29

Solvency Capital Requirement under Standard Approach UNIPOLSAI Case Study Alma Mater Studiorum- Universita di Bologna Balutel Daniela Błachut Marek Wanek Roman Oliver Arturo De Martino

Solvency Capital Requirement under Standard Approach

UNIPOLSAI Case Study

Alma Mater Studiorum- Universita di Bologna

Balutel Daniela Błachut Marek Wanek Roman Oliver Arturo De Martino

Where do we operate within art 138 of Solvency II Directive?

Introduction

PILAR I

Quantitative Capital Requirements:

Technical Provisions

Minimal Capital Requirements

(MCR)

Solvency Capital Requirement (SCR)

SCR Basic Solvency Capital Requirement

Interest rate

Equity

Property

Spread

Currency

Concentration

Counter cyclical

premium

SCR

M

A

R

K

E

T

R I

S

K

Adj Op

Account for taxes and loss absorbing capacity of Life Insurance business

Operational Risk margin, full correlation

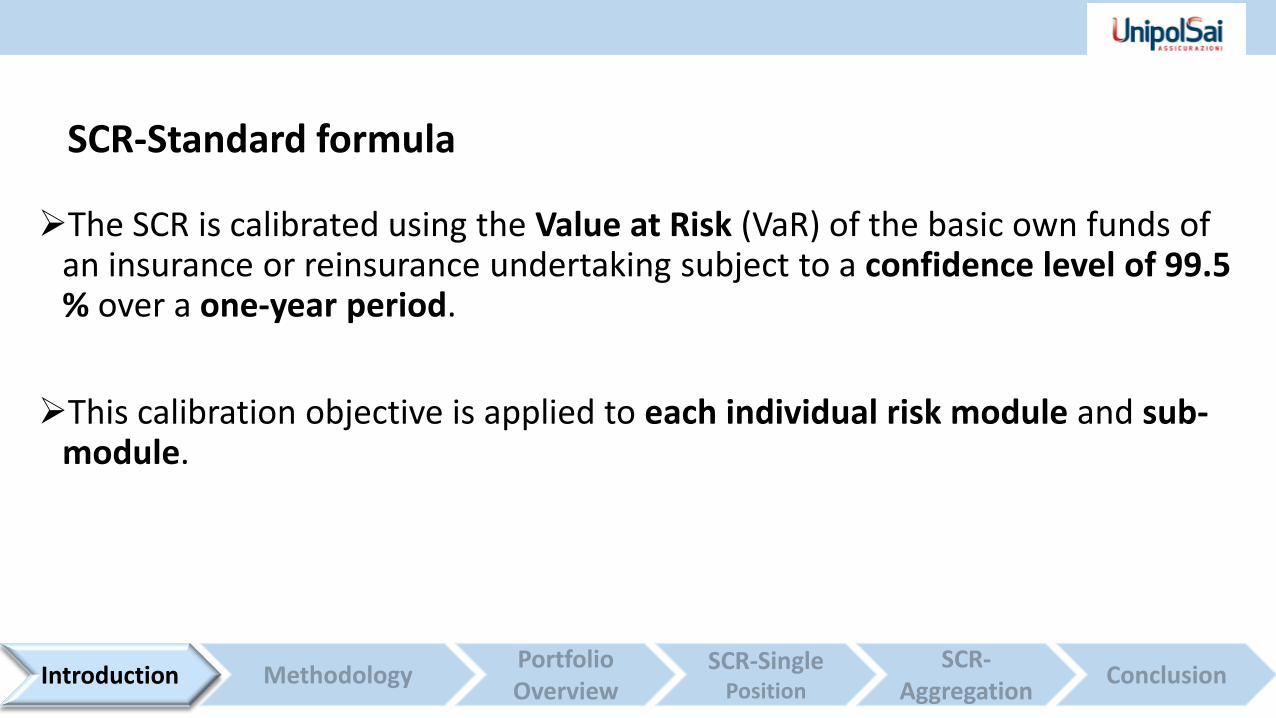

The SCR is calibrated using the Value at Risk (VaR) of the basic own funds of an insurance or reinsurance undertaking subject to a confidence level of 99.5 % over a one-year period.

This calibration objective is applied to each individual risk module and sub-module.

Introduction

SCR-Standard formula

Methodology

In appliance to art 103 of Solvency II Directive we are going to present the estimation of the SCR for the Market risk module solely.

Market risk in the Solvency II standard model is calculated through a scenario based and risk factor approach.

(Linear) Aggregation of sub-modules is done through a standardized correlation matrix.

NAV = difference between assets A and liabilities L, excluding subordinated liabilities.

