39

SME Development Initiatives State Bank of Pakistan Muhammad Ishfaq Sr. Joint Director, I H &SME Finance Department State Bank of Pakistan

SME Development Initiatives

State Bank of Pakistan

Muhammad Ishfaq Sr. Joint Director, I H &SME Finance Department State Bank of Pakistan

Development Initiatives

1. Refinance Schemes

2. SME Credit Guarantee Scheme

3. Capacity Building of Banks

4. SME Cluster Development Surveys

2

SBP Credit Schemes 4

Export Finance Scheme (Islamic & Conventional)

Long Term Financing Facility for Plant and Machinery (LTFF)

Refinance Facility for Modernization of SMEs Financing Facility for Storage of Agricultural Produce

(FFSAP)

Scheme for Financing Power Plants Using Renewable Energy

4

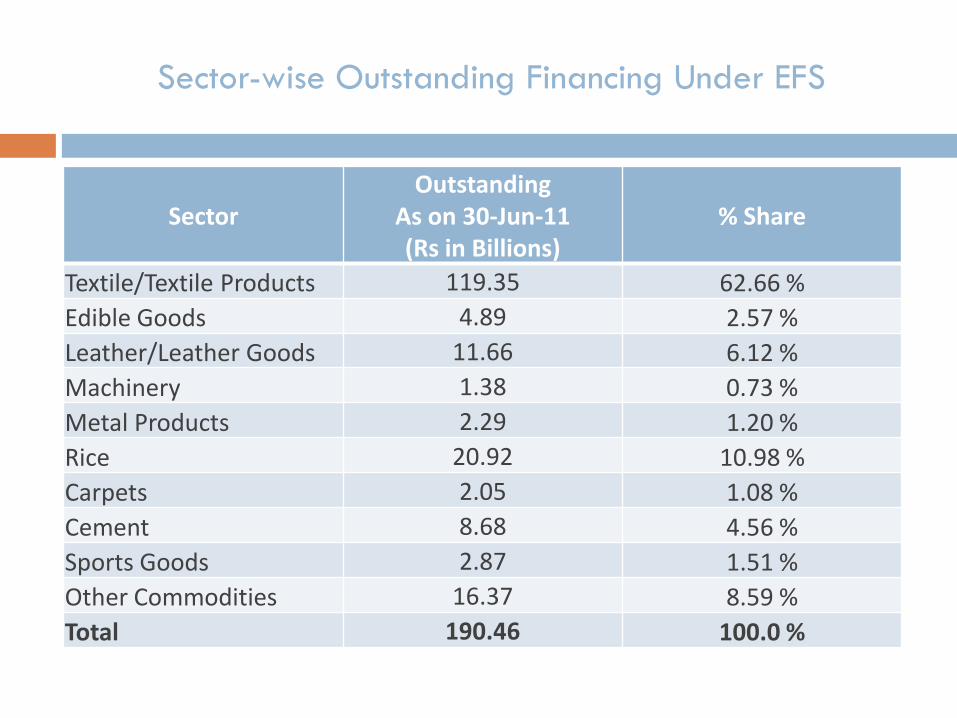

Sector-wise Outstanding Financing Under EFS

Sector Outstanding

As on 30-Jun-11 (Rs in Billions)

% Share

Textile/Textile Products 119.35 62.66 %

Edible Goods 4.89 2.57 %

Leather/Leather Goods 11.66 6.12 %

Machinery 1.38 0.73 %

Metal Products 2.29 1.20 %

Rice 20.92 10.98 %

Carpets 2.05 1.08 %

Cement 8.68 4.56 %

Sports Goods 2.87 1.51 %

Other Commodities 16.37 8.59 %

Total 190.46 100.0 %

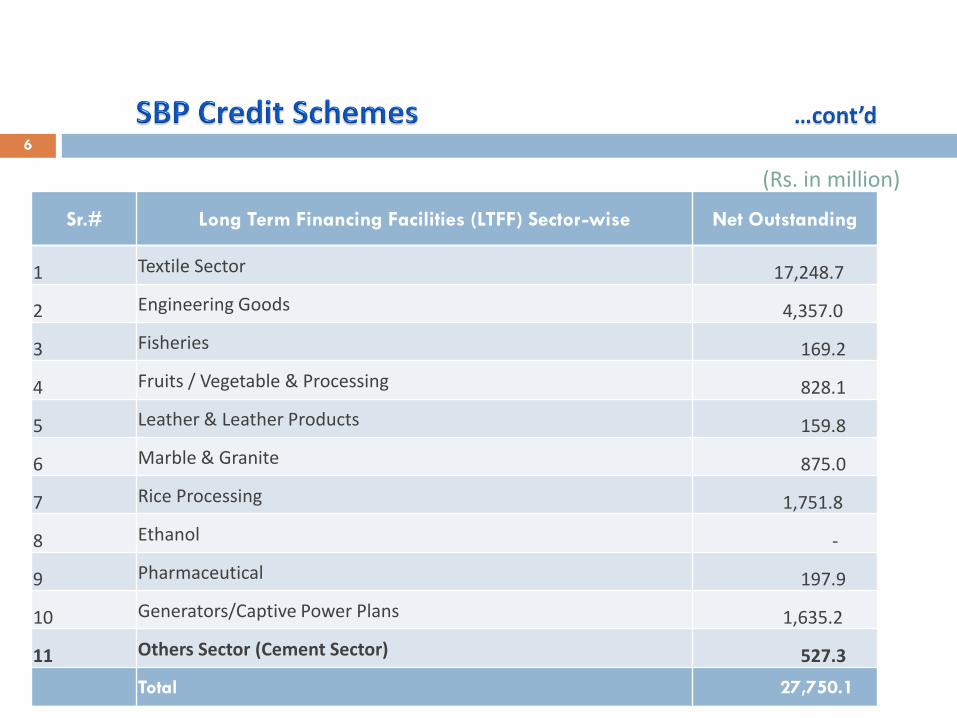

(Rs. in million)

6

Sr.# Long Term Financing Facilities (LTFF) Sector-wise Net Outstanding

1 Textile Sector 17,248.7

2 Engineering Goods 4,357.0

3 Fisheries 169.2

4 Fruits / Vegetable & Processing 828.1

5 Leather & Leather Products 159.8

6 Marble & Granite 875.0

7 Rice Processing 1,751.8

8 Ethanol -

9 Pharmaceutical 197.9

10 Generators/Captive Power Plans 1,635.2

11 Others Sector (Cement Sector) 527.3

Total 27,750.1

Background:

SMEs plays an important role in creation of employment opportunities, economic growth, poverty reduction and equitable distribution of economic prosperity.

Limited access of SMEs to financing facilities from the formal sources.

Fixed investment financing of SMEs constitutes a small proportion of total SME Financing.

7

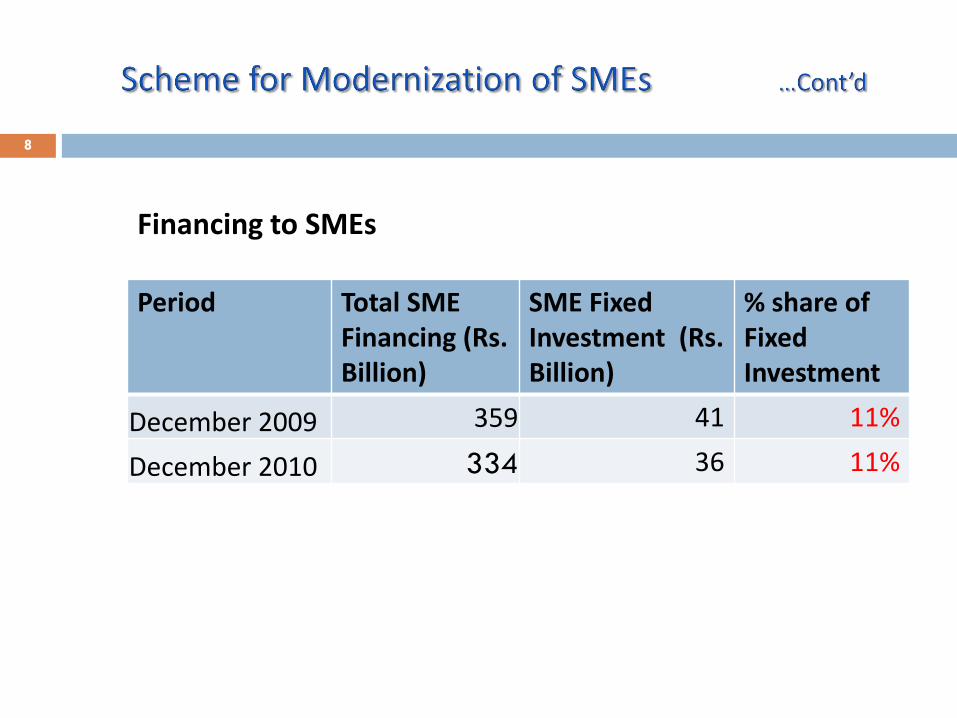

Financing to SMEs

Period Total SME Financing (Rs. Billion)

