8

State of Grocery July 2017 - June 2018

State of Grocery July 2017 - June 2018

2© 2018 1010data Inc.

It’s hard to believe that it’s been a year since Amazon acquired Whole Foods. Grocery retailers are still feeling the aftershocks of this game-changing announcement as new entrants to the grocery industry enter from all fronts. First, activity like Target acquiring Shipt have blurred the lines between traditional retail and grocery, adding pressure to traditional grocers to compete with “one-stop” shopping options. Plus, there’s increased competition from European grocery leaders. Lidl entered the US market last year and Aldi has continued to expand their footprint. Both grocers are known for their breadth of affordable and high-quality private label products that consumers are seeking out more and more. And yet what’s most concerning is the rise of online delivery options. Falling behind in this channel is what should be keeping most grocers up at night. While many still think that customers prefer to shop at the last minute and like to pick out their own food, a rising number of consumers are preferring the convenience that delivery options provide.

Staying on top of this amorphous market is essential for anyone looking to compete and succeed for the highest share of consumers’ stomachs. Looking back on this industry-defying year, 1010reveal analyzed the current state of grocery to deliver a view of the industry’s biggest disruptors and emerging consumer trends.

3© 2018 1010data Inc.

Rise of Online Grocery

Online grocery has expanded immensely in the past few years. Legacy pure-play delivery companies, such as Peapod and FreshDirect, are being outpaced by delivery aggregators, such as Instacart and Shipt, which let the consumer chose their grocer. And now mass merchants, like Walmart and Amazon, are making strides in this space by offering delivery and click-and-collect options to consumers nationwide. 1010reveal demonstrates that online grocery sales are growing at 75% year over year and is becoming a larger piece of consumers’ wallets. Of those who made an online grocery purchase this past year, 32% of their grocery spend was made with online grocery retailers, up from 29% the year prior. This translates to an $83 increase in yearly online grocery spend from those consumers. In fact, the number of US consumers using online grocery services is up 59% in the past year. 9% of consumers have shopped for groceries online, a percentage that will only continue to grow.

Online Grocery’s Market Leader

The 5th Annual Alphawise Food Retail Survey found that 56% of consumers that are most likely to order groceries online in the next six months said that Amazon would be their retailer of choice. However, purchase behavior from 1010reveal Merchant Insights indicates otherwise. Of the seven top online grocery providers, 35% of sales came from Walmart Grocery in the past year, while AmazonFresh comprised just 8%. Plus, Walmart Grocery is the fastest growing online provider, up 143% year over year. AmazonFresh had healthy growth at 80%, but was outpaced by Instacart and Shipt, Target’s expansion into online grocery and claims 10% of sales in the space. Thrive Market focuses on organic grocery items and is the newest grocery delivery service with modest but healthy growth.

Walmart Grocery

Instacart

FreshDirect

Shipt

Peapod

AmazonFresh

Thrive Market

35%

25%

11%

10%

9%

8%

2%

July 2017 – June 2018

July 2016 – June 2017

Share of Online Grocery Sales YOY Online Grocery Growth

Walmart Grocery

Instacart

FreshDirect

Shipt

Peapod

AmazonFresh

Thrive Market

143%

117%

-3%

113%

1%

80%

19%

4© 2018 1010data Inc.

