INVENTORY MANAGEMENT INTRODUCTION: •What is inventory? •Why is inventory important in supply chain management? •The five rights with focus on the right QUANTITY Inventory and Warehouse Management for Business Professionals 2014

Transcript

INVENTORY MANAGEMENT

INTRODUCTION: •What is inventory?

•Why is inventory important in supply chain management?

•The five rights with focus on the right QUANTITY

Inventory and Warehouse Management for Business Professionals 2014

Inventory and Warehouse Management for Business Professionals 2014

The institute of Logistics and Transport defines

inventory as a term used to describe :

•All the goods and materials held by the organization for sale or use.

• A list of items held in stock.

An alternative definition is ; materials in a supply chain or in a

segment of a supply chain , expressed in quantities , locations and or

values , also called stock

Inventory and Warehouse Management for Business Professionals 2014

CASE EXAMPLE:

Power generation company : inventory is classified as materials used

to support the power generation activity and consists of Stock, Non

stock and special items inventory

Inventory and Warehouse Management for Business Professionals 2014

Why is inventory important in supply chain management? A supply chain is the process that involves the creation or manufacture

of a finished good or product from raw material stage. It involves

many processes of which materials or stock must be a part of.

Inventory might be responsible for the very existence of a supply

chain as materials and the proper management of materials promotes

customer satisfaction and eventual profit.

Inventory and Warehouse Management for Business Professionals 2014

The five rights with focus on the right QUANTITY

The course work seeks to discuss ways of holding the right

quantity or just the right amount of inventory for the job. The

right quantity must emphasize the right amount of stock to hold

at any given time without any negative impact to the

organization..

Inventory and Warehouse Management for Business Professionals 2014

Inventory and Warehouse Management for Business Professionals 2014

In a popular store on High street San Fernando, stock levels have

been experiencing a very high turnover rating. Outline two

advantages and two disadvantages of this behavior to the

organization.

My Question

Inventory and Warehouse Management for Business Professionals 2014

- Inventory Manager as a Money Manager

- Inventories place on the Organization Balance Sheet

- Inventory Management Cycle

Inventory and Warehouse Management for Business Professionals 2014

Inventory manager as a money manager

Inventories reflect capital tied up in stock. In other words, inventory

or monies spent on stock can be used for something else. This cost

can be used to pay bills, wages, salaries, bonuses and monies can also

be reused for the purchase of some viable capital equipment or future

investment.

Apart from this, it is difficult to convert inventory immediately into

cash. Take for instance a warehouse filled with bearings some 15

years old or a roll on roll off dealer with 20 cars - wanting to get cash

the following day to pay off a loan with the intention of selling off

stock. In most cases it is highly unlikely .

Inventory and Warehouse Management for Business Professionals 2014

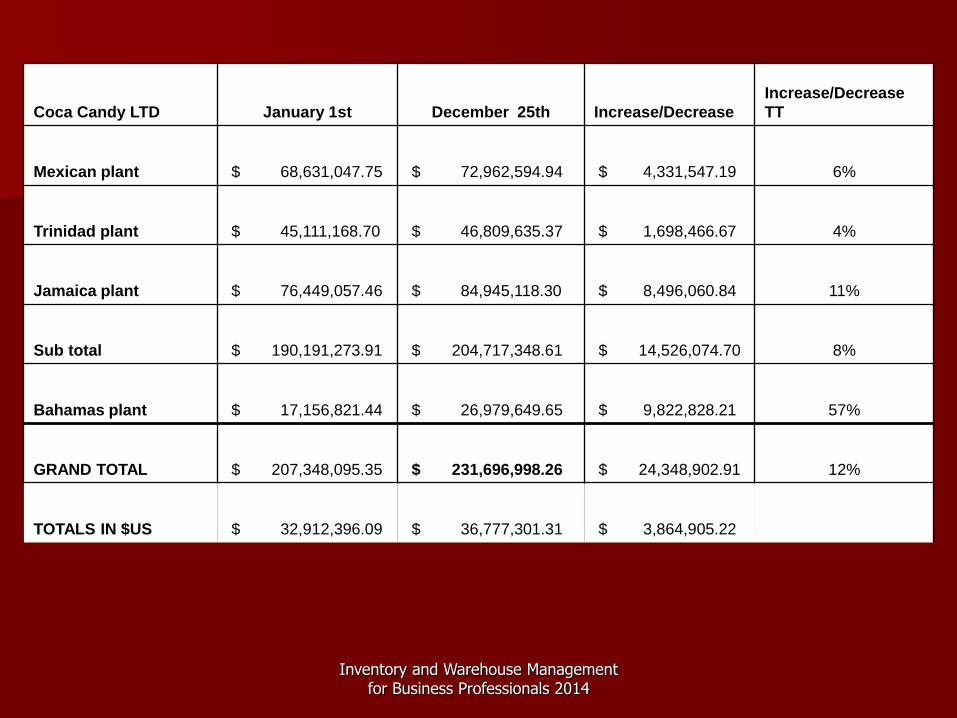

Before we get to the cost of holding stock, it is important that we

observe as managers, the growth of our inventories and seek

answers from users / stakeholders for growth. When inventory

grows, the holding cost and the high value on the balance sheet also

grows. See below.