SME Fixed Investment (Rs. Billion)

% share of Fixed Investment

December 2009 359 41 11%

December 2010 334 36 11%

8

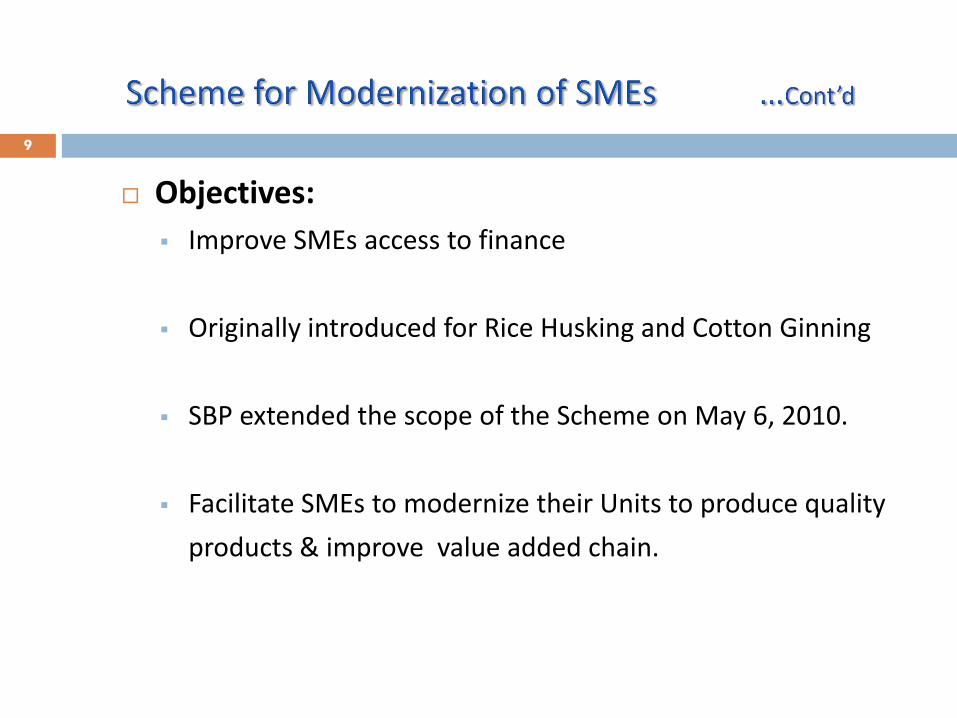

Objectives:

Improve SMEs access to finance

Originally introduced for Rice Husking and Cotton Ginning

SBP extended the scope of the Scheme on May 6, 2010.

Facilitate SMEs to modernize their Units to produce quality

products & improve value added chain.

9

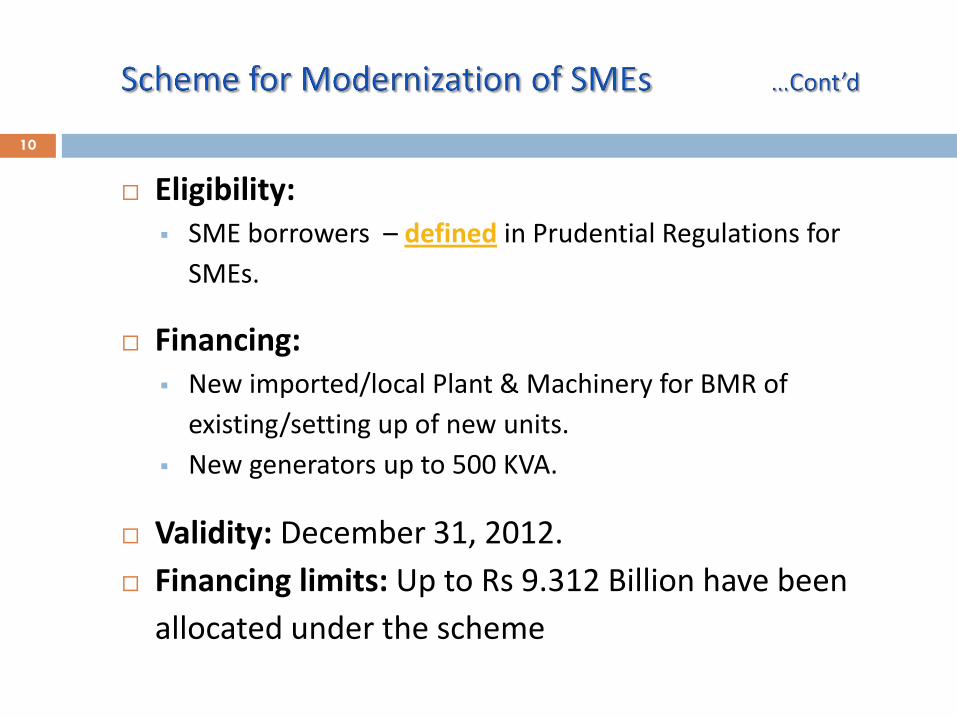

Eligibility: SME borrowers – defined in Prudential Regulations for

SMEs.

Financing: New imported/local Plant & Machinery for BMR of

existing/setting up of new units.

New generators up to 500 KVA.

Validity: December 31, 2012.

Financing limits: Up to Rs 9.312 Billion have been

allocated under the scheme

10

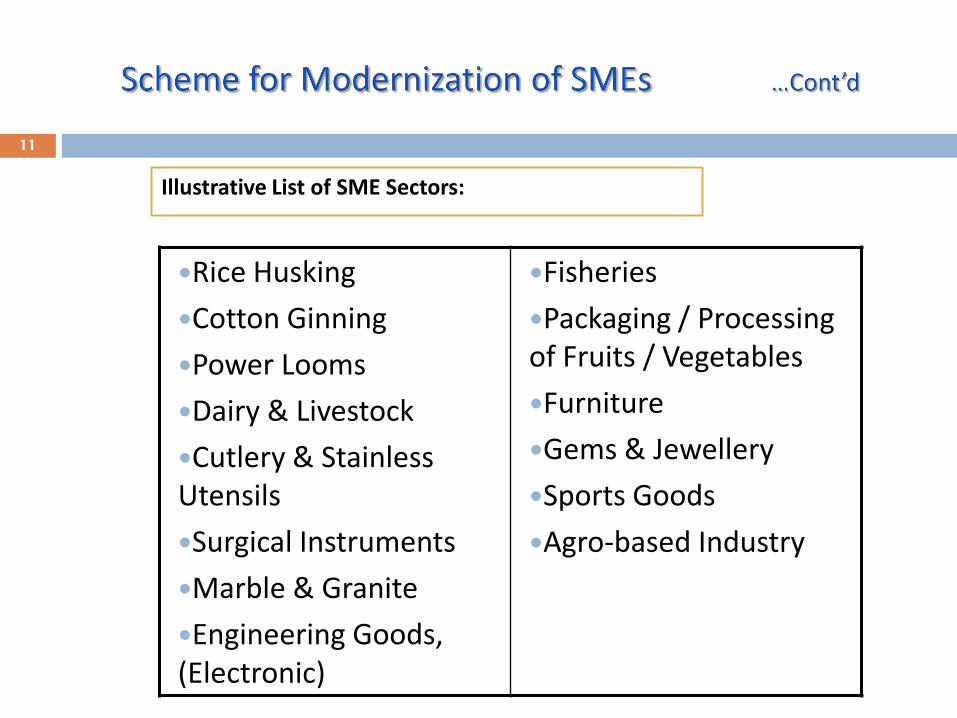

Illustrative List of SME Sectors:

Rice Husking

Cotton Ginning

Power Looms

Dairy & Livestock

Cutlery & Stainless Utensils

Surgical Instruments

Marble & Granite

Engineering Goods, (Electronic)

