0 Attia- Solar in the Americas Benjamin Attia Analyst, Global Solar Markets [email protected]@solarbenattia Solar in the Americas Market Conditions, Policy and Finance Outlook Intersolar Europe 2017

North America: Resumption of Growth in 2019 as US utility-scale pipeline stalls

2020: US returns to 2016 installation levels

2019: Resumption of total market growth

US: 95% YoY GrowthCanada: National carbon tax, coal retirement timeline, federal 100% RE target, state-level tenders, and a MircoFITreboot in Ontario created uncertainty and limited 2016 installs.

3Attia- Solar in the Americas

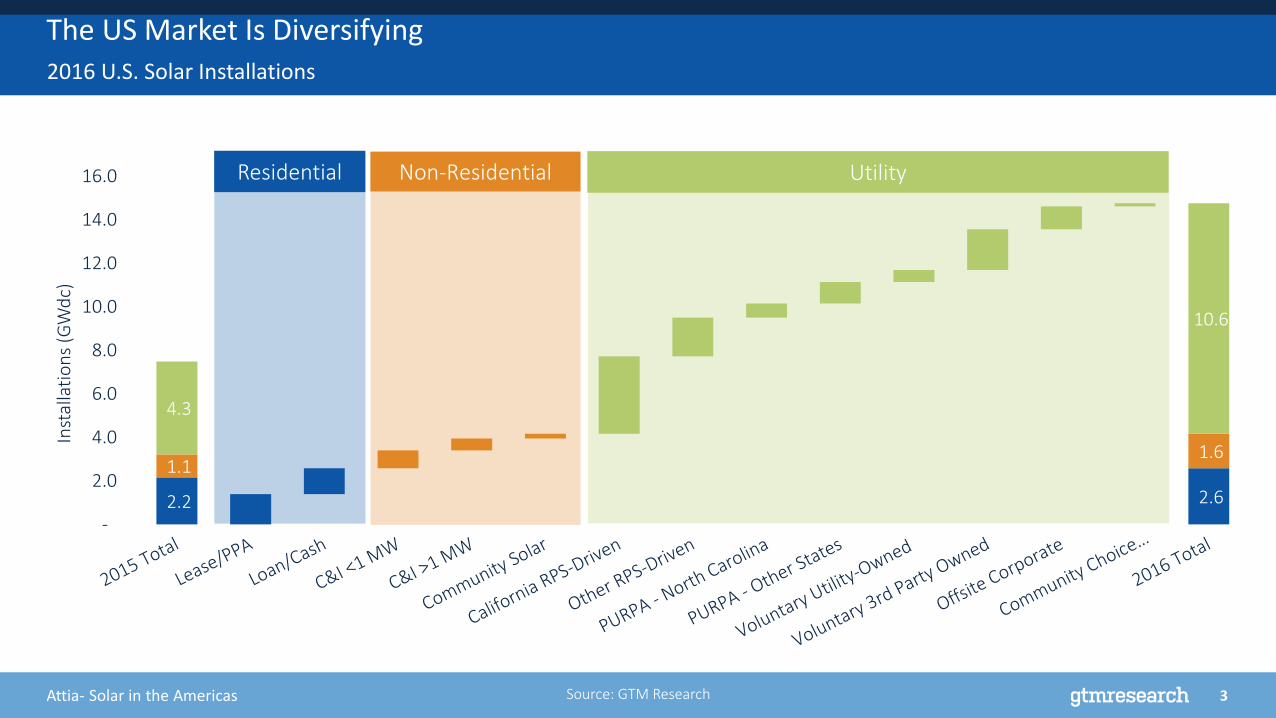

The US Market Is Diversifying2016 U.S. Solar Installations

2.2 2.6

1.1 1.6

4.3

10.6

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Inst

alla

tio

ns

(GW

dc)