Methodology

Methodology

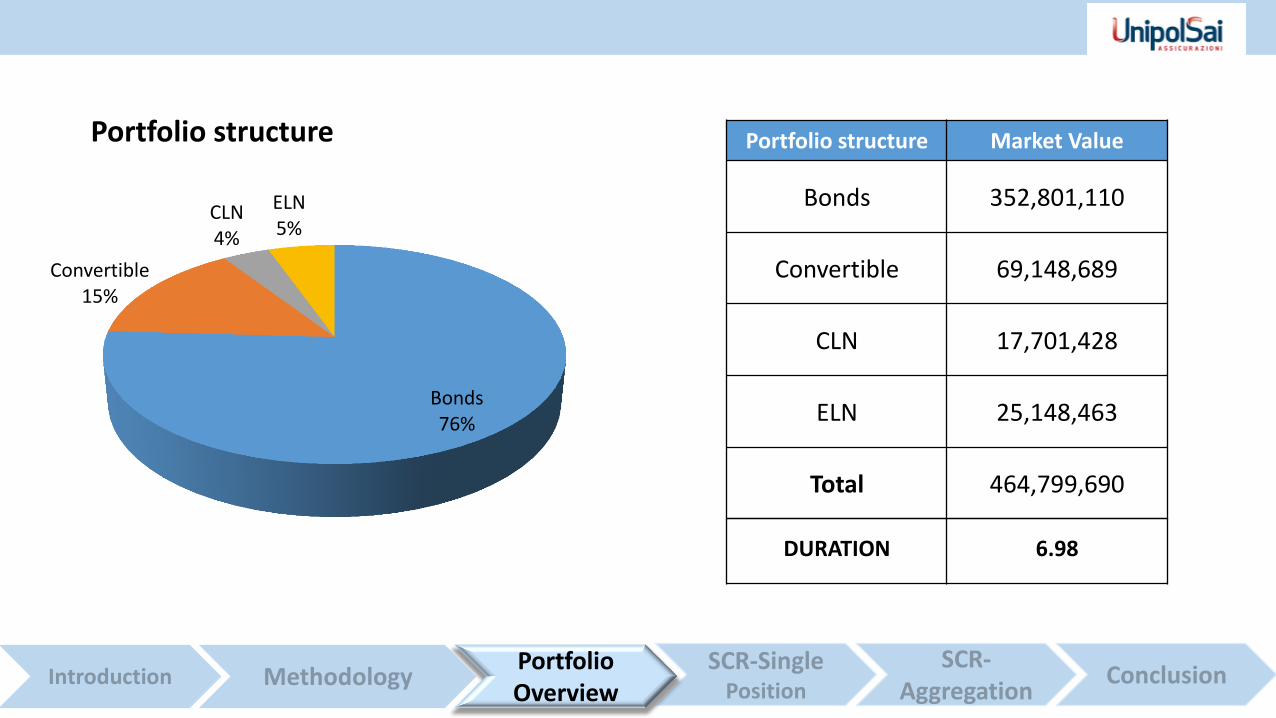

Portfolio Overview

Bonds 76%

Convertible 15%

CLN 4%

ELN 5%

Portfolio structure Market Value

Bonds 352,801,110

Convertible 69,148,689

CLN 17,701,428

ELN 25,148,463

Total 464,799,690

Portfolio structure

Portfolio Overview

DURATION 6.98

Bond Issuer Nominal Dirty Price Market Value Mod. Duration

XS1169707087 UNICREDIT SPA 20,000,000 106.233 21,246,535 2.98

XS0357578722 INTESA SANPAOLO SPA 30,000,000 122.983 36,894,840 14.30

FR0012432904 DANONE SA 30,000,000 102.051 30,615,366 2.89

XS1403015156 UNILEVER NV 40,000,000 101.427 40,570,704 10.34

ES0413900392 BANCO SANTANDER SA 10,000,000 99.219 9,921,881 8.26

XS0420558248 BNP PARIBAS 35,000,000 125.917 44,070,778 4.40

IT0000366721 BUONI POLIENNALI DEL TES 80,000,000 140.871 112,696,985 5.38

IT0003934657 BUONI POLIENNALI DEL TES 50,000,000 113.568 56,784,021 13.85

Subtotal 352,801,110

Portfolio structure - Bonds

Portfolio Overview

Convertible

XS1327914062 TOTAL SA 15,000,000 102.869 15,430,312 5.69

XS1394957309 ENI SPA 15,000,000 103.043 15,456,380 5.16

DE000A1ML0D9 ADIDAS AG 20,000,000 191.310 38,261,996 3.03

Subtotal 69,148,689

CLN

UBS 01/12/2021 CNL Italy UBS 5,000,000 107.700 5,385,007 4.29 SOC GEN 01/03/2019 CNL

Intesa San PaoloSOCIETE GENERALE 12,000,000 102.637 12,316,421 6.20

Subtotal 17,701,428

ELN