Fisheries

Packaging / Processing of Fruits / Vegetables

Furniture

Gems & Jewellery

Sports Goods

Agro-based Industry

11

12

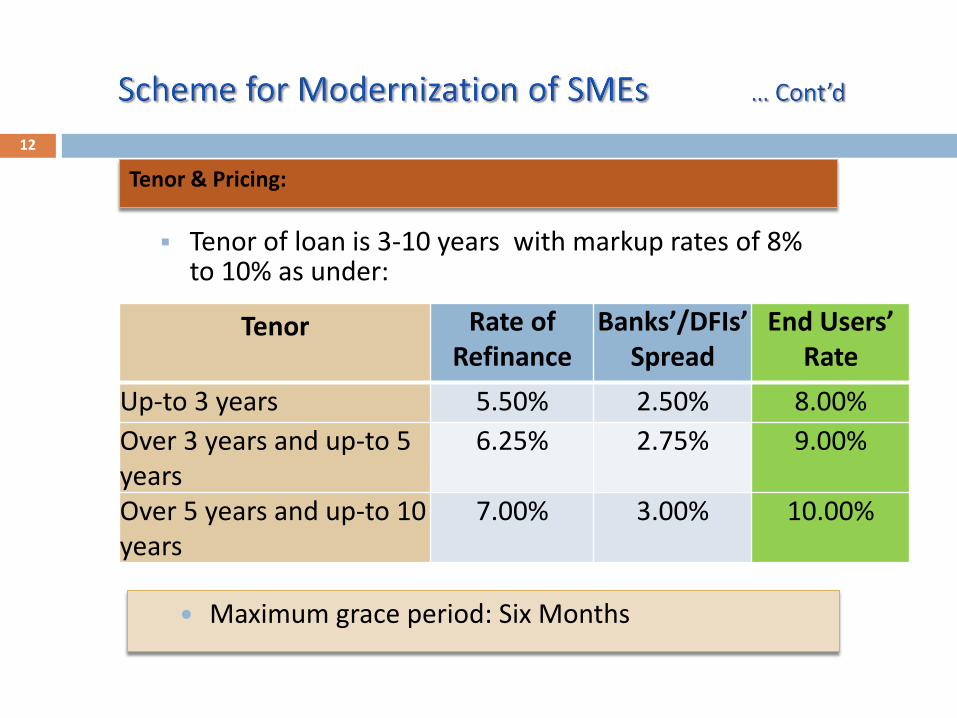

Tenor of loan is 3-10 years with markup rates of 8% to 10% as under:

Tenor

Rate of Refinance

Banks’/DFIs’ Spread

End Users’ Rate

Up-to 3 years 5.50% 2.50% 8.00%

Over 3 years and up-to 5 years

6.25% 2.75% 9.00%

Over 5 years and up-to 10 years

7.00% 3.00% 10.00%

Maximum grace period: Six Months

Tenor & Pricing:

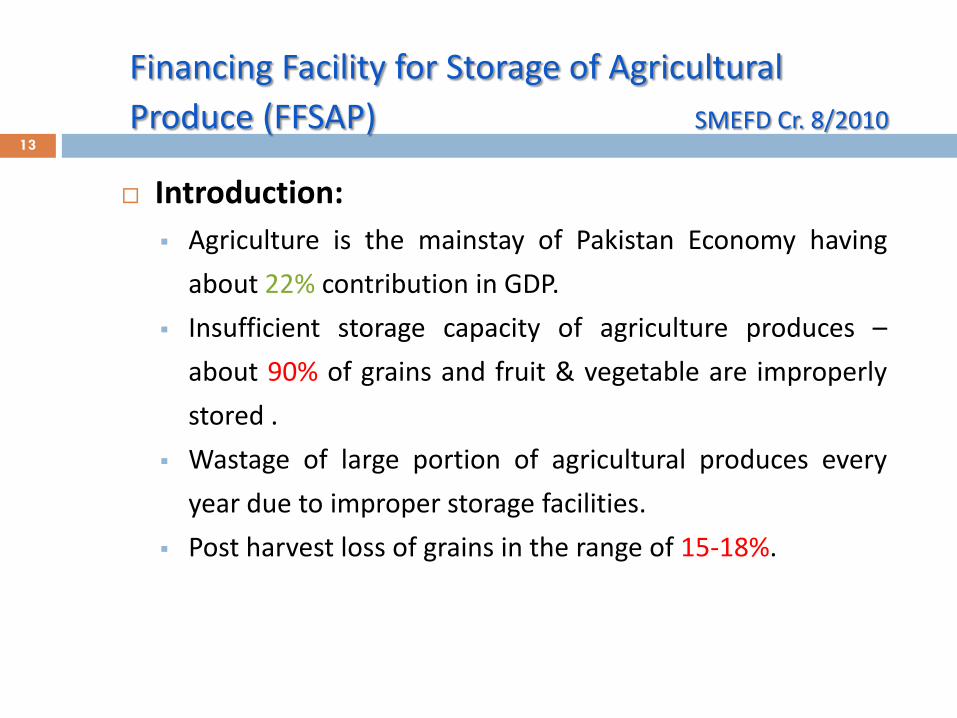

Introduction:

Agriculture is the mainstay of Pakistan Economy having

about 22% contribution in GDP.

Insufficient storage capacity of agriculture produces –

about 90% of grains and fruit & vegetable are improperly

stored .

Wastage of large portion of agricultural produces every

year due to improper storage facilities.

Post harvest loss of grains in the range of 15-18%.

Financing Facility for Storage of Agricultural

Produce (FFSAP) SMEFD Cr. 8/2010 13

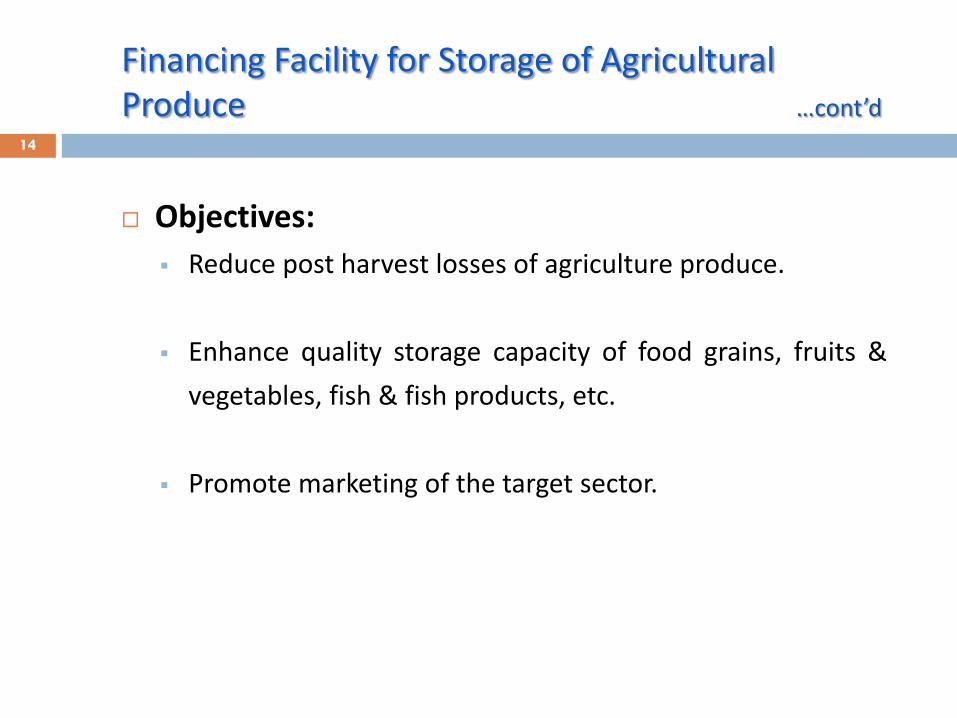

Objectives:

Reduce post harvest losses of agriculture produce.

Enhance quality storage capacity of food grains, fruits &

vegetables, fish & fish products, etc.

Promote marketing of the target sector.