Residential Non-Residential Utility

Source: GTM Research

4Attia- Solar in the Americas

There are a number of key non-RPS drivers in US Utility-scale Solar

Non RPS Drivers

Voluntary

Procurement

PURPA

Wholesale

Retail

Procurement

CCAs

MT

WY

ID

WA

OR

NV

UTCA

AZ

ND

SD

NE

CO

NM

TX

OK

KS

AR

LA

MO

IA

MN

WI

IL IN

KY

TN

MS AL GA

FL

SC

NC

VAWV

OH

MI

NY

PA

MDDE

NJ

CTRI

MA

ME

VT

NH

MD

37%

63%

4908

3549

1903543

RPS Driven Non RPS Driven

PURPA Voluntary Procurement

Retail Procurement CCA

% Share of Utility PV Pipeline

US States with 50 MW+ Contracted, Non-RPS Utility PV Pipeline as of March 2017

5Attia- Solar in the Americas

Emergence of Community Solar: Legislative and Voluntary Segments Both Set to Scale

126 9 6

2952

223

410

0

100

200

300

400

500

600

700

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

An

nu

al In

stal

lati

on

s (M

Wd

c)

Third Party Led Utility Led

3744

62

26

227

113

0

50

100

150

200

250

Coop IOU Muni

Uti

lity

Led

Co

mm

un

ity

Sola

r (M

Wd

c)

Operating In Development

Source: <Insert source>

Community Solar Installation Outlook:Third Party Led vs Utility Led Community Solar

Source: <Insert source>

Within Utility Led Community Solar:Emergence of IOUs Procuring Large Scale Community Solar

6Attia- Solar in the Americas

Source: GTM Research

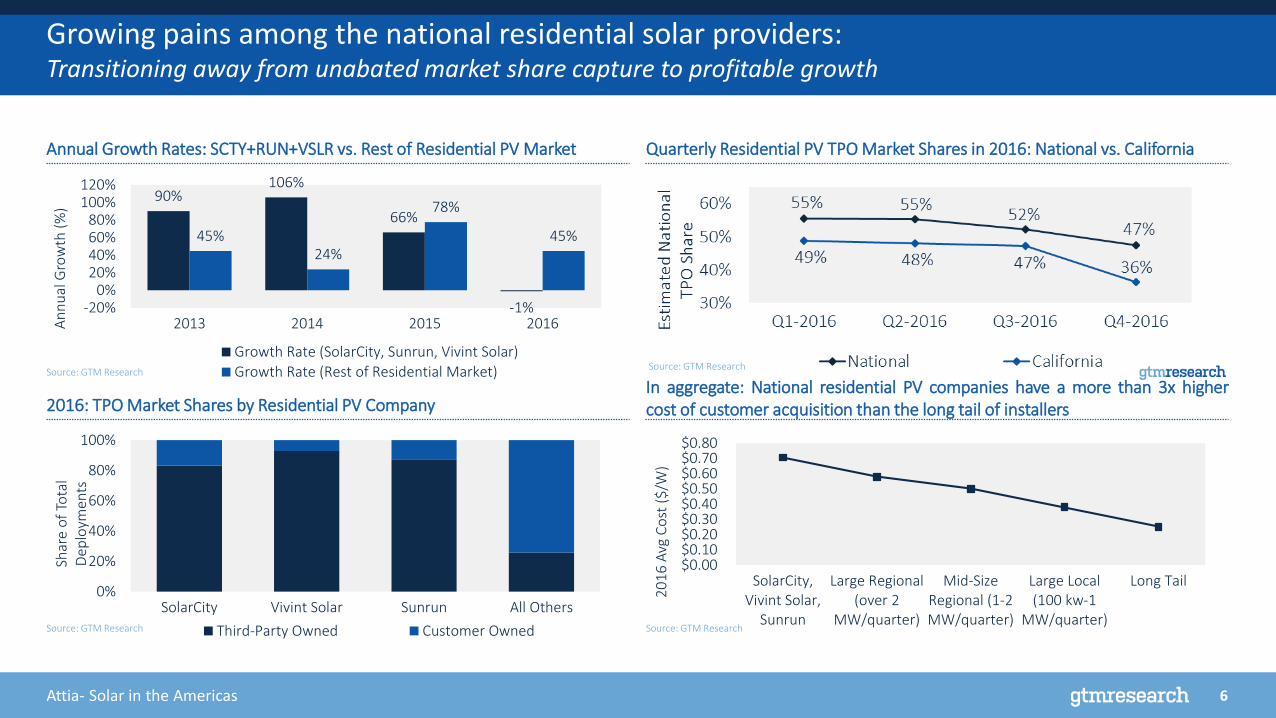

Growing pains among the national residential solar providers:Transitioning away from unabated market share capture to profitable growth

