ASSESSMENT REPORT ADB LOAN NO. 2127 – INO (SF) December 31, 2010 Republic of Indonesia National Development Planning Agency ILMU Secretariat Jl. Besuki No. 9, Menteng Jakarta Pusat 10310 State Audit Reform Sector Development Project (STAR-SDP)

Transcript

ASSESSMENT REPORT

ADB LOAN NO. 2127 – INO (SF) December 31, 2010

Republic of Indonesia National Development Planning Agency

ILMU Secretariat Jl. Besuki No. 9, Menteng

Jakarta Pusat 10310

State Audit Reform Sector Development Project (STAR-SDP)

State Audit Reform Sector Development Project (STAR-SDP)

Republic of Indonesia National Development Planning Agency

ILMU Secretariat Jl. Besuki No. 9 Menteng

Jakarta Pusat 10310

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

TABLE OF CONTENTS

Page

ABREVIATIONS 2 EXECUTIVE SUMMARY 3 STAR SDP BASIC DATA 6 1. PROJECT DESCRIPTION........................................................................................ 7 1.1 Background of STAR-SDP ……….................................................................. 7 1.2 The Goal and Objectives of the Investment Loan……………………………. 7 1.3 Objectives of the Assessment Report and Methodology …..………………... 8 2. EVALUATION OF DESIGN AND IMPLEMENTATION................................ 9 2.1 Relevance to Design and Formulation ………………………………………. 9 2.1.1 Introduction of New Systems and Practices for Effective External Audit ….. 9

2.1.2 Introduction of New Regulatory Structures and Practices for Effective Internal Audit…………………………………………………………………

11

2.1.3 Designing a Professional Degree Education and Non-degree Education Program for Internal Auditors………………………………………………...

13

2.1.4 Introduction of New Practices for Parliamentary Oversight of Public Sector Audit …………………………………………………………………………

APPENDIX 1: Details of Activities Implemented and Output

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

ABREVIATIONS

ADB Asian Development Bank BAPPENAS National Development Planning Agency (Badan Perencanaan Pembangunan

Nasional) BAWASDA Inspectorate of Province/ Municipal/ City (Badan Pengawas Daerah)

BAKN State Budget Accountability Body (Badan Akuntabilitas Keuangan Negara) BPK The Audit Board of Indonesia (Badan Pemeriksa Keuangan)

BPKP Supervision of Financial and Development Agency (Badan Pengawasan Keuangan dan Pembangunan)

BPPK Financial Education and Training Agency of MOF-IG (Badan Pendidikan dan Pelatihan Keuangan)

CIU Component Implementation Unit DIPA List of Budget Implementation (Daftar Isian Pelaksanaan Anggaran) DPR Parliament (Dewan Perwakilan Rakyat)

DPRD Regional Parliament (Dewan Perwakilan Rakyat Daerah) EA Executing Agency

HRM Human Resources Management IDP Institutional Development Plan

IG Inspectorate General ILMU Investment Loan Monitoring Unit

IT Information Technology KEPPRES Presidential Decree / (Keputusan Presiden)

MOF-IG Ministry of Finance – Inspectorate General MOHA-IG Ministry of Home Affairs – Inspectorate General MONE-IG Ministry of National Education – Inspectorate General

PCU Project Coordination Unit PERDA Regulation of Regional Government (Peraturan Daerah)

PIU Project Implementation Unit PLMU Program Loan Monitoring Unit

PP Government Regulation (Peraturan Pemerintah) RPP Draft of Government Law (Rancangan Peraturan Pemerintah) SAI Supreme Audit Institution

SDM Human Resources (Sumber Daya Manusia) SEKWAN Secretariat of DPRD

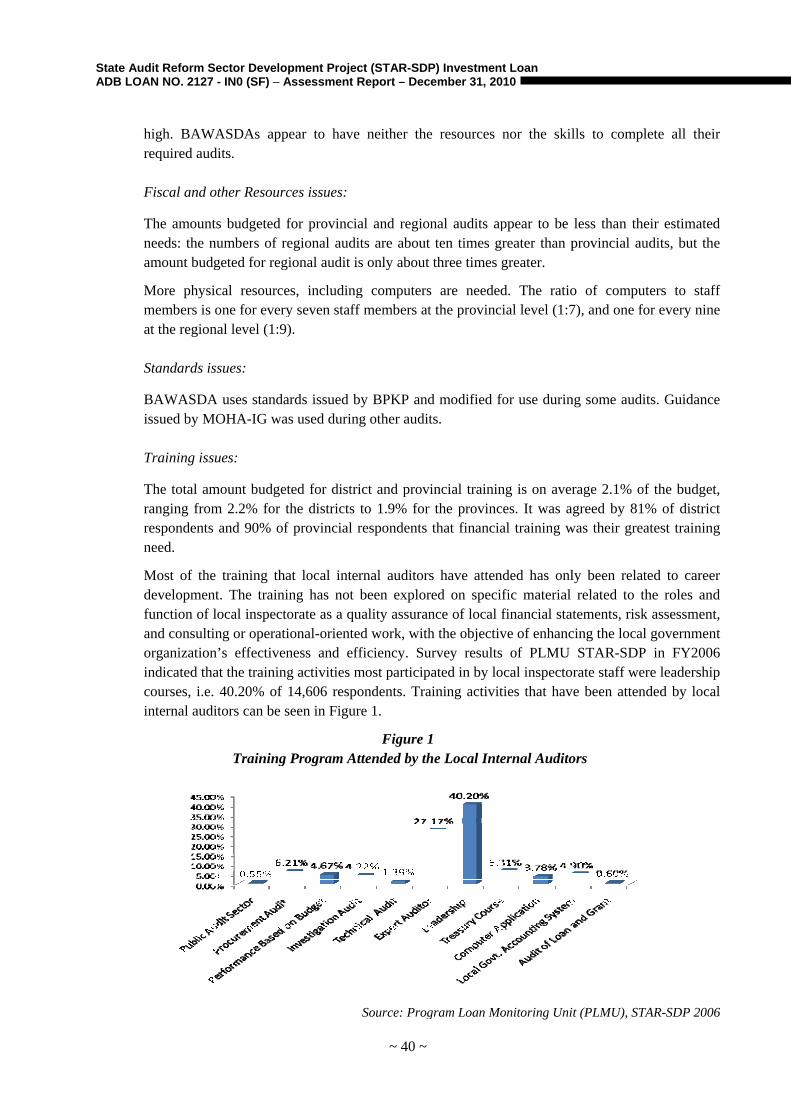

SISWASDANAS National Level Regional Governance Information System (Sistem Informasi Penyelenggaraan Urusan Pemerintah Daerah)

SK Decision Letter (Surat Keputusan) SPKN State Audit Standard (Standar Pemeriksaan Keuangan Negara)

STAR-SDP State Audit Reform - Sector Development Program

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 3 ~

EXECUTIVE SUMMARY

STAR-SDP is a response to support both the external and internal audit function at central and regional level to ensure good governance, accountability and transparency. STAR-SDP establishes the foundations for a strong audit sector through a mixture of policies and capacity building initiatives. To leverage this reform the combination of policy-based and investment lending support is considered appropriate and timely at the present stage of public expenditure reform. STAR-SDP is supported by the Project Loan having the objectives of enhancing the capability of audit institutions by building upon past support, and by introducing techniques and approaches that allow the institutions to operate effectively and efficiently and incorporate international best practices. Achievements were achieved through implementation of activities under the five main components approaches as mentioned below.

New systems and practices for effective external audit have been established. The quality and coverage of BPK audits have been improved through the development and adoption of auditing standards and practices that meet international standards such as the State Finance Audit Standard (SPKN), Code of Ethics, Audit Management Guideline (PMP), new techniques for presenting audit reports, new procedures for specialized audits, and quality assurance system. BPK has also improved the capacity and management of its human resources in carrying out high quality audits through the establishment of a HRM Plan that is consistent with the new audit procedures, and participation of its staff in overseas and domestic degree and non-degree capacity building programs. Technology Information of BPK has strongly been enhanced, through the expansion and establishment of IT systems in its headquarter and regional offices. Under the STAR-SDP Project, BPK has managed to raise the ratio of total notebooks against professional staff from 1:6.55 in year 2004 to 1:2.00 in 2010. The above BPK achievements have been confirmed by the results of the peer review conducted by the Netherland Court of Audit (2008-2009), which concluded that since 2004 BPK has transformed its organization into a modern Supreme Audit Institution with legally embedded independence, a strong mandate and qualified staff to realize its tasks and objectives.

New Regulatory Structures and Practices for Effective Internal Audit has been introduced under the STAR-SDP efforts through the institutions of MOF-IG, BPKP, MOHA-IG, BAWASDA, and MONE. MOF-IG has successfully established a ministerial financial statement review manual, which has assisted MOF-IG in better management of risk-based audit procedures that have led to the improved quality of MOF financial statements. This was indicated by the audited MOF Financial Statement of 2008, which obtained a qualified opinion, an improvement in comparison to the audited 2007 MOF Financial Statements that obtained a disclaimer opinion.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 4 ~

The issuance of Government Regulation (PP) 60/2008 concerning Government Internal Control System has made the mandates of BPKP clear. The clear mandates include conducting cross-sector treasury and other audit activities as instructed by the President, reviewing the government's financial statements prior to submission to the President, and managing the implementation of the Government's internal audit system. BPKP has also started to implement the GICS (Government Internal Control System) through the issuance of a decree (Perka BPKP-1326/K/LB/2009) in December 2009, which requires development of a task-force in each government institution to assist government agencies in the implementation of GICS. Currently, the required task-forces have been established and are operational in each government institution. A number of decrees of Head of Region concerning Internal Control System Implementation had been issued as a result of BPKP’s continuous effort in socializing the GICS. MOHA-IG has successfully issued a regulation (Permendagri No. 8 Year 2009) concerning Guideline of Regional Governance Supervision, which provides guidance for BAWASDA in carrying out a supervisory function on the implementation of the obligatory and voluntary functions of Local Governments. In order to support the implementation of Permendagri No. 8 Year 2009, MOHA-IG has developed an information system (SIWASDANAS) for handling audit mechanism carried out by BAWASDA and has enforced its implementation through the issuance of Permendagri No.1 Year 2010. These achievements have extended the scope of audit to Local Governments and improved the effectiveness of planning and management of internal audit carried out by BAWASDA. MOHA-IG has also developed and disseminated a standardized Model regulation in the Format of a Head of Region’s Decree and Regional Law that addresses the roles and responsibilities of BAWASDA. Given clearer roles and responsibilities in combination with STAR-SDP funded in-house training through the BAWASDA’s Institutional Development Plan, improved consistency and quality in the audit activities have started to be shown by the 50 participating BAWASDAs. The technical training (BIMTEK) in special topics which was part of the IDP, was effective in enhancing the individual capacity of BAWASDA staff, particularly those not having an accounting or public finance educational background. Approximately four to five topics of training were carried out for each individual BAWASDA and about three to four training topics were carried out for each SEKWAN.