Financing Facility for Storage of Agricultural Produce …cont’d

14

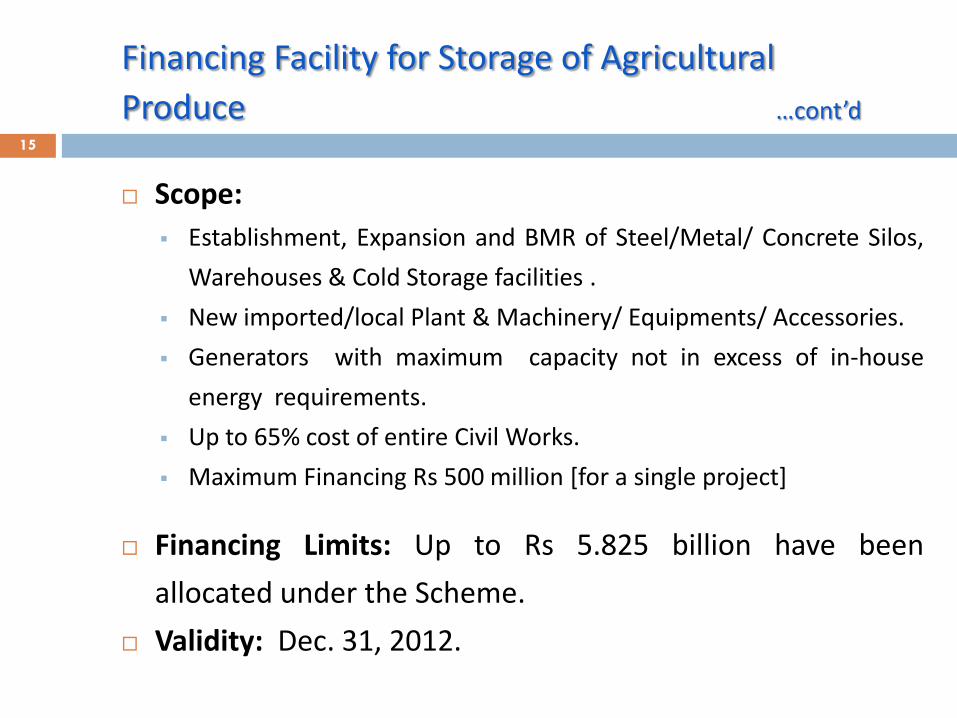

Financing Facility for Storage of Agricultural

Produce …cont’d

Scope:

Establishment, Expansion and BMR of Steel/Metal/ Concrete Silos,

Warehouses & Cold Storage facilities .

New imported/local Plant & Machinery/ Equipments/ Accessories.

Generators with maximum capacity not in excess of in-house

energy requirements.

Up to 65% cost of entire Civil Works.

Maximum Financing Rs 500 million [for a single project]

Financing Limits: Up to Rs 5.825 billion have been

allocated under the Scheme.

Validity: Dec. 31, 2012.

15

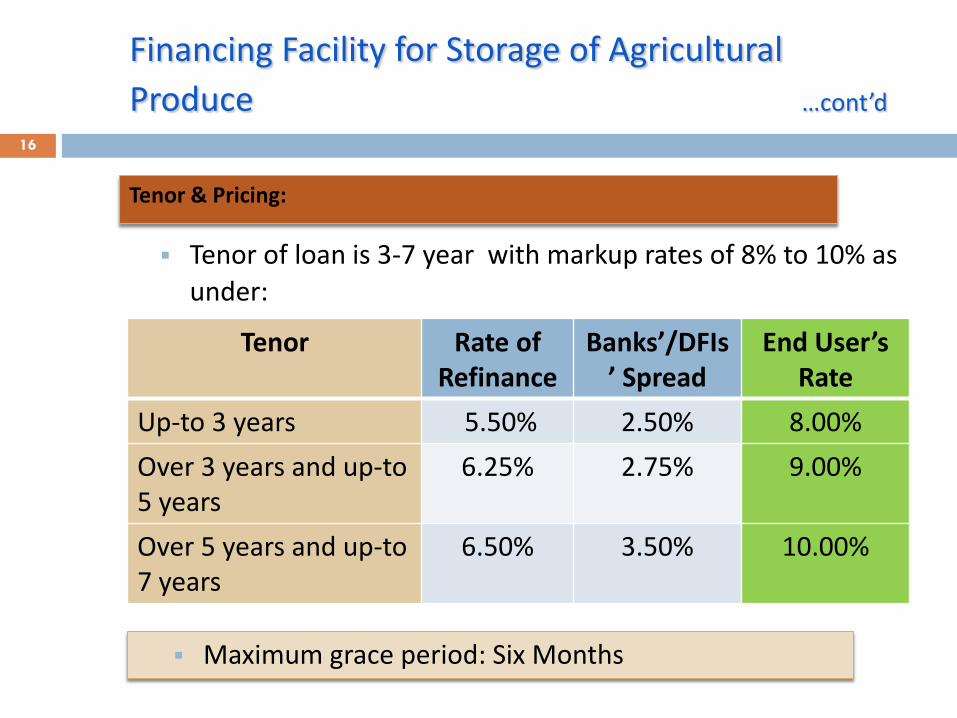

Financing Facility for Storage of Agricultural

Produce …cont’d

Tenor of loan is 3-7 year with markup rates of 8% to 10% as

under:

Tenor Rate of Refinance

Banks’/DFIs’ Spread

End User’s Rate

Up-to 3 years 5.50% 2.50% 8.00%

Over 3 years and up-to 5 years

6.25% 2.75% 9.00%

Over 5 years and up-to 7 years

6.50% 3.50%

10.00%

Maximum grace period: Six Months

Tenor & Pricing:

16

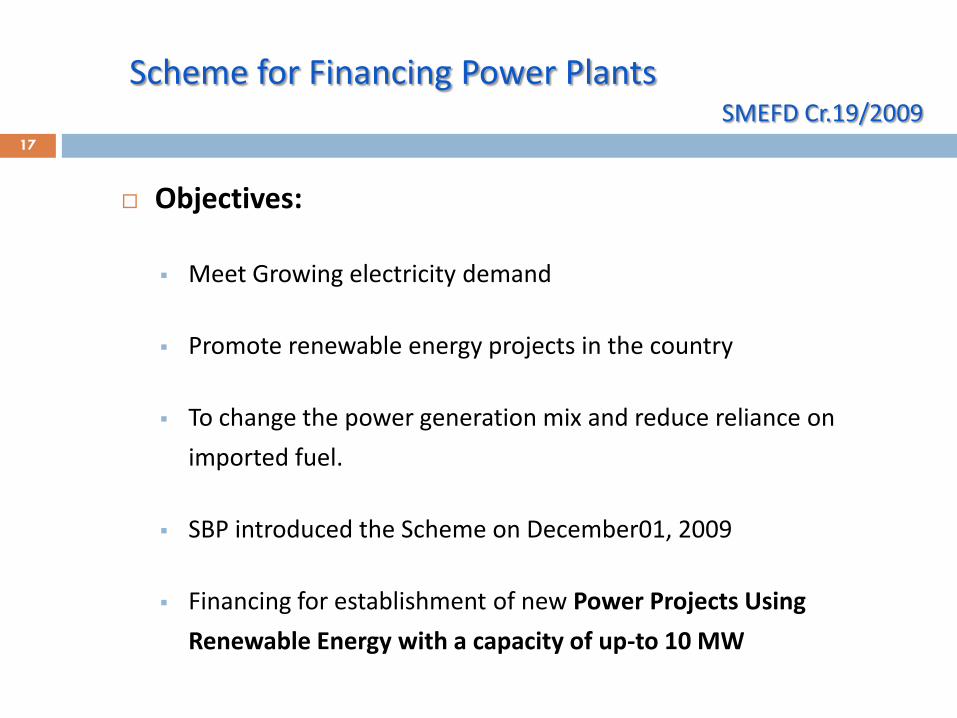

Scheme for Financing Power Plants SMEFD Cr.19/2009

Objectives:

Meet Growing electricity demand

Promote renewable energy projects in the country

To change the power generation mix and reduce reliance on

imported fuel.

SBP introduced the Scheme on December01, 2009

Financing for establishment of new Power Projects Using

Renewable Energy with a capacity of up-to 10 MW

17

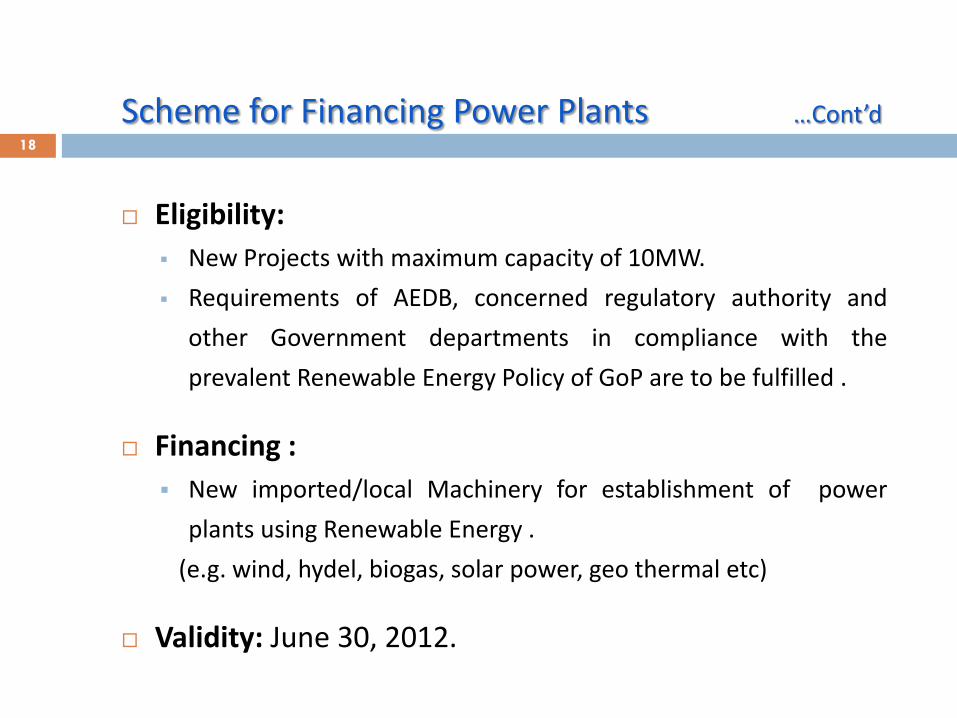

Eligibility:

New Projects with maximum capacity of 10MW.

