54

February 2014

Feb

rua

ry 2

01

4

2

Dis

cla

imer

Sta

tem

en

ts

ma

de

in

th

is

Pre

sen

tati

on

d

esc

rib

ing

th

e Company’s

o

bje

ctiv

es,

pro

ject

ion

s, e

stim

ate

, e

xpe

cta

tio

ns

ma

y b

e “Forw

ard

-lo

ok

ing

statements”

wit

hin

the

me

an

ing

of

ap

pli

cab

le s

ecu

riti

es

law

s &

re

gu

lati

on

s. A

ctu

al

resu

lts

cou

ld d

iffe

r

fro

m t

ho

se e

xpre

sse

d o

r im

pli

ed

. Im

po

rta

nt

fact

ors

th

at

cou

ld m

ak

e a

dif

fere

nce

to

the

Company’s

o

pe

rati

on

s in

clu

de

e

con

om

ic

con

dit

ion

s a

ffe

ctin

g

de

ma

nd

sup

ply

an

d p

rice

co

nd

itio

ns

in t

he

do

me

stic

& o

ve

rse

as

ma

rke

ts i

n w

hic

h t

he

com

pa

ny o

pe

rate

s, ch

an

ge

s in

th

e g

ove

rnm

en

t re

gu

lati

on

s, ta

x la

ws

& o

the

r

sta

tute

s &

oth

er

inci

de

nta

l fa

cto

rs.

Dis

cla

ime

r

3

§In

fla

tio

n

imp

act

ing

D

iscr

eti

on

ary

Sp

en

din

g

§G

DP

Gro

wth

Sli

pp

ing

§H

igh

In

tere

st R

ate

Re

gim

e

Ma

cro

Th

em

es

§D

ecl

ine

of

ove

r 2

0%

in

th

e f

ine

din

ing

ma

rke

t in

m

ajo

r ci

tie

s in

In

dia

-

AS

SO

CH

AM

§Lo

ng

Te

rm P

ote

nti

al

rem

ain

s in

tact

Ind

ust

ry T

he

me

s

§S

tea

dy

Fo

otf

all

s

§9

0 r

est

au

ran

ts a

nd

14

co

nfe

ctio

na

rie

s a

s o

n 3

1st

De

cem

be

r, 2

01

3

§M

ain

lan

d C

hin

a r

em

ain

s th

e f

lag

ship

bra

nd

co

ntr

ibu

tin

g t

o 5

8%

of

reve

nu

es

for

9M

FY

14

§

Pri

ce h

ike

im

ple

me

nte

d i

n e

nd

No

vem

be

r 2

01

3

§E

xpa

nsi

on

pla

ns

on

tra

ck

§D

esp

ite

ma

cro

he

ad

win

ds,

op

en

ed

1

4 r

est

au

ran

ts i

n 9

M F

Y1

4 (

FY

14

ta

rge

t -

15

re

sta

ura

nts

) §

Exp

an

din

g G

lob

al

foo

tpri

nt

th

rou

gh

a J

oin

t V

en

ture

in

Do

ha

, Q

ata

r

Ho

w w

e f

are

d ?

FY

20

13

-14

Th

us

far

4

Bra

nd

Le

ad

ers

hip

Op

era

tio

nal

Levera

ge

Lo

yal

Cu

sto

mer

Base

Str

on

g

Man

ag

em

en

t T

eam

Esta

bli

sh

ed

Pre

sen

ce a

t h

igh

er

en

d o

f V

alu

e C

hain

Ou

r C

om

pe

titi

ve

Str

en

gth

s

Co

re B

ran

ds

Pa

rtic

ula

rs

•M

en

u

fea

ture

s a

uth

en

tic

Ch

ine

se

cuis

ine

e

mb

raci

ng

th

e

pri

nci

ple

o

f “h

arm

on

y

in

con

tra

st,”

wh

ich

ste

ms

fro

m t

he

Ch

ine

se c

on

cep

t o

f y

in a

nd

ya

ng

•E

rstw

hil

e O

nly

Fis

h,

wa

s re

bra

nd

ed

as

Oh

! C

alc

utt

a

•M

en

u f

ea

ture

s d

ish

es

fro

m K

olk

ata

, cr

ea

ted

th

rou

gh

re

sea

rch

in

lib

rari

es

an

d o

ld B

riti

sh

colo

nia

l cl

ub

s

•A

mb

ien

ce:

rese

mb

les

a B

riti

sh c

olo

nia

l cl

ub

in

Ko

lka

ta

•A

ne

w c

on

cep

t o

f d

inin

g a

nd

a r

ece

nt

ad

dit

ion

to

th

e g

rou

p’s

co

re b

ran

d p

ort

foli

o,

insp

ire

d b

y c

ha

ng

ing

ta

ste

-bu

ds

•T

he

me

nu

fe

atu

res

a m

ela

ng

e o

f fr

esh

, g

rill

ed

fla

vou

rs f

rom

all

aro

un

d t

he

glo

be

Oth

er

Bra

nd

s P

art

icu

lars

•

A n

ew

co

nce

pt

of

pro

vid

ing

fin

e d

inin

g e

xpe

rie

nce

th

rou

gh

Ou

tdo

or

Ca

teri

ng

Se

rvic

e

•C

ust

om

ize

s G

ou

rme

t cu

isin

e f

rom

le

ad

ing

bra

nd

s in

th

e c

ou

ntr

y u

nd

er

on

e r

oo

f a

t th

e

cust

om

ers

pre

ferr

ed

lo

cati

on

•S

we

et

Co

nfe

ctio

na

ry

•S

erv

es

Mo

de

rn C

hin

ese

cu

isin

e i

de

al

for

gu

est

s o

n-t

he

-go

•A

n a

ll-d

ay

ca

sua

l d

inin

g f

orm

at

serv

ing

co

nti

ne

nta

l d

ish

es

wit

h M

ed

ite

rra

ne

an

,

Mo

rocc

an

, E

ast

Asi

an

an

d I

tali

an

fla

vou

rs.