Highlands Deutsche Bank AG 20,000,000 125.742 25,148,463 3.71

Subtotal 25,148,463

Portfolio structure - Convertibles, CLNs and ELNs

Portfolio Overview

Bond Issuer Nominal Dirty Price Market Value Mod. Duration

XS1169707087 UNICREDIT SPA 20,000,000 106.233 21,246,535 2.98

XS0357578722 INTESA SANPAOLO SPA 30,000,000 122.983 36,894,840 14.30

FR0012432904 DANONE SA 30,000,000 102.051 30,615,366 2.89

XS1403015156 UNILEVER NV 40,000,000 101.427 40,570,704 10.34

ES0413900392 BANCO SANTANDER SA 10,000,000 99.219 9,921,881 8.26

XS0420558248 BNP PARIBAS 35,000,000 125.917 44,070,778 4.40

IT0000366721 BUONI POLIENNALI DEL TES 80,000,000 140.871 112,696,985 5.38

IT0003934657 BUONI POLIENNALI DEL TES 50,000,000 113.568 56,784,021 13.85

Subtotal 352,801,110

SCR - Single Positions

-0,01

-0,005

0

0,005

0,01

0,015

0,02

0,025

0,03

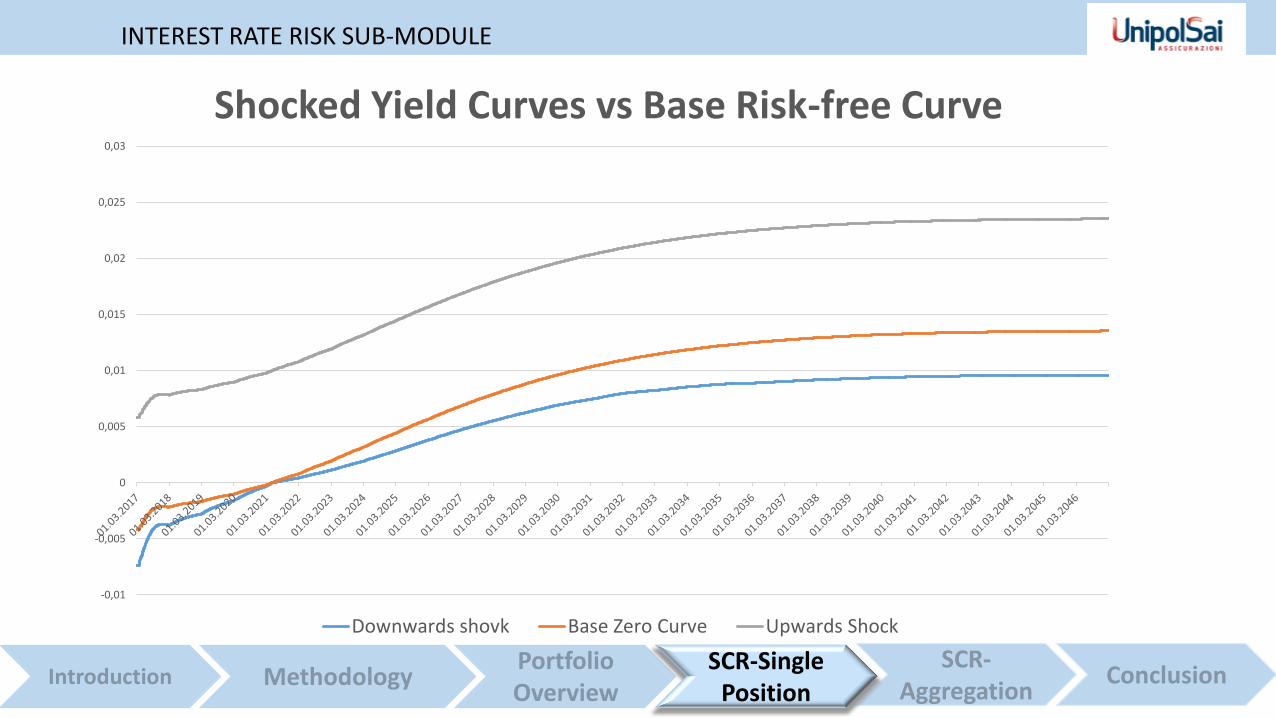

Shocked Yield Curves vs Base Risk-free Curve

Downwards shovk Base Zero Curve Upwards Shock

SCR-Single Position

INTEREST RATE RISK SUB-MODULE

Scenario IntUp IntDown

Market Value Market Value Market Value

Bonds 352,801,110 333,068,221 357,172,796

Convertibles 69,148,689 67,842,140 69,230,365

CLNs 17,701,428 16,734,011 17,796,739

ELNs 25,148,463 25,148,463 25,148,463

Total 464,799,690 442,792,835 469,348,362

Unshocked

Interest rate risk sub-module summary

SCR-Single Position