Requirements of AEDB, concerned regulatory authority and

other Government departments in compliance with the

prevalent Renewable Energy Policy of GoP are to be fulfilled .

Financing :

New imported/local Machinery for establishment of power

plants using Renewable Energy .

(e.g. wind, hydel, biogas, solar power, geo thermal etc)

Validity: June 30, 2012.

Scheme for Financing Power Plants …Cont’d

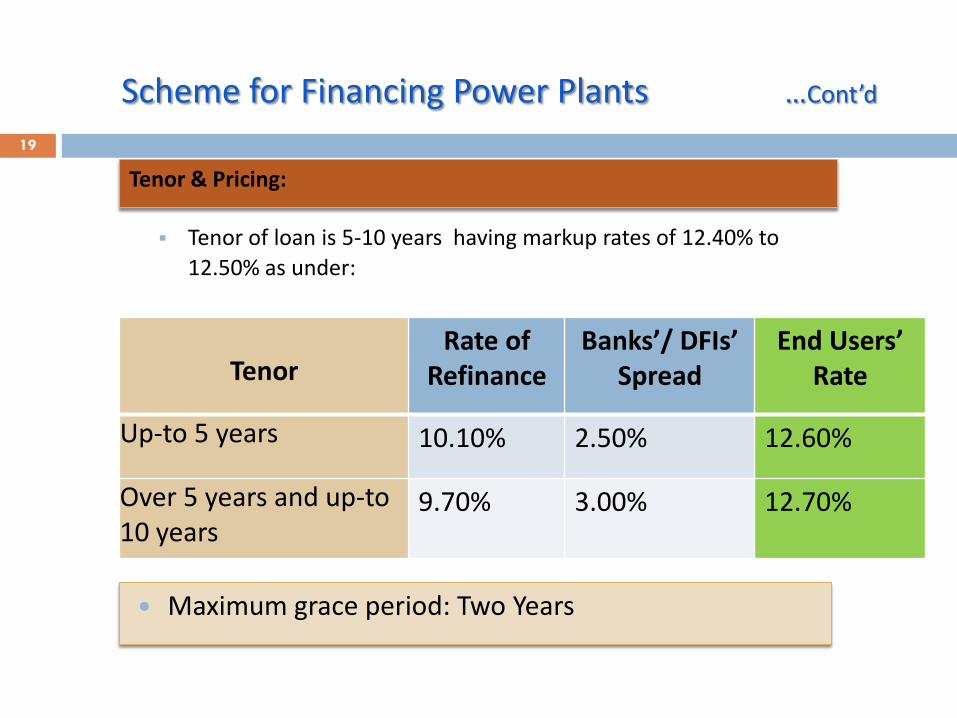

18

Tenor

Rate of Refinance

Banks’/ DFIs’ Spread

End Users’ Rate

Up-to 5 years 10.10% 2.50% 12.60%

Over 5 years and up-to 10 years

9.70% 3.00%

12.70%

Maximum grace period: Two Years

Tenor of loan is 5-10 years having markup rates of 12.40% to

12.50% as under:

Tenor & Pricing:

Scheme for Financing Power Plants …Cont’d

19

20

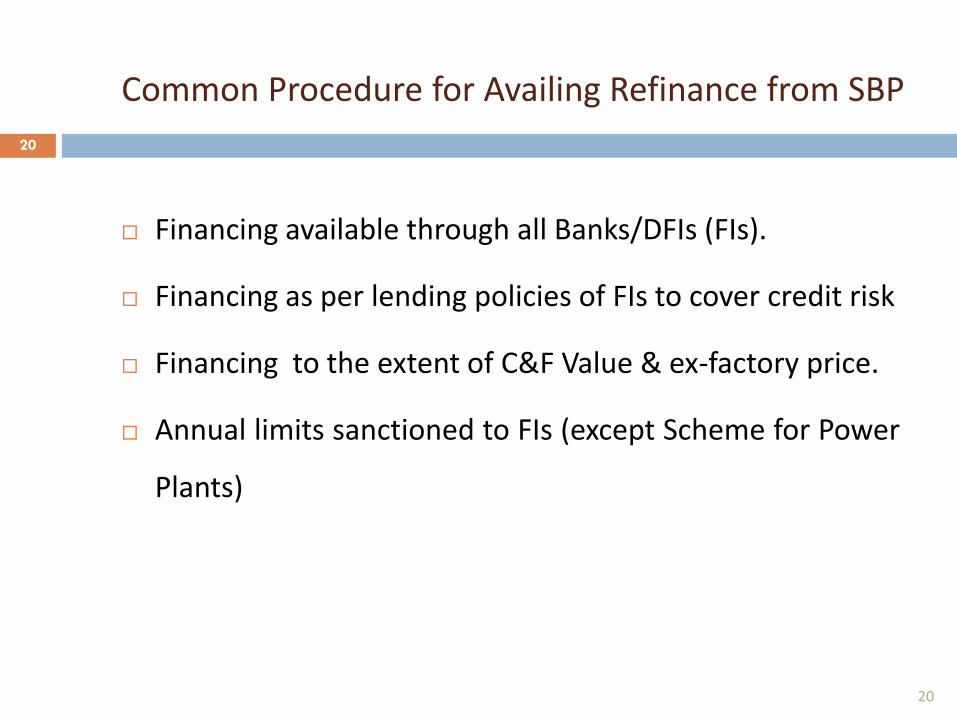

Financing available through all Banks/DFIs (FIs).

Financing as per lending policies of FIs to cover credit risk

Financing to the extent of C&F Value & ex-factory price.

Annual limits sanctioned to FIs (except Scheme for Power

Plants)

Common Procedure for Availing Refinance from SBP

20

Direct payment by FIs to supplier/manufacturer against LC/ILC

Repayment in equal quarterly/half yearly installments

Quarterly recovery of markup

Fixed markup rate for entire period of loan.

21

Common Procedure for Availing Refinance from SBP …Cont’d

21

Common Procedure for Availing Refinance from

SBP …Cont’d

Linkage of rates

Short Term Loans – T. Bills

Long Term Loans - PIBs

Yearly announcement of markup rates.

Fine in case of violation of the terms & conditions of the Scheme:

SBP reserve the right to recover the amount of refinance along-with fine at the rate of Paisa 60 per day per Rs 1000/- or part thereof.

22

22

Documentation by FIs

23

Common Procedure fro Availing Refinance from SBP …Cont’d

23

Documentation by FIs

24

Common Procedure fro Availing Refinance from SBP …Cont’d

24

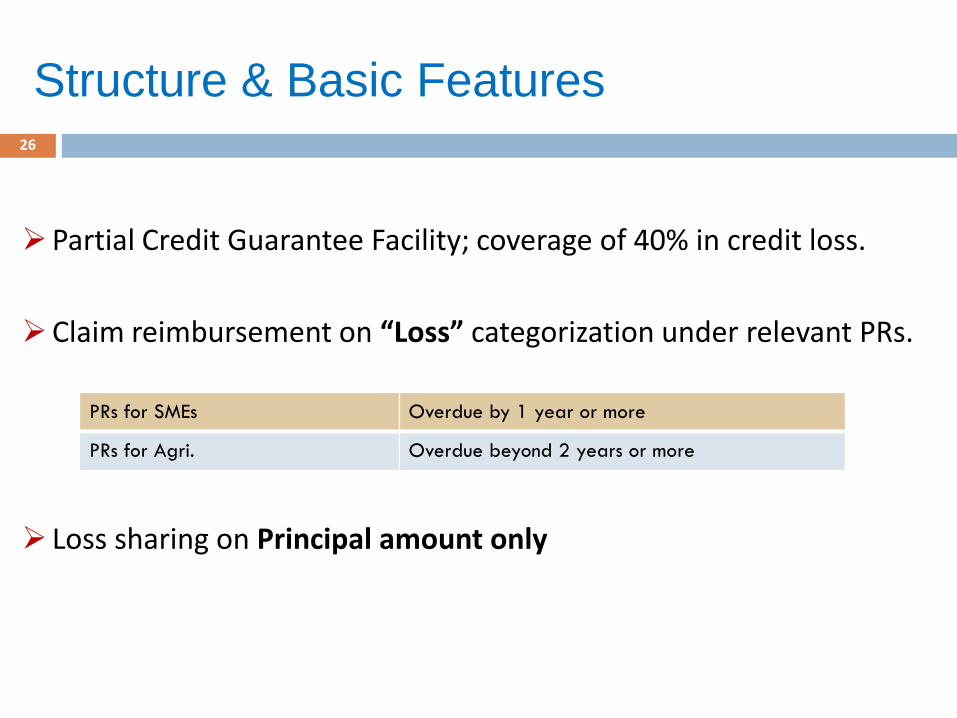

Structure & Basic Features

Partial Credit Guarantee Facility; coverage of 40% in credit loss.

