26

Slide 3-1 3 CHAPTER 3 PARTIALLY OWNED CREATED SUBSIDIARIES

| Date post: | 03-Jan-2016 |

| Category: |

Documents |

| Upload: | diana-joseph |

| View: | 219 times |

| Download: | 0 times |

Slide 3-1

3 CHAPTER 3

PARTIALLY OWNED CREATED SUBSIDIARIES

Slide 3-2

3 FOCUS OF CHAPTER 3

Partially Owned Created Subsidiaries Preparing Consolidated Statements:

The Cost Method The Equity Method

Control Other Than by Owning a Majority Voting Interest

Unconsolidated Subsidiaries--Ways to Value the Parent’s Investment

Taxation of domestic subsidiaries.

Slide 3-3

3 Proportional vs. Full Consolidation: At Opposite Ends of the Spectrum

Propor-tional Full

Percent consolidated. < 100% 100%

Reports NCI amounts.. NO YES

Complies--U.S. GAAP.. NO YES

Relative complexity.. EASY HARD

Slide 3-4

3

ParentCompanyConcept

EconomicUnit

ConceptPercent consolidated...... 100% 100%NCI reported as equity.. NO YESCurrent U.S. GAAP........ YES YESFASB’s 1995 proposedGAAP (now on hold)….. NO YES

Parent Company Concept vs. Economic Unit Concept: Not Much Difference for “Created “ Subsidiaries

Slide 3-5

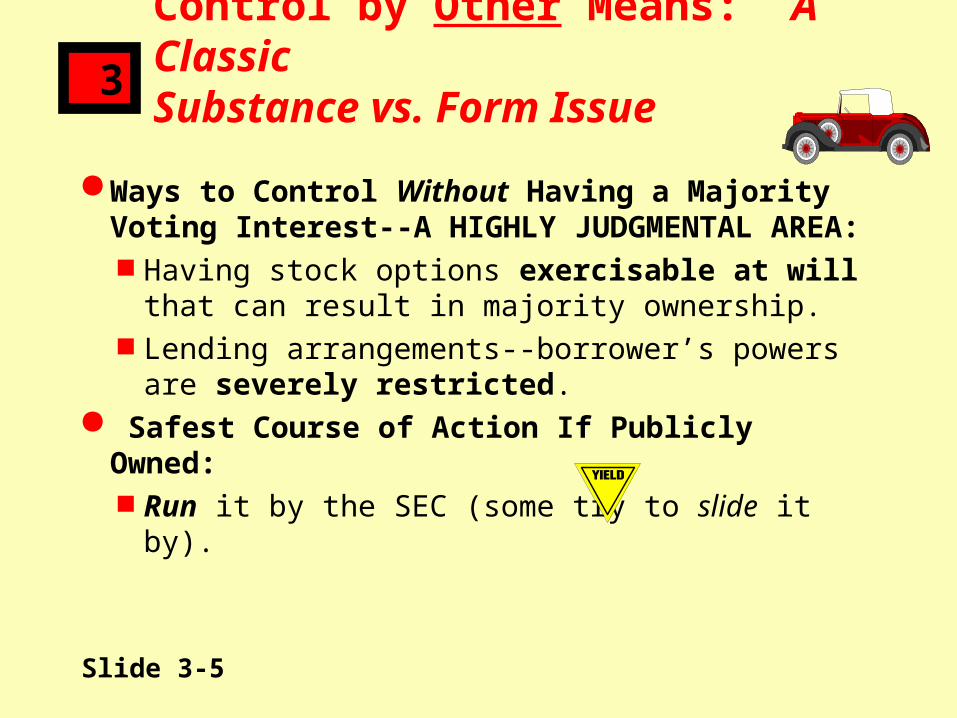

3 Control by Other Means: A ClassicSubstance vs. Form Issue

Ways to Control Without Having a Majority Voting Interest--A HIGHLY JUDGMENTAL AREA: Having stock options exercisable at will

that can result in majority ownership. Lending arrangements--borrower’s powers

are severely restricted. Safest Course of Action If Publicly

Owned: Run it by the SEC (some try to slide it by).

Slide 3-6

3 Unconsolidated Subsidiaries: 100% Ownership Situations

Permissible Valuation Methods(for when control has been lost): Equity Method--but ONLY IF

significant influence exists. Cost Method--makes sense to use

when realization of sub’s expected future earnings is doubtful. The default method if NO

significant influence exists.