90%106%

66%

-1%

45%24%

78%

45%

-20%0%

20%40%60%80%

100%120%

2013 2014 2015 2016An

nu

al G

row

th (

%)

Growth Rate (SolarCity, Sunrun, Vivint Solar)

Growth Rate (Rest of Residential Market)

$0.00$0.10$0.20$0.30$0.40$0.50$0.60$0.70$0.80

SolarCity,Vivint Solar,

Sunrun

Large Regional(over 2

MW/quarter)

Mid-SizeRegional (1-2MW/quarter)

Large Local(100 kw-1

MW/quarter)

Long Tail

20

16

Avg

Co

st (

$/W

)

0%

20%

40%

60%

80%

100%

SolarCity Vivint Solar Sunrun All Others

Shar

e o

f To

tal

Dep

loym

ents

Third-Party Owned Customer Owned

Source: GTM Research

Annual Growth Rates: SCTY+RUN+VSLR vs. Rest of Residential PV Market Quarterly Residential PV TPO Market Shares in 2016: National vs. California

Source: GTM Research

2016: TPO Market Shares by Residential PV Company

Source: GTM Research

In aggregate: National residential PV companies have a more than 3x highercost of customer acquisition than the long tail of installers

7Attia- Solar in the Americas

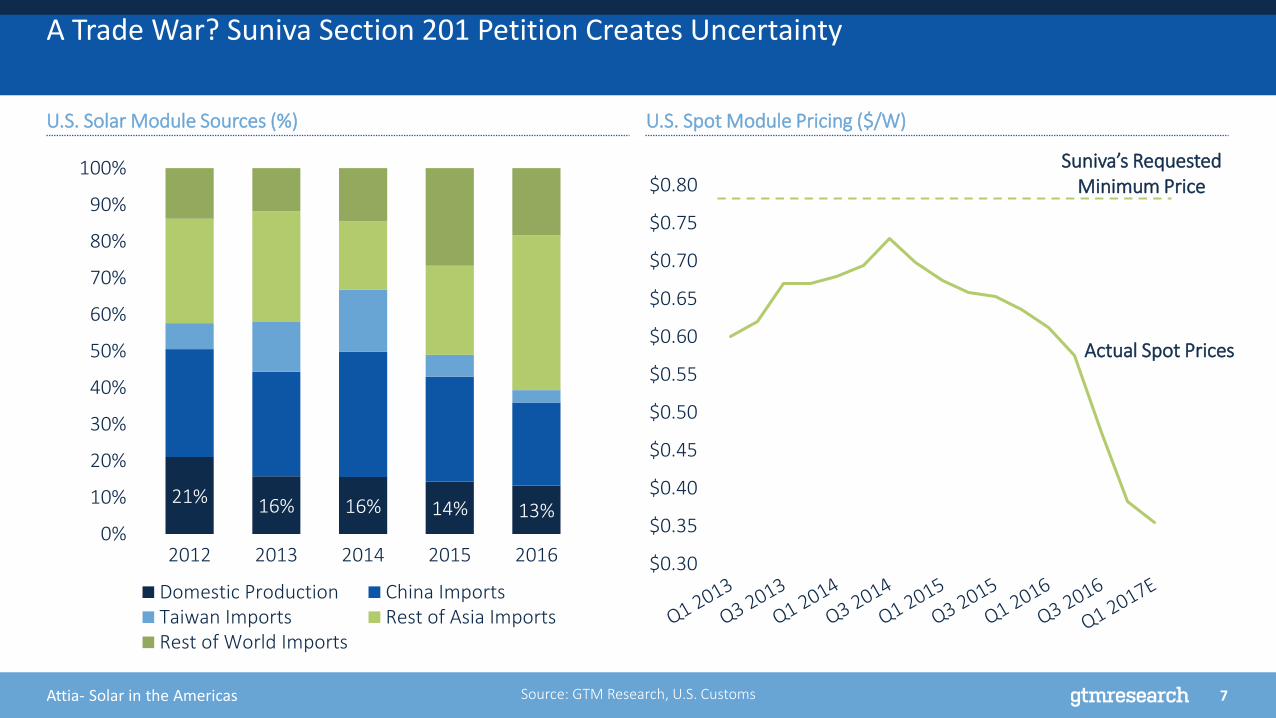

A Trade War? Suniva Section 201 Petition Creates Uncertainty

Source: GTM Research, U.S. Customs

21% 16% 16% 14% 13%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016

Domestic Production China ImportsTaiwan Imports Rest of Asia ImportsRest of World Imports