Claim reimbursement on “Loss” categorization under relevant PRs.

Loss sharing on Principal amount only

PRs for SMEs Overdue by 1 year or more

PRs for Agri. Overdue beyond 2 years or more

26

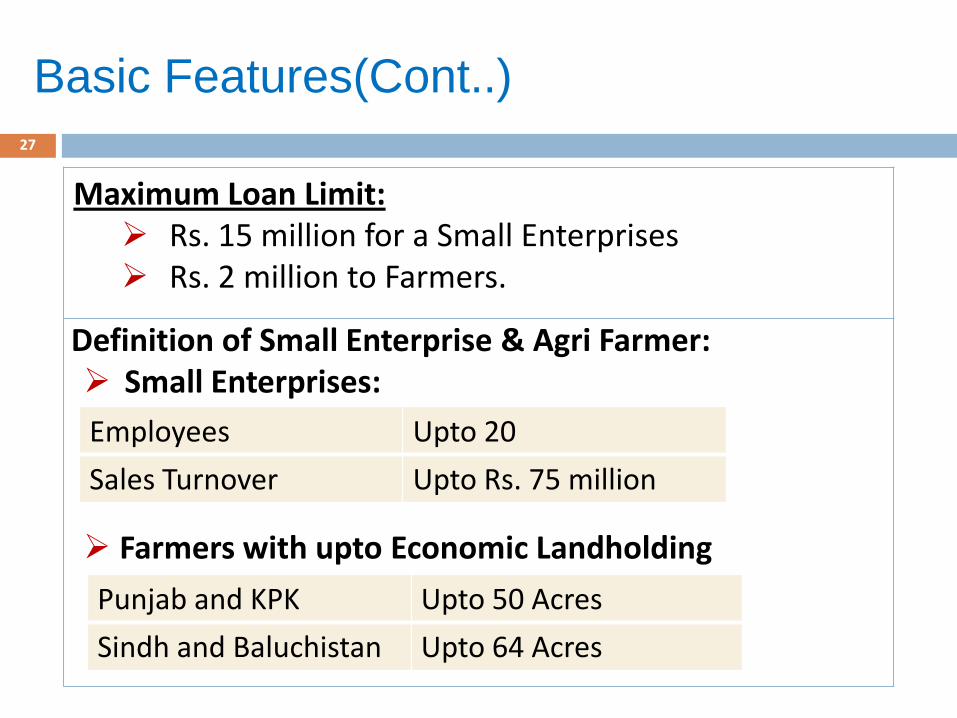

Basic Features(Cont..)

Maximum Loan Limit: Rs. 15 million for a Small Enterprises Rs. 2 million to Farmers.

Definition of Small Enterprise & Agri Farmer: Small Enterprises:

Farmers with upto Economic Landholding

Employees Upto 20

Sales Turnover Upto Rs. 75 million

Punjab and KPK Upto 50 Acres

Sindh and Baluchistan Upto 64 Acres

27

Basic Features(Cont..)

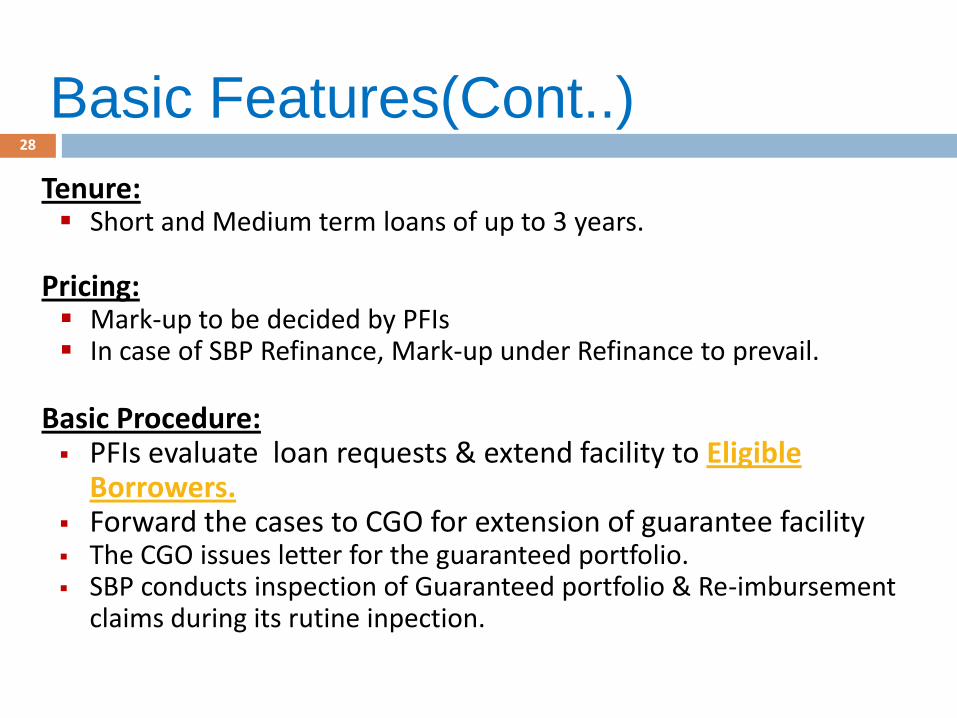

Tenure: Short and Medium term loans of up to 3 years.

Pricing: Mark-up to be decided by PFIs In case of SBP Refinance, Mark-up under Refinance to prevail.

Basic Procedure: PFIs evaluate loan requests & extend facility to Eligible

Borrowers. Forward the cases to CGO for extension of guarantee facility The CGO issues letter for the guaranteed portfolio. SBP conducts inspection of Guaranteed portfolio & Re-imbursement

claims during its rutine inpection.

28

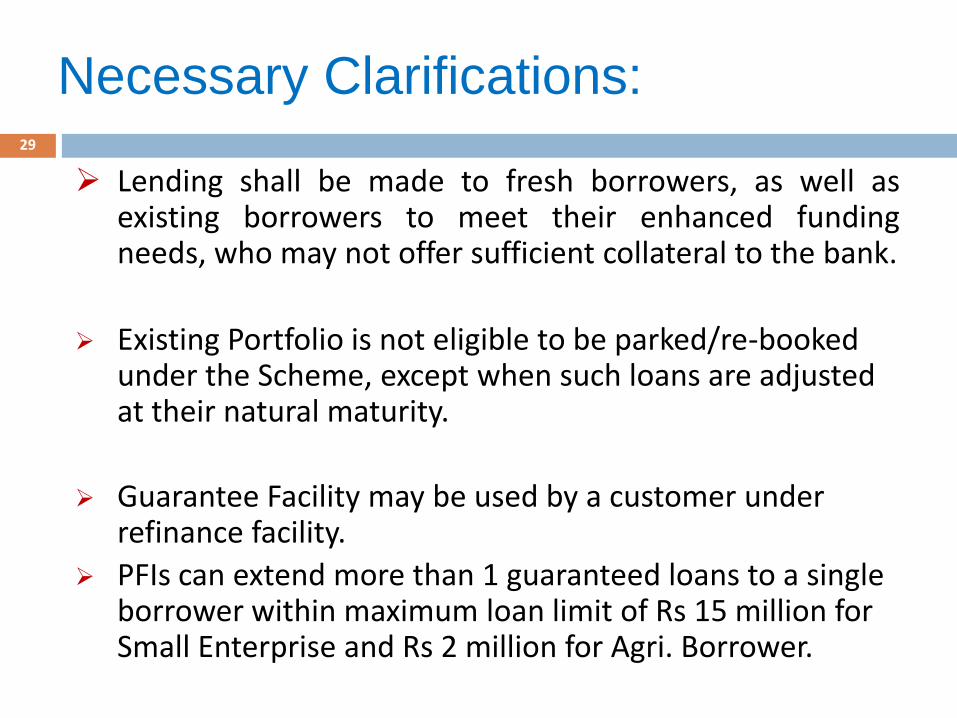

Lending shall be made to fresh borrowers, as well as existing borrowers to meet their enhanced funding needs, who may not offer sufficient collateral to the bank.

