors have contributed to activity weakening, especially:

i) structural deceleration of the Chinese economy; ii) protectionism; iii) Uncertainty in Europe related to brexit and the

automotive sector; and iv) the cyclical moderation in the US economy. We expect global growth in 2019 and 2020 of 3.4%.

Central Banks will be more cautious in their hiking cycles in this new scenario and will help to reduce global volatility.

Internal demand, though leading growth in Colombia, will continue showing significant differences within its components.

Investment will accelerate thanks to machinery and equipment. Building construction will be limited in 2019, but will

accelerate in 2020. Civil Works will be very dynamic in 2019, but not as much in 2020 due to the political cycle of regional

governments. On the other hand, private consumption will grow in 2019 and 2020 at similar rates as observed in 2018,

given that a weak consumer confidence and the deterioration of the labor market reduce the capacity of consumption

acceleration. Finally, public expenditure will progressively decelerate.

Inflation will remain close to 3,0% in 2019 and 2020. With activity recovering slowly, controlled inflation will allow the

Central Bank to delay its interest rate hiking cycle further down in 2019, and achieve its neutral level of 4,75% in early

2020. However, BanRep will remain vigilant of the reasons behind the deterioration of the current account deficit this year,

explained more by investment than consumption, and the mid term structural fiscal adjustment needed.

BBVA Research – Colombia Outlook 2Q19 / 32

BBVA Research – Colombia Outlook 2Q19 / 33

Colombia Outlook2Q19

April 2019

BBVA Research – Colombia Outlook 2Q19 / 34

Colombia Outlook2Q19 (Annex)

April 2019

BBVA Research – Colombia Outlook 2Q19 / 35

Main macroeconomic variables

Tabla A1. Macroeconomicforecast

2015 2016 2017 2018 2019 2020

GDP (% y/y) 3,0 2,1 1,4 2,7 3,0 3,3

Private consumption (% y/y) 3,1 1,6 2,1 3,5 3,4 3,6

Public consumption (% y/y) 4,9 1,8 3,8 5,9 4,1 2,9

Fixed investment (% y/y) 2,8 -2,9 1,9 1,1 2,9 4,0

Inflation (% y/y, eoy) 6,8 5,7 4,1 3,2 3,0 3,2

Inflation (% y/y, average) 5,0 7,5 4,3 3,2 3,0 3,1

Exchange rate (eoy) 3.149 3.001 2.984 3.250 3.150 3.020

Devaluation (%, eoy) 31,6 -4,7 -0,3 7,3 -1,9 -4,1

Exchange rate (average) 2.742 3.055 2.951 2.956 3.141 3.088

Devaluation (%, eoy) 37.0 11,4 -3,4 0,2 6,1 -1,6

Politcy Rate (%, eoy) 5,75 7,50 4,75 4,25 4,50 4,75

DTF rate (%, eoy) 5,2 6,9 5,3 4,5 4,7 5,

Fiscal Balance (% GPD) -3,0 -4,0 -3,6 -3,1 -2,7 -2,3

Current Account (% GDP) -6,5 -4,4 -3,3 -3,8 -4,3 -4,0

Urban Unemployment Rate (%, eoy) 9,8 9,8 9,8 10,7 10,6 10,5

BBVA Research – Colombia Outlook 2Q19 / 36

Main macroeconomic variables

Tabla A2. Quarterly macroeconomic forecast

GDP

(% y/y)

Inflation

(% y/y, eoy)

Exchange rate

(vs. USD, eoy)

Policy Rate

(%, eoy)

Q1 16 2,4 8,0 3.022 6,50

Q2 16 2,0 8,6 2.916 7,50

Q3 16 1,8 7,3 2.880 7,75

Q4 16 2,2 5,7 3.001 7,50

Q1 17 1,2 4,7 2.880 7,00

Q2 17 1,4 4,0 3.038 5,75

Q3 17 1,6 4,0 2.937 5,25

Q4 17 1,3 4,1 2.984 4,75

Q1 18 2,1 3,1 2.780 4,50

Q2 18 2,9 3,2 2.931 4,25

Q3 18 2,7 3,2 2.972 4,25

Q4 18 2,8 3,2 3.250 4,25

Q1 19 3,0 3,2 3.175 4,25

Q2 19 2,7 2,8 3.130 4,25

Q3 19 2,9 2,9 3.143 4,25

Q4 19 3,1 3,0 3.150 4,50

Q1 20 3,2 3,0 3.139 4,75

Q2 20 3,2 3,0 3.090 4,75

Q3 20 3,4 3,1 3.051 4,75

Q4 20 3,6 3,2 3.020 4,75

BBVA Research – Colombia Outlook 1Q19 / 37

This document, prepared by the BBVA Research Department, is informative in nature and contains data, opinions or estimates as at the date of its publication. These derive from the

department’s own research or are based on sources believed to be reliable, and have not been independently verified by BBVA. BBVA therefore makes no guarantee, either express or

implied, as to the document's accuracy, completeness or correctness.

Any estimates contained in this document have been made in accordance with generally accepted methods and are to be taken as such, i.e. as forecasts or projections. Historical trends in

economic variables (positive or negative) are no guarantee that they will evolve in the same way in the future.

The contents of this document are subject to change without prior notice, depending on (for example) the economic context or market fluctuations. BBVA assumes no commitment to update

any of the content or communicate such changes.

BBVA assumes no liability for any loss, direct or indirect, that may result from the use of this document or its contents.

Neither this document nor its contents constitute an offer, invitation or solicitation to acquire, disinvest or obtain any in terest in assets or financial instruments, nor can they form the basis of

any contract, undertaking or decision of any kind.

In particular, as regards investment in financial assets that could be related to the economic variables referred to in this document, readers should note that in no case should investment

decisions be made based on the contents of this document; and that any persons or entities who may potentially offer them investment products are legally obliged to provide all the

information they need to take such decisions.

The contents of this document are protected by intellectual property law. The reproduction, processing, distribution, public dissemination, availabil ity, taking of excerpts, reuse, forwarding or

use of the document in any way and by any means or process is expressly prohibited, except where this is legally permitted or expressly authorised by BBVA.

BBVA Colombia is a credit institution, overseen by the Superintendence of Finance.

BBVA Colombia promotes such documents for purely academic ends. It assumes no responsibil ity for the decisions that are taken on the basis of the information set forth herein, nor may it

be deemed to be a tax, legal or financial consultant. Neither shall it be liable for the quality or content thereof.

BBVA Colombia is holder of the copyright of all textual and graphic content of this document, which is protected by copyright law and other relevant Colombian and international legislation.

The use, circulation or copy thereof without the express prior authorisation of BBVA Colombia is prohibited.

Legal Notice