$0.30

$0.35

$0.40

$0.45

$0.50

$0.55

$0.60

$0.65

$0.70

$0.75

$0.80

Actual Spot Prices

Suniva’s Requested Minimum Price

U.S. Solar Module Sources (%) U.S. Spot Module Pricing ($/W)

8Attia- Solar in the Americas

-60%-40%-20%

0%20%40%60%

HI

MA AZ

CA VT

NY

NM DE NJ

SC DC

MD

NH

MN CT

UT RI

PA FL ME KY TX MI

WI

CO

WY

GA

OH

NC

AR IL LA VA

MO KS IA

MT IN NE

OR

MS

NV ID AK AL

WV

WA

TN OK

SD NDYe

ar 1

Bill

Imp

act

fro

m

Sola

r (%

)

-60%

-40%

-20%

0%

20%

40%

HI

MA VT

CA

DE

AZ

NM N

J

NY

DC SC MD

MN

NH CT

UT RI

PA KY ME FL TX MI

WI

CO

WY

OH

GA IL

NC

AR LA

MO

MT

VA IA KS IN NE

OR ID MS

NV

AK

WV AL

WA

TN OK

ND SD

Year

1 B

ill Im

pac

t fr

om

So

lar

(%)

If Suniva’s minimum module price proposal is approved in H2 2017: The number of states at residential PV grid parity in 2018 will drop from 36 to 27

Source: GTM Research

U.S. States At Residential Grid Parity, 2018: Base Case System Pricing

Source: GTM Research

U.S. States At Residential Grid Parity, 2018: Including Suniva’s Proposed Minimum $0.72/W Price for Imported Modules (Year 2)

Note: Grid parity metrics account for all NEM and rate reforms currently in effect for modeled utilities.

9Attia- Solar in the Americas

1. Macro level uncertainty: Solar trade dispute, corporate tax reform, NEM and rate reform risk

2. Residential: Sub 15% annual growth in a more fragmented installer landscape, paired with the emergence of loans and cash sales collectively outpacing third party owned leases and PPAs

3. Non-Residential: Continued growth hinges on community solar (near term) and solar-plus-storage (long term) amidst state incentive reductions and TOU rate reforms across major markets

What comes next for U.S. solar?

4. Utility-Scale: On track for another boom in procurement heading into 2019 in response to the scheduled stepdown of the 30% federal ITC, supporting growth in the 2019-2021 timeframe

10Attia- Solar in the Americas

Latin America

11Attia- Solar in the Americas

0.2 0.7

2.4 2.8 3.14.2 4.8

0.00.4

1.01.3 1.1

1.4

1.9

0.80.5

0.7

0.9 1.1

1.2

1.3

0.9

1.11.3

1.5

1.7

0.9

1.1

1.1

1.21.3

1.3

1.4

1.5 1.62.4

5.8

7.17.8

9.7

11.5174%

9%

49%

147%

22%

10%24% 18%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

0

2

4

6

8

10

12

14

2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

GW

dc

Mexico Brazil Chile Argentina Rest of Latin America Annual Growth

Latin American Markets, led by Mexico and Brazil, will take off in 2018

Close to 3GW of projects in Brazil and Mexico are

under construction and set to come online next year

12Attia- Solar in the Americas

Source: GTM Research Latin America PV Project Tracker

Regional Project Pipelines (MWdc)

Chile approaches 2GW; Mexico Begins Construction for a Huge 2018 as Investment Booms