Inventory and Warehouse Management for Business Professionals 2014

Coca Candy LTD January 1st December 25th Increase/Decrease

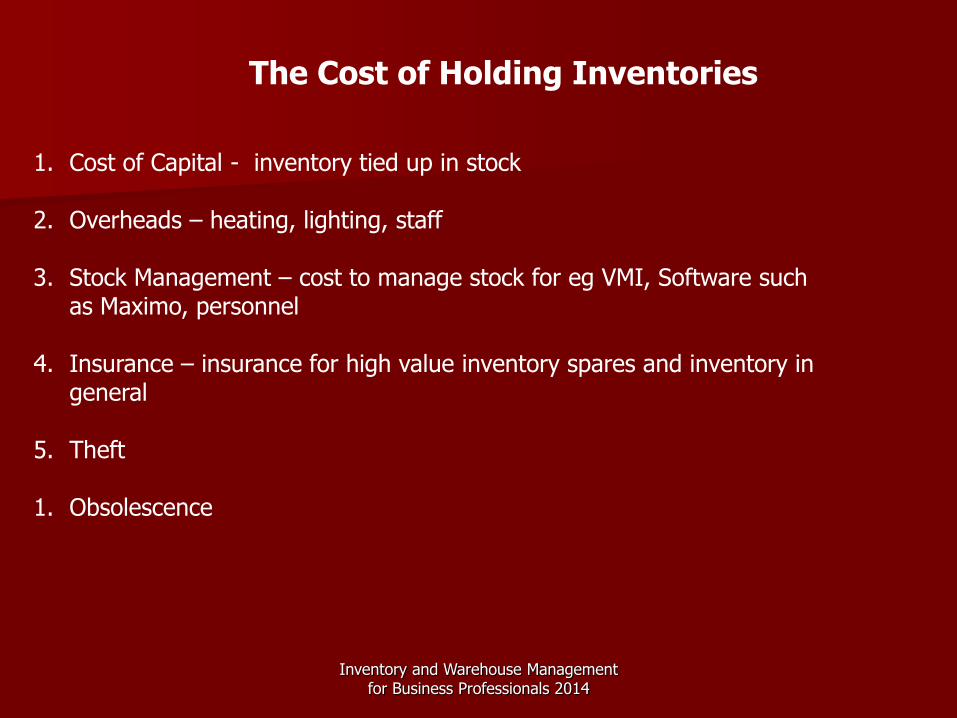

•Stock management. Management of inventory comes with a cost. Such

would include inventory software such as maximo, personnel that are

qualified

•Stores security and insurance. Cost to insure inventory.

•Stock deterioration , loss and obsolescence.

Inventory and Warehouse Management for Business Professionals 2014

•Stock deterioration , loss and obsolescence.

Inventory and Warehouse Management for Business Professionals 2014

Reasons for having inventory. Is it necessary in

your organization ?

Inventory and Warehouse Management for Business Professionals 2014

•Reduce risk of supplier failure.

•To protect against lead time uncertainty

•Hedge against shortages

•To take advantage of discounts

•To meet unexpected demands

Inventory and Warehouse Management for Business Professionals 2014

LET’S DISCUSS THESE REASONS

Inventory and Warehouse Management for Business Professionals 2014

Inventories place on the Organization Balance Sheet

Inventories are reflected in the balance sheet of the organization’s accounts. It is also part of the current assets of the balance sheet. Inventories can consist of raw material , finished goods and work in progress. Inventories can be seen often, as capital tied up in stock since it is difficult to convert inventory immediately into cash as mentioned earlier. Liquidity. Like the acid and quick ratios which are calculated to determine how liquid or to determine if a firm can meet its debts efficiently, Inventory, through the use of a stock turnover calculation, tells the business if its stock is turning over fast enough. In other words, is the stock selling?, is it moving? If inventory has a poor turn over ratio then its not good for the business.

Inventory and Warehouse Management for Business Professionals 2014

But we’ve got some questions ?

1. Why, is a faster turn over better ?

2. Why my inventory isn't turning over fast ?

3. Any solutions for faster stock turn ?

Inventory and Warehouse Management for Business Professionals 2014

Inventories place on the Organization Balance Sheet. Where can we find it?