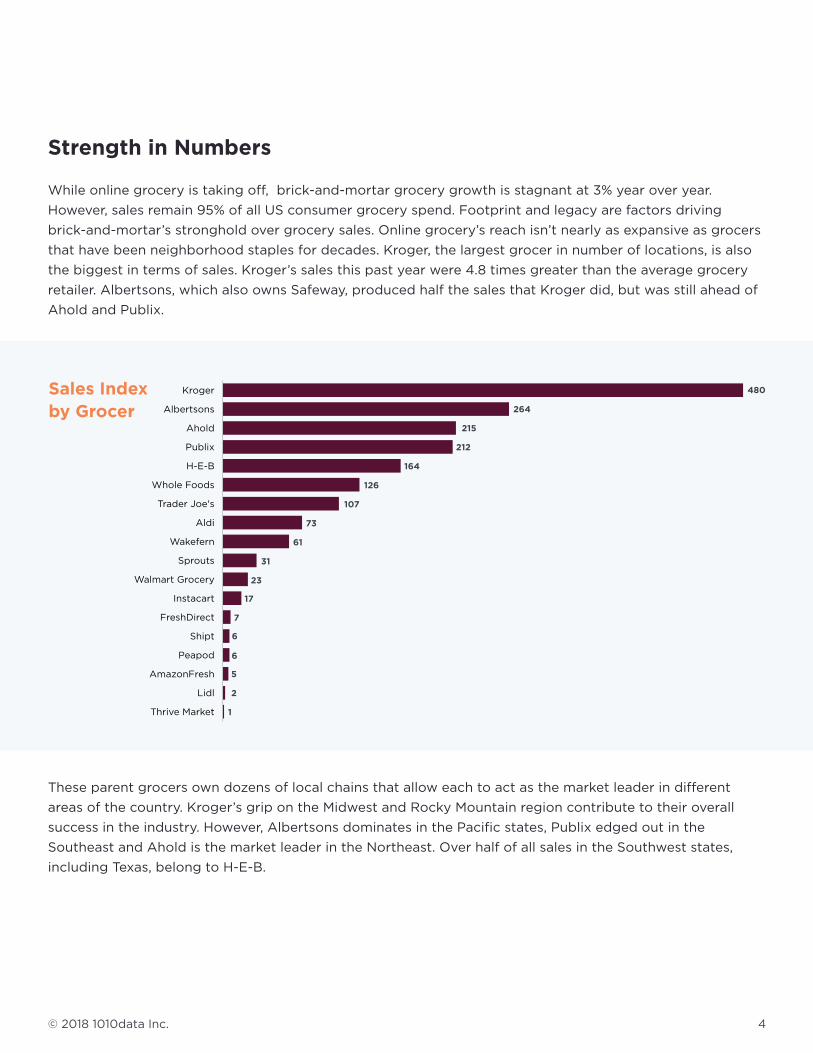

These parent grocers own dozens of local chains that allow each to act as the market leader in different areas of the country. Kroger’s grip on the Midwest and Rocky Mountain region contribute to their overall success in the industry. However, Albertsons dominates in the Pacific states, Publix edged out in the Southeast and Ahold is the market leader in the Northeast. Over half of all sales in the Southwest states, including Texas, belong to H-E-B.

Sales Indexby Grocer

Strength in Numbers

While online grocery is taking off, brick-and-mortar grocery growth is stagnant at 3% year over year. However, sales remain 95% of all US consumer grocery spend. Footprint and legacy are factors driving brick-and-mortar’s stronghold over grocery sales. Online grocery’s reach isn’t nearly as expansive as grocers that have been neighborhood staples for decades. Kroger, the largest grocer in number of locations, is also the biggest in terms of sales. Kroger’s sales this past year were 4.8 times greater than the average grocery retailer. Albertsons, which also owns Safeway, produced half the sales that Kroger did, but was still ahead of Ahold and Publix.

Thrive Market

Lidl

AmazonFresh

Peapod

Shipt

FreshDirect

Instacart

Walmart Grocery

Sprouts

Wakefern

Aldi

Trader Joe's

Whole Foods

H-E-B

Publix

Ahold

Albertsons

Kroger 480

264

215

212

164

126

107

73

61

31

23

17

7

6

6

5

2

1

5© 2018 1010data Inc.

Grocers with regional strongholds shouldn’t get too comfortable. Aldi, a German grocer that entered the US market about 5 years ago, is growing at 24% year over sales. Note that brick-and-mortar grocery as a whole is only up 3% and Trader Joe’s, an Aldi subsidiary, has above average growth at 5%. Lidl, another German transplant, opened their first US locations last summer and have quickly expanded across the southern Atlantic states.

Publix

Albertson’s

H-E-B

Kroger

Ahold

YOY B&M Grocery Growth

Aldi Sprouts Publix H-E-B TraderJoe’s

Kroger Wakefem WholeFoods

Albertsons

Ahold

24%

15%13%

6% 5%2% 1% 0% 0% -8%

Top Grocer by U.S. Region

6© 2018 1010data Inc.