Existing Portfolio is not eligible to be parked/re-booked under the Scheme, except when such loans are adjusted at their natural maturity.

Guarantee Facility may be used by a customer under refinance facility.

PFIs can extend more than 1 guaranteed loans to a single borrower within maximum loan limit of Rs 15 million for Small Enterprise and Rs 2 million for Agri. Borrower.

Necessary Clarifications: 29

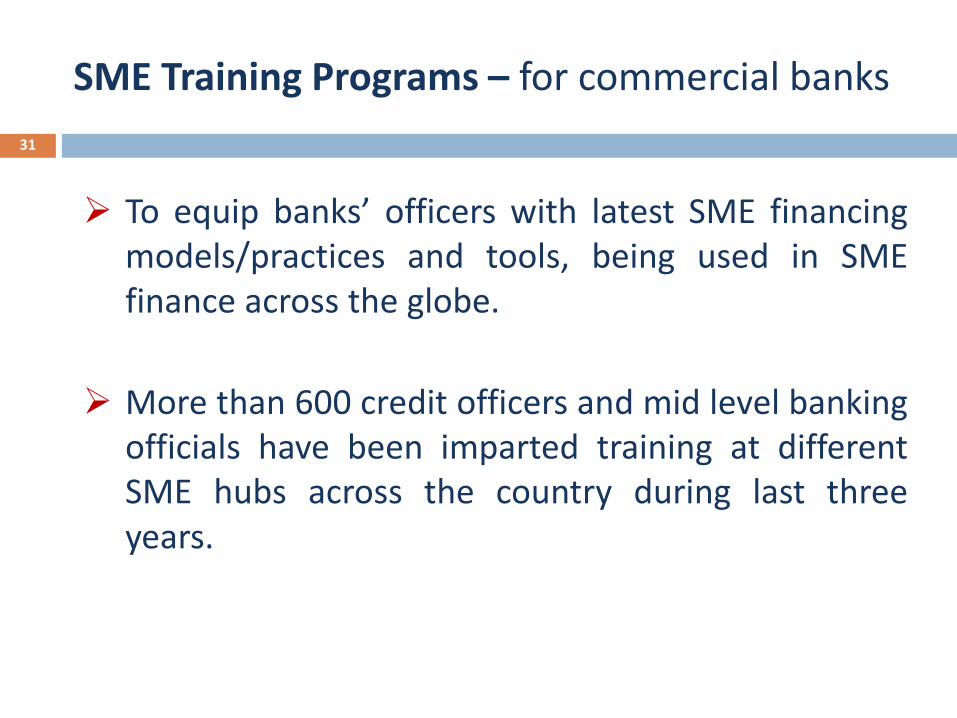

SME Training Programs – for commercial banks

To equip banks’ officers with latest SME financing models/practices and tools, being used in SME finance across the globe.

More than 600 credit officers and mid level banking officials have been imparted training at different SME hubs across the country during last three years.

31

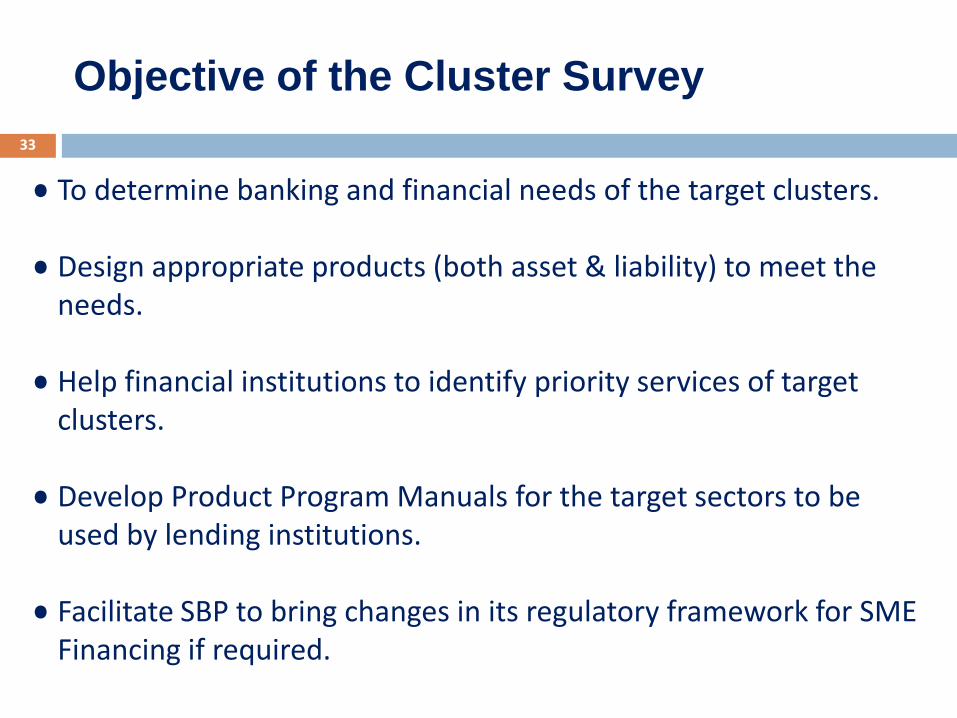

Objective of the Cluster Survey

• To determine banking and financial needs of the target clusters.

• Design appropriate products (both asset & liability) to meet the needs.

• Help financial institutions to identify priority services of target clusters.

• Develop Product Program Manuals for the target sectors to be used by lending institutions.

• Facilitate SBP to bring changes in its regulatory framework for SME Financing if required.

33

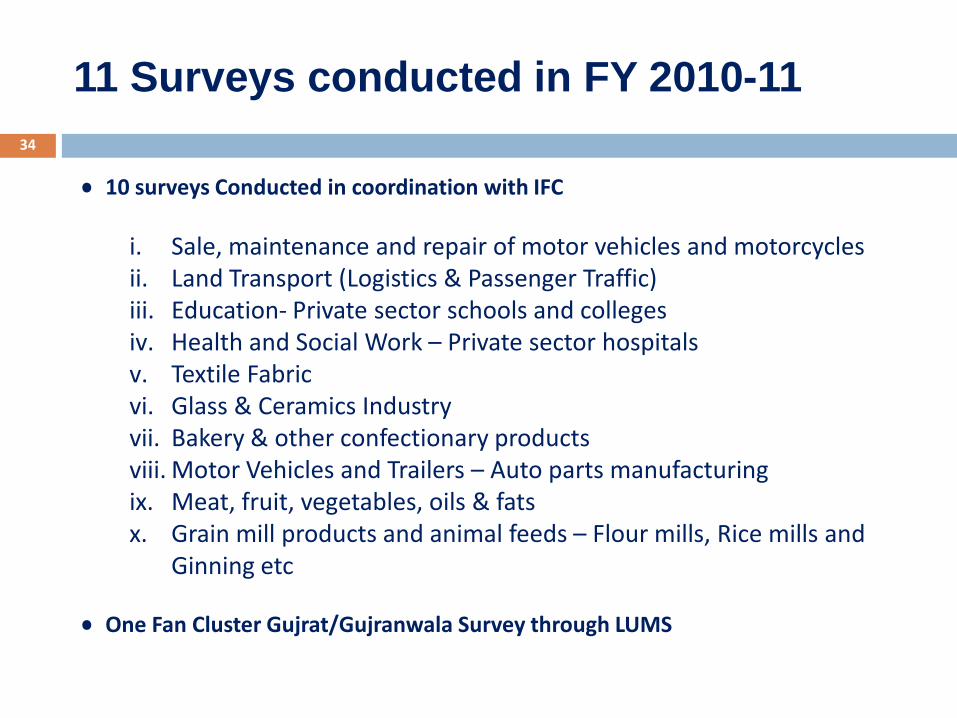

11 Surveys conducted in FY 2010-11

• 10 surveys Conducted in coordination with IFC

i. Sale, maintenance and repair of motor vehicles and motorcycles ii. Land Transport (Logistics & Passenger Traffic) iii. Education- Private sector schools and colleges iv. Health and Social Work – Private sector hospitals v. Textile Fabric vi. Glass & Ceramics Industry vii. Bakery & other confectionary products viii. Motor Vehicles and Trailers – Auto parts manufacturing ix. Meat, fruit, vegetables, oils & fats x. Grain mill products and animal feeds – Flour mills, Rice mills and