Ou

r B

ran

d P

lay

bo

ok

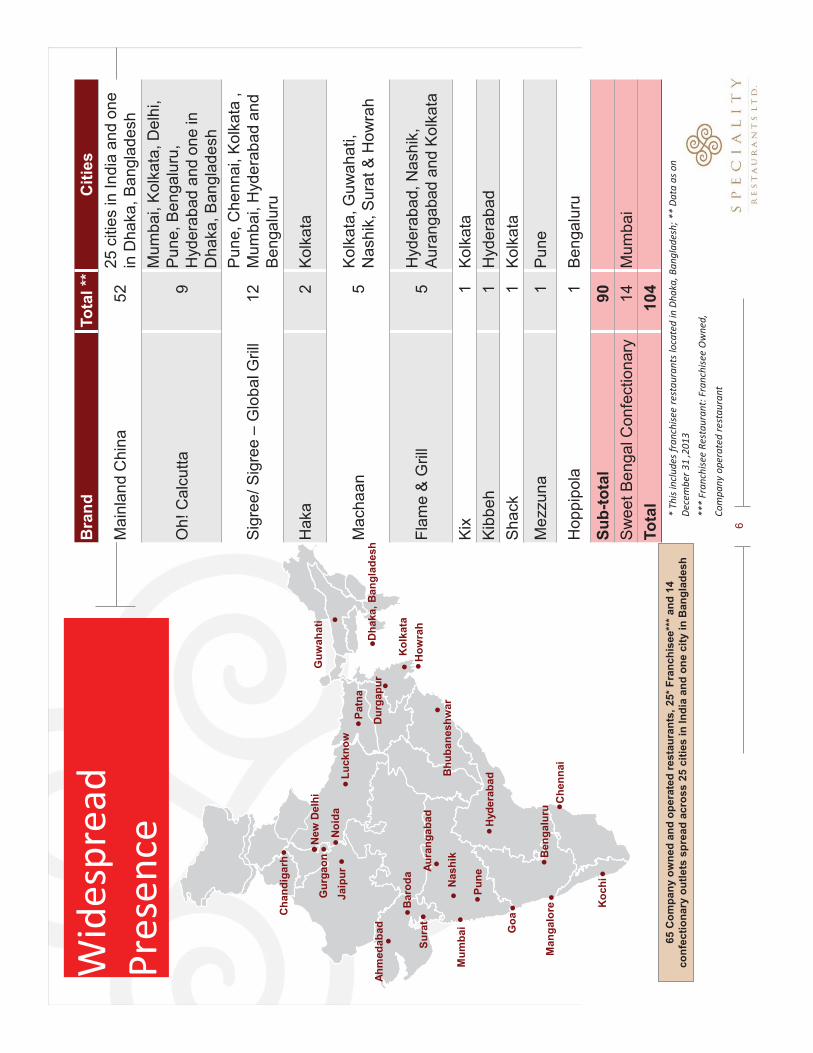

6

Bra

nd

To

tal

**

Cit

ies

Ma

inla

nd C

hin

a

52

2

5 c

itie

s in

In

dia

an

d o

ne

in D

ha

ka

, B

an

gla

desh

Oh

! C

alc

utt

a

9

Mu

mb

ai, K

olk

ata

, D

elh

i,

Pu

ne

, B

en

ga

luru

,

Hyd

era

ba

d a

nd o

ne

in

Dha

ka

, B

an

gla

de

sh

Sig

ree

/ S

igre

e –

Glo

ba

l G

rill

12

Pu

ne

, C

he

nnai, K

olk

ata

,

Mu

mb

ai, H

yd

era

ba

d a

nd

Be

nga

luru

Haka

2

K

olk

ata

Ma

ch

aa

n

5

Ko

lkata

, G

uw

ah

ati,

Nash

ik, S

ura

t &

Ho

wra

h

Fla

me

& G

rill

5

Hyd

era

ba

d, N

ash

ik,

Au

ran

ga

bad

an

d K

olk

ata

Kix

1

K

olk

ata

Kib

be

h

1

Hyd

era

ba

d

Sh

ack

1

Ko

lkata

Me

zzu

na

1

P

un

e

Hop

pip

ola

1

B

en

ga

luru

Su

b-t

ota

l 9

0

Sw

ee

t B

en

ga

l C

on

fectio

nary

1

4

Mu

mb

ai

To

tal

10

4

Ben

ga

luru

Ch

en

nai

Hyd

era

ba

d

Pu

ne

Nash

ik

Mu

mb

ai

Ah

med

ab

ad

Baro

da

Su

rat

Ch

an

dig

arh

New

Delh

i

Lu

ckn

ow

Gu

wah

ati

Dh

aka,

Ban

gla

de

sh

Ko

lkata

Au

ran

ga

bad

Man

ga

lore

Ko

ch

i

Du

rga

pu

r

Patn

a

65 C

om

pa

ny o

wn

ed

an

d o

pe

rate

d r

esta

ura

nts

, 25*

Fra

nc

his

ee**

* an

d 1

4

co

nfe

cti

on

ary

ou

tle

ts s

pre

ad

acro

ss 2

5 c

itie

s i

n In

dia

an

d o

ne

cit

y i

n B

an

gla

de

sh

*

Th

is in

clu

de

s fr

an

chis

ee

re

sta

ura

nts

lo

cate

d i

n D

ha

ka

, B

an

gla

de

sh;

**

Da

ta a

s o

n

De

cem

be

r 3

1 ,2

01

3

**

* F

ran

chis

ee

Re

sta

ura

nt:

Fra

nch

ise

e O

wn

ed

,

Co

mp

an

y o

pe

rate

d r

est

au

ran

t

Go

a

No

ida

Ho

wra

h

Wid

esp

rea

d

Pre

sen

ce

Bh

ub

an

esh

war

Jaip

ur

Gu

rgao

n

7

58

%

10

%

14

%

4%

2%

3

%

5%

4

%

Ma

inla

nd

Ch

ina

Oh

Ca

lcu

tta

Sig

ree

/Glo

ba

l G

rill

Fla

me

& G

rill

Ma

cha

an

Ha

ka

Sw

ee

t B

en

ga

l

Oth

ers

Bra

nd

wis

e c

on

trib

uti

on

to r

eve

nu

es

for

9M

FY

14

8

Str

ate

gic

Dir

ect

ion

20

13

-14

•M

ezz

un

a

•S

igre

e -

Glo

ba

l G

rill

2

. B

RA

ND

AD

DIT

ION

S

•P

rese

nce

acr

oss

Va

lue

Ch

ain

•M

ob

i-Fe

ast

•H

op

pip

ola

3.