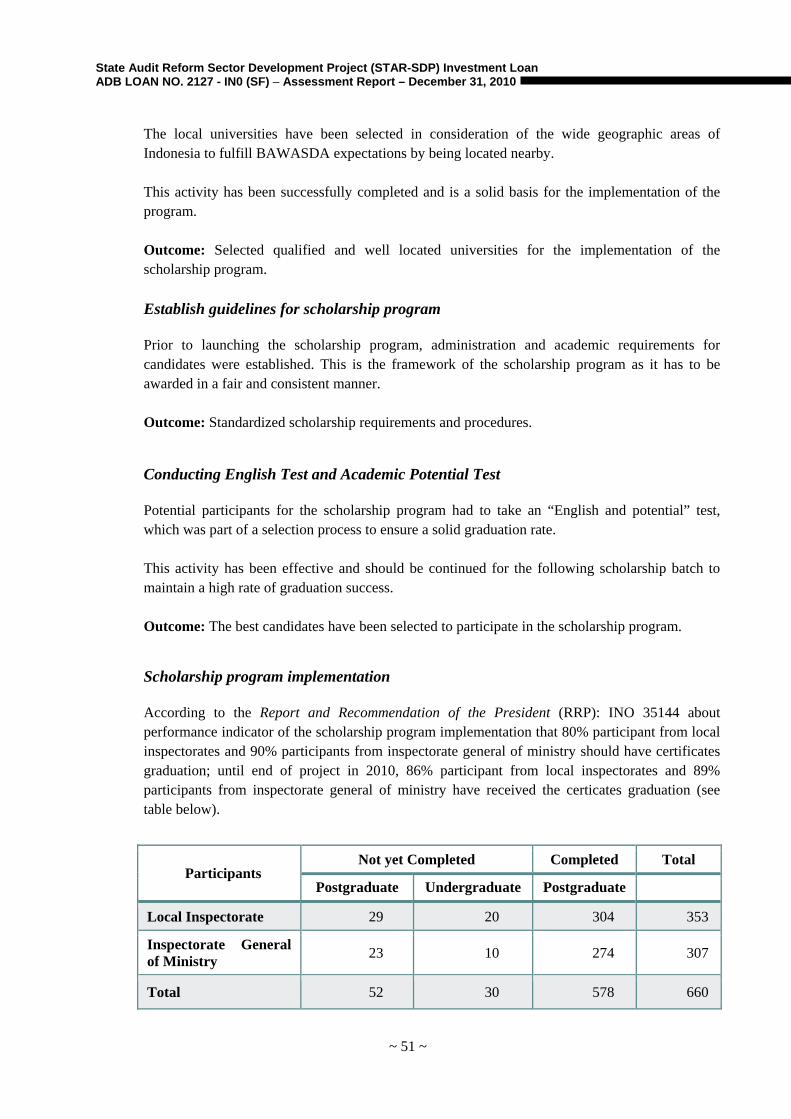

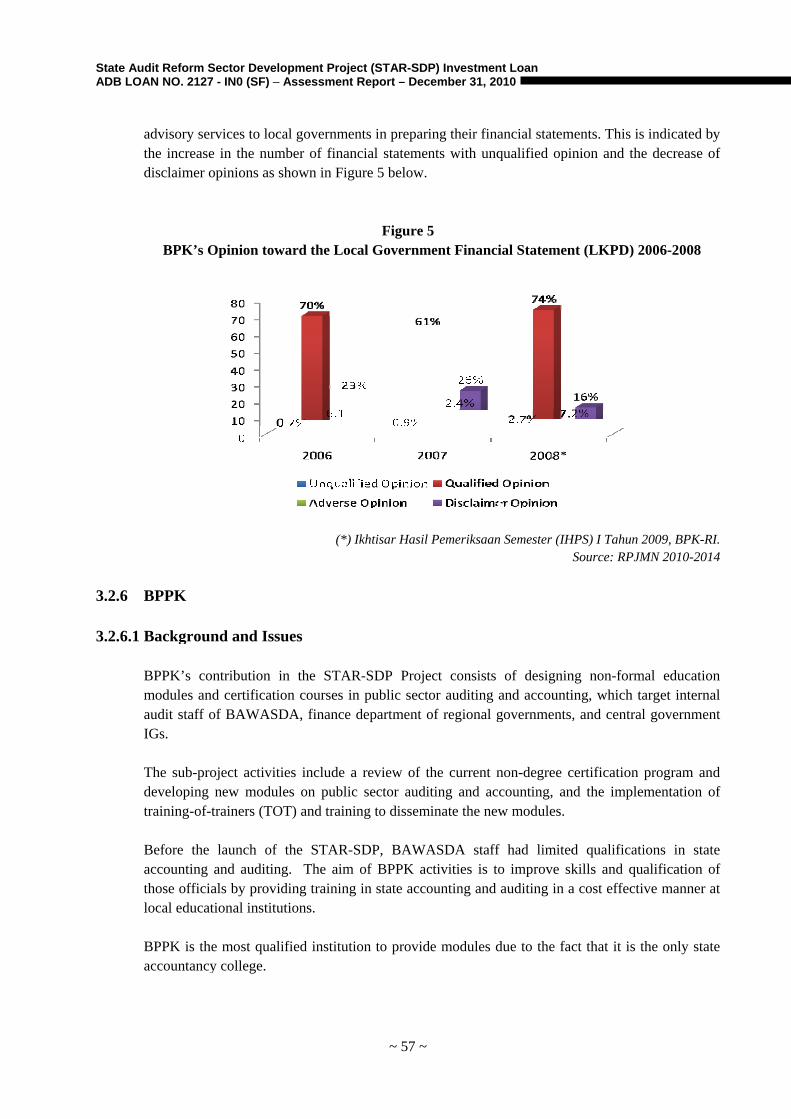

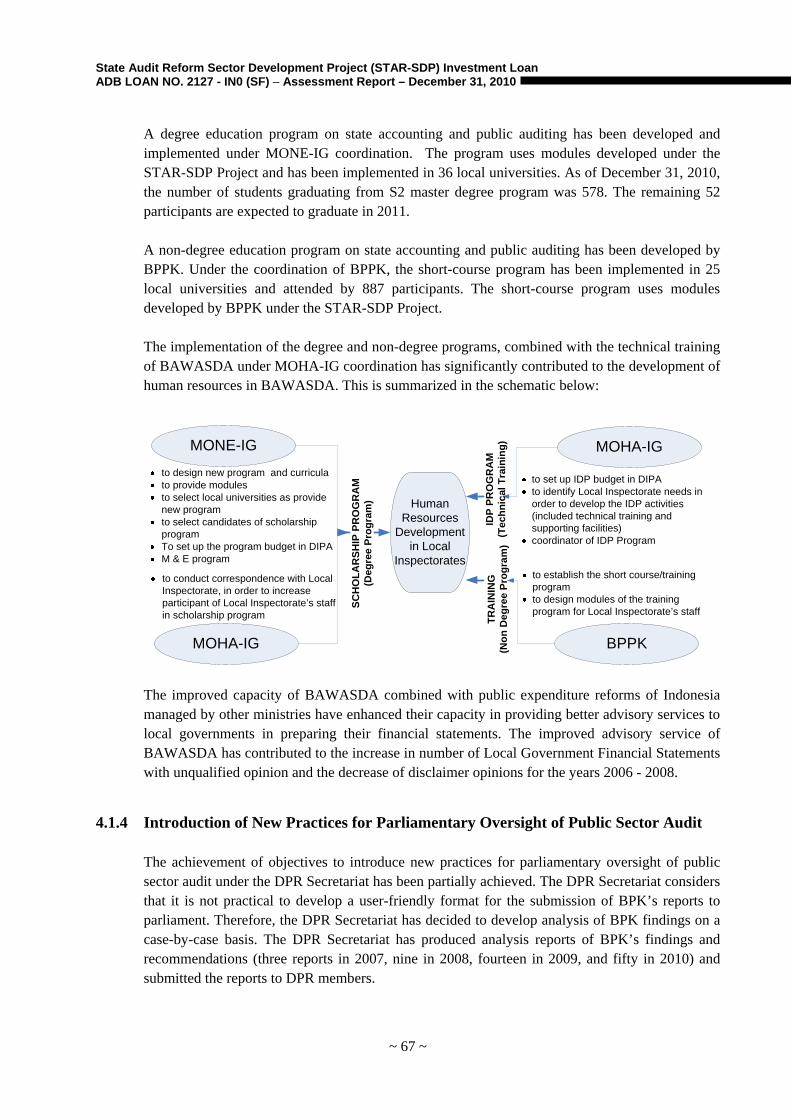

A Professional Degree Education and Non-degree Education Program on state accounting and public auditing for Internal Auditors have been established by MONE-IG and BPPK, respectively. As of 31 December 2010, more than 80% of Bawasda and 90% of IG’s participants have successfully graduated from the scholarship program. This achievement has exceeded the project’s log frame target. The total number of graduates (578 participants) has increased the number of government internal auditors trained with accounting skill and knowledge. The participation of BAWASDA staff in the degree and non-degree programs combined with the technical training carried out in BAWASDA has significantly contributed to the capacity development of human resources, which in turn has improved the advisory capacity of BAWASDA. The results can be seen by the increase in the number of Local Government Financial Statements with unqualified opinion and the decrease of disclaimer opinions for the year 2006 - 2008.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 5 ~

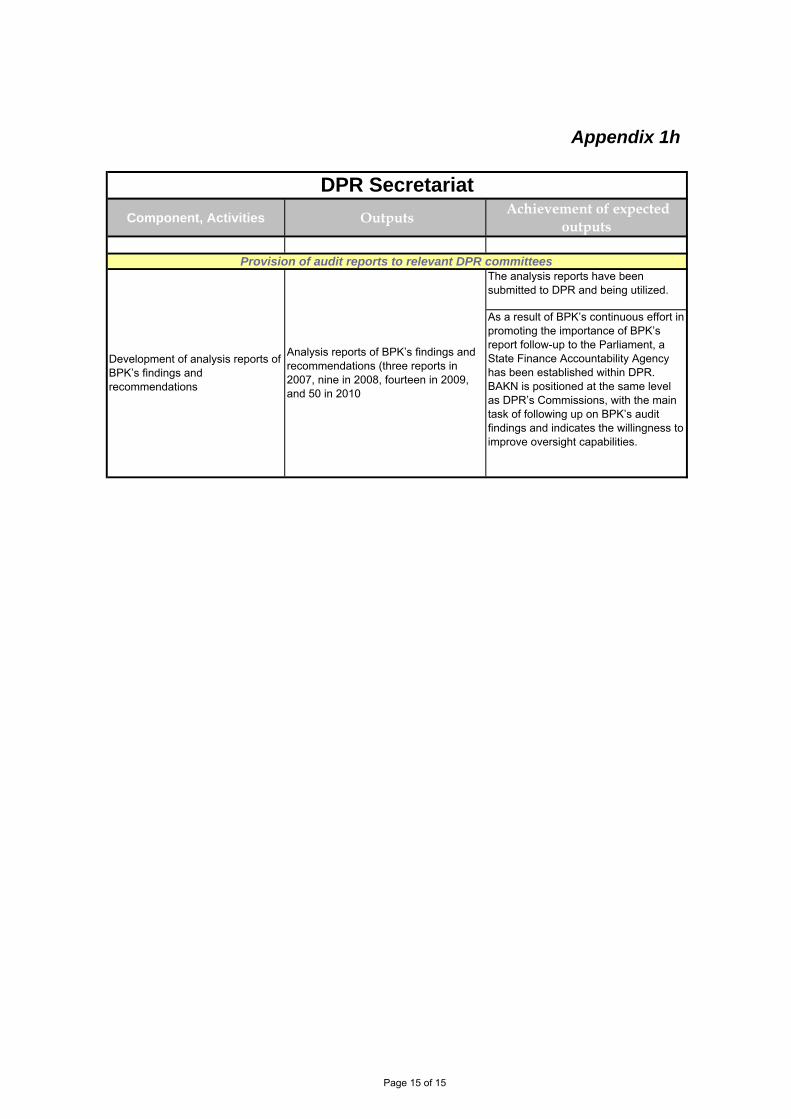

New Practices for Parliamentary Oversight of Public Sector Audit has started to be introduced. From 2007 to 2010 DPR Secretariat has developed BPK analysis reports and presented them to the Parliaments. These reports have assisted Parliament in better and easier understanding of BPK audit reports. The continuous effort in promoting the importance of BPK’s report follow-up to the Parliament has resulted in the establishment of the State Finance Accountability Agency (Badan Akuntabilitas Keuangan Negara or BAKN) within DPR with the main task of following up BPK’s audit findings. Furthermore, DPR Secretariat has developed the Standard Operating Procedures (SOP) for the BAKN. At regional level, a guideline on the follow-up of Audit Result of BPK by DPRD has also been developed and enforced through the issuance of Permendagri No. 13/2010. As a result of this achievement there has been an increase in the use of audit reports by DPRD members. The above achievements have resulted in the increased willingness of parliament to improve their oversight capabilities. This in turn will have a positive impact on the improvement of governance in the Republic of Indonesia.

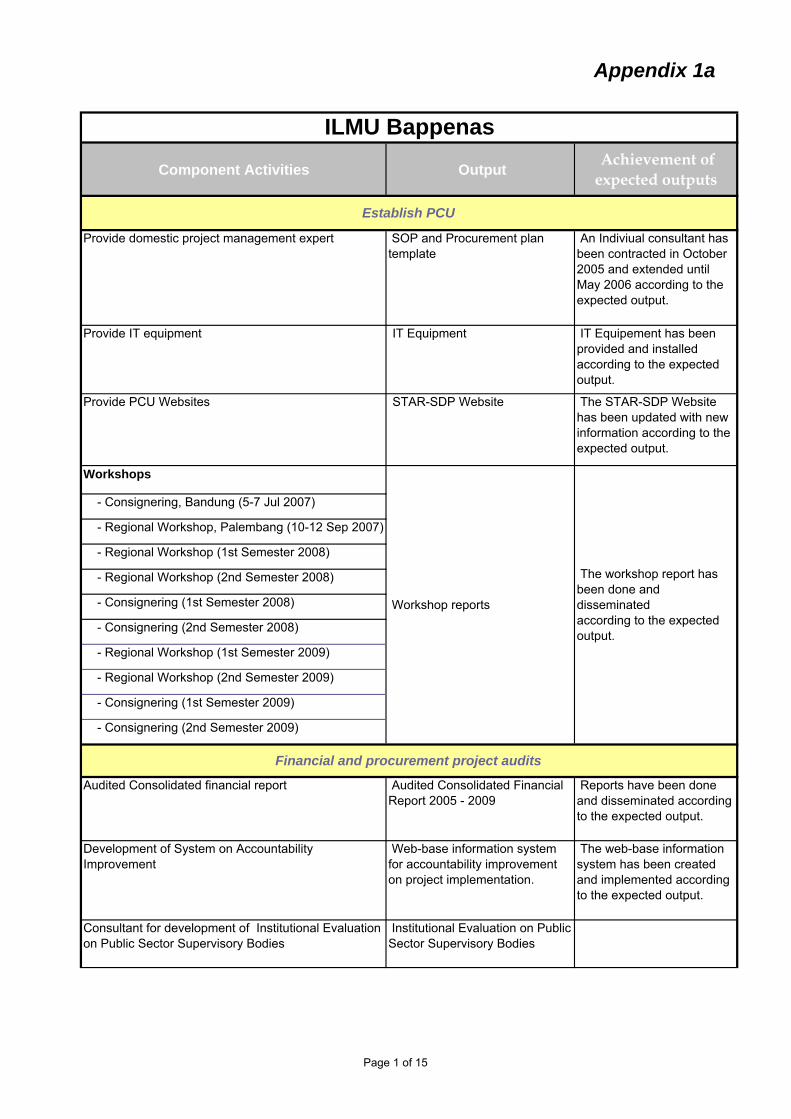

Establishment of the Investment Loan Monitoring Unit (ILMU) in BAPPENAS. Since the beginning of the project, ILMU has successfully coordinated, supervised and monitored the project implementation. ILMU has ensured that the activities conducted by the Project Implementation Units (PIUs) were consistent with STAR-SDP’s objectives by performing a review of the PIU’s work-plan and by monitoring the work-plan to be implemented in a timely and cost effective manner. This has given support to PIUs in the achievement of the expected outputs and outcomes. In addition, ILMU has successfully submitted Audited Project Financial Statements (AFS) with unqualified opinion to ADB for the years 2005-2009.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 6 ~

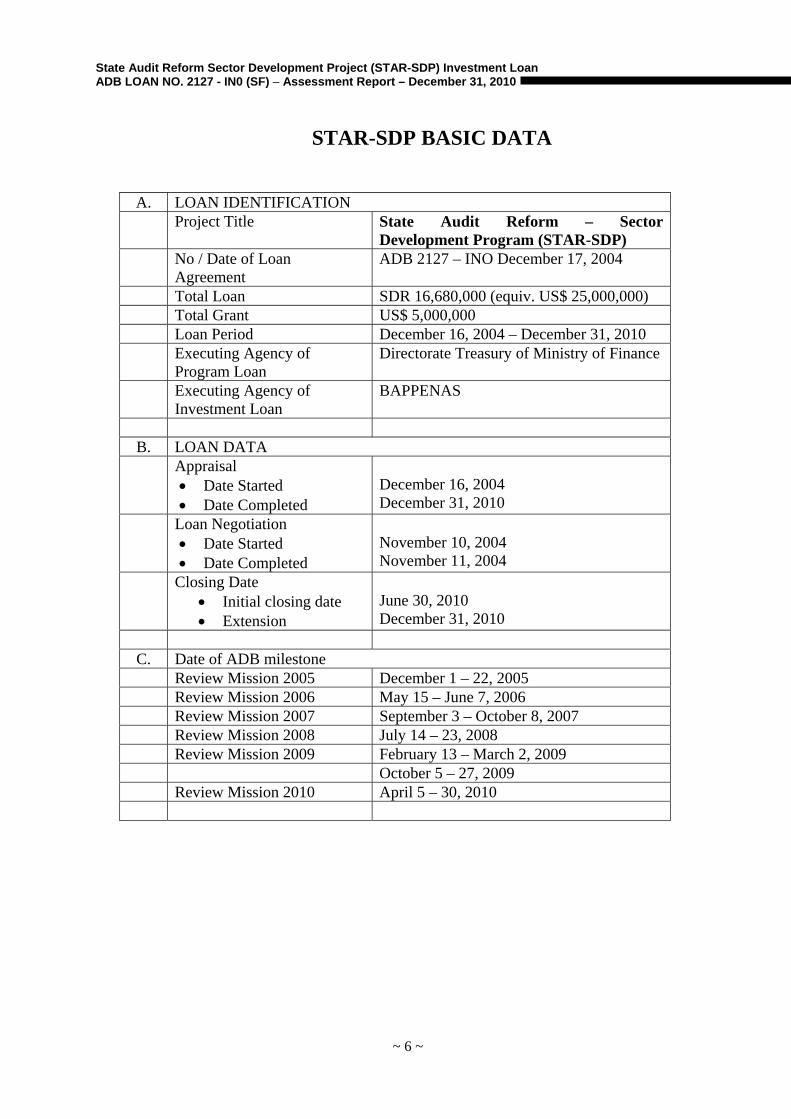

STAR-SDP BASIC DATA

A. LOAN IDENTIFICATION Project Title State Audit Reform – Sector

Development Program (STAR-SDP) No / Date of Loan

Agreement ADB 2127 – INO December 17, 2004

Total Loan SDR 16,680,000 (equiv. US$ 25,000,000) Total Grant US$ 5,000,000 Loan Period December 16, 2004 – December 31, 2010 Executing Agency of