Flavor of Consumer Behavior

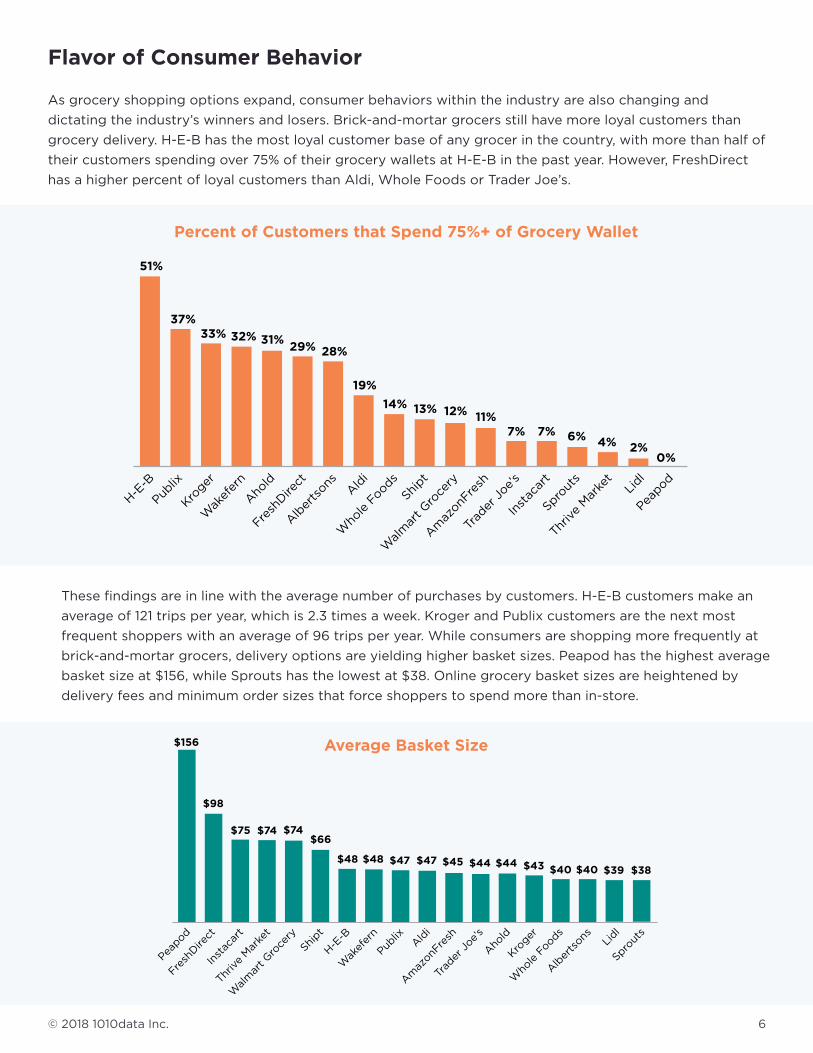

As grocery shopping options expand, consumer behaviors within the industry are also changing and dictating the industry’s winners and losers. Brick-and-mortar grocers still have more loyal customers than grocery delivery. H-E-B has the most loyal customer base of any grocer in the country, with more than half of their customers spending over 75% of their grocery wallets at H-E-B in the past year. However, FreshDirect has a higher percent of loyal customers than Aldi, Whole Foods or Trader Joe’s.

These findings are in line with the average number of purchases by customers. H-E-B customers make an average of 121 trips per year, which is 2.3 times a week. Kroger and Publix customers are the next most frequent shoppers with an average of 96 trips per year. While consumers are shopping more frequently at brick-and-mortar grocers, delivery options are yielding higher basket sizes. Peapod has the highest average basket size at $156, while Sprouts has the lowest at $38. Online grocery basket sizes are heightened by delivery fees and minimum order sizes that force shoppers to spend more than in-store.