FO

CU

S O

N

SW

EA

TIN

G O

F A

SS

ET

S

•E

nh

an

ce E

mp

loye

e S

kil

ls

•B

ack

en

d C

ost

Co

ntr

ols

•Im

ple

me

nta

tio

n o

f P

rice

Hik

e

4.

EN

HA

NC

E

OP

ER

AT

ION

AL

EF

FIC

IEN

CIE

S

•E

xpa

nsi

on

in

Exi

stin

g C

itie

s w

ith

in I

nd

ia

•In

tern

ati

on

al F

ora

ys

5.

EN

LAR

GE

OU

R

PR

ES

EN

CE

•Fo

cus

on

Fla

gsh

ip B

ran

ds

•In

no

vate

ou

r O

ffe

rin

gs

wit

ho

ut

dil

uti

ng

or

com

pro

mis

ing

on

Qu

ali

ty

1.

LEV

ER

AG

E O

UR

ST

RE

NG

TH

S

Str

ate

gic

Dir

ect

ion

FY

13

-14

1.L

EV

ER

AG

E O

UR

ST

RE

NG

TH

S

Main

land C

hin

a a

nd O

h! C

alc

utta

9

11

Lev

era

ge

th

e e

qu

ity

of

Ma

inla

nd

Ch

ina

•Le

vera

ge

th

e b

ran

d e

qu

ity

en

joye

d b

y M

ain

lan

d C

hin

a b

ran

d b

y e

xpa

nd

ing

in

ne

w lo

cati

on

s in

Me

tro

an

d T

ier

1 c

itie

s

•S

ele

ctiv

ely

un

de

rta

ke e

xpa

nsi

on

pla

ns

in l

ine

wit

h M

acr

oe

con

om

ic

De

velo

pm

en

ts

Ex

pa

nsi

on

Pla

ns

•P

lan

to

exp

an

d n

ew

re

sta

ura

nt

form

ats

su

ch a

s C

om

bo

s a

nd

Mu

lti

bra

nd

s

•In

clu

de

sn

ack

me

nu

an

d k

ee

p r

est

au

ran

ts o

pe

n t

hro

ug

h t

he

da

y in

Ma

lls

–

Incr

ea

se C

ove

r Tu

rno

ver.

•“M

ain

lan

d C

hin

a –

Asi

a K

itch

en

” to

op

en

so

on

in

Ob

ero

i M

all

, G

ore

ga

on

,

Mu

mb

ai a

s a

ll d

ay

fo

rma

t

12

Fo

cus

on

CO

CO

Mo

de

l fo

r E

xp

an

sio

n

•C

ost

Cu

rve

– 1

20

da

ys t

o l

au

nch

an

d 6

- 9

mo

nth

s th

ere

aft

er

to b

rea

keve

n

•Fo

cus

on

CO

CO

mo

de

l fo

r e

xpa

nsi

on

co

mb

ine

d w

ith

FO

CO

mo

de

l

op

po

rtu

nis

tica

lly

Inn

ov

ati

ve

Off

eri

ng

s

•S

ma

lle

r P

ort

ion

in

ad

dit

ion

to

exi

stin

g R

eg

ula

r P

ort

ion

Me

nu

ba

sed

on

Re

sea

rch

co

nd

uct

ed

, im

ple

me

nte

d i

n r

est

au

ran

ts a

cro

ss I

nd

ia

•S

ave

s C

ost

s a

nd

Ge

ne

rate

s h

igh

er

Re

ven

ue

s

•T

ie u

p w

ith

IC

ICI

Ba

nk

Ltd

. to

cre

ate

sp

eci

al

off

er

for

ICIC

I C

ard

Ho

lde

rs

17

•R

ecr

ea

tin

g t

he

ma

gic

of

the

fla

vou

rs o

f a

gre

at

city

wh

ere

no

sta

lgia

an

d t

ast

e

me

lts

tog

eth

er

on

th

e p

ala

te

•T

he

bra

nd

ca

ters

to

eve

r g

row

ing

de

ma

nd

of

the

dis

cern

ing

In

dia

n G

ue

st t

o

ven

ture

ou

t b

eyo

nd

th

e T

an

do

ori

Ch

icke

n a

nd

Ma

kh

an

i D

aa

l.

2. B

RA

ND

AD

DIT

ION

S

Mezzuna a

nd S

igre

e -

Glo

bal G

rill

23

25

•A

ll d

ay

ba

r a

nd

re

sta

ura

nt,

se

rvin

g I

nte

rna

tio

na

l cu

isin

e,

wa

s la

un

che

d i

n A

pri

l

20

13

.

•T

he

tr

en

d o

f th

is

you

ng

T

G

(19

–

2

6 ye

ars

) w

ith

h

igh

d

isp

osa

ble

in

com

e

is

“ch

illi

ng

– s

pe

nd

ing

tim

e i

n a

n i

nfo

rma

l v

ibra

nt

sett

ing

” -

dri

nk

ing

ou

t w

ith

frie

nd

s a

nd

ha

vin

g f

ing

er

foo

d.