Program Loan Directorate Treasury of Ministry of Finance

Executing Agency of Investment Loan

BAPPENAS

B. LOAN DATA

Appraisal • Date Started • Date Completed

December 16, 2004 December 31, 2010

Loan Negotiation • Date Started • Date Completed

November 10, 2004 November 11, 2004

Closing Date • Initial closing date • Extension

June 30, 2010 December 31, 2010

C. Date of ADB milestone

Review Mission 2005 December 1 – 22, 2005 Review Mission 2006 May 15 – June 7, 2006 Review Mission 2007 September 3 – October 8, 2007 Review Mission 2008 July 14 – 23, 2008 Review Mission 2009 February 13 – March 2, 2009 October 5 – 27, 2009 Review Mission 2010 April 5 – 30, 2010

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 7 ~

1. PROJECT DESCRIPTION

1.1 BACKGROUND OF STAR-SDP

State Audit Reform - Sector Development Program (STAR-SDP) is a program initiated by the Government of Republic of Indonesia to enhance public sector audit reform in line with the government bureaucratic reform. Substantially, the public sector audit reform will provide a significant contribution in establishing good governance. The reform will be a part of the government bureaucratic reform, which has become a priority in implementing national development, as stated in Rencana Pembangunan Jangka Menengah Nasional (RPJMN) 2004-2009. The government will perform better when the public sector audit reform is functioning for both external and internal audit. STAR-SDP will be the basis for the development of the audit sector through several supporting policies and activities aimed at supporting the public sector audit institutions. STAR-SDP requires financial support for the implementation of its activities, which has been provided by the Government of Indonesia through a loan from ADB and a grant from the Government of the Netherlands. On 13 December 2004, the Asian Development Bank (ADB) approved a package of financial assistance to the Republic of Indonesia to support the State Audit Reform Sector Development Program (STAR-SDP). The package comprised (i) a program loan, (ii) a project loan, and (iii) administration of two technical assistance (TA) grants for program loan coordination and monitoring, and project loan monitoring and quality assurance, and the other to assist implementation of the project loan. The program loan of $200 million (No. 2126-INO) was from ADB’s ordinary capital resources (OCR). The project loan [No. 2127-INO (SF)], came from the Asian Development Fund (ADF), in an amount of Special Drawing Rights 16,680,000 (about $25 million). The loan agreement of the project loan was signed on December 16, 2004. The Government of the Netherlands provided a total amount of $10 million in co-financing, $5 million in grant for the project loan and the remaining $5 million being allocated for technical assistance ($1.3 million for the program loan and $3.7 million for the project loan [TA 4474]) in respect of the above two grants).

1.2 THE GOAL AND OBJECTIVES OF THE INVESTMENT LOAN

The goal of STAR-SDP was to enhance governance, and the efficiency, economy, and effectiveness of the public sector audit. This would be achieved by strengthening audit institutions, which would operate to internationally accepted standards.

The objectives of the investment loan are to enhance the capability of the audit institutions by building upon past support and introducing techniques and approaches that will allow the institutions to meet their immediate mandates by operating effectively and efficiently, and incorporating international best practices. Investment support is expected to: (i) build a strong external audit function able to effectively operate at the national level; (ii) enhance the capability

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 8 ~

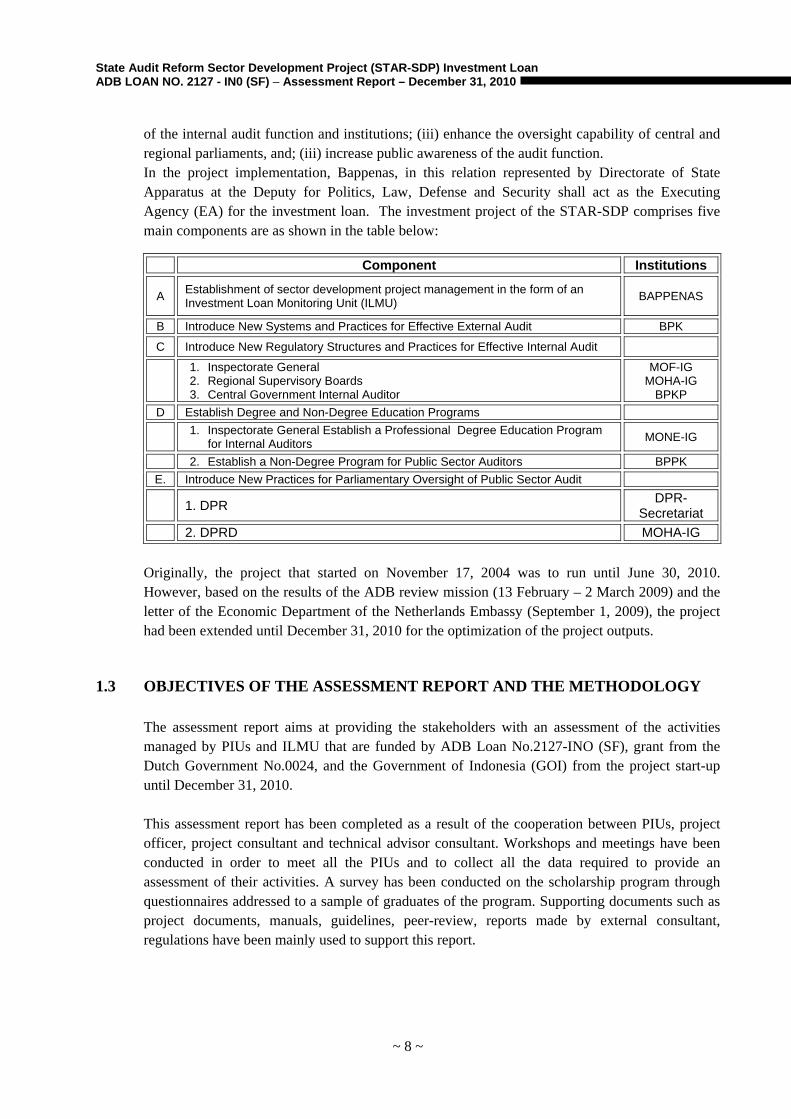

of the internal audit function and institutions; (iii) enhance the oversight capability of central and regional parliaments, and; (iii) increase public awareness of the audit function. In the project implementation, Bappenas, in this relation represented by Directorate of State Apparatus at the Deputy for Politics, Law, Defense and Security shall act as the Executing Agency (EA) for the investment loan. The investment project of the STAR-SDP comprises five main components are as shown in the table below:

Component Institutions

A Establishment of sector development project management in the form of an Investment Loan Monitoring Unit (ILMU) BAPPENAS

B Introduce New Systems and Practices for Effective External Audit BPK

C Introduce New Regulatory Structures and Practices for Effective Internal Audit

1. Inspectorate General 2. Regional Supervisory Boards 3. Central Government Internal Auditor

MOF-IG MOHA-IG

BPKP D Establish Degree and Non-Degree Education Programs

1. Inspectorate General Establish a Professional Degree Education Program for Internal Auditors MONE-IG

2. Establish a Non-Degree Program for Public Sector Auditors BPPK E. Introduce New Practices for Parliamentary Oversight of Public Sector Audit

1. DPR DPR-Secretariat

2. DPRD MOHA-IG

Originally, the project that started on November 17, 2004 was to run until June 30, 2010. However, based on the results of the ADB review mission (13 February – 2 March 2009) and the letter of the Economic Department of the Netherlands Embassy (September 1, 2009), the project had been extended until December 31, 2010 for the optimization of the project outputs.

1.3 OBJECTIVES OF THE ASSESSMENT REPORT AND THE METHODOLOGY The assessment report aims at providing the stakeholders with an assessment of the activities managed by PIUs and ILMU that are funded by ADB Loan No.2127-INO (SF), grant from the Dutch Government No.0024, and the Government of Indonesia (GOI) from the project start-up until December 31, 2010. This assessment report has been completed as a result of the cooperation between PIUs, project officer, project consultant and technical advisor consultant. Workshops and meetings have been conducted in order to meet all the PIUs and to collect all the data required to provide an assessment of their activities. A survey has been conducted on the scholarship program through questionnaires addressed to a sample of graduates of the program. Supporting documents such as project documents, manuals, guidelines, peer-review, reports made by external consultant, regulations have been mainly used to support this report.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 9 ~

2. EVALUATION OF DESIGN AND IMPLEMENTATION

2.1 RELEVANCE TO DESIGN AND FORMULATION

Activities of STAR-SDP have been designed in accordance with the government bureaucratic reform implementation and objectives stated in the project documents. However, during the implementation of the activities per PIU, some activities have been added while others have been cancelled. This adaptation was sometimes necessary to implement new activities that appeared more relevant in regard to the achievements of the STAR-SDP and to cancel those that appeared less necessary or had already been carried out through other sources. We present below, the different changes in project activities, assessment on the modifications, and comparison of their relevance to the objectives of the project.

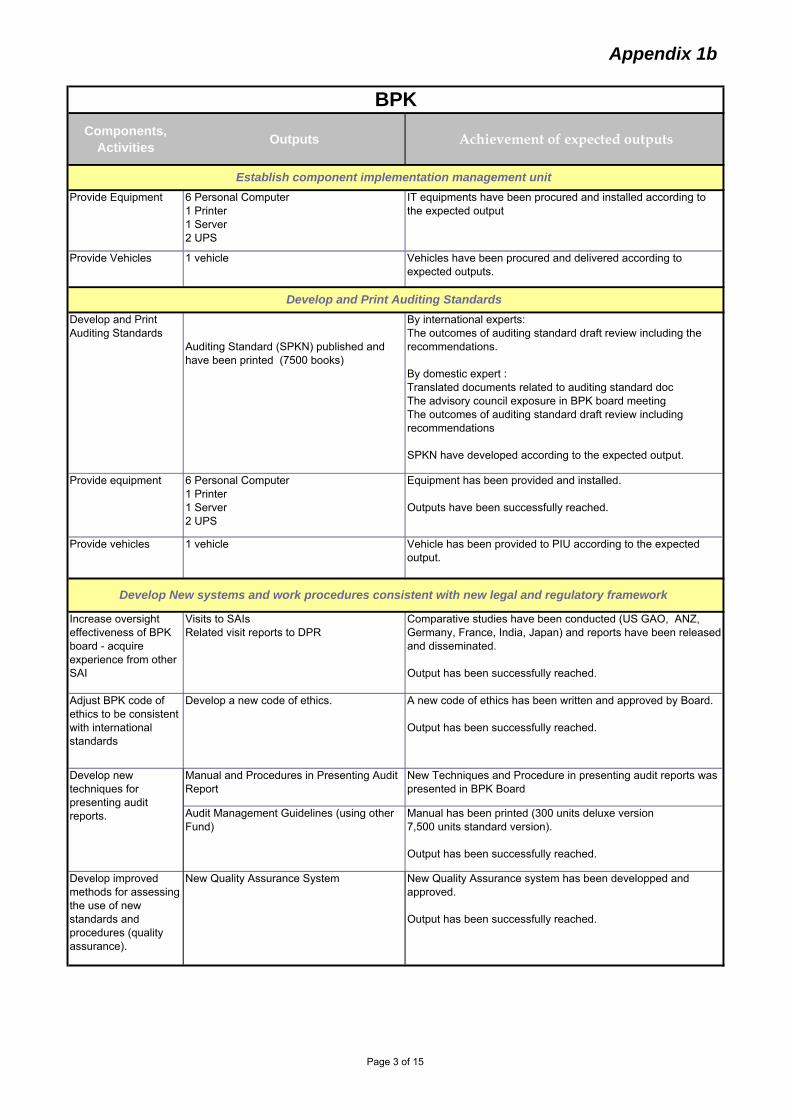

2.1.1 Introduction of New Systems and Practices for Effective External Audit

BPK

The main activities under BPK are focused on the development of new standards and work procedures that are consistent with legal and regulatory framework, as well as the development of the human resources management strategy and plan. Some of the project activities under the BPK component have been cancelled because they have been implemented using funding from the Government of Indonesia and not the investment loan facility. The cancelled activities are as below: (i) The printing of the newly revised code of ethics for management and staff that has been

developed to adjust BPK’s code of ethics to be consistent with international standards;

(ii) The revision approach to Audit Management, which was to assess the current work practices, revise audit management, validate and use new practices. This activity has been conducted directly by BPK without using STAR-SDP funding, except for printing the manual of new practices for staff;

(iii) The development of a risk-based audit manual with the objective of familiarizing BPK

staff with risk audit issues, developing new procedures for risk-based auditing, printing the manual for auditors, carrying out pilot-testing of the new procedures and obtaining validation from lessons learned from the experiences have been implemented by the BPK team using its own funding;

(iv) The development of a new specialized audit with the objectives of assessing current audit

practices, developing guidelines for specialized audits and covering government-wide

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 10 ~

audits, printing manual for staff, and pilot-testing for validation through lessons learned from the experiences have been implemented by the BPK team using its own funding;

(v) The introduction of pedagogic skills required for new audit standards with the purpose of

conducting quality professional courses for BPK staff that meet international best practices, according to Pusdiklat review, has been transferred to be included in the consultant activities in developing the competency-based curricula;

(vi) The development of audit report and disposition information system with the objectives

of developing a prototype system and implementing a version of SIPPA has been implemented by BPK using its own funding;

(vii) The development of electronic archiving of audit files and reports with the objective of

developing a prototype system and implementing a beta-version of electronic archiving has been directly implemented by BPK using its own funding;

(viii) The pilot-testing of new procedures for selected audit with the objectives of conducting

pilot-audit, providing specialist technical support and reviewing pilot-audit lessons learned have been implemented by BPK using its own funding;

(ix) The implementation of an in-service professional staff development program consistent

with the HRM plan was finally carried out by BPK using its own funding;

(x) The development of the program and courses to introduce the new procedures into regular BPK work practices has been transferred to be included in the consultant activities in developing curricula for competence-based training.