Scenario

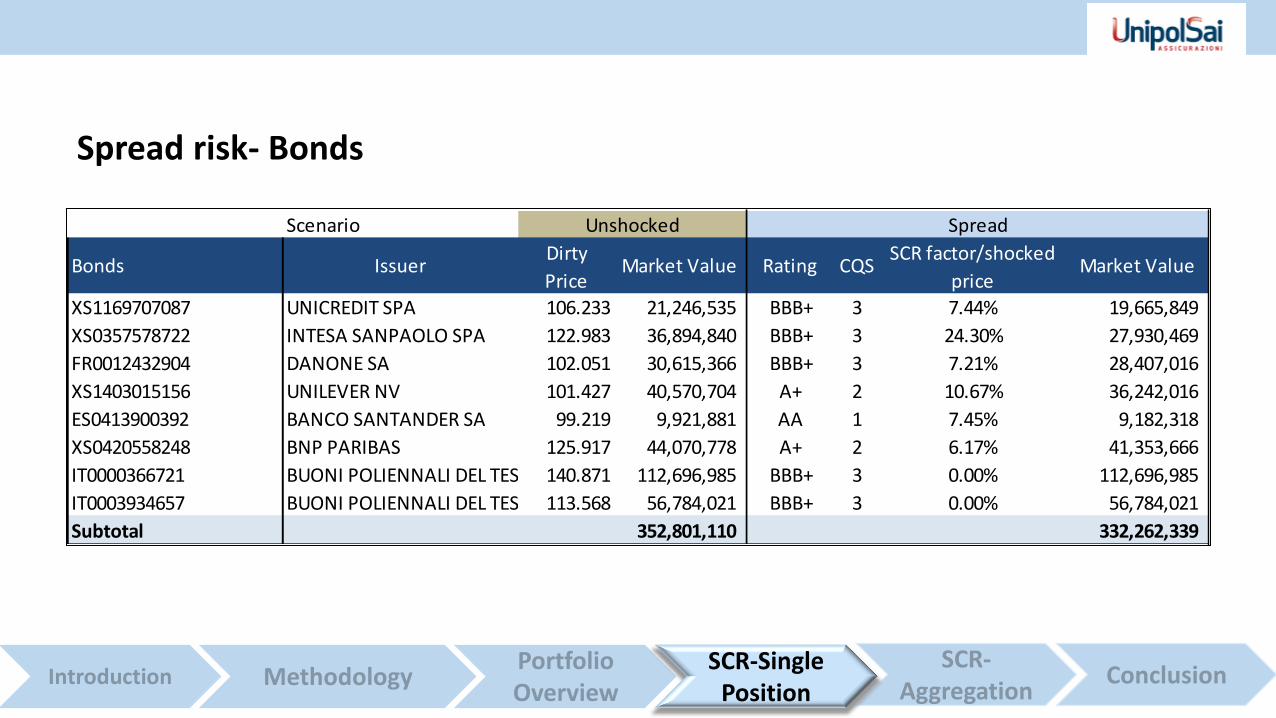

Bonds IssuerDirty

PriceMarket Value Rating CQS

SCR factor/shocked

priceMarket Value

XS1169707087 UNICREDIT SPA 106.233 21,246,535 BBB+ 3 7.44% 19,665,849

XS0357578722 INTESA SANPAOLO SPA 122.983 36,894,840 BBB+ 3 24.30% 27,930,469

FR0012432904 DANONE SA 102.051 30,615,366 BBB+ 3 7.21% 28,407,016

XS1403015156 UNILEVER NV 101.427 40,570,704 A+ 2 10.67% 36,242,016

ES0413900392 BANCO SANTANDER SA 99.219 9,921,881 AA 1 7.45% 9,182,318

XS0420558248 BNP PARIBAS 125.917 44,070,778 A+ 2 6.17% 41,353,666

IT0000366721 BUONI POLIENNALI DEL TES 140.871 112,696,985 BBB+ 3 0.00% 112,696,985

IT0003934657 BUONI POLIENNALI DEL TES 113.568 56,784,021 BBB+ 3 0.00% 56,784,021

Subtotal 352,801,110 332,262,339

Unshocked Spread

Spread risk- Bonds

SCR-Single Position

Scenario

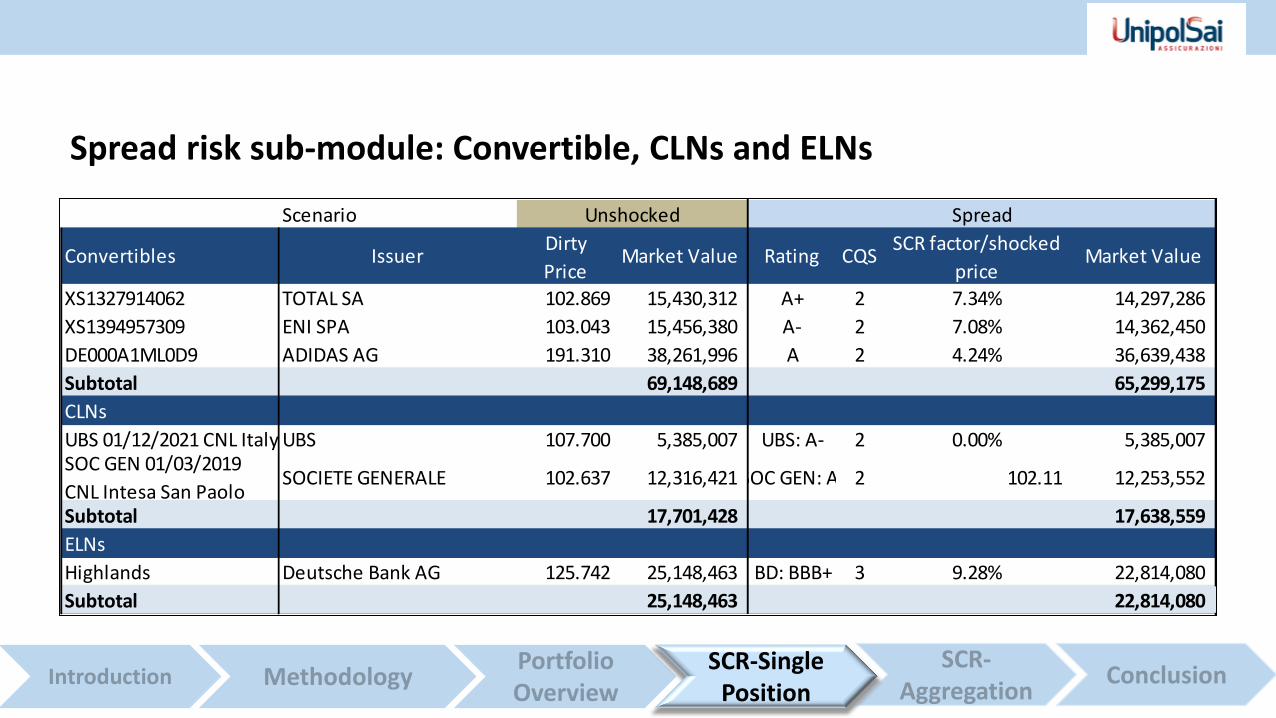

Convertibles IssuerDirty

PriceMarket Value Rating CQS

SCR factor/shocked

priceMarket Value

XS1327914062 TOTAL SA 102.869 15,430,312 A+ 2 7.34% 14,297,286

XS1394957309 ENI SPA 103.043 15,456,380 A- 2 7.08% 14,362,450

DE000A1ML0D9 ADIDAS AG 191.310 38,261,996 A 2 4.24% 36,639,438

Subtotal 69,148,689 65,299,175

CLNs

UBS 01/12/2021 CNL Italy UBS 107.700 5,385,007 UBS: A- 2 0.00% 5,385,007 SOC GEN 01/03/2019

CNL Intesa San PaoloSOCIETE GENERALE 102.637 12,316,421 SOC GEN: A- 2 102.11 12,253,552