THE BALANCE SHEET Balance sheet can be defined as – A STATEMENT WHICH TELL US WHERE THE COMPANY MONEY IS INVESTED AND WHERE IT CAME FROM. IT WILL SHOW THE DEGREE OF RISK ASSOCIATED WITH THE MONEY INVESTED IN A BUSINESS

Inventory and Warehouse Management for Business Professionals 2014

HOW A BALANCE SHEET IS MADE UP ASSETS – WHERE THE COMPANY MONEY IS COMING FROM AND LIABILITIES WHICH SHOWS THE SOURCE OF FINANCE FOR THE FIRM. THEY CAN BE LONG TERM AND SHORT TERM

FIXED CURRENT

Inventory and Warehouse Management for Business Professionals 2014

FIXED ASSETS – LONG TERM INVESTMENTS (LAND BUILDING CAPITAL EQUIPMENT)

CURRENT ASSETS – STOCK , CASH ,DEBTORS (MONEY OWED TO SUPPLIER)

Inventory and Warehouse Management for Business Professionals 2014

XLP CONSTRUCTION LTD PROFIT AND LOSS ACCOUNT

2011 2012 2013

TURNOVER (SALES REVENUE ) 6100 6500 6750

COST OF SALES (COST OF PRODUCTION) 5400 5850 6025

GROSS PROFIT (TURNOVER - COST OF PRODUCTION) 700 650 725

SELLING , DISTRIBUTION, ADMIN EXPENSES 60 75 95

PROFIT BEFORE INTEREST AND TAX (GROSS - EXPENSES) 640 575 630

INTEREST PAYABLE 45 68 76

TAXATION PAYABLE 270 250 230

PROFIT AFTER INTEREST AND TAX 325 257 324

DIVIDENDS PAID 125 112 164

RESERVES (RETAINED PROFIT FOR THE YEAR) 200 145 160

P&L ACCOUNTS - A financial statement that summarizes the revenues, costs and expenses incurred during a specific period of time. Investopedia

Inventory and Warehouse Management for Business Professionals 2014

BALANCE SHEET XLP CONSTRUCTION 2011 2012 2013

FIXED ASSETS

PROPERTY 400 845 1325

PLANT AND EQUIPMENT 1200 1350 2250

CURRENT ASSETS

STOCK 1000 1050 1450

DEBTORS (MONEY OWED BY SUPPLIER CUSTOMERS OR MONEY OWED TO THE SUPPLIER) 1400 1300 1850

CASH 50 250 0

CURRENT LIABILITIES

CREDITORS( MONEY OWED BY SUPPLIER TO SUPPLIERS) 1100 1400 1600

TAX OWING (MONEY OWED TO GOVERNMENT) 270 250 230

DIVIDENDS OWING(PROFITS ISSUED TO SHAREHOLDERS) 100 120 60

BANK DRAFT 900

LONG TERM LIABILITIES

LONG TERM LOANS 400 500 1100

SHARE CAPITAL (MONEY INVESTEDBY SHAREHOLDERS) 800 1000 1300

RESERVES ( MONEY REINVESTED IN BUSINESS WHICH IS BALANCE FROM P&L ACCOUNT) 1380 1525 1685 Inventory and Warehouse Management

for Business Professionals 2014

Inventory and Warehouse Management for Business Professionals 2014

Using the information provided along with the formula sheet, let’s calculate the following ratios which involves stock or inventories in some way. Our intention here is to show how stock can impact a company’s performance.

Inventory and Warehouse Management for Business Professionals 2014

BREAK FOR LUNCH

Inventory and Warehouse Management for Business Professionals 2014

• The Profit Impact of Good Inventory Management • - Reasons for having inventory • - The Life Cycle of Inventory • - Objectives of Inventory Management • - The Cost of Carrying Inventory (K- Cost) • - Stock Valuation Methods

Inventory and Warehouse Management for Business Professionals 2014

• The Profit Impact of Good Inventory Management

Recently, our exercise with the balance sheet and Profit and Loss Accounts afforded the inventory manager or supply chain professional, the ability to now determine the financial importance of inventory to the business. Further, we can all agree , that inventory values, if not managed, can lead to : • Stock deterioration • Obsolescence • Firm’s inability to pay suppliers and employees • Theft • And many other issues. The above can easily be translated into a weakening profit margin as not only would the inventory be dead capital which can be used elsewhere, but can lead to firm now having to borrow funds for example, to meet these debts. As we know , loans can attract high interest, further cutting profits

Inventory and Warehouse Management for Business Professionals 2014

Reasons for Holding inventory

There might be many reasons to suggest why a firm must hold inventories. If given the choice, Ohno (1978); Womack and Jones (1994), major contributors of lean inventory, may not want firms to hold inventory at any given time. However, any reason for holding inventory, must come with sufficient justification. Why ? Because lean thinking seems to drive a firms competitive advantage ((Wang and Huzzard 2011; Corbett 2007; Wong and Wong 2011; Ravet 2011; Oliver 2003; Taylor 2006; Alukal 2003; Cudney 2011; Womack and Jones 1994). Lean here can be achieved by the way a firm manages inventory holdings. So let’s think this out and answer the question our selves.