•C

on

sult

an

ts/

Ch

efs

fro

m E

uro

pe

an

d r

ecr

uit

me

nts

fro

m B

est

Ho

tels

/Re

sta

ura

nts

in I

nd

ia

26

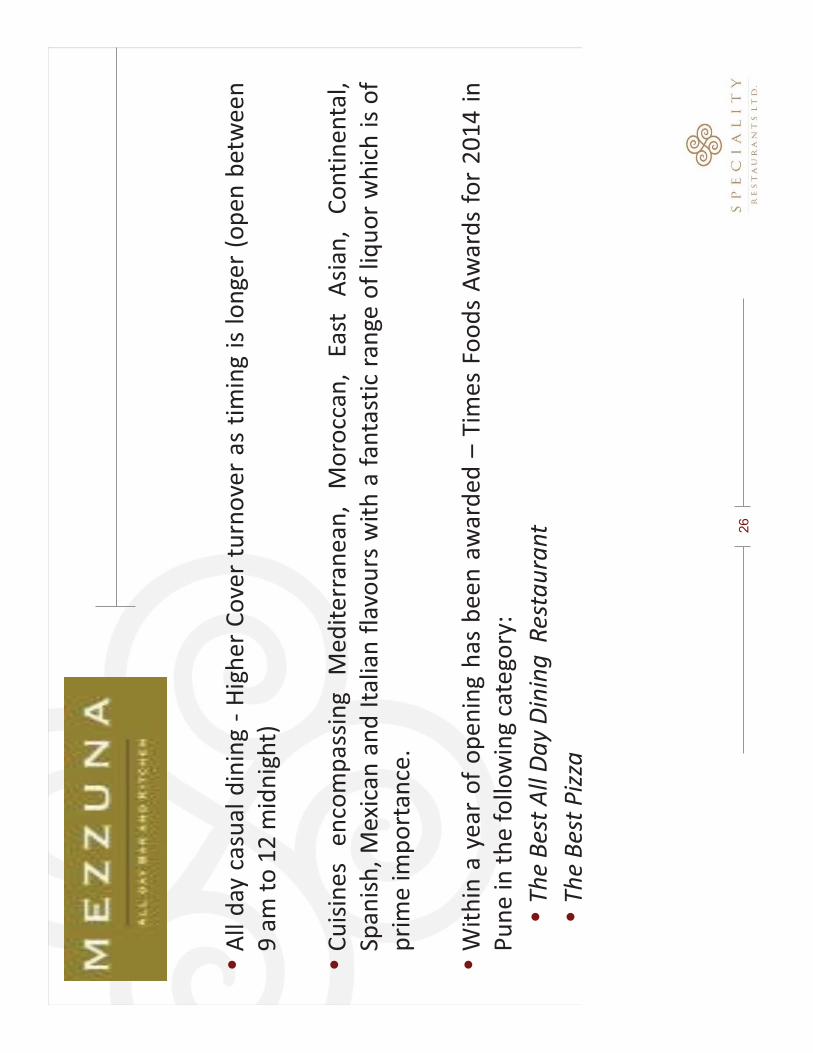

•A

ll d

ay c

asu

al

din

ing

- H

igh

er

Co

ver

turn

ove

r a

s ti

min

g i

s lo

ng

er

(op

en

be

twe

en

9 a

m t

o 1

2 m

idn

igh

t)

•C

uis

ine

s e

nco

mp

ass

ing

M

ed

ite

rra

ne

an

, M

oro

cca

n,

Ea

st

Asi

an

, C

on

tin

en

tal,

Sp

an

ish

, M

exi

can

an

d I

tali

an

fla

vou

rs w

ith

a f

an

tast

ic r

an

ge

of

liq

uo

r w

hic

h i

s o

f

pri

me

im

po

rta

nce

.

•W

ith

in a

ye

ar

of

op

en

ing

ha

s b

ee

n a

wa

rde

d –

Tim

es

Fo

od

s A

wa

rds

for

20

14

in

Pu

ne

in

th

e f

oll

ow

ing

ca

teg

ory

:

•T

he

Be

st A

ll D

ay D

inin

g R

est

au

ran

t

•T

he

Be

st P

izza

32

•A

ne

w c

on

cep

t o

f d

inin

g a

nd

la

test

ad

dit

ion

to

th

e g

rou

p p

ort

foli

o s

erv

ing

a

me

lan

ge

o

f fr

esh

, g

rill

ed

fl

avo

urs

fr

om

a

ll

aro

un

d

the

g

lob

e

like

M

ed

ite

rra

ne

an

, O

rie

nta

l, S

pa

nis

h,

Me

xica

n a

nd

In

dia

n c

uis

ine

.

•Li

ve g

rill

s o

n e

ach

ta

ble

- U

nli

mit

ed

sta

rte

rs t

ha

t si

zzle

an

d g

rill

on

ea

ch t

ab

le.

•

Dis

pla

y k

itch

en

an

d i

nte

ract

ive

co

ok

ing

, e

nh

an

ced

by t

he

th

rill

ing

an

d s

kil

lfu

l d

isp

lay

by

ma

ste

r ch

efs

. D

ram

ati

c a

mb

ien

ce o

f fr

esh

in

gre

die

nts

an

d e

xcit

ing

cu

lin

ary

sty

les.

•

Pla

ns

to e

xpa

nd

th

e n

um

be

r o

f o

utl

ets

giv

en

th

e e

nco

ura

gin

g r

esp

on

se

3.