Operational6%, 60 MW

Contracted94%, 916 MW

Argentina

Operational50%, 761 MW

Under Construction27%, 401 MW

Contracted23%, 350 MW

Central America & Caribbean

Operational24%, 1941

MW

Under Construction

40%, 3142 MW

Contracted36%, 2886 MW

Chile

Operational7%, 390 MW

Under Construction

33%, 1948 MWContracted

60%, 3456 MW

Mexico

Operational2%, 62 MW

Under Construction

32%, 1031 MW

Contracted66%, 2092 MW

Brazil

Operational27%, 230 MW

Under Construction

39%, 328 MW

Contracted34%, 284 MW

Rest of South America

13Attia- Solar in the Americas

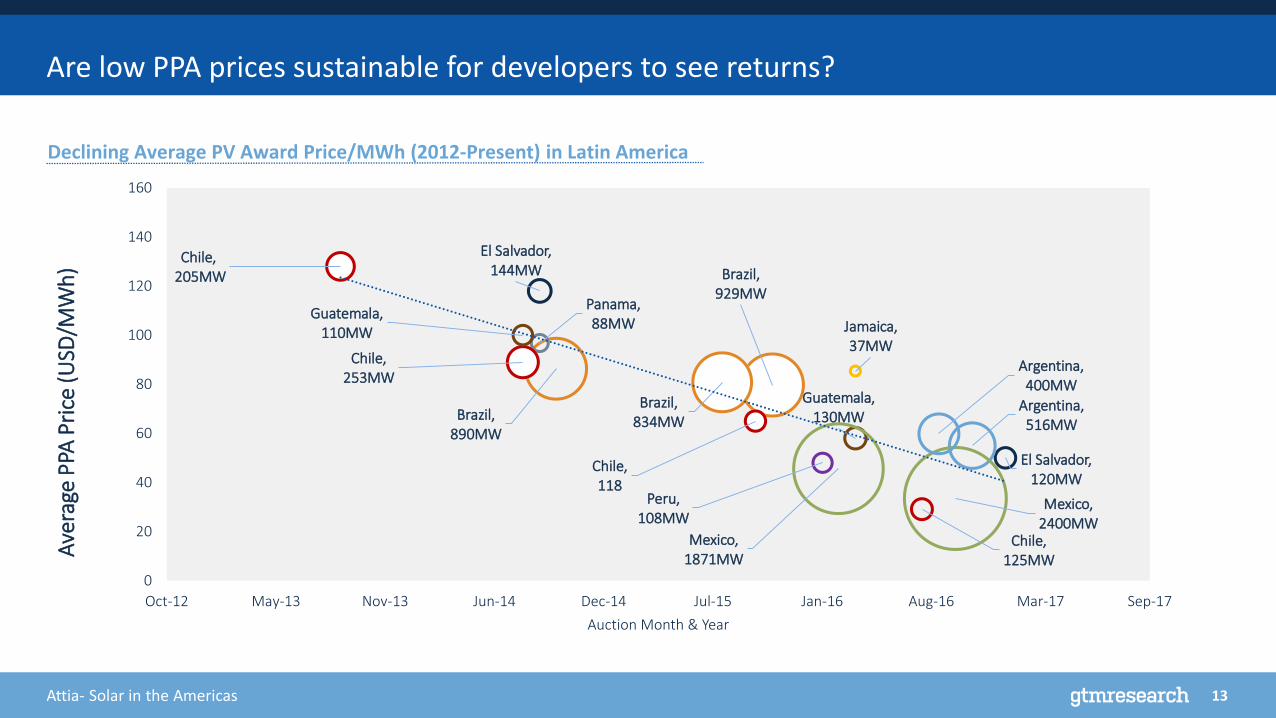

Are low PPA prices sustainable for developers to see returns?

Declining Average PV Award Price/MWh (2012-Present) in Latin America

14Attia- Solar in the Americas

Third Mexican Auction likely to include Export Zone Preferences as in A1

Average Export Zone Preference Adjustment in A1 was -$10.90/MWh. Highest was in Yucatan at -$21.98/MWh.

30% reduction in average pre-adjusted solar bid from A1 to A2, with a leading bid of $26.99/MWh in San Luis Potosi by FRV.

15Attia- Solar in the Americas

Chile: Despite Large Developer Pipelines, SIC-SING IC Delays Limit 2017 Installations