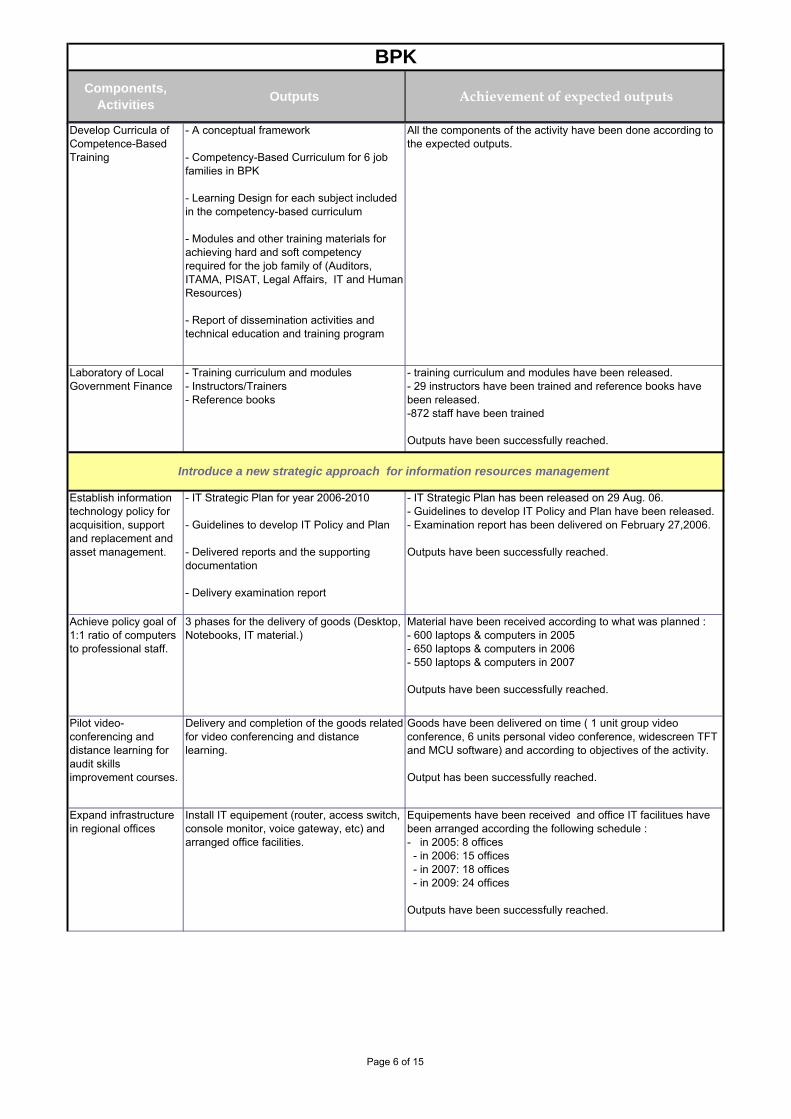

(xi) Procurement of computers was also cancelled. The cancellation of above mentioned activities has had no impact on the relevance of the project design nor has it affected the objectives of STAR-SDP. Activities that were added to the original project work plan with the objective of optimizing and complementing the activities under the BPK activities were as follows: (xii) The BPK Education and Training Center in cooperation with consultants, will prepare

Curricula for a Competency-based Training for the position groups of Auditor, Chief Inspectorate (ITAMA), Heads of Working Units (PISAT), Legal Affairs, Information Technology and Human Resources. The curricula will contain education and training materials that are expected to address the needs for the development of competencies of BPK Human Resources within the stated position groups.

The development of curricula for competence-based training activity shall include preparation of competency-based curriculum, delivery design, modules and other training instruments for achieving human resources competency standards as designated by the BPK Board.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 11 ~

The addition of this activity is in line with the objective of supporting the Education and Training Center in the capacity enhancement of BPK Human Resources.

(xiii) In order to enhance the regional finance management auditing competency of BPK

auditors at the BPK regional representative offices, the Education and Training Center of BPK intends to develop a local government finance accounting and local government finance auditing laboratory and training modules. The development of a Laboratory of Local Government Finance activity shall include the development of curriculum and modules for education and training programs in local government finance management practices, training modules in local government finance management audit, the design of a training laboratory, and to provide training in the subjects of Local Government Finance Management.

This activity is relevant to the main objective of this project, which is to make available a

Local Government Financial Management and Audit Laboratory in order to meet the competencies required in the Standards of State Financial Auditing (SPKN).

(xiv) The development of new organization according to new regulations shall include the

development of an action plan and a design for an organizational and management structure that shall be in line with the new regulation.

This activity was added to be in compliance with the new regulation Law 15/2006.

(xv) The allocation of investment loan facility for the cancelled procurement of desktop and

laptop computers for BPK year 2008 was reallocated for use in activity that supports the development of BPK’s human resources. This newly added activity for obtaining a degree program for BPK staff has covered 90 persons for the domestic degree program and 5 persons in the overseas degree program.

All of the above stated additional activities reinforce the role of BPK and are relevant to ADB expectations, as they will improve the project objectives by adding value and complementing the other project activities. The outcomes and expected outcomes of these added activities are further described in Chapter 3.

2.1.2 Introduction of New Regulatory Structures and Practices for Effective Internal

Audit

MOHA-IG

The key role of MOHA-IG in STAR-SDP is to facilitate the empowerment and capacity building of BAWASDA at the Provincial and District level by developing a new model regulation, developing new audit procedures and introducing these regulations into provincial and local government.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 12 ~

The recruitment of a legal expert through the loan to develop model regulation to be applied by BAWASDA was cancelled, and a local consultant has acquired international experience for developing the model regulation using non-loan facility. There has been no impact on the relevance, as the activity has been conducted through other sources. Considering the numerous activities to be implemented and the lack of staff in both numbers and skills to manage the project, MOHA-IG has been supported by a consultant. The consultant assists MOHA-IG in managing its daily activities including monitoring and reporting of BAWASDA activities. This activity is relevant to the aim of STAR-SDP, as it supports in the implementation of the overall MOHA-IG’s activities.

BAWASDA

BAWASDA has developed and implemented Institution Development Plan (IDP) as planned. Activities in the Institution Development Plan focus on the capacity building of BAWASDA.

MOF-IG

At the beginning of the project, MOF-IG was expected to develop new audit work procedures and carry out training of staff to introduce new procedures and skills to IG staff. However, this activity had been cancelled due to the development of Standard Operating Procedures (SOP) of IG’s audit on ministry’s operations and financial performance in 2007, in line with the reform program within MOF. This SOP development was funded by other sources, Rupiah Murni.

Accordingly, MOF-IG replaced the activity with development of ministerial financial statement review manual for IG, which was completed in early 2010. As stated in the Ministry of Finance’s regulation No.41/PMK.09/2010 dated 23 February 2010, the manual shall be used as a guideline for conducting review on the Ministry’s Financial Statements. The replacement of the major activity of MOF-IG is relevant with ADB’s expectations, as it will support the implementation of effective internal audit. The outcomes and expected outcomes of these added activities are further described in Chapter 3.

BPKP

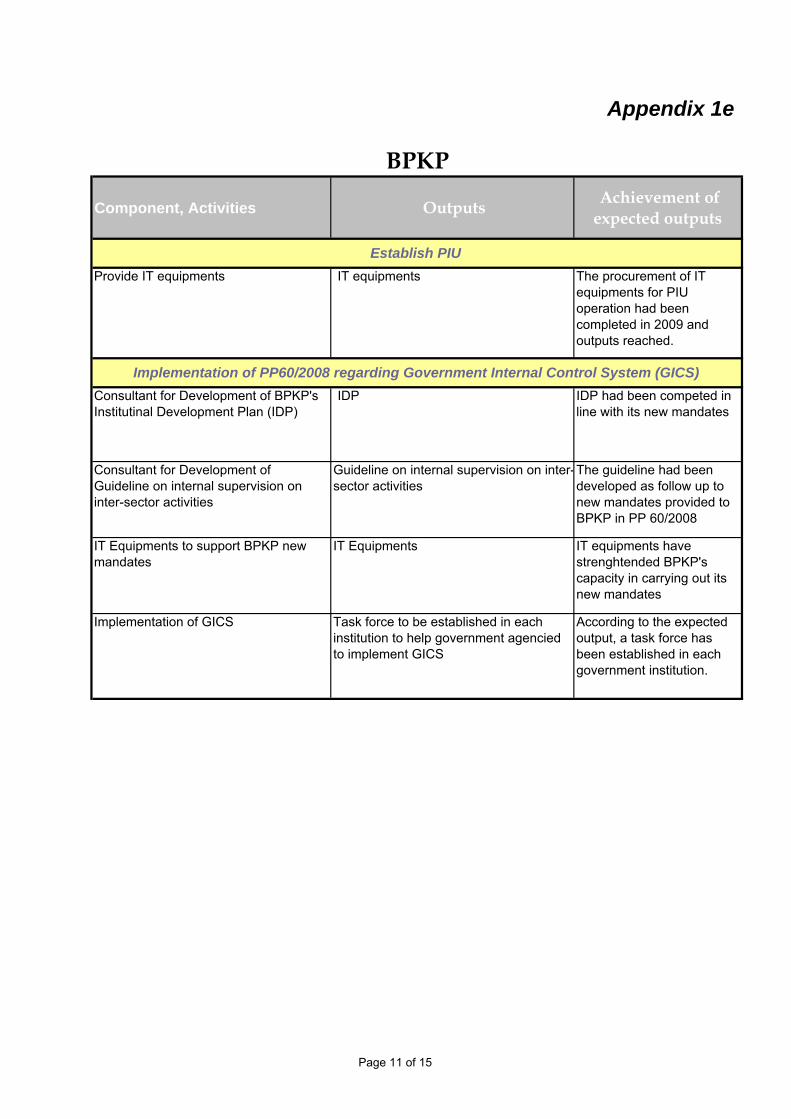

The main activities of BPKP as originally planned were to develop an Institutional Development Plan consistent with the new legal framework and introduce new work procedures into regular BPKP work practices. The long-anticipated legal framework, PP 60/2008 concerning implementation of Government Internal Control System, was issued in 2008. This regulation provides clear mandates for BPKP.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 13 ~

In order to support the implementation of BPKP’s mandates in the PP60/2008 according to articles 49 and 59, the following activities have been added: (i) Socialization and dissemination of PP60/2008 according to article 59 of the regulation to

ensure that related parties (government officials) are aware of the new law. (ii) Training on the implementation of government internal control system (GICS), which

includes development of technical guidelines, promotion and training of GICS, training and consultancy, capacity of state internal audit institutions as per article 59-c of the regulation.

(iii) Provide technical assistance for central and local government to assist them in GICS

implementation as per article 59-d of the regulation. (iv) Socialization of guidelines to support fungsi pengawasan internal (guidelines for internal

supervision) as per article 49 of the regulation. (v) The establishment of the Head of BPKP’s decree No. BPKP-1326/K/L/2009 dated 7

December 2009 regarding the guidelines on how to implement GICS as follow up to PP60/2008.

BPKP considers that in order to support implementation of BPKP’s mandates in the PP 60/2008, it has to improve the capacity of its human resources. Thus, BPKP has added activities, which include domestic and overseas training in several related audit topics, benchmarking several related professional auditor areas, international courses related to the capacity development of internal auditors, domestic technical training, comparative study in several related audit topics, domestic professional certification, and domestic training on IT development. In addition, BPKP will also procure IT equipments to equip its personnel in implementing the mandates.

All the activities added to the original plan are relevant and in line with ADB expectations, as they are supporting the implementation of the new regulation and improving the capacity of the entity. The outcomes and expected outcomes of these added activities are further described in Chapter 3.