Inventory and Warehouse Management for Business Professionals 2014

MARKET SECTOR DESCRIPTONYES TO

INVENTORIES?

NO TO

INVENTORIES? REASON FOR ANSWER

SERVICE AIRLINE

ENERGY POWER PLANT IN TRINIDAD

MANUFACTURING ANGOSTURA

SERVICE USED CAR DEALER IN TRINIDAD

CHEMICAL ATLANTIC LNG

SERVICE COURTS

SERVICE KFC

Inventory and Warehouse Management for Business Professionals 2014

• - The Life Cycle of Inventory

Inventory and Warehouse Management for Business Professionals 2014

Inventory and Warehouse Management for Business Professionals 2014

DEFINE YOUR INVENTORY LIFE CYCLE AND EXPLORE WAYS OF : REDUCING ENVIRONMENTAL IMPACT INCREASING PROFIT ADDING GREATER VALUE TO CUSTOMER WHEN PURCHASED

Inventory and Warehouse Management for Business Professionals 2014

Inventory and Warehouse Management for Business Professionals 2014

Objectives of Inventory management – Viale’s four objectives

Inventory and Warehouse Management for Business Professionals 2014

certificate in inventory management - 2011

Stock : determination of demand.

seasonal demand

What items are likely to be in demand during this Easter period.

What is demand

What is dependant and independent demand

2013

certificate in inventory management - 2011

A pharmaceutical firm offers a new drug:

The firm can try to predict demand for the drug, or even try to

manipulate demand through pricing incentives and other

marketing efforts, BUT… …ultimately, demand is determined

by the marketplace.

An item whose demand is:

Tied directly to the demand or production level of another

item

Dependent demand items, and the systems for managing them,

are usually most relevant to manufacturers

2013

certificate in inventory management - 2011

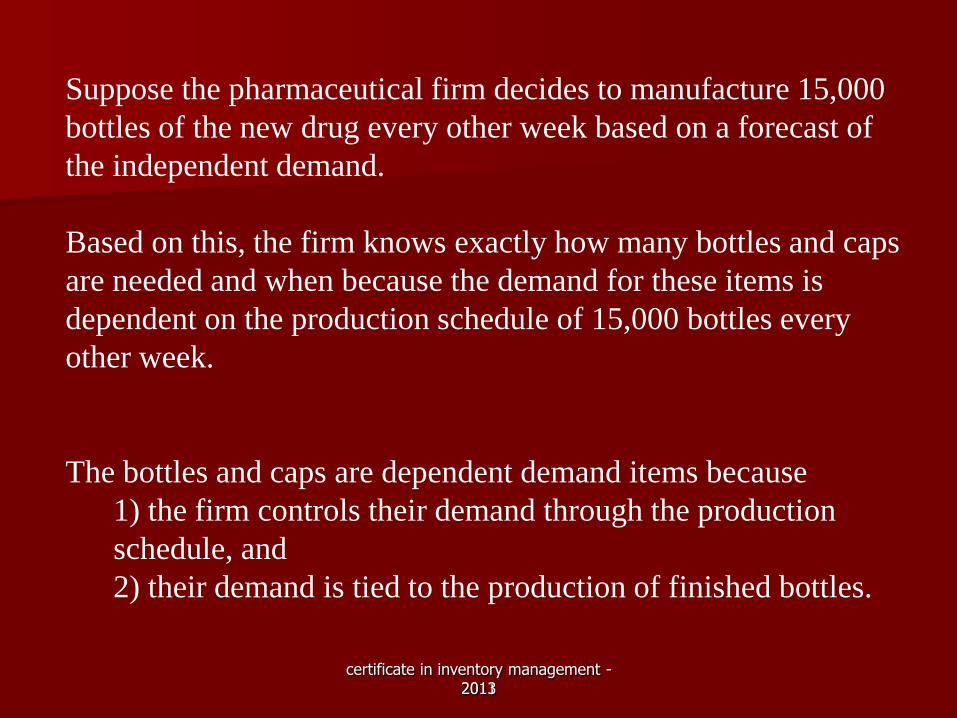

Suppose the pharmaceutical firm decides to manufacture 15,000

bottles of the new drug every other week based on a forecast of

the independent demand.

Based on this, the firm knows exactly how many bottles and caps

are needed and when because the demand for these items is

dependent on the production schedule of 15,000 bottles every

other week.

The bottles and caps are dependent demand items because

1) the firm controls their demand through the production

schedule, and

2) their demand is tied to the production of finished bottles.

2013

certificate in inventory management - 2011

An item has independent demand when we can’t control it or tie it

directly to another item’s demand

An item has dependent demand when the demand for an item is

controlled directly, or tied to the production of something else.