FO

CU

S O

N S

WE

AT

ING

OF

AS

SE

TS

Mob

ife

ast,

Ho

ppip

ola

and

QS

Rs

37

38

• B

uil

d p

rese

nce

acr

oss

th

e v

alu

e c

ha

in

•C

ate

r u

niq

ue

fo

od

off

eri

ng

fro

m t

he

kit

che

ns

of

the

le

ad

ing

bra

nd

s in

th

e

cou

ntr

y u

nd

er

on

e r

oo

f

•O

pe

rate

s th

rou

gh

th

e C

en

tra

l Fo

od

Pro

cess

ing

Un

it a

t S

an

kra

il n

ea

r H

ow

rah

•T

he

bu

sin

ess

mo

de

l in

volv

es

no

ma

jor

fixe

d c

ost

s w

hil

e d

ep

loys

id

le r

eso

urc

es

resu

ltin

g i

n o

nly

incr

em

en

tal

vari

ab

le c

ost

s

Mo

bif

ea

st

39

•A

ll d

ay B

ar

off

eri

ng

Co

nte

mp

ora

ry f

oo

d i

ncl

ud

ing

re

gu

lar

nib

ble

s a

nd

fin

ge

r fo

od

•N

o r

en

tal

cost

s a

s it

op

era

tes

fro

m v

aca

nt

terr

ace

s a

t e

xist

ing

Co

mp

an

y’s

lo

cati

on

s

•M

ark

eti

ng

th

rou

gh

th

e S

oci

al

Me

dia

ro

ute

ta

rge

tin

g a

ge

gro

up

of

18

-24

•In

itia

tive

is

focu

sed

on

ma

rgin

exp

an

sio

n

Ho

pp

ipo

la

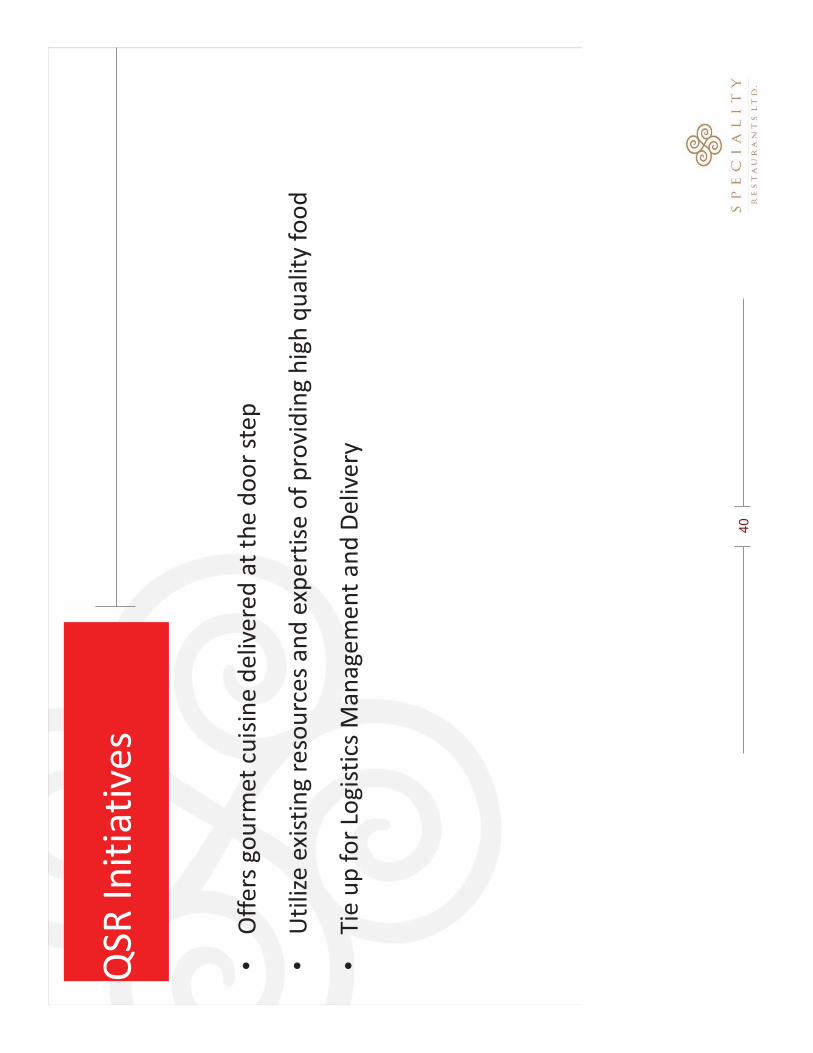

40

•O

ffe

rs g

ou

rme

t cu

isin

e d

eli

vere

d a

t th

e d

oo

r st

ep

•U

tili

ze e

xist

ing

re

sou

rce

s a

nd

exp

ert

ise

of

pro

vid

ing

hig

h q

ua

lity

fo

od

•T

ie u

p f

or

Log

isti

cs M

an

ag

em

en

t a

nd

De

live

ry

QS

R I

nit

iati

ve

s

4. O

PE

RA

TIO

NA

L E

FF

ICIE

NC

IES

41

42

•Tr

imm

ing

wo

rk f

orc

e a

nd

tra

inin

g e

mp

loye

es

to b

e m

ult

ifa

cete

d t

o e

nh

an

ce

pro

du

ctiv

ity

•Sy

ne

rgie

s o

n t

he

flo

or

to s

ave

tim

e

•R

e-n

eg

oti

ati

on

of

Re

nta

ls t

o e

nsu

re p

rofi

tab

ilit

y g

ive

n t

he

str

on

g b

ran

d e

qu

ity

en

joye

d b

y t

he

Co

mp

an

y

Op

era

tio

na

l E

ffic

ien

cie

s

5. E

NL

AR

GE

OU

R P

RE

SE

NC

E

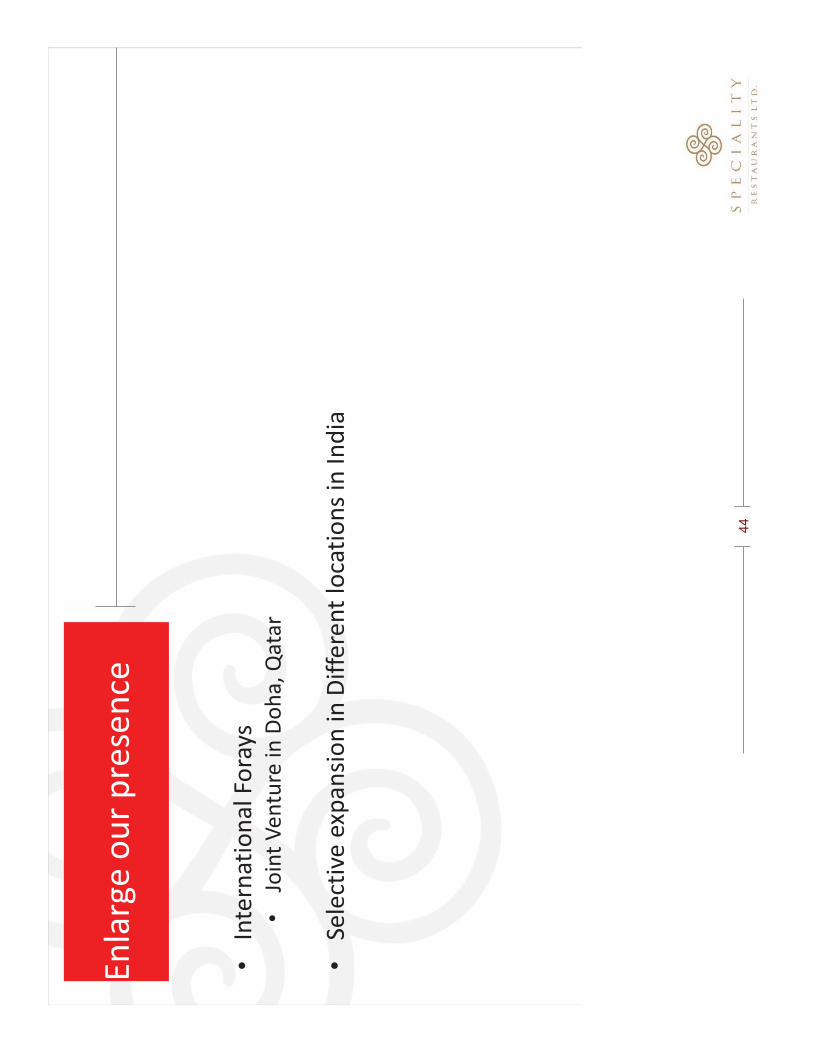

43

44

•In

tern

ati

on

al

Fo

rays

•

Join

t V

en

ture

in

Do

ha

, Q

ata

r

•S

ele

ctiv

e e

xpa

nsi

on

in

Dif

fere

nt

loca

tio

ns

in I

nd

ia

En