56

55

81

163

145

41

122

72

334

255

490

11

58

131

188

23

309

185

300

235

265

123

71

432

60

75

47

74

146

232

129

229

34

225

234

65

343

134

0 200 400 600 800 1000 1200

AES

Grenergy

X-Elio

SunPower

Etrion

First Solar

Colbun

Solairedirect/Engie

Solarpack

EDF

Ingenostrum

Pattern Energy

Rijn Capital

Austrian Solar

Mainstream Renewable…

Actis

Acciona

Enel Green Power

MWdcOperational Under Construction Contracted

16Attia- Solar in the Americas

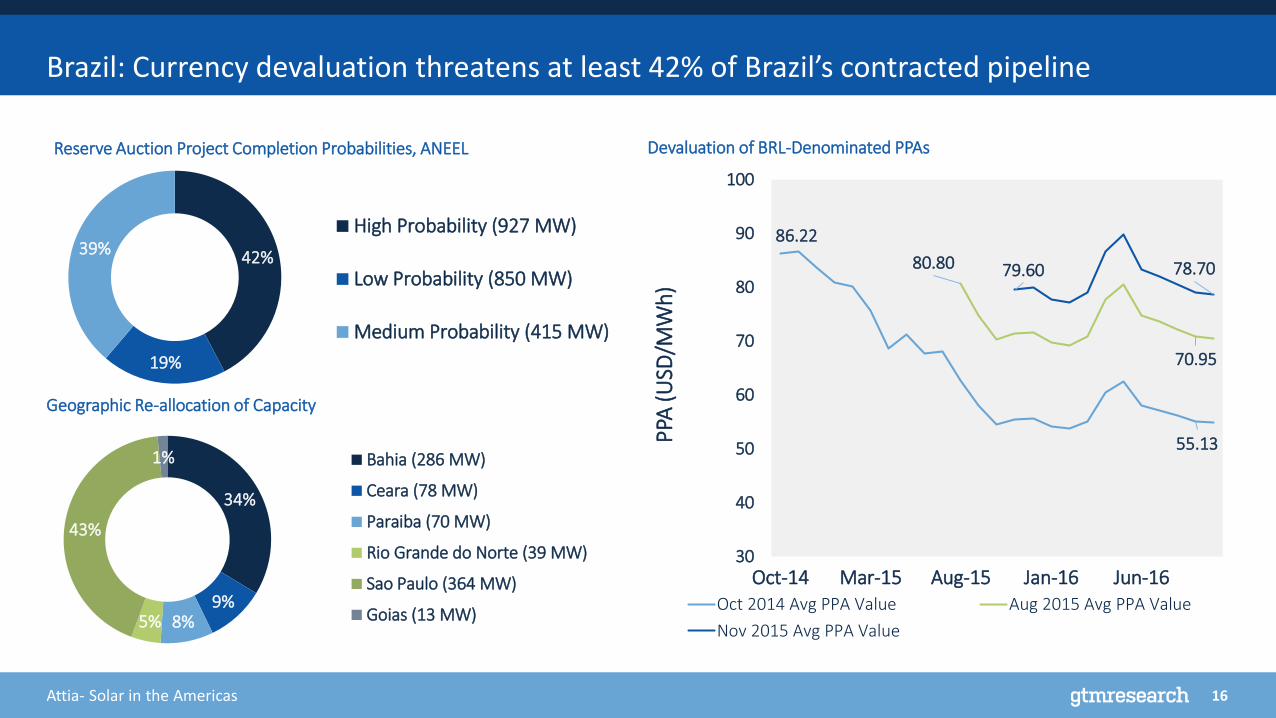

Brazil: Currency devaluation threatens at least 42% of Brazil’s contracted pipeline

86.22

55.13

80.80

70.95

79.60 78.70

30

40

50

60

70

80

90

100

Oct-14 Mar-15 Aug-15 Jan-16 Jun-16

PPA

(USD

/MW

h)

Oct 2014 Avg PPA Value Aug 2015 Avg PPA Value

Nov 2015 Avg PPA Value

42%

19%

39%High Probability (927 MW)

Low Probability (850 MW)

Medium Probability (415 MW)

34%

9%8%5%

43%

1% Bahia (286 MW)

Ceara (78 MW)

Paraiba (70 MW)

Rio Grande do Norte (39 MW)

Sao Paulo (364 MW)

Goias (13 MW)

Geographic Re-allocation of Capacity

Reserve Auction Project Completion Probabilities, ANEEL Devaluation of BRL-Denominated PPAs