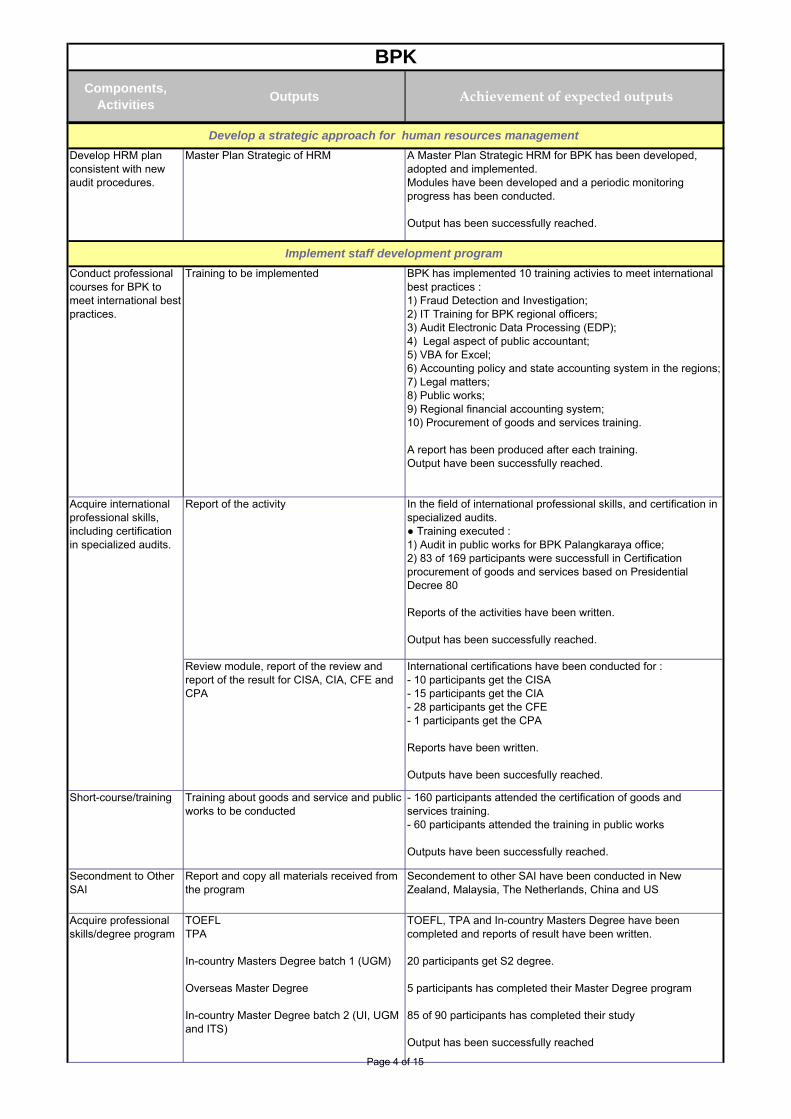

2.1.3 Designing a Professional Degree Education and Non-degree Education Program for Internal Auditors

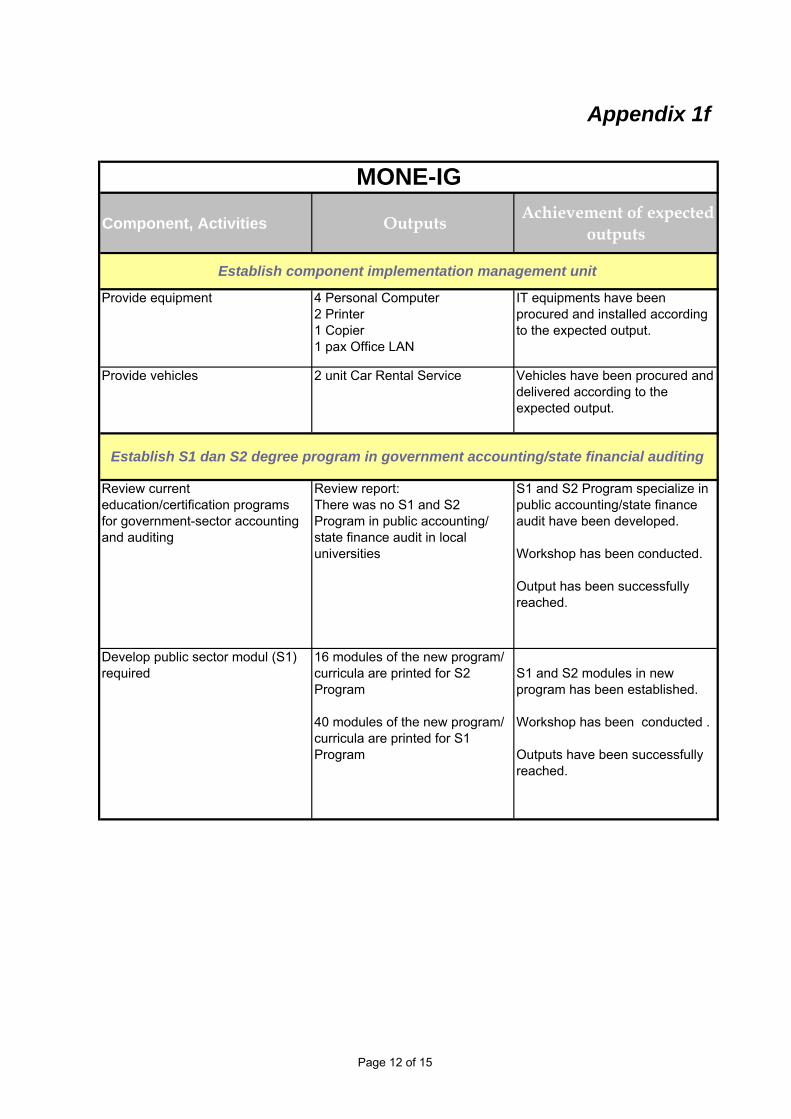

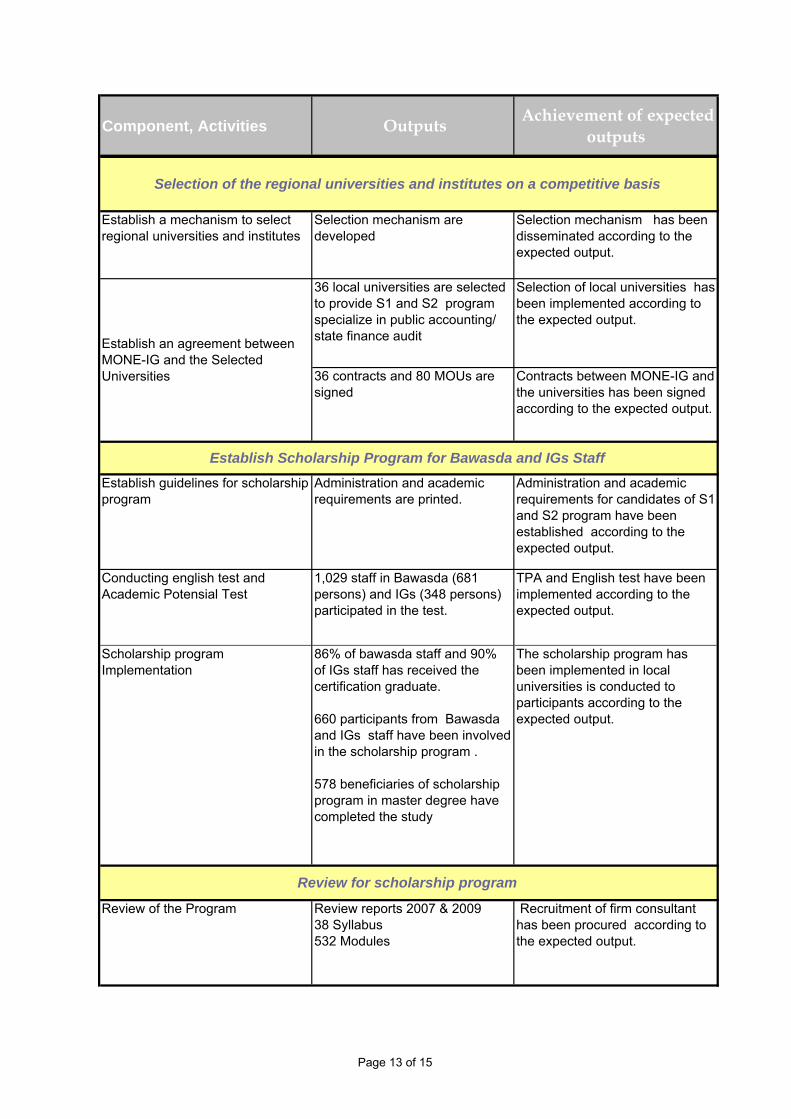

MONE-IG

The main activities of MONE-IG are related to the preparation of a degree education program in public accounting and auditing. The activities consist of reviewing the current education program for public sector auditing and accounting, developing new curricula for public sector auditing and accounting, implementing the new educational module through selected local universities, selecting candidates from IG and BAWASDA staff to participate in the scholarship supported program and evaluating the performance of the scholarship program.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 14 ~

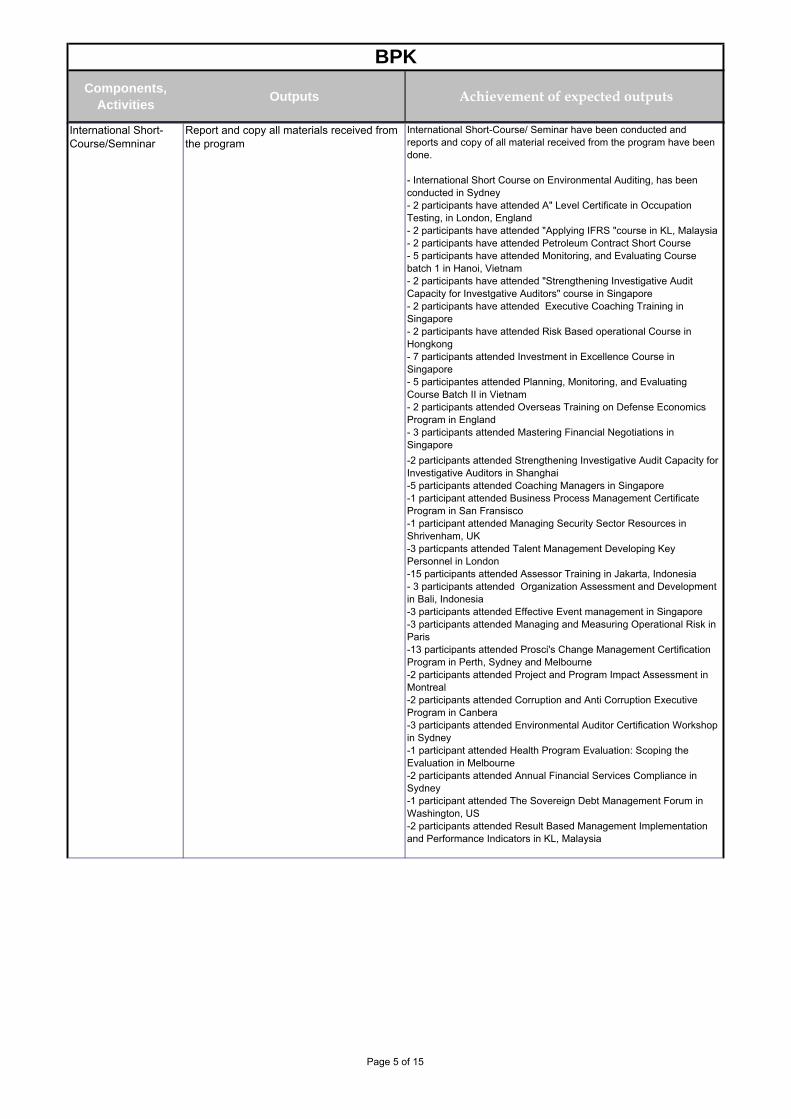

To ensure the successful implementation of the scholarship program, MONE-IG planned to hire an individual consultant for Quality Assurance to be in charge of conducting the survey in regard to the MONE-IG scholarship activities. However, MONE-IG was not able to find a consultant after two tenders, as the budget allocated to the assignment was too low and hence this activity has been carried out internally. There has been no impact on the relevance, as the review of the scholarship program has been conducted internally. In order to implement the scholarship program and to be more efficient, the local lecturers have been trained in Public Accounting and State Finance Audit, as lecturers in local universities lack skills in these fields. To improve the skills of internal auditors and reach international standards, international short-courses in IIA Australia and Netherlands have been scheduled. As the coordination between local government and local universities must be improved, as well as the contribution of local universities, MONE-IG has organized a workshop on coordination for updating the status of the scholarship program. These added activities are relevant to the objectives of STAR-SDP, as they support to develop skills and ensure a sound implementation of the scholarship program. The outcomes and expected outcomes of these added activities are further described in Chapter 3.

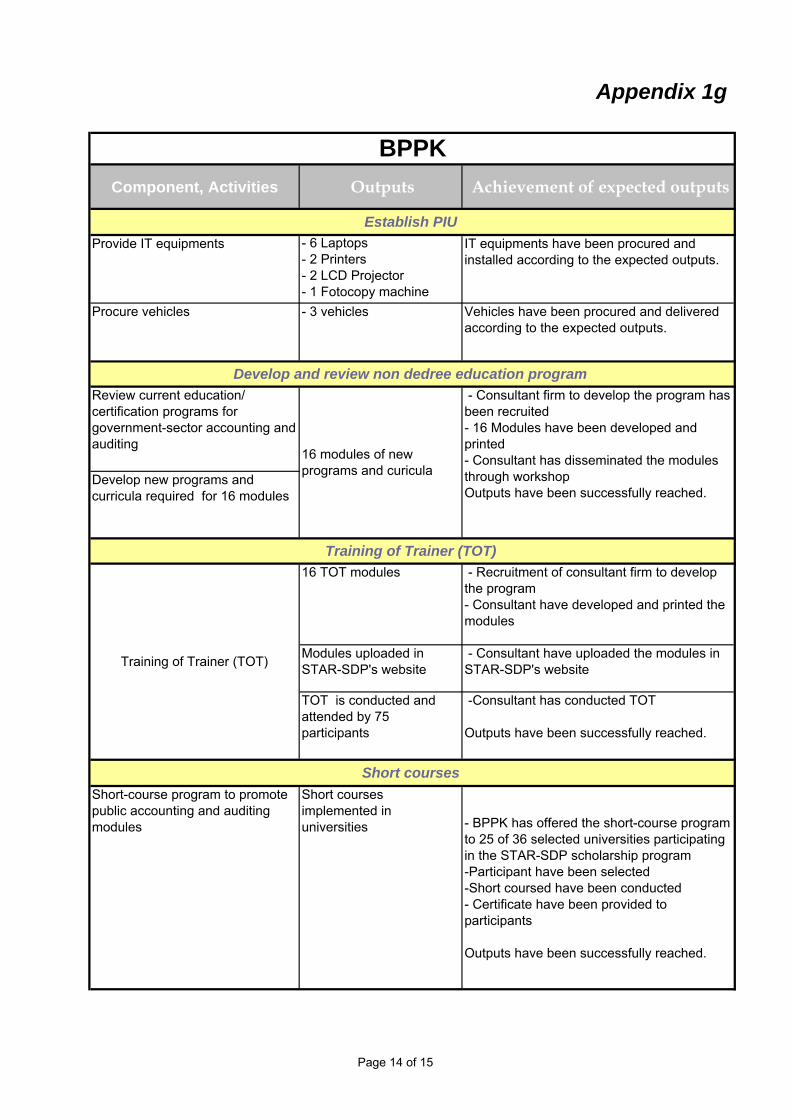

BPPK

According to the original plan, BPPK was only expected to review the current education/certification programs for government-sector accounting and auditing and subsequently develop the curriculum for a non-degree education program and the training modules for the program implementation. However, after completing development of the curriculum and modules, the Executing Agency and BPPK decided to extend the role of BPPK with implementation of short-course training to BAWASDA employees using the curriculum and modules previously developed. This additional activity is in line with the project expectation because it supports the capacity development of BAWASDA and utilizes the output of previous activity. Moreover, BPPK has solid experience in preparing and conducting training. The outcome of this added activity is further described in Chapter 3.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 15 ~

2.1.4 Introduction of New Practices for Parliamentary Oversight of Public Sector Audit

DPRD Secretariat

DPRD Secretariat has developed an Institution Development Plan (IDP) for their capacity building, which has enabled DPRD to implement the new practices in delivering BPK’s audit report to DPRD committees as originally planned.

DPR Secretariat

DPR Secretariat was expected to implement the introduction of new practices for parliamentary oversight of public sector audit. Accordingly, DPR Secretariat would develop user-friendly formats of BPK’s audit report to be followed up by Parliament. DPR Secretariat has continuously developed such formats and introduced these to Parliament. In addition, Parliament has been introduced to the importance of BPK’s report follow-up. As a result, members of Parliament are now aware of the importance of BPK’s audit findings follow-up, indicated by the establishment of the State Budget Accountability Body (Badan Akuntabilitas Keuangan Negara or BAKN) within DPR. The Board’s main task is to follow-up BPK’s audit findings. To improve the capacity of BAKN members, thus enabling them to carry out their duties, the DPR Secretariat had included a new activity, i.e. comparative study for the BAKN team with the Netherlands. This activity is in line with the expectations of ADB and DPR Secretariat’s expected outcomes. The outcome of this added activity is further described in Chapter 3.