Independent demand and dependent demand items require very

different solutions.

In the remainder of this section, we will discuss two classic

independent demand systems.

2013

certificate in inventory management - 2011

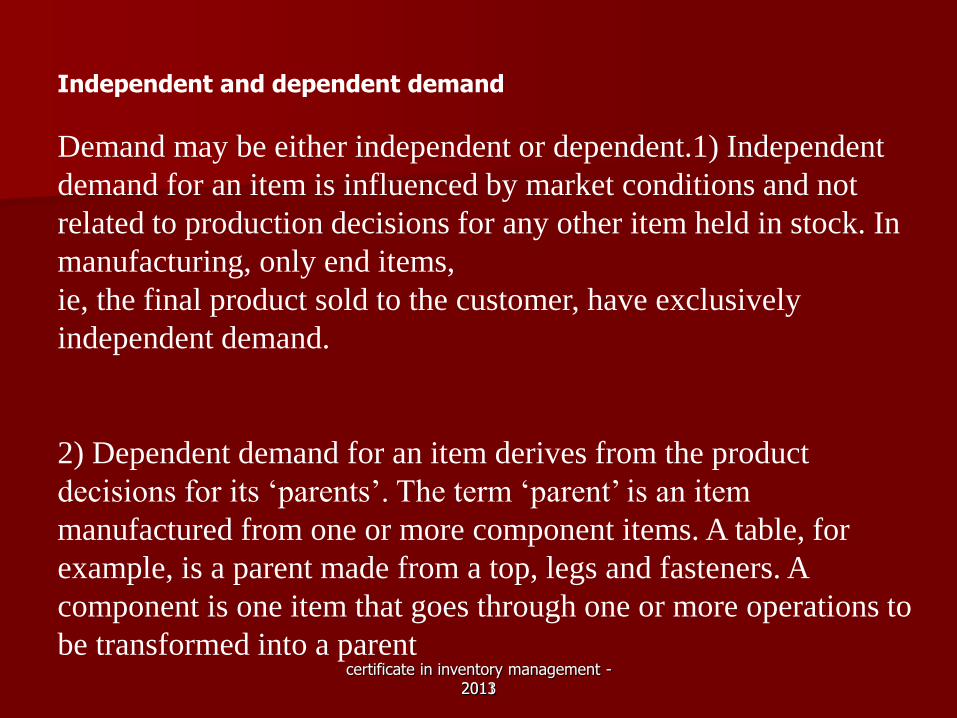

Independent and dependent demand

Demand may be either independent or dependent.1) Independent

demand for an item is influenced by market conditions and not

related to production decisions for any other item held in stock. In

manufacturing, only end items,

ie, the final product sold to the customer, have exclusively

independent demand.

2) Dependent demand for an item derives from the product

decisions for its ‘parents’. The term ‘parent’ is an item

manufactured from one or more component items. A table, for

example, is a parent made from a top, legs and fasteners. A

component is one item that goes through one or more operations to

be transformed into a parent

2013

certificate in inventory management - 2011

Independent demand

• can only be estimated

• although fluctuating with random market influences,

usually demonstrates a continuous and definable pattern.

Dependent demand

• derives from production decisions for its parents and can

therefore be forecast

• due to the practice of scheduling manufacturing in lots,

is usually discontinuous and ‘lumpy’.

certificate in inventory management - 2011

Techniques for independent demand

2013

certificate in inventory management - 2011

Before an effective system of inventory control can be

implemented it is essential to analyse, from records of usage,

what has been the trend of demand for a given item of stock over

an approximate period of time with a view to forecasting future

requirements.

The two most common approaches are detailed below:

Forecasting

2013

certificate in inventory management - 2011

Moving averages. A moving average is an artificially constructed

time series in which each annual (or monthly, daily, etc) figure is replaced by the

average or mean of itself and values corresponding to a number of preceding

and succeeding periods. There is no precise rule about the number of periods

to use when calculating a moving average. The most suitable, obtained by trial

and error, is that which best smoothes out fluctuations. A useful guide is to use

the number of periods between consecutive peaks and troughs.