Slide 3-7

3 Unconsolidated Subsidiaries: Partial Ownerships--NCI Shares Are NOT Publicly Traded

Permissible Valuation Methods(for when control has been lost): Equity Method--but ONLY IF

significant influence exists. Cost Method.

The default method if NO significant influence exists.

Slide 3-8

3 Unconsolidated Subsidiaries:Partial Ownerships--NCI SharesARE Publicly Traded

Permissible Valuation Methods(for when control has been lost): Equity Method--but ONLY IF significant

influence exists.

Fair Value Method (the new kid)--must use if significant influence does NOT exist.

WSJ--12/31/04....”33 7/8”

Look for a new kid on the block.

Slide 3-9

3 Review Question #1

Which of the following is NOT permitted under GAAP?

A. The economic unit concept.B. The parent company concept.C. Full consolidation.D. Proportional consolidation.E. None of the above.

Slide 3-10

3 Review Question #1--With Answer

Which of the following is NOT permitted under GAAP?

A. The economic unit concept.B. The parent company concept.C. Full consolidation.D. Proportional consolidation.E. None of the above.

Slide 3-11

3 Review Question #2

The noncontrolling interest (NCI) is reported OUTSIDE consolidated stockholders’ equity under:

A. The economic unit concept.B. The parent company concept.C. Full consolidation.D. Proportional consolidation.E. None of the above.

Slide 3-12

3 Review Question #2--With Answer

The noncontrolling interest (NCI) is reported OUTSIDE consolidated stockholders’ equity under:

A. The economic unit concept.B. The parent company concept.C. Full consolidation.D. Proportional consolidation.E. None of the above.

Slide 3-13

3 Review Question #3

The noncontrolling interest (NCI) is reported AS PART OF consolidated stockholders’ equity under:

A. The economic unit concept.B. The parent company concept.C. Full consolidation.D. Proportional consolidation.E. None of the above.

Slide 3-14

3 Review Question #3--With Answer

The noncontrolling interest (NCI) is reported AS PART OF consolidated stockholders’ equity under:

A. The economic unit concept.B. The parent company concept.C. Full consolidation.D. Proportional consolidation.E. None of the above.

Slide 3-15

3 Review Question #4

On 1/1/04, Parco invested $900,000 in Sarco (90%-owned). For 2004, Sarco: (1) earned $60,000, (2) declared dividends of $50,000, and (3) paid dividends of $40,000. What amounts does Parco report? Cost EquityInvestment income for 2004.....

Investment in Sarco at Y/E......Retained earnings increase.......

Slide 3-16

3 Review Question #4--With Answer

On 1/1/04, Parco invested $900,000 in Sarco (90%-owned). For 2004, Sarco: (1) earned $60,000, (2) declared dividends of $50,000, and (3) paid dividends of $40,000. What amounts does Parco report? Cost EquityInvestment income for 2004.....

Investment in Sarco at Y/E......Retained earnings increase.......