larg

e o

ur

pre

sen

ce

45

Ma

rket

se

gm

en

ts a

nd

gro

wth

pro

jec

tio

n –

Org

an

ise

d S

eg

me

nt

2010

2015*

Org

an

ize

d

16

.0%

Un

org

an

ize

d

84

.0%

Un

org

an

ize

d

55

.0%

Org

an

ize

d

45

.0%

To

tal

Ind

ustr

y:

Rs 4

,30,0

00 m

n (

Rs 4

30 b

n.)

To

tal

Ind

ustr

y:

Rs 6

,25,0

00 m

n (

Rs 6

25 b

n.)

C

AG

R:

8%

Org

an

ized

Seg

men

t: R

s 6

9,0

00 m

n

(Rs 7

0 b

n.)

Org

an

ized

Seg

men

t: ~

Rs 2

,80,0

00 m

n.

(Rs 2

80 b

n.)

CA

GR

: 3

0-3

2%

Org

an

ized

Seg

men

t: o

ver

3,0

00 o

utl

ets

So

urc

e : T

ech

no

pa

k R

ep

ort

20

09

; N

RA

I R

ep

ort

20

10

Ind

ust

ry p

ote

nti

al

46

nO

ver

65%

of In

dia

’s p

opula

tion is b

elo

w 3

5

years

of age, and the a

ge g

roup b

etw

een 2

1

and 4

0 y

ears

constitu

tes the m

ajo

rity

am

ong

those w

ho e

at out re

gula

rly

nIn

cre

asin

g p

opula

tion o

f th

e m

iddle

-cla

ss a

nd

incre

asin

g p

roport

ion o

f th

e p

opula

tion liv

ing in

urb

an c

entr

es

Ch

an

gin

g D

em

og

rap

hic

Pro

file

Gro

wth

Dri

ve

rs

nH

isto

rically

difficult to o

bta

in f

inancin

g

nR

ecent in

cre

ase in p

rivate

equity f

inancin

g for

esta

blis

hed industr

y p

laye

rs w

ith m

atu

re

opera

tions

Inte

rest

fro

m P

E p

layers

nW

ork

ing p

opula

tion in I

ndia

is e

stim

ate

d to

constitu

te 6

2%

of th

e tota

l popula

tion b

y 2016

nB

y 2

030, In

dia

n c

itie

s a

re lik

ely

to h

ouse 4

0%

of

India

’s p

opula

tion a

nd a

ccount fo

r 69%

of

India

’s G

DP

Gro

win

g W

ork

ing

Po

pu

lati

on

an

d

Ris

ing

Urb

an

izati

on

nU

rban India

expecte

d to h

ave a

nearly

fourf

old

incre

ase in t

he p

er

capita d

isposable

incom

e

from

2008 to 2

030

Ris

ing

In

co

me L

evels

So

urc

e : T

ech

no

pa

k R

ep

ort

20

09

; In

dia

Re

tail

Re

po

rt 2

00

9; N

RA

I R

ep

ort

20

10

; M

cK

inse

y R

ep

ort

20

10

Ind

ust

ry p

ote

nti

al

47

` I

n M

illi

on

Fin

an

cia

l O

ve

rvie

w

Sr.