For example the usage of a ‘dongle’ for six successive periods was

83,85,90,86,102 and 108. If a five period moving average is required, the

average of the first term will be:

83+85+90+86+102 = 89.2

5

The average for the second term will be:

85+90+86+102+108 = 94.2

5

2013

certificate in inventory management - 2011

PARETO ANALYSIS AND SUPPLY CHAIN MANAGEMENT

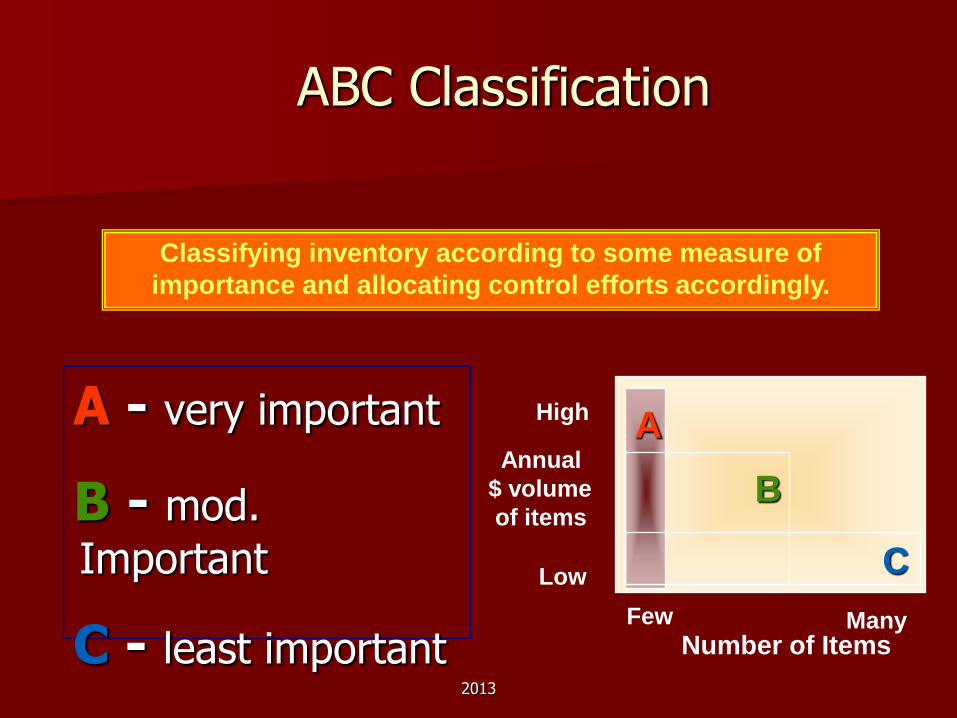

The Pareto principle serves as the basis for ABC analysis (also known as the 80/20 or 90/10 rule) with which it is often, though not entirely accurately, regarded as synonymous. ABC analysis may be defined as: `The application of Pareto's principle to the analysis of supply data. If items in a store are arranged in descending order of usage-value and the cumulative number of items are plotted against the cumulative usage-value the result would be (expected to) show a curve of the general form associated with Pareto's Principle.’

2013

ABC Classification

A - very important

B - mod.

Important

C - least important

Annual

$ volume

of items

A

B

C

High

Low

Few Many Number of Items

Classifying inventory according to some measure of

importance and allocating control efforts accordingly.

2013

certificate in inventory management - 2011

In a store, stock may be categorized in broad accordance with the

Pareto principle as follows:

Group A: Items that account for 10% of total volume, but

account for 60% of total

stock value.

Group B: Items that account for 30% of stock volume, and

account for 30% of stock

value.

Group C: Items that account for 60% of total stock volume, but

only account for

10% of total stock value.

2013

You are carrying out a pareto analysis of your inventory. Lets illustrate on graph

75% of the cost of (turbines) spares contribute to 15% of cost of inventory.

(category A )

15% of the cost of (bearings) spares is concentrated in 10% of the service

range.(category B)

10% of the cost of (rivets and nuts) spares contribute to 75% in volume of spares.

(category C)

TASK:

a) Construct a standard pareto classification distribution graph that categorizes

the distribution above. (10 marks)

b) Explain why this type of analysis is important for inventory .

2013

0

10

20

30

40

50

60

70

80

90

100

15 25 30

40

50

60

70

80

90

100

A

B

C

Cost

of

invento

ry

Inventory volume 2013

Inventory and Warehouse Management for Business Professionals 2014

• Identifying Different Forecasting Techniques (MOVING AVERAGES

STANDARD DEVIATION)

- Inventory Management vs. Inventory Control

• Reorder Point Systems / Stock replenishment ( DEPENDENT DEMAND METHOD)

- Economic Order Quantity (DEPENDENT DEMAND METHOD)

- Safety Stock and Service Levels

- Stock Classification Systems (ABC ANALYSIS)

- Inventory Monitoring and Control (TWO BIN SYSTEM)

• - Stock coding systems

Inventory and Warehouse Management for Business Professionals 2014

STANDARD DEVIATION

Step 1 – calculate the mean Step 2 – find the sum of the squares of the deviations of items from the mean Step 3 – divide this sum by number of items and taker the square root

Inventory and Warehouse Management for Business Professionals 2014

So let’s demonstrate with the following : 2,4,6 and 8

Inventory and Warehouse Management for Business Professionals 2014

STANDARD DEVIATION

1 2 3 4

TIME PERIOD ACTUAL SALES FORECAST FORECAST ERROR FORECAST SQUARED

1 1520 1510 10 100

2 1490 1500 -10 100

3 1510 1500 10 100

4 1520 1500 20 400

5 1470 1510 -40 1600

6 1510 1500 10 100

2400

ABC Classification

A - very important

B - mod.