$45,000 $54,000

$900,000 $909,000

$45,000 $54,000

Slide 3-17

3 Review Question #5

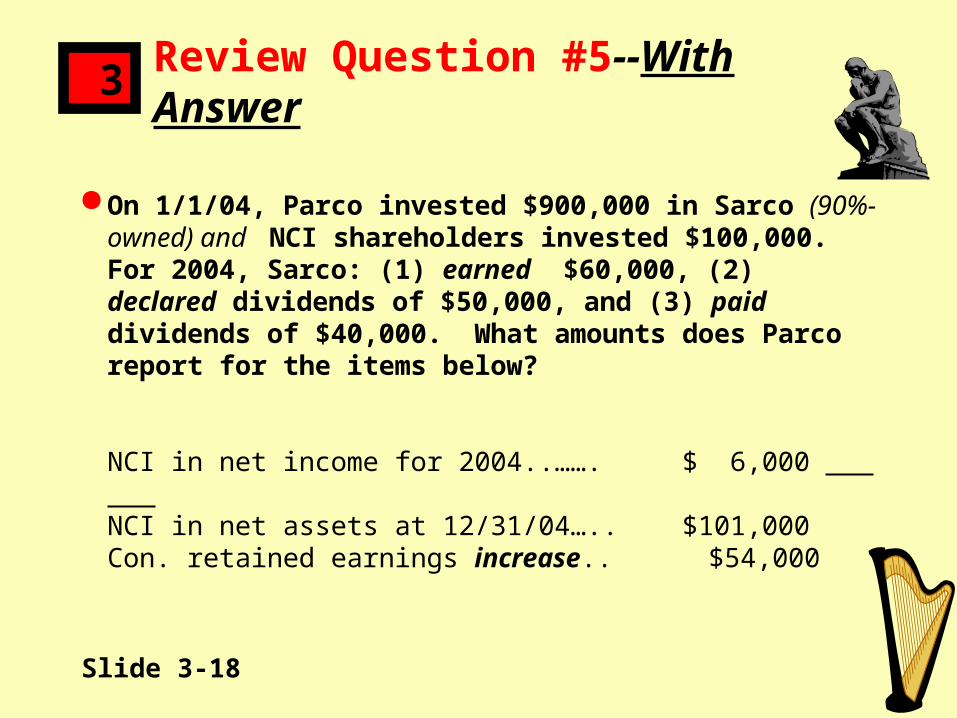

On 1/1/04, Parco invested $900,000 in Sarco (90%-owned) and NCI shareholders invested $100,000. For 2004, Sarco: (1) earned $60,000, (2) declared dividends of $50,000, and (3) paid dividends of $40,000. What amounts does Parco report for the items below? NCI in net income for 2004..……. _________ NCI in net assets at 12/31/04….. _________Con. retained earnings increase.. _________

Slide 3-18

3 Review Question #5--With Answer

On 1/1/04, Parco invested $900,000 in Sarco (90%-owned) and NCI shareholders invested $100,000. For 2004, Sarco: (1) earned $60,000, (2) declared dividends of $50,000, and (3) paid dividends of $40,000. What amounts does Parco report for the items below? NCI in net income for 2004..……. $ 6,000 NCI in net assets at 12/31/04….. $101,000 Con. retained earnings increase.. $54,000

Slide 3-19

3 Review Question #6

A 100%-owned subsidiary is NOT consolidated. The parent could definitely NOT use:

A. The cost method B. The equity method. C. The lower of cost or market method. D. The fair market value method. E. None of the above.

Slide 3-20

3 Review Question #6--With Answer

A 100%-owned subsidiary is NOT consolidated. The parent could definitely NOT use:

A. The cost method B. The equity method. C. The lower of cost or market method. D. The fair market value method. E. None of the above.

Slide 3-21

3 Review Question #7

A LESS THAN 100%-owned subsidiary is NOT consolidated--the NCI shares ARE publicly traded. The parent definitely could NOT use:

A. The cost methodB. The equity method.C. The fair market value method.D. None of the above.

Slide 3-22

3 Review Question #7--With Answer

A LESS THAN 100%-owned subsidiary is NOT consolidated--the NCI shares ARE publicly traded. The parent definitely could NOT use:

A. The cost methodB. The equity method.C. The fair market value method.D. None of the above.

Slide 3-23

3 End of Chapter 3(Appendix material follows)

Time to Clear Things Up--Any Questions?

Slide 3-24

3 Appendix: Domestic Subs: Recording Taxes at Parent Level on Sub’s Income

Double vs. Triple Taxation--Ways to Easily Avoid the THIRD Tax: Own 80% or More of Sub’s Stock:

Can file a consolidated tax return or File separate tax returns--parent

uses a dividend received

deduction of 100%.Sub files its own IRS Form 1120

Slide 3-25

3 Appendix: Consolidated Tax Returns--Advantages Versus Disadvantages

Major Advantages: Can offset X’s LOSS against Y’s INCOME. Can offset X’s CAPITAL LOSS against

Y’s CAPITAL GAIN. Avoids Sec. 482 transfer pricing problems.

Major Disadvantages: X’s loss on intercompany sale is deferred. Complexity.

Slide 3-26

3 Appendix: Domestic Subs: Less Than 80% Ownership Situations

Triple Taxation CANNOT be Entirely Avoided: Dividend received deduction is only 80%. FASB: Parent must record any triple tax in

the year in which sub earns its income--NO EXCEPTIONS ARE ALLOWED FOR DOMESTIC SUBSIDIARIES.

Sub must file its own IRS Form 1120