No

P

art

icu

lars

Fo

r th

e Q

ua

rte

r e

nd

ed

on

Fo

r th

e N

ine

Mo

nth

s e

nd

ed

on

F

ina

nci

al

Ye

ar

31

.12

.20

13

3

1.1

2.2

01

2

31

.12

.20

13

3

1.1

2.2

01

2

20

13

2

01

2

1

Inco

me

fro

m o

pe

rati

on

s

(a

) N

et

Sa

les

67

1.8

5

85

.4

1,8

25

.6

1,6

03

.9

2,1

48

.3

1,8

78

.1

(b

) O

the

r o

pe

rati

ng

inco

me

5

0.2

2

6.1

1

37

.9

80

.8

12

0.9

8

4.2

To

tal

Inco

me

fro

m o

pe

rati

on

s 7

22

.0

61

1.5

1

,96

3.5

1

,68

4.7

2

,26

9.2

1

,96

2.3

E

xp

en

ses

(a

) C

ost

of

ma

teri

als

co

nsu

me

d

21

0.1

1

70

.9

55

8.3

4

55

.5

60

9.6

5

10

.2

(b

) E

mp

loye

es

be

ne

fits

exp

en

se

15

8.9

1

36

.4

45

9.5

3

81

.1

51

2.8

4

23

.1

(c

) D

ep

reci

ati

on

an

d a

mo

rtis

ati

on

exp

en

se

47

.2

37

.6

13

5.5

1

05

.0

14

9.3

1

28

.7

(d

) O

the

r e

xpe

nse

s 1

46

.2

11

5.7

3

87

.9

31

3.9

4

42

.3

36

6.9

(e

) Le

ase

Re

nt

97

.6

85

.5

28

5.3

2

51

.3

33

6.6

2

87

.0

2

Tota

l E

xp

en

ses

66

0.0

5

46

.1

1,8

26

.4

1,5

06

.8

2,0

50

.6

1,7

15

.9

3

Pro

fit

fro

m o

pe

rati

on

s b

efo

re o

the

r in

com

e

an

d f

ina

nce

co

sts

(1-2

) 6

2.0

6

5.4

1

37

.1

17

7.9

2

18

.6

24

6.4

4

Oth

er

Inco

me

2

7.5

2

3.4

7

1.9

6

4.9

9

1.2

2

7.1

5

Pro

fit

fro

m o

rdin

ary

act

ivit

ies

be

fore

fin

an

ce c

ost

s (3

+4

) 8

9.5

8

8.8

2

09

.0

24

2.8

3

09

.8

27

3.5

6

Fin

an

ce c

ost

s 0

.3

0.1

0

.5

4.9

5

.0

26

.6

7

Pro

fit

fro

m o

rdin

ary

act

ivit

ies

be

fore

ta

x

(5-6

) 8

9.2

8

8.7

2

08

.5

23

7.9

3

04

.8

24

6.9

8

Tax

exp

en

se

22

.3

22

.0

53

.9

57

.2

70

.7

74

.4

9

Ne

t P

rofi

t a

fte

r ta

x (

7-8

) 6

6.9

6

6.7

1

54

.6

18

0.7

2

34

.1

17

2.5

48

Inc

om

e F

rom

Op

era

tio

ns a

nd

Ou

tle

ts

EB

ITD

A a

nd

EB

ITD

A M

arg

ins

PA

T a

nd

PA

T M

arg

ins

No. of R

esta

ura

nts

& C

onfe

ctionaries a

s o

f M

arc

h 2

013

EB

ITD

A:

Earn

ings b

efo

re inte

rest, tax, depre

cia

tion a

nd a

mort

ization

Ne

t w

ort

h a

nd

To

tal D

eb

t

`. In Million

`. In Million

`. In Million

12

6

19

7

26

4

38

2

40

2

45

9

15

.1%

1

7.0

%

20

.5%

2

2.0

%

20

.5%

2

0.2

%

0.0

%

5.0

%

10

.0%

15

.0%

20

.0%

25

.0%

0

10

0

20

0

30

0

40

0

50

0

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

EB

IDT

A (

LH

S)

EB

IDT

A M

arg

ins (

RH

S)

0

50

0

10

00

15

00

20

00

25

00

30

00

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

491

556

709

976

1149

2905

282

242

237

198

292

2.2

Ne

twort

hT

ota

l D

ebt

833

1158

1288

1732

1962

2269

40

52

63

74

83

96

020

40

60

80

10

0

12

0

0

50

0

10

00

15

00

20

00

25

00

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

Inco

me F

rom

Ope

ratio

ns (

LH

S)

No

. O

f O

ute

ts (

RH

S)

`. In Million

44

65

113

160

173

234

5.3

0%

5.6

0%

8.7

0%

9.0

0%

9.0

0%

10.3

0%

0.0

0%

2.0

0%

4.0

0%

6.0

0%

8.0

0%

10

.00

%

12

.00

%

0

50

10

0

15

0

20

0

25

0

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

PA

T (

LH

S)

PA

T M

arg

ins (

RH

S)

Se

lect

Fin

an

cia

ls

49

Ba

lan

ce S

he

et

Hig

hli

gh

ts H

1 F

Y 2

01

4

•C

ash a

nd C

ash E

quiv

ale

nts

`

61.9

•To

tal F

ixe

d A

sse

ts

` 1

,28

8.1

•To

tal C

urr

en

t A

sse

ts

` 1

,61

9.9

•C

urr

en

t In

ve

stm

en

ts

` 1

,22

7.5

` In

Mill

ion ;

Fig

ure

s a

s o

n S

epte

mb

er

30, 2

01

3

•To

tal D

eb

t `

8.1

50

Sa

les

Ex

pe

ns

es

•Toplin

e in

cre

ase h

elp

ed

absorb

ris

ing c

osts

•In

flationary

Pre

ssure

s p

ers

ist

•G

ood T

raction d

ue t

o M

atu

rity

of

new

sto

res o

pened

•P

rice h

ike im

ple

mente

d in e

nd N

ovem

ber

2013

EB

ITD

A

•S

tabili

zation o

f M

arg

ins

in a

tough e

nvironm

ent

Pro

fit

aft

er

Ta

x

•H

igh

er

Ta

x e

xp

en

se

s o

n a

cco

unt

of

imp

rove

d O

pe

ration

al e

ffic

ien

cie

s

•D

efe

rre

d F

MP

Div

ide

nd

bo

osts

Oth

er

Inco

me

(o

ne

-tim

e)

Fin

an

cia

l H

igh

lig

hts

Fo

r Q

3 F

Y 2

01

4

51

AN

NE

XU

RE

S

52

19

92

¾P

rom

ote

rs la

un

ch t

he first re

sta

ura

nt u

nd

er

the

nam

e O

nly

Fis

h w

hic

h w

as la

ter

rena

me

d O

h!

Ca

lcu

tta

19

94

¾P

rom

ote

rs o

pe

n

firs

t M

ain

land

Ch

ina r

esta

ura

nt

in M

um

bai

19

99

¾

Incorp

ora

ted a

s

Sp

ecia

lity

Re

sta

ura

nts

Priva

te L

imite

d

20

01

¾M

ain

land

Ch

ina

in K

olk

ata

20

02

¾M

ain

land

Ch

ina in

Pu

ne

an

d C

hen

na

i

¾A

cq

uire

d tw

o

Main

land C

hin

a

resta

ura

nts

(M

um

ba

i

and

Hyd

era

ba

d)

fro

m P

rom

ote

rs

20

03

¾N

etw

ork

of five

resta

ura

nts

in 5

citie

s

20

05

¾A

cq

uired O

h!

Ca

lcu

tta r

esta

ura

nt

in M

um

ba

i fr

om

Pro

mo

ters

20

06

¾O

pen

ed

its

10

th

Re

sta

ura

nt

20

07

¾A

llott

ed

Pre

fere

ntia

l

Sh

are

s to

SA

IF

¾A

cq

uire

d J

ust

Birya

ni and S

we

et

Be

ng

al

¾O

pen

ed

Ma

cha

an

in M

um

ba

i

20

08

¾O

pen

ed

first fr

anch

ise

resta

ura

nt in

Gu

wa

ha

ti

¾O

pen

ed

a F

lam

e &

Grill

Re

sta

ura

nt in

Ko

lka

ta

20

10

¾O

pen

ed

its

50

th

resta

ura

nt

¾O

pen

ed

its

first

inte

rnatio

na

l

fra

nch

ise

in

Dh

aka

,

Bang

ladesh

20

12

¾R

esta

ura

nts

and

co

nfe

ction

arie

s

netw

ork

exp

an

de

d t

o 9

6 (

25 c

itie

s

in I

ndia

and

one

city in

Ba

ng

lade

sh)