Ginning etc

• One Fan Cluster Gujrat/Gujranwala Survey through LUMS

34

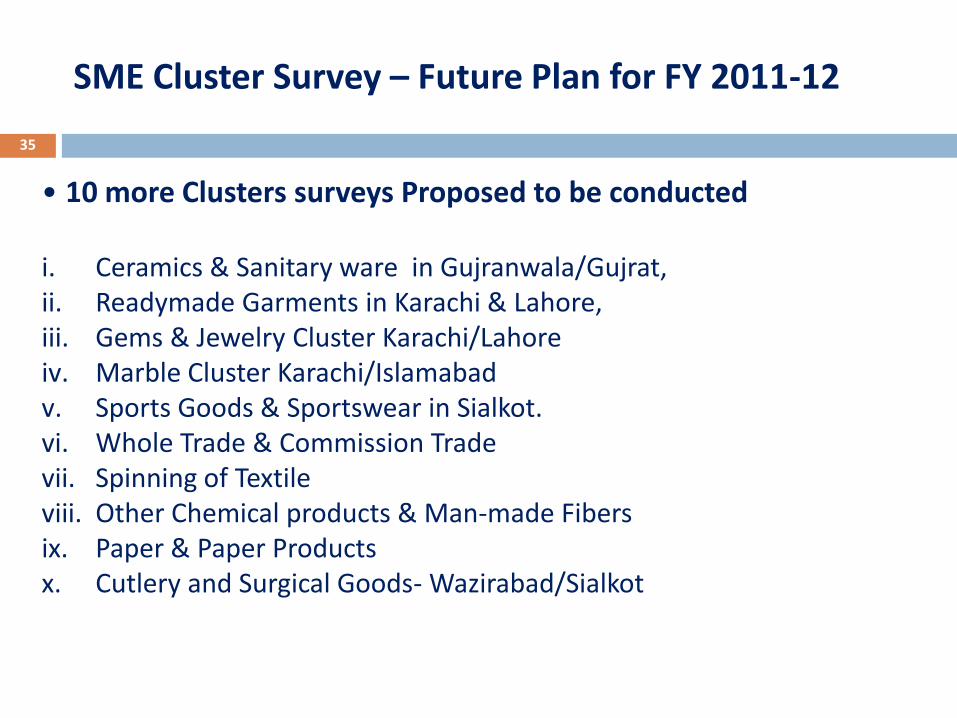

SME Cluster Survey – Future Plan for FY 2011-12

• 10 more Clusters surveys Proposed to be conducted i. Ceramics & Sanitary ware in Gujranwala/Gujrat, ii. Readymade Garments in Karachi & Lahore, iii. Gems & Jewelry Cluster Karachi/Lahore iv. Marble Cluster Karachi/Islamabad v. Sports Goods & Sportswear in Sialkot. vi. Whole Trade & Commission Trade vii. Spinning of Textile viii. Other Chemical products & Man-made Fibers ix. Paper & Paper Products x. Cutlery and Surgical Goods- Wazirabad/Sialkot

35

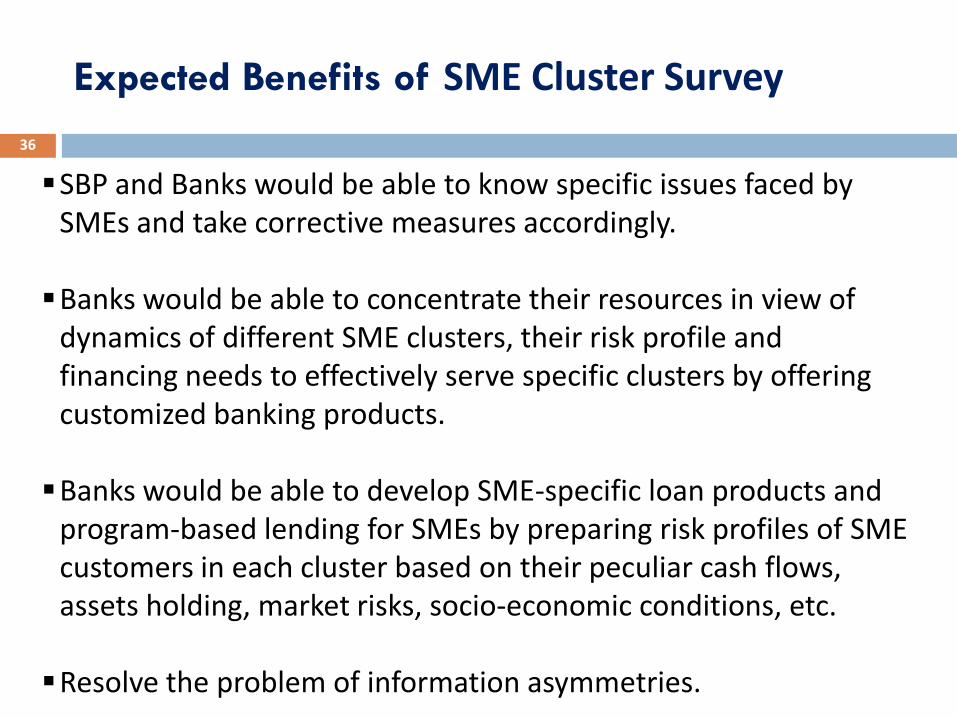

Expected Benefits of SME Cluster Survey

SBP and Banks would be able to know specific issues faced by SMEs and take corrective measures accordingly.

Banks would be able to concentrate their resources in view of

dynamics of different SME clusters, their risk profile and financing needs to effectively serve specific clusters by offering customized banking products.

Banks would be able to develop SME-specific loan products and

program-based lending for SMEs by preparing risk profiles of SME customers in each cluster based on their peculiar cash flows, assets holding, market risks, socio-economic conditions, etc.

Resolve the problem of information asymmetries.

36

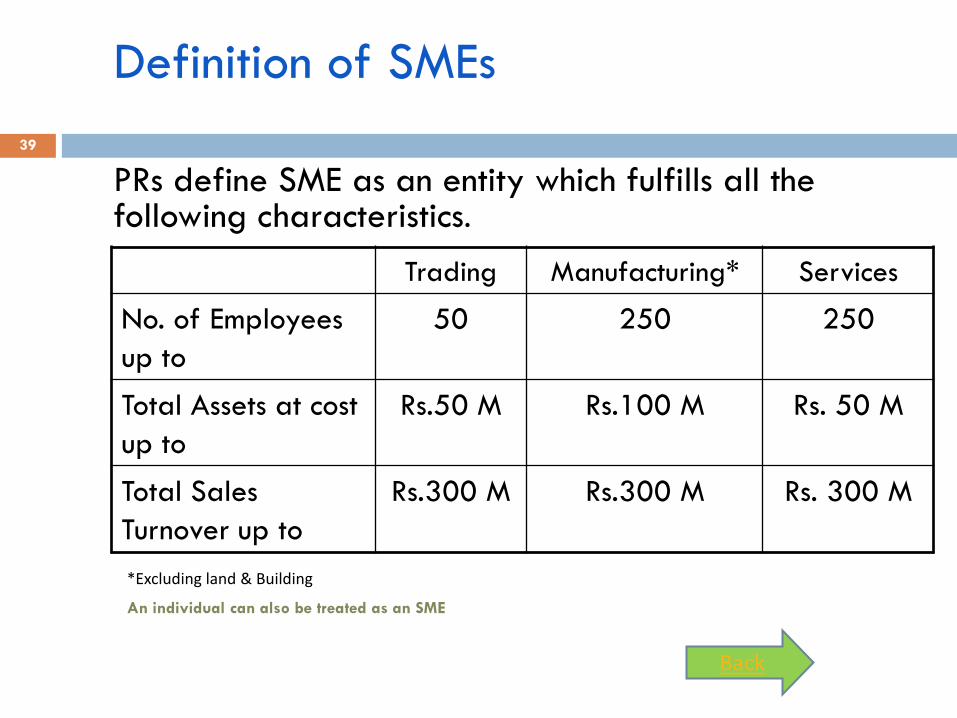

Definition of SMEs

PRs define SME as an entity which fulfills all the following characteristics.

Trading Manufacturing* Services

No. of Employees

up to

50 250 250

Total Assets at cost

up to

Rs.50 M Rs.100 M Rs. 50 M

Total Sales

Turnover up to

Rs.300 M Rs.300 M Rs. 300 M

*Excluding land & Building An individual can also be treated as an SME

Back

39