Subtotal 17,701,428 17,638,559

ELNs

Highlands Deutsche Bank AG 125.742 25,148,463 BD: BBB+ 3 9.28% 22,814,080

Subtotal 25,148,463 22,814,080

Unshocked Spread

Spread risk sub-module: Convertible, CLNs and ELNs

SCR-Single Position

Scenario Unshocked Spread

Assets Market Value Market Value

Bonds 352,801,110 332,262,339

Convertibles 69,148,689 65,299,175

CLNs 17,701,428 17,638,559

ELNs 25,148,463 22,814,080

Total 464,799,690 438,014,154

Spread risk sub-module summary

SCR-Single Position

Scenario

Convertibles Issuer Market Value Dirty Price Market Value

XS1327914062 TOTAL SA 15,430,312 99.056 14,858,345

XS1394957309 ENI SPA 15,456,380 96.032 14,404,764

DE000A1ML0D9 ADIDAS AG 38,261,996 115.752 23,150,385

Subtotal 69,148,689 52,413,493

CLNs

UBS 01/12/2021 CNL Italy UBS 5,385,007 107.700 5,385,007 SOC GEN 01/03/2019

CNL Intesa San PaoloSOCIETE GENERALE 12,316,421 102.637 12,316,421

Subtotal 17,701,428 17,701,428

ELNs

Highlands Deutsche Bank AG 25,148,463 94.829 18,965,750

Subtotal 25,148,463 18,965,750

Unshocked Equity

Equity risk sub-module: Convertibles, CLNs and ELNs

SCR-Single Position

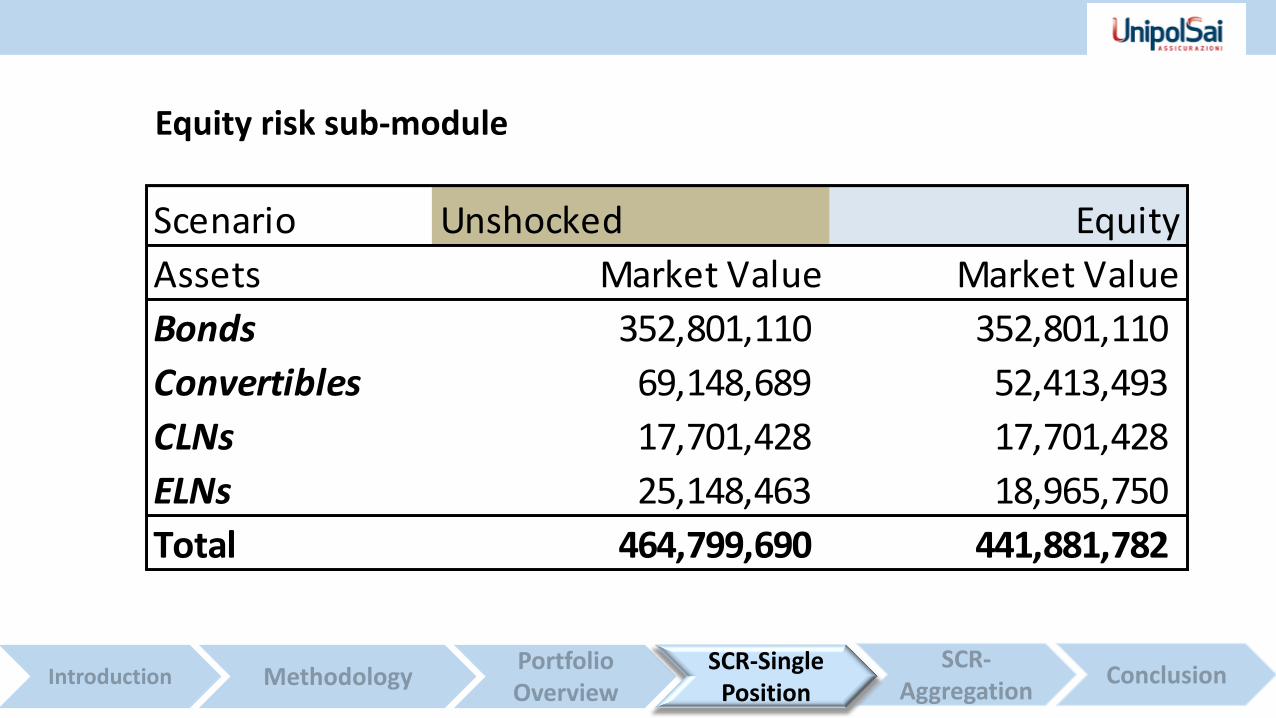

Scenario Unshocked Equity

Assets Market Value Market Value

Bonds 352,801,110 352,801,110

Convertibles 69,148,689 52,413,493

CLNs 17,701,428 17,701,428

ELNs 25,148,463 18,965,750

Total 464,799,690 441,881,782

Equity risk sub-module

SCR-Single Position

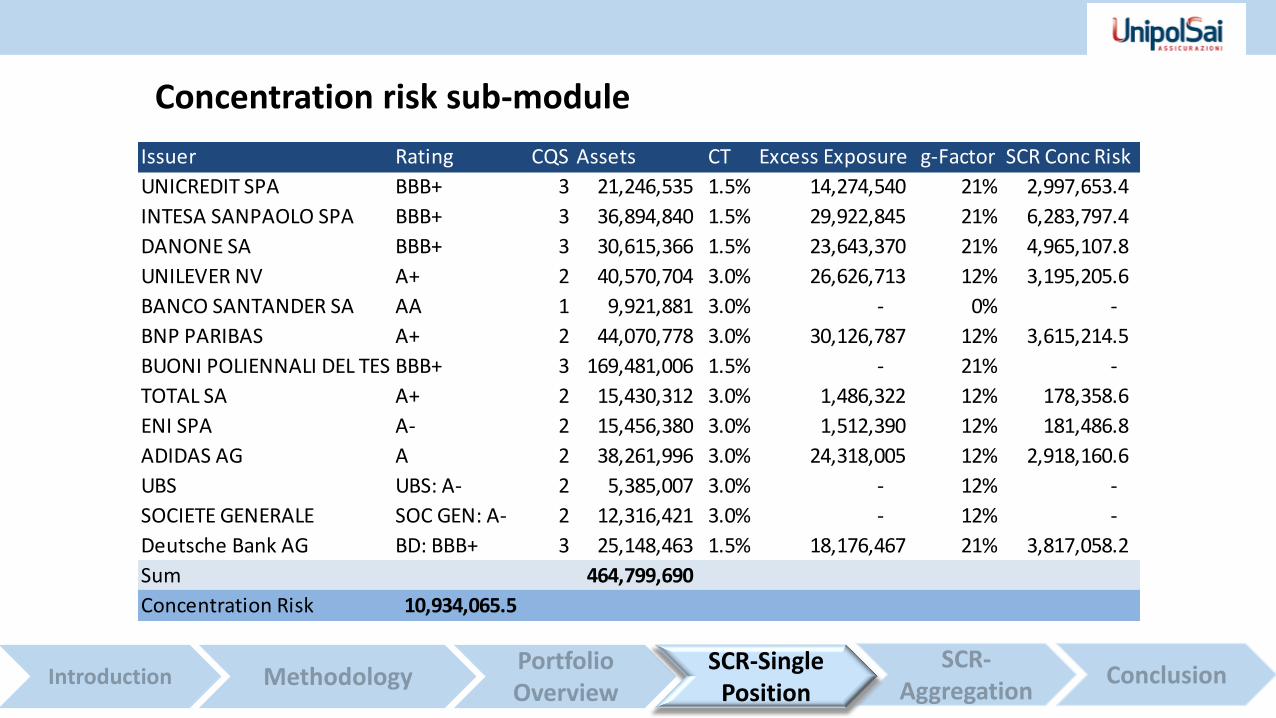

Issuer Rating CQS Assets CT Excess Exposure g-Factor SCR Conc Risk

UNICREDIT SPA BBB+ 3 21,246,535 1.5% 14,274,540 21% 2,997,653.4

INTESA SANPAOLO SPA BBB+ 3 36,894,840 1.5% 29,922,845 21% 6,283,797.4

DANONE SA BBB+ 3 30,615,366 1.5% 23,643,370 21% 4,965,107.8

UNILEVER NV A+ 2 40,570,704 3.0% 26,626,713 12% 3,195,205.6

BANCO SANTANDER SA AA 1 9,921,881 3.0% - 0% -

BNP PARIBAS A+ 2 44,070,778 3.0% 30,126,787 12% 3,615,214.5

BUONI POLIENNALI DEL TES BBB+ 3 169,481,006 1.5% - 21% -