2.1.5 ILMU

Bappenas as the Executing Agency established an Investment Loan Monitoring Unit (ILMU), the activities of which are to coordinate, control and monitor the activities of STAR-SDP within other PIUs. The detailed tasks of ILMU include preparing consolidated quarterly report from the PIUs, completing mid-term reviews, carrying out surveys, hiring external auditors for annual audits, preparing the project completion report, and supporting the administration of ILMU including office rental, office operations and other administration. Most of the detailed tasks have been carried out successfully as planned. However, development of mid-term review was not carried out due to still insignificant number of activities that have been implemented until mid 2007. This activity has been replaced by Development of project Assessment Report as of 31 December 2009. The cancellation of these activities had no impact on the relevance of the design as the activities have been implemented through other source, TA 4479.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 16 ~

Some activities were added to the initial work plan to optimize and complete the action of ILMU: (i) The development of a system on accountability improvement, which consists of creating a

web-based information system for accountability improvement on project implementation, (data storage software) and was added to simplify the transfer of documents between STAR-SDP stakeholders.

(ii) The development of performance evaluation indicators, which consist of the development

of a performance evaluation indicator report in order to provide indicators to evaluate the output of tasks in accordance with the national mid-term development plan.

(iii) The development of an institutional evaluation on public sector supervisory bodies to

evaluate the policies and the internal audit institutions prior to and after the issuance of PP60/2008, and to provide inputs for the development of the national mid-term development plan.

(iv) The development of a system for keeping archives. This activity was added to support the

compliance to the loan agreement, which requires for the project closing purposes to collect the data of the project.

(v) The recruitment of a consultant for implementation of a public campaign on the functions

of internal audit institutions. This activity is a continuation of the baseline survey conducted in 2008.

All these added activities reinforce the role of ILMU and are relevant to the ADB expectations, as they improve the project by adding relevant and useful activities. The outcomes and expected outcomes of these added activities are further described in Chapter 3.

2.2 PROJECT DISBURSEMENT

The accumulated disbursement of loan and grant as of December 31, 2010 was US$26.54 million or 88% of the total budget. The cumulative disbursements under the loan stood at about US$21.89 million or 87%. With regards to the US$ 5.0 million Dutch grant, US$4.65 million had been disbursed or 93% of the total grant.

2.3 PROJECT OUTPUTS

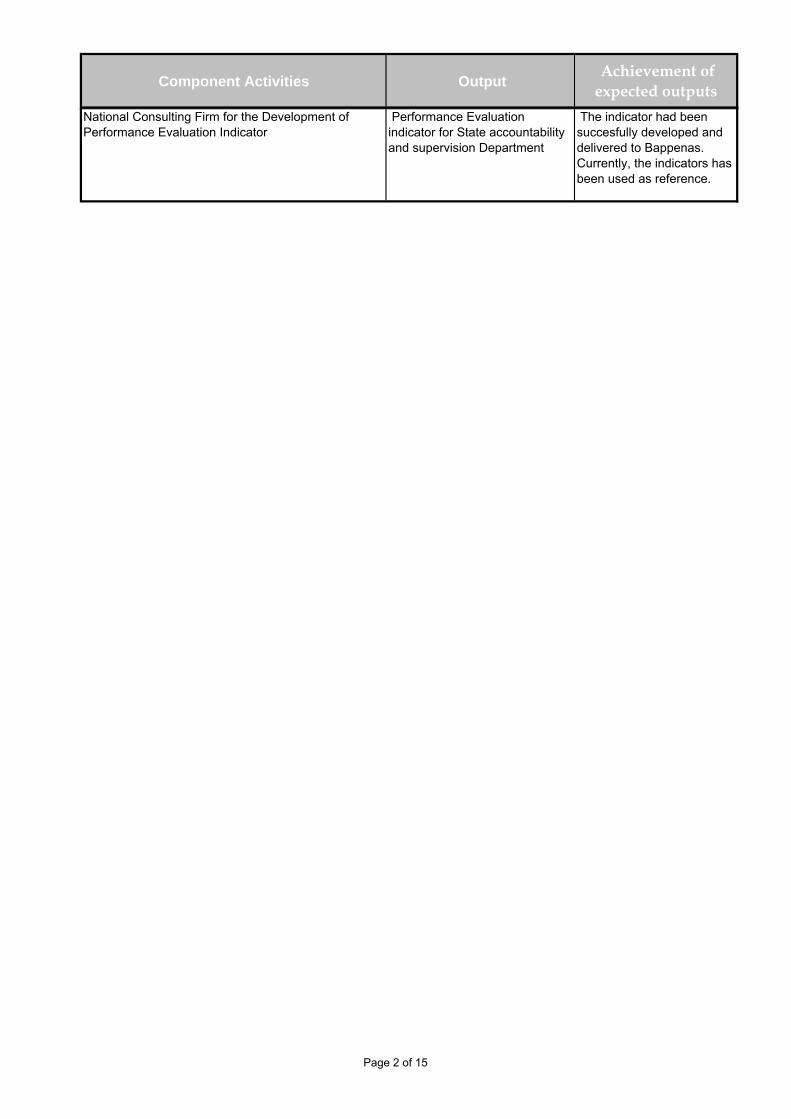

The project outputs are numerous and many activities have been already implemented by each PIU. Appendix 1 presents per PIU the different outputs and information on the extent to which the expected outputs were achieved for the completed activities. All the outputs achieved as at 31 December 2010 are in line with the deliverables expected at the beginning of the project. Although some activities have been postponed, creating a slippage in schedule, the results of the project in term of outputs is a success.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 17 ~

3. EVALUATION OF PROJECT PERFORMANCE

3.1 INTRODUCTION An effective state audit function is key to an effective and well functioning accountability framework for parliaments, the executive, the judiciary, and civil society. As part of the overall control of public sector management, the function provides an independent, objective, and professionally conducted assessment on the veracity, accuracy, credibility, and reliability of information on the economy, effectiveness, and efficiency of government. While Indonesia has had institutional arrangements for public sector audit since the early 1940s the legal, policy, and institutional frameworks have not been significantly evolved to promote transparency and accountability.

Firstly, a weak legal framework exacerbates the lack of clarity between internal and external audit functions. Secondly, the allocation of resources has not always been in line with policy and legal mandates. Thirdly, parliamentary oversight has been deficient. Fourthly, public awareness of the benefits of audit has been very low. Fifthly, capacity has been weak. Due to decentralization, the enormous transfer of resources has necessitated strengthening the regional audit institutions to effectively fulfill their internal control and audit functions.

3.2 EVALUATION OF PROJECT PERFORMANCE PER PROJECT IMPLEMENTATION UNIT (PIU) AND ACTIVITIES

3.2.1 BPK 3.2.1.1 Background

Since Indonesia’s independence in 1945 until about 2003, the management and audit policy of the State Finance in Indonesia still referred to the Dutch heritage system, the Indische Comptabiliteitswet (ICW) and the Instructie en voor de verdure bepalingen Algemeene Rekenkamer (IAR). During that period, it was difficult to create an atmosphere of fiscal accountability and transparency and as a result this had a negative impact on the performance of state finance audit performed by BPK. Some of the causes that led to the ineffectiveness of state finance at that time were largely due to the lack of clarity in the definition of state finance as BPK’s audit object; the lack of clarity in the separation of review and oversight functions between agencies including the purpose and scope of their duties; the absence of government accounting standards; the lack of clarity on the period for submission of the government report to BPK and the House of Representatives, as well as the BPK audit period; and the lack of clarity in the follow-up process and utilization of BPK’s audit findings by the Government and Parliament. In May 2002, the Minister of Finance of the Republic of Indonesia produced a White Paper entitled “Reform of Public Financial Management System in Indonesia, Principles and Strategy,” which was a response to improve state financial management, as well as to help restore the Indonesian economy that had collapsed due to the economic crisis in 1997. The first step to improve the

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 18 ~

management and financial accountability of the state finances was started by amending the Indonesian Constitution 1945. Within the framework of ensuring that the State Finance Management shall be carried out in a transparent and accountable manner for the welfare of the people, the 1945 Constitution of the Republic of Indonesia declares in Chapter 23E article (1) that the Audit Board of the Republic of Indonesia (BPK) is the external auditor and Indonesia’s Supreme Audit Institution (SAI):

“In order to audit the management and accountability concerning the state finances a Supreme Audit Institution shall be established.”

1945 Constitution of the Republic of Indonesia

The objectives of establishing BPK to audit state finances in accordance with the above statement are to achieve transparency and accountability in state financial management. Audit shall be carried out on all state financial matters, including all state revenues – either from tax or non-tax sources, all state assets, state receivables and liabilities, state treasury, and also the management of state expenditures.

Chapter 23E article (2) of the 1945 Constitution declares that the BPK’s audit result shall be handed to the House of Representatives (DPR), Regional Representative Councils (DPD) and Regional House of Representatives (DPRD), in accordance with each house’s respective line of authority. This declaration shall be carried out in order for each of the houses of representatives to be aware of how the Government is managing the state finances so that they can carry out their function of budgetary oversight. The amended Constitution provided clearer definition of BPK’s position, roles, authorities, and how to elect members of BPK’s Board. The State Finance Law (Law Number 17 Year 2003), passed in March 2003, details the entities over which BPK has audit jurisdiction. In all, about 10,000 auditable entities are spread across the country, including Parliament, the Supreme Court, 70 Government departments and agencies, some 480 regional governments and as many regional parliaments, Central Bank and approximately 8,500 central and regional state-owned enterprises. Issuance of Law Number 15 Year 2006 concerning the State Audit Board, provides a mandate to BPK to audit Central and Regional Government, other State Institutions, Central Bank of Indonesia (Bank Indonesia), State Owned Enterprises, Regionally Owned Enterprises, Public Service Agencies, Foundations, Institutions or other Agencies required due to the nature of their respective duties. Thus, in order to enforce its constitutional mandate under the Law Number 15 Year 2006, BPK needs to expand and improve its institutional capacity. As part of the state financial reform initiative package, in October 2004 the government of Indonesia approved the start of Project-STAR-SDP to support the state audit reform. The purpose of this project is to strengthen the coordination and development of public sector audit.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 19 ~

3.2.1.2 Issues The primary issues:

Some audits and the resultant audit reports lacked quality. Some audit reports did not comply with a model comprising best practices and related audit report standards, reflecting on the internal systems in place to ensure quality audits and quality audit reports. Audit managers and auditors in charge, rather than organization officials such as the chairmen or other officials sign reports. BPK, as the Supreme Audit Institution of Indonesia, notwithstanding some direct help from external funding agencies, has insufficient numbers of qualified audit staff to carry out its mandate as stated above, particularly those required to carry out the various specialized audits now considered integral to effective auditing. In 2004, BPK could only audit 12% of the entities from its estimated audit universe and, in particular, only 30% of the regional governments. A weak BPK, particularly one with little regional presence, leaves the public sector without an effective external auditor.

Moreover, BPK could not meet the State Finances Law requirement that states by 2007, the financial accountability statements of some 480 regional governments have to be audited within 6 months of the end of the financial year. Given the significant resource transfers after decentralization, this weak fiduciary environment needs to be urgently addressed. The oversight issues:

Parliament does not usually receive or have regular access to individual BPK audit reports, and even when they do, Parliament receives only summaries of edited versions of individual reports. Line Ministries appear to have no legislated obligation to address issues raised in audit reports. According to new laws and regulations, Regional Parliaments have the right to approve the audited annual accountability report of the Head of Local Government. However, in the main they do not have the skills to carry out this oversight function. Types of audit issues: Too few types of audits are conducted. Financial audits comprise the vast majority, with performance audits making up most of the remainder. Other types of audits such as forensic, contract, compliance, program, computer, public debt, environmental, export/import, policy, and privatization audits are rarely if ever conducted. Recruiting issues: Recruiting requirements that limit hiring accountants and exclude multi-disciplinary candidates may be impeding expansion of the nature and types of audits that can be conducted. Training issues: Training has not been adequate to increase performance audits and/or the variety of types of audits that could be conducted. Training has not kept pace with the movement to increase use of

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 20 ~

computerization and enhanced information technology. Training has been unable to correct deficient audit and report quality or to strengthen the internal quality assurance system. Computerization and enhanced IT issues: Audit follow-up may be limited because the system does not adequately track audit recommendations so that they can be followed up. Substantive follow-up on fraud cases referred to the Attorney General’s Office is lacking and does not result in an affirmative prosecutorial action. An electronic system for tracking compliance with continuing professional education requirements is still under development, and responsibility for managing the system has yet to be decided.

3.2.1.3 Objectives

It is expected that the STAR-SDP activities carried out in BPK will support development of new systems and work procedures for BPK that would be consistent with an enhanced legal and regulatory framework. The activities shall also provide support for: (i) enhancing audit planning and management; revising the code of ethics; training for risk-based auditing procedures; undertaking specialized audits; presenting audit reports; (ii) managing human resources, including implementing a strategic human resources development program; (iii) enhancing IT management, including establishing an extensive IT policy and providing IT equipment; introducing a strategic approach for information resources management and undertaking testing for practical applicability of procedures; computers and equipment to utilize IT-based audit techniques shall also be provided; and (iv) developing a model public relations program, implementing a program for raising public awareness, and gaining public support for an effective public sector audit function.