17Attia- Solar in the Americas

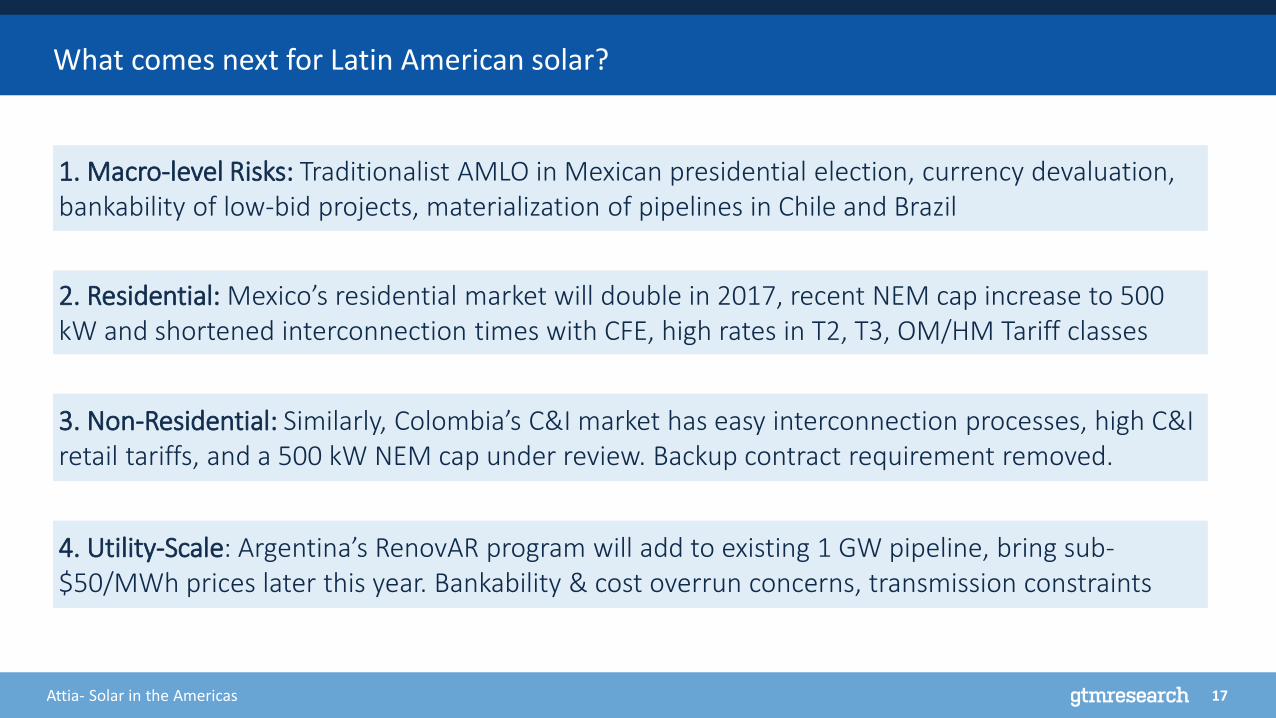

1. Macro-level Risks: Traditionalist AMLO in Mexican presidential election, currency devaluation, bankability of low-bid projects, materialization of pipelines in Chile and Brazil

2. Residential: Mexico’s residential market will double in 2017, recent NEM cap increase to 500 kW and shortened interconnection times with CFE, high rates in T2, T3, OM/HM Tariff classes

3. Non-Residential: Similarly, Colombia’s C&I market has easy interconnection processes, high C&I retail tariffs, and a 500 kW NEM cap under review. Backup contract requirement removed.

What comes next for Latin American solar?

4. Utility-Scale: Argentina’s RenovAR program will add to existing 1 GW pipeline, bring sub-$50/MWh prices later this year. Bankability & cost overrun concerns, transmission constraints

18Attia- Solar in the Americas

Q2 2017 Global Outlook by Region: Americas Will Comprise 19% of 2017 Global Demand

Global PV Demand by Regional Demand Share, 2007-2022E

Source: GTM Research Global Solar DemandMonitor Q2 2017

17%9% 10% 10% 11% 12% 13% 13%

55%

57%51%

45%39% 32% 28% 25%

4%

7%13%

12%

12%14%

14%14%

2%3% 2%

3%4%

4%5%

6%

2%2% 3%

6%8%

9% 9% 10%

3%2%

3% 7%8% 8% 9% 10%

16%20% 16% 14% 16% 17% 17% 17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

Glo

bal

Dem

and

Sh

are

(%)

Europe East Asia South Asia Southeast Asia MENAT Latin America North America Sub-Saharan Africa West Africa