TOTAL SA A+ 2 15,430,312 3.0% 1,486,322 12% 178,358.6

ENI SPA A- 2 15,456,380 3.0% 1,512,390 12% 181,486.8

ADIDAS AG A 2 38,261,996 3.0% 24,318,005 12% 2,918,160.6

UBS UBS: A- 2 5,385,007 3.0% - 12% -

SOCIETE GENERALE SOC GEN: A- 2 12,316,421 3.0% - 12% -

Deutsche Bank AG BD: BBB+ 3 25,148,463 1.5% 18,176,467 21% 3,817,058.2

Sum 464,799,690

Concentration Risk 10,934,065.5

Concentration risk sub-module

SCR-Single Position

SCR -Aggregation

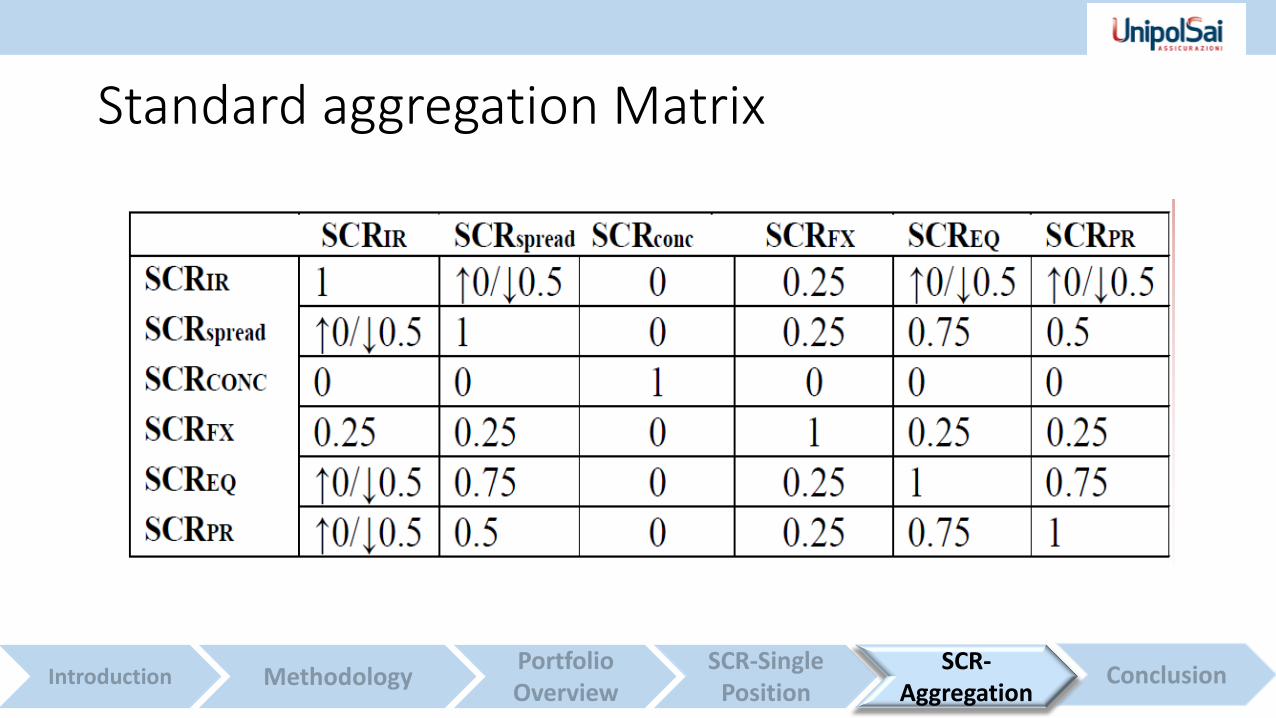

Standard aggregation Matrix

SCR-Aggregation

Market Risk 48,596,716

Interest rate risk 1,533,823

Equity risk 22,917,908

Property risk -

Spread risk 26,785,536

Currency risk -

Concentration risk 10,934,066

Sum 62,171,333

Diversification absolut 13,574,616

Diversification in % 21.83%

Market risk module:

SCR- Aggregation

• Assets and liabilities are well matched

Low interest rate risk

• Equity risk mainly driven by Adidas convertible Equity risk

Conclusion

THANK YOU!

Methodology

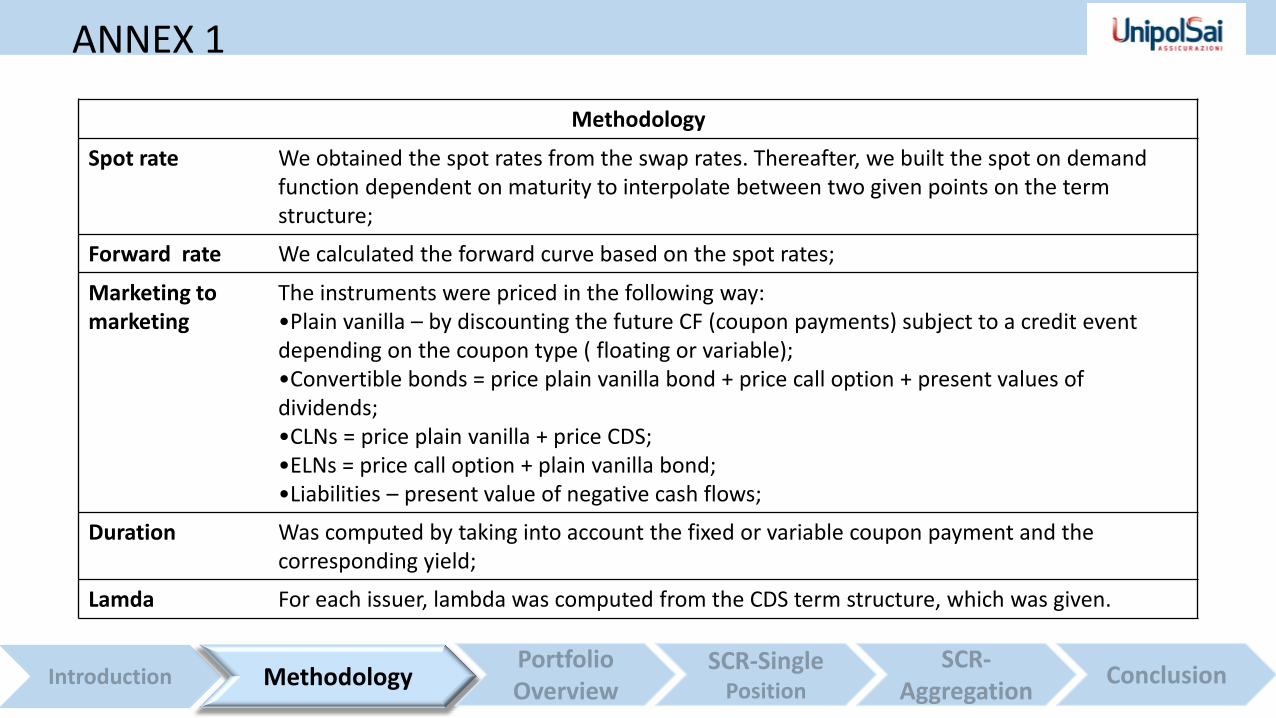

Spot rate We obtained the spot rates from the swap rates. Thereafter, we built the spot on demand function dependent on maturity to interpolate between two given points on the term structure;

Forward rate We calculated the forward curve based on the spot rates;

Marketing to marketing

The instruments were priced in the following way: •Plain vanilla – by discounting the future CF (coupon payments) subject to a credit event depending on the coupon type ( floating or variable); •Convertible bonds = price plain vanilla bond + price call option + present values of dividends; •CLNs = price plain vanilla + price CDS; •ELNs = price call option + plain vanilla bond; •Liabilities – present value of negative cash flows;

Duration Was computed by taking into account the fixed or variable coupon payment and the corresponding yield;

Lamda For each issuer, lambda was computed from the CDS term structure, which was given.