Important

C - least important

Annual

$ volume

of items

A

B

C

High

Low

Few Many Number of Items

Classifying inventory according to some measure of

importance and allocating control efforts accordingly.

2013

Reorder point

Profile of Inventory Level Over Time

Quantity

on hand

Q

Receive

order

Place

order Receive

order

Place

order Receive

order

Lead time

Reorder

point

Demand

rate

Time

2013

D. Fixed Order Quantity/Reorder Point Model:

Determining the Reorder Point

Reorder Point (ROP)

– When the quantity on hand of an item drops to this amount, the item should be reordered

Safety Stock

– Stock that is held in excess of expected demand due to variable demand rate and/or lead time.

Service Level

– Probability that demand will not exceed supply during lead time.

2013

Lets calculate the order point for coffee at a local

supermarket with the - Average usage in lead time

+ required level of safety stock

Safety stock for coffee – 100 drums

Supply lead time – 6 weeks

Average weekly demand - 200

2013

Answer : Re order level – 1300 . That is average in a lead time = 200 x 6 + 100

2013

EOQ

2013

EOQ Assumptions

Known & constant demand

Known & constant lead time

Instantaneous receipt of material

No quantity discounts

Only order (setup) cost & holding cost

No stockouts

2013

Inventory Holding Costs LOCAL SUPERMARKET

Housing (building) cost 6%

Material handling costs 3%

Labor cost 3%

Inventory investment costs 11%

Pilferage, scrap, & obsolescence 3%

Total holding cost 26%

% of Category Inventory Value

2013

EOQ Example

You’re a buyer for SaveMart.

Save Mart needs 1000 coffee makers per year.

The cost of each coffee maker is $78. Ordering

cost is $100 per order. Carrying cost is 40% of

per unit cost. Lead time is 5 days. SaveMart is

open 365 days/yr.

What is the optimal order quantity & ROP?

2013

SaveMart EOQ

H

SDEOQ

2

20.31$

100$10002 EOQ

D ( annual usage in units) = 1000

S (ordering cost) = $100

C (unit price) = $ 78

I (carrying cost) = 40%

H = C x I

H(holding cost per unit) = $31.20

EOQ = 80 coffeemakers

2013

Lets change the variables a bit.

If the demand was 2500 per year, with an

ordering cost of $240; unit price of $120 and

cost of storage now 45%, then what would be

the calculated optimum quantity the firm

should carry.

2013

Lets change the variables a bit.

If the demand was 2500 per year, with an

ordering cost of $240; unit price of $120 and

cost of storage now 45%, then what would be

the calculated optimum quantity the firm

should carry.

2013

The aim of EOQ is to find the lowest acquisition

cost . The higher the ordering cost , the higher

will be the cost to hold the stock(lights ,

insurance , risk of damage etc.). This is

balanced against the purchasing cost – in that

the high qty purchased will mean fewer orders

in the future leading to reduced administrative

cost, and also impacting on vendor transport

cost

2013

Inventory and Warehouse Management for Business Professionals 2014

Stocking policy - Material requirements Planning - Manufacturing Resource Planning - Enterprise resource Planning - Just In Time - Lean manufacturing Storeroom / Warehouse Management (Learning Outcome 7) - Physical Layout of Storeroom / Warehouse - Transactions Recording - Periodic Stock taking vs. Cycle Counting - Stores Warehousing Location and Layout - Dealing with Excess and Obsolete Inventory - Dealing with Fraud in your Warehouse

Inventory and Warehouse Management for Business Professionals 2014

- Periodic Stocktaking vs. Cycle Counting

Inventory and Warehouse Management for Business Professionals 2014

Stock taking consists of two types. Continuous or perpetual stock taking and periodic stock taking . Periodic stocktaking is done at the end of the financial year and may involve a percentage count of the inventory. This is necessary to meet the financial requirements of the company’s shareholders. Continuous stocktaking or cycle counting can be conducted quarterly or at any given time, often targeting the high value inventory or items that attract high usage values. This is often based on the 80/20 or 90/10 rule of the thumb.

Inventory and Warehouse Management for Business Professionals 2014

Year end Count Reporting and the stock count program

Inventory and Warehouse Management for Business Professionals 2014

MRP

Inventory management for manufacturing organizations

Today we look at ;

MRP

MRP II

DRP

JIT Systems

MRP (Material requirement planning)

Developed in the 1960s is a technique that assists in the

detailed planning of production and has the following

characteristics;

It is geared specifically to assembly operations

It is a dependent demand technique

It is a computer – based information system

Quick question.

When we say that it is geared towards dependent demand

what do we mean by this ?