Source: STAR-SDP Loan Agreement 3.2.1.4 Assessment of Performances

Develop and Print Auditing Standards From 1995 until 2006, BPK had used the Government Audit Standard (Standar Audit Pemerintahan, SAP) as guidance for its operation and duties. In line with the state financial reform initiative and in consideration of the development of audit theory, the people’s dynamics that requires the application of good governance principles, which stresses on the issues of transparency and accountability, and in particular to meet the requirements as stated in Chapter 5 of Law No.15 Year 2004 concerning State Finance Accountability and Management Audit and Chapter 9 article (1) letter e of Law No.15 Year 2006 concerning Finance Audit Board (BPK), BPK has to revise and enhance the SAP 1995. Support for the development of the new Auditing Standards by STAR-SDP began in 2005 and was completed by January 2007 through the assistance of two International Consultants (Mr. Jan Van Dam and Mr. Terry McLaughlin) and a Team of Domestic Auditing Standards (Center for Development of Accounting – University of Indonesia). The process of producing the new audit standard comprised of preparation on review of the draft by the BPK revision team, evaluation of the revision draft by the STAR-SDP consultants, consultation and discussion with government,

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 21 ~

academics, and practitioners, exposure to the BPK Board Meeting to gain approval and feedback, and finally a public hearing (assisted by PT. Yurindo Utama) to obtain final input and feedback from the public. The project also funded the printing of the new auditing standard for distribution. After the New Auditing Standard was approved by BPK’s Board in January 2007, BPK issued Regulation 1 Year 2007 concerning the State Finance Audit Standard (Standar Pemeriksaan Keuangan Negara, SPKN) and with that the State Finance Audit Standard (SPKN) was formally implemented and is in full force for audits carried out from FY2008. The changes that SPKN has covered that were specified in Law 15 Year 2004 and Law 15 Year 2006 among others were the type of audits, audit standards, implementation and reporting of audit results, and observation of audit result follow-up by auditee. SPKN lays down the professional requirements for auditors, audit quality and audit reports. Audits carried out based on the SPKN have enhanced the credibility of information that is reported or obtained from the entity that is being audited because the collection and evidence-testing is carried out objectively. The SPKN also provides clear methodology and audit standard of procedures for auditors to carry out three types of audits: financial audit, performance audit, and special purpose audit. Therefore, external auditors now have a clear reference to carry out state finance accountability and management audit. The methodology and approaches defined in the SPKN are also compliant to international standard as development of the SPKN, referring to among others the Generally Accepted Auditing Standards United States General Accounting Office (US GAO), the Auditing Standards of International Organization of Supreme Audit Institutions (INTOSAI), the Generally Accepted Auditing Standards AICPA 2002, and the Standards for the Professional Practice of Internal Auditing 2003. Development of SPKN clearly has met one of the objectives, which are for it to be a reference to quality audit for auditors and auditing institutions in carrying out audit on state finance accountability and management. The establishment of the State Finance Audit Standard has initiated further development of audit guidelines that are useful to BPK’s auditors. Development of the Audit Management Guideline (Panduan Manajemen Pemeriksaan, PMP) in 2008, which is a revision of SAP 2002, has provided BPK with standardized audit procedures, forms, notes, and reports that will be used for preparing Audit Work Plan (RKP), audit planning, audit implementation, audit reporting, and observation of audit result follow-up, audit evaluation, and references related to state finance accountability and management audit. The audit procedures guideline provided by PMP is linked to each stage of audit as follows: the audit planning phase, the audit execution phase, the reporting phase, and the monitoring and evaluation phase. Audit implementation using a combination of SPKN, PMP and BPK’s Code of Ethics has ensured that the audit carried out shall be well managed, strictly controlled, properly guided, and using standardized procedures for each of the three types of audit, as well as for each phases of audit. Highlight of achievements: In order for BPK to optimally carry out its task and mandates in promoting transparency and accountability of state finance in consideration of its limited human resources and budget but also taking into account the large number of objects to be audited, BPK needs a well structured audit strategy based on scale of priority. BPK uses audit priority as follows: Firstly, audit of financial statements that have to be carried out routinely every year. Secondly, audit of state revenues and expenditures both at central and local levels. Thirdly, audit

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 22 ~

of state expenditures that are susceptible to corruption, such as procurement of goods and services. Fourthly, audit of strategic sectors in the economy and those that would affect a large number of people.

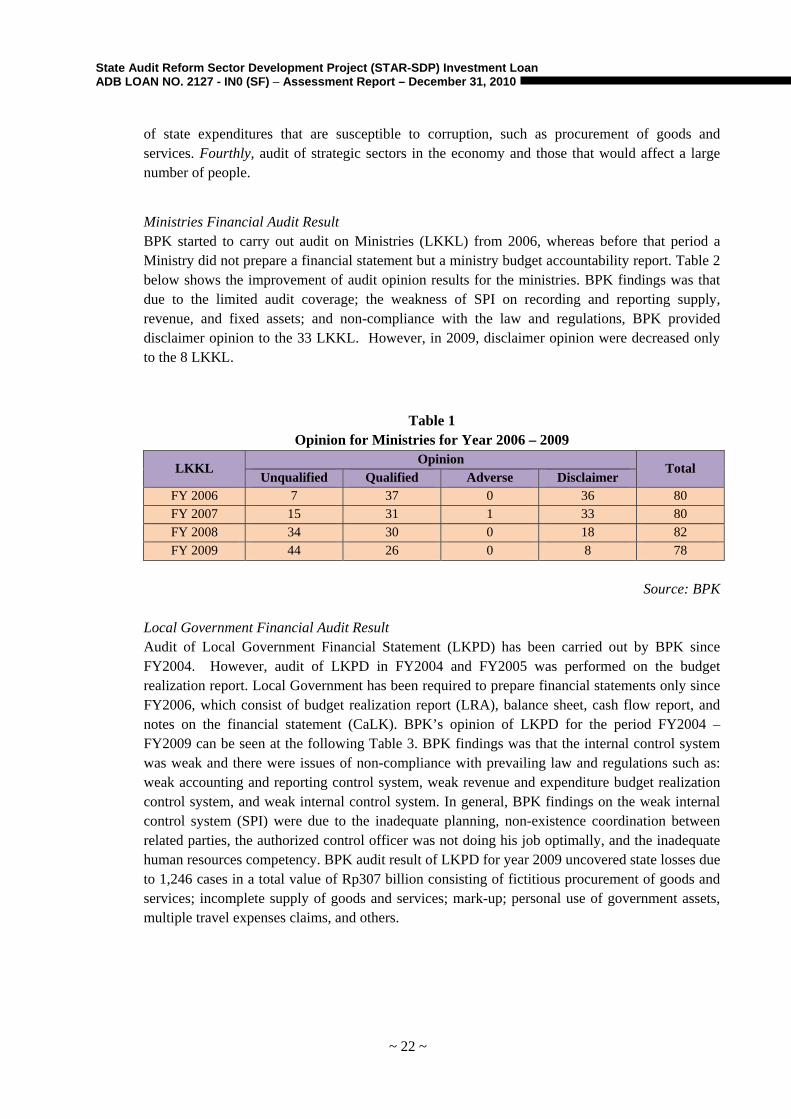

Ministries Financial Audit Result BPK started to carry out audit on Ministries (LKKL) from 2006, whereas before that period a Ministry did not prepare a financial statement but a ministry budget accountability report. Table 2 below shows the improvement of audit opinion results for the ministries. BPK findings was that due to the limited audit coverage; the weakness of SPI on recording and reporting supply, revenue, and fixed assets; and non-compliance with the law and regulations, BPK provided disclaimer opinion to the 33 LKKL. However, in 2009, disclaimer opinion were decreased only to the 8 LKKL.

Local Government Financial Audit Result Audit of Local Government Financial Statement (LKPD) has been carried out by BPK since FY2004. However, audit of LKPD in FY2004 and FY2005 was performed on the budget realization report. Local Government has been required to prepare financial statements only since FY2006, which consist of budget realization report (LRA), balance sheet, cash flow report, and notes on the financial statement (CaLK). BPK’s opinion of LKPD for the period FY2004 – FY2009 can be seen at the following Table 3. BPK findings was that the internal control system was weak and there were issues of non-compliance with prevailing law and regulations such as: weak accounting and reporting control system, weak revenue and expenditure budget realization control system, and weak internal control system. In general, BPK findings on the weak internal control system (SPI) were due to the inadequate planning, non-existence coordination between related parties, the authorized control officer was not doing his job optimally, and the inadequate human resources competency. BPK audit result of LKPD for year 2009 uncovered state losses due to 1,246 cases in a total value of Rp307 billion consisting of fictitious procurement of goods and services; incomplete supply of goods and services; mark-up; personal use of government assets, multiple travel expenses claims, and others.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 23 ~

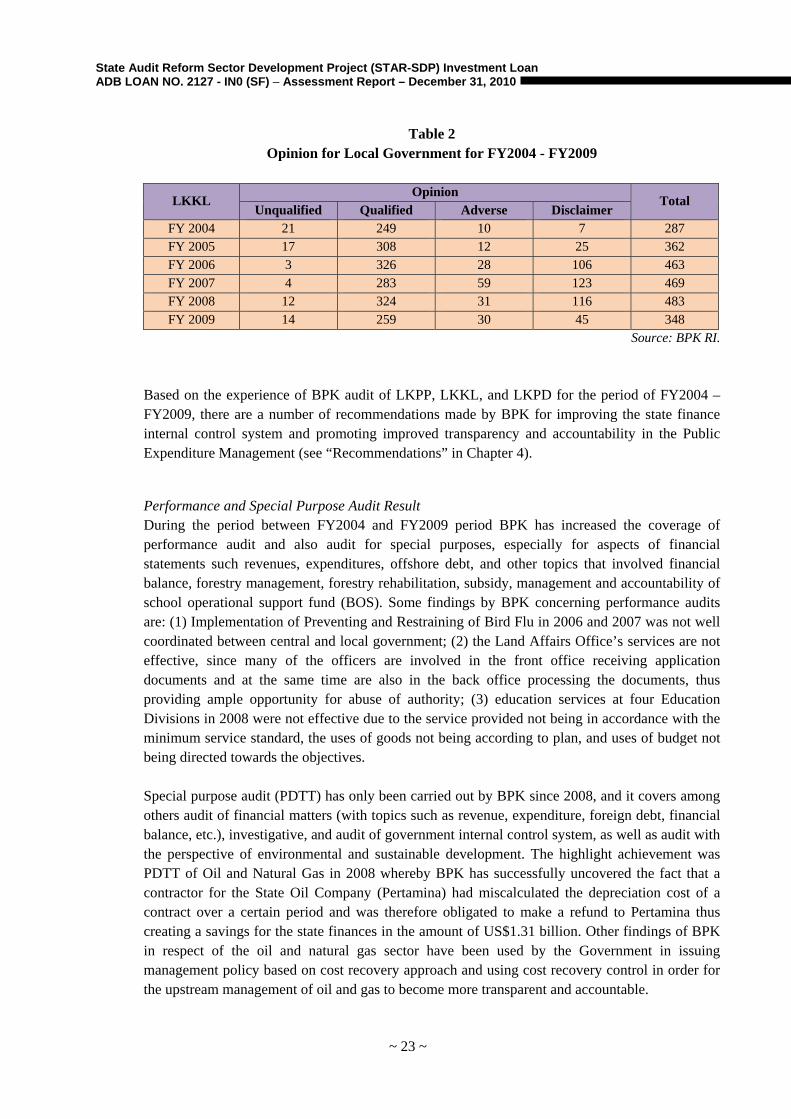

Table 2 Opinion for Local Government for FY2004 - FY2009

Source: BPK RI. Based on the experience of BPK audit of LKPP, LKKL, and LKPD for the period of FY2004 – FY2009, there are a number of recommendations made by BPK for improving the state finance internal control system and promoting improved transparency and accountability in the Public Expenditure Management (see “Recommendations” in Chapter 4).

Performance and Special Purpose Audit Result During the period between FY2004 and FY2009 period BPK has increased the coverage of performance audit and also audit for special purposes, especially for aspects of financial statements such revenues, expenditures, offshore debt, and other topics that involved financial balance, forestry management, forestry rehabilitation, subsidy, management and accountability of school operational support fund (BOS). Some findings by BPK concerning performance audits are: (1) Implementation of Preventing and Restraining of Bird Flu in 2006 and 2007 was not well coordinated between central and local government; (2) the Land Affairs Office’s services are not effective, since many of the officers are involved in the front office receiving application documents and at the same time are also in the back office processing the documents, thus providing ample opportunity for abuse of authority; (3) education services at four Education Divisions in 2008 were not effective due to the service provided not being in accordance with the minimum service standard, the uses of goods not being according to plan, and uses of budget not being directed towards the objectives. Special purpose audit (PDTT) has only been carried out by BPK since 2008, and it covers among others audit of financial matters (with topics such as revenue, expenditure, foreign debt, financial balance, etc.), investigative, and audit of government internal control system, as well as audit with the perspective of environmental and sustainable development. The highlight achievement was PDTT of Oil and Natural Gas in 2008 whereby BPK has successfully uncovered the fact that a contractor for the State Oil Company (Pertamina) had miscalculated the depreciation cost of a contract over a certain period and was therefore obligated to make a refund to Pertamina thus creating a savings for the state finances in the amount of US$1.31 billion. Other findings of BPK in respect of the oil and natural gas sector have been used by the Government in issuing management policy based on cost recovery approach and using cost recovery control in order for the upstream management of oil and gas to become more transparent and accountable.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 24 ~

In connection with Law No. 15 Year 2004 and Law No.15 Year 2006, BPK has achieved the establishment of better cooperation with Public Accountant Firms (KAP) and has issued BPK Decree No.10/K/I-XIII.2/7/2008 concerning Requirements of Public Accountants and Public Accountant Firms for carrying out state finance audit. As of August 2009, there were already 109 KAP and 340 auditors that have been registered and published on BPK’s website. The KAP and registered auditors have eased the burden of BPK to a degree, as they have been carrying out external audit on financial statements of State Owned Enterprises (BUMN), Local Government Owned Enterprises (BUMD) and Public Service Institutions (BLU) since 2008. Outcome: The development and implementation of the State Finance Audit Standard, the Audit Management Guideline, the Audit Guidelines (for Financial Audit, Performance Audit, and Special Purpose Audit) and other Technical Audit Guidelines have significantly improved the performance and quality of BPK audit. Since the audit reform has started, BPK has successfully increased its audit coverage in the performance audit, special topic audits such as in foreign debts, fiscal balance, implementation of subsidy, and a number of high profile audits. Currently, BPK’s audit quality has earned more recognition from the public, as well as from the international circle as reflected in the peer review report carried out by The Netherlands Court of Audit in July 2009, which stated the following conclusions and recommendations:

• The manuals for financial audit, performance audit and special purpose audit are appropriate and explain the different types of audit. They define general principles and set more specific criteria and approaches for the phases in the audit process (planning, fieldwork, reporting, follow-up and evaluation). The audit methodology has been compared with international auditing standards and it has been concluded that it was compliant;

• The general approach to financial audit complies with international standards;

• The performance audit manual complies with international standards, but there is some room for improvement to make it more useful to the auditors;

• BPK's Board approved the special purpose audit manual in February 2009. The manual complies with international standards. However, it does not adequately clarify what type of audit should be used when or the procedural differences between the three types of special purpose audit.

Source: Peer Review by NCA

Increase Oversight Effectiveness of BPK Board - Acquire Experience from Other SAIs

From FY2006 through FY2009, and supported by STAR-SDP, BPK has carried out comparative study activities at other Supreme Audit Institutions in order to increase the oversight effectiveness of the BPK Board. BPK’s activities covered: The comparative study at US GAO and OAG Canada in FY2006 provided knowledge and experience in Human Resources Management, Research and Development, Training Center, IT Audit and International Relations.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 25 ~

The comparative study at Auditor-General New Zealand in FY2006 provided an opportunity to enhance oversight effectiveness of the BPK Board through acquiring knowledge on Quality Assurance of Audit, Information Technology, Local Government Audit, and Human Resources Management. The comparative study at SAI Germany and France in FY2007 focused on obtaining knowledge and experience on Organizational Issues, Human Resources Management, Education and Training, Research and Development, Information Technology, Internal and External Relationships, and Auditing. The comparative study at SAI India in FY2008 covered knowledge and lessons learned in Utilization of Information Technology in Audit Implementation in India, Roles of SAI in Corruption Eradication Efforts in India, Assessment Centers at CAG India, which are used to assess the performance of the auditors, Standard Operating Procedures (SOP) applicable to CAG India, Manual / guidelines used in audits, and Quality Assurance System applied at CAG India. The objectives of the comparative studies were to obtain knowledge, experience and sound lessons learned from the other SAI so that BPK-RI has the capacity to:

• Enhance the quality of audit by improving the audit planning process, implementation and reporting phases, and better application of information technology in supporting the auditor in carrying out the audit, as well as making for easier handling of the monitoring and supervision efforts by the managers;

• Identify policies, tasks, functions, methods, facilities and infrastructure available in INTOSAI members that could be implemented in BPK-RI;

• Improve utilization of information technology for supporting the implementation of performance audit, financial audit, compliance audit, and managing quality assurance.