Methodology

ANNEX 1

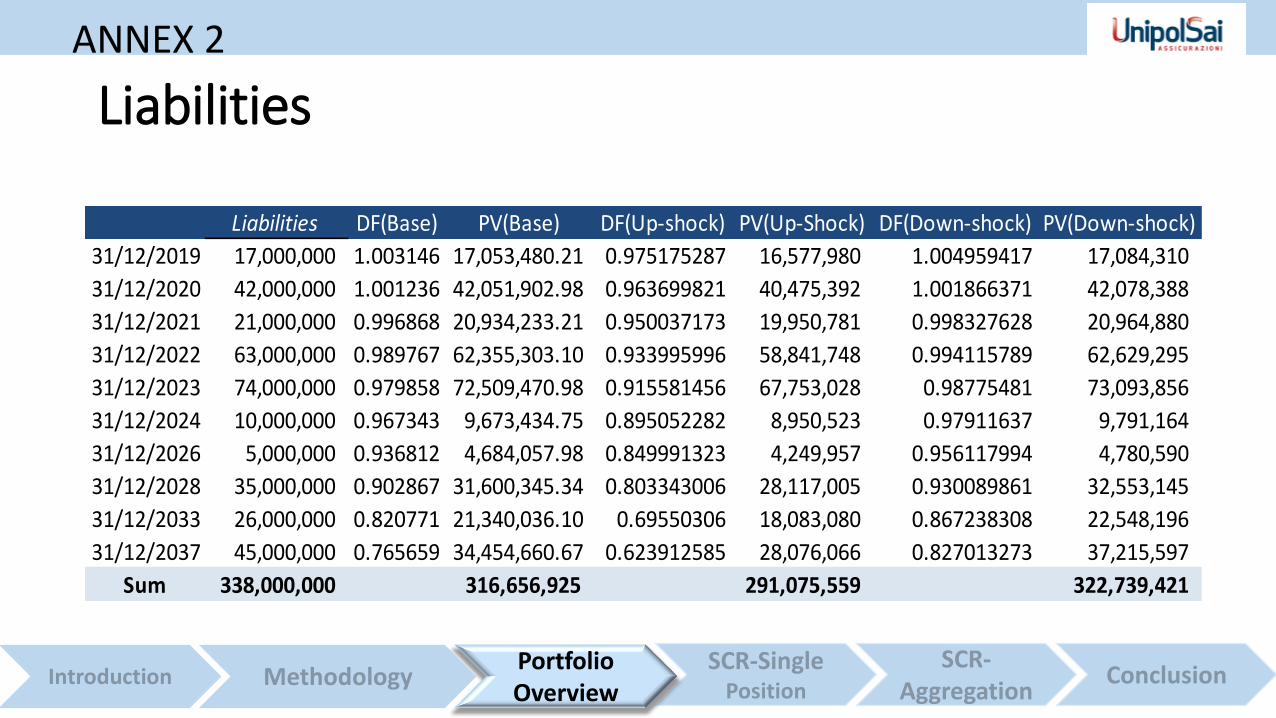

Liabilities

Liabilities DF(Base) PV(Base) DF(Up-shock) PV(Up-Shock) DF(Down-shock) PV(Down-shock)

31/12/2019 17,000,000 1.003146 17,053,480.21 0.975175287 16,577,980 1.004959417 17,084,310

31/12/2020 42,000,000 1.001236 42,051,902.98 0.963699821 40,475,392 1.001866371 42,078,388

31/12/2021 21,000,000 0.996868 20,934,233.21 0.950037173 19,950,781 0.998327628 20,964,880

31/12/2022 63,000,000 0.989767 62,355,303.10 0.933995996 58,841,748 0.994115789 62,629,295

31/12/2023 74,000,000 0.979858 72,509,470.98 0.915581456 67,753,028 0.98775481 73,093,856

31/12/2024 10,000,000 0.967343 9,673,434.75 0.895052282 8,950,523 0.97911637 9,791,164

31/12/2026 5,000,000 0.936812 4,684,057.98 0.849991323 4,249,957 0.956117994 4,780,590

31/12/2028 35,000,000 0.902867 31,600,345.34 0.803343006 28,117,005 0.930089861 32,553,145

31/12/2033 26,000,000 0.820771 21,340,036.10 0.69550306 18,083,080 0.867238308 22,548,196

31/12/2037 45,000,000 0.765659 34,454,660.67 0.623912585 28,076,066 0.827013273 37,215,597

Sum 338,000,000 316,656,925 291,075,559 322,739,421

ANNEX 2

Portfolio Overview

Scenario

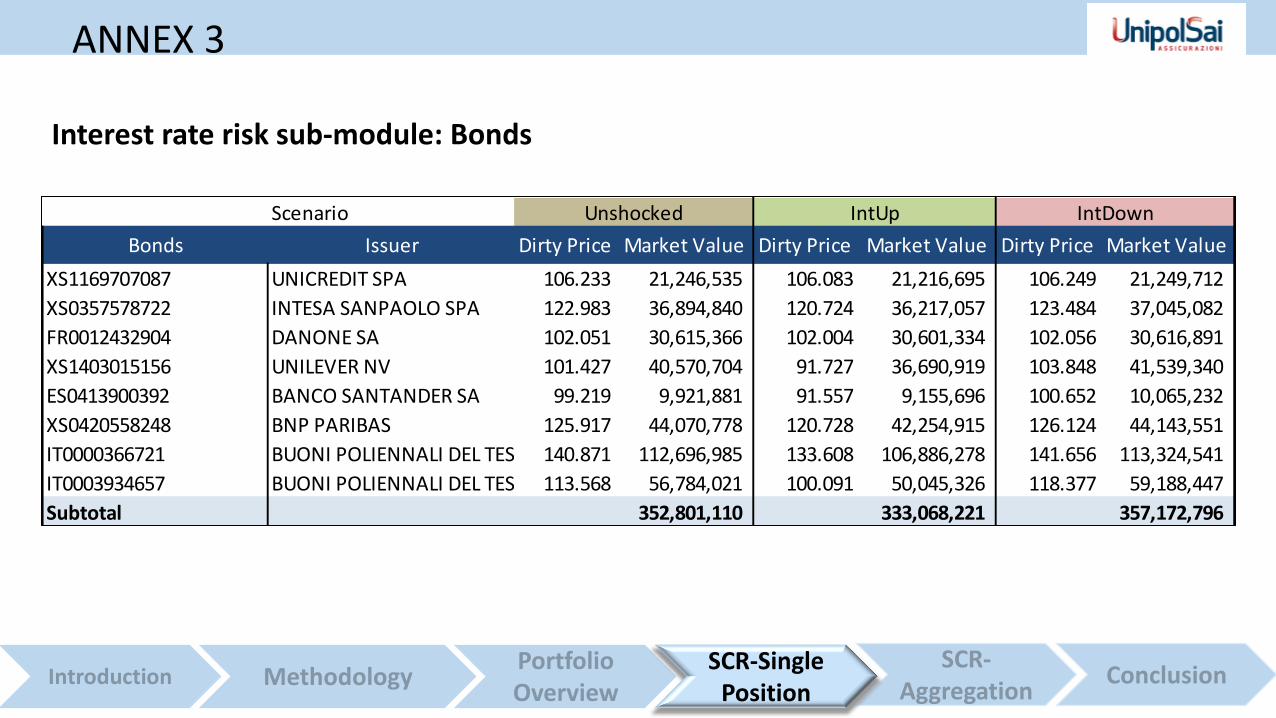

Bonds Issuer Dirty Price Market Value Dirty Price Market Value Dirty Price Market Value