Let’s see how it works

Main components of MRP :

The BOM

The ISF

The MPS

So then what might be the benefits of such a system ?

•Reduced Inventory Levels

• Reduced Component Shortages

• Improved Shipping Performance

• Improved Customer Service

• Improved Productivity

• Simplified and Accurate Scheduling

• Reduced Purchasing Cost

• Improve Production Schedules

• Reduced Manufacturing Cost

• Reduced Lead Times

• Less Scrap and Rework

• Higher Production Quality

• Improved Communication

• Improved Plant Efficiency

• Reduced Freight Cost

• Reduction in Excess Inventory

• Reduced Overtime

• Improved Supply Schedules

• Improved Calculation of Material Requirements

• Improved Competitive Position

What is Manufacturing Resources Planning (MRP II)?

MRP II stands for Manufacturing Resources Planning, a

computer modelling technique for analysing and controlling

complicated Manufacturing operations. When the manufacturing

data has been collected (parts, assemblies, resources) the lead

time and cost of every component can be predicted under any

manufacturing conditions. As soon as an order is received the

workload on the manufacturing organisation and the delivery

time can be calculated.

MRP II systems also keep track of customers, suppliers and

accounting functions. Inventory can be purchased and assemblies

made "Just in Time". The records kept by an MRP system

highlight inadequacies such as overloaded production centres and

delays by suppliers. The effect of new orders, changes in

capacity, shortages, delays and a myriad of other disturbances are

calculated and tracked with confidence.

The major effects that an MRP II system will have on a

manufacturing operation will be:

- Reduced inventory.

- Accurately predicted delivery times.

- Accurate costing at every stage of the manufacturing

process.

- Improved use of manufacturing facilities.

- Faster response to changing conditions.

- Control of every stage of production

Lets refer to the text for example

DRP – Distribution resource planning

This is an inventory control and scheduling technique that

applies MRP principles to distribution inventories. It may

also be regarded as a method of handling stock

replenishment in a multi echelon environment .

Lets review in the study guide.

JIT

Just In Time Production or Lean Production systems focus on the

efficient delivery of products or services. Some of the distinguishing

elements of the JIT systems are a pull method to manage material

flow, consistently high quantity, small lot sizes, uniform work

station loads.

The JIT systems provide an organizational structure for improved

supplier coordination by integrating the logistics, production and

purchasing processes. When Operations Manager focuses on their

organization’s competitive advantage they aim for low cost of

production, consistent quality with reductions in inventory, space

requirements, paperwork and increases in productivity, employee

participation and effectiveness.

Physical Stock management

•Goods access

•Hazardous materials

•Essential services

•Material flow

•Warehouse layout

•Inventory count exercises

The warehouse environment

• What are the principles of a warehouse ?

• What are the role of warehouses

• What are the different types of warehouses

• Let’s design a warehouse

• Importance of cycle count / perpetual counting

• JIT

• Technology and the modern warehouse

A

B

C

D

E

F

G

Where might we find an issue of poor accountability when goods leave and come into warehouse and how do we address it Which letter highlights danger to employees with machinery of warehouse and what is recommended to address the issue At which point we might be seeing as breach of users entering the warehouse . How do we resolve this A diesel forklift is used on this warehouse. Employees don't complain about it. Would you change out unit or continue as part of your cost savings scheme Bulk items are stored at a point shown. These items are moved only when major repairs to the plant is needed. Should they remain there ? Are our employees comfortable in moving around the shelves,. Where is this point highlighted. How do we make work easier for them

Inventory and Warehouse Management for Business Professionals 2014

Inventory Fraud

INVENTORY MANAGEMENT. NOT JUST HOLDING STOCK

WHAT DID WE LEARN ?

What is inventory ?

Name three types of inventory

What does MRO abbreviate?

MRO is a type of inventory category . True or false

What is safety stock

What influences independent demand inventories

ROP = DLT + SS is the formula for …………?

What is lead time

Explain ABC analysis

Outline 3 cost s associated in holding inventory

What is the current ratio formula ?

Define quick ratio

Explain the term, “capital tied up in stock

What do ratios help us identify ? Outline 3 concerns

Name one type of warehouse

Explain the difference between periodic and continuous stocktaking

What is muda

Outline three ways in which an organization can reduce excessive inventories

How do you calculate absolute variance

Is JIT a pull or push system. Give reason for your choice

Inventory and Warehouse Management for Business Professionals 2014

Name three variables that must remain constant for EOQ to work

Inventory and Warehouse Management for Business Professionals 2014

Where does usage value in Pareto give the highest priority ?

Inventory and Warehouse Management for Business Professionals 2014

What’s the formula for EOQ

Inventory and Warehouse Management for Business Professionals 2014

What are the four variables identified for JIT to work

Inventory and Warehouse Management for Business Professionals 2014