20

13

¾O

pen

ed

Sig

ree

Glo

ba

l

Grill

¾O

pen

ed

Me

zzu

na

Co

mp

an

y’s

Jo

urn

ey

•O

ve

rall

in c

harg

e o

f th

e C

om

pa

ny

•O

ve

r 3

0 y

ears

of e

xp

erie

nce

in t

he a

dve

rtis

ing

and

hosp

ita

lity in

du

str

y

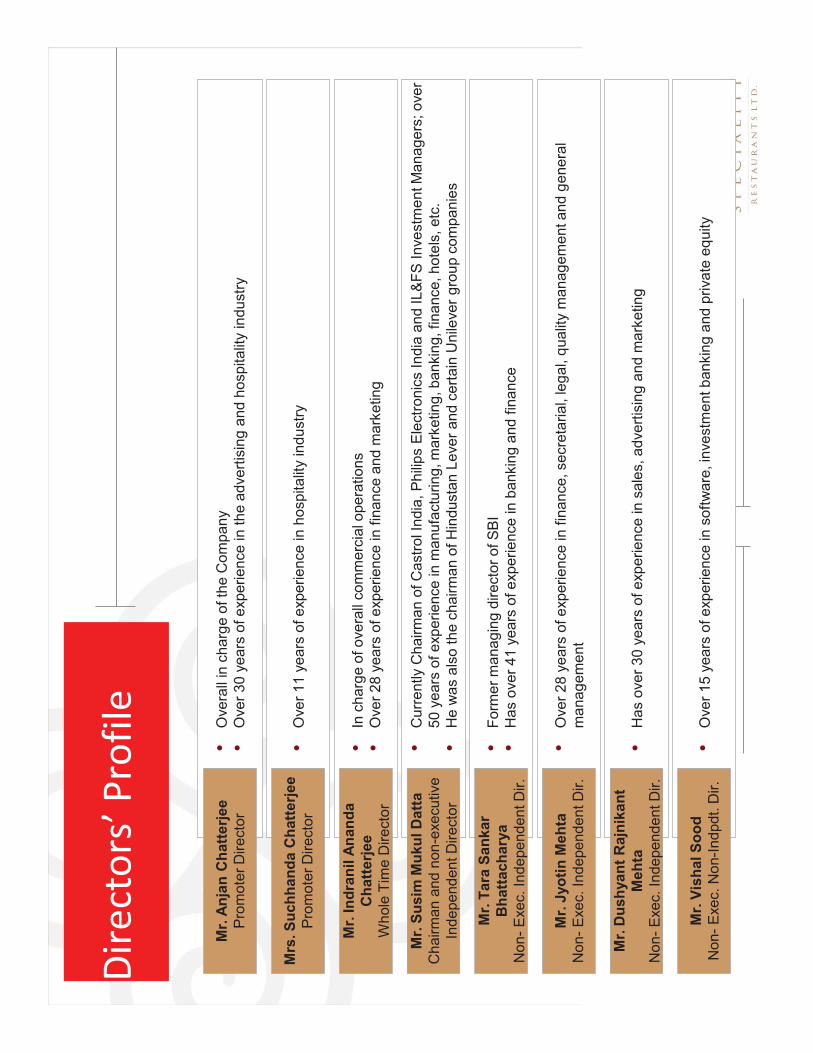

Mr.

An

jan

Ch

att

erj

ee

Pro

mo

ter

Dire

cto

r

•O

ve

r 1

1 y

ears

of e

xp

erie

nce

in h

osp

ita

lity in

du

str

y

Mrs

. S

uch

ha

nd

a C

hatt

erj

ee

Pro

mo

ter

Dire

cto

r

•In

ch

arg

e o

f o

ve

rall

co

mm

erc

ial o

pe

ratio

ns

•O

ve

r 2

8 y

ears

of e

xp

erie

nce

in f

inan

ce a

nd

ma

rke

tin

g

Mr.

In

dra

nil

An

an

da

Ch

att

erj

ee

Wh

ole

Tim

e D

ire

cto

r

•C

urr

ently C

hairm

an o

f C

astr

ol In

dia

, P

hili

ps E

lectr

onic

s In

dia

and

IL

&F

S I

nve

stm

ent M

ana

ge

rs; o

ve

r

50 y

ears

of e

xp

erie

nce

in m

anu

factu

rin

g, m

ark

etin

g, b

an

kin

g, fin

an

ce, h

ote

ls, e

tc.

•H

e w

as a

lso

th

e c

hairm

an o

f H

indu

sta

n L

eve

r a

nd

ce

rta

in U

nile

ve

r g

roup

co

mp

an

ies

Mr.

Su

sim

Mu

ku

l D

att

a

Chairm

an a

nd n

on-e

xecutive

Inde

pe

nd

en

t D

ire

cto

r

•F

orm

er

ma

na

gin

g d

ire

cto

r o

f S

BI

•H

as o

ve

r 4

1 y

ears

of e

xp

erie

nce

in b

an

kin

g a

nd

fin

an

ce

Mr.

Ta

ra S

an

kar

Bh

att

ach

ary

a

No

n-

Exe

c. In

de

pe

nd

en

t D

ir.

•O

ve

r 2

8 y

ears

of e

xp

erie

nce

in f

inan

ce, se

cre

tarial, le

ga

l, q

ualit

y m

ana

ge

me

nt a

nd

ge

ne

ral

ma

na

ge

me

nt

Mr.

Jyo

tin

Me

hta

No

n-

Exe

c. In

de

pe

nd

en

t D

ir.

•H

as o

ve

r 3

0 y

ears

of e

xp

erie

nce

in s

ale

s, a

dve

rtis

ing

and

ma

rke

tin

g

Mr.

Du

sh

ya

nt

Ra

jnik

an

t

Me

hta

No

n-

Exe

c. In

de

pe

nd

en

t D

ir.

•O

ve

r 1

5 y

ears

of e

xp

erie

nce

in s

oft

wa

re, in

ve

stm

ent b

an

kin

g a

nd

priva

te e

qu

ity

Mr.

Vis

ha

l S

oo

d

No

n-

Exe

c. N

on-I

ndp

dt.

Dir.

Dir

ect

ors

’ P

rofi

le

54

Than

k Y

ou