XS1169707087 UNICREDIT SPA 106.233 21,246,535 106.083 21,216,695 106.249 21,249,712

XS0357578722 INTESA SANPAOLO SPA 122.983 36,894,840 120.724 36,217,057 123.484 37,045,082

FR0012432904 DANONE SA 102.051 30,615,366 102.004 30,601,334 102.056 30,616,891

XS1403015156 UNILEVER NV 101.427 40,570,704 91.727 36,690,919 103.848 41,539,340

ES0413900392 BANCO SANTANDER SA 99.219 9,921,881 91.557 9,155,696 100.652 10,065,232

XS0420558248 BNP PARIBAS 125.917 44,070,778 120.728 42,254,915 126.124 44,143,551

IT0000366721 BUONI POLIENNALI DEL TES 140.871 112,696,985 133.608 106,886,278 141.656 113,324,541

IT0003934657 BUONI POLIENNALI DEL TES 113.568 56,784,021 100.091 50,045,326 118.377 59,188,447

Subtotal 352,801,110 333,068,221 357,172,796

Convertibles

Unshocked IntUp IntDown

Interest rate risk sub-module: Bonds

SCR-Single Position

ANNEX 3

Scenario

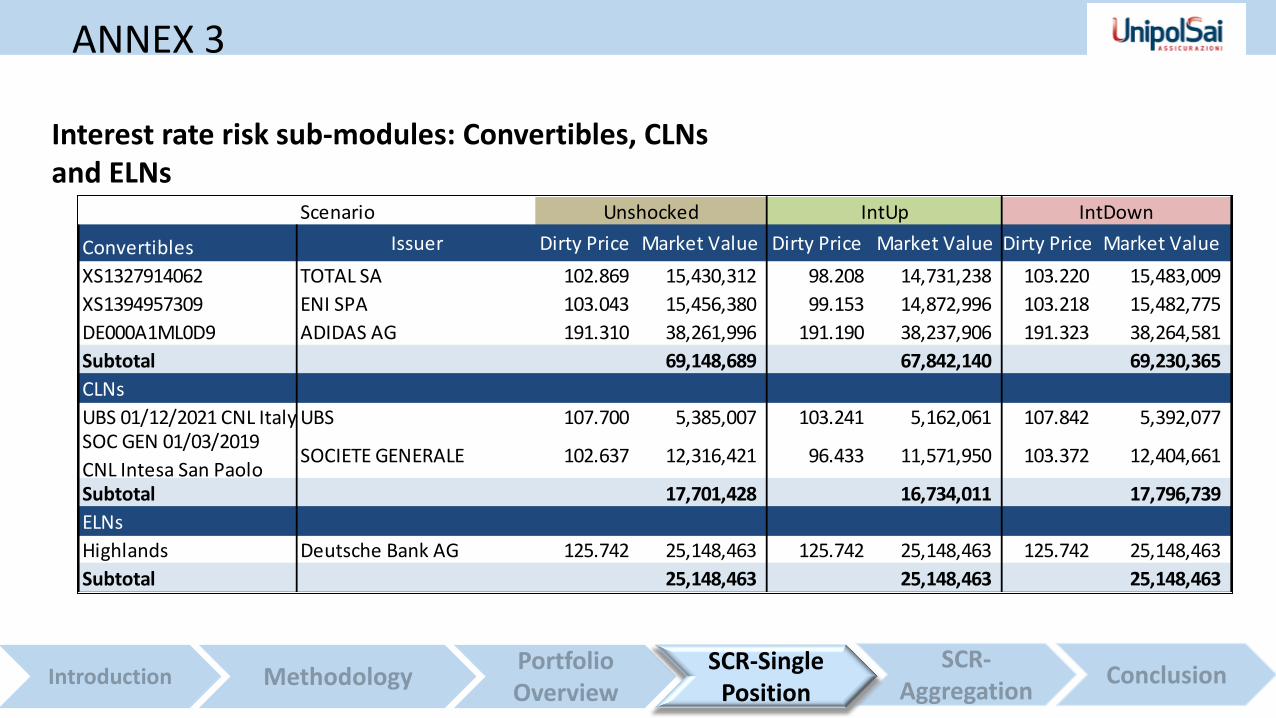

Convertibles Issuer Dirty Price Market Value Dirty Price Market Value Dirty Price Market Value

XS1327914062 TOTAL SA 102.869 15,430,312 98.208 14,731,238 103.220 15,483,009

XS1394957309 ENI SPA 103.043 15,456,380 99.153 14,872,996 103.218 15,482,775

DE000A1ML0D9 ADIDAS AG 191.310 38,261,996 191.190 38,237,906 191.323 38,264,581

Subtotal 69,148,689 67,842,140 69,230,365

CLNs

UBS 01/12/2021 CNL Italy UBS 107.700 5,385,007 103.241 5,162,061 107.842 5,392,077 SOC GEN 01/03/2019

CNL Intesa San PaoloSOCIETE GENERALE 102.637 12,316,421 96.433 11,571,950 103.372 12,404,661

Subtotal 17,701,428 16,734,011 17,796,739

ELNs

Highlands Deutsche Bank AG 125.742 25,148,463 125.742 25,148,463 125.742 25,148,463

Subtotal 25,148,463 25,148,463 25,148,463

Unshocked IntUp IntDown

Interest rate risk sub-modules: Convertibles, CLNs and ELNs

SCR-Single Position

ANNEX 3

Interest rate risk 1,533,823Applicable interest rate shock downward

Assets

Market value before shock 464,799,690

Market value after interest up shock 442,792,835

Market value after interest down shock 469,348,362

SCR due to interest up shock 22,006,855

SCR due to interest down shock -4,548,672

Liabilities

Market value before shock 316,656,925

Market value after interest up shock 291,075,559

Market value after interest down shock 322,739,421

SCR due to interest up shock -25,581,366

SCR due to interest down shock 6,082,495

Interest rate risk

SCR-Aggregation

ANNEX 3