H-E

-B

Publix

Kroger

Wak

efer

n

Aho

ld

Fresh

Dire

ctAld

i

Alb

erts

ons

Who

le F

oods

Shipt

Walm

art G

roce

ry

Am

azonF

resh

Inst

acar

t

Trad

er J

oe’s

Sprout

s

Thriv

e M

arke

tLi

dl

Peapod

51%

37%33% 32% 31%

29% 28%

19%

14% 13% 12% 11%7% 7% 6% 4% 2%

0%

Percent of Customers that Spend 75%+ of Grocery Wallet

Average Basket Size

Peapod

Fresh

Dire

ct

Inst

acar

t

Thriv

e M

arke

t

Walm

art G

roce

ry

Shipt

Wak

efer

n

H-E

-B

Publix

Ald

i

Am

azonF

resh

Trad

er J

oe’s

Kroger

Aho

ld

Who

le F

oods

Alb

erts

ons Lidl

Sprout

s

$156

$98

$75 $74 $74$66

$48 $48 $47 $47 $45 $44 $44 $43 $40 $40 $39 $38

7© 2018 1010data Inc.

Save Money, Live Better

Today’s consumers are living Walmart’s slogan when it comes to the way they shop for groceries. Private-label sales are growing rampantly online. Brands from Kroger, Walmart, Target, Meijer and ShopRite’s private-label lines have increased sales by at least 4x in the past year. Consumers are flocking to these brands because they are more cost effective and the retailers are providing on the promise of quality products for less. In terms of living better, consumers are buying more products labeled “natural” or “organic”. Online sales for these healthier items are up 65% this year.

The grocery industry is rapidly changing and it’s more important than ever for it to stay ahead of consumers. While brick-and-mortar staples are still the majority of sales, there is much to learn from new market entrants online and abroad. Online delivery options are yielding higher basket sizes and expanding their reach quickly. Aldi and Lidl, which focus on quality private-label brands, can attribute their success to growing consumer affection for private-label products. Brick-and-mortars that have expanded their reach through partnerships with Instacart, such as Aldi, Sprouts and Publix, are outpacing the competition in overall growth. Similarly, Walmart and Kroger, which both offer click & collect services, are the top grocers online and in-store, respectively. While expanding grocery delivery and pick-up services have proved most fruitful for retailers, anticipating consumer preference shifts is ultimately what retailers need to respond to effectively change and ahead of the market. Leveraging consumer purchase behavior data can help you compete in this amorphous market for the highest share of consumers’ stomachs.

Online Grocery Private-Label Growth YOY

Simple Truth 6.9

FirstStreet 4.9

Kroger 6.8

Marketside 4.2

Market Pantry 4.2

True Goodness 4.1

Wholesome Pantry 4.0

8© 2018 1010data Inc.

Methodology

This report monitors purchases from 18 brick-and-mortar and online grocery services based on the spending activity of millions of shoppers across the U.S. The data was analyzed using 1010data Merchant Insights to assess the performance and growth of different retailers within the grocery industry and the consumer behavior across these retailers from July 2017 - June 2018. Purchases made through Instacart or Shipt are only attributed to Instacart or Shipt and not to the grocer that the items were ordered from, i.e. Publix transactions fulfilled by Instacart are considered Instacart sales.

To learn more about how you can leverage 1010data’s suite of consumer behavior products to anticipate and respond to the changing grocery landscape in real-time, contact [email protected].

1010data transforms Big Data into smart insights to create the high-definition enterprise that can anticipate and respond to change. Our modern cloud-based analytical intelligence and consumer insights solutions enable over 850 clients to achieve improved business outcomes quicker, with less risk.

The world’s foremost companies, including Rite Aid, Dollar General, Coca Cola, GSK, 3M, Bank of America and JP Morgan, consider 1010data the partner of choice for mastering customer touchpoints, optimizing product portfolio health and digitally renovating operations. We’ve been recognized as a Challenger in the Gartner Magic Quadrant for Data Analytics Solutions, named a Leader in the Forrester Wave for Cloud Business Intelligence Platforms and honored as a Big Data Analytics Player by Information Week. 1010data delivers on the promise of Big Data, and we’re just getting started.