Highlight of achievements: As a result of these comparative study activities, BPK is currently actively involved in several committees, working group, task force of International Organization of Supreme Audit Institutions (INTOSAI) and Asian Organization of Supreme Audit Institutions (ASOSAI). BPK involvement in the international institution circle is in order to improve its audit performance, organization and human resources quality. BPK also has bilateral cooperation with several other SAI in order to strengthen, enhance, and develop the framework for cooperation based on mutual beneficial relationships between the SAIs in the field of public sector audits. As of December 2009, BPK has signed 13 MOU with other foreign SAI for improving institutional capacity and human resources capability. BPK has been involved in the Working Group on Environmental Audit (WGEA), as a member of the steering committee in 2004 and since then being responsible for preparing a Guidance Material on Auditing Forestry, and BPK was actively involved in the preparation of Guidance Material on Auditing Mining & Minerals, Auditing Fisheries, and Auditing Climate Change. BPK hosted the 8th WGEA meeting in August 2009 in Ubud, Bali. The outcome of this activity has been the improvement of BPK in carrying out environmental audit as shown by one example of the findings of BPK special purpose audits between 2006 – 2007 on the Department of Energy

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 26 ~

and Minerals Resources (ESDM), 4 provinces, 28 local governments, 1358 holders of Mining License, 40 contractors, and related institutions: from the concession provided by the Department ESDM to 3 contractors and one holder of KP concerning a total land area of 238,962 Ha it was found that 98,548 Ha was in Kutai National Park, and 130.82Ha was in protected forest in the East Kutai region. Sixteen heads of local government in South, Central, and East Kalimantan and South Sumatra provided concessions of 1,757,477 Ha of land, whereas 1,209,712Ha was in production forest, protected forest and conservation forest. Moreover, BPK has also taken six initiatives beyond the call of duty that have had an effect on executives and legislatives: extending the audit objects, both from the revenue side and state expenditure side; requiring auditee to hand in their management representation letter; requesting auditee to prepare action plan for improving the opinion of financial report audit; assisting government entity in the implementation of their action plan, including to overcome the scarcity of human resources with knowledge in accounting and financial management; structural reorganization of State Owned Enterprises (BUMN), Local Government Owned Enterprises (BUMD), and Public Services Institution (BLU) so that they are managed in a more corporate manner and become sustainable; and suggesting to the House of Representatives (DPR), Regional Board of Representatives (DPD), and Regional House of Representatives (DPRD) to establish a Public Accountability Board (PAP). As a result to the six initiatives since year 2008 there have been signs of positive improvements in the state finance system: (1) significant number of government institutions at central and regional level have provided action plans to BPK for the improvement on their financial audit opinion; (2) increased improvement has been noted on financial statement audit opinion of government institutions, including for large ministries such as Ministry of Industry, Ministry of Finance, Ministry of Defense, Ministry of Agriculture, and Ministry of Education; (3) there has also been notable improvement in local government financial statements audit opinion between 2006 and 2008; (4) legislative institutions have also met BPK’s recommendations to establish a State Finance Accountability Board through Law No. 27 Year 2009 concerning MPR, DPR, DPD and DPRD; and finally the Directorate General of Tax has become more cooperative in being audited by BPK. Outcome: As a result of the number of comparative studies carried out by BPK under -STAR-SDP support the leadership and direction from BPK’s Board have been improved. BPK’s Board has broadened the coverage of audit objects, issued direction to increase the number of performance audits, provided more and more advisory services, and boldly carried out a number of high profile audits. Clearly all of these initiatives show that the oversight effectiveness of BPK Board has improved.

Adjust BPK Code of Ethics to be Consistent with International Standards

Through this STAR-SDP activity, Domestic Consultants (Sukrisno Agus and Dwi Andayani Budi Setyowati) were contracted in June 2006 to assist BPK in developing a new code of ethics. The consultants reviewed the draft of the new code of ethics prepared by the BPK’s drafting team and provided feedback and recommendations. As of August 2007, BPK supported by the consultants has successfully developed a comprehensive New Code of Ethics for the Board members and

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 27 ~

auditors. Embedded in the code of ethics are the three basic elements of independence, integrity, and professionalism. These three elements shall be the basis for regulating the attitude of BPK’s staff and auditors in carrying out their jobs for the sake of upholding the prestige, honor, image, and credibility of the institution. The code of ethics also includes the mechanism for the enforcement of the code of ethics, as well as the type of sanctions. Enforcement of the Code of Ethics received serious attention from the Board of BPK because the position of state finance auditors is a profession that is most susceptible to issues such as abuse of authority and conflict of interest. Therefore, BPK has established an Honorary Council of Code of Ethics (consisting of three BPK officers and two academics) to enforce the Code of Ethics. BPK has also taken the initiative of properly disseminating the Code of Ethics among the management and professional staff to ensure that all of its auditors are familiar with the values and principles. For example, in order to ensure independency in carrying out an audit the auditor is prohibited from: (1) being submissive to intimidation or pressure from another party; (2) leaking any information of the auditee, and; (3) being influenced by prejudice, interpretation or other interest, be this the auditor’s personally or another party’s interest in the audit result. Furthermore, in accordance with the new Code of Ethics in every audit engagement, the auditors must sign a statement of independence to ensure the state of independence from the entities to be audited.

A peer review carried out by the Netherlands Court of Audit recommended that in order to keep the Code of Ethics alive, BPK should periodically reiterate its values and principles in various ways for both newcomers and established employees and for both senior and junior staff. Furthermore, the peer review team recommended that in addition to the Code of Ethics, a self-assessment method for SAIs could improve awareness among BPK’s personnel of risks to their own integrity. Outcome: The development and enforcement of BPK’s Code of Ethics has provided BPK auditors with a high standard of self-esteem, respect, image, and credibility in carrying out their duties. Such outcomes can certainly be enhanced if BPK diligently follows-up the recommendations provided by the NCA peer-review.

Develop New Techniques for Presenting Audit Reports A domestic consultant (PPA Economic Faculty of University of Indonesia) was contracted in May 2007 and started work in June 2007 to develop new techniques for presenting BPK-RI audit reports. After a draft was developed by the consultant, a workshop and afterwards simulated tests were carried out by the consultant for every type of audit before the techniques were tested on a selected pilot-project. A final workshop was organized to validate the draft manual based on the pilot-project results. Final drafting of the Techniques and Procedures Manual for BPK Audit Reports was completed by taking into account BPK feedback and recommendations. The final draft manual was presented to the BPK Board in February 2008 to obtain its approval.

State Audit Reform Sector Development Project (STAR-SDP) Investment Loan ADB LOAN NO. 2127 - IN0 (SF) – Assessment Report – December 31, 2010

~ 28 ~

According to the assessment made by The Netherlands Court of Audit, the BPK Audit Reports were very long, contained many findings and referred in most cases to shortcomings only and not to causes and effects. Because some financial audit objectives can be defined as performance audit objectives, the review team suggested that when BPK auditors are assessing an internal control system and compliance with laws and regulations, for example, the BPK auditors have already partly assessed in some aspects the performance audit domain.

“To increase the effectiveness of BPK reports, it was recommended that BPK reports should be more concise with a strong focus on causes, effects and solutions and not merely on findings. Furthermore, BPK should make an effort to enhance the attractiveness of its reports by using communication experts and more visualizations to present its analysis and conclusions”.

Netherlands Court of Audits Peer Review July 2009 Outcome: Currently BPK’s audit reports are better understood and used more by its stakeholders especially by DPR and DPRD.

Develop Improved Methods for Assessing the Use of New Standards and Procedures (Quality Assurance)

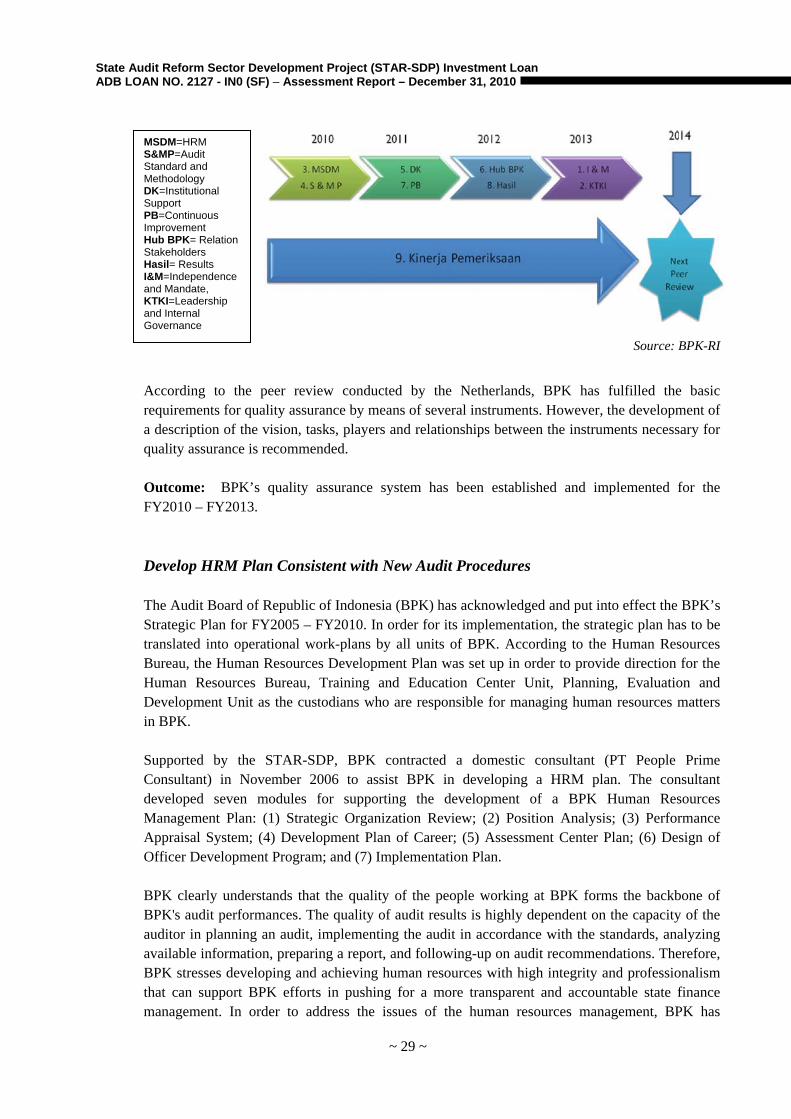

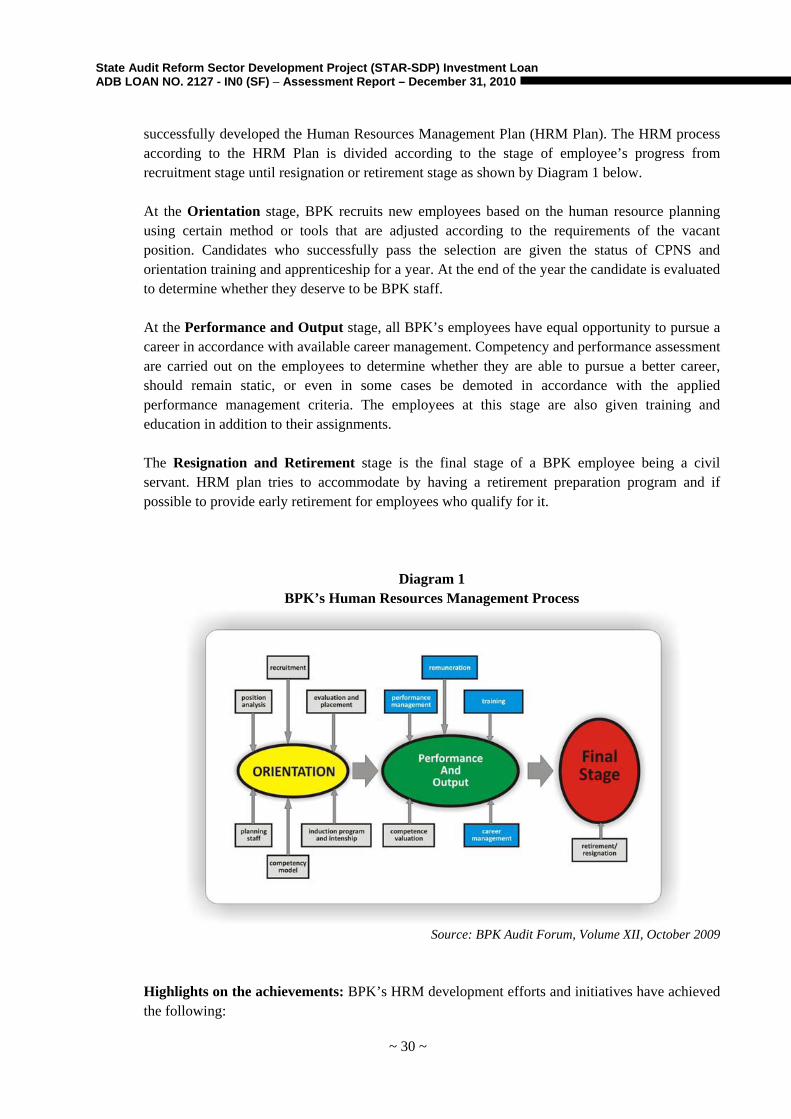

A domestic consultant (Public Accountant Office of Kosasih and Nurdiyaman) was contracted in May 2007 to assist BPK in developing a quality assurance system. The consultant developed the first draft of new standards and procedures in quality assurance based on the analysis of five Supreme Audit Institutions practices. After the draft of Quality Assurance Guideline was discussed with BPK and tested on a pilot basis, a final version was prepared and presented to the BPK Board to obtain their final approval. In order to ensure the quality of state finance audit, BPK established and implemented the Quality Control System (Sistim Pengendalian Mutu, SPM). The SPM is an important element to achieve reliable assurance in that an audit is in compliance with prevailing laws and regulations, as well as the BPK Audit Guidelines. SPM, which supports quality of an audit consists of nine elements: (1) Independence and Mandate; (2) Leadership and Self-governance; (3) Management of Human Resources; (4) Audit Standard and Methodology; (5) Institutional Support; (6) Relations with Stakeholders; (7) Continuous Improvement; (8) Results, and; (9